Embed Size (px)

Citation preview

Download this presentation

1. Go to www.HotelNewsNow.com

2. Click “STR Data Presentations”

3. Select “STAY WYSE 2019: Hostel Performance” to download.

AGENDA

1. Who we are

2. London spotlight

3. Amsterdam spotlight

4. Key takeaways

Who we are

Nashville, TN

• 30+ years in business

• Privately-held company

• Collect data from 62,000+ accommodations worldwide

• 98% client retention rate

• Office Areas in 16 countries worldwide

• Expanded focus now includes serviced apartments, hostels,self storage, and more

STR is the leading provider of global data benchmarking,

analytics and marketplace insights

of STR customers Select snapshot

STR Locations:

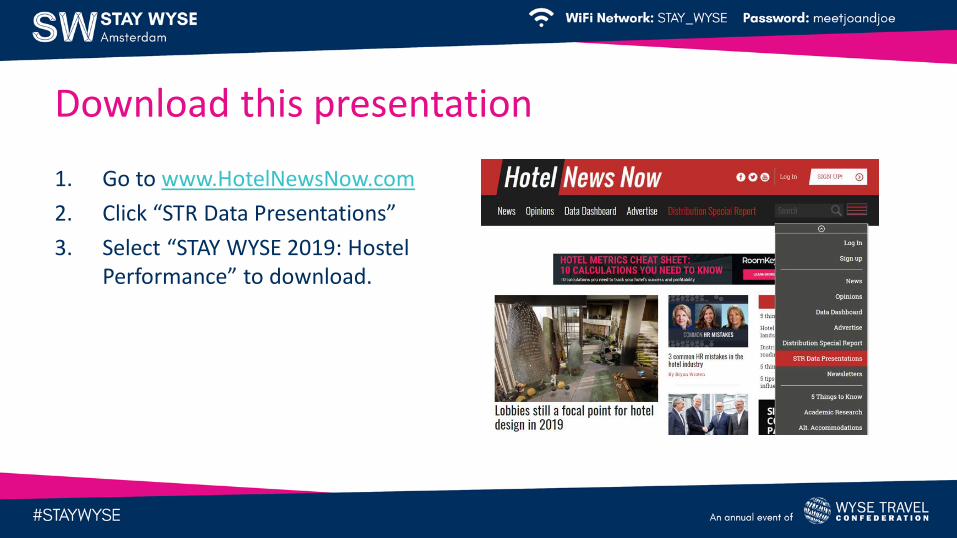

Our Key Performance Indicators:

MYTHS

Occupancy The percentage of available beds sold over a specific time period.

Average Daily Rate (ADR) The average rate paid for beds sold during a specific time period.

Revenue Per Available Bed (RevPAB) Bed revenue allocated across all available beds.

Total Revenue Per Available Bed Total revenue (Bed + F&B + Other) allocated across all available beds.

(TrevPAB)

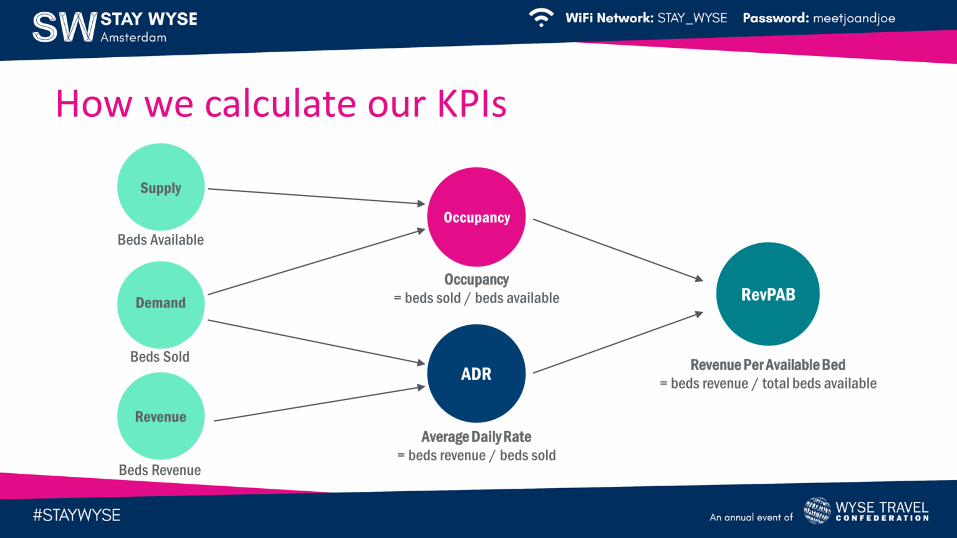

How we calculate our KPIs

Supply

Revenue

Demand

Occupancy

ADR

RevPAB

Beds Available

Beds Sold

Beds Revenue

Occupancy

= beds sold / beds available

Average Daily Rate

= beds revenue / beds sold

Revenue Per Available Bed

= beds revenue / total beds available

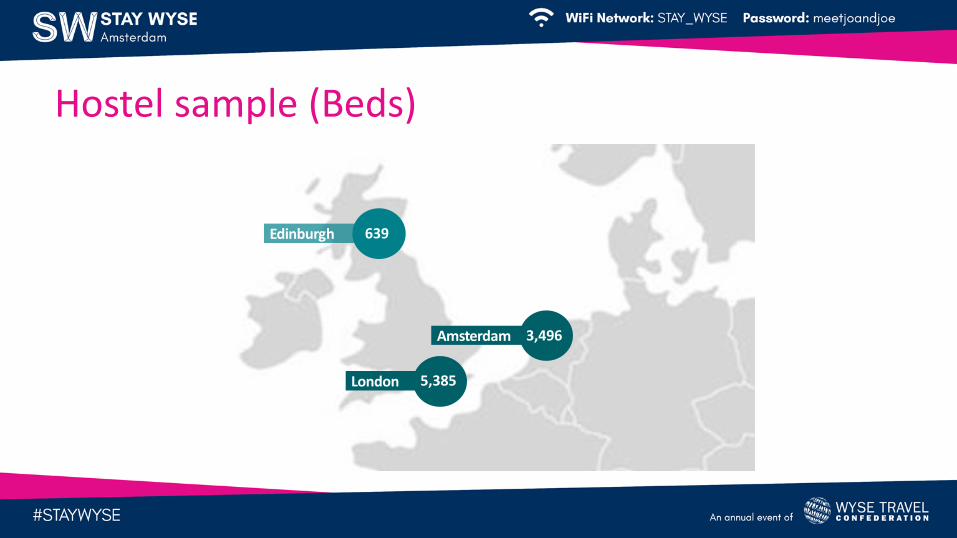

Hostel sample (Beds)

London 5,385

Amsterdam 3,496

Edinburgh 639

London Overview

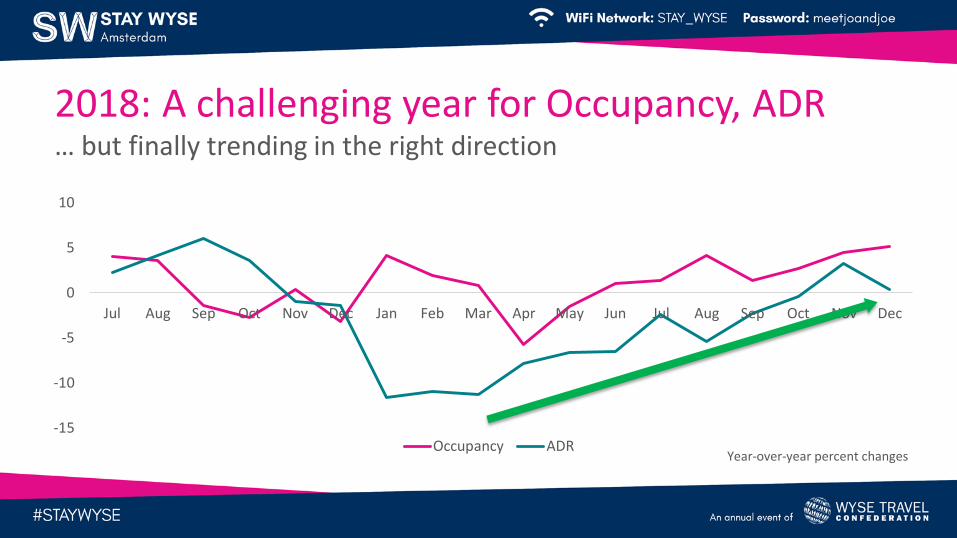

2018: A challenging year for Occupancy, ADR… but finally trending in the right direction

-15

-10

-5

0

5

10

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Occupancy ADRYear-over-year percent changes

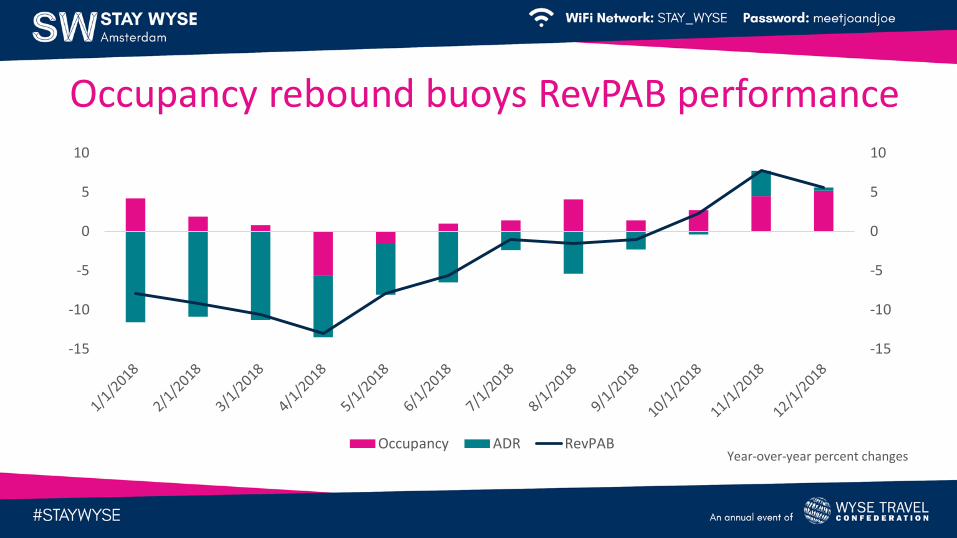

Occupancy rebound buoys RevPAB performance

-15

-10

-5

0

5

10

-15

-10

-5

0

5

10

Occupancy ADR RevPABYear-over-year percent changes

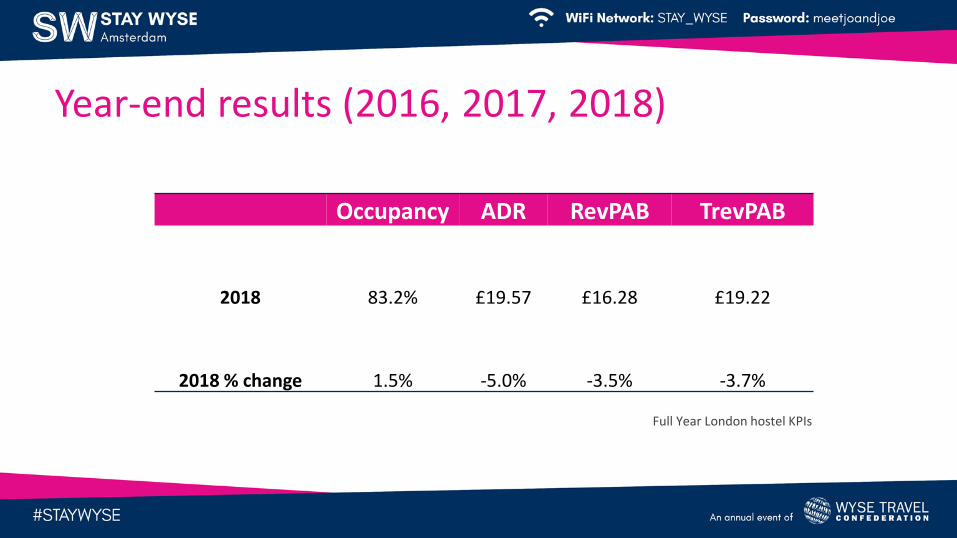

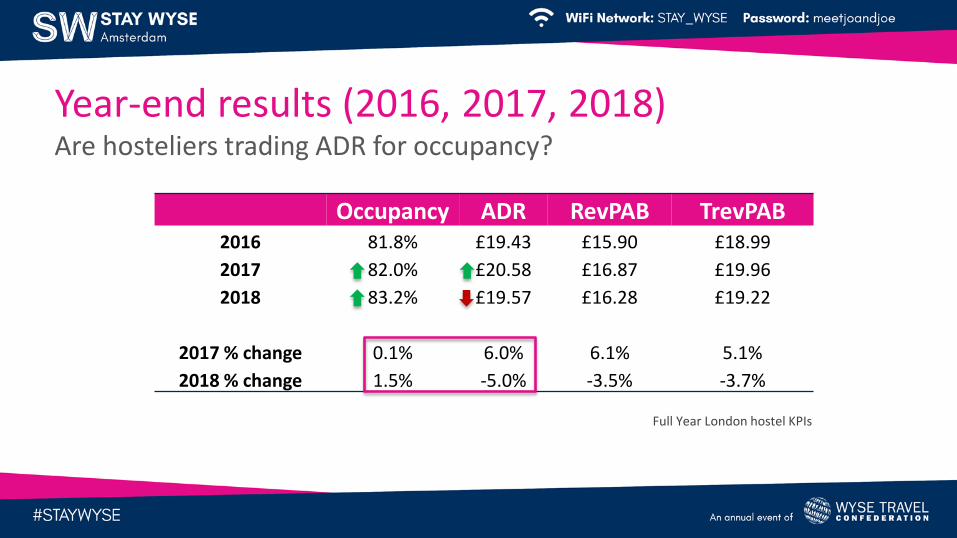

Occupancy ADR RevPAB TrevPAB

2018 83.2% £19.57 £16.28 £19.22

2018 % change 1.5% -5.0% -3.5% -3.7%

Full Year London hostel KPIs

Year-end results (2016, 2017, 2018)

Occupancy ADR RevPAB TrevPAB2016 81.8% £19.43 £15.90 £18.99

2017 82.0% £20.58 £16.87 £19.96

2018 83.2% £19.57 £16.28 £19.22

2017 % change 0.1% 6.0% 6.1% 5.1%

2018 % change 1.5% -5.0% -3.5% -3.7%

Year-end results (2016, 2017, 2018)Are hosteliers trading ADR for occupancy?

Full Year London hostel KPIs

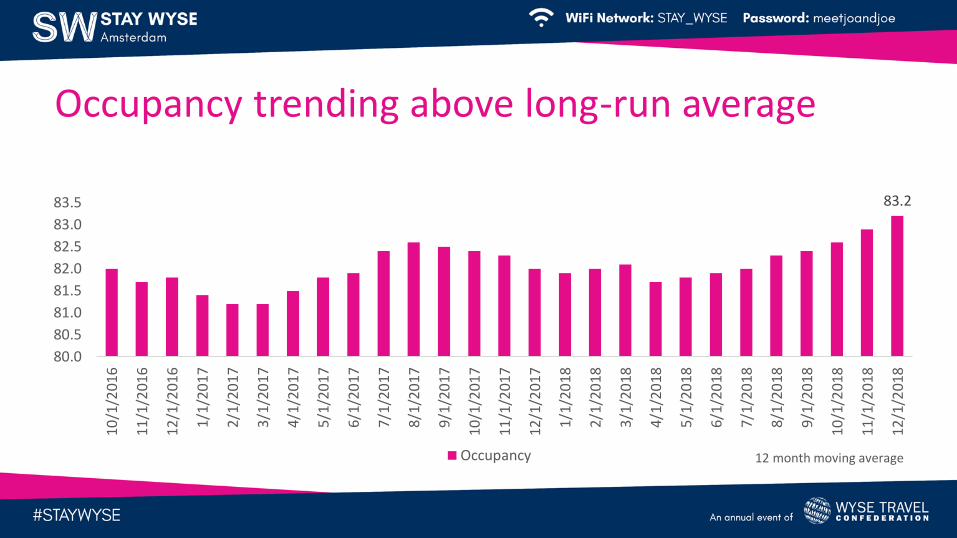

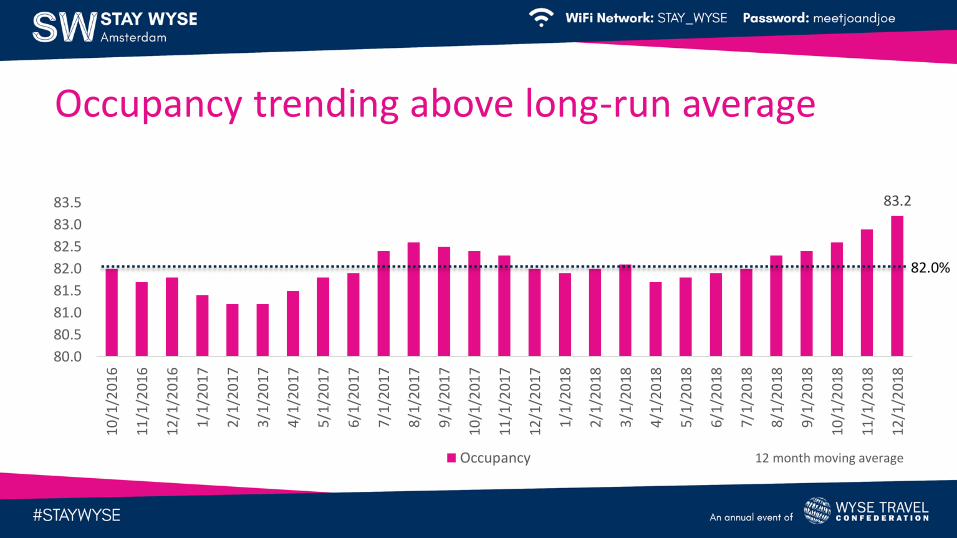

Occupancy trending above long-run average

83.2

80.0

80.5

81.0

81.5

82.0

82.5

83.0

83.5

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

1/1/

2018

2/1/

2018

3/1/

2018

4/1/

2018

5/1/

2018

6/1/

2018

7/1/

2018

8/1/

2018

9/1/

2018

10/1

/201

8

11/1

/201

8

12/1

/201

8

Occupancy 12 month moving average

Occupancy trending above long-run average

83.2

80.0

80.5

81.0

81.5

82.0

82.5

83.0

83.5

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

1/1/

2018

2/1/

2018

3/1/

2018

4/1/

2018

5/1/

2018

6/1/

2018

7/1/

2018

8/1/

2018

9/1/

2018

10/1

/201

8

11/1

/201

8

12/1

/201

8

Occupancy 12 month moving average

82.0%

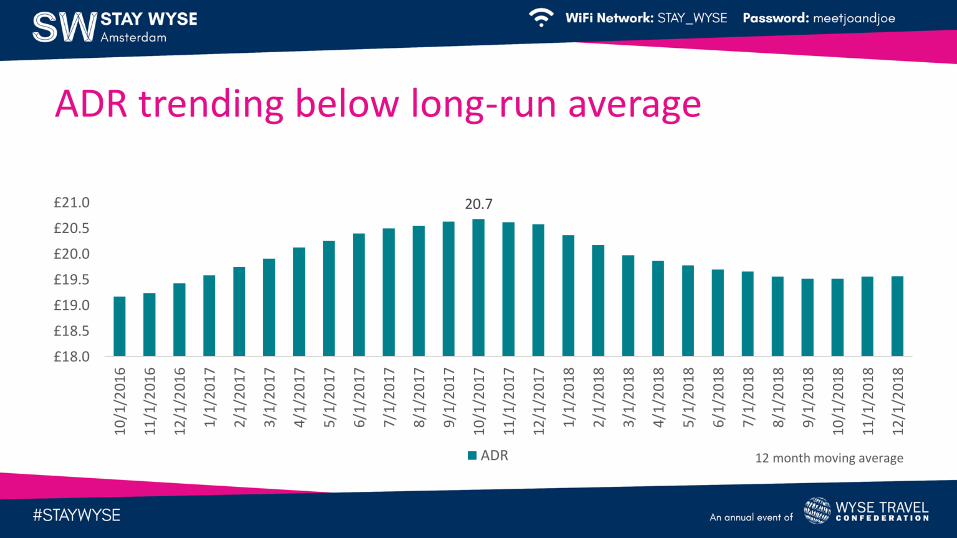

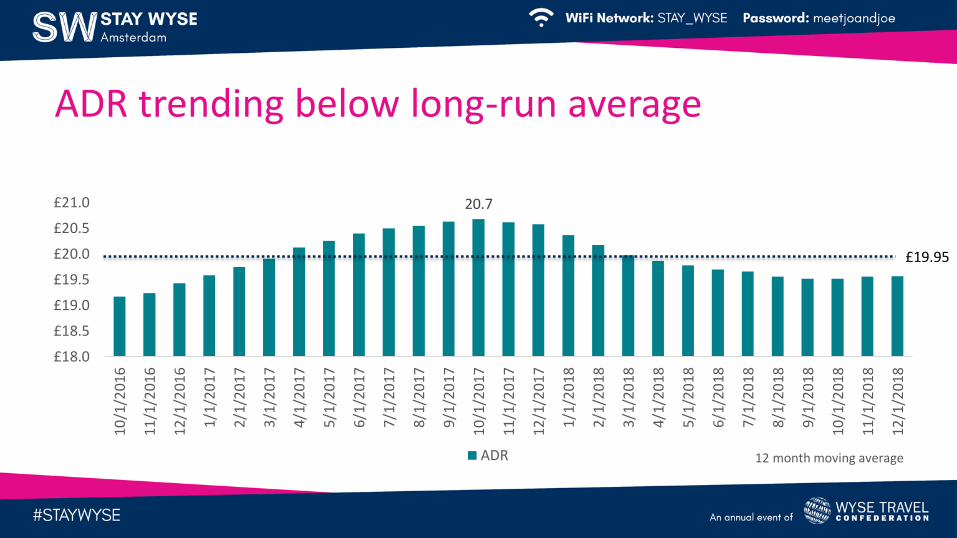

ADR trending below long-run average

20.7

£18.0

£18.5

£19.0

£19.5

£20.0

£20.5

£21.0

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

1/1/

2018

2/1/

2018

3/1/

2018

4/1/

2018

5/1/

2018

6/1/

2018

7/1/

2018

8/1/

2018

9/1/

2018

10/1

/201

8

11/1

/201

8

12/1

/201

8

ADR 12 month moving average

ADR trending below long-run average

20.7

£18.0

£18.5

£19.0

£19.5

£20.0

£20.5

£21.0

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

1/1/

2018

2/1/

2018

3/1/

2018

4/1/

2018

5/1/

2018

6/1/

2018

7/1/

2018

8/1/

2018

9/1/

2018

10/1

/201

8

11/1

/201

8

12/1

/201

8

ADR

£19.95

12 month moving average

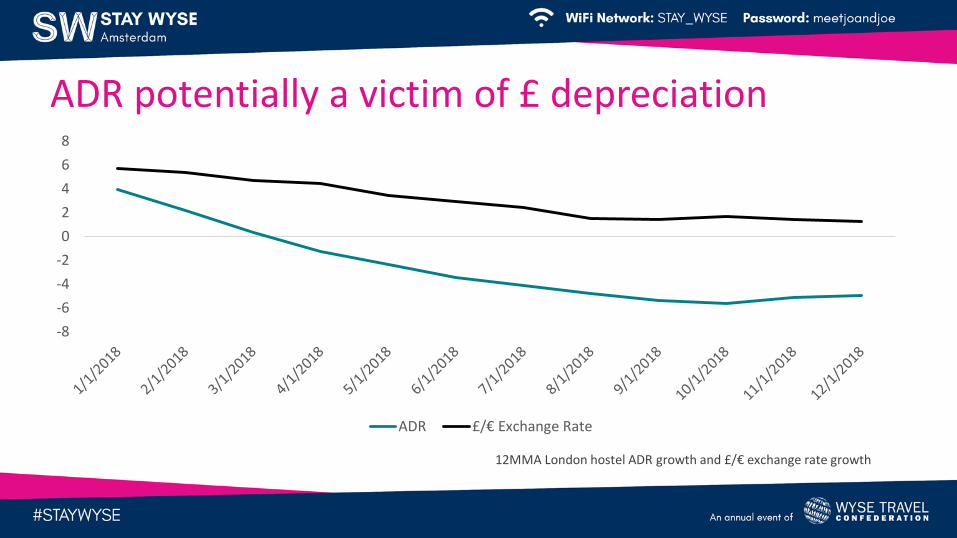

ADR potentially a victim of £ depreciation

-8

-6

-4

-2

0

2

4

6

8

ADR £/€ Exchange Rate

12MMA London hostel ADR growth and £/€ exchange rate growth

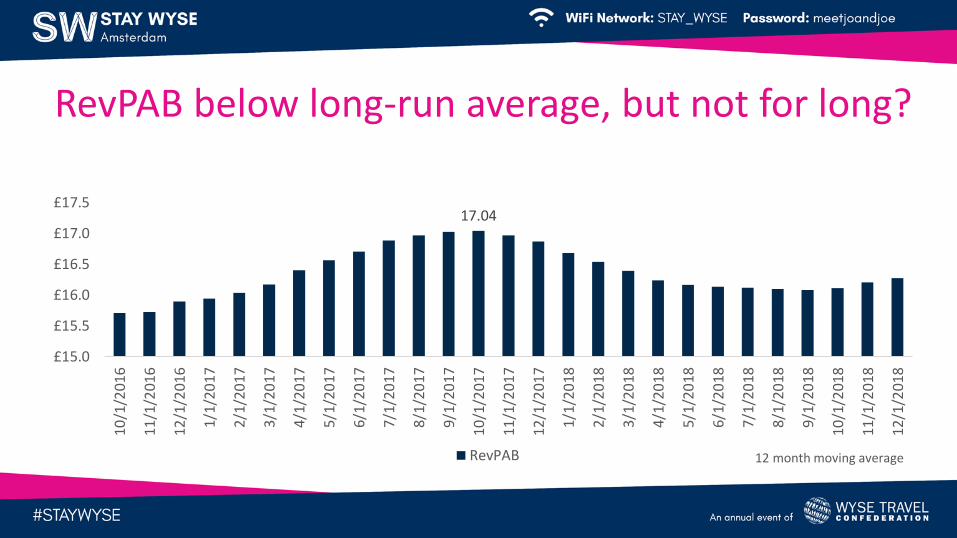

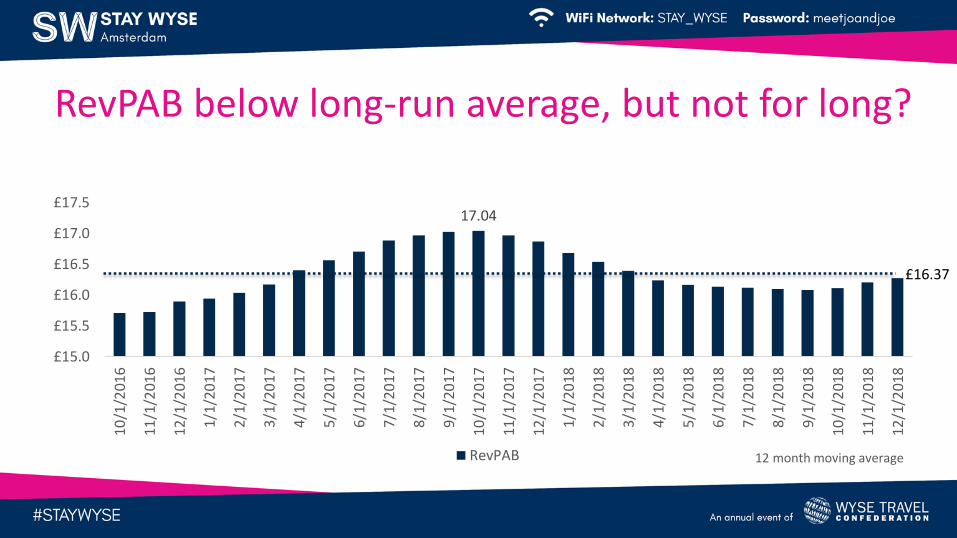

RevPAB below long-run average, but not for long?

17.04

£15.0

£15.5

£16.0

£16.5

£17.0

£17.5

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

1/1/

2018

2/1/

2018

3/1/

2018

4/1/

2018

5/1/

2018

6/1/

2018

7/1/

2018

8/1/

2018

9/1/

2018

10/1

/201

8

11/1

/201

8

12/1

/201

8

RevPAB 12 month moving average

RevPAB below long-run average, but not for long?

17.04

£15.0

£15.5

£16.0

£16.5

£17.0

£17.5

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

1/1/

2018

2/1/

2018

3/1/

2018

4/1/

2018

5/1/

2018

6/1/

2018

7/1/

2018

8/1/

2018

9/1/

2018

10/1

/201

8

11/1

/201

8

12/1

/201

8

RevPAB

£16.37

12 month moving average

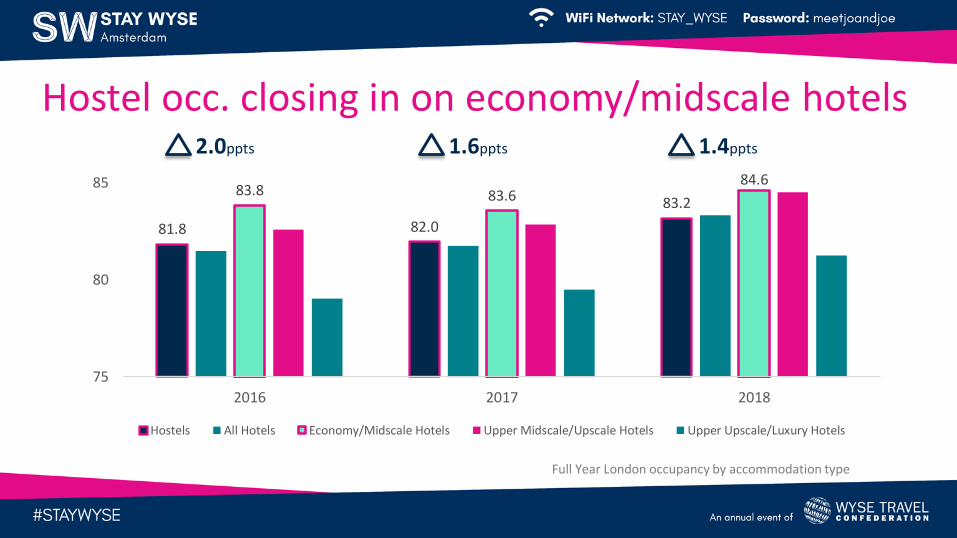

Hostel occ. closing in on economy/midscale hotels

81.8 82.0

83.283.8 83.6

84.6

75

80

85

2016 2017 2018

Hostels All Hotels Economy/Midscale Hotels Upper Midscale/Upscale Hotels Upper Upscale/Luxury Hotels

Full Year London occupancy by accommodation type

2.0ppts 1.6ppts 1.4ppts

2018 not the best year for pricing power

6.0

-5.0

2.2

0.0

-6

-4

-2

0

2

4

6

8

2017 2018

Hostels All Hotels Economy/Midscale Hotels Upper Midscale/Upscale Hotels Upper Upscale/Luxury Hotels

Full Year London occupancy by accommodation type

Amsterdam Overview

Guests and overnight hotel stays2007 - 2017

Source: Amsterdam Research, Information and Statistics

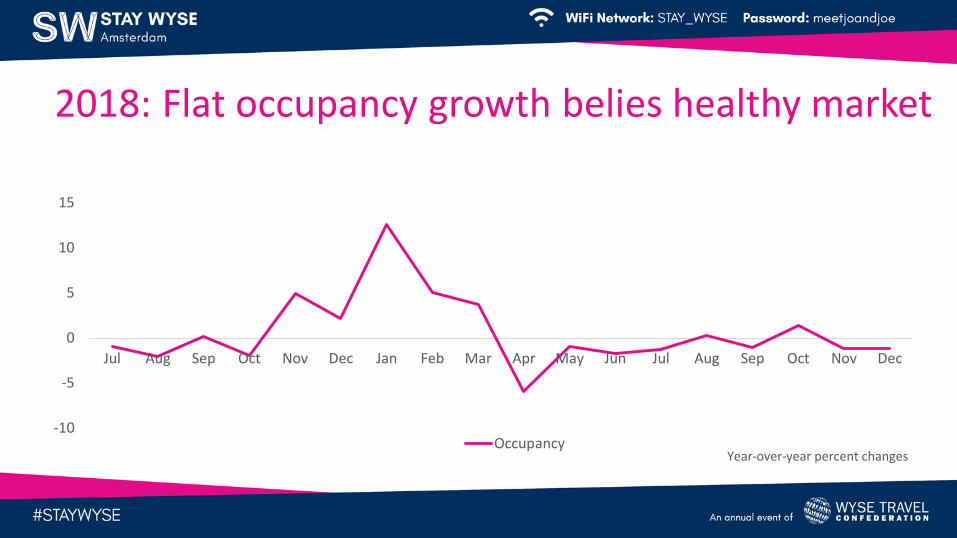

2018: Flat occupancy growth belies healthy market

-10

-5

0

5

10

15

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

OccupancyYear-over-year percent changes

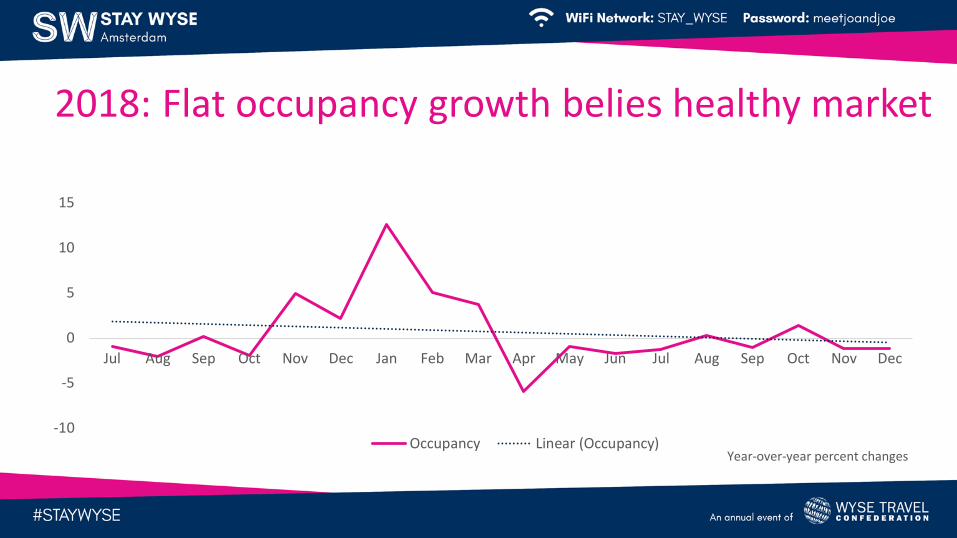

2018: Flat occupancy growth belies healthy market

-10

-5

0

5

10

15

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Occupancy Linear (Occupancy)Year-over-year percent changes

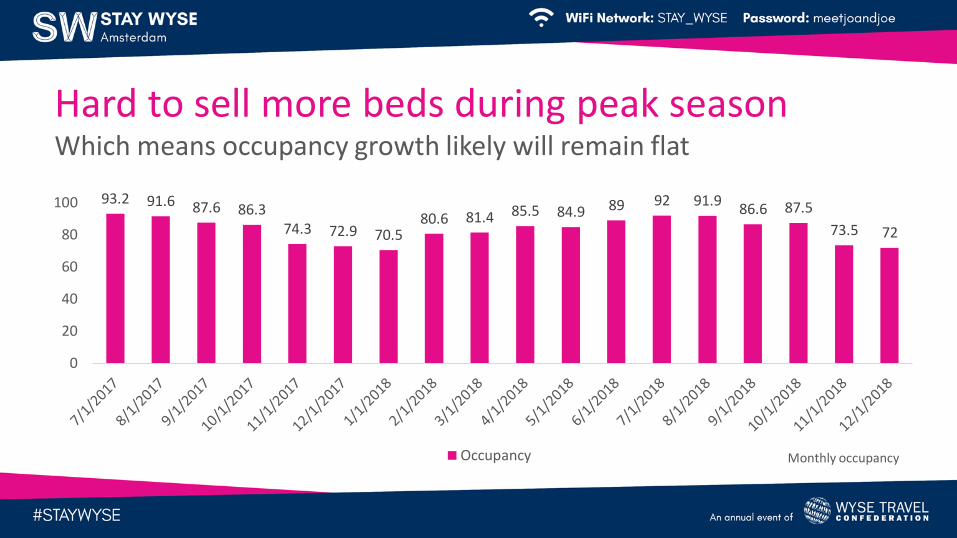

93.2 91.6 87.6 86.374.3 72.9 70.5

80.6 81.4 85.5 84.9 89 92 91.986.6 87.5

73.5 72

0

20

40

60

80

100

Occupancy Monthly occupancy

Hard to sell more beds during peak seasonWhich means occupancy growth likely will remain flat

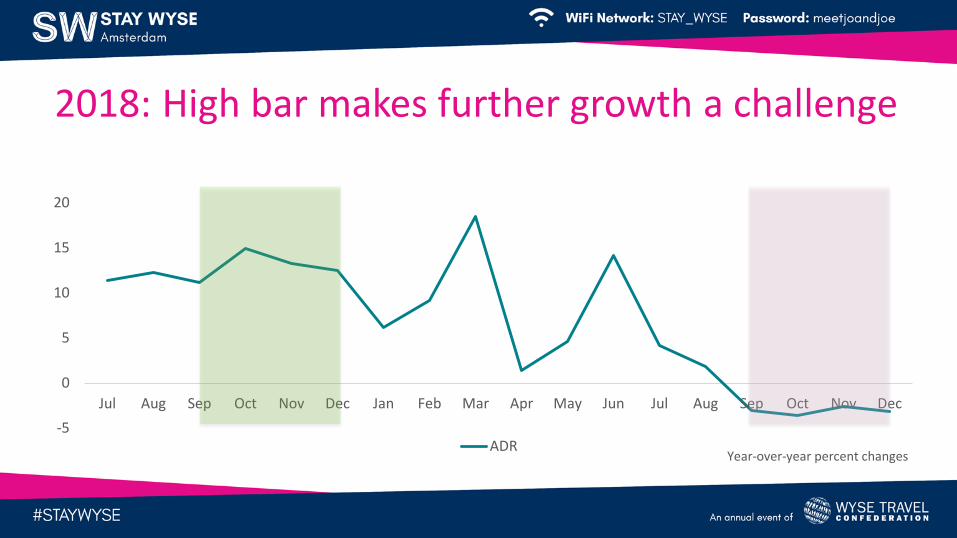

2018: High bar makes further growth a challenge

-5

0

5

10

15

20

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

ADRYear-over-year percent changes

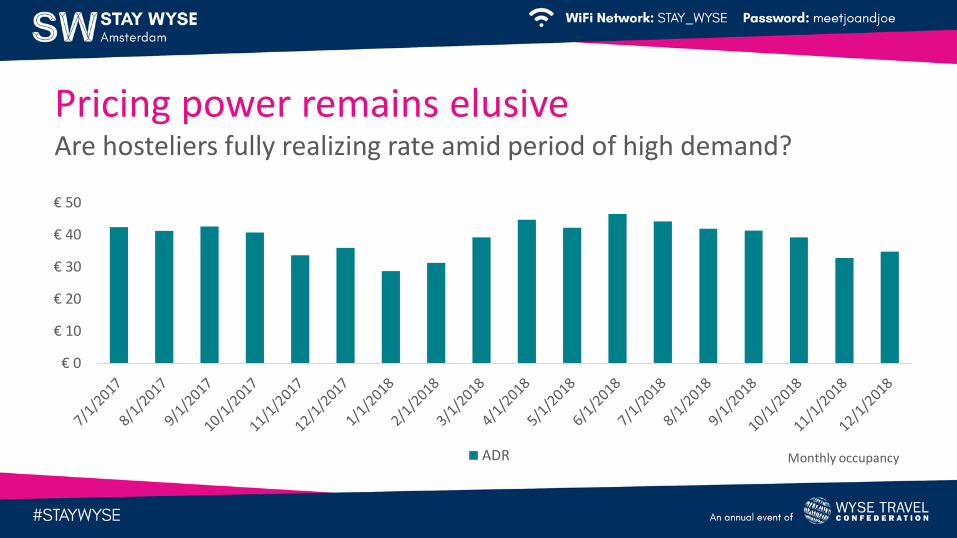

€ 0

€ 10

€ 20

€ 30

€ 40

€ 50

ADR Monthly occupancy

Pricing power remains elusiveAre hosteliers fully realizing rate amid period of high demand?

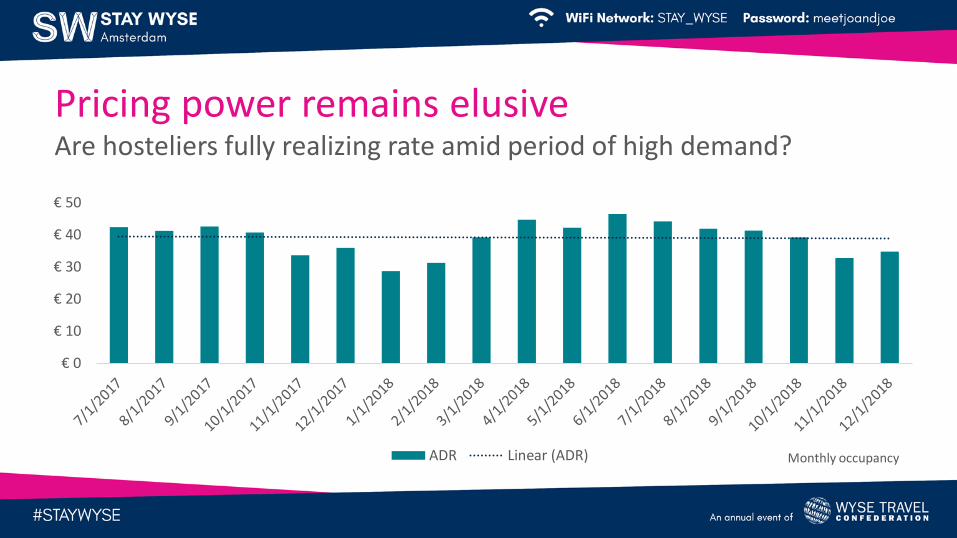

€ 0

€ 10

€ 20

€ 30

€ 40

€ 50

ADR Linear (ADR) Monthly occupancy

Pricing power remains elusiveAre hosteliers fully realizing rate amid period of high demand?

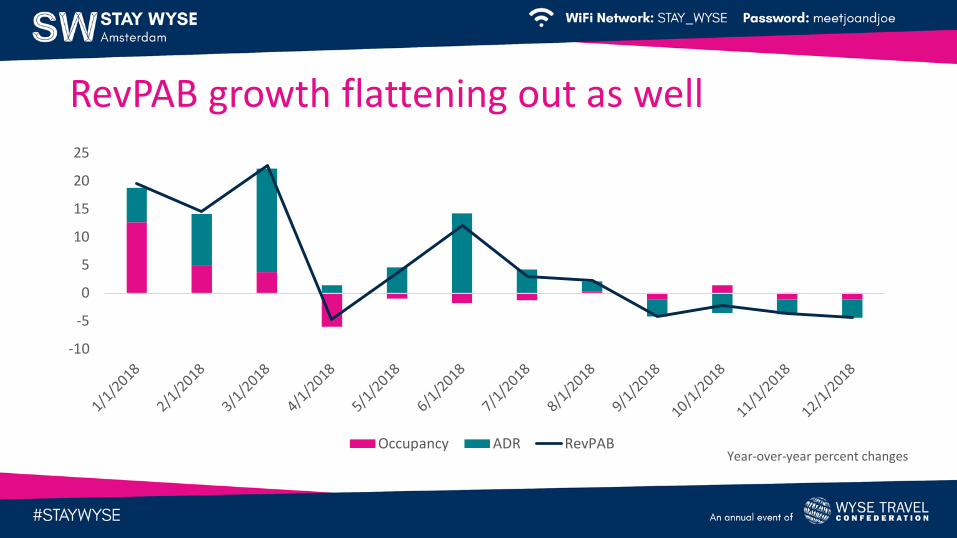

RevPAB growth flattening out as well

-10

-5

0

5

10

15

20

25

Occupancy ADR RevPABYear-over-year percent changes

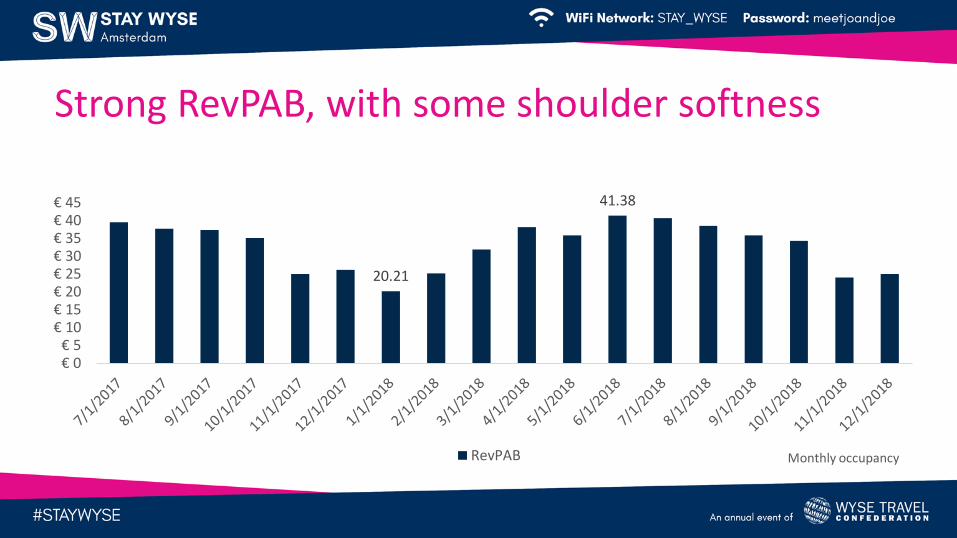

20.21

41.38

€ 0€ 5

€ 10€ 15€ 20€ 25€ 30€ 35€ 40€ 45

RevPAB Monthly occupancy

Strong RevPAB, with some shoulder softness

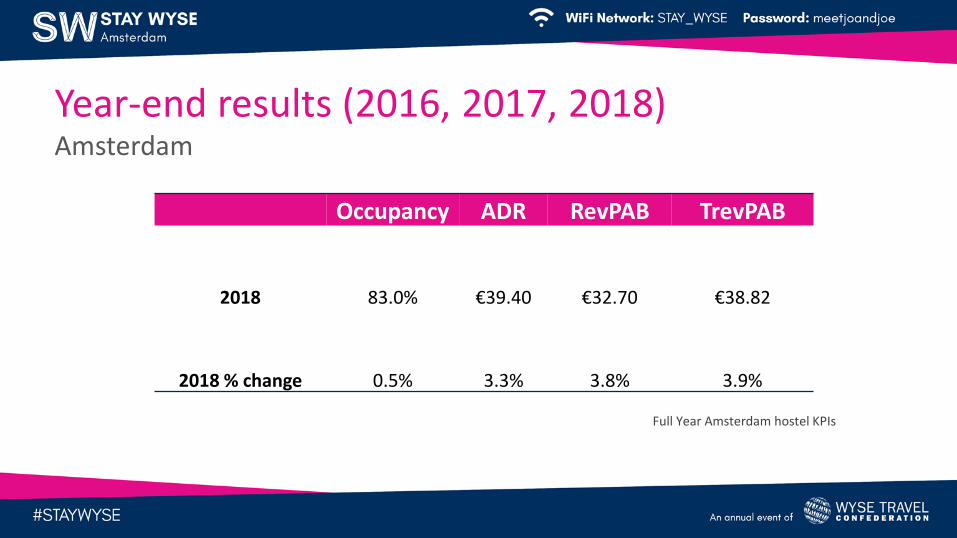

Occupancy ADR RevPAB TrevPAB

2018 83.0% €39.40 €32.70 €38.82

2018 % change 0.5% 3.3% 3.8% 3.9%

Full Year Amsterdam hostel KPIs

Year-end results (2016, 2017, 2018)Amsterdam

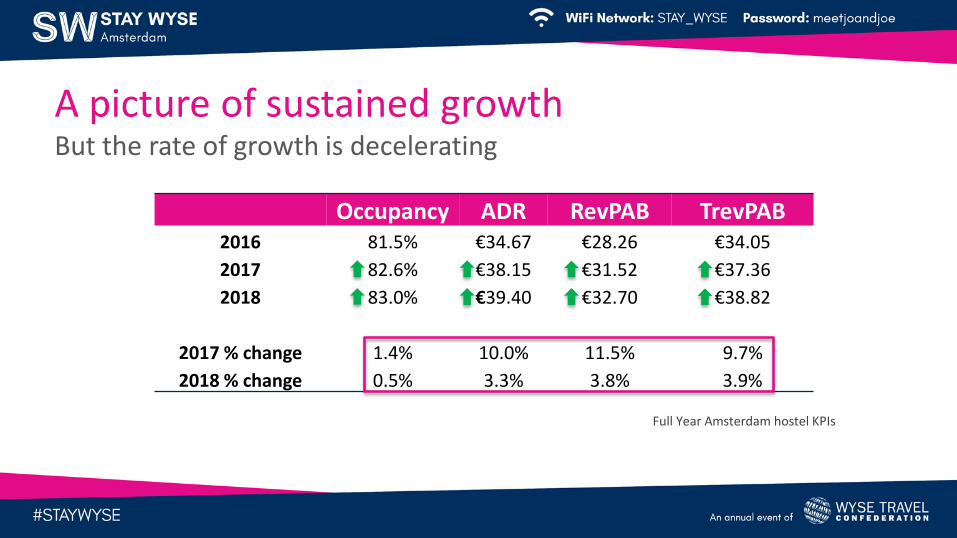

Occupancy ADR RevPAB TrevPAB2016 81.5% €34.67 €28.26 €34.05

2017 82.6% €38.15 €31.52 €37.36

2018 83.0% €39.40 €32.70 €38.82

2017 % change 1.4% 10.0% 11.5% 9.7%

2018 % change 0.5% 3.3% 3.8% 3.9%

Full Year Amsterdam hostel KPIs

A picture of sustained growthBut the rate of growth is decelerating

0

2

4

6

8

10

12

14

16

Occupancy ADR RevPAB TrevPAB

12MMA Amsterdam occupancy growth

Growth is decelerating across the boardOccupancy, ADR, RevPAB and TrevPAB

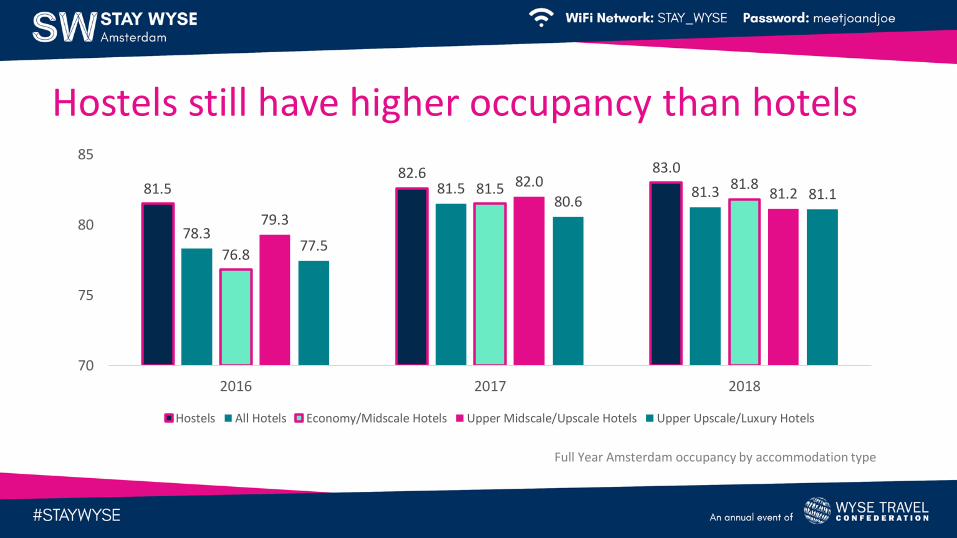

Hostels still have higher occupancy than hotels

81.582.6 83.0

78.3

81.5 81.3

76.8

81.5 81.8

79.3

82.081.2

77.5

80.6 81.1

70

75

80

85

2016 2017 2018

Hostels All Hotels Economy/Midscale Hotels Upper Midscale/Upscale Hotels Upper Upscale/Luxury Hotels

Full Year Amsterdam occupancy by accommodation type

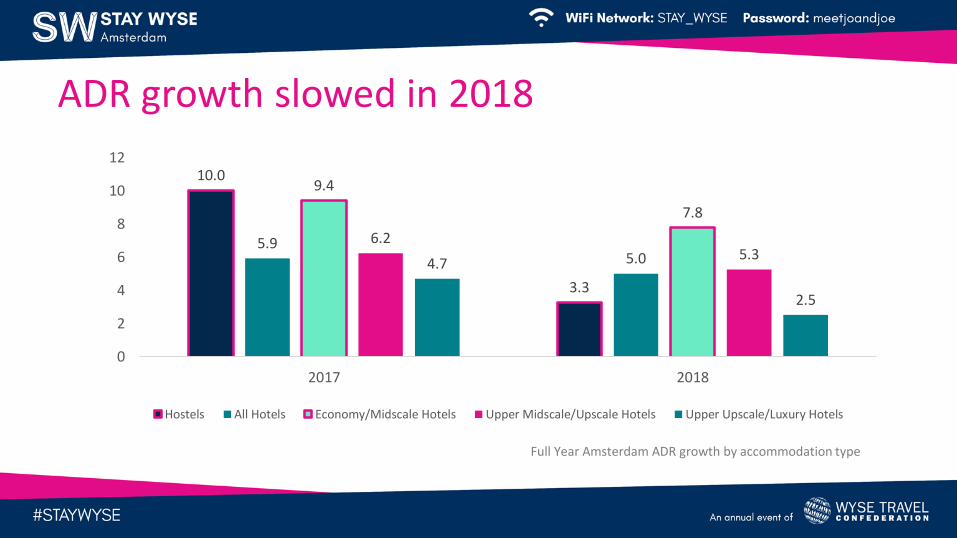

ADR growth slowed in 2018

10.0

3.3

5.95.0

9.4

7.8

6.25.3

4.7

2.5

0

2

4

6

8

10

12

2017 2018

Hostels All Hotels Economy/Midscale Hotels Upper Midscale/Upscale Hotels Upper Upscale/Luxury Hotels

Full Year Amsterdam ADR growth by accommodation type

Takeaways

1. Decreases in London ADR have outweighed any gains made in occupancy.

2. Unprecedented demand in Amsterdam is fueling strong performance.

3. Amsterdam: Hosteliers are nearing capacity in occupancy, which means ADR is the remaining growth vehicle.

4. ADR growth decelerated (or went negative) in both markets during 2018.

5. Fundamentals are strong going into 2019, although various market factors could impede performance.

Download our free report

Visit strglobal.com/hostel-performance-trends to download our free report.