Embed Size (px)

Citation preview

A world leader in IP commerce

Patents ● Copyright ● Trademarks ● Trade

Secrets ● Designs ● Know how ● Technology ● Research collaborations

www.ipexchange.global

Twitter: @BirgitteBIC

1990 2000 2010 1948 1968 1988 2008

Investment in UK intangibles is exceeding

tangibles

Intangible contributions to the economy

today are exceeding tangible assets

(US example)

Trends in intangible investment and contribution

Intangibles Tangibles Financial burst

£ billion %

50

150

100

2

4

6

8

10

12

14

What are intangible assets? (OECD classification)

• Software

• Databases

• Big Data

Computerised information

• Scientific and non-scientific R&D

• Copyrights, designs, trademarks, patents (IPR)

• Creative and inventive activities

Innovative property

• Branding and reputation (advertising)

• Firm specific human capital (training)

• Business process investments

• Networks

Economic competencies

Stone Age

Bronze Age

Iron Age

1760-1830: Early mechanisation

Water power

1830-1890: Steam

Steel

Railway

1890-1940: Electrical

engineering

Chemistry

1940-1985: Mass

production

Petrochemicals

Oil

1985-2020: Software

New media

Internet

Big Data

2020-2040: Health & life sciences

Sustainability

Low carbon

Waves of economic progress towards the intangible economy

Rate

of

Econom

ic A

ctivity

Unknown

future

Artificial

intelligence Virtual reality

© Big Innovation Centre

THE GLOBAL ADDRESSABLE IP EXCHANGE MARKET IS HUGE BUT THERE ARE IP HOT-SPOTS

Dominant countries are: • China, Japan, India & Republic of Korea • USA and Canada • Brazil • Germany & France

Patent Utility Model Trademark Industrial Design

Geographical

region Applications

Share of

total (%) Applications

Share of total

(%) Applications

Share of

total (%) Applications

Share

of total

(%)

Africa 14,900 0.6 175 0.02 207,017 2.8 17,300 1.5

Asia 1,607,500 60.0 893,276 94.1 3,855,689 51.8 764,600 67.2

Europe 346,200 12.9 49,640 5.2 1,982,973 26.6 290,000 25.5

Latin America &

the Caribbean 64,100 2.4 4,282 0.5 626,168 8.4 15,600 1.4

North America 614,300 22.9 617,439 8.3 41,100 3.6

Oceania 33,900 1.3 1,523 0.2 160,108 2.1 9,800 0.9

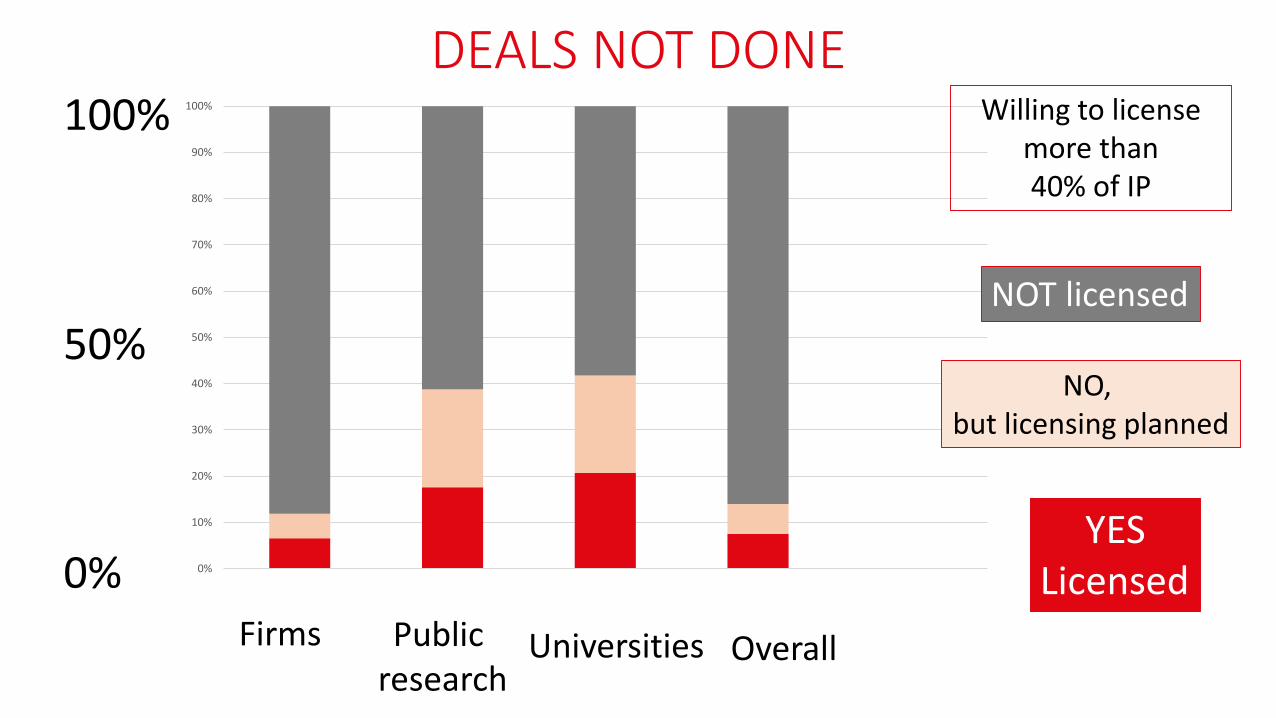

DEALS NOT DONE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Firms Public Research Organizations Universities Total of all organizations

Yes No, but licensing planned No

Firms Public research

Universities Overall

YES Licensed

NO, but licensing planned

NOT licensed

0%

100%

50%

Willing to license more than 40% of IP

Stage 1: Unlicensed IP

40.2% of unlicensed IP has an identifiable seller and buyer

Stage 2: Negotiation

50.1% of those start negotiations

Stage 3: Agreement

56.3% of those reach an agreement

11 % probability of a successful transaction

DEALS NOT DONE even when seller and buyers are identified

SEARCH:

No ‘marketplace’ for sellers and buyers to meet

IP tends to be traded in a ponderous bespoke

manner

CONTRACT NEGOTIATION:

Too many parties at the table - internal decision

makers, lawyers, brokers…

Long process - bureaucracy and paperwork

TRANSPARENCY:

Unclear deal terms and trust of potential traders

No single market for IP - Lack of agreed standard,

norms & rules

A SIGN OF MARKET FAILURE !

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Average Brokerage Commissions

UK top 16 IP agents have combined revenue of £400m & profit of £100m

PATENTS 25%

Residential real estate

5.3%

Large and small capitalization equities: < 1%

Source: ITG, Real Trends, CDC Group IAM (Intellectual Asset Management) magazine March/April 2014

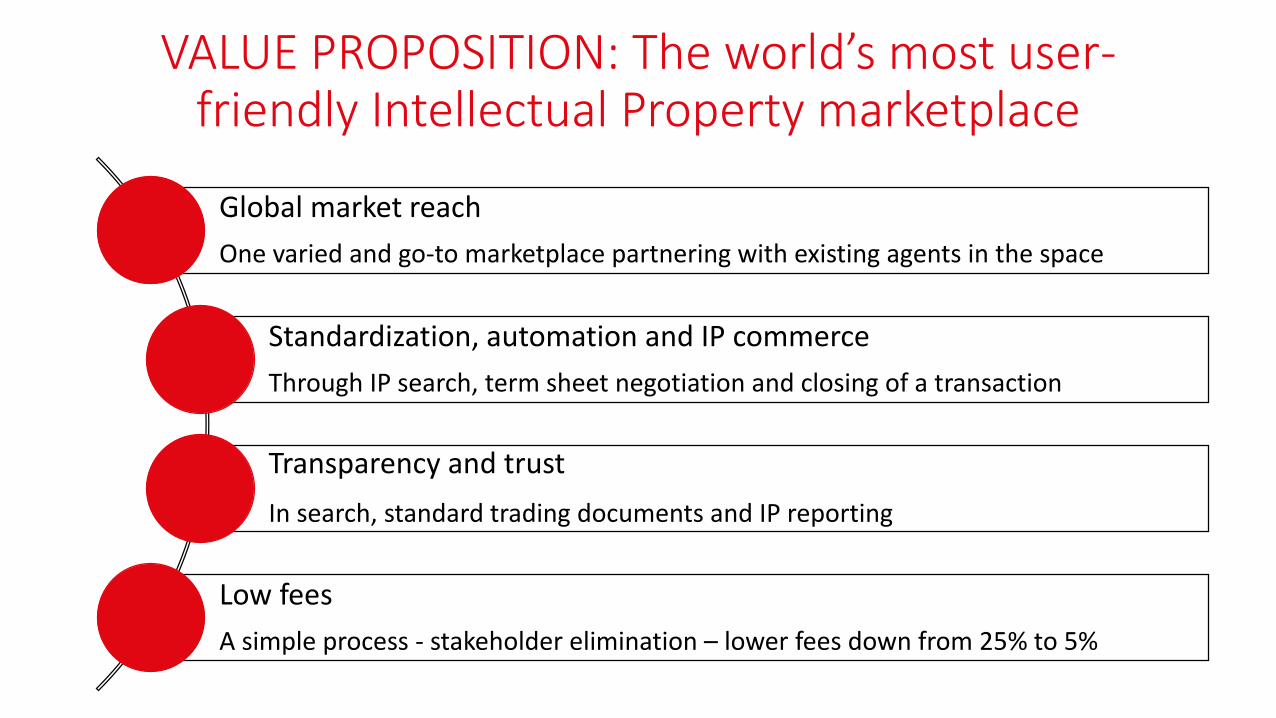

VALUE PROPOSITION: The world’s most user-friendly Intellectual Property marketplace

Global market reach

One varied and go-to marketplace partnering with existing agents in the space

Standardization, automation and IP commerce

Through IP search, term sheet negotiation and closing of a transaction

Transparency and trust

In search, standard trading documents and IP reporting

Low fees

A simple process - stakeholder elimination – lower fees down from 25% to 5%

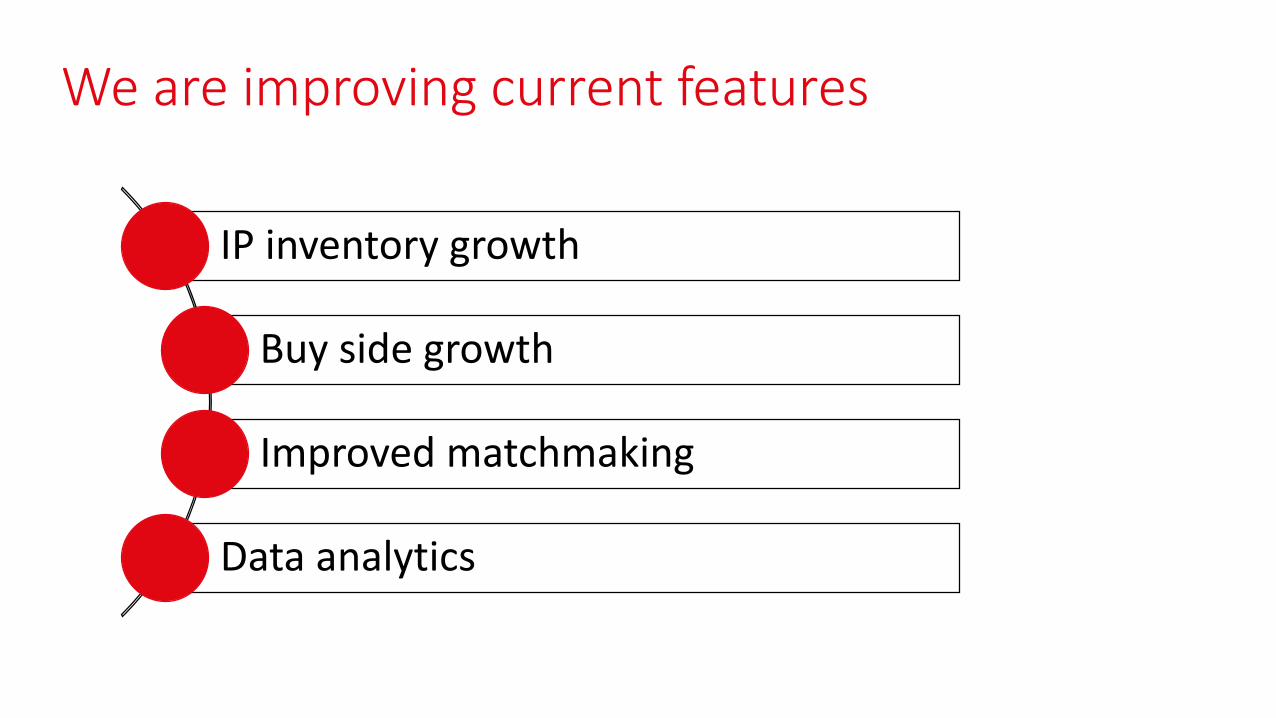

IP inventory growth

Buy side growth

Improved matchmaking

Data analytics

We are improving current features

IP clusters

Your own branded space

Thought leadership

Members (open vs closed)

Bespoke IP exchange

Videos

Photos

Relevant links

Publications

Discussions

Adverts

Events & tradeshows

Calls

Testimonials

IP bundles

Solutions / applications

Entrepreneurial finance (buy-back

scheme)

IP Pavilions with community features Innovation – Competitiveness – Strategic networks –Financial flows

A STANDARDIZED IP REPORT

For:

Inventory management

Investment

Recapture value

ARTIFICIAL INTELLIGENCE (AI)

Machine learning

Natural Language Processing

Why investment is needed? New features: Virtual reality, reporting and data analytics

AGENTS IN OUR SPACE

TYPE OF IP AGENTS

Licensing Agents

(e.g. real-estate agents in renting markets)

Company Portals

IP Brokers

(e.g. real-estate agents in buying–selling markets)

IP Auction Houses

(e.g. Christies auction house)

Clearinghouses, Bulletin Boards, and Innovation Portals

(e.g. the Gumtree of patents)

Analytics Software and Services Firms

(e.g. software tools to help valuing patents)

University Technology Transfer Intermediaries

(e.g. brokers but focusing on universities)

IP Trading Platforms/IP Transaction on agreed new rules.

(e.g. NASDAQ of IP)

Government Sponsored

(e.g. IP services and aiming to establish connections)

In contrast INTELLECTUAL PROPERTY

EXCHANGE do:

Not experiment with new models

to monetize patents

Use an automated and

standardized process for IP trade

Trade a whole variety of IP from

low to high value

Operate cross sector, cross

institution type, and globally

Develop IP communities

Key assets

COMPANY SPECIFIC:

• Registered company INTELLECTUAL PROPERTY EXCHANGE LIMITED (Company No. 09597427)

• Registered trademark: UK00003113470

• Web domain: www.ipexchange.global

SOFTWARE PLATFORM SPECIFIC:

• No technology risk - a robust, secure and scalable cloud architecture

• Proprietary software enabled database architecture for classifying and searching on IP (including assets transferred from Montreal Medical International)

• Proprietary software enabled database architecture for peer to peer IP transactions: buyer, selling, licensing (exclusive or non exclusive), IP pricing (fixed, negotiated)

• Proprietary IP user licenses: IP browser , buyer, seller licenses for trading IP (working with Olswang)

• Proprietary standardized and customizable IP transaction contracts for selling and licensing IP, including Patents, Copyright, Trademarks, Trade Secrets, Designs, Technology, Ideas, Research collaborations)

• Critical mass of users and 8000 units of IP across 600 categories: More than 100 class universities plus a handful of companies

WHAT:

• 10 000 IP postings

• 700 organizations / users

• 600 IP categories (strong in medical, pharma, chemistry, engineering, communications, high tech)

Examples: IP from a 150 world class universities plus a dozen companies

For example:

• Johns Hopkins, Columbia, Rockefeller University (USA)

• McGill University (Canada)

• Inserm-Transfert (France)

• Yissum – Hebrew University (Israel)

• Parque Scientifico Technologico Pando (Uruguay)

• CONICET (Argentina)

• Misr El Kheir Foundation (Egypt)

• King’s College London (UK)

• Merck KGaA

• BASF

• Johnson & Johnson

• National Research Council of Canada

• Canadian Space Agency

WHO: Have on-boarded IP or cross-linked with (or about to) existing platforms: • Malaysia PatentMall • Australian SourceIP • Danish IP market place • UK Copyright Hub of the Digital Catapult • Global Tech IP in China • A major science park in China • Similar organizations across central Europe,

United States and Israel

Three types of investors for IP EXCHANGE

Venture Capitalist Strategic investor to share business

model

Big user of IP Exchange

Audacious Goals for Europe by 2025! – and how we can support

1. Democratize access to knowledge, ideas and creativity: 2. Put all of Europe’s private and university IP on one go-to global market place 3. Enforce standardized, high-speed and low-cost IP commerce for all types of IP 4. World leader in novel IP services: IP markets, IP valuation, IP insurance, Big Data analytics 5. EU backed finance (grants, loans or equity) should be captured and listed on IP Exchanges for IP

inventory management and de-risking (e.g. Horizon 2020) 6. Create a Digital Single Market 7. Build Europe a network of IP clusters in IP Pavilions: Europe’s challenge to Silicon Valley and Boston as

hi-tech hub 8. IP backed finance to scale-up 1000 IP-rich companies (Europe’s challenge to Google, Amazon etc.) 9. Intangible investment: 20% of GDP (of which 3% is R&D) 10. Every European citizen a digital citizen

BIRGITTE ANDERSEN [email protected]

Ergon House, Horseferry Road, London SW1P 2AL

Telephone +44 (0)20 3713 4036 | [email protected] | Twitter @BigInnovCentre