Embed Size (px)

Citation preview

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 1/35

CMBS Market Trends andOutlook

Presentation to

CREW CT -- REX

Thomas A. FinkSenior Vice President

March 23, 2011

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 2/35

2

CMBS Background

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 3/35

3

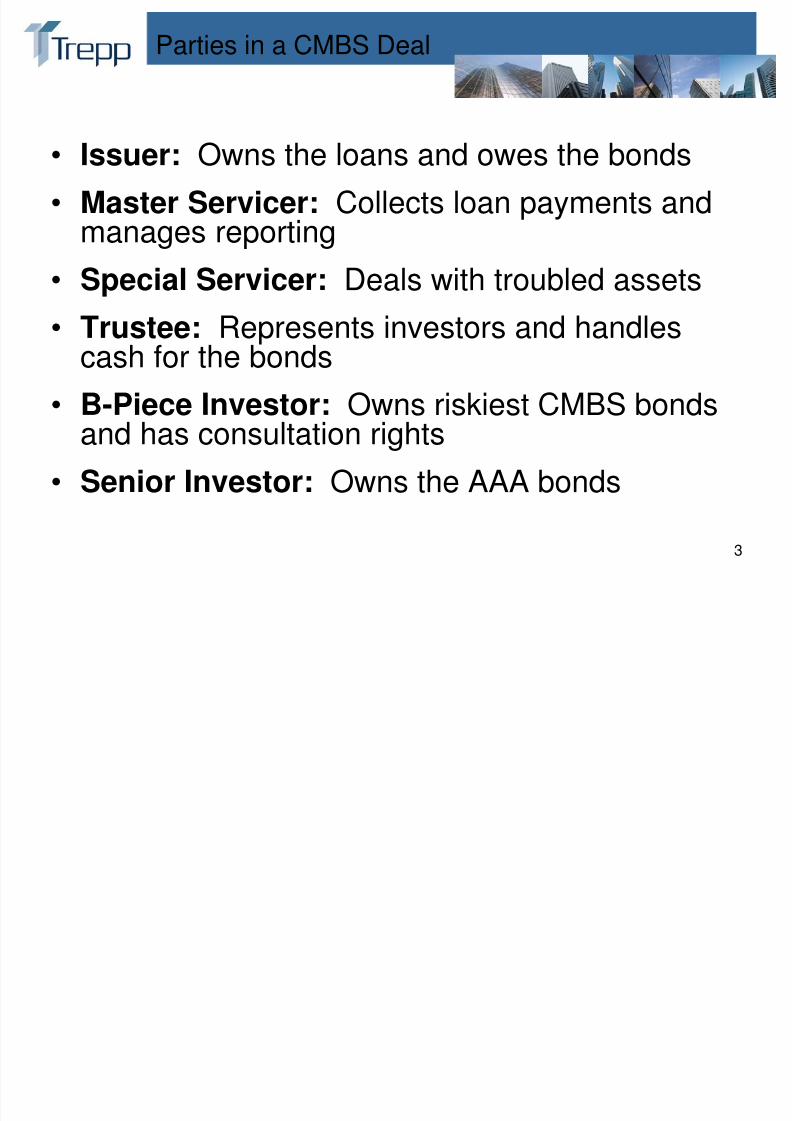

Parties in a CMBS Deal

• Issuer: Owns the loans and owes the bonds

• Master Servicer: Collects loan payments andmanages reporting

• Special Servicer: Deals with troubled assets

• Trustee: Represents investors and handlescash for the bonds

• B-Piece Investor: Owns riskiest CMBS bondsand has consultation rights

• Senior Investor: Owns the AAA bonds

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 4/35

4

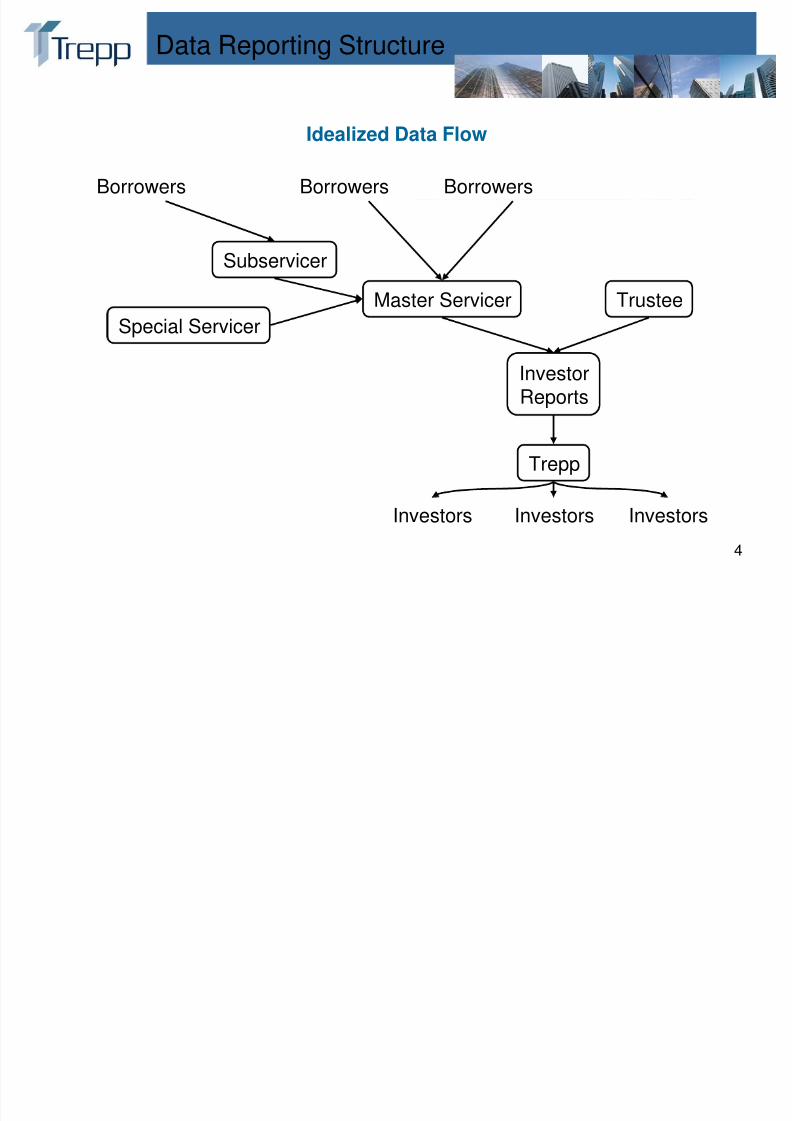

Data Reporting Structure

Idealized Data Flow

Borrowers Borrowers Borrowers

Subservicer

Master ServicerSpecial Servicer Trustee

InvestorReports

Trepp

InvestorsInvestors Investors

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 5/35

5

CMBS Market Trends

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 6/35

6

CMBS Market Trends

• CMBS Secondary Market Spreads

• Balance Sheet Lender Spreads• CMBS Primary Market

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 7/35

7

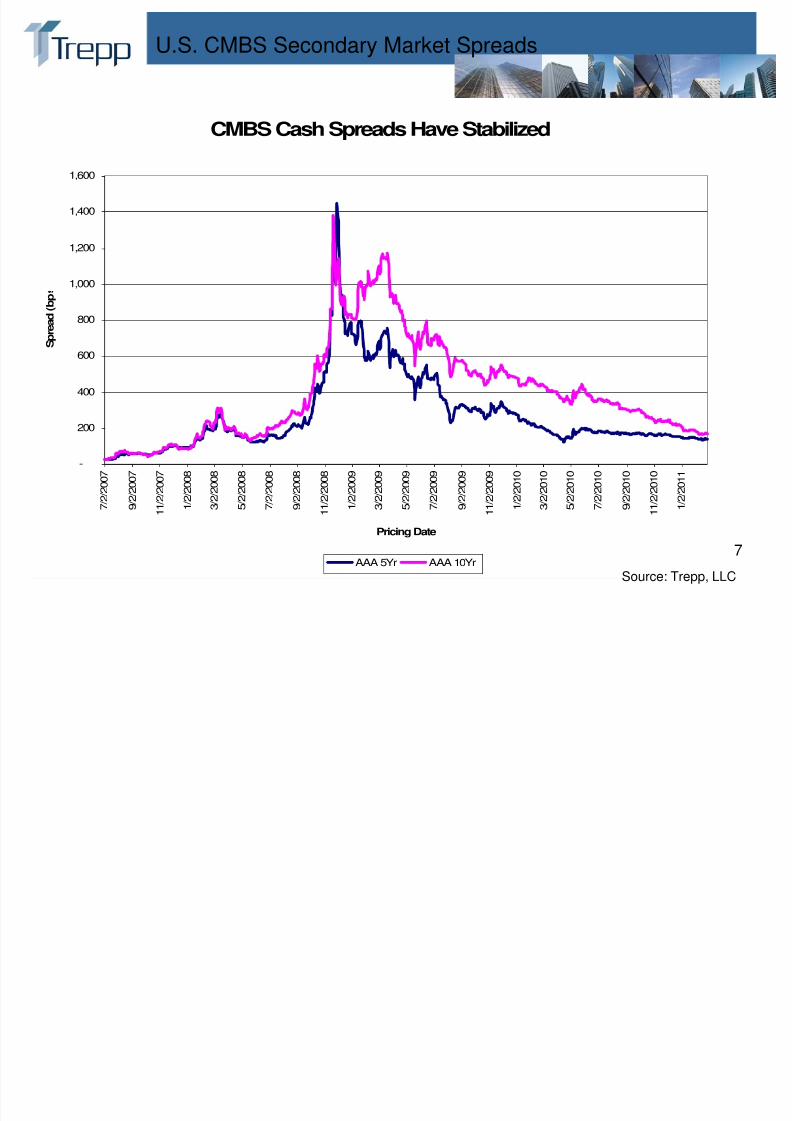

U.S. CMBS Secondary Market Spreads

CMBS Cash Spreads Have Stabilized

-

200

400

600

800

1,000

1,200

1,400

1,600

7 / 2 / 2 0 0 7

9 / 2 / 2 0 0 7

1 1 / 2 / 2 0 0 7

1 / 2 / 2 0 0 8

3 / 2 / 2 0 0 8

5 / 2 / 2 0 0 8

7 / 2 / 2 0 0 8

9 / 2 / 2 0 0 8

1 1 / 2 / 2 0 0 8

1 / 2 / 2 0 0 9

3 / 2 / 2 0 0 9

5 / 2 / 2 0 0 9

7 / 2 / 2 0 0 9

9 / 2 / 2 0 0 9

1 1 / 2 / 2 0 0 9

1 / 2 / 2 0 1 0

3 / 2 / 2 0 1 0

5 / 2 / 2 0 1 0

7 / 2 / 2 0 1 0

9 / 2 / 2 0 1 0

1 1 / 2 / 2 0 1 0

1 / 2 / 2 0 1 1

Pricing Date

S p r e a d ( b p

AAA 5Yr AAA 10Yr

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 8/35

8

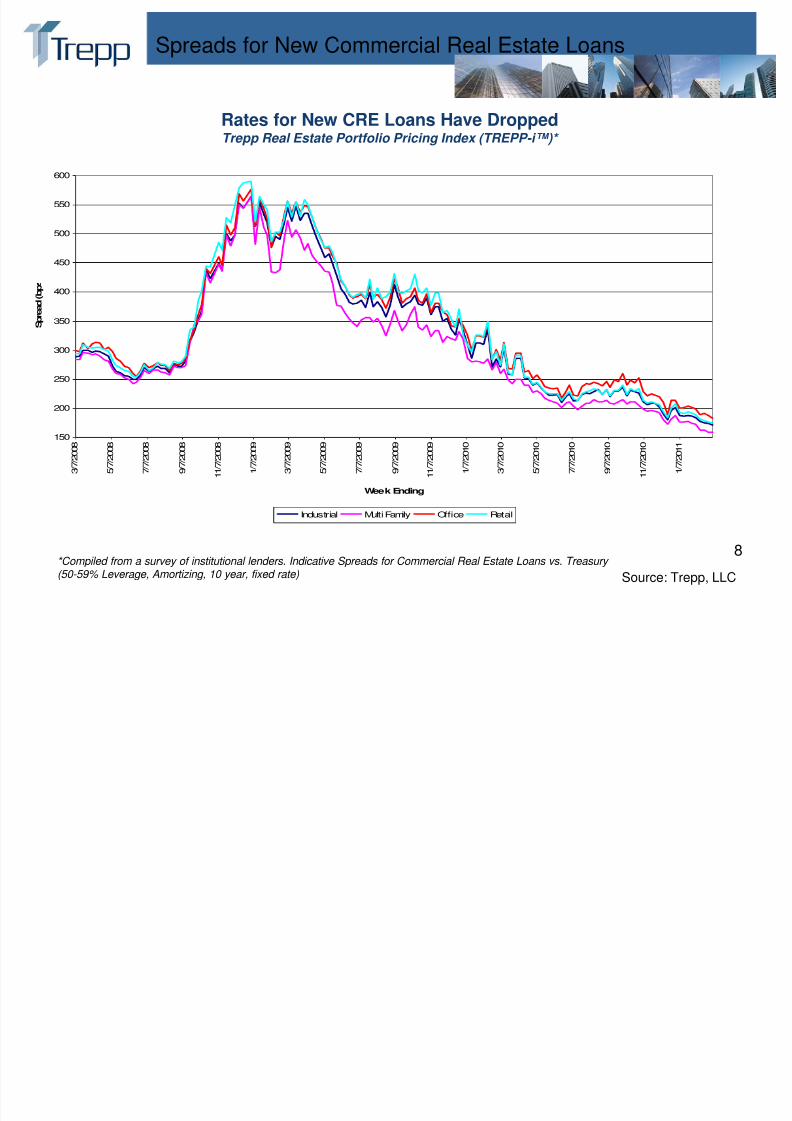

Spreads for New Commercial Real Estate Loans

*Compiled from a survey of institutional lenders. Indicative Spreads for Commercial Real Estate Loans vs. Treasury (50-59% Leverage, Amortizing, 10 year, fixed rate)

Rates for New CRE Loans Have DroppedTrepp Real Estate Portfolio Pricing Index (TREPP-i™)*

Source: Trepp, LLC

150

200

250

300

350

400

450

500

550

600

3 / 7 / 2 0 0 8

5 / 7 / 2 0 0 8

7 / 7 / 2 0 0 8

9 / 7 / 2 0 0 8

1 1 / 7 / 2 0 0 8

1 / 7 / 2 0 0 9

3 / 7 / 2 0 0 9

5 / 7 / 2 0 0 9

7 / 7 / 2 0 0 9

9 / 7 / 2 0 0 9

1 1 / 7 / 2 0 0 9

1 / 7 / 2 0 1 0

3 / 7 / 2 0 1 0

5 / 7 / 2 0 1 0

7 / 7 / 2 0 1 0

9 / 7 / 2 0 1 0

1 1 / 7 / 2 0 1 0

1 / 7 / 2 0 1 1

Week Ending

S p r e a d ( b p

Industrial Multi Family Office Retail

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 9/35

9

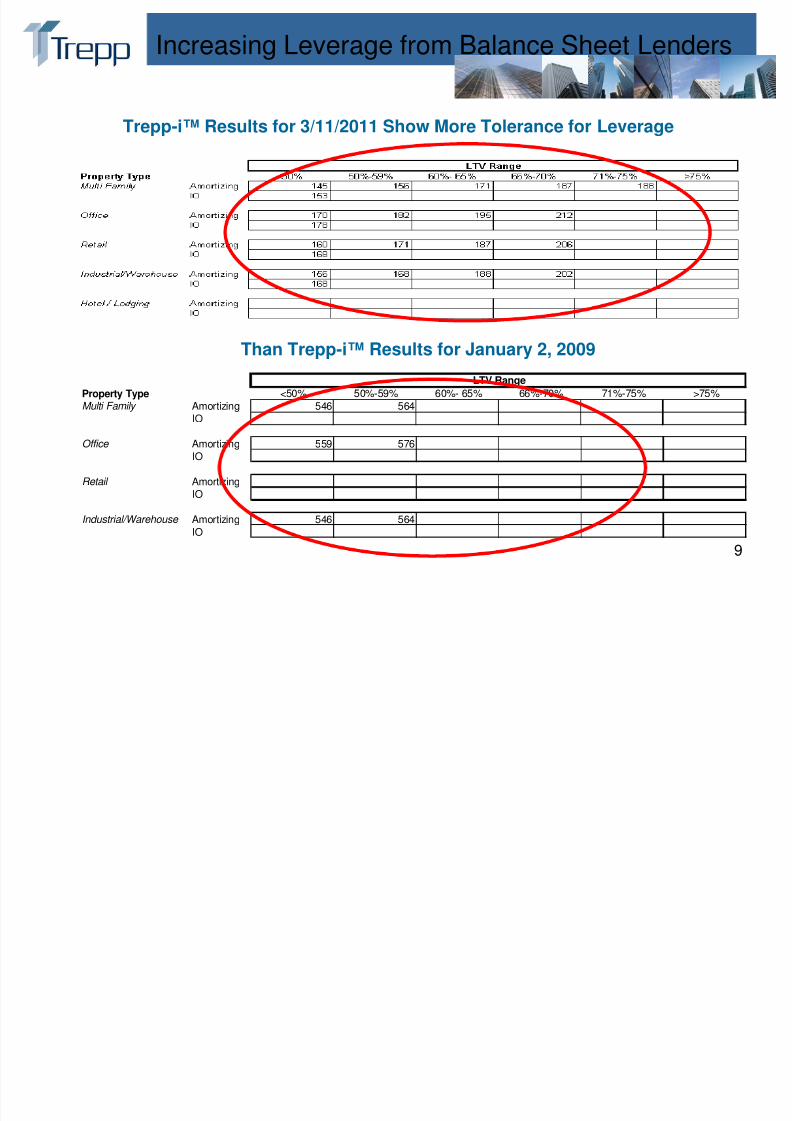

Increasing Leverage from Balance Sheet Lenders

Trepp-i™ Results for 3/11/2011 Show More Tolerance for Leverage

Than Trepp-i™ Results for January 2, 2009

Property Type <50% 50%-59% 60%- 65% 66%-70% 71%-75% >75%Multi Family Amortizing 546 564

IO

Office Amortizing 559 576IO

Retail AmortizingIO

Industrial/Warehouse Amortizing 546 564IO

LTV Range

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 10/35

10

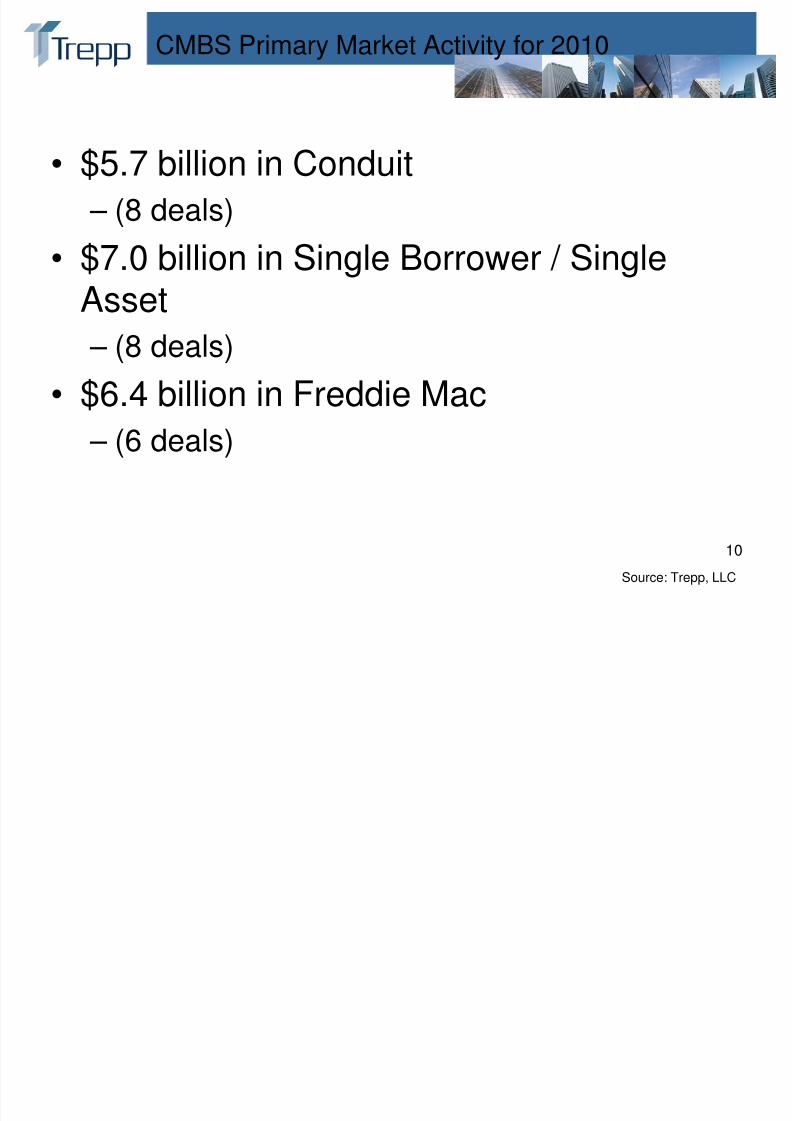

CMBS Primary Market Activity for 2010

• $5.7 billion in Conduit

– (8 deals)

• $7.0 billion in Single Borrower / Single

Asset – (8 deals)

• $6.4 billion in Freddie Mac

– (6 deals)

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 11/35

11

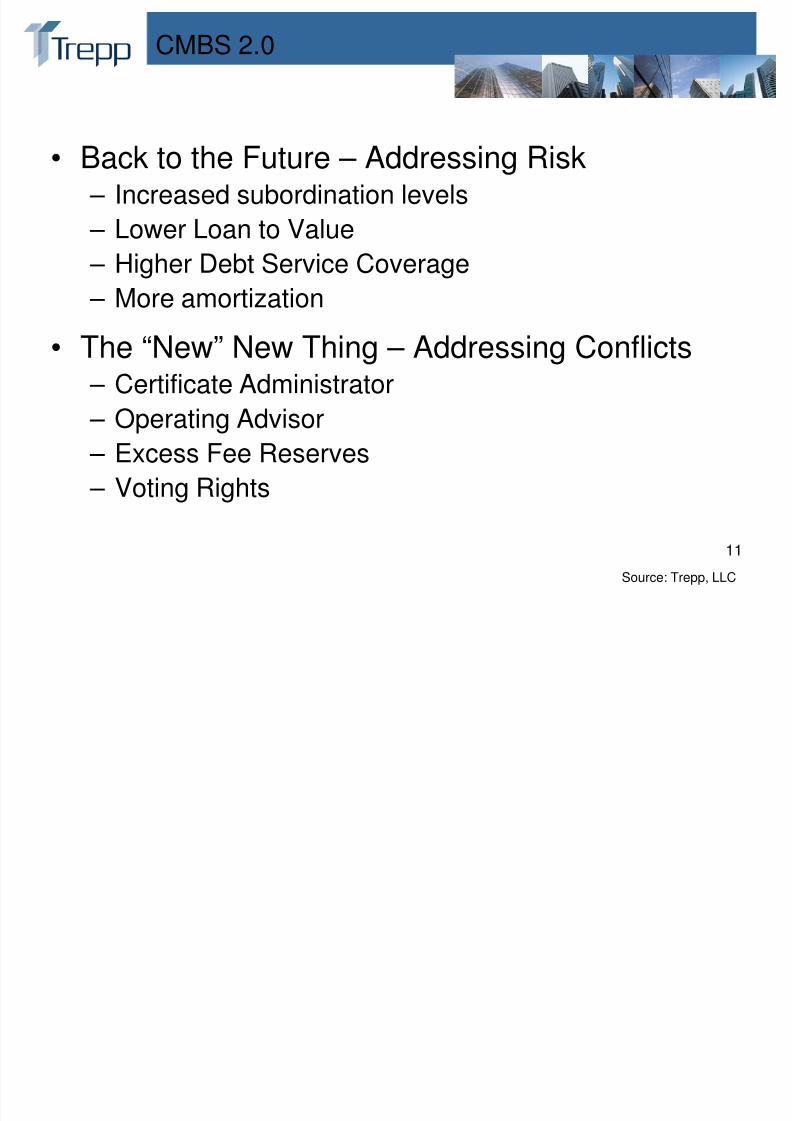

CMBS 2.0

• Back to the Future – Addressing Risk

– Increased subordination levels – Lower Loan to Value

– Higher Debt Service Coverage

– More amortization• The “New” New Thing – Addressing Conflicts

– Certificate Administrator

– Operating Advisor – Excess Fee Reserves

– Voting Rights

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 12/35

12

Loan Performance in Outstanding CMBS

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 13/35

13

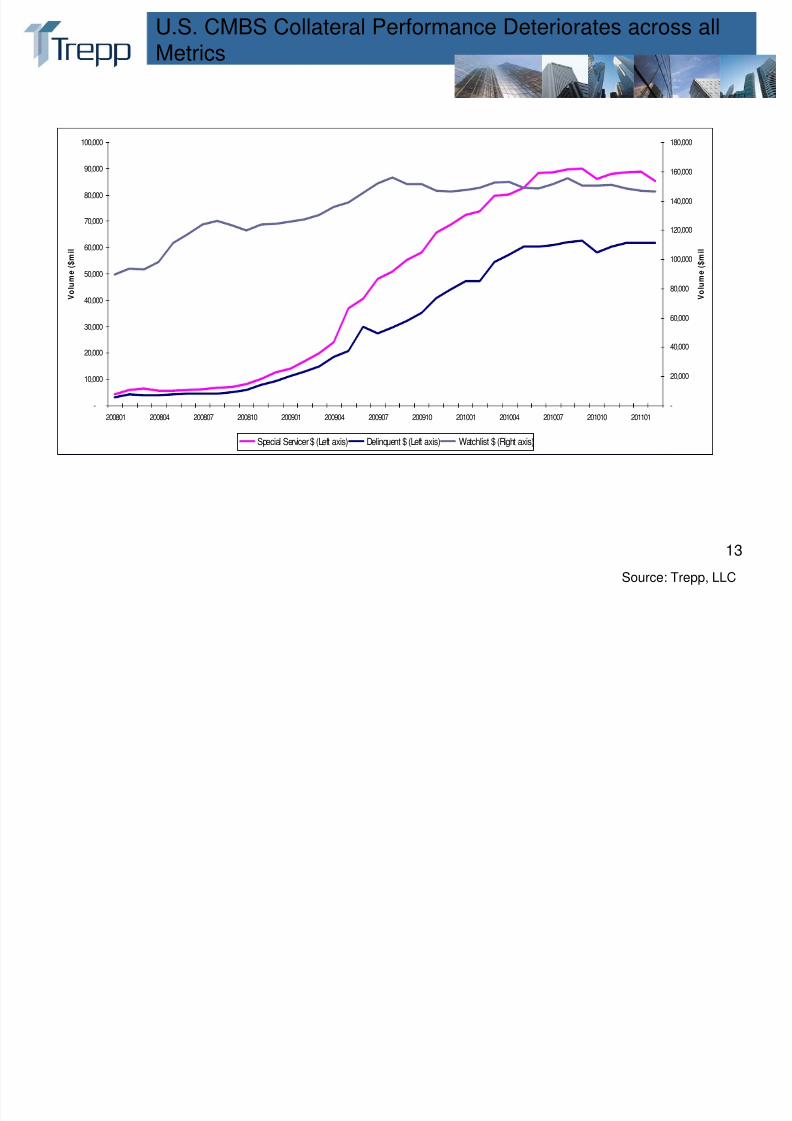

U.S. CMBS Collateral Performance Deteriorates across allMetrics

Source: Trepp, LLC

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

200801 200804 200807 200810 200901 200904 200907 200910 201001 201004 201007 201010 201101

V o l u m

e ( $ m

i l

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

V o l u m

e ( $ m

i l

Special Servicer $ (Left axis) Delinquent $ (Left axis) Watchlist $ (Right axis)

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 14/35

14

U.S. CMBS Delinquency Rates: Significance of RegionalVariation

10.46%

12.23

8.7317.39%

5.67%

7.32%

7.44%

9.64% 9.90%

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 15/35

15

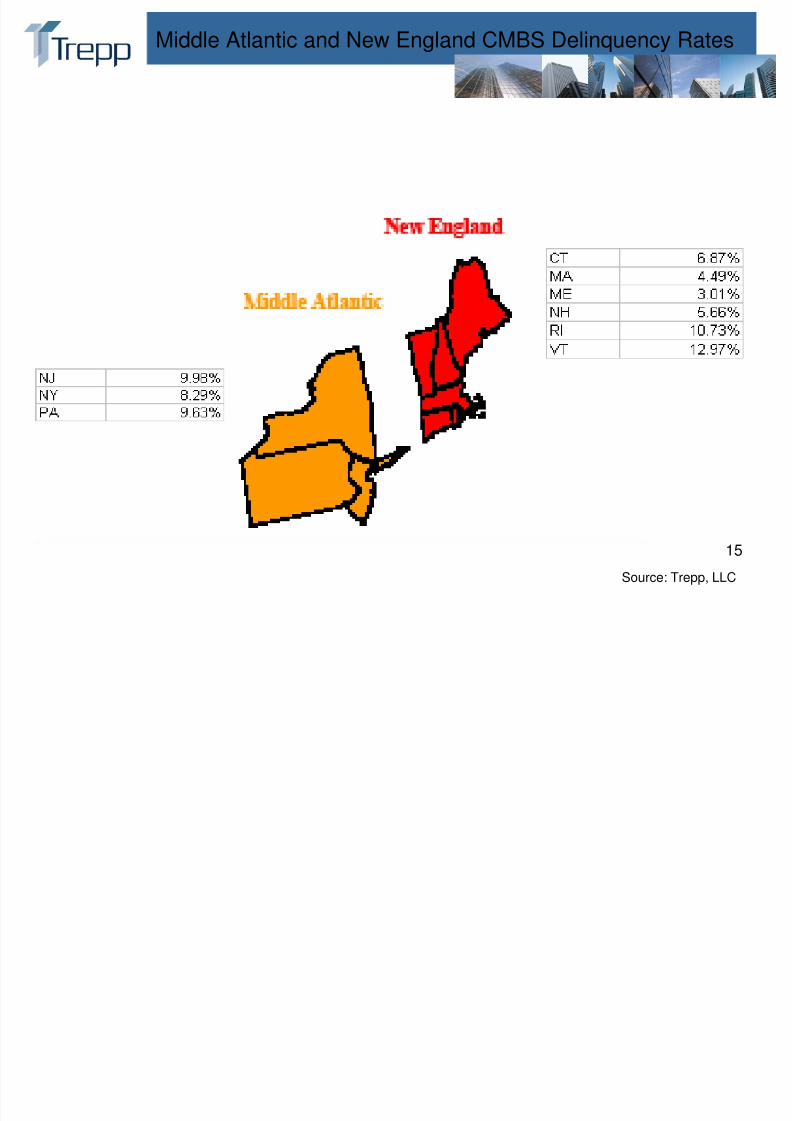

Middle Atlantic and New England CMBS Delinquency Rates

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 16/35

16

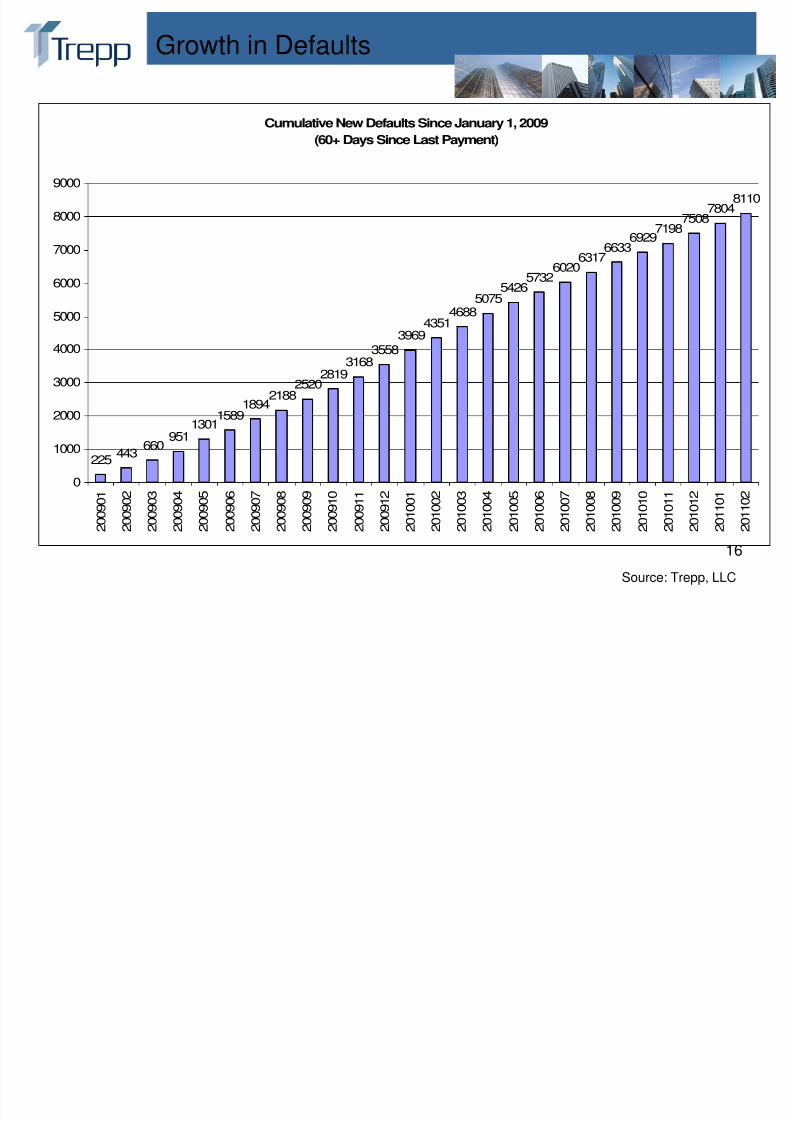

Growth in Defaults

Cumulative New Defaults Since January 1, 2009

(60+ Days Since Last Payment)

225443

660951

13011589

18942188

25202819

31683558

396943514688

50755426

57326020

63176633

69297198

75087804

8110

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2 0 0 9 0 1

2 0 0 9 0 2

2 0 0 9 0 3

2 0 0 9 0 4

2 0 0 9 0 5

2 0 0 9 0 6

2 0 0 9 0 7

2 0 0 9 0 8

2 0 0 9 0 9

2 0 0 9 1 0

2 0 0 9 1 1

2 0 0 9 1 2

2 0 1 0 0 1

2 0 1 0 0 2

2 0 1 0 0 3

2 0 1 0 0 4

2 0 1 0 0 5

2 0 1 0 0 6

2 0 1 0 0 7

2 0 1 0 0 8

2 0 1 0 0 9

2 0 1 0 1 0

2 0 1 0 1 1

2 0 1 0 1 2

2 0 1 1 0 1

2 0 1 1 0 2

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 17/35

17

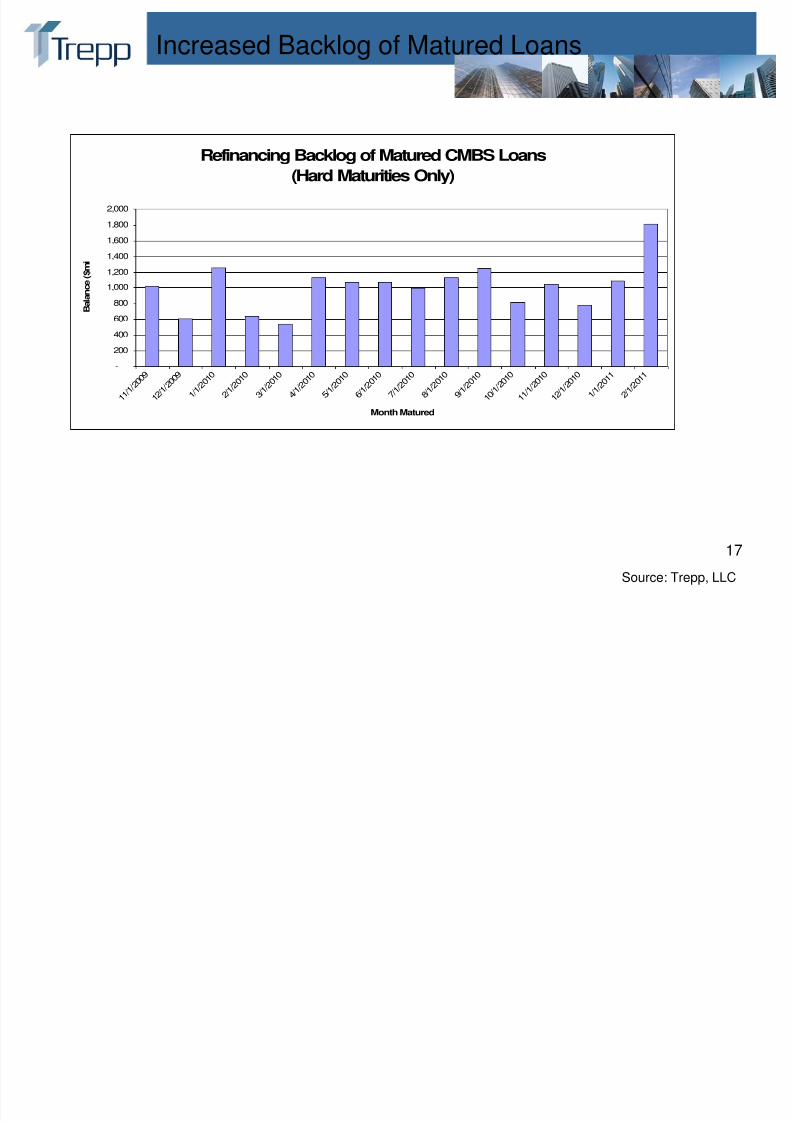

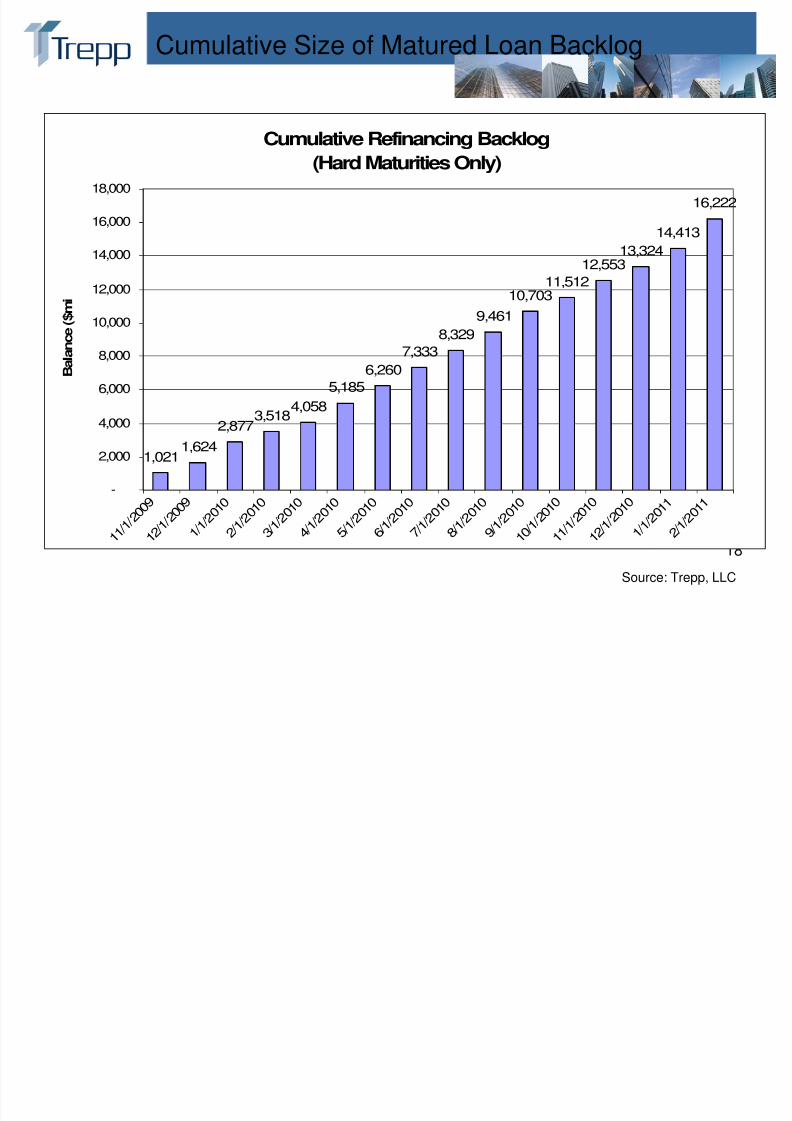

Increased Backlog of Matured Loans

Refinancing Backlog of Matured CMBS Loans

(Hard Maturities Only)

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1 1 / 1 / 2 0 0 9

1 2 / 1 / 2 0 0 9

1 / 1 / 2 0 1 0

2 / 1 / 2 0 1 0

3 / 1 / 2 0 1 0

4 / 1 / 2 0 1 0

5 / 1 / 2 0 1 0

6 / 1 / 2 0 1 0

7 / 1 / 2 0 1 0

8 / 1 / 2 0 1 0

9 / 1 / 2 0 1 0

1 0 / 1 / 2 0 1 0

1 1 / 1 / 2 0 1 0

1 2 / 1 / 2 0 1 0

1 / 1 / 2 0 1 1

2 / 1 / 2 0 1 1

Month Matured

B

a l a n c e ( $ m i

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 18/35

18

Cumulative Size of Matured Loan Backlog

Cumulative Refinancing Backlog

(Hard Maturities Only)

1,0211,624

2,8773,5184,058

5,185

6,260

7,333

8,3299,461

10,70311,512

12,55313,324

14,413

16,222

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1 1 / 1 / 2

0 0 9

1 2 / 1 / 2

0 0 9

1 / 1 / 2

0 1 0

2 / 1 / 2

0 1 0

3 / 1 / 2

0 1 0

4 / 1 / 2

0 1 0

5 / 1 / 2

0 1 0

6 / 1 / 2

0 1 0

7 / 1 / 2

0 1 0

8 / 1 / 2

0 1 0

9 / 1 / 2

0 1 0

1 0 / 1 / 2

0 1 0

1 1 / 1 / 2

0 1 0

1 2 / 1 / 2

0 1 0

1 / 1 / 2

0 1 1

2 / 1 / 2

0 1 1

B a l a n c e ( $ m

i

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 19/35

19

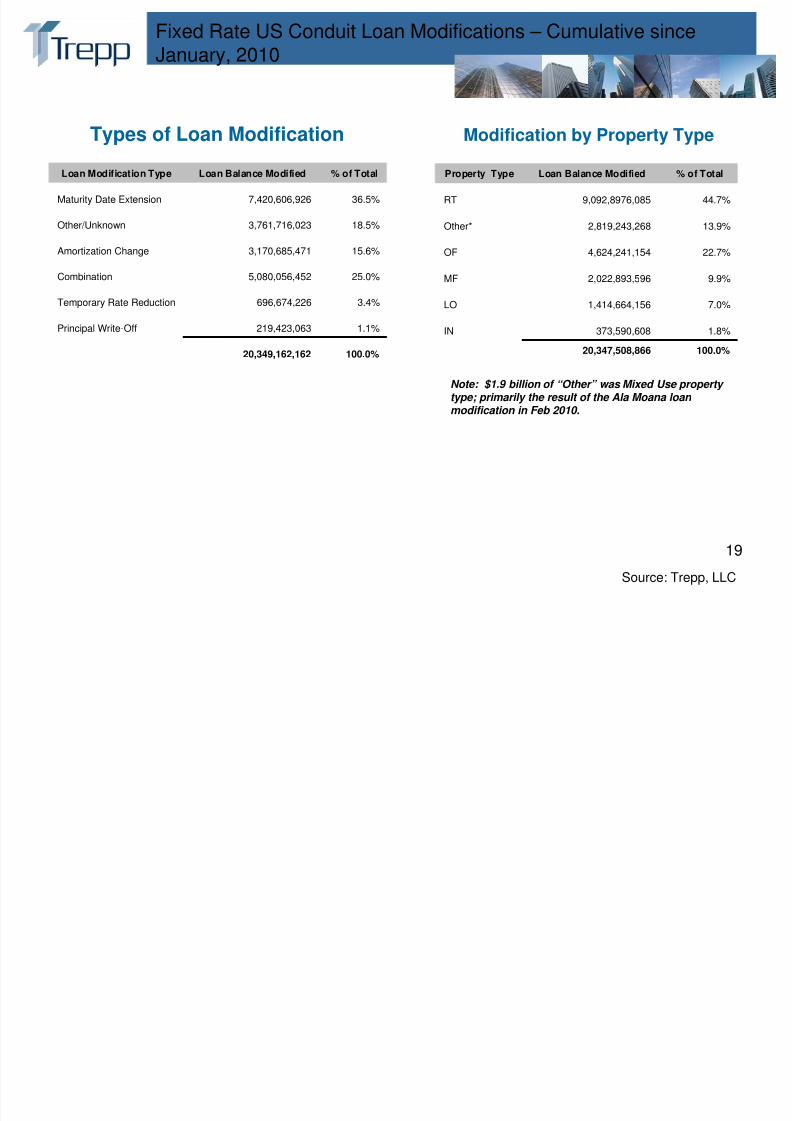

Fixed Rate US Conduit Loan Modifications – Cumulative sinceJanuary, 2010

Loan Modification Type Loan Balance Modified % of Total

Maturity Date Extension 7,420,606,926 36.5%

Other/Unknown 3,761,716,023 18.5%

Amortization Change 3,170,685,471 15.6%

Combination 5,080,056,452 25.0%

Temporary Rate Reduction 696,674,226 3.4%

Principal Write-Off 219,423,063 1.1%

20,349,162,162 100.0%

Property Type Loan Balance Modified % of Total

RT 9,092,8976,085 44.7%

Other* 2,819,243,268 13.9%

OF 4,624,241,154 22.7%

MF 2,022,893,596 9.9%

LO 1,414,664,156 7.0%

IN 373,590,608 1.8%

20,347,508,866 100.0%

Note: $1.9 billion of “Other” was Mixed Use property type; primarily the result of the Ala Moana loan

modification in Feb 2010.

Source: Trepp, LLC

Types of Loan Modification Modification by Property Type

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 20/35

20

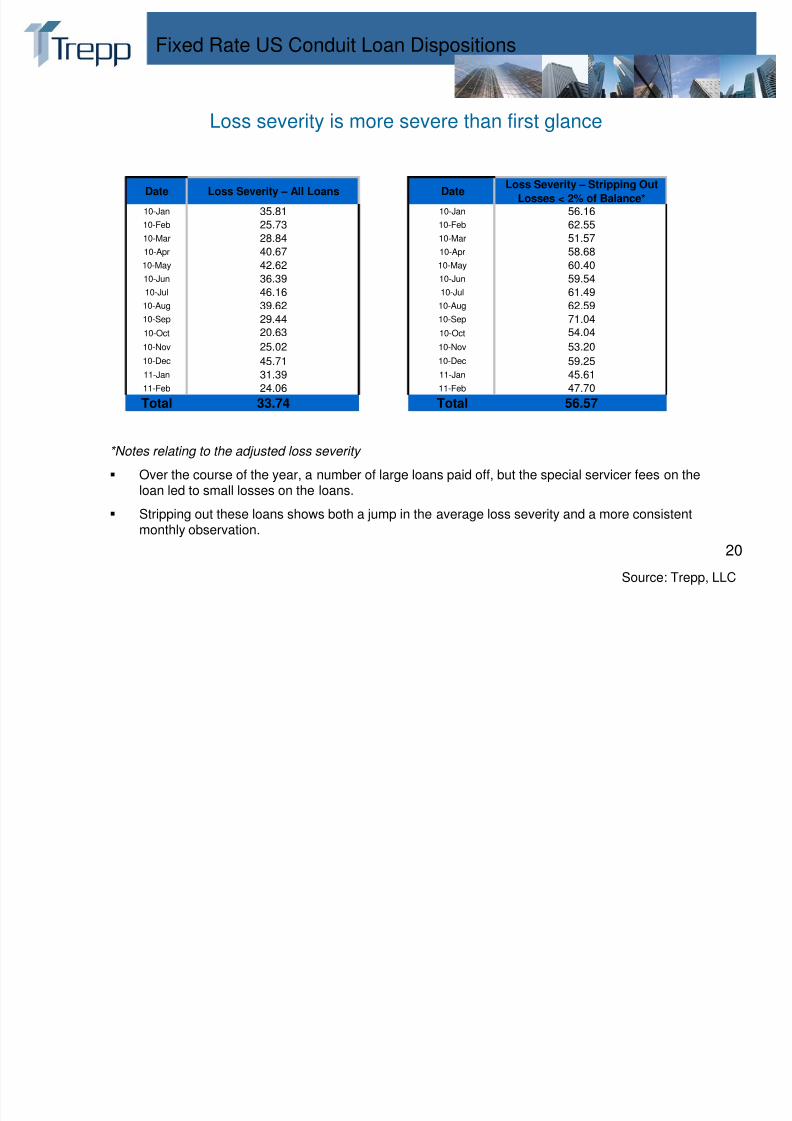

Fixed Rate US Conduit Loan Dispositions

*Notes relating to the adjusted loss severity

Over the course of the year, a number of large loans paid off, but the special servicer fees on theloan led to small losses on the loans.

Stripping out these loans shows both a jump in the average loss severity and a more consistentmonthly observation.

Source: Trepp, LLC

Loss severity is more severe than first glance

Date Loss Severity – All Loans DateLoss Severity – Stripping Out

Losses < 2% of Balance*

10-Jan 35.81 10-Jan 56.1610-Feb 25.73 10-Feb 62.5510-Mar 28.84 10-Mar 51.5710-Apr 40.67 10-Apr 58.6810-May 42.62 10-May 60.4010-Jun 36.39 10-Jun 59.5410-Jul 46.16 10-Jul 61.4910-Aug 39.62 10-Aug 62.5910-Sep 29.44 10-Sep 71.04

10-Oct 20.63 10-Oct 54.04

10-Nov 25.02 10-Nov 53.20

10-Dec 45.71 10-Dec 59.2511-Jan 31.39 11-Jan 45.6111-Feb 24.06 11-Feb 47.70

Total 33.74 Total 56.57

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 21/35

21

Property Performance in Outstanding CMBS

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 22/35

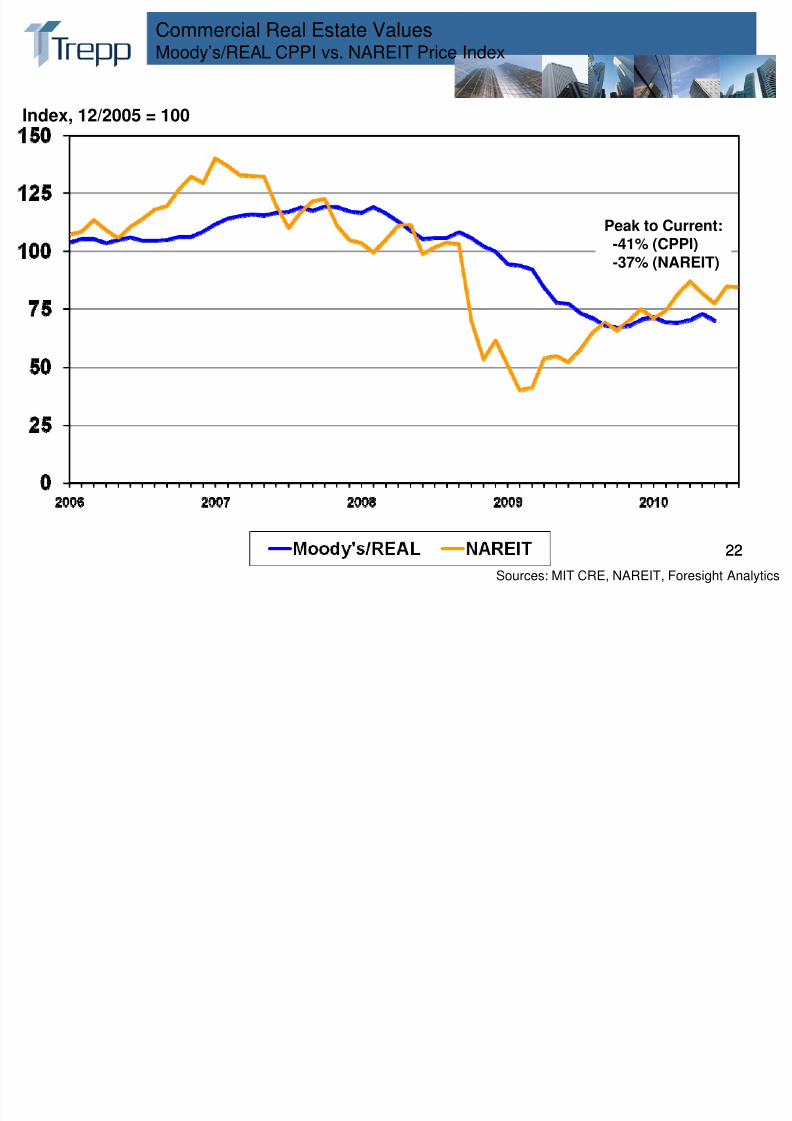

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 23/35

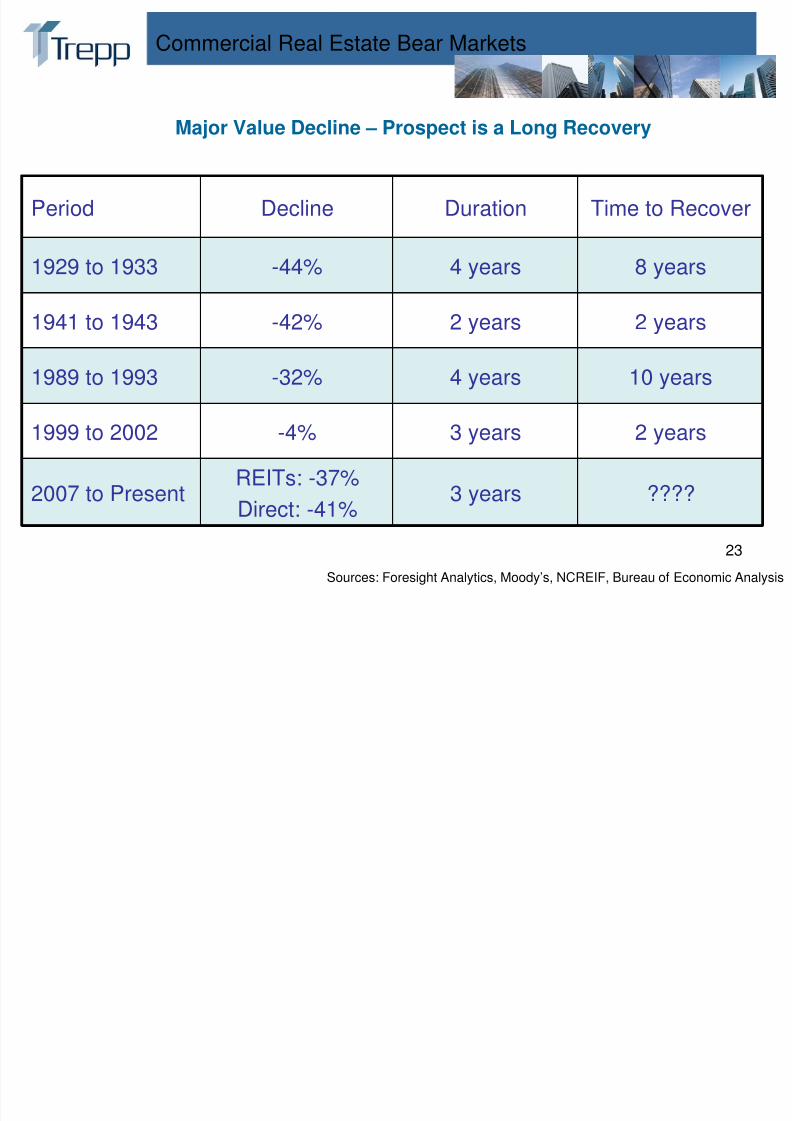

23

Commercial Real Estate Bear Markets

Sources: Foresight Analytics, Moody’s, NCREIF, Bureau of Economic Analysis

Period Decline Duration Time to Recover

1929 to 1933 -44% 4 years 8 years

1941 to 1943 -42% 2 years 2 years

1989 to 1993 -32% 4 years 10 years

1999 to 2002 -4% 3 years 2 years

2007 to PresentREITs: -37%

Direct: -41%

3 years ????

Major Value Decline – Prospect is a Long Recovery

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 24/35

24

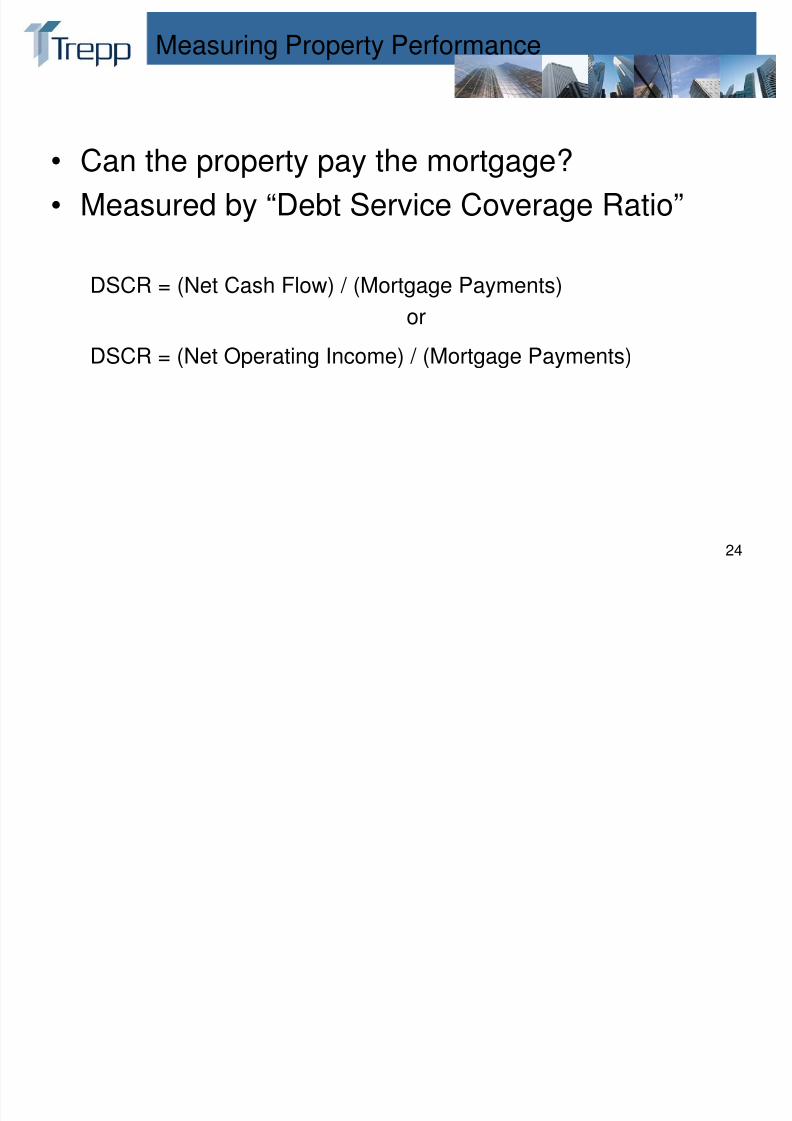

Measuring Property Performance

• Can the property pay the mortgage?

• Measured by “Debt Service Coverage Ratio”

DSCR = (Net Cash Flow) / (Mortgage Payments)

or

DSCR = (Net Operating Income) / (Mortgage Payments)

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 25/35

25

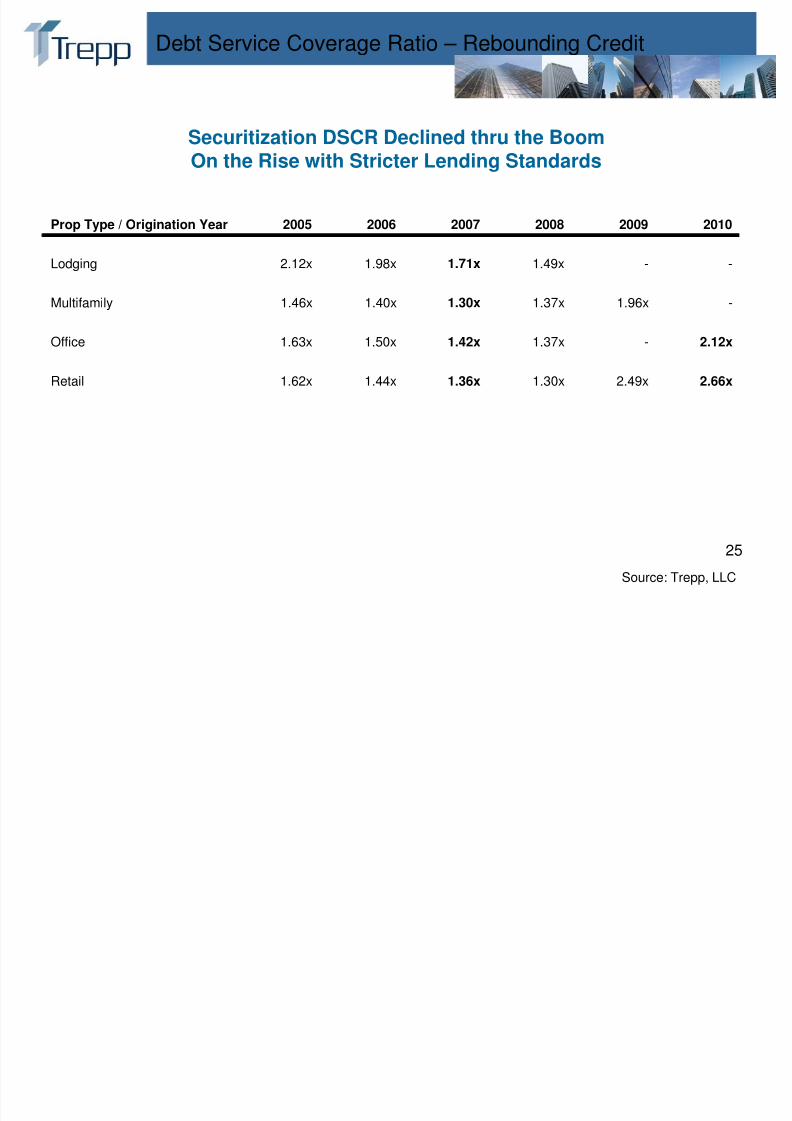

Debt Service Coverage Ratio – Rebounding Credit

Prop Type / Origination Year 2005 2006 2007 2008 2009 2010

Lodging 2.12x 1.98x 1.71x 1.49x - -

Multifamily 1.46x 1.40x 1.30x 1.37x 1.96x -

Office 1.63x 1.50x 1.42x 1.37x - 2.12x

Retail 1.62x 1.44x 1.36x 1.30x 2.49x 2.66x

Source: Trepp, LLC

Securitization DSCR Declined thru the BoomOn the Rise with Stricter Lending Standards

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 26/35

26

2011 and Into the Future

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 27/35

27

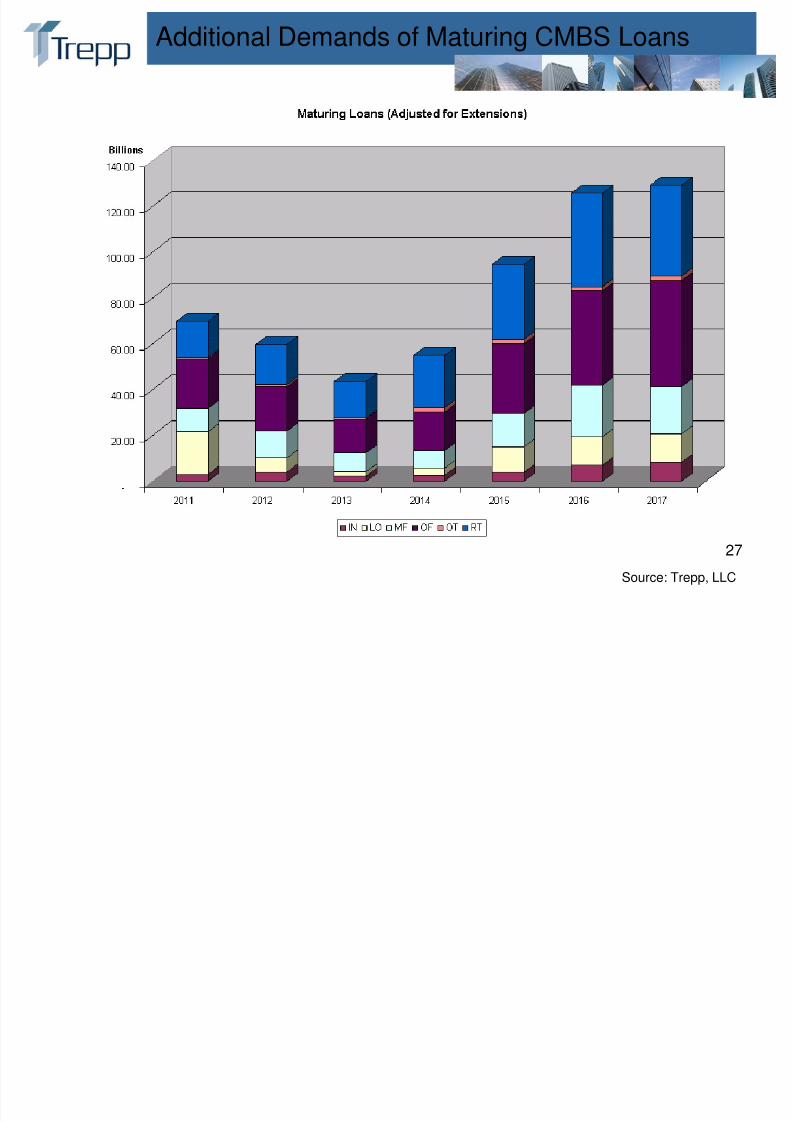

Additional Demands of Maturing CMBS Loans

Source: Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 28/35

28

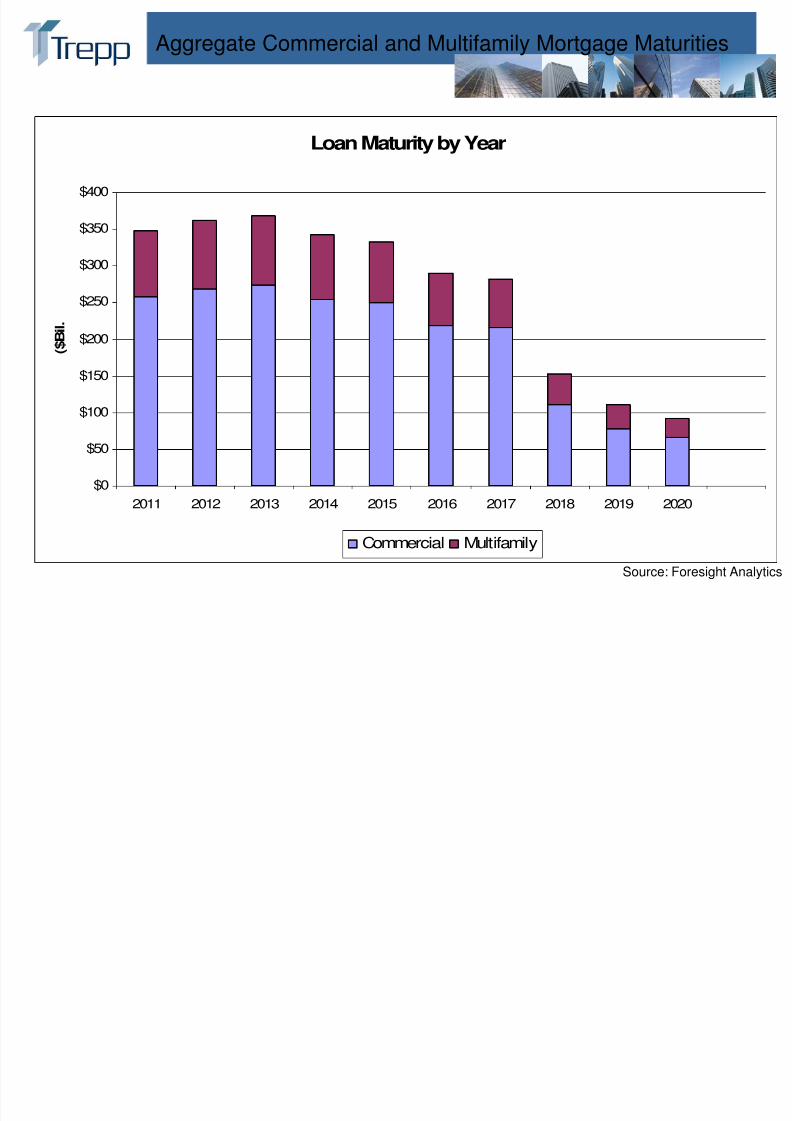

Aggregate Commercial and Multifamily Mortgage Maturities

Source: Foresight Analytics

Loan Maturity by Year

$0

$50

$100

$150

$200

$250

$300

$350

$400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

( $ B i l .

Commercial Multifamily

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 29/35

2929

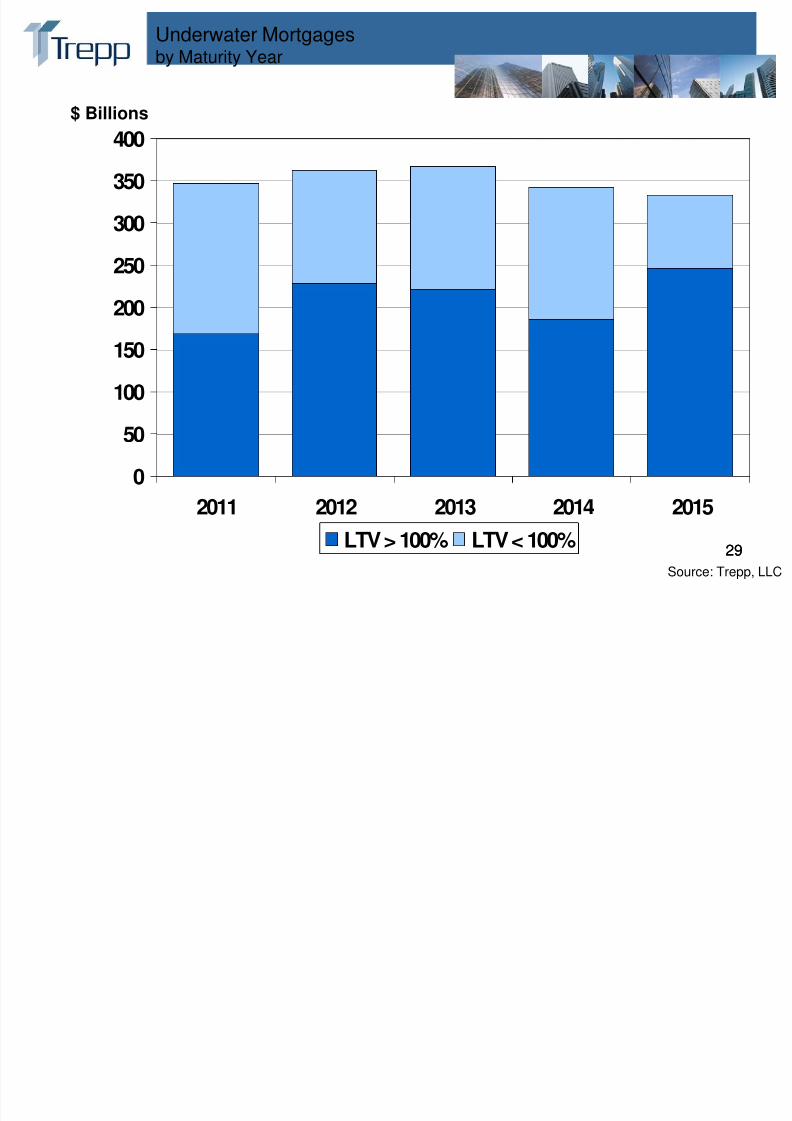

Underwater Mortgagesby Maturity Year

0

50

100

150

200

250

300

350

400

2011 2012 2013 2014 2015

LTV > 100% LTV < 100%

Source: Trepp, LLC

$ Billions

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 30/35

30

Looking Forward

• Dodd Frank• FDIC Proposals

• SEC Proposals• New lending platforms

• Covered Bonds

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 31/35

31

Introduction to Trepp, LLC

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 32/35

3232

about Trepp, LLC

• Trepp is the leading provider of analytics, information and technology to the global CMBS and

commercial mortgage finance industry

• Foresight Analytics is a division of Trepp

• 30 year history in structured finance with a focus on CMBS the past 15 years

• Headquartered in New York City with offices in San Francisco and London

• Deal coverage includes North American, European, and Asian CMBS as well as Commercial Real

Estate backed CDOs

• Largest commercially available database containing detailed information on over 1800 deals and

more than 100,000 loans which support close to $800 billion in securities

• Trepp is a wholly-owned subsidiary of DMG Information, which is a part of the Daily Mail Group, a

multi-billion pound media company in Britain.

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 33/35

33

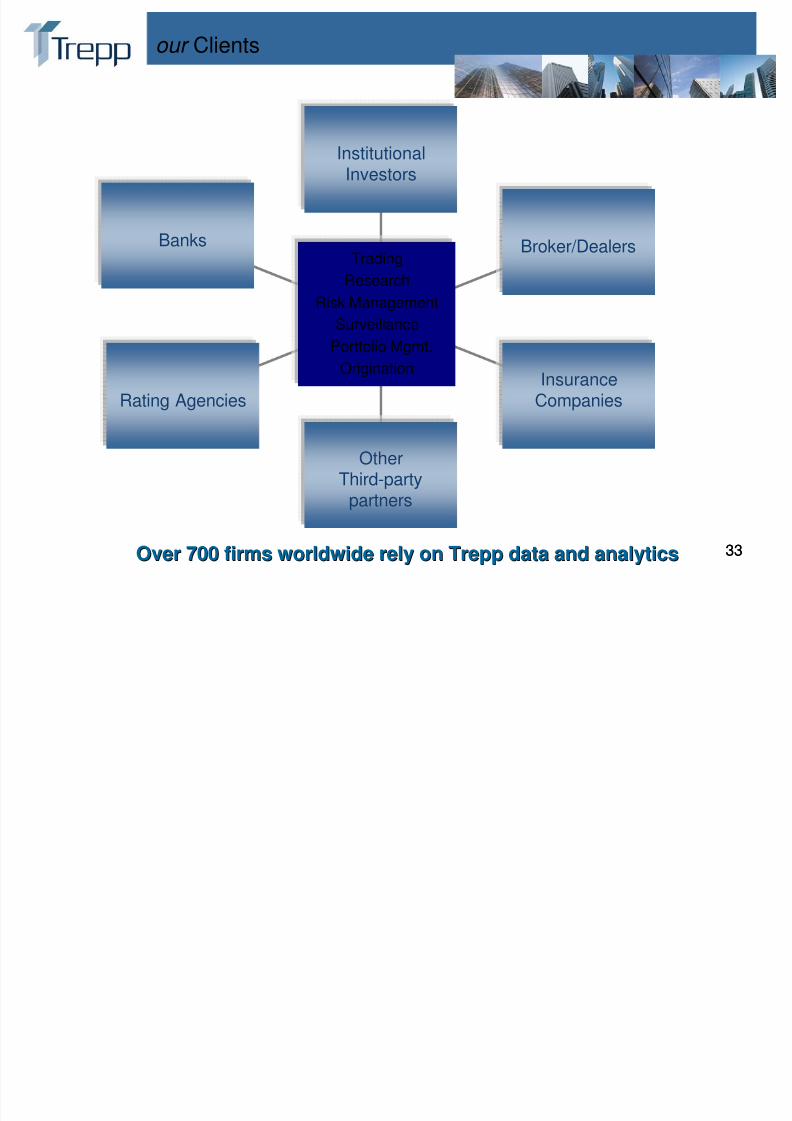

our Clients

Banks

Rating Agencies

OtherThird-party

partners

InsuranceCompanies

Broker/Dealers

InstitutionalInvestors

Trading

Research

Risk Management

Surveillance

Portfolio Mgmt.

Origination

Over 700 firms worldwide rely on Trepp data and analyticsOver 700 firms worldwide rely on Trepp data and analytics 33

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 34/35

34

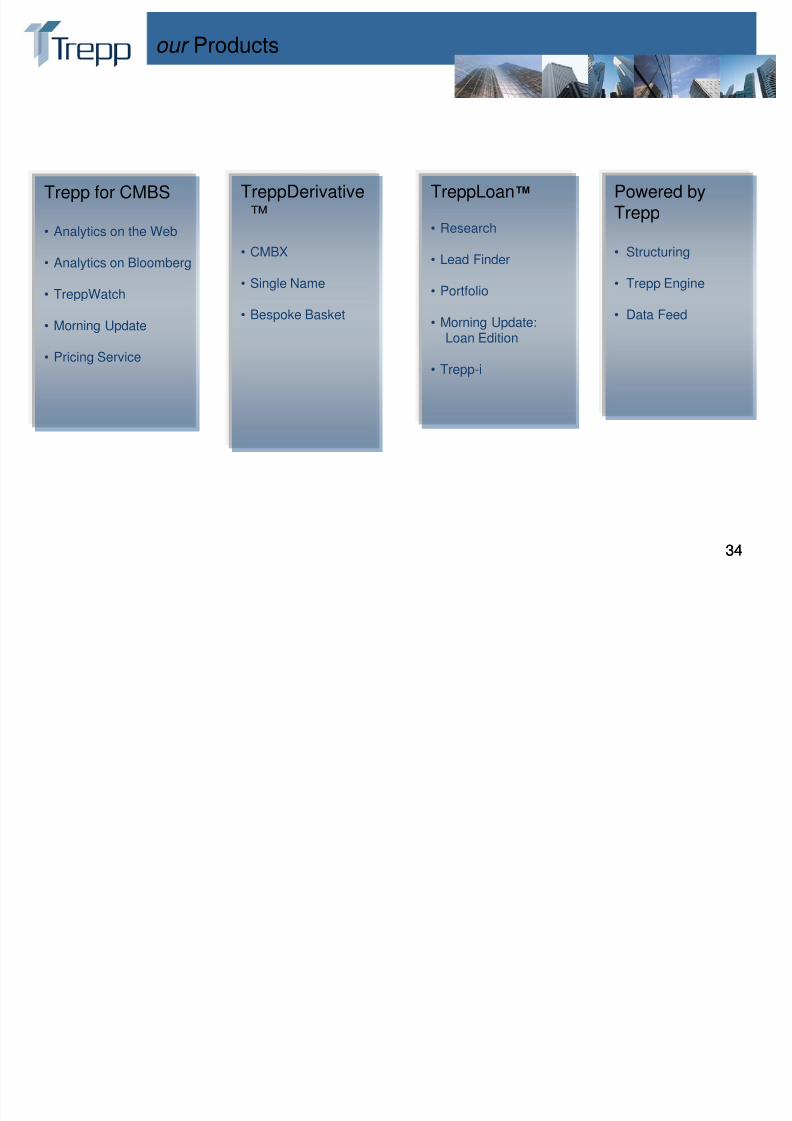

our Products

TreppLoan™

• Research

• Lead Finder

• Portfolio

• Morning Update:Loan Edition

• Trepp-i

Trepp for CMBS

• Analytics on the Web

• Analytics on Bloomberg

• TreppWatch

• Morning Update

• Pricing Service

Powered by

Trepp

• Structuring

• Trepp Engine

• Data Feed

TreppDerivative

™

• CMBX

• Single Name

• Bespoke Basket

34

8/3/2019 TREPP CMBS 2011 Q2

http://slidepdf.com/reader/full/trepp-cmbs-2011-q2 35/35

3535