-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

1/24

Types of Foreign Exchange Rates and Interest rate.

International Transactions and Currency Values

The Balance of Payments

Measures transactions in the current and capital accounts.

The Current Account

1. Merchandise trade - value of exports and imports2. Service

balance - value of exports and imports of services.3. Unilateral

Transfers - gifts and foreign aid to foreign interests.

The Capital Account

1. Short-term capital flows - purchase of financial assets in

the money market with amaturity of less than one year. E.g.

T-bills

2. Direct investments - refers to the purchase of property or

the aquisition of ownershipshares in order to control a foreign

business.

3. Portfolio investments - purchases of securities to hold in

order to receive interest,dividends or capital gains.

Direct investments and portfolio investments represent purchases

of stocks, bonds and other

financial assets with a maturity of over 1 year. - Capital

market.

The BOP = 0

Since the U.S. runs a large current account deficit - over $200

billion in 1997 and expected to

reach nearly $300 billion in 1998, there is an offsetting

capital account surplus (with a bit of a

fudge)

This makes the U.S. the world's largest debtor nation when

looking at the difference between the

value of U.S. fiancial assets held by foreign investors and the

value of foreign assets held by U.S.

investors.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

2/24

Foreign investors are attracted to U.S. financial markets

because:

Develop production facilities in the U.S. to serve U.S. markets

(reduce transporationcosts) and to avoid import tariffs and quotas

(the average U.S. tariff on imports is about

3.5%). However, the U.S. is more restrictive on auto

imports.

The U.S. is very stable politically and economically - this is a

major attraction for foreigninvestors who can purchase U.S.

Treasury debt with zero default risk.

If conditions change in the U.S. there could be the same capital

flight that has plauged some of

the developing countries. In this case we could expect:

higher U.S. interest rates as the supply of loanable funds

decreases A sharp devaluation of the dollar A reduction in the

current account deficit as U.S. consumers purchase fewer

foreign

goods since the dollar has devalued. And U.S. goods become

cheaper abroad.

Exchange Rate Determination

Foreign exchange markets are amoung the largest markets in the

world with an annual trading

volume in excess of $160 trillion

It is an over-the-counter market, with no central trading

location and no set hours of trading.

Prices and other terms of trade are determined by computerized

negotiation.

There are three markets for foreign exchange:

Spot market - deals with currency for immediate delivery (within

one or two businessdays)

Forward market - involves the future (one, three or six months

from today) delivery offoreign currency

Currency futures and options market - deals in contract to hedge

against futurechanges in foreign exchange rates.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

3/24

Simple model of spot market exchange rates using supply and

demand

Current Account Factors

Changes in relative inflation rates, Changes in tastes, Factors

that determine comparative advantage.

Capital Account Factors

Changes in interest rates

Exchange rates can be

floating pegged floating peg

Floating exchange rates

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

4/24

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

5/24

Exchange rates are also affected by specualation over future

currency values. A currency that is

considered undervalued brings forth buy orders.

The Forward Market for Currencies

Investors, businesses and other involved in foreign currency

markets may want to guarentee the

exchange rate that they will receive at some time in the

future.

Take out a forward contract in the forward exchange market.

If the customer does not know if they will actually need the

foreign currency, they can take out

an option forward contract.

Methods of measureing and quoting forward exchange rates:

Outright rate - defines an exchange rate (e.g. 100 = $1)

Express the forward rate as a premium or discount from the spot

rate, know as the swap rate.

Express the forward rate as an annualized percentage rate above

or below the current spot rate

Functions of the Forward Exchange Market

Commercial Covering

For transaction of goods and services that are to be delivered

in the future.

e.g. U.S. importer of Japanese radios agrees to pay 1 million

for the shipment upon receipt in 30

days.

if current spot rate is 100 = $1, and stays constant, then will

cost importer $10,000

Importer faces the risk that the dollar will depreciate.

Takes out a 30-day forward contract for the delivery of 1

million at the forward market rate of

$.01/ (or 100 = $1).

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

6/24

When the 1 million payment is due by the importer, the importer

also takes delivery of the 1

million yen as given by the forward contract in exchange for

$10,000. The

1 million is then used to pay for the radio shipment.

Hedging of an Investment Position

Suppose there is a U.S.-based mutual fund (e.g. The Japan Fund)

that purchases Japanese stocks

and bonds for (primarily) U.S. investors.

The fund manager faces two types of risk:

market risk- the value of his or her assets will decline,

exchange rate risk- since the assets are denominated in yen, but

the value of theseassets are reported in dollars, a depreciation of

the yen will reduce the NAV of the

portfolio even if the yen value of the portfolio remains

constant.

To reduce exchange rate risk, the fund manager can hedge with

currency forwards.

Fund manager sells forward contracts of yen.

e.g. fear is that the yen will depreciate from 100 = $1

Managersells forward contracts worth 1 billion ($10m) at

exchange rate of 100 = $1.

When this forward contract matures, if the spot price of the yen

has depreciated to 120 = $1, the

fund can buy yen on the spot market and deliver them at the

contract price of 100 = $1.

Will cost the fund manager $8.3 million to purchase 1 billion

and then can sell yen for $10

million.

For a profit of $1.7 million on the foreign exchange

transaction.

If the fund manager sells contracts in an amount that covers

both principal and interest or

dividends, then the manager has "locked in" their investment

return regardless of which way

exchange rates go.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

7/24

If instead the yen were to appreciate, the currency trading

losses are offset by the increased

dollar value of the portfolio due to the yen's appreciation.

Speculation on Future Currency Prices

Speculators will buy currency for future delivery if they

believe the spot rate will be higher on

the delivery date than at the current forward rate

(appreciate).

Speculators will sell currency forward contracts if they believe

the spot rate will be lower on the

delivery date than at the current forward rate (depreciate).

Covered Interest Arbitrage

Arises when an investor invests in foreign securities because

the interest rate is higher than on

comparable domestic securities.

Covered Interest Arbitrage - reduce currency risk by using a

forward contract.

Currency Futures

While forward contracts usually result in the actual delivery of

the currency, futures contracts in

foreign currency are increasingly used. These contracts are

typically zeroed out and the currency

is not delivered.

e.g. you buy one ton of pork belly futures, rather than taking

delivery, you zero out the contract

by selling an opposite contract before the first contract

matures.

Note that as currencies appreciate in the spot market, the

market value of currency futures also

rise along with the market value of the underlying currency.

The Principle of Interest Rate Parity

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

8/24

the net rate of return to the investor from any foreign

investment is equal to the interest earned

plus or minus the forward premium or discount on the price of

the foreign currency involved in

the transaction.

Under normal circumstances, the forward discount or premium on

one currency relative to

another is directly related to the difference in interest rates

between the two countries involved.

The currency of a nation with the higher market interest rates

normally sells at a forward

discount in relation to the currency of the nation with lower

interest rates.

The currency of a nation with the lower market interest rates

normally sells at a forward

premium in relation to the currency of the nation with lower

interest rates.

Interest rate parity exists when the interest rate differential

between two nations exactly equals

the forward discount or premium of the two currencies.

When parity exists, the currency markets are in equilibrium and

there is no net flow of capital

funds between the two countries seeking a higher return.

In this case, the higher return from interest rates abroad is

fully offfset by the cost of covering

currency risk in the forward exchange market.

e.g. Interest rates in the U.S. are 3% higher than in Japan.

As a result, the dollar, when in equilibrium, sells at a 3%

discount in the forward exchange

market. While the yen sells at a 3% premium.

In this case, once currency risk is covered, there is no yield

benefit for Japanese investors to

purchase U.S. securities.

Unless, they also expected the prices of these U.S. securities

to rise.

When interest rate parity does not exist, then there are

international net capital flows.

**** e.g. Interest rates in the U.S. are 3% higher than in

Japan.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

9/24

And the dollar sells at only a 1% discount in the forward

exchange market.

Money flows from Japan to the U.S. as Japanese investors have a

net return of 2% after covering

for exchange rate risk.

Also the $ appreciates relative to the yen due to the increased

demand for dollars.

But if the dollar is considered overvalued, then expect it to

depreciate back to normal value.

Fearing the dollars depreciation, Japanese investors are selling

forward contracts on dollar,

increasing the discount on these contract and also increasing

the premium on contracts to buy

yen.

Comparing Expected returns on domestic and foreign assets

Assume that the spot exchange rate is 100 = $1 and the expected

exchange rate in one year

(EXe) is 105 = $1, a 5% increase in the value of the dollar.

Assume that the present yield on a one-year 100,000 Japanese

government bond equals 5%.

If you buy this bond, the cost in dollars is $1,000 that is then

converted to yen.

After one year, the value of the investment equals 105,000.

The expected dollar value of the investment is:

105,000/105 = $1,000

A general formula to compare total returns from investing $1 in

a domestic or foreign asset.

Value of $1 investment after one year = EX ( 1 + if) / EXe

where:

i = interest rate on the domestic security

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

10/24

if= interest rate on the foreign security EX = current exchange

rate EXe = expected future exchange rate

in this example:

(100 = $1)(1.05) / (105 / $1) = $1.00

can rewrite the formula so it divides the return into two parts,

interest and expected exchange

rate change:

Value of $1 investment after one year = 1 + if - (change)EXe /

EX

in our example the expected change in the exchange rate was 5%

as the yen depreciated from

100 = $1 to 105 = $1

Foreign-exchange Market Equilibrium

Would a situation in which investors could earn a higher

expected rate of return from buying

Japanese rather than U.S. assets persist for a long time? The

opportunity for traders in the foreign

exchange market to make a profit eliminates these

opportunities.

If a U.S. asset has a higher expected return than a comparable

Japanese asset, traders would sell

Japanese assets and buy the U.S. assets, increasing the demand

for dollars. As a result, the dollar

will appreciate relative to the yen to the point at which

investors are indifferent between holding

U.S. or Japanese assets.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

11/24

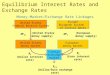

The concept is illustrated in the above graph.

The y-axis measures the current exchange rate (EX) The x-axis is

the expected rate of return, in dollar terms from investing in a

U.S. or

Japanese asset.

o for U.S. assets, the expected rate of return, R, equals the

U.S. interest rate io the expected rate of return on foreign assets

in dollar terms, Rf , equals if - (change)EX

e

/ EX.

For Japanese assets, the expected rate of return, Rf equals the

Japanese interest rate ifless the

expected appreciation of the dollar.

R is a vertical line because the return on U.S. assets is the

same regardless of the exchange rate.

Assume a U.S. interest rate of 5%

To graph Rfagainst the exchange rate, we must first specify the

expected future yen/dollar

exchange rate.

This is done by calculating the dollar's expected rate of

appreciation, a component of Rf .

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

12/24

If the current yen/dollar spot rate exceeds that expected future

exchange rate, investors believe

that the dollar is unually strong and it will eventually

depreciate.

For a given expected exchange rate, a graph of Rfagainst the

current exchange rate slopes

upward; as the yen/dollar exchange rate rises, the dollar's

expected rate of appreciation falls,

pushing up Rf.

the more the yen depreciates, the less we expect it to

depreciate in the future.

e.g assume that the future yen/dollar exchange rate is expected

to be 100 and that Japanese

interest rates are 5%.

a.

If the current exchange rate is also 100/$1, no dollar

appreciation is expected and Rfequals the 5% Japanese interest

rate.

b. If the current exchange rate is 105/$1, the dollar is

expected to depreciate back to100/$1 (for a decrease of 4.8%) and

Rfequals the 5% Japanese interest rate plus the

appreciation of the yen of 4.8% for a total of 9.8%.

c. If the current exchange rate is 97/$1, the dollar is expected

to appreciate back to100/$1 (for an increase of 3.1%) and Rfequals

the 5% Japanese interest rate minus the

depreciation of the yen of 3.1% for a total of 1.9%.

connecting these three points yields the Rfline.

The equilibrium exchange rate is the one that equates R and Rf .

In this case it is 100/$1

Suppose the exchange rate is 97/$1.

The dollar is expected to appreciate by 3.1%

Since the rate of return on Japanese assets is 1.9%, investors

switch to U.S. assets.

The increased demand for dollars leads to a dollar appreciation.

The appreciation of the dollar

continues as long as the relative yield on U.S. assets is

higher. Finally the yields are in

equilibrium at 100/$1.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

13/24

Interest Rate Parity

The exchange rate market condition described here is known as

the interest rate parity condition.

Given identical characteristics regarding risk, liquidity, time

to maturity, etc, domestic andforeign assets should have identical

nominal returns.

Any difference in the nominal rate of return between identical

assets in two countries reflects

expected currency appreciation or depreciation.

When the domestic interest rate is higher than the foreign

interest rate, the domestic currency is

expected to depreciate.

Equilibrium condition is: Expected return on domestic asset -

Expected return on foreign asset

i = if - (change)EXe / EX

This does not imply that nominal interest rates are the same

throughout the world. Rather that

expected nominal returns on comparable domestic and foreign

assets are the same.

In real terms, the real interest rate parity condition is:

i + r = (1 + rf)(EXr/ EXer)

Expected real return on domestic investment = expected real

return on foreign investment.

Exchange Rate Fluctutations

Changes in domestic real interest rates

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

14/24

The expected return on domestic bonds depends on the interest

rate i.

That interest rate is the sum of the expected real rate of

interest and the expected rate of inflation

Holding expected inflation constant, an increase in the domestic

interest rate increases the

expected rate of return on domestic assets, shifting the R curve

to the right.

The increased demand for dollars leads to an appreciation of the

dollar.

Changes in domestic expected inflation

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

15/24

Hold foreign real rate of return Rfconstant

If domestic inflatonary expectations increase, then domestic

currency loses purchasing power,

causing it to depreciate.

Two things happen:

1. The higher domestic nominal interest rate shifts the expected

rate of return to the right(foreign investors will not be affected

by the domestic inflation increase but have the

benefits of higher return on assets). As a result, the current

exchange rate rises.

2. An increase in expected inflation reduces expected

appreciation of the domestic currency,so the expected foreign rate

of return shifts to the right, increasing the attractiveness of

foreign assets to consumers.

Although the two effects work in opposite directions, we can

usually expect the domestic

currency to depreciate with higher inflation.

Changes in foreign interest rates

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

16/24

An increase in the foreign real interest rate shifts the foreign

expected rate of return from Rf0 to

Rf1 because at any exchange rate, the foreign rate of return

increases.

Currency depreciates as money moves abroad.

Changes in the Expected Future Exchange Rate

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

17/24

If the expected future exchange rate increases, expected

appreciation of the domestic currency

rises.

Since an appreciation of the domestic currency is good for the

value of domestic assets, investors

increase their demand for the domestic currency.

And the expected rate of return on the foreign assets falls due

to the relative depreciation of that

currency shift inward the return on foreign assets.

Resulting in an increase in the actual exchange rate.

Currency Premiums in Foreign-Exchange Markets

The interest rate parity condition is based on the assumption

that domestic and foreign assets

with similar attributes are perfect substitutes.

But if we allow for imperfect substitutability, we can modify

the equation to allow for a currency

premium where investors have a preference for the financial

assets denominated in one currency

over the other.

i = if - (change)EXe / EX - hf,d

For example, assume that the one year T-bill rate in the U.S. is

8% and the one-year government

bond rate in Germany is 5%.

Also assume that investors expect the dollar to depreciate

against the mark by 4% over the

coming year.

The one-year mark/dollar currency premium is

8% = 5% - ( -4%) - hf,d , or hf,d= 1%

This implies that investors require a 1% higher expected rate of

return on the German bond

relative to the U.S. T-bill to make the two financial assets

equally attractive.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

18/24

If hf,dis positive, it implies that investors prefer the

domestic currency asset.

In this case, investors will not buy a foreign bond if the

expected rate of return just equals that of

a domestic bond.

Investors require an additional incentive to buy the foreign

asset, the currency premium in the

form of a higher yield on foreign assets.

The size of the currency premium depends on:

investors aversion to currency risks, differences in liquidity

in markets

information about foreign investment opportunities investors'

belief that one currency is more stable or safer than another.

Traditional view of exchange rates results in adjustments to

international trade in goods. Other

approaches include the capital account as a determinent of

exchange rates.

Explore the role of financial assets.

Monetary Approach to the Balance of Payments

The basic premise of the MABP is that any balance-of-payments

disequilibrium is based on

monetary disequilibrium.

The exchange rate between any two currencies is determined by

relative money demand andmoney supply between the two

countries.

Monetary disequilibrium implies a difference exists between the

amount of money people wish

to hold and the amount supplied by the monetary authorities.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

19/24

If people demand more money than is supplied domestically by the

central bank, then the excess

demand for money would be satisfied by inflows of money from

abroad.

In contrast, an oversupply of money domestically, leaves the

economy for other countries.

The Fed controls the money supply by altering base money (equal

to banking reserves plus

currency in circulation). Increases in the monetary base leads

to increases in the money supply.

The monetary base can be divided into domestic and international

components:

domestic component is comprised of domestic credit. the

remainder is comprised of international reserves. (money items that

can be used to

settle international debts, primarily foreign exchange)

Example: A U.S. exporter receives payment in foreign

currency

payment is presented to a commercial bank to be converted into

dollars and deposited inthe firm's account.

If the commercial bank has no use for the foreign currency, the

bank will exchange theforeign currency for dollars with the

Fed.

The Fed creates new money to buy the foreign currency by

increasing the commericalbank's reserve deposit with the Fed (part

of required reserves).

Thus the Fed is accumulating international reserves, and this

process expands themonetary base.

Note: the Fed make undertake currency sterilization by using

monetary policy tools to absorb

the increase in reserves from the banking system.

The Model:

Assume a small open economy that has no effect on the

international price of goods or the

interest rate it faces in foreign markets.

The demand for money equals:

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

20/24

L = kPY

where:

L = money demand

P = domestic price level Y = real income or wealth k= constant

fraction indicating how much money demand will change given a

change in

P or Y

If increase P and/or Y will increase L

The supply of money equals:

M = R + D

where:

M = money supply R = international reserves D = domestic

credit

Assume equilibrium in the money market of M = L

The adjustment mechanism that ensures equilibrium of M = L will

vary with the exchange rate

regime.

With fixed exchange rates, money supply adjusts to money demand

through internationalflows of money via balance-of-payments

imbalances.

With flexible exchange rates, money demand will be adjusted to a

money supply set bythe central bank via exchange rate changes.

With a floating peg, there are both international monetary flows

and exchange ratechanges.

skipping some mathematical steps, we have:

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

21/24

With Flexible Exchange Rates:

- E = PF + Y - D

P

F

= foreign prices

all variables are in percentage changes (e.g. E is percentage

change in the exchange rate)

(note the negative before the E)

and assume reserve flows (R) equal zero

Implications:

E is measured in domestic currency units per foreign currency

unit, as increase in E means that

foreign currency is becoming more expensive or appreciating in

value and the domestic currency

is depreciating.

e.g. at E0, $1 = 100

at E1, $1 = 90

In the equation, E has a positive relation to changes in D and

an inverse relation to changes in PF

and Y.

an increase in the domestic credit (D) given a constant PF and Y

(so that the demand for money

is constant) will result in a depreciation of the domestic

currency. The increase in the money

supply leaves the country.

An increase in PF will increase the domestic demand for money as

imports become more costly.

With constant domestic credit, there is an excess demand for

money. Individuals try to increase

their money balances, increasing the demand for domestic

currency. There is a decrease in E or

an appreciation of the domestic currency.

With Fixed Exchange Rates:

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

22/24

R - E = PF + Y - D

all variables are in percentage changes (e.g. E is percentage

change in the exchange rate)

R = international reserves

This is the same as before, but reserves are used to offset

changes in the exchange rate. If a

currency is devaluing below desired levels, the central bank

will intervene buy purchasing its

domestic currency with some of its foreign currency

reserves.

for example, an increase in domestic credit, D, everything else

constant, will lead to a decrease in

international reserves as the central bank buys the domestic

currency to support its value.

Portfolio-balance Approach to the Balance of Payments

In the monetary approach, the exchange rate between any two

currencies is determined by

relative money demand and money supply between the two

countries. Relative supplies of

domestic and foreign bonds are not a factor.

The portfolio-balance approach allows for both relative money

market condition and for bond

markets to determine the exchange rate.

The monetary approach assumes that domestic and foreign bonds

are perfect substitutes and thus

investors are indifferent as to which ones they hold. Bond

holders only care about relative rates

of return and require no risk premium to hold foreign bonds.

In the portfolio-balance approach foreign and domestic bonds are

imperfect substitutes. Savers

have preferences in how they distribute their portfolio over

different country's assets. As

investors increase their allocation of portfolio assets in a

given country, their risk rises and they

desire a greater risk premium to compensate.

The PB approach assumes that assets are imperfect substitutes

internationally because investors

percieve foreign exchange risk to be attached to

foreign-currency-denominated bonds.

The spot exchange rate is modified to:

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

23/24

- E = PF + Y - D - B + BF

all variables are in percentage changes

B = percentage change in the supply of domestic bonds

BF = percentage change in the supply of foreign bonds

If the supply of domestic bonds rises relative to the supply of

foreign bonds (increase B holding

BF constant), there will be an increased risk premium on the

domestic bonds that will cause the

domestic currency to depreciate in the spot market.

But we also need to consider adjustments to international trade

in financial assets.

Since financial assets are traded almost continuously, exchange

rates constantly adjust as

changes in demand and supply of financial assets in diffierent

nations change.

Assume perfect capital mobility => capital will flow freely

between nations because there are no

significant transactions costs or capital controls that act as

barriers to investment.

In this case, spot and forward exchange rates will adjust

instantly to changing financial market

conditions.

-

7/27/2019 Types of Foreign Exchange Rates and Interest

rate.docx

24/24

In this case, relative bond supplies and demands as well as

relative money market conditions

determine the exchange rate.

Conclusion

The exchange rate of the currency in which a portfolio holds the

bulk of its investments

determines that portfolio's real return. A declining exchange

rate obviously decreases the

purchasing power of income and capital gains derived from any

returns. Moreover, the exchange

rate influences other income factors such as interest rates,

inflation and even capital gains from

domestic securities. While exchange rates are determined by

numerous complex factors that

often leave even the most experienced economists flummoxed,

investors should still have some

understanding of how currency values and exchange rates play an

important role in the rate of

return on their investments.

http://www.investopedia.com/terms/c/capitalgain.asphttp://www.investopedia.com/terms/c/capitalgain.asp