Embed Size (px)

Citation preview

©UFS

For Producer or Broker Dealer Use Only. Not for Public Distribution.

Providing Clients Flexibility and Cash Value

Using Trust and Product Design

Agenda

• Taxes

• Traditionally Safe Asset Classes

• Insurance as an Asset

• Flexible Trust Design

• Product Choice

• Alternative Investments

2For Producer or Broker Dealer Use Only. Not for Public Distribution.

For Producer or Broker Dealer Use Only. Not for Public Distribution.

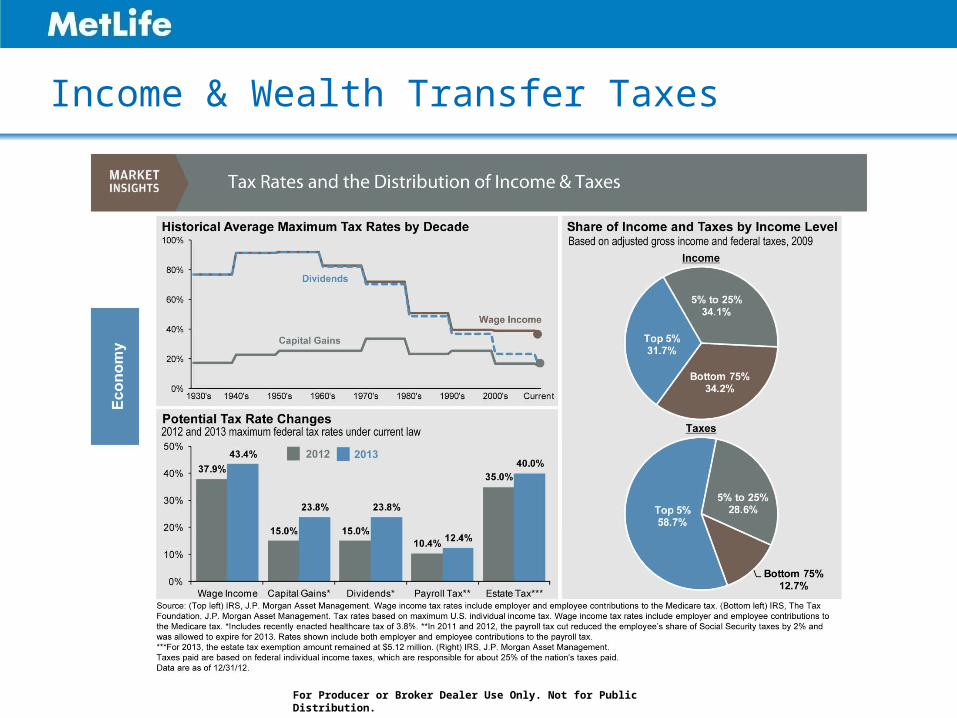

Income & Wealth Transfer Taxes

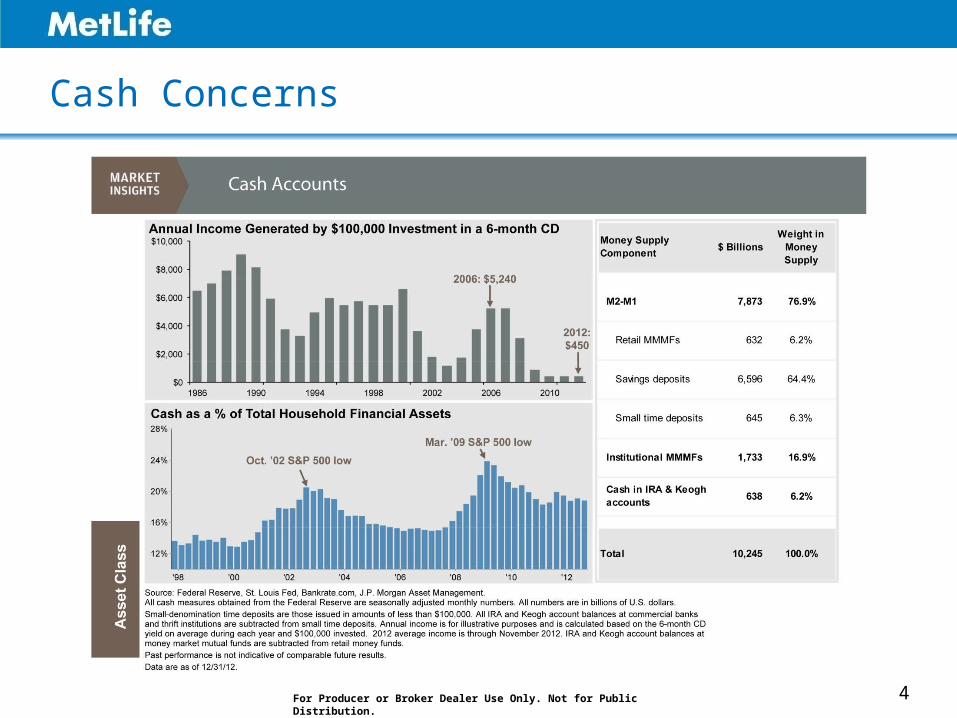

Cash Concerns

4For Producer or Broker Dealer Use Only. Not for Public Distribution.

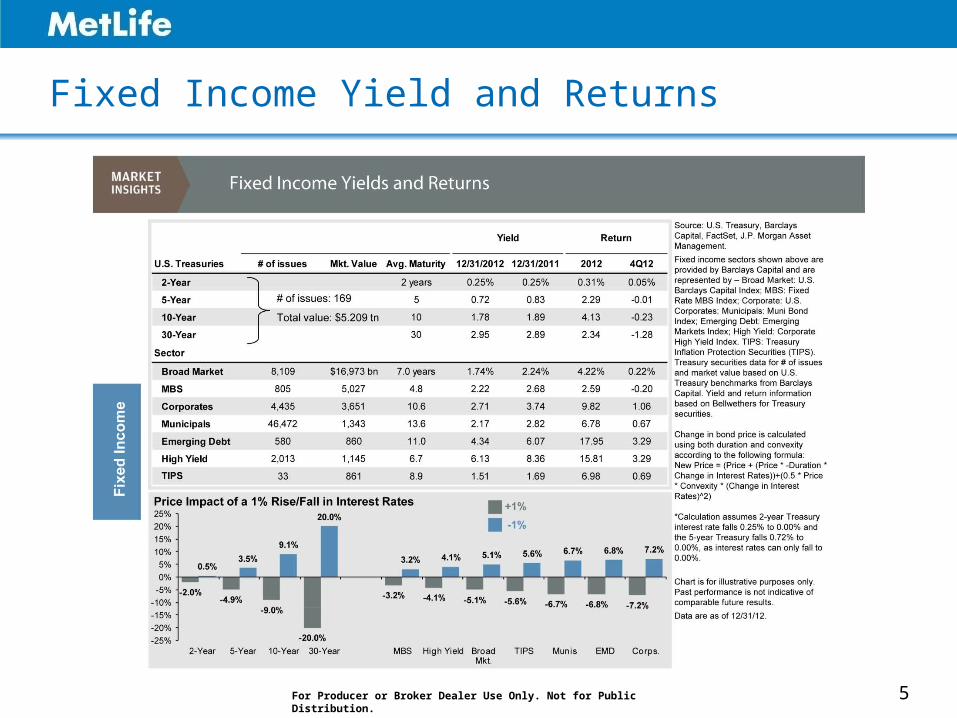

Fixed Income Yield and Returns

5For Producer or Broker Dealer Use Only. Not for Public Distribution.

• Tax-Free Death Benefit– Primary purpose of life insurance

– Income and estate tax-free

• Tax-Deferred Growth

• Potential for Tax-Free Distributions– Policy loans and withdrawals

• Flexible Asset– No contribution limits based on income

– Distributions prior to age 59 ½

Loans and withdrawals will decrease the cash value and death benefit. Distributions are generally treated first as tax-free recovery of basis and then as taxable income, assuming the policy is not a Modified Endowment Contract (MEC). However, different rules apply in the first fifteen policy years, when distributions accompanied by benefit reductions may be taxable prior to basis recovery. Non-MEC loans are generally not subject to tax but may be taxable when the policy lapses, is surrendered, exchanged or otherwise terminated. In the case of a MEC, loans and withdrawals are taxable to the extent of policy gain and a 10% penalty may apply if taken prior to age 59½. Always confirm the status of a particular loan or withdrawal with a qualified tax advisor. Cash value accumulation may not be guaranteed depending on the type of product selected. Investments in variable life insurance are subject to market risk, including loss of principal.

Cash value life insurance offers the advantage of a tax-free death benefit and the potential for income tax-free withdrawals and policy loans provided the policy is properly structured and remains in force.1

For Producer or Broker Dealer Use Only. Not for Public Distribution.

Life Insurance as an Asset

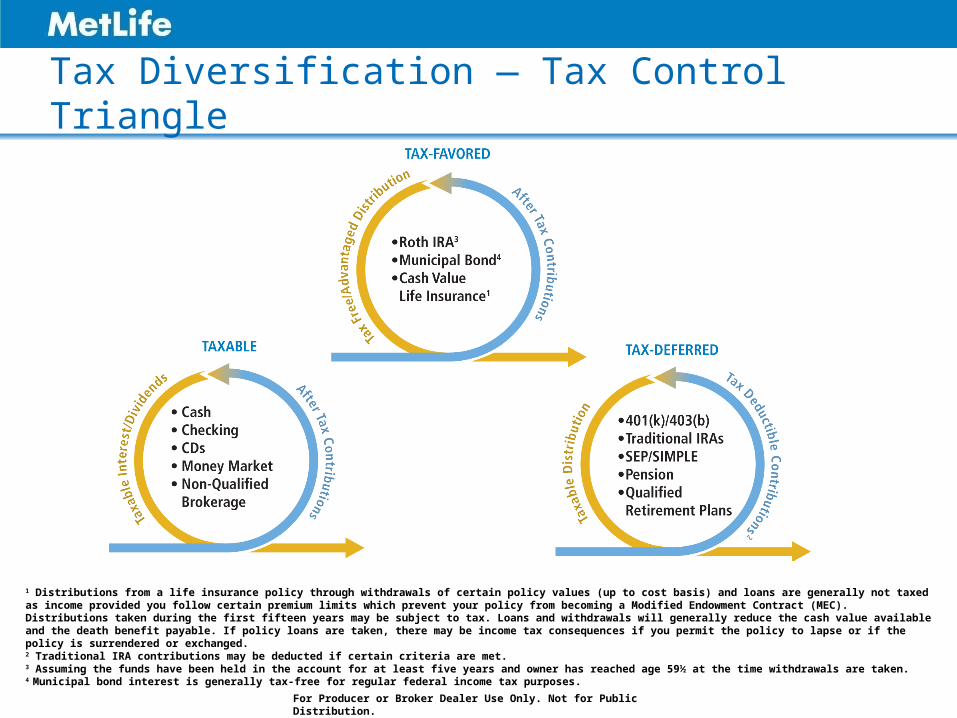

1 Distributions from a life insurance policy through withdrawals of certain policy values (up to cost basis) and loans are generally not taxed as income provided you follow certain premium limits which prevent your policy from becoming a Modified Endowment Contract (MEC). Distributions taken during the first fifteen years may be subject to tax. Loans and withdrawals will generally reduce the cash value available and the death benefit payable. If policy loans are taken, there may be income tax consequences if you permit the policy to lapse or if the policy is surrendered or exchanged.2 Traditional IRA contributions may be deducted if certain criteria are met.3 Assuming the funds have been held in the account for at least five years and owner has reached age 59½ at the time withdrawals are taken.4 Municipal bond interest is generally tax-free for regular federal income tax purposes.

For Producer or Broker Dealer Use Only. Not for Public Distribution.

Tax Diversification — Tax Control Triangle

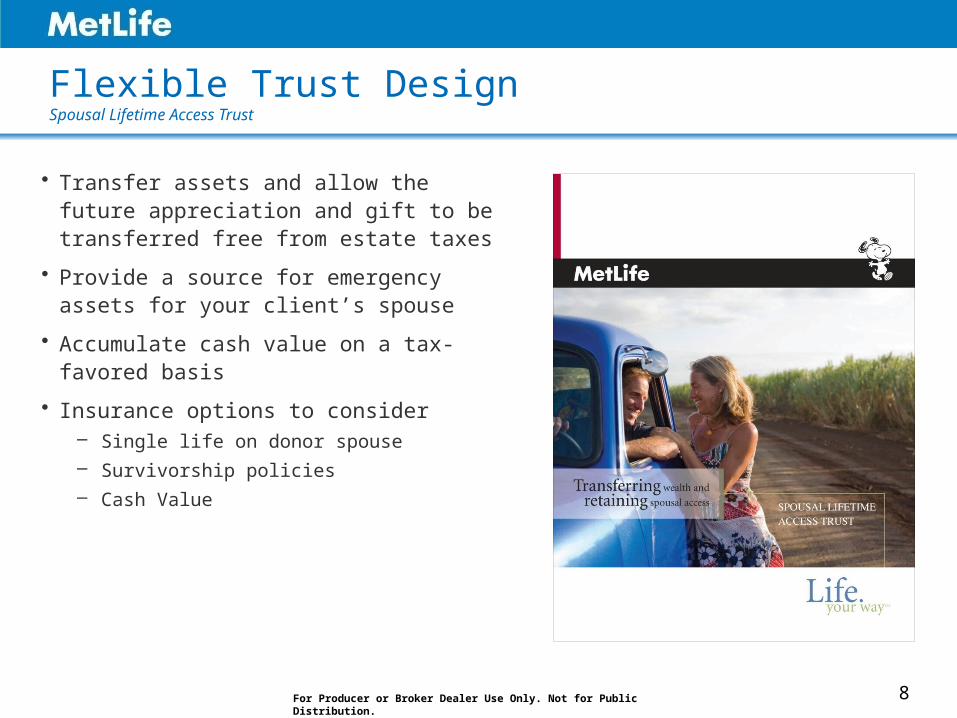

Flexible Trust DesignSpousal Lifetime Access Trust

• Transfer assets and allow the future appreciation and gift to be transferred free from estate taxes

• Provide a source for emergency assets for your client’s spouse

• Accumulate cash value on a tax-favored basis

• Insurance options to consider– Single life on donor spouse

– Survivorship policies

– Cash Value

8For Producer or Broker Dealer Use Only. Not for Public Distribution.

Product Choice

9

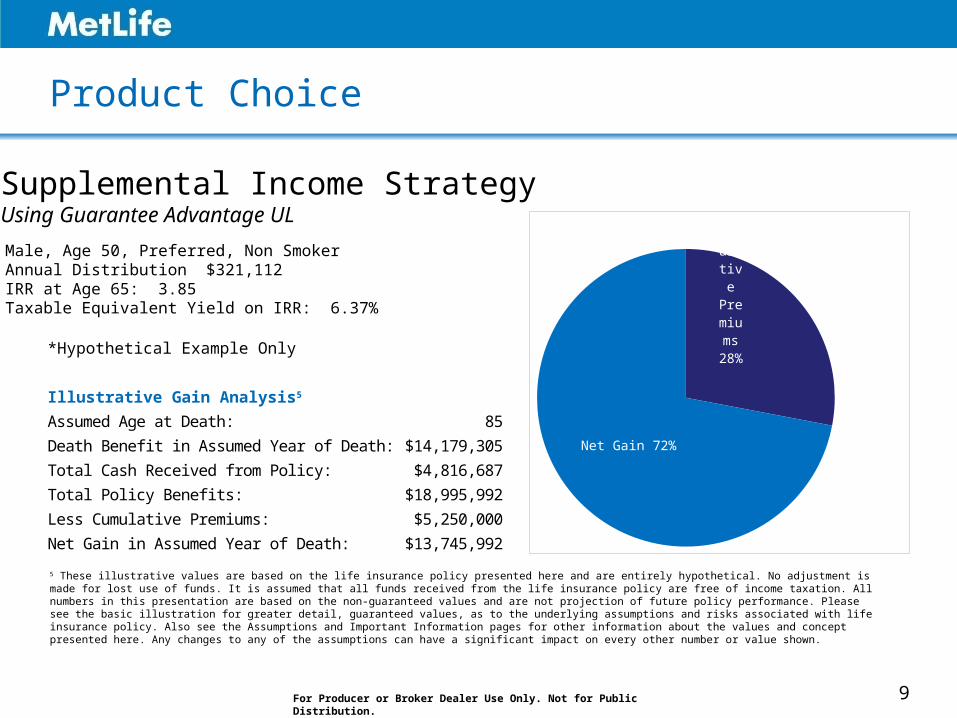

Supplemental Income StrategyUsing Guarantee Advantage UL

Male, Age 50, Preferred, Non SmokerAnnual Distribution $321,112IRR at Age 65: 3.85Taxable Equivalent Yield on IRR: 6.37%

For Producer or Broker Dealer Use Only. Not for Public Distribution.

5 These illustrative values are based on the life insurance policy presented here and are entirely hypothetical. No adjustment is made for lost use of funds. It is assumed that all funds received from the life insurance policy are free of income taxation. All numbers in this presentation are based on the non-guaranteed values and are not projection of future policy performance. Please see the basic illustration for greater detail, guaranteed values, as to the underlying assumptions and risks associated with life insurance policy. Also see the Assumptions and Important Information pages for other information about the values and concept presented here. Any changes to any of the assumptions can have a significant impact on every other number or value shown.

Cu-mula-tive Pre-mi-ums 28%

Net Gain 72%

*Hypothetical Example Only

Illustrative Gain Analysis5

Assumed Age at Death: 85

Death Benefit in Assumed Year of Death: $14,179,305

Total Cash Received from Policy: $4,816,687

Total Policy Benefits: $18,995,992

Less Cumulative Premiums: $5,250,000

Net Gain in Assumed Year of Death: $13,745,992

Product Choice

10

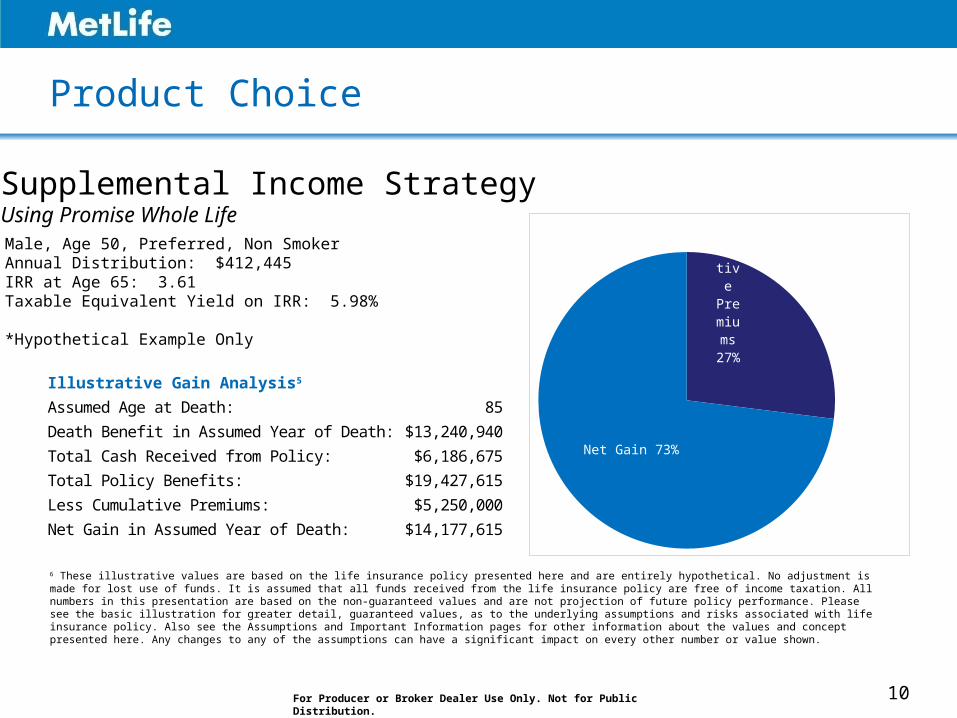

Supplemental Income StrategyUsing Promise Whole Life Male, Age 50, Preferred, Non SmokerAnnual Distribution: $412,445IRR at Age 65: 3.61Taxable Equivalent Yield on IRR: 5.98%

*Hypothetical Example Only

For Producer or Broker Dealer Use Only. Not for Public Distribution.

Cu-mu-

lative Pre-mi-ums 27%

Net Gain 73%

6 These illustrative values are based on the life insurance policy presented here and are entirely hypothetical. No adjustment is made for lost use of funds. It is assumed that all funds received from the life insurance policy are free of income taxation. All numbers in this presentation are based on the non-guaranteed values and are not projection of future policy performance. Please see the basic illustration for greater detail, guaranteed values, as to the underlying assumptions and risks associated with life insurance policy. Also see the Assumptions and Important Information pages for other information about the values and concept presented here. Any changes to any of the assumptions can have a significant impact on every other number or value shown.

Illustrative Gain Analysis5

Assumed Age at Death: 85

Death Benefit in Assumed Year of Death: $13,240,940

Total Cash Received from Policy: $6,186,675

Total Policy Benefits: $19,427,615

Less Cumulative Premiums: $5,250,000

Net Gain in Assumed Year of Death: $14,177,615

Product Choice

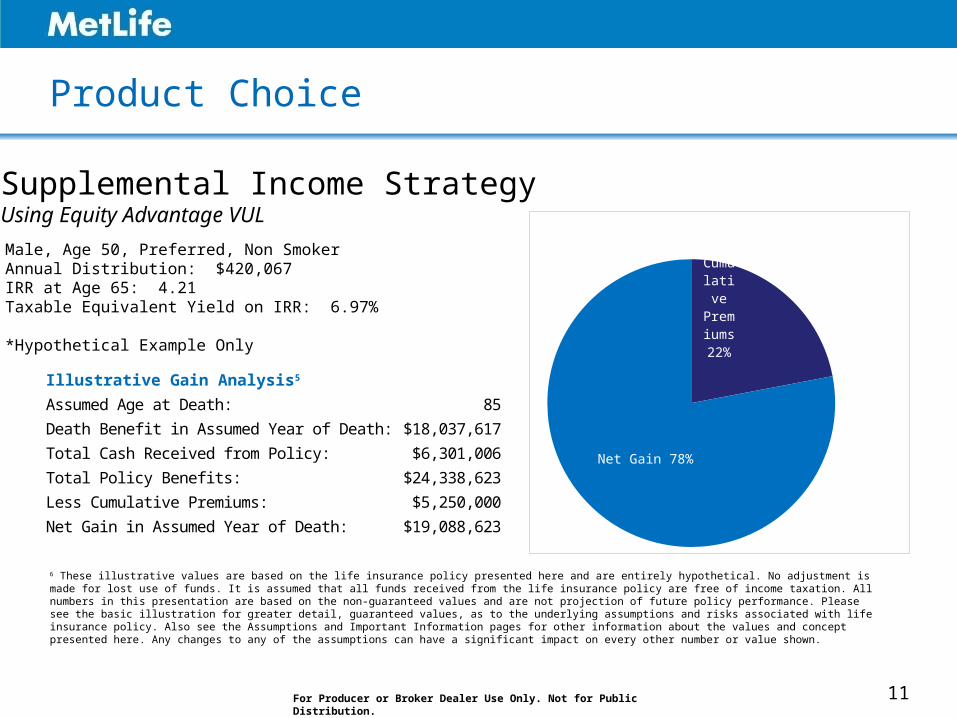

11

Male, Age 50, Preferred, Non SmokerAnnual Distribution: $420,067IRR at Age 65: 4.21Taxable Equivalent Yield on IRR: 6.97%

*Hypothetical Example Only

For Producer or Broker Dealer Use Only. Not for Public Distribution.

Supplemental Income StrategyUsing Equity Advantage VUL

Cumu-la-tive Premi-ums 22%

Net Gain 78%

6 These illustrative values are based on the life insurance policy presented here and are entirely hypothetical. No adjustment is made for lost use of funds. It is assumed that all funds received from the life insurance policy are free of income taxation. All numbers in this presentation are based on the non-guaranteed values and are not projection of future policy performance. Please see the basic illustration for greater detail, guaranteed values, as to the underlying assumptions and risks associated with life insurance policy. Also see the Assumptions and Important Information pages for other information about the values and concept presented here. Any changes to any of the assumptions can have a significant impact on every other number or value shown.

Illustrative Gain Analysis5

Assumed Age at Death: 85

Death Benefit in Assumed Year of Death: $18,037,617

Total Cash Received from Policy: $6,301,006

Total Policy Benefits: $24,338,623

Less Cumulative Premiums: $5,250,000

Net Gain in Assumed Year of Death: $19,088,623

Product Choice

12

Summary Comparison

Male, Age 50, Preferred Nonsmoker

Guarantee Advantage UL without CCR

Promise Whole Life Equity Advantage Variable Universal Life

Initial Death Benefit 18,995,992 22,687,475 20,005,415

Annual Premium for 5 Years 1,050,000 1,050,000 1,050,000

Total Premium 5,250,000 5,250,000 5,250,000

Withdrawals from 66 to 85 321,112 412,445 420,067

IRR at Age 66 3.85% 3.61% 4.21%

Taxable Equivalent Yield 6.37% 5.98% 6.97%

Total Loans & Withdrawals 4,816,687 6,186,675 6,301,006

Current CV Year 10 6,741,2532 6,627,6152,3,4 6,899,1222

Guaranteed CV Year 10 1,576,682 7,192,8211 0

Current CV Year 20 8,645,2462 8,246,1422,3,4 9,029,2572

Guaranteed CV Year 20 0 12,967,5811 0

Current Interest Crediting Rate 5.20% N/A 7.00% Hypothetical Gross Rate6.26% Hypothetical Net Rate

Dividend Interest Rate N/A 5.25% N/A

Commissionable Premium Target – 203,560 Base – 420,000 Target – 376,984Other Attributes General Account

Flexible PremiumsOverloan Protection Rider5

General AccountDividends Will be Paid If and

When Declared by the Issuing Company

Guaranteed CV

Guaranteed Minimum Death Benefit ProtectionFlexible Premiums

No Investment Restrictions including Protected Growth

Strategy Funds

1 Assumes Premiums are paid on time each year and no Loans or Withdrawals

2 Assumes Premiums are paid on time for 5 years and Loans and Withdrawals as specified

3 Assumes dividends are paid at current rate.

4 Dividends are not guaranteed.

5 Optional riders can be purchased for an additional charge. Age and state availability restrictions may apply.

Alternative Investments

Protective Growth Strategies

13For Producer or Broker Dealer Use Only. Not for Public Distribution.

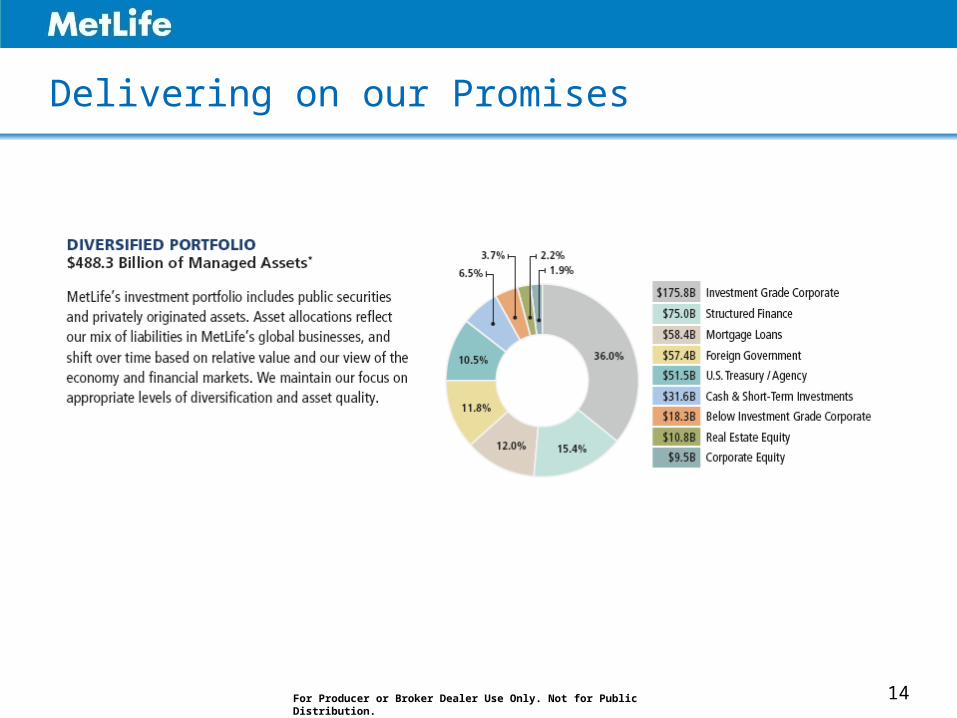

Delivering on our Promises

14For Producer or Broker Dealer Use Only. Not for Public Distribution.

Implementation

15

• Review strategic relationship

• Practice review

• Schedule time for client meetings and discuss method of approaching client

• Set client meeting to confirm data, identify problems/ solutions, initiate underwriting

• Deliver presentation materials if required

• Implement Solutions

• Repeat Steps

For Producer or Broker Dealer Use Only. Not for Public Distribution.

MetLife Brand• MetLife, Inc. is a leading global provider of insurance, annuities and employee

benefit programs, serving 90 million customers.

• Founded in 1868, MetLife continues to build upon its long history of providing unique solutions for its customers by launching new and innovative products, expanding its role as a leader, and continuing to provide high quality financial solutions that are backed by a trusted, well-recognized brand name and strong financial performance

• MetLife counts over 90 of the top one hundred FORTUNE 500® companies among its corporate clients and is the largest life insurer in the U.S. and Mexico.

* Source: MetLife.com/Investor Relations 2013

For Producer or Broker Dealer Use Only. Not for Public Distribution.

Life Insurance Products are:• Not A Deposit • Not FDIC-Insured • Not Insured By Any Federal Government Agency

• Not Guaranteed By Any Bank Or Credit Union • May Go Down In Value

L0213305067[exp0214]© 2013 METLIFE INC. PEANUTS © 2013 Peanuts Worldwide

Pursuant to IRS Circular 230, MetLife is providing you with the following notification: The information contained in this document is not intended to (and cannot) be used by anyone to avoid IRS penalties. This document supports the promotion and marketing of insurance products. You should seek advice based on your particular circumstances from an independent tax advisor. MetLife, its agents and representatives may not give legal or tax advice. Any discussion of taxes herein or related to this document is for general information purposes only and does not purport to be complete or cover every situation. Tax law is subject to interpretation and change. Tax results and the appropriateness of any product for any specific taxpayer may vary depending on the facts and circumstances. You should consult with and rely on your own independent legal and tax advisors regarding your particular set of facts and circumstances.

Like most insurance policies, MetLife's policies contain charges, limitations, exclusions, termination provisions and terms for keeping them in force. Contact your financial representative for costs and complete details.

Guarantee Advantage Universal Life is issued by MetLife Investors USA Insurance Company on Policy Form 5E-34-07 and in New York only by Metropolitan Life Insurance Company on Policy Form 1E-34-07-NY. All product guarantees are subject to the financial strength and claims-paying ability of the issuing insurance company.

Life insurance products are issued by: MetLife Investors USA Insurance Company, Irvine, CA 92614 and in NY only by: Metropolitan Life Insurance Company, First MetLife Investors Insurance Company, New York, NY 10166.

Life insurance products are issued by:MetLife Investors USA Insurance Company5 Park Plaza, Suite 1900Irvine, CA 92614

And in NY only by:Metropolitan Life Insurance CompanyFirst MetLife Investors Insurance Company 200 Park AvenueNew York, NY 10166metlife.com

For Producer or Broker Dealer Use Only. Not for Public Distribution.

![©UFS MetLife’s New DI Term Premium Conversion Rider E1010135054[exp1011] For Producer Use Only. Not For Use With the General Public](https://img.pdfslide.us/doc/110x75/56649c915503460f9494b219/ufs-metlifes-new-di-term-premium-conversion-rider-e1010135054exp1011.jpg)

![For Producer or Broker/Dealer Use Only. Not for Public Distribution. [Presenter Name] [Date]](https://img.pdfslide.us/doc/110x75/56649f325503460f94c4dddc/for-producer-or-brokerdealer-use-only-not-for-public-distribution-presenter.jpg)