Embed Size (px)

Citation preview

COUNTRY PROFILE 2001

TurkeyThis Country Profile is a reference tool, which providesanalysis of historical political, infrastructural and economictrends. It is revised and updated annually. The EIU’squarterly Country Reports analyse current trends andprovide a two-year forecast

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through our digital portfolio, where our latest analysis isupdated daily; through printed subscription products ranging from newsletters to annual referenceworks; through research reports; and by organising seminars and presentations. The firm is a member ofThe Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at http://store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-linedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

London: Jan Frost Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023New York: Dante Cantu Tel: (1.212) 554 0643 Fax: (1.212) 586 1181Hong Kong: Amy Ha Tel: (852) 2802 7288/2585 3888 Fax: (852) 2802 7720/7638

Copyright© 2001 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-6029

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

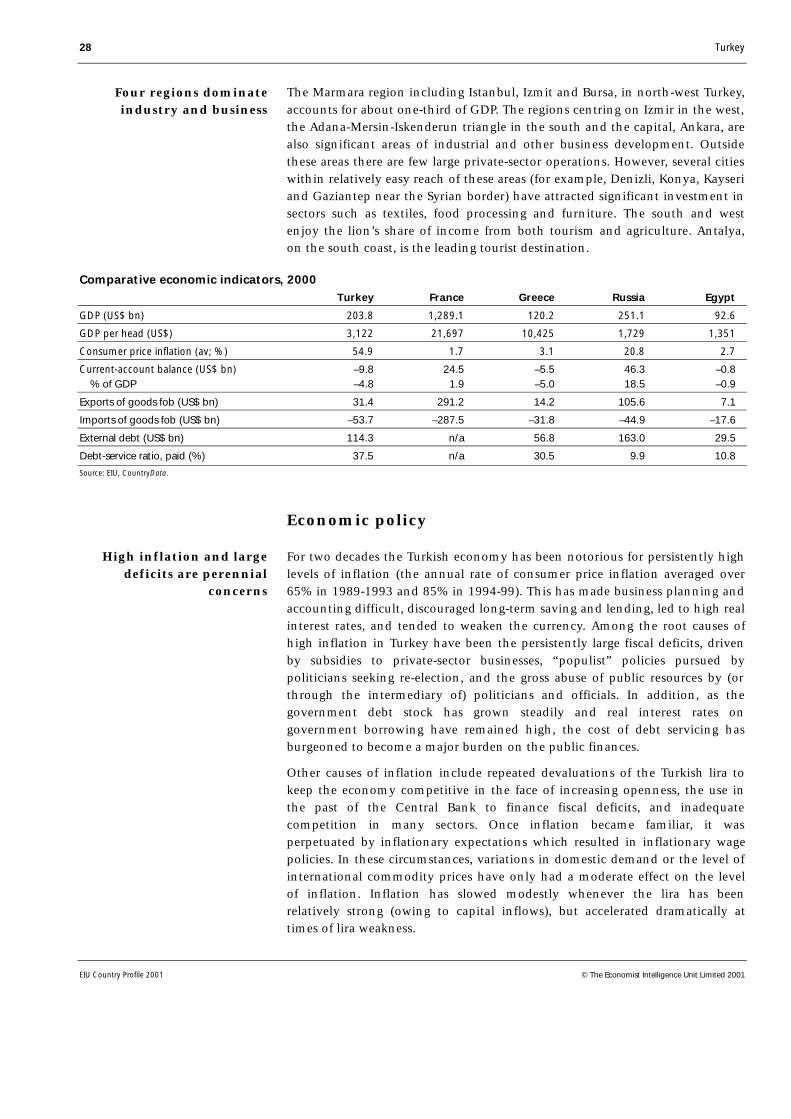

Comparative economic indicators, 2000

1

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Contents

3 Basic data

4 Political background4 Historical background

10 Constitution and institutions15 International relations and defence

18 Resources and infrastructure18 Population20 Education21 Health21 Natural resources and the environment22 Transport and communications24 Energy

27 The economy27 Economic structure28 Economic policy33 Economic performance35 Regional trends

36 Economic sectors36 Agriculture38 Mining and semi-processing39 Manufacturing42 Construction43 Financial services47 Tourism

47 The external sector47 Trade in goods50 Invisibles and the current account51 Capital flows and foreign debt53 Foreign reserves and the exchange rate

55 Appendices55 Sources of information57 Reference tables57 Population57 Labour force57 Transport statistics58 National energy statistics59 Consolidated government finances59 Money supply and interest rates60 Gross domestic product60 Gross domestic product by expenditure61 Gross domestic product by expenditure61 Gross value added by sector62 Gross value added by sector62 Prices and earnings62 Agricultural production

2 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

63 Livestock numbers63 Minerals production63 Manufacturing production64 Construction statistics64 The stockmarket64 Exports64 Imports65 Main trading partners65 Direction and composition of trade, 199866 Balance of payments, Central Bank of Turkey series67 Balance of payments, IMF series68 External debt68 Foreign reserves68 Exchange rates

Turkey 3

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Turkey

Basic data

779,452 sq km, of which 35% arable, 4% permanent crops, 26% forestry

63.5m (State Planning Organisation estimate of annual average in 2000)

Population, city (city and province in brackets), in ‘000, 1997 (State Institute ofStatistics)

Istanbul 8,567 (9,199)Ankara (capital) 3,085 (3,693)Izmir 2,118 (3,115)Adana 1,185 (1,682)Bursa 1,160 (1,958)

Mediterranean on the south coast, continental inland

Hottest month, August, 15-31°C (average daily minimum and maximum);coldest month, January, –4-4°C; driest month, August, 10 mm average rainfall;wettest month, December, 48 mm average rainfall

Turkish

Metric system

Turkish lira. Annual average exchange rate in 2000: TL625,218:US$1; exchangerate on May 30th 2001: TL1,163,851:US$1

2 hours ahead of GMT; 3 hours in summer

Calendar year

January 1st, April 23rd, May 19th, three days for Ramadan and four days forKurban depending on the Muslim calendar, August 30th, October 28th (half-day), October 29th

Land area

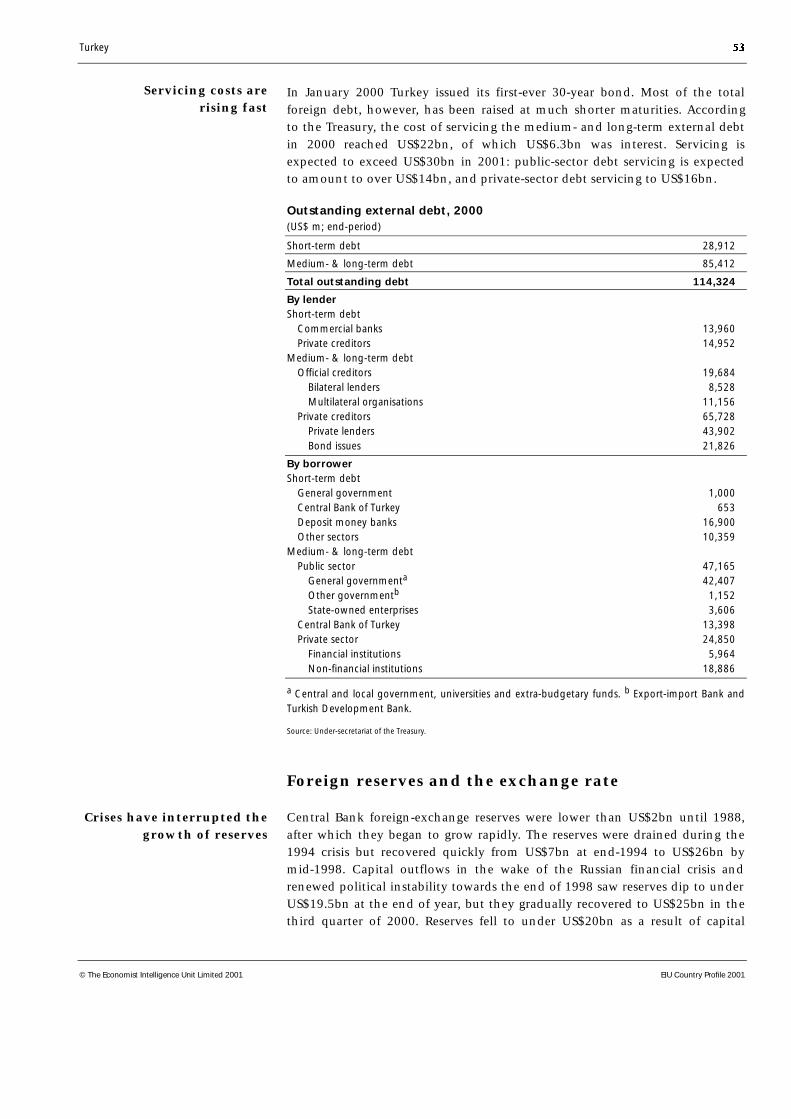

Population

Main towns

Climate

Weather in Ankara(altitude 861 metres)

Language

Measures

Currency

Time

Fiscal year

Public holidays

4 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Political background

The current government, which emerged from the April 1999 general election,is headed by Bulent Ecevit and comprises Mr Ecevit’s centre-left DemocraticLeft Party (DSP), the ultra-nationalist Nationalist Action Party (MHP) led byDevlet Bahceli, and Mesut Yilmaz’s Motherland Party (Anap). It has lastedlonger than any of its predecessors since 1995, but domestic and internationalconfidence in its ability to address Turkey’s urgent political and economicproblems received a severe shock after the eruption of a serious financial crisisin February-March 2001.

Historical background

Modern Turkish politics have been shaped by two crucial historicalexperiences: the foundation by Mustafa Kemal (who assumed the surnameAtaturk in 1936) of a secular, unitary republic in the 1920s, and theestablishment of a multiparty democratic regime since 1945. This has beeninterrupted by three periods of military rule in 1960-61, 1971-73 and 1980-83.

The Republic of Turkey was established in 1923 on the ruins of the Ottomanempire, which reached its zenith in the 16th century before suffering a longperiod of decline. Its fate was finally sealed when it joined the German side inthe first world war (1914-18). After the war, the victorious Entente powersdetached the remaining Arab provinces and prepared an elaborate plan todivide Anatolia, the Turkish-inhabited heartland of the former empire. In 1919Greek forces occupied Izmir (Smyrna) and fanned out into western Anatolia.The occupation triggered off a nationalist resistance movement, led by Ataturk,which decisively defeated the Greeks in 1922. In November of that year thesultanate was officially abolished. Following the signature of the Treaty ofLausanne in July 1923, Turkey became a republic, with Ataturk as its presidentand Ankara its capital.

Until his death in 1938 Ataturk presided over a single-party state. He brokewith the country’s Islamic past and promoted a secular national identity. Anetatist programme of state-led industrialisation was also instituted. Hissuccessor as president, Ismet Inonu, managed to maintain Turkey’s neutralityduring the second world war (1939-45). In 1945 he ended the single-party era,allowing the Democrat Party (DP), led by Adnan Menderes, to come to powerin Turkey’s first genuinely free election in 1950. Meanwhile, direct territorialthreats from the Soviet Union had pushed Turkey into the Western camp inthe cold war, and it was admitted to NATO in 1952.

Against a backdrop of growing economic difficulties, the military ousted theDP government on May 27th 1960, ostensibly because of its increasingintolerance towards the opposition. The army held power until October 1961,when a general election was held following the trial and execution ofMenderes and two of his former cabinet members. A period of weak coalitiongovernments followed until 1965, when the Justice Party (AP), led by

The establishment ofthe republic

The 1960s and 1970s

Turkey 5

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Suleyman Demirel and viewed as the successor to the DP, won the generalelection. Steady economic growth maintained the popularity of the AP, whichretained power in the 1969 election.

Nonetheless, increased left- and right-wing terrorism led to a second putsch bythe military in March 1971 and the installation of a technocratic governmentuntil 1973. In democratic elections in 1973 and 1977 none of the partiessucceeded in winning an overall majority. Thus, between 1974 and 1980Turkey was ruled by five feeble coalitions, headed alternately by the AP and thecentre-left Republican People’s Party (CHP), now headed by Bulent Ecevit. Bythe end of the 1970s the government and the economy seemed to be headingfor total collapse, with political violence claiming about 5,000 lives. A thirdmilitary takeover in September 1980 was greeted with general relief.

The leader of the 1980 coup, General Kenan Evren, established a five-manjunta which stayed in power until November 1983. During this period themilitary regime restored law and order through the draconian curtailment ofcivil rights. Economic reforms directed by the then deputy prime minister,Turgut Ozal, reduced inflation and the trade deficit, and economic growth wasrestored. In November 1982 a more restrictive constitution, intended toprovide stable government, was accepted in a national referendum, andGeneral Evren was elected president for the next seven years. Only three partieswere allowed to contest the September 1983 general election, in whichMr Ozal’s new Motherland Party (Anap) won a majority.

Under Ozal, who stayed in office as prime minister until 1989, parties excludedfrom the 1983 election emerged as important players. They included mostnotably the Social Democrat Party, led by Erdal Inonu, which merged with thePopulist Party in 1985 to become the Social Democrat Populist Party (SHP), andthe True Path Party (DYP), set up by Mr Demirel. Mr Ecevit, who had beenimprisoned for a time by the military after the 1980 coup, formed theDemocratic Left Party (DSP), while the Islamist tendency was represented bythe Welfare Party (Refah) led by Necmettin Erbakan. Following constitutionalamendments all these parties were allowed to compete in the 1987 election,but Ozal was returned to power with an increased majority.

When General Evren retired as president in November 1989, he was succeededby Ozal who, as president, won approval in the west for his support of Kuwaitfollowing the Iraqi invasion in August 1990, but failed to turn this to domesticpolitical advantage. His successor as prime minister, Yildirim Akbulut, wasreplaced by Mesut Yilmaz in June 1991. The latter opted for an early generalelection in October 1991, but Anap lost its majority. Mr Demirel thus returnedto office at the head of a coalition between the DYP and the SHP, withMr Inonu as deputy prime minister.

The Demirel government lasted until April 1993, when Ozal died suddenly.Mr Demirel was elected president the following month. His successor as partyleader and prime minister was Tansu Ciller. In March 1995 the SHP mergedwith the CHP under the latter’s name. On September 20th the CHP leader,Deniz Baykal, decided to withdraw the CHP from the coalition, following

The military regime,1980-83

Turgut Ozal’s leadership,1983-89

Mrs Ciller becomes primeminister in 1993

6 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Mrs Ciller’s refusal to meet his demands on the terms for the coalition. Sheresigned the same day, paving the way for a general election in December1995. Although serious financial and balance-of-payments crises in the firstquarter of 1994 marred Mrs Ciller’s record in office, one of her majorachievements was an agreement with the EU on the terms of a customs union,which came into force on January 1st 1996.

By this time the Kurdish issue had become Turkey’s major internal politicalproblem. About 15-20% of the population are Kurds, of whom about half livein their traditional homeland in the south-east, the other half havingmigrated to the industrial cities of western Turkey. The war in the south-eastern provinces against militants of the Kurdistan Workers’ Party (PKK)claimed around 30,000 lives between 1984 and 2000. By 1999 the army hadre-established control over most of the south-east. However, the counter-insurgency campaign led to serious human rights abuses by governmentforces, the compulsory evacuation of thousands of villages, severe disruptionof the region’s economy, and a cost to the government of an estimatedUS$6bn per year.

The results of the general election of December 24th 1995 confirmed the risingpopularity of Welfare (Refah), which received the largest share of the vote(21.4%). Welfare’s victory was made possible mainly by the even split of thecentre-right vote between the DYP and Anap, which together received 38.9%of the vote, and the rivalry between the two centre-left parties (DSP and CHP),which together won 25.3%. All other parties, notably the Nationalist ActionParty (MHP) and the pro-Kurdish People’s Democracy Party (Hadep), failed toovercome the 10% vote threshold to qualify for parliamentary seats.

After the election the two secular centre-right parties, Anap and DYP, formed acoalition at the end of February 1996, which lasted only until mid-June. Putinto place principally to keep Welfare from power, the coalition fell apart whenthe Anap leader, Mr Yilmaz, agreed to parliamentary investigations into allegedmalpractice by Mrs Ciller when she was prime minister. To avert corruptioninvestigations, Mrs Ciller then agreed to form a coalition with Welfare. TheWelfare-DYP coalition government, headed by Mr Erbakan, took office on June25th, bringing to power an Islamist-led government for the first time inTurkey’s history.

Mrs Ciller’s party controlled the most important ministerial portfolios, butMr Erbakan set the tone of the new administration. From the start the coalitionwas wracked by dissent between its two constituents, on both economic andforeign policy issues. It was further weakened by the revelation of damaginglinks between parts of the government and the police service with organisedcrime. Meanwhile, Mr Erbakan’s moves towards creeping Islamisation(especially in education) aroused the anger of the staunchly secularist generals,as well as much of an emerging civil society of intellectuals, businessorganisations, trades unions, and women’s groups. On June 18th 1997, in theface of repeated warnings from the military-dominated National SecurityCouncil as well as mounting public protests Mr Erbakan resigned, hoping toreconstruct the government under Mrs Ciller’s premiership. However,

The 1995 electionconfirms the rise of the

Welfare Party

An Islamist-led governmentlasts just 11 months

Turkey 7

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

backbench defections from the DYP to a short-lived Democratic Turkey Party(DTP) robbed the coalition of its majority. Accordingly, President Demirelpassed on the baton to Mr Yilmaz (Anap), who on June 30th 1997 formed aminority government, in coalition with DSP and the DTP, with outside supportfrom the CHP.

Mr Yilmaz’s third government—and Turkey’s fifth since the 1991 election—washampered by its minority status, which exaggerated the power of the CHP. Itcollapsed in November 1988, when Mr Yilmaz and the state minister for theeconomy, Gunes Taner, became embroiled in a corruption scandal related tothe privatisation of Turk Bank, and the CHP withdrew its support. In January1999 Mr Ecevit replaced Mr Yilmaz as the head of a minority DSP caretakergovernment, supported externally by Anap and DYP, with a mandate to takethe country to local and parliamentary elections on April 18th 1999.

The April 1999 legislative election produced an unlikely coalition government,led by Mr Ecevit and comprising his DSP, the ultra-nationalist MHP led byDevlet Bahceli, and Mr Yilmaz’s Anap. The election outcome was influenced toa considerable extent by the capture of the leader of the PKK, Abdullah Ocalan,on February 16th. The resultant upsurge in nationalist sentiment contributedto the growth in support for Mr Ecevit’s staunchly nationalist party, which wasenhanced by Mr Ecevit’s general reputation for honesty and by publicdisaffection with the mainstream centre-right parties, Anap and the DYP, andthe pro-Islamic Virtue Party. The strong nationalist sentiment also aided therise of the MHP. Accordingly, the DSP topped the poll. The MHP, which hadbeen excluded from parliament after the 1995 election because it did notsurmount the 10% vote threshold for representation, finished a close second.Anap, DYP and the Virtue Party (Fazilet, the successor to Welfare, banned inFebruary 1998), which were the other three parties to win representation inparliament, performed poorly, while the CHP was excluded because it failed toreach the 10% threshold.

Election results

Oct 1991 Dec 1995 Apr 1999 Seats % of votes Seats % of votes Seats % of votes

Democratic Left Party (DSP) 7 10.4 76 14.6 136 22.2

Nationalist Action Partya (MHP) 0 0.0 0 8.2 129 18.0

Virtue Partyb (Fazilet) 0 0 0 0 111 15.4

Welfare Partyb (Refah) 62 16.4 158 21.4 0 0

Motherland Party (Anap) 115 23.3 132 19.7 86 13.2

True Path Party (DYP) 178 26.2 135 19.2 85 12.0

Republican People’s Partyc (CHP) 88 20.1 49 10.7 0 8.7

People’s Democracy Party (Hadep) 0 0.0 0 4.2 0 4.8

Independents/others 0 3.6 0 2.1 3 5.7

Total 450 100.0 550 100.0 550 100.0

a In 1991 the Nationalist Action Party, then known as the Nationalist Endeavour Party (MCP), temporarily merged with the Islamist Welfare Party(Refah) in the general election. It then re-established itself as the MHP. b Formed in 1998 following the banning of Welfare. c In 1991 this was theSocial Democrat Populist Party (SHP), which merged with the Republican People’s Party under the latter’s title in February 1995.

Source: EIU.

Mr Yilmaz succeedsMr Erbakan asprime minister

The 1999 electionproduces a three-party

ruling coalition

8 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Important recent events

December 1995: The general election result is indecisive, but the pro-Islamist WelfareParty (Refah) receives 21.4% of the vote, becoming the largest party in parliament.

January 1996: The customs union with the EU comes into effect, but a clash withGreece over territorial rights in the Aegean sours Turkish-EU relations.

July 1996-June 1997: Welfare-True Path Party (DYP) form a government led by theWelfare leader, Necmettin Erbakan. Mr Erbakan resigns and his government collapsesfollowing a period of intense pressure from the military and public protests.

July 1997: A new three-party minority coalition government is formed, led by Anap’sMesut Yilmaz and including the Democratic Left Party (DSP) and the Democratic TurkeyParty (DTP). The external support of the Republican People’s Party (CHP) allows thegovernment to win a vote of confidence.

December 1997: At the European Council meeting in Luxembourg, the EU decidesnot to include Turkey as a candidate for EU membership in the next round ofenlargement.

November 1998: Mr Yilmaz resigns as prime minister following unproven allegationsof corruption.

January 1999: Bulent Ecevit, the leader of DSP, forms a one-party minority pre-electiongovernment with the external support of the Motherland Party (Anap) and the DYP.

April 1999: Boosted by the capture of Abdullah Ocalan. the leader of the KurdistanWorkers’ Party (PKK) in February, the DSP tops the poll with 22.2% of the vote in thegeneral election, followed unexpectedly by the Nationalist Action Party (MHP) with18%.

June 1999: The DSP, MHP and Anap form a government with a clear majority of 321out of 550 seats in parliament, and Mr Ecevit as prime minister.

August-November 1999: Two major earthquakes strike the areas around Izmit andBolu causing over 18,000 deaths, injuries to about 50,000 people and massivedestruction. The first provoked overseas sympathy and a dramatic improvement inrelations with Greece and the EU.

December 1999: The European Council meeting in Helsinki places Turkey on the list ofcandidates for eventual EU membership.

May 2000: Parliament elects Ahmet Necdet Sezer president after months of rulingcoalition wranglings which threatened to destabilise the government.

February-May 2001: A public quarrel between Mr Ecevit and President Sezer triggersa financial crash. The government appoints Kemal Dervis, a respected economist fromthe World Bank, to formulate a new programme of economic reforms. Although it isapproved by the government, the ruling coalition’s support is far from convincing. TheIMF and the World Bank pledge additional financial support.

Turkey 9

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Following its installation, Mr Ecevit’s government chalked up some notableachievements, mainly in the economic and foreign policy fields—most notablyby reforming the social security system, thereby helping to pave the way forapproval by the IMF of a three-year stand-by credit in December 1999. Adisastrous earthquake on August 17th 1999, which badly damaged the city ofIzmit, one of Turkey’s main industrial centres, provoked harsh criticisms of thegovernment for its slow and complacent reaction, but also brought about adramatic improvement in the climate of relations with Greece and westernEurope, as these countries, among many others, responded swiftly andgenerously with emergency assistance.

This led up to a crucial turning-point in Turkey’s relations with the EU. At themeeting of the European Council in December 1999 the EU heads ofgovernment reversed the decision made in Luxembourg two years earlier, bydeclaring Turkey a candidate for EU accession. But besides laying downimportant conditions regarding Turkey’s relations with Greece and settlementof the Cyprus problem (see below), the EU also made it clear that accessionnegotiations could not begin until Turkey met the political conditionsstipulated by the Council in June 1993—the so-called Copenhagen criteria. InNovember 2000 the EU Commission issued an Accession PartnershipDocument for Turkey which added some detail to these conditions. But whilethe government’s response—contained in the National Programme for theAdoption of the Acquis published in March 2001—on paper met most of the EU’srequirements, it did so in rather vague terms and failed to give precisecommitments regarding the abolition of capital punishment, the reform of theNational Security Council (which gives the military a powerful role ingovernment) or the legalisation of Kurdish-language broadcasting oreducation.

In April 2000 Mr Ecevit suffered a serious setback when parliament, includingmembers of the ruling coalition, turned down his proposed amendments tothe constitution which would, among other things, have allowed theincumbent president, Mr Demirel, to be elected for a second five-year termwhen his existing term expired on May 15th. Subsequently, faced with thepossibility of an early general election, the coalition party leaders agreed to putforward as their candidate the chief justice of the Constitutional Court, AhmetNecdet Sezer, who was elected on the third ballot by a simple majority onMay 5th. Before long, however, it became clear that relations between the newpresident and the government would not be easy, as Mr Sezer refused to signgovernment decrees which would, among other things, have allowed it todismiss supposedly politically suspect civil servants, and pressed for thoroughinvestigations of corruption allegations, notably in the banking sector.

On February 19th, just three months after narrowly avoiding financial collapse,a row between Mr Ecevit and the president triggered a collapse of internationaland domestic confidence. This forced the government to abandon thecrawling-peg exchange-rate regime, which was followed by a sharp devaluationof the Turkish lira and the suspension of its disinflation strategy which hadenjoyed the backing of the IMF since the end of 1999. On March 2nd the

The government introducessome reforms

Turkey becomes an EUaccession candidate

Tensions between Mr Ecevitand Mr Sezer trigger a

financial crisis

10 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

government appointed Kemal Dervis, a respected economist at the WorldBank, as the new economy minister. He drew up a programme of financial andeconomic reforms which obtained substantial financial support from the IMFon May 15th, despite the fact that the government coalition’s commitment tothe programme was far from convincing. In the wake of the crisis publicsupport for the government evaporated, but Mr Ecevit resisted calls for hisresignation and vowed to stay in government.

Constitution and institutions

Turkey is a unitary republic, in which power is exercised by a unicameralparliament (Meclis) and the prime minister. The prime minister is designatedby the president and is customarily the leader of the biggest party. The Mecliselects the president, who can serve only one seven-year term. He can delay, butnot veto, legislation. The president is supposed to be a neutral figurehead andis obliged to resign from a political party before assuming office. In practice, hecan have substantial influence behind the scenes, particularly in periods ofgovernmental crisis. The constitution can be altered only by a two-thirdsmajority in the Meclis, with a subsequent referendum if this is ordered by thepresident, or a three-fifths majority plus a compulsory referendum.

Parliament currently has 550 members with a parliamentary term of five years,although early elections can be held if the Meclis votes to this effect. Theelectoral system is based on multi-seat constituencies, with the exclusion ofparties failing to overcome a threshold of 10% of the national vote. The 10%threshold does not apply to independent candidates. The system favours thelarger parties over the smaller ones, particularly if there is a large difference inthe share of the vote won by the first- and second-placed parties. Elections arenormally fairly conducted, but groups considered to endanger the unitarynature of the state (in effect, Kurdish nationalist parties) have been banned.Despite continuing official efforts to shut it down, the pro-Kurdish People’sDemocracy Party (Hadep) contested the 1995 and 1999 elections but failed toovercome the 10% threshold on both occasions, although it captured themayoralties in a number of important cities in the south-east in 1999.

According to the constitution, parties should not exploit religion for politicalpurposes, although they often flout this prohibition. In February 1998,however, Welfare was closed down by the Constitutional Court for violatingthis principle, and its successor, Virtue, is threatened with the same fate. Inprinciple, Turkey accepts the European Convention on Human Rights andother international human rights instruments, but in practice the right to freespeech can be severely restricted. The regular torture of suspects by the police isanother serious abuse, although it has been curtailed somewhat in recent years.In November 2000 the EU specified a wide-ranging series of reforms of thehuman rights regime—particularly as it affects freedom of expression, theending of torture and of capital punishment, and the Kurdish question—whichTurkey was required to enact as a precondition for the start of accessionnegotiations. In principle, the government is committed to reforms, although

Parliament

Turkey 11

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

opposition from the MHP, the second largest party in the coalition, as well asparts of the military and police, will make these hard to apply (see above).

The administrative system is highly centralised. The country is divided into 73provinces, each under a governor appointed by the central administration, anddistricts within these. Since the 1980s elected municipalities have been givenmore powers and resources, but these are still fairly limited. A specialemergency regime, under a regional governor, is applied in four Kurdish-inhabited provinces in the south-east. This gives the police and army specialand much criticised powers, which must be renewed by parliament at four-month intervals.

The independence of the judiciary is respected in Turkey, and rulings by theConstitutional Court can overturn acts of parliament, with the exception oflegislation passed during the last period of military rule (1980-83). Followingseveral rulings by the European Court of Human Rights, the assembly voted inJune 1999, in the midst of the trial of the PKK leader Abdullah Ocalan, tocivilianise the quasi-military state security courts in which liberal, pro-Kurdishand Islamist dissidents are tried. Further reforms to increase the efficiency andeffectiveness of the judicial system are also being called for by the EU.

Among the important ministries, the foreign ministry has traditionally enjoyeda respected and non-partisan position, but the economic ministries and theministries of the interior and education have frequently been weakened bypartisan appointments and interference, with widespread corruption of parts ofthe civil service frequently reported. The defence ministry has little real controlover the armed forces. These are effectively controlled by the chief of thegeneral staff, who theoretically reports to the prime minister but in practiceenjoys wide autonomy.

Political forces

The main political parties and movements may be divided into five blocs.

• The centre right: the Motherland Party (Anap) under Mesut Yilmaz, and the TruePath Party (DYP) led by Tansu Ciller.

• The centre left: Bulent Ecevit’s Democratic Left Party (DSP) and the RepublicanPeople’s Party (CHP), led by Deniz Baykal.

• Islamic conservatives: Virtue (Fazilet), under Recai Kutan.

• The ultra-nationalist right (with Islamic sympathies): the Nationalist Action Party(MHP) led by Devlet Bahceli.

• Pro-Kurdish political groupings: People’s Democracy Party (Hadep), led byMurat Bozlak.

The administrative system

The judiciary

The ministries

12 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

The centre right has traditionally attracted most support, but it is currentlyweakened by its division into two rival parties, Anap and the DYP. There islittle ideological difference between the two, which maintain their separateexistence mainly as a legacy of the personal rivalry between Suleyman Demireland Turgut Ozal. The latter’s death in 1993 should have removed this factor,but the current Anap leader, Mesut Yilmaz, and Tansu Ciller have been unableto co-operate. Despite poor performances by Anap and the DYP in the 1999elections and calls for their resignations, Mr Yilmaz and Mrs Ciller remained incharge of their respective parties.

Until the 1999 general election there were two main centre-left parties inparliament, the DSP and the CHP. The DSP, which is mainly a personal vehiclefor the charismatic Bulent Ecevit, became the largest party after the April 1999election. Mr Ecevit is a staunch nationalist who is probably best knowninternationally for ordering the invasion of the northern part of Cyprus in1974. He became caretaker prime minister in January 1999 and head of thecoalition government comprising the DSP, MHP and Anap formed in June ofthat year. Traditionally opposed to free-market reforms, the DSP has adopted afar more moderate stance on economic policy since 1997, but its publicsupport was badly eroded by the financial crash of February 2001. Meanwhile,the CHP failed to reach the 10% threshold for representation in parliament inthe April 1999 general election. Shortly afterwards the party leader, DenizBaykal, was forced to resign, to be succeeded by Altan Oymen. However,Mr Baykal succeeded in re-installing himself as leader in October 2000,provoking several resignations from the party’s senior ranks. Although the CHPis currently out of parliament, it may make a comeback as centre-left voterslose sympathy for the DSP.

After the February 1998 closure of Welfare and Necmettin Erbakan’s banningfrom politics for five years, the Islamists regrouped to form the Virtue Party(Fazilet). However, in the 1999 general election the party’s share of the votedropped to 15.4%, compared with Welfare’s 21.4% in 1995. At the partyconvention held in May 2000 a challenge Recai Mr Kutan’s leadership ofFazilet was mounted by the “modernist” faction within the party, led byAbdullah Gul and Tayyip Erdogan. Mr Kutan won the ballot by a fairly narrowmargin, but the modernists may renew their challenge in the near future,especially if the party is officially closed own by the Constitutional Court (as iscurrently threatened) and a successor party or parties are established. Althoughthe Islamists were a failure in national government, Virtue remains strong inmunicipal government in several cities, notably in Istanbul and Ankara, whereits relatively efficient and uncorrupted administration is appreciated.

The ultra-nationalist right is represented by the Nationalist Action Party(MHP), which under the leadership of Devlet Bahceli became the secondlargest party with 18% of the vote in the April 1999 general election. After alow-profile election campaign the MHP appears to have shifted towards thecentre in its successful bid to join the Ecevit government in May 1999,disavowing its previous rabidly anti-leftist stance. The MHP can be expected to

The centre right

The centre left

The Islamic conservatives

The ultra-nationalist right

Turkey 13

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

oppose reforms of human rights where these affect the Kurds, but hassupported the DSP and Anap on a wide-range of economic reforms.

Kurdish nationalism was previously represented in parliament by theDemocracy Party, originally a splinter group of the Social Democrat PopulistParty (SHP). This was closed down by court order in 1994 and was succeededby the People’s Democracy Party (Hadep). Hadep failed to overcome the 10%threshold in the 1995 and 1999 elections, but won an important role inmunicipal government in the south-east in 1999. Although the partydenounces the use of force, many of its grass-roots supporters are probablysympathetic to the illegal Kurdistan Workers’ Party (PKK). This is the mostmilitant of the Kurdish political groupings and waged a campaign of violenceand terrorism against the government between 1984 and 2000. It suffered amajor setback in February 1999, when its leader, Abdullah Ocalan, wascaptured in Nairobi, Kenya, by Turkish security agents. Recognising realities,the PKK has abandoned its previously Marxist discourse and claims that it hasended its armed campaign. However, its demand that it should now beaccepted as a legitimate negotiator for a peaceful settlement of the Kurdishproblem is unlikely to be accepted.

Among non-party actors, the army has played a crucial role in the recent past,staging three coups since 1960, the last time in 1980. It was instrumental inthe removal of the Welfare-led government in June 1997 and considers itselfthe guardian of the secular republic. The army wields power mainly throughthe half-military, half-civilian National Security Council (NSC), which issupposed to advise the government on security questions, but in practiceexercises considerable influence on a wider range of issues. The EU has calledfor a reduction of the NSC’s constitutional powers and an increase in thenumber of civilian members. Senior military commanders will probably resistthis, but since they officially support Turkey’s bid for eventual accession to theEU, they may be forced to make some concessions, at least on paper.

Main political figures

Bulent Ecevit: Leader of the Democratic Left Party (DSP) founded in 1983, hebecame prime minister for the fifth time in June 1999 at the head of a DSP-MHP-Anap coalition government. Respected for his honesty, Mr Ecevit is astaunch nationalist advocating a hard-line stance on issues such as Cyprus andthe Kurds, but his popularity has been badly dented by the financial crisiswhich erupted in February 2001. Moreover, he is now 76 years of age and inpoor health, so he may not be able to hold on to the party leadership andpremiership for much longer. If he is forced to leave the stage, then his partywill be seriously weakened, as it is very much his personal creation.

Devlet Bahceli: Leader of the Nationalist Action Party (MHP), he is deputyprime minister in the Ecevit government formed in June 1999. Mr Bahcelibecame leader of the MHP in 1997 following the death of the party’s fieryfounder, Alparslan Turkes, and gives the impression of an able but distinctlyuncharismatic figure. As far as national identity and the Kurdish question are

Kurdish politicalmovements

The army

14 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

concerned, his party adopts an uncompromising line, maintaining that there is“no Kurdish problem”—merely one of PKK terrorism.

Kemal Dervis: A vice-president of the World Bank for the Middle East andNorth Africa, Mr Dervis was appointed minister of the economy with wide-ranging powers in early March 2001. His presence in the cabinet should help torestore the credibility of the government’s economic policy after the collapse ofthe IMF-backed programme and the resignation of top bureaucrats, includingthe Central Bank governor, who played a leading role in relations with the IMFand the World Bank. But there is a risk that he may become isolated, aselements within the ruling coalition are not happy that their parties have lostresponsibility for key areas of economic management.

Mesut Yilmaz: Chairman of the Motherland Party (Anap) and a former primeminister, Mr Yilmaz served for many years in the reform cabinets of the lateTurgut Ozal but has little of the charisma, acumen or reformist zeal of hismentor. He replaced Necmettin Erbakan as prime minister in July 1997 but wasforced to resign in November 1998 amid unproven allegations of corruption.Despite his party’s poor performance in the April 1999 election, Mr Yilmazremains leader of Anap, a junior partner in the Ecevit government formed inJune 1999, and a deputy prime minister. His rivalry with and personalanimosity towards Tansu Ciller, the leader of the True Path Party (DYP), is seenas the main obstacle to a merger of the parties of the centre right.

Tansu Ciller: A former prime minister, she has managed to survive as leaderof the True Path Party (DYP) despite her party’ s poor performance in the April1999 election. She is now widely perceived to have been a disastrous economicand political manager, and her bad judgment and poor choice of lieutenantshelped to precipitate the economic crisis of 1994. Frequent but so far unprovenallegations of corruption have further dented her political image.

Ahmet Necdet Sezer: Mr Sezer was unexpectedly elected president in May2000. At the time of his election he was the chief justice of the ConstitutionalCourt, making him the first president of Turkey to have been neither aprominent politician nor a former senior military commander. He is 60 yearsold, widely respected and known as a liberal. He has acquired an unexpectedlyimportant political role through his challenges to high-handed actions by thegovernment and its failure to follow up serious charges of corruption. His mainweakness is that he does not have any direct experience of party politics orpersonal influence within the parliament, unlike both Suleyman Demirel andTurgut Ozal. Opinion polls suggest that he has far more public support thanany of the present government leaders, which has greatly enhanced hisinfluence in the political sphere.

Necmettin Erbakan: As the most prominent leader of the Islamist right,Mr Erbakan’s fate seems to be to form parties which get closed down by themilitary or the courts. He was a junior partner in three coalition governmentsduring the 1970s, but his previous National Salvation Party was closed downby the then military regime in 1981. Mr Erbakan then formed the WelfareParty (Refah), which emerged as the biggest party in the 1995 election,propelling him into the premiership in June 1996. Faced with the possibility of

Turkey 15

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

military intervention and rising public protests, he resigned in June 1997.While in power, the party showed a weak grasp of international politics and aninability to run a modern economy. Following the February 1998 decision bythe Constitutional Court to ban him from politics for five years and closedown Welfare, Mr Erbakan has managed to retain an impressive amount ofcontrol over Welfare’s successor, Virtue (Fazilet).

The press and numerous private television and radio stations can have animportant effect on public opinion. However, increasing monopolisation hasdampened press independence, and two media groups now control around70% of circulation. Parts of the media have also been hit by financial frauds,notably affecting the Sabah newspaper group, which also owns ATV television:Sabah’s owner, Dinc Bilgin, was arrested in April 2001. Pressure groups are alsoof growing importance. The main business organisations are the TurkishIndustrialists’ and Businessmen’s Association (TUSIAD) and the Union ofChambers of Commerce (TTOBB). The industrial workforce is fairly heavilyunionised, particularly in the state sector. There are two main trade unionconfederations: the Turkish Trade Union Confederation (Turk-Is), whichofficially adopts a centrist, non-partisan position, and the Reformist TradeUnion Confederation (DISK), on the political left. Other promotional pressuregroups have acquired an enhanced political role; these include the Fethullahcisand other religious brotherhoods, and groups modelled on movements inwestern countries, such as those promoting secularist values, women’s rightsand environmental protection.

International relations and defence

Turkey’s relations with many of its neighbours have been radically changed bythe end of the cold war and the Gulf crisis of 1990-91. Long-running disputeswith Greece and the Greek Cypriots have not been resolved, although sincemid-1999 Greece and Turkey have been moving towards agreement onbilateral issues. Talks between the Greek and Turkish Cypriot leaders wererestarted in 1999-2000 but stalled at the beginning of 2001. Since thedissolution of the Soviet Union Turkey has developed political, economic andcultural links with the Turkic countries of Azerbaijan, Kazakhstan, Uzbekistan,the Kyrgyz Republic and Turkmenistan. However, Turkey’s main political,economic and military ties are still with western Europe and the US.

Relations with Bulgaria, Georgia and the other Black Sea countries are generallyexcellent, and Turkey has taken the lead in forming a Black Sea Economic Co-operation (BSEC) region, which includes all the above as well as Greece,Albania, Azerbaijan, Russia and Armenia. Strong economic, trade and energylinks with Russia have tended to counterbalance underlying historic tensionsover competition for influence in the former Soviet republics and rivalrybetween the two countries over projected export oil pipelines from the Caspianbasin. In the absence of a resolution to the Azeri-Armenian conflict overNagorny Karabakh after the May 1994 ceasefire, Turkey has not normalisedrelations with Armenia and the Turco-Armenian land border remains closed.

The media and pressuregroups

Relations with Russia andother Black Sea neighbours

16 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

However, Turkey would probably seek to establish normal relations withArmenia if peace talks between the Armenian and Azeri presidents producedpositive results.

For many years relations with Syria were tense because of Syrian support forthe PKK and disputes over the Euphrates waters, following the construction ofthe Ataturk dam in Turkey. By expelling the PKK leader from Syria in October1998 the then Syrian president, Hafiz al-Assad, removed a major bone ofcontention between Ankara and Damascus. Although the Euphrates disputeremains unsettled, relations with Syria, mainly in the economic field, havemoved forward since the installation of Bashar al-Assad as president of Syria inJune 2000. The expanded relationship between Turkey and Israel hasexacerbated tensions with the Arab world, following the signature of a Turkish-Israeli military training and co-operation agreement, although this falls wellshort of a full military alliance between the two countries. However, Turkeybenefits from access to Israel’s advanced military technology and the supportof the pro-Israeli lobby in the US Congress. With the exception of a briefflirtation during the Islamist-led Erbakan government, Turkey tends to becautious in its relations with Iran, since it is suspicious of actual or potentialattempts by Iran to export Islamic radicalism.

Relations with Iraq are currently affected by partial UN sanctions against Iraq,but the Turkish government would like these to be lifted entirely and as soonas possible, since they have caused serious commercial loss to Turkey. Turkeystrongly opposes the formal establishment of an independent Kurdish state innorthern Iraq, but has established fairly close links with the two local Kurdishfactions, the Kurdistan Democratic Party (KDP) and the Patriotic Union ofKurdistan (PUK) in an effort to interdict PKK bases in the region.

The main point of tension in Turkey’s relations with its immediate neighboursis still the conflict with Greece over Cyprus and the Aegean. After years ofbitterness, relations between the two countries began to improve in 1999. Theatmosphere was significantly improved also by the generous Greek response tothe Turkish earthquake disaster, and Greece’s agreement to accept Turkey as acandidate for eventual EU membership at the European Council meeting inDecember of that year. The two governments have signed agreements on non-contentious issues, such as economic and cultural co-operation andenvironmental protection. Motivated by financial constraints in bothcountries, they have also begun to curb defence spending.

In the Aegean Sea, Turkey is opposed to the potential declaration by Greece ofa 12-mile limit for territorial waters, and disputes the Greek claim to offshoremineral rights over almost the whole of the Aegean. However, when acceptingEU candidacy in December 1999, Turkey also agreed to the possibility ofarbitration by the International Court at The Hague if bilateral discussions failto produce a positive result by 2004.

In parallel to the détente between the two mainland governments, the GreekCypriot president of the Republic of Cyprus, Glafcos Clerides, restarted“proximity talks” with Rauf Denktash, the leader of the breakaway Turkish

Syria, Israel, Iran and Iraq

Greece and Cyprus

Turkey 17

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Republic of Northern Cyprus, under UN auspices in December 1999. However,the two sides’ positions had moved no closer when Mr Denktash decided towithdraw from the talks at the beginning of 2001. Although both seemedprepared to accept a federal constitution in principle, Mr Denktash and Turkeyhave been pressing for a settlement based on a confederation of two states,with weaker powers for the central government. Mr Denktash insists that thesovereign equality of his self-declared Turkish Republic of Northern Cyprusmust be recognised if the talks are to resume.

Turkey has been a committed member of NATO for 50 years. It initiallyopposed the EU’s plans to establish a new European security structure outsideNATO but with access to NATO capability and assets, fearing that under theproposed structure it would have no say in how NATO assets and capabilitieswould be used, particularly in cases of vital security interest or geographicproximity, unless or until it acquired EU membership. Relations with the UShave generally been good, since the US values Turkey’s role as a strategicpartner. The administration of George W Bush continues to supportTurkey’s strategic role in the middle east, the Balkans and Transcaucasia.

In the Balkans, Turkey has shunned unilateral action but joined UN and NATOpeacekeeping missions. In the war over Kosovo in March-June 1999 Turkeygave its full support to NATO operations, providing jet fighters based at NATObases in Italy and offering the use of air bases in Turkey. It has also given strongsupport to the Macedonian government against attacks by Albanian militants.

Turkey has had an association agreement with the EU since December 1st 1964and entered into a customs union with the EU on January 1st 1996. However,in December 1997 at the Luxembourg meeting of the European Council the EUexcluded Turkey from the list of candidates for enlargement, despite the factthat its application to become a full member dated from April 14th 1987. As aresult, the Turkish government froze its relations with the EU until 1999. Therelationship then improved, following the installation of the Ecevitgovernment in Turkey and that of the Social Democrat-Green coalition underGerhard Schröder in Germany in 1998. This paved the way for Turkey’sinclusion as a candidate for EU membership at the Helsinki meeting of theEuropean Council in December 1999. But the EU has made clear that Turkeyhas a great deal to do in the areas of democratisation and human rights andprotection of minorities before accession negotiations can even begin (seeHistorical background).

The military is trying to move towards domestic production to avoid the threatof an arms embargo, such as that imposed by the US after the invasion ofCyprus which lasted until 1978. In 1998 Turkey announced a ten-year,US$31bn defence modernisation programme which was expected to includemain battle tanks, attack helicopters and assault rifles. A portion of the heavyweapons, such as the helicopters and tanks, will be produced or assembled inthe country under licence. Turkey already assembles its own advancedweapons, notably the F-16 aircraft, under an agreement with GeneralDynamics of the US. However, the financial crisis of February-March 2001 is

Western Europe and the US

Armed forces

18 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

expected to lead to delays or cancellations in the planned purchases ofhelicopters, tanks and some warships.

Armed forces, 2000

Active 609,700 Army 495,000 Navy 54,600 Air force 60,100

Reserves 378,700

Paramilitary (gendarmerie/national guard) 218,200

Total armed forces 1,206,600

Forces in Cyprus 36,000

Source: International Institute for Strategic Studies, The Military Balance, 2000/01.

Resources and infrastructure

Population

The State Planning Organisation (DPT) estimates that the average populationin 2000 was 65.3bn, the third largest in Europe after Russia and Germany. Thepopulation growth rate is estimated to have fallen to below 1.5% a year—highby European standards but low by the norms of the Middle East. Thedeceleration in the birth rate since the 1950s is related to an improvement inthe educational level of women, migration to urban areas and the wider use ofmodern birth-control practices. The DPT estimates the birth rate for 1998 at2.1% and the fertility rate at 2.35%. The declining birth rate has been partlyoffset by a declining mortality rate (about 0.65%). As of 2000, infant mortalityis estimated to have dropped to about 3.5%, while life expectancy is put at67 years for men and 71.6 for women. A census was held in 2000, but theresults have not yet been finalised.

Population, sex and age distribution, 1998 estimates(‘000)

Age group Total Males Females

0-19 26,149 13,359 12,790

20-39 21,290 10,859 10,426

40-64 12,780 6,362 6,416

65+ 3,232 1,474 1,759

Total 63,451 32,055 31,396

Source: UN, Demographic Yearbook.

Turkey’s population is still young, with 67.6% below the age of 35 in 1998,according to UN figures. This compares with 49% in France (based on 1993data) and 48% in Portugal (based on 1997 data). According to researchpublished by the Businessmen’s Association, TUSIAD, the number ofhouseholds—currently around 15m—is likely to reach 18.5m in 2010. There

Population growth hasbegun to slow

Cities are expandingthrough migration from

rural areas

Turkey 19

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

has been a high level of migration from rural areas to major cities andincreasingly other regional centres. In the largest cities, the inhabitants of theshanty towns account for half or more of the population. (However, some ofthe shanty town areas are rapidly being transformed into regular multi-storeyhousing areas benefiting from all urban services.) The 1997 census estimatesthat the urban population (comprising provincial and district centres)accounted for 65% of the total, compared with 59% in 1990 and 27% in 1960.The 1990s was the first decade in which the rural population of the republicdeclined in absolute terms.

One-quarter of the population is concentrated in the Marmara region in thenorth-west, including Istanbul. According to the census results, this is also thearea of most rapid population growth (28% between 1990 and 1997). Anotherquarter lives along or close to the western and southern coasts. The Black Searegion accounts for about one-eighth of the population, but it is the onlyregion where the population is declining. Inland areas east of the capital,Ankara, are sparsely populated. However, the south-east accounts for about10% of the total population, and population growth is strong.

There are large discrepancies in income distribution between regions, betweenurban and rural parts of the same region, and within the individual urbanareas. According to a survey by AC Nielsen Zet, carried out in 2000, some 9mTurks, or approximately 15% of the population, may be classified as “A” or “B”group consumers with a monthly expenditure of more than US$2,750. Ofthese, more than 2.8m fall into the “A” group with a spend of more thanUS$5,200 per month. The bulk of the population, almost 42m, fall into the“C” and “D” classes, which include semi-skilled and unskilled manual workers.An estimated 11m are classified in the poorest “E” group, with a monthlyspend of just US$266 per month.

The size of the workforce varies according to seasonal trends, particularly inagriculture. In 2000 the workforce averaged 22m. Unemployment averaged6.6%. Work for wages and salaries accounts for about half of all employment,with about a quarter of these jobs provided by the public sector. 30% of theworking population are employers or self-employed—a broad definition whichincludes, for example, street-hawkers, shopkeepers, taxi drivers andindependent professionals, farmers and owner-managers in industry andservices. The remaining 20% are unpaid family workers on farms and in otherfamily-sized enterprises. (See Reference table 2 for historical employment data.)By sector, services account for about 40% of employment, agriculture for about35% and industry including construction for 25%. Women make up just underhalf of the population but only about one-quarter of the workforce.Approximately 60% of working women are employed in agriculture.

Over 99% of the population is at least nominally Muslim. The Greek,Armenian and Jewish communities have steadily declined. Among theMuslims, the unorthodox Alevi minority is estimated at anywhere betweenone-tenth and one-quarter of the total. Massacres of Alevis have occurred, mostrecently in Kahramanmaras in 1978 and in Sivas in 1993. Kurds form themajority of the population in the south-east and parts of the east, where

The service sector hasbecome the largest

employer

The population is almostentirely Muslim

20 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Kurdish is commonly spoken and many villagers still cannot speak Turkish.People of wholly or partly Kurdish origin also make up a substantial minorityof the population of many major cities, where they are often indistinguishablefrom other people. Kurds also live in neighbouring regions of Iran, Iraq andSyria. Arabic-speakers, who live mainly along the southern frontier with Syria,account for 1.5-2% of the total population. There are believed to be severalhundred thousand illegal immigrants living in Istanbul and other Turkishcities, mainly from Romania and other poor former communist countries.

Education

The minimum period of schooling was raised from five to eight years in 1997,and there is a single curriculum for the 6-14 age group. All those successfullycompleting their primary education are entitled to go on to attend three yearsat secondary school. Most secondary schools have broad curriculums aimed atpreparing students for university. But there is also a range of specialist schools,including the religious Imam Hatip secondary schools which can only takepupils from the age of 14, rather than 11. This has reversed the rapidexpansion of the Imam Hatip schools, which are seen by the authorities astraining ground for religious radicals.

Entry to university for secondary-school graduates is by national examination.The Open University has had some success in catering for the large number ofsecondary-school graduates unable to obtain full-time university places. Thissituation has also encouraged the establishment of a large number of privateuniversities in the last couple of years. All levels of education, from the stilllimited pre-school level upwards, are available in both public and privatesectors. Public-sector education dominates and is in principle free with theexception of partial university fees. A World Bank study (Turkey: EconomicReforms, Living Standards and Social Welfare Study 2000) put consolidated budgetspending on education at 3.1% in 1998, well below the 4.8% average formiddle- and lower-middle-income countries, and comparable to the 3.3%average for low-income countries. Many of the most prestigious universitiesand secondary schools, public and private, use a foreign language, usuallyEnglish, as the medium of education.

Today’s young people are much better educated than the older population,most of whom completed five years of primary education at best. Literacy isover 80%, compared with 30% in 1950, and the gap between the genders hasbeen closing. In 1998/99 the enrolment rate was estimated by the StatePlanning Organisation at 92.8% for primary education, 57.7% for secondaryand 25.7% for tertiary education (including the Open University). There aresome 14m students in primary, secondary and tertiary education, and abouthalf a million teachers. The quality of education is uneven. It suffers from anemphasis on rote-learning and centralised multiple-choice examinations,outdated curriculums, a lack of practical facilities, a failure to encourageinitiative and free debate, poorly trained and poorly rewarded teachers, andlarge class sizes. In rural areas schools can be severely under-equipped, and insome cases they barely function.

Eight-year educationis compulsory

The public sector has thedominant role

The quality ofeducation varies

Turkey 21

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Health

Healthcare standards in Turkey are well below those of the developedcountries. Public expenditure on healthcare is under 3% of GDP, comparedwith 5-8% for developed countries. Total expenditure on healthcare isestimated at 3.5–4% of GDP. There is about one doctor for every 875 people,and one hospital bed for every 400. Apart from the overall shortage ofresources, the fact that about 35% of the population still lives in small andoften isolated rural settlements increases the difficulties of adequate provision.There is far more health provision in the western than in the eastern provincesof the country.

Access to health services is mainly via three social security organisations, whichalso provide pensions. 80-90% of the population have now been included inthe system, but resources are stretched. There are plans to separate health andpension provision as part of ongoing social security reform.

Just as the inadequacies of the state education system have encouraged themiddle classes to turn to private-sector education providers, so the bureaucracyand overcrowding associated with the public health system have encouragedthe growth of private health services. Private specialists are commonlyconsulted, particularly in the big cities, and many new private clinics andhospitals have opened in recent years. The development of private healthinsurance, however, has had teething problems.

Natural resources and the environment

At 779,452 sq km, the land area is about the same as that of France and the UKtogether. Approximately 275,000 sq km (35%) is agricultural land and much ofthe rest can be used as grazing. However, there is also a substantial area ofexposed highland, particularly in central and eastern Anatolia, much of whichis extremely cold in winter. Water resources are less plentiful than in westernEurope but much less scarce than in most of the Middle East. The Black Searegion is warm and wet. Other parts of the country enjoy considerablesunshine, with varying degrees of precipitation. This climatic variety allows awide range of crops to be grown.

Mineral resources include much lignite and some hard coal, iron ore, metalsand salts. Turkish boron minerals and chromium are significant forinternational trade. Only relatively small oil and natural gas reserves have beenfound and exploited, but several rivers have been or are being dammed forhydroelectricity generation as well as irrigation. Wind power also has potential.Long coastlines offer opportunities for shipping, fishing and, above all,tourism, which also benefits from warm summers, fine coastal scenery andhistorical remains (see Economic sectors).

The earthquake disasters of August and November 1999 served as a reminderthat large areas of Turkey are at risk from active fault lines. Both the 1999earthquakes occurred towards the western end of the country-wide NorthAnatolian fault. A major earthquake or series of quakes, centred further west

Health provision isunder-resourced

Land and climate favouragriculture and tourism

Earthquakes are frequent

22 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

under the Sea of Marmara, is considered likely within the next 10-15 years,potentially causing more damage in Istanbul. The south-west and south-eastare also particularly prone to earthquakes.

Transport and communications

Long distances, mountainous terrain and lack of resources have hindered road-building projects. The length of the state and provincial road network isaround 60,000 km and has increased little since the early 1990s. However, roadsurfaces have been improved, and some roads have been widened. The Ankara-Istanbul toll road (motorway) has almost been completed. This forms part ofthe E-5 link between Europe and the Middle East. The total vehicle stock(excluding motorcycles) rose from around 1.2m in 1980 to 2.4m in 1990 and6.2m in 2000. Traffic deaths and urban congestion are both major problems.Projects awaiting financing include a road crossing of the Gulf of Izmit, cuttingjourney times between Istanbul and the Aegean region, and morecontroversially a bridge across the Dardanelles. (See Reference table 3 forhistorical transport data.)

Most railway lines are single-track and circuitous, and rail travel is slow. All areowned by the loss-making state railways (TCDD). Only a few suburban linesare commercially successful, while services to the east have been run at a loss.All in all, the railways account for only 5% of land transport. Attempts are inhand to streamline the TCDD and to build branch lines to industrial zones.There are already rail links to some ports and state enterprises producing basicgoods. There have long been plans for an Istanbul-Ankara high-speed train or,more realistically, an upgrading of the existing line to cut the journey time.Rail is making a comeback as a form of urban transport. Several municipalitieshave built “metro” systems, and the Marmaray project, a line running east-west through Istanbul including a tunnel under the Bosporus, is due to be putout to tender in 2001.

Air transport, both domestic and international, is dominated by the state-controlled Turkish Airlines (THY). Its young fleet of some 75 aircraft carriesabout 10.5m passengers a year to over 100 Turkish and internationaldestinations. A majority stake in THY is slated for privatisation in 2001. Thenew international terminal at Istanbul’s main Ataturk Airport was completedin early 2000. The main tourist airport at Antalya has also been expanded.These projects were carried out on a build-operate-transfer basis. Most airportsare owned and run by the state.

Sea transport is important for domestic and international trade and travel, asthree of Turkey’s main industrial conurbations (Istanbul-Izmit, Izmir andAdana) are located on the coast. The establishment of private ports and thetrend towards private management of state-owned ports have gone some waytowards mitigating overcrowding and inefficiency in recent years. There areseveral ports concentrated in and around Istanbul. Mersin and Izmir are themain ports on the Mediterranean and Aegean coasts respectively. Many

Roads are the main meansof land transport

The railways havebeen neglected

Istanbul has a newair terminal

The ports are improving

Turkey 23

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

commuters in Istanbul use the mainly state-owned steamers and ferries. Thetonnage of the Turkish merchant marine has been stable at just over 10m dwtsince 1996. However, the share of Turkish-flag vessels in the transport ofexports and imports has slipped to under 30%. Shipping is dominated by theprivate sector.

The telecommunications network improved and expanded rapidly in the1980s and early 1990s. Digitalisation is almost complete, but pressure on theinfrastructure has continued to rise, augmented by the introduction of mobilephone and Internet services. The state-controlled Turk Telekom has about18.5m fixed-line subscribers and owns the national infrastructure. TurkTelekom also has significant satellite, Internet and cable TV assets and has beengranted a mobile operator licence. Attempts to part-privatise Turk Telekomfailed in 2000 and early 2001. However, new legislation passed in mid-May2001 envisages the sale of 99% of the company (the state will retain a 1%“golden share”), but the stake to be sold to a strategic foreign investor cannotexceed 45% of total capital. The ceiling on foreign ownership, the state’sgolden share and waning demand for telecoms shares worldwide will make itdifficult to privatise Turk Telekom in 2001. The company’s monopoly on fixed-line services is due to end in 2003, but this date may be brought forward tospeed up the liberalisation of the sector.

A framework law for the future free market in telecommunications was passedby parliament in January 2000, and a semi-autonomous watchdog, theTelecommunications Agency, has been set up. So far, the main private-sectorinvolvement in telecommunications services in Turkey has been in mobiletelephony. The established operators, Turkcell (Cukurova group-Sonera) andTelsim (Uzan group), were joined in early 2001 by Is-Tim (Aria), jointly ownedby Turkiye Is Bankasi and Telecom Italia. Is-Tim bid an unexpectedly high priceof US$2.35bn for its licence in an April 2000 auction. Turk Telekom’s service(Aycell) is also expected to start up in 2001. There are about 15m mobilesubscribers. Third-generation licences have yet to be issued.

The Post Office (PTT) continues to dominate traditional mail and parcelservices. There are a large number of Internet service providers operating inconjunction with Turk Telekom. Most of the leading Internet service providersand portals are associated with established banking and/or media groups,notably Cukurova (Superonline), Dogan (E-kolay) and Dogus (Ixir). There werean estimated 1.5m-2m Internet subscribers at the end of 2000.

There are a plethora of newspapers, television and radio channels. The bestknown are owned by large media groups which aim at a wide audience. Thesmaller ones tend to have a clear local and/or cultural-ideological bias. Theleading newspapers are Hurriyet (Dogan) and Sabah (Bilgin group), selling about500,000 each, but there are numerous alternatives. Top TV channels includeKanal D and CNN Turk (Dogan), ATV (Bilgin), Star (Uzan), Show TV(Cukurova), NTV and CNBCE (Dogus) and TGRT (Ihlas). The state-owned TRT,which held a monopoly of broadcasting until the 1980s, continues to runseveral TV and radio channels. Broadcasting is supervised by an independent

The sale of Turk Telekomis still awaited

Mobile telephone servicesare booming

The Internet iscoming of age

Newspapers and TV are stillthe key media

24 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

agency, RTUK, which is best known for ordering television channels to closedown for a day or more as punishment for showing offensive programmes.RTUK was due to settle chaotic frequency allocations in the first half of 2001.There are a handful of pay-TV services, including the new digital channels,Digiturk and Star-Digital, set up by the Cukurova and Uzan groups.

Energy

With very limited domestic production, Turkey is a major importer of oil and,increasingly, of natural gas. Both oil and gas are used by industry and forresidential heating, alongside coal, which is mainly produced locally. Ligniteaccounts for the vast majority of coal production. Reserves are put at 8.3bntonnes but may well be much higher. The state-owned TKI is the mainproducer. Hard coal is mainly found on the declining Zonguldak field on theBlack Sea coast. Reserves are put at 1.3bn, but production—controlled by thestate-owned TTK—has fallen to 2-2.5m tonnes/year. Hard coal is also imported.

The Baku-Ceyhan oil pipeline project

Turkey has ambitious plans for a 1,730-km pipeline to take 1m barrels a day of oil fromAzerbaijan to the Ceyhan export terminal on Turkey’s Mediterranean coast. A series ofagreements were signed in September and October 2000 involving the Azerbaijani,Georgian and Turkish governments and AIOC, the BP-led consortium set up to produceAzerbaijani oil. The hope is to begin construction work in 2002 and complete it in 2004,at a cost of at least US$2.4bn. But uncertainty prevails regarding throughputcommitments and financing. The discovery of gas, rather than oil, in Azerbaijan’s ShahDeniz field has also complicated the issue. On the one hand, it has raised the possibilityof an oil pipeline being built in parallel with the construction of an Azerbaijan-Turkey gaspipeline. But on the other hand it may mean that the Baku-Ceyhan project is short ofthe critical volume of oil needed to convince the oil companies of its feasibility.

Much hangs on whether producers in Kazakhstan can be persuaded to export some oftheir crude via this route with the help of a connecting pipeline. Ironically, oil from theTengiz field in Kazakhstan is now being exported to world markets via the Russian BlackSea port of Novorossisk using a separate line completed in March 2000. This givesRussia control of Caspian oil export routes and poses human and environmental risksresulting from the large number of oil tankers sailing through the Bosporus, both ofwhich supporters of the Baku-Ceyhan pipeline claim they want to avoid. Also, backed bythe US the Baku-Ceyhan pipeline would add to Turkey’s strategic importance andgenerate employment and transit fees. Basic engineering work is under way on the1,037-km stretch of the route crossing Turkish territory, and detailed engineering work isto start in mid-2001.

Since natural gas was first imported from Russia in the 1990s, Turkey hasturned rapidly to gas as a clean fuel for residential use and power generation.The Ministry of Energy and Natural Resources expects demand to rise fromabout 15bn cu metres in 2000 to 55bn cu metres in 2010. The current pipelinefrom Russia via Ukraine and Bulgaria is being upgraded, and a second pipelinefor Russian gas, known as the Blue Stream project, is to be built under the Black

Aside from coal, Turkeydepends on imports

Gas supplies hinge onpipeline projects

Turkey 25

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Sea, with the first deliveries due in early 2002. Meanwhile, the necessarypipelines are largely in place for Iran to start supplying Turkey with gas in July2001. An inter-governmental agreement signed with Azerbaijan in March 2001envisages the construction of a pipeline to bring Azerbaijani gas to Turkey viaGeorgia, with a start-up date of 2004. US-backed plans for a sub-Caspian linereaching Turkey from Turkmenistan via Kazakhstan, Azerbaijan and Georgiaare currently stalled.

There are also projects to pipe gas from Iraq and Egypt and to increase lignite-receiving capacity. At the same time, Turkey is co-operating with Greece on theEU-sponsored INOGATE project, whereby the two countries may become atransit country for the transport of natural gas (and possibly oil) from theCaspian region to Europe. Domestically, gas is transported by the state company,BOTAS, which has a monopoly on imports. Households and small businesses insome cities are supplied by municipally owned companies. Legislation toliberalise the gas market in line with EU norms is on the agenda for 2001.

Energy balance, 2000(m tonnes oil equivalent)

Oil Gas Coal Electricitya Other Total

Primary supplyProduction 3.0 0.6 18.5 7.6 7.0 36.7Imports 29.5 11.9 5.5 0.8 0.8 47.7Exports –1.0 0.0 0.0 –0.1 0.0 –1.1Stock change 0.0 0.0 0.0 0.0 0.0 0.0Total 31.5 12.5 24.0 8.3 7.0 83.3

Processing & transformationInput to refining –22.0 0.0 0.0 0.0 0.0 –22.0Input to transformation –2.4 –6.9 –11.8 –8.3 -–0.1 –29.5Refining/transformation output 22.0 0.4 0.0 11.2 0.0 33.6Energy industry fuel/loss –2.1 –0.1 –0.4 –2.8 0.0 –5.4

Final consumptionTransport fuels 11.8 0.0 0.0 0.0 0.0 11.8Industrial fuels 4.4 2.1 9.6 4.3 0.0 20.4Residential etc 6.3 3.1 2.2 4.1 6.9 22.6Non-energy uses 4.5 0.7 0.0 0.0 0.0 5.2Total 27.0 5.7 11.8 8.4 6.9 60.0

a Primary electricity output and imports/exports of electricity are expressed as input equivalents, on an assumed generating efficiency of 38.5%.

Source: Energy Data Associates.

Electricity production has more than doubled in the last decade, reachingabout 125bn kwh in 2000. At the end of 1999 total installed electricity-generating capacity was 26bn kwh, of which thermal plants accounted for59.3%. These plants are mainly fuelled by lignite, although gas and oil are alsoused. The remainder of Turkey’s electricity comes from hydroelectric plants,principally the Ataturk and Karakaya dams on the Euphrates. However, waterlevels have run low in 1999-2000, and hydroelectric plants cannot be run atfull capacity. Small amounts of electricity have been imported in recent yearsfrom Bulgaria, Iran and Georgia. Decades-old plans for a nuclear plant atAkkuyu on the Mediterranean coast have been shelved. (See Reference table 4for historical energy data.)

Electricity supply isstruggling to keep up with

demand

26 Turkey

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Electricity Market Act

The Electricity Market Act, approved by Parliament in February 2001, introduces radicalchanges in the way electricity is produced, traded and distributed to bring Turkey’slegislation into line with that already existing in the EU. The private sector will be free toproduce electricity and sell it to trading companies, large users and distributors undercontracts freely negotiated by the parties. The state will privatise its generation anddistribution assets and make the transmission network available to all comers.

With a few exceptions—mainly projects already under way—the Act puts an end toschemes such as build-operate-transfer projects that rely on state guarantees for thepurchase or supply of power, the supply of fuel, and/or the repayment of loans. Underthe new system private companies will have to take full market risks as in any otherindustry. While this ensures competition and reduces the scope for sleaze, it may alsomake investment—whether through privatisation or greenfield plants—unattractive,particularly in the early years, when newcomers will have to compete mainly against thestate and privileged producers.

The state generation and transmission company, TEAS, is being divided into threecompanies: TEUAS, to manage the generation capacity that remains in state hands;TEIAS, to handle transmission, and TETTAS, to buy electricity wholesale from producersand sell it wholesale to distributors, until such time as this function is taken over entirelyby a free market.