Embed Size (px)

Citation preview

Two Standard and Defensible Approaches for Valuing the Common Stock of EarlyStage, PrivatelyHeld Companies That 1

Have Issued Only Common and Convertible Securities 2

By Jeron Paul, Dan Eyman, Scott Lockhart, Trent Read, and Matt Stapleton 3 4 5 6 7

Executive Summary Valuing private companies with limited or no financial traction that have only issued common and convertible securities presents both practical and technical problems for founders, service providers, and the IRS. Currently, no standard or widelyaccepted approaches exist leaving practitioners to implement a wide array of possible approaches. As practitioners consider approaches, they are often looking for the least problematic methodology rather than one that will provide the most accurate result. Many of the more commonlyused approaches are complicated, hard to defend, and can lead to auditrelated issues and problems for all parties involved. Even if a valuation analyst can produce a defensible approach to arrive at an enterprise or equity value of the subject company, there is no consistency in how to treat the convertible security in the equity allocation step of the valuation. In this paper, we discuss the limitations and benefits of current approaches and propose two approaches that could lead to simplification and standardization of such valuations, while in some cases increasing accuracy of the concluded value. We hope that adoption of these approaches could lead to simplification and standardization and ultimately decrease valuation costs for earlystage companies and their valuation analysts. The approaches that we suggest are:

A market approach based on a probabilityweighted backsolve option pricing model A cost approach based on adjusted book value or cost to build or recreate

1 We define “earlystage” in this white paper as a company with only the earliest customer adoption and little or no revenue. 2 Convertible securities as we are using the term in this paper includes convertible debt as well as nondebt convertibles like SAFE or KISS securities. 3 Jeron Paul is the Founder and CEO of Capshare, Inc., and the Founder and former CEO of Scalar Analytics. 4 Dan Eyman is the Founder and Managing Partner of Meld Valuation. 5 Scott Lockhart, CPA/ABV, is the Founding Partner of Tower49 and the Founder of Simple409A. 6 Trent Reed is a Managing Director of Greener Equity. 7 Matt Stapleton is a Founder and the President of Capshare, Inc.

The Problem Most USbased private companies need a valuation of common stock when they begin to issue stock options. The United States Internal Revenue Code sections 422 and 409A require that companies issuing stock options set the strike price of those options at fair market value or risk incurring significant tax penalties. Audited private companies also need to expense their stock 8

options according to accounting standard ASC 718. Complying with these requirements necessitates finding and justifying a fair market value of the company’s stock. Most private companies do not have the inhouse expertise to do this and typically seek service and guidance from qualified valuation professionals. Earlystage private companies (especially startups) have a high failure rate and often very little 9

cash. For these reasons, they have a very low tolerance for spending money that doesn’t directly relate to increasing their probability of success. So earlystage companies typically want to minimize any compliance costs even more than their betterfunded laterstage peers. Finding standardized, simple, and defensible valuation approaches can help lower compliance costs. However, valuing an earlystage company with no real financial traction is difficult. Most of the current approaches do not work well in either the equity valuation or the equity allocation steps of the valuation. Problems in the Equity Valuation Step In developing an equity valuation, guideline company and guideline transaction methodologies fail if the company has limited or no financial results against which to apply the guideline data and multiples. Income approaches can produce an indication of value but require many assumptions and significant use of estimates. It’s often easy to confuse increased complexity with increased precision, and the income approach for earlystage companies can often be an exercise of complex modeling with imprecise and unsupported assumptions. One of the easiest and most defensible approaches is to value the earlystage company based on any recent securities transactions in the company’s stock. If a standard equity investment has occurred, valuation professionals can use a broadlyaccepted approach like a Backsolve Option Pricing Method. Valuation experts frequently consider this approach one of the best conceptually because it bases a valuation of the company on a recent objective transaction in the closest possible company “comparable”the company’s own securities.

8 Detailing specifics of 409A/422 compliance including potential penalties goes beyond the scope of this white paper. Capshare has written an article on the topic or you can learn more on the 409A Wikipedia page. 9 Most industry experts believe that between 65 and 75% of startups fail.

Increasingly, however, the earlieststage companies are raising money through convertible securities and not through equity. Convertible securities are designed to bridge gaps in the valuation estimates between market participants at the time of financing, and thus by their nature provide little help in providing a single indication of the market value of the company. Another relatively easy approach is to use a cost method. However, as we will discuss below, valuation experts often consider cost methods to be a last resort for valuing goingconcern companies. Problems in the Equity Allocation Step Even if a standard approach existed for handling equity valuation, there are no standardized approaches for handling convertible securities in any kind of an equity allocation method like a waterfall, CVM, PWERM or OPM (collectively representing the equity allocation step of the valuation). Some valuation analysts model the convertible securities as debt and others model them as equity.

Goal of This Paper Before making our recommendations regarding a possible solution for this problem, we recognize that:

1. It is likely impossible to codify a standard valuation approach and process that is accurate and relevant in every possible scenario,

2. We have no formal authority to establish any kind of accounting or generally applicable valuation standard, and

3. Actually performing a valuation requires practical knowhow and judgment that goes beyond the generic guidance contained in most accounting and valuation standards

Our goal in this paper is to propose an acceptable approach for most but not all cases. We are not trying to establish a “standard” in the same sense that FASB creates accounting standards but rather are trying to propose a practical and repeatable approach that will be useful to earlystage companies and their valuation firms. We had the following goals in looking for acceptable approaches:

They should be defensible and consistent with published valuation standards They should be consistent with the understanding of market participants They should be as simple as possible without compromising the other goals

In writing this paper, we seek feedbackespecially from auditorsso that we can create a more defensible approach.

Understanding Convertible Securities Convertible securities have always been an important tool for investors. Historically, investors referred to these instruments as “bridge notes” and used them to fund a company’s shortterm

costs to keep the company solvent until it could raise a formal equity round. The term “bridge” highlighted the temporary nature of the investment. Over time, investors used “bridge” notes to fund companies in more cases rather than bridge financings to a next round because they found the process easy, fast, and inexpensive relative to priced equity investments. As this happened, market participants often referred to these instruments as “convertible debt” or “convertible notes” rather than “bridge notes.” Many investors and companies found convertible debt problematic because it gave the investor an ability to foreclose on a company in the case where the company could not repay the debt. This was generally not the intention of the investors and companies found this possibility unfriendly and frightening. In response to this concern and a few others, pioneering lawyers began to work on new securities that would have all of the benefits of convertible debt without any debtrelated drawbacks. These lawyers created new kinds of nondebt convertible securities. In December of 2013, Carolynn Levy, a partner at Y Combinator who had previously worked on standardizing financing docs for startups at Wilson Sonsini, introduced the SAFE, or Simple Agreement for Future Equity. The SAFE eliminated many of the perceived problems of convertible debt while preserving the benefits. Since then, other investor groups have introduced similar nondebt, convertible securities agreements like 500 Startups’ equity KISS document. After these innovations, usage of convertible securities including convertible debt has increased among startups. Because of this development, convertible securities can be either debt instruments or a type of equity futures contract. While nondebt convertible securities have become increasingly popular over the past 3 years, many market participants still use convertible debt. Convertible securities (both debt and nondebt) are typically shortterm investment instruments with an ability to convert into a future round of equity financing. Depending on the preferences of the market participants involved, these instruments can feature debtlike properties, including interest, maturity dates, and liquidation preference seniority, or not. There are several advantages to using convertible securities instead of equity:

Market participants can agree to an investment amount without agreeing to a valuation They allow companies to raise money from investors at different prices Legal costs are low Market participants can understand and negotiate terms quickly

While some prominent investors have pointed to disadvantages associated with convertible notes, over time there has been dramatic enough adoption of convertible notes that prominent investor Paul Graham tweeted in August 2010, “Convertible notes have won. Every investment so far in this YC batch (and there have been a lot) has been done on a convertible note.” From a valuation perspective, convertible securities can still be complex. Convertible securities often have warrant coverage, discount conversions, and/or valuation caps. Unless there is a valuation cap, these securities provide little information that would indicate an agreed upon

valuation by the market participants. One of the primary features of convertible securities is that they are designed to facilitate investments without an explicit agreement on company valuation. If a valuation cap is present, it may provide some valuation information, though the usefulness is debatable. Sophisticated valuation professionals have differing opinions how to use valuation cap information. Dan Eyman (a coauthor of this paper) at Meld Valuation has written a white paper where he argues that you can logically take a position either that 1) the valuation cap provides no “known or knowable” information about the valuation of the company or 2) that the valuation cap provides a reasonable estimate of the current valuation of the company. There is also some uncertainty about how to handle convertible securities in the waterfall portion of any equity allocation analysis. Some valuation analysts model the security as debt, especially if it is debt or has debtlike features. Others choose to model the security as equity. We believe that market participants’ view of the security is that convertible securities are essentially equity. In the case of nondebt convertible securities, it seems obvious that market participants do not consider these instruments debt. After all, these instruments are often used to avoid debtlike terms. The very name of the SAFE instrument (Simple Agreement for Future Equity (our emphasis)) implies that the creators view it as an equity instrument. Even in the case of convertible debt, the market participants involved in the deal fully expect the debt to convert into equity in the vast majority of cases. In a blog post on the topic, the wellrespected valuation firm Teknos stated in part:

“When we value of a company with a convertible note in its capital structure, we treat the convertible note as “equity,” not as “debt”; that is, we assume that the note will be converted, not repaid. This matches the expectations of the issuing company and the investors which both anticipate that the note will convert.

We agree with this position. Further, the actual and expected returns of convertible security investments could arguably exceed those of equity investments and, at a minimum, will be much closer to equity returns than debt returns. So we believe that, whenever practical, valuation analysts should prefer methods that model convertible securities as equity rather than debt investments.

Review of Existing Valuation Standards Before looking for ways to simplify and standardize valuation approaches, we searched existing GAAP and valuation standards for related insights. The first and most obvious standard would be a standard identified in GAAP (or generally accepted accounting principles in the United States). ASC 820 addresses fair value measurements and some of the information is 10

10 This document will only address the valuation and accounting issues affecting companies seeking to comply with the laws and regulations of the United States.

applicable to general valuation approaches but ASC 820 does not address the particular issues associated with valuing a company’s common stock as a form of equity compensation. Other broad valuation standards exist. Valuation practitioners and other standardsetting bodies often reference the Uniform Standards of Professional Appraisal Practice (USPAP) established by the Appraisal Standards Board. But again, USPAP does not offer any specific guidance related to our particular valuation scenario. The most widelyaccepted valuation reference for valuing the common stock of private companies is the AICPA’s “Valuation of Privately Held Company Equity Securities Issued as Compensation.” Valuation professionals often refer to this guide as the “cheap stock” guide. Section .08 of the cheap stock guide emphasizes the lack of GAAP standards for valuing privately held equity securities issued as compensation:

“In the context of discussing valuation issues or concepts, no specific valuation standards exist that address detailed aspects when valuing privately held company equity securities issued as compensation.”

Section .01 of the cheap stock guide also states:

“This guide is not intended to serve as a detailed “how to” guide, but, rather, to provide (a) an overview and understanding of the valuation process and the roles and responsibilities of the parties to the process and (b) best practice recommendations.”

So while the cheap stock guide is the best resource for finding what the AICPA thinks about different approaches for valuing private companies, it is not a howto guide. Further, the cheap stock guide does not address valuation of convertible securities transactions anywhere in the document.

Possible Valuation Approaches Though no standards exist, valuation professionals are performing these valuations every day. Collectively, the authors have performed or reviewed thousands of these valuations. Based on our experience the most commonlyused approaches are:

Asset/costbased approaches (typically using invested capital) Discounted cash flow (DCF) approaches Backsolve approaches

We will review each of these approaches, discuss the pros and cons of each, identify limitations with existing methods, and identify the approaches we feel work the best.

Asset/Cost Approaches Asset/cost approaches assume that the value of a company is equal to the value of the company’s assets. There are many variants of this approach including using the book value of the company’s assets, assuming the value of the company is equal to the total amount of capital invested into the company, finding the cost to build or recreate the company, etc. We will give more detailed examples of the following (commonly used) approaches:

Invested capital Market adjusted book value Cost to build or recreate

As we go through examples, let’s assume the following about the convertible security the company is using:

It is a convertible note issued on 3/1/2016 Face value of $1,000,000 Simple interest at 8% per annum Maturity in 1 year Valuation cap of $10,000,00 or a conversion discount of 20% Management and investor’s best guess is that the company will ultimately raise a

followon round of $5M in one year and that the round is expected to occur at or above the note’s $10,000,000 valuation cap

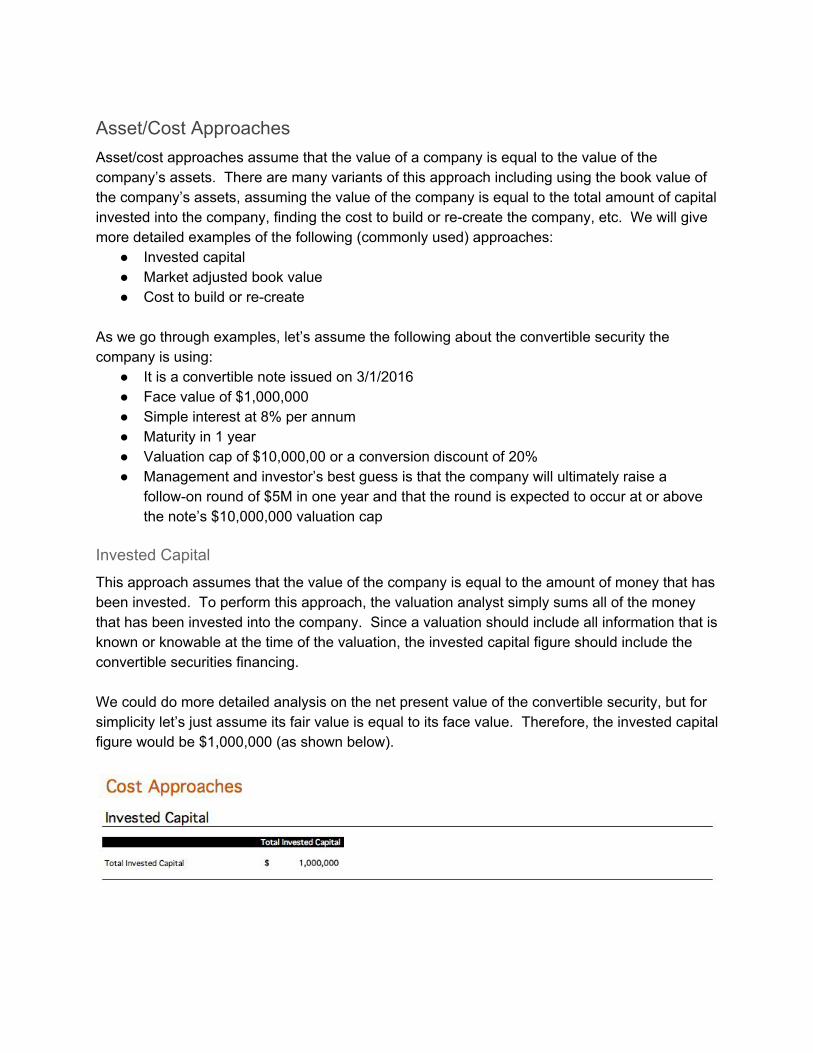

Invested Capital This approach assumes that the value of the company is equal to the amount of money that has been invested. To perform this approach, the valuation analyst simply sums all of the money that has been invested into the company. Since a valuation should include all information that is known or knowable at the time of the valuation, the invested capital figure should include the convertible securities financing. We could do more detailed analysis on the net present value of the convertible security, but for simplicity let’s just assume its fair value is equal to its face value. Therefore, the invested capital figure would be $1,000,000 (as shown below).

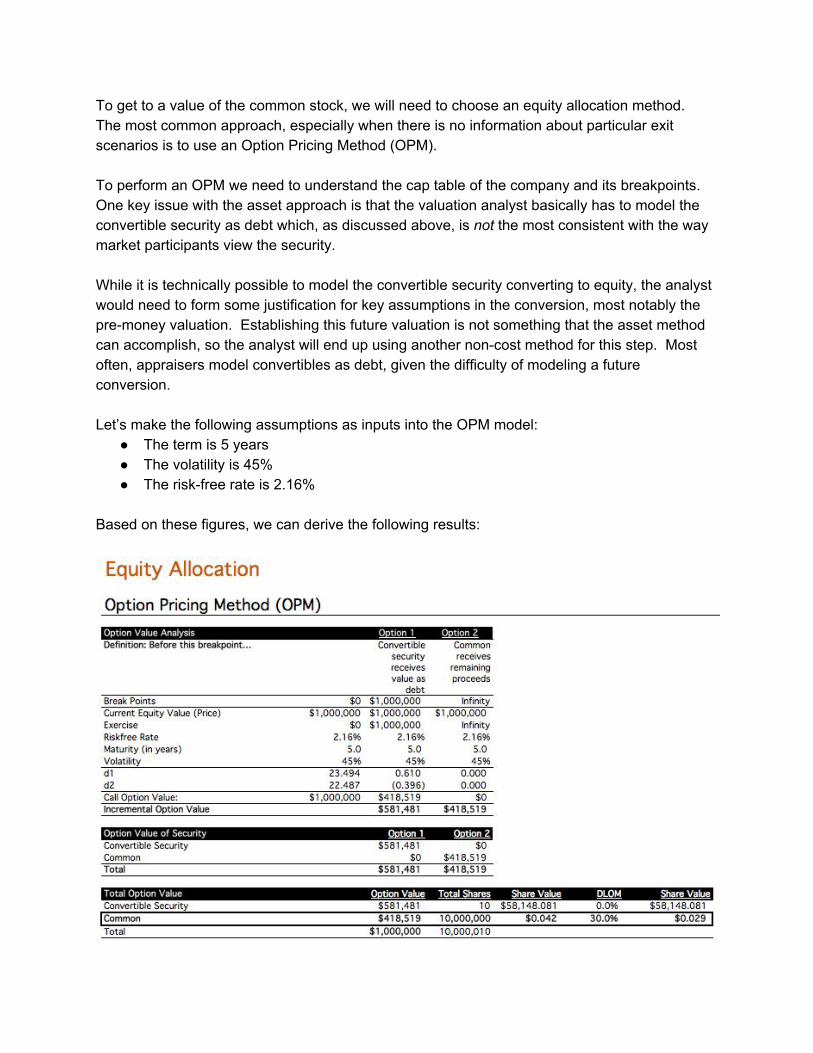

To get to a value of the common stock, we will need to choose an equity allocation method. The most common approach, especially when there is no information about particular exit scenarios is to use an Option Pricing Method (OPM). To perform an OPM we need to understand the cap table of the company and its breakpoints. One key issue with the asset approach is that the valuation analyst basically has to model the convertible security as debt which, as discussed above, is not the most consistent with the way market participants view the security. While it is technically possible to model the convertible security converting to equity, the analyst would need to form some justification for key assumptions in the conversion, most notably the premoney valuation. Establishing this future valuation is not something that the asset method can accomplish, so the analyst will end up using another noncost method for this step. Most often, appraisers model convertibles as debt, given the difficulty of modeling a future conversion. Let’s make the following assumptions as inputs into the OPM model:

The term is 5 years The volatility is 45% The riskfree rate is 2.16%

Based on these figures, we can derive the following results:

This approach will yield a valuation of the common stock at $0.029.

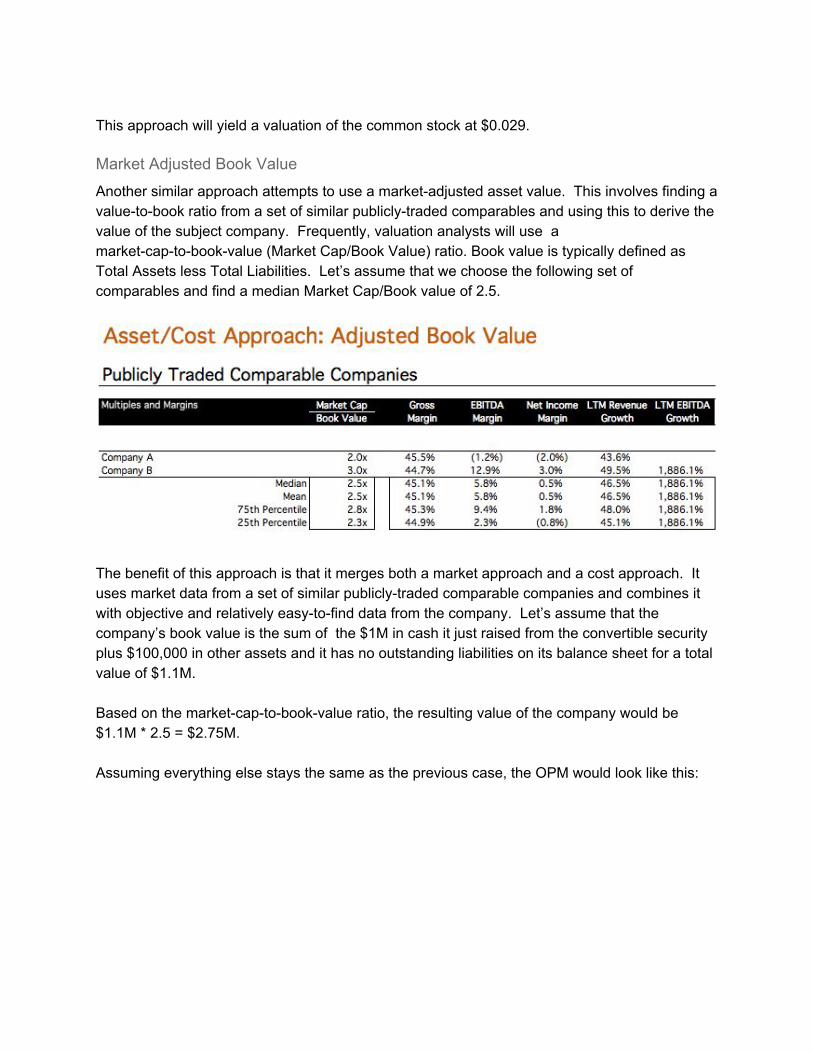

Market Adjusted Book Value Another similar approach attempts to use a marketadjusted asset value. This involves finding a valuetobook ratio from a set of similar publiclytraded comparables and using this to derive the value of the subject company. Frequently, valuation analysts will use a marketcaptobookvalue (Market Cap/Book Value) ratio. Book value is typically defined as Total Assets less Total Liabilities. Let’s assume that we choose the following set of comparables and find a median Market Cap/Book value of 2.5.

The benefit of this approach is that it merges both a market approach and a cost approach. It uses market data from a set of similar publiclytraded comparable companies and combines it with objective and relatively easytofind data from the company. Let’s assume that the company’s book value is the sum of the $1M in cash it just raised from the convertible security plus $100,000 in other assets and it has no outstanding liabilities on its balance sheet for a total value of $1.1M. Based on the marketcaptobookvalue ratio, the resulting value of the company would be $1.1M * 2.5 = $2.75M. Assuming everything else stays the same as the previous case, the OPM would look like this:

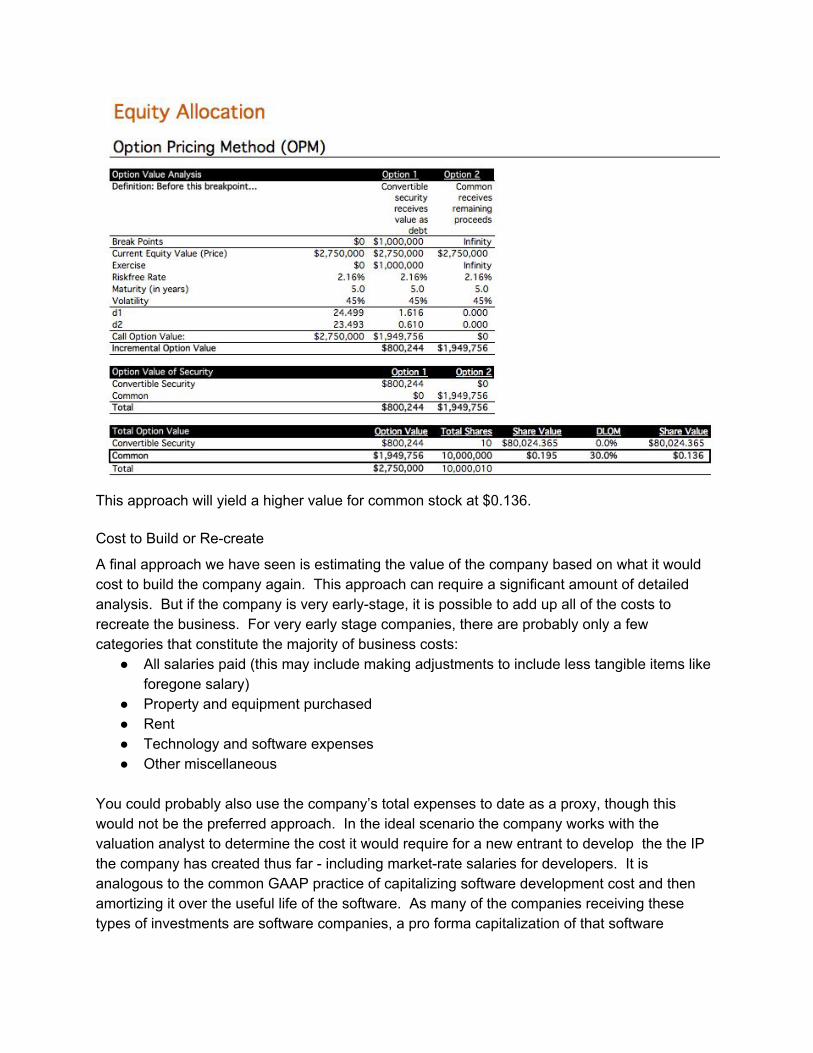

This approach will yield a higher value for common stock at $0.136.

Cost to Build or Recreate A final approach we have seen is estimating the value of the company based on what it would cost to build the company again. This approach can require a significant amount of detailed analysis. But if the company is very earlystage, it is possible to add up all of the costs to recreate the business. For very early stage companies, there are probably only a few categories that constitute the majority of business costs:

All salaries paid (this may include making adjustments to include less tangible items like foregone salary)

Property and equipment purchased Rent Technology and software expenses Other miscellaneous

You could probably also use the company’s total expenses to date as a proxy, though this would not be the preferred approach. In the ideal scenario the company works with the valuation analyst to determine the cost it would require for a new entrant to develop the the IP the company has created thus far including marketrate salaries for developers. It is analogous to the common GAAP practice of capitalizing software development cost and then amortizing it over the useful life of the software. As many of the companies receiving these types of investments are software companies, a pro forma capitalization of that software

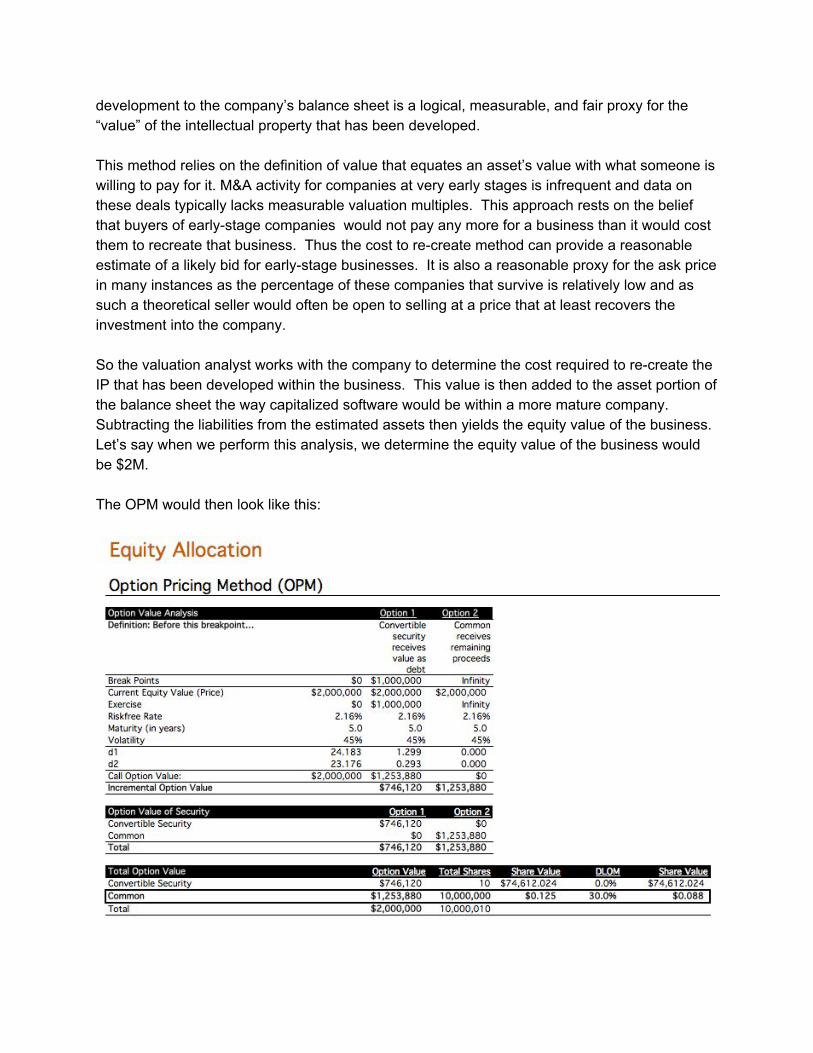

development to the company’s balance sheet is a logical, measurable, and fair proxy for the “value” of the intellectual property that has been developed. This method relies on the definition of value that equates an asset’s value with what someone is willing to pay for it. M&A activity for companies at very early stages is infrequent and data on these deals typically lacks measurable valuation multiples. This approach rests on the belief that buyers of earlystage companies would not pay any more for a business than it would cost them to recreate that business. Thus the cost to recreate method can provide a reasonable estimate of a likely bid for earlystage businesses. It is also a reasonable proxy for the ask price in many instances as the percentage of these companies that survive is relatively low and as such a theoretical seller would often be open to selling at a price that at least recovers the investment into the company. So the valuation analyst works with the company to determine the cost required to recreate the IP that has been developed within the business. This value is then added to the asset portion of the balance sheet the way capitalized software would be within a more mature company. Subtracting the liabilities from the estimated assets then yields the equity value of the business. Let’s say when we perform this analysis, we determine the equity value of the business would be $2M. The OPM would then look like this:

This approach will yield a value of common stock at $0.088.

Pros and Cons of Asset/Cost Approaches These cost approaches certainly have some benefits. The approaches use easily available, objectively verifiable data and the valuations are often easy to perform. Conceptually, most valuation experts take issue with asset/cost approaches by pointing out the most businesses are worth much more than the sum of their tangible parts. The following sources of value are often ignored or underestimated in asset/cost approaches:

Brand value or reputational effects Market and competitive dynamics (network effects, competitive dynamics, firstmover

advantages) IP and other forms of intangible value

However, one could argue that earlieststage companies probably have not had the time or ability, as evidenced by their lack of financial results, to create much value in any of the categories mentioned above. Most general valuation guidelines indicate that you should only use this kind of approach if a company is no longer a going concern. For example, the cheap stock guide emphasizes: 11

Of the three approaches to valuing an operating enterprise and its securities under a going concern premise of value, the asset (or assetbased) approach, under most circumstances is considered to be the weakest from a conceptual standpoint. It may, however, serve as a “reality check” on the market and income approaches and provide a “default value” if the available data for the use of those other approaches are fragmentary or speculative. The asset approach is typically more relevant for valuing enterprises and the securities within the enterprise in the earliest stages of development, prior to raising arm’slength financing, when there may be limited (or no) basis for using the income or market approaches. The use of the asset approach is generally less appropriate in the later stages of development once an enterprise has generated significant intangible and goodwill value.

So the cheap stock guide highlights that the asset or cost approach is generally the weakest from a conceptual standpoint but that it may provide a “default value” if:

Available data for other approaches are fragmentary or speculative The company is in the earliest stages of development The company has not raised an arm’s length financing There is limited or no basis for using the Income and market approaches

11 Going concern is a technical valuation term that means that the underlying assumption in performing the valuation is that the company will continue to operate for the foreseeable future.

The companies we are trying to value would generally fit this profile with the exception that they have all recently raised money in an arm’s length transaction. However, in the case of convertible securities, especially those with no valuation cap, you could argue that any available valuation data is fragmentary and speculative. This leads to a difficult tradeoff. The valuation analyst can either:

1. Assume that the recent convertible securities transaction provides no meaningful data for a market approach and use an asset/cost approach, as the only viable “default value”, OR

2. Assume that the recent securities transaction could provide some meaningful data for a market approach and avoid using an asset approach

Another, possibly bigger, concern about the cost approach is dealing with the convertible security in the equity allocation portion of the valuation. The valuation analyst still has to decide whether or not to treat the convertible security as debt or as equity. The former is not consistent with the view that market participants have of the instrument. The latter is more intuitive, but requires some subjective assumptions in practice. Treating convertibles as equity could also at times create illogical results if the implied costbased valuation is not line with a reasonable valuation that the market participants would expect. Estimating the valuation at which the convertible security would convert generally requires using a different valuation approach like a market or income approach. If the appraiser has already determined that these approaches are not viable because the data is fragmentary and speculative, then the analyst is at an impasse. If the analyst feels comfortable using alternative valuation approaches, then the analyst should probably not use a cost approach since it is generally not acceptable in situations where it is possible to use an alternative approach. Though the valuation analyst faces some difficult decisions in applying the cost approach, we generally feel that approach has merit in a number of situations. We would recommend leaving the decision about how and when to use this approach to the valuation analyst’s professional judgment. Of the cost methods, we prefer the MarketAdjusted Book Value and Cost to Build or Recreate methods. The Invested Capital approach seems like it could create an artificially low value since it does not consider any market adjustments to book value or costs to build.

Discounted Cash Flow (DCF) Approaches In a Discounted Cash Flow approach, a company’s value is assumed to be the present value of its future free cash flows. Valuation professionals and regulators agree that DCF approaches are acceptable for valuing goingconcern companies. Conceptually we agree but, practically speaking, creating a DCF for an earlystage company is extremely complex, artificially precise, and overly reliant on hardtojustify assumptions.

If a company has generated no real financial results, the inputs for a DCF model are subjective “guesses.” Further, the method itself is designed to facilitate finegrained control over hundreds of valuation assumptions. Since there is no basis for supporting any of these assumptions the complexity of the method just layers assumption on assumption for no real benefit. This means DCFs are costly, complicated, and often difficulttodefend for earlystage companies. For these reasons, we will not go into greater detail on the DCF approach and we do not generally recommend it as a standardized approach for valuing earlystage companies. The DCF approach can work well if the valuation analyst is willing to do a very large amount of research and justification for each assumption. So a big factor for us is that this approach is costly and our goal in writing this paper was to identify approaches that are as lowcost as possible. We also feel that DCF approaches may not be as objective and defensible as other approaches either. The combination of questionable objectivity and defensibility and high costs are why we are not proponents of this approach for earlystage companies. We recognize that there may be situations where the DCF is the only viable approach or the best alternative but we believe that these situations should be rare.

Backsolve Approaches Of the three commonlyused approaches we referenced at the beginning of this paper, the backsolve has a unique appeal. It is a market approach and market approaches often have a unique strength because they are often relatively easytoperform while retaining a high degree of objectivity. One critique of most market approaches is that they typically rely on deriving valuation ratios from a set of comparable companies and then applying these ratios to a subject company. This aspect of the valuation feels less subjective because valuation analysts can defend a wide range of valuation ratios by claiming different sets of comparable companies as more accurate than othersintroducing quite a bit of subjectivity into the process. But the backsolve is a market approach that derives a company’s valuation based on a recent transaction in a subject company’s own securities so the typical argument regarding compselection does not apply. In short, the backsolve approach seems like one of the most 12

defensible approaches available. So, how complex and costly is performing a backsolve? Backsolve approaches derive a value of the company based on optionbased math. The math is difficult to understand conceptually but easy to perform in practice due to the automation available in commonlyused software and spreadsheet programs.

12 Some of the inputs for a typical backsolve OPM may still pull from a set of company comparables. However, there is generally agreement on the ranges of these assumptions based on the stage of the subject company so in practice the comp selection for OPM models alone tends to be less controversial.

In practice, we have seen valuation analysts use the backsolve approach for early stage companies in the following ways:

1. Backsolving based on a valuation cap, if a cap is available, 2. Backsolving using an estimated current premoney value, if a cap is not available, or 3. Backsolving using a projected future premoney value, also if a cap is not available

Below are some example models.

Backsolving Based on a Valuation Cap Some firms assume that if a valuation cap is present in a note it could provide an indication of value. While others feel that this indication of value is probably too high, some firms feel that they have no other choice but to use the value since they have no other valuation information available from the convertible security. 13

In this scenario, let’s assume the following about a subject convertible security:

It is a convertible note issued on 3/1/2016 Face value of $1,000,000 Simple interest at 8% per annum Maturity in 1 year Valuation cap of $10,000,000 or a conversion discount of 20% Management and investor’s best guess is that the company will ultimately raise a

followon round of $5M in one year and that the round is expected to occur at or above the note’s $10,000,000 valuation cap

The first step is to assume that the convertible note will convert at its valuation cap of $10M according to management’s expectations. By assuming the cap, the economics of the note become known and the value of the company and common stock can be derived. If desired, we could attempt to estimate the timing of the next round and take into consideration the interest on the note. However, for simplicity, let’s just assume that the fair value of the note is its face value. Let’s assume the convertible security converts into a new hypothetical Series A. We will now need to make some assumptions about the specific attributes of the new Series A.

13 For example, Teknos wrote about this approach in a blog article several years ago though it may or may not be their suggested approach any longer. The blog article states:

“Some notes contain a “cap,” which is essentially a “nottoexceed” upper limit on a future value. In that case, we have no alternative but to treat the “cap” as the value indication and to work backward, through a BlackScholes option model, to calculate an implied value of the company and the common stock – even though this work will result in a suggested future value for the common stock too.”

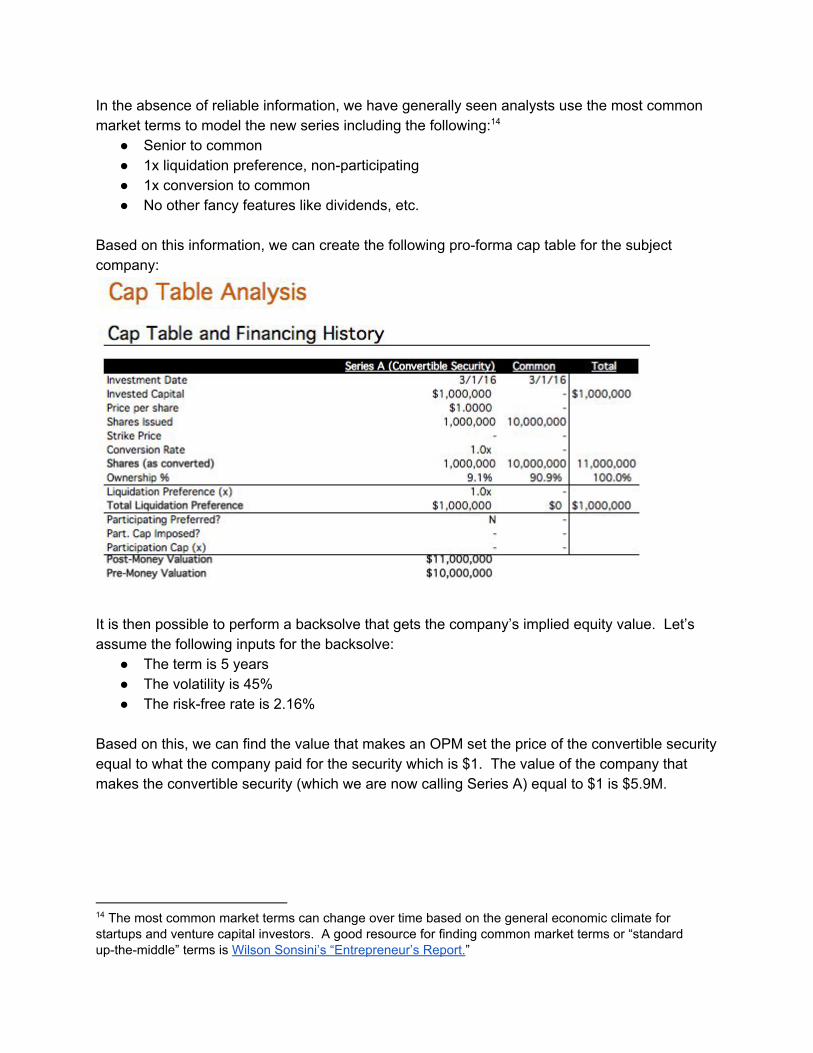

In the absence of reliable information, we have generally seen analysts use the most common market terms to model the new series including the following: 14

Senior to common 1x liquidation preference, nonparticipating 1x conversion to common No other fancy features like dividends, etc.

Based on this information, we can create the following proforma cap table for the subject company:

It is then possible to perform a backsolve that gets the company’s implied equity value. Let’s assume the following inputs for the backsolve:

The term is 5 years The volatility is 45% The riskfree rate is 2.16%

Based on this, we can find the value that makes an OPM set the price of the convertible security equal to what the company paid for the security which is $1. The value of the company that makes the convertible security (which we are now calling Series A) equal to $1 is $5.9M.

14 The most common market terms can change over time based on the general economic climate for startups and venture capital investors. A good resource for finding common market terms or “standard upthemiddle” terms is Wilson Sonsini’s “Entrepreneur’s Report.”

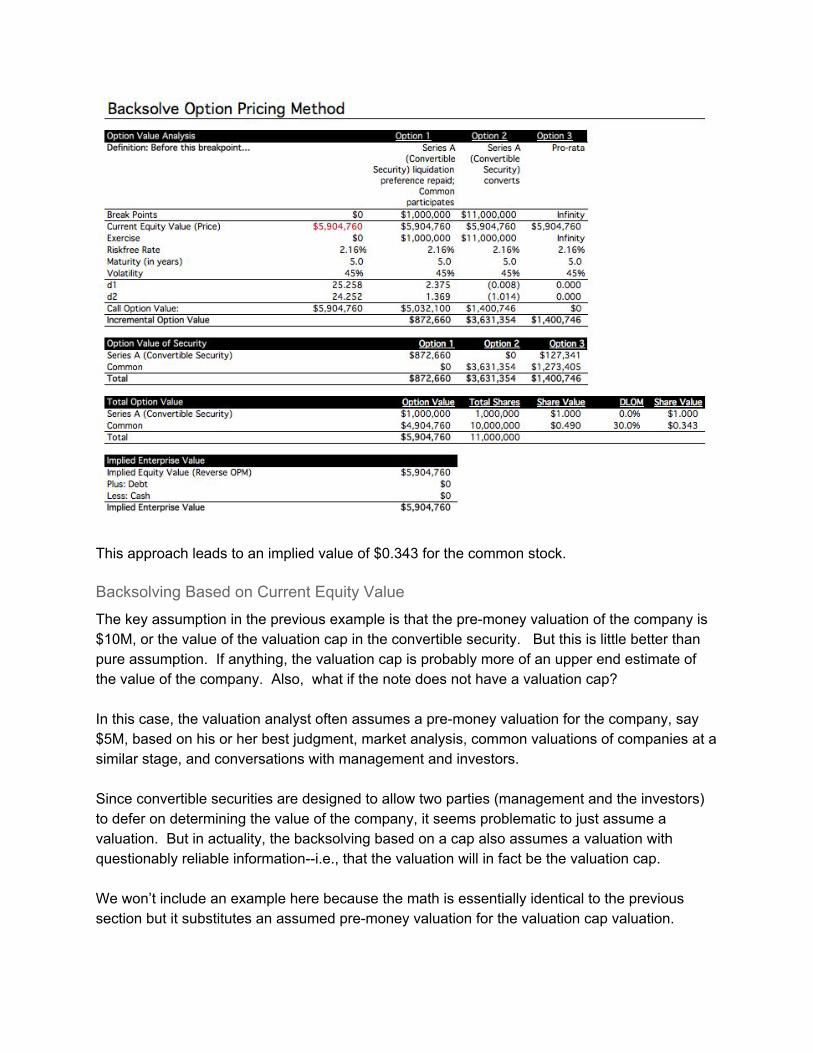

This approach leads to an implied value of $0.343 for the common stock.

Backsolving Based on Current Equity Value The key assumption in the previous example is that the premoney valuation of the company is $10M, or the value of the valuation cap in the convertible security. But this is little better than pure assumption. If anything, the valuation cap is probably more of an upper end estimate of the value of the company. Also, what if the note does not have a valuation cap? In this case, the valuation analyst often assumes a premoney valuation for the company, say $5M, based on his or her best judgment, market analysis, common valuations of companies at a similar stage, and conversations with management and investors. Since convertible securities are designed to allow two parties (management and the investors) to defer on determining the value of the company, it seems problematic to just assume a valuation. But in actuality, the backsolving based on a cap also assumes a valuation with questionably reliable informationi.e., that the valuation will in fact be the valuation cap. We won’t include an example here because the math is essentially identical to the previous section but it substitutes an assumed premoney valuation for the valuation cap valuation.

Backsolving Based on Future Equity Value A third possibility that we have seen, albeit more rarely, is to model a future round. In this case, the valuation analyst assumes the specific details of a future round including participation from hypothetical coinvestors. This approach has the benefit of avoiding estimating the value of the company now and deferring that question to the future, which exactly matches the intentions of the market participants. However, it still involves making an educated “guess” about the future premoney value of the company. To perform this analysis, the valuation analyst will model out a future cap table, run a backsolve analysis based on future values, and then will need to discount the implied share values back to present at the cost of equity. To model it out, let’s again assume the following about the convertible security:

It is a convertible note issued on 3/1/2016 Face value of $1,000,000 Simple interest at 8% per annum Maturity in 1 year Valuation cap of $10,000,000 or a conversion discount of 20% Management and investor’s best guess is that the company will ultimately raise a

followon round of $5M in one year Now let’s assume that the company closes a new round on the maturity date of the note. Let’s assume that management and the entrepreneurs think it is reasonable to expect that the company will achieve a $10M premoney valuation. Let’s assume new investors put in $4M and the note converts into the round as well. Since we are now modeling a future round, we will factor in the accumulated interest on the note. Let’s also use the same terms we used above for the new hypothetical series A:

Senior to common 1x liquidation preference, nonparticipating 1x conversion to common No other fancy features like dividends, etc.

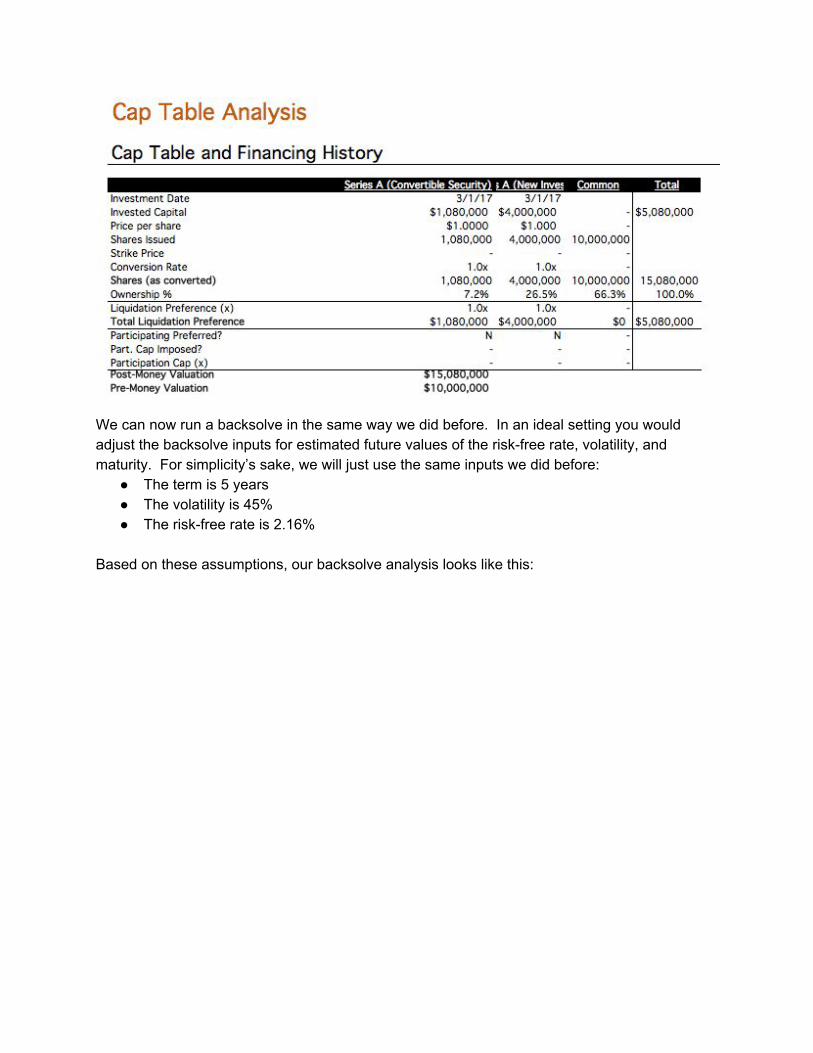

Based on this information, the cap table of the company’s cap table will look like this in one year:

We can now run a backsolve in the same way we did before. In an ideal setting you would adjust the backsolve inputs for estimated future values of the riskfree rate, volatility, and maturity. For simplicity’s sake, we will just use the same inputs we did before:

The term is 5 years The volatility is 45% The riskfree rate is 2.16%

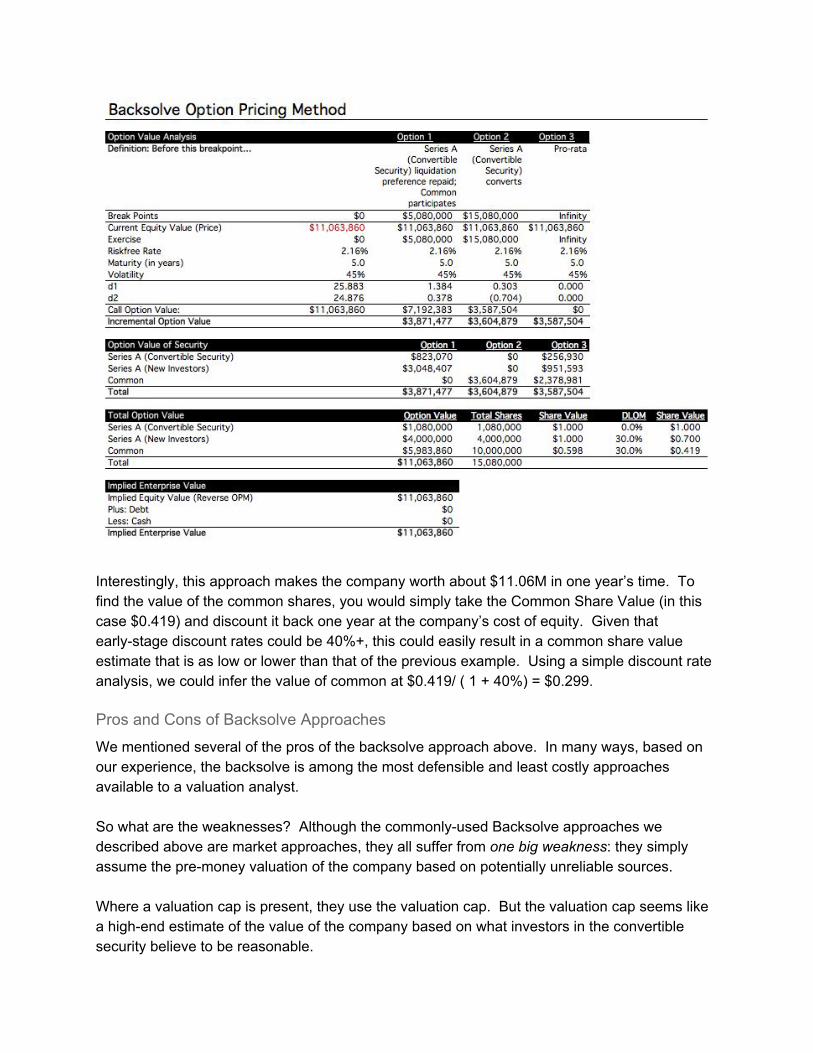

Based on these assumptions, our backsolve analysis looks like this:

Interestingly, this approach makes the company worth about $11.06M in one year’s time. To find the value of the common shares, you would simply take the Common Share Value (in this case $0.419) and discount it back one year at the company’s cost of equity. Given that earlystage discount rates could be 40%+, this could easily result in a common share value estimate that is as low or lower than that of the previous example. Using a simple discount rate analysis, we could infer the value of common at $0.419/ ( 1 + 40%) = $0.299.

Pros and Cons of Backsolve Approaches We mentioned several of the pros of the backsolve approach above. In many ways, based on our experience, the backsolve is among the most defensible and least costly approaches available to a valuation analyst. So what are the weaknesses? Although the commonlyused Backsolve approaches we described above are market approaches, they all suffer from one big weakness: they simply assume the premoney valuation of the company based on potentially unreliable sources. Where a valuation cap is present, they use the valuation cap. But the valuation cap seems like a highend estimate of the value of the company based on what investors in the convertible security believe to be reasonable.

Our Proposal for a Better Backsolve Method Our proposal to solve the assumption problem of picking a single valuation for a backsolve OPM is to pick multiple, with two probably working in most cases. While at first this may seem counterintuitive, the basic idea is that convertible securities are designed to facilitate highresolution negotiations where the two market participants involved (investor(s) and company representative(s)) do not need to (or cannot) agree on a current valuation of the company. So the idea is to represent both of the market particpants’ views in our model and arrive at a weighted average.

ProbabilityWeighted Backsolve Approach The basic idea of the probabilityweighted backsolve approach is to build a backsolve scenario based on the investors’ expectations and another distinct backsolve scenario based on the company’s expectations and then take a weighted average of the two cases. Since we will base the enterprise value of the company 100% on these backsolve approaches (and not weighting other approaches like market comps or a DCF), we can simply take the weighted average implied price of the common stock across the two backsolve scenarios as the common stock value. As mentioned above, in practice, the valuation analyst could use as many probabilityweighted scenarios as she wanted and assign whatever probability seems appropriate. However, in the majority of cases, we feel that it would probably be appropriate to use a 50% weighting on just the two cases we mentioned above. We feel that this approach allows the analyst to more accurately model the unknowns explicit in the convertible note fundraise in a quantitative way. As mentioned above, convertible securities were designed specifically to avoid prematurely setting a value in situations where market participants can’t agree on the price. While all of the above backsolve approaches attempt to ignore that fact, a probability weighting can model that ambiguity while making the included assumptions accessible for review. If a valuation cap is present, then the analyst can use this valuation as the premoney valuation for one scenario (the high scenario). If this information isn’t available and to estimate the lowend valuation, the analyst will need to use judgment, available market data, and conversations with the management team. However, these all seem reasonable given the lack of hard data available to the analyst. You could perform this analysis assuming a current round of financing or a hypothetical future round of financingthese options mirror those we described above for the more traditional backsolve approaches. Choosing which is best is a perfect area for the valuation analyst’s professional judgment in our opinion. While modeling a projected future round seems to adhere

to the market participants expectations more closely, it introduces the need for several additional assumptions:

Information about potential coinvestors and the amounts they would invest Identifying a discount rate to make present value assumptions

Example of Using a ProbabilityWeighted Backsolve Approach Let’s walk through an example of using this new approach but assume that we are modeling a hypothetical current financing round not a future round involving other investors. Further, let’s assume that we want to find the weighted average of two backsolve scenarios: a high valuation scenario and a low valuation scenario.

High Valuation Scenario

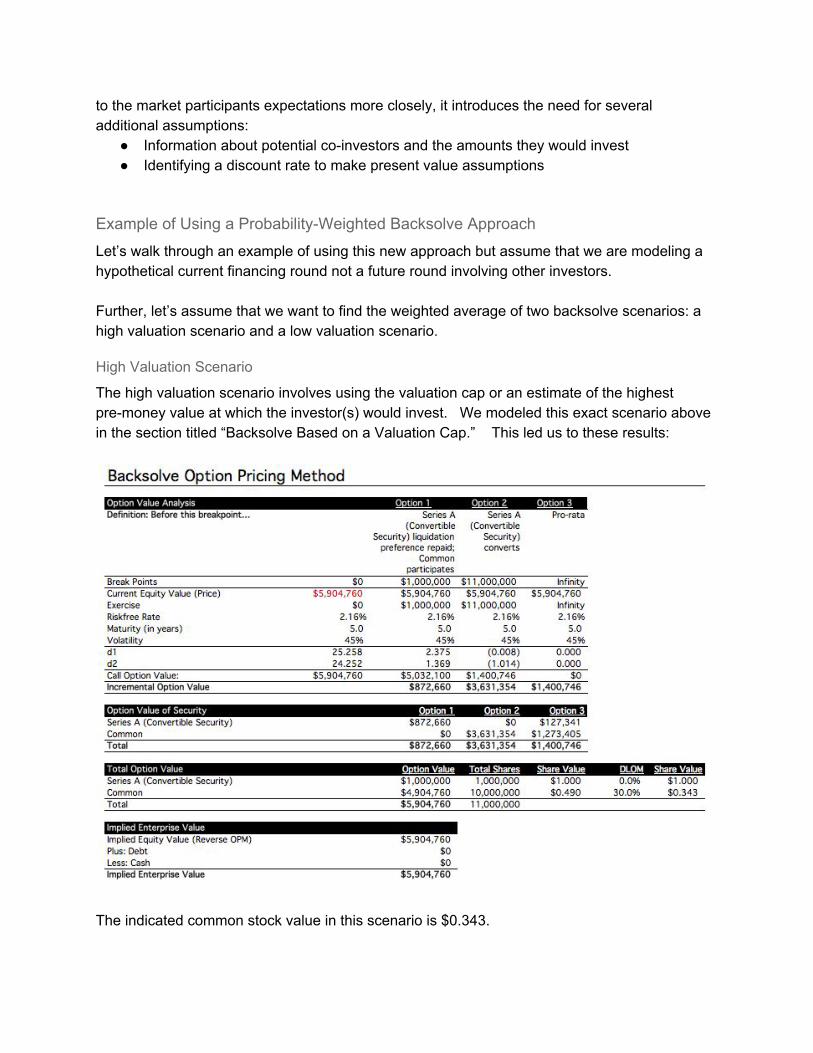

The high valuation scenario involves using the valuation cap or an estimate of the highest premoney value at which the investor(s) would invest. We modeled this exact scenario above in the section titled “Backsolve Based on a Valuation Cap.” This led us to these results:

The indicated common stock value in this scenario is $0.343.

Low Valuation Scenario

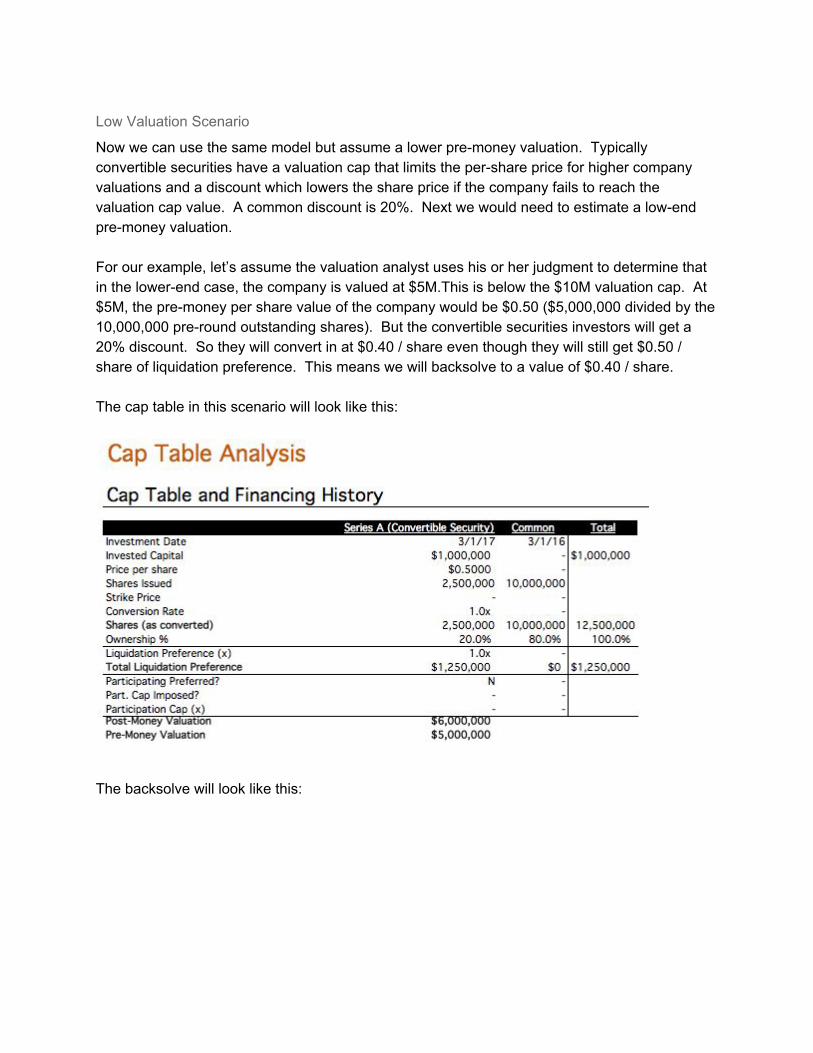

Now we can use the same model but assume a lower premoney valuation. Typically convertible securities have a valuation cap that limits the pershare price for higher company valuations and a discount which lowers the share price if the company fails to reach the valuation cap value. A common discount is 20%. Next we would need to estimate a lowend premoney valuation. For our example, let’s assume the valuation analyst uses his or her judgment to determine that in the lowerend case, the company is valued at $5M.This is below the $10M valuation cap. At $5M, the premoney per share value of the company would be $0.50 ($5,000,000 divided by the 10,000,000 preround outstanding shares). But the convertible securities investors will get a 20% discount. So they will convert in at $0.40 / share even though they will still get $0.50 / share of liquidation preference. This means we will backsolve to a value of $0.40 / share. The cap table in this scenario will look like this:

The backsolve will look like this:

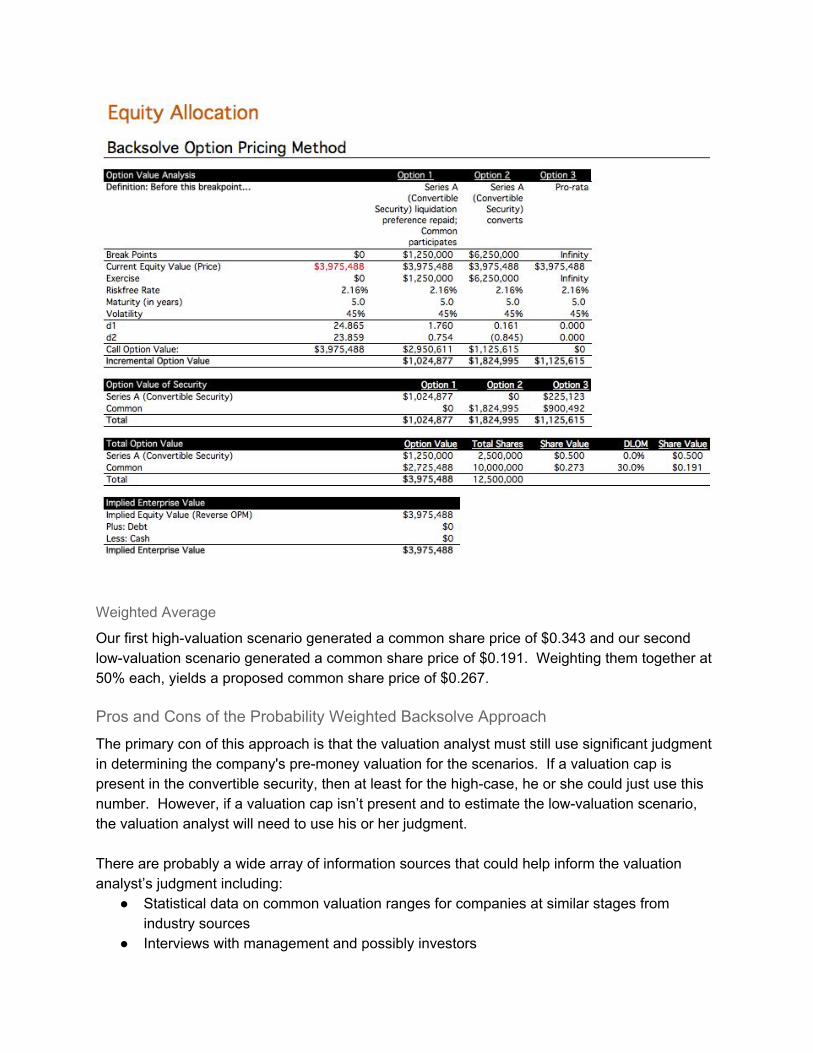

Weighted Average

Our first highvaluation scenario generated a common share price of $0.343 and our second lowvaluation scenario generated a common share price of $0.191. Weighting them together at 50% each, yields a proposed common share price of $0.267.

Pros and Cons of the Probability Weighted Backsolve Approach The primary con of this approach is that the valuation analyst must still use significant judgment in determining the company's premoney valuation for the scenarios. If a valuation cap is present in the convertible security, then at least for the highcase, he or she could just use this number. However, if a valuation cap isn’t present and to estimate the lowvaluation scenario, the valuation analyst will need to use his or her judgment. There are probably a wide array of information sources that could help inform the valuation analyst’s judgment including:

Statistical data on common valuation ranges for companies at similar stages from industry sources

Interviews with management and possibly investors

Previous experience of the valuation analyst Further, applying a scenariobased approach seems like a reasonable and effective way of managing systematic uncertainty surrounding the company’s ultimate valuation. The PWERM is a comparable example of a widelyaccepted valuation approach that uses a scenariobased approach to manage the uncertainty of multiple different possible outcomes. The pros of the approach include:

It is a market approach not a cost approach (which is often a less preferred approach conceptually)

It is consistent with market participants’ views of the attributes of convertible securities It does not require treating the convertible security as debt in the equity allocation step of

the valuation It is simple and relatively easy to perform

For these reasons, we view this approach as a strong candidate and one of the two that we would most recommend in valuing earlystage companies.

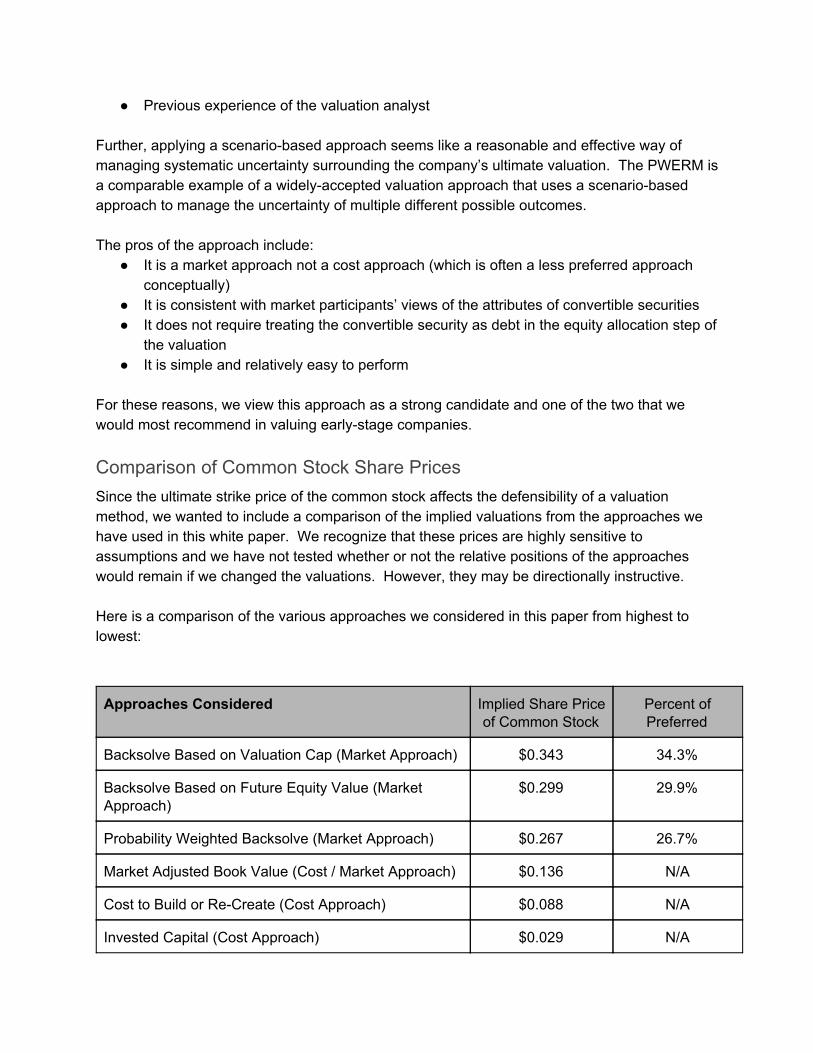

Comparison of Common Stock Share Prices Since the ultimate strike price of the common stock affects the defensibility of a valuation method, we wanted to include a comparison of the implied valuations from the approaches we have used in this white paper. We recognize that these prices are highly sensitive to assumptions and we have not tested whether or not the relative positions of the approaches would remain if we changed the valuations. However, they may be directionally instructive. Here is a comparison of the various approaches we considered in this paper from highest to lowest:

Approaches Considered Implied Share Price of Common Stock

Percent of Preferred

Backsolve Based on Valuation Cap (Market Approach) $0.343 34.3%

Backsolve Based on Future Equity Value (Market Approach)

$0.299 29.9%

Probability Weighted Backsolve (Market Approach) $0.267 26.7%

Market Adjusted Book Value (Cost / Market Approach) $0.136 N/A

Cost to Build or ReCreate (Cost Approach) $0.088 N/A

Invested Capital (Cost Approach) $0.029 N/A

A possible benefit of the two approaches that involve a cost approach is the significantly lower indicated common stock value. However, this could also lead to defensibility concerns. The results also seem consistent with the idea that cost approaches could artificially minimize any intangible value.

Conclusion We believe that a consideration of costs and benefits would indicate that using a Probability Weighted Backsolve or a cost approach like the Cost to Build or Recreate or Market Adjusted Book Value approach are the best options for valuation analysts seeking to value the common stock of earlystage companies with only convertible and common securities on their cap table. It might also be possible to combine any of these approaches and weight them based on the valuation analyst’s judgment. Regardless the costbased approaches and the Probability Weighted Backsolve seem simple, inexpensive, and defensible if they are performed well. Between the two, the cost approach will lead to a lower strike but may not capture future option value as well as the Probability Weighted Backsolve its strength is in its use of observable inputs and the fact that strategic buyers are unlikely to pay more for a business than the cost to recreate that business in their build versus buy decision process. Conversely the strength of the Probability Weighted Backsolve approach is in capturing future option value while it’s challenge is the requirement of judgement in creating necessary underlying assumptions. We believe the best solution is to leave the decision of which approach to take to the judgment of the valuation analyst performing the valuation.