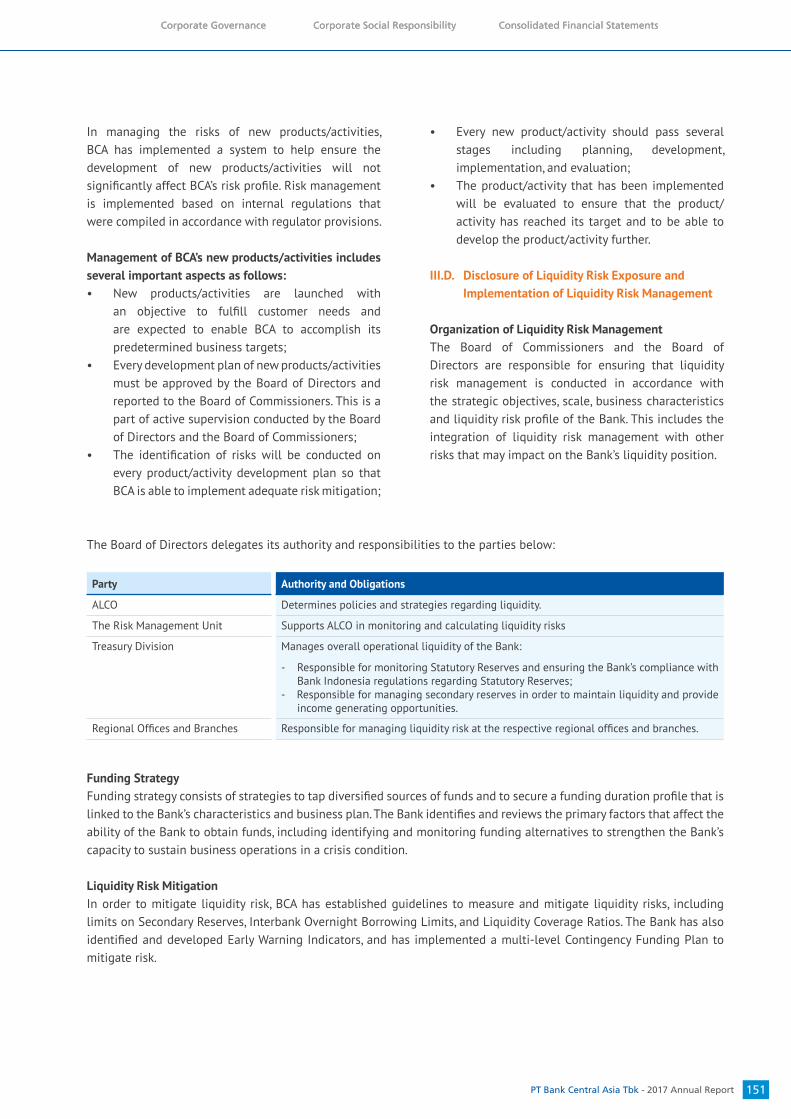

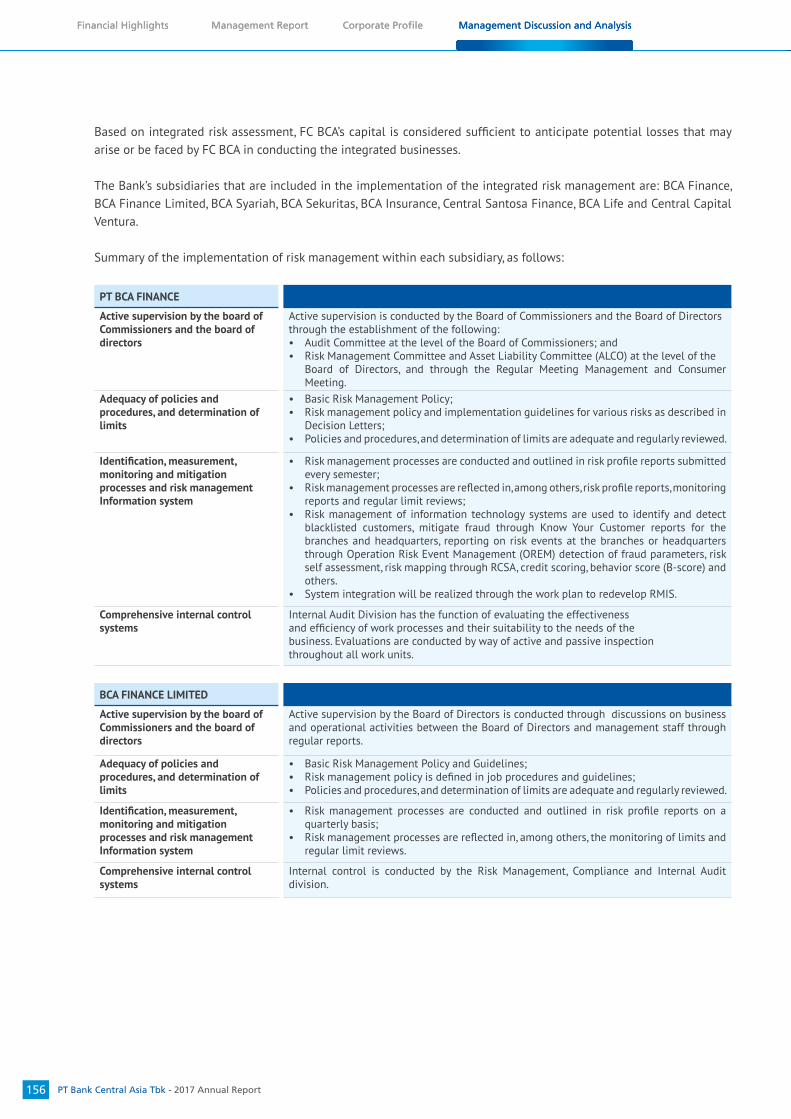

Embed Size (px)

Citation preview

Trust Through Quality

2017

Annual Report

Annual Report

2014

Steadfast in an Uncertain

Global Environment

2013 Annual Report

PT Bank Central Asia Tbk

Always by your side

Theme Continuity

Steadfast in an UncertainGlobal Environment

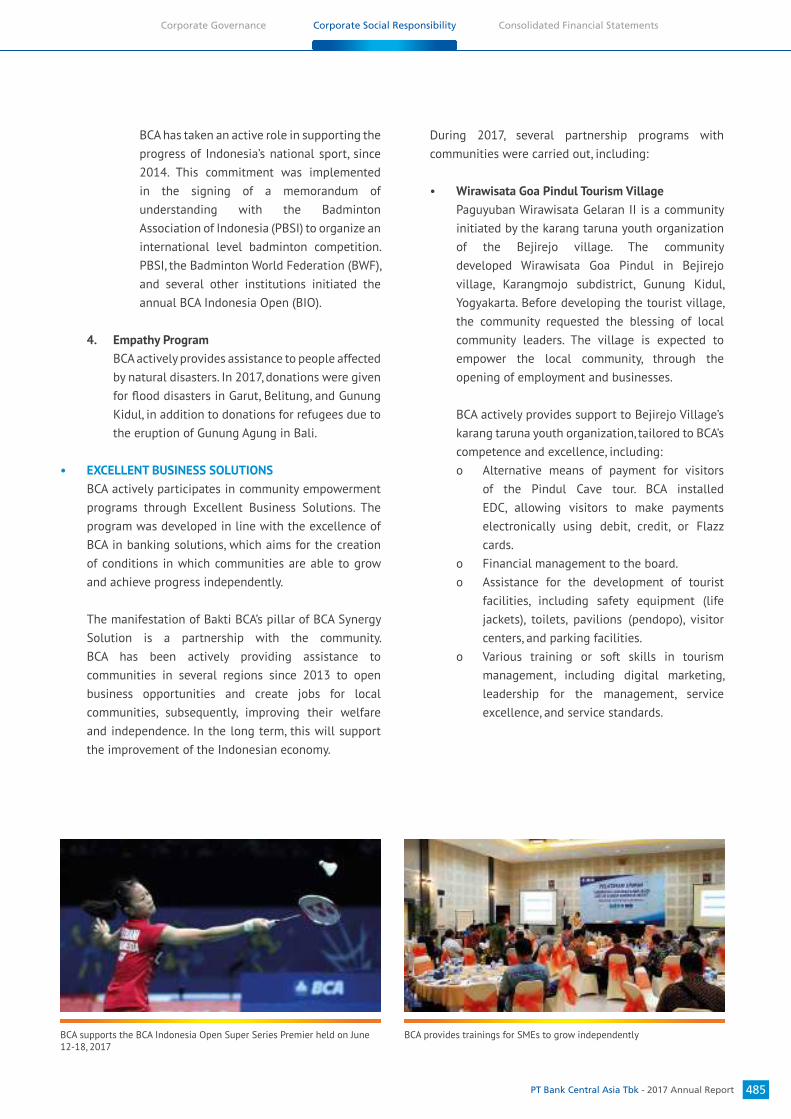

2013 was a challenging year for the Indonesian economy. In an environment of global economic uncertainty and slowing domestic economic growth, BCA leveraged off its solid financial position to support the financial needs of its customers and maintain its position as a leading transaction bank in Indonesia.

Customer satisfaction is at the heart of BCA’s business strategy. The Bank understands the importance of standing by its customers especially during volatile economic periods. Lending prudence and understanding the needs of its customers were key to remaining steadfast in an uncertain global environment.

Delivering Value During a Transition Period

2014 was a year of both political and economic transition for Indonesia marked by high volatility in the foreign exchange and capital markets and continuing pressure on commodity prices. The solid foundation laid by the previous government provides a sound basis for facing the macro economic issues now impacting the Indonesian economy. The new administration is taking steps to address these issues, including the reallocation of a large part of the fuel subsidy budget to other strategic areas, that should pave the way for future sustainable economic development. New challenges for the Indonesian banking industry surfaced in 2014 as the result of a slowing economy and tightening liquidity which both limited the capacity for loan growth and led to higher sector NPL’s. BCA successfully maintained its solid performance and delivered value to its stakeholders throughout this transition year by boosting liquidity and maintaining prudential lending guidelines.

Maintaining a Solid PositionNavigating Challenges, Capturing Opportunities

The Indonesian economy continued to be negatively impacted by a weak global economy and a variety of domestic macro-economic challenges. The relative slowdown in the domestic economy was reflected in the Indonesian banking industry with deterioration in loan quality and slower loan and third party funds growth.

BCA successfully maintained its solid position in 2015 by consistently implementing prudent policies focused on maintaining loan quality, a strong capital and a healthy liquidity position.

BCA’s solid financial position allows the Bank to support its customers through all economic conditions while providing a strong base to capture business opportunities for future growth.

fulfill the evolving financial needs of the Bank’s

financial performance.

20132014

2015

the banking industry on the whole and BCA specifically,

from its customers facilitated a year of strong financial

Expanding CapabilitiesCapturing Opportunities

Ongoing improvements ensure the Bank to provide the best possible services to customers; fulfill the evolving financial needs of the Bank’s customers and remain at the cutting edge of technological developments. BCA remains committed to invest in both transaction banking franchise and lending capabilities while supporting development of the Bank’s subsidiaries.

The challenging environment faced by the Bank in 2016 served as a test of the resilience of BCA’s business model. Throughout the year, BCA focused on exploring and optimizing various business opportunities while remaining prudent at all times. The Bank’s solid business model allowed BCA to deliver another year of sound financial performance.

2016

2017 provided both challenges and opportunities for the banking industry in Indonesia, and BCA specifically. Throughout the year, BCA invested in infrastructure and resources to strengthen its core transaction banking and lending business.

BCA continues to adapt, embracing technological advances and capturing business opportunities, while maintaining a prudent approach to business. The Bank always prioritizes the comfort of its customers by providing convenient, secure and reliable services at all times.

With the loyal support of its customers, BCA successfully delivered a year of strong financial performance and maintained its position as the bank of choice in Indonesia.

2017

Trust th

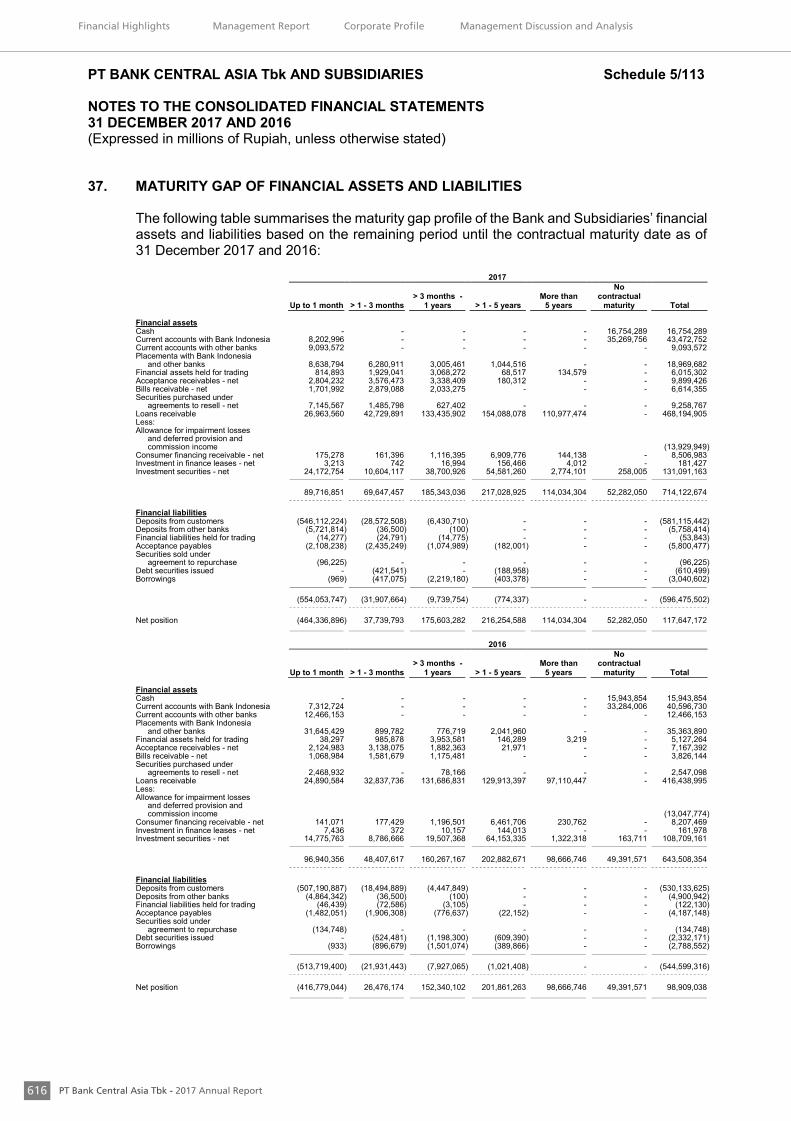

rou

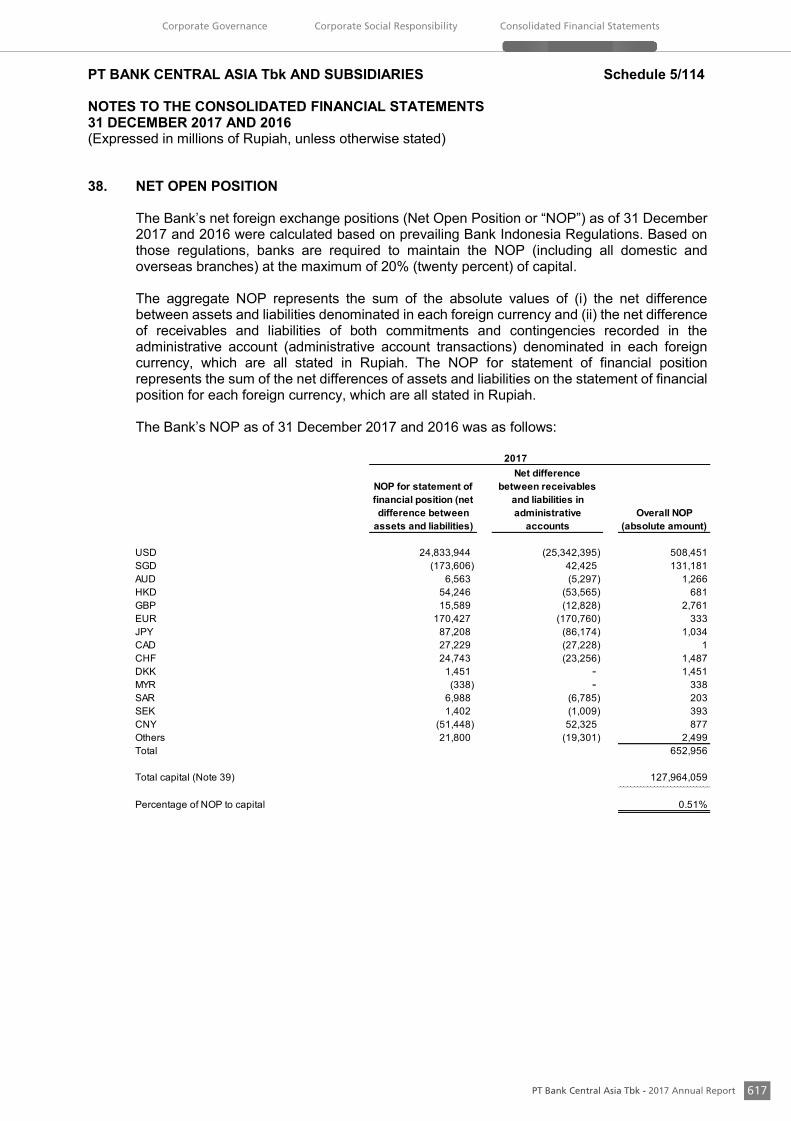

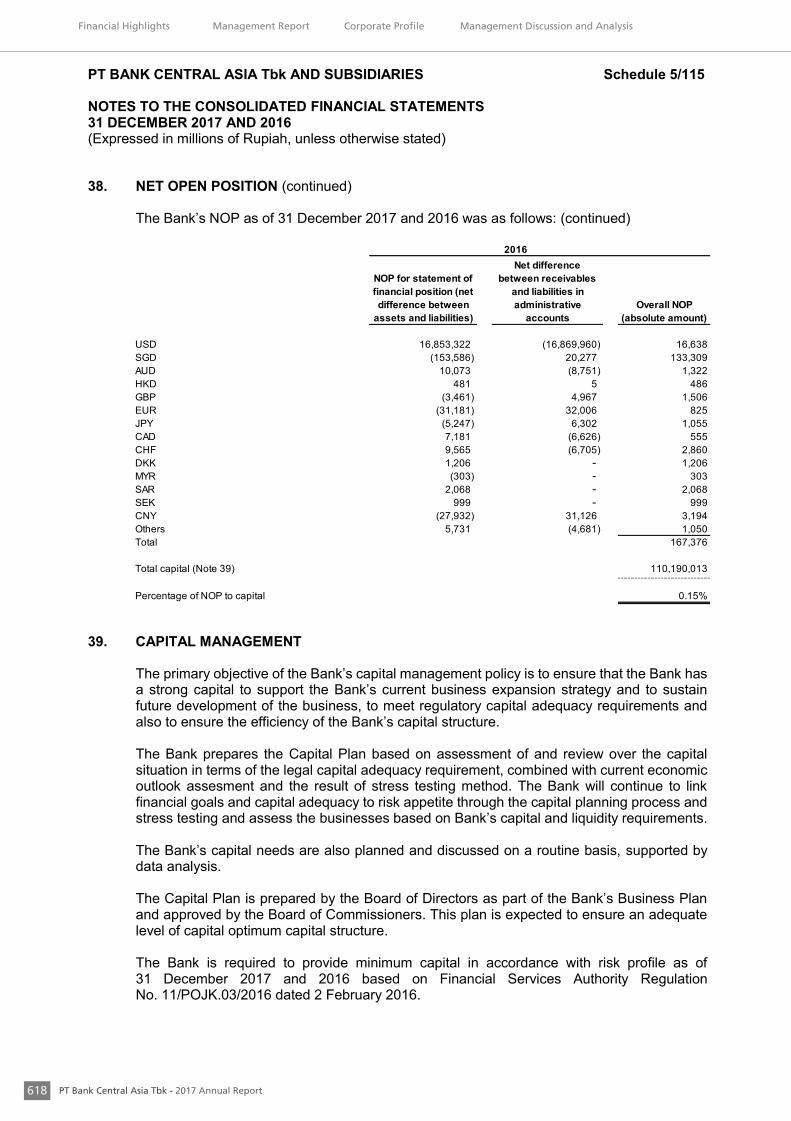

gh

Qu

ality

Trust Through Quality

2017

Annual Report

Trust ThroughQuality

PT Bank Central Asia Tbk - 2017 Annual Report2

42 Company General Information

43 Line of Business

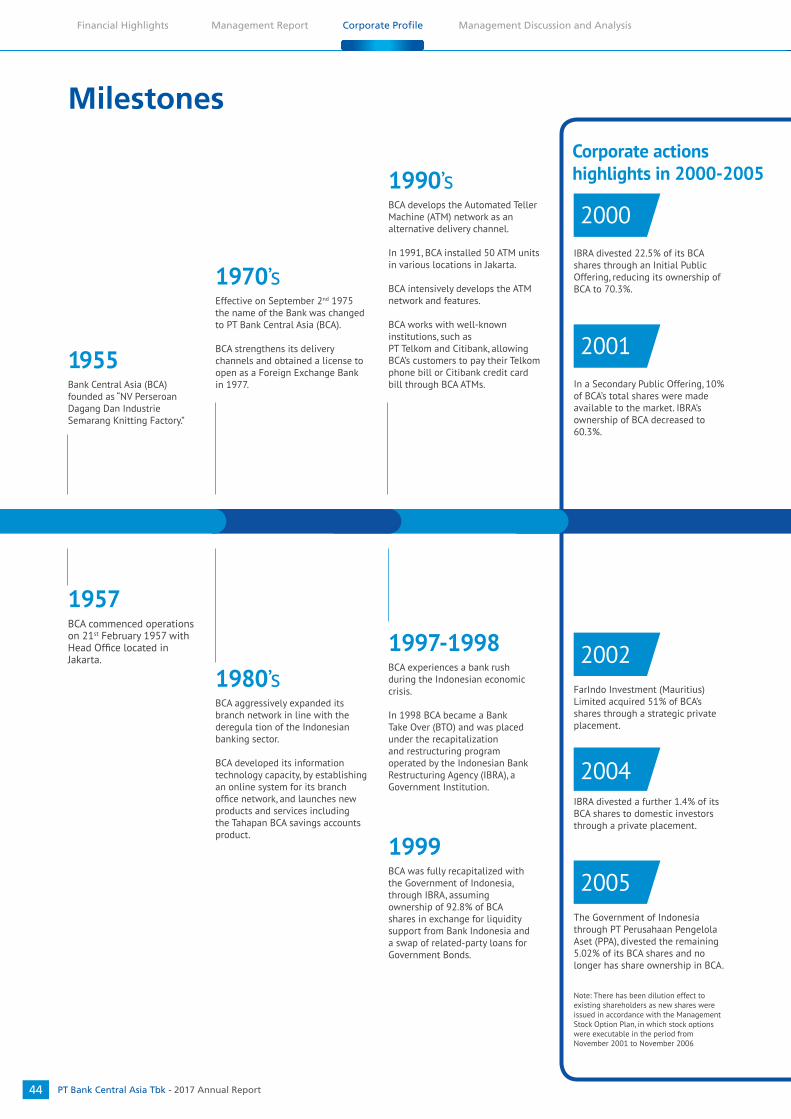

44 Milestones

46 Event Highlights 2017

50 Corporate Culture

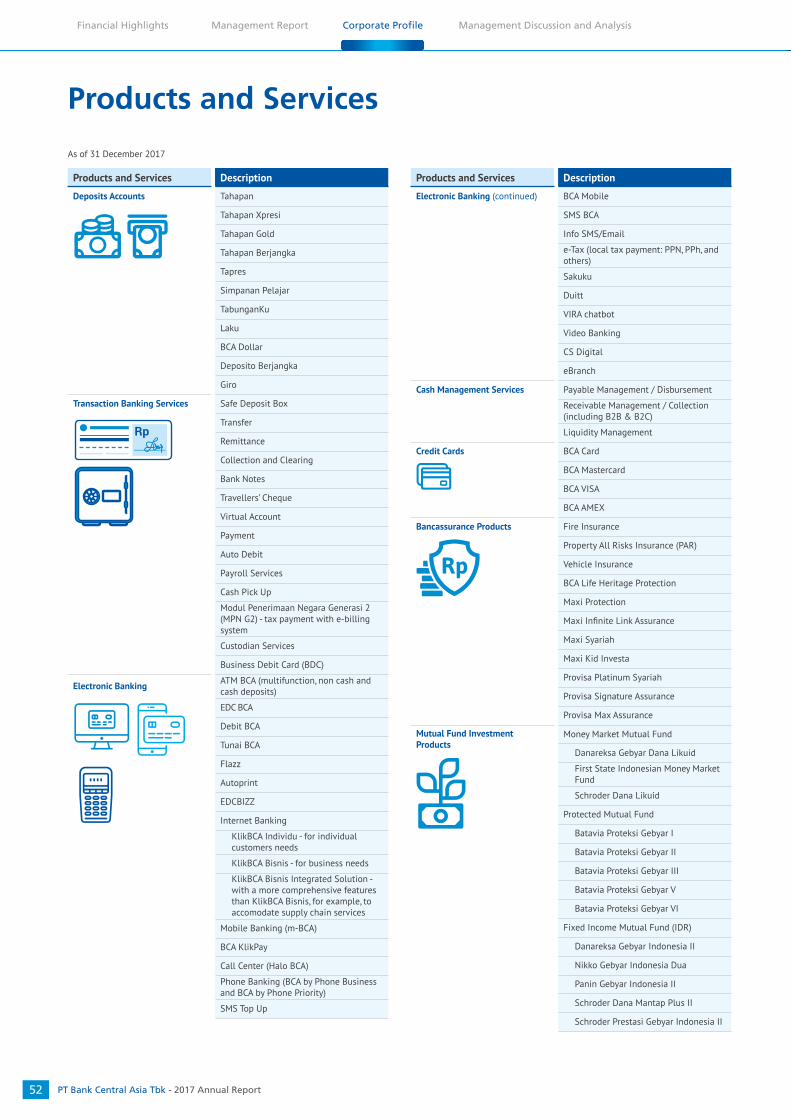

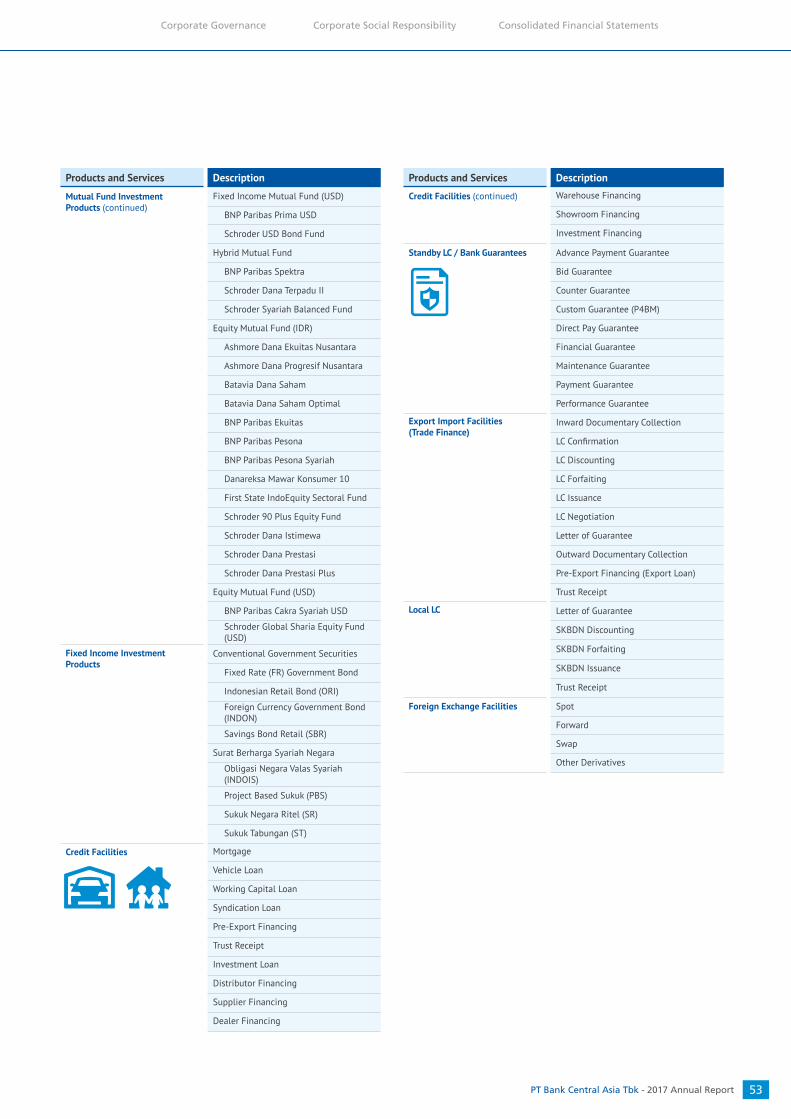

52 Products and Services

54 Organization Structure

56 Board of Directors and Board of Commissioners Profiles70 Board of Commissioners Committee Members and

Corporate Secretary Profiles80 Senior Officers

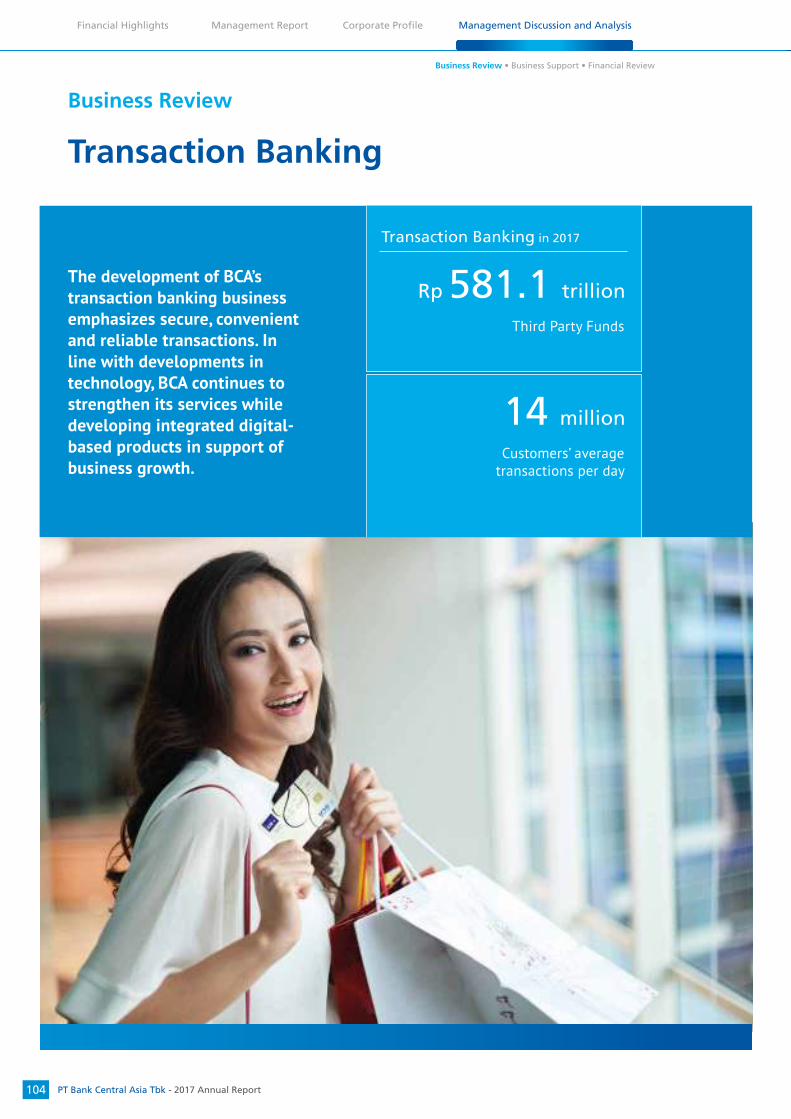

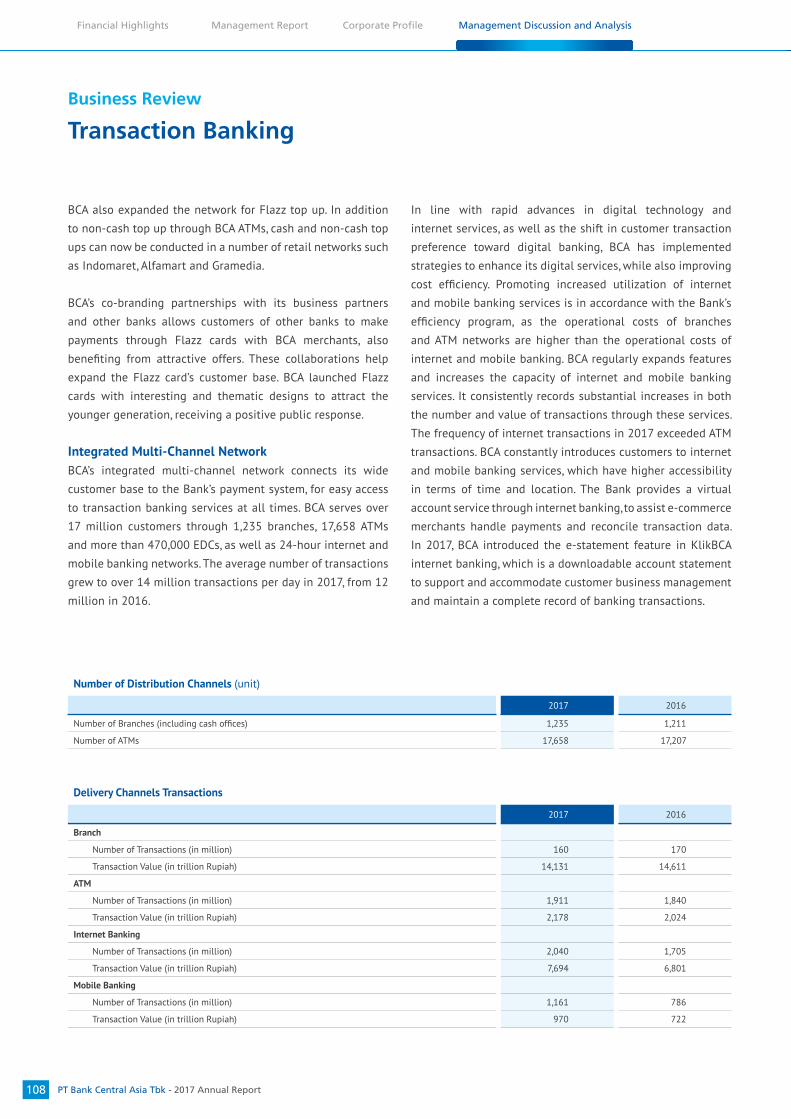

103 Business Review104 Transaction Banking

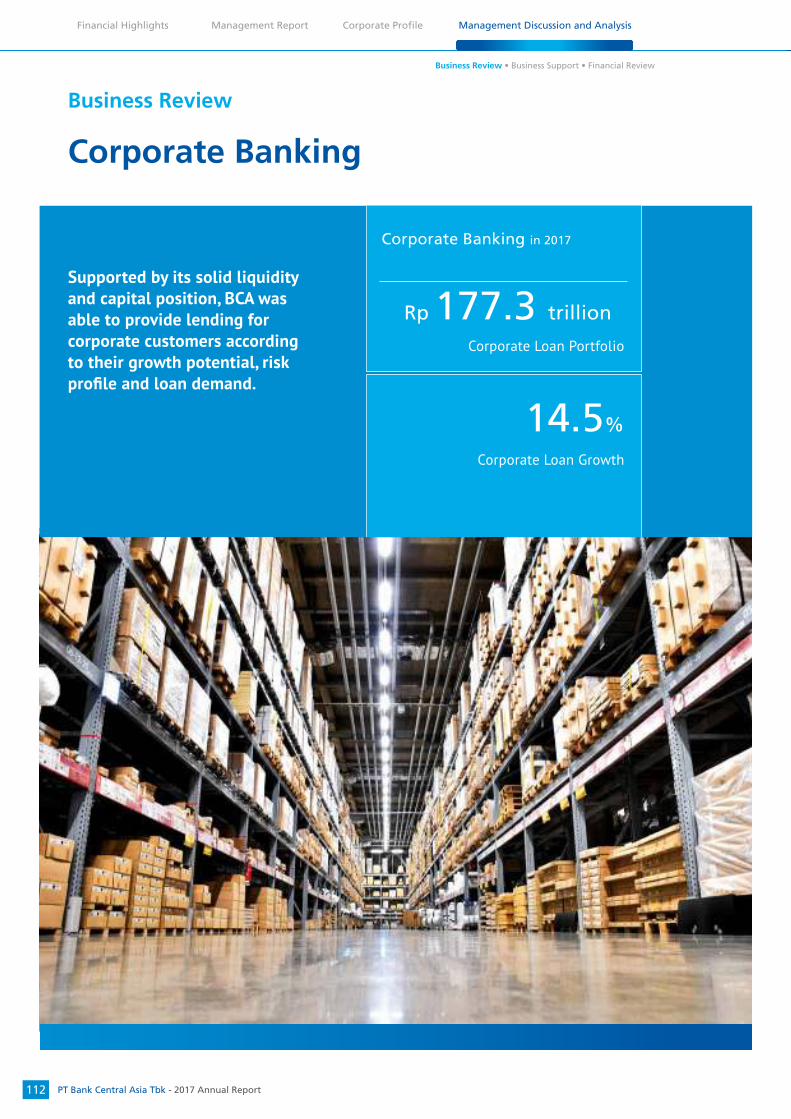

112 Corporate Banking

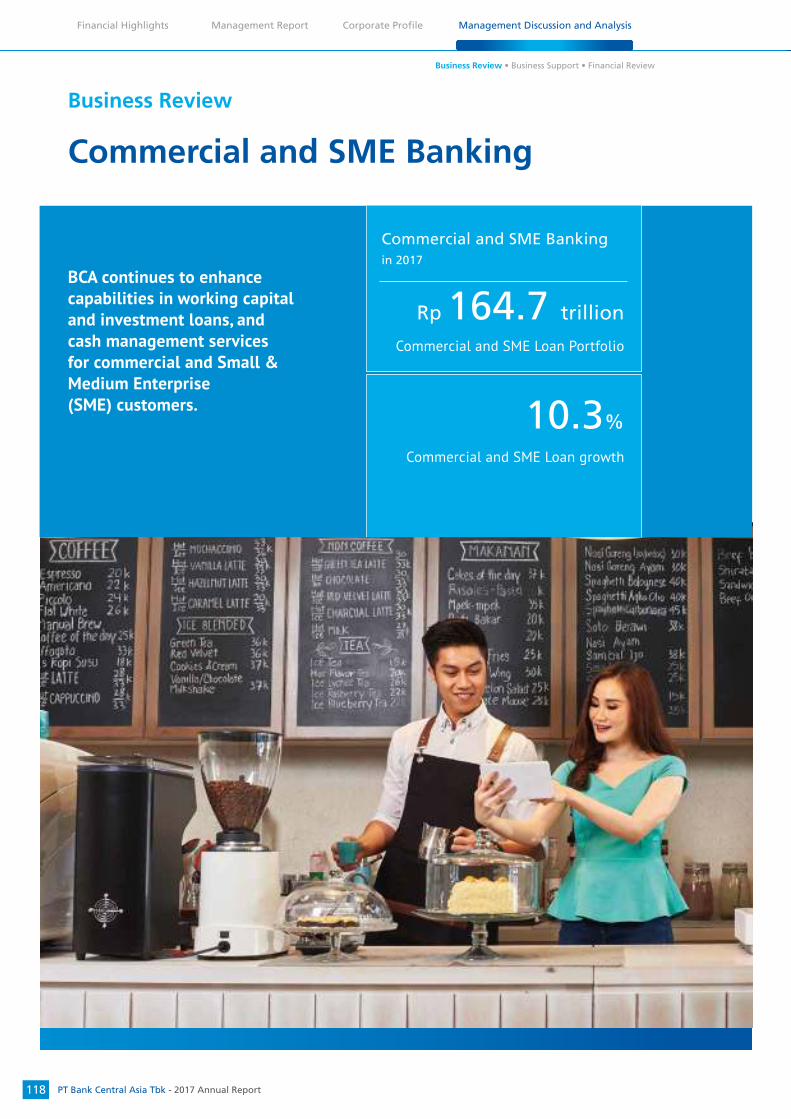

118 Commercial and SME Banking

124 Individual Banking

130 Treasury and International Banking

12 Financial Highlights

16 Stock and Bond Highlights

22 Report of The Board of Directors

32 Board of Commissioners’ Supervisory Report

04

Contents

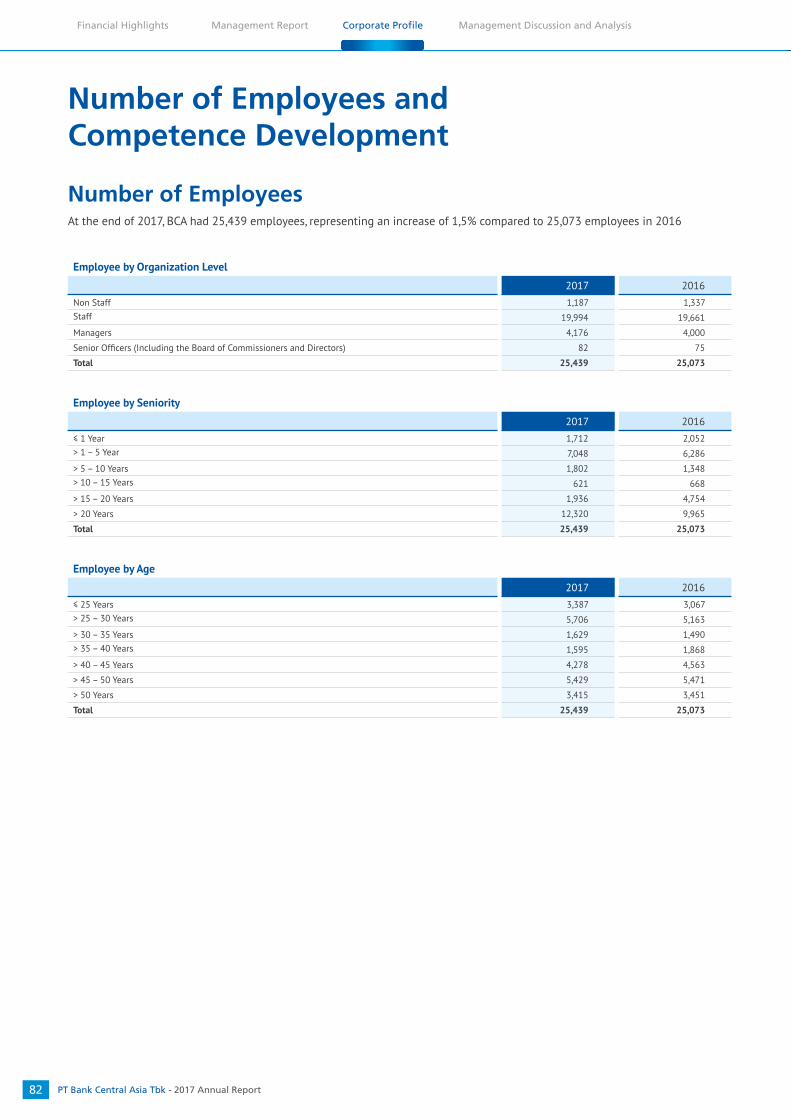

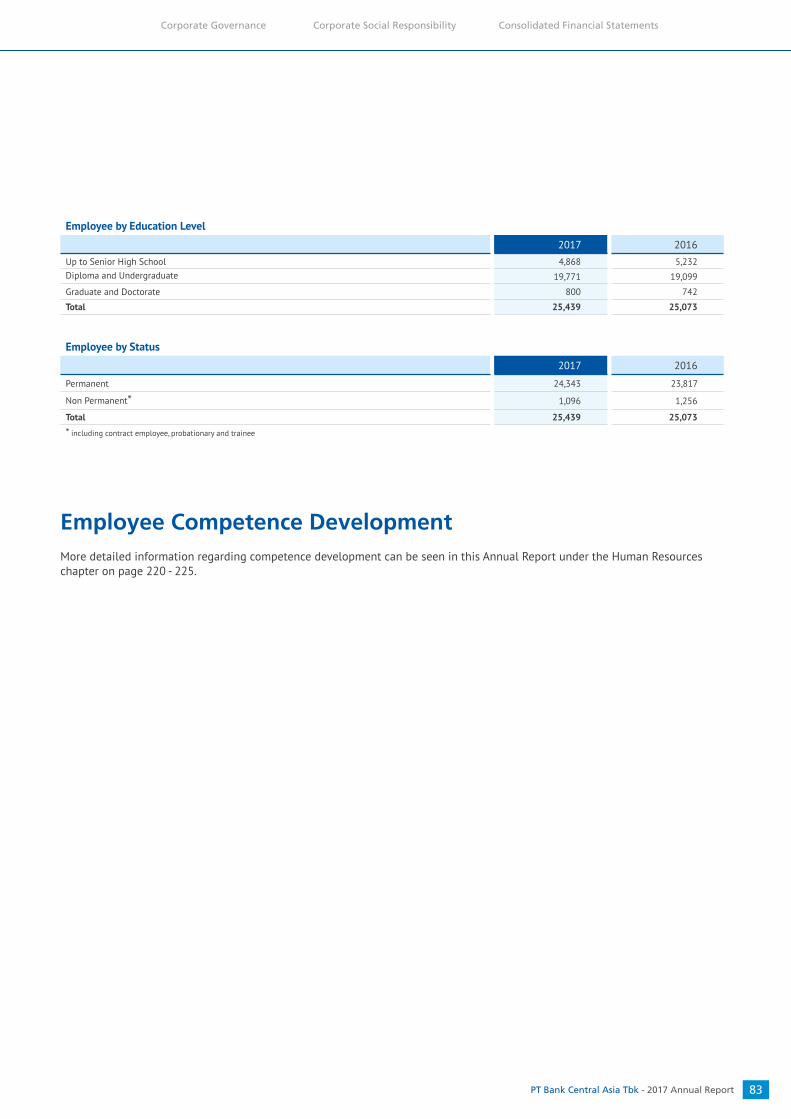

82 Number of Employees and Competence Development Number of Employees by Organization Level, Seniority, Age, Education Level and Status

Employee Competence Development

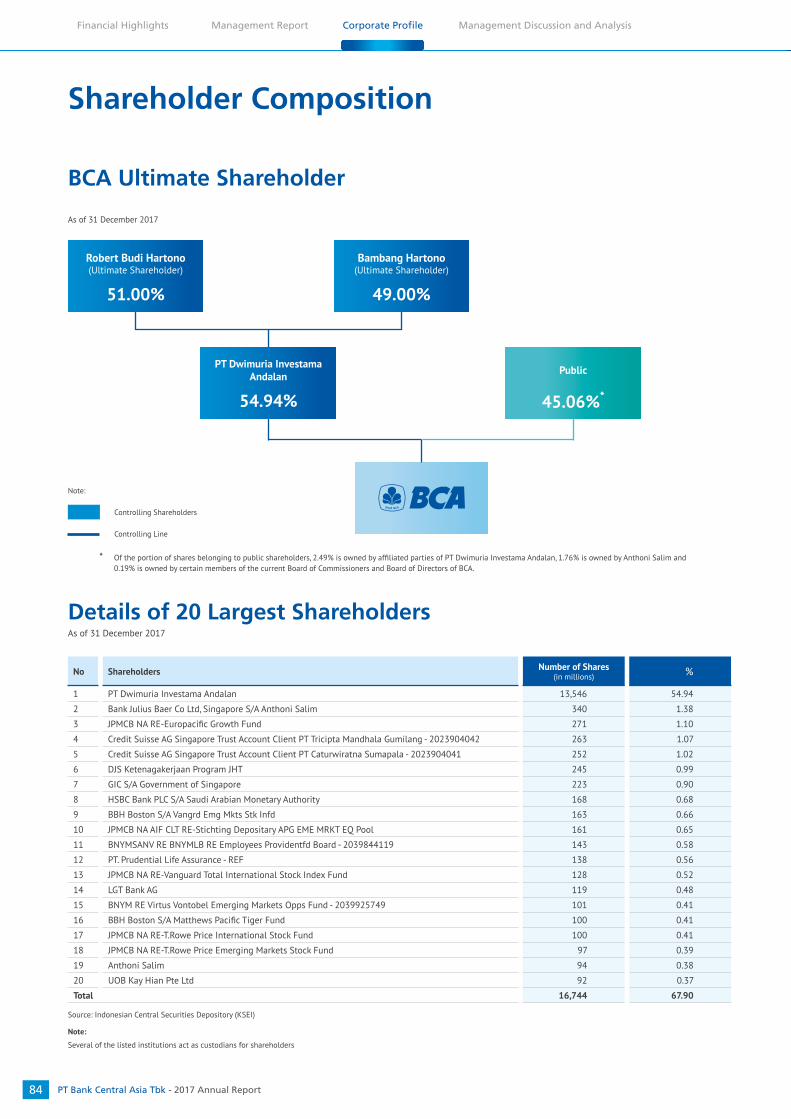

84 Shareholder Composition BCA Ultimate Shareholder

Details of 20 Largest Shareholders

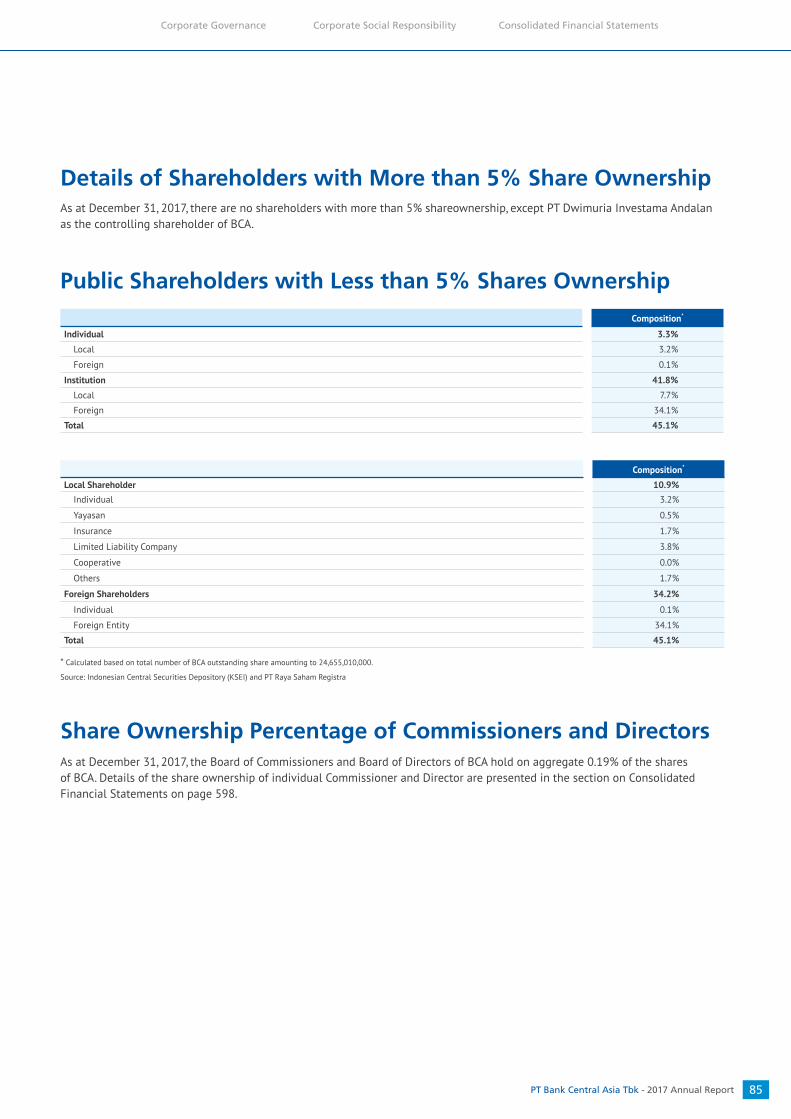

Details of Shareholders with More than 5% Share Ownership

Public Shareholders with Less than 5% Share Ownership

Share Ownership Percentage of Commissioners and Directors

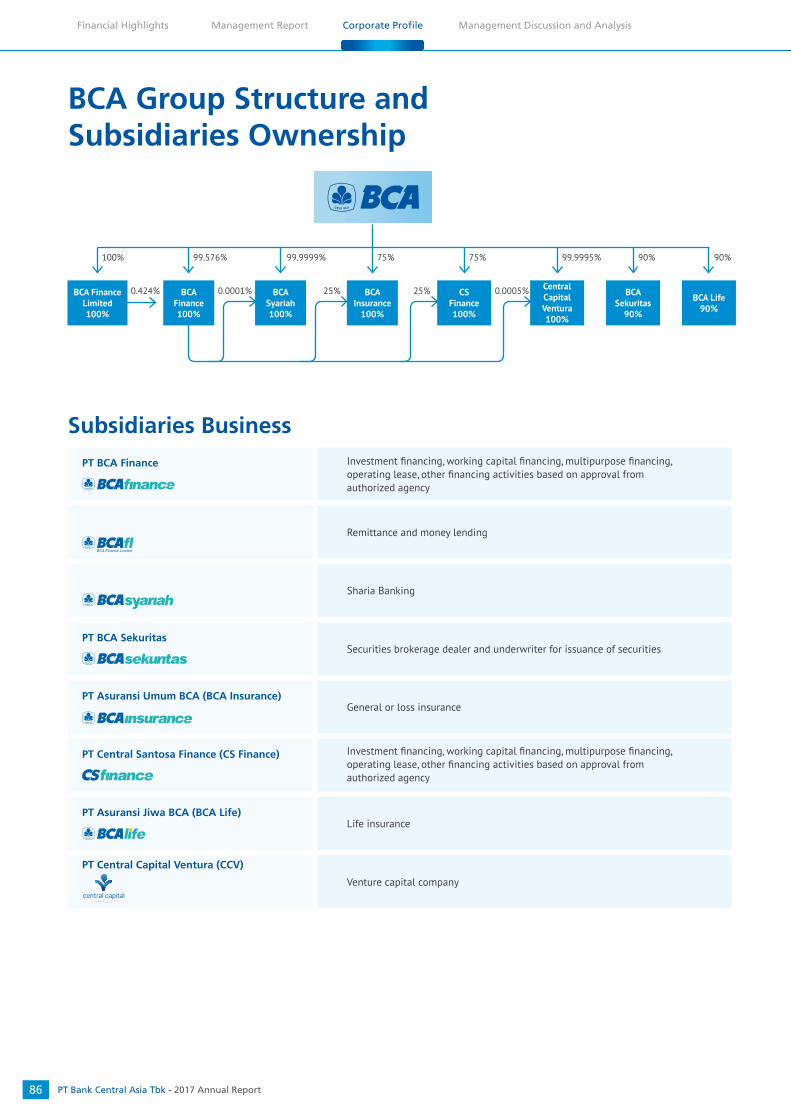

86 BCA Group Structure and Subsidiaries Ownership

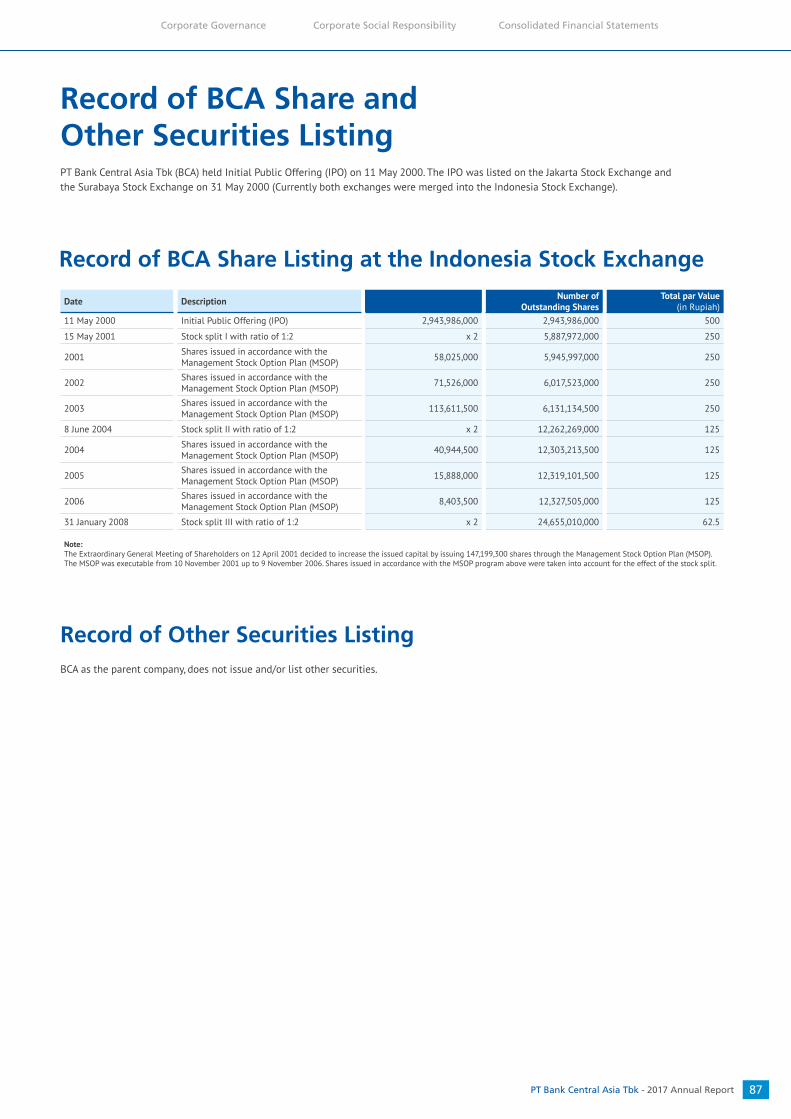

87 Record of BCA Share and Other Securities Listing

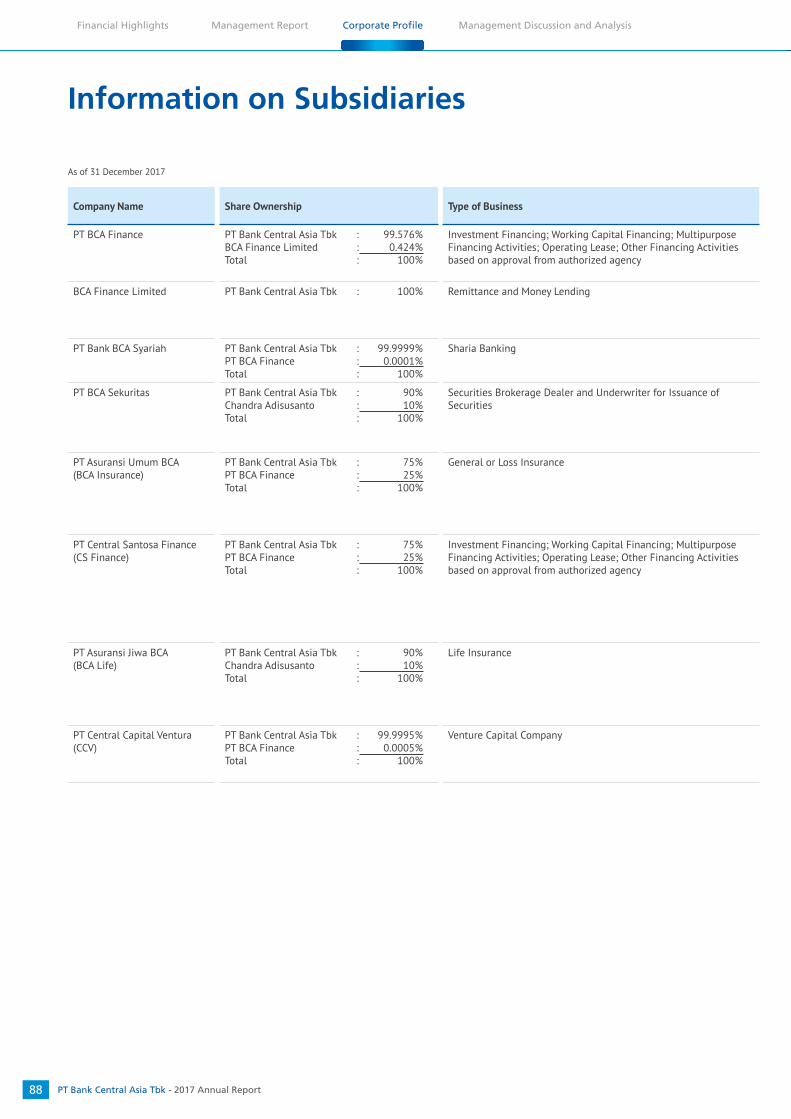

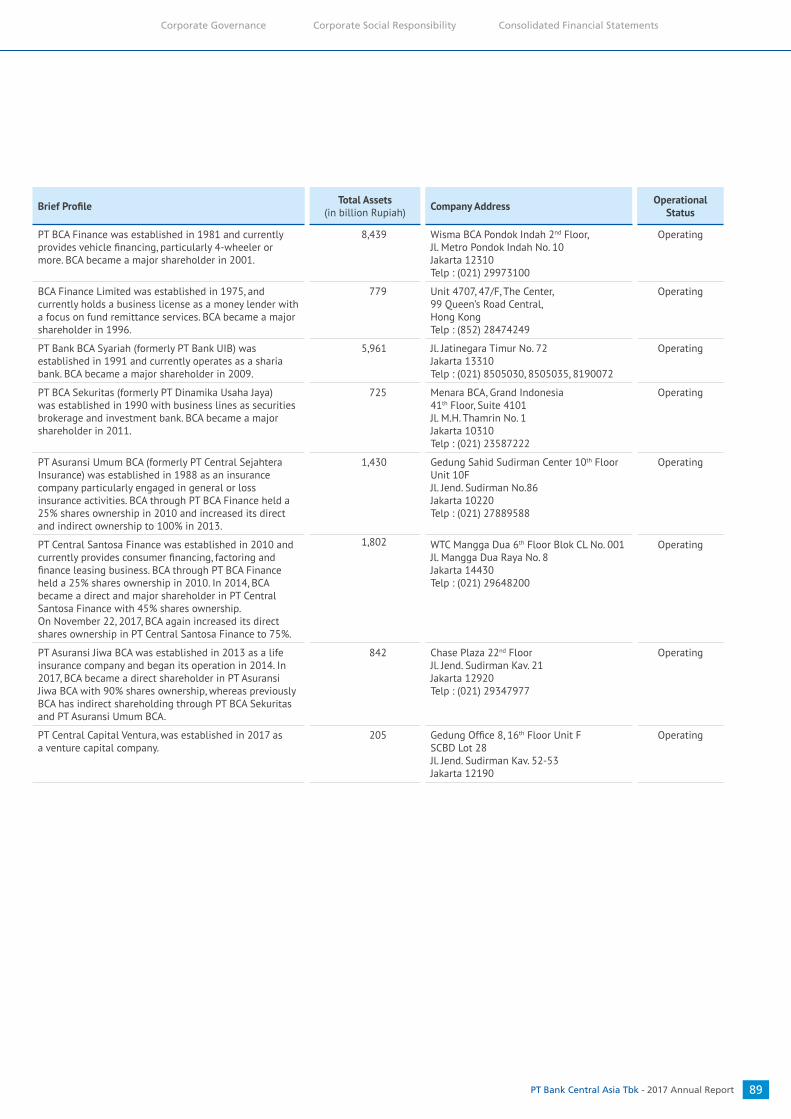

88 Information on Subsidiaries

90 Capital Market Supporting Institution

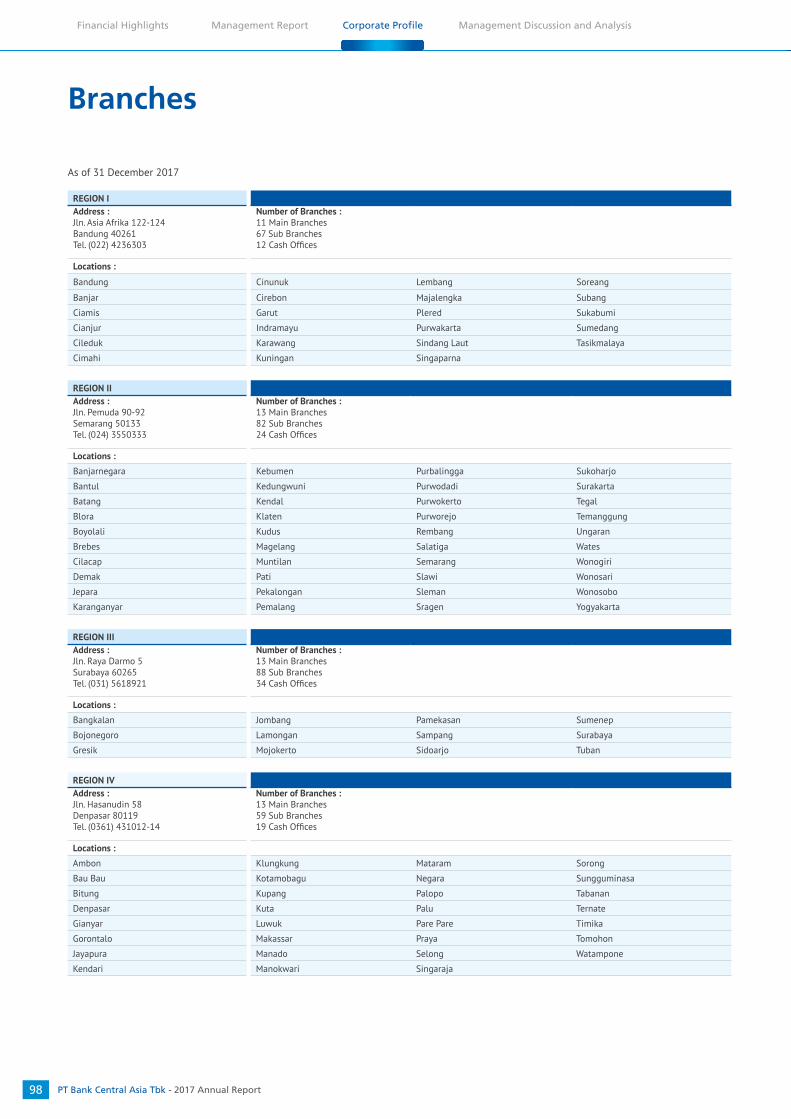

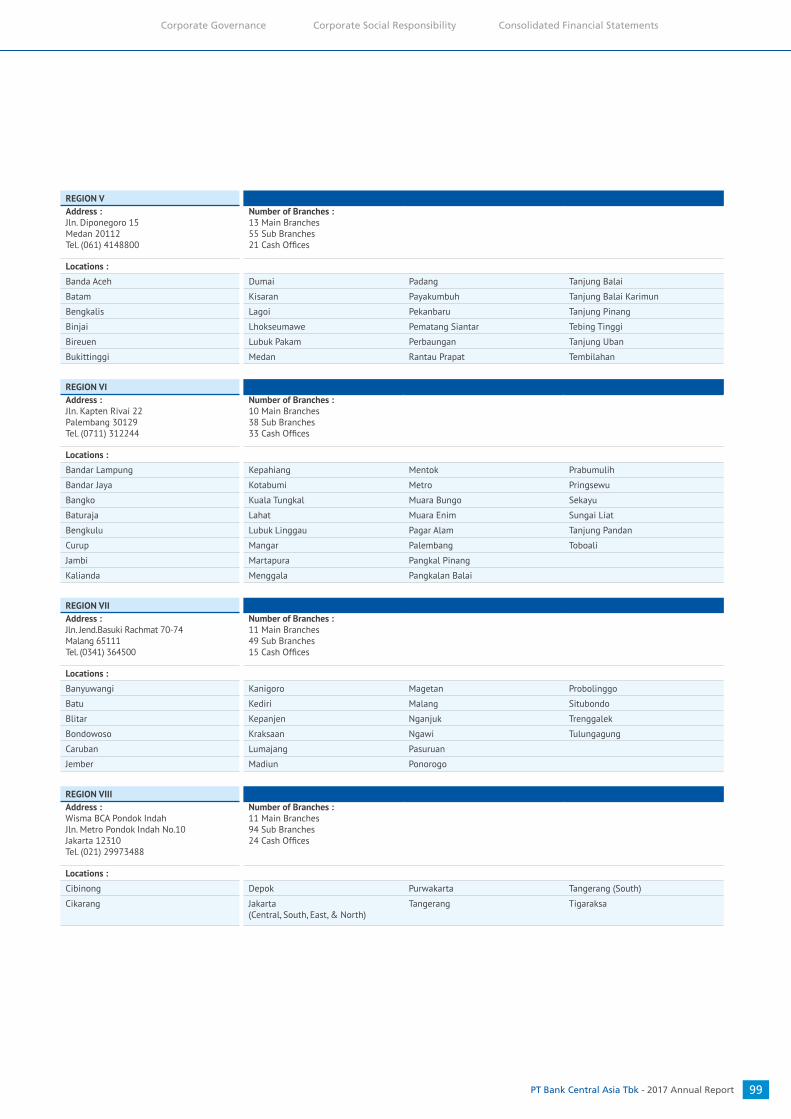

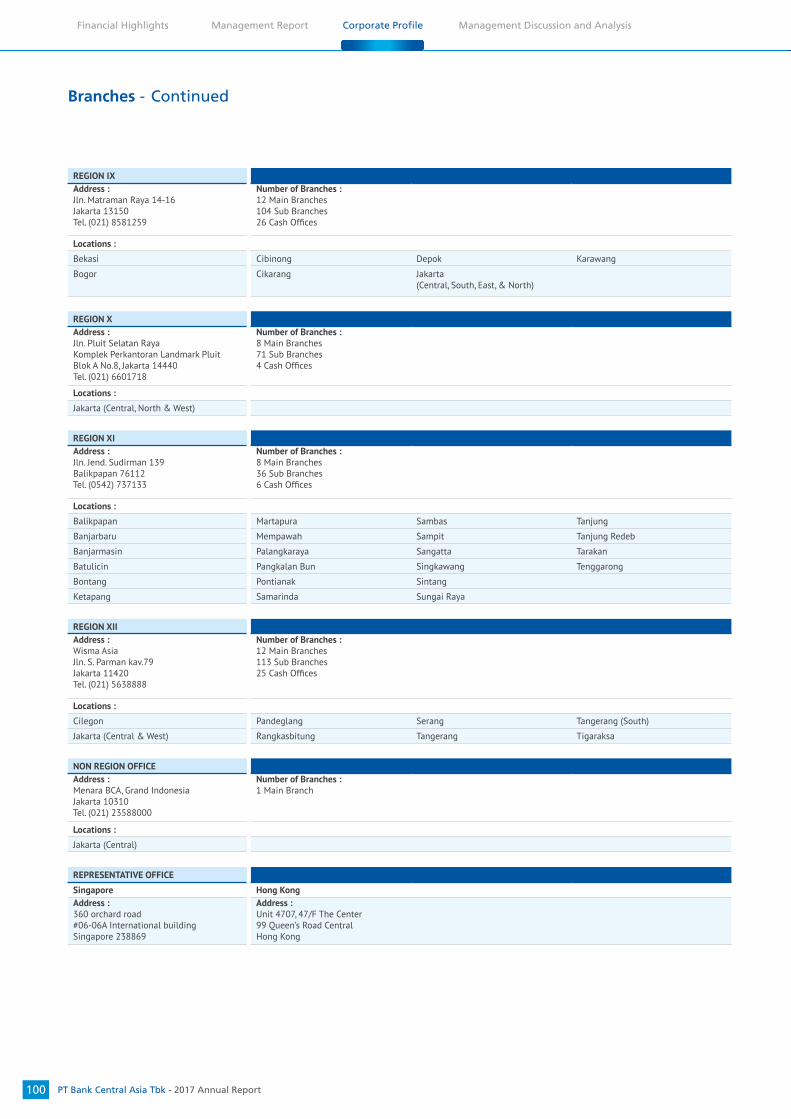

91 Awards and Certifications98 Branches

101 Data Access and Corporate Information

101 Information on Corporate Website

101

Training and/or Education for the Board of Commissioners, the Board of Directors, Committees, Corporate Secretary and Internal Audit Unit

PT Bank Central Asia Tbk - 2017 Annual Report 3

281 Introduction

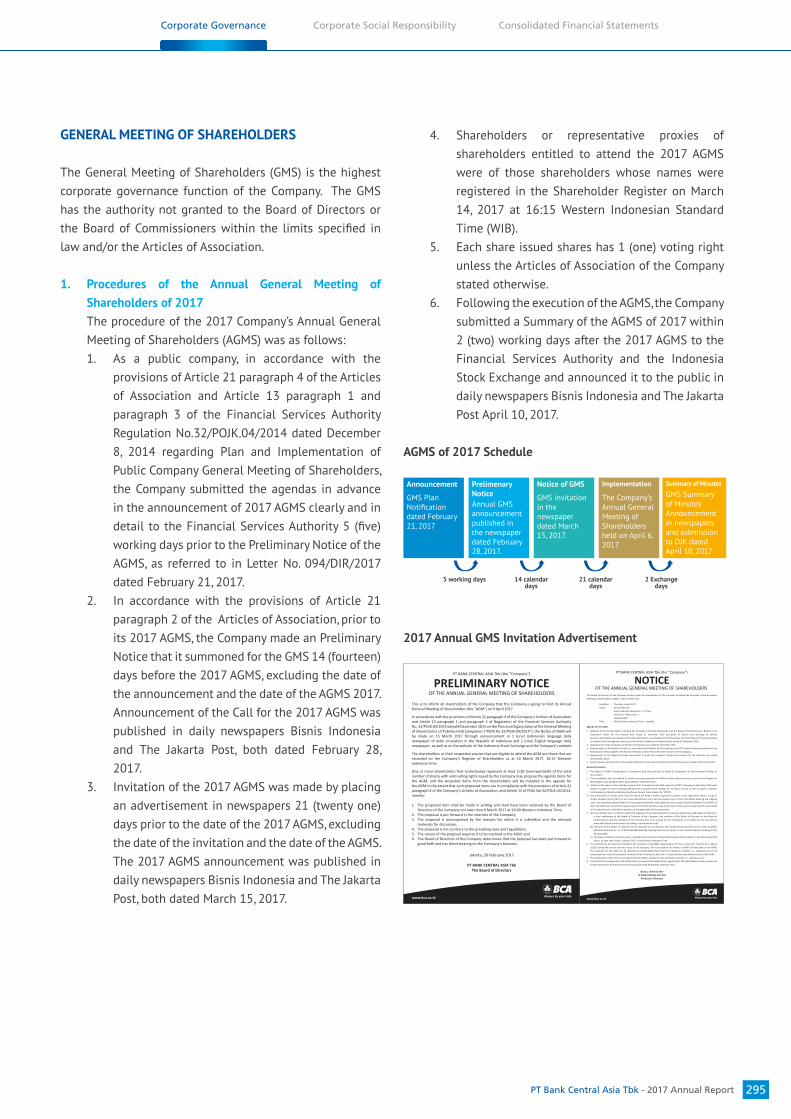

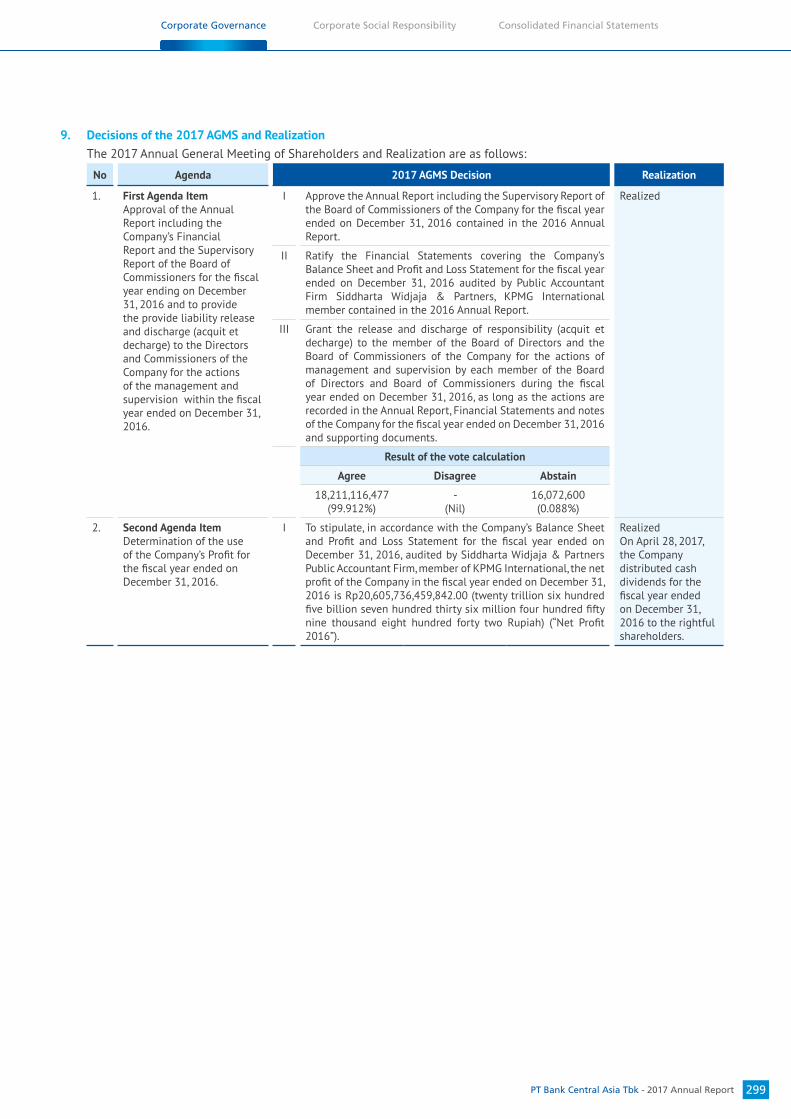

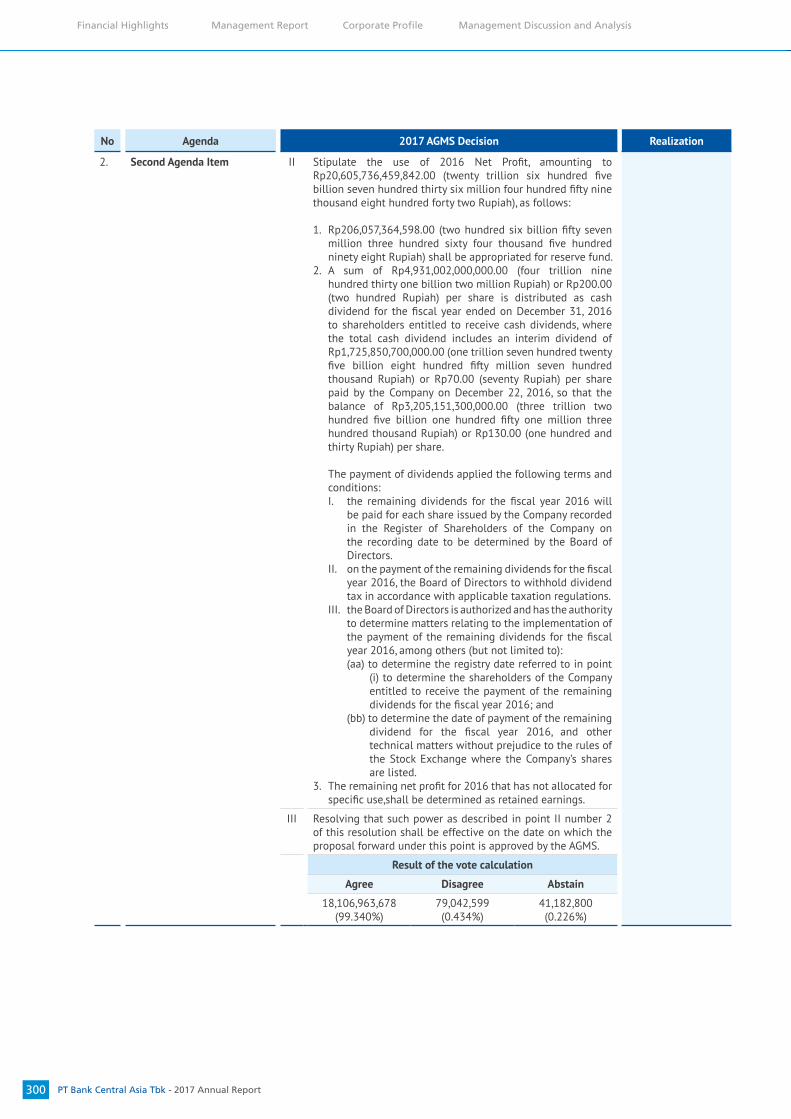

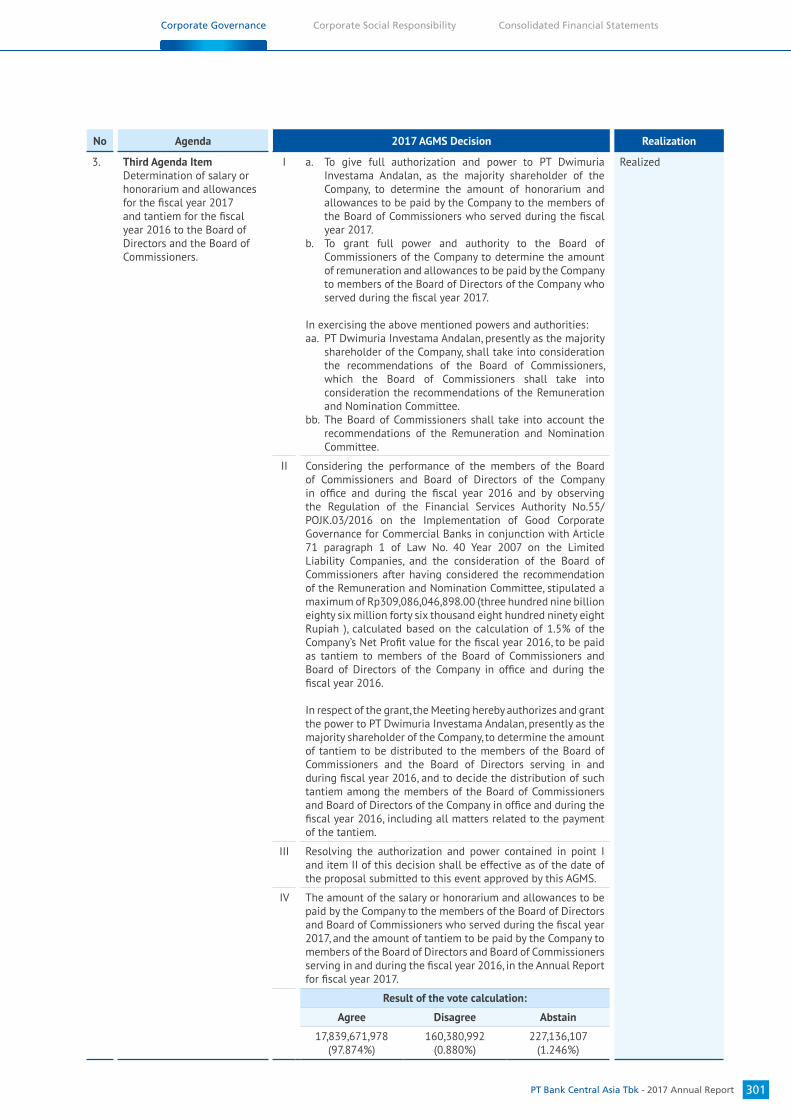

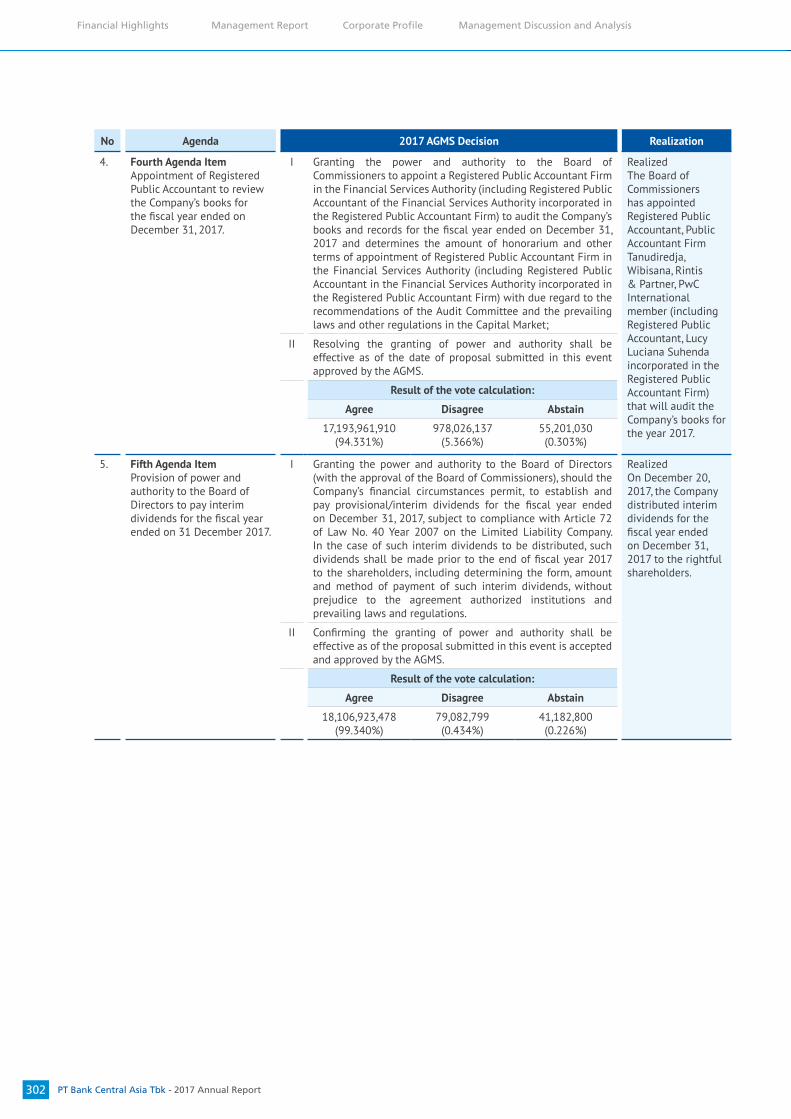

295 General Meeting of Shareholders

309 Major Shareholder/Controller Information

309 Board of Commissioners

323 Board of Directors

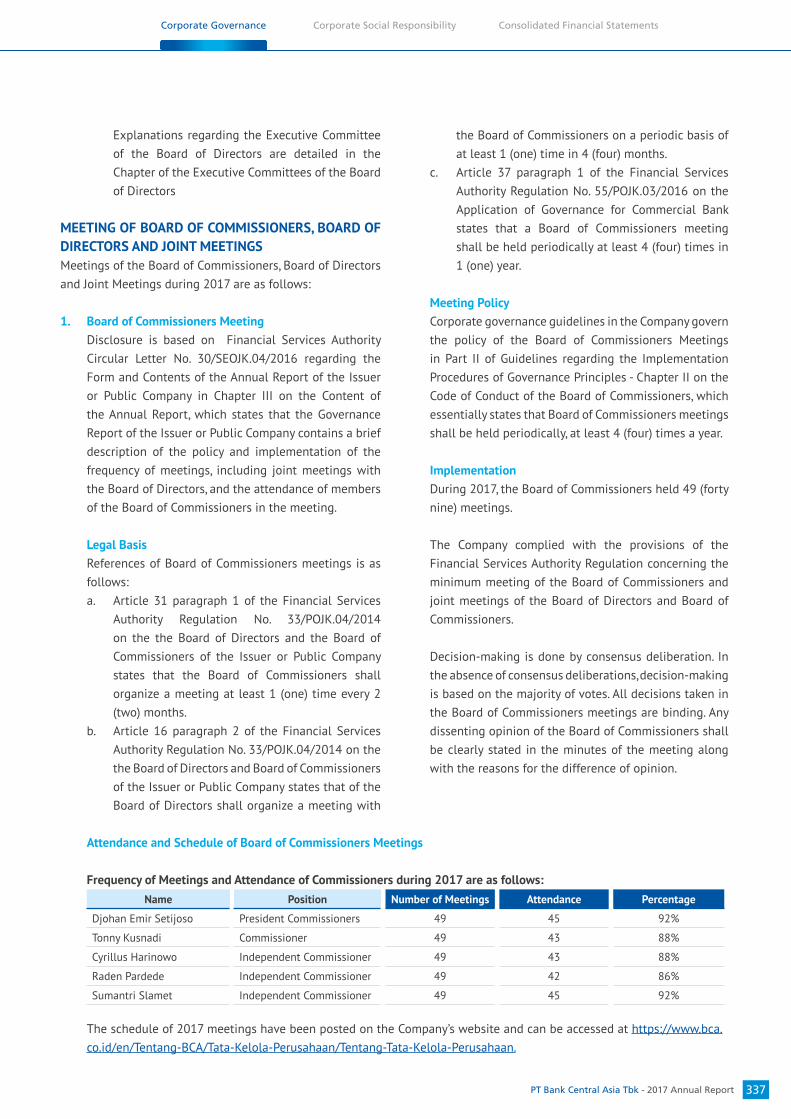

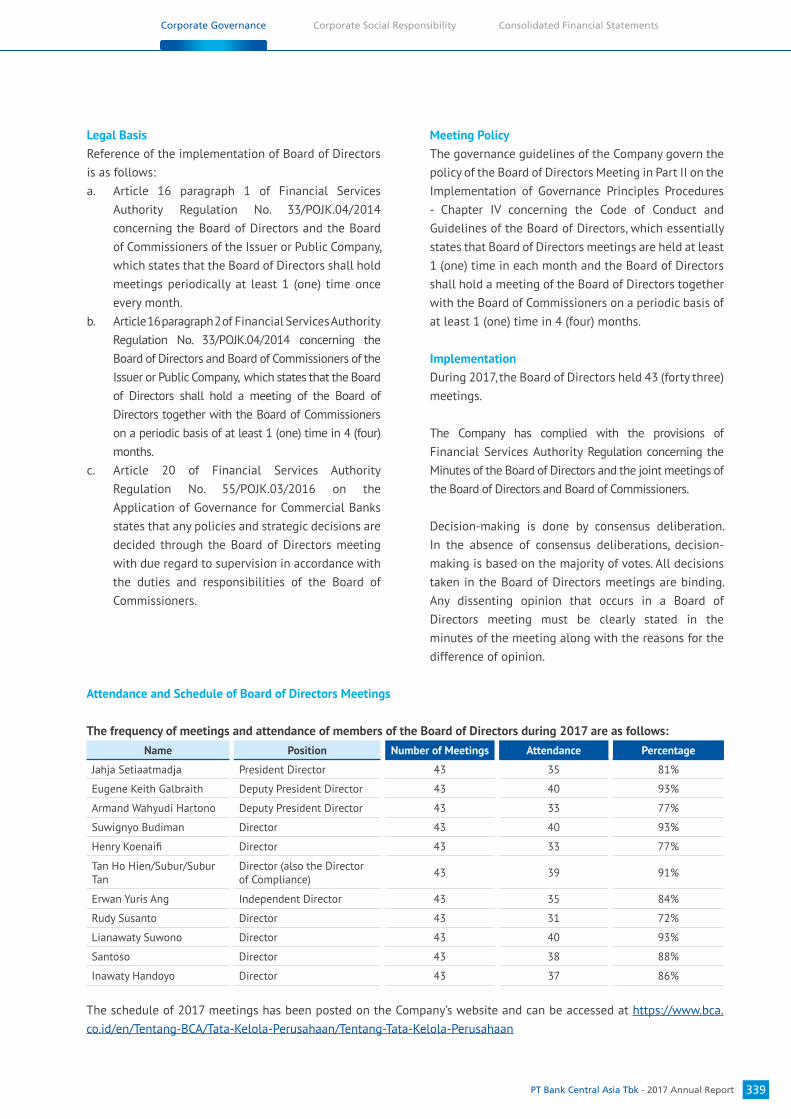

337 Meeting of Board of Commissioners, Board of Directors and Joint Meetings

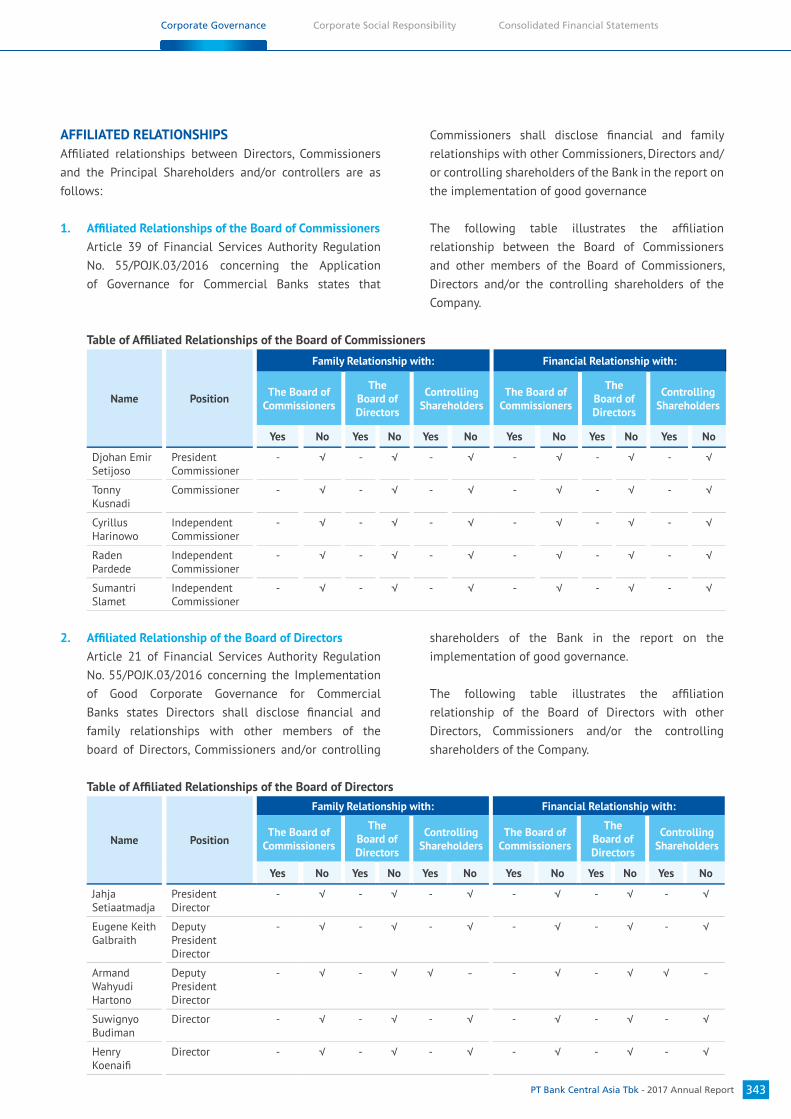

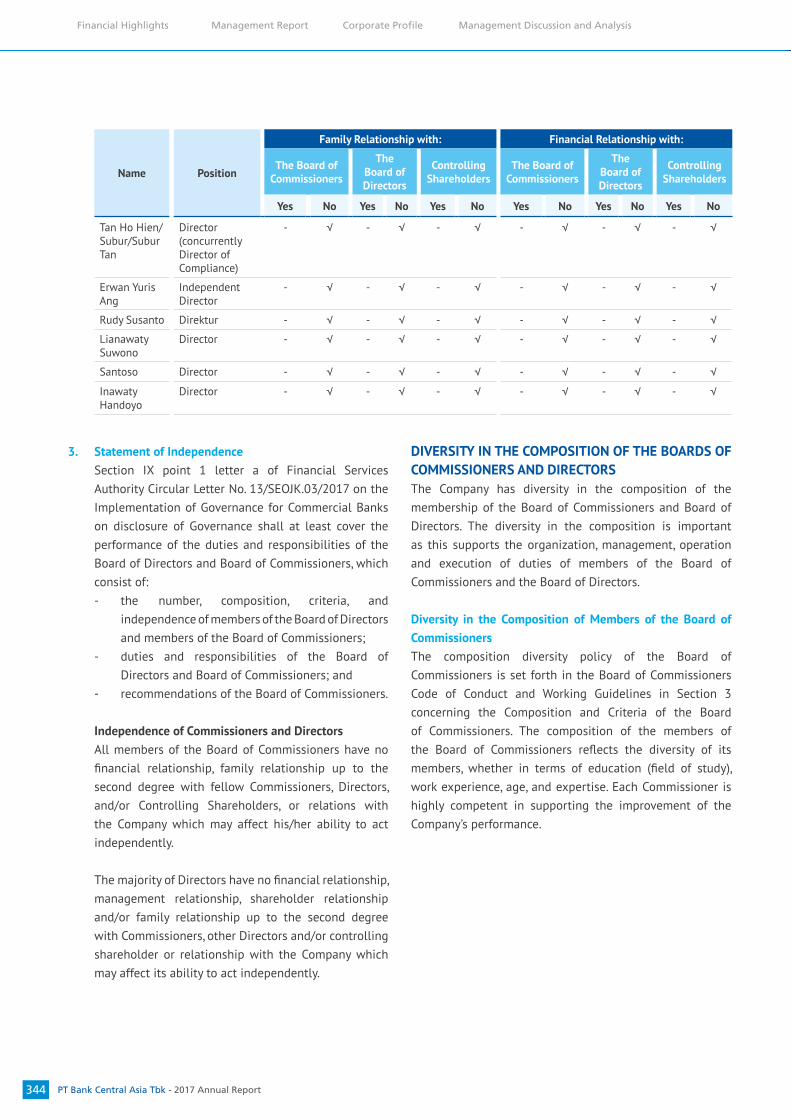

343 Affiliated Relationship

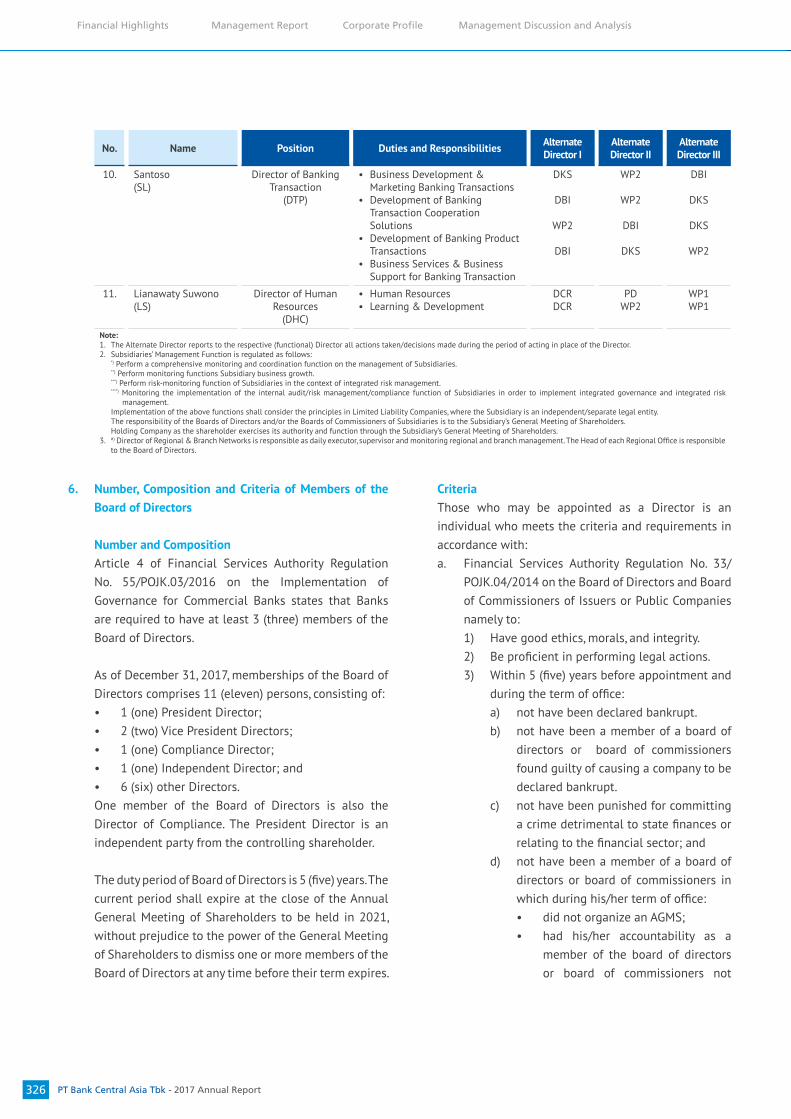

344 Diversity in The Composition of the Boards of Commissioners and Directors

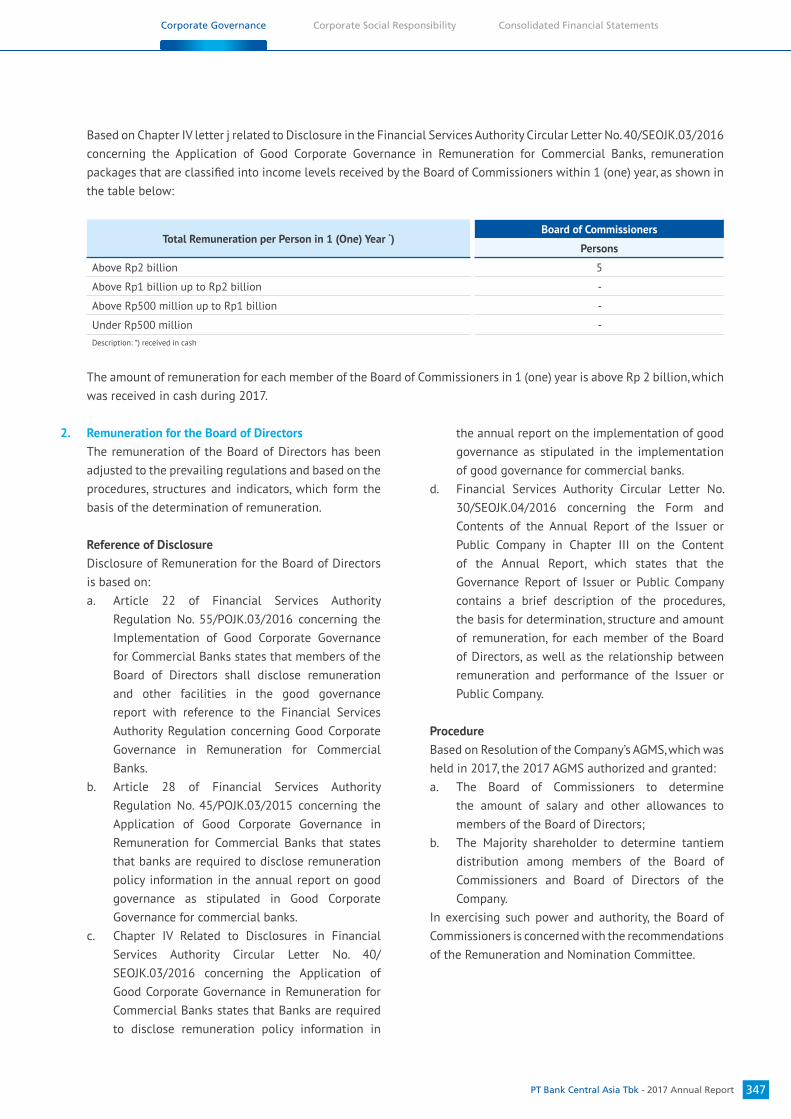

345 Remuneration Policy

356 Committees Under Board of Commissioners

371 Executive Committees of Board of Directors

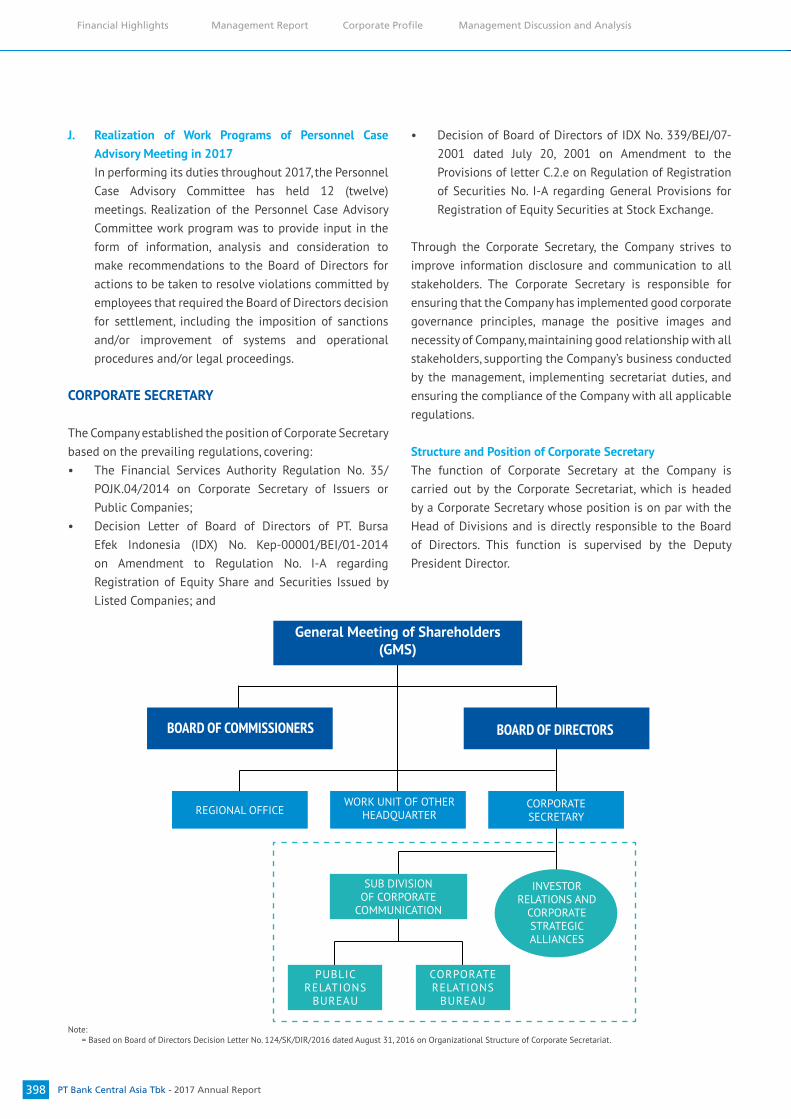

398 Corporate Secretary

404 Internal Audit

408 Public Accountant Firm (External Auditor)

409 Compliance Function

411 Implementation of Risk Management

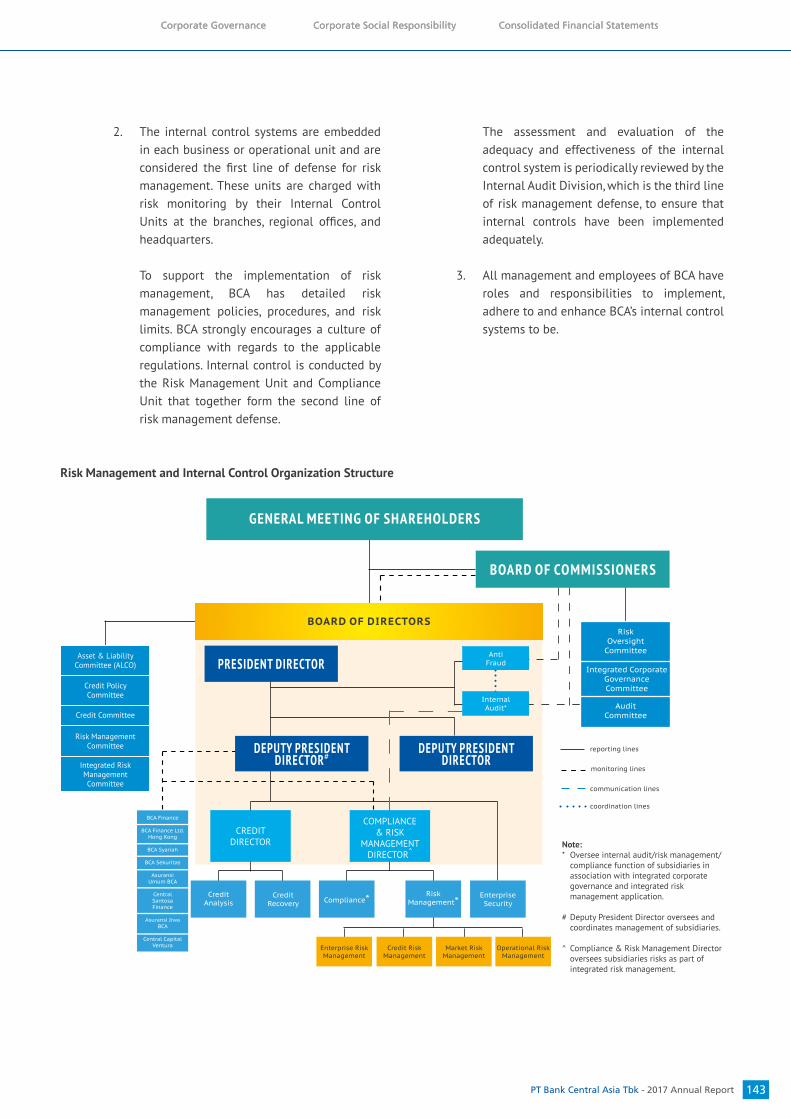

417 Internal Control System

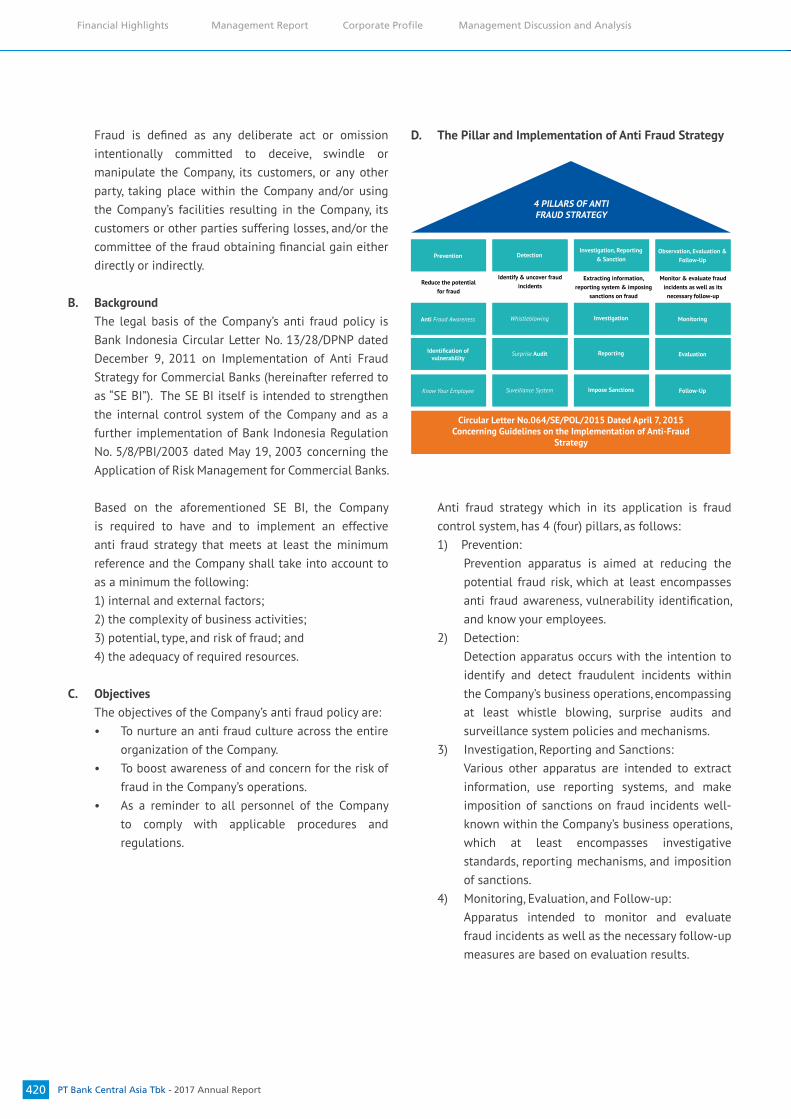

419 Corruption Prevention

424 Affiliated Transactions & Transactions with Conflict of Interest

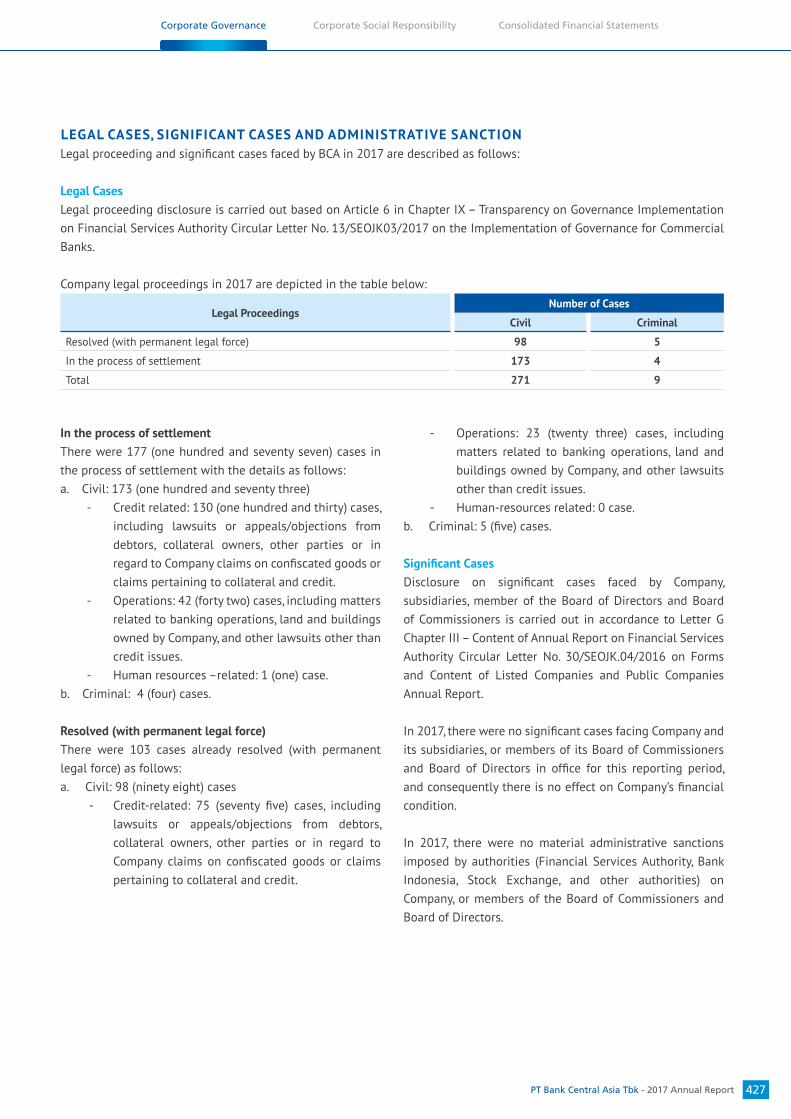

427 Legal Cases, Significant Cases and Administrative Saction

428 Access to Information and Corporate Data

443 Code of Conduct

445 Corporate Culture

446 Stock Option Plan

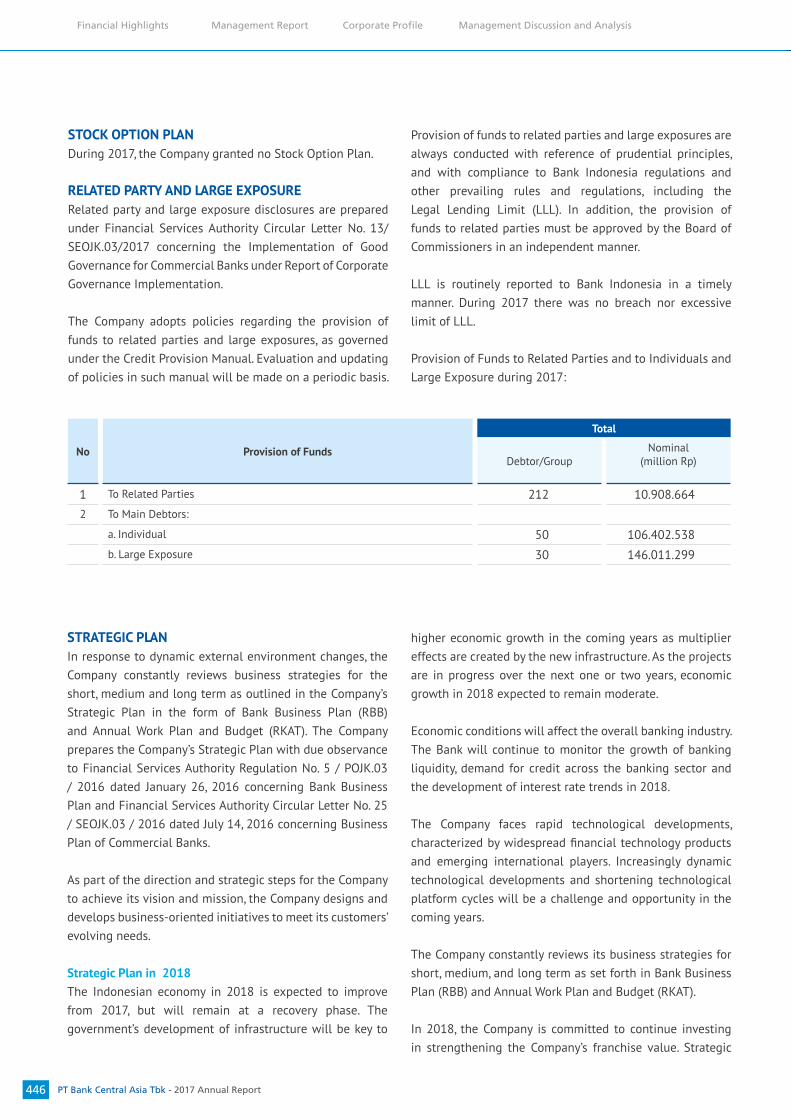

446 Related Party And Large Exposure

446 Strategic Plan

448 Transparency of Financial and Non-Financial Conditions Undisclosed in other Reports

449 Shares Buy Back

450 Provision of Funds for Social Activities

450 Provision of Funds for Political Activities

450 Implementation of Integrated Governance

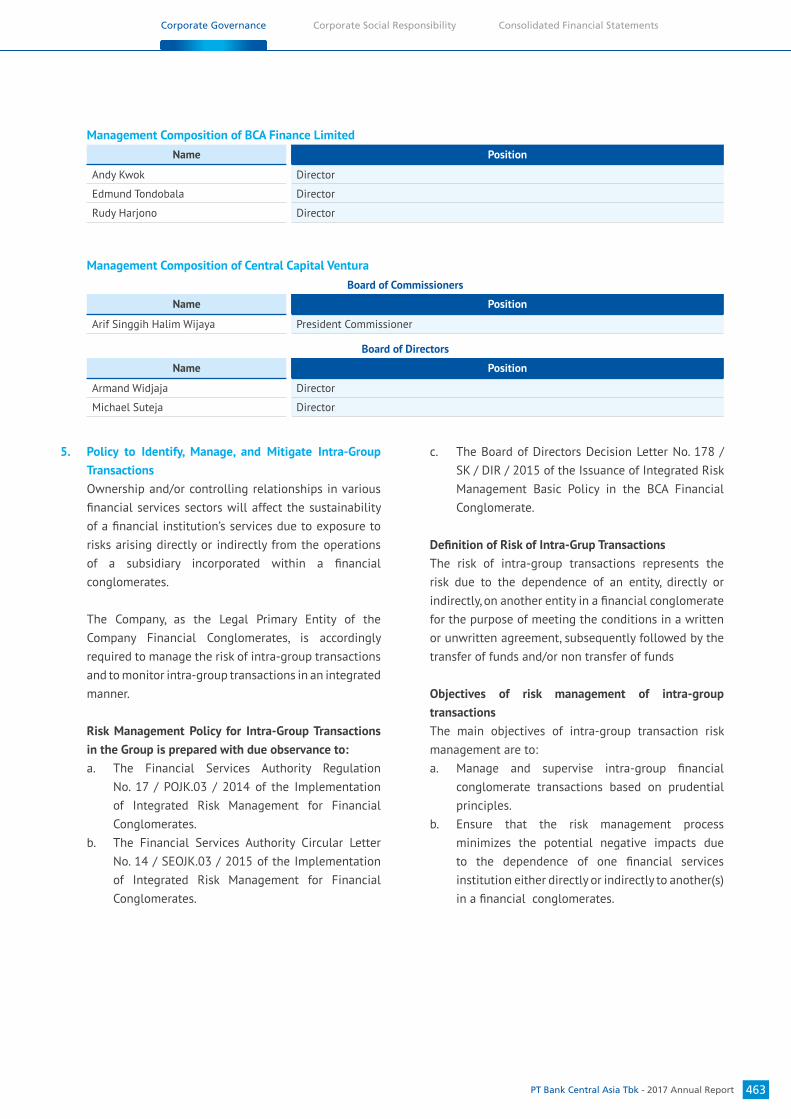

05

493 Consolidated Financial Statements

06

07

136 Business Support136 Risk Management

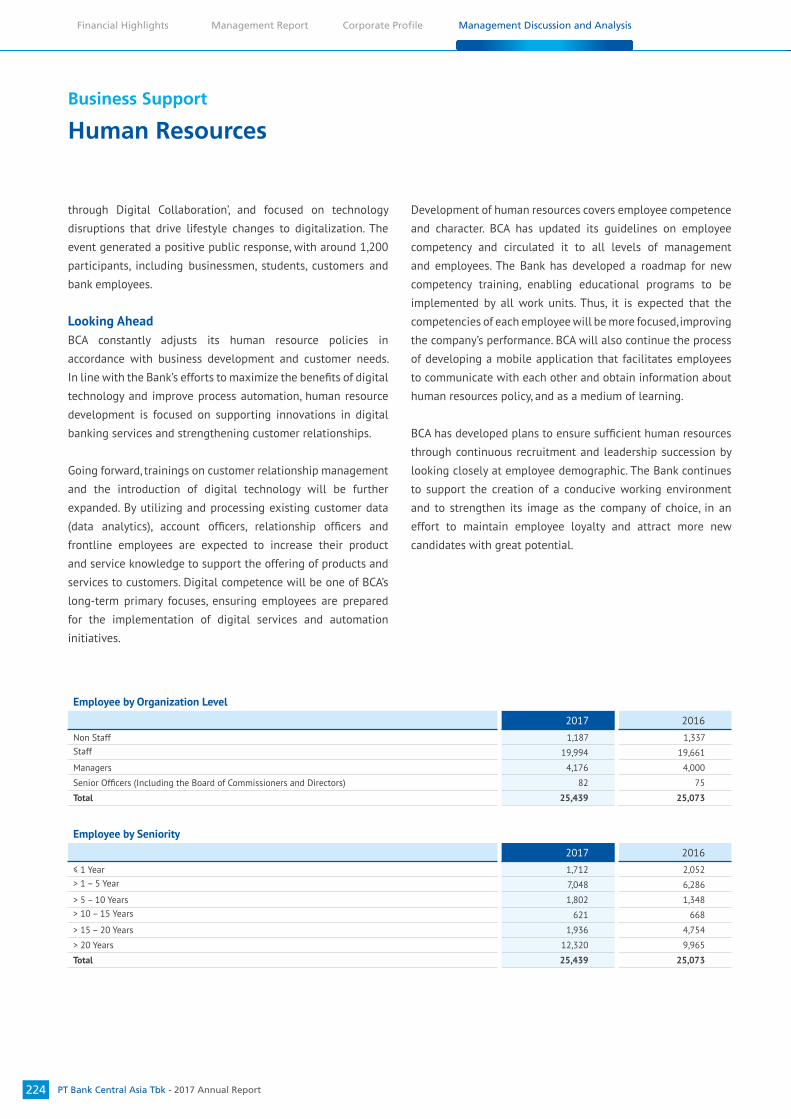

220 Human Resources

226 Network and Operation

230 Information Technology

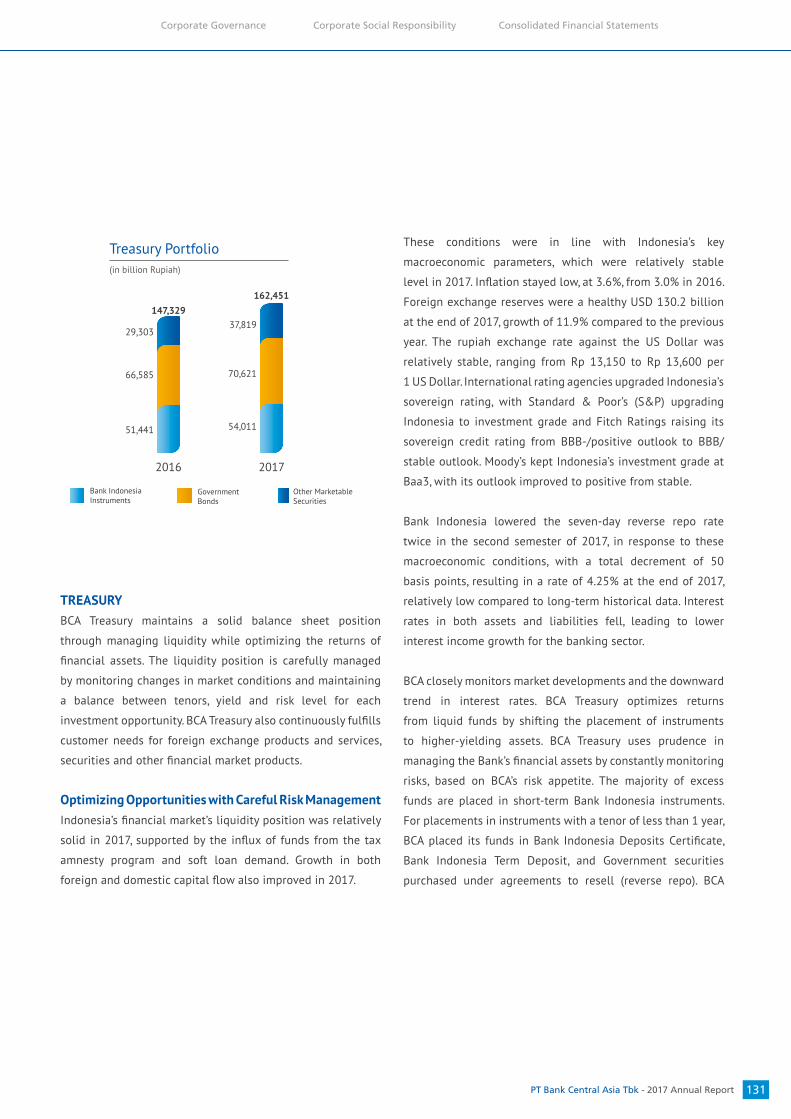

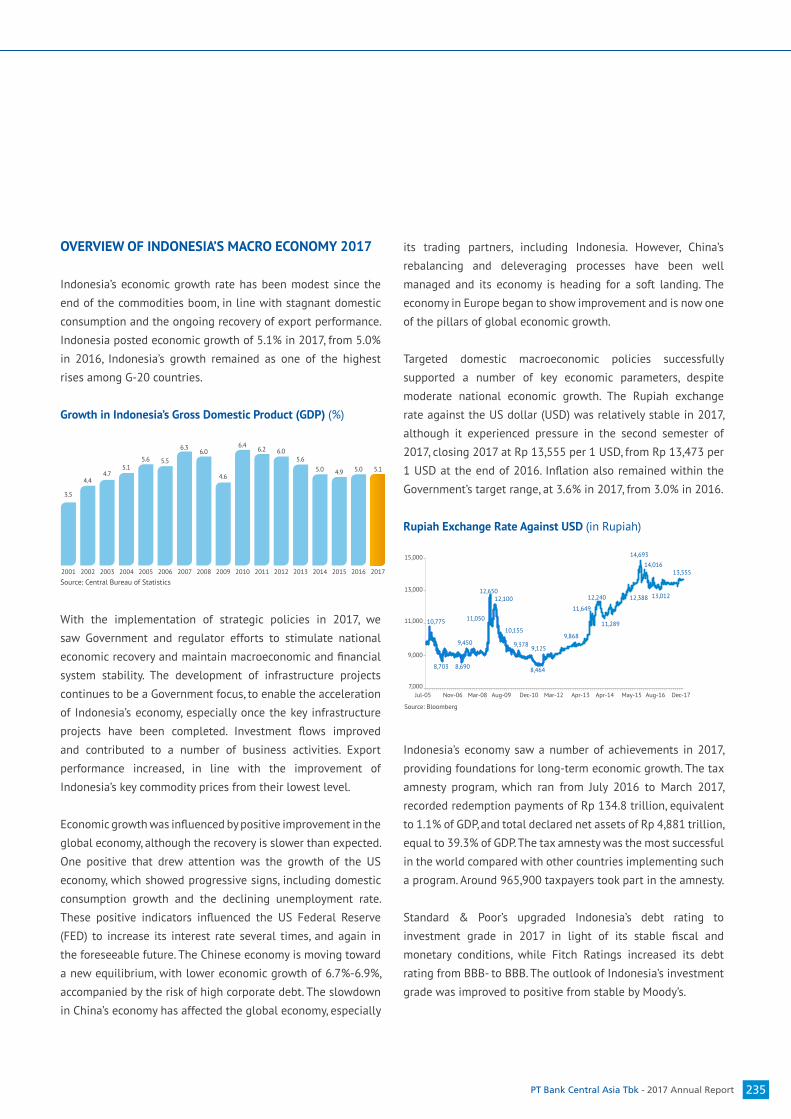

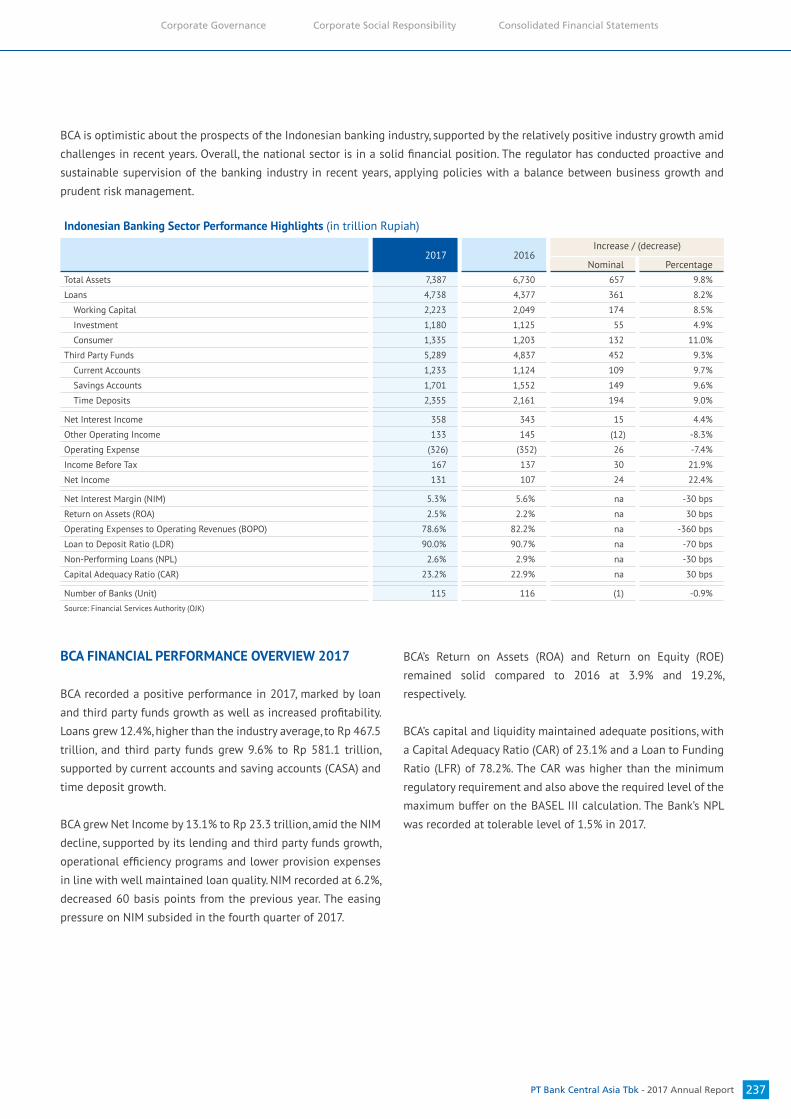

234 Financial Review235 Overview of Indonesia’s Macro Economy 2017

236 Indonesian Banking Sector Performance Overview 2017

237 BCA Financial Performance Overview 2017

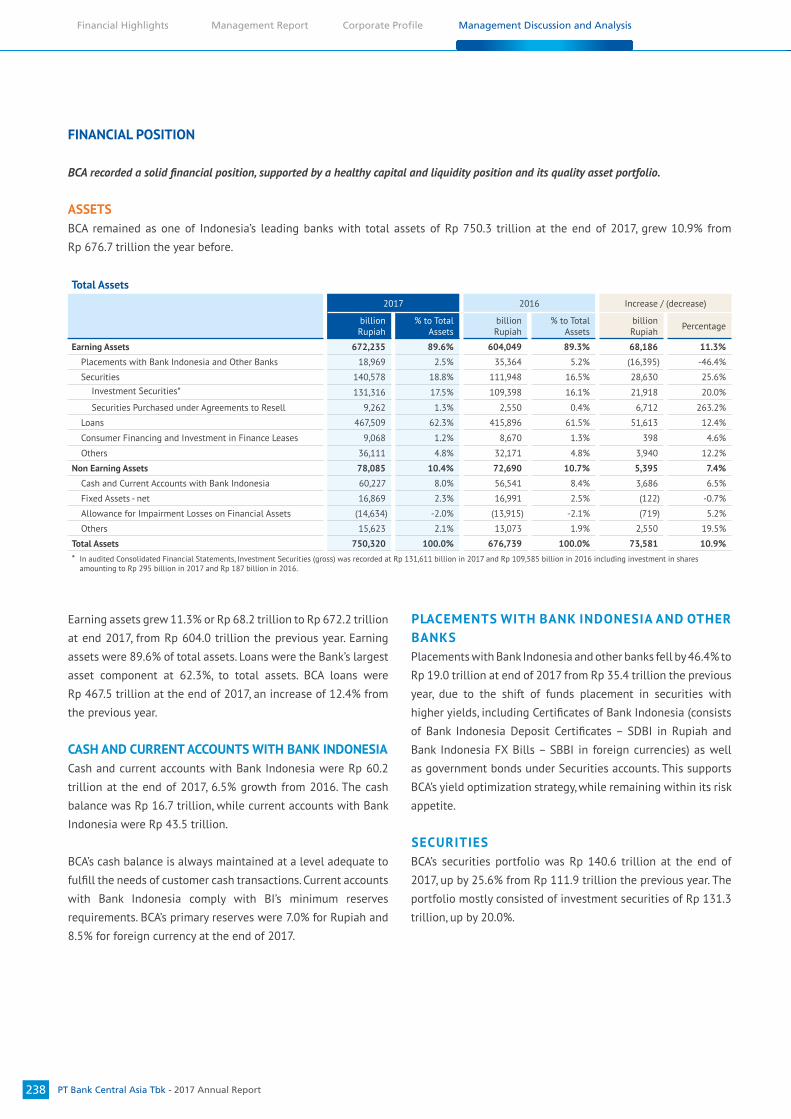

238 • Financial Position

238 - Assets

244 - Liabilities

248 - Equity

248 • Profit or Loss Statements

248 - Net Interest Income

251 - Operating Income other than Interest

252 - Operating Expenses

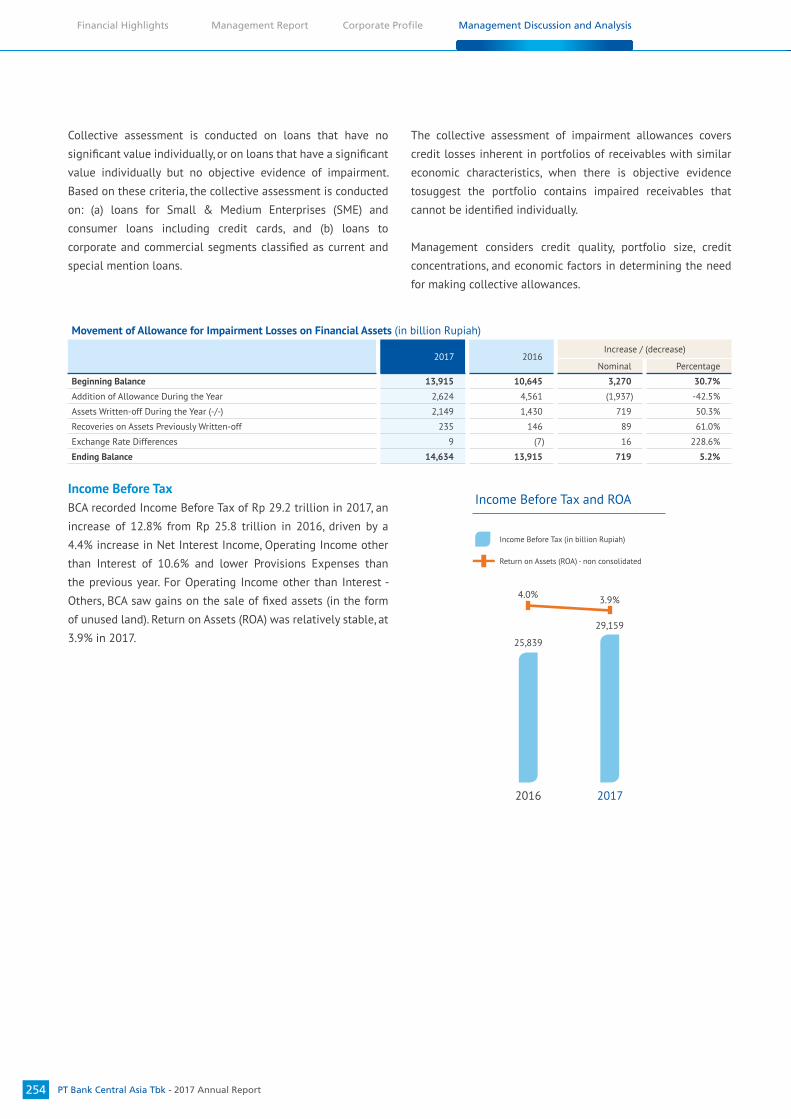

253 - Allowance for Impairment Losses on Financial Assets

254 - Income Before Tax

255 - Net Income

255 - Statements of Comprehensive Income

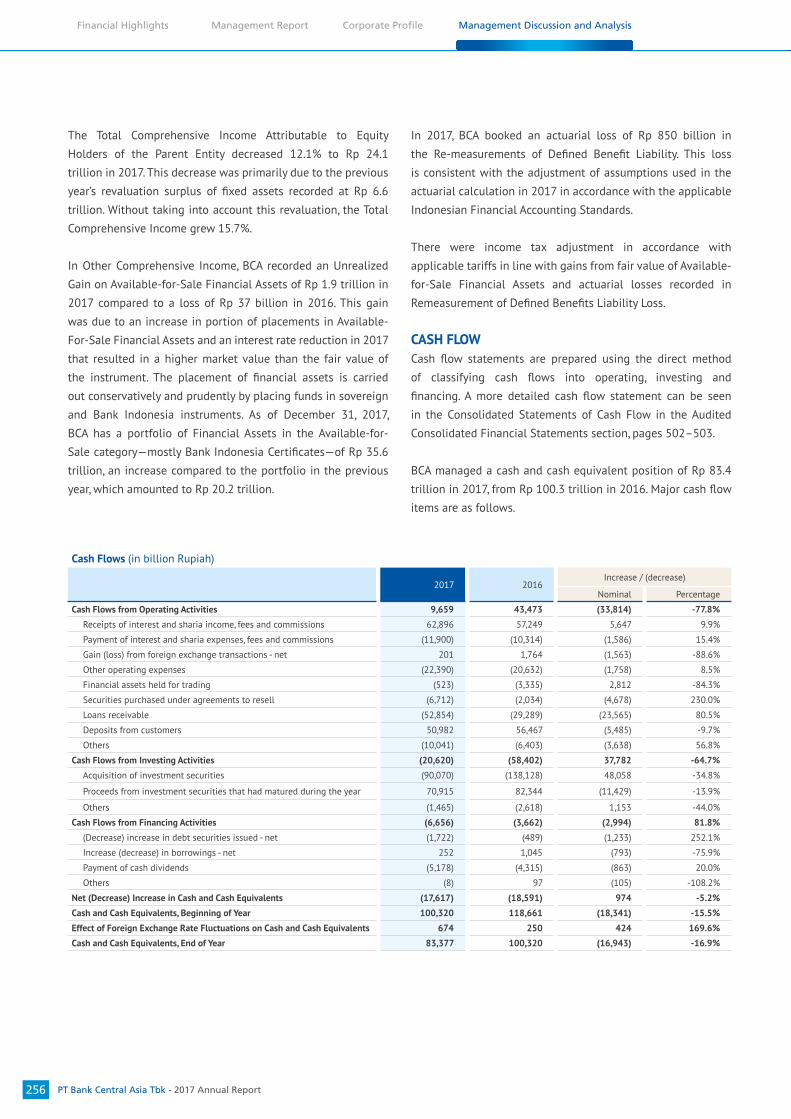

256 • Cash Flow

258 • Financial Ratios

260 Target Achievements in 2017

260 Capital Structure and Management Policy

260 • Capital Policy

260 • Capital Adequacy and Dividend Policy

261 • Capital Requirement of Subsidiaries

261 • BCA Capital Position

261 Material Information about Investment, Expansion, Divestment and Aquisition

262 Information on Material Transactions with Conflicts of Interest

262 Group-Wide Funding Commitments and Other Facilities to Single Outside Debtor

262 Impact of Changes in Laws and Regulations

263 Changes in Accounting Policies

263 Prime Lending Rate

264 Material Commitments for Capital Expenditures

264 Capital Expenditure Realized in 2016 and 2017

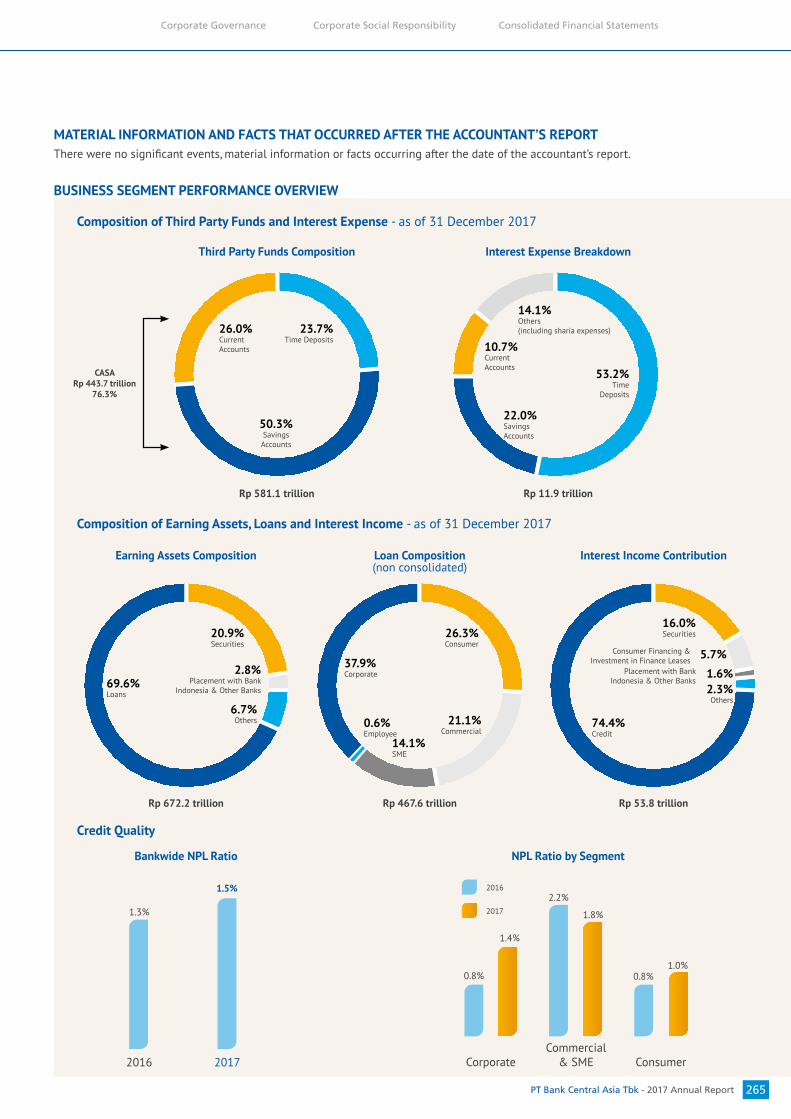

265Material Information and Facts that Occurred after the Date of Accountants’ Report

265 Business Segment Performance Overview

267 Marketing

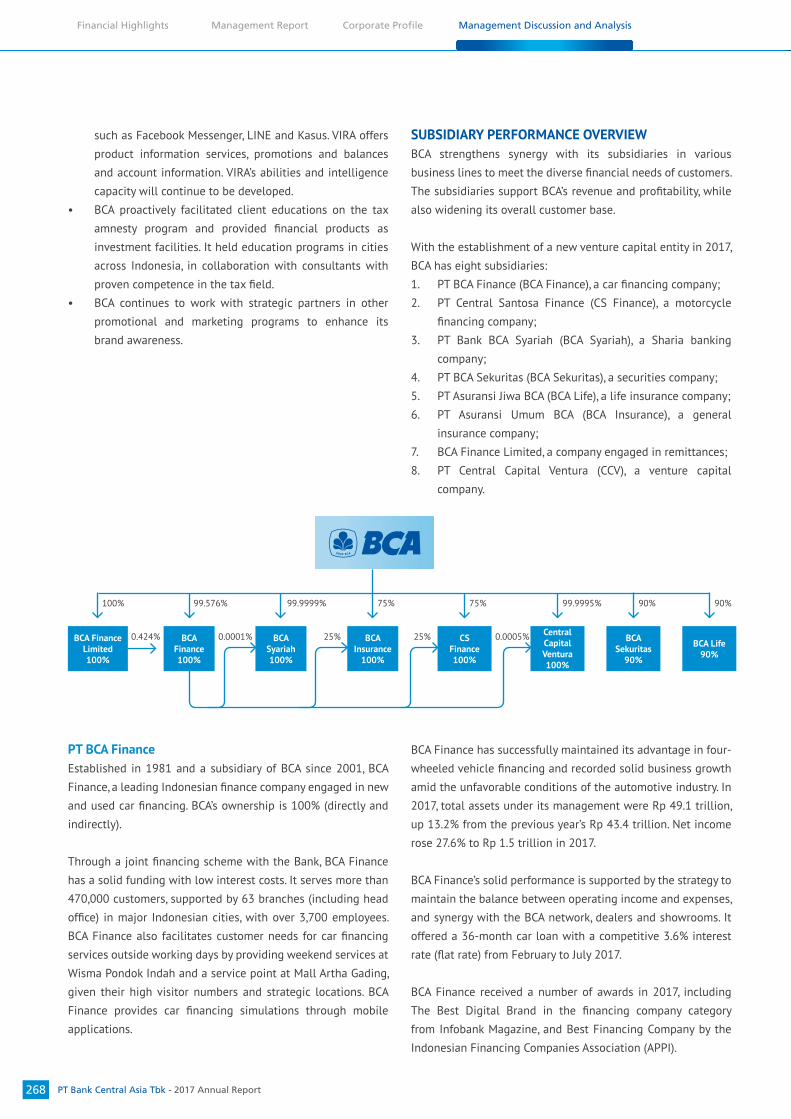

268 Subsidiary Performance Overview

270 Prospects and Strategic Priorities in 2018

270 • Indonesian Economy and Banking Sector Prospects in 2018

271 • BCA Business Prospects and Strategic Priorities in 2018

272 • Financial Projections in the 2018 Business Plan

272 Business Continuity

470 Corporate Social Responsibility

PT Bank Central Asia Tbk - 2017 Annual Report4

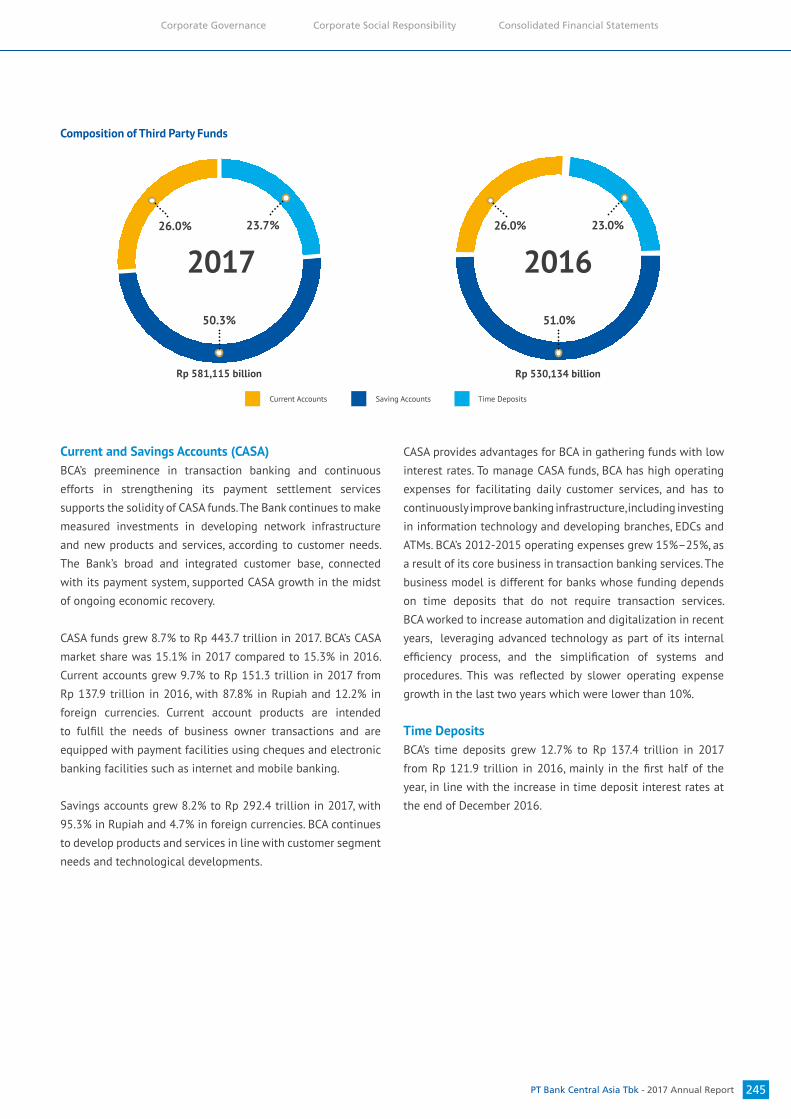

2017 provided both challenges and

opportunities for the banking industry

in Indonesia, and BCA specifically. Throughout the year, BCA invested in infrastructure and resources to

strengthen its core transaction

banking and lending business.

BCA continues to adapt, embracing technological advances and capturing

business opportunities, while maintaining a prudent approach to

business. The Bank always prioritizes

the comfort of its customers by

providing convenient, secure and reliable services at all times.

With the loyal support of its

customers, BCA successfully delivered a year of strong financial performance and maintained its position as the

bank of choice in Indonesia.

TRUSTTHROUGHQUALITY

PT Bank Central Asia Tbk - 2017 Annual Report 5

Adapting to Customer Preferences

Leveraging on technology advancement, BCA consistently refines its banking products and services to fit customer needs. Adoption of the latest technology supports automation in every business line, enhancing operational efficiency.

Improving the Quality of Our People

The collective contribution of employees at all levels of the organization is key to maintaining customer trust and providing quality service to customers. BCA thus remains committed to the development of employee competences and skills throughout the head office, regions and branches. In the past couple of years we have emphasized nurturing innovation and the ability to build strong relationships with customers.

Recruitment

People regeneration to maintain and

further develop BCA’s competitive advantages

Enhancing the capabilities of our people to enable

continuous innovation and promptly adapt to changes

Competitive remuneration and appreciation for

high-performing employees

Conducive work environment with emphasis on work-life

balance toward higher employee productivity

Development

Work Environment

Appreciation

PT Bank Central Asia Tbk - 2017 Annual Report10

Maintaining Sustainable Performance

Upholding professionalism in providing banking services has built customer trust. In that regard, the Bank’s transaction payment services and intermediary function continue to grow, enabling it to achieve solid financial performance.

PT Bank Central Asia Tbk - 2017 Annual Report 11

BCA continuously develops its intermediary function, promoting quality loan growth by exploring business opportunities and utilizing capacities

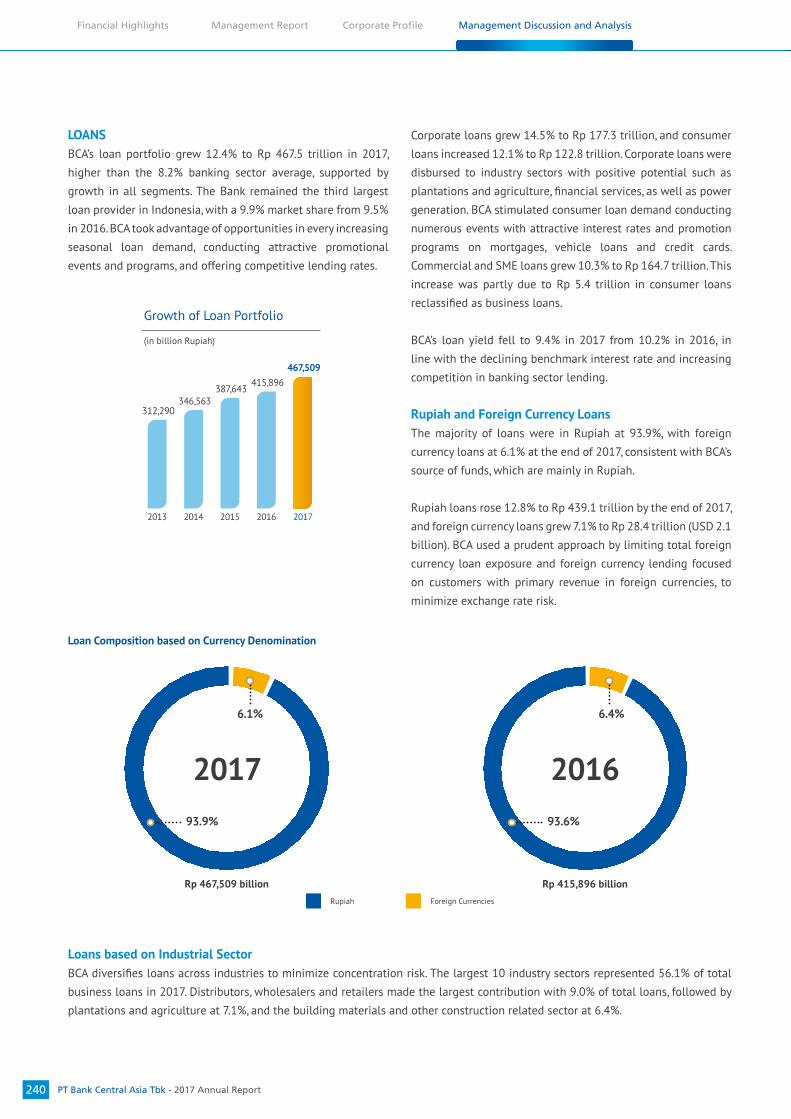

Growth in 2017

Loan Portfolio

12.4%

The development of payment settlement services plays an important role in strengthening BCA’s funding position

Growth in 2017

Third Party Funds

9.6%

The effort to enhance efficiency and healthy loan quality sustains BCA’s profitability

Growth in 2017

Net Income

13.1%

PT Bank Central Asia Tbk - 2017 Annual Report12

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

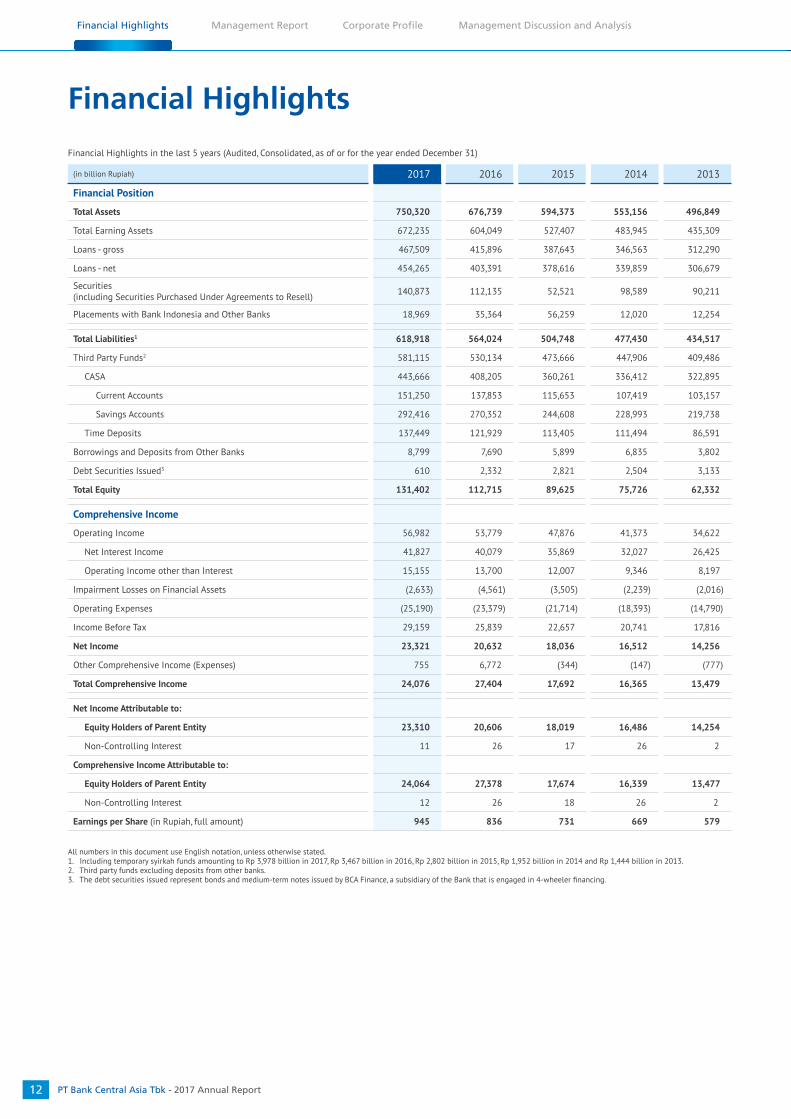

Financial Highlights

(in billion Rupiah) 2017 2016 2015 2014 2013

Financial Position

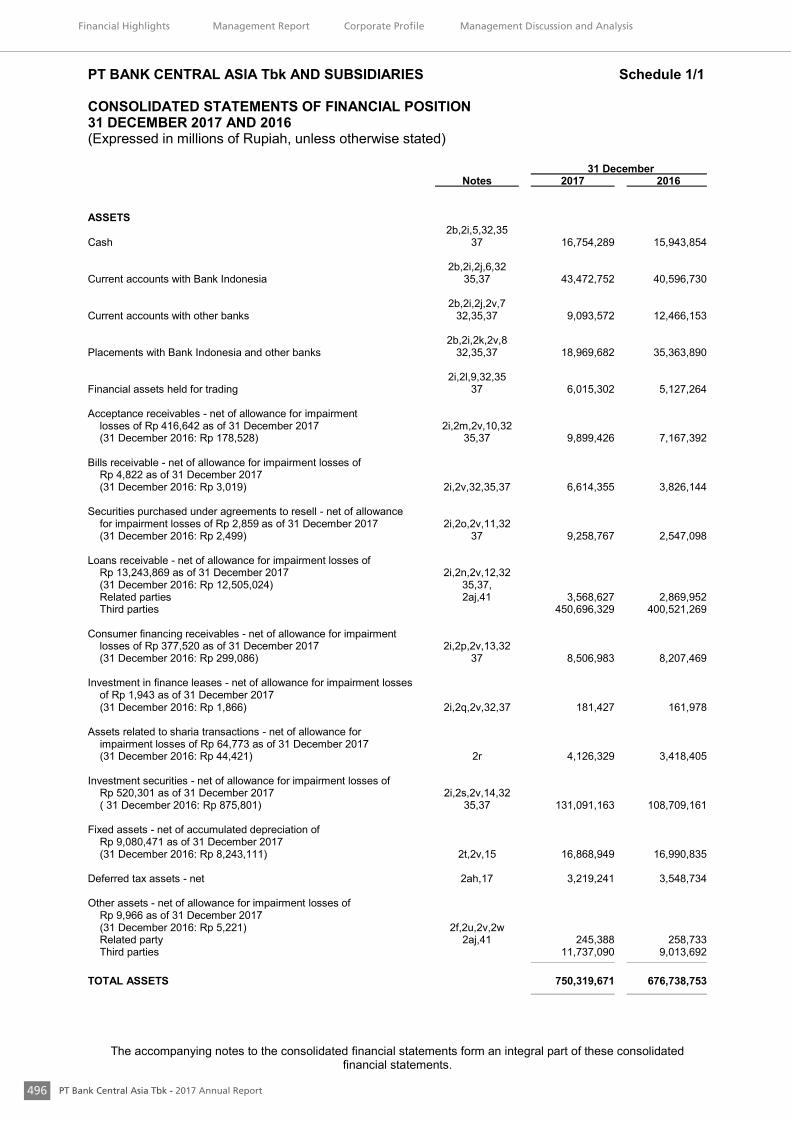

Total Assets 750,320 676,739 594,373 553,156 496,849

Total Earning Assets 672,235 604,049 527,407 483,945 435,309

Loans - gross 467,509 415,896 387,643 346,563 312,290

Loans - net 454,265 403,391 378,616 339,859 306,679

Securities (including Securities Purchased Under Agreements to Resell) 140,873 112,135 52,521 98,589 90,211

Placements with Bank Indonesia and Other Banks 18,969 35,364 56,259 12,020 12,254

Total Liabilities1 618,918 564,024 504,748 477,430 434,517

Third Party Funds2 581,115 530,134 473,666 447,906 409,486

CASA 443,666 408,205 360,261 336,412 322,895

Current Accounts 151,250 137,853 115,653 107,419 103,157

Savings Accounts 292,416 270,352 244,608 228,993 219,738

Time Deposits 137,449 121,929 113,405 111,494 86,591

Borrowings and Deposits from Other Banks 8,799 7,690 5,899 6,835 3,802

Debt Securities Issued3 610 2,332 2,821 2,504 3,133

Total Equity 131,402 112,715 89,625 75,726 62,332

Comprehensive Income

Operating Income 56,982 53,779 47,876 41,373 34,622

Net Interest Income 41,827 40,079 35,869 32,027 26,425

Operating Income other than Interest 15,155 13,700 12,007 9,346 8,197

Impairment Losses on Financial Assets (2,633) (4,561) (3,505) (2,239) (2,016)

Operating Expenses (25,190) (23,379) (21,714) (18,393) (14,790)

Income Before Tax 29,159 25,839 22,657 20,741 17,816

Net Income 23,321 20,632 18,036 16,512 14,256

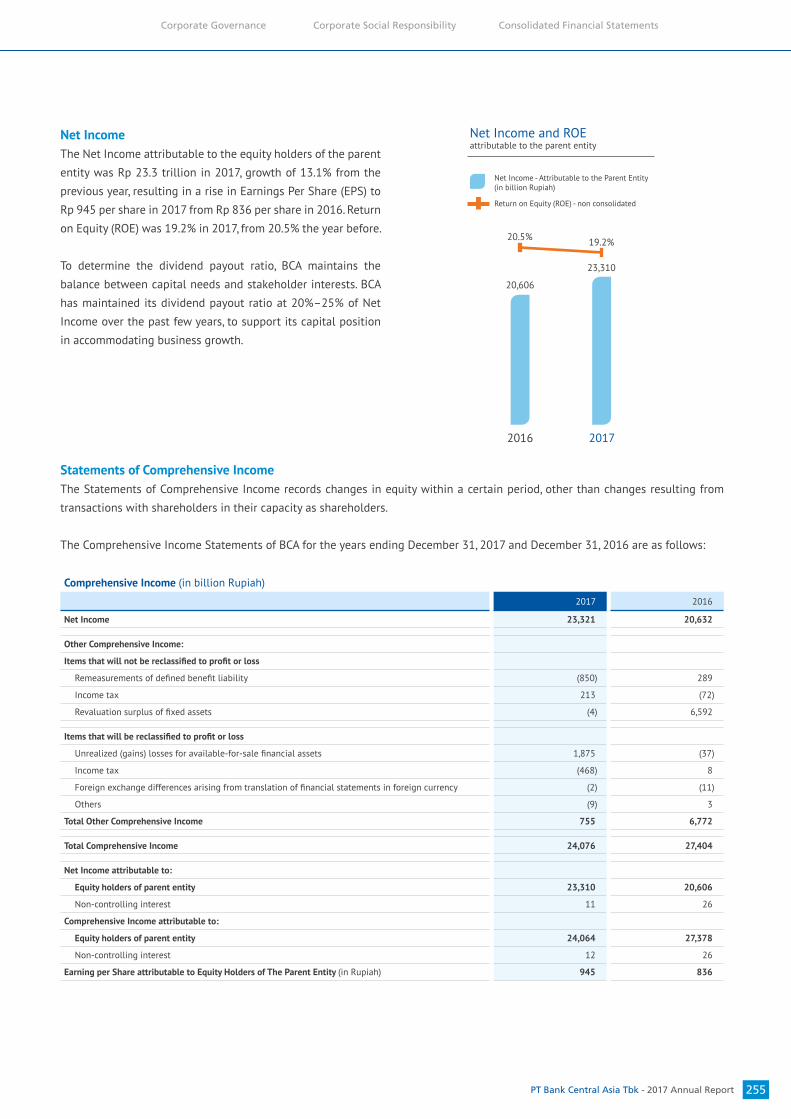

Other Comprehensive Income (Expenses) 755 6,772 (344) (147) (777)

Total Comprehensive Income 24,076 27,404 17,692 16,365 13,479

Net Income Attributable to:

Equity Holders of Parent Entity 23,310 20,606 18,019 16,486 14,254

Non-Controlling Interest 11 26 17 26 2

Comprehensive Income Attributable to:

Equity Holders of Parent Entity 24,064 27,378 17,674 16,339 13,477

Non-Controlling Interest 12 26 18 26 2

Earnings per Share (in Rupiah, full amount) 945 836 731 669 579

Financial Highlights in the last 5 years (Audited, Consolidated, as of or for the year ended December 31)

All numbers in this document use English notation, unless otherwise stated.1. Including temporary syirkah funds amounting to Rp 3,978 billion in 2017, Rp 3,467 billion in 2016, Rp 2,802 billion in 2015, Rp 1,952 billion in 2014 and Rp 1,444 billion in 2013.2. Third party funds excluding deposits from other banks.3. The debt securities issued represent bonds and medium-term notes issued by BCA Finance, a subsidiary of the Bank that is engaged in 4-wheeler financing.

PT Bank Central Asia Tbk - 2017 Annual Report 13

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

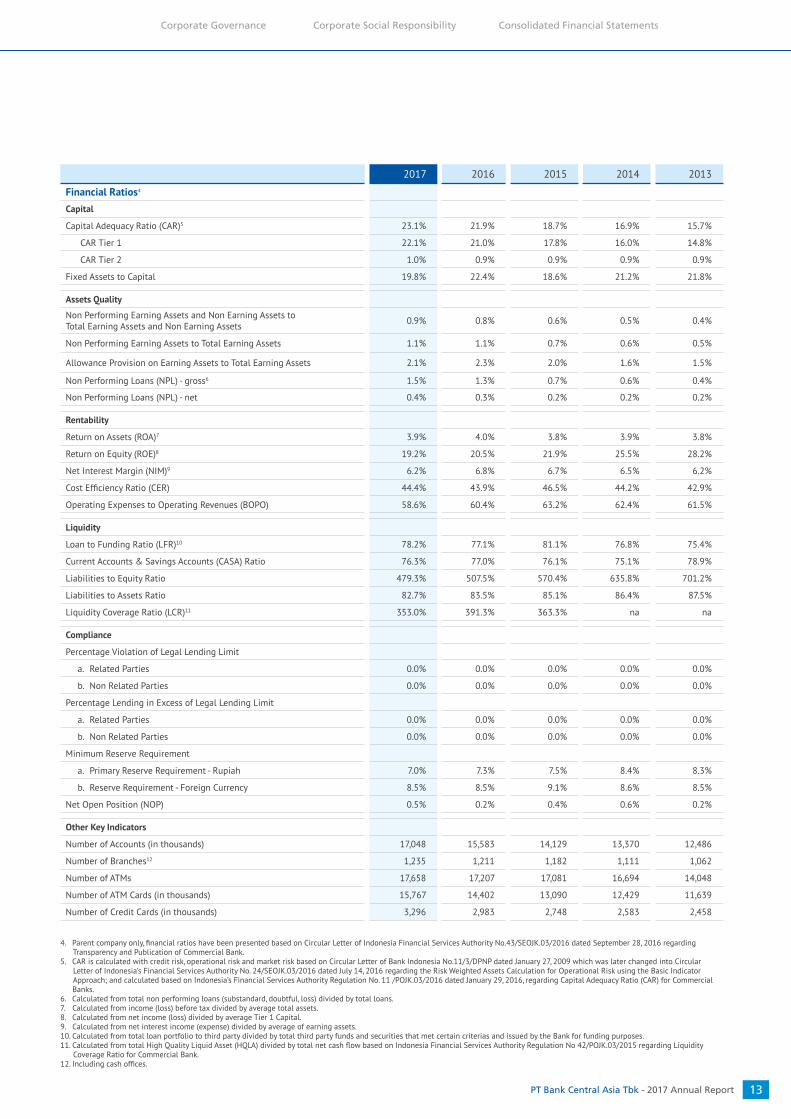

2017 2016 2015 2014 2013

Financial Ratios4

Capital

Capital Adequacy Ratio (CAR)5 23.1% 21.9% 18.7% 16.9% 15.7%

CAR Tier 1 22.1% 21.0% 17.8% 16.0% 14.8%

CAR Tier 2 1.0% 0.9% 0.9% 0.9% 0.9%

Fixed Assets to Capital 19.8% 22.4% 18.6% 21.2% 21.8%

Assets Quality

Non Performing Earning Assets and Non Earning Assets to Total Earning Assets and Non Earning Assets

0.9% 0.8% 0.6% 0.5% 0.4%

Non Performing Earning Assets to Total Earning Assets 1.1% 1.1% 0.7% 0.6% 0.5%

Allowance Provision on Earning Assets to Total Earning Assets 2.1% 2.3% 2.0% 1.6% 1.5%

Non Performing Loans (NPL) - gross6 1.5% 1.3% 0.7% 0.6% 0.4%

Non Performing Loans (NPL) - net 0.4% 0.3% 0.2% 0.2% 0.2%

Rentability

Return on Assets (ROA)7 3.9% 4.0% 3.8% 3.9% 3.8%

Return on Equity (ROE)8 19.2% 20.5% 21.9% 25.5% 28.2%

Net Interest Margin (NIM)9 6.2% 6.8% 6.7% 6.5% 6.2%

Cost Efficiency Ratio (CER) 44.4% 43.9% 46.5% 44.2% 42.9%

Operating Expenses to Operating Revenues (BOPO) 58.6% 60.4% 63.2% 62.4% 61.5%

Liquidity

Loan to Funding Ratio (LFR)10 78.2% 77.1% 81.1% 76.8% 75.4%

Current Accounts & Savings Accounts (CASA) Ratio 76.3% 77.0% 76.1% 75.1% 78.9%

Liabilities to Equity Ratio 479.3% 507.5% 570.4% 635.8% 701.2%

Liabilities to Assets Ratio 82.7% 83.5% 85.1% 86.4% 87.5%

Liquidity Coverage Ratio (LCR)11 353.0% 391.3% 363.3% na na

Compliance

Percentage Violation of Legal Lending Limit

a. Related Parties 0.0% 0.0% 0.0% 0.0% 0.0%

b. Non Related Parties 0.0% 0.0% 0.0% 0.0% 0.0%

Percentage Lending in Excess of Legal Lending Limit

a. Related Parties 0.0% 0.0% 0.0% 0.0% 0.0%

b. Non Related Parties 0.0% 0.0% 0.0% 0.0% 0.0%

Minimum Reserve Requirement

a. Primary Reserve Requirement - Rupiah 7.0% 7.3% 7.5% 8.4% 8.3%

b. Reserve Requirement - Foreign Currency 8.5% 8.5% 9.1% 8.6% 8.5%

Net Open Position (NOP) 0.5% 0.2% 0.4% 0.6% 0.2%

Other Key Indicators

Number of Accounts (in thousands) 17,048 15,583 14,129 13,370 12,486

Number of Branches12 1,235 1,211 1,182 1,111 1,062

Number of ATMs 17,658 17,207 17,081 16,694 14,048

Number of ATM Cards (in thousands) 15,767 14,402 13,090 12,429 11,639

Number of Credit Cards (in thousands) 3,296 2,983 2,748 2,583 2,458

4. Parent company only, financial ratios have been presented based on Circular Letter of Indonesia Financial Services Authority No.43/SEOJK.03/2016 dated September 28, 2016 regarding Transparency and Publication of Commercial Bank.5. CAR is calculated with credit risk, operational risk and market risk based on Circular Letter of Bank Indonesia No.11/3/DPNP dated January 27, 2009 which was later changed into Circular Letter of Indonesia’s Financial Services Authority No. 24/SEOJK.03/2016 dated July 14, 2016 regarding the Risk Weighted Assets Calculation for Operational Risk using the Basic Indicator Approach; and calculated based on Indonesia’s Financial Services Authority Regulation No. 11 /POJK.03/2016 dated January 29, 2016, regarding Capital Adequacy Ratio (CAR) for Commercial

Banks.6. Calculated from total non performing loans (substandard, doubtful, loss) divided by total loans.7. Calculated from income (loss) before tax divided by average total assets.8. Calculated from net income (loss) divided by average Tier 1 Capital.9. Calculated from net interest income (expense) divided by average of earning assets.10. Calculated from total loan portfolio to third party divided by total third party funds and securities that met certain criterias and issued by the Bank for funding purposes.11. Calculated from total High Quality Liquid Asset (HQLA) divided by total net cash flow based on Indonesia Financial Services Authority Regulation No 42/POJK.03/2015 regarding Liquidity Coverage Ratio for Commercial Bank.12. Including cash offices.

PT Bank Central Asia Tbk - 2017 Annual Report14

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Financial Highlights - Continued

Total Assets

(in billion Rupiah)

Third Party Funds

(in billion Rupiah)

Operating Income

(in billion Rupiah)

Loans - gross

(in billion Rupiah)

Total Equity

(in billion Rupiah)

Net IncomeAttributable to Equity Holders of Parent Entity

(in billion Rupiah)

750,320

20172016

676,739594,373

2015

553,156

2014

496,849

2013

467,509

20172016

415,896 387,643

2015

346,563

2014

312,290

2013

581,115

20172016

530,134 473,666

2015

447,906

2014

409,486

2013

131,402

20172016

112,715

89,625

2015

75,726

2014

62,332

2013

56,982

20172016

53,779 47,876

2015

41,373

2014

34,622

2013

23,310

20172016

20,606 18,019

2015

16,486

2014

14,254

2013

PT Bank Central Asia Tbk - 2017 Annual Report 15

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

Return on Assets (ROA)

Net Interest Margin (NIM)

Loan to Funding Ratio (LFR)

Return on Equity (ROE)

Capital Adequacy Ratio (CAR)

Non-Performing Loans (NPL) - gross

3.9%

20172016

4.0%3.8%

2015

3.9%

2014

3.8%

2013

6.2%

20172016

6.8%6.7%

2015

6.5%

2014

6.2%

2013

78.2%

20172016

77.1%

81.1%

2015

76.8%

2014

75.4%

2013

19.2%

20172016

20.5%21.9%

2015

25.5%

2014

28.2%

2013

23.1%

20172016

21.9%

18.7%

2015

16.9%

2014

15.7%

2013

1.5%

20172016

1.3%

0.7%

2015

0.6%

2014

0.4%

2013

PT Bank Central Asia Tbk - 2017 Annual Report16

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

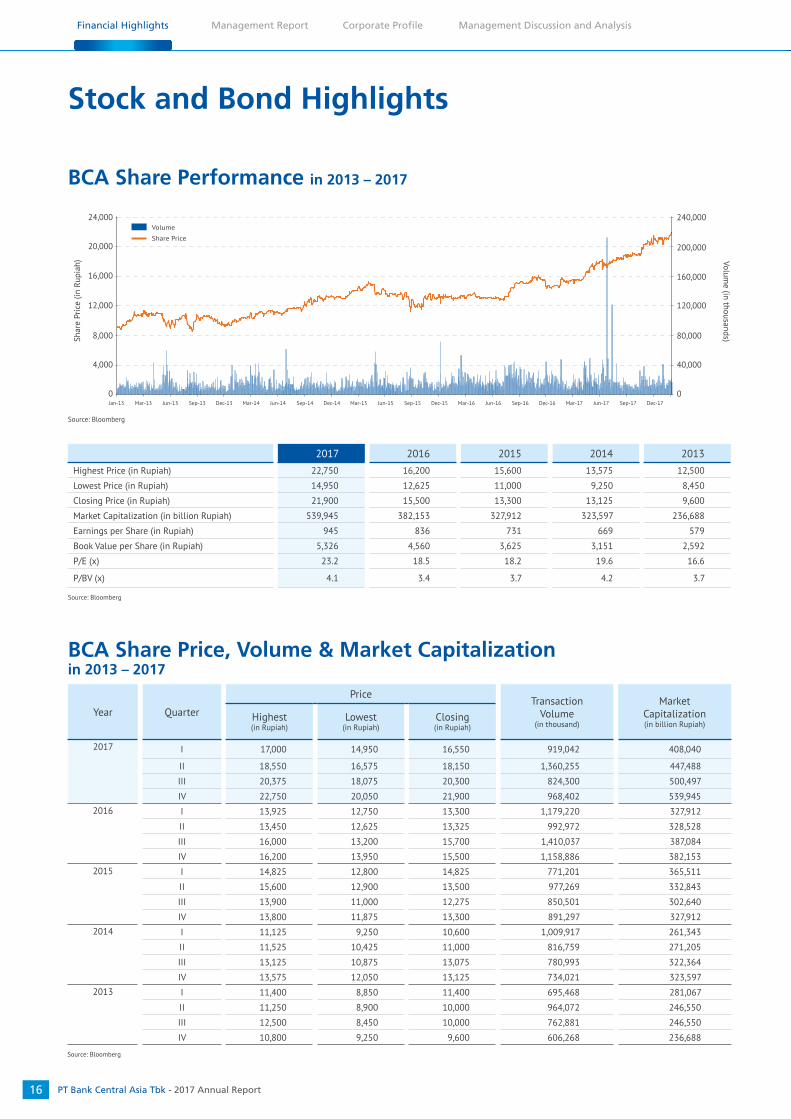

Stock and Bond Highlights

2017 2016 2015 2014 2013

Highest Price (in Rupiah) 22,750 16,200 15,600 13,575 12,500

Lowest Price (in Rupiah) 14,950 12,625 11,000 9,250 8,450

Closing Price (in Rupiah) 21,900 15,500 13,300 13,125 9,600

Market Capitalization (in billion Rupiah) 539,945 382,153 327,912 323,597 236,688

Earnings per Share (in Rupiah) 945 836 731 669 579

Book Value per Share (in Rupiah) 5,326 4,560 3,625 3,151 2,592

P/E (x) 23.2 18.5 18.2 19.6 16.6

P/BV (x) 4.1 3.4 3.7 4.2 3.7

Year Quarter

PriceTransaction

Volume(in thousand)

Market Capitalization(in billion Rupiah)

Highest(in Rupiah)

Lowest(in Rupiah)

Closing(in Rupiah)

2017 I 17,000 14,950 16,550 919,042 408,040

II 18,550 16,575 18,150 1,360,255 447,488

III 20,375 18,075 20,300 824,300 500,497

IV 22,750 20,050 21,900 968,402 539,945

2016 I 13,925 12,750 13,300 1,179,220 327,912

II 13,450 12,625 13,325 992,972 328,528

III 16,000 13,200 15,700 1,410,037 387,084

IV 16,200 13,950 15,500 1,158,886 382,153

2015 I 14,825 12,800 14,825 771,201 365,511

II 15,600 12,900 13,500 977,269 332,843

III 13,900 11,000 12,275 850,501 302,640

IV 13,800 11,875 13,300 891,297 327,912

2014 I 11,125 9,250 10,600 1,009,917 261,343

II 11,525 10,425 11,000 816,759 271,205

III 13,125 10,875 13,075 780,993 322,364

IV 13,575 12,050 13,125 734,021 323,597

2013 I 11,400 8,850 11,400 695,468 281,067

II 11,250 8,900 10,000 964,072 246,550

III 12,500 8,450 10,000 762,881 246,550

IV 10,800 9,250 9,600 606,268 236,688

Source: Bloomberg

Source: Bloomberg

BCA Share Price, Volume & Market Capitalizationin 2013 – 2017

BCA Share Performance in 2013 – 2017

Shar

e Pr

ice

(in R

upia

h)

24,000

20,000

16,000

12,000

8,000

4,000

0

Source: Bloomberg

0

40,000

80,000

120,000

160,000

200,000

240,000

Vo

lum

e (in

tho

usan

ds)

Share Price

Volume

Jun-13 Jun-14 Jun-15 Jun-16 Jun-17Mar-13 Mar-14 Mar-15 Mar-16 Mar-17Jan-13 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17Sep-13 Sep-14 Sep-15 Sep-16 Sep-17

PT Bank Central Asia Tbk - 2017 Annual Report 17

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

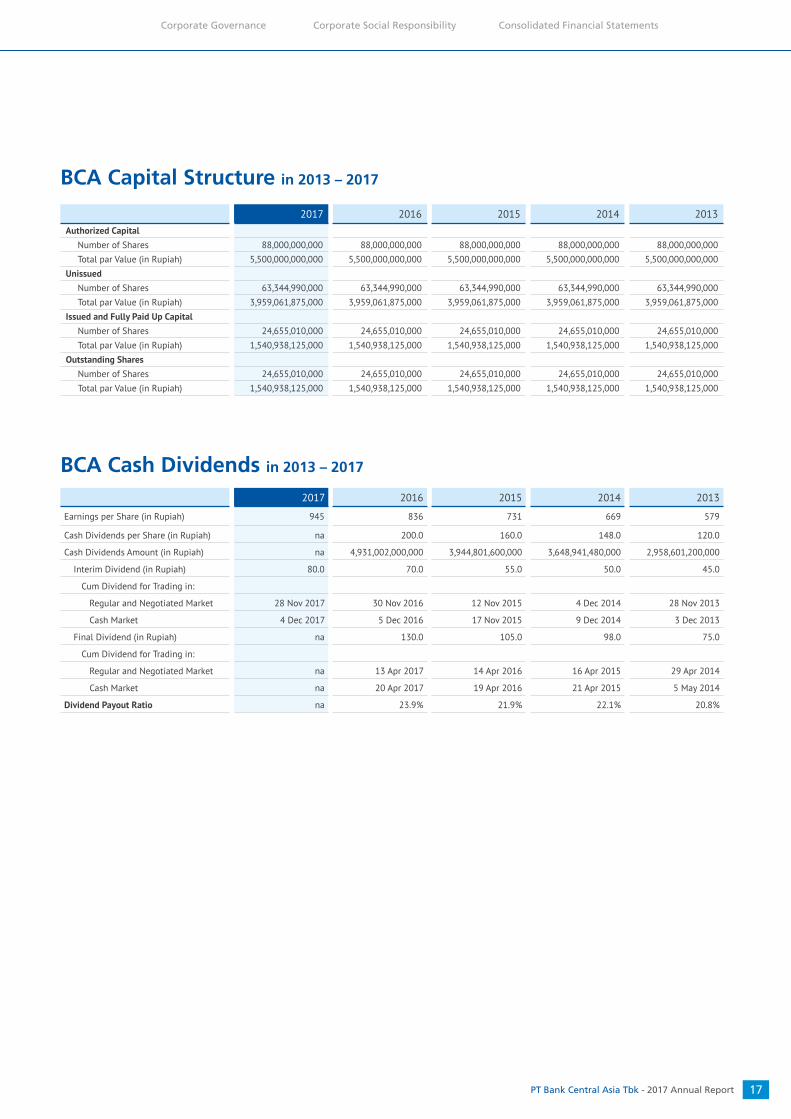

2017 2016 2015 2014 2013

Authorized Capital

Number of Shares 88,000,000,000 88,000,000,000 88,000,000,000 88,000,000,000 88,000,000,000 Total par Value (in Rupiah) 5,500,000,000,000 5,500,000,000,000 5,500,000,000,000 5,500,000,000,000 5,500,000,000,000 Unissued

Number of Shares 63,344,990,000 63,344,990,000 63,344,990,000 63,344,990,000 63,344,990,000 Total par Value (in Rupiah) 3,959,061,875,000 3,959,061,875,000 3,959,061,875,000 3,959,061,875,000 3,959,061,875,000 Issued and Fully Paid Up Capital

Number of Shares 24,655,010,000 24,655,010,000 24,655,010,000 24,655,010,000 24,655,010,000 Total par Value (in Rupiah) 1,540,938,125,000 1,540,938,125,000 1,540,938,125,000 1,540,938,125,000 1,540,938,125,000 Outstanding Shares

Number of Shares 24,655,010,000 24,655,010,000 24,655,010,000 24,655,010,000 24,655,010,000 Total par Value (in Rupiah) 1,540,938,125,000 1,540,938,125,000 1,540,938,125,000 1,540,938,125,000 1,540,938,125,000

BCA Capital Structure in 2013 – 2017

BCA Cash Dividends in 2013 – 2017

2017 2016 2015 2014 2013

Earnings per Share (in Rupiah) 945 836 731 669 579

Cash Dividends per Share (in Rupiah) na 200.0 160.0 148.0 120.0

Cash Dividends Amount (in Rupiah) na 4,931,002,000,000 3,944,801,600,000 3,648,941,480,000 2,958,601,200,000

Interim Dividend (in Rupiah) 80.0 70.0 55.0 50.0 45.0

Cum Dividend for Trading in:

Regular and Negotiated Market 28 Nov 2017 30 Nov 2016 12 Nov 2015 4 Dec 2014 28 Nov 2013

Cash Market 4 Dec 2017 5 Dec 2016 17 Nov 2015 9 Dec 2014 3 Dec 2013

Final Dividend (in Rupiah) na 130.0 105.0 98.0 75.0

Cum Dividend for Trading in:

Regular and Negotiated Market na 13 Apr 2017 14 Apr 2016 16 Apr 2015 29 Apr 2014

Cash Market na 20 Apr 2017 19 Apr 2016 21 Apr 2015 5 May 2014

Dividend Payout Ratio na 23.9% 21.9% 22.1% 20.8%

PT Bank Central Asia Tbk - 2017 Annual Report18

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

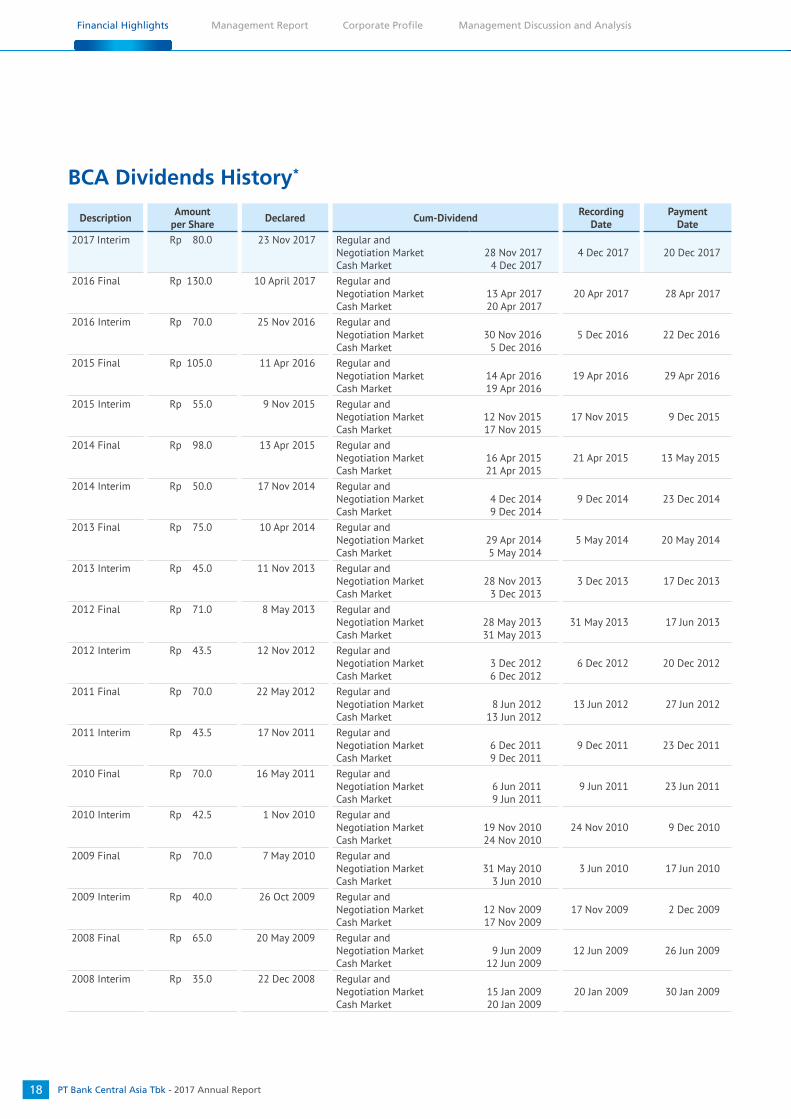

BCA Dividends History*

DescriptionAmount

per ShareDeclared Cum-Dividend

RecordingDate

PaymentDate

2017 Interim Rp 80.0 23 Nov 2017 Regular and Negotiation MarketCash Market

28 Nov 20174 Dec 2017

4 Dec 2017 20 Dec 2017

2016 Final Rp 130.0 10 April 2017 Regular and Negotiation MarketCash Market

13 Apr 201720 Apr 2017

20 Apr 2017 28 Apr 2017

2016 Interim Rp 70.0 25 Nov 2016 Regular and Negotiation MarketCash Market

30 Nov 20165 Dec 2016

5 Dec 2016 22 Dec 2016

2015 Final Rp 105.0 11 Apr 2016 Regular and Negotiation MarketCash Market

14 Apr 201619 Apr 2016

19 Apr 2016 29 Apr 2016

2015 Interim Rp 55.0 9 Nov 2015 Regular and Negotiation MarketCash Market

12 Nov 201517 Nov 2015

17 Nov 2015 9 Dec 2015

2014 Final Rp 98.0 13 Apr 2015 Regular and Negotiation MarketCash Market

16 Apr 201521 Apr 2015

21 Apr 2015 13 May 2015

2014 Interim Rp 50.0 17 Nov 2014 Regular and Negotiation MarketCash Market

4 Dec 20149 Dec 2014

9 Dec 2014 23 Dec 2014

2013 Final Rp 75.0 10 Apr 2014 Regular and Negotiation MarketCash Market

29 Apr 20145 May 2014

5 May 2014 20 May 2014

2013 Interim Rp 45.0 11 Nov 2013 Regular and Negotiation MarketCash Market

28 Nov 20133 Dec 2013

3 Dec 2013 17 Dec 2013

2012 Final Rp 71.0 8 May 2013 Regular and Negotiation MarketCash Market

28 May 201331 May 2013

31 May 2013 17 Jun 2013

2012 Interim Rp 43.5 12 Nov 2012 Regular and Negotiation MarketCash Market

3 Dec 20126 Dec 2012

6 Dec 2012 20 Dec 2012

2011 Final Rp 70.0 22 May 2012 Regular and Negotiation MarketCash Market

8 Jun 201213 Jun 2012

13 Jun 2012 27 Jun 2012

2011 Interim Rp 43.5 17 Nov 2011 Regular and Negotiation MarketCash Market

6 Dec 20119 Dec 2011

9 Dec 2011 23 Dec 2011

2010 Final Rp 70.0 16 May 2011 Regular and Negotiation MarketCash Market

6 Jun 20119 Jun 2011

9 Jun 2011 23 Jun 2011

2010 Interim Rp 42.5 1 Nov 2010 Regular and Negotiation MarketCash Market

19 Nov 201024 Nov 2010

24 Nov 2010 9 Dec 2010

2009 Final Rp 70.0 7 May 2010 Regular and Negotiation MarketCash Market

31 May 20103 Jun 2010

3 Jun 2010 17 Jun 2010

2009 Interim Rp 40.0 26 Oct 2009 Regular and Negotiation MarketCash Market

12 Nov 200917 Nov 2009

17 Nov 2009 2 Dec 2009

2008 Final Rp 65.0 20 May 2009 Regular and Negotiation MarketCash Market

9 Jun 200912 Jun 2009

12 Jun 2009 26 Jun 2009

2008 Interim Rp 35.0 22 Dec 2008 Regular and Negotiation MarketCash Market

15 Jan 200920 Jan 2009

20 Jan 2009 30 Jan 2009

PT Bank Central Asia Tbk - 2017 Annual Report 19

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

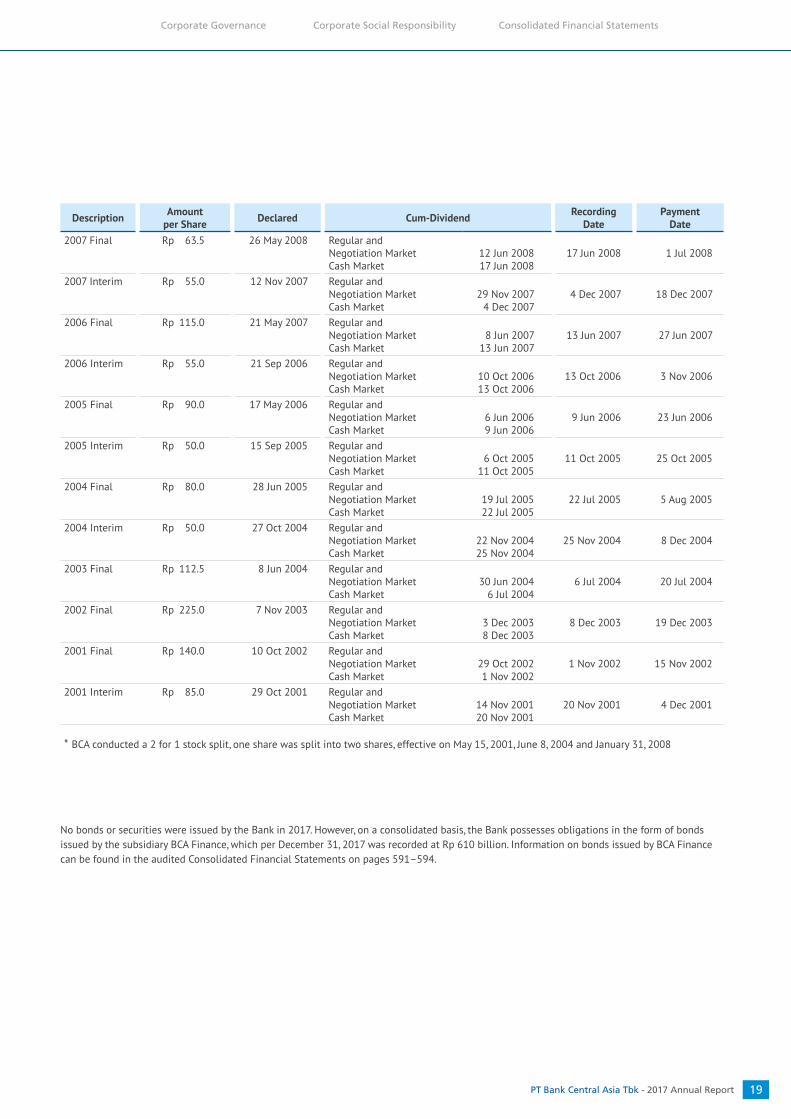

DescriptionAmount

per ShareDeclared Cum-Dividend

RecordingDate

PaymentDate

2007 Final Rp 63.5 26 May 2008 Regular and Negotiation MarketCash Market

12 Jun 200817 Jun 2008

17 Jun 2008 1 Jul 2008

2007 Interim Rp 55.0 12 Nov 2007 Regular and Negotiation MarketCash Market

29 Nov 20074 Dec 2007

4 Dec 2007 18 Dec 2007

2006 Final Rp 115.0 21 May 2007 Regular and Negotiation MarketCash Market

8 Jun 200713 Jun 2007

13 Jun 2007 27 Jun 2007

2006 Interim Rp 55.0 21 Sep 2006 Regular and Negotiation MarketCash Market

10 Oct 200613 Oct 2006

13 Oct 2006 3 Nov 2006

2005 Final Rp 90.0 17 May 2006 Regular and Negotiation MarketCash Market

6 Jun 20069 Jun 2006

9 Jun 2006 23 Jun 2006

2005 Interim Rp 50.0 15 Sep 2005 Regular and Negotiation MarketCash Market

6 Oct 200511 Oct 2005

11 Oct 2005 25 Oct 2005

2004 Final Rp 80.0 28 Jun 2005 Regular and Negotiation MarketCash Market

19 Jul 200522 Jul 2005

22 Jul 2005 5 Aug 2005

2004 Interim Rp 50.0 27 Oct 2004 Regular and Negotiation MarketCash Market

22 Nov 200425 Nov 2004

25 Nov 2004 8 Dec 2004

2003 Final Rp 112.5 8 Jun 2004 Regular and Negotiation MarketCash Market

30 Jun 20046 Jul 2004

6 Jul 2004 20 Jul 2004

2002 Final Rp 225.0 7 Nov 2003 Regular and Negotiation MarketCash Market

3 Dec 20038 Dec 2003

8 Dec 2003 19 Dec 2003

2001 Final Rp 140.0 10 Oct 2002 Regular and Negotiation MarketCash Market

29 Oct 20021 Nov 2002

1 Nov 2002 15 Nov 2002

2001 Interim Rp 85.0 29 Oct 2001 Regular and Negotiation MarketCash Market

14 Nov 200120 Nov 2001

20 Nov 2001 4 Dec 2001

* BCA conducted a 2 for 1 stock split, one share was split into two shares, effective on May 15, 2001, June 8, 2004 and January 31, 2008

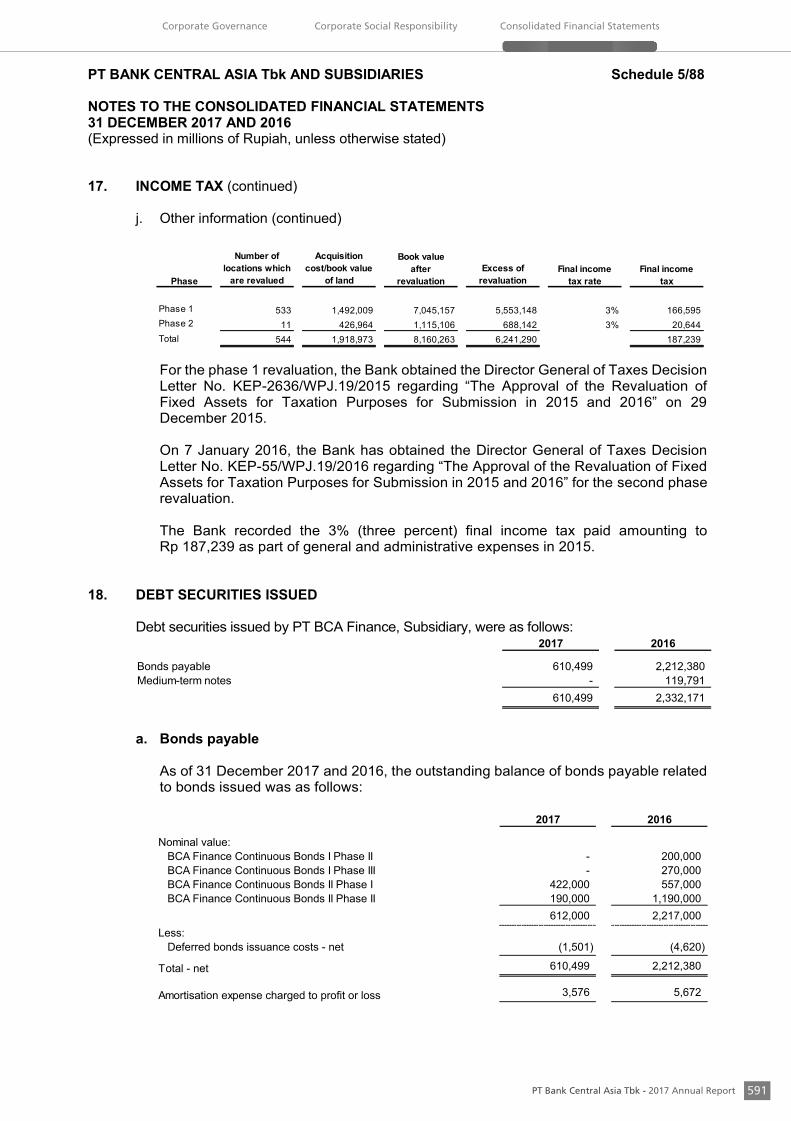

No bonds or securities were issued by the Bank in 2017. However, on a consolidated basis, the Bank possesses obligations in the form of bonds issued by the subsidiary BCA Finance, which per December 31, 2017 was recorded at Rp 610 billion. Information on bonds issued by BCA Finance can be found in the audited Consolidated Financial Statements on pages 591–594.

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

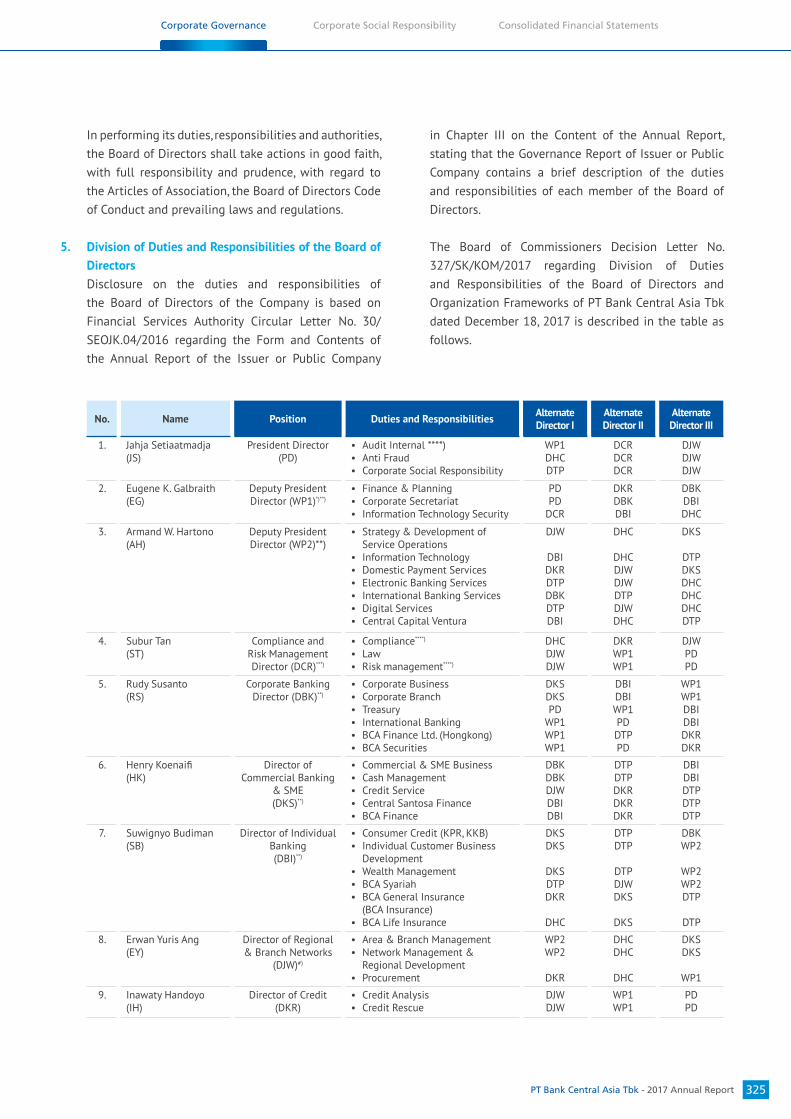

BCA management has successfully led the Bank and applied appropriate measures to adapt and capture opportunities arising in many areas of business and maintaining a focus on building relationships with customers.

Management Report

PT Bank Central Asia Tbk - 2017 Annual Report22

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Report of The Board of Directors

Jahja Setiaatmadja President Director

PT Bank Central Asia Tbk - 2017 Annual Report 23

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

We are pleased to report that BCA successfully recorded a

positive performance in 2017 by capturing a number of business

opportunities amid moderate economic growth in Indonesia.

Customer trust in the quality of BCA’s products and services was the key principle of this solid performance.

BCA consistently provides high quality services, supported by measured investment in strengthening its core transaction

banking business and intermediating function. The Bank’s strategy is to fulfill the evolving financial needs of customers, in line with the recent trend in technological developments.

Review of the Indonesian Economy and Banking Industry

in 2017

The growth of the Indonesian economy cannot be separated

from the influence of the global economy, which saw positive improvements, although the recovery has been slower than expected. The Indonesian economy grew 5.1% in 2017, supported by improved export performance and investment activity. The

ongoing development and completion of infrastructure projects

across the country supported the economy. Indonesia’s economic growth experienced a bottoming out in the last 12 months. The

government and regulators implemented a number of efforts and

policies to stimulate national economic recovery and maintain

stability in the macroeconomic and financial systems.

Indonesia received rating upgrade from the world’s leading rating agencies in 2017, recognizing the improvement in its economy. Standard & Poor’s upgraded Indonesia’s sovereign debt to investment grade, while Fitch Ratings upgraded its debt rating from BBB- to BBB. The outlook of Indonesia’s investment grade was improved to positive from stable by Moody’s.

“BCA’s success in maintaining its business results was owed to our customer trust. BCA closely examines the changing needs of its customers and provides suitable banking solutions.”

Respected Shareholders and Stakeholders,

Bank Indonesia (BI) continued to implement relaxation policies

pursued in previous years to further stimulate GDP growth, with stable macroeconomic conditions where inflation and exchange rates were sustained at a manageable level. BI lowered the 7-day

reverse repo rate by 50 basis points, leading to a rate of 4.25% at the end of 2017.

The Indonesian banking industry experienced a slowdown in loan

and third party funds growth in recent years, with the moderation of the economy. Soft loan demand resulted from the internal

consolidation and efficiency strategy adopted by business. As a result, the banking industry experienced moderate loan growth of 8.2% to Rp 4,738 trillion in 2017. Third party funds grew higher than loans at 9.3% to Rp 5,289 trillion, partly due to the success of the Government’s tax amnesty program.

The banking industry also experienced pressure on its Net Interest

Margin (NIM), in line with decreasing interest rates and moderate loan demand in 2017. The sector’s NIM fell 30 basis points to 5.3% in 2017, from 5.6% in 2016. However, the decreased pressure on non-performing loans resulted in a declining expense for loan

loss reserve compared to previous years. This supported positive

growth of the banking industry’s profitability in 2017, despite moderate loan growth and pressure on the NIM. The banking

system remained stable, with recovering profitability and healthy levels of capital and liquidity. The sector’s CAR ratio was 23.2%, and an LDR ratio of 90.0% at the end of 2017.

PT Bank Central Asia Tbk - 2017 Annual Report24

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

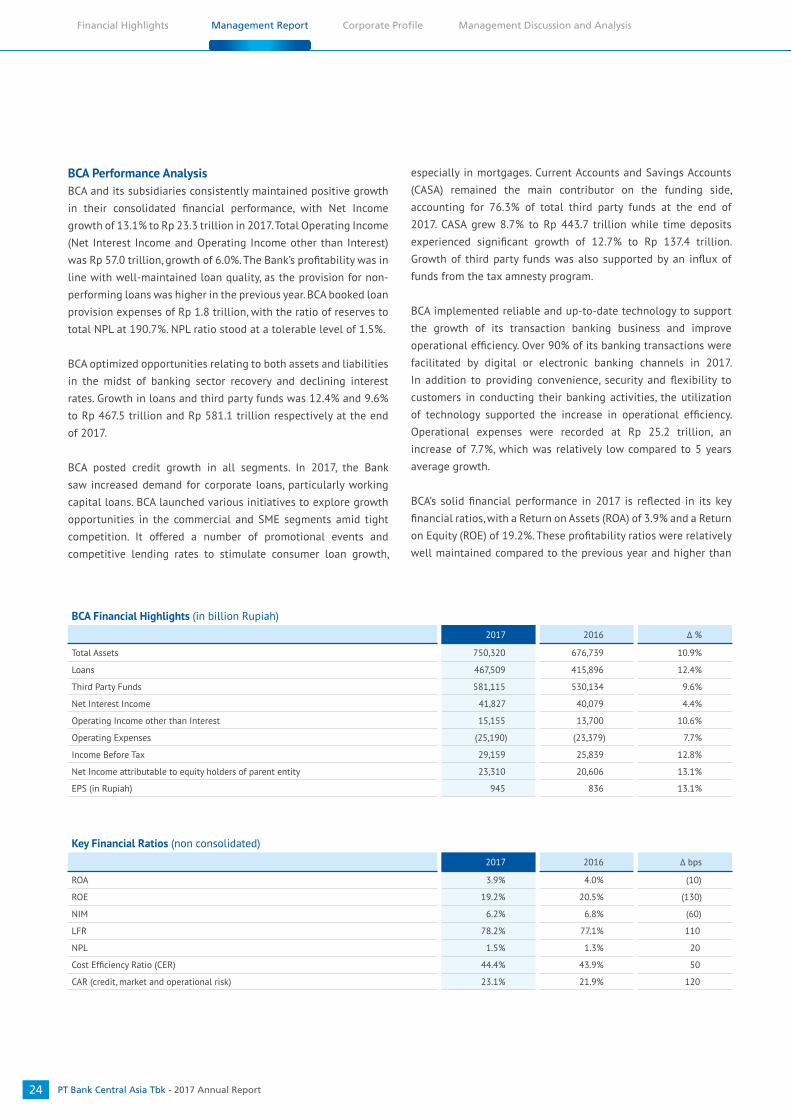

BCA Performance Analysis

BCA and its subsidiaries consistently maintained positive growth

in their consolidated financial performance, with Net Income growth of 13.1% to Rp 23.3 trillion in 2017. Total Operating Income (Net Interest Income and Operating Income other than Interest)

was Rp 57.0 trillion, growth of 6.0%. The Bank’s profitability was in line with well-maintained loan quality, as the provision for non-performing loans was higher in the previous year. BCA booked loan

provision expenses of Rp 1.8 trillion, with the ratio of reserves to total NPL at 190.7%. NPL ratio stood at a tolerable level of 1.5%.

BCA optimized opportunities relating to both assets and liabilities

in the midst of banking sector recovery and declining interest

rates. Growth in loans and third party funds was 12.4% and 9.6%

to Rp 467.5 trillion and Rp 581.1 trillion respectively at the end of 2017.

BCA posted credit growth in all segments. In 2017, the Bank saw increased demand for corporate loans, particularly working capital loans. BCA launched various initiatives to explore growth

opportunities in the commercial and SME segments amid tight

competition. It offered a number of promotional events and

competitive lending rates to stimulate consumer loan growth,

especially in mortgages. Current Accounts and Savings Accounts

(CASA) remained the main contributor on the funding side, accounting for 76.3% of total third party funds at the end of

2017. CASA grew 8.7% to Rp 443.7 trillion while time deposits experienced significant growth of 12.7% to Rp 137.4 trillion. Growth of third party funds was also supported by an influx of funds from the tax amnesty program.

BCA implemented reliable and up-to-date technology to support

the growth of its transaction banking business and improve

operational efficiency. Over 90% of its banking transactions were facilitated by digital or electronic banking channels in 2017.

In addition to providing convenience, security and flexibility to customers in conducting their banking activities, the utilization of technology supported the increase in operational efficiency. Operational expenses were recorded at Rp 25.2 trillion, an increase of 7.7%, which was relatively low compared to 5 years average growth.

BCA’s solid financial performance in 2017 is reflected in its key financial ratios, with a Return on Assets (ROA) of 3.9% and a Return on Equity (ROE) of 19.2%. These profitability ratios were relatively well maintained compared to the previous year and higher than

BCA Financial Highlights (in billion Rupiah)

2017 2016 Δ %

Total Assets 750,320 676,739 10.9%

Loans 467,509 415,896 12.4%

Third Party Funds 581,115 530,134 9.6%

Net Interest Income 41,827 40,079 4.4%

Operating Income other than Interest 15,155 13,700 10.6%

Operating Expenses (25,190) (23,379) 7.7%

Income Before Tax 29,159 25,839 12.8%

Net Income attributable to equity holders of parent entity 23,310 20,606 13.1%

EPS (in Rupiah) 945 836 13.1%

Key Financial Ratios (non consolidated)

2017 2016 Δ bps

ROA 3.9% 4.0% (10)

ROE 19.2% 20.5% (130)

NIM 6.2% 6.8% (60)

LFR 78.2% 77.1% 110

NPL 1.5% 1.3% 20

Cost Efficiency Ratio (CER) 44.4% 43.9% 50

CAR (credit, market and operational risk) 23.1% 21.9% 120

PT Bank Central Asia Tbk - 2017 Annual Report 25

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

the banking sector average. BCA continuously monitored the

adequacy of its liquidity and capital in managing lending and

investment activities. Its capital and liquidity position remained

solid, with a Capital Adequacy Ratio (CAR) of 23.1% and a Loan to Funding Ratio (LFR) of 78.2%.

Implementation of Strategic Policy

BCA carefully observes economic conditions and banking sector

developments to anticipate challenges and capture opportunities.

Sustaining the balance between business objectives and prudent

risk management is an important part of the management of

the Bank’s lines of business, for its core business in payment settlement services, lending activities, and the development of subsidiaries.

Strengthening Payment Settlement Services

To maintain the Bank’s preeminence in transaction banking, the development of payment settlement services plays an important

role in strengthening the CASA funding position. BCA connects

customers through an extensive and integrated multi-channel

network. Security, convenience and reliability of transactions are top priorities for BCA in providing quality services to customers

and strengthening its franchise value, so measured investment in transaction banking infrastructure is a constant area of focus.

BCA observes closely the evolving needs of customers and works

to provide solutions in line with developing trends. With the

ongoing advancement in digital technology, BCA has seen a significant shift in customer transaction preferences in recent years. The frequency of digital transactions continues to

increase, while the frequency of transactions through branch offices decreases. The frequency of transactions through digital channels contributed 97.0% to the Bank’s overall transactions in 2017, up from 96.2% in 2016. This growth was driven mainly by increased use of internet and mobile banking. BCA saw the

number of transactions through BCA internet banking exceeded

ATM transactions in 2017.

BCA capitalizes on latest technological developments to improve

customer experience and operational efficiency. It continues to improve the use of internet and mobile banking services, which serve as more efficient platforms than ATMs and branches. BCA socializes to customers that internet and mobile banking

services are more convenient and easier to use, with unrestricted accessibility, 24 hours a day, seven days a week. BCA also continues to enrich the functionality and increase the transaction capacity

of internet and mobile banking platforms.

Branches remain effective channels to strengthen customer

relationships and facilitate large amount transactions. Although

transactions through branch offices contribute less than 3% to total frequency, they account for 57% of total transaction value. BCA continues to selectively develop new branches and

ATM networks to facilitate the ongoing need for large cash

transactions. Branch expansion focuses on compact formats, such as cash offices and kiosks. BCA has enhanced branch automation through the installation of deposit/withdrawal machines at the

tellers, and by developing the e-branch app to support branch banking services.

Investment in ATM networks is focused on the conversion from

conventional ATMs and Cash Deposit Machines (CDM) to Cash

Recycling Machines (CRM). While conventional ATMs only allow for cash withdrawals and CDMs only allow customers to deposit

cash, CRMs combine both functions into a single machine, reusing deposited cash for later withdrawals. Most CDMs and hundreds of

conventional ATMs were upgraded to CRMs by the end of 2017. Investment in CRMs is to increase efficiency by reducing regular cash refill maintenance visits.

The Bank continues to enhance its working methods and increase

information technology capacity and capability to become more

agile and innovative, to support development of the latest digital products and services. BCA constantly introduces new products

and monitors digital development trends. It introduced a card-less

cash withdrawal facility at its ATMs in 2017 through the use of

BCA Mobile, in addition to the e-wallet app Sakuku, and launched VIRA virtual assistant using an the online chat banking system. The Bank also closely cooperates with a number of e-commerce

players and enriches payment products and services on online

platforms.

Prudent Lending Activities

BCA continues to capture opportunities, despite modest loan demand. It recorded relatively high loan growth both in the

consumer and corporate segments in 2017, through offering competitive interest rates in both segments and attractive

consumer loan promotional programs. It facilitates the credit

needs of well-known corporations in line with prevailing market

interest rates, supported by its liquid balance sheet, which is one of the largest in Indonesia. BCA’s loan portfolio was Rp 467.5 trillion, growth of 12.4% in 2017.

PT Bank Central Asia Tbk - 2017 Annual Report26

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Board of Directors

Armand Wahyudi Hartono Deputy President Director

Jahja Setiaatmadja President Director

Subur Tan Director

Henry KoenaifiDirector

Suwignyo BudimanDirector

Eugene Keith Galbraith Deputy President Director

PT Bank Central Asia Tbk - 2017 Annual Report 27

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

Erwan Yuris AngIndependent Director

SantosoDirector

Rudy Susanto Director

Inawaty Handoyo Director

Lianawaty SuwonoDirector

PT Bank Central Asia Tbk - 2017 Annual Report28

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Growth in consumer loans was mainly driven by the increase in

the mortgage portfolio. BCA launched an attractive mortgage

program at its 2017 birthday celebration with a competitive five-year Fix & Cap arrangement, offering a fixed rate at 6% for the first two years and a 6.88% cap for the following three years. This offer received a positive response from customers. Further, BCA offered other attractive mortgage products, such as mortgages with low initial installments, in line with customer needs. Strong mortgage growth increased BCA market share and supported the

overall growth of consumer loans.

BCA cooperates with its subsidiaries, PT BCA Finance and PT Central Santosa Finance, to disburse vehicle financing. It took part in a series of autoshow events and offered its popular

vehicle financing product, the Fix & Cap program, which offers competitive interest rates to encourage vehicle financing growth. BCA prioritizes service quality, offers fast application processing and provides reliable marketing personnel to ensure the best

experience for its customers. BCA collaborates in the credit

card segment with renowned partners and conducts numerous

promotional programs. It continues to enhance the preeminence

of its proprietary BCA Card by expanding collaborations and

offering attractive programs in line with customer needs.

For the corporate segment, BCA continuously capitalizes on opportunities in every seasonal peak in loan demand. Corporate

lending is targeted on reputable corporations with proven track

records. BCA sought to increase its penetration of the commercial

and SME segments, which were experiencing fierce competition. To expand SME lending, BCA initiated a pilot project of Micro, Small and Medium-sized Enterprises (MSME) centers at several

branches. BCA also adjusted the limit on the commercial and SME

segments in 2017 to expand its target market and its exposure

towards these markets. It lowered lending rates across all

segments, in line with interest rate trends, resulting in a decline in loan yield of 80 basis points at the end of 2017 compared to 2016.

BCA continues to enhance its loan infrastructure, including improving the quality and quantity of its account officers and relationship managers, developing loan products, refining lending policies and strengthening regional business development

infrastructure.

BCA’s lending activities are balanced with carefully maintained quality. BCA constantly applies prudent lending practices

to sustain lending quality and carefully monitors economic

conditions. It also consistently monitors the quality of its loan

portfolio and proactively takes preventive measures when

customers encounter loan repayment difficulties, including initiating loan restructuring for quality customers showing long-

term business solidity but facing temporary financial difficulties. Lending is diversified across a number of potential sectors to mitigate concentration risks.

Developing Subsidiaries

BCA continues to support the business development of its

subsidiaries, which includes businesses in vehicle financing, remittances, Sharia banking, securities, general and life insurance and venture capital, in order to provide comprehensive financial solutions for customers. The Bank’s large customer base provides opportunities for the development of these subsidiaries, and it is expected they will in turn strengthen BCA’s transaction banking business.

BCA established PT Central Capital Ventura (CCV), a new venture capital subsidiary, in 2017. The development of internet and telecommunications technology brings opportunities for start-

up companies to create innovations in digital financial services. BCA, through CCV, intends to invest in and collaborate with fintech companies and support companies in the financial industry that enhance the overall financial service ecosystem of BCA and its subsidiaries, while delivering added value to stakeholders.

BCA increased its share ownership of PT Central Santosa Finance

(CS Finance), a motorcycle financing subsidiary, in 2017. BCA now has 100% ownership of CS Finance (directly and indirectly), from previously 70%.

PT Asuransi Jiwa BCA (BCA Life), a subsidiary previously owned indirectly through the Bank’s subsidiaries; PT BCA Sekuritas; and PT Asuransi Umum BCA (BCA Insurance) became directly owned by

BCA in 2017. The Bank also raised its effective ownership in BCA

Life and BCA Sekuritas, from 75% to 90% in each company, with no remaining ownership belonging to affiliated parties. Increasing ownership in these subsidiaries further supports integration, enhance cooperation and strengthen alignment between the

strategic direction of the subsidiaries and the Bank.

PT Bank Central Asia Tbk - 2017 Annual Report 29

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

Targets, Challenges and Achievements in 2017

• Targets and Achievements in 2017

BCA’s performance in 2017 exceeded its initial targets. CASA funds grew 8.7% to Rp 443.7 trillion, higher than the 5%–7% target. BCA recorded loan portfolio growth of 12.4% to Rp 467.5 trillion, exceeding the 8%–10% target.

Net profit was Rp 23.3 trillion in 2017, growth of 13.1%. Return on Assets (ROA) and Return on Equity (ROE) were 3.9% and 19.2% respectively, better than the year’s targets.

• Challenges and Solutions

Bank Indonesia’s falling benchmark interest rate, and adequate national banking sector liquidity, reduced interest rates across the market in 2017. BCA gradually lowered interest rates on

both its loans and third party funds. However, amidst recovering business conditions, the decline in BCA’s interest rates did not boost its loans. Demand is more influenced by national business conditions, as reflected by moderate economic growth. Under this condition, the Bank’s net interest margin declined in 2017, putting pressure on operating income.

BCA works to improve efficiency and increase fee-based income. The highest operational expense is transaction banking. The

Bank optimized operational efficiency through technology and automation. BCA’s preeminence in payment settlement services supported the collection of fee-based income. Collaborations

with subsidiaries were continuously developed. In 2017, BCA saw an increased non-interest income contribution from BCA

Insurance and BCA Sekuritas.

Furthermore, to increase bancassurance fees, BCA and PT AIA Financial signed an amendment of the bancassurance

partnership agreement in the first semester of 2017 to expand its scope for 10 years. The strategic partnership is expected

to provide long-term benefits for both parties, and facilitate increasingly diverse customer needs.

BCA made several adjustments to its source of funds’ interest rates, considering the relatively stable and adequate liquidity

conditions. The Bank reduced its maximum savings interest rate

by 10 basis points in October 2017. Since June 2017, BCA also gradually lowered time deposits rate. The maximum rate for

its one-month time deposit decreased 275 basis points from

6.75% at the end of 2016 to 4.0% at the end of 2017. With

these strategies, BCA reduced cost of funds particularly in the second half of 2017. The decline in time deposits interest rates

minimized pressure on NIM in 2017.

Another important factor affecting BCA’s performance is asset quality. Well-maintained loan quality also supported its net

profit growth, despite its relatively minimal growth in profit before tax and provision. Net profit was driven by a fall in the expense of allowance for impairment losses on financial assets by 42.5% to Rp 2.6 trillion 2017, in line with the healthy level of non-performing loans. BCA applied prudent lending policies

across all segments amidst moderate turnover from business

activities.

Business Prospects and Strategy for 2018

The national economy in 2018 will improve from 2017, but will remain at a moderate level as it continues to recover.

Infrastructure development will progressively have a positive

impact in the coming years as various projects reach completion.

Ongoing improvement of global economic conditions is expected

to support an increase in Indonesian exports.

BCA is optimistic that Indonesian economic development will

continue, and long term economic growth will remain prospective as one of the pillars of the ASEAN region’s economy, even though 2018 is a political year, with regional head elections in some main provinces, and the early stages of the legislative and presidential elections.

We expect moderate growth in the banking sector, in line with Indonesia’s ongoing economic recovery. Declining interest rates led the Net Interest Margin (NIM) to a relatively low level, which has left minimal downside in the coming year, resulting in a positive effect on BCA’s performance. The Bank will continue to monitor interest rate trends in 2018, the dynamic policies of the world’s central banks, and domestic monetary policies.

Target vs Achievement 2017

Target Achievement

Loan growth 8% - 10% 12.4%

CASA growth 5% - 7% 8.7%

ROA ≥ 3.5% 3.9%

ROE 18%-20% 19.2%

PT Bank Central Asia Tbk - 2017 Annual Report30

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Going forward, BCA and national banking players face the impact of rapid technological development disrupting the banking

business in its current form. Investments in the near future will

be in development and innovation in technology to support

sustainable growth in the banking business and improve efficiency.

BCA faces rapid technological developments, characterized by widespread financial technology products, emerging e-commerce businesses and the entrance of global e-commerce and payment

players. Increasingly dynamic technological developments and

shortening technological platform cycles will be a challenge in

the coming years.

To maintain solid performance, strategic measures and efforts in 2017 will continue to be implemented in 2018. The use of

technology, both to adapt to digital trends and improve efficiency, will be important, especially in payment settlement services. BCA will continue to develop its payment settlement services to

strengthen CASA funding, which remains its main source of funds. Investments in transaction banking multi-channel infrastructure

and digital technology will continually be conducted to enhance

customer experience, thus allowing BCA to make its transaction banking platform more convenient, while not forgoing security and reliability. The Bank is constantly adapting to the development

of online payment settlement methods utilized by e-commerce

businesses.

Lending capability will constantly be enhanced to support BCA’s intermediating function. Investment in improvements in loan

infrastructure, loan processing enhancement and continuous assessment of credit policies in line with economic developments

will remain a priority. BCA targets positive growth in all loan

segments — corporate, commercial and SME, and consumer — in 2018. The Bank will actively review its competitive interest

rates and develop new programs to optimize loan growth, while maintaining prudent banking principles.

BCA will seek further opportunities to increase fee-based income

by exploring opportunities arising from its competitive capabilities

in payment settlements and lending, and by collaborating with its subsidiaries. The subsidiaries are expected to make more

contributions through various cooperations with BCA, as well as increased collaboration between subsidiaries.

Improving Corporate Governance

Stakeholder trust in BCA is a reflection of the Bank’s commitment to good corporate governance (GCG). All members of BCA - the

Board of Commissioners, Board of Directors, and all management and employees - always apply the principles of transparency, accountability, responsibility, independence and fairness.

BCA follows relevant national and international policies, such as regulations issued by the Financial Services Authority (OJK), Bank Indonesia, the ASEAN Corporate Governance Scorecard and best practices in the banking industry to improve the

quality of corporate governance. The Bank also maintains active

communication with customers, regulators and the capital market community to support transparency with stakeholders.

BCA recognizes the importance of GCG to strengthen banking

infrastructure and corporate culture to sustain business

performance and minimize risks. The Bank applies a system of

checks and balances and a good internal control system while

ensuring division of duties and responsibilities between work

units. In 2017, BCA appointed a new external auditor, Tanudiredja, Wibisana, Rintis & Rekan (a member company of the global PwC network), replacing Siddharta, Widjaja & Rekan (a member company of KPMG International) that audited BCA for five years.

BCA conducts self-assessment on GCG and achieved a composite

rank of ‘Very Good’ in 2017, individually and with subsidiaries. In recognition of its good corporate governance, BCA received awards or recognition from leading institutions, including The Most Trusted Companies of Indonesia from the Institute

for Corporate Governance (IICG) and SWA Magazine, and Best Disclosure and Transparency from the Indonesia Institute for

Corporate Directorship (IICD).

Strategies for Human Resources’ Development

BCA is committed to develop its human resources as part of its

strategic direction and goal of providing high quality services to

its customers, due to the importance of human resources as an essential asset for business sustainability.

BCA provides career development opportunities and a clear

career path for employees. Leadership regeneration and

succession processes are priorities to ensure solid organizational

sustainability. BCA provides training for employees at every level

to enhance their skills and ability to adapt to changes, to ensure the availability of quality human resources.

In line with technological developments, we implement automation to support more efficient branch operations. Accordingly, the frontliners in the branch can be further directed to introduce and market BCA products and services, and strengthen relationships with customers.

BCA strives to be an employer of choice to attract qualified workers to join its workforce and retain qualified employees to contribute to business growth.

PT Bank Central Asia Tbk - 2017 Annual Report 31

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

Corporate Social Responsibility

BCA actively participates in various social activities, aimed at the welfare of Indonesian society, through its corporate social responsibility (CSR) programs. Social activities are directed at education and culture preservation; health and sport; and

community empowerment. BCA collaborates with experienced

and competent institutions leading their fields, including WWF, UNICEF, Indonesian Red Cross, and several leading universities in Indonesia.

The educational aspect remains a priority of BCA’s CSR activities and plays an important role in improving the quality and

competitiveness of Indonesian society for the future. The Bakti

BCA internship program provides work experience in the banking

industry. The Bank offers accounting and information technology

educational programs with on the job trainings in BCA.

BCA plays an active role in the preservation and development

of national culture, especially wayang (Indonesia’s puppetry culture), by conducting a series of ‘Wayang for Students’ events. To supports health and sports, the Bank conducted various activities, including badminton.

BCA collaborates with local communities to support tourism

village development programs, which improve productivity and provide employment opportunities, as part of its community empowerment work. The Bank inaugurated Desa Wisata Kampung Batik Gemah Sumilir (Gemah Sumilir Batik Village), a community developed by BCA to promote Pekalongan as the World Batik

Center for domestic and foreign tourists in 2017.

Performance of Committees

The Board of Directors appreciates the role of executive

committees the Assets and Liabilities Committee (ALCO); the Credit

Policy Committee; the Credit Committee; the Risk Management Committee; the Integrated Risk Management Committee; the Information Technology Steering Committee; and the Personal

Case Advisory Committee, for the service and support given to the board in managing the Bank.

The Board of Directors determined that the committees

performed in accordance with their duties and responsibilities in

2017, providing useful advice supporting the duties of the Board of Directors. The committees periodically discuss their work

programs in accordance with the progress of BCA’s performance, the economy and prevailing regulations. The Board of Directors

expresses appreciation for the support and commitment of the

committees.

Changes to the Board of Directors

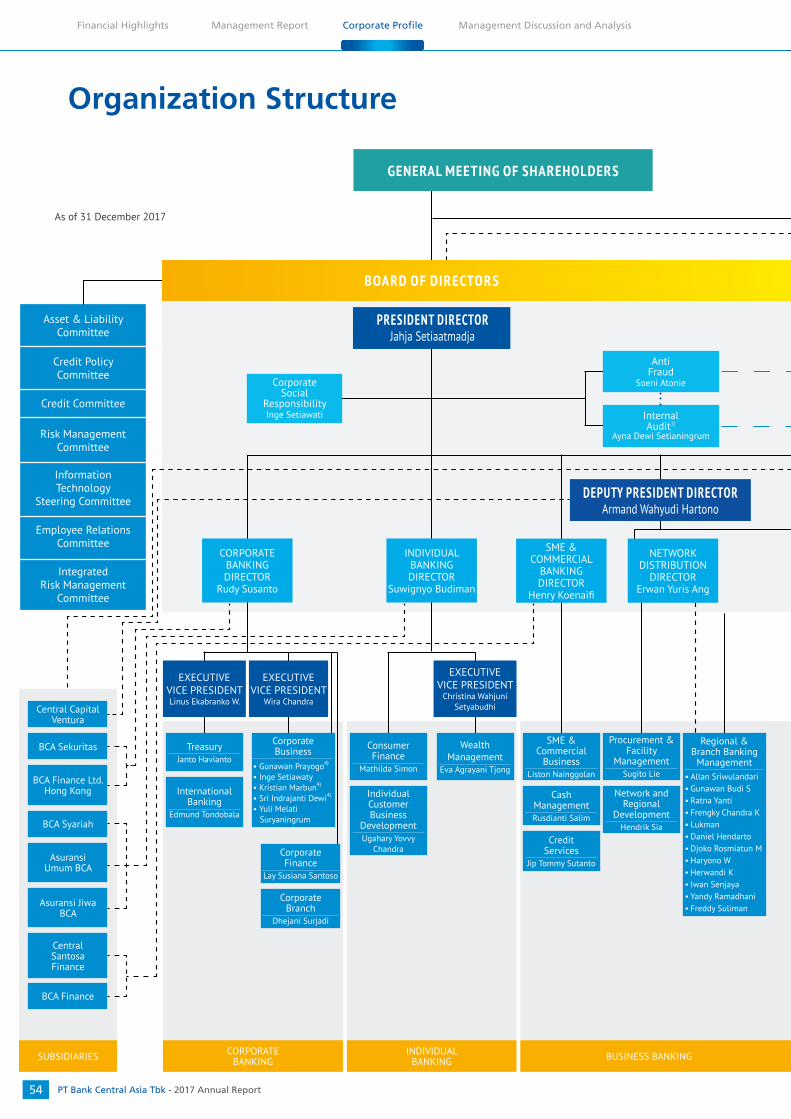

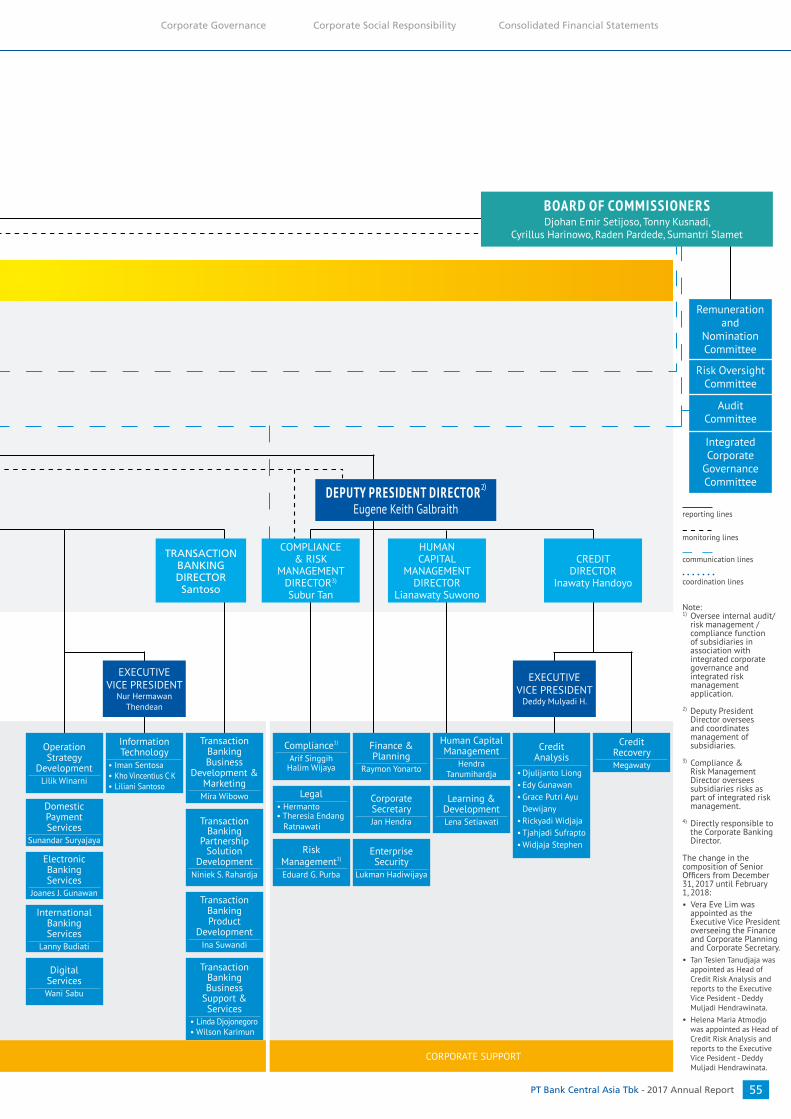

In 2017 there was no change to the composition of BCA’s Board of Directors. The Board’s profile can be seen in the Company Profile section, on pages 56–65. The 11 members of the Board of Directors reflects its diversity in terms of education, work experience and expertise, and the competencies required to support the improvement of the Bank’s performance. Each member has tasks and responsibilities that support the achievement of BCA’s business strategy, in line with its vision and mission, adhering to the company’s core values.

Appreciation for All Stakeholders

We acknowledge that BCA’s success in maintaining its business performance is due to the trust of our customers, trust that motivates all BCA employees to work hard to provide the best

quality products and services.

The Board of Directors appreciates the role of the Board of

Commissioners in carrying out its oversight function and

providing strategic advice, thus allowing BCA to sustain its positive performance in 2017. We appreciate active measures from the

Financial Services Authority and Bank Indonesia in supervising

the banking system as a whole and in maintaining the stability of

Indonesia’s financial system.

Finally, on behalf of the Board of Directors and the management of BCA, we would like to thank all stakeholders for the support and trust they have given throughout the year, enabling us to look ahead with optimism.

Jahja Setiaatmadja President Director

Jakarta, March 2018

On behalf of the Board of Directors,

PT Bank Central Asia Tbk - 2017 Annual Report32

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Board of Commissioners’ Supervisory Report

Djohan Emir Setijoso President Commissioner

PT Bank Central Asia Tbk - 2017 Annual Report 33

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

We are pleased to report that BCA successfully maintained its

positive performance and adapted to changes in the business

environment in 2017. The Bank closed the year with a solid

balance sheet and a 13.1% increase in net profit of Rp 23.3 trillion, despite moderate economic growth.

For an aligned view of the Bank’s business strategy, the Board of Commissioners and the Board of Directors continuously

communicate. The Board of Commissioners assessed that the

Board of Directors successfully guided BCA in maintaining

business continuity by prioritizing strategic objectives. The Board

of Directors implemented prudent strategies in managing the Bank

and capitalized on opportunities throughout the year. Adequate

liquidity, capital position and loan quality were priorities in the Bank’s 2017 business plan. BCA improved operational efficiency and strengthened the capabilities of its business line and

subsidiaries through a number of initiatives and work programs.

The Board of Commissioners acknowledges the Bank’s solid business performance was due to customer trust, which is the foundation of BCA’s business development. As such, we constantly work to improve the quality of our services and provide financial solutions to accommodate customer needs.

Review of Indonesian Economy and Banking Industry

in 2017

Indonesia’s economic growth rate has been in a modest pace since 2014, in line with stagnant domestic consumption and the ongoing recovery of export performance. Indonesia posted

economic growth of 5.1% in 2017, a slight growth from 5.0% in 2016, one of the highest among G-20 countries.

With the implementation of strategic policies in 2017, we saw Government and regulator efforts to stimulate national economic

recovery and maintain macroeconomic and financial system stability. The development of infrastructure projects continues to

“BCA has applied appropriate measures to adapt to increasingly tight competition in the banking sector and changing business trends, improving its capability for continuous growth.”

Valued Shareholders and Stakeholders,

be a Government focus, aiming for the acceleration of Indonesia’s economy, especially once key infrastructure projects have been completed. Investment flows improved and contributed to a number of business activities. National export performance grew, in line with the improvement of Indonesia’s key commodity prices.

Indonesia’s economic growth was influenced by positive improvement in the global economy, although the recovery is slower than expected. Growth of the US economy, which showed progressive signs, including domestic consumption growth and a declining unemployment rate, was a positive. This influenced the US Federal Reserve (FED) to increase its interest rate several times, and it will likely do so again in the foreseeable future. The Chinese economy is moving toward a new equilibrium

with lower economic growth of 6.7%-6.9%, accompanied by the risk of high Chinese corporate debt. The slowdown in China’s economy has affected the global economy, especially its trading partners, including Indonesia. However, China’s rebalancing and deleveraging processes have been well managed and its economy

is heading for a soft landing. The European improved and is now

one of the pillars of global economic growth.

Targeted domestic macroeconomic policies successfully supported

a number of key macro parameters, despite moderate national economic growth. The Rupiah exchange rate against the US Dollar (USD) was relatively stable in 2017, although it experienced pressure at the second semester, closing 2017 at Rp 13,555 per 1 USD, from Rp 13,473 at the end of 2016. Inflation also remained within the Government’s target range, at 3.6% by the end of the year, compared to 3.0% at the end of 2016.

Indonesia’s economy saw a number of achievements, providing foundations for long-term economic growth in 2017. The tax

amnesty program, which began in July 2016 and was applied gradually to the end of March 2017, recorded a redemption payment equivalent to 1.1% of Gross Domestic Product (GDP), and total

PT Bank Central Asia Tbk - 2017 Annual Report34

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Board of Commissioners

Cyrillus Harinowo Independent Commissioner

Tonny Kusnadi Commissioner

Sumantri Slamet Independent Commissioner

Djohan Emir SetijosoPresident Commissioner

Raden Pardede Independent Commissioner

PT Bank Central Asia Tbk - 2017 Annual Report 35

Consolidated Financial StatementsCorporate Social ResponsibilityCorporate Governance

assets declared equal to 39.3% of GDP. The amnesty was the most

successful in the world, with the highest ratio of redemption levy to total GDP compared to other countries that have implemented

such a program. Standard & Poor’s upgraded Indonesia’s debt ratings to investment grade in 2017, due to fiscal and monetary conditions, while Fitch Ratings increased Indonesia’s debt rating from BBB- to BBB. The outlook of Indonesia’s investment grade was improved to positive from stable by Moody’s.

Bank Indonesia loosened several monetary policies, including adjusting interest rates, to stimulate economic growth. In second semester 2017, Bank Indonesia lowered its seven-day reverse repo rate in August and September by 25 basis points each, standing at 4.25% at the end of year, in response to stable inflation, Rupiah exchange rates and investment flow. Interest rates in Indonesia were relatively low compared to long-term

historical data. However, national banks need to pay attention to the direction of global interest rates, especially the impact of the increased FED rate in the US and the European Central

Bank’s (ECB) plan to reduce its stimulus plan in the Eurozone. The normalization of the FED rate, both in terms of magnitude and implementation schedule, will have an impact on emerging countries, including Indonesia. The rate of reduction of the ECB’s monetary stimulus program will depend on economic recovery in

European countries. The prevailing macroeconomic conditions in

many countries will affect the monetary policies of the world’s major central banks and impact global capital flow.

The banking sector experienced moderate loan growth of 8.2%

in 2017, in line with the ongoing recovery of the economy. Third party funds grew by 9.3%, and the sector’s Non-Performing Loans (NPL) ratio was relatively stable at 2.6% at the end of 2017, from 2.9% at the end of 2016. Net income grew by 23.1%, consistent with the easing pressure on NPLs. The banking industry saw a

drop in its Net Interest Margin (NIM) to 5.3% in 2017 from 5.6%

in 2016, in line with declining domestic interest rates in 2017. Financial system stability was well maintained, with a solid banking sector capital position (Capital Adequacy Ratio – CAR per December 2017 of 23.2%) and liquidity position (Loan to Deposit

Ratio – LDR at the end of December 2017 of 90.0%).

Performance of the Board of Directors and Bases of

Assessment

The Board of Commissioners assessed the Board of Directors’ performance in 2017 based on the annual business plan

submitted by the Directors and approved by the Commissioners.

In its supervisory capacity, the Board of Commissioners decided that, overall, the Board of Directors successfully managed BCA in 2017 amid Indonesia’s moderate economic conditions.

The Board of Commissioners and the Board of Directors are

committed to creating a transparent, accountable, responsible, fair and independent organization. The implementation of

good corporate governance, sound risk management and internal auditing serves as foundations for sustainable business

performance, and creating added value for the Bank’s stakeholders. BCA and its corporate governance systems have been properly

managed by the Board of Directors.

We report that in 2017, BCA maintained a healthy business performance, posting a 13.1% increase in net income to Rp 23.3 trillion. The loan portfolio grew 12.4% to Rp 467.5 trillion, and third party funds grew 9.6% to Rp 581.1 trillion. Return on Assets (ROA) and Return on Equity (ROE) exceeded pre-defined targets. BCA also maintained strong capital and liquidity positions, reflected in the CAR, Loan to Funding Ratio (LFR) and Liquidity Coverage Ratio (LCR). BCA’s solid performance was partly due to prudent risk management, particularly in the management of credit, market and operational risk. The Bank’s loan quality was well maintained, with an NPL ratio of 1.5% in 2017, lower than the Indonesian banking sector average. Other risks, including operational, were adequately managed, supported by an integrated risk management framework covering strategies, organizational structure, policies and guidelines, and the infrastructure of the Bank’s risk management, allowing BCA to identify, measure, control and report risks. Operational losses were well below the

standard capital charge stipulated by the regulator.

The Board of Commissioners supports the Board of Directors’ strategies in adapting to changes in customer needs and the

latest banking trends. The Board of Directors successfully steered

the Bank to take advantage of technology and enhance its digital

services, despite the rapid growth in digital technology. BCA responded to growing customer preference for digital services

and increased automation for operational efficiency. This resulted in improved business, in particular transaction banking, as the key driver for Current Accounts and Savings Accounts (CASA). BCA

established PT Central Capital Ventura, a venture capital company as a subsidiary in response to the advancement of fintech and e-commerce start-up companies in 2017, enabling the Bank to invest in fintech companies. The subsidiary will collaborate with fintech companies and support BCA’s business ecosystem and its subsidiaries, and enable it to adapt to the changing needs and demands of customers.

PT Bank Central Asia Tbk - 2017 Annual Report36

Management Discussion and AnalysisCorporate ProfileManagement ReportFinancial Highlights

Supervision of BCA’s Strategy

The Board of Commissioners, in its supervisory role, concludes that the Board of Directors successfully managed the Bank in

accordance with its annual business plan, BCA’s vision, mission, and strategic direction. We see that the Board of Directors applied

appropriate measures to adapt to increasingly tight competition

in the banking sector and changing business trends, improving its capability for continuous growth.

BCA continued to strengthen its core transaction banking business

in 2017. A solid source of CASA funding was secured by the Bank’s preeminence in transaction banking and its continuous efforts

to maintain interconnection between customers and its payment

system.

BCA leverages on digital technology to expand its products

and services in accommodating customer needs, and improve operational efficiency. Investments are continuously made to develop internet and mobile banking, and application-based services. BCA maintains its investment in efficiency-oriented programs, including the development of Cash Recycling Machines (CRM). These efforts have shown positive results. In line with the shift of customer preferences toward digital-based services, the number of transactions conducted through internet, mobile and ATMs accounts for 97% of total customer transactions processed

by BCA. The Bank still expanded its branch offices, considering the significant value of the transactions they process. BCA also implemented various automation initiatives across its branch

network and developing a more compact format.

CASA funds continue to grow, despite Indonesia’s ongoing economic recovery, due to the Bank’s focus on the development of its transaction banking franchise. CASA funds grew 8.7% to

Rp 443.7 trillion in 2017. CASA accounted for 76.3% of total third party funds of Rp 581.1 trillion at the end of 2017. The tax amnesty also contributed to the Bank’s CASA turnover. In 2017, BCA supported the tax amnesty program by facilitating customers

in making tax amnesty redemptions and investing repatriated

funds. The Bank also provided tax amnesty education to its

customers.

The Board of Commissioners assesses that the Directors

appropriately lowered deposit rates gradually, helping the Bank to maintain low cost of funds, in line with the national banking system‘s increased liquidity in 2017.

The Board of Commissioners appreciates the Board of Director’s prudent and disciplined lending risk management principles. The

Bank’s loan portfolio was diversified into a number of potential sectors, and continued to grow with a relatively low NPL and loan restructuring rate compared to the industry average. BCA

consistently monitors debtor business conditions to proactively

provide solutions for debtors experiencing financial difficulties.

The Bank’s loan portfolio was Rp 467.5 trillion in 2017, growth of 12.4% compare to the previous years. BCA captured the opportunity

of increasing corporate loan demand by providing lending to

major debtors with proven track records. BCA implemented the

consumer loan strategy of offering attractive products with

low interest rates, especially on mortgages. This successfully increased mortgage growth. BCA sought to increase penetration

for the commercial and SME segments, which experienced more fierce competition compared to other segments.