Embed Size (px)

Citation preview

JS/V6Not a statement of Government PolicyNot a statement of Government Policy 1August 10

UK Government ICT Storyboard

July 2010

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

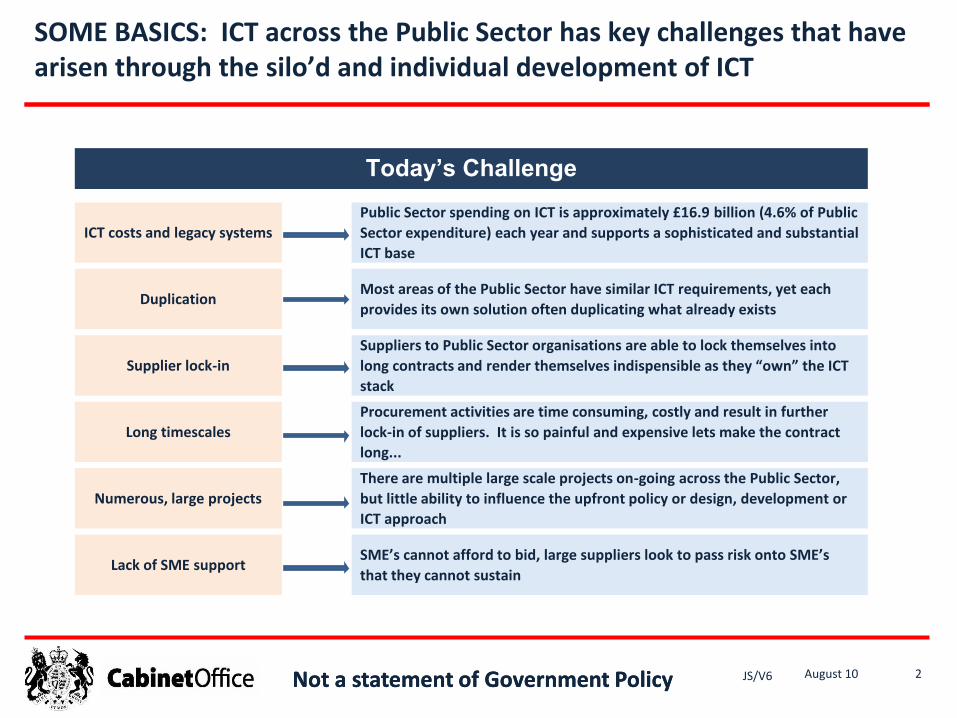

SOME BASICS: ICT across the Public Sector has key challenges that have arisen through the silo’d and individual development of ICT

2August 10

Public Sector spending on ICT is approximately £16.9 billion (4.6% of Public

Sector expenditure) each year and supports a sophisticated and substantial

ICT base

Today’s Challenge

Most areas of the Public Sector have similar ICT requirements, yet each

provides its own solution often duplicating what already exists

Suppliers to Public Sector organisations are able to lock themselves into

long contracts and render themselves indispensible as they “own” the ICT

stack

Procurement activities are time consuming, costly and result in further

lock-in of suppliers. It is so painful and expensive lets make the contract

long...

There are multiple large scale projects on-going across the Public Sector,

but little ability to influence the upfront policy or design, development or

ICT approach

SME’s cannot afford to bid, large suppliers look to pass risk onto SME’s

that they cannot sustain

ICT costs and legacy systems

Duplication

Supplier lock-in

Long timescales

Numerous, large projects

Lack of SME support

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

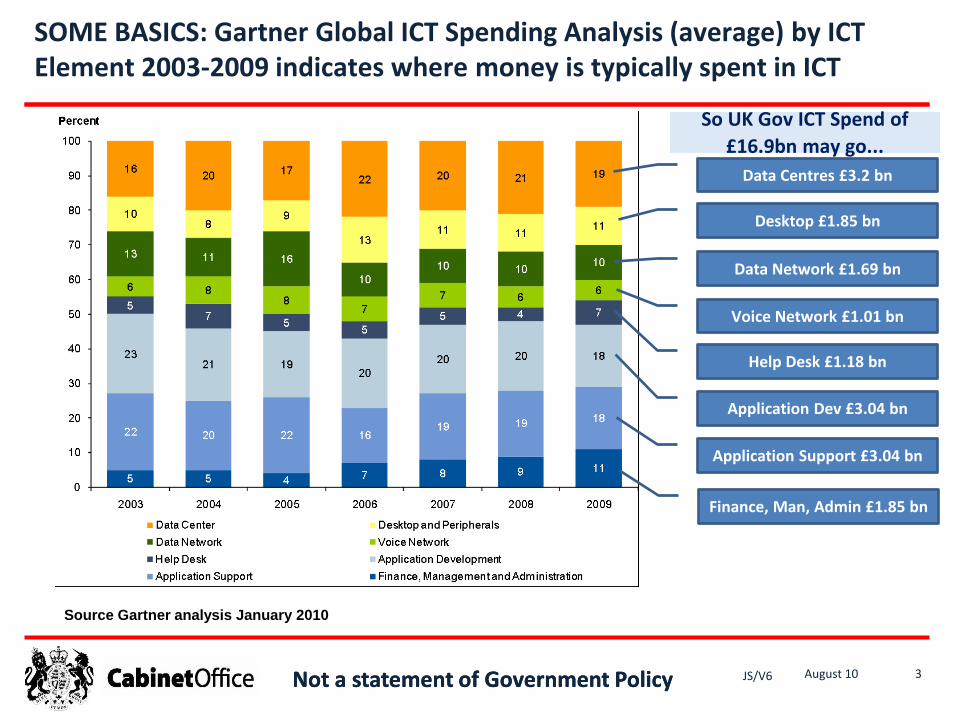

SOME BASICS: Gartner Global ICT Spending Analysis (average) by ICT Element 2003-2009 indicates where money is typically spent in ICT

3August 10

So UK Gov ICT Spend of

£16.9bn may go...

Data Centres £3.2 bn

Desktop £1.85 bn

Data Network £1.69 bn

Voice Network £1.01 bn

Help Desk £1.18 bn

Application Dev £3.04 bn

Application Support £3.04 bn

Finance, Man, Admin £1.85 bn

Source Gartner analysis January 2010

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

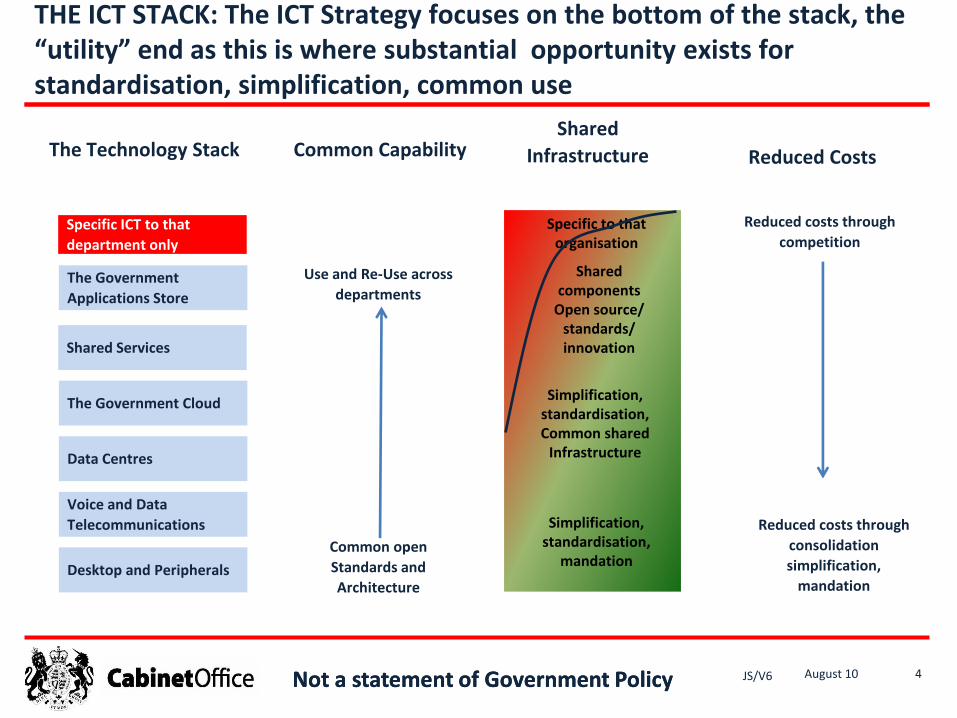

THE ICT STACK: The ICT Strategy focuses on the bottom of the stack, the “utility” end as this is where substantial opportunity exists for standardisation, simplification, common use

4August 10

The Technology Stack Common Capability

Use and Re-Use across

departments

Common open

Standards and

Architecture

Reduced Costs

Reduced costs through

competition

Reduced costs through

consolidation

simplification,

mandation

Shared

Infrastructure

Shared Services

The Government

Applications Store

The Government Cloud

Data Centres

Voice and Data

Telecommunications

Desktop and Peripherals

Specific ICT to that

department only

Simplification, standardisation,

mandation

Specific to that organisation

Simplification, standardisation, Common shared

Infrastructure

Shared components

Open source/ standards/innovation

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

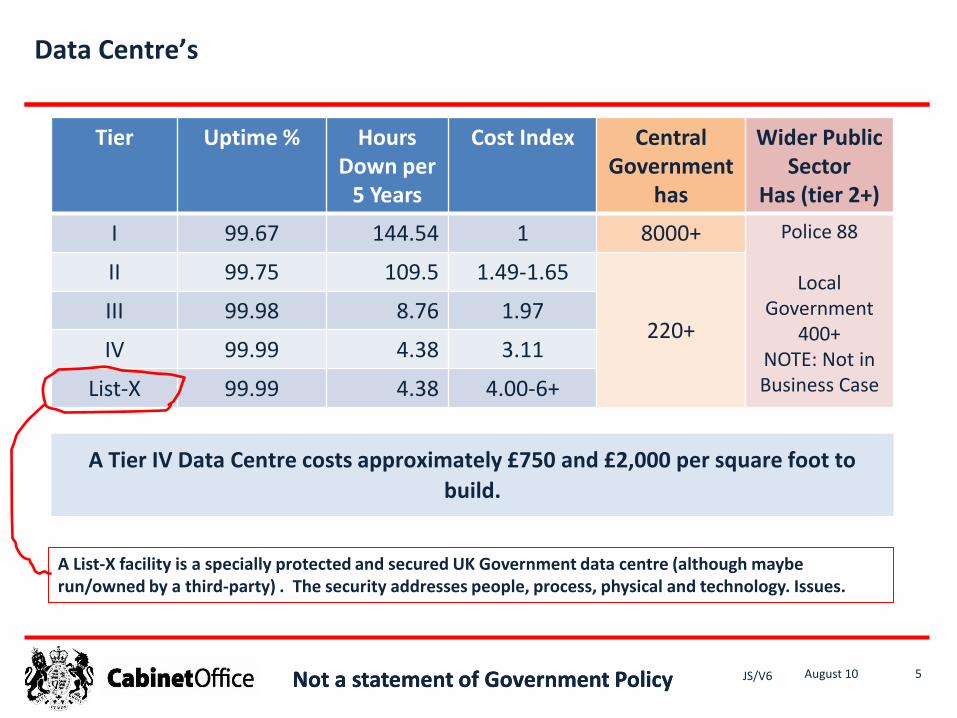

Data Centre’s

5August 10

A Tier IV Data Centre costs approximately £750 and £2,000 per square foot to

build.

Tier Uptime % Hours Down per

5 Years

Cost Index CentralGovernment

has

Wider Public Sector

Has (tier 2+)

I 99.67 144.54 1 8000+ Police 88

Local Government

400+NOTE: Not in Business Case

II 99.75 109.5 1.49-1.65

220+III 99.98 8.76 1.97

IV 99.99 4.38 3.11

List-X 99.99 4.38 4.00-6+

A List-X facility is a specially protected and secured UK Government data centre (although maybe run/owned by a third-party) . The security addresses people, process, physical and technology. Issues.

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

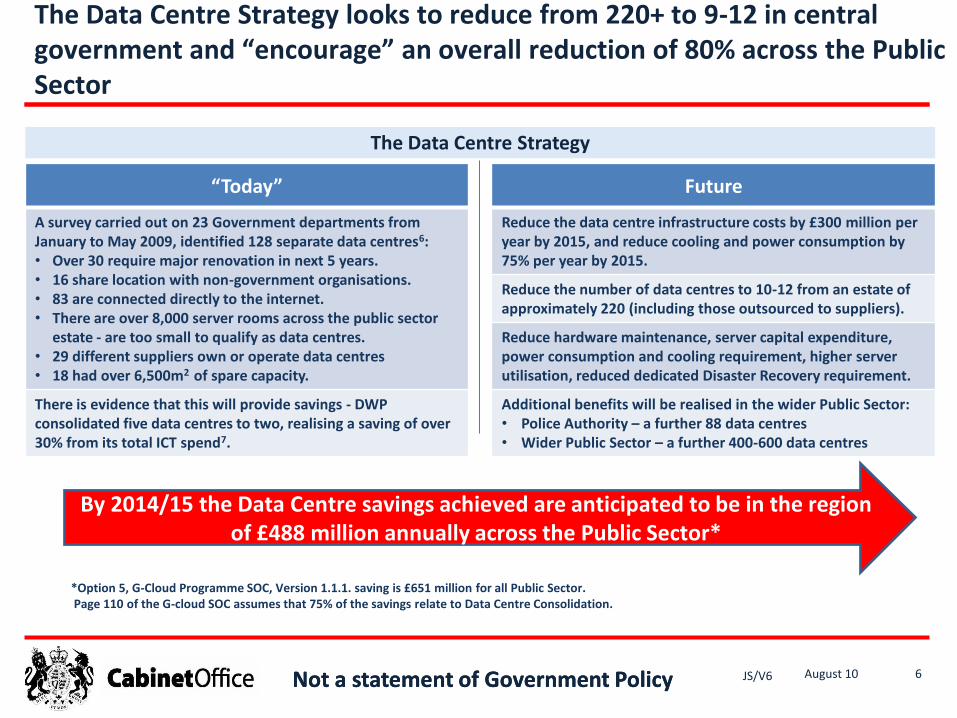

The Data Centre Strategy looks to reduce from 220+ to 9-12 in central government and “encourage” an overall reduction of 80% across the Public Sector

6August 10

“Today”

A survey carried out on 23 Government departments from January to May 2009, identified 128 separate data centres6: • Over 30 require major renovation in next 5 years. • 16 share location with non-government organisations. • 83 are connected directly to the internet. • There are over 8,000 server rooms across the public sector

estate - are too small to qualify as data centres.• 29 different suppliers own or operate data centres• 18 had over 6,500m2 of spare capacity.

There is evidence that this will provide savings - DWPconsolidated five data centres to two, realising a saving of over 30% from its total ICT spend7.

Future

Reduce the data centre infrastructure costs by £300 million per year by 2015, and reduce cooling and power consumption by 75% per year by 2015.

Reduce the number of data centres to 10-12 from an estate of approximately 220 (including those outsourced to suppliers).

Reduce hardware maintenance, server capital expenditure, power consumption and cooling requirement, higher server utilisation, reduced dedicated Disaster Recovery requirement.

Additional benefits will be realised in the wider Public Sector:• Police Authority – a further 88 data centres• Wider Public Sector – a further 400-600 data centres

The Data Centre Strategy

By 2014/15 the Data Centre savings achieved are anticipated to be in the region of £488 million annually across the Public Sector*

*Option 5, G-Cloud Programme SOC, Version 1.1.1. saving is £651 million for all Public Sector. Page 110 of the G-cloud SOC assumes that 75% of the savings relate to Data Centre Consolidation.

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

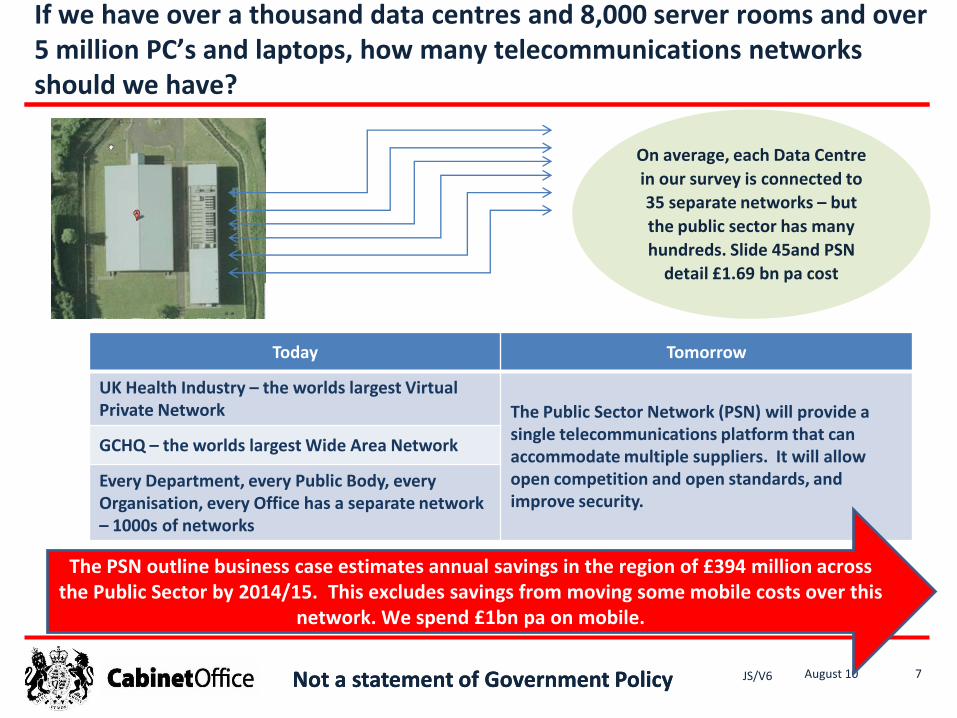

If we have over a thousand data centres and 8,000 server rooms and over 5 million PC’s and laptops, how many telecommunications networks should we have?

7August 10

On average, each Data Centre

in our survey is connected to

35 separate networks – but

the public sector has many

hundreds. Slide 45and PSN

detail £1.69 bn pa cost

Today Tomorrow

UK Health Industry – the worlds largest Virtual Private Network The Public Sector Network (PSN) will provide a

single telecommunications platform that can accommodate multiple suppliers. It will allow open competition and open standards, and improve security.

GCHQ – the worlds largest Wide Area Network

Every Department, every Public Body, every Organisation, every Office has a separate network – 1000s of networks

The PSN outline business case estimates annual savings in the region of £394 million across the Public Sector by 2014/15. This excludes savings from moving some mobile costs over this

network. We spend £1bn pa on mobile.

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

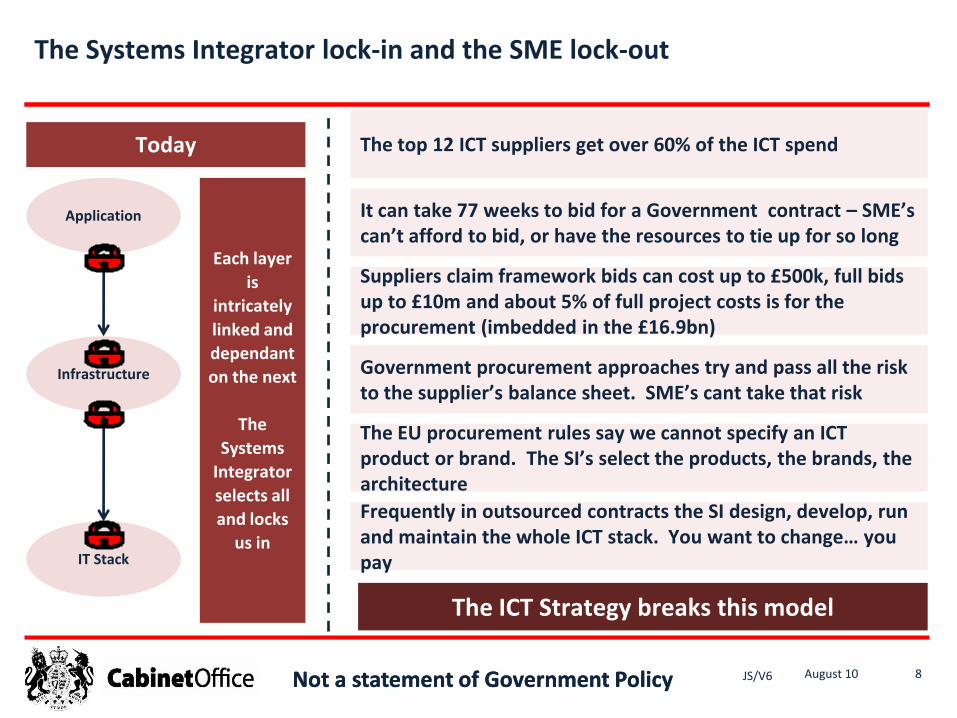

The Systems Integrator lock-in and the SME lock-out

8August 10

Each layer

is

intricately

linked and

dependant

on the next

The

Systems

Integrator

selects all

and locks

us in

Today

Application

Infrastructure

IT Stack

The top 12 ICT suppliers get over 60% of the ICT spend

It can take 77 weeks to bid for a Government contract – SME’s can’t afford to bid, or have the resources to tie up for so long

Government procurement approaches try and pass all the risk to the supplier’s balance sheet. SME’s cant take that risk

The EU procurement rules say we cannot specify an ICT product or brand. The SI’s select the products, the brands, the architecture

Frequently in outsourced contracts the SI design, develop, run and maintain the whole ICT stack. You want to change… you pay

Suppliers claim framework bids can cost up to £500k, full bids up to £10m and about 5% of full project costs is for the procurement (imbedded in the £16.9bn)

The ICT Strategy breaks this model

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

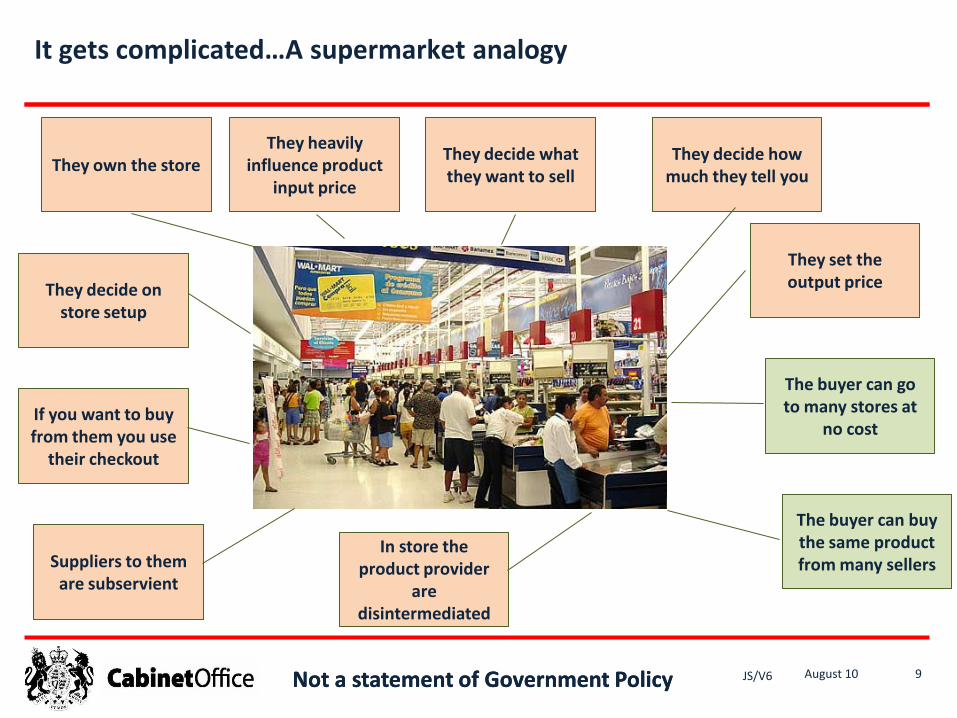

It gets complicated…A supermarket analogy

9August 10

They own the storeThey heavily

influence product input price

They decide what they want to sell

They decide how much they tell you

They set the output priceThey decide on

store setup

The buyer can go to many stores at

no cost

The buyer can buy the same product from many sellers

If you want to buy from them you use

their checkout

Suppliers to them are subservient

In store the product provider

are disintermediated

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

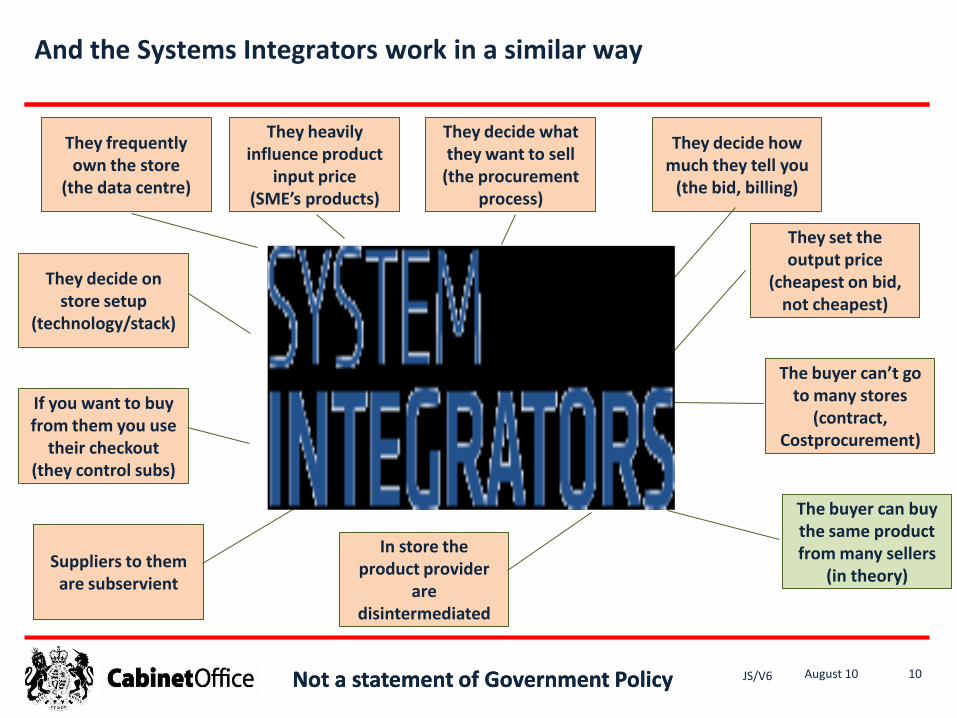

And the Systems Integrators work in a similar way

10August 10

They frequently own the store

(the data centre)

They heavily influence product

input price(SME’s products)

They decide what they want to sell

(the procurement process)

They decide how much they tell you

(the bid, billing)

They set the output price

(cheapest on bid, not cheapest)

They decide on store setup

(technology/stack)

The buyer can’t go to many stores

(contract, Costprocurement)

The buyer can buy the same product from many sellers

(in theory)

If you want to buy from them you use

their checkout(they control subs)

Suppliers to them are subservient

In store the product provider

are disintermediated

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

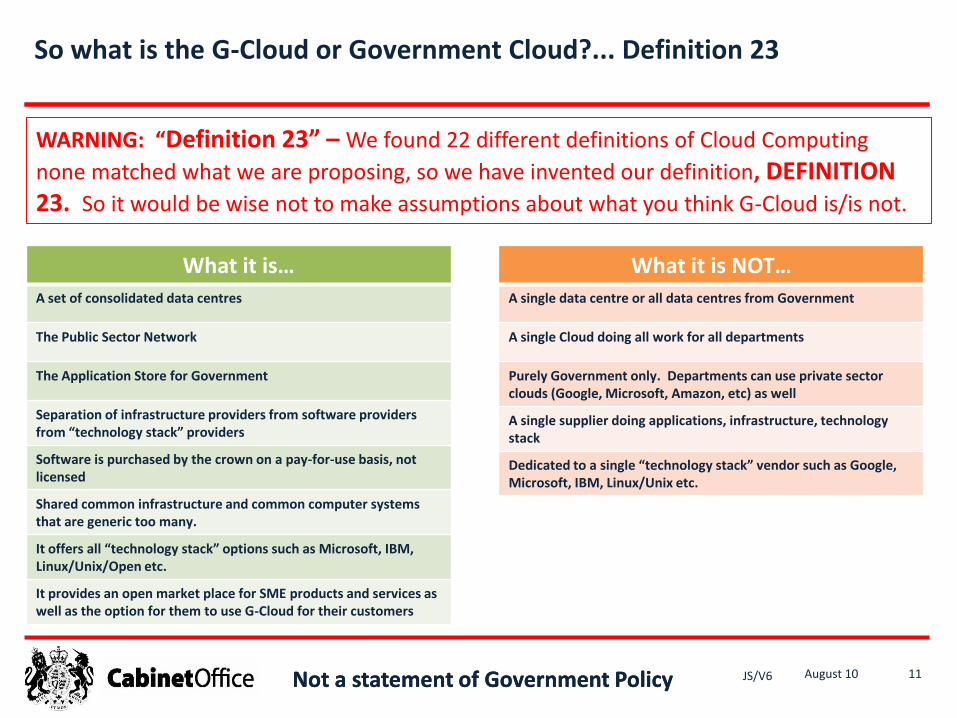

So what is the G-Cloud or Government Cloud?... Definition 23

11August 10

WARNING: “Definition 23” – We found 22 different definitions of Cloud Computing

none matched what we are proposing, so we have invented our definition, DEFINITION 23. So it would be wise not to make assumptions about what you think G-Cloud is/is not.

What it is…A set of consolidated data centres

The Public Sector Network

The Application Store for Government

Separation of infrastructure providers from software providers from “technology stack” providers

Software is purchased by the crown on a pay-for-use basis, not licensed

Shared common infrastructure and common computer systems that are generic too many.

It offers all “technology stack” options such as Microsoft, IBM, Linux/Unix/Open etc.

It provides an open market place for SME products and services as well as the option for them to use G-Cloud for their customers

What it is NOT…A single data centre or all data centres from Government

A single Cloud doing all work for all departments

Purely Government only. Departments can use private sector clouds (Google, Microsoft, Amazon, etc) as well

A single supplier doing applications, infrastructure, technology stack

Dedicated to a single “technology stack” vendor such as Google, Microsoft, IBM, Linux/Unix etc.

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

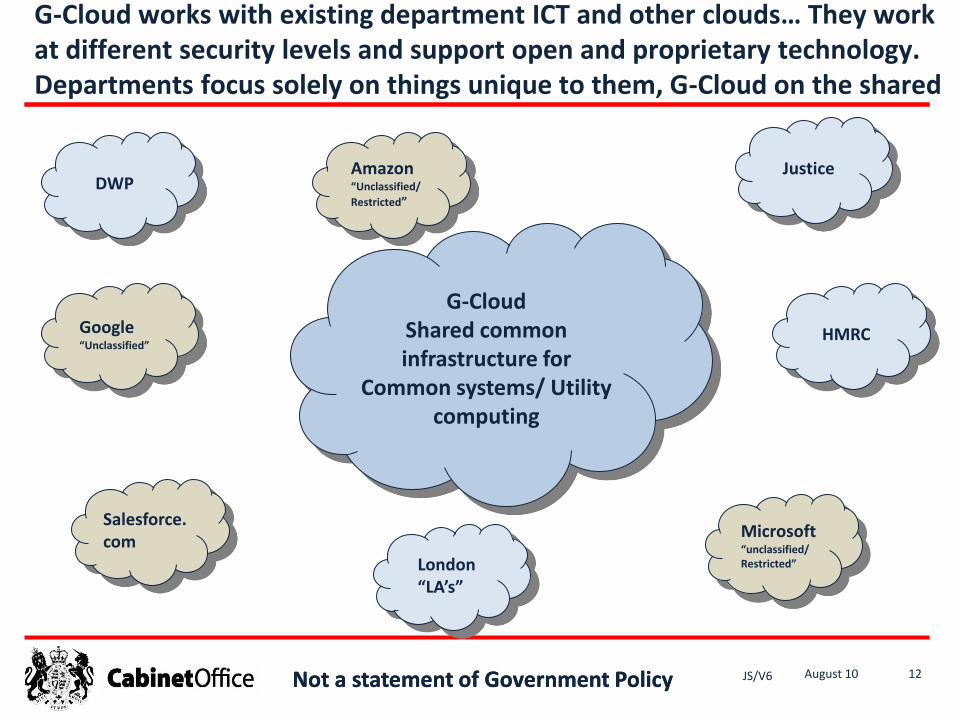

G-Cloud works with existing department ICT and other clouds… They work at different security levels and support open and proprietary technology. Departments focus solely on things unique to them, G-Cloud on the shared

12August 10

G-CloudShared common infrastructure for

Common systems/ Utility computing

DWP

HMRC

JusticeAmazon“Unclassified/

Restricted”

Google“Unclassified”

Microsoft“unclassified/ Restricted”London

“LA’s”

Salesforce.com

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

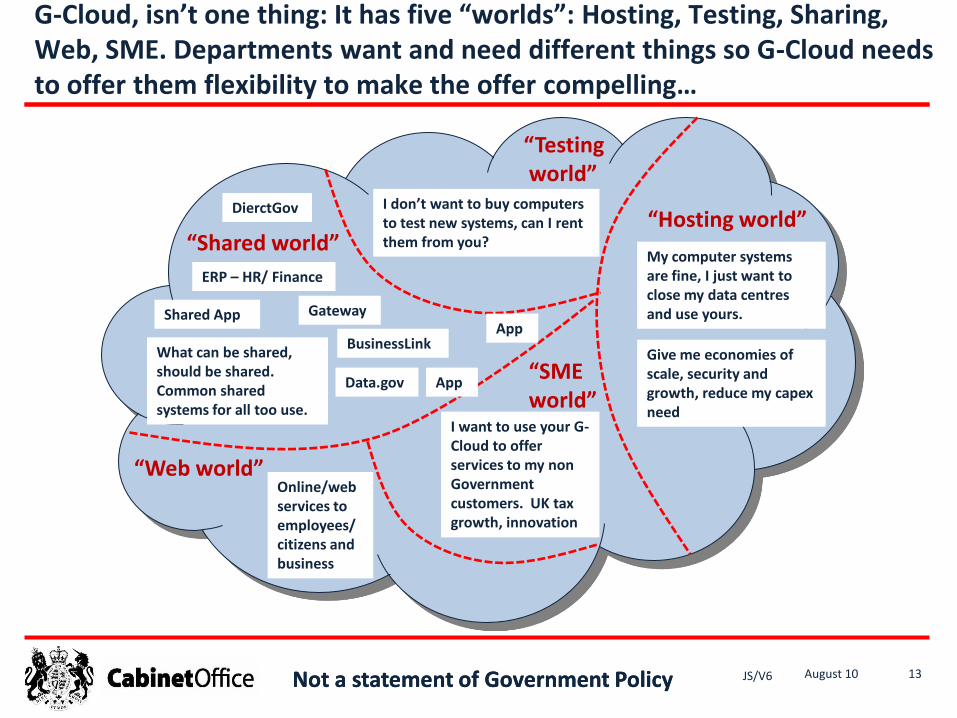

G-Cloud, isn’t one thing: It has five “worlds”: Hosting, Testing, Sharing, Web, SME. Departments want and need different things so G-Cloud needs to offer them flexibility to make the offer compelling…

13August 10

“Hosting world”

My computer systems are fine, I just want to close my data centres and use yours.

Give me economies of scale, security and growth, reduce my capexneed

“Testingworld”

I don’t want to buy computers to test new systems, can I rent them from you?“Shared world”

ERP – HR/ Finance

DierctGov

Gateway

BusinessLink

Shared App

What can be shared, should be shared. Common shared systems for all too use.

Data.gov“SMEworld”

I want to use your G-Cloud to offer services to my non Government customers. UK tax growth, innovation

“Web world”Online/web services to employees/ citizens and business

App

App

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

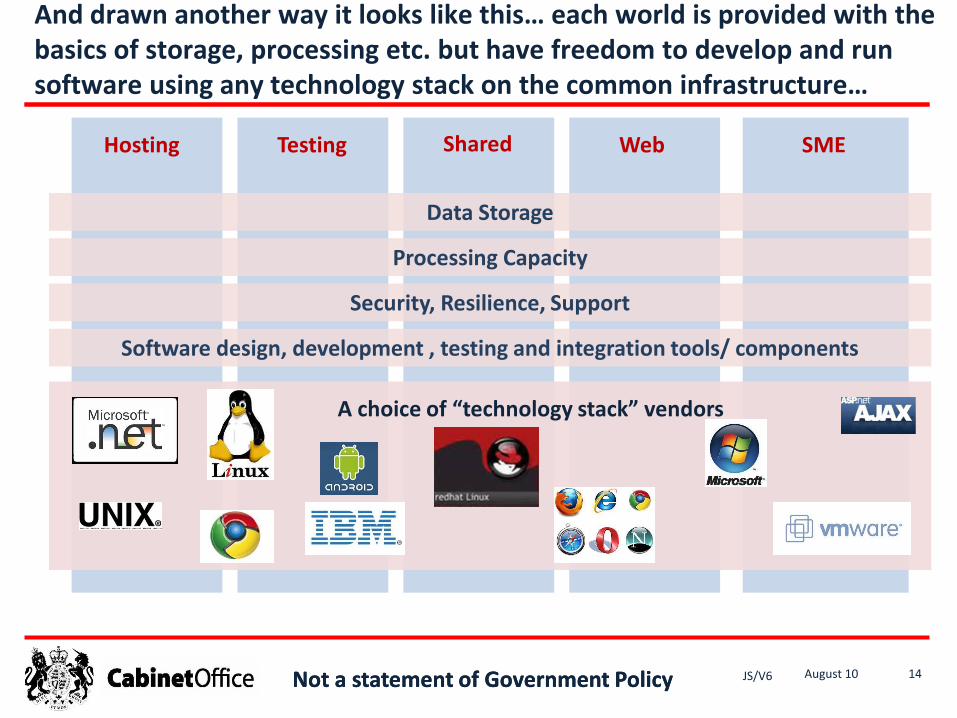

And drawn another way it looks like this… each world is provided with the basics of storage, processing etc. but have freedom to develop and run software using any technology stack on the common infrastructure…

14August 10

Hosting Testing Shared Web SME

Data Storage

Processing Capacity

Security, Resilience, Support

Software design, development , testing and integration tools/ components

A choice of “technology stack” vendors

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

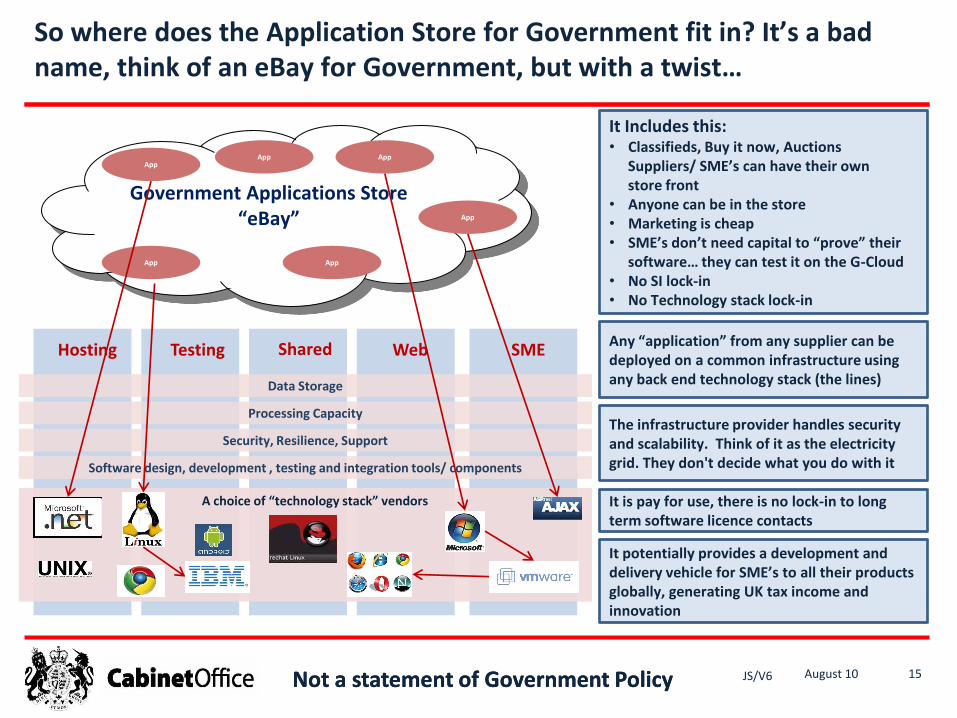

So where does the Application Store for Government fit in? It’s a bad name, think of an eBay for Government, but with a twist…

15August 10

Hosting Testing Shared Web SME

Data Storage

Processing Capacity

Security, Resilience, Support

Software design, development , testing and integration tools/ components

A choice of “technology stack” vendors

Government Applications Store“eBay”

App

App App

App App

App

It Includes this:• Classifieds, Buy it now, Auctions

Suppliers/ SME’s can have their own store front

• Anyone can be in the store• Marketing is cheap• SME’s don’t need capital to “prove” their

software… they can test it on the G-Cloud• No SI lock-in• No Technology stack lock-in

Any “application” from any supplier can be deployed on a common infrastructure using any back end technology stack (the lines)

It is pay for use, there is no lock-in to long term software licence contacts

The infrastructure provider handles security and scalability. Think of it as the electricity grid. They don't decide what you do with it

It potentially provides a development and delivery vehicle for SME’s to all their products globally, generating UK tax income and innovation

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

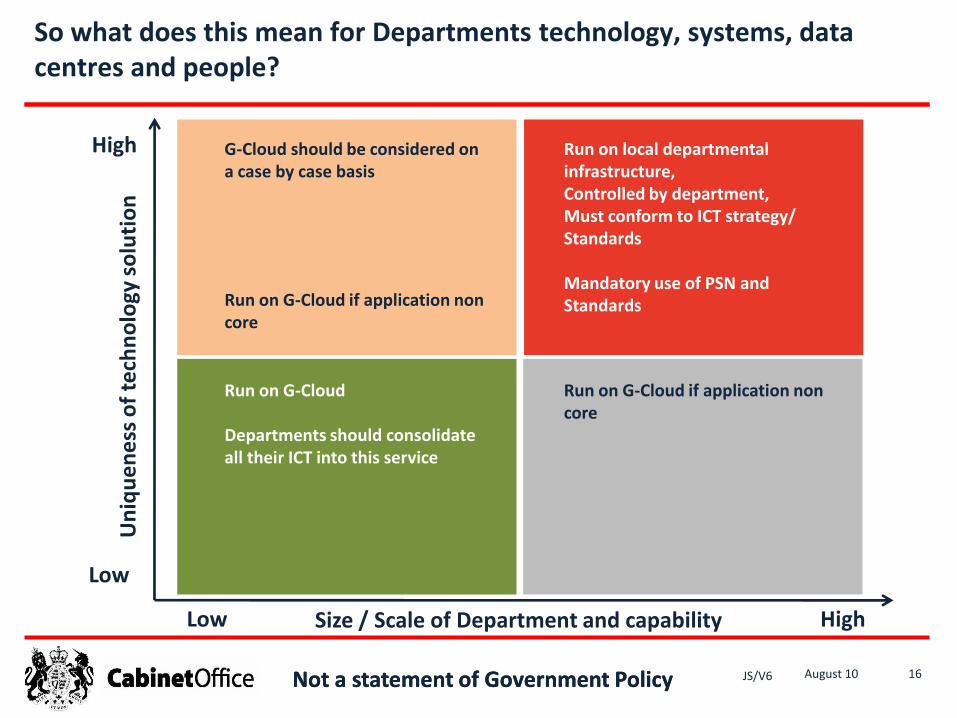

So what does this mean for Departments technology, systems, data centres and people?

16August 10

Size / Scale of Department and capability

Un

iqu

enes

s o

f te

chn

olo

gy s

olu

tio

nHigh

High

Low

Low

Run on local departmental infrastructure,Controlled by department,Must conform to ICT strategy/ Standards

Mandatory use of PSN and Standards

Run on G-Cloud

Departments should consolidate all their ICT into this service

Run on G-Cloud if application non core

Run on G-Cloud if application non core

G-Cloud should be considered on a case by case basis

JS/V6Not a statement of Government PolicyNot a statement of Government Policy

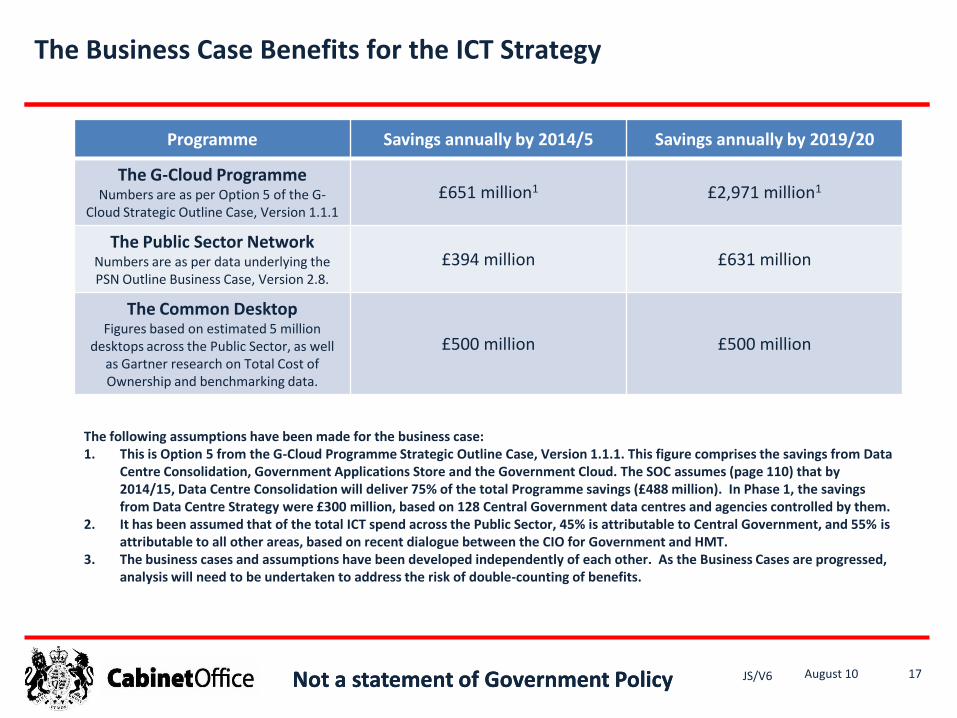

The Business Case Benefits for the ICT Strategy

17August 10

Programme Savings annually by 2014/5 Savings annually by 2019/20

The G-Cloud ProgrammeNumbers are as per Option 5 of the G-

Cloud Strategic Outline Case, Version 1.1.1

£651 million1 £2,971 million1

The Public Sector NetworkNumbers are as per data underlying the PSN Outline Business Case, Version 2.8.

£394 million £631 million

The Common DesktopFigures based on estimated 5 million

desktops across the Public Sector, as well as Gartner research on Total Cost of Ownership and benchmarking data.

£500 million £500 million

The following assumptions have been made for the business case:1. This is Option 5 from the G-Cloud Programme Strategic Outline Case, Version 1.1.1. This figure comprises the savings from Data

Centre Consolidation, Government Applications Store and the Government Cloud. The SOC assumes (page 110) that by 2014/15, Data Centre Consolidation will deliver 75% of the total Programme savings (£488 million). In Phase 1, the savings from Data Centre Strategy were £300 million, based on 128 Central Government data centres and agencies controlled by them.

2. It has been assumed that of the total ICT spend across the Public Sector, 45% is attributable to Central Government, and 55% is attributable to all other areas, based on recent dialogue between the CIO for Government and HMT.

3. The business cases and assumptions have been developed independently of each other. As the Business Cases are progressed, analysis will need to be undertaken to address the risk of double-counting of benefits.