Embed Size (px)

Citation preview

©UFS

Financial Planning 101

Investment Advisory Services offered through Investment Advisor

Representatives of MetLife Securities, Inc. (MSI), 200 Park Avenue, New York, NY 10166, a Registered Investment Advisor. MSI is a MetLife, Inc.

company L0609046410[exp0510][AZ]

2

Financial Planning Profession and Industry Overview

• Financial Planner profession description

• Industry Changes / Trends

• Employment / Earnings

• Job Outlook

• Education / Training

• Qualifications / Skill Sets

• Certifications / Advancement

• Resources

3

• Where are you today?

• Where do you want to go?

• How do you get there?

What Is Financial Planning?

4

The Planning Process

• Get organized

• Analyze and compare financial resources against goals

• Develop personalized, written analysis

• Evaluate recommendations and alternatives

• Put the plan into action (implementation)

• Keep the plan up-to-date

5

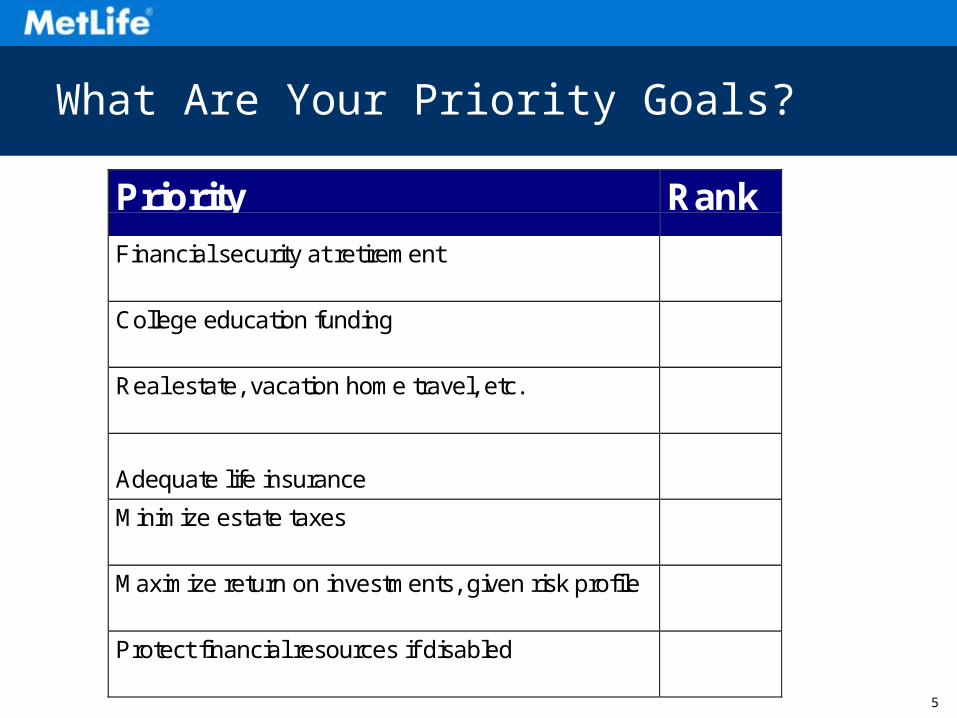

What Are Your Priority Goals?

Priority Rank

Financial security at retirement

College education funding

Real estate, vacation home travel, etc.

Adequate life insurance

Minimize estate taxes

Maximize return on investments, given risk profile

Protect financial resources if disabled

6

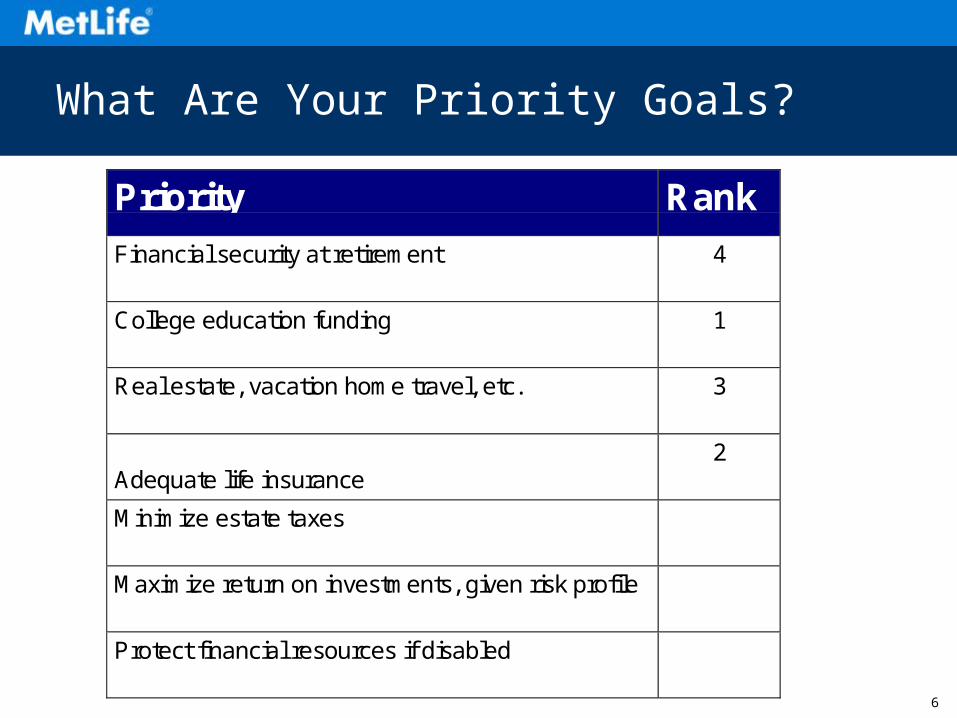

What Are Your Priority Goals?

Priority Rank

Financial security at retirement 4

College education funding 1

Real estate, vacation home travel, etc. 3

Adequate life insurance2

Minimize estate taxes

Maximize return on investments, given risk profile

Protect financial resources if disabled

7

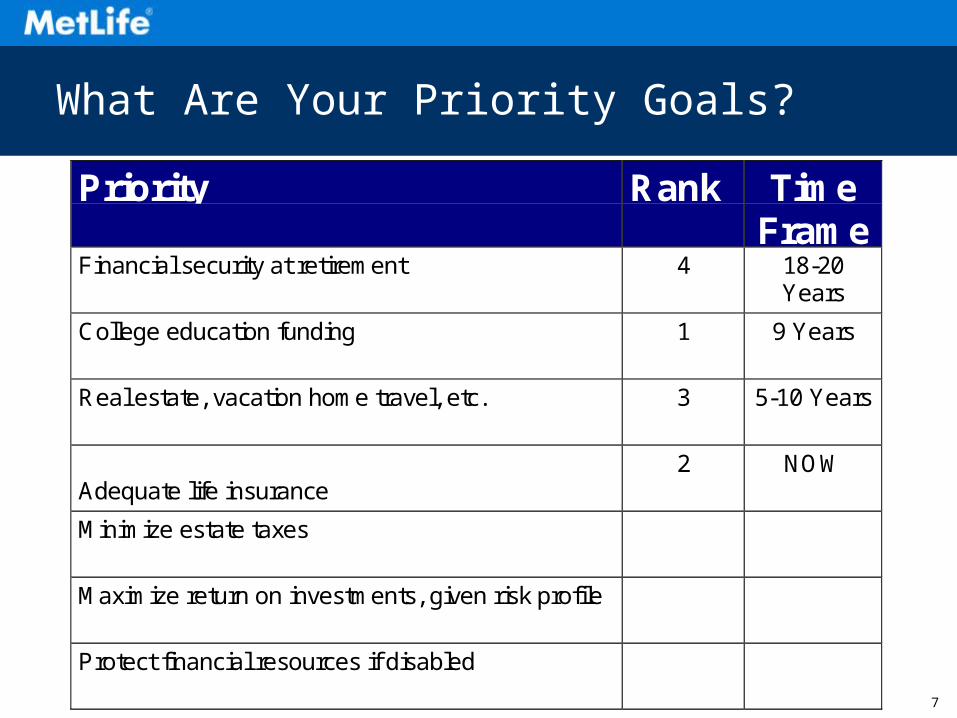

What Are Your Priority Goals?

Priority Rank TimeFrame

Financial security at retirement 4 18-20Years

College education funding 1 9 Years

Real estate, vacation home travel, etc. 3 5-10 Years

Adequate life insurance2 NOW

Minimize estate taxes

Maximize return on investments, given risk profile

Protect financial resources if disabled

8

How Are You Going to Achieve Your Goals?

• Current assets

• Additional savings and investments

• Earnings and compound earnings

9

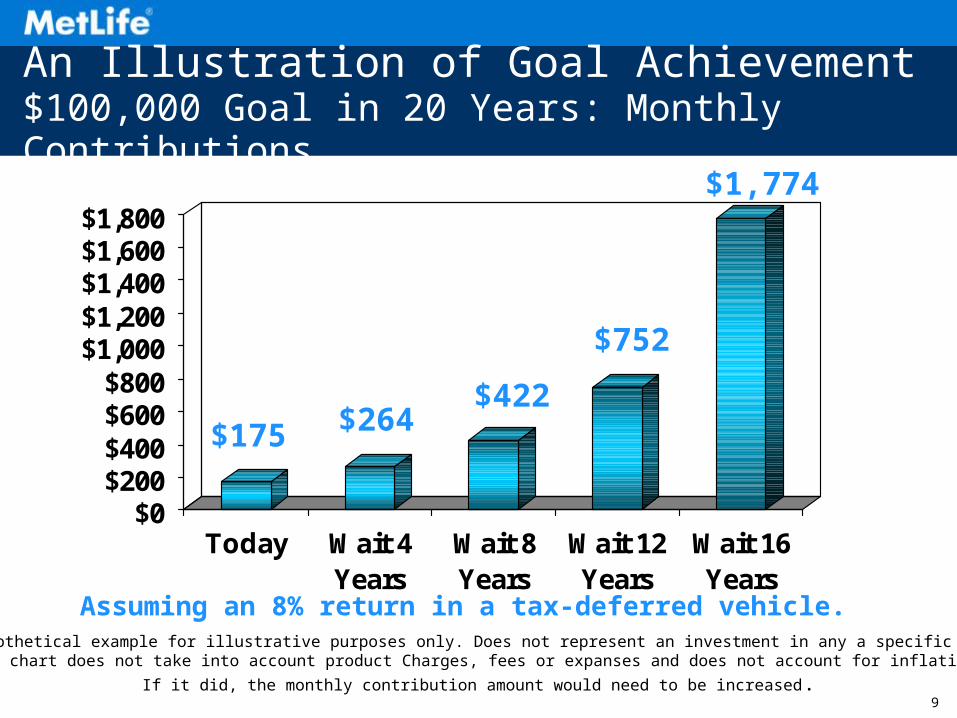

An Illustration of Goal Achievement$100,000 Goal in 20 Years: Monthly Contributions

$0$200$400$600$800

$1,000$1,200$1,400$1,600$1,800

Today Wait 4Years

Wait 8Years

Wait 12Years

Wait 16Years

Assuming an 8% return in a tax-deferred vehicle.

$175 $264$422

$752

$1,774

Note: Hypothetical example for illustrative purposes only. Does not represent an investment in any a specific product. This chart does not take into account product Charges, fees or expanses and does not account for inflation.

If it did, the monthly contribution amount would need to be increased.

10

What Are the Benefits of Financial Planning?

• Set your goals and prioritize them• Have a plan to help you achieve your goals• Learn to have more financial control and to take

advantage of investment opportunities• Prepare for the unexpected• Develop solid financial strategies• Get professional direction every step of the way• Work toward financial security for your:

– Estate (wills, trusts, tax issues, etc.)– Retirement plans– Employee Benefits

11

Getting Yourself Organized

• Personal statement of net worth

• Income and expense statement

12

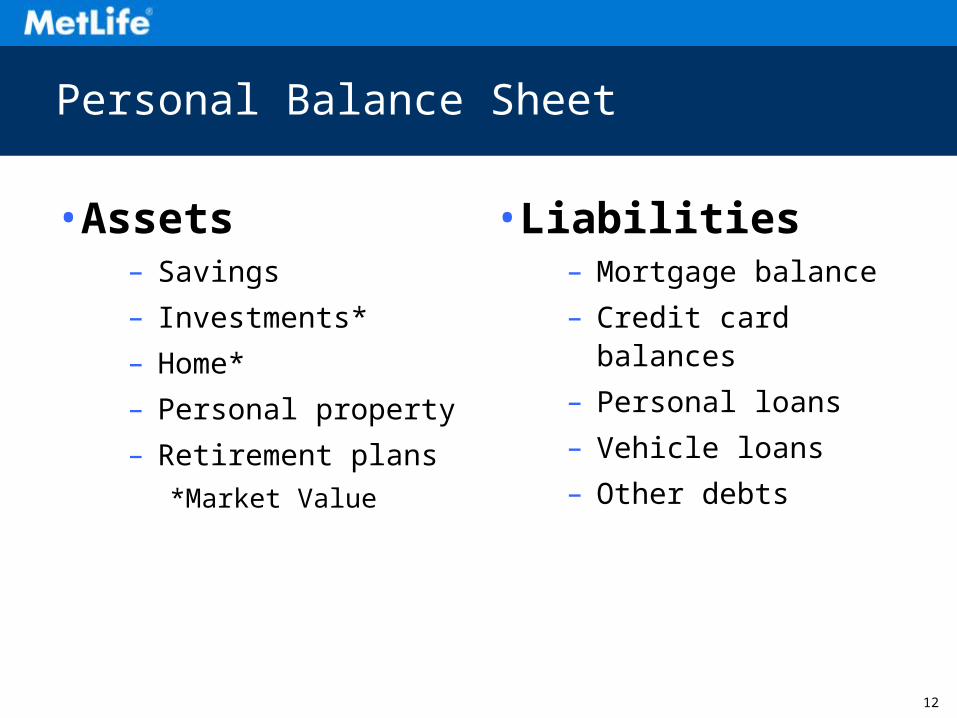

Personal Balance Sheet

• Assets– Savings

– Investments*

– Home*

– Personal property

– Retirement plans

*Market Value

• Liabilities– Mortgage balance

– Credit card balances

– Personal loans

– Vehicle loans

– Other debts

13

Three Ways to Increase Your Net Worth

• Save or invest more money

• Pay down debts

• Increase asset value through appreciation or reinvestment

14

Income & Expense Statement

• Income– Salary

– Savings and investment earnings

– Self-employment

– Social Security and pensions

• Expenses– Housing

– Transportation

– Food and clothing

– Medical and insurance

– Discretionary

– Personal

– Income and employment taxes

15

Income & Expense Statement: Example

Monthly IncomeWife - $2,900Husband - 2,900Interest onSavings - 200

Total - $6,000

Monthly ExpensesFood $ 725Clothing 380Personal Care 75Housing 1,240Transportation 400Discretionary 350Misc. income andemployment taxes 770

Total $4,200Discretionary cash flow:$1,800 per month

16

$0

$10,000

$20,000

$30,000

$40,000

$50,000

Year 5 Year 10 Year 15 Year 20 Year 30

Tax-Deferred at 5% Taxable at 5%

$10,000 investment that assumes a 28% tax bracket; does not take any other taxes into consideration.

Hypothetical example, for illustrative purposes only. Does not represent an investment in any specific product. *The $14,326 will be taxable at your federal and, if applicable, state rates upon withdrawal.

$14,326* Difference!

Impact of Taxes:Tax Deferred Vs. Taxable

17

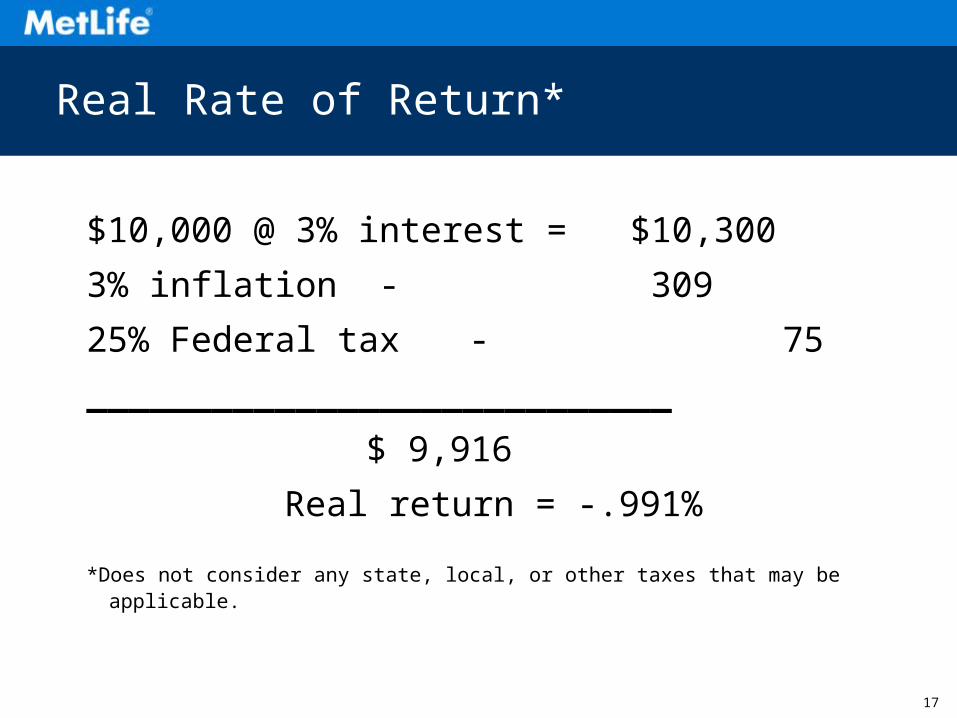

$10,000 @ 3% interest = $10,300

3% inflation - 309

25% Federal tax - 75

____________________________

$ 9,916

Real return = -.991%

*Does not consider any state, local, or other taxes that may be applicable.

Real Rate of Return*

18

In Summary

• Recognize that financial planning is a process, not a product. It can help you to:

– Determine where you are today and where you want to be in the future

– Get organized with a personal statement of net worth and income and expense statement

– Increase your net worth through new savings, paying down debt, and realizing appreciation on your assets

– Invest discretionary cash flow systematically for the future

– Take into account both inflation and taxes

©UFS

Pursuant to IRS Circular 230, MetLife is providing you with the following notification: The information contained in this document is not intended to (and cannot) be used by anyone to avoid IRS penalties. This document supports the promotion and marketing of financial products and services. You should seek advice based on your particular circumstances from an independent tax advisor.

MetLife, its affiliates, agents, and representatives may not give legal or tax advice. Any discussion of taxes herein or related to this document is for general information purposes only and does not purport to be complete or cover every situation. Tax law is subject to interpretation and legislative change. Tax results and the appropriateness of any product for any specific taxpayer may vary depending on the facts and circumstances. You should consult with and rely on your own independent legal and tax advisers regarding your particular set of facts and circumstances.

RR

Thank you for attending today’s seminar!