Embed Size (px)

Citation preview

TSR, Executive Compensation, and Firm Performance∗

A Brief Prepared by the Institute for Compensation Studies

ILR School, Cornell University

Hassan Enayati, Kevin Hallock, and Linda Barrington

October 1, 2015

∗Funding for this study was provided by Pearl Meyer & Partners, jointly agreeing with the Institute for

Compensation Studies (ICS) authors on the research question of interest. Pearl Meyer & Partners obtained

the underlying data from Equilar, Inc., a leading independent provider of executive and board compensation

data and analysis. Pearl Meyer & Partners provided these data to ICS for analysis, including additional

data on companies from Capital IQ, and “compensation plan TSR existence and weight” variables that they

constructed. Pearl Meyer & Partners provided valuable insight on how executive compensation is structured

in the corporate landscape, which helped ICS ensure its models were valid in terms of real-world practice

and terminology. Independently, ICS conducted the statistical analyses herein.

We thank Stephanie Thomas and the consultants at Pearl Meyer & Partners for helpful comments.

1

1 Overview

• Particularly since the recent recession, the general public and policy makers have been

interested in aligning the incentives of executives with the incentives of shareholders.

• Embedding Total Shareholder Return (TSR) target metrics into top executive com-

pensation plans have been described as a simple and direct tool to align incentives.

• Despite the increased popularity of such TSR plans, the empirical evidence supporting

the expansion of this compensation strategy is limited.

• This brief aims to shed light on whether the inclusion of TSR measures in long-term

incentive plans result in improved firm performance.1

2 Data

The population of study for this research were identified using the 2014 S&P 500 index. A

rich longitudinal dataset was constructed using compensation data and firm financial data

covering fiscal years 2004 through 2013. Our analytical sample excluded 47 firms from this

population due to missing data concerns and another two firms as outliers.2 The information

regarding compensation was derived from Equilar’s executive compensation data. These data

contain detailed records of the compensation types and amounts for named executive officers

from firms in our sample. For example, we observe base salary, bonus payouts, stock awards,

option awards, and several types of incentive plan awards. Measures of firm performance

include 1, 3 and 5-year TSR as well as annual measures of return on equity (ROE), earning

per share (EPS) growth, and total revenue growth. Firm performance measures came from

1This brief is meant only to summarize the analytical research conducted to date. A full-length academicworking paper is forthcoming.

2These two outliers were classified as such because they had firm performance measures outside of thereasonable range of values, suggesting data error. The trimming parameters were set to flag observationswhere total revenue growth exceeded 100 percent, 1/3/5 TSR was above 5, or ROE was not between negativeone and positive one.

2

Capital IQ.3

3 Methodology

To examine how the inclusion of TSR plans impact firm performance, we used both de-

scriptive analysis and also regression analysis. The descriptive analysis compared the raw

patterns among groups of firms with and without TSR plans over time. The resulting tables

and figures are valuable in understanding the unconditional relationship between TSR plans

and firm performance. All analysis was conducted on three subsamples of executives: top

five named executive officers (NEOs), CEOs only, and top five NEOs excluding CEOs.

Regression analysis was used to as a way to control for other factors related to the role of

TSR measures on firm performance. Our baseline model uses the following Ordinary Least

Squares regression framework:

Yit = β1 + Zitβ2 + Sitβ3 + Ctβ4 + β5Xit + β6Xi,t−1 + β7Xi,t−2 + εit (1)

Yit represents a given performance measure for firm i in fiscal year t. The set of firm

performance measures studied in this brief are 1-year TSR, 3-year TSR, 5-year TSR, ROE,

EPS growth, and total revenue growth. Zit is a set of control variables including functions of

market capitalization and an indicator for change in CEO. Our model also accounts for sector

performance and year fixed effects with Sit and Ct, respectively. The key variables in this

project capture the existence and weight of TSR measures in the top executive compensation

plans, represented by Xit. For the existence of a TSR plan, Xit, is an indicator variable equal

to one when a firm has any executive in the relative sample with a TSR plan during the

current fiscal year. To analyze the role of weight on performance, Xit is set to the firm-

level average of the ratio of TSR award to either long term incentives (LTI) or total direct

3We would like to thank Pearl Meyer & Partners for providing us with the data used in this brief and alsofor constructing the key measures of TSR plan existence, TSR plan awards, performance-based compensation,long-term incentive pay, total compensation, and others.

3

compensation (TDC).4 Our baseline model includes two lags of Xit. Finally, the remaining

error in the model is captured by εit, which is clustered at the firm level.

Multiple extensions of the baseline model were investigated to assess the sensitivity of our

findings. One extension replaced the sector fixed effects with firm effects, which allows the

model to control for unobserved firm-specific and fixed attributes.5 We also partitioned the

sample by firm size and by TSR plan history. Additional sensitivity checks include removing

the Financials sector from the analysis and running models with a richer set of lag measures.

4 Results

Descriptive Statistics

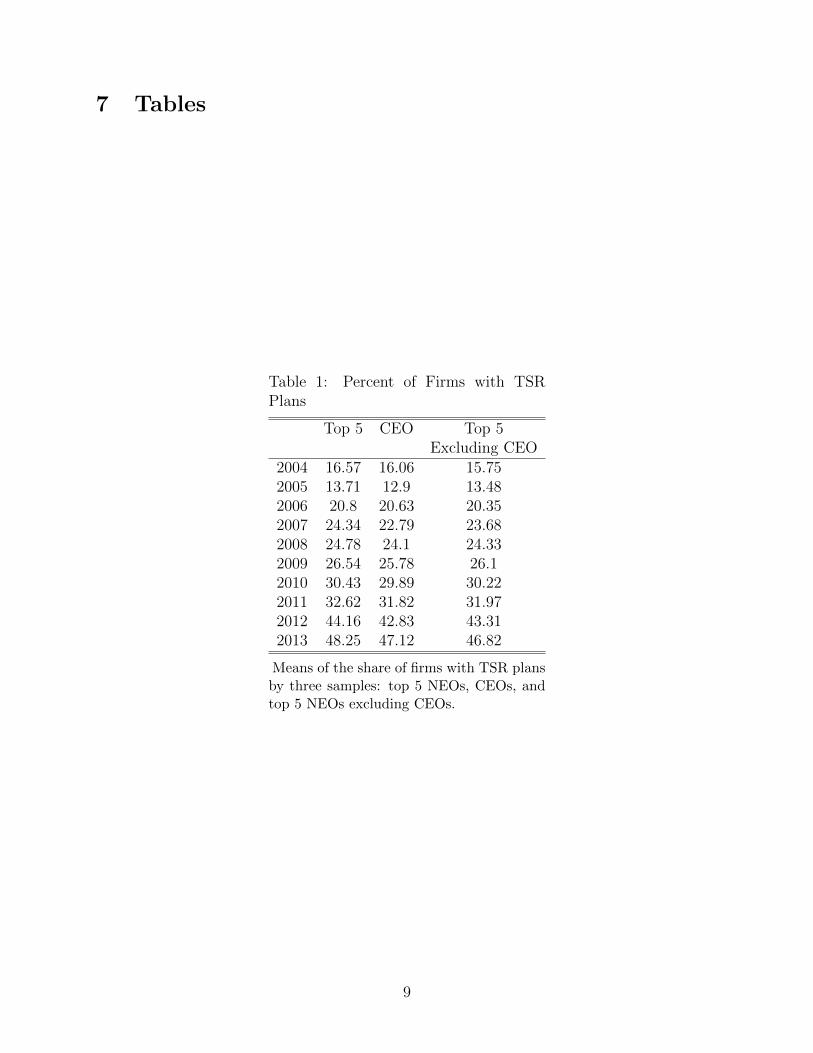

• Table 1 shows that for all three groups (Top 5, CEOs, and Top 5 Excluding CEOs)

the share of firms with TSR plans has increased from roughly 16 percent of firms to

just under 50 percent of firms.

• Table 2 reports how the weight of TSR has changed over time. The increasing pat-

terns in the unconditional columns and decreasing patterns in the conditional columns

suggests that more executives are receiving TSR measures in their compensation plans

but that the relative weight of those TSR plans is decreasing.

• Table 3 confirms the findings from Table 2 by demonstrating that the growth in the

weight of performance-based grants is a result of growth in non-TSR components.

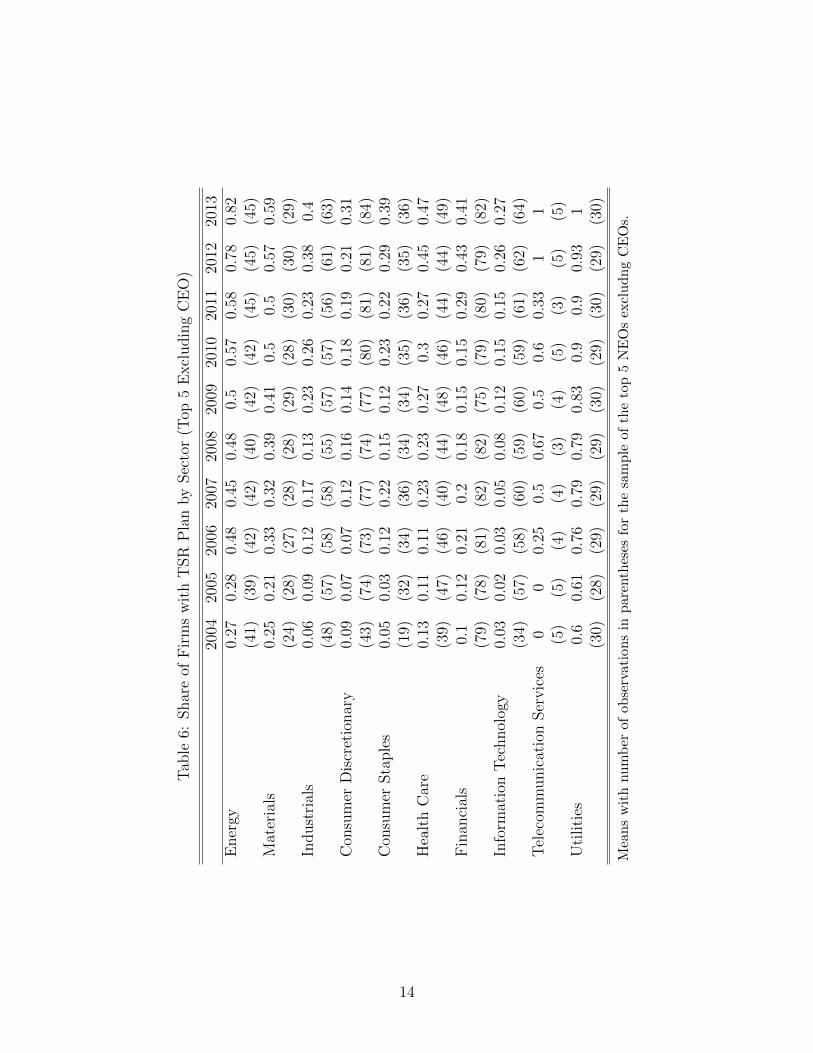

• Tables 4 through 6 show that firms in all sectors have increasingly included TSR plans

in the compensation of their executives.

• Table 7 groups firms by whether they always had a TSR plan, never had a TSR plan, or

changed. This grouping indicates that the firms that change are larger while upholding

4See Appendix for variable definitions.5For a thorough explanation of fixed effects techniques see Wooldridge, Jeffrey M. Econometric analysis

of cross section and panel data. MIT press, 2010.

4

the previous finding that those with TSR plans tend to be less profitable.

Regression Analysis

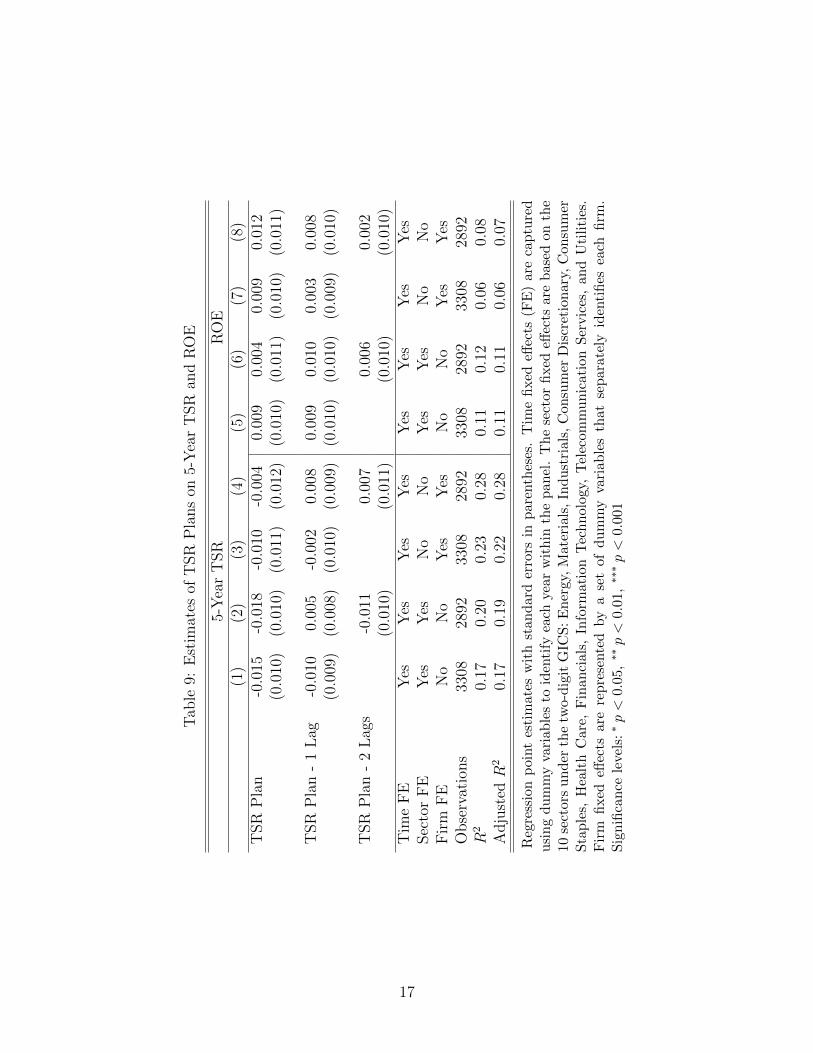

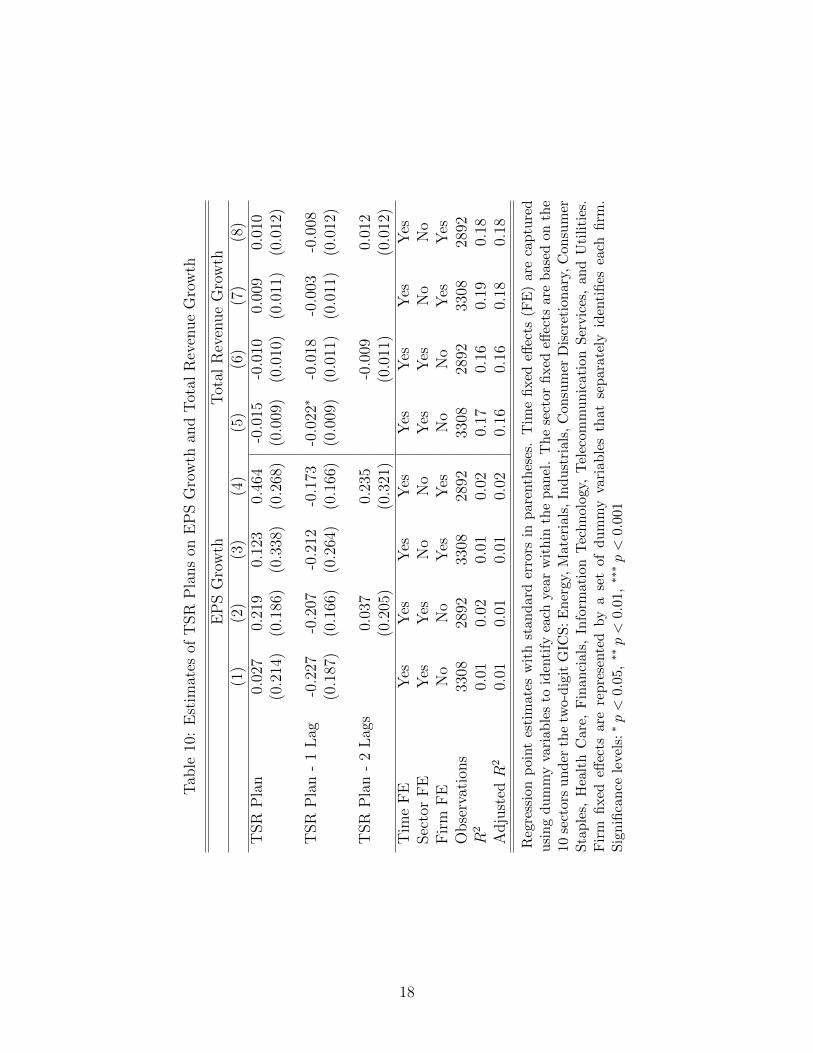

• Estimates of TSR plans on firm performance (Tables 8 through 10) indicate that there is

no strong evidence of a positive impact of TSR plans on firm performance. Moreover,

we find that point estimates of TSR plans on 1/3/5 year TSR measures are often

negative while only occasionally being statistically significant.

• For example, the right panel of Table 10 reports the estimates of the role of TSR plans

on total revenue growth.

– The estimates of the first lag of TSR plan on revenue growth, i.e., how is the

existence of a TSR plan among any of the company’s NEOs one year ago related

to current revenue growth, are negative.

– Column 5 indicates that the existence of a TSR plan one year ago is associated

with a decline in current revenue growth by 2.2 percentage points.

• Moreover, further analyses find a consistent pattern of a negative relationship between

TSR plans and total revenue growth, where the one year lag appears to be the driving

factor.

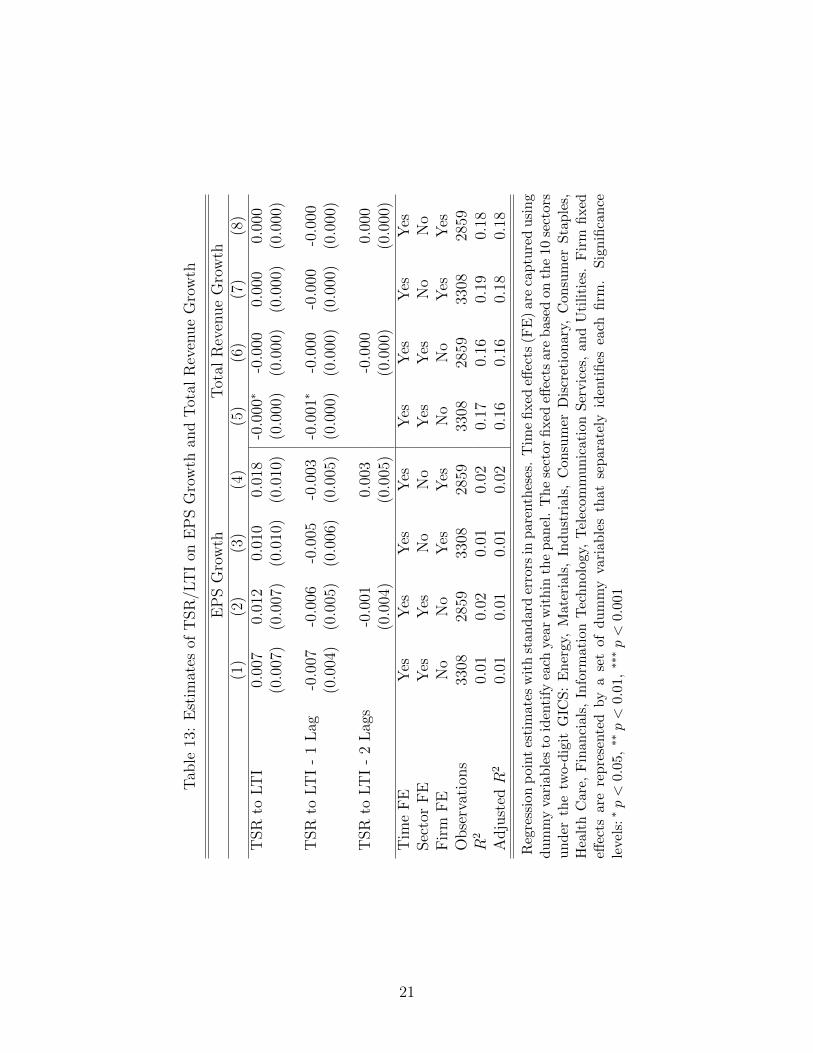

• Estimates of relative TSR to LTI on firm performance (Tables 11 through 13) continue

to present evidence of a negative relationship between TSR measures and total revenue

growth.

– Models incorporating firm fixed effects find small but statistically significant pos-

itive estimates of the role of contemporaneous TSR weights on ROE

– Specifically, a one percent increase in the ratio of TSR to LTI is associated with

a 0.1 percent increase in ROE.

5

• Additional analyses examined the sensitivity of the above regression estimates by quar-

tile of market capitalization, exclusion of the Financials sector, exclusion of firms with-

out changing TSR policies, richer five year lagged dependent variable structure, and

limiting the analysis to only those firms with relative TSR to LTI greater than 50

percent.6

5 Discussion and Future Direction

Currently, almost half of the 2014 S&P 500 firms offer TSR plans to their named executive

officers (NEO) - a twofold increase between 2004 and 2013. As evidenced by Table 2, the

increase in the weight of TSR awards to both LTI and TDC appears to be the result of

more NEOs receiving low weighted TSR plans. Furthermore, increases in the weight of

performance-based pay to both LTI and TDC over time are related to the increases in both

the frequency and weight of performance-based grants over time. The expansion of TSR

plans is observed across all sectors, with particularly large uptake within the Consumer

Staples and Information Technology sectors.

Differences are observable in the firms that include TSR measures into the compensation

plans of their executives compared to those that do not include TSR plans. Firms with TSR

plans tend to be larger (as measured by market capitalization and total revenue) and less

profitable (as measured by 10 year compound annual growth rates (CAGR) of Net Income,

ROIC, EBIT, EPS, ROA, ROE, and Free Cash Flow). The evidence from our primary model

specifications as well as numerous sensitivity checks indicate that there is either no impact

of TSR plans on firm performance or weak evidence of a negative relationship.

An important caution of these results needs to be noted. As with any regression models

of the type deployed here, statistical results only indicate relationship, not causation. That

said, the models controlled for a wide range of likely influential factors, including firm size,

sector, change in CEO leadership, time effects, and firm-specific fixed effects.

6The results of these analyses are available from the authors upon request.

6

The academic literature around TSR awards and firm performance is very limited. This

project represents the first academic effort to address this topic. The importance of this work

is not only to clarify the trends associated with expanding TSR plans for executives of S&P

500 companies, but to surface the need for further empirical research on the relationship

between including TSR and other metrics of firm performance in the compensation plans of

top executives and the ultimate sustainable financial success for the firms they lead. The

future steps in this line of research could examine, for example, more refined measures of

TSR awards. This work is an important first, not final, step in the examination of executive

performance pay.

7

6 Appendix

This appendix provides variable definitions for key measures used in this study.

• TSR outcome measures, where the closing price is adjusted for dividends

– 1-Year TSR: (Fiscal year end stock price/previous fiscal year end stock price)-1

– 3-Year TSR: {(Fiscal year end stock price/three fiscal year priors end stock

price)(̂1/3)}-1

– 5-Year TSR: {(Fiscal year end stock price/five fiscal year priors end stock price)(̂1/5)}-

1

• TDC measures

– For FY 2006-2013: TDC = Long-Term Incentives + Base Salary + Short-Term

Portion of NEIP Compensation + Bonus

– For FY 2004-2005: TDC = Base Salary + Bonus + Other Annual Compensation

+ Restricted Stock + Value of Stock Options (FAS 123(R)) + LTIP Payouts +

Other Compensation

• LTI measures

– For FY 2006-2013: LTI = Grant Date Present Value of Securities + Grant Date

Present Value of Option (FAS 123(R)) + Grant Date Present Value of Target

Award

– For FY 2004-2005: LTI = Restricted Stock Awards + Grant Date Present Value

of Option (FAS 123(R)) + FYE Target Value

8

7 Tables

Table 1: Percent of Firms with TSRPlans

Top 5 CEO Top 5Excluding CEO

2004 16.57 16.06 15.752005 13.71 12.9 13.482006 20.8 20.63 20.352007 24.34 22.79 23.682008 24.78 24.1 24.332009 26.54 25.78 26.12010 30.43 29.89 30.222011 32.62 31.82 31.972012 44.16 42.83 43.312013 48.25 47.12 46.82

Means of the share of firms with TSR plansby three samples: top 5 NEOs, CEOs, andtop 5 NEOs excluding CEOs.

9

Tab

le2:

Wei

ght

ofT

SR

Pla

n

Top

5C

EO

Top

5E

xcl

udin

gC

EO

Unco

ndit

ional

Con

dit

ional

onT

SR

Unco

ndit

ional

Con

dit

ional

onT

SR

Unco

ndit

ional

Con

dit

ional

onT

SR

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

Yea

rLT

IT

DC

LT

IT

DC

LT

IT

DC

LT

IT

DC

LT

IT

DC

LT

IT

DC

2004

7.77

546

.64

31.6

57.

875.

2750

.13

37.6

47.

584.

6247

.86

30.9

220

056.

293.

4845

.68

26.6

16.

343.

4948

.23

29.9

66.

333.

3246

.54

25.8

2006

7.87

4.89

38.0

424

.24

8.8

5.73

41.6

428

.66

7.87

4.91

38.5

724

.65

2007

8.69

5.41

36.2

322

.86

9.37

6.12

41.1

27.8

38.

595.

2536

.47

22.6

2008

8.8

5.71

35.2

623

.04

10.0

66.

9740

.24

28.7

38.

565.

4134

.96

22.2

520

098.

915.

8334

.12

22.5

410

.23

6.99

38.9

427

.53

8.68

5.57

33.8

321

.920

1010

.29

6.44

33.8

221

.27

11.5

17.

6537

.94

25.7

210

.05

6.16

33.3

20.4

820

1110

.88

7.04

34.0

522

.12

11.6

98.

0336

.78

25.7

10.7

46.

8134

.321

.83

2012

14.8

59.

6735

.28

23.0

716

.74

11.5

140

28.2

314

.46

9.23

35.0

822

.47

2013

16.3

810

.77

35.2

423

.31

18.3

512

.95

39.9

628

.62

15.9

510

.24

35.4

122

.87

Mea

ns

ofth

ew

eigh

tof

TS

Rp

lan

sby

thre

esa

mp

les:

top

5N

EO

s,C

EO

s,an

dto

p5

NE

Os

excl

udin

gC

EO

s.U

nco

nd

itio

nal

esti

mat

esin

clu

de

firm

sw

ith

zero

ind

ivid

uals

(wit

hre

spec

tto

the

sam

ple

)re

por

ted

toh

ave

aT

SR

pla

n.

Con

dit

ion

alon

TS

Res

tim

ates

excl

ud

efi

rms

wit

hze

roin

div

idu

als

(wit

hre

spec

tto

the

sam

ple

)re

por

ted

toh

ave

aT

SR

pla

n.

10

Tab

le3:

Wei

ght

ofP

erfo

rman

ceP

ay

Un

con

dit

ion

alC

ond

itio

nal

onP

erfo

rman

ceP

ay

Yea

rN

on

-TS

RP

PN

on-T

SR

PP

PP

PP

Non

-TS

RP

PN

on-T

SR

PP

PP

PP

toLT

Ito

TD

Cto

LT

Ito

TD

Cto

LT

Ito

TD

Cto

LT

Ito

TD

C(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)

Top

52004

8.8

55.

9616

.62

10.9

52.

983.

5749

.62

35.2

220

05

9.35

615

.64

9.49

1.87

1.7

47.5

528

.31

2006

30.3

17.3

838

.17

22.2

822

.44

13.7

360

.48

37.9

720

07

38.2

422

46.9

327

.41

21.7

613

.31

57.9

936

.17

2008

39.3

324

.14

48.1

329

.85

26.7

517

.35

62.0

140

.39

2009

40.5

424

.72

49.4

430

.55

29.3

218

.48

63.4

341

.02

2010

40.1

423

.79

50.4

230

.23

28.1

717

.15

61.9

938

.42

2011

41.8

425

.952

.72

32.9

329

.14

18.2

663

.19

40.3

820

12

41.6

326

.44

56.4

836

.11

29.9

219

65.2

42.0

720

13

42.8

327

.56

59.2

138

.33

3119

.86

66.2

443

.17

CE

O20

04

8.6

6.79

16.4

712

.06

1.63

1.82

51.7

639

.45

2005

10.0

97.

3516

.43

10.8

40.

510.

548

.74

30.4

620

06

30.7

19.0

439

.524

.77

19.2

413

.260

.88

41.8

620

07

38.5

223

.53

47.9

29.6

519

.53

13.5

160

.63

41.3

420

08

39.0

125

.73

49.0

732

.724

.01

17.1

164

.25

45.8

420

09

41.0

526

.66

51.2

833

.65

26.6

418

.53

65.5

946

.06

2010

40.3

525

.551

.86

33.1

525

.88

17.1

463

.82

42.8

620

11

41.9

627

.73

53.6

535

.76

26.7

418

.36

63.5

244

.06

2012

41.5

428

.21

58.2

839

.72

28.0

419

.59

68.0

547

.83

2013

42.4

829

.92

60.8

342

.87

28.0

720

.03

68.0

348

.65

Top

5-

2004

9.0

55.

816

.63

10.4

21.

41.

4449

.26

32.3

6E

xcl

ud

ing

CE

O2005

9.2

85.

6715

.62

8.99

0.49

0.41

47.0

326

.22

2006

30.3

17.0

438

.18

21.9

522

.08

13.3

360

.65

37.9

820

07

38.2

421

.65

46.8

326

.922

.38

13.2

758

.85

35.8

720

08

39.4

223

.77

47.9

929

.19

27.3

217

.36

62.2

839

.61

2009

40.4

424

.27

49.1

229

.85

29.9

618

.46

63.7

940

.36

2010

40.1

823

.38

50.2

429

.53

28.6

117

.11

61.9

137

.59

2011

41.8

625

.44

52.6

32.2

529

.28

17.9

163

.57

39.7

420

12

41.7

325

.99

56.1

935

.22

29.8

518

.48

64.9

340

.94

2013

42.9

826

.96

58.9

337

.230

.86

19.2

466

.27

42.1

2

Mea

ns

ofth

ew

eigh

tof

per

form

an

cepay

by

thre

esa

mp

les:

top

5N

EO

s,C

EO

s,an

dto

p5

NE

Os

excl

udin

gC

EO

s.U

nco

nd

itio

nal

esti

mat

esin

clu

de

firm

sw

ith

zero

ind

ivid

ual

s(w

ith

resp

ect

toth

esa

mp

le)

rep

orte

dto

hav

ep

erfo

rman

ce-b

ased

com

pen

sati

on.

Con

dit

ion

alon

TS

Res

tim

ates

excl

ud

efi

rms

wit

hze

roin

div

idu

als

(wit

hre

spec

tto

the

sam

ple

)re

por

ted

toh

ave

per

form

ance

-b

ased

com

pen

sati

on

.

11

Tab

le4:

Shar

eof

Fir

ms

wit

hT

SR

Pla

nby

Sec

tor

(Top

5)

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Ener

gy0.

270.

280.

480.

450.

480.

50.

570.

580.

780.

84(4

1)(3

9)(4

2)(4

2)(4

0)(4

2)(4

2)(4

5)(4

5)(4

5)M

ater

ials

0.25

0.21

0.33

0.32

0.39

0.41

0.5

0.5

0.57

0.59

(24)

(28)

(27)

(28)

(28)

(29)

(28)

(30)

(30)

(29)

Indust

rial

s0.

080.

090.

140.

220.

150.

250.

260.

270.

380.

41(4

8)(5

7)(5

8)(5

8)(5

5)(5

7)(5

7)(5

6)(6

1)(6

3)C

onsu

mer

Dis

cret

ionar

y0.

090.

070.

070.

120.

160.

140.

190.

190.

230.

32(4

3)(7

4)(7

3)(7

7)(7

4)(7

7)(8

0)(8

1)(8

1)(8

4)C

onsu

mer

Sta

ple

s0.

050.

030.

120.

220.

150.

120.

230.

220.

290.

42(1

9)(3

2)(3

4)(3

6)(3

4)(3

4)(3

5)(3

6)(3

5)(3

6)H

ealt

hC

are

0.13

0.11

0.11

0.23

0.25

0.29

0.3

0.27

0.45

0.49

(39)

(47)

(46)

(40)

(44)

(48)

(46)

(44)

(44)

(49)

Fin

anci

als

0.1

0.12

0.21

0.2

0.18

0.15

0.15

0.3

0.43

0.44

(79)

(78)

(81)

(82)

(82)

(75)

(79)

(80)

(79)

(82)

Info

rmat

ion

Tec

hnol

ogy

0.03

0.02

0.03

0.05

0.08

0.12

0.15

0.15

0.29

0.27

(34)

(57)

(58)

(60)

(59)

(60)

(59)

(61)

(62)

(64)

Tel

ecom

munic

atio

nSer

vic

es0.

20.

20.

50.

50.

670.

50.

60.

331

1(5

)(5

)(4

)(4

)(3

)(4

)(5

)(3

)(5

)(5

)U

tiliti

es0.

630.

610.

760.

790.

790.

830.

90.

90.

931

(30)

(28)

(29)

(29)

(29)

(30)

(29)

(30)

(29)

(30)

Mea

ns

wit

hnu

mb

erof

obse

rvat

ion

sin

par

enth

eses

for

the

sam

ple

ofth

eto

p5

NE

Os.

12

Tab

le5:

Shar

eof

Fir

ms

wit

hT

SR

Pla

nby

Sec

tor

(CE

O)

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Ener

gy0.

250.

280.

490.

430.

480.

50.

590.

590.

760.

78(4

0)(3

9)(4

1)(4

2)(4

0)(4

2)(4

1)(4

4)(4

5)(4

5)M

ater

ials

0.25

0.21

0.33

0.32

0.39

0.38

0.5

0.5

0.53

0.59

(24)

(28)

(27)

(28)

(28)

(29)

(28)

(30)

(30)

(29)

Indust

rial

s0.

090.

090.

140.

220.

150.

250.

250.

270.

350.

4(4

7)(5

7)(5

8)(5

8)(5

5)(5

7)(5

7)(5

6)(6

0)(6

3)C

onsu

mer

Dis

cret

ionar

y0.

070.

040.

070.

10.

140.

120.

180.

160.

230.

31(4

2)(7

3)(7

1)(7

7)(7

3)(7

6)(7

8)(8

0)(7

9)(8

4)C

onsu

mer

Sta

ple

s0.

050.

030.

120.

170.

120.

120.

230.

230.

290.

42(1

9)(3

2)(3

3)(3

5)(3

3)(3

4)(3

5)(3

5)(3

5)(3

6)H

ealt

hC

are

0.13

0.11

0.11

0.23

0.25

0.27

0.26

0.25

0.45

0.49

(39)

(47)

(46)

(40)

(44)

(48)

(46)

(44)

(44)

(49)

Fin

anci

als

0.1

0.1

0.2

0.17

0.18

0.15

0.15

0.3

0.41

0.44

(78)

(78)

(80)

(81)

(82)

(71)

(79)

(80)

(79)

(82)

Info

rmat

ion

Tec

hnol

ogy

0.03

0.02

0.04

0.03

0.09

0.1

0.16

0.13

0.3

0.25

(31)

(55)

(57)

(58)

(57)

(59)

(57)

(60)

(61)

(63)

Tel

ecom

munic

atio

nSer

vic

es0.

20.

20.

50.

50.

670.

50.

60.

331

1(5

)(5

)(4

)(4

)(3

)(4

)(5

)(3

)(5

)(5

)U

tiliti

es0.

60.

570.

720.

760.

760.

830.

90.

870.

91

(30)

(28)

(29)

(29)

(29)

(30)

(29)

(30)

(29)

(30)

Mea

ns

wit

hnu

mb

erof

obse

rvat

ion

sin

par

enth

eses

for

the

sam

ple

ofC

EO

s.

13

Tab

le6:

Shar

eof

Fir

ms

wit

hT

SR

Pla

nby

Sec

tor

(Top

5E

xcl

udin

gC

EO

)

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Ener

gy0.

270.

280.

480.

450.

480.

50.

570.

580.

780.

82(4

1)(3

9)(4

2)(4

2)(4

0)(4

2)(4

2)(4

5)(4

5)(4

5)M

ater

ials

0.25

0.21

0.33

0.32

0.39

0.41

0.5

0.5

0.57

0.59

(24)

(28)

(27)

(28)

(28)

(29)

(28)

(30)

(30)

(29)

Indust

rial

s0.

060.

090.

120.

170.

130.

230.

260.

230.

380.

4(4

8)(5

7)(5

8)(5

8)(5

5)(5

7)(5

7)(5

6)(6

1)(6

3)C

onsu

mer

Dis

cret

ionar

y0.

090.

070.

070.

120.

160.

140.

180.

190.

210.

31(4

3)(7

4)(7

3)(7

7)(7

4)(7

7)(8

0)(8

1)(8

1)(8

4)C

onsu

mer

Sta

ple

s0.

050.

030.

120.

220.

150.

120.

230.

220.

290.

39(1

9)(3

2)(3

4)(3

6)(3

4)(3

4)(3

5)(3

6)(3

5)(3

6)H

ealt

hC

are

0.13

0.11

0.11

0.23

0.23

0.27

0.3

0.27

0.45

0.47

(39)

(47)

(46)

(40)

(44)

(48)

(46)

(44)

(44)

(49)

Fin

anci

als

0.1

0.12

0.21

0.2

0.18

0.15

0.15

0.29

0.43

0.41

(79)

(78)

(81)

(82)

(82)

(75)

(79)

(80)

(79)

(82)

Info

rmat

ion

Tec

hnol

ogy

0.03

0.02

0.03

0.05

0.08

0.12

0.15

0.15

0.26

0.27

(34)

(57)

(58)

(60)

(59)

(60)

(59)

(61)

(62)

(64)

Tel

ecom

munic

atio

nSer

vic

es0

00.

250.

50.

670.

50.

60.

331

1(5

)(5

)(4

)(4

)(3

)(4

)(5

)(3

)(5

)(5

)U

tiliti

es0.

60.

610.

760.

790.

790.

830.

90.

90.

931

(30)

(28)

(29)

(29)

(29)

(30)

(29)

(30)

(29)

(30)

Mea

ns

wit

hnu

mb

erof

obse

rvat

ion

sin

par

enth

eses

for

the

sam

ple

ofth

eto

p5

NE

Os

excl

ud

ng

CE

Os.

14

Tab

le7:

Fir

mC

har

acte

rist

ics

by

TSR

Pla

nP

atte

rn(T

op5)

Alw

ays

TSR

Chan

geT

SR

Nev

erT

SR

Mar

ket

Cap

-A

vg

2538

0.28

2574

6.1

1922

3.57

(0.3

1)(0

.1)

Tot

alR

even

ue

-A

vg

1884

6.49

1722

3.51

1507

2.41

(0.3

9)(0

.46)

10Y

rN

etIn

cC

AG

R6.

667.

711

.51

(0.0

2)(0

)10

Yr

RO

ICC

AG

R0.

880.

421.

82(0

.5)

(0.1

5)10

Yr

EB

ITC

AG

R5.

757.

6612

.38

(0)

(0)

10Y

rE

PS

CA

GR

6.95

6.05

11.4

7(0

.03)

(0)

10Y

rR

OA

CA

GR

0.05

0.06

0.07

(0)

(0)

10Y

rR

OE

CA

GR

0.31

0.14

0.18

(0.0

4)(0

.29)

10Y

rF

CF

CA

GR

4.33

8.56

11.3

7(0

.01)

(0.0

9)O

bse

rvat

ions

5518

820

8

Mea

ns

wit

hp

-val

ues

inp

aren

thes

esfo

rth

esa

mp

leof

the

top

five

NE

Os.

Fir

ms

are

gro

up

edin

toth

ree

grou

ps

bas

edon

the

sam

ple

per

iod

:th

ose

that

alw

ays

had

aT

SR

pla

n,

thos

eth

atn

ever

had

aT

SR

pla

n,

and

thos

eth

atch

anged

thei

rT

SR

pla

ns

by

eith

erin

trod

uci

ng

orre

mov

ing

them

.

15

Tab

le8:

Est

imat

esof

TSR

Pla

ns

on1-

Yea

rT

SR

and

3-Y

ear

TSR

1-Y

ear

TSR

3-Y

ear

TSR

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

TSR

Pla

n-0

.010

-0.0

090.

011

0.01

0-0

.004

-0.0

020.

016

0.02

1(0

.028

)(0

.023

)(0

.034

)(0

.028

)(0

.010

)(0

.011

)(0

.013

)(0

.012

)

TSR

Pla

n-

1L

ag-0

.008

0.02

2-0

.012

0.00

2-0

.009

0.01

00.

007

0.01

0(0

.029

)(0

.039

)(0

.033

)(0

.036

)(0

.011

)(0

.012

)(0

.014

)(0

.013

)

TSR

Pla

n-

2L

ags

-0.0

48-0

.021

-0.0

21-0

.003

(0.0

30)

(0.0

31)

(0.0

13)

(0.0

15)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

3308

2892

3308

2892

3308

2892

3308

2892

R2

0.15

0.17

0.18

0.21

0.16

0.21

0.19

0.29

Adju

sted

R2

0.14

0.16

0.18

0.21

0.15

0.21

0.19

0.29

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Car

e,F

inan

cial

s,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

16

Tab

le9:

Est

imat

esof

TSR

Pla

ns

on5-

Yea

rT

SR

and

RO

E

5-Y

ear

TSR

RO

E(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)T

SR

Pla

n-0

.015

-0.0

18-0

.010

-0.0

040.

009

0.00

40.

009

0.01

2(0

.010

)(0

.010

)(0

.011

)(0

.012

)(0

.010

)(0

.011

)(0

.010

)(0

.011

)

TSR

Pla

n-

1L

ag-0

.010

0.00

5-0

.002

0.00

80.

009

0.01

00.

003

0.00

8(0

.009

)(0

.008

)(0

.010

)(0

.009

)(0

.010

)(0

.010

)(0

.009

)(0

.010

)

TSR

Pla

n-

2L

ags

-0.0

110.

007

0.00

60.

002

(0.0

10)

(0.0

11)

(0.0

10)

(0.0

10)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

3308

2892

3308

2892

3308

2892

3308

2892

R2

0.17

0.20

0.23

0.28

0.11

0.12

0.06

0.08

Adju

sted

R2

0.17

0.19

0.22

0.28

0.11

0.11

0.06

0.07

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Car

e,F

inan

cial

s,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

17

Tab

le10

:E

stim

ates

ofT

SR

Pla

ns

onE

PS

Gro

wth

and

Tot

alR

even

ue

Gro

wth

EP

SG

row

thT

otal

Rev

enue

Gro

wth

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

TSR

Pla

n0.

027

0.21

90.

123

0.46

4-0

.015

-0.0

100.

009

0.01

0(0

.214

)(0

.186

)(0

.338

)(0

.268

)(0

.009

)(0

.010

)(0

.011

)(0

.012

)

TSR

Pla

n-

1L

ag-0

.227

-0.2

07-0

.212

-0.1

73-0

.022

∗-0

.018

-0.0

03-0

.008

(0.1

87)

(0.1

66)

(0.2

64)

(0.1

66)

(0.0

09)

(0.0

11)

(0.0

11)

(0.0

12)

TSR

Pla

n-

2L

ags

0.03

70.

235

-0.0

090.

012

(0.2

05)

(0.3

21)

(0.0

11)

(0.0

12)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

3308

2892

3308

2892

3308

2892

3308

2892

R2

0.01

0.02

0.01

0.02

0.17

0.16

0.19

0.18

Adju

sted

R2

0.01

0.01

0.01

0.02

0.16

0.16

0.18

0.18

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Car

e,F

inan

cial

s,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

18

Tab

le11

:E

stim

ates

ofT

SR

/LT

Ion

1-Y

ear

TSR

and

3-Y

ear

TSR

1-Y

ear

TSR

3-Y

ear

TSR

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

TSR

toLT

I-0

.001

-0.0

00-0

.000

0.00

0-0

.000

-0.0

000.

000

0.00

1(0

.001

)(0

.000

)(0

.001

)(0

.001

)(0

.000

)(0

.000

)(0

.000

)(0

.000

)

TSR

toLT

I-

1L

ag-0

.000

0.00

10.

000

0.00

00.

000

0.00

00.

001

0.00

0(0

.001

)(0

.001

)(0

.001

)(0

.001

)(0

.000

)(0

.000

)(0

.000

)(0

.000

)

TSR

toLT

I-

2L

ags

-0.0

01-0

.001

-0.0

000.

000

(0.0

01)

(0.0

01)

(0.0

00)

(0.0

00)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

3308

2859

3308

2859

3308

2859

3308

2859

R2

0.15

0.17

0.18

0.21

0.16

0.21

0.19

0.29

Adju

sted

R2

0.14

0.16

0.18

0.21

0.15

0.21

0.19

0.29

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Indu

stri

als,

Con

sum

erD

iscr

etio

nar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are

,F

inan

cials

,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.05,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

19

Tab

le12

:E

stim

ates

ofT

SR

/LT

Ion

3-Y

ear

TSR

and

RO

E

5-Y

ear

TSR

RO

E(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)T

SR

toLT

I-0

.000

-0.0

00-0

.000

0.00

00.

000

0.00

00.

001∗

0.00

1∗

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

TSR

toLT

I-

1L

ag-0

.000

0.00

00.

000

0.00

0∗0.

000

0.00

00.

000

0.00

0(0

.000

)(0

.000

)(0

.000

)(0

.000

)(0

.000

)(0

.000

)(0

.000

)(0

.000

)

TSR

toLT

I-

2L

ags

-0.0

000.

000

0.00

00.

000

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

3308

2859

3308

2859

3308

2859

3308

2859

R2

0.17

0.20

0.23

0.28

0.11

0.12

0.07

0.08

Adju

sted

R2

0.17

0.19

0.22

0.28

0.11

0.11

0.06

0.08

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Indu

stri

als,

Con

sum

erD

iscr

etio

nar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are

,F

inan

cials

,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.05,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

20

Tab

le13

:E

stim

ates

ofT

SR

/LT

Ion

EP

SG

row

than

dT

otal

Rev

enue

Gro

wth

EP

SG

row

thT

otal

Rev

enue

Gro

wth

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

TSR

toLT

I0.

007

0.01

20.

010

0.01

8-0

.000

∗-0

.000

0.00

00.

000

(0.0

07)

(0.0

07)

(0.0

10)

(0.0

10)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

TSR

toLT

I-

1L

ag-0

.007

-0.0

06-0

.005

-0.0

03-0

.001

∗-0

.000

-0.0

00-0

.000

(0.0

04)

(0.0

05)

(0.0

06)

(0.0

05)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

TSR

toLT

I-

2L

ags

-0.0

010.

003

-0.0

000.

000

(0.0

04)

(0.0

05)

(0.0

00)

(0.0

00)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

3308

2859

3308

2859

3308

2859

3308

2859

R2

0.01

0.02

0.01

0.02

0.17

0.16

0.19

0.18

Adju

sted

R2

0.01

0.01

0.01

0.02

0.16

0.16

0.18

0.18

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Indu

stri

als,

Con

sum

erD

iscr

etio

nar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are

,F

inan

cials

,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.05,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

21