Embed Size (px)

DESCRIPTION

trips

Citation preview

Retail Parks: Spatial and Functional Integration of Retail Units in the Swansea Enterprise ZoneAuthor(s): Rosemary D. F. Bromley and Colin J. ThomasSource: Transactions of the Institute of British Geographers, New Series, Vol. 13, No. 1 (1988),pp. 4-18Published by: The Royal Geographical Society (with the Institute of British Geographers)Stable URL: http://www.jstor.org/stable/622771 .

Accessed: 02/12/2013 06:04

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

The Royal Geographical Society (with the Institute of British Geographers) is collaborating with JSTOR todigitize, preserve and extend access to Transactions of the Institute of British Geographers.

http://www.jstor.org

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

4

Retail parks: spatial and functional integration of retail units in the Swansea Enterprise Zone ROSEMARY D. F. BROMLEY Tutor in Geography, Department of Geography, University College of Swansea, Swansea, SA2 8PP

COLIN J. THOMAS Lecturer in Geography, Department of Geography, University College of Swansea, Swansea, SA2 8PP

Revised MS received 5 January, 1987

ABSTRACT Retail parks form an important new element in the retail system of British cities and constitute a significant modification to the traditional hierarchy of shopping centres. They comprise loose groupings of superstores and retail warehouses at highly accessible suburban and out-of-town locations. The relaxation of planning controls on retailing in a number of Enterprise Zones has encouraged such developments. The individual stores may function as largely separate entities or together as integrated shopping centres. However, considering the existing scale of such developments and the substantial commercial pressures for further schemes, evidence on this issue is lacking. The article outlines the general functional characteristics of retail parks before focussing on the shopping linkages between stores in the Swansea Enterprise Zone retail park. All the stores predominantly serve car-owning households drawn from a wide trade area. The retail park functions as a loosely structured collection of stores rather than as a strongly integrated shopping centre. The shopping linkages between stores demonstrate a low level of interrelationships and a functional dichotomy between the superstores and retail warehouses. Nevertheless, a number of significant functional linkages are identified reflecting comparison shopping, the spatial contiguity of some stores and 'spin-off' trips generated by a small number of key retail units. The commercial disadvantages of a peripheral site and the traffic congestion resulting from vehicular circulation within the retail park are apparent. The commercial and environmental advantages of an integrated spatial structure for future retail parks are stressed.

KEY WORDS: Shopping linkages; Enterprise Zone Retailing; Retail parks; Superstores; Retail warehouses; Out-of-town shopping

INTRODUCTION Retail parks are a very recent and expanding feature of the 'retail revolution' (Dawson, 1983, p. 87) which has occurred in British cities. They usually comprise a loose grouping of superstores and retail warehouses located at nodal points in the suburbs. Commonly, they are adjacent to major roads, close to motorway junctions or have been developed on industrial estates and in Enterprise Zones (EZ), where access and visibility to potential customers is good.

The retail park is essentially the culmination of two earlier developments in the retail environment. The first, beginning in the mid-1960s, involved the development of superstores and hypermarkets, and

initiated the process of retail decentralization and suburbanization (Davies and Kirby, 1980). The second change which followed in the mid-1970s saw the establishment of retail warehouses, initially selling DIY products and comparison goods such as furniture, carpets and electricals (Jones, 1984, p. 42). More recently, the array of goods being sold in retail ware- houses has expanded dramatically and now includes clothing, footwear, toys and car accessories (Bernard Thorpe and Partners, 1985, p. 10). The locational preferences and styles of trading of most superstores, hypermarket and retail warehouse operators have been similar. Generally, large accessible sites on the edges of cities have been favoured, and as a result of

Trans. Inst. Br. Geogr. N.S. 13: 4-18 (1988) ISSN: 0020-2754 Printed in Great Britain

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 5

ad hoc planning decisions individual stores were usually developed in isolated locations (Gibbs, 1981; 1985).

Since the early 1980s planning authorities have increasingly directed retail warehouse developments to industrial estate sites. This has resulted in the emergence of loose agglomerations or, occasionally, planned concentrations of retail warehouses in indus- trial estate locations. Such developments have been termed 'retail warehouse parks' (Bernard Thorpe and Partners, 1985). Where such developments incorpor- ate superstores or hypermarkets a more balanced shopping area results, with a potentially greater impact on the local and regional retail environment. These have been termed retail parks (Wade, 1985, p. 13), interesting examples of which are the Cribbs Causeway development on the northern periphery of Bristol and the Merry Hill retail park in the Dudley Enterprise Zone (Dudley Metropolitan Borough, 1985). Unlike conventional shopping centres, how- ever, retail parks are characterized to date by little other than superstores and retail warehouses. The wide range of specialist shops and retail services found in district and city centres is absent.

The development of retail parks has undoubtedly been encouraged by recent policies pursued by large retailing chains and by the actions of central govern- ment. The structure plans of the 1970s generally aimed to preserve existing shopping hierarchies, but this constraint has diminished under intense pressure from retailers for edge-of-town sites. This pressure has resulted in the revision of national policy guidance. In recent years this has led to the relaxation of earlier restrictions on such developments, albeit in an im- plicit and uncoordinated manner rather than through a comprehensive new strategy. It is noteworthy that for superstore applications alone, 62 out of the 180 applications refused by local councils in the period 1970-85 were accepted on appeal (Lee Donaldson Associates, 1986). The increasingly lenient attitude towards out-of-town shopping developments was further indicated by the Government circular of July 1985 which supported a policy favouring permission for development unless 'demonstrable harm' could be proven (URPI Newsletter, Nov. 1985).

Enterprise Zone policy announced by the Govern- ment in 1980, offering financial incentives and a simplified planning regime (Bromley and Morgan, 1985, p. 404), has also encouraged the growth of retail parks in those Enterprise Zones where large- scale retail activity has not been specifically excluded (Dawson and Sparks, 1982; Sparks, 1987). The

Swansea, Dudley and Gateshead EZ, for example all include major retail developments. The Dudley Enterprise Zone included a hypermarket and eleven retail warehouses in the summer of 1986 (Dudley Metropolitan Borough, 1986), while the large scale development at Gateshead was under construction (Cameron Hall Developments, 1985).

The newly emerging retail parks may well function as shopping centres in the sense that the separate stores might incorporate significant reciprocal func- tional relationships or combined attractive power for a large proportion of the more mobile sections of the community; but the evidence is lacking. There is a substantial body of literature on individual super- stores and hypermarkets (URPI, 1980; 1985; Gibson and Hurdle, 1985a) and limited, but growing research publication on retail warehouses (Gibbs, 1985; Gibson and Hurdle, 1985b; URPI, 1986); but the functioning and characteristics of the retail park, where these retail units are combined, are largely unknown. In terms of the internal functional linkages of shoppers within retail parks publication is confined to a number of intuitive design suggestions incorpor- ated in a review of retail warehouse parks (Bernard Thorpe and Partners, 1985).

In view of the paucity of evidence, this article outlines the general functional characteristics of the Swansea Enterprise Zone retail park before focussing on the shopping linkages between the stores. The study examines the degree to which the various stores function as a shopping centre or as a loose collection of functionally isolated units. This focus is particularly appropriate since Bernard Thorpe and Partners (1985) single out the concentration of retail development in the Swansea Enterprise Zone, along with the Newport, Maesglas industrial estate as '.... not laid out to encourage shoppers to move from one (store) to another', (p. 6). Currently, the Swansea Enterprise Zone retail area is one of the foremost examples of an out-of-town retail park, but other unplanned retail parks emerging elsewhere in Britain are likely to yield similar research findings when they reach the same stage of development.

RETAIL PARKS IN GREATER SWANSEA

In the mid-1970s the system of shopping centres in Greater Swansea conformed to the traditional British pattern dominated by the regional centre of Swansea with circa 131 000 m2 (1.4 million sq. ft.) of net retail sales area (West Glamorgan County Council, 1978). This was complemented by the four large district

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

6 ROSEMARY D. F. BROMLEY and COLIN]. THOMAS

Superstores Fitted Kitchens, Mammoth Bedrooms

DI Y,E Autoand Eectricals Quasi-retail

Furnishings, Major landscape OFurniture belts

Clothing, Enterprise Zone

U dcShoes Boundary

Update Interview sites 6 SWest End

.Pub...

Norman's *.

. Shoe T Tesco * rp Kingsway

8Alliedr Lupcas utrice M

Sigma 3 5 City Queensway N ~/" *

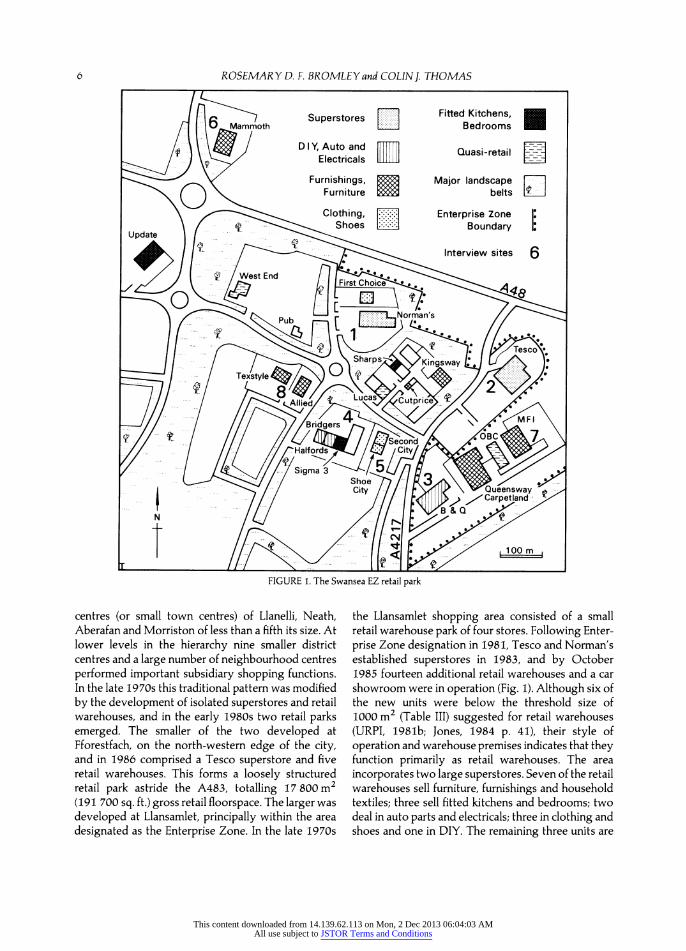

loomm FIGURE 1. The Swansea EZ retail park

centres (or small town centres) of Llanelli, Neath, Aberafan and Morriston of less than a fifth its size. At lower levels in the hierarchy nine smaller district centres and a large number of neighbourhood centres performed important subsidiary shopping functions. In the late 1970s this traditional pattern was modified by the development of isolated superstores and retail warehouses, and in the early 1980s two retail parks emerged. The smaller of the two developed at Fforestfach, on the north-western edge of the city, and in 1986 comprised a Tesco superstore and five retail warehouses. This forms a loosely structured retail park astride the A483, totalling 17 800 m2 (191 700 sq. ft.) gross retail floorspace. The larger was developed at Llansamlet, principally within the area designated as the Enterprise Zone. In the late 1970s

the Llansamlet shopping area consisted of a small retail warehouse park of four stores. Following Enter- prise Zone designation in 1981, Tesco and Norman's established superstores in 1983, and by October 1985 fourteen additional retail warehouses and a car showroom were in operation (Fig. 1). Although six of the new units were below the threshold size of 1000 m2 (Table III) suggested for retail warehouses (URPI, 1981b; Jones, 1984 p. 41), their style of operation and warehouse premises indicates that they function primarily as retail warehouses. The area incorporates two large superstores. Seven of the retail warehouses sell furniture, furnishings and household textiles; three sell fitted kitchens and bedrooms; two deal in auto parts and electricals; three in clothing and shoes and one in DIY. The remaining three units are

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 7

TABLE I. Numbers of respondents by interview site: Swansea EZ retail park survey, 1985

Interview Site No. on Store name and No. of Fig. I description respondents

1 Norman's Superstore 112 2 Tesco Superstore 131 3 B & Q (DIY) 103 4 Halfords-Bridgers (Auto, Elects) 105 5 Second City (Clothing)-Shoe City 103 6 Mammoth (Furniture) 40 7 MFI (Furniture) 42 8 Texstyle World-Allied Carpets 40

Total 676

quasi-retail premises and include a builders' supplier, a car showroom and an auto-electrical supplier. At the time of the survey the retail park totalled almost 36 000 m2 (387 500 sq. ft.) gross retail floorspace, which is equivalent to approximately a fifth of that in the city centre (Rees, 1986, p. 37). In terms of scale, this ranks amongst the second tier of large district shopping centres in Greater Swansea.

In order to investigate the functioning of the Swansea Enterprise Zone retail park a shopper survey was conducted in collaboration with Swansea City Council. Following a pilot survey in June 1985, 676 interviews were subsequently completed on a Friday and Saturday in October 1985 at eight locations (Table I).

THE ATTRACTION OF THE RETAIL PARK

Retailers are attracted by the good access and the relatively cheap land or premises in retail parks. Such conditions allow for the easy delivery and purchase of goods and permit ample display and storage space. Investment in premises is limited because the warehouse-style buildings of retail parks are rarely constructed to last more than thirty years. All these conditions conform with the '.... development strategies geared to raising profit levels' (Jones, 1984, p. 41) currently being pursued by many large scale retailing chains.

Customers are also attracted by the good access which is such a basic feature of the retail park. How- ever, access is usually only good for the car-borne shopper since public transport is poor to most edge- of-town locations. Bernard Thorpe and Partners

(1985, p. 58) reported that 83 per cent of shoppers visiting the Aireside Centre in Leeds travelled by car, as did 97 per cent of shoppers at a retail furnishings 'superstore' at Fareham (Hallsworth, 1983, p. 20). The shopper survey conducted at the Swansea Enterprise Zone retail park showed that a similarly high pro- portion had arrived by car (93 per cent). As a result, the clientele of the retail park is necessarily biased towards the more affluent car-owning section of the community. As many as 95 per cent of the respondents were from car-owning households whereas the 1981 census records only a 60 per cent car ownership level in West Glamorgan. Moreover, Social Class I and II were over-represented compared with the county figure (26 per cent and 17 per cent respectively).

The shopper survey also investigated respondents reasons for shopping in the retail park. The respon- dents were asked to ascribe one of three levels of importance to each of thirteen statements relating to their reasons for shopping in the area. Ease of parking and convenient shopping hours were identified as very important by half of all shoppers, and as either important or very important by 91 per cent and 87 per cent respectively. Ample parking spaces exist adjacent to all the stores and shopping hours extend to 8.00 p.m. on most evenings. A second group of important attractions embraced the wide choice of goods, the competitive prices and the freedom to browse. A third group of factors identified as import- ant by three quarters of respondents comprised the convenient grouping of the shops (see later discus- sion), the quality of goods and service in the stores, and the convenient car journey to the stores.

THE SUPERSTORE-RETAIL WAREHOUSE FUNCTIONAL DICHOTOMY

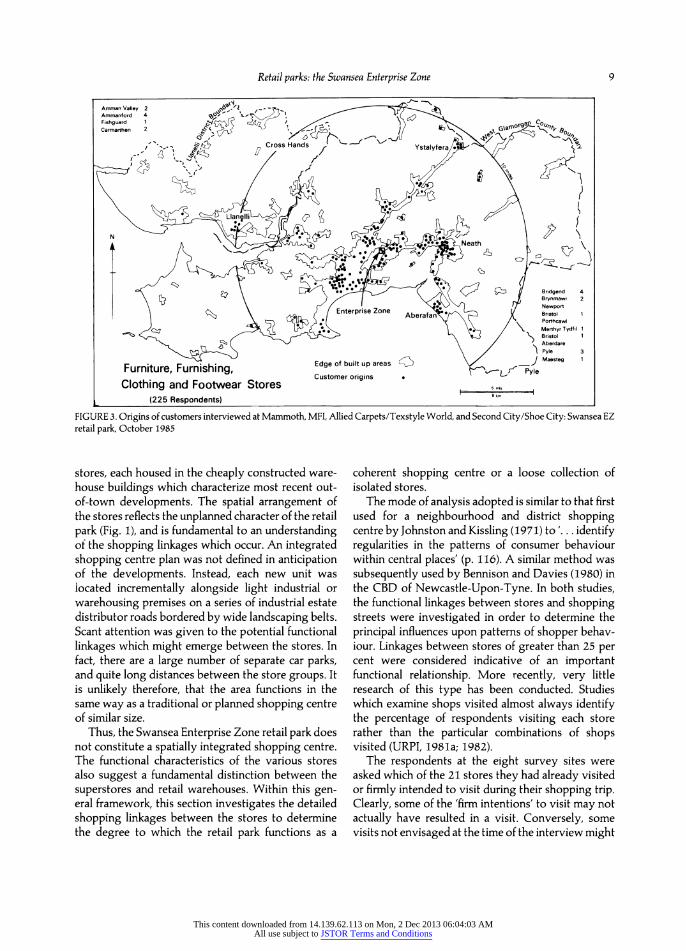

The superstore-retail warehouse dichotomy is funda- mental to an understanding of the functioning of the retail park. The survey data revealed the importance of the distinction in terms of trade areas, frequency of visits and degree of customer allegiance (Thomas and Bromley, 1987). The trade area of the superstores was far more restricted than that of the retail warehouses. Of the shoppers at the superstores 55 per cent had travelled less than three miles, whereas for those at the retail warehouses only 36 per cent had come from the same area. Conversely, only 18 per cent of super- store respondents travelled further than seven miles, while 28 per cent of retail warehouse clients had travelled such distances. These differences reflect the convenience grocery functions of the superstores and

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

8 ROSEMARY D. F. BROMLEY and COLIN]. THOMAS

Lampeter 1 -

efd 1 re 1

Enterp Aberafan Merthyr Tydfil 2

Edge of built up areas

Superstores Customer originsP

(243 Respondents)

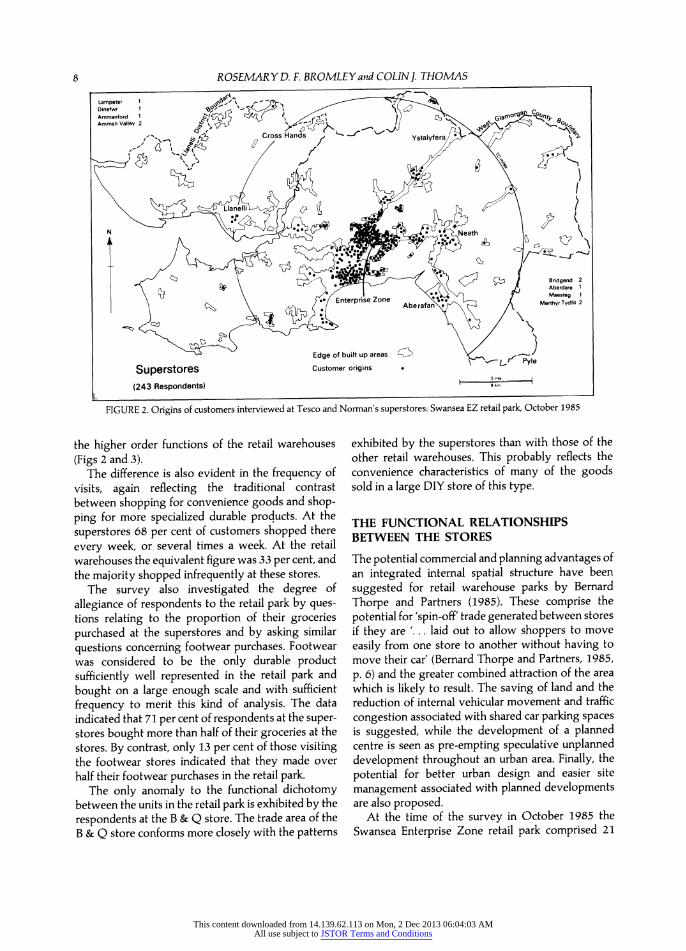

FIGURE 2. Origins of customers interviewed at Tesco and Norman's superstores: Swansea EZ retail park, October 1985

the higher order functions of the retail warehouses (Figs 2 and 3).

The difference is also evident in the frequency of visits, again reflecting the traditional contrast between shopping for convenience goods and shop- ping for more specialized durable products. At the

superstores 68 per cent of customers shopped there every week, or several times a week. At the retail warehouses the equivalent figure was 33 per cent, and the majority shopped infrequently at these stores.

The survey also investigated the degree of allegiance of respondents to the retail park by ques- tions relating to the proportion of their groceries purchased at the superstores and by asking similar

questions concerning footwear purchases. Footwear was considered to be the only durable product sufficiently well represented in the retail park and bought on a large enough scale and with sufficient frequency to merit this kind of analysis. The data indicated that 71 per cent of respondents at the super- stores bought more than half of their groceries at the stores. By contrast, only 13 per cent of those visiting the footwear stores indicated that they made over half their footwear purchases in the retail park.

The only anomaly to the functional dichotomy between the units in the retail park is exhibited by the respondents at the B & Q store. The trade area of the B & Q store conforms more closely with the patterns

exhibited by the superstores than with those of the other retail warehouses. This probably reflects the convenience characteristics of many of the goods sold in a large DIY store of this type.

THE FUNCTIONAL RELATIONSHIPS BETWEEN THE STORES

The potential commercial and planning advantages of an integrated internal spatial structure have been suggested for retail warehouse parks by Bernard Thorpe and Partners (1985). These comprise the

potential for 'spin-off' trade generated between stores if they are '... laid out to allow shoppers to move easily from one store to another without having to move their car' (Bernard Thorpe and Partners, 1985, p. 6) and the greater combined attraction of the area which is likely to result. The saving of land and the reduction of internal vehicular movement and traffic congestion associated with shared car parking spaces is suggested, while the development of a planned centre is seen as pre-empting speculative unplanned development throughout an urban area. Finally, the

potential for better urban design and easier site management associated with planned developments are also proposed.

At the time of the survey in October 1985 the Swansea Enterprise Zone retail park comprised 21

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 9

Amman Valley 2 6 .. Ammanford 4 001

Fishguard 1 co u a \*o

I . Cross Hands Ystalyfera/*

N N

Bridgend 4 Bnmawr 2

EnterpriseZoneAbaNewport

e0000 Merthyr Tydfil 1

(22 Rmi

Bristol 1

Clothing and Footwear Stores (1225 Respondents)

FIGURE 3. Origins of customers interviewed at Mammoth, MFI, Allied Carpets/Texstyle World, and Second City/Shoe City: Swansea EZ retail park, October 1985

stores, each housed in the cheaply constructed ware- house buildings which characterize most recent out- of-town developments. The spatial arrangement of the stores reflects the unplanned character of the retail park (Fig. 1), and is fundamental to an understanding of the shopping linkages which occur. An integrated shopping centre plan was not defined in anticipation of the developments. Instead, each new unit was located incrementally alongside light industrial or warehousing premises on a series of industrial estate distributor roads bordered by wide landscaping belts. Scant attention was given to the potential functional linkages which might emerge between the stores. In fact, there are a large number of separate car parks, and quite long distances between the store groups. It is unlikely therefore, that the area functions in the same way as a traditional or planned shopping centre of similar size.

Thus, the Swansea Enterprise Zone retail park does not constitute a spatially integrated shopping centre. The functional characteristics of the various stores also suggest a fundamental distinction between the superstores and retail warehouses. Within this gen- eral framework, this section investigates the detailed shopping linkages between the stores to determine the degree to which the retail park functions as a

coherent shopping centre or a loose collection of isolated stores.

The mode of analysis adopted is similar to that first used for a neighbourhood and district shopping centre by Johnston and Kissling (1971) to '. .. identify regularities in the patterns of consumer behaviour within central places' (p. 116). A similar method was subsequently used by Bennison and Davies (1980) in the CBD of Newcastle-Upon-Tyne. In both studies, the functional linkages between stores and shopping streets were investigated in order to determine the principal influences upon patterns of shopper behav- iour. Linkages between stores of greater than 25 per cent were considered indicative of an important functional relationship. More recently, very little research of this type has been conducted. Studies which examine shops visited almost always identify the percentage of respondents visiting each store rather than the particular combinations of shops visited (URPI, 1981a; 1982).

The respondents at the eight survey sites were asked which of the 21 stores they had already visited or firmly intended to visit during their shopping trip. Clearly, some of the 'firm intentions' to visit may not actually have resulted in a visit. Conversely, some visits not envisaged at the time of the interview might

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

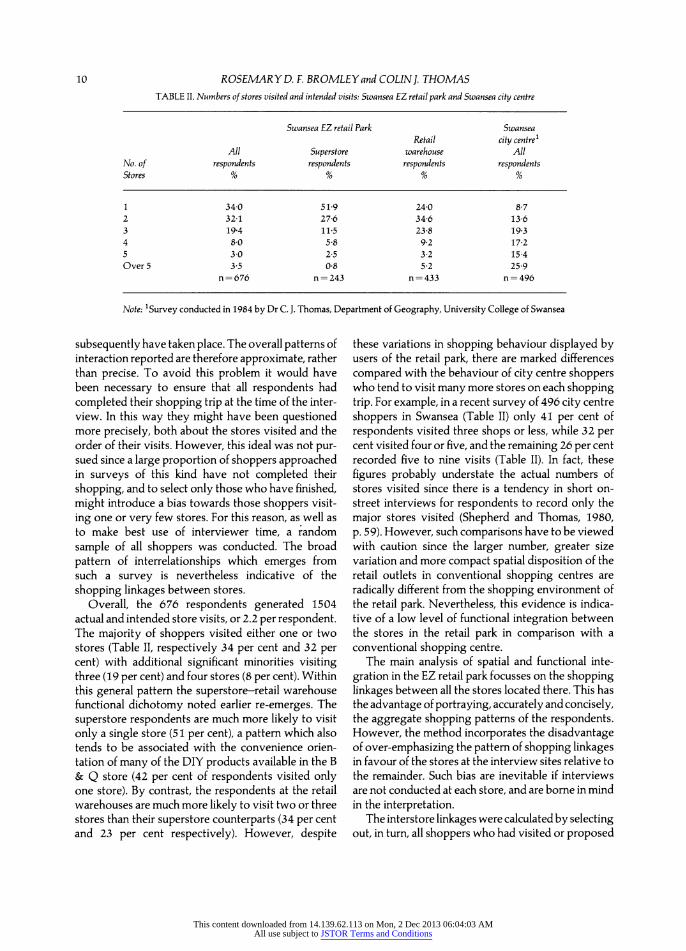

10 ROSEMARY D. F. BROMLEY and COLINI. THOMAS TABLE II. Numbers of stores visited and intended visits: Swansea EZ retail park and Swansea city centre

Swansea EZ retail Park Swansea Retail city centre'

All Superstore warehouse All No. of respondents respondents respondents respondents Stores % % % %

1 34-0 51-9 24.0 837 2 32.1 27-6 34.6 13.6 3 19.4 11-5 23.8 19.3 4 8-0 5-8 9.2 17-2 5 3-0 2-5 3.2 15.4 Over 5

3.5 0-8

5.2 25-9

n= 676 n= 243 n= 433 n = 496

Note: 'Survey conducted in 1984 by Dr C. J. Thomas, Department of Geography, University College of Swansea

subsequently have taken place. The overall patterns of interaction reported are therefore approximate, rather than precise. To avoid this problem it would have been necessary to ensure that all respondents had completed their shopping trip at the time of the inter- view. In this way they might have been questioned more precisely, both about the stores visited and the order of their visits. However, this ideal was not pur- sued since a large proportion of shoppers approached in surveys of this kind have not completed their shopping, and to select only those who have finished, might introduce a bias towards those shoppers visit- ing one or very few stores. For this reason, as well as to make best use of interviewer time, a random sample of all shoppers was conducted. The broad pattern of interrelationships which emerges from such a survey is nevertheless indicative of the shopping linkages between stores.

Overall, the 676 respondents generated 1504 actual and intended store visits, or 2.2 per respondent. The majority of shoppers visited either one or two stores (Table II, respectively 34 per cent and 32 per cent) with additional significant minorities visiting three (19 per cent) and four stores (8 per cent). Within this general pattern the superstore-retail warehouse functional dichotomy noted earlier re-emerges. The superstore respondents are much more likely to visit only a single store (51 per cent), a pattern which also tends to be associated with the convenience orien- tation of many of the DIY products available in the B & Q store (42 per cent of respondents visited only one store). By contrast, the respondents at the retail warehouses are much more likely to visit two or three stores than their superstore counterparts (34 per cent and 23 per cent respectively). However, despite

these variations in shopping behaviour displayed by users of the retail park, there are marked differences compared with the behaviour of city centre shoppers who tend to visit many more stores on each shopping trip. For example, in a recent survey of 496 city centre shoppers in Swansea (Table II) only 41 per cent of respondents visited three shops or less, while 32 per cent visited four or five, and the remaining 26 per cent recorded five to nine visits (Table II). In fact, these figures probably understate the actual numbers of stores visited since there is a tendency in short on- street interviews for respondents to record only the major stores visited (Shepherd and Thomas, 1980, p. 59). However, such comparisons have to be viewed with caution since the larger number, greater size variation and more compact spatial disposition of the retail outlets in conventional shopping centres are radically different from the shopping environment of the retail park. Nevertheless, this evidence is indica- tive of a low level of functional integration between the stores in the retail park in comparison with a conventional shopping centre.

The main analysis of spatial and functional inte- gration in the EZ retail park focusses on the shopping linkages between all the stores located there. This has the advantage of portraying, accurately and concisely, the aggregate shopping patterns of the respondents. However, the method incorporates the disadvantage of over-emphasizing the pattern of shopping linkages in favour of the stores at the interview sites relative to the remainder. Such bias are inevitable if interviews are not conducted at each store, and are borne in mind in the interpretation.

The interstore linkages were calculated by selecting out, in turn, all shoppers who had visited or proposed

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 11

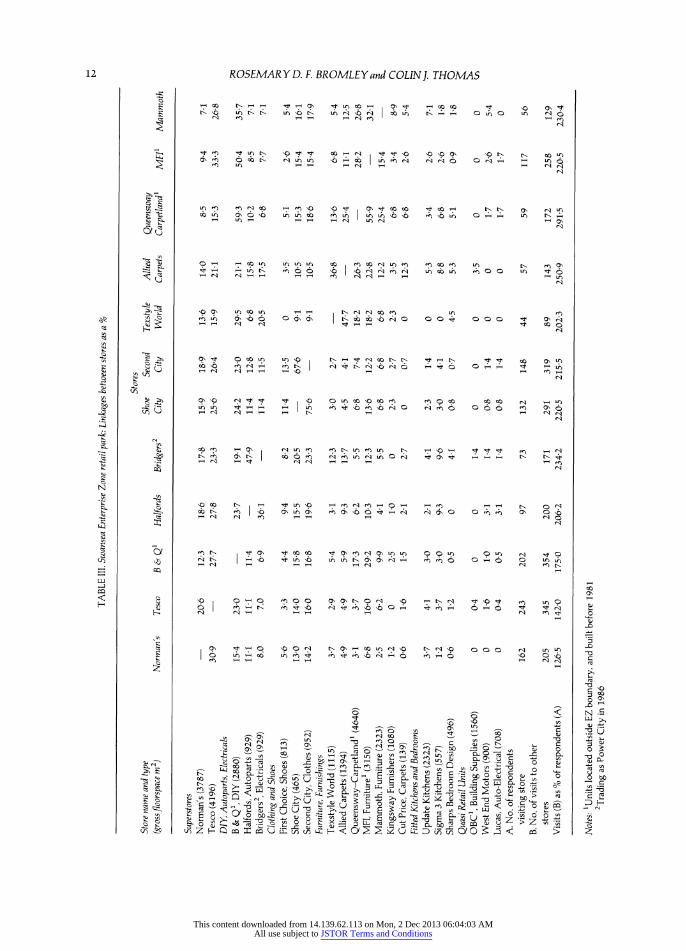

to visit a particular store. The number of visits conducted by these shoppers to all other stores in the retail park were then identified. This approach was repeated for the shoppers at each store. The data presented in percentage form on Table III are confined to those stores which attracted more than 40 shoppers, since linkage percentages based on figures smaller than this were considered unreliable. Not unexpectedly, all but one of the twelve stores included were sites where interviews had been under- taken. The exception, Queensway-Carpetland, was adjacent to the B & Q interview site. Many of the linkage percentages are low compared with those reported in the earlier studies noted of conventional shopping centres. In order to highlight the weaker patterns of store association which exist in the retail park, linkages of more than 5 per cent are considered sufficiently strong for investigation.

In order to obtain a complete picture of the shopping linkages of each store, Table III should be interpreted in two ways: by column and by row. For example, column one represents the shopping link- ages between Norman's superstore and all the other stores in the retail park expressed as a percentage of the shoppers visiting Norman's. Thus, of the 162 shoppers at Norman's, 31 per cent visited or intended to visit Tesco and 15 per cent B & Q. Row one, on the other hand, indicates the linkage between Norman's and the other stores, but in this case the linkage is expressed as a percentage of the total shoppers visiting the other stores. For example, the eighteen shoppers at Norman's who also visited Halfords com- prise 11 per cent of the Norman's shoppers but nearly 19 per cent of the Halfords shoppers. Each linkage in the matrix is therefore represented in two different ways. The principal diagonal is, of course, 100 per cent in each instance.

Shopping linkages between stores The shopping linkages which emerge from the analysis exhibit a number of interesting patterns. The superstore-retail warehouse dichotomy can again be recognized. The two superstores tend to generate proportionally fewer visits to other stores than the retail warehouses (Norman's 127 per cent and Tesco 142 per cent of their shoppers respectively: see base of Table III). This is indicative of the primarily bulk convenience shopping trips of the majority of super- store shoppers previously mentioned. They appear to be using the superstores to a large degree as one stop convenience shopping centres (51 per cent of shoppers). This is reflected in the relatively low level

of shopping linkages associated with these stores (Fig. 4, Table III), and suggests their isolated functional status. In fact their strongest association is a moderate reciprocal relationship between themselves. A signifi- cant 31 per cent of Norman's shoppers also visit Tesco, which can also be expressed as 21 per cent of Tesco shoppers. This is probably indicative of an element of price conscious comparison shopping for grocery products.

Other linkages involving the superstores are generally smaller, although large minorities of Tesco and Norman's shoppers also visit B & Q (23 per cent and 15 per cent respectively). In addition, 16 per cent of Tesco shoppers visit MFI, while both superstores record notable but smaller associations with the clothing and footwear outlets and Halfords. The low level and functional variety of these linkages suggest an additional element of 'spin-off' shopping by the superstore shoppers. The wider significance of this effect will be examined in more detail at a later stage of the analysis.

Amongst the retail warehouses the B & Q store again emerges as an anomaly. It exhibits a level of shopping linkages mid-way between those of the superstores and the other retail warehouses. In part, this probably reflects the fact that many DIY products are convenience goods. The lack of a store offering a closely similar array of DIY goods in the retail park would have also deflated any tendency for compari- son shopping linkages. However, the limited range of furniture and furnishing items stocked does appear to encourage comparison linkages between B & Q and some of the furniture retail warehouses (29 per cent with MFI and 17 per cent with Queensway- Carpetland: Fig. 4).

In general, however, the shopping linkages from the other retail warehouses are greater in degree, and in some cases, more spatially diffuse. For all retail warehouses the level of visits exceeds 200 per cent and for Queensway-Carpetland it reaches 292 per cent (Table III). The patterns reflect two principal types of shopping linkages. The 'comparison shop- ping' tendency is strongest for the furniture and fur- nishings stores. For example, large percentages of those shopping at Queensway-Carpetland also visit MFI (56 per cent), Mammoth (25 per cent) and Allied Carpets (25 per cent). For those shopping at Allied Carpets the strongest linkages, apart from those with the adjacent store, are with two other stores, selling carpets: 26 per cent with Queensway-Carpetland and 23 per cent with MFI. There is even a 12 per cent linkage with the small retail unit operating as Cut-

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

TABLE III. Swansea Enterprise Zone retail park: Linkages between stores as a %

Stores Store name and type Shoe Second Texstyle Allied Queensway (gross floorspace m2) Norman's Tesco B & Q1 Halfords Bridgers2 City City World Carpets Carpetland' MFI1 Mammoth

Superstores Norman's (3787)

20.6 12-3 1836 1738

15.9 1839

13.6 14-0 8-5 9-4

7-1 Tesco (4196) 30-9 27.7

2738 23.3 25.6 26.4

15-9 21.1

15-3 333 2638 DIY, Autoparts, Electricals B & Q', DIY (2880) 15-4 230 - 23-7 19-1 24-2 23-0 29-5 21-1

59.3 504 357

Halfords, Autoparts (929) 11-1 11.1 11-4 47-9 11-4 12-8 6-8 15-8 10-2 835 781 Bridgers2, Electricals (929) 8.0 7.0 6-9 36-1 - 114

11.5 20.5 17.5 638

7.7 771

Clothing and Shoes First Choice, Shoes (813) 5.6

3"3 4.4 9-4 832

11.4 13-5 0 3-5

5.1 2-6 54

Shoe City (465) 13.0 14.0

1538 15-5 205 -

67.6 9-1

10.5 15-3

15.4 16.1 Second City, Clothes (952) 14.2 16.0

1638 19.6 23.3

756 - 91 10.5

1836 15.4 17.9 Furniture, Furnishings

Texstyle World (1115) 3"7

2-9 5-4 3-1 12.3 3.0

2-7 3638 13.6

638 5.4 Allied Carpets (1394)

4.9 4-9 5-9 9-3

13.7 4.5 4.1 477 - 254 11.1

12.5 Queensway-Carpetland' (4640) 3-1 3-7 17.3 6.2 5.5

638 7-4 1832 26-3 2832 2638 MFI, Furniture' (3150) 6-8

16.0 29.2 10.3 12.3 13.6 12.2 1832 22-8 55-9

32.1 Mammoth, Furniture (2323) 2.5 6.2

9-9 4-1 5-5 638 638 638 12.2 25.4

154 -

Kingsway Furnishers (1080) 1.2

0 2.5

1-0 0 2.3 2.7

2-3 3-5 638 3-4 8.9 Cut Price, Carpets (139) 0-6 1.6 1.5 2.1

2-7 0 0.7

0 12-3 6-8 2-6 524

Fitted Kitchens and Bedrooms Update Kitchens (2323) 3-7 4-1 3-0

2.1 4-1 2-3

1.4 0 5-3 3-4 2-6

7-1 Sigma 3 Kitchens (557) 1.2

3-7 3-0 9-3 9.6

3-0 4-1 0 838 6-8 2.6

18 Sharps Bedroom Design (496)

0.6 1-2 0-5 0 4-1 0-8 0-7 4-5 5-3 5-1 0.9

1.8 Quasi Retail Units OBC1, Building Supplies (1560) 0 0-4 0 0

1.4 0 0 0

3.5 0 0 0

West End Motors (900) 0 1-6 1-0 3-1 1.4

0-8 1-4 0 0 1-7 2.6

5.4 Lucas, Auto-Electrical (708) 0

0.4 0-5 3-1

1.4 0 8 1-4 0 0 1-7 1-7 0

A. No. of respondents visiting store 162 243 202 97 73 132 148 44 57 59 117 56

B. No. of visits to other stores 205 345 354 200 171 291 319 89 143 172 258 129

Visits (B) as % of respondents (A) 126-5 142-0 175-0 206-2 234-2 220-5 215-5 202-3 250-9 291-5 220-5 230.4

Notes: 1Units located outside EZ boundary, and built before 1981 2Trading as Power City in 1986

tA

O

r)

r)

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 13

Mammoth ,

500 metres 4

Update

P =b Norman's

Texstyle Shaps Kingsway

Tco

0uwTesco

BSeconand MF

CitySecond City

ity OBC Carpetland

Linkages

Over 40%

S25-40% \\ 10-25%

\-\ - - - 5-10%

B and Q

\\I MFI

Second City

.

---

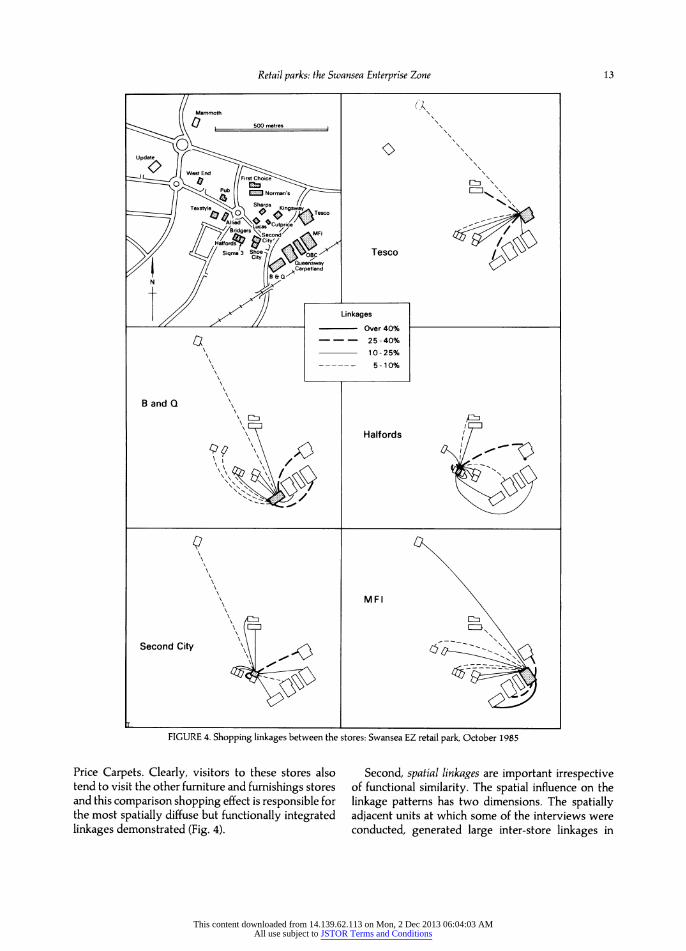

FIGURE 4. Shopping linkages between the stores: Swansea EZ retail park, October 1985

Price Carpets. Clearly, visitors to these stores also tend to visit the other furniture and furnishings stores and this comparison shopping effect is responsible for the most spatially diffuse but functionally integrated linkages demonstrated (Fig. 4).

Second, spatial linkages are important irrespective of functional similarity. The spatial influence on the linkage patterns has two dimensions. The spatially adjacent units at which some of the interviews were conducted, generated large inter-store linkages in

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

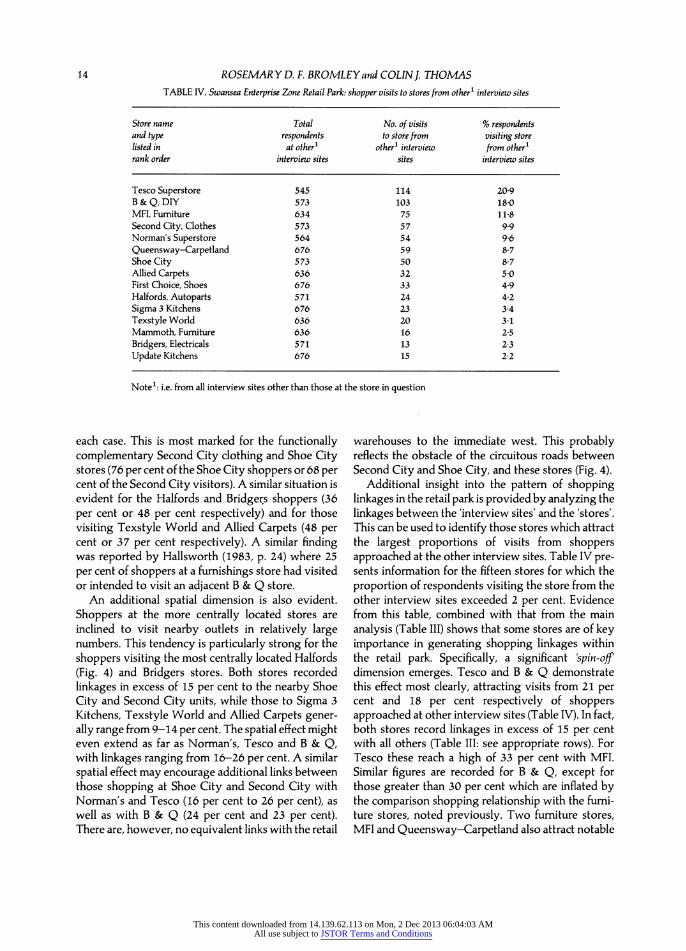

14 ROSEMARY D. F. BROMLEY and COLINJ. THOMAS TABLE IV. Swansea Enterprise Zone Retail Park: shopper visits to stores from other' interview sites

Store name Total No. of visits % respondents and type respondents to store from visiting store listed in at other1 other1 interview from other1 rank order interview sites sites interview sites

Tesco Superstore 545 114 20-9 B & Q, DIY 573 103 18.0 MFI, Furniture 634 75 11.8 Second City, Clothes 573 57 9.9 Norman's Superstore 564 54

9.6 Queensway-Carpetland 676 59 8.7 Shoe City 573 50 8.7 Allied Carpets 636 32 5-0

First Choice, Shoes 676 33 4-9 Halfords, Autoparts 571 24

4.2 Sigma 3 Kitchens 676 23 3.4 Texstyle World 636 20 3.1 Mammoth, Furniture 636 16 2.5 Bridgers, Electricals 571 13 2.3 Update Kitchens 676 15 2.2

Note1: i.e. from all interview sites other than those at the store in question

each case. This is most marked for the functionally complementary Second City clothing and Shoe City stores (76 per cent of the Shoe City shoppers or 68 per cent of the Second City visitors). A similar situation is evident for the Halfords and Bridgers shoppers (36 per cent or 48 per cent respectively) and for those visiting Texstyle World and Allied Carpets (48 per cent or 37 per cent respectively). A similar finding was reported by Hallsworth (1983, p. 24) where 25 per cent of shoppers at a furnishings store had visited or intended to visit an adjacent B & Q store.

An additional spatial dimension is also evident. Shoppers at the more centrally located stores are inclined to visit nearby outlets in relatively large numbers. This tendency is particularly strong for the shoppers visiting the most centrally located Halfords (Fig. 4) and Bridgers stores. Both stores recorded linkages in excess of 15 per cent to the nearby Shoe City and Second City units, while those to Sigma 3 Kitchens, Texstyle World and Allied Carpets gener- ally range from 9-14 per cent. The spatial effect might even extend as far as Norman's, Tesco and B & Q, with linkages ranging from 16-26 per cent. A similar spatial effect may encourage additional links between those shopping at Shoe City and Second City with Norman's and Tesco (16 per cent to 26 per cent), as well as with B & Q (24 per cent and 23 per cent). There are, however, no equivalent links with the retail

warehouses to the immediate west. This probably reflects the obstacle of the circuitous roads between Second City and Shoe City, and these stores (Fig. 4).

Additional insight into the pattern of shopping linkages in the retail park is provided by analyzing the linkages between the 'interview sites' and the 'stores'. This can be used to identify those stores which attract the largest proportions of visits from shoppers approached at the other interview sites. Table IV pre- sents information for the fifteen stores for which the proportion of respondents visiting the store from the other interview sites exceeded 2 per cent. Evidence from this table, combined with that from the main analysis (Table III) shows that some stores are of key importance in generating shopping linkages within the retail park. Specifically, a significant 'spin-off' dimension emerges. Tesco and B & Q demonstrate this effect most clearly, attracting visits from 21 per cent and 18 per cent respectively of shoppers approached at other interview sites (Table IV). In fact, both stores record linkages in excess of 15 per cent with all others (Table III: see appropriate rows). For Tesco these reach a high of 33 per cent with MFI. Similar figures are recorded for B & Q, except for those greater than 30 per cent which are inflated by the comparison shopping relationship with the furni- ture stores, noted previously. Two furniture stores, MFI and Queensway-Carpetland also attract notable

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 15

proportions of shoppers from the other interview sites (12 per cent and 9 per cent respectively). In part, these linkages reflect the comparison shopping with the other furniture and furnishings stores already mentioned, but MFI demonstrates a wider functional pattern of associations which includes Tesco (16 per cent), Shoe City (14 per cent) and Halfords (10 per cent). This suggests a significant 'spin-off' shopping dimension for this store and it probably reflects a combination of the broad product range and moderate prices offered by MFI. MFI, apparently, has the potential to attract a wider range of customers than the other furniture and furnishings outlets. Three additional stores show a similar, but less well marked tendency to generate a broad range of shopping link- ages. Norman's, Second City (clothes) and Shoe City all attract 8-10 per cent of respondents interviewed at other sites (Table IV), and their linkages with other stores lie largely between 10 and 23 per cent (Table III).

Thus, it can be suggested that superstores (particu- larly the higher status chains like Tesco), DIY outlets, clothing and footwear stores, in roughly rank order, are key units for generating 'spin-off' shopping linkages. There is also some evidence that furniture and furnishings stores function in this manner, but the generation of linkages from these stores more strongly reflects comparison shopping for the more specialized items.

The fitted kitchen and bedroom showrooms and the quasi-retail' units demonstrate an additional feature. In each case, much smaller percentages of shoppers are attracted from the other stores. Only nine of the possible 72 linkages exceeded 5 per cent (Table III). The proximity of the Halfords and Bridgers stores to Sigma 3 Kitchens explains the highest linkages (9 per cent and 10 per cent respectively), while all but one of the others reflects a low level of comparison shopping with the furniture and furnishings stores. None of the stores in these two categories was used as an inter- view site so that interrelationships with the other stores are likely to be understated. However, the generally low levels of linkage recorded in the survey suggests that these kinds of outlets largely attract one-stop shoppers, interested specifically in their specialized products. This suggests their isolated functional status, which is not strongly dependent upon their location in the retail park. Their functional linkages are more likely to be with similarly specialized outlets located throughout the wider urban area.

Two further shopping linkage effects can be hypothesized from the data set. For as many as five of

the stores at which interviews were undertaken, only very small numbers of additional shoppers were attracted from the other interview sites (less than 4 per cent, Table IV). This appears to reflect a number of influences. Allied Carpets and Texstyle World stock only a narrow range of items within the broader category of furniture and furnishings, while Halfords and Bridgers offer specialized items not represented elsewhere in the retail park. Consequently, in both situations their attraction for shoppers visiting the area primarily for other purposes is not likely to be great: the more specialized the function of the store, the more isolated its functional characteristics are likely to be.

The Mammoth store, however, does not conform to this general pattern since it sells a wide range of furniture items. Its low level of links from the other interview sites almost certainly reflects its peripheral location, approximately a quarter of a mile from the centre of the retail park and at the opposite side of the barrier of the A48 road. It appears that the constrain- ing influence of the 'friction of distance' and the 'barrier effect' of a crossroads noted by Johnston and Kissling (1971) for pedestrians at the micro-scale of analysis also has some significance for patterns of shopping behaviour demonstrated by motorists. The availability of a car for short distance journeys within an area like the Enterprise Zone retail park does not appear to overcome the inconvenience of using it, even for relatively short journeys involving traffic barriers to a peripheral location. By contrast, the analysis of the linkages of respondents starting their shopping visit at an eccentric site, such as the Mammoth store, shows that the same constraints appear to present no real difficulties for their subse- quent activities. For example, of those interviewed at the Mammoth Store, a substantial 40 per cent also visit B & Q, while 33 per cent and 30 per cent respectively visit MFI and Queensway-Carpetland. The attraction presented by the relative concentration of other com- parable stores apparently supercedes the restrictive influences of short distances or traffic barriers. In fact, the linkages of those interviewed at the Mammoth store with the other stores in the retail park are amongst the highest in the survey. This suggests the adverse commercial implications of a peripheral location, even in the context of a loosely structured shopping area such as an unplanned retail park.

Transport linkages between stores For the 75 per cent of respondents who visited more than one store, their mode of travel between the stores

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

16 ROSEMARY D. F. BROMLEY and COLIN]. THOMAS

was examined. This provided additional insight into the structural and functional coherence of the retail park, as well as suggesting traffic implications. Only 20 per cent of respondents walked between the stores, but almost all of these were visiting adjacently located stores. A further 12 per cent walked between adjacent stores visited, but drove between the others. The large majority (68 per cent), however, drove between stores reflecting a combination of the distance involved, the landscaping barriers and the lack of easy pedestrian linkages free of traffic hazards. The absence of shared parking facilities, apart from those at survey sites 4 and 5, even by some adjacent stores accentuates this tendency (Fig. 1). The between store shopping journeys have resulted in considerable internal circulation traffic within the retail park which frequently causes delays at peak shopping times.

Traffic congestion is particularly marked between the subsidiary road and the A4217 near the Second City Store (Fig. 1). A traffic count on a Wednesday in May 1985 showed that 1300-1450 vehicles per hour passed through the junction.' Counts on the feeder roads in May 1986 suggest heavier traffic on Thursdays and Fridays when the combination of through traffic and shopping traffic is greatest.2 Traffic lights will be installed if congestion is con- sidered to reach a 'critical' level. In the meantime the traffic on a road network designed to serve an industrial rather than a retail area may form an obstacle, physically and perceptually, to the develop- ment of shopping linkages between the stores.

Respondents were not asked directly whether they considered that journeys between stores presented any difficulties. However, amongst the reasons that respondents were invited to indicate as important to their decision to shop in the Enterprise Park was 'convenient grouping of shops to each other'. This was ranked sixth of the thirteen reasons listed and as many as 80 per cent of shoppers gave this reason as important (44 per cent) or very important (36 per cent) to their decision to visit the retail park. This suggests that internal shopping linkages do not present severe problems for multi-purpose shopping trips for the car-borne users of the retail park. In fact, the opposite appears to be the case. Nevertheless, it is interesting to note that the favourable response to this reason falls to 65 per cent for the peripherally located Mammoth store respondents. The question, however, is insufficiently refined to gauge whether spatial frag- mentation suppresses more inter-store linkages. This issue requires a more direct form of analysis than was undertaken in this study. Suffice it to say that the

oblique evidence available does not suggest consider- able dissatisfaction with this characteristic of the Enterprise Zone retail park at current traffic levels.

CONCLUSION

Retail developments in the Swansea Enterprise Zone have created a concentration of superstores and retail warehouses which form an unplanned retail park. In 1985 the park offers a comparatively restricted range of goods and services, although it achieves secondary status in the retail system of Greater Swansea. All the stores predominantly serve car-owning households drawn from a wide trade area. They are attracted by the convenience of the shopping environment offered by the car parking facilities and extended shopping hours, and by the perceived competitive- ness and quality of goods available.

The retail park does not appear to function as a strongly integrated shopping centre. Instead, a superstore-retail warehouse dichotomy is identified. The superstores attract shoppers from a compara- tively restricted trade area. Their customers are loyal to one of the superstores for the regular and frequent purchase of most of their groceries. The retail ware- houses attract more occasional shoppers, who at the same time might well use the superstores. The retail warehouse shoppers travel from a wider trade area.

The evidence derived from the shopping linkages between the stores appears to confirm the functional dichotomy of stores and shoppers. In addition, the relatively weak functional and spatial patterns of association between the units suggest that the retail park constitutes a loosely structured collection of stores rather than a functionally coherent shopping centre. However, a number of interesting functional linkages are identified. The use of the superstores for one-stop convenience shopping by a substantial pro- portion of shoppers limits their integration with the other stores. This functional isolation is more marked for the most specialized of the furnishings outlets (Allied Carpets and Texstyle World) and the single specialist stores (Halfords and Bridgers). The same effect dominates the minimal shopping linkages demonstrated by the specialist fitted kitchen and bedroom outlets, along with the 'quasi-retail' units.

By contrast, there is evidence of moderate func- tional integration reflecting comparison shopping between the furniture and furnishings stores. Spatial linkages are also identified, particularly between adjacent stores which are functionally similar or functionally complementary, while similar linkages

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

Retail parks: the Swansea Enterprise Zone 17

are evident for stores occupying a central location. The disadvantageous commercial implications of a site peripheral to the main shopping concentration is suggested by the Mammoth store. In addition, the potential for enhanced shopping linkages is indicated by the functional variety of 'spin-off' shopping trips generated by a number of key stores, in particular Tesco and B & Q. The problem of traffic congestion resulting from internal vehicular circulation con- tingent upon the loose spatial structuring of the stores is also suggested.

Together, these findings suggest that had a strongly integrated spatial structure been advocated for the Enterprise Zone retail park at the outset of its development, its commercial status would have been even further enhanced by the encouragement of easier inter-store shopping linkages, while at the same time some of the problems associated with the internal circulation traffic would have been avoided.

ACKNOWLEDGEMENTS

The authors wish to acknowledge the assistance of Swansea City Council (in particular Dr Joan Rees) with the questionnaire surveys, and to thank Guy Lewis and Paul Taylor for drawing the maps.

NOTES

1. West Glamorgan County Council, County Transpor- tation Unit Manual Traffic Census, Wednesday, 29th May, 1985

2. West Glamorgan County Council, County Transpor- tation Unit, Automatic Traffic Count, Week beginning 20th May, 1985

REFERENCES

BENNISON, D. J. and DAVIES, R. L. (1980) 'The impact of town centre shopping schemes in Britain: their impact on traditional retail environments', Prog. Plann. 14: 1-104

BERNARD THORPE and PARTNERS (1985) Retail ware- house parks: an approach to planned development (Bernard Thorpe and Partners, London)

BROMLEY, R. D. F. and MORGAN, R. H. (1985) 'The effects of enterprise zone policy: evidence from Swansea', Reg. Stud. 19: 403-13

CAMERON HALL DEVELOPMENTS (1985) The Metro- centre, Gateshead (Cameron Hall Developments, Gateshead)

DAVIES, R. L. and KIRBY, D. A. (1980) 'Retail organization', in DAWSON, J. A. (ed.) Retail Geography (Croom Helm, London) pp. 156-92

DAWSON, J. A. (1983) Shopping centre development (Longman, London)

DAWSON, J. A. and SPARKS, L. (1982) 'Retailing develop- ments and enterprise zones', Retail and Distribution Mgmt. 10: 43-6

DUDLEY METROPOLITAN BOROUGH (1985) 'Dudley Enterprise Zone retailing provision: proposals for modification of planning scheme' (Dudley Metropolitan Borough, Dudley)

DUDLEY METROPOLITAN BOROUGH (1986) 'Retail at Merry Hill. History' (Dudley Metropolitan Borough, Dudley)

GIBBS, A. (1981) 'An analysis of retail warehouse planning inquiries', URPI report U22, Reading

GIBBS, A. (1985) 'Planners and retail innovation', The Planner 71 No. 5: 9-10

GIBSON, P. and HURDLE, D. (1985a) 'Superstores and regional centres', in GREATER LONDON COUNCIL, The future of planning: planning for retailing (Greater London Council, London) pp. 23-32

GIBSON, P. and HURDLE, D. (1985b) 'Planning and retail innovation-a rejoinder', The Planner 71 No. 10: 30

HALLSWORTH, A. G. (1983) 'Trading patterns of a retail furnishings superstore: Brown Bear, Fareham; Dept. of Geography, Portsmouth Poly.

JOHNSTON, R. J. and KISSLING, C. C. (1971) 'Establish- ment use patterns within central places', Aust. Geogr. Stud. 9: 116-32

JONES, P. (1984) 'Retail warehouse developments in Britain', Area 16: 41-7

LEE DONALDSON ASSOCIATES (1986) 'Superstore Appeals: review 1986' (Lee Donaldson Assoc., London)

REES, J. C. M. (1986) 'Retail growth in the Swansea Enter- prise Zone: a study of the impact of an out-of-town shopping centre', unpubl. dissertation, Dept. of Town Planning, Bristol Poly.

SPARKS, L. (1987) 'Retailing in Enterprise Zones: the example of Swansea', Reg. Stud. 21:3 7-42

SHEPHERD, I. D. H. and THOMAS, C. J. (1980) 'Urban consumer behaviour', in DAWSON, J. A. (ed.) Retail Geography (Croom Helm, London) pp. 18-94.

THOMAS, C. J. and BROMLEY, R. D. F. (1987) 'The growth and functioning of an unplanned retail park: the Swansea Enterprise Zone', Reg. Stud. 21: 287-300

URPI (UNIT FOR RETAIL PLANNING INFORMATION) (1980) 'Hypermarkets and superstores bibliography', URPI Bibliography 2, Reading

URPI (1981a) 'Shopping in Petersfield', URPI Information Brief 81/2, Reading

URPI (1981b) 'Retail warehouses: the present position', URPI Information Brief 81/5, Reading

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions

18 ROSEMARY D. F. BROMLEY and COLINI. THOMAS

URPI (1982) 'Shopping at Central Milton Keynes: 1979 and 1981', URPI Information Brief, 82/5, Reading

URPI (1985) 'Hypermarkets and superstores-general', URPI Information Source Sheet I, First Supplement, Reading

URPI (1986) 'Retail Warehouses Supplement 1', URPI Information Source Sheet 20, Reading

WADE, B. (1985) 'New directions in retailing', in GREATER LONDON COUNCIL, The future of planning: planning for retailing (Greater London Council, London) pp. 11-15

WEST GLAMORGAN COUNTY COUNCIL (1978) 'Shops and offices floorspace survey' (West Glamorgan County Council, Swansea)

This content downloaded from 14.139.62.113 on Mon, 2 Dec 2013 06:04:03 AMAll use subject to JSTOR Terms and Conditions