Embed Size (px)

Citation preview

Turkey: Recent Developments

and Future Prospects

ISBANK

Economic Research Division August 2018

Macroeconomic Outlook

Strong Economic Growth Cycle

GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Average GDP growth rate of 5.5% between 2005-2017

17th largest economy in the world & 6th largest economy amongst the EU countries

More than 9 mn job creation since 2005

Prudent fiscal policy since 2002

3

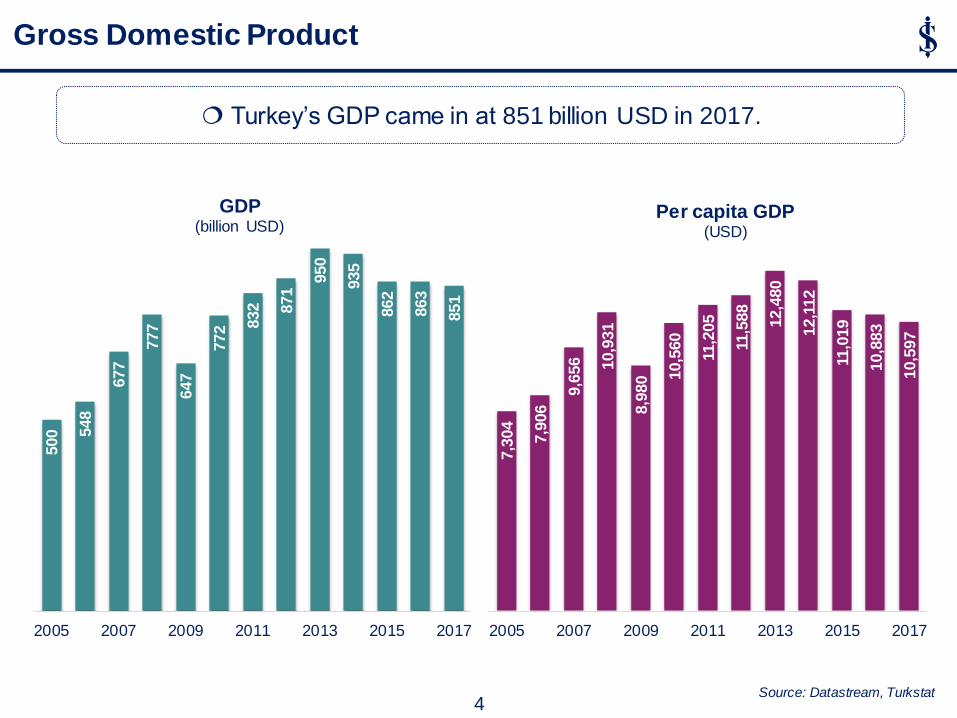

Gross Domestic Product

Source: Datastream, Turkstat

500 548

677

777

647

772 832

871 9

50

935

862

863

851

2005 2007 2009 2011 2013 2015 2017

GDP (billion USD)

7,3

04

7,9

06

9,6

56

10,9

31

8,9

80 10,5

60

11,2

05

11,5

88

12,4

80

12,1

12

11,0

19

10,8

83

10,5

97

2005 2007 2009 2011 2013 2015 2017

Per capita GDP (USD)

Turkey’s GDP came in at 851 billion USD in 2017.

4

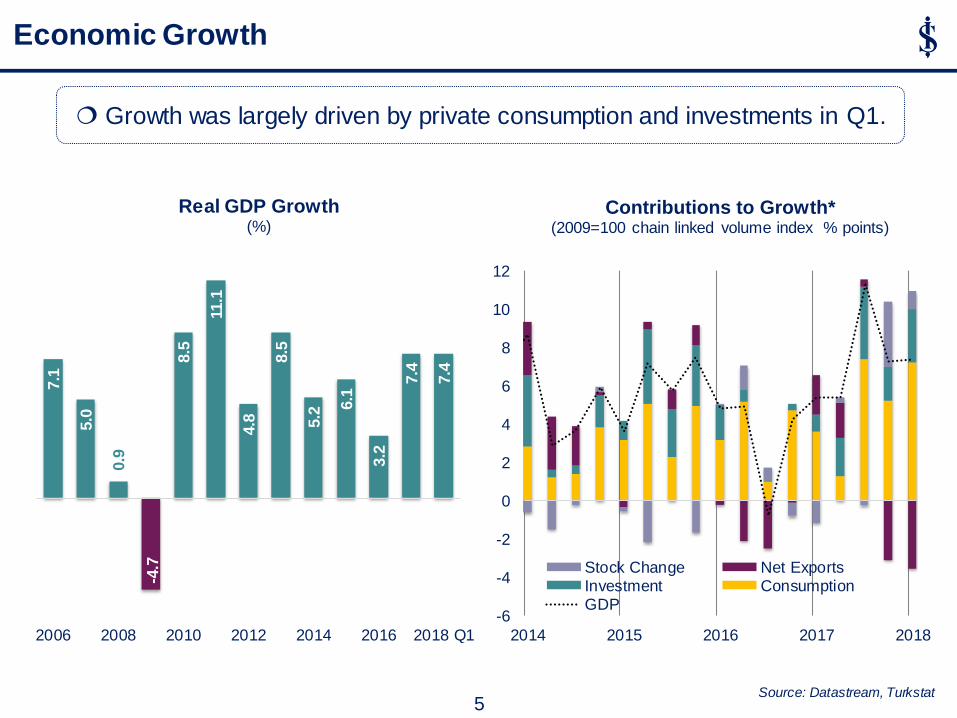

Growth was largely driven by private consumption and investments in Q1.

Source: Datastream, Turkstat

7.1

5.0

0.9

-4.7

8.5

11.1

4.8

8.5

5.2

6.1

3.2

7.4

7.4

2006 2008 2010 2012 2014 2016 2018 Q1

Real GDP Growth (%)

-6

-4

-2

0

2

4

6

8

10

12

2014 2015 2016 2017 2018

Contributions to Growth* (2009=100 chain linked volume index % points)

Stock Change Net ExportsInvestment ConsumptionGDP

Economic Growth

5

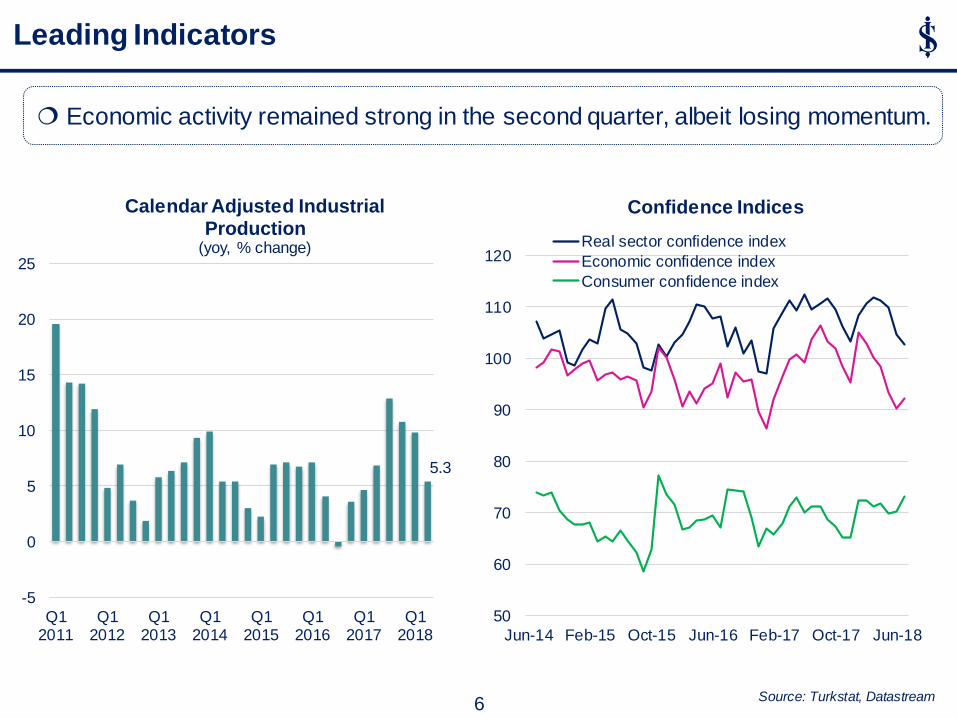

Leading Indicators

Economic activity remained strong in the second quarter, albeit losing momentum.

6

5.3

-5

0

5

10

15

20

25

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

Q12018

Calendar Adjusted Industrial Production

(yoy, % change)

50

60

70

80

90

100

110

120

Jun-14 Feb-15 Oct-15 Jun-16 Feb-17 Oct-17 Jun-18

Confidence Indices

Real sector confidence index

Economic confidence index

Consumer confidence index

Source: Turkstat, Datastream

More than 9 million new jobs were created since 2005.

Labor Market

7

9.7

8.9 9.2

12.0 11.9

10.0

8.5 8.8 9.1

10.3 10.2

12.0

9.9 10.6

45 45 44 45 47 47 47 49 49

51 52 52 53 53

2005 2007 2009 2011 2013 2015 2017

Labor Market Indicators* (%)

Unemployment

Labor Participation Rate

20 20 20 20 21

23 23 24 25

26 27 27

29 29

2005 2007 2009 2011 2013 2015 2017

Employment* (millions)

(*) Seasonally adjusted figures. Latest figure as of May 2018. Source: Turkstat, Datastream

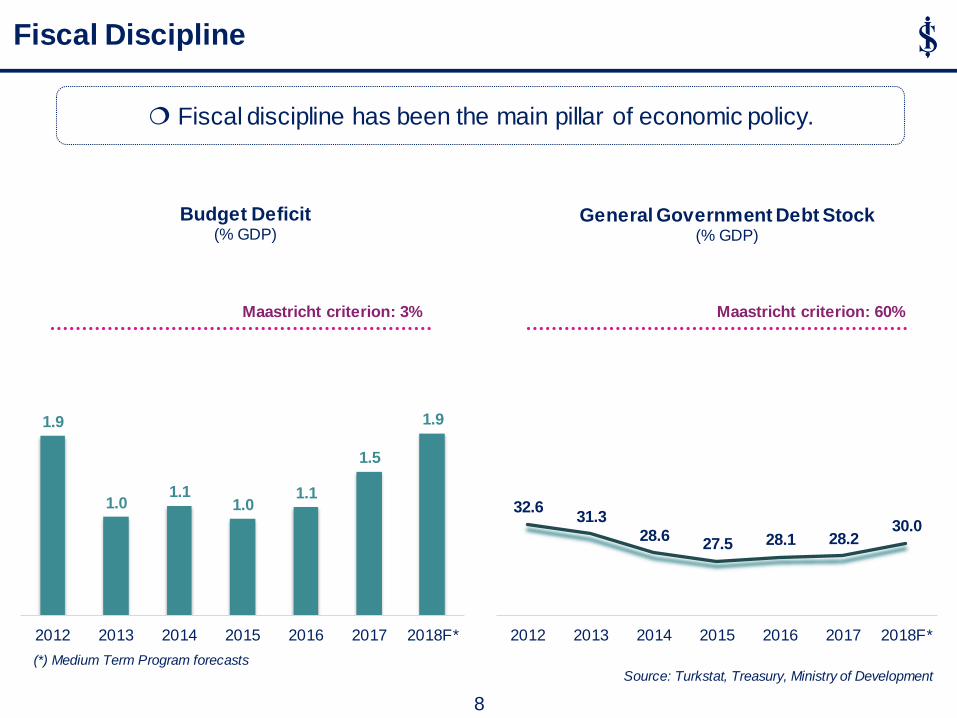

Fiscal discipline has been the main pillar of economic policy.

1.9

1.0 1.1

1.0 1.1

1.5

1.9

2012 2013 2014 2015 2016 2017 2018F*

Budget Deficit (% GDP)

Maastricht criterion: 3%

32.6 31.3

28.6 27.5 28.1 28.2

30.0

2012 2013 2014 2015 2016 2017 2018F*

General Government Debt Stock (% GDP)

Maastricht criterion: 60%

Fiscal Discipline

8

(*) Medium Term Program forecasts Source: Turkstat, Treasury, Ministry of Development

Export volume reached all-time highs.

2.6

3.6

3.7

3.8

4.8

5.4

5.6

5.7

9.4

15.8

Edible fruits and nuts

Plastic and articles

Articles of iron and steel

Non knitted and crochetedgoods

Precious stones

Electrical machinery andequipment

Knitted and crocheted goods

Iron and steel

Boilers and machineries

Motor vehicles

Exports* (% of total)

Exports

9

73

86

107

132

102 11

4

135

152

152

158

144

143 1

57

162

2005 2007 2009 2011 2013 2015 2017

Exports* (billion USD)

(*) 12-month cumulative figures as of June 2018 Source: Turkstat, Datastream

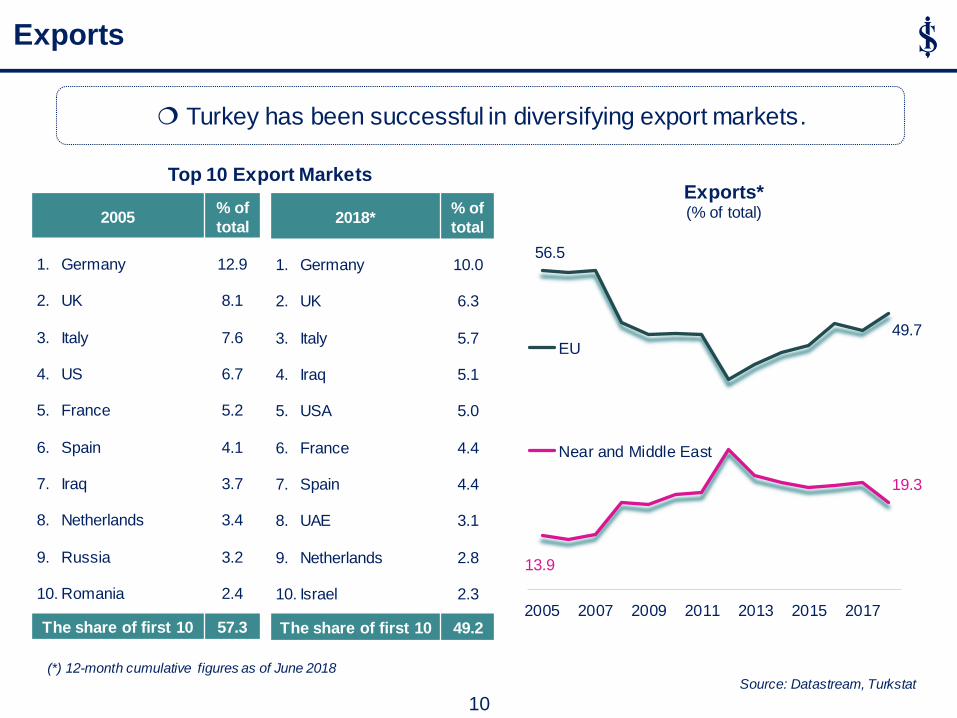

Turkey has been successful in diversifying export markets.

Top 10 Export Markets

2005 % of

total

1. Germany

2. UK

3. Italy

4. US

5. France

6. Spain

7. Iraq

8. Netherlands

9. Russia

10. Romania

12.9

8.1

7.6

6.7

5.2

4.1

3.7

3.4

3.2

2.4

The share of first 10 57.3

2018* % of

total

1. Germany

2. UK

3. Italy

4. Iraq

5. USA

6. France

7. Spain

8. UAE

9. Netherlands

10. Israel

10.0

6.3

5.7

5.1

5.0

4.4

4.4

3.1

2.8

2.3

The share of first 10 49.2

Exports

56.5

49.7

13.9

19.3

2005 2007 2009 2011 2013 2015 2017

Exports* (% of total)

EU

Near and Middle East

10

(*) 12-month cumulative figures as of June 2018 Source: Datastream, Turkstat

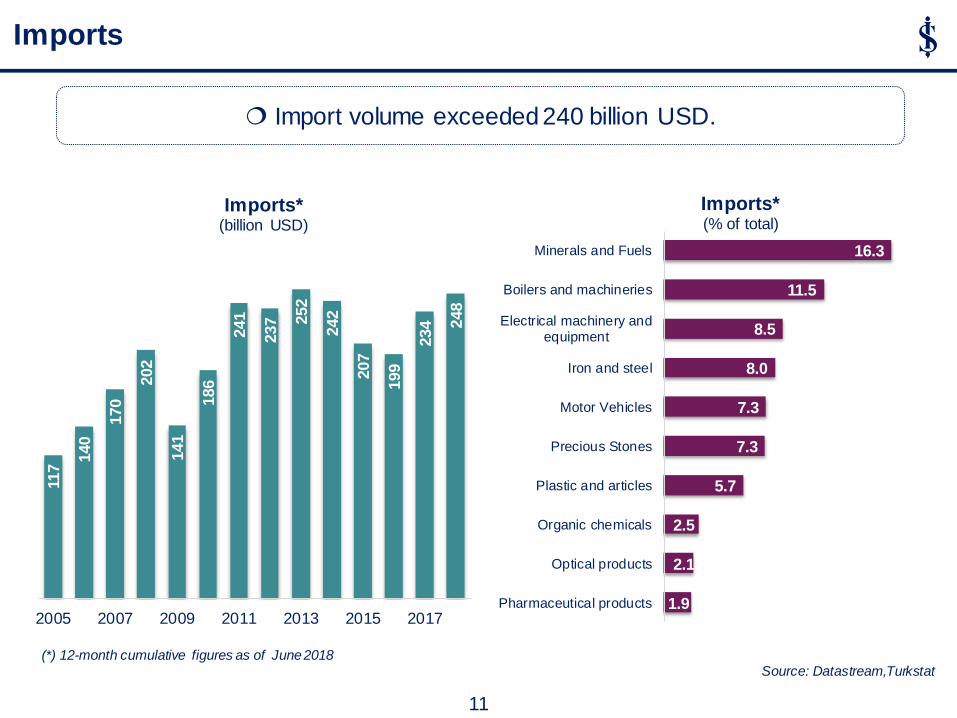

Import volume exceeded 240 billion USD.

1.9

2.1

2.5

5.7

7.3

7.3

8.0

8.5

11.5

16.3

Pharmaceutical products

Optical products

Organic chemicals

Plastic and articles

Precious Stones

Motor Vehicles

Iron and steel

Electrical machinery andequipment

Boilers and machineries

Minerals and Fuels

Imports* (% of total)

117 1

40

170

202

141

186

241

237 252

242

207

199

234

248

2005 2007 2009 2011 2013 2015 2017

Imports* (billion USD)

Imports

11

(*) 12-month cumulative figures as of June 2018 Source: Datastream,Turkstat

17.4

70.1

12.0

2005

Capital Goods

Intermediate Goods

Consumption Goods

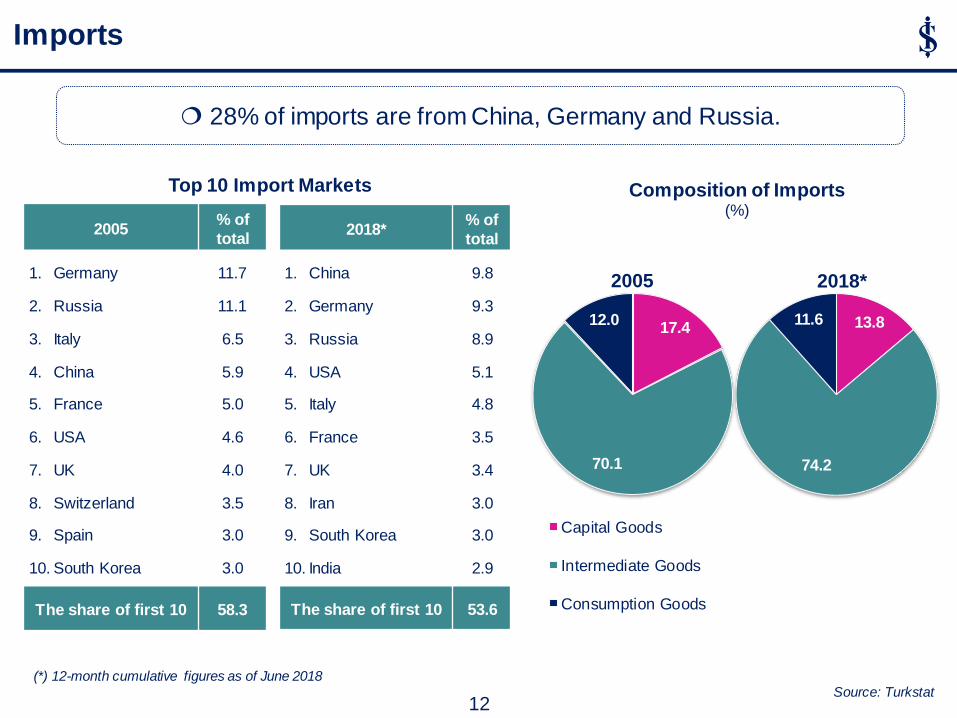

28% of imports are from China, Germany and Russia.

Top 10 Import Markets

2005 % of

total

1. Germany

2. Russia

3. Italy

4. China

5. France

6. USA

7. UK

8. Switzerland

9. Spain

10. South Korea

11.7

11.1

6.5

5.9

5.0

4.6

4.0

3.5

3.0

3.0

The share of first 10 58.3

2018* % of

total

1. China

2. Germany

3. Russia

4. USA

5. Italy

6. France

7. UK

8. Iran

9. South Korea

10. India

9.8

9.3

8.9

5.1

4.8

3.5

3.4

3.0

3.0

2.9

The share of first 10 53.6

13.8

74.2

11.6

2018*

Imports

Composition of Imports (%)

12

(*) 12-month cumulative figures as of June 2018 Source: Turkstat

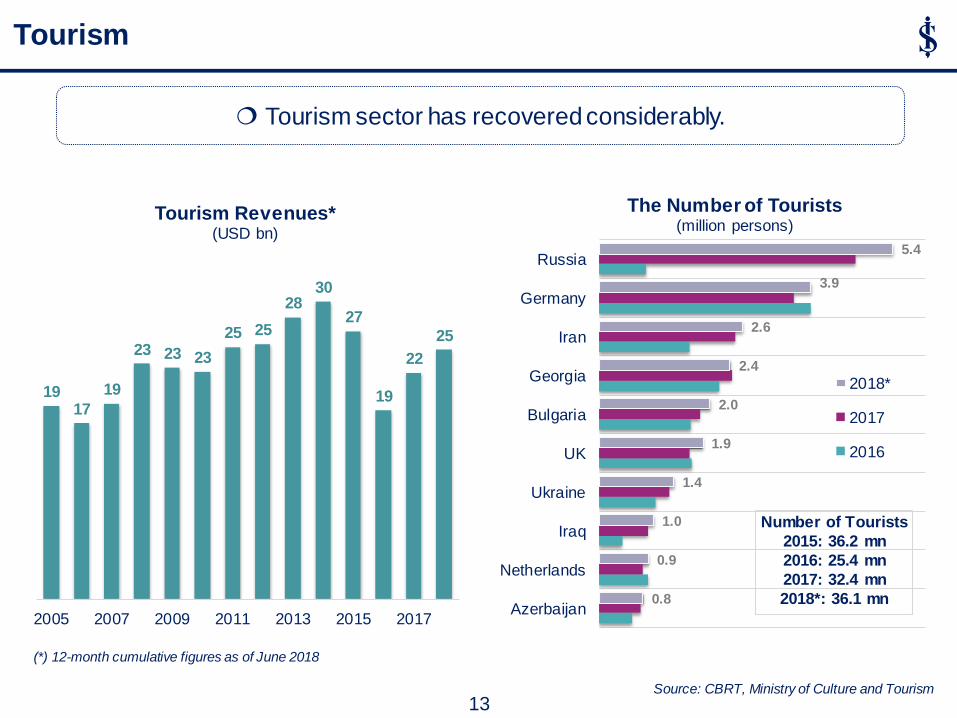

Tourism

19 17

19

23 23 23

25 25

28 30

27

19

22

25

2005 2007 2009 2011 2013 2015 2017

Tourism Revenues* (USD bn)

Tourism sector has recovered considerably.

13

0.8

0.9

1.0

1.4

1.9

2.0

2.4

2.6

3.9

5.4

Azerbaijan

Netherlands

Iraq

Ukraine

UK

Bulgaria

Georgia

Iran

Germany

Russia

The Number of Tourists (million persons)

2018*

2017

2016

Number of Tourists

2015: 36.2 mn

2016: 25.4 mn

2017: 32.4 mn

2018*: 36.1 mn

(*) 12-month cumulative figures as of June 2018

Source: CBRT, Ministry of Culture and Tourism

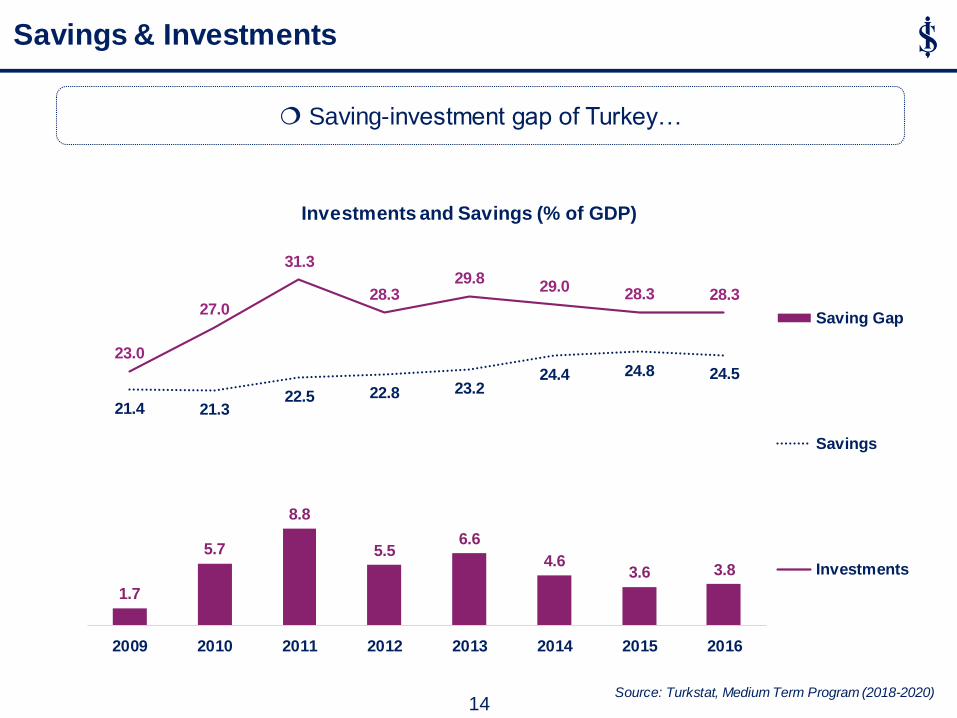

Saving-investment gap of Turkey…

Savings & Investments

Source: Turkstat, Medium Term Program (2018-2020)

1.7

5.7

8.8

5.5 6.6

4.6 3.6 3.8

21.4 21.3 22.5 22.8 23.2

24.4 24.8 24.5

23.0

27.0

31.3

28.3 29.8

29.0 28.3 28.3

2009 2010 2011 2012 2013 2014 2015 2016

Investments and Savings (% of GDP)

Saving Gap

Savings

Investments

14

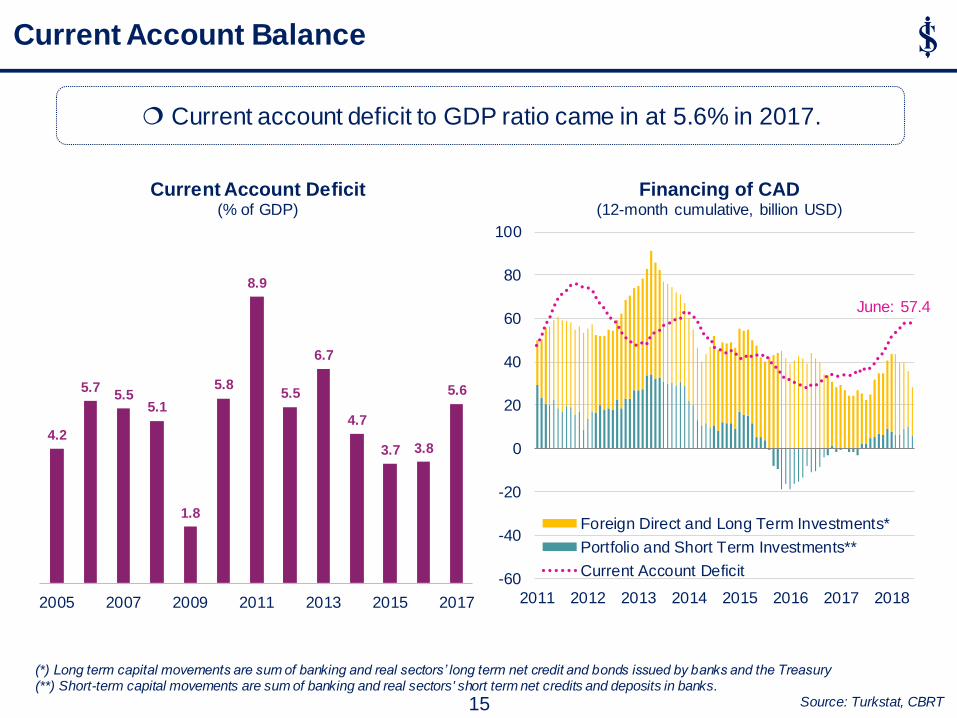

Current account deficit to GDP ratio came in at 5.6% in 2017.

4.2

5.7 5.5

5.1

1.8

5.8

8.9

5.5

6.7

4.7

3.7 3.8

5.6

2005 2007 2009 2011 2013 2015 2017

Current Account Deficit (% of GDP)

Current Account Balance

June: 57.4

-60

-40

-20

0

20

40

60

80

100

2011 2012 2013 2014 2015 2016 2017 2018

Financing of CAD (12-month cumulative, billion USD)

Foreign Direct and Long Term Investments*

Portfolio and Short Term Investments**

Current Account Deficit

(*) Long term capital movements are sum of banking and real sectors’ long term net credit and bonds issued by banks and the Treasury (**) Short-term capital movements are sum of banking and real sectors' short term net credits and deposits in banks.

Source: Turkstat, CBRT 15

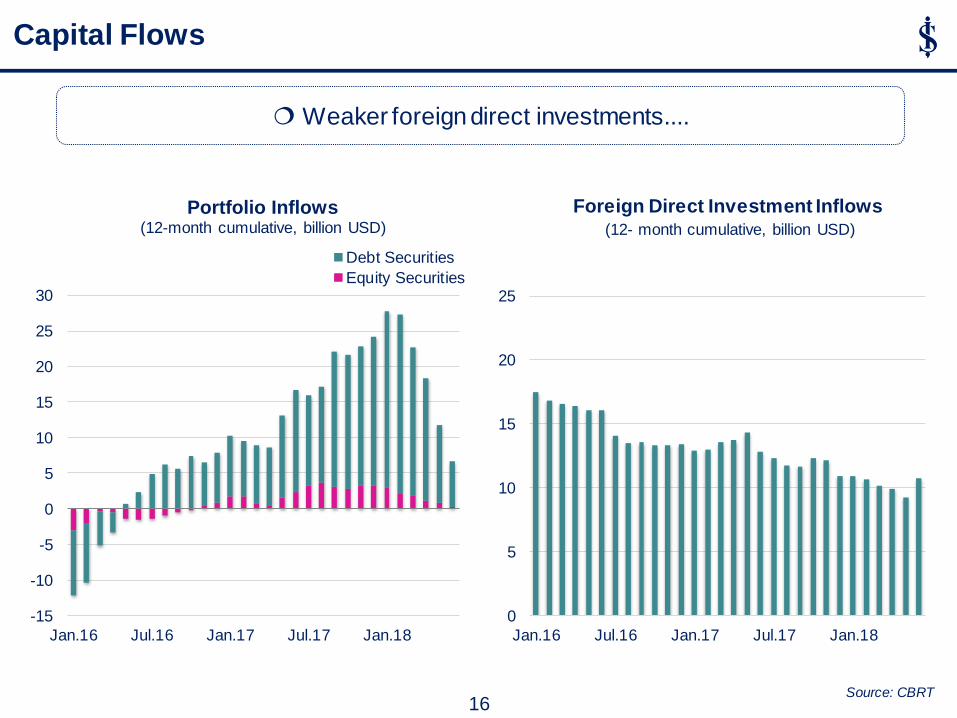

Weaker foreign direct investments....

Source: CBRT

Capital Flows

-15

-10

-5

0

5

10

15

20

25

30

Jan.16 Jul.16 Jan.17 Jul.17 Jan.18

Portfolio Inflows (12-month cumulative, billion USD)

Debt Securities

Equity Securities

0

5

10

15

20

25

Jan.16 Jul.16 Jan.17 Jul.17 Jan.18

Bin

ler

Foreign Direct Investment Inflows (12- month cumulative, billion USD)

16

6

8

10

12

14

16

18

20

22

Jan.17 May.17 Sep.17 Jan.18 May.18

Interest Rates (%)

Interest Rate CorridorOne Week Repo RateCBRT Weighted Average Cost of FundingLate Liquidity Window

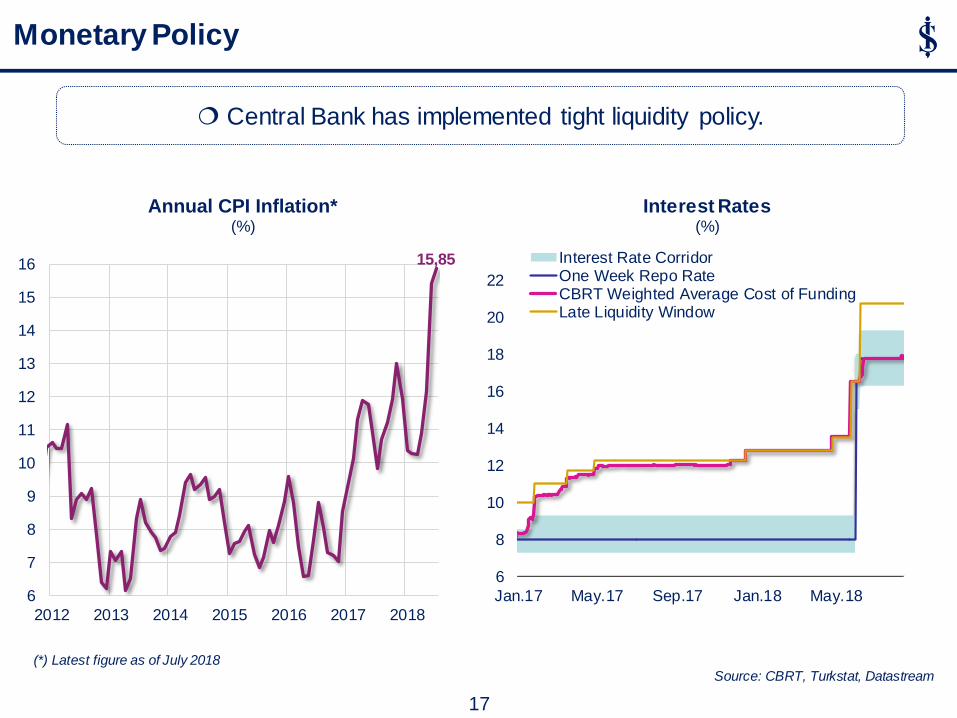

Monetary Policy

Central Bank has implemented tight liquidity policy.

15,85

6

7

8

9

10

11

12

13

14

15

16

2012 2013 2014 2015 2016 2017 2018

Annual CPI Inflation* (%)

17

(*) Latest figure as of July 2018 Source: CBRT, Turkstat, Datastream

80

100

120

140

160

180

200

Jan.17 May.17 Sep.17 Jan.18 May.18

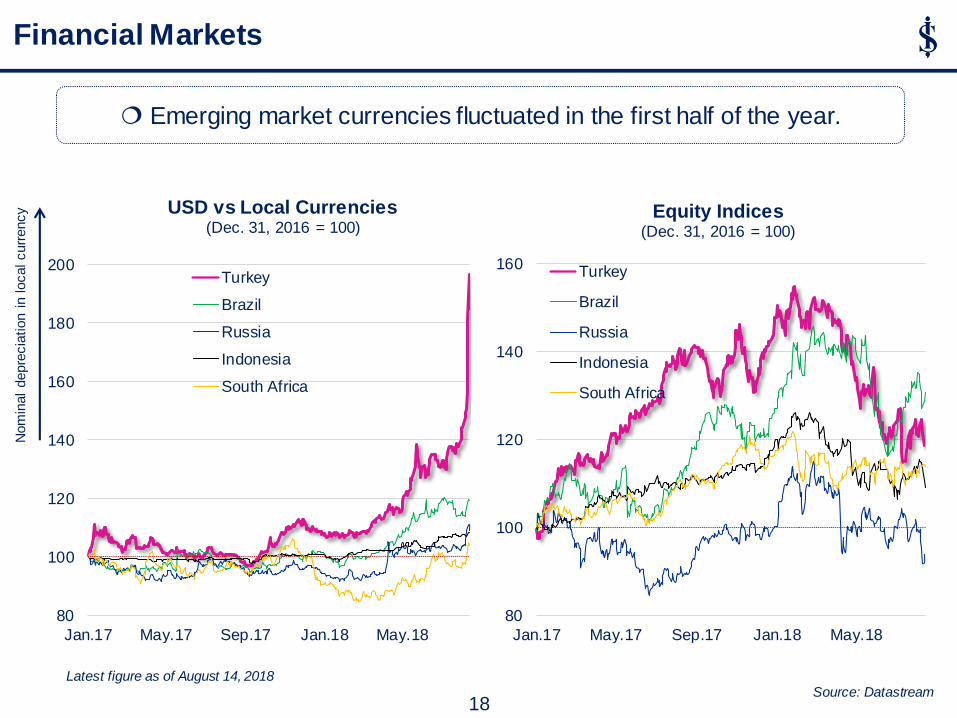

USD vs Local Currencies (Dec. 31, 2016 = 100)

Turkey

Brazil

Russia

Indonesia

South Africa

Latest figure as of August 14, 2018 Source: Datastream

Financial Markets N

om

inal

depre

cia

tion i

n local curr

ency

Emerging market currencies fluctuated in the first half of the year.

18

80

100

120

140

160

Jan.17 May.17 Sep.17 Jan.18 May.18

Equity Indices (Dec. 31, 2016 = 100)

Turkey

Brazil

Russia

Indonesia

South Africa

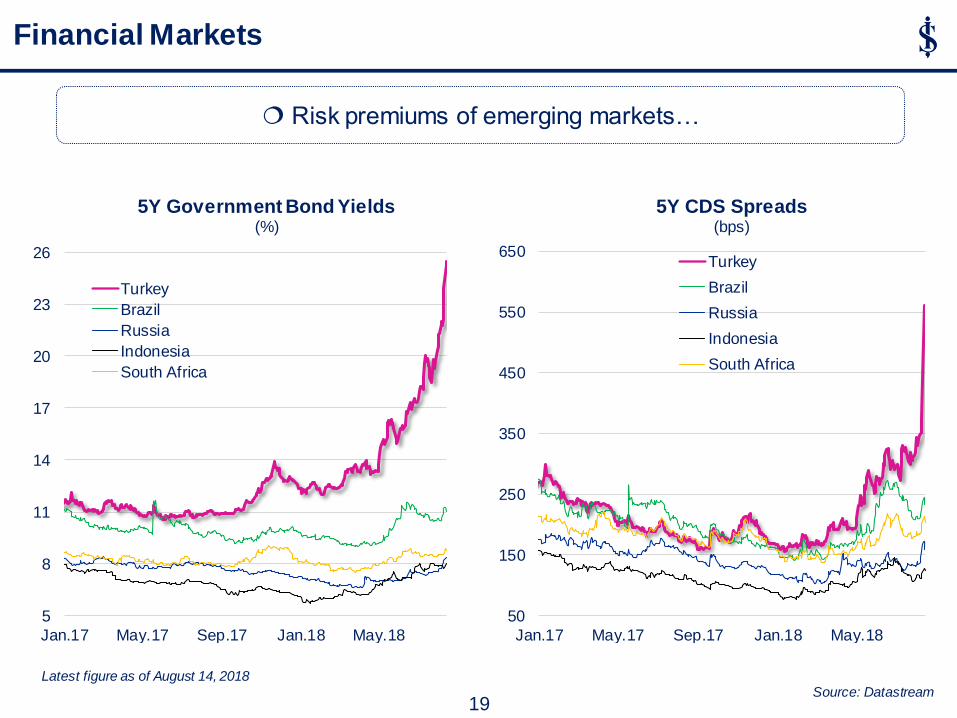

Financial Markets

Risk premiums of emerging markets…

Latest figure as of August 14, 2018 Source: Datastream

19

5

8

11

14

17

20

23

26

Jan.17 May.17 Sep.17 Jan.18 May.18

5Y Government Bond Yields (%)

Turkey

Brazil

Russia

Indonesia

South Africa

50

150

250

350

450

550

650

Jan.17 May.17 Sep.17 Jan.18 May.18

5Y CDS Spreads (bps)

Turkey

Brazil

Russia

Indonesia

South Africa

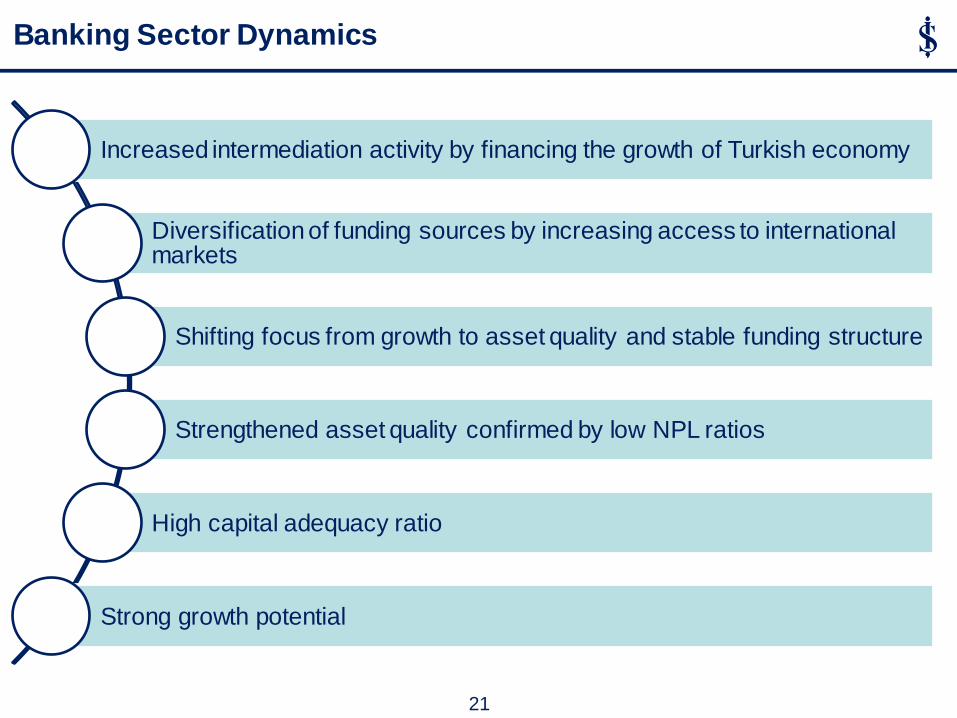

Banking Sector Dynamics

Banking Sector Dynamics

Increased intermediation activity by financing the growth of Turkish economy

Diversification of funding sources by increasing access to international markets

Shifting focus from growth to asset quality and stable funding structure

Strengthened asset quality confirmed by low NPL ratios

High capital adequacy ratio

Strong growth potential

21

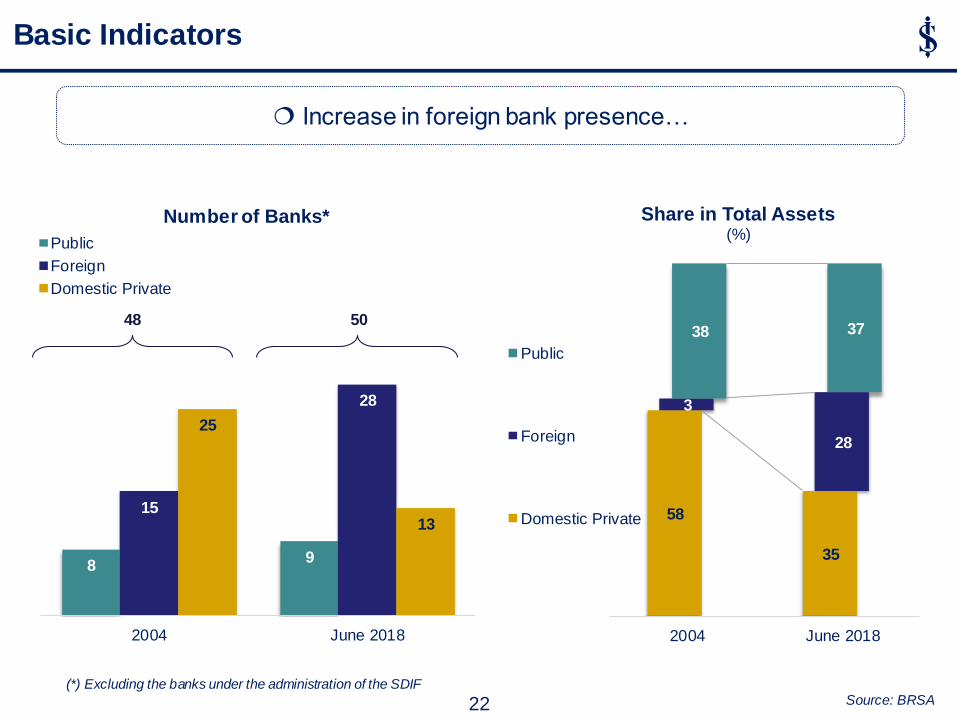

Increase in foreign bank presence…

(*) Excluding the banks under the administration of the SDIF Source: BRSA

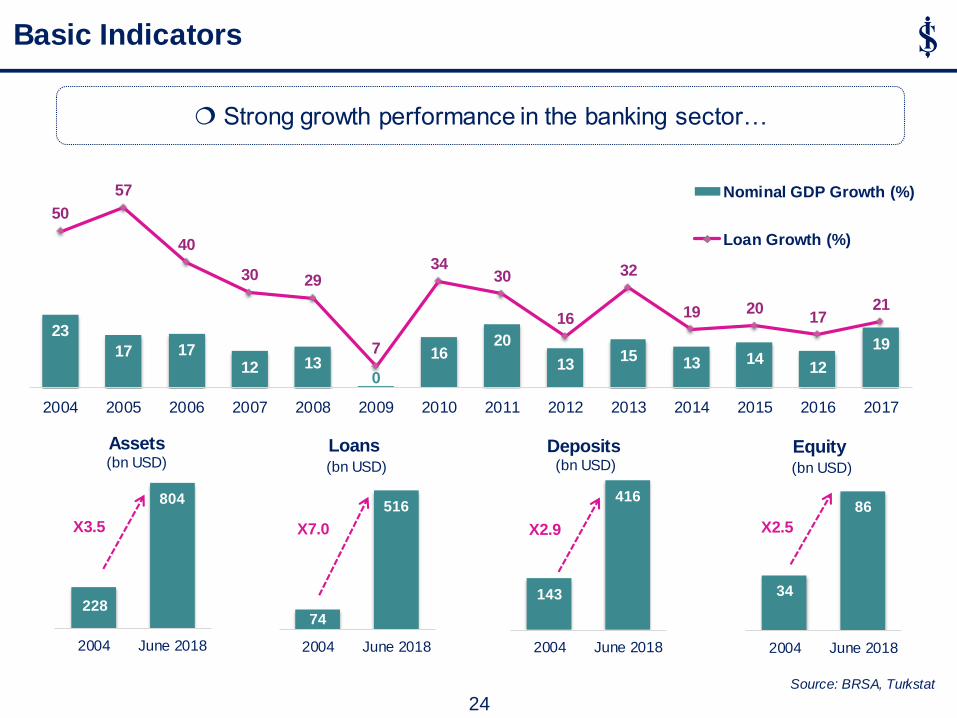

Basic Indicators

22

8 9

15

28

25

13

2004 June 2018

Number of Banks*

Public

Foreign

Domestic Private

50 48

58

35

3

28

38 37

2004 June 2018

Share in Total Assets (%)

Public

Foreign

Domestic Private

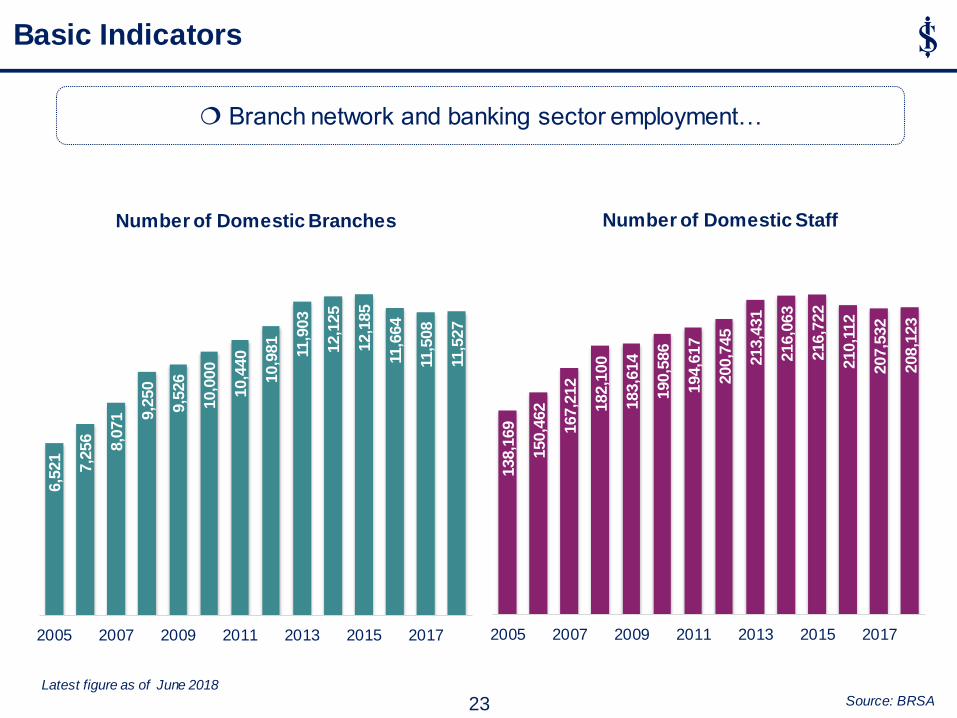

Branch network and banking sector employment…

Latest figure as of June 2018 Source: BRSA

Basic Indicators 6,5

21

7,2

56

8,0

71 9,2

50

9,5

26

10,0

00

10,4

40

10,9

81

11,9

03

12,1

25

12,1

85

11,6

64

11,5

08

11,5

27

2005 2007 2009 2011 2013 2015 2017

Number of Domestic Branches

23

138,1

69

150,4

62

167,2

12

182,1

00

183,6

14

190,5

86

194,6

17

200,7

45

213,4

31

216,0

63

216,7

22

210,1

12

207,5

32

208,1

23

2005 2007 2009 2011 2013 2015 2017

Number of Domestic Staff

23

17 17 12 13

0

16 20

13 15 13 14

12

19

50

57

40

30 29

7

34 30

16

32

19 20 17

21

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Nominal GDP Growth (%)

Loan Growth (%)

228

804

2004 June 2018

Assets (bn USD)

X3.5

Basic Indicators

143

416

2004 June 2018

Deposits (bn USD)

X2.9

74

516

2004 June 2018

Loans (bn USD)

X7.0

34

86

2004 June 2018

Equity (bn USD)

X2.5

Strong growth performance in the banking sector…

24 Source: BRSA, Turkstat

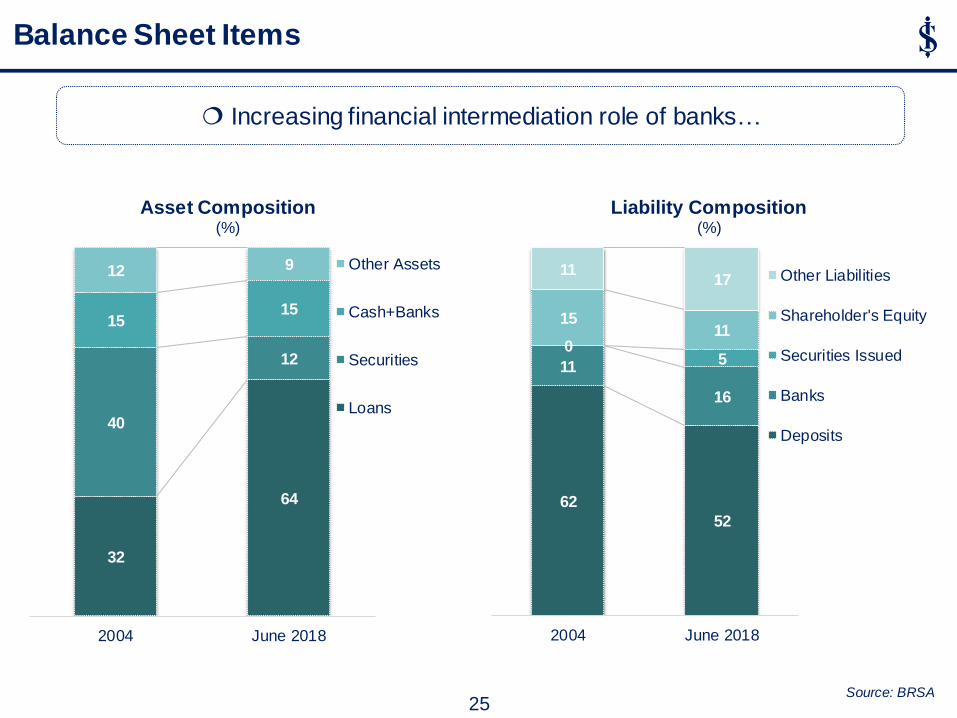

Increasing financial intermediation role of banks…

Source: BRSA

Balance Sheet Items

25

32

64

40

12

15 15

12 9

2004 June 2018

Asset Composition (%)

Other Assets

Cash+Banks

Securities

Loans

62

52

11

16

0 5

15 11

11 17

2004 June 2018

Liability Composition (%)

Other Liabilities

Shareholder's Equity

Securities Issued

Banks

Deposits

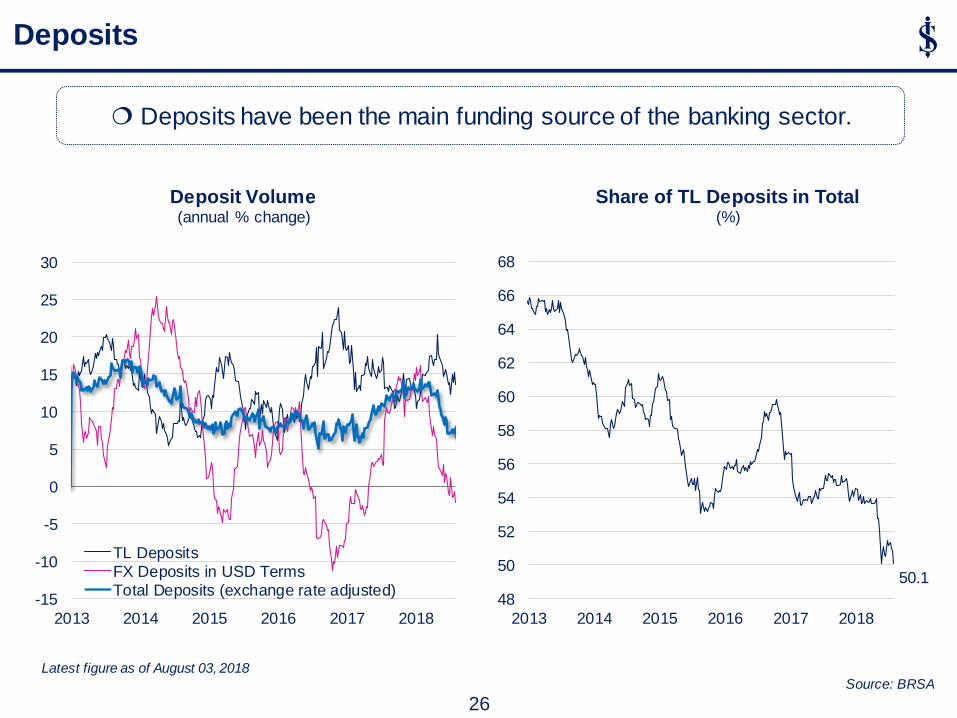

Deposits

Latest figure as of August 03, 2018 Source: BRSA

Deposits have been the main funding source of the banking sector.

26

-15

-10

-5

0

5

10

15

20

25

30

2013 2014 2015 2016 2017 2018

Deposit Volume (annual % change)

TL DepositsFX Deposits in USD TermsTotal Deposits (exchange rate adjusted)

50.1

48

50

52

54

56

58

60

62

64

66

68

2013 2014 2015 2016 2017 2018

Share of TL Deposits in Total (%)

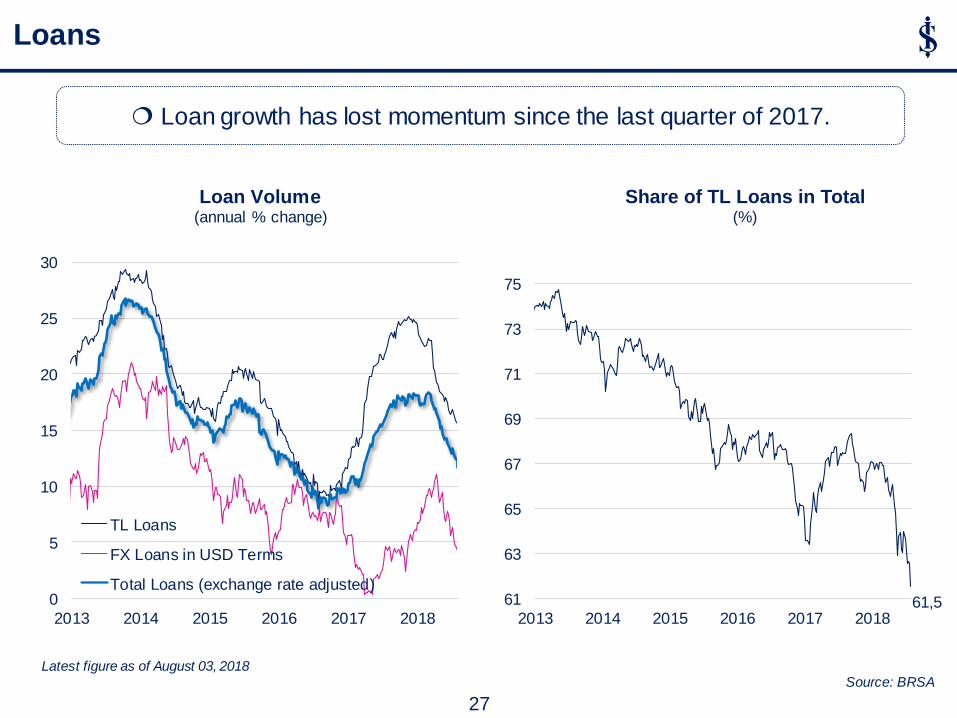

Loans

Loan growth has lost momentum since the last quarter of 2017.

27

61,5 61

63

65

67

69

71

73

75

2013 2014 2015 2016 2017 2018

Share of TL Loans in Total (%)

0

5

10

15

20

25

30

2013 2014 2015 2016 2017 2018

Loan Volume (annual % change)

TL Loans

FX Loans in USD Terms

Total Loans (exchange rate adjusted)

Latest figure as of August 03, 2018 Source: BRSA

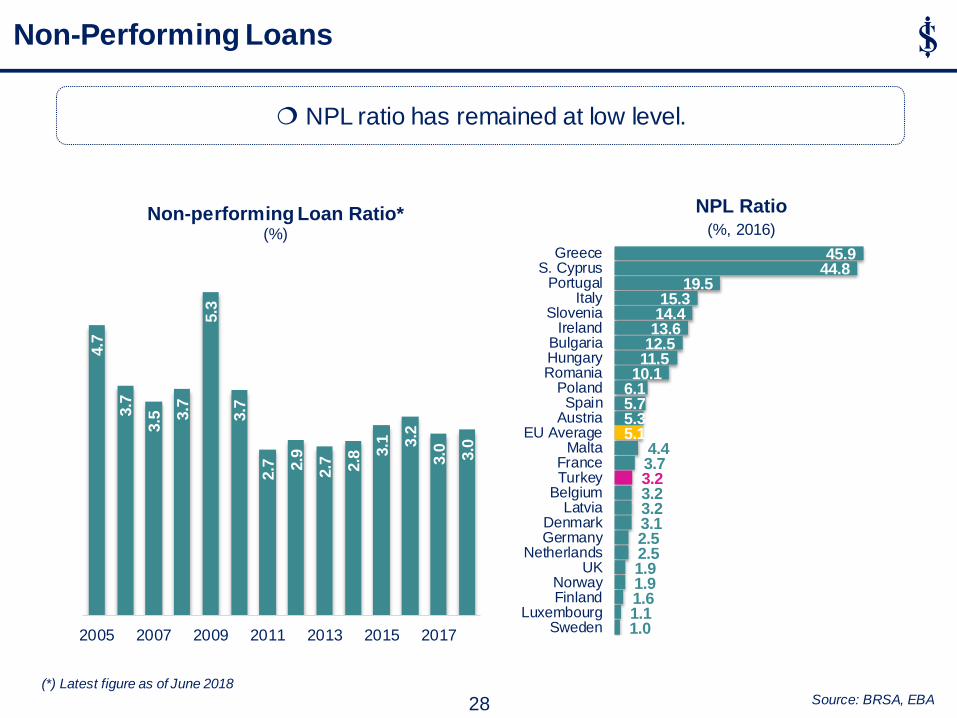

NPL ratio has remained at low level.

(*) Latest figure as of June 2018 Source: BRSA, EBA

Non-Performing Loans

1.0 1.1 1.6 1.9 1.9 2.5 2.5 3.1 3.2 3.2 3.2 3.7 4.4

5.1 5.3 5.7 6.1 10.1 11.5 12.5 13.6 14.4 15.3

19.5 44.8 45.9

SwedenLuxembourg

FinlandNorway

UKNetherlands

GermanyDenmark

LatviaBelgiumTurkeyFrance

MaltaEU Average

AustriaSpain

PolandRomaniaHungaryBulgaria

IrelandSlovenia

ItalyPortugal

S. CyprusGreece

NPL Ratio (%, 2016)

28

4.7

3.7

3.5

3.7

5.3

3.7

2.7

2.9

2.7

2.8

3.1

3.2

3.0

3.0

2005 2007 2009 2011 2013 2015 2017

Non-performing Loan Ratio* (%)

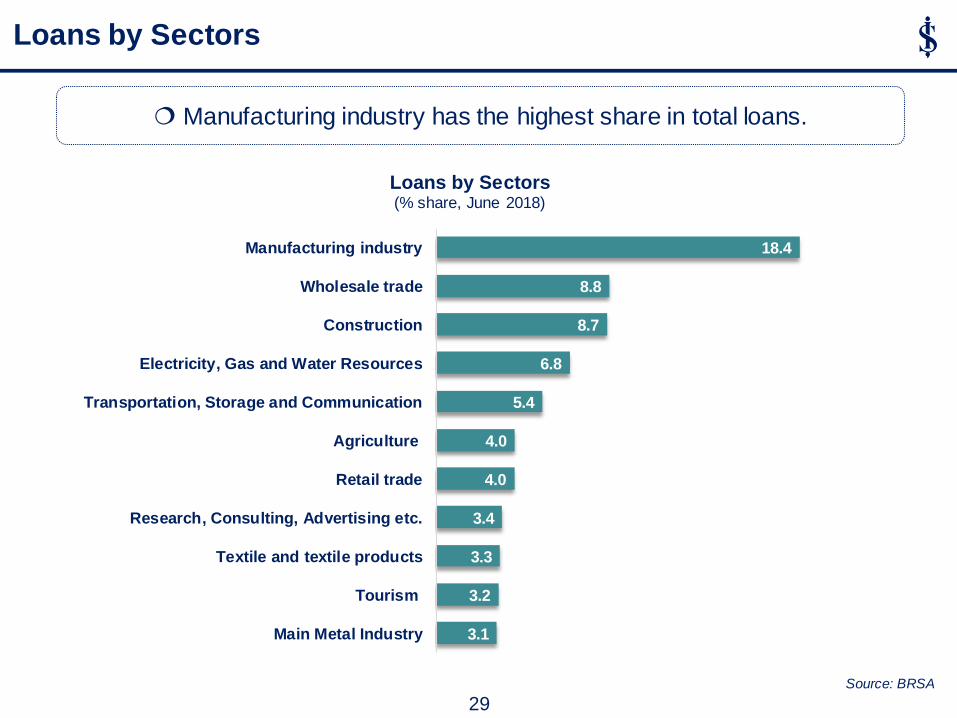

Manufacturing industry has the highest share in total loans.

Loans by Sectors

29

3.1

3.2

3.3

3.4

4.0

4.0

5.4

6.8

8.7

8.8

18.4

Main Metal Industry

Tourism

Textile and textile products

Research, Consulting, Advertising etc.

Retail trade

Agriculture

Transportation, Storage and Communication

Electricity, Gas and Water Resources

Construction

Wholesale trade

Manufacturing industry

Loans by Sectors (% share, June 2018)

Source: BRSA

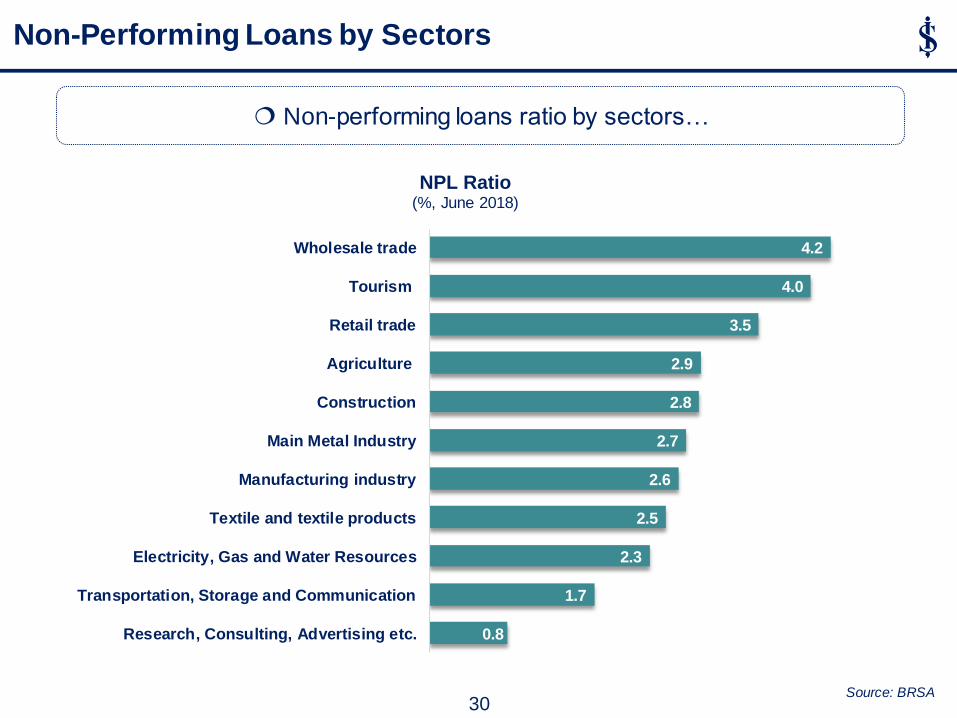

Non-performing loans ratio by sectors…

Source: BRSA

0.8

1.7

2.3

2.5

2.6

2.7

2.8

2.9

3.5

4.0

4.2

Research, Consulting, Advertising etc.

Transportation, Storage and Communication

Electricity, Gas and Water Resources

Textile and textile products

Manufacturing industry

Main Metal Industry

Construction

Agriculture

Retail trade

Tourism

Wholesale trade

NPL Ratio (%, June 2018)

Non-Performing Loans by Sectors

30

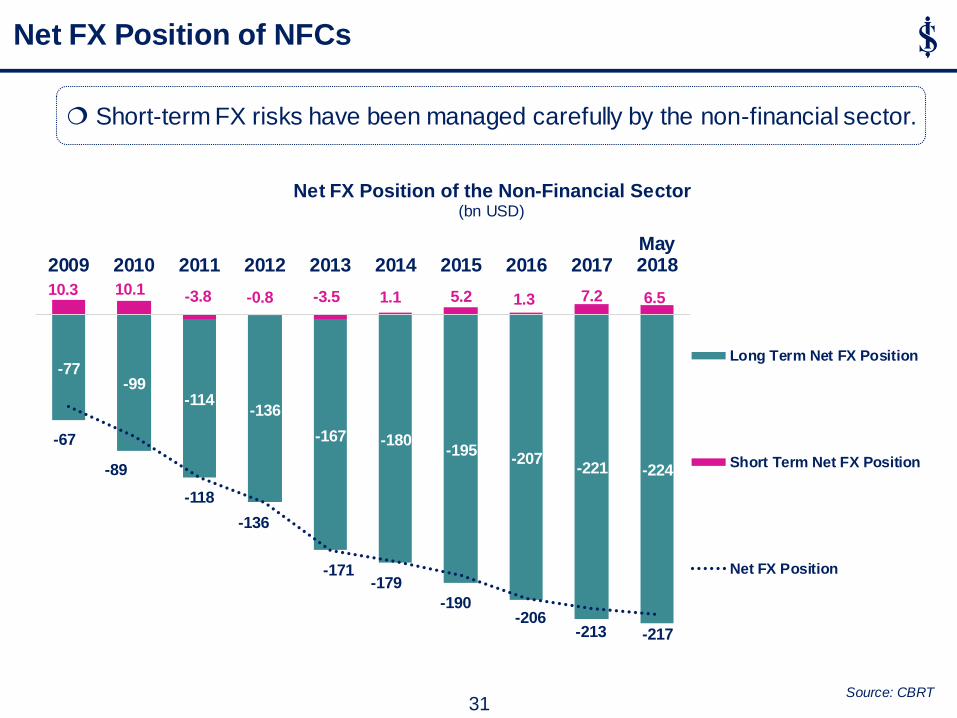

Short-term FX risks have been managed carefully by the non-financial sector.

Source: CBRT

Net FX Position of NFCs

10.3 10.1 -3.8 -0.8 -3.5 1.1 5.2 1.3 7.2 6.5

-77 -99

-114 -136

-167 -180 -195

-207 -221 -224

-67

-89

-118

-136

-171 -179

-190 -206

-213 -217

2009 2010 2011 2012 2013 2014 2015 2016 2017May2018

Net FX Position of the Non-Financial Sector (bn USD)

Long Term Net FX Position

Short Term Net FX Position

Net FX Position

31

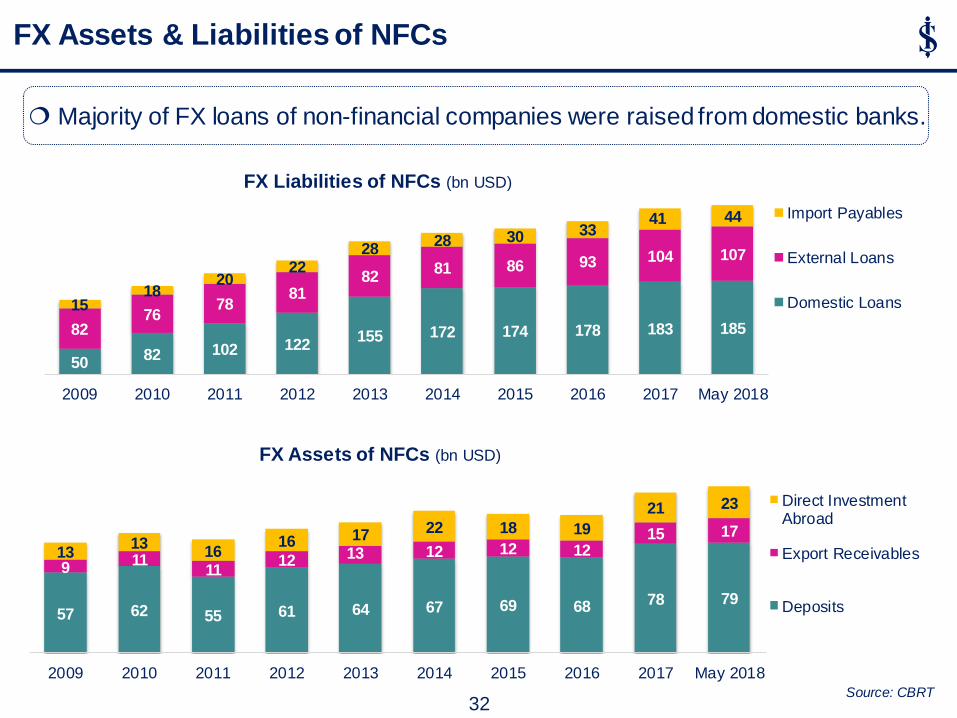

Majority of FX loans of non-financial companies were raised from domestic banks.

57 62 55 61 64 67 69 68 78 79

9 11

11 12 13 12 12 12

15 17

13 13

16 16 17 22 18 19

21 23

2009 2010 2011 2012 2013 2014 2015 2016 2017 May 2018

FX Assets of NFCs (bn USD)

Direct InvestmentAbroad

Export Receivables

Deposits

50 82 102 122

155 172 174 178 183 185 82 76

78 81

82 81 86 93 104 107

15 18

20 22

28 28 30 33

41 44

2009 2010 2011 2012 2013 2014 2015 2016 2017 May 2018

FX Liabilities of NFCs (bn USD)

Import Payables

External Loans

Domestic Loans

Source: CBRT

FX Assets & Liabilities of NFCs

32

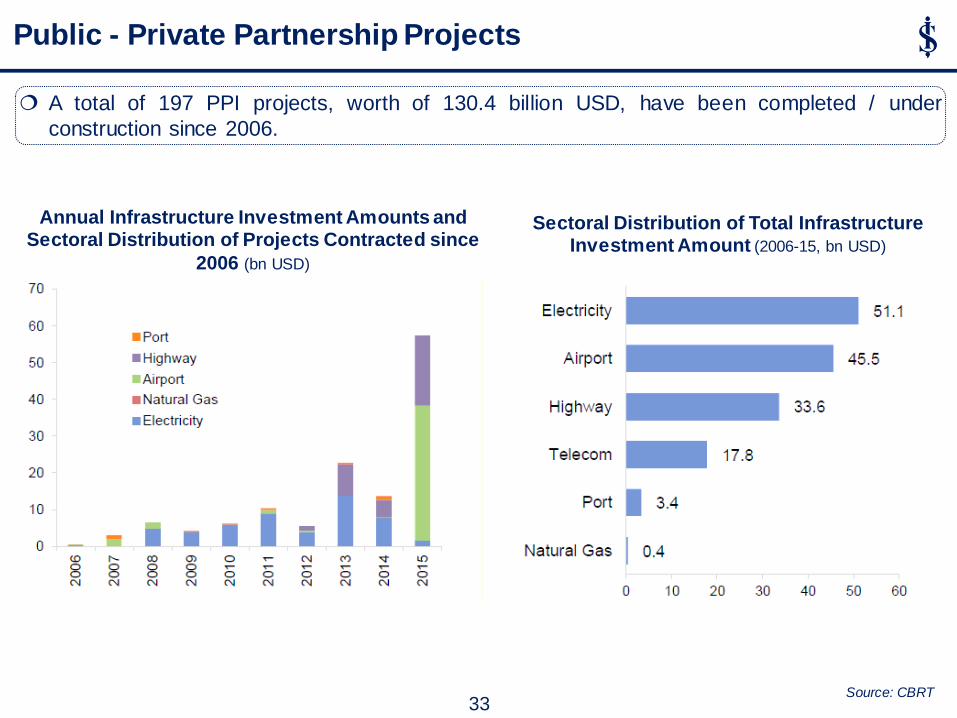

A total of 197 PPI projects, worth of 130.4 billion USD, have been completed / under

construction since 2006.

Source: CBRT

Annual Infrastructure Investment Amounts and Sectoral Distribution of Projects Contracted since

2006 (bn USD)

Public - Private Partnership Projects

Sectoral Distribution of Total Infrastructure Investment Amount (2006-15, bn USD)

33

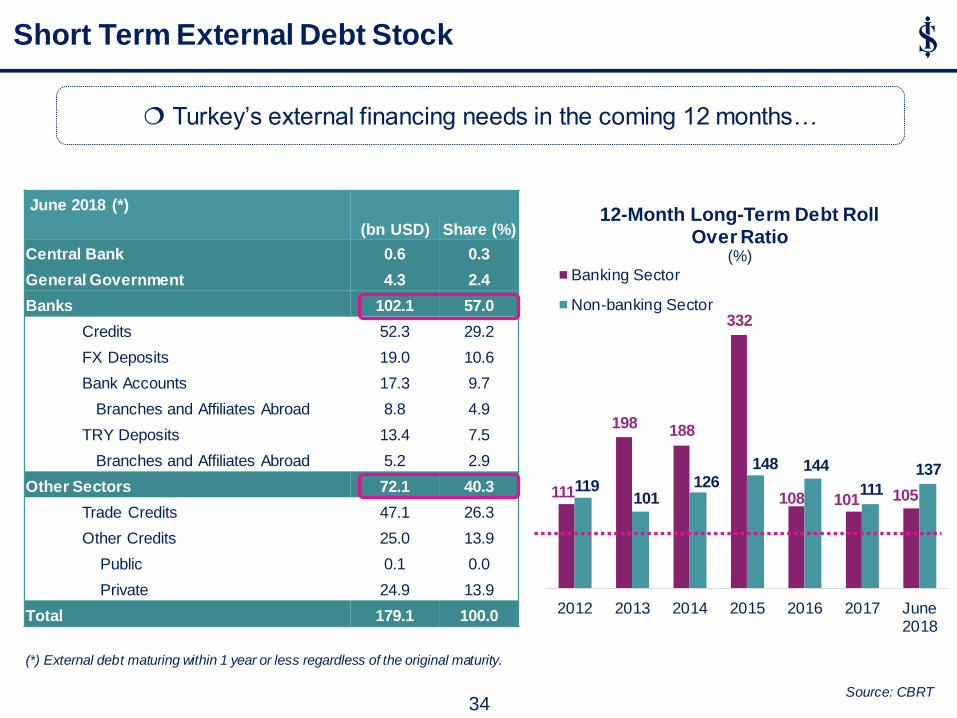

Turkey’s external financing needs in the coming 12 months…

June 2018 (*)

(bn USD) Share (%)

Central Bank 0.6 0.3

General Government 4.3 2.4

Banks 102.1 57.0

Credits 52.3 29.2

FX Deposits 19.0 10.6

Bank Accounts 17.3 9.7

Branches and Affiliates Abroad 8.8 4.9

TRY Deposits 13.4 7.5

Branches and Affiliates Abroad 5.2 2.9

Other Sectors 72.1 40.3

Trade Credits 47.1 26.3

Other Credits 25.0 13.9

Public 0.1 0.0

Private 24.9 13.9

Total 179.1 100.0

(*) External debt maturing within 1 year or less regardless of the original maturity.

Source: CBRT

Short Term External Debt Stock

111

198 188

332

108 101 105 119

101 126

148 144

111

137

2012 2013 2014 2015 2016 2017 June2018

12-Month Long-Term Debt Roll Over Ratio

(%)

Banking Sector

Non-banking Sector

34

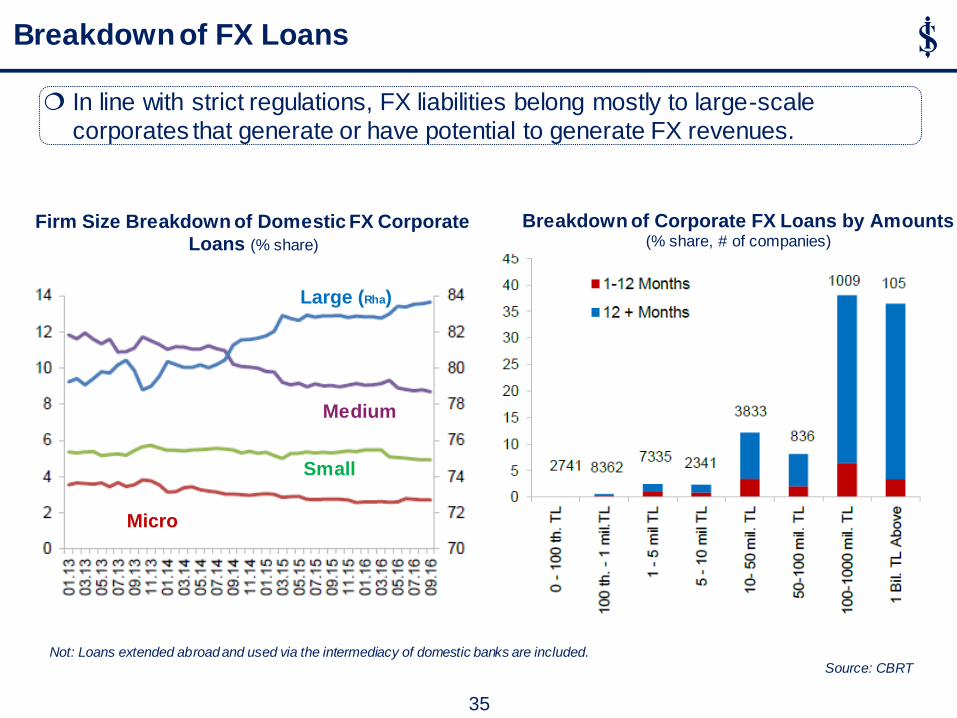

In line with strict regulations, FX liabilities belong mostly to large-scale

corporates that generate or have potential to generate FX revenues.

Not: Loans extended abroad and used via the intermediacy of domestic banks are included. Source: CBRT

Firm Size Breakdown of Domestic FX Corporate Loans (% share)

Breakdown of FX Loans

Micro

Medium

Small

Large (Rha)

Breakdown of Corporate FX Loans by Amounts (% share, # of companies)

35

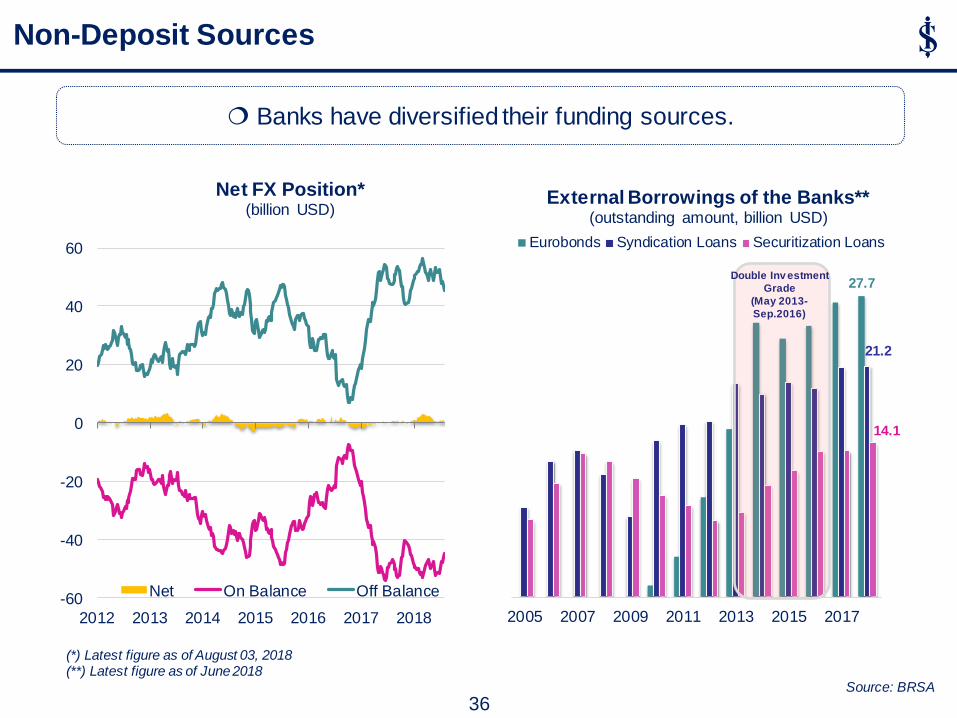

Non-Deposit Sources

(*) Latest figure as of August 03, 2018 (**) Latest figure as of June 2018

Source: BRSA

Banks have diversified their funding sources.

36

27.7

21.2

14.1

2005 2007 2009 2011 2013 2015 2017

External Borrowings of the Banks** (outstanding amount, billion USD)

Eurobonds Syndication Loans Securitization Loans

Double Inv estment

Grade

(May 2013-

Sep.2016)

-60

-40

-20

0

20

40

60

2012 2013 2014 2015 2016 2017 2018

Net FX Position* (billion USD)

Net On Balance Off Balance

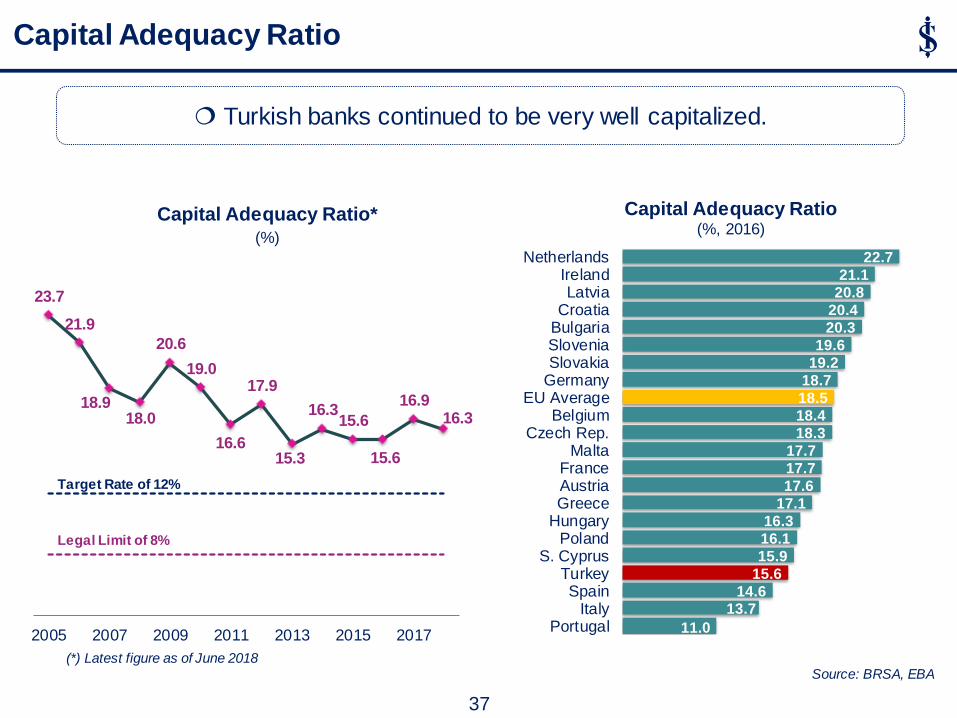

Turkish banks continued to be very well capitalized.

Capital Adequacy Ratio

11.0

13.7 14.6

15.6

15.9

16.1

16.3

17.1

17.6

17.7

17.7

18.3

18.4

18.5

18.7

19.2

19.6

20.3

20.4

20.8

21.1

22.7

PortugalItaly

SpainTurkey

S. CyprusPoland

HungaryGreeceAustriaFrance

MaltaCzech Rep.

BelgiumEU Average

GermanySlovakiaSloveniaBulgariaCroatiaLatvia

IrelandNetherlands

Capital Adequacy Ratio (%, 2016)

37

23.7

21.9

18.9 18.0

20.6

19.0

16.6

17.9

15.3

16.3 15.6

15.6

16.9 16.3

2005 2007 2009 2011 2013 2015 2017

Capital Adequacy Ratio* (%)

Legal Limit of 8%

Target Rate of 12%

(*) Latest figure as of June 2018 Source: BRSA, EBA

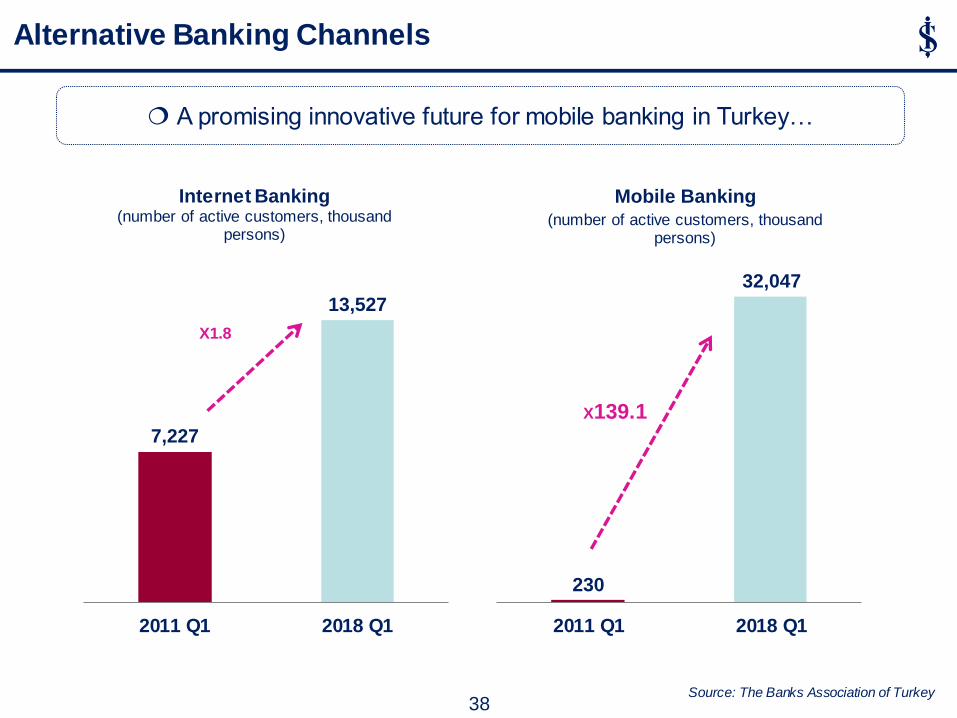

Alternative Banking Channels

Source: The Banks Association of Turkey

230

32,047

2011 Q1 2018 Q1

Mobile Banking (number of active customers, thousand

persons)

7,227

13,527

2011 Q1 2018 Q1

Internet Banking (number of active customers, thousand

persons)

X1.8

X139.1

38

A promising innovative future for mobile banking in Turkey…

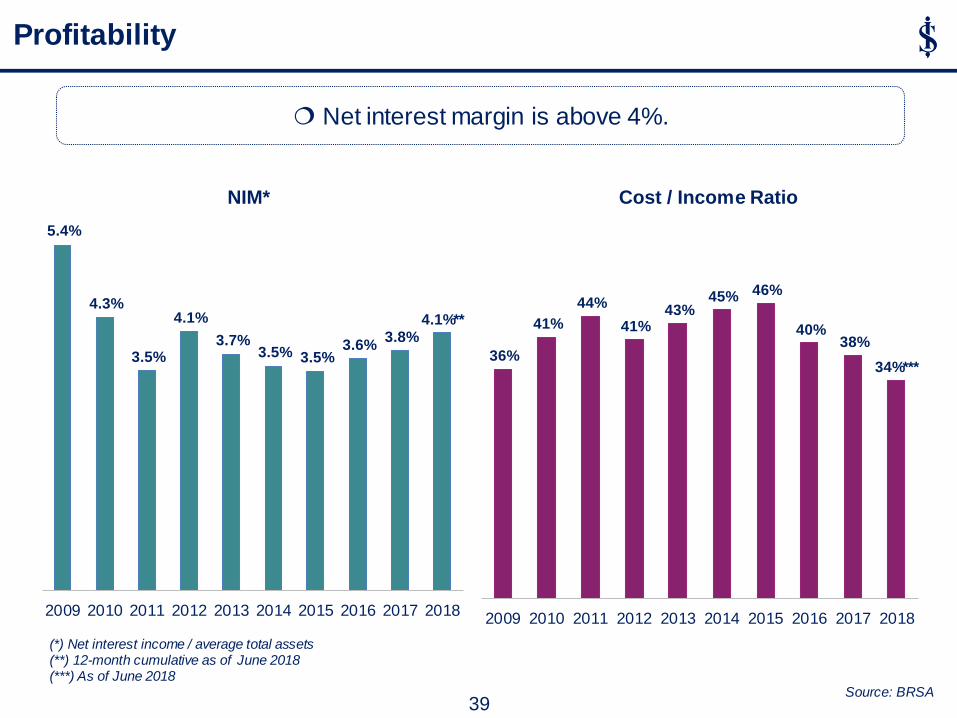

Profitability

Net interest margin is above 4%.

39

5.4%

4.3%

3.5%

4.1%

3.7% 3.5% 3.5%

3.6% 3.8%

4.1%**

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

NIM*

36%

41%

44%

41% 43%

45% 46%

40% 38%

34%***

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Cost / Income Ratio

(*) Net interest income / average total assets (**) 12-month cumulative as of June 2018 (***) As of June 2018

Source: BRSA

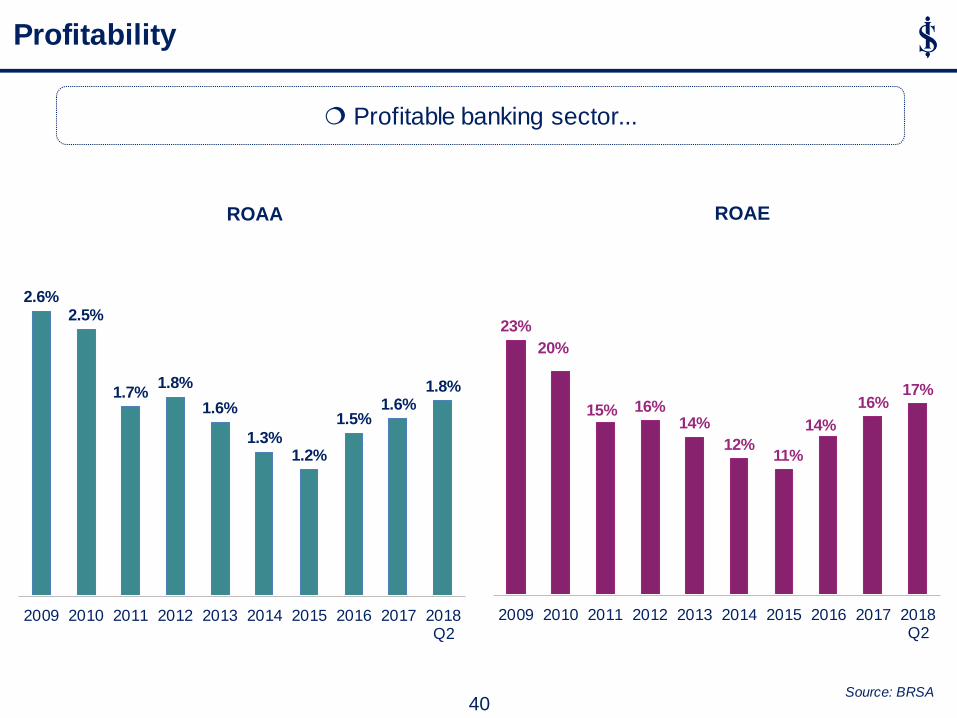

Profitable banking sector...

Profitability

2.6% 2.5%

1.7% 1.8%

1.6%

1.3% 1.2%

1.5% 1.6%

1.8%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Q2

ROAA

23%

20%

15% 16% 14%

12% 11%

14%

16% 17%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Q2

ROAE

40

Source: BRSA

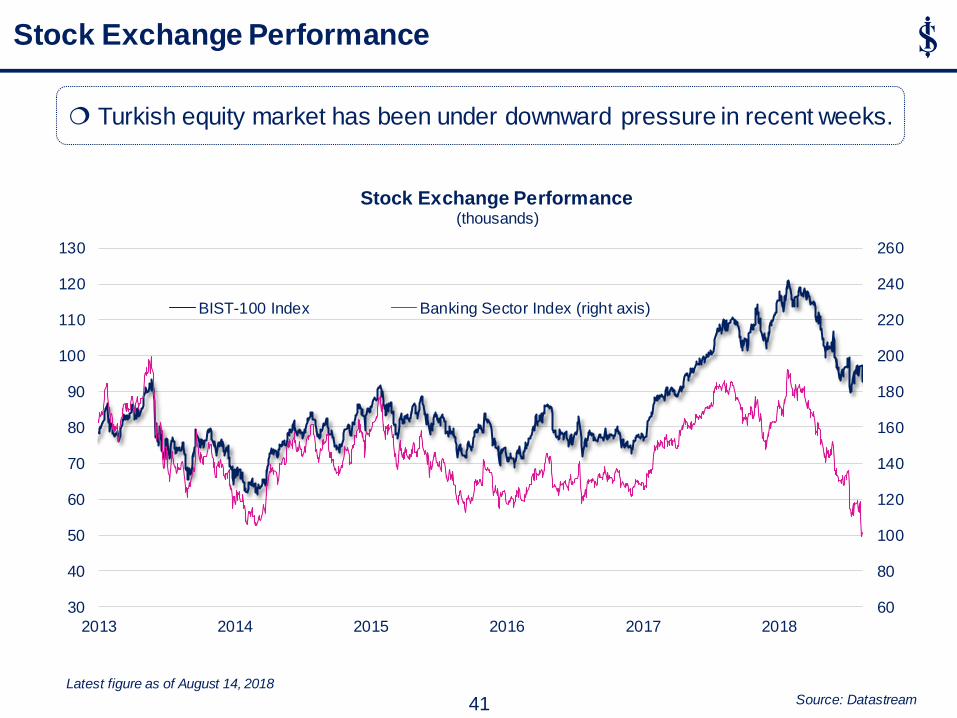

Latest figure as of August 14, 2018 Source: Datastream

Stock Exchange Performance

41

60

80

100

120

140

160

180

200

220

240

260

30

40

50

60

70

80

90

100

110

120

130

2013 2014 2015 2016 2017 2018

Bin

ler

Stock Exchange Performance (thousands)

BIST-100 Index Banking Sector Index (right axis)

Turkish equity market has been under downward pressure in recent weeks.

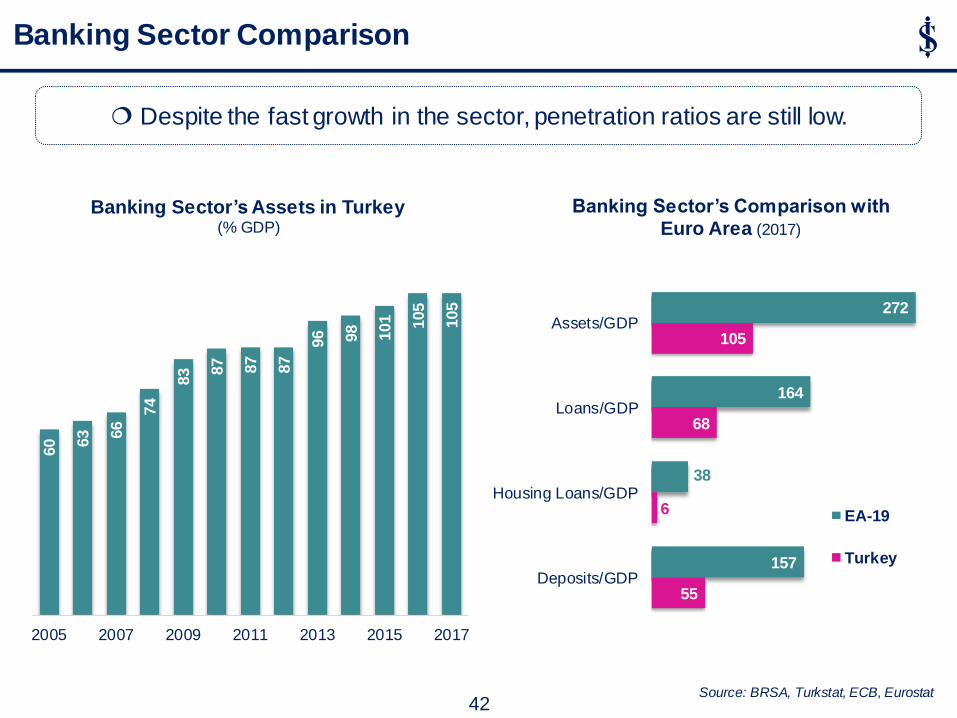

Source: BRSA, Turkstat, ECB, Eurostat

272

164

38

157

105

68

6

55

Assets/GDP

Loans/GDP

Housing Loans/GDP

Deposits/GDP

Banking Sector’s Comparison with Euro Area (2017)

(%, 2015)

EA-19

Turkey

Despite the fast growth in the sector, penetration ratios are still low.

60

63

66 7

4

83 87

87

87

96

98

101

105

105

2005 2007 2009 2011 2013 2015 2017

Banking Sector’s Assets in Turkey (% GDP)

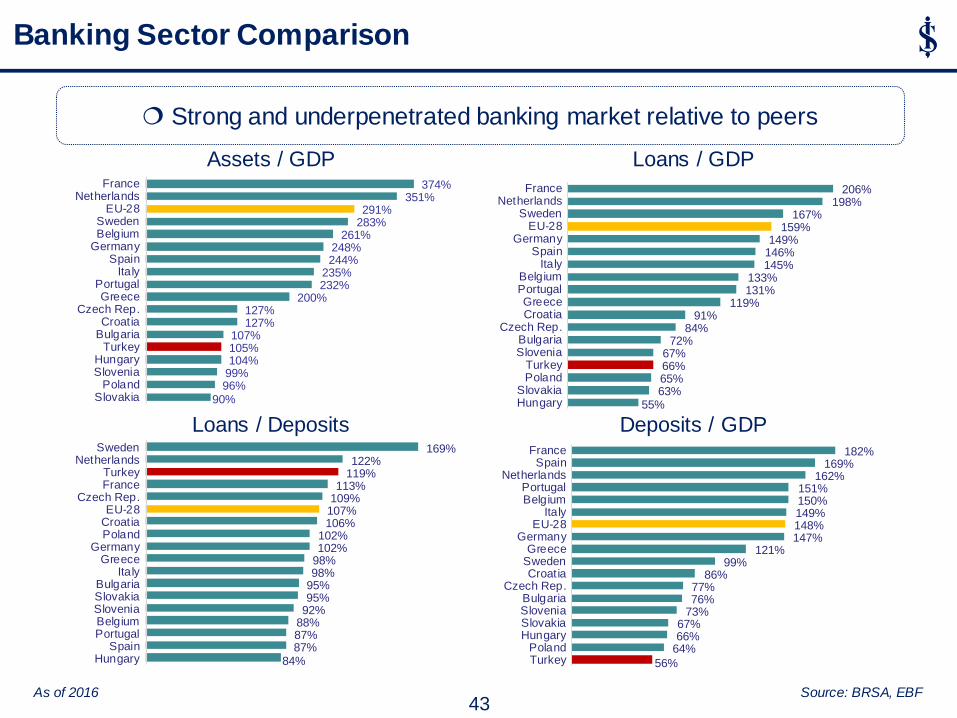

Banking Sector Comparison

42

Banking Sector Comparison

Assets / GDP Loans / GDP

Deposits / GDP Loans / Deposits

90% 96% 99% 104% 105% 107%

127% 127%

200% 232% 235%

244% 248%

261% 283% 291%

351% 374%

SlovakiaPoland

SloveniaHungary

TurkeyBulgariaCroatia

Czech Rep.Greece

PortugalItaly

SpainGermanyBelgiumSweden

EU-28Netherlands

France

55% 63% 65% 66% 67%

72% 84%

91% 119%

131% 133%

145% 146% 149%

159% 167%

198% 206%

HungarySlovakia

PolandTurkey

SloveniaBulgaria

Czech Rep.CroatiaGreece

PortugalBelgium

ItalySpain

GermanyEU-28

SwedenNetherlands

France

56%

64% 66% 67%

73% 76% 77%

86% 99%

121% 147% 148% 149% 150% 151%

162% 169%

182%

TurkeyPoland

HungarySlovakiaSloveniaBulgaria

Czech Rep.Croatia

SwedenGreece

GermanyEU-28

ItalyBelgiumPortugal

NetherlandsSpain

France

84% 87% 87% 88% 92% 95% 95% 98% 98% 102% 102%

106% 107% 109% 113%

119% 122%

169%

HungarySpain

PortugalBelgiumSloveniaSlovakiaBulgaria

ItalyGreece

GermanyPolandCroatiaEU-28

Czech Rep.FranceTurkey

NetherlandsSweden

As of 2016 Source: BRSA, EBF

Strong and underpenetrated banking market relative to peers

43

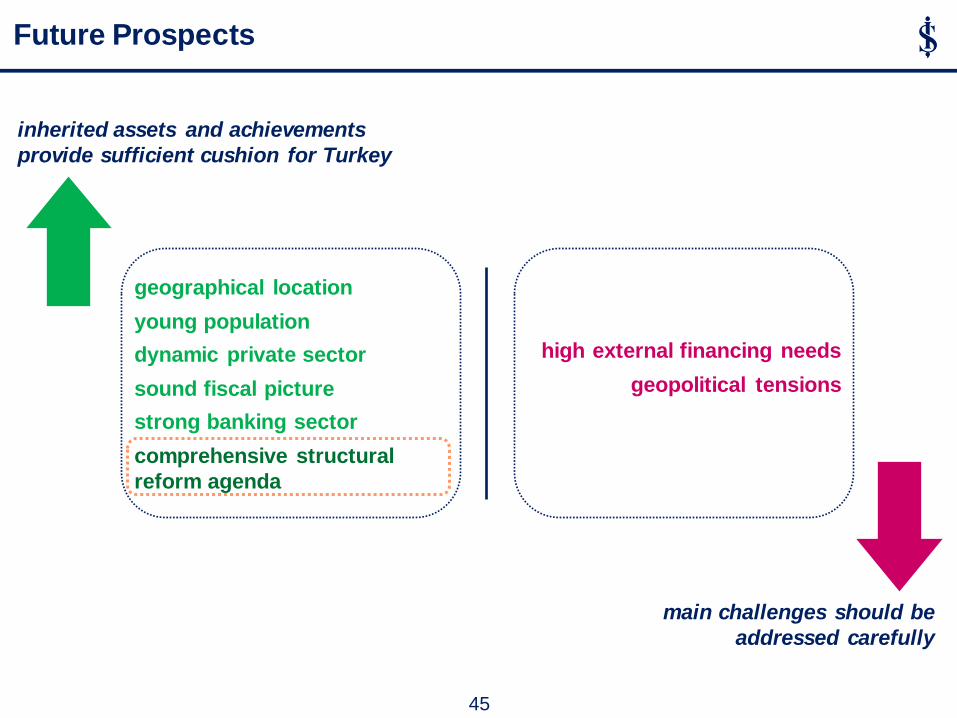

Future Prospects

Future Prospects

inherited assets and achievements

provide sufficient cushion for Turkey

main challenges should be

addressed carefully

geographical location

young population

dynamic private sector

sound fiscal picture

strong banking sector

comprehensive structural

reform agenda

high external financing needs

geopolitical tensions

45

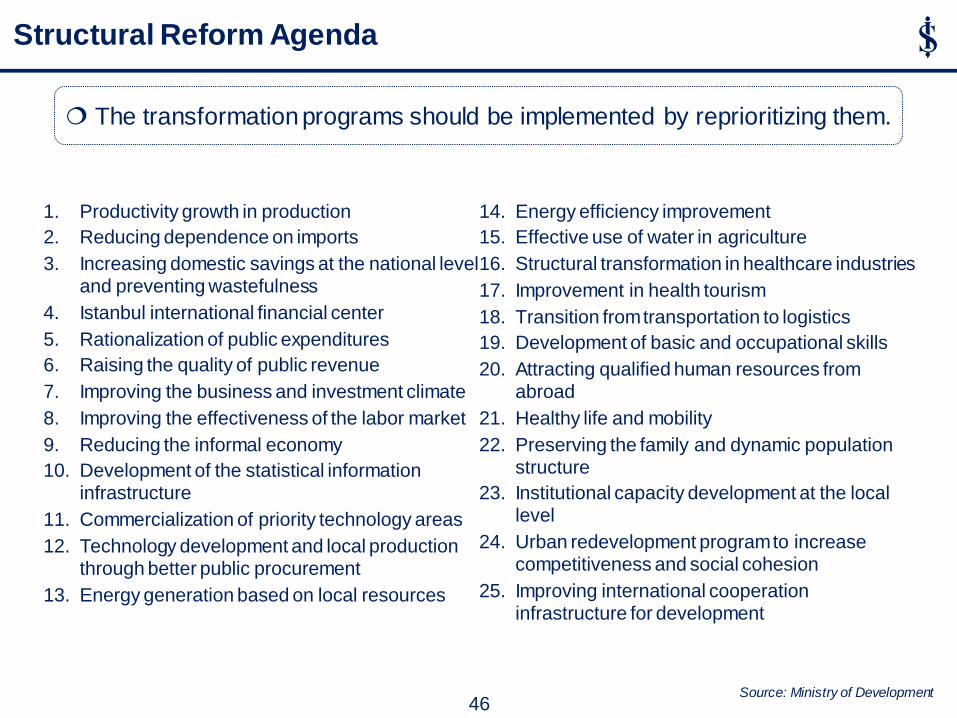

The transformation programs should be implemented by reprioritizing them.

Source: Ministry of Development

Structural Reform Agenda

1. Productivity growth in production

2. Reducing dependence on imports

3. Increasing domestic savings at the national level and preventing wastefulness

4. Istanbul international financial center

5. Rationalization of public expenditures

6. Raising the quality of public revenue

7. Improving the business and investment climate

8. Improving the effectiveness of the labor market

9. Reducing the informal economy

10. Development of the statistical information infrastructure

11. Commercialization of priority technology areas

12. Technology development and local production through better public procurement

13. Energy generation based on local resources

14. Energy efficiency improvement

15. Effective use of water in agriculture

16. Structural transformation in healthcare industries

17. Improvement in health tourism

18. Transition from transportation to logistics

19. Development of basic and occupational skills

20. Attracting qualified human resources from abroad

21. Healthy life and mobility

22. Preserving the family and dynamic population structure

23. Institutional capacity development at the local level

24. Urban redevelopment program to increase competitiveness and social cohesion

25. Improving international cooperation infrastructure for development

46

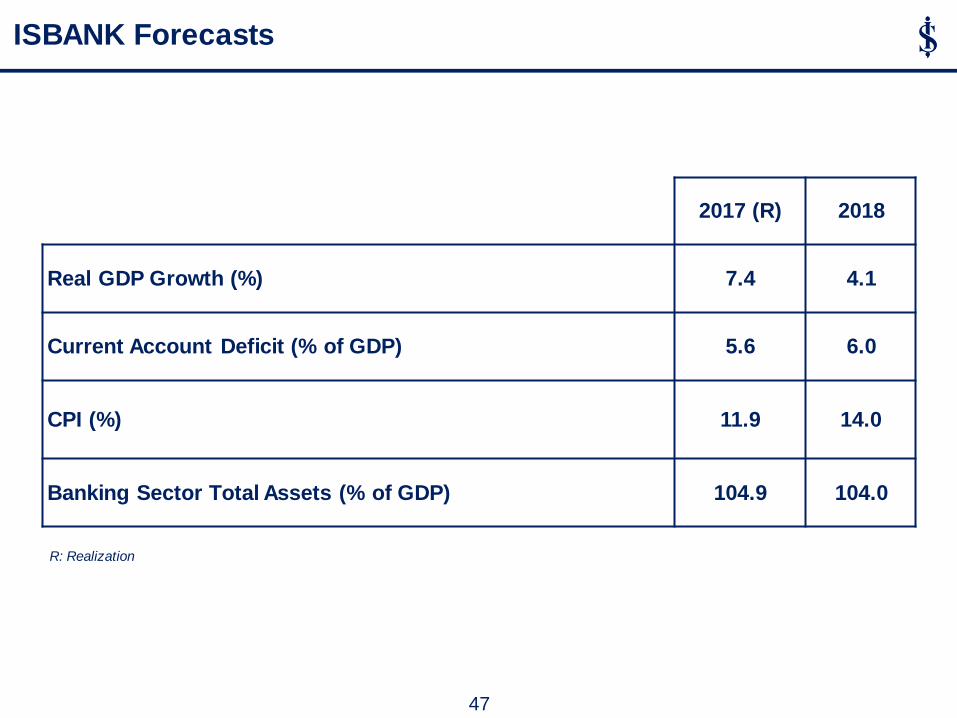

2017 (R) 2018

Real GDP Growth (%) 7.4 4.1

Current Account Deficit (% of GDP) 5.6 6.0

CPI (%) 11.9 14.0

Banking Sector Total Assets (% of GDP) 104.9 104.0

ISBANK Forecasts

R: Realization

47

LEGAL NOTICE

This report has been prepared by Türkiye İş Bankası A.Ş. economists and analysts by using the information from publicly available sources

believed to be reliable, solely for information purposes; and they are not intended to be construed as an offer or solicitation for the purchase

or sale of any financial instrument or the provision of an offer to provide investment services. The views, opinions and analyses expressed

do not represent the official standing of Türkiye İş Bankası A.Ş. and are personal views and opinions of the analysts and economists who

prepare the report. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information

contained in this report. All information contained in this report is subject to change without notice, Türkiye İş Bankası A,Ş, accepts no

liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

This report is copyright-protected. Reproducing, publishing and/or distributing this report in whole or in part is therefore prohibited. All rights

reserved.

Our reports are available on our website https://research.isbank.com.tr