Embed Size (px)

Citation preview

Turning Analytics From

“Nice to Have” to “Must Have”

February 10, 2016

AuditNet and AuditSoftwareVideos.com

Collaboration

Brought to you by AuditNet® and

AuditSoftwareVideos.com working together to provide:

Practical audit software training

Resource links

Survey benchmarking

Independent analysis

Tools to improve audit software usage

Page 1

About Jim Kaplan, CIA, CFE

President and Founder of AuditNet®,

the global resource for auditors (now

available on iOS, Android and

Windows devices)

Auditor, Web Site Guru,

Internet for Auditors Pioneer

Recipient of the IIA’s 2007 Bradford

Cadmus Memorial Award.

Author of “The Auditor’s Guide to

Internet Resources” 2nd Edition

Page 2

Housekeeping and Disclaimers

This webinar and its material are the property of Cash Recovery Partners LLC. Unauthorized usage or recording of this webinar or any of its material is strictly forbidden. We are recording the webinar. Downloading or otherwise duplicating the webinar recording is expressly prohibited.

The views expressed by the presenters do not necessarily represent the views, positions, or opinions of AuditNet® or the presenters’ respective organizations.

These materials, and the oral presentation accompanying them, are for educational purposes only and do not constitute accounting or legal advice or create an accountant-client relationship.

Webinar recording link will be sent to the Email registered in GoToWebinar.

Submit questions via the chat box on your screen.

NASBA rules require us to ask polling questions during the Webinar and CPE certificates will be sent via email to those who answer ALL the polling questions

CPE certificates and recording will be sent to the email address you registered with in GTW. We are not responsible for delivery problems due to spam filters, attachment restrictions or other controls in place for your email client.

Post Webinar Feedback. Please complete the feedback questionnaire to help us continuously improve our Webinars

Page 3

Additional Disclaimers

While AuditNet® makes every effort to ensure information is accurate and complete, AuditNet® makes no representations, guarantees, or warranties as to the accuracy or completeness of the information provided via this presentation. AuditNet® specifically disclaims all liability for any claims or damages that may result from the information contained in this presentation, including any websites maintained by third parties and linked to the AuditNet® website

Any mention of commercial products is for information only; it does not imply recommendation or endorsement by AuditNet®

Page 4

Richard B. Lanza, CPA, CFE, CGMA

• Over two decades of analytic and cost recovery experience (focused on ACL and Excel with associated add-ins)

• Has written and spoken on the use of audit data analytics for over 20 years.

• Received the Outstanding Achievement in Business Award by the Association of Certified Fraud Examiners for developing the publication Proactively Detecting Fraud Using Computer Audit Reports as a research project for the IIA

• Discovered a letter analytic approach for text analysis (LALA)

• Recently was a contributing author of:

• Global Technology Audit Guide (GTAG #13) Fraud in an Automated World – Institute of Internal Auditors.

• Data Analytics – A Practical Approach - research whitepaper for the Information System Accountability Control Association.

• Cost Recovery – Turning Your Accounts Payable Department into a Profit Center – Wiley and Sons.

Please see full bio at www.richlanza.com

Learning Objectives

Review results from a variety of online and in-person surveys

focused on analytics over the past decade

Extract for presentation analytic best practices being deployed by

top performing organizations

Explain the need for an effective culture around the analytics

program to bolster the technology implementation

Discuss the varying types of technology alternatives, outlining their

relative strengths and place at the analytics table

6

The Surveys The State of Auditing & Analytics

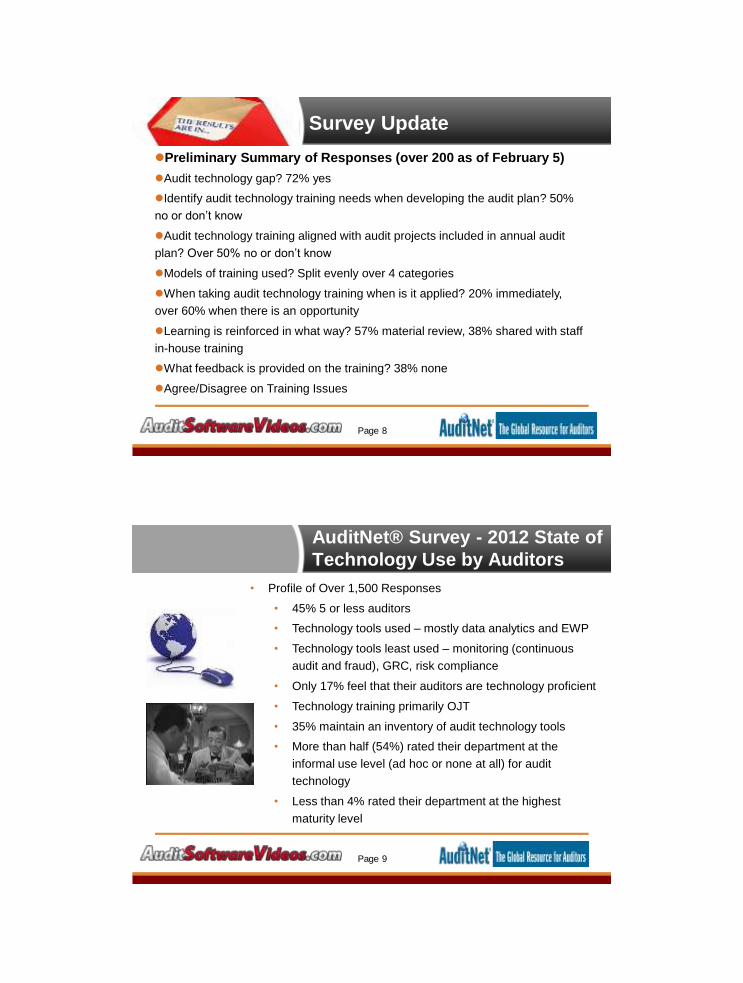

Survey Update

Page 8

Preliminary Summary of Responses (over 200 as of February 5)

Audit technology gap? 72% yes

Identify audit technology training needs when developing the audit plan? 50%

no or don’t know

Audit technology training aligned with audit projects included in annual audit

plan? Over 50% no or don’t know

Models of training used? Split evenly over 4 categories

When taking audit technology training when is it applied? 20% immediately,

over 60% when there is an opportunity

Learning is reinforced in what way? 57% material review, 38% shared with staff

in-house training

What feedback is provided on the training? 38% none

Agree/Disagree on Training Issues

AuditNet® Survey - 2012 State of

Technology Use by Auditors

• Profile of Over 1,500 Responses

• 45% 5 or less auditors

• Technology tools used – mostly data analytics and EWP

• Technology tools least used – monitoring (continuous

audit and fraud), GRC, risk compliance

• Only 17% feel that their auditors are technology proficient

• Technology training primarily OJT

• 35% maintain an inventory of audit technology tools

• More than half (54%) rated their department at the

informal use level (ad hoc or none at all) for audit

technology

• Less than 4% rated their department at the highest

maturity level

Page 9

AuditNet® Survey - 2015 State of

Technology Use by Auditors

• Profile of Over 370 Responses

• 33% do not use data analysis / 20% more use it ad-hoc

• 67% do not use continuous controls monitoring

• 50% are moderately satisfied or less with their data

analytic implementation

• 55% have on the job training for technology

• Nearly 50% have no technology training budget

• 85% feel it is moderate to highly important to invest in

technology in order to improve its use

• 80% feel it is moderate to highly important that the CAE

embrace technology to increase usage

• Only 42% have a strategy for developing data analysis or

CCM software

Page 10

AuditNet® Survey - 2012 Data

Analysis Audit Software

• Profile of Over 550 Responses:

• 70% 10 or less auditors

• 30% had not purchased data analysis software

• Cost was the top reason for not buying the software

followed by training

• 57% felt that training was the key reason analytics is not

required on audits

• 59% of auditors do not require analytic steps in audits

• 64% felt that analytic audit programs would increase usage

• 91% said they do no “fear the software”

Page 11

AuditNet® Survey - 2015 Data

Analysis Software Survey

• Profile of Over 650 Responses

• 44% 5 or less auditors

• 40% have not purchased a data analytic software

• Nearly 45% have no data analysis skills or use them in an

ad hoc basis

• 45% have no staff trained in analytic software with 26%

noting they have no funding for training and 25% not

having the time to train on the software

• 23% are advanced / power users

• Less than 45% have ever scripted their work

• 73% use Excel as an analytic tool

• 78% do not link performance objectives to using analytics

Page 12

Key Word / Textual AnalyticsAuditNet® Survey Results

Page 13

Queries of Unstructured

Data for Fraud

Compliance with Data

Analytic Tools?

Yes: 25%

No: 75%

Data Analytics used to

perform Key Word Search

for FCPA, Fraud, or

Keyword Compliance?

Yes: 33%

No: 67%

December 2014 Viewing and Key Word Data Files Available at:

http://www.auditnet.org/audit-data-analytics--4

2015 Internal Audit Capabilities

and Needs Survey - Protiviti

• Over 800 responses

• Top focus is cybersecurity with leading firms having top support

from the board and senior management

• To avoid analytics being a never-ending journey, audit teams

need to address the question head-on

• GTAG-16 – Data Analysis Technologies is see as the top

needed guidance…and it was written in 2011

• In the last 3 years, it is the 1st appearance on the CAE’s list of focus

areas

• Of the top 13 areas to improve, 11 of them are focused on I.T.,

analytics, continuous assurance and other I.T topics• Using analytics is a top priority as is mobile apps and the cloud

• Of the audit process knowledge areas, IT security and CAATS

are the top areas (tied for 1st)

• Audit efficiencies from CAATS opens time for more

collaboration with the business

Page 14

http://www.protiviti.com/IAsurvey

2015 Internal Audit Capabilities

and Needs Survey - Protiviti

Page 15

http://www.protiviti.com/IAsurvey

EY Global Forensic Data

Analytics Survey 2014

450 executives surveyed 72% of respondents believe that emerging big data

technologies can play a key role in fraud

Only 7% of respondents are aware of any specific big

data / Only 2% are using them

12% utilize visualization / 26% apply key word searches

62% of respondents indicate that they need to improve

management’s awareness of the benefits of analytics

65% report the use of spreadsheet tools such as Microsoft

Excel for analytics with most reporting having databases

less than 1MM records

Page 16

IIA’s Staying a Step Ahead

Internal Audit’s Use of Technology

14,518 internal auditors surveyed 1 out of 10 entering the profession had education in

information systems or computer science

Data mining increased by 14% among survey respondents

from 2006 to 2015

• 80% of CEOs say data mining and analysis is strategic

Computer assisted audit techniques dropped 4% in the same

timeframe?!?!?

Fewer than 4 out of 10 chief audit executives (CAEs)

worldwide feel their departments' use of technology is

appropriate or better

30% do not use data analysis and 22% more use it minimally

Page 17

http://bit.ly/1odDnbY

Polling Question #1

Page 18

The Surveys Why Are We Not Using Analytics?

What Did the I.I. Analytics Find?

Page 20

21

News Flash: Projects Fail

Nothing New – KPMG Study

56% of firms have had to write off at least one IT project in the last year as a failure.

The average loss incurred – approximately $13 Million

The single biggest write-off - almost $210m Among the reasons cited for failure:

inadequate planning

poor scope management

poor communication between the IT function and the business

“IT project failure is rampant – KPMG” The Register

Published 26th November 2002

http://www.theregister.co.uk/2002/11/26/it_project_failure_is_rampant/

Why Do You Not Include

Steps for Data Analytics

2015 AuditNet® Audit Data Analysis Software Survey

Page 22

Why Are They Not Buying

Data Analytics - 2012

Page 23

2012 AuditNet® Audit Data Analysis Software Survey

Why Have You Not Purchased

Data Analytics - 2015

Page 24

2015 AuditNet® Audit Data Analysis Software Survey

Reasons For Not Using

Data Analytic Software

2015 AuditNet® Audit Data Analysis Software Survey

Page 25

Best PracticesPeople, Process and Technology

People and Culture

“Competing on Analytics”

Thomas H. Davenport - Cofounder

Harvard Business Review – 2005 - Named by HBR as

“One of the twelve most important management ideas of the past decade”

Champion analytics from the top

Put data collection and analysis under one leader

Focus analytics on your competitive strengths

Establish an analytics culture

Hire the right people

Use the right technology for the job

Page 27

Ensure Tone at the Top for Analytics

The person with the purse strings needs to see the value of

In almost all best practice companies, the CAE was a past analytic auditor

In others the audit committee was burnt in the past ad asks for it now

Build the Business Case

“You can have brilliant ideas, but if you can't get them across, your ideas won't

get you anywhere “- Lee Iacocca

Attach analytics to a regulation or a standard

Find and track cost savings to prove and report analytic value

Audit more with less / Reduce audit fees / Have an easier day

Show audit sustainability with coded procedures

Back Door the Business Case – Project: Embarrass the Boss Send the boss to a roundtable of audit VPs who do analytics well

Find something so large with analytics that it gets the audit committee to wake up

My best audit finding: http://bit.ly/1S7mFY1

Page 28

People

The Carrot and the Stick

Collaborate with the external auditors (They create budget)

Identify top areas of manual effort or deficiency

Explain how risk will be lowered

Focus on revenue testing - http://on.wsj.com/1IuYeQx

Collaborate with I.T. (They have budget)

Build testing modulus to automate security and data privacy concerns

Make their life easier / Reduce risk in their areas of domain

Play to their ego / They can use best practice automated control

Collaborate with BPOs (They have more budget)

Make their life easier / Reduce manual testing & questions

Reduce risk in their areas of domain

Focus less on risk testing and more on business value opportunities

Page 29

PeopleCollaborate With the “Purse Strings”

Analytic Benefit in Sum:

Doing More With Less

Page 30

2015 AuditNet® Audit Data Analysis Software Survey

Benefits Per the I.I.AnalyticsImproper Payment Analytic Benefits

Page 31

Polling Question #2

Page 32

Surveillance is the quickest and

lowers fraud impacts

2014 Report to the Nation – Association of Certified Fraud Examiners

33

2/3 less value

Half the time

Managing Fraud in the

Digital Era – Deloitte Survey

3,600 responses

Page 34

http://bit.ly/20fcVKA

Audit Standards Are Moving

Towards More Analytics

Page 35

http://bit.ly/1PXdNhiRADAR Initiative

Rutgers and AICPA Unveil

Data Analytics Research

Initiative (Dec 16, 2015)

http://bit.ly/1T3Tcyy

Audit Standards Are Moving

Towards More Analytics

Page 36

http://bit.ly/1VSoAxGhttp://bit.ly/1K1FfhQ

http://bit.ly/20LwA7a

Hire people with the experience and plan time for commitment Analytics needs a weekly, if not daily usage to retain knowledge

Make it part of “annual objectives” Every time you see the staff member – ask them – “Where’s the Analytics?”

78% do not link performance objectives to the use of data analytics per the 2015

AuditNet® Data Analytics Survey

Ironically, 64% view analytical/critical thinking skills to be the top skill for internal

auditors (CBOB 2015 Practitioner Survey)

Train like MetLife to make the “Auditor of 2020” MetLife trains auditors to become “The Auditor of 2020”

Where We’re Going - Internal Auditor – Feb 2016

• Auditors need to strengthen their foundational (analytic) skills, know how to increase their

use of data and analytics, and know when to leverage outside experts

• The auditor of 2020 is not just about data and analytics. It is advancing internal auditors

skills’ and experiences

Page 37

Turning Programmers into Auditors or

Auditors into Programmers

That is the Question

AuditNet® Who’s Training

Your Auditor Survey 2015

Page 38

KPMG 2015 View From the TopApplying Technology Seen As Key Skill

Page 39

http://bit.ly/1nT5o8T

The Effect of a Champion

Page 40

Enhancing Audit Technology Effectiveness:

Teammate’s 2015 Global Technology Surveyhttp://bit.ly/1QiN5jG

The Effect of a Champion

Page 41

Enhancing Audit Technology Effectiveness:

Teammate’s 2015 Global Technology Surveyhttp://bit.ly/1QiN5jG

Train everyone (Opportunists and Champions)

Different training for each group

Both are experts in their own right

• Q builds the tools and understands how to optimize them

• Bond knows how to point & shoot it

Communicate frequently

• Have a Data Analytics Bi-Weekly Meeting

Train staff with competency based training

Just in time training of key skills seen as most desirable

Hire a coach

Get the experience you need when you need it – private lesson style

Provide a safe place to talk about what worked….and what didn’t

Page 42

People

Training Approaches

AuditNet® Who’s Training

Your Auditor Survey 2015

Over 300 Responses: Nearly 80% were not educated in college on audit technology

40% consider themselves in the late majority or worse in

technology adoption

Only 20% had “equal to all” technology training

44% receive no technology training

Of those trained, nearly 70% is in data analytics

What is your department’s leveraging strategy

Page 43

What Training Are You Most

Likely To Purchase

Page 44

2015 AuditNet® Audit Data Analysis Software Survey

Effective Analytic Training Strategies

Don’t Have a Lone Ranger:

Train the Team

Build on a Common Learning

Ground – ExcelTM

Be Consistent With Monthly

Learning & Discussion

Provides a low-cost opportunity

to train on analytics throughout

2016 with 22 CPE credits

Get access to webinar data

files, audit programs, and Excel

macros prior to the event

http://bit.ly/1SkA6Ep

Page 45

Have a backup

There can not be only one!

Code their knowledge

Less than 45% have ever scripted their work

Document, save, and videotape your work

Audit logs in software, flowcharts, and documents take minutes

to develop to the hours to later remember what was done

Video editing (Camtasia) can be used to show how to run

applications for future auditors

Video tape how to use reports in two-minute segments

Page 46

People - Get Past the “Lone

Ranger” Revolving Door

Polling Question #3

Page 47

Best PracticesPeople, Process and Technology

Audit Process Integration

Have a 1, 3 and 5 year plan

Set a realistic plan and stick to it vs. pushing it off

You can’t be “too busy” or “time bankrupt” to change

Make analytics a priority on every audit

Move up the curve: data collection to automated analytics (the 80/20 to 20/80)

Use analytics to predict the top areas of risk / locations to review

48% of CAEs use analytics for scoping decisions and only 43% leverage data to

inform their risk assessment ( 2015 PwC State of the Internal Audit Profession).

Use previous year trends to risk score current year business processes

Have a better conversation with a process owner, now armed with data, to improve

your “critical thinking” skills

Quantify your findings (2016 approach) vs. using hand-picked samples (1970 / 1980

approach to auditing)

Page 49

Process

Plan to Predict

Does Data Analysis Improve

Your Audit Plans

2015 AuditNet® Audit Data Analysis Software Survey

Page 50

PredPol – Even the Police Use It

http://www.predpol.com/

Santa Cruz experienced:

27% decrease in burglary

11% decrease in robbery

56% increase in arrests

51

Predictive Modeling To Improve Police Detection

http://bit.ly/1VyQPQY

“PredPol does not replace the experience and intuition of our great officers, but is rather an invaluable added tool that allows our police force to use their patrol time more efficiently and helps stop crime before it happens.” Chief Mark Yokoyama

PredPol Simple

Big Data Approach

Working Smarter Using Algorithms Tested By

Earthquake Software

52

Type

Time

Place

Crime strikes in the same dimensions

People are needed to validate activity

Focuses on a box of predicted crime

Uses three prediction variables

53

Cost Recovery Analysis

Trial Balance Analysis

Expenses for Analysis

Primarily SG&A

Cost of goods sold (i.e., freight)

Data Files

General Ledger (trial balance)

A/P Invoice Detail Distribution

Purchase Orders

Pricing List

54

A/P and G/L Review Factors Accounts that are sole sourced

Accounts that have too many vendors

Categories that map to the “recovery list”

Assess to industry cost category benchmarks

Top 100 vendors

Trend analysis over time

Trend analysis by vendor (scatter graph)

Cost Recovery Analysis

Trial Balance Analysis

Process - Take

My Manual Audit

Make data analytics a priority on every audit Data exists for every process

“Toto, we are not in the 90s anymore”

Brainstorm the use data analytics in the audit planning process

Replace manual tests with automated ones You need to replace to provide the time for analytics

Focus on I T testing – user and segregation of duties testing

Focus on reconciliations with dashboards and notifications (6 Tips for Reconciliations – Journal of Accountancy – Feb 2016)

Reduce false positives (and negatives) in the final reports Prioritize the likelihood of findings / Use mathematical scoring

Utilize data visualization to audit with pictures

Involve the business units to improve / “adopt the analytics”

Page 55

56

Automated Person Power

There are 159 million, million, million possible

Enigma settings. All we had to do was try each

one. But if we had 10 men checking one setting a

minute for 24 hours every day and seven days

every week, how many days do you think it would

take to check each of the settings? Well, it’s not

days; it’s years. It’s 20 million years. To stop an

incoming attack, we would have to check 20

million years’ worth of settings in 20 minutes

- The Imitation Game movie

BBC Reith Lecture Series

Why Doctors Fail

http://www.bbc.co.uk/programmes/b04sv1s5

Page 57

•Use a checklist so you don’t miss a step

2M infections in the US alone due to not following a checklist

Would You Use Data Analytics More

If You Knew the Audit Steps?

Page 58

2015 AuditNet® Audit Data Analysis Software Survey

The Standard Setters Are

Chiming In on Audit Steps

Page 59

Best Place to Get Audit Steps

With 2,500 Audit Templates

Page 60

http://www.auditnet.org/subscription_plans

Would You Use Data Analytics More

If There Was a Script Library

2015 AuditNet® Audit Data Analysis Software Survey

Page 61

Scripting the Tests

The Road to Continuous

Prototype the test - http://bit.ly/20LP3jX Build something in Excel (or other simple tools) – Make sure it works

Then build something more repetitive using script coding tools

Understand the first year will be rough 30 unit samples will be replaced by 100% testing

This is the year of investment “clean up”

2nd and 3rd year tests should be a blank report

Move to a continuous audit and monitoring model

Focus on key risks to start with “friendly departments”

Have a results manager organize the remediation and follow up

Page 62

Polling Question #4

Page 63

Best PracticesPeople, Process and Technology

Technology Tools (& S.A.A.S)

Technology Tools

and Software as a Service

Use low-cost solutions to start / Train the “Team of Rangers” Excel is a great starter tool / Provides a common language

Realize you will need a small set of tools to manage your data normalization

and scripting (which is beyond Excel)

Consider a results-focused approach to start Consider focused consulting or cost recovery firms to learn from their past

Identify a provider willing to provide the “toolkit” vs. just the “reports”

Moved to advanced analytics and collaboration over time Communicate with images and specific drill down capability

Consider integration with results management tools

Page 65

What Is Your Main Analytic Tool?

All Inexpensive / Simple Products

Page 66

2015 AuditNet® Audit Data Analysis Software Survey

Capitalize on Other People’s

Experience & TechnologyNo upfront cost

Cost recovery firms have an interest in every $ they find

Then, learn from their technology

http://www.auditsoftwarevideos.com/our-services/save-costs

Minimize upfront cost and risk of failure

Report service option provides a proof of concept within hours

http://www.auditsoftwarevideos.com/our-services/report-services

Page 67

The Old Way Was To Invest in

Software & Training Before Results

Page 68

http://bit.ly/1PdGCc1

Business Process Diagnostic Reporting: Data

analytic service applied to core business cycles

focusing on results: improving operations,

identifying cash savings and detecting anomalies

such as errors, fraud and inefficiencies.

Advanced Analytic Tools

Gartner 2015 Magic Quadrant Vendors

Page 69

http://gtnr.it/1Pbl8MX

SAS

IBM

KNMINE

Rapid Miner

Alteryx

“Gartner defines advanced

analytics as the analysis of

all kinds of data using

sophisticated quantitative

methods (for example,

statistics, descriptive and

predictive data mining,

simulation and optimization)

to produce insights that

traditional approaches to

business intelligence (BI) —

such as query and reporting

— are unlikely to discover”

Best PracticesPeople, Process and Technology

Technology (Data Considerations)

Technology

Data Considerations

Automate the data import and normalization process

Move to a tool that can manage disparate data in one software

Automate the data extraction, file cleansing, and data validation

Consider all types of data – not just ERP data

Manage the execution and store in a server

Utilize server technology for secure storage and scalability

Centralized data and backups

Audit knowledge is saved in one place

Manage user security consistently and in a controlled manner

Page 71

Overcoming Data Challenges

Normalizing data is 80% of the time (in the beginning) “By most accounts, 80 percent of the development effort in a big data project

goes into data integration and only 20 percent goes toward data analysis.” —

Intel Corporation

Once its built, it normally takes very little to maintain normalization

Data is in every process. Thus, we should scan/mine it It may not be ERP / It may be in your “Big Data”

90% of data is text

Internal Audit is the best partner to get the data They are independent / Not proving the data is a scope limitation

Some best practice audit depts. have data warehouses larger than I.T.

Page 72

Automated Data Normalization

Store procedures for data cleanup once

Create a normalized set of data fields named by YOU

Ensure data quality tests are run prior to analysis

Automate these routine tasks to increase analyst’s time

Page 73

Data Types

74

Structured Data

Accounting records

Sub ledger details

Monthly performance measures

Unstructured Data

Documents (Excel, PDF, Word)

Emails

Network Logs

External Data

Geomap Service

OFAC, SAM.Gov Watch Lists

IRS Tax ID Match

Polling Question #5

Page 75

What Accounting System

Do You Use

Page 76

2015 AuditNet® Audit Data Analysis Software Survey

BIG DATA Already Available

Large Majority Is Text

Page 77

2007 Buyers Guide to Audit, Anti-Fraud and Assurance Software

Sample Data Validation

Accounts Payable Other QuestionsMake a checklist (to make sure you follow it):

Statistical analysis should also be completed as part of the validation

analysis

Agreement to batch totals, sample data and hardcopies is critical

Page 78

Stratify the Values / Volumes

Benford’s Law of the Digit Patters

Textual Analytics• Letter Analytics

• Word Summary

• Key Words / Sentiment Analysis

Rule Calculator Tools

Regression Analysis

Predictive Miners

Automate Full Data Scan / Mining

Page 79

1) Lanza Approach to Letter Analytics “LALA”: http://bit.ly/1kZlb4h

2) Practical Applications of LALA: http://bit.ly/1PF3GBY

A Benford’s Law

For Letters and Words?

Page 80

Protiviti Reports on Internal Auditing

2006 to 2012 vs. 2013 to 2015 - LALA

Page 81

Protiviti Reports on Internal Auditing 2006 to 2012 vs. 2013 to 2015 – Key Words

Page 82

Polling Question #6

Page 83

Audit Technology Training

AuditNet® Survey on the Effectiveness of Audit

Technology Training

Page 84

Please take the survey now! http://bit.ly/1Prn0is

Join us for our next free Webinar on Moving Periodic Analytics to Continuous Tests (June 8, 2016)

http://bit.ly/1L5L491

Business Process Diagnostics

Report Servicehttp://www.auditsoftwarevideos.com/our-services/report-services

Minimize Upfront Cost & Limit Project Risk

No software or training costs to start

Fixed price set for data loading and report run

Data requests already built for SAP, Oracle, & JDE

…and many other systems (we help on the extract regardless)

Obtain Fast Results

Reports are run within hours of data delivery

Focus on process savings and improvements

Gain From Our Two Decade Experience

Benchmark to our “report toolkits” – now with “LALA”

Visualize the results in pre-built dashboards

Benefit from our knowledge in selecting final samples

Page 85

Course Calendar and Approach

See www.auditnet.org

Offering 11 Unique Training Courses / 22 CPE

Get More For Your Training Dollar

$14 per CPE on an individual subscription

Much lower rates for groups – BEST WAY TO TRAIN

Video playback of past / missed courses

Don’t forget the data files and templates to get you started

Page 86

Learn More: Go to AuditNet® or http://bit.ly/1SkA6Ep

In the Queue – 2016

First Semester of Courses

February 24 - Best Practices in Visualizing and

Dashboarding Data

March 23 - Enhance Audit and Fraud Sampling Productivity

April 20 - Top 10 Analytic Tests to Find PCard / Travel Cost

Frauds and Misuse

May 11 - Continuous Analytic Risk Management

June 8 - Moving Periodic Analytics to Continuous Tests *

June 29 - Top 10 Analytic Tests to Find Procure to Pay

Frauds and Errors

July 13 - Maximize Everything With Excel Pivot Tables

August 17 - Utilize Big Data Analytics Now

Page 87

Learn More: Go to AuditNet® or http://bit.ly/1SkA6Ep

AuditSoftwareVideos.com

70+ Hours of videos accessible for FREE subscriptions

Repeat video and text instruction as much as you need

Sample files, scripts, and macros in ACL™, Excel™, etc. available for purchase

Bite-size video format (3 to 15 minutes)

>> Professionally produced videos by instructors with over 20 years experience in ACL™, Excel™ , and more

Page 88

AuditNet® LLC

• AuditNet®, the global resource for auditors, is available on the

Web, iPad, iPhone, Windows and Android devices and features:

• Over 2,500 Reusable Templates, Audit Programs, Checklists

• Training Webinars focusing on fraud, audit software, IT audit,

and internal audit

• Audit guides, manuals, books on using audit technology

• LinkedIn Networking Groups

• Monthly Newsletters with Expert Guest Columnists

• Surveys on timely topics and best practices for internal auditors

• NOT A SUBSCRIBER? Send an email to [email protected] with

the subject “Must Have” and we will give you $25 off a Premium

Individual Subscription (offer to new subscribers only)

Page 89

Questions?

Any Questions?

Don’t be Shy!

Page 90

Thank You!

Jim Kaplan

AuditNet® LLC

1-800-385-1625

Email:[email protected]

www.auditnet.org

Richard B. Lanza, CPA, CFE, CGMA

Cash Recovery Partners, LLC

Phone: 973-729-3944

Email: [email protected]

www.AuditSoftwarePros.com

Page 91

![Have A Nice Day[1]](https://img.pdfslide.us/doc/110x75/54c48dad4a7959a0218b4730/have-a-nice-day1.jpg)