Embed Size (px)

Citation preview

Tuesday 25th September 2012

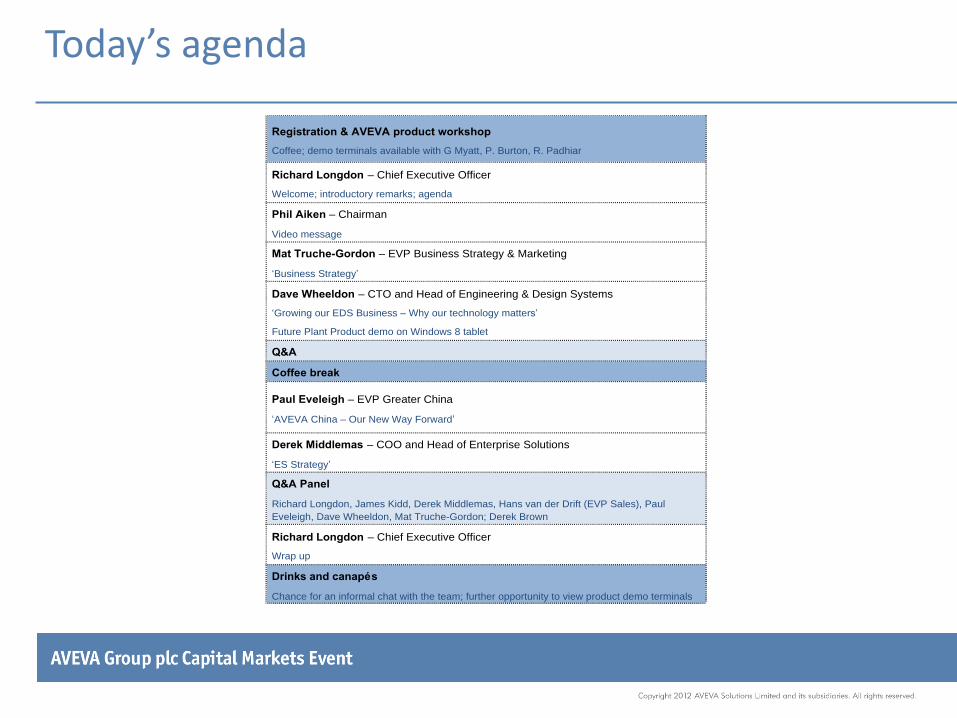

Today’s agenda

14:00 Registration & AVEVA product workshop

Coffee; demo terminals available with G Myatt, P. Burton, R. Padhiar

Richard Longdon – Chief Executive Officer

Welcome; introductory remarks; agenda

Phil Aiken – Chairman

Video message

Mat Truche-Gordon – EVP Business Strategy & Marketing

‘Business Strategy’

Dave Wheeldon – CTO and Head of Engineering & Design Systems

‘Growing our EDS Business – Why our technology matters’

Future Plant Product demo on Windows 8 tablet

Q&A

Coffee break

Paul Eveleigh – EVP Greater China

‘AVEVA China – Our New Way Forward’

Derek Middlemas – COO and Head of Enterprise Solutions

‘ES Strategy’

Q&A Panel

Richard Longdon, James Kidd, Derek Middlemas, Hans van der Drift (EVP Sales), Paul

Eveleigh, Dave Wheeldon, Mat Truche-Gordon; Derek Brown

Richard Longdon – Chief Executive Officer

Wrap up

17:00 Drinks and canapés

Chance for an informal chat with the team; further opportunity to view product demo terminals

Business Strategy

Mat Truche-Gordon

EVP Business Strategy & Marketing

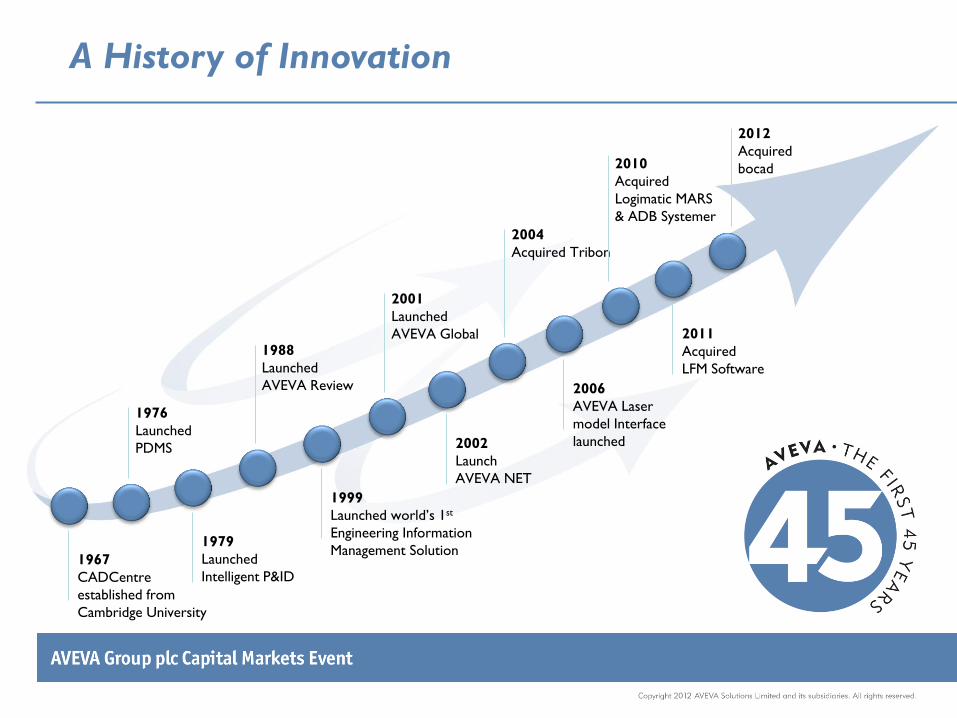

1976

Launched

PDMS

1967

CADCentre

established from

Cambridge University

1979

Launched

Intelligent P&ID

1999

Launched world’s 1st

Engineering Information

Management Solution

2002

Launch

AVEVA NET

2011

Acquired

LFM Software

1988

Launched

AVEVA Review

2001

Launched

AVEVA Global

2004

Acquired Tribon

2006

AVEVA Laser

model Interface

launched

2010

Acquired

Logimatic MARS

& ADB Systemer

2012

Acquired

bocad

A History of Innovation

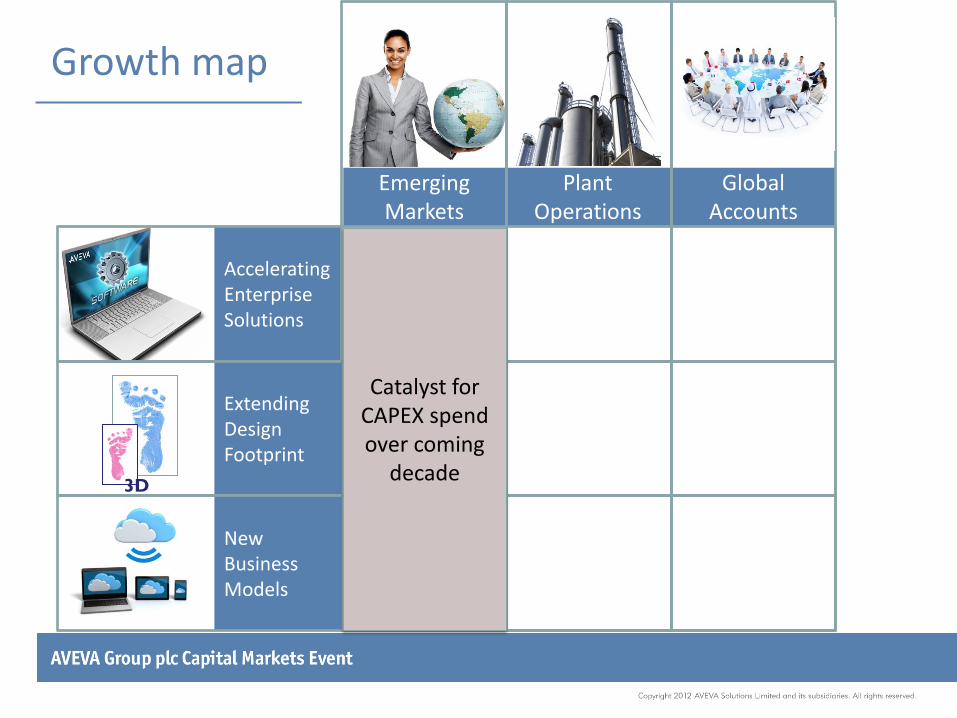

So what about the future?

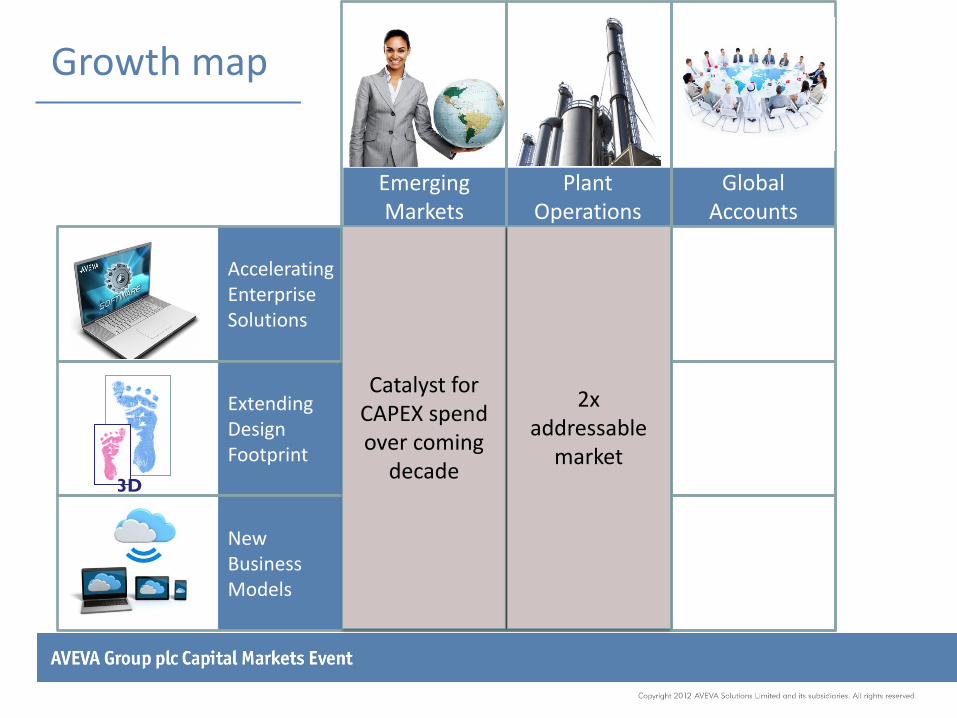

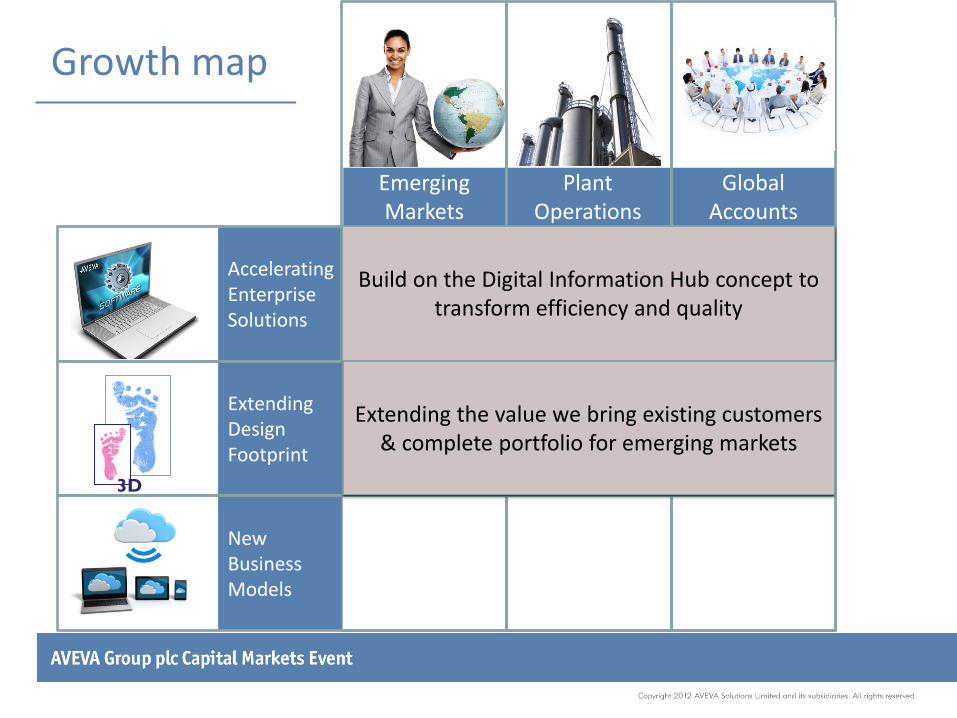

Emerging Markets

Plant Operations

Global Accounts

Accelerating Enterprise Solutions

3D

Extending Design Footprint

New Business Models

Growth map

Catalyst for CAPEX spend over coming

decade

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014 2015

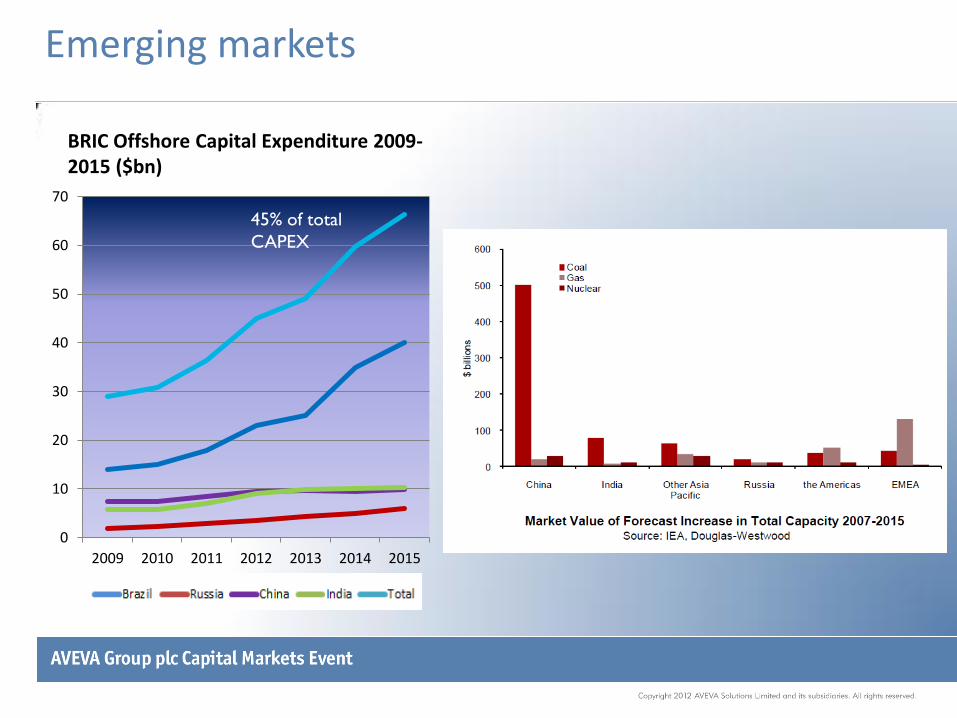

BRIC Offshore Capital Expenditure 2009-2015 ($bn)

45% of total

CAPEX

Emerging markets

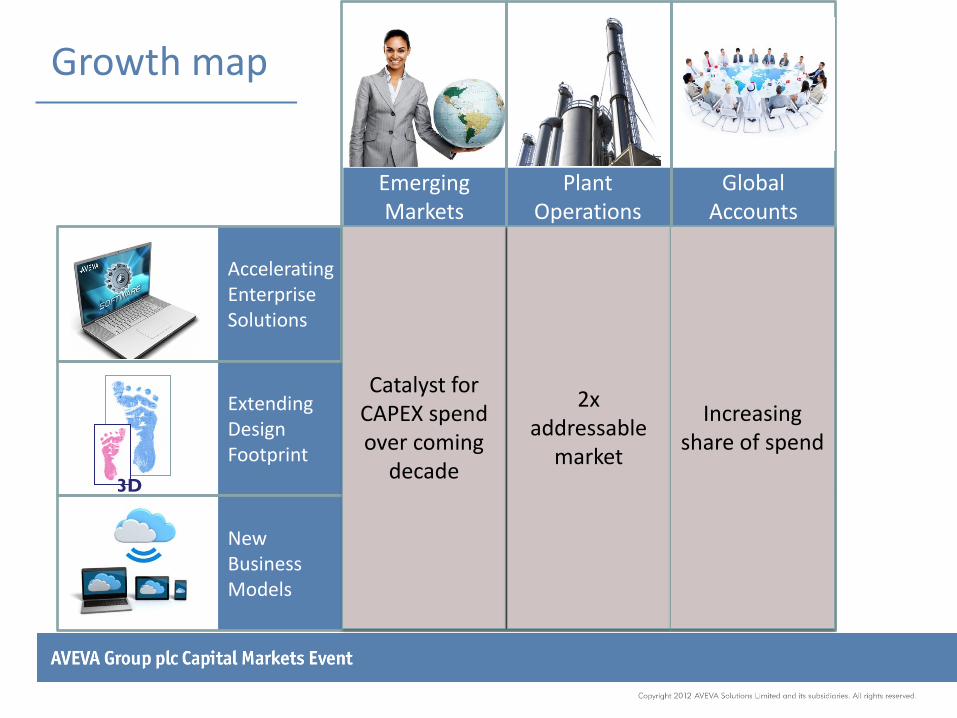

Emerging Markets

Plant Operations

Global Accounts

Accelerating Enterprise Solutions

3D

Extending Design Footprint

New Business Models

Growth map

Catalyst for CAPEX spend over coming

decade

2x addressable

market

Plant operations

Emerging Markets

Plant Operations

Global Accounts

Accelerating Enterprise Solutions

3D

Extending Design Footprint

New Business Models

Growth map

Catalyst for CAPEX spend over coming

decade

2x addressable

market

Increasing share of spend

• Acting locally, co-coordinating globally

• Building stronger relationships

• Barometer for key industry trends

• Partner of choice for global project execution

• Helping our customers standardisation efforts

Future strength in global accounts

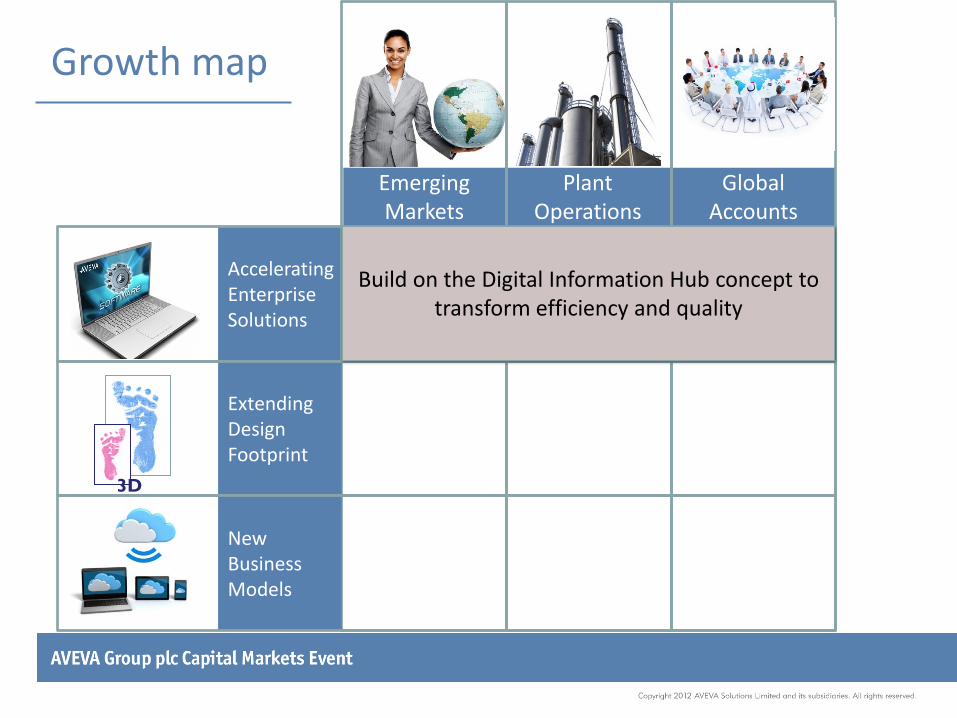

Emerging Markets

Plant Operations

Global Accounts

Accelerating Enterprise Solutions

3D

Extending Design Footprint

New Business Models

Growth map

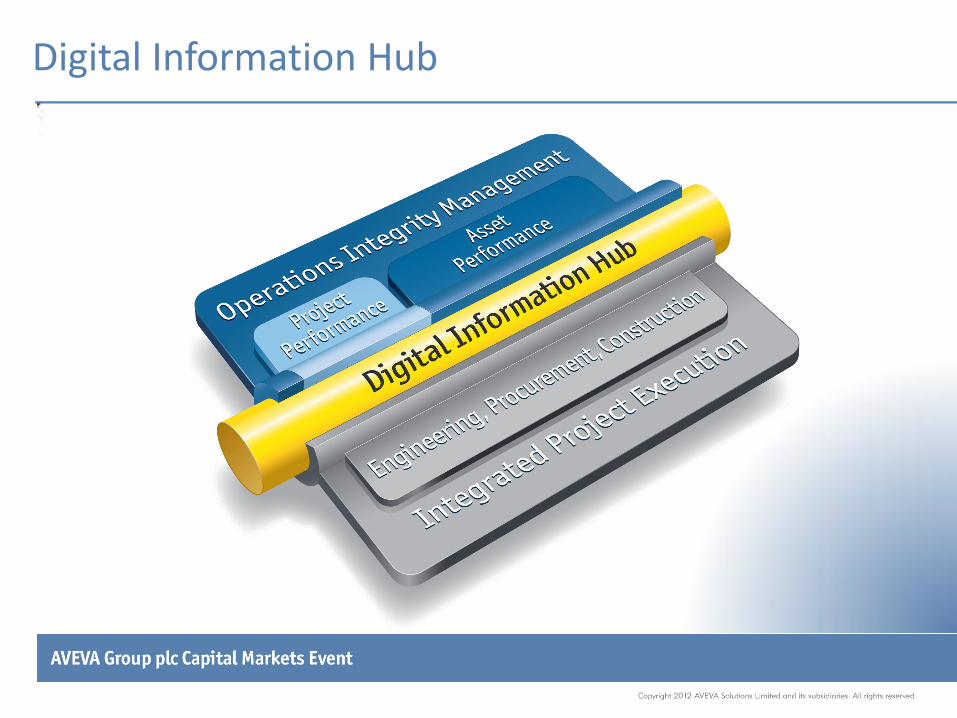

Build on the Digital Information Hub concept to transform efficiency and quality

Digital Information Hub

Emerging Markets

Plant Operations

Global Accounts

Accelerating Enterprise Solutions

3D

Extending Design Footprint

New Business Models

Growth map

Build on the Digital Information Hub concept to transform efficiency and quality

Extending the value we bring existing customers & complete portfolio for emerging markets

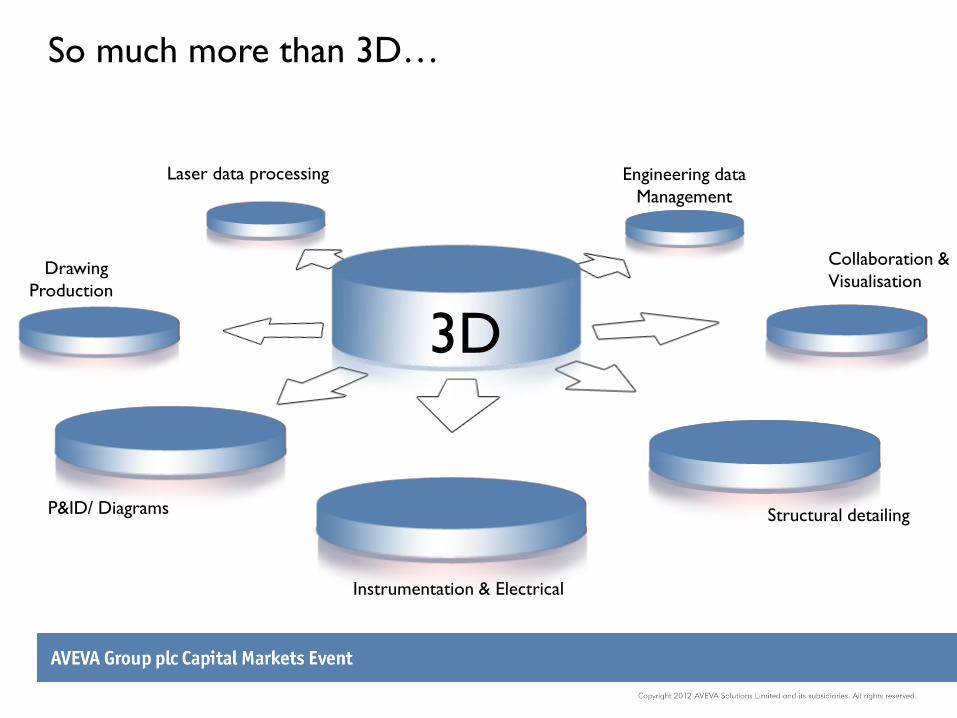

Laser data processing

Drawing

Production

P&ID/ Diagrams

Instrumentation & Electrical

Structural detailing

Collaboration &

Visualisation

Engineering data

Management

3D

So much more than 3D…

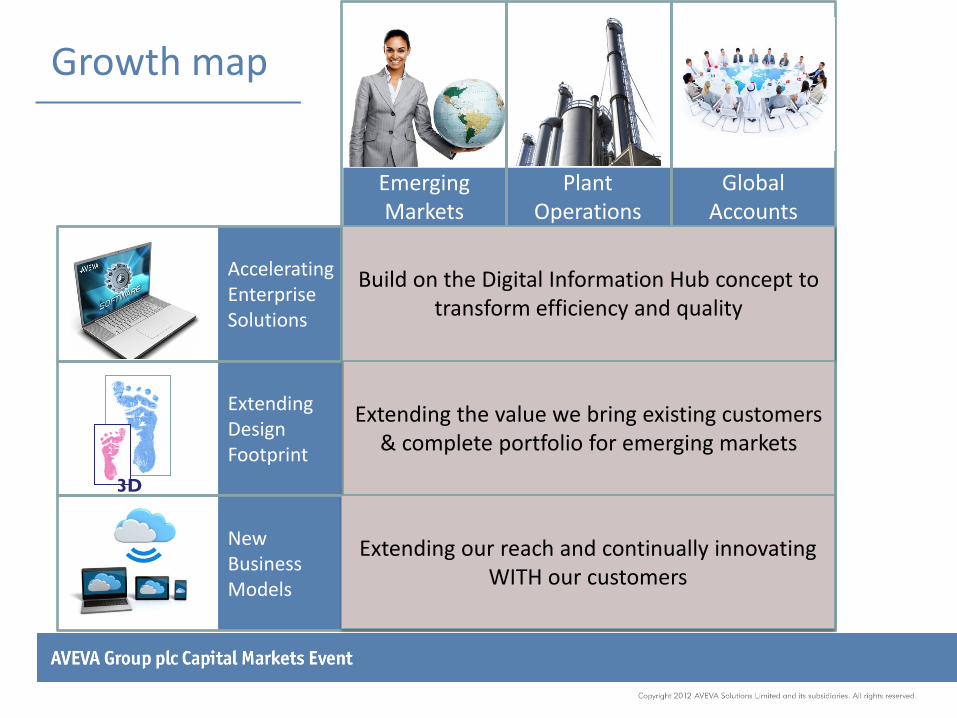

Emerging Markets

Plant Operations

Global Accounts

Accelerating Enterprise Solutions

3D

Extending Design Footprint

New Business Models

Growth map

Build on the Digital Information Hub concept to transform efficiency and quality

Extending the value we bring existing customers & complete portfolio for emerging markets

Extending our reach and continually innovating WITH our customers

New Business Models

New Products

Growing our EDS Business - Why our technology matters

Dave Wheeldon

CTO & Head of EDS

Original vision of AVEVA PDMS

Error-free design

Integrated Engineering & Design

Extending the vision

Plant Design for LEAN Construction

Challenges

No physical prototype to prove the assembly

Challenges

Engineering and design is still evolving after fabrication and construction

has started

Challenges

Construction remote from fabrication and design

Challenges

Construction work with “snap-shots” of information not the whole evolving

picture

Challenges

Feed-back from construction to design is forced by crisis not routine

Opportunity

Mobile & Cloud technologies enabling the construction teams to see the whole

picture and contribute as equal stakeholders

Opportunity

Availability of low-cost of laser-scanning allows the still-evolving design to be adapted to what has already been

fabricated and constructed

Plant design for LEAN construction

Extending our mission - to create the most comprehensive and efficient 3D plant modelling system for designing and constructing new plant and for making modifications

“Future of Plant Design”

• No.1 for Rapid Project Start Up

• No.1 for Design Efficiency

• No.1 for Compliance

• No.1 for Removing Rework in Construction New 3D product architecture combining advances in Laser

Scanning, Mobile and Cloud technology with AVEVA’s proven object data modelling and management capabilities

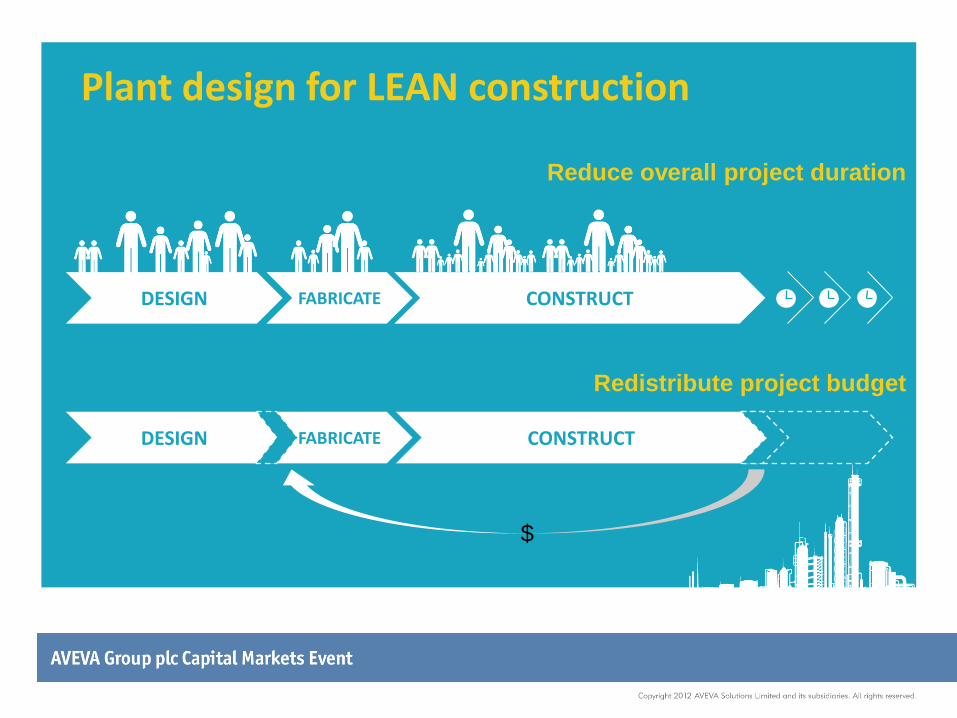

Plant design for LEAN construction

FABRICATE DESIGN CONSTRUCT

DESIGN FABRICATE CONSTRUCT

Reduce overall project duration

Redistribute project budget

$

How are we developing

“The Future of Plant Design” ?

Always the leading innovator and our customers’ most trusted partner

Continual Progression

Mutually Supportive Aligned System Elements

Lean

Product

Development

Process

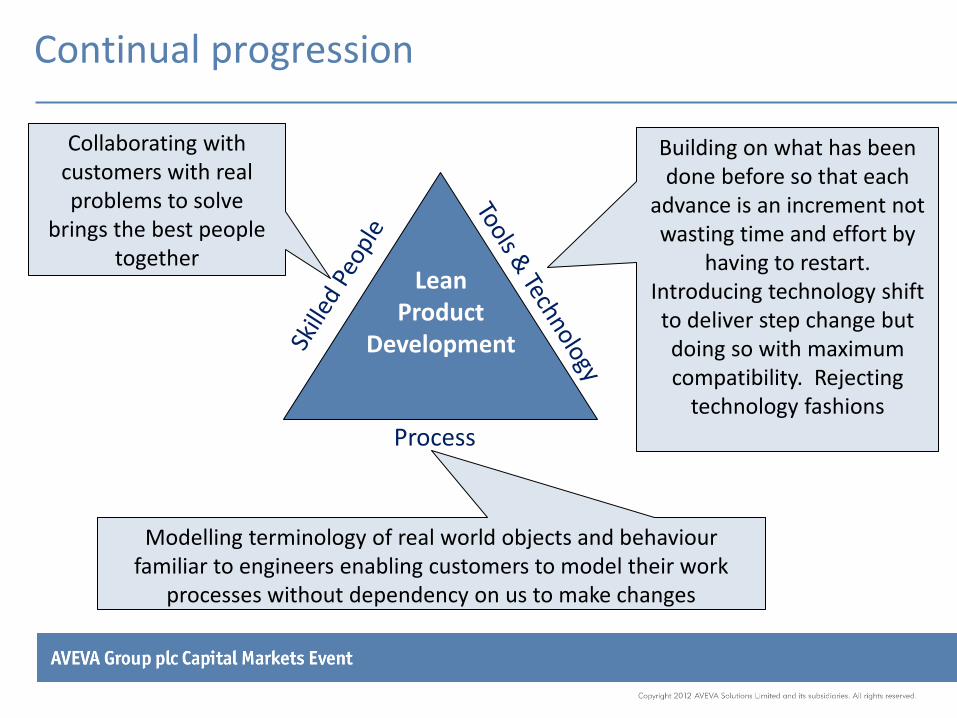

Continual progression

Collaborating with customers with real problems to solve

brings the best people together

Building on what has been done before so that each

advance is an increment not wasting time and effort by

having to restart. Introducing technology shift to deliver step change but doing so with maximum compatibility. Rejecting

technology fashions

Modelling terminology of real world objects and behaviour familiar to engineers enabling customers to model their work

processes without dependency on us to make changes

Lean Product

Development

Process

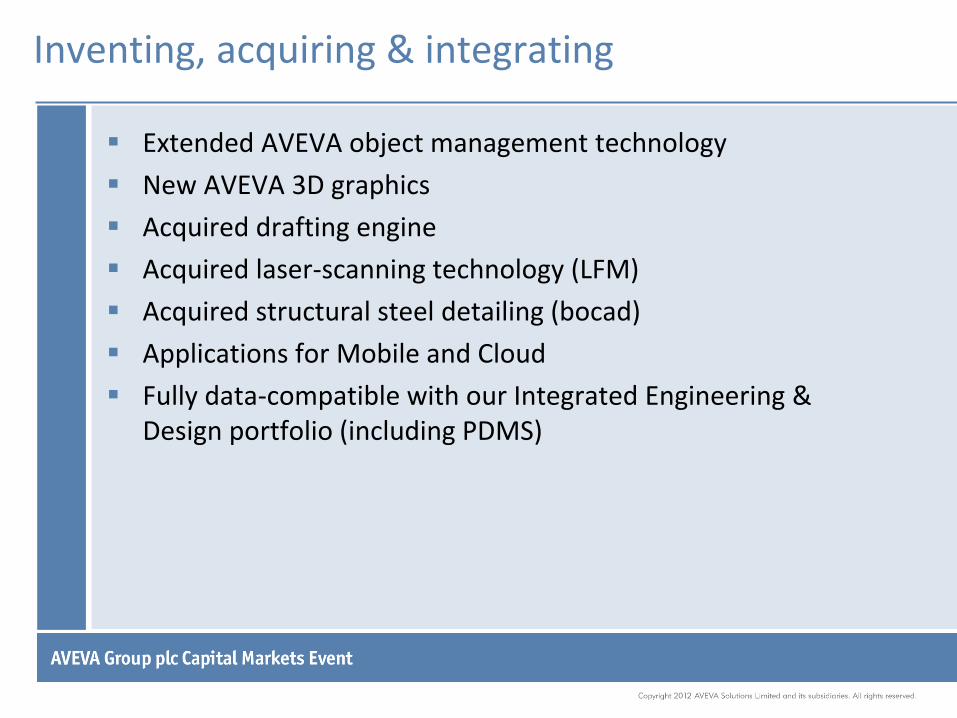

Inventing, acquiring & integrating

Extended AVEVA object management technology

New AVEVA 3D graphics

Acquired drafting engine

Acquired laser-scanning technology (LFM)

Acquired structural steel detailing (bocad)

Applications for Mobile and Cloud

Fully data-compatible with our Integrated Engineering & Design portfolio (including PDMS)

Mobile / CLOUD demo

Fresh from the lab ...

AVEVA Greater China Our New Way Forward

Paul Eveleigh EVP, Head of Greater China

Paul Eveleigh – EVP Greater China

British-Canadian

– University major: Finance

– 11 Years in Securities Trading & Portfolio Management

– Fluent in Chinese

2004 – founded Honiton Energy

– 1st producing WOFE

– 2nd Largest land area

Raised over $300m in Equity and Debt financing

2011 – joined AVEVA

Why did we change China organisation?

Why did we re-organise a well established Chinese Business?

Inefficient , legacy set-up run from Hong Kong

AVEVA needed greater control, integration and direction for the China operation

How was the reorganisation achieved?

After a 6 month assessment - complete management makeover

Headcount increased from 60+ to almost 100 in less than 2 years

WOFE created for direct selling (no withholding tax)

Increased agility in the region for delivery and face

Sales redefined to industry rather than geography

– Now focusing on higher-up decision-making in SOE Groups

– Recognising growth potential of ES - change staff skill-sets

Unusual characteristics of China market

State Owned Entities – 95% of our market – Pinpointing the right part of the food chain

– Desire for big deals (vs our previous focus)

– Need to make the right decisions (or career threat)

– Budget cycle

– The usefulness & annoyance of contract

– They will always pay

Why MOUs? – Intent

– Building walls & respect

Why be the most Chinese British company? – Prestige but respect

– Speed & ease to deal with

危机

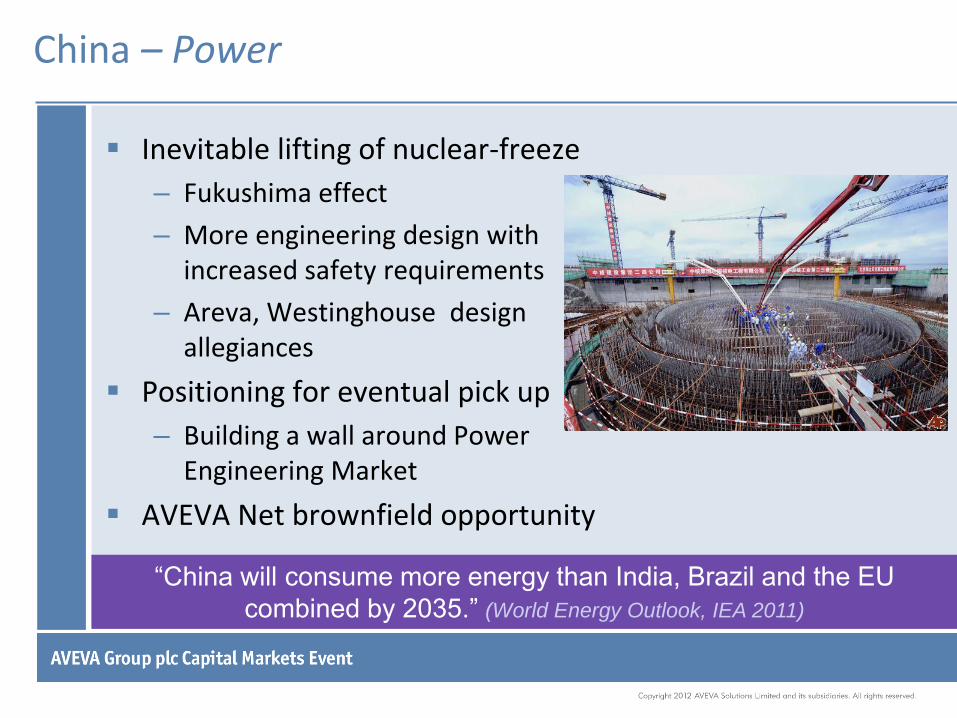

China – Power

Inevitable lifting of nuclear-freeze

– Fukushima effect

– More engineering design with increased safety requirements

– Areva, Westinghouse design allegiances

Positioning for eventual pick up

– Building a wall around Power Engineering Market

AVEVA Net brownfield opportunity

“China will consume more energy than India, Brazil and the EU

combined by 2035.” (World Energy Outlook, IEA 2011)

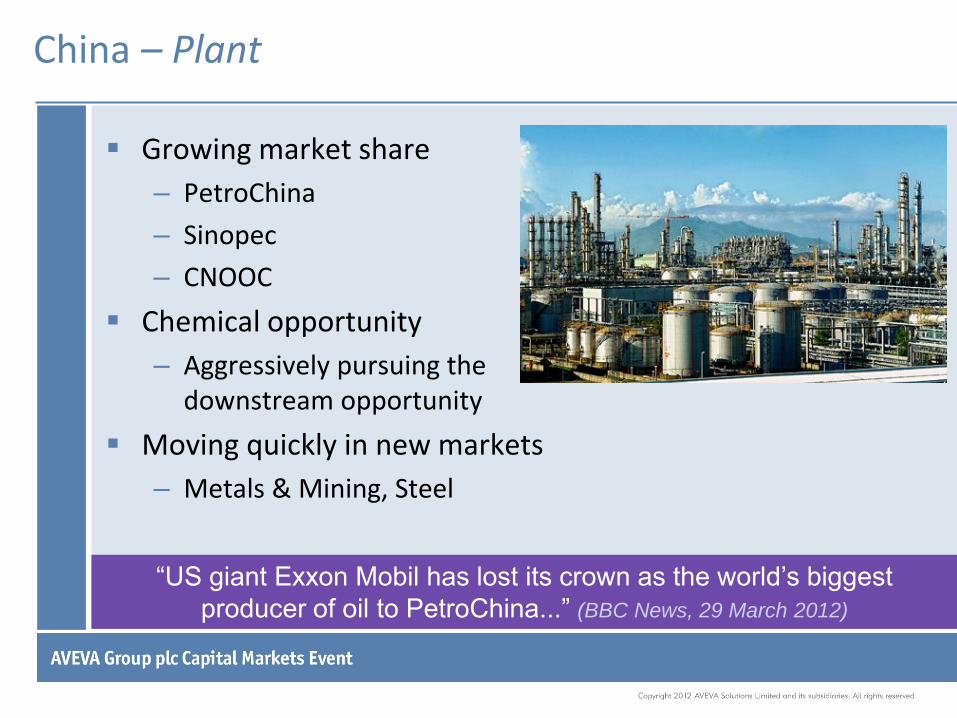

China – Plant

Growing market share

– PetroChina

– Sinopec

– CNOOC

Chemical opportunity

– Aggressively pursuing the downstream opportunity

Moving quickly in new markets

– Metals & Mining, Steel

“US giant Exxon Mobil has lost its crown as the world’s biggest

producer of oil to PetroChina...” (BBC News, 29 March 2012)

China - Marine

Second year of downturn

– Outlook still bleak

New management

– Focus on customer service

Opportunities lie in Navy and Offshore

Not anticipating a near term pick up

Market share still strong

– Opportunity to ‘build walls’

“A recovery is unlikely to happen within the next three years...” (China

Shipbuilding Industry Corp., quoted in China Daily 14 Sep 2012)

SEDIN – customer example

SEDIN Engineering co., Ltd, – China’s 2nd largest Chemical Engineering Institute

– Focused on technological efficiency since 1988

– Offered a trial use of AVEVA products

– SEDIN purchased one PDMS license in the same year, and used it only in one project

The final outcome: SEDIN is now 100% AVEVA

– Further cooperation between SEDIN and AVEVA ensued, including further products like VPRM and Diagrams

– SEDIN signed a strategic cooperation agreement with AVEVA in March 2012

– Will use AVEVA solutions in all projects, including an AVEVA NET engineering information solution

Summary

AVEVA now has a truly local presence on mainland China

The end market outlook,…

– Strengthening AVEVA’s competitive position in Power

– Also growing market share in Oil & Gas, Chemical

– Significant opportunities in other industries

– Expect Marine to remain subdued over medium term

Management action to reshape the business

– Executed rapidly, back on track operationally

China is clearly a top priority for AVEVA

Enterprise Solutions Strategy

Derek Middlemas COO and Head of Enterprise Solutions

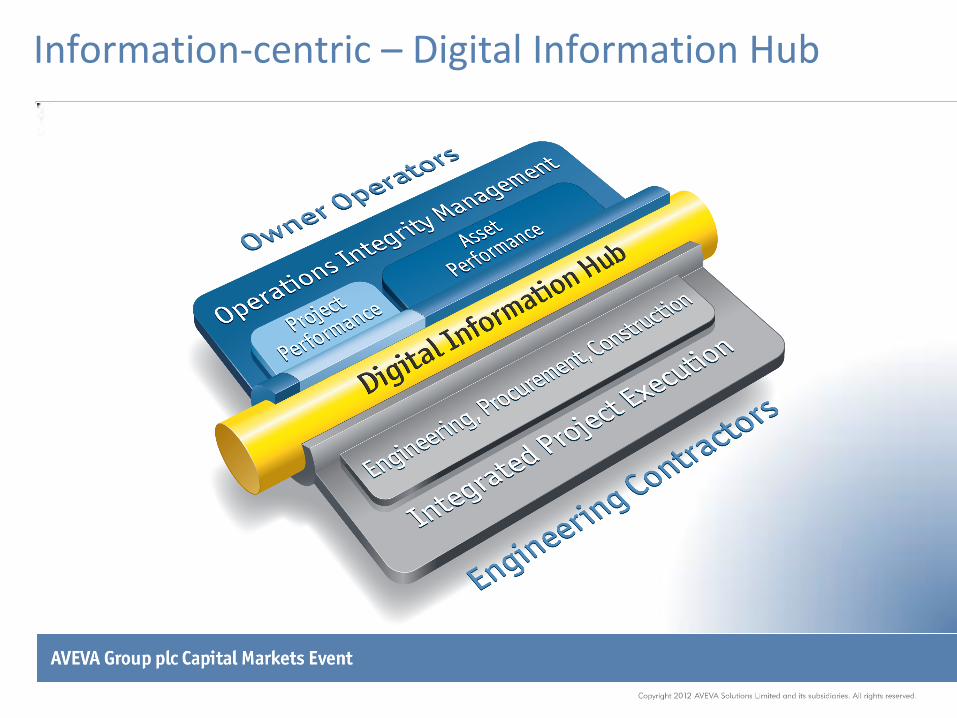

Digital Information Hub

Information engineering

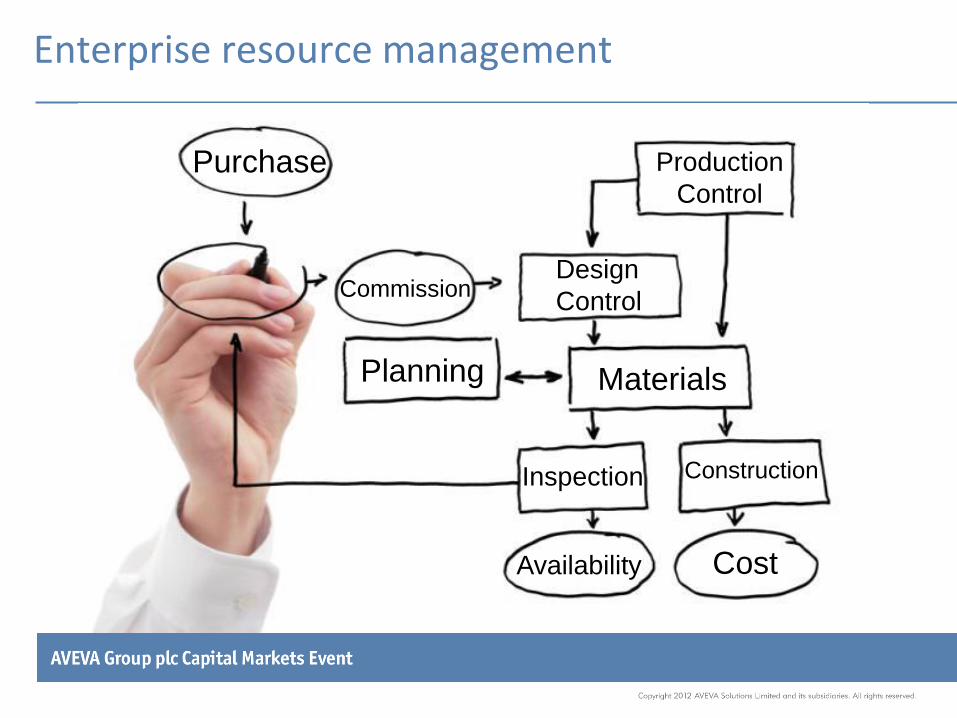

Enterprise resource management

Construction

Materials

Production

Control

Design

Control

Cost

Planning

Purchase

Inspection

Availability

Commission

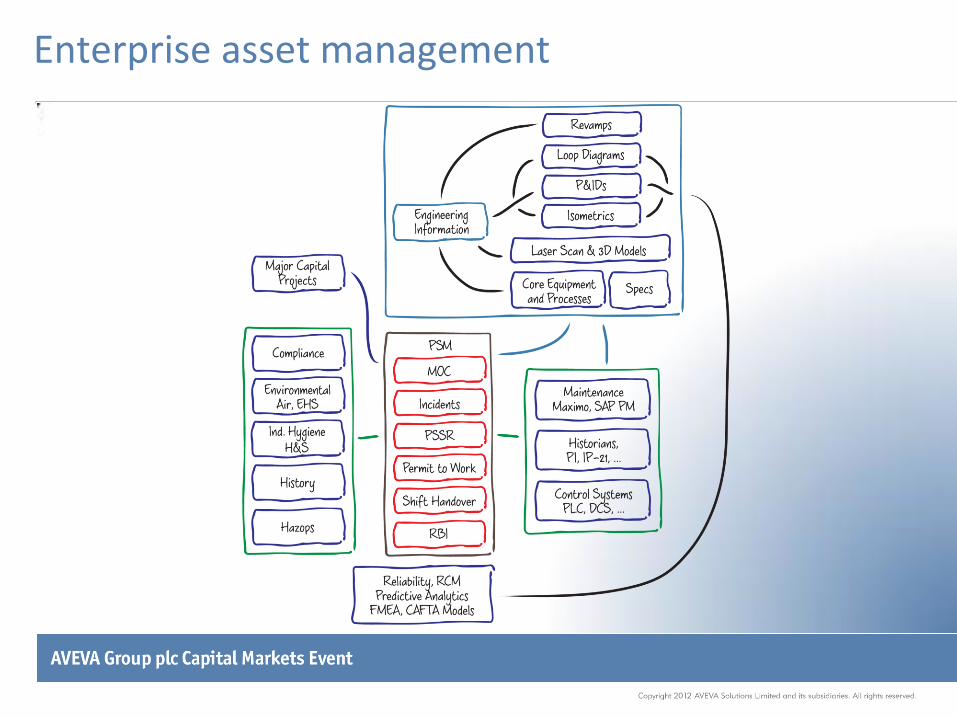

Enterprise asset management

Information-centric – Digital Information Hub

Delivery Model

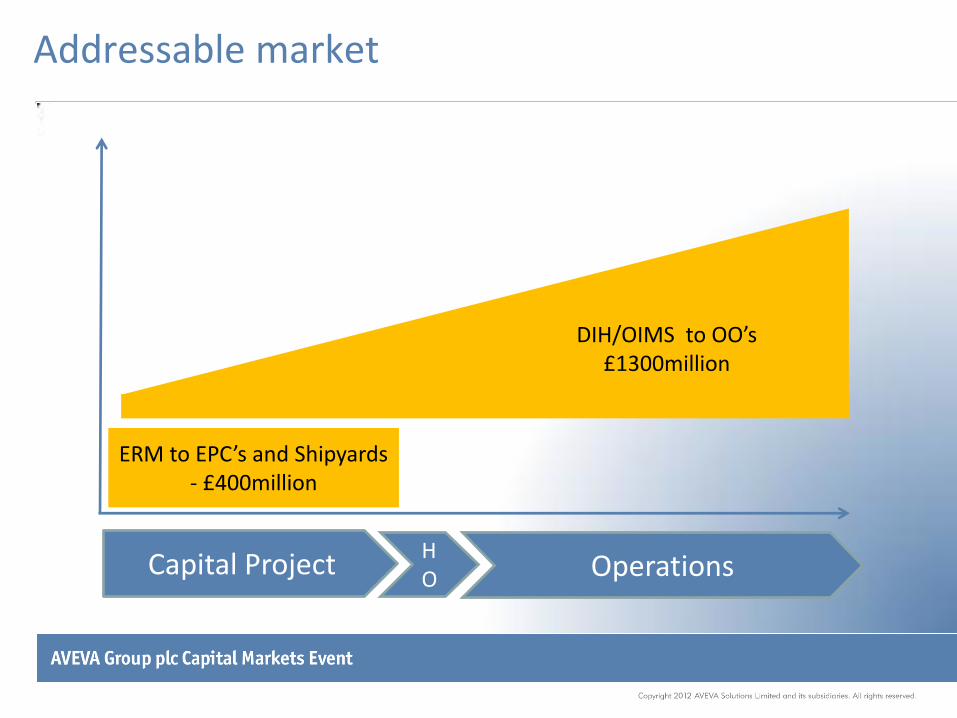

Addressable market

Capital Project HO Operations

ERM to EPC’s and Shipyards - £400million

DIH/OIMS to OO’s £1300million

Number one Priority

Operations

Construction & materials management

Strategic wins this year

Pipeline and backlog

Licencing model

Wrap up

Richard Longdon Chief Executive Officer

Thank you www.aveva.com/investors