Embed Size (px)

Citation preview

Speaker Introduction:

Kathleen Cunningham, BComm, LLB, MPS, TEP• 20+ years in the trust industry

• Experience as a Trust Officer• Led national team of lawyers

• Supported trust management and staff • Provided estate and trust education to staff responsible for estate, trust

and tax administration, business development, financial planning, and operations

• Chair STEP Trust & Estate Technical Committee • Lead Author, STEP Certificate in Estate and Trust Administration • Past Chair STEP Canada Education Committee• Past Chair STEP Vancouver• Co‐chair STEP Canada Symposium on Trust Law Reform (2007)• Member of the BC Law Institute Committee on the Modernization of the Trustee Act (Dated Oct 2004)• Member of the BC Law Institute Committee on Recommended Practices for Wills Practitioners Relating to Potential Undue Influence: A Guide (Dated Oct 2011)• Frequent speaker at STEP Canada national conferences• Currently on contract at Public Guardian and Trustee of BC dealing with issues related to abuse and neglect of vulnerable adults and introduction of related legislation

1

2

This is the first course of the STEP diploma.

The exam is open book . It requires application of the law to realistic client situations. The sample exam questions in student resources show question styles and examples of how to approach answers.

For example, rather than asking students to “Briefly explain the rule in Saunders v Vautier and provide an example”, students may be asked to consider a scenario and respond to a question such as: “Can this trust be terminated? Why or why not?” An examiner will look for an answer that sets out the relevant legal rule(s), identifies relevant facts, and discusses the facts that lead to the proposed conclusion.

Student Resources online: Critical to your studies and exam preparation. Take time to review

• Examinable Content – lists the sections of each chapter that are examinable. Important to review. Some content in text is included to complete a summary of the law and/or to explain a concept, but it will not be tested.

• Online Course Content/Applying the Concepts. This is part of the text and has two purposes:

a) provides examples of the rules being applied in real situations

b) provides an opportunity to practice the analytical approach required on the exam.

• Review Questions – these are provided to assist you in your studies. Close your materials and answer without referring back to assess your recall

• Sample Exam – not a complete exam

• Post tutorial notes from prior sessions. Recordings cover points we do not get to today.

• Provides links to legislation, resources, sample documents

• Remember to review Tips for Preparing and writing a STEP Diploma For Canada Exam

Access the site as follows:

• Path: public website/joining step/student route/Diploma route/student resources

• URL: http://step.ca/joining/studentresources.aspx

• Password: dipstu2009

3

While all of the chapters are important, some are more critical for exam purposes and general knowledge. Each chapter has a detailed set of learning objectives. You should be comfortable that you have met the objectives. Some concepts are complex and/or more esoteric. These are for lawyers who specialize in the field. As a TEP, your responsibility is to be aware of the rules, recognize when they may be relevant and understand the relevance. Therefore, for examination purposes, sections of the text have been deliberately excluded. It is important for you to keep this in mind as you prepare for the exam so that you do not spend time on rules that will not be examined, to the detriment of the critical knowledge you will be examined on.

Tutorials deal with key concepts to ensure their importance is not overlooked, as well as the concepts that tend to cause the most discussion and/or confusion. Accordingly, the following notes on each chapter are offered as an overview and to complement the learning objectives and examinable content information already provided.

Introduction and Classifications: Terminology and general concepts. Helps TEPs ensure they are speaking the same language and alerts TEPs to situations when words should be clarified before jumping to assumptions and/or advice. Classifications demonstrate that trusts can be viewed from different perspectives, influencing terminology and understanding about how trusts are used.

Creation of a trust: Fundamental to the course and understanding this area of the law. Knowledge requirements for TEPs will vary depending on the profession. Each element must be understood and a TEP is expected to be able to recognize potential issues in order to ensure appropriate actions are taken if creation is an issue/at risk. The 3 certainties and some legal and public policy constraints are important parts of this chapter.

Termination and Variation: As TEPS we see situations where a termination or variation could address a conflict, a legal issue, or a tax liability. The law varies across the country. It is important to understand the rules, when they can and cannot be used, and the mechanics.

Express trusts: As TEPs, we will advise clients on when to consider a trust, and/or be responsible for providing services to a trustee. Accordingly, it is necessary to understand the purposes for which trusts are can be made, and any constraints or rules that may apply.

Non‐charitable and charitable purpose trusts: “Purpose” trusts are only valid in certain situations. This is an extension of the “creation of a trust/legal constraints” chapter. Given that in Canada, “charitable donations” can be made to organizations that do not meet the requirements of a “charitable purpose trust, it is important for TEPs to recognize the distinction between charitable and non‐charitable purposes

4

Charitable purpose trusts: These rules are important. They determine whether a gift may survive or fail. TEPs need to be able to recognize the issues and identify situations where a gift which appears to fail, can be saved.

Duties and powers of trustees; breach of trust: Ultimately, these three chapters are critical to this course and the advice and/or service that a TEP provides to someone who is a trustee. The online course content is intended to help students consider the rules in the context of real life scenarios. In addition, it is important to be able to recognize that although an action may seem “practical” or “appropriate” in the circumstances, if there is a breach of a duty or power the trustee and/or advisor may be at risk of liability if anything goes wrong. Tutorial reviews some examples to help students prepare for the analysis required on the exam.

Appointment, retirement, death and removal: These rules are established by the laws in each jurisdiction. A trust may modify the default rules. TEPs should be aware of the default rules and know how they might apply in order to be able to advise clients when they need to be addressed.

Powers of Attorney, Resulting Trusts and Constructive Trusts: These chapters deal with legal relationships related to or similar to trust relationships. The common law governing them is often guided by principles found in trust law. In order to recognize and deal with the issues, or help a client solve a problem, a TEP must have a firm grounding in the fundamentals of trust law (3 certainties, duties and powers), and the relevant law in these three chapters. They deal with what someone can/cannot do as an attorney, and court ordered remedies where an express trust is not in place.

Drafting trusts: This chapter is self explanatory. Students should review it, bearing in mind the course materials, as well as the precedents found on the Student Resource Area.

Notes on the Trust in Quebec: This chapter has been deliberately included for students outside of Quebec and should not be ignored. While laws are similar in the common law provinces and territories, there are some differences that need to be noted by a practitioner. The differences are magnified for a TEP in Quebec. The chapter does not purport to be a review of Quebec trust law. However, if a trust “moves” (for example, the trustees change or move to another province) a TEP in a common law province may find that a client is a trustee of a Quebec law trust. As a result, TEPs have a responsibility to be familiar with the key similarities and differences so that they can adapt their services and/or recognize when additional legal advice will be required. The content in this chapter is mandatory for common law students. See examinable content.

5

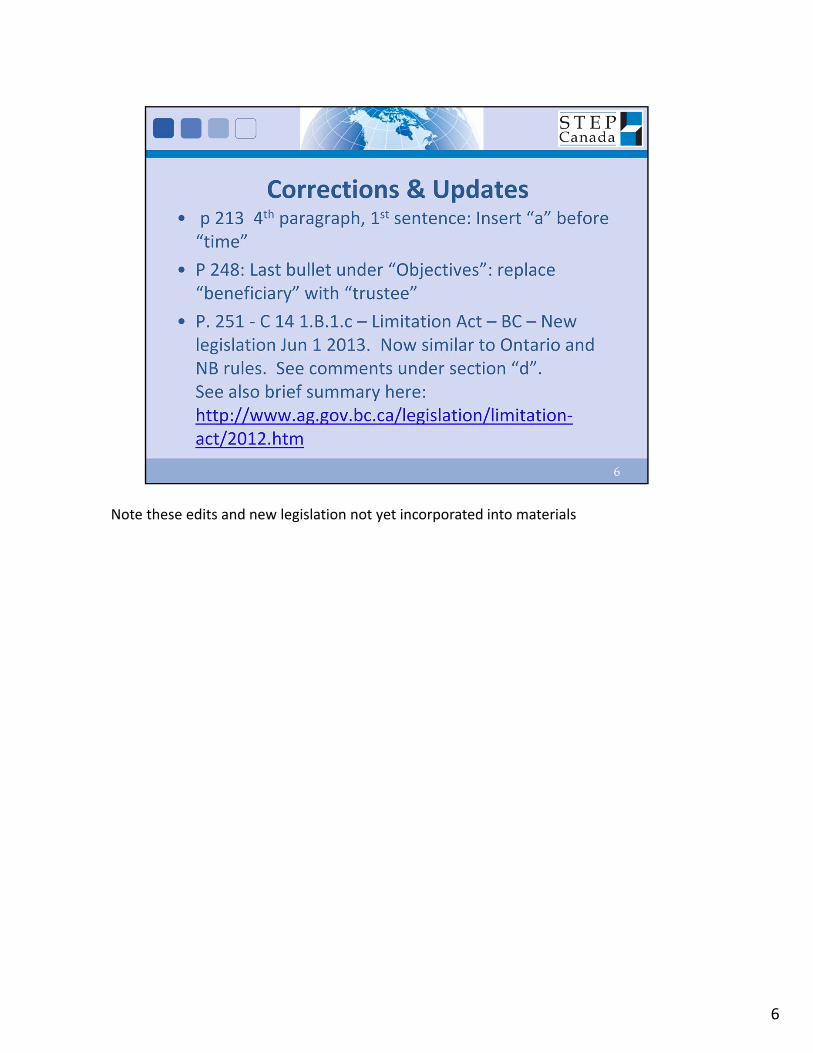

Note these edits and new legislation not yet incorporated into materials

6

7

Be aware that there is a uniform Trustee Act that STEP has expressed general support for. Each jurisdiction now needs to look at whether or not to accept some or all of the recommendations and incorporate into their trustee acts. BC is looking at it. NB has introduced a new act but it is not yet in force and no date has been announced. Alberta is expected to make decisions.

This course does not incorporate the recommendations or the NB statute.

8

• Decision was made in 2011 that tutorials should focus on specific topics and we would build a library over the coming years on key areas.

• This is an update to the May 2014 tutorial on these topics.

• Chose these topics because they are fundamental to the operation of a trust.

• Creation of the trust is obviously critical, but once it is in place, these are core concepts to working with trusts and dealing with clients. Many concepts apply to the administration of estates as well.

• Trustees have to understand these rules

• Advisors need to know them so they can explain to clients and help set expectations; the rules also influence the advice and services provided

• Lawyers need to ensure that the planning and ultimate drafting addresses them to ensure testator/settlor wishes are carried out.

• Misunderstandings and misplaced expectations are often at the root of disputes between trustees and beneficiaries.

9

• Fundamental to the trustee’s role is the concept of trustee duties and trustee powers.

• Subject to specific instructions in the trust document, the trustee has to be aware of his or her duties … those things that must be done or complied with and where failure leads to liability for loss and/or a requirement to remedy the breach of that duty.

• Powers on the other hand, give the trustee authority to do something

• A power may also give the trustee discretion as to how to exercise a duty

• This is why we often say a duty may be coupled with a power

• Trustees take actions and make decisions every day.

• They need to understand the consequences if they make a mistake.

• They need to know how to protect themselves if there is a need or pressure to do something.

• Beneficiaries have rights too. Advisers need to know what they are (and the limits)

• Note: Duties and powers governing trustees are set down in case law, may be established or modified in statutes, and can be imposed or modified in the trust document itself.

10

• The text reviews the core trustee duties. Those familiar with director’s duties to a company will notice the similarity. May seem obvious and easy enough to understand, but they can become a challenge for trustees in practice.

• It is important to understand each and how they apply in practice. This informs the planning and drafting of the terms of the trust so the trustee is not unnecessarily constrained.

1. The duty to comply with the terms seems trite. But … to be clear, a trustee cannot disregard the terms of the trust because the trustee or a group of beneficiaries think it is appropriate to do so. It constitutes a breach. See “breach of trust”.

2. The duty of care (Slides 11&12)• What is it? • Is it the same for everyone? • The law continues to evolve

3. Delegation is a problematic duty. A trustee must exercise duties and powers personally. However, the law permits delegation of tasks that are often delegated by a person when he or she does not have the knowledge or skill, and the task is administrative in nature.

• When is it appropriate? • What is required? • Most provinces specifically permit delegation of investment powers. • Delegation does not mean abandoning responsibility. Prudence is required. What is that?

4. Impartiality is a duty that comes up in many contexts including: (slides 13‐15)• Capital or income receipt?• Is a decision to “encroach” impartial?• Investment strategy? Income v. growth

5. The duty of loyalty deals with conflicts of interest. The rule is strict. • Comes up often. • An issue where trustees have services that they can offer to the trust (e.g. investment management). A

trustee cannot hire himself or his firm unless it is permitted.6. The duty to account or to provide information is fundamental to ensuring enforcement of the trust.

Requirements are not entirely clear: Who, what, when? 7. Exculpation clauses try to remove liability for breach – see slide 17.

11

This test may seem vague to some. So, look to case law for examples of what is expected.

Some talk about “managing the affairs of others” which suggests one may take fewer risks.

Law in Canada today (and the reality for professionals acting as trustee):

• Fales v Canada Permanent continues to be cited as the general law.

• There is no distinction between the lay trustee and a professional trustee

• But: legislation allows the court to excuse a trustee for breach(see pp 253/4 in Ch 14 for list by province. Note: Ontario excludes this for purposes of breach of investment provisions (s.35(2))

• In Fales, the trustees were held liable, but the court relieved the widow/lay trustee from liability.

• Professional trustees and trustees who are paid will want to be careful

• BC Law Institute tackled this issue in a 2004 report. Suggested a compromise. Not yet implemented

• Saskatchewan new Trustee Act tackled it (in 2009)

• All professionals acting as trustee need to beware …

• Use your special skills and knowledge.

• Uniform Trustee Act – Uniform Law Conference of Canada proposal:

26(1) In the administration of a trust, a trustee must act in good faith and in accordance with the following:

(a) the terms of the trust;

(b) the best interests of the objects of the trust;

(c) this Act.

Good faith means an honest belief on the part of the trustee that what the trustee has done, or proposes to do, is proper, appropriate and for the best interests of the objects of the trust

12

The basics: Protect the property

• What insurance is possible, what is needed, what is affordable?

• Arrange for inspections if necessary to ensure property remains in good condition

Hiring agents and delegation (if permitted)

• Selection requires a process

• ensure appropriate skills, recommendations etc

• ensure fees are fair and within industry standard

• Advice must make sense

• Courts do not exonerate trustees if advice is bad.

• May have to pursue advisor.

• Ensure reporting is received, reviewed and queries addressed

• Expenditures

• must be fair and in line with services provided

• must meet an industry standard

• Or else…. Trustee may be personally liable!

13

• Trustee duty to be impartial prevails unless will/trust removes it

• Broad encroachment power may displace duty

• Trust/Will can specifically permit “favouring” one person or class

• Examples: trust for disabled person, spouse trust

• “to exclusion of others”; “may exhaust the trust”

• Trustee should not confuse impartiality with “equality”

• Example: Power to pay capital to “children” for “their benefit”

• Just because A received $10,000, B is not automatically entitled to receive $10,000

• But, trustee must turn mind to the decision

• Cannot reject approval out of hand

• Cannot approve once and forever annually (unless clearly approved as such)

• See “breach of trust” cases at end of ch 11 (summary notes on slide 27 – court intervention)

• Trust capital: original assets, growth in value, realized net capital gains

• Trust income: rent, dividends, interest

• Historical note: Prior to introduction of prudent investor rules in 1990s and later, each investment had to produce income and have growth potential or should not decline in value (ie. A GIC). In addition, if one asset had a gain and another a loss, there could not be an offset. Now the laws generally look at overall performance. See slides on investment powers.

• Important to be aware of the different beneficial interests and not favour one over another

• E.g. through investment choices or amounts paid out under discretionary powers

• Will not matter if trust is fully discretionary and no separate interests, but there still may be residual beneficiaries on the death of a beneficiary/class of beneficiaries.

14

• Materials review these details

• Similar in concept to business income and income tax BUT, different rules may apply

• E.g. capital gains are capital, not income.

• Make the distinction for some receipts and expenses

• Some are obvious/clear, others are not so clear. General rule:

• ongoing and/or regular receipts or expenses are recorded under revenue/expenses

• one time expenses are recorded under capital (pp 188‐193 materials)

• corporate transactions: analyze for true nature, review law and trust terms (pp 185‐187 materials)

• Note:

• Saskatchewan legislation and proposed Uniform Law Conference of Canada Uniform Trustee Act give trustee’s some discretionary powers for allocation http://www.ulcc.ca/en/uniform‐acts‐new‐order/current‐uniform‐acts/633‐trusts/trustee‐act/1255‐uniform‐trustee‐act

• Some trusts may as well.

15

• See text for discussion and principles.

• Note some rules are strict. Others depend on facts

• Some rules consider apportionment

• Note amortization rules for bond premiums and discounts

• Amortization is less of a concern now given prudent investor approach to selecting investments.

16

• See c 11 beginning p 181 for a discussion of these rules

• Caution: Be aware of when it applies and when it doesn’t

17

Corporate distributions are important to watch and consider if trustee does not have power to allocate receipts based on the “substance” of a distribution.

Canadian law: Form of the distribution guides allocation

Issue: Form may not follow substance. E.g. Capital gain could be paid out of corporate account as a cash dividend; or a dividend in kind might be paid out by transferring an asset from the company.

Trustees have to monitor publicly traded company decisions; may have to take pre‐emptive action to ensure a declared dividend is not received (e.g. sell the shares) if the proper allocation of the receipt would lead to a large amount going to the income beneficiary which, in substance, represents capital.

When dealing with private companies, the trustee may be able to influence the decision on how to make a distribution.

18

The duty to provide information requires the trustee to consider how much and when to provide information and to who.

Generally, beneficiaries need to be aware of the trust and the terms.

Consider: if a discretionary beneficiary is not aware of the potential entitlement, he or she will not make a request; it is also not possible to review the trustee’s management of the trust to ensure compliance with the duties and the terms.

Unless there are sound reasons not to provide information a trustee is well advised to ensure all those currently entitled do have sufficient information. See materials for a discussion of the balance of interests approach.

Recommended practices:

• Provide ongoing information so issues can be dealt with as they arise

• If unsure, seek legal advice given case law in Schmidt v Rosewood

• But, do not refuse generally, or may be risking liability for court costs

19

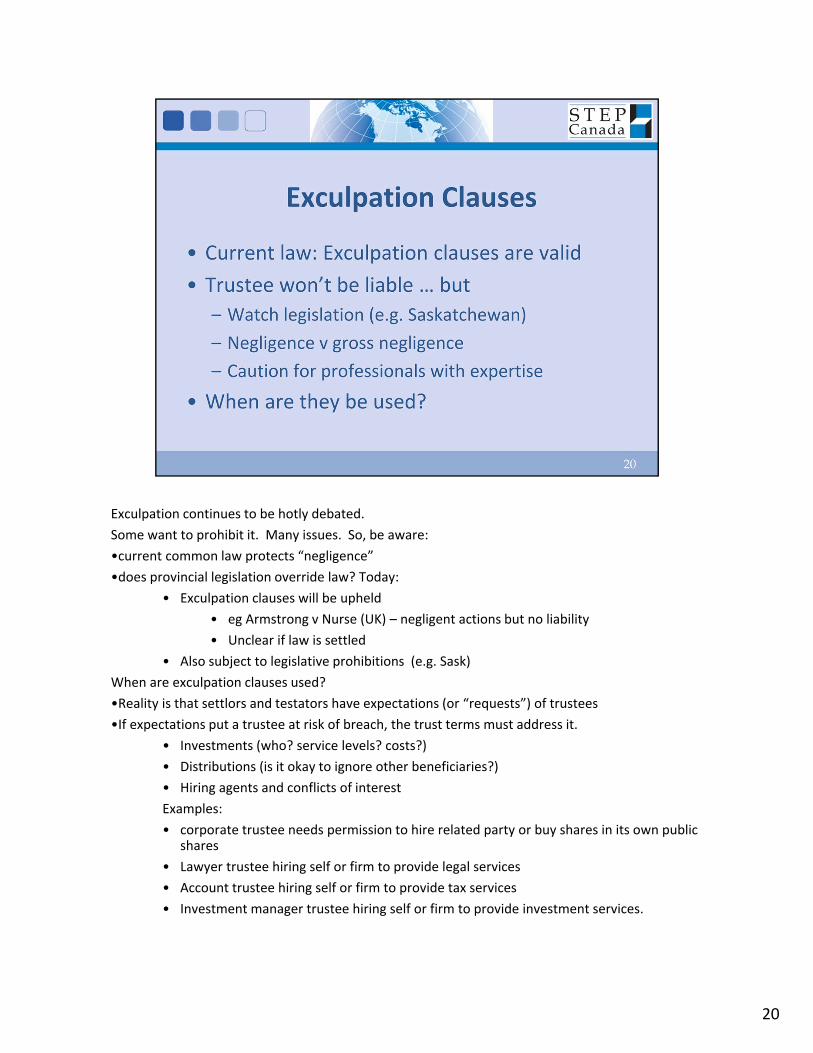

Exculpation continues to be hotly debated.

Some want to prohibit it. Many issues. So, be aware:

•current common law protects “negligence”

•does provincial legislation override law? Today:

• Exculpation clauses will be upheld

• eg Armstrong v Nurse (UK) – negligent actions but no liability

• Unclear if law is settled

• Also subject to legislative prohibitions (e.g. Sask)

When are exculpation clauses used?

•Reality is that settlors and testators have expectations (or “requests”) of trustees

•If expectations put a trustee at risk of breach, the trust terms must address it.

• Investments (who? service levels? costs?)

• Distributions (is it okay to ignore other beneficiaries?)

• Hiring agents and conflicts of interest

Examples:

• corporate trustee needs permission to hire related party or buy shares in its own public shares

• Lawyer trustee hiring self or firm to provide legal services

• Account trustee hiring self or firm to provide tax services

• Investment manager trustee hiring self or firm to provide investment services.

20

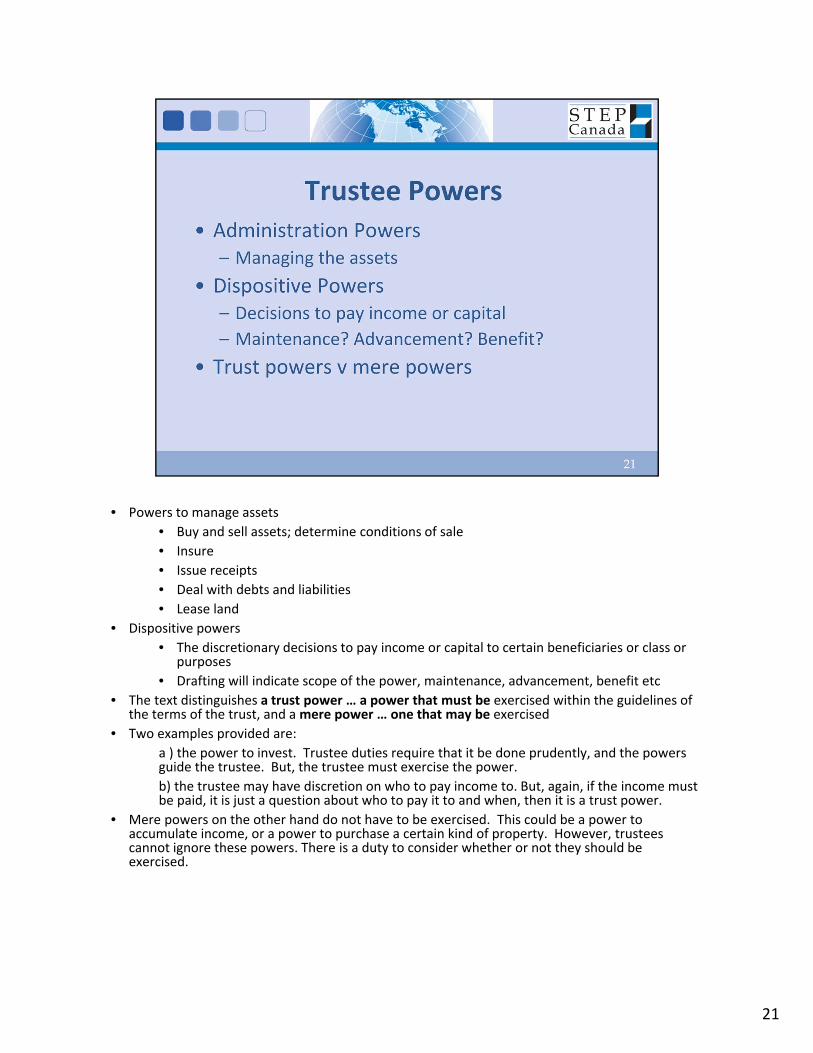

• Powers to manage assets

• Buy and sell assets; determine conditions of sale

• Insure

• Issue receipts

• Deal with debts and liabilities

• Lease land

• Dispositive powers

• The discretionary decisions to pay income or capital to certain beneficiaries or class or purposes

• Drafting will indicate scope of the power, maintenance, advancement, benefit etc

• The text distinguishes a trust power … a power that must be exercised within the guidelines of the terms of the trust, and a mere power … one that may be exercised

• Two examples provided are:

a ) the power to invest. Trustee duties require that it be done prudently, and the powers guide the trustee. But, the trustee must exercise the power.

b) the trustee may have discretion on who to pay income to. But, again, if the income must be paid, it is just a question about who to pay it to and when, then it is a trust power.

• Mere powers on the other hand do not have to be exercised. This could be a power to accumulate income, or a power to purchase a certain kind of property. However, trustees cannot ignore these powers. There is a duty to consider whether or not they should be exercised.

21

• Many trusts have significant discretionary powers over income and/or capital

• Must review the drafting when making a decision to encroach

• When a request is made, trustee must turn mind to the decision

• Does the request fall within the criteria?

• If so, is the request reasonable? Does it make sense in the broader context?

• Examples of considerations

• If the request is to purchase a home or vehicle, is it a fair price?

• If payment is only a down payment, and the beneficiary is taking out a loan, can he/she support the loan or will there be more requests in future from the trust?

• If the payment is made, what impact on future income and/or capital growth? Who is impacted? Is that impact relevant to this decision?

• Do not confuse impartiality with equality

• Documenting decisions: (not highlighted in materials)

• How much to document? Balance between:

• If no reasons provided … the court can intervene if decision is patently unreasonable on its face

• If reasons are provided … the court can review for bad faith, out of scope, etc and set aside

• Even if a decision is to reject the request, documentation of the decision is required

22

• What questions would you ask?

• Does your response change if the trust has $2million and the beneficiary making the request is the sole life tenant?

• What if the beneficiary is the sole capital beneficiary?

23

• Trustees have a duty to invest and powers will establish scope of decisions to be made

• In absence of direction in trust or will, see legislation

• Prudent Investor rule in most provinces now.

• Need to be familiar with what your legislation says in your province and be able to look at a scenario and consider how it might fit.

• If in BC, consider what it means given that the legislation does not set out the criteria. The drafters took the view that the lists in the other provinces could become too narrow and/or a checklist and would ignore other relevant factors. It was not intended to suggest the same criteria wouldn’t be relevant.

• Some provinces still have “prudent person”. Unclear how it still differs. May be subject to some of the laws described. When reviewing a scenario, think about the criteria generally as any prudent person would do.

Generally now:

• Trustee’s defence begins with the evidence of a prudent investment plan that considers relevant factors

• Compliance with the plan, monitoring, ongoing review will be required

• Diversification is required but must be appropriate to liquidity needs, markets, purpose of the trust

• Delegation is permitted, but must be prudent, appropriate, costs reasonable

• “special assets” may have a role and if so, can be retained. Need to document decision

• Liability – offset is required; Ontario: note that the court does not have authority to relieve from breach of trust – must fit within the investment provisions

24

What is required for impartiality when investing?

• No encroachment powers; therefore spouse requires income

• Preservation and growth of capital for remainder beneficiaries

• Prudence

• 1st step is an investment policy statement

• Treat trust like any other investor – risk tolerance and needs of the trust, not the trustee

• Diversification of asset classes and assets

• Is 50% in real estate appropriate?

• Where applicable – does the apartment have a special purpose? Need more facts

• No longer require income and growth for each asset, so consider a mix

• Consider other criteria on list where applicable, and generally in other provinces

• When investing, decision on whether or not to hire an investment manager

• Permitted in most provinces – see your trustee acts

• Must still be prudent – skills, cost, supervise

• Generally, trustees must make own decisions; practical issues arise when beneficiaries have their own ideas and/or advisors and may request trustees to make decisions which may be in breach of a trustee duty, create a conflict of interest, or be inappropriate for a trust.

• Remember that the investor is the trust/trustee, and not the trustee in his/her personal capacity. Risk tolerance can be very different.

25

Practical issue:

• Beneficiaries and co‐trustees want something done that would amount to a breach.

• Trustee has an opportunity to provide a better interest rate on cash balances using internal services

In absence of express permission in the trust, and/or an exculpation clause, consider:

• Written consent accompanied with a release from liability, and if appropriate an indemnity for claims from other beneficiaries.

• Ensure independent legal advice

• Reinforces the defences that the trustee has (see next slide)

26

Limitation periods: But caution – When does it start?

• Age of majority?

• When breach is discovered?

• Depends on nature of claim

Laches – delay in taking action; too long ago

Acquiescence – had information; did not do anything; good reason to provide accounts

Beneficiary instigated breach – e.g. asked for a payment or a purchase

Trustee beneficiary cannot claim as a beneficiary

Statutory relief in most provinces (note Ontario exception on investments)

27

Tempest v Lord Camoy:

• will not intervene to force exercise of an unfettered discretion

• But if there is a duty, will require it be exercised properly and in reasonable time

• Will prevent improper exercise

Gisborne:

• Uncontrolled authority; court will not intervene unless there is mala fides

• Beneficiary’s own resources are not necessarily a good reason to refuse

Fox:

• Mala fides: improper reason for refusal to distribute to son; extraneous reason (religion)

Wright:

• Followed Fales; trustee “deadlock”; asked court intervention

• Refused; trustee cannot shift its responsibility to the court

• Only intervene if mala fides or refusing to exercise discretion

Schipper:

• Corporate trustee refused – putting priority on contingent future benes

• Ignored unanimous consent of living beneficiaries

Re Blow:

• Mala fides is more than dishonesty; includes not considering duty/decision

• Blindly followed testator guidelines on when to make payments (in a memo, not trust powers)

Kordyban

• Example of court intervening to break a deadlock to protect assets

28

29

30

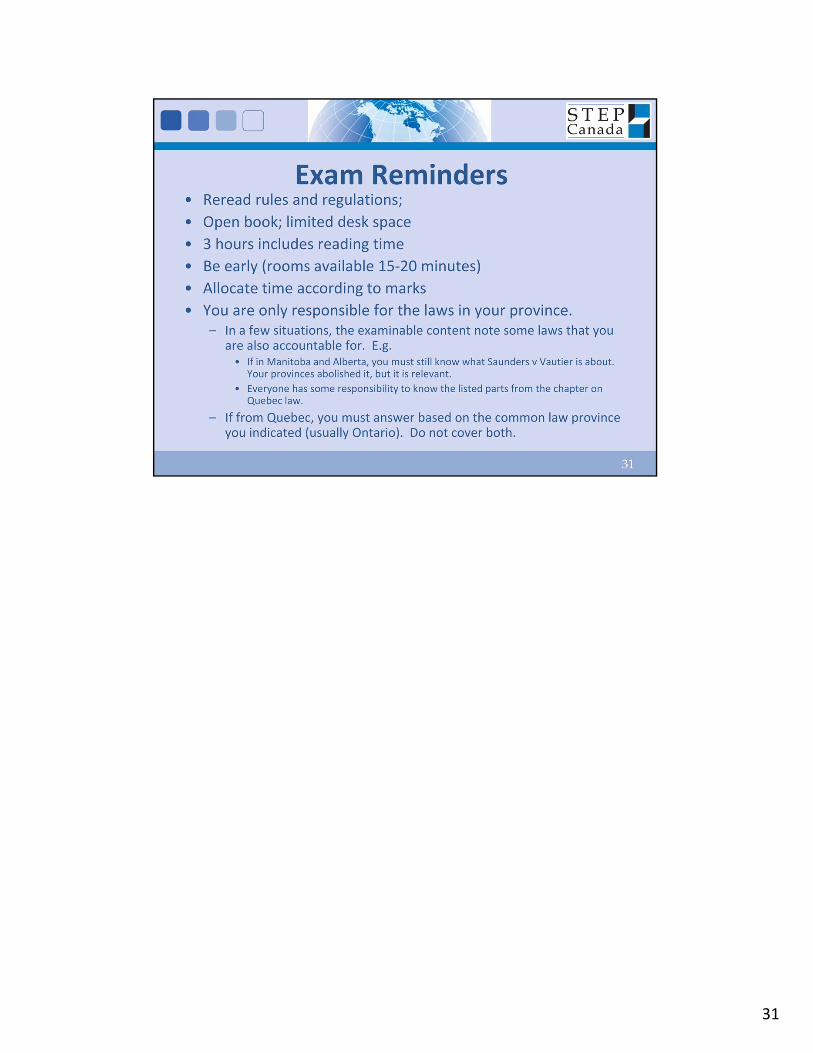

31

32

33