Embed Size (px)

Citation preview

1 23

Journal of Business Ethics ISSN 0167-4544 J Bus EthicsDOI 10.1007/s10551-016-3048-3

Truthfulness in Accounting: How toDiscriminate Accounting Manipulatorsfrom Non-manipulators

Alina Beattrice Vladu, Oriol Amat &Dan Dacian Cuzdriorean

1 23

Your article is protected by copyright and all

rights are held exclusively by Springer Science

+Business Media Dordrecht. This e-offprint

is for personal use only and shall not be self-

archived in electronic repositories. If you wish

to self-archive your article, please use the

accepted manuscript version for posting on

your own website. You may further deposit

the accepted manuscript version in any

repository, provided it is only made publicly

available 12 months after official publication

or later and provided acknowledgement is

given to the original source of publication

and a link is inserted to the published article

on Springer's website. The link must be

accompanied by the following text: "The final

publication is available at link.springer.com”.

Truthfulness in Accounting: How to Discriminate AccountingManipulators from Non-manipulators

Alina Beattrice Vladu1 • Oriol Amat2 • Dan Dacian Cuzdriorean1

Received: 18 August 2014 / Accepted: 28 January 2016

� Springer Science+Business Media Dordrecht 2016

Abstract Accountants preparing information are in a

position to manipulate the view of economic reality pre-

sented in such information to interested parties. These

manipulations can be regarded as morally reprehensible

because they are not fair to users, they involve in an unjust

exercise of power, and they tend to weaken the authority of

accounting regulators. This paper develops a model for

detecting earnings manipulators using financial statements’

ratios in a sample of Spanish listed companies. Our results

provide evidence that accounting data can be extremely

useful in detecting manipulators. This approach can be

used by a large category of users of accounting information

among which we can cite stock exchange supervisors or

investing professionals.

Keywords Accounting ethics � Earnings manipulation �Accounting users � Earnings management �Financial reporting

Introduction

Akerlof and Shiller (2009), giving their view on financial

corruption, asserted that accounting plays its role in this

context since it makes it appear that the firm is doing better

than its true performance. Major corporate scandals like

Enron, WorldCom or Tyco have all been linked directly or

indirectly to deception, misleading, and untruthful

accounting. Similarly, the former global crisis of the

financial system was associated with false accounting. In

the light of such evidence, the accounting profession con-

tinues to struggle with the problem of veracity of its

reports.

Over time, the users of accounting information gravi-

tated to a coherence notion of truth despite the fact that

accounting-standard setters agreed that the usefulness of

decision making is the ultimate objective of financial

reporting, and not truthfulness.

Truthfulness and pernicious earnings management (re-

garded as antithetical, in the view of Ronen and Yaari

2010) raised a host of questions that are of concern to

regulators, academics, practitioners, and press. For

instance, Briloff (1972, 1981, 1990, 2001), among other

scholars, asserted that the accounting profession is keen to

revive a moral order where the truth must be provided

along with true and fair presentations of corporate

performance.

The problem with the truthfulness of accounting

reports was examined by previous research in the con-

text of managers using discretion for both informational

and opportunistic reasons (Feltham et al. 2006; Chris-

tensen and Demski 2003; Bradshaw and Sloan 2002).

While the informative role arises from a large category

of users‘ demand for information about the underlying

economics of their firms, opportunistic motivations

appear when managers bias users‘ perspectives. There-

fore, sometimes managers use their rationality equated

with pursuing self-interest in the opportunistic sense

(Fama 1980; Fama and Jensen 1983; Hsiang-Lin et al.

2008).

& Alina Beattrice Vladu

Oriol Amat

Dan Dacian Cuzdriorean

1 Babes-Bolyai University, Cluj-Napoca, Romania

2 Universitat Pompeu Fabra, Barcelona, Spain

123

J Bus Ethics

DOI 10.1007/s10551-016-3048-3

Author's personal copy

The past few years have seen a significant increase in

the degree of empirical evidence consistent with oppor-

tunism in accounting (McVay 2006; Bowen et al. 2002;

Schrand and Walther 2000). As a result, there has also been

an increased interest in the mechanisms used to promote

truthfulness in accounting, such as harsh penalties for

violating the code of ethics; professional skepticism; and

enforcing rules, laws, and regulations or continuous efforts

conducted in order to improve the models used to assess

the existence and magnitude of opportunistic behavior.

Regarded as a problem in ‘‘need of immediate remedial

action’’ (Dechow and Skinner 2000), earnings manipula-

tion and opportunism have been linked to lax ethics (Lucas

2004). A basic cornerstone of all previous ideas regarding

the earnings manipulation conceals short- or long-term

value, affecting the earnings numbers and their interpre-

tations, with the scope to hide or distort the real financial

performance or financial condition of a firm. In the end,

what makes earnings management practices scandalous is

not only their violation of investor protection laws but their

clash with general, accepted social norms or good practices

(Ball 2009). In this respect, empirical analysis of financial

reporting is beneficial, if for no other reason than to help

increase awareness and ethical behavior.

This paper is concerned with gray earnings management

practices consisting of the ‘‘manipulation of reports within

the boundaries of compliance with bright-line standards,

which could be either opportunistic or efficiency enhanc-

ing’’ (Ronen and Yaari 2010, p. 25). The connotation of

gray earnings management is that it is immoral even when

it does not involve fraud (Bruns and Merchant 1990;

Carpenter and Reimers 2001; Shafer 2002). Therefore, our

study regards the manipulation of earnings as an obstacle

for truthfulness and a potential factor for destabilization of

companies.

Despite the large number of papers purporting to iden-

tify techniques to assess earnings management practices

used by manipulators, few studies approached simple

methods to detect such behavior and even fewer utilized

ratio analysis in this demarche. According to Altman

(1968), academics seem to move toward the elimination of

ratio analysis as an analytical technique used in assessing

the performance of the firm. Widely used by practitioners,

ratio analysis is abandoned by scholars worldwide in their

attempt to develop more and more sophisticated tools to

assess the effects of opportunistic behavior of managers.

The preferred methods used to assess the behavior of

manipulators, are based on the assumption that accruals

unexplained by a linear projection on firm-level observ-

ables (known as discretionary accruals) represent either

explicit earnings management or poor quality earnings.

Such techniques often assume that the residual from a

linear regression represents earnings management.

Despite their popularity, a major limitation of this

research is that existing techniques for measuring earnings

management lack power and are often misspecified. In this

respect, the large majority of the existing techniques suffer

from measurement error and correlated omitted variables,

which lead to Type 1 errors (i.e., rejection of a true null

hypothesis of no earnings management) and Type 2 errors

(i.e., failure to reject a false null hypothesis of no earnings

management). However, there is no systematic evidence

bearing on the relative performance of the most popular

models used at detecting earnings management practices.

Moreover, the most common techniques for measuring

earnings management have not significantly changed in

over 30 years. The main limitations are enumerated in

Dechow et al. (1995).

Since few improvements have been made since Dechow

et al. (1995), alternative techniques have been proposed for

assessing the behavior of manipulators. Concerned mainly

with the negative side of earnings manipulation practices

(Gong et al. 2008), our paper builds upon the literature

approaching the improvement of various models used for

detecting earnings manipulation and assessing its magni-

tude (Dechow et al. 1995, 2012).

Specifically, we build upon the literature by examining a

simple and cost-effective way to discriminate between the

behavior of manipulators and non-manipulators using

financial statement ratios. Similarly to Beneish (1999) we

tried to follow a more traditional path to uncover the

behavior of manipulators using ratio analysis combined

with a multiple discriminant statistical methodology. Our

investigation was motivated by the controversial interpre-

tations of previous evidence on identifying manipulators

and by the fact that this stream of research has not reached

a definite conclusion (Dechow and Skinner 2000; Healy

and Wahlen 1999; Schipper 1989). In addition, our paper is

motivated by standard-setters’ interest in financial report-

ing quality, and by theoretical debates on whether truth-

fulness has a place in business world.

The prediction of manipulative behavior of Spanish

companies is used as an illustrative case. We have con-

ducted our tests using a sample of listed companies that

manipulated their earnings and available companies listed

on the Spanish Stock Exchange that were known as fol-

lowing ‘‘good practices’’ in the period 2005–2012. There-

fore, our paper extends the literature of ratio analysis

combined with rigorous statistical technique used in the

context of earnings manipulation. Our ultimate goal is to

stimulate further research in an area that has the potential

to yield valuable insights.

The remainder of our paper is organized as follows.

Section ‘‘Truthfulness and the Ethics of Earnings Manip-

ulation in Accounting’’ reviews and evaluates existing

research on truthfulness and ethics in accounting.

A. B. Vladu et al.

123

Author's personal copy

Section ‘‘Earnings Management and the Spanish Economic

Environment’’ motivates our investigation of earnings

management practices in the Spanish environment. Sec-

tion ‘‘Research Design’’ describes the research design, and

the results are analyzed in ‘‘Analysis of Data’’ Section.

Section ‘‘Discussion’’ concludes the paper.

Truthfulness and the Ethics of EarningsManipulation in Accounting

If to be taken as objective, communication must respond to

reality. However, in the last years, the business environ-

ment has learned that communication should be treated

with caution.

Today’s business environment is trying to grapple with a

painful past of economic scandals, fraud, and abuse of rules

and principles. In the light of such events, the trust between

individuals was affected. Being an essential feature of

correct communication (as Kant argued), truth-telling and

ethics must provide the blueprint for the future. Both ethics

and truthfulness must be placed in the context of human

relationships (Mele 2009), as individuals’ thoughts about

economic reality can become norms partially linked to how

the world is.

The matter of truth and ethics in accounting is a com-

plex one. Despite the fact that it was extensively approa-

ched in philosophy, and economics, truthfulness is viewed

as an appealing concept with various nuances; depending

on the individual’s concern with ethics, morality, and the

commitment with which they perform their tasks.

Empirical studies like those conducted by Kirkham

(1997) revealed significant disputes regarding the nature of

the philosophical problem of truth. For instance, McKernan

and O’Donnell (2002) concluded that it is better not to

engage in any search for the meaning of truth in accounting.

Shapiro (1997) adds that no scientific method will permit

anyone to discover or observe absolute accounting truth.

Defined as ‘‘an understanding of truth’’ (Rescher 2007),

it is important to assess the truthfulness concept since

‘‘truth and depth, not practical usefulness, power, or con-

sensus, have the last word’’ in the social practice of

accounting (Bunge 1996). Ueno (1948) defines truthfulness

as that in which ‘‘there has to be no manipulation’’ (p. 5),

while Kurosawa (1979) regarded it as similar to being

‘‘fair.’’

Truthfulness, unlike the truth, depends on the will.

Therefore, truthfulness has to do with the agreement

between our statement and our beliefs. In the case of truth,

the emphasis is on the relationship between our statements

and the facts to which they refer, as Kant asserted.

Bayou et al. (2011) argued that the question of true

accounting created a problem that the accounting

profession considered to be largely a technical, economic

measurement matter, ignoring its ethical ramifications. In

this regard, Bayou et al. (2011), using McCumber (2005)

work on the question of truth, concluded that accounting

truth inescapably has a significant ethical dimension.

The issue of truthfulness in accounting should be a

helpful tool used for assessing social relationships or

mediating human affairs. Ethics, on the other hand, directs

human actions and provides the basis to develop profes-

sional behavior.

When manipulating accounting information, both

truthfulness and ethics concur. Moreover, when discussing

acceptance or rejection of such practices, scholars use the

argument of truthfulness or truth (Beaudoin et al. 2014;

Marsh 2013). In this respect, the emphasis is on the

rightness or wrongness of individual actions. Popularly,

scholars make reference to false, misleading or fraudulent

financial reporting as if there could exist absolute true, non-

fraudulent, non-misleading financial reporting.

Since there are many ways to describe reality, to think

appropriately about truthfulness and ethics in accounting is

a challenge. Our claim is that, accounting should faithfully

represent the economic reality, and should not mislead.

Only when the information provided by accounting is not

false, misleading or fraudulent can it be inferred that it is

somehow true. Assessed under a technical view, truthful-

ness can be defined by its qualitative characteristics such as

reliability, neutrality or representational faithfulness.

Concerning the quality of communicative relationships

between managers and shareholders in the light of con-

flicting interests (i.e., compensation, insider trading, turn-

over, and management buyouts), the ethics of accounts

manipulation provides interesting discussions regarding the

acceptance of such practices. Moreover, when considering

the ethicality or truthfulness of certain accounting prac-

tices, the importance of situating (as McCumber 2005

approached it), should be taken into consideration.

Under such view, the accounting construction of what is

considered to be the truth is based on a certain framework,

generally accepted, as a norm of good practices in society,

respecting both the spirit and the letter of the law. Doyle

et al. (2003) broke down the difference between GAAP and

non-GAAP earnings, and explained the cases where dis-

cretion is not legitimate. In this respect, Doyle et al. (2003)

associated non-GAAP earnings reporting with opportunis-

tic earnings management. As such, a perfectly legitimate

‘‘discretion can be found in firms that are telling the truth

within the framework of Generally Accepted Accounting

Principles’’ (Parfet 2000).

Defined as psychological projections onto the world,

norms have the potential to help accountants to enhance

truthfulness and ethics, as Bunge (1996) concluded: ‘‘Thou

shalt search for the truth, pursue it wherever it may lead,

Truthfulness in Accounting: How to Discriminate Accounting Manipulators from Non-manipulators

123

Author's personal copy

and communicate it to whoever may be interested in it.’’

On the other hand, both truthfulness and ethics can help

individuals and society to act in such a way as to commit to

maxim.

One particular aspect of business ethics is the high

information asymmetry between management and the users

of accounting information, where usually the former has

information that it keeps from the other side. Sometimes,

the information disclosed is simply not presented according

to economic reality.

Dye (1988) rationalizes that manipulative behavior is

possible due to external and internal demands for such

behavior. In this respect, the external demand follows from

the capital market’s need to price the company. Due to

external demand, managers often apply the type of rea-

soning expounded in utilitarian rather than in deontological

theories of ethics. Moreover, there may be circumstances in

which the utilitarian approach does not require any moral

considerations (MacIntyre 1981, pp. 14–15; Williams

1985, p. 75). On the other hand, the internal demand comes

from the principal–agent relationship (Jensen and Meck-

ling 1976).

Analyzed by Kreps (1990, p. 745), the behavior of

manipulators can be explained through the actions of such

individuals who are engaging in manipulation and ‘‘would

break their word or engage in misrepresentation under the

right circumstances.’’ Ronen and Yaari (2010), described

the manipulation of earnings as a deliberate action to

influence reported earnings and their interpretation. Also

defined as non-truth-telling, earnings management prac-

tices are marked as pernicious by Ronen and Yaari (2010)

similar to DePree and Grant (1999) or Kaplan (2001a, b).

In this respect, earnings manipulation fits in with the

general conception that such activities involve manipula-

tion, lack of ethicality, lack of truthfulness, and misrepre-

sentation (Shafer 2002; Demski 2003).

Based on the results documented by Francis et al.

(2003), reported earnings numbers are more closely asso-

ciated with prices when compared to cash flow or sales.

Therefore, when investors want to forecast future cash flow

or assess their risk, their focus is on reported earnings.

Being an important performance measure, earnings are

often found to be the object of manipulation (Healy and

Wahlen 1999; Miller and Bahnson 2002), given the fact

that: (a) Sometimes the accounting policies enable a

company to have a choice from a menu of accepted

treatments (Schipper 1989; Apellaniz and Labrador 1995;

Bowen et al. 2002). The manipulation of earnings occurs

when managers exercise opportunistic discretion over

earnings with the goal of achieving self-centered objectives

(Scott 2003), or reaching a ‘‘desired number instead of

pursuing some sort of protocol to produce a number that

gets reported regardless of what some analysts predict’’

(Miller and Bahnson 2002, p. 184); (b) Certain entries in

the accounts require an unavoidable degree of estimation,

judgment, and prediction (He and Yang 2014), discretion

that could lead to documented earnings manipulation using

items like: depreciation (Bishop and Eccher 2000); asset

write-offs (Riedl and Srinivasan 2006); separation of con-

sistent earnings from transitory ones (Lin et al. 2006) or

restructuring charges (Bens and Johnston 2009); (c) Man-

agers have the flexibility of timing the recognition of rev-

enues and expenses (i.e., timing the sales of assets in order

to manipulate earnings) (Bartov 1993; Gunny 2005);

(d) Managers have the flexibility of structuring transactions

to alter a financial report either to mislead some stake-

holders or to influence contractual outcomes (Healy and

Wahlen 1999); (e) Managers have the possibility of using

investment and production decision to manage earnings, as

documented by previous empirical studies conducted by

Roychowdhury (2006) or Zang (2012).

Ueno (1948) regards truthfulness and accounts manip-

ulation as antithetical. Further, the lack of truthfulness was

regarded as antithetical to truthfulness, referring to terms

like: false, misleading or fraudulent.

Being part of accounts manipulation, earnings manage-

ment practices are regarded by the great majority of

scholars as being unethical (i.e., Johnson et al. 2012; Huang

et al. 2008; Vinciguerra and O’Reilly-Allen 2004; Kaplan

2001a). Their main arguments are based on the fact that

earnings manipulation makes the company value unclear.

Also, earnings management activities are viewed as

eroding the trust between shareholders and managers and

harming the quality of financial reporting. Other scholars

regarded accounts manipulation as being intolerable (i.e.,

Loomis 1999; Grant et al. 2000), immoral (Solomon 1993)

or against the principle of justice (Rawls 1972).

On the other hand, there are scholars who find certain

earnings management practices as being acceptable (Arya

et al. 2003; Parfet 2000) and others who documented a

higher acceptance of such practices (Merchant and Rock-

ness 1994; Bruns and Merchant 1990). For instance, Arya

et al. (2003) argued that ‘‘earnings management and

managerial discretion are intricately linked to serve mul-

tiple functions; accounting reform that ignores these

interconnections could do more harm than good’’ (p. 111,

emphasis added). Parfet (2000) distinguishes between good

and bad earnings management practices. In this respect,

when managers generate stable financial performance

though earnings management activities, such practices are

considered as ‘‘good earnings management.’’ On the other

hand, ‘‘bad earnings management’’ practices can be found

when managers generate misleading accounting entries or

extend estimates beyond realistic limits.

Merchant and Rockness (1994) documented that earn-

ings management practices implemented for self-interested

A. B. Vladu et al.

123

Author's personal copy

purposes are perceived as being less ethical compared to

earnings management practices for the benefit of the

company. Bruns and Merchant (1990) documented empir-

ical results that they assessed as ‘‘frightening’’ based on the

high rate of acceptability of such practices in the business

context.

Prior empirical research documented that ethical issues

can limit business practices characterized by a lack of

truthfulness (i.e., Chung et al. 2005; Greenfield et al. 2008;

Kaplan 2001b). Empirical studies like those conducted by

Elias (2002), Choi and Jinhan (2011) or Shafer (2013)

characterized the relationship between ethics and earnings

manipulations as an inverse relationship. For instance,

Elias (2002) found a negative relationship between focus

on short-term gains and the ethical perception of earnings

manipulation. Choi and Jinhan (2011) documented that

commitment to business ethics has perpetuating effects on

future financial reporting quality. Shafer (2013) docu-

mented that perceptions of the organization ethical climate

were significantly associated with the beliefs over the

importance of corporate ethics responsibility, which was

also associated with ethical judgments and behavioral

intentions of accountants regarding accounting and earn-

ings manipulation.

Summarizing the above, the opinions on the accept-

ability of earnings manipulation vary, but even so, are very

often perceived as reprehensible.

Merchant and Rockness (1994) concluded that earnings

management practices raised the most important ethical

issues facing the business profession.

Earnings Management and the Spanish EconomicEnvironment

According to Leuz et al. (2003) earnings management is a

pervasive corporate phenomenon, less prominent in coun-

tries with developed equity markets, dispersed ownership

structures, strong investor rights, and legal enforcement.

The empirical study conducted by Leuz et al. (2003)

grouped countries under analysis in three clusters. Among

those, Spain was part of the insider economies with weak

legal enforcement cluster. The results documented sig-

nificant differences in the magnitude of earnings man-

agement practices across analyzed clusters. The cluster

that comprised the analysis of Spain exhibited signifi-

cantly higher earnings management compared to the other

two clusters.

Other studies documented that certain practices of

earnings management (e.g., income smoothing or payout-

driven income decreasing) are typical for code-law coun-

tries with less-developed stock markets and lower disclo-

sure levels such as Spain (Azofra et al. 2003).

Nobes (1998) previously approached the factors influ-

encing the differencing in financial reporting and argued

for both the strength of equity markets and the degree of

cultural dominance as being among the most important

ones.

La Porta et al. (1998) included Spain in the ‘‘French

family’’ within the code-law tradition and argued for

comparison with two other code-law ‘‘families’’ (e.g.,

Scandinavian and German), the ‘‘French family’’ countries

giving shareholders and creditors the weakest protection.

Confirming this trend, Hope (2003) placed Spain in the last

position among 22 countries regarding legal enforcement

and disclosure level.

Based on the view of Callao et al. (2007), Spain is a

country where the legal system is based on Roman law

with accounting rules enshrined in legislation.

Being part of the Continental European accounting

system, the Spanish accounting rules have taken the form

of companies’ legislation, the General Chart of Accounts

with its implementing regulations and also other Securities

Market and Bank of Spain legislation.

When assessing the differences between Spain and other

developed countries (e.g., USA); the institutional discrep-

ancies are among the most important ones. For instance,

while in USA, the stock market is highly developed, Spain

comprises far fewer developed stock markets, with far

fewer firms listed on the interconnected market. Banks are

the major source of business finance in Spain (Ojah and

Manrique 2005) sustaining important incentives for

opportunistic behavior of managers (DeFond and Jiam-

balvo 1994).

Important differences can be found both in legal and

judicial enforcements (La Porta et al. 1998), confirming the

central role of enforcement mechanisms over financial-re-

porting practices (Nobes 1998; Burgstahler et al. 2006).

Based on the results documented by Pindado and de la

Torre (2006), Spanish CEOs managing quoted firms face

little control by shareholders. Their evidence suggests that

managers face few restrictions to maintain their informa-

tive advantage over different creditors and shareholders.

Research shows that social norms and specific cultural

practices seem to drive the assessment about ethicality, and

morality of people and their actions (Appiah 2008; Knobe

and Nichols 2008). Building on this evidence, Lara et al.

(2006) discussed potential incentives encouraging conti-

nental European managers to engage in earnings manage-

ment, such as: existing links between reported income and

current payouts to different stakeholders; the pecking order

theory or the less-pronounced market pressure to manage

earnings upward.

All above references support the possibility of high

levels of manipulation in insider economies, with weak

legal enforcement and low levels of disclosure.

Truthfulness in Accounting: How to Discriminate Accounting Manipulators from Non-manipulators

123

Author's personal copy

In terms of incentives for engaging in earnings man-

agement practices, various differences can be found,

between countries with highly developed financial markets

and those with fewer developed stock markets. Among

them, we can summarize the following: the reluctance of

managers to make direct disclosures of private information

to shareholders based on both institutional and legal con-

straints (Schipper 1989); lack of credible channels for

appropriate disclosures (Demski and Sappington 1987);

communicating proper knowledge regarding firms’ supe-

rior earnings prospects to investors (Alissa et al. 2013);

differentiating from inferior prospects in the capital mar-

kets (Chaney and Lewis 1995); obtaining a higher valua-

tion for the shares (Barth et al. 1999; Baker et al. 2009);

obtaining a lower cost of capital (Francis et al. 2004);

meeting earnings thresholds (Daniel et al. 2008); man-

agement–compensation plans (Healy 1985; Holthausen

et al. 1995), debt contracts (DeFond and Jiambalvo 1994);

avoiding decreases and losses (Burgstahler and Eames

2003).

Research Design

Despite being the most used models to detect earnings

management, much attention has been paid to both relative

and absolute accuracies of accrual models (Dechow et al.

1995; Guay et al. 1996; Thomas and Zhang 2002; Dechow

et al. 2010; DeFond 2010). Mainly their ability to identify

Type I and II errors was and still is under scrutiny (Dechow

et al. 2012). Another important limit consists of the fact

that almost all techniques used so far are based on the

assumption that unexplained or abnormal accruals repre-

sent explicit earnings management. One can also argue that

those abnormal accruals can be poor quality earnings.

Our paper is an empirical exercise developed with the

goal to set the tools to discriminate manipulator from non-

manipulator firms for the case of the Spanish market.

Taking into account the advantages of ratio analysis, our

model comprises a simple and cost-effective way to dis-

criminate manipulators from non-manipulators, using only

two years of data. Previous research documented ratio

analysis as being useful in detecting earnings management

practices (Beneish 1999; Jansen et al. 2012).

On the other hand, ratio analysis can also be susceptible

to faulty interpretation and is potentially confusing (Alt-

man 1968). The challenge regarding ratio analysis is to

combine several measures into a meaningful predictive

model. The most important questions are which ratios

should be used and what weights should be attached to

those ratios to discriminate manipulative from non-

manipulative behavior. In order to fill this gap, we con-

ducted this empirical study. In this respect, two relevant

research questions arise:

(1) Which accounting ratios can be used as influential

ones to distinguish between manipulator versus non-

manipulator companies?

(2) What should their relative importance be?

After careful consideration of the nature of the problem

and the purpose of the paper, two different statistical

methodologies were used: (i) Linear Discriminant Analysis

(hereafter LDA), and (ii) Probit model. Both of these sta-

tistical methodologies are grounded in a multivariate

approach as encouraged by Altman (1968), implying a

natural extension for a univariate analysis.

While the Probit model deserves no additional expla-

nations, LDA was preferred based on three arguments.

First, this technique considers an entire profile of charac-

teristics common to the relevant firms and the interaction of

these properties. Second, since this study is concerned with

only two groups, LDA is useful in terms of reduction of the

space dimensionality. Finally, LDA is useful in terms of

classification problems when analyzing the entire variable

profile of the object simultaneously rather than sequentially

by examining its individual characteristics. Since financial

ratios, by their nature, have the effect of deflating statistics

by size, the size effect is eliminated.

Prior research indicates that certain variables are sig-

nificant indicators when assessing manipulative behavior

(Schilit 2010; Mulford and Comiskey 2002; Beneish 1999).

As a result, a list of 12 explanatory variables (ratios) was

compiled for evaluation. The variables were selected based

on the results documented in the literature and potential

relevance to our study.

In order to obtain the final profile of variables, we used

similar procedures to those in Altman (1968), consisting of

(a) Observation of the statistical significance of various

alternative functions comprising the determination of the

relative contributions of each independent variable;

(b) Evaluation of intercorrelations between the relevant

variables; (c) Observation of the predictive accuracy of the

various profiles; and (d) Judgment of the analyst.

Statistical Methodology

Since LDA and Probit Models are the appropriate tech-

niques to classify observations between groups, the next

subsections give a brief description of their salient features.

In addition, Multivariate Analysis of Variance (hereunder

MANOVA) was used in order to detect those independent

variables with the highest discriminant power.

A. B. Vladu et al.

123

Author's personal copy

Multivariate ANOVA (MANOVA)

Assume a sample coming out from two possible different

groups (manipulators and non-manipulators), where each

observation has different variables (accounting ratios).

The question is to what extent the two groups are dif-

ferent regarding these variables. This technique is partic-

ularly useful in identifying the group of variables

(accounting ratios) that exhibit a different performance

between manipulators and non-manipulators. Variables not

presenting different profiles between groups are of little use

to discriminate observations.

Linear Discriminant Analysis (LDA): Two-Group

Case

LDA technique attempts to derive a linear combination of

variables (accounting ratios) that maximizes the separation

between two groups. The discriminant power consists in

identifying the vector that best separates individual obser-

vations coming from manipulator versus non-manipulator

groups. When assessing the discriminant accuracy of the

model, two alternatives were proposed, consisting of the

classification matrix.

Since our study is a multigroup case, we used the

classification chart presented in Table 1, where main

diagonal accounts for both correct classification and for the

classification errors.

The actual membership is equivalent to the a priori

grouping as in Beneish (1999) where the model attempts to

correctly classify these companies. When new companies

are classified, the nature of our model is predictive.

PROBIT and LOGIT Models

Models for binary choice are a class of econometric models

where the ‘‘dependent’’ variable is qualitative, assuming

only two values (0/1). It is traditional to quantify a success

with 1 and a failure with 0. In the present case, manipulator

and non-manipulator firms will be set equal to 1 and

0-respectively.

Accounting Variables Indicating Earnings

Manipulation

This study comprises explanatory variables from positive

accounting theory (Watts and Zimmerman 1986) and from

accruals research (Healy 1985; Jones 1991; Dechow et al.

1995). Other variables were selected based on the inves-

tigation work conducted by Mulford and Comiskey (2002)

and Schilit (2010). The explanatory accounting variables

were computed based on financial accounting disclosed by

the examined companies. As in Beneish (1999), some of

the variables were designated as indices, in order to capture

distortions that could arise from manipulation, by com-

paring financial statement measures in the year of the first

reporting violation to the year prior to that.

In order to estimate our models, a list of firms identified

as manipulators (12) (including the year of the manipula-

tion) or non-manipulators (59) was used. In addition,

accounting information for analyzed firms was also pro-

vided in order to calculate a set of independent variables

(12 in total). Those variables were used to capture different

dimensions of earnings manipulation.

From the perspective of the guidance from the literature,

we summarized a list of 12 independent variables. It is

worth mentioning that period t found in the definition of the

variables, corresponds to the year of manipulation. Below,

a brief explanation of their meanings and expected signs in

the regressions is offered, as follows:

1. Receivables index (RI) RI is the ratio of accounts

receivables in sales in the first year in which earnings

manipulation is uncovered (year t) to the corre-

sponding measure in year t - 1. RI was analyzed

due to the fact that it gages whether receivables and

revenues are in or out-of-balance in two consecutive

years. RI was documented by Beasley et al. (2000)

as one of the most misstated asset accounts on the

balance sheet. In this regard, a large increase in

receivables can be the result of a change in credit

policy used to increase sales. This can happen due to

increased competition or revenue inflation. A posi-

tive association with the probability of manipulation

is expected, when receivables take on a dispropor-

tionally large value relative to sales for the year of

manipulation. Allowances for doubtful accounts are

conflated into the receivables index.

2. Inventories index (II) II is the ratio of inventories in

cost of goods sold in year t to the corresponding

measure in previous year. A disproportional increase

in inventories could indicate possible manipulation

Table 1 Classification chart

Predicted group

Actual Group Manipulator Non-manipulator

Manipulator A B

Non-manipulator C D

Source Authors’ projection

Truthfulness in Accounting: How to Discriminate Accounting Manipulators from Non-manipulators

123

Author's personal copy

by misleadingly changing its value. A positive

association is expected.

3. Gross margin index (GMI) GMI is the ratio of gross

margin in year t - 1 to gross margin in year t. A

value higher than 1 indicates that gross margins have

deteriorated. This could be interpreted as a negative

sign for firm’s prospects (Lev and Thiagarajan

1993). Since companies with poor prospects are

more likely to engage in earnings manipulation, a

positive sign is expected (Kellogg and Kellogg

1991). Deterioration in Gross Margins increases the

possibility of engaging in earnings manipulation.

4. Sales growth (SG) SG is the ratio of sales in year t to

sales in previous year (t - 1). Growth per se does

not have to be regarded as a manipulative even.

Nevertheless, according to professional bodies like

the National Association of Certified Fraud Exam-

iners (1993), growth companies must be treated with

caution. Given the need to achieve earnings targets

which are higher compared to other types of

companies, growth companies are more susceptible

to commit fraud. Moreover, since losing stock prices

or decelerating growth can be costly (Loebbecke

et al. 1989; Fridson 1993), growth companies face

important incentives to manipulate earnings. A

positive relationship is expected based on the fact

that a reduction in sales would encourage manage-

ment to engage in manipulation.

5. Depreciation index (DI) DI is the ratio of depreci-

ation in year t - 1 to the corresponding measure in

year t. A significant change in depreciation is

associated with a change in the estimates of assets

lives. Those firms reducing the rate of depreciation

are susceptible of manipulation by aggressively

increasing the useful lives of company’s assets. A

positive relationship is expected between DI and the

probability of manipulation. This variable did not

enhance either the specification of our model or alter

the magnitude of the significance of the coefficients

of the other explanatory variables used.

6. Discretionary expenses index (DEI) DEI is the ratio

of discretionary expenses in year t to discretionary

expenses in t - 1. Reducing discretionary expenses

in the year of manipulation is done with the scope of

improving the firm’s prospects aggressively (Lev

and Thiagarajan 1993). Such demarche used for

manipulative purposes has no connection to the

economic reality. A positive association is expected

between DEI and the probability of manipulation.

7. Leverage index 1 (LI1) LI1 is the ratio of current

debt to total assets in year t relative to the

corresponding measure in the previous year. When

the value of LI 1 is higher than 1, an increase in the

leverage index is obtained. High leverage could

encourage earnings manipulation through its effect

on debt covenants with the firm’s (current and

future) counterparties (Beneish and Press 1993). A

positive sign in the regression is expected between

LI1 and the probability of manipulation.

8. Leverage index 2 (LI2) Idem to LI1 but standardized

by Sales. A positive association is expected, between

LI2 and the probability of manipulation.

9. Asset quality (AQ) AQ is the ratio of asset quality in

year t relative to asset quality in the previous year.

AQ measures the proportion of total assets for which

future benefits are potentially less certain (e.g., assets

realization risk analysis suggested by Siegel 1991).

A value of AQ higher than 1 indicates that the firm

has potentially increased its involvement in cost

deferral (Beneish 1999). Since that part of the

increase is possible to be attributable to acquisitions

involving Goodwill, the manipulators sample was

assessed in terms of acquisitions. Since this is not the

case for our manipulators sample, we predict a

positive relationship between AQ and earnings

manipulation.

10. CFO index 1 (CFO1) A fall in CFO relative to Net

Income indicates an increase in the proportion of

accrual relative to Net Income. This provides more

room to manipulate. Therefore, a positive associa-

tion is expected, between CFO1 and earnings

manipulation.

11. CFO index 2 (CFO2) Idem to CFO1 but standard-

ized by Total Assets. Similar to CFO1 a positive

sign is expected between CFO2 and earnings manip-

ulation.

12. Sales index (SI) SI is the ratio of sales in year t to

CFO in year t, relative to the same measure in

previous year (t - 1). A disproportionate increase in

sales not mapped into CFO could indicate an

intended and aggressive inflation with the purpose

of misleading in respect of the underlying economic

performance (Mulford and Comiskey 2002). There-

fore, a positive sign of this variable is predicted, in

the case in which a manipulation case is indicated.

Dataset Construction

In this study, companies that make use of earnings man-

agement practices are regarded as manipulators. On the

other hand, companies that do follow the ‘‘good practices’’

are regarded as non-manipulators. The central idea behind

it is simple: if companies engage in earnings management

activities, their attitude toward ethicality, and truthfulness

is not severe, and vice versa.

A. B. Vladu et al.

123

Author's personal copy

The final dataset consists of 12 manipulators and 59

non-manipulators matched by industry, and year of

manipulation (71 data points). The financial industry was

discarded because of its specific characteristics which are

endowed with the industry‘s own accounting and financial

rules.

The sample of manipulators consists of firms that have

been targeted by the Spanish Stock Exchange supervisor

for allegedly overstating annual earnings. The external

validity of the results rests on the assumption that this

supervisor has correctly identified firms that managed their

earnings. Our assumption seems reasonable since this

supervisor pursues only cases involving significant inci-

dences of earnings management practices.

All companies examined in our study are listed on the

Spanish Stock Exchange, tier 1, and for period 2005–2012.

As asserted above, these data were obtained from CNMV,

the Spanish stock exchange supervisor. There is one firm

identified as belonging to the first group that is outside the

sample because it does not present information for the year

previous to the event. In addition, there are two firms not

considered in the control group in particular years based on

the lack of financial information.

It is worth mentioning that since information regarding

the CFO starts from 2007, nine observations of the dataset

were discarded when variables including CFO in their

calculation were considered. In this case, the dataset has 62

data points (10 manipulators and 52 non manipulators).

Finally, since several of the independent variables are

indices with a small denominator, we winsorized the

dataset at 5 and 95 % percentiles for each variable.

In addition, some of the balance sheet items assume zero

value in different years affecting the calculation of the

independent variables when they appear in the denomina-

tor. In this case, we put 1 as is suggested by Beneish

(1999).

Analysis of Data

MANOVA and LDA

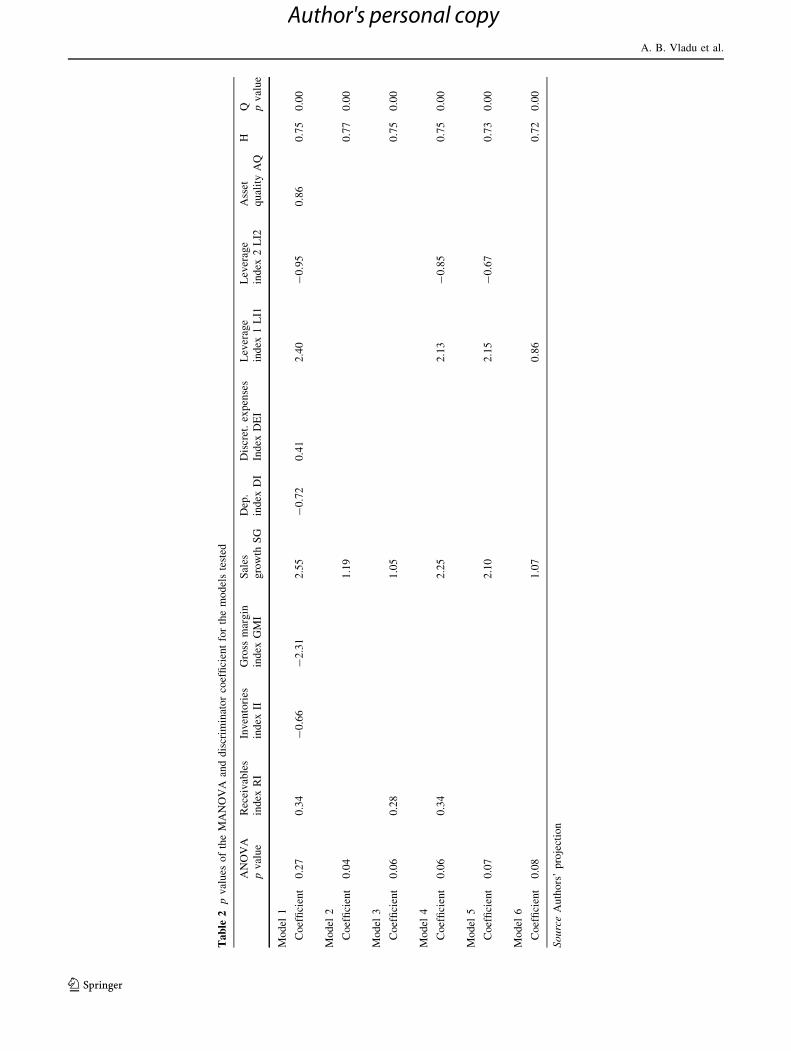

Among all possible combinations of variables (there are

512 possible models); MANOVA was used to select those

arrangements showing the greatest discriminatory power.1

Table 2 reports the p values of the MANOVA and the

discriminator coefficient for the complete model (a model

including all the accounting variables) and for five models

showing the smallest p value from the MANOVA test.

Based on the values presented in Table 2, some

important conclusions can be drawn. Starting with our

complete model (including RI, II, GMI, SG, DI, DEI, LI1,

LI2, and AQ) we can assert that the p value of the

MANOVA test (e.g., 0.27) is not significant. In this respect,

we can conclude that not every accounting ratio can act as

a discriminator used to identify companies that do manip-

ulate their earnings.

When analyzing the secondmodel (presented in Table 2),

the p value of the MANOVA test (e.g., 0.04) shows that this

model is significant in predicting a differential profile

betweenmanipulators and non-manipulators. In this respect,

the SG ratio can be used to discriminate between manipu-

lators and non- manipulators. The third model is also found

to be significant (p value of the MANOVA test: 0.06).

Therefore, RI and SG ratios are found to be significant in

discriminating manipulators from non-manipulators. Mod-

els 5 and 6 introduce as a significant discriminator the LI1

(p value of the MANOVA test in Model 5: 0.06 and p value

of the MANOVA test in Model 6: 0.07).

According to the results presented in Table 2, it seems

that the critical explanatory variables identifying a

manipulator are: (1) Receivables index; (2) Sales Growth

and (3) Leverage index 1 (LI1, e.g., current debt/total

assets). All those explanatory variables show the expected

sign (e.g., positively associated).

LI2 (e.g., leverage index 2: current debt to sales)

deserves a special comment since it seems to act as a

discriminator variable according to the results presented in

Table 2, but its sign is opposite to the expected one (neg-

atively associated).

The Hit ratio (H) takes on values between 72 and 77 %,

showing that the models are performing well in matching

the actual group of companies with the one expected from

the Z-scores. The lowest value obtained for the Hit ratio

was for Model 6 (including accounting ratios like SG and

LI1), while the highest value is obtained for Model 2 (in-

cluding SG as the accounting ratio). Finally, the Q test

shows strong evidence in favor of our models. The

assignment of a firm to a particular group is by no means

made randomly.

Table 3 presents the major statistic regarding Z-scores

for our six models including the region of ignorance

(Altman 1968). In this respect, our models correctly clas-

sify a non-manipulator firm when its Z-score is lower than

the minimum of the ‘‘region of ignorance’’ and correctly

classify it as a manipulator when its Z-score is above the

maximum of the same region. When Z-scores belong to the

region of ignorance, the discriminant power of the models

is undermined. The ‘‘region of ignorance’’ is that range of

Z-scores where misclassifications are observed. Hence, it is

desirable to establish a guideline for classifying firms in the

‘‘region of ignorance.’’

1 Since there are 9 independent variables, the total number of

possible models is 512.

Truthfulness in Accounting: How to Discriminate Accounting Manipulators from Non-manipulators

123

Author's personal copy

Table

2pvalues

oftheMANOVA

anddiscrim

inatorcoefficientforthemodelstested

ANOVA

pvalue

Receivables

index

RI

Inventories

index

II

Gross

margin

index

GMI

Sales

growth

SG

Dep.

index

DI

Discret.expenses

Index

DEI

Leverage

index

1LI1

Leverage

index

2LI2

Asset

qualityAQ

HQ pvalue

Model

1

Coefficient

0.27

0.34

-0.66

-2.31

2.55

-0.72

0.41

2.40

-0.95

0.86

0.75

0.00

Model

2

Coefficient

0.04

1.19

0.77

0.00

Model

3

Coefficient

0.06

0.28

1.05

0.75

0.00

Model

4

Coefficient

0.06

0.34

2.25

2.13

-0.85

0.75

0.00

Model

5

Coefficient

0.07

2.10

2.15

-0.67

0.73

0.00

Model

6

Coefficient

0.08

1.07

0.86

0.72

0.00

So

urc

eAuthors’projection

A. B. Vladu et al.

123

Author's personal copy

According to the results presented in Table 3, the min-

imum value obtained for the Z-score of the complete model

was -0.80, while the maximum value was 5, 67. The range

value for the centroids was 1.29. The minimum of the

‘‘region of ignorance’’ was 1.40, while the maximum was

4.59, with a range of 3.19. Model 2 and Model 3 obtained a

similar value for the minimum of Z-score (e.g., 0.11),

while the maximum values were higher in the case of

Model 3 (e.g., 2.86—Model 2; 5.67—Model 3).

In the case of the second model, the values obtained for

the minimum and maximum of the ‘‘region of ignorance’’

were similar to the minimum and maximum of the values

obtained for its Z-score.

The highest value of the Z-score was 7.16, obtained in

Model 4, when compared to the other models. Model 4 also

exhibited the highest maximum for the ‘‘region of igno-

rance’’ (6.49). The centroids value for manipulators was

4.35 in Model 5 and 3.58 in non-manipulators. In the last

model tested, the value of the centroids was only 2.59 for

manipulators and 2.05 for non-manipulators, with a range

of only 0.54, the second lowest value obtained after Model

2.

Summarizing, the lowest value obtained for the mini-

mum of the ‘‘region of ignorance’’ is found in the second

model (0.11), while the highest among maximum values is

obtained as we asserted earlier in Model 4 (6.49).

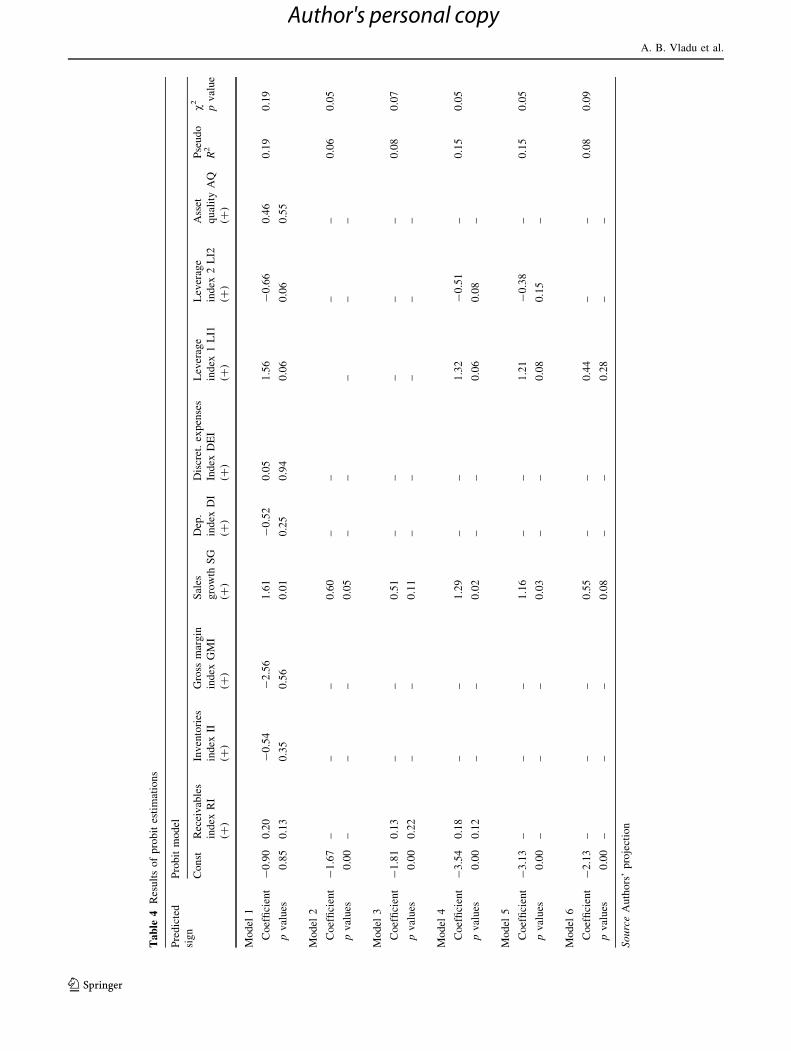

PROBIT Model

As a robustness check, the results of The Probit estimations

for each of the six models are reported in Table 4. Each of

the six models was assessed in terms of descriptive

validity.

Consistent with the results obtained from the discrimi-

nate analysis conducted, the Models 2–6 present descrip-

tive validity (with p values of v2 between 0.05 and 0.09). Inthis respect, Models 2 and 4 have the same p value of v2 of0.05, while Model 5 obtained a value of 0.06. The p value

for v2 in the case of Model 6 is 0.09.

The p value of v2 in our complete model (Model 1) is

0.19 which is consistent with previous results obtained.

Further, in most of the cases, the estimated coefficients

show signs in accordance with the theory (e.g., positively

associated), and they are statistically significant.

Accordingly, the explanatory accounting ratios are

found to be significant in terms of manipulation indication

based on the discriminate analysis conducted (e.g.,

Receivables Index, Sales Growth, and Leverage Index 1)

are also found to be significant in terms of manipulation

indication, according to Probit estimations. Finally, as was

mentioned previously, Leverage Index 2 (LI2) shows a

negative and significant coefficient, an unexpected phe-

nomenon since it is the opposite of the theory.

Discussion

As previously mentioned, since information regarding the

CFO is available starting from the year 2007, it entails a

13 % reduction in the sample size, which undermines the

robustness of the estimations. Nevertheless, our results do

not suffer any changes when CFO variables are included.

Therefore, below we present the results considering the

larger dataset (the results from the smaller dataset are

available on request).

Among all possible combination of variables, MAN-

OVA is used to select those arrangements showing the

greatest discriminatory power. This is a fundamental step

in determining which variables significantly differentiate a

manipulator from a non-manipulator firm.

Based on the results presented in Table 2, it seems that

the critical explanatory variables identifying a manipulator

are: (a) Receivables index: when it increases; (b) Leverage

index 1 (e.g., current debt/total assets): when it increases;

(c) Sales Growth: when it decreases.

All above explanatory variables show the expected sign

(e.g., positively associated).

Table 3 presents the major statistic regarding Z-scores

for the six models including the region of ignorance (Alt-

man 1968). In this respect, our models correctly classify a

non-manipulator firm when its Z-score is lower than the

minimum of the ‘‘region of ignorance’’ and correctly

Table 3 Z-scores: key

parametersMin Max Centroids Region of ignorance

Manipulator Non-manipulator Range Min Max Range

Model 1 -0.80 5.67 3.23 1.94 1.29 1.40 4.59 3.19

Model 2 0.11 2.86 1.68 1.25 0.43 0.11 2.86 2.76

Model 3 0.11 5.67 2.14 1.52 0.62 0.37 3.85 3.48

Model 4 1.31 7.16 4.99 3.97 1.02 3.70 6.49 2.79

Model 5 1.32 5.67 4.35 3.58 0.78 2.67 5.55 2.89

Model 6 0.62 4.55 2.59 2.05 0.54 1.52 4.55 3.03

Source Authors’ projection

Truthfulness in Accounting: How to Discriminate Accounting Manipulators from Non-manipulators

123

Author's personal copy

Table

4Resultsofprobitestimations

Predicted

sign

Probitmodel

Const

Receivables

index

RI

Inventories

index

II

Gross

margin

index

GMI

Sales

growth

SG

Dep.

index

DI

Discret.expenses

Index

DEI

Leverage

index

1LI1

Leverage

index

2LI2

Asset

qualityAQ

Pseudo

R2

v2

pvalue

(?)

(?)

(?)

(?)

(?)

(?)

(?)

(?)

(?)

Model

1

Coefficient

-0.90

0.20

-0.54

-2.56

1.61

-0.52

0.05

1.56

-0.66

0.46

0.19

0.19

pvalues

0.85

0.13

0.35

0.56

0.01

0.25

0.94

0.06

0.06

0.55

Model

2

Coefficient

-1.67

––

–0.60

––

––

0.06

0.05

pvalues

0.00

––

–0.05

––

––

–

Model

3

Coefficient

-1.81

0.13

––

0.51

––

––

–0.08

0.07

pvalues

0.00

0.22

––

0.11

––

––

–

Model

4

Coefficient

-3.54

0.18

––

1.29

––

1.32

-0.51

–0.15

0.05

pvalues

0.00

0.12

––

0.02

––

0.06

0.08

–

Model

5

Coefficient

-3.13

––

–1.16

––

1.21

-0.38

–0.15

0.05

pvalues

0.00

––

–0.03

––

0.08

0.15

–

Model

6

Coefficient

-2.13

––

–0.55

––

0.44

––

0.08

0.09

pvalues

0.00

––

–0.08

––

0.28

––

So

urc

eAuthors’projection

A. B. Vladu et al.

123

Author's personal copy

classify as manipulator when its Z-score is above the

maximum of the same region.

Accordingly, the explanatory accounting ratios found to

be significant in terms of manipulation indication based on

the discriminate analysis conducted (e.g., Receivables

Index, Sales Growth, Leverage Index 1) are shown to be

fundamental ratios in indicating manipulation also

according to Probit estimations (Table 4).

Conclusion

In this paper, we investigate how earnings manipulators

can be detected using financial statement ratios. The

empirical evidence in our paper is based on a sample of

companies manipulation of earnings of which was dis-

covered and a sample of companies known for following

the ‘‘good practices’’ in accounting for the period

2005–2012.

We extend prior research of ratio analysis used in the

context of earnings manipulation by combining it with

rigorous statistical technique, useful to distinguish manip-

ulator from non-manipulator companies.

Our results document significant predictive content of

the explanatory variables (e.g., accounting ratios) that take

into account the simultaneous bloating in asset accounts. In

this regard, our results document that receivables and

leverage have significant discriminatory power. Our find-

ings highlight that a prime characteristic of manipulators

was the higher growth in the value of explanatory variables

prior to periods during which manipulation is in force. The

context of earnings manipulation was the annual report.

Our evidence documents that the probability of manip-

ulation increases with the following: (1) unusual increase

in receivables; (2) increasing leverage; and (3) decrease in

sales. In addition, we have obtained several Z-scores that

can be used to assess the probability of a company

manipulating its accounts.

Given the results documented, we believe the systematic

association between earnings manipulation and financial

statement data to be of interest to both accounting scholars

and professionals. We regard our paper sheds light on a yet

under-explored facet driving accounting in the academic

debates on business ethics.

Regarded from an ethical perspective as morally repre-

hensible, earnings manipulation is not fair to users, and it

involves an unjust exercise of power. In this regard, such

practices used by manipulators tend to weaken the

authority of the regulators and supervisors. Our results

have specific implications for those whose main function in

an organization is to use financial data in the process of

decision making. The practical relevance of our findings is

important when building reliable models used to examine

companies that are conducive to decreasing earnings and

not only companies that overstate earnings. Such a

demarche may ultimately lead to analysis techniques that

better permit investors to evaluate firm performance.

The extent to which manipulators succeed in misleading

the users of financial information depends on the ability of

the latter to detect and unravel earnings manipulation.

In the light of previous documented financial scandals,

there is a stringent need for moral behavior and people of

moral integrity, willing to act in accordance with accepted

moral standards. As such, individual practitioners, profes-

sional associations, and accounting regulators should all

take steps to identify, and deter earnings management

practices, by developing specific tools to assess its exis-

tence and magnitude.

Our study has several important limitations. First, we

recognized the explored distortions as a result of manipu-

lation. On the other hand, in the period under analysis,

there were no significant changes in the firm’s economic

environment. Second, potential sampling errors can be

found, given the fact that part of the sample was con-

structed manually. Third, inherent bias in the process of

reducing the original set of variables to the best variable

profile is susceptible to be found (Altman 1968). Finally,

the sample size and the fact that the prediction models were

not tested out of sample to assess their accuracy can

comprise important limitations.

Our model regarded only Spanish listed firms, but fur-

ther research can extend this rather limited scope.

Future research can approach the association between

the failure of reason-based morality, and earnings manip-

ulation. In addition, a Kantian approach (Kant 1994)

regarding the organization can act as an adequate debate.

Committed to achieving common goals and moral com-

munities, a Kantian approach to the business environment

will regard the organization as other than merely a means

of achieving individual goals. Also, it will be interesting

for future research to assess the self-deception that man-

agers sometimes undertake to justify morally questionable

actions for the greater good of the company when the cost

of telling the truth is too high.

Given the economic and social consequences of their

actions, companies usually depend on the moral integrity of

their managers. In this respect, core values like truthfulness

or honesty in letter and spirit should be respected per se

and not only to avoid penal action.

References

Akerlof, G. A., & Shiller, R. J. (2009). Animal spirits. Princeton:

Princeton University Press.

Truthfulness in Accounting: How to Discriminate Accounting Manipulators from Non-manipulators

123

Author's personal copy

Alissa, W., Bonsall, S. B, I. V., Koharki, K., & Penn, M. W, Jr.

(2013). Firms’ use of accounting discretion to influence their

credit ratings. Journal of Accounting and Economics, 55,

129–147.

Altman, E. I. (1968). Financial ratios, discriminant analysis and the

prediction of corporate bankruptcy. The Journal of Finance,

23(4), 589–609.

Apellaniz, P., & Labrador, M. (1995). El impacto de la regulacion

contable en la manipulacion del beneficio. Estudio empırico de

los efectos del PGC de 1990. Revista Espanola de Financiacion

y Contabilidad, 24(82), 13–40.

Appiah, K. A. (2008). Experiments in Ethics. Cambridge, MA:

Harvard University Press.

Arya, A., Glover, J., & Sunder, S. (2003). Are unmanaged earnings

always better for shareholders? The Accounting Horizon,

17(Suppl), 111–116.

Azofra, V., Castrillo, L., & Delgado, M. M. (2003). Ownership

concentration, debt financing and the investment opportunity set

as determinants of accounting discretion: Empirical evidence

from Spain. Spanish Journal of Finance and Accounting, 115,

215–255.

Baker, T. A., Collins, D. L., & Reitenga, A. R. (2009). Incentives and

Opportunities to Manage Earnings around Option Grants.

Contemporary Accounting Research, 26(3), 649–672.

Ball, R. (2009). Market and political regulatory perspectives on the

recent accounting scandals. Journal of Accounting Research, 47,

277–323.

Barth, M. E., Elliott, J. A., & Finn, M. W. (1999). Market rewards

associated with patterns of increasing earnings. Journal of

Accounting Research, 37(2), 387–413.

Bartov, E. (1993). The timing of asset sales and earnings manipu-

lation. The Accounting Review, 68(4), 840–855.

Bayou, M., Reinstein, A., & Williams, P. F. (2011). To tell the truth:

A discussion of issues concerning truth and ethics in accounting.

Accounting, Organizations and Society, 36, 109–124.

Beasley, M., Carcello, J., Hermanson, D., & Lapides, P. (2000).

Fraudulent financial reporting. Accounting Horizons, 14(4),

441–455.

Beaudoin, C., Cianci, A. and Tsakumis, G. (2014). The impact of CFOs’

incentives and earnings management ethics on their financial

reporting decisions: The mediating role of moral disengagement.

Journal of Business Ethics, published on-line: March 2014.

Beneish, M. D. (1999). The detection of earnings manipulation.

Financial Analysts Journal, 55, 24–36.

Beneish, M. D., & Press, E. (1993). Costs of technical violation of

accounting-based debt covenants. The Accounting Review, 68(2),

233–257.

Bens, D. A., & Johnston, R. (2009). Accounting discretion: Use or

Abuse? An analysis of restructuring charges surrounding regu-

lator action. Contemporary Accounting Research, 26(3),

673–699.

Bishop, M. L. and Eccher, E. A. (2000). Do markets remember

accounting changes? An examination of subsequent years.

Available at SSRN: http://ssrn.com/abstract=218448 or http://

dx.doi.org/10.2139/ssrn.218448

Bowen, R., Davis, A. K., & Rajgopal, S. (2002). Determinants of

revenue reporting practices for internet firms. Contemporary

Accounting Research, 19(4), 523–562.

Bradshaw, M. T., & Sloan, R. G. (2002). GAAP versus the street: An

empirical assessment of two alternative definitions of earnings.

Journal of Accounting Research, 40(1), 41–66.

Briloff, A. J. (1972). Unaccountable accounting. New York, NY:

Harper & Row Publishers.

Briloff, A. J. (1981). The truth about corporate accounting. New

York, NY: Harper & Row Publishers.

Briloff, A. J. (1990). Accounting and society: A covenant desecrated.

Critical Perspectives on Accounting, 1(1), 5–30.

Briloff, A. J. (2001). Garbage in/garbage out: a critique of fraudulent

financial reporting: 1987–1997 (the COSO Report) and the SEC

accounting regulatory process. Critical Perspectives on Account-

ing, 12(2), 125–148.

Bruns, W. J., & Merchant, K. A. (1990). The dangerous morality of

managing earnings. Management Accounting, 72(2), 22–25.

Bunge, M. (1996). Finding philosophy in social science. New Haven,

CN: Yale University Press.

Burgstahler, D., & Eames, M. (2003). Earnings management to avoid

losses and earnings decreases: Are analysts fooled? Contempo-

rary Accounting Research, 20, 253–276.

Burgstahler, D., Hail, L., & Leuz, C. (2006). The importance of

reporting incentives: earnings management in European private

and public firms. The Accounting Review, 81(5), 983–1016.

Callao, S., Jarne, J. I., & Lainez, J. A. (2007). Adoption of IFRS in

Spain: Effect on the comparability and relevance of financial

reporting. Journal of International Accounting, Auditing and

Taxation, 16, 148–178.

Carpenter, T. D., & Reimers, J. L. (2001). Unethical and fraudulent

financial reporting: Applying the theory of planned behavior.

Journal of Business Ethics, 60(2), 115–129.

Chaney, P. K., & Lewis, C. M. (1995). Earnings management and

firm valuation under asymmetric information. Journal of Cor-

porate Finance, 1(1), 319–345.

Choi, T. H., & Jinhan, P. (2011). Business ethics and financial

reporting quality: Evidence from Korea. Journal of Business

Ethics, 103(3), 403–427.

Christensen, J., & Demski, J. S. (2003). Accounting theory: An

information content perspective. New York: McGraw-Hill Irwin.

Chung, R., Firth, M., & Kim, J. B. (2005). Earnings management,

surplus free cash flow and external monitoring. Journal of

Business Research, 58, 766–776.

Daniel, N. D., Denis, D. J., & Naveen, L. (2008). Do firms manage

earnings to meet dividend thresholds? Journal of Accounting and

Economics, 45, 2–26.

Dechow, P. M., Ge, W., & Schrand, K. M. (2010). Understanding

earnings quality: A review of the proxies, their determinants and

their consequences. Journal of Accounting and Economics, 50,

344–401.

Dechow, P., Hutton, A., Kim, J. H., & Sloan, R. G. (2012). Detecting

earnings management: A new approach. Journal of Accounting

Research, 50(2), 275–334.

Dechow, P. M., & Skinner, D. J. (2000). Earnings management:

Reconciling the views of accounting academics, practitioners,

and regulators. Accounting Horizons, 14, 235–250.

Dechow, P. M., Sloan, R. G., & Sweeny, A. P. (1995). Detecting

earnings management. The Accounting Review, 70, 193–225.

DeFond, M. L. (2010). Earnings quality research: Advances,

challenges and future research. Journal of Accounting and

Economics, 50, 402–409.

DeFond, M. L., & Jiambalvo, J. (1994). Debt covenant violation and

manipulation of accruals. Journal of Accounting and Economics,

17, 145–176.

Demski, J. S. (2003). Corporate conflicts of interest. Journal of

Economic Perspectives, 17(2), 51–72.

Demski, J. S., & Sappington, D. E. M. (1987). Delegated expertise.

Journal of Accounting Research, 25(1), 68–89.

DePree, C. M., & Grant, T. C. (1999). Earnings management and

ethical decision making: Choices in accounting for security

investments. Issues in Accounting Education, 14(4), 613–640.

Doyle, J. T., Lundhom, R. J., & Soliman, M. T. (2003). The predictive

value of expenses excluded from ‘‘pro forma’’ earnings. Review

of Accounting Studies, 8(2–3), 145–174.

A. B. Vladu et al.

123

Author's personal copy

Dye, R. A. (1988). Earnings management in an overlapping

generations model. Journal of Accounting Research, 26,

195–235.

Elias, R. (2002). Determinants of earnings management ethics among

accountants. Journal of Business Ethics, 40(1), 33–45.

Fama, E. (1980). Agency problems and the theory of the firm. Journal

of Political Economy, 88(2), 288–307.

Fama, E., & Jensen, M. (1983). Separation of ownership and control.

Journal of Law and Economics, 26, 301–325.

Feltham, G. A., Raffi, I., & Dhananjay, N. (2006). Dynamic

incentives and dual-purpose accounting. Journal of Accounting

and Economics, 42(3), 417–437.

Francis, J., LaFond, R., Olsson, P., & Schipper, K. (2004). Costs of

equity and earnings attributes. The Accounting Review, 79(4),

967–1010.

Francis, J., Schipper, K., & Vincent, L. (2003). The relative and

incremental explanatory power of alternative (to earnings)

performance measures for returns. Contemporary Accounting

Research, 21(1), 121–164.

Fridson, M. S. (1993). Financial statement analysis: A practitioner’s

guide. New York: John Wiley.

Gong, G., Louis, H., & Sun, A. X. (2008). Earnings management,

lawsuits, and stock-for-stock acquirers’ market performance.

Journal of Accounting and Economics, 46, 62–77.

Grant, C., Depree, M., & Grant, G. (2000). Earnings management and

the abuse of materiality. Journal of Accountancy, 190, 41–44.

Greenfield, A. C., Norman, C. S., & Wier, B. (2008). The effect of

ethical orientation and professional commitment on earnings

management behavior. Journal of Business Ethics, 83, 419–434.

Guay, W. R., Kothari, S. P., & Watts, R. (1996). A market-based

evaluation of discretionary accrual models. Journal of Account-

ing Research, 34(Supplement 3), 83–105.

Gunny, K. (2005). What are the consequences of real earnings

management? Available at SSRN.com/abstract = 816025.

He, L., & Yang, R. (2014). Does industry regulation matter? new

evidence on audit committees and earnings management.

Journal of Business Ethics, 123, 573–589.

Healy, P. M. (1985). The effect of bonus schemes on accounting

decisions. Journal of Accounting and Economics, 7, 85–107.

Healy, P. M., & Wahlen, M. (1999). A review of the earnings

management literature and its implications for standard setting.

Accounting Horizons, 13(4), 365–383.

Holthausen, R., Larker, D., & Sloan, R. (1995). Annual bonus

schemes and the manipulation of earnings. Journal of Account-

ing and Economics, 19, 29–74.

Hope, O.-K. (2003). Disclosures practices, enforcement and account-

ing standards and analysts’ forecast accuracy: An international

study. Journal of Accounting Research, 41(2), 235–272.

Hsiang-Lin, C., Chung-Hua, S., & Feng-Ching, K. (2008). Corporate

social responsibility, investor protection, and earnings manage-

ment: Some international evidence. Journal of Business Ethics,

79(1–2), 179–198.

Huang, P., Louwers, T. J., Moffitt, J. S., & Zhang, Y. (2008). Ethical

management, corporate governance, and abnormal accruals.

Journal of Business Ethics, 83(3), 469–487.

Jansen, I. P., Ramnath, S., & Yohn, T. L. (2012). A diagnostic for

earnings management using changes in asset turnover and profit

margin. Contemporary Accounting Research, 29(1), 221–251.

Jensen, M., & Meckling, W. (1976). Theory of the firm: managerial

behavior, agency costs, and ownership structure. Journal of

Financial Economics, 3(4), 305–360.

Johnson, E., Fleishman, G., Valentine, S., & Walker, K. (2012).

Managers’ ethical evaluations of earnings management and its

consequences. Contemporary Accounting Research, 29(3),910–927.

Jones, J. J. (1991). Earnings management during import relief

investigations. Journal of Accounting Research, 29, 193–228.

Kant, I. (1994). The metaphysics of moral. The metaphysical

principles of virtue (1797). In I. Kant, Ethical Philosophy 2nd

edn, Trans. by James W. Ellington. Hackett Publishing Com-