Embed Size (px)

Citation preview

Trends in HealthcareInvestments and Exits 2016

Investor Confidence and Innovation Drive

Healthcare Venture to New Heights

Written by

Jonathan Norris

Managing Director

Silicon Valley Bank

M 650.575.1377

@jonnysvb

Paul Schuber

Valuations Associate

SVB Analytics

Caitlin Tolman

Senior Associate

Silicon Valley Bank

2

Table of Contents

3 Overview

4 Healthcare Venture Fundraising and Investment: A Year of Record Highs

16 Crossover Activity Peaks in Q3, Slows in Q4

19 Healthcare Venture Exits: M&A Climate Improves as IPOs Slow

34 2016 Outlook

35 Glossary

36 Authors

3

2015: Another Banner Year for Healthcare

At the start of 2015, it was hard to imagine that we would have another year as successful as 2014. And yet, by most measures, 2015 came very close.

• Led by a blockbuster M&A deal at the end of the year, potential returns to investors in 2015 rocketed to a new

high. By SVB estimates, three years of strong performance has generated more than $55 billion in potential value

back to investors.

• With record investments in biopharma, 2015 saw more capital invested in healthcare VC-backed companies

than in any other year.

• Non-traditional “crossover investors” increased activity, participating in large mezzanine rounds to take advantage

of the biopharma IPO market.

• While IPOs dipped versus 2014, the public markets continued to be receptive to healthcare companies. Also,

many companies going public in the past two years had very successful public follow-on fundings.

• Biopharma M&A activity increased, culminating in AstraZeneca’s $4 billion payment to Acerta in

December 2015.

• Higher returns, greater investor confidence and faster investment cycles led some funds to raise again within two

years of their previous fund.

• Such a speedy fundraising cycle means venture healthcare has fresh capital to support existing investments and

create new ones, and create a critical cash cushion as IPOs decline and crossover investors pull back.

Despite the slowdown in Q4, the healthcare industry is poised for a strong 2016, though activity likely will not match 2015.

4

Healthcare Venture Fundraising and Investment: A Year of Record Highs

5

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q'15

$ B

illi

on

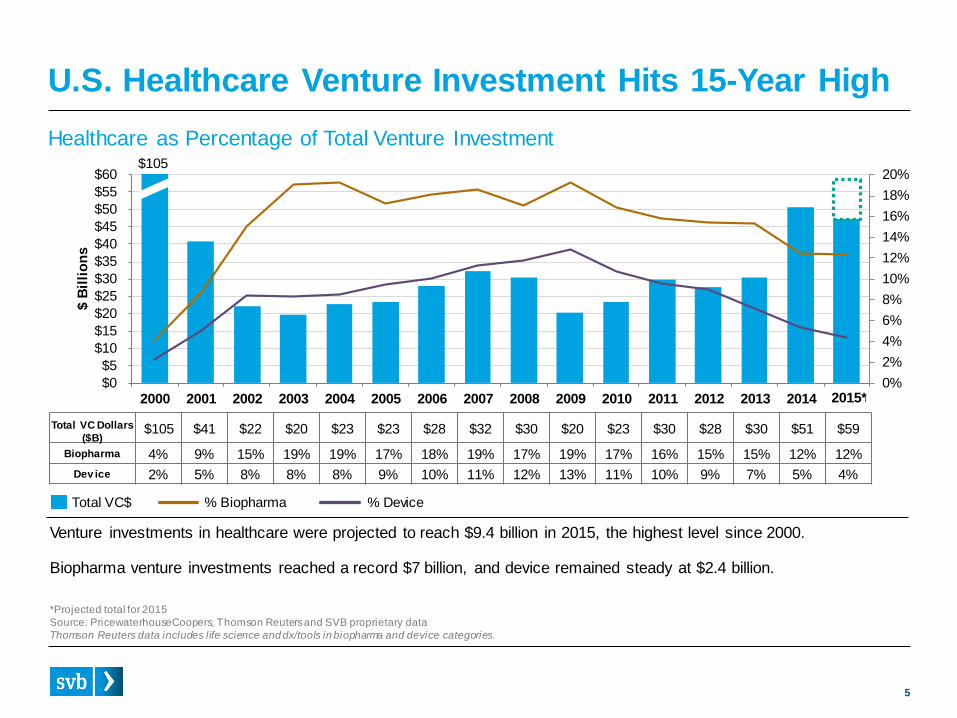

sU.S. Healthcare Venture Investment Hits 15-Year High

Healthcare as Percentage of Total Venture Investment

Venture investments in healthcare were projected to reach $9.4 billion in 2015, the highest level since 2000.

Biopharma venture investments reached a record $7 billion, and device remained steady at $2.4 billion.

Total VC Dollars

($B)$105 $41 $22 $20 $23 $23 $28 $32 $30 $20 $23 $30 $28 $30 $51 $59

Biopharma 4% 9% 15% 19% 19% 17% 18% 19% 17% 19% 17% 16% 15% 15% 12% 12%

Dev ice 2% 5% 8% 8% 8% 9% 10% 11% 12% 13% 11% 10% 9% 7% 5% 4%

$105

Total VC$ % Biopharma % Device

*Projected total for 2015

Source: PricewaterhouseCoopers, Thomson Reuters and SVB proprietary data

Thomson Reuters data includes life science and dx/tools in biopharma and device categories.

2015*

6

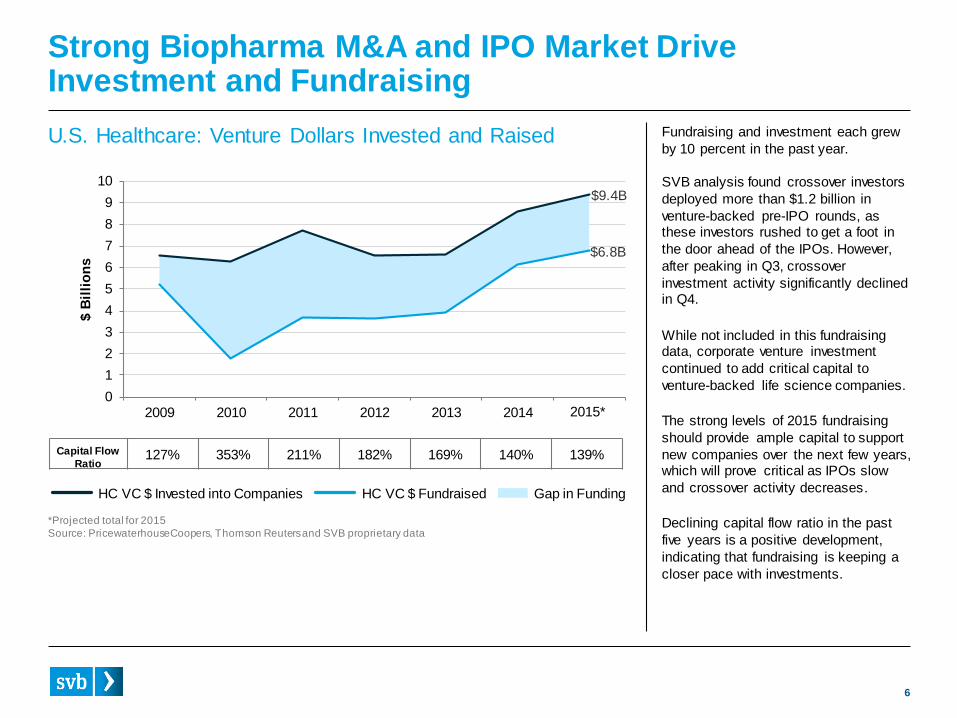

Strong Biopharma M&A and IPO Market Drive Investment and Fundraising

U.S. Healthcare: Venture Dollars Invested and Raised Fundraising and investment each grew

by 10 percent in the past year.

SVB analysis found crossover investors

deployed more than $1.2 billion in

venture-backed pre-IPO rounds, as these investors rushed to get a foot in

the door ahead of the IPOs. However,

after peaking in Q3, crossover

investment activity significantly declined in Q4.

While not included in this fundraising data, corporate venture investment

continued to add critical capital to

venture-backed life science companies.

The strong levels of 2015 fundraising

should provide ample capital to support

new companies over the next few years, which will prove critical as IPOs slow

and crossover activity decreases.

Declining capital flow ratio in the past

five years is a positive development,

indicating that fundraising is keeping a

closer pace with investments.

Capital Flow

Ratio127% 353% 211% 182% 169% 140% 139%

*Projected total for 2015

Source: PricewaterhouseCoopers, Thomson Reuters and SVB proprietary data

$9.4B

$6.8B

0

1

2

3

4

5

6

7

8

9

10

2009 2010 2011 2012 2013 2014 2015 Proj

$ B

illi

on

s

HC VC $ Invested into Companies HC VC $ Fundraised Gap in Funding

2015*

7

46 45 4517

0

40

80

120

# o

f D

ea

ls

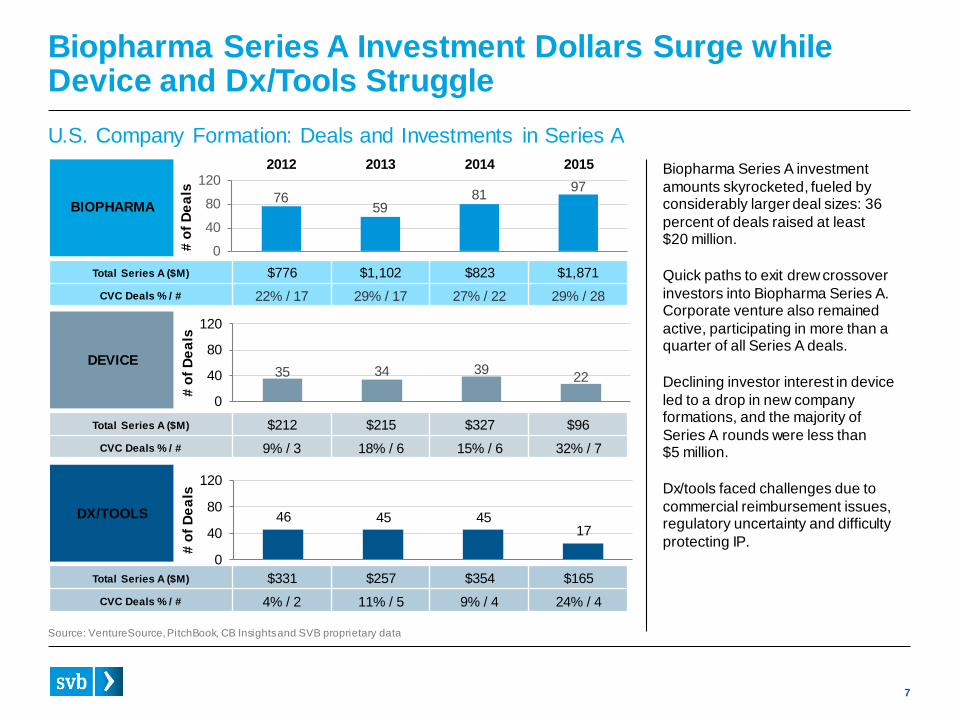

Biopharma Series A Investment Dollars Surge while Device and Dx/Tools Struggle

Source: VentureSource, PitchBook, CB Insights and SVB proprietary data

Biopharma Series A investment

amounts skyrocketed, fueled by considerably larger deal sizes: 36

percent of deals raised at least$20 million.

Quick paths to exit drew crossover

investors into Biopharma Series A. Corporate venture also remained

active, participating in more than a quarter of all Series A deals.

Declining investor interest in device

led to a drop in new company formations, and the majority of

Series A rounds were less than $5 million.

Dx/tools faced challenges due to

commercial reimbursement issues, regulatory uncertainty and difficulty

protecting IP.

7659

8197

0

40

80

1202012 2013 2014 2015

# o

f D

ea

ls

Total Series A ($M) $776 $1,102 $823 $1,871

CVC Deals % / # 22% / 17 29% / 17 27% / 22 29% / 28

BIOPHARMA

35 34 3922

0

40

80

120

# o

f D

ea

ls

Total Series A ($M) $212 $215 $327 $96

CVC Deals % / # 9% / 3 18% / 6 15% / 6 32% / 7

DEVICE

Total Series A ($M) $331 $257 $354 $165

CVC Deals % / # 4% / 2 11% / 5 9% / 4 24% / 4

DX/TOOLS

U.S. Company Formation: Deals and Investments in Series A

8

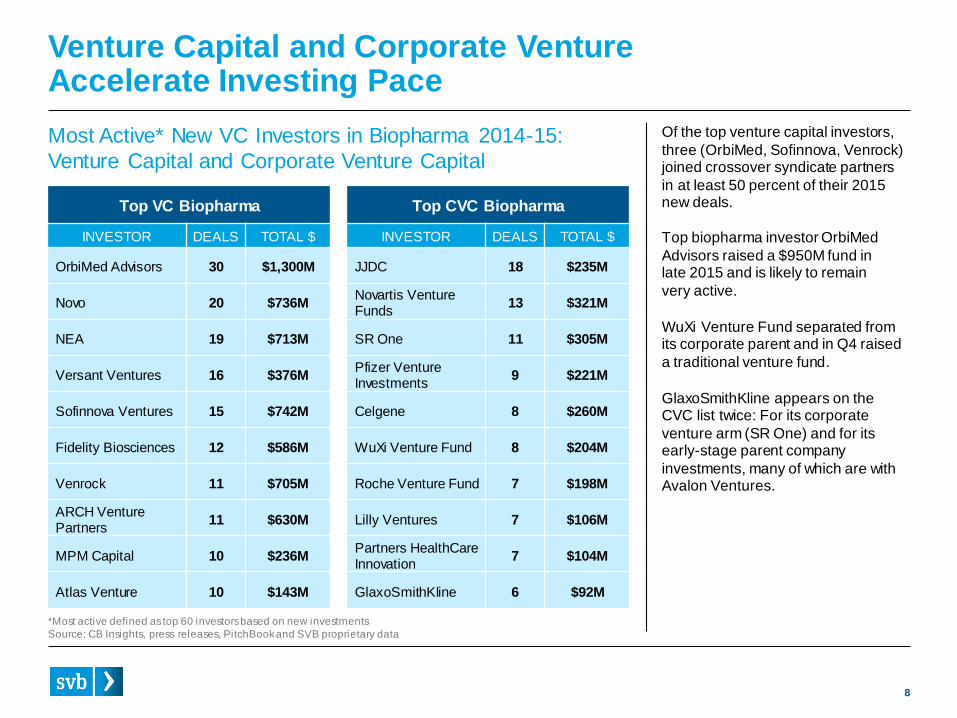

Venture Capital and Corporate VentureAccelerate Investing Pace

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

Of the top venture capital investors,

three (OrbiMed, Sofinnova, Venrock) joined crossover syndicate partners

in at least 50 percent of their 2015 new deals.

Top biopharma investor OrbiMed

Advisors raised a $950M fund in late 2015 and is likely to remain

very active.

WuXi Venture Fund separated from its corporate parent and in Q4 raised

a traditional venture fund.

GlaxoSmithKline appears on the CVC list twice: For its corporate

venture arm (SR One) and for its early-stage parent company

investments, many of which are with Avalon Ventures.

Top VC Biopharma

INVESTOR DEALS TOTAL $

OrbiMed Advisors 30 $1,300M

Novo 20 $736M

NEA 19 $713M

Versant Ventures 16 $376M

Sofinnova Ventures 15 $742M

Fidelity Biosciences 12 $586M

Venrock 11 $705M

ARCH Venture Partners

11 $630M

MPM Capital 10 $236M

Atlas Venture 10 $143M

Top CVC Biopharma

INVESTOR DEALS TOTAL $

JJDC 18 $235M

Novartis Venture Funds

13 $321M

SR One 11 $305M

Pfizer Venture Investments

9 $221M

Celgene 8 $260M

WuXi Venture Fund 8 $204M

Roche Venture Fund 7 $198M

Lilly Ventures 7 $106M

Partners HealthCare Innovation

7 $104M

GlaxoSmithKline 6 $92M

Most Active* New VC Investors in Biopharma 2014-15:

Venture Capital and Corporate Venture Capital

9

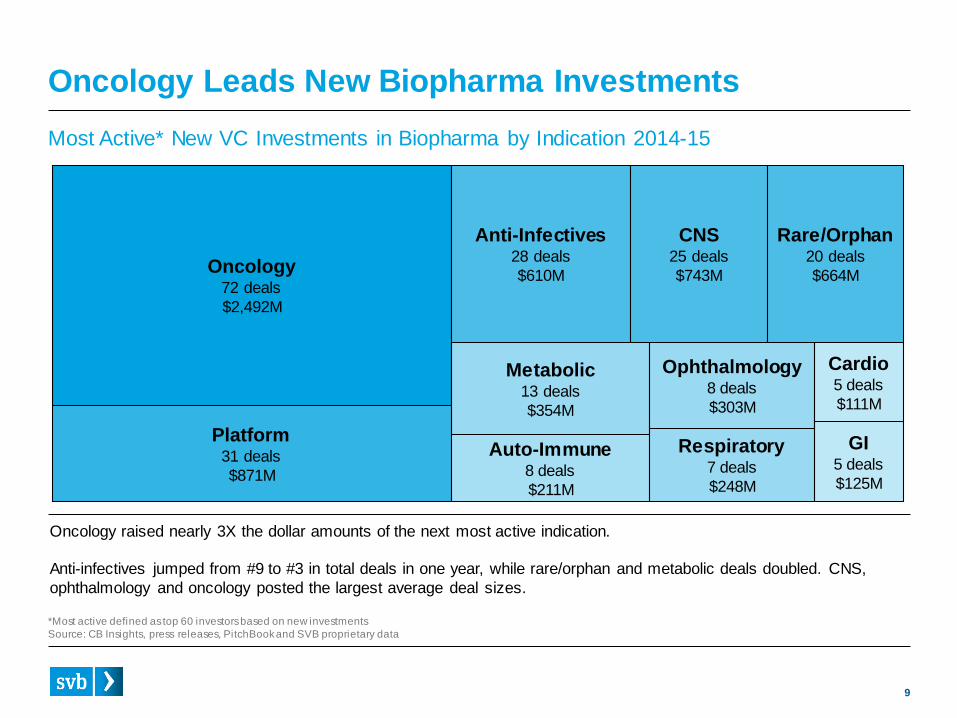

Oncology Leads New Biopharma Investments

Oncology72 deals

$2,492M

Platform31 deals

$871M

Anti-Infectives28 deals

$610M

CNS25 deals

$743M

Rare/Orphan20 deals

$664M

Metabolic13 deals

$354M

Auto-Immune8 deals

$211M

Respiratory7 deals

$248M

Ophthalmology8 deals

$303M

GI5 deals

$125M

Cardio5 deals

$111M

Most Active* New VC Investments in Biopharma by Indication 2014-15

Oncology raised nearly 3X the dollar amounts of the next most active indication.

Anti-infectives jumped from #9 to #3 in total deals in one year, while rare/orphan and metabolic deals doubled. CNS,

ophthalmology and oncology posted the largest average deal sizes.

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

10

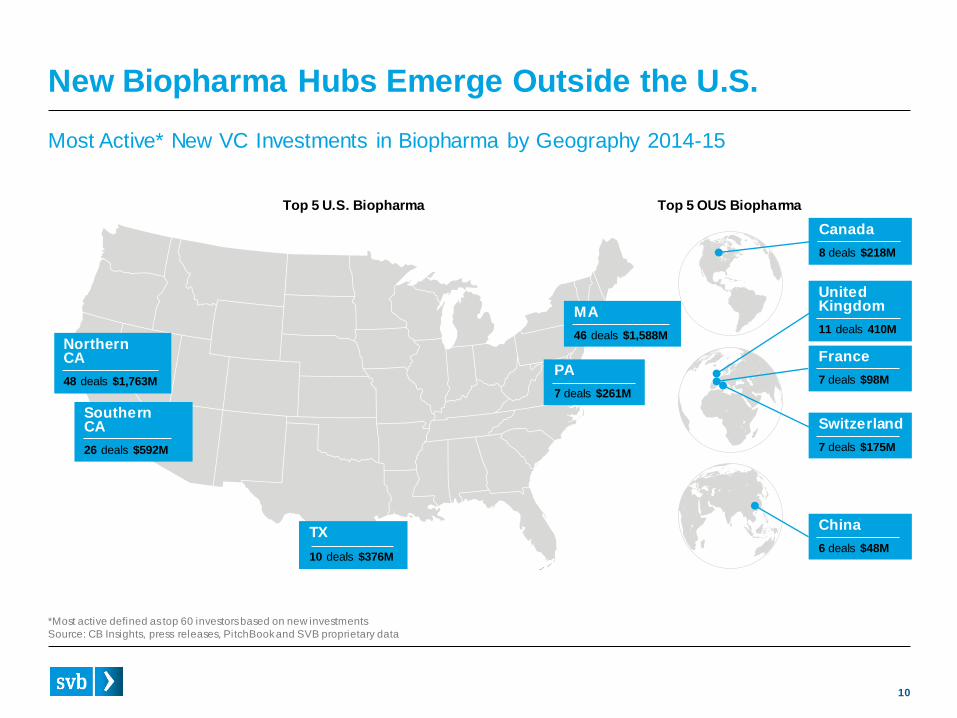

New Biopharma Hubs Emerge Outside the U.S.

Most Active* New VC Investments in Biopharma by Geography 2014-15

NorthernCA

48 deals $1,763M

Southern CA

26 deals $592M

Canada

8 deals $218M

Top 5 U.S. Biopharma Top 5 OUS Biopharma

United Kingdom

11 deals 410M

France

7 deals $98M

China

6 deals $48M

Switzerland

7 deals $175M

MA

46 deals $1,588M

TX

10 deals $376M

PA

7 deals $261M

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

11

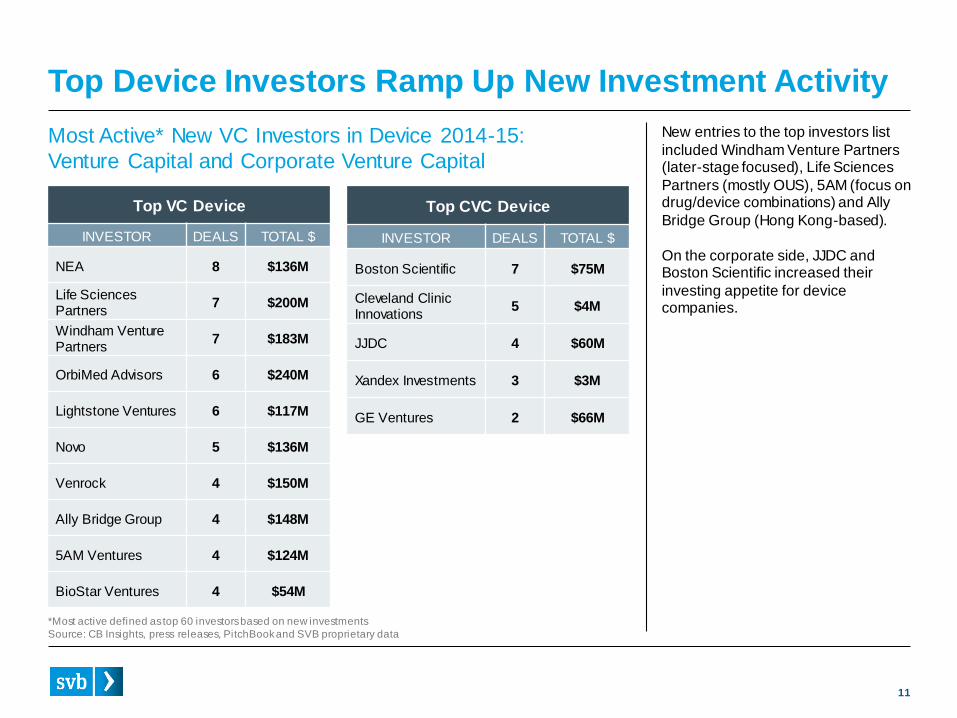

Top Device Investors Ramp Up New Investment Activity

Top VC Device

INVESTOR DEALS TOTAL $

NEA 8 $136M

Life Sciences Partners

7 $200M

Windham Venture Partners

7 $183M

OrbiMed Advisors 6 $240M

Lightstone Ventures 6 $117M

Novo 5 $136M

Venrock 4 $150M

Ally Bridge Group 4 $148M

5AM Ventures 4 $124M

BioStar Ventures 4 $54M

Top CVC Device

INVESTOR DEALS TOTAL $

Boston Scientific 7 $75M

Cleveland Clinic Innovations

5 $4M

JJDC 4 $60M

Xandex Investments 3 $3M

GE Ventures 2 $66M

Most Active* New VC Investors in Device 2014-15:

Venture Capital and Corporate Venture Capital

New entries to the top investors list

included Windham Venture Partners (later-stage focused), Life Sciences

Partners (mostly OUS), 5AM (focus on drug/device combinations) and Ally

Bridge Group (Hong Kong-based).

On the corporate side, JJDC and Boston Scientific increased their

investing appetite for device companies.

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

12

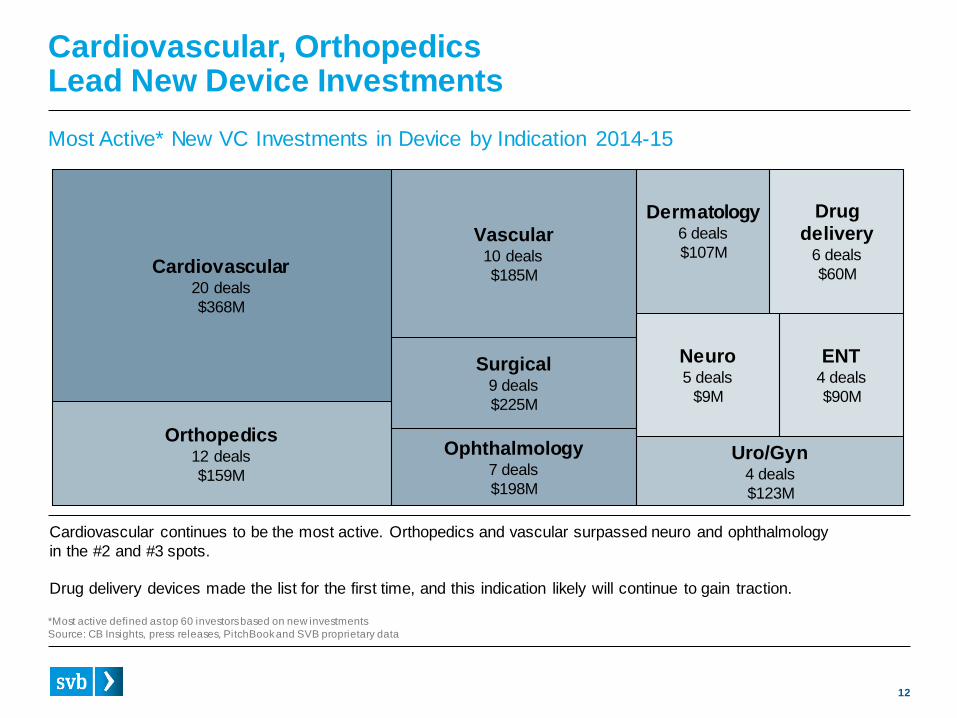

Cardiovascular continues to be the most active. Orthopedics and vascular surpassed neuro and ophthalmology

in the #2 and #3 spots.

Drug delivery devices made the list for the first time, and this indication likely will continue to gain traction.

Cardiovascular, OrthopedicsLead New Device Investments

Most Active* New VC Investments in Device by Indication 2014-15

Cardiovascular20 deals

$368M

Orthopedics12 deals

$159M

Dermatology6 deals

$107M

Drug delivery

6 deals

$60M

Vascular10 deals

$185M

Surgical9 deals

$225M

Ophthalmology7 deals

$198M

Uro/Gyn4 deals

$123M

Neuro5 deals

$9M

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

ENT4 deals

$90M

13

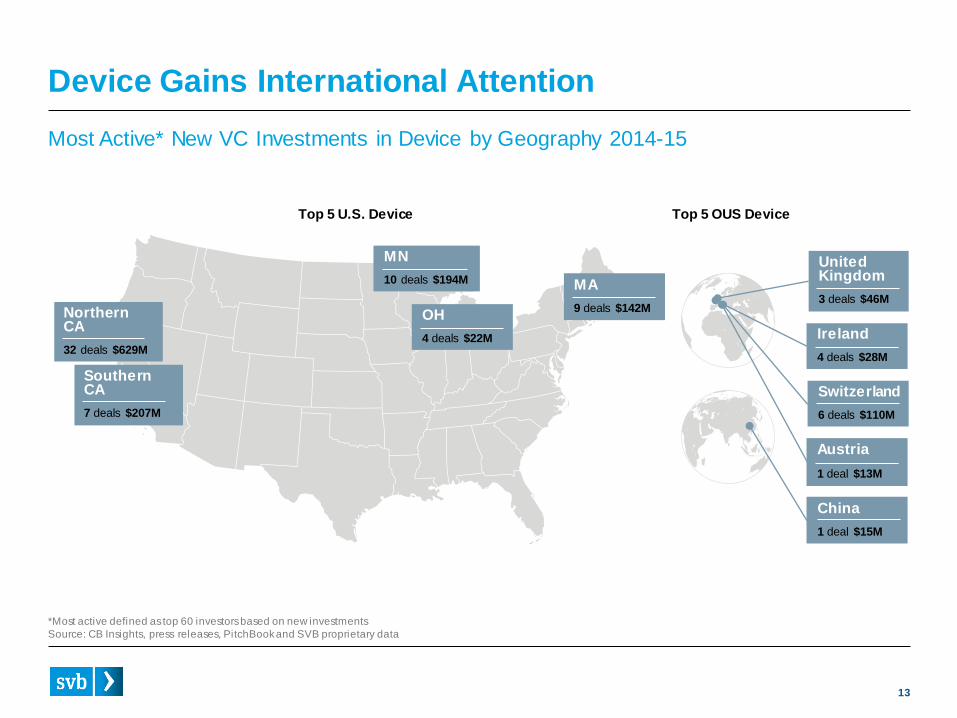

Device Gains International Attention

Most Active* New VC Investments in Device by Geography 2014-15

Top 5 U.S. Device Top 5 OUS Device

NorthernCA

32 deals $629M

SouthernCA

7 deals $207M

MN

10 deals $194M

OH

4 deals $22M

MA

9 deals $142M

United Kingdom

3 deals $46M

Ireland

4 deals $28M

Switzerland

6 deals $110M

Austria

1 deal $13M

China

1 deal $15M

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

14

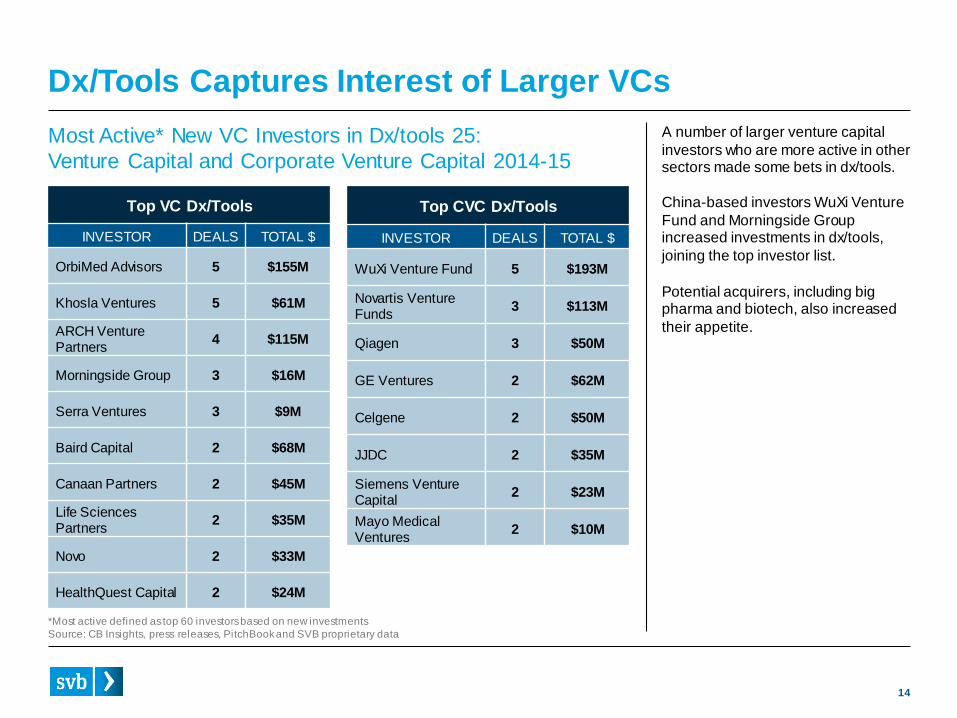

Top CVC Dx/Tools

INVESTOR DEALS TOTAL $

WuXi Venture Fund 5 $193M

Novartis Venture Funds

3 $113M

Qiagen 3 $50M

GE Ventures 2 $62M

Celgene 2 $50M

JJDC 2 $35M

Siemens Venture Capital

2 $23M

Mayo Medical Ventures

2 $10M

Dx/Tools Captures Interest of Larger VCs

Top VC Dx/Tools

INVESTOR DEALS TOTAL $

OrbiMed Advisors 5 $155M

Khosla Ventures 5 $61M

ARCH Venture Partners

4 $115M

Morningside Group 3 $16M

Serra Ventures 3 $9M

Baird Capital 2 $68M

Canaan Partners 2 $45M

Life SciencesPartners

2 $35M

Novo 2 $33M

HealthQuest Capital 2 $24M

Most Active* New VC Investors in Dx/tools 25:

Venture Capital and Corporate Venture Capital 2014-15

A number of larger venture capital

investors who are more active in other sectors made some bets in dx/tools.

China-based investors WuXi Venture

Fund and Morningside Group increased investments in dx/tools,

joining the top investor list.

Potential acquirers, including big pharma and biotech, also increased

their appetite.

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

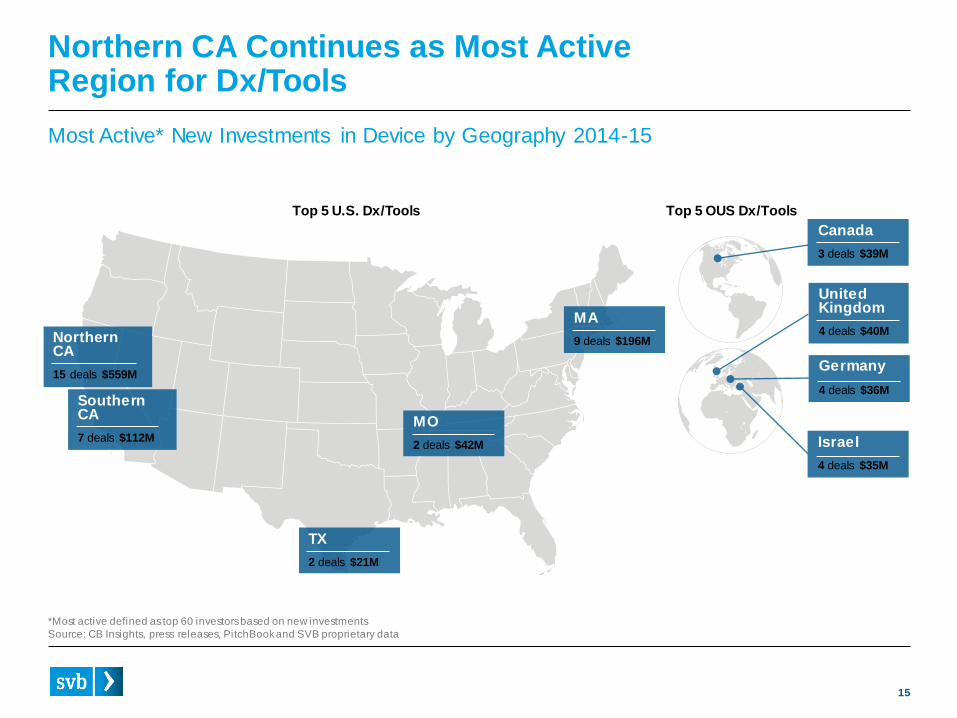

15

Canada

3 deals $39M

United Kingdom

4 deals $40M

Northern CA Continues as Most Active Region for Dx/Tools

Top 5 U.S. Dx/Tools Top 5 OUS Dx/Tools

Most Active* New Investments in Device by Geography 2014-15

NorthernCA

15 deals $559M

SouthernCA

7 deals $112M

TX

2 deals $21M

MO

2 deals $42M

MA

9 deals $196M

Germany

4 deals $36M

Israel

4 deals $35M

*Most active defined as top 60 investors based on new investments

Source: CB Insights, press releases, PitchBook and SVB proprietary data

16

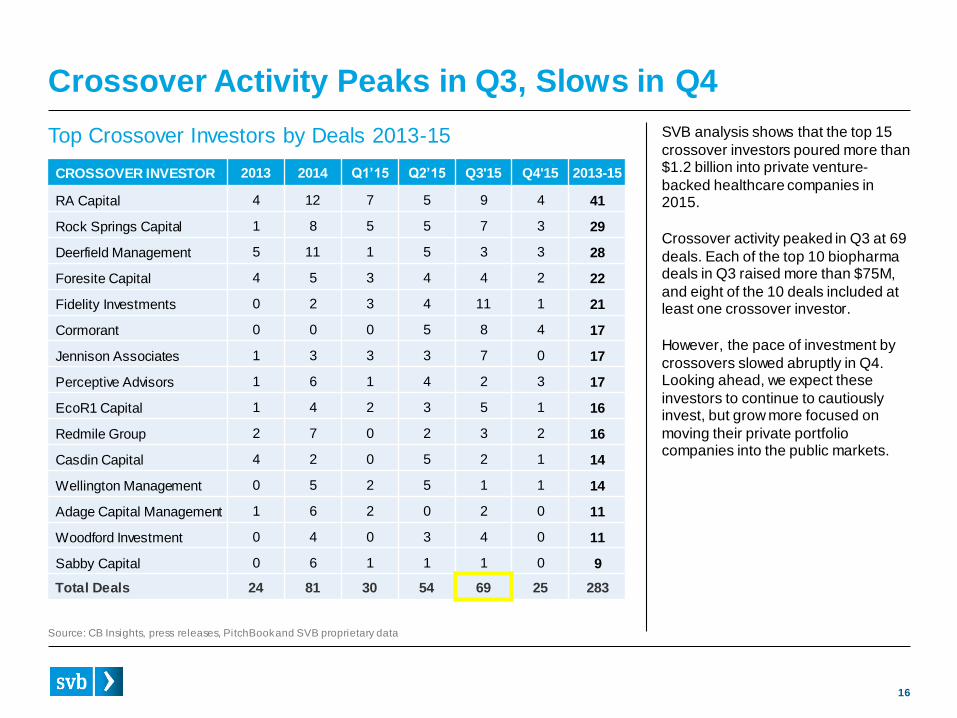

Crossover Activity Peaks in Q3, Slows in Q4

CROSSOVER INVESTOR 2013 2014 Q1’15 Q2’15 Q3'15 Q4'15 2013-15

RA Capital 4 12 7 5 9 4 41

Rock Springs Capital 1 8 5 5 7 3 29

Deerfield Management 5 11 1 5 3 3 28

Foresite Capital 4 5 3 4 4 2 22

Fidelity Investments 0 2 3 4 11 1 21

Cormorant 0 0 0 5 8 4 17

Jennison Associates 1 3 3 3 7 0 17

Perceptive Advisors 1 6 1 4 2 3 17

EcoR1 Capital 1 4 2 3 5 1 16

Redmile Group 2 7 0 2 3 2 16

Casdin Capital 4 2 0 5 2 1 14

Wellington Management 0 5 2 5 1 1 14

Adage Capital Management 1 6 2 0 2 0 11

Woodford Investment 0 4 0 3 4 0 11

Sabby Capital 0 6 1 1 1 0 9

Total Deals 24 81 30 54 69 25 283

Top Crossover Investors by Deals 2013-15 SVB analysis shows that the top 15

crossover investors poured more than $1.2 billion into private venture-

backed healthcare companies in 2015.

Crossover activity peaked in Q3 at 69

deals. Each of the top 10 biopharma deals in Q3 raised more than $75M,

and eight of the 10 deals included at least one crossover investor.

However, the pace of investment by

crossovers slowed abruptly in Q4. Looking ahead, we expect these

investors to continue to cautiously invest, but grow more focused on

moving their private portfolio companies into the public markets.

Source: CB Insights, press releases, PitchBook and SVB proprietary data

17

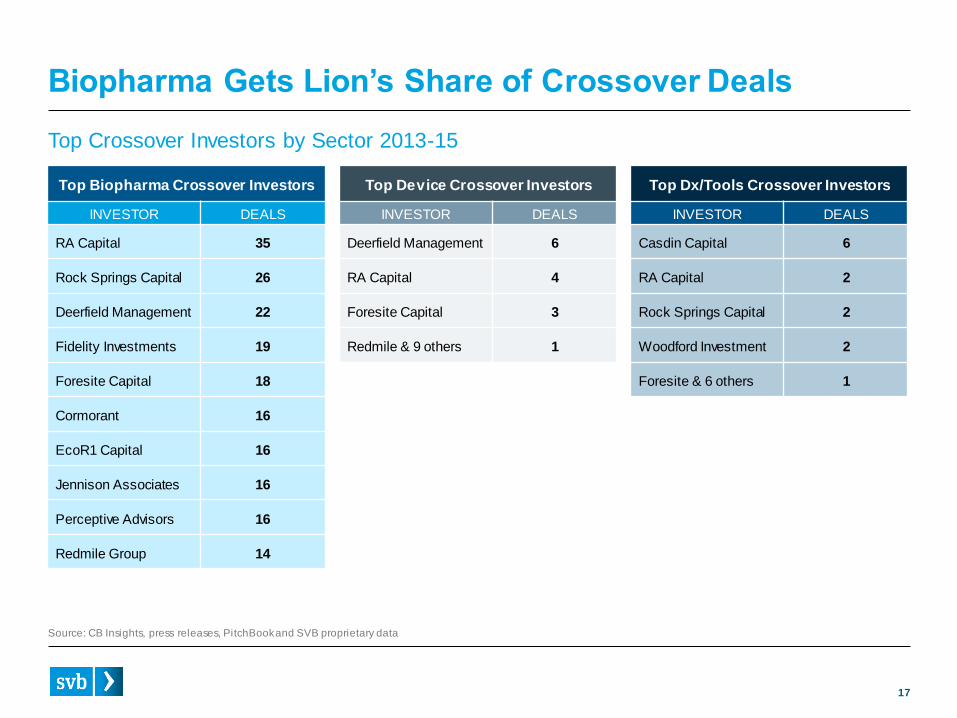

Biopharma Gets Lion’s Share of Crossover Deals

Top Crossover Investors by Sector 2013-15

Source: CB Insights, press releases, PitchBook and SVB proprietary data

Top Biopharma Crossover Investors

INVESTOR DEALS

RA Capital 35

Rock Springs Capital 26

Deerfield Management 22

Fidelity Investments 19

Foresite Capital 18

Cormorant 16

EcoR1 Capital 16

Jennison Associates 16

Perceptive Advisors 16

Redmile Group 14

Top Device Crossover Investors

INVESTOR DEALS

Deerfield Management 6

RA Capital 4

Foresite Capital 3

Redmile & 9 others 1

Top Dx/Tools Crossover Investors

INVESTOR DEALS

Casdin Capital 6

RA Capital 2

Rock Springs Capital 2

Woodford Investment 2

Foresite & 6 others 1

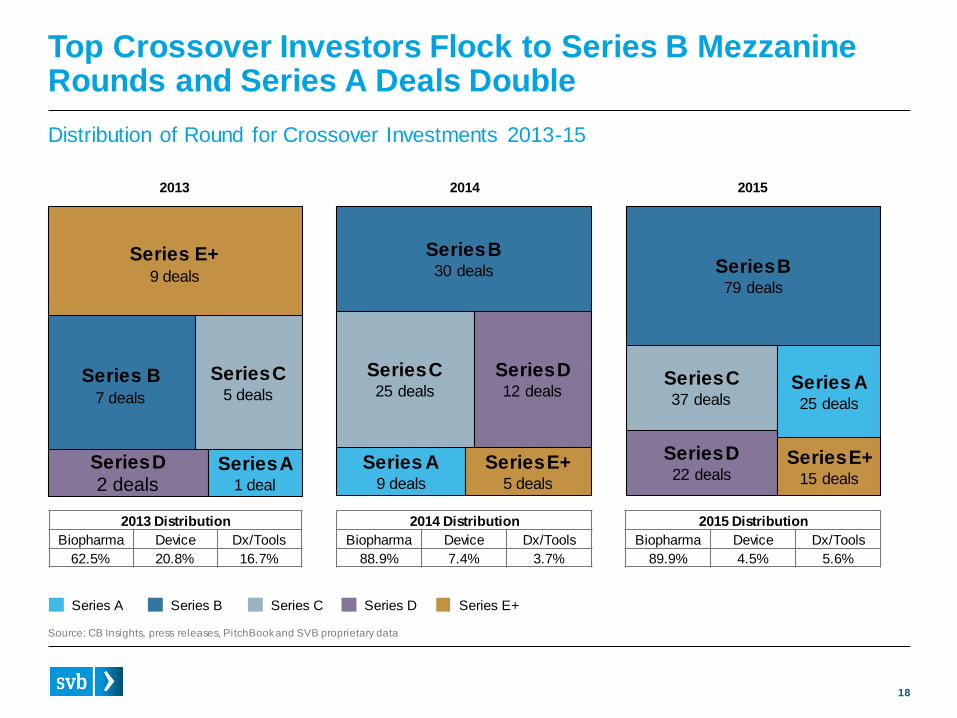

18

Series B30 deals

Series C25 deals

Series D12 deals

Series A9 deals

Series E+5 deals

Series E+9 deals

Series B7 deals

Series C5 deals

Series D2 deals

Series A1 deal

Top Crossover Investors Flock to Series B Mezzanine Rounds and Series A Deals Double

Distribution of Round for Crossover Investments 2013-15

Source: CB Insights, press releases, PitchBook and SVB proprietary data

2013 Distribution

Biopharma Device Dx/Tools

62.5% 20.8% 16.7%

2014 Distribution

Biopharma Device Dx/Tools

88.9% 7.4% 3.7%

2015 Distribution

Biopharma Device Dx/Tools

89.9% 4.5% 5.6%

2013

Series B79 deals

Series D22 deals

Series C37 deals

Series A25 deals

Series E+15 deals

2014 2015

Series A Series B Series C Series D Series E+

19

Healthcare Venture Exits:M&A Climate Improves as IPOs Slow

20

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2009 2010 2011 2012 2013 2014 2015

To

tal V

alu

e ($ B

illi

on

s)

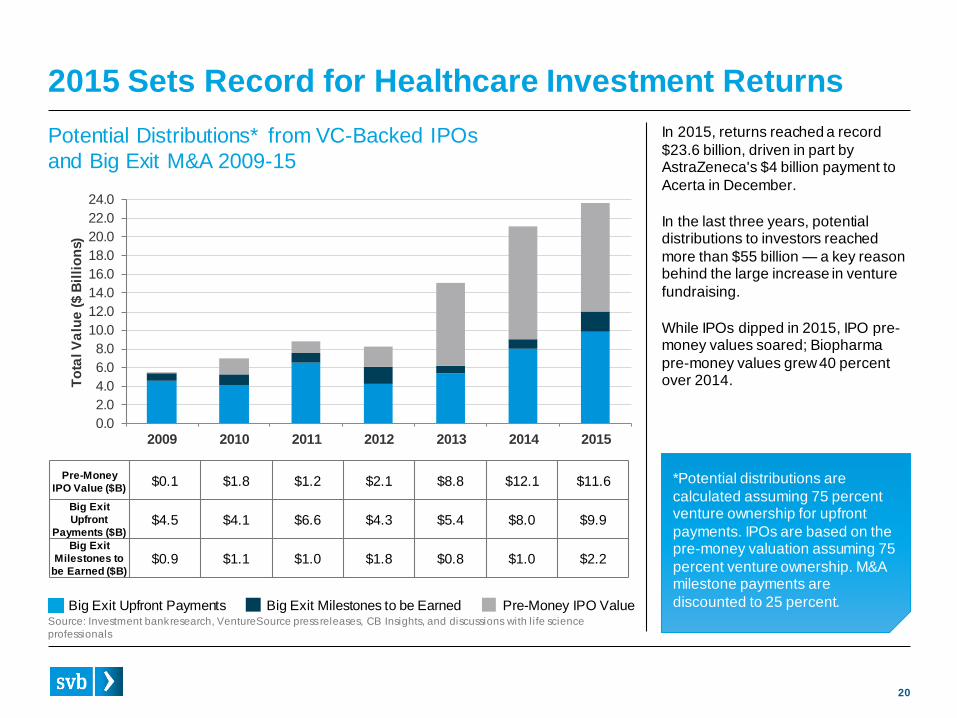

2015 Sets Record for Healthcare Investment Returns

Pre-Money

IPO Value ($B)$0.1 $1.8 $1.2 $2.1 $8.8 $12.1 $11.6

Big Exit

Upfront

Payments ($B)$4.5 $4.1 $6.6 $4.3 $5.4 $8.0 $9.9

Big Exit

Milestones to

be Earned ($B)$0.9 $1.1 $1.0 $1.8 $0.8 $1.0 $2.2

Pre-Money IPO ValueBig Exit Milestones to be EarnedBig Exit Upfront PaymentsSource: Investment bank research, VentureSource press releases, CB Insights, and discussions with life science

professionals

Potential Distributions* from VC-Backed IPOs

and Big Exit M&A 2009-15

In 2015, returns reached a record

$23.6 billion, driven in part by AstraZeneca's $4 billion payment to

Acerta in December.

In the last three years, potential distributions to investors reached

more than $55 billion — a key reason behind the large increase in venture

fundraising.

While IPOs dipped in 2015, IPO pre-money values soared; Biopharma

pre-money values grew 40 percent over 2014.

*Potential distributions are

calculated assuming 75 percent venture ownership for upfront

payments. IPOs are based on the pre-money valuation assuming 75

percent venture ownership. M&A milestone payments are

discounted to 25 percent.

21

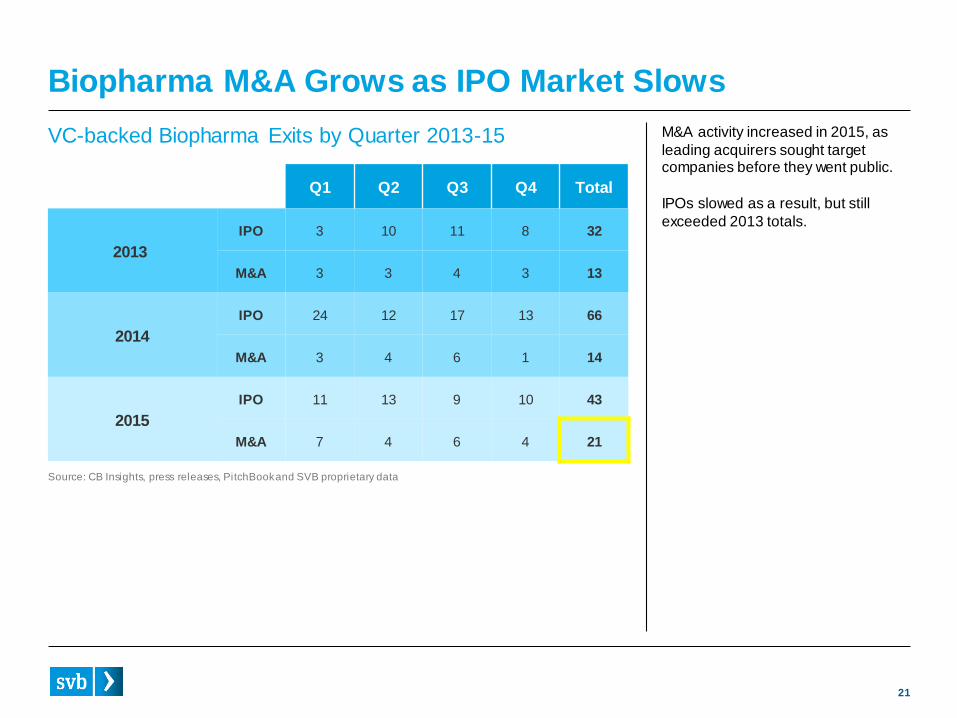

Biopharma M&A Grows as IPO Market Slows

Q1 Q2 Q3 Q4 Total

2013

IPO 3 10 11 8 32

M&A 3 3 4 3 13

2014

IPO 24 12 17 13 66

M&A 3 4 6 1 14

2015

IPO 11 13 9 10 43

M&A 7 4 6 4 21

VC-backed Biopharma Exits by Quarter 2013-15 M&A activity increased in 2015, as

leading acquirers sought target companies before they went public.

IPOs slowed as a result, but still

exceeded 2013 totals.

Source: CB Insights, press releases, PitchBook and SVB proprietary data

22

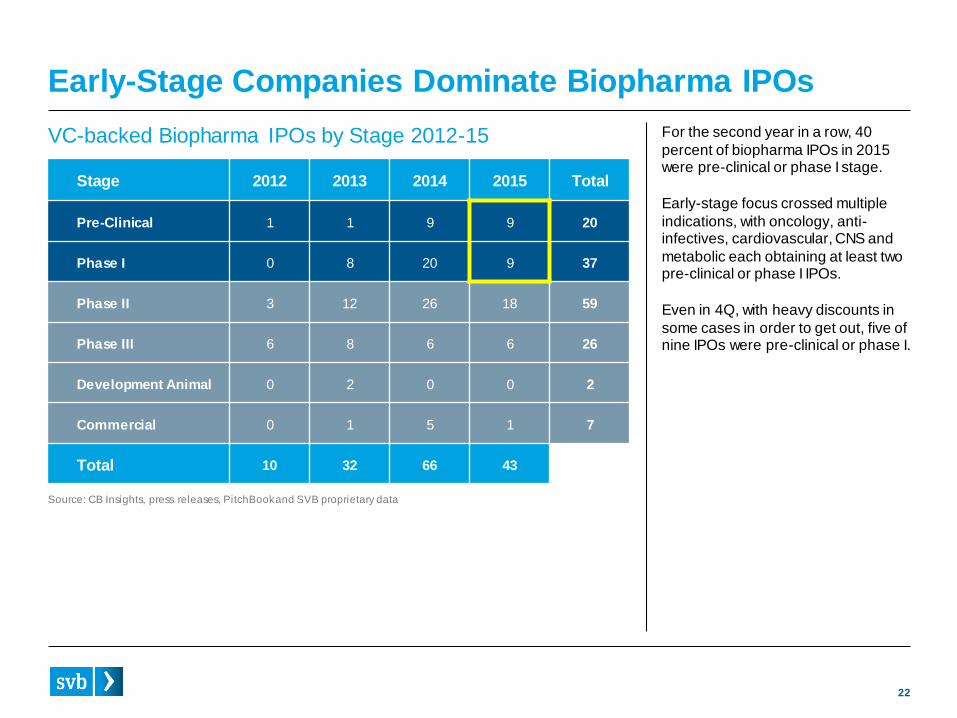

Early-Stage Companies Dominate Biopharma IPOs

VC-backed Biopharma IPOs by Stage 2012-15 For the second year in a row, 40

percent of biopharma IPOs in 2015 were pre-clinical or phase I stage.

Early-stage focus crossed multiple

indications, with oncology, anti-infectives, cardiovascular, CNS and

metabolic each obtaining at least two pre-clinical or phase I IPOs.

Even in 4Q, with heavy discounts in

some cases in order to get out, five of nine IPOs were pre-clinical or phase I.

Stage 2012 2013 2014 2015 Total

Pre-Clinical 1 1 9 9 20

Phase I 0 8 20 9 37

Phase II 3 12 26 18 59

Phase III 6 8 6 6 26

Development Animal 0 2 0 0 2

Commercial 0 1 5 1 7

Total 10 32 66 43

Source: CB Insights, press releases, PitchBook and SVB proprietary data

23

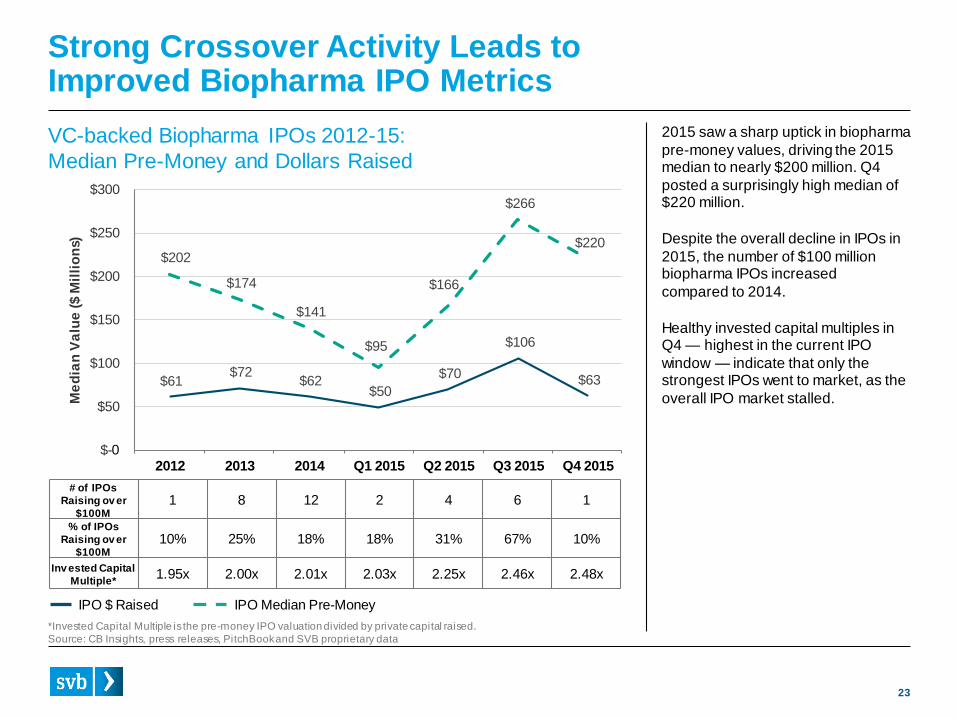

$61 $72

$62 $50

$70

$106

$63

$202

$174

$141

$95

$166

$266

$220

$-

$50

$100

$150

$200

$250

$300

2012 2013 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Me

dia

n V

alu

e ($ M

illi

on

s)

2015 saw a sharp uptick in biopharma

pre-money values, driving the 2015 median to nearly $200 million. Q4

posted a surprisingly high median of $220 million.

Despite the overall decline in IPOs in

2015, the number of $100 million biopharma IPOs increased

compared to 2014.

Healthy invested capital multiples in Q4 — highest in the current IPO

window — indicate that only the strongest IPOs went to market, as the

overall IPO market stalled.

Strong Crossover Activity Leads toImproved Biopharma IPO Metrics

# of IPOs

Raising ov er

$100M1 8 12 2 4 6 1

% of IPOs

Raising ov er

$100M10% 25% 18% 18% 31% 67% 10%

Inv ested Capital

Multiple*1.95x 2.00x 2.01x 2.03x 2.25x 2.46x 2.48x

*Invested Capital Multiple is the pre-money IPO valuation divided by private capital raised.

Source: CB Insights, press releases, PitchBook and SVB proprietary data

VC-backed Biopharma IPOs 2012-15:

Median Pre-Money and Dollars Raised

0

IPO $ Raised IPO Median Pre-Money

24

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

# o

f B

ig E

xit

s

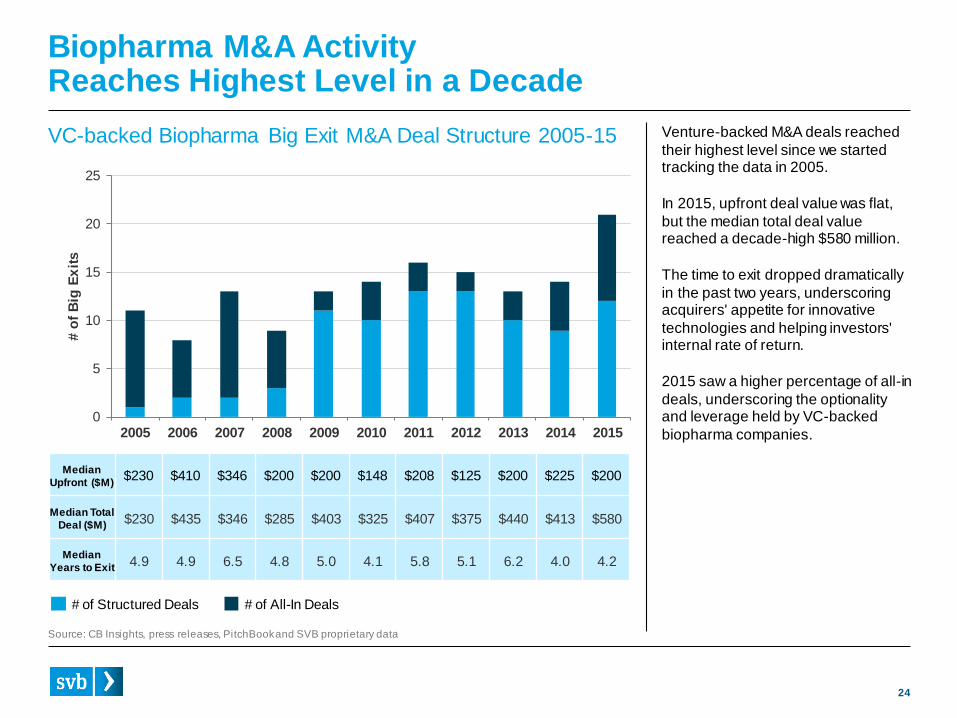

Biopharma M&A Activity Reaches Highest Level in a Decade

# of Structured Deals # of All-In Deals

Median

Upfront ($M)$230 $410 $346 $200 $200 $148 $208 $125 $200 $225 $200

Median Total

Deal ($M)$230 $435 $346 $285 $403 $325 $407 $375 $440 $413 $580

Median

Years to Exit4.9 4.9 6.5 4.8 5.0 4.1 5.8 5.1 6.2 4.0 4.2

Source: CB Insights, press releases, PitchBook and SVB proprietary data

VC-backed Biopharma Big Exit M&A Deal Structure 2005-15 Venture-backed M&A deals reached

their highest level since we started tracking the data in 2005.

In 2015, upfront deal value was flat,

but the median total deal value reached a decade-high $580 million.

The time to exit dropped dramatically

in the past two years, underscoring acquirers' appetite for innovative

technologies and helping investors' internal rate of return.

2015 saw a higher percentage of all-in

deals, underscoring the optionality and leverage held by VC-backed

biopharma companies.

25

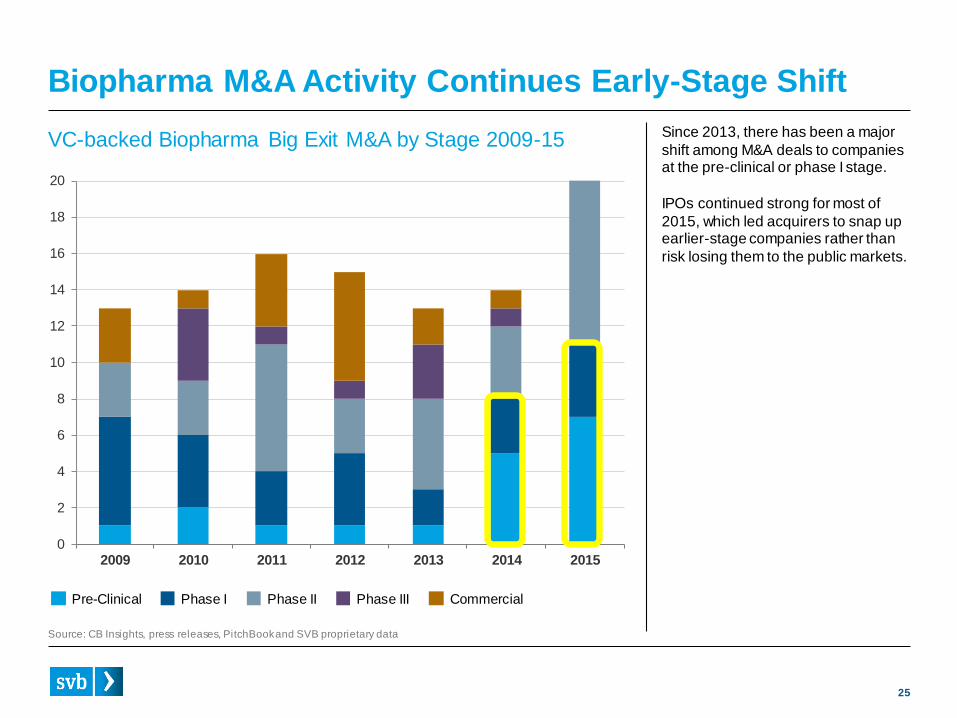

Biopharma M&A Activity Continues Early-Stage Shift

VC-backed Biopharma Big Exit M&A by Stage 2009-15

Pre-Clinical Phase I Phase II Phase III Commercial

Source: CB Insights, press releases, PitchBook and SVB proprietary data

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 2015

Since 2013, there has been a major

shift among M&A deals to companies at the pre-clinical or phase I stage.

IPOs continued strong for most of

2015, which led acquirers to snap up earlier-stage companies rather than

risk losing them to the public markets.

26

0

1

2

3

4

5

2013 2014 2015

# o

f B

ig E

xit

s

Oncology

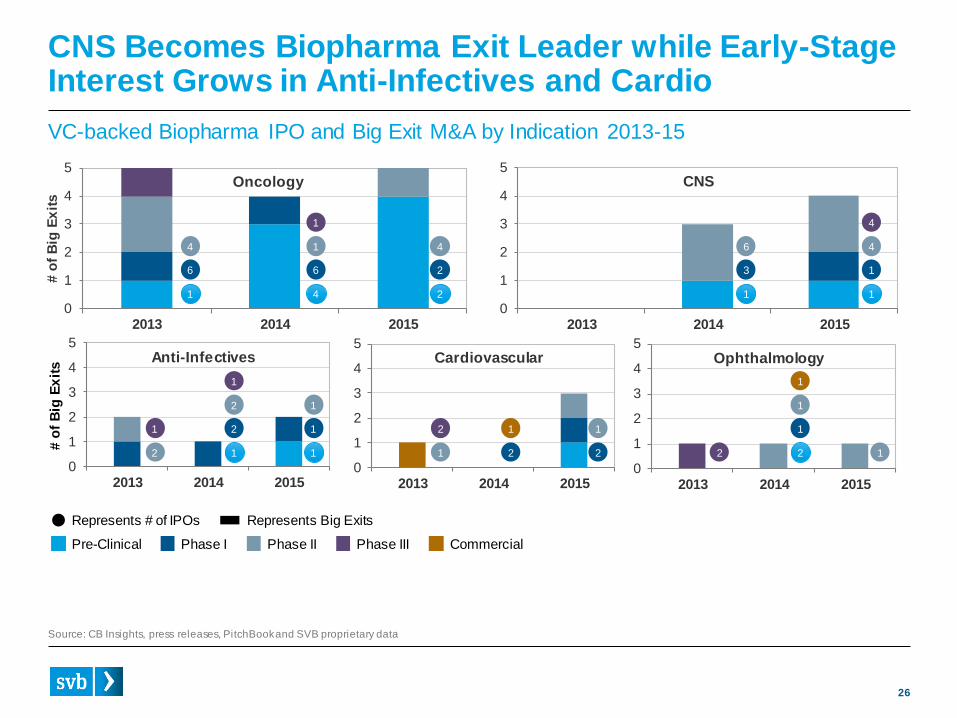

CNS Becomes Biopharma Exit Leader while Early-Stage Interest Grows in Anti-Infectives and Cardio

Source: CB Insights, press releases, PitchBook and SVB proprietary data

0

1

2

3

4

5

2013 2014 2015

CNS

0

1

2

3

4

5

2013 2014 2015

Anti-Infectives

0

1

2

3

4

5

2013 2014 2015

Cardiovascular

0

1

2

3

4

5

2013 2014 2015

Ophthalmology

VC-backed Biopharma IPO and Big Exit M&A by Indication 2013-15

Pre-Clinical Phase I Phase II Phase III Commercial

Represents # of IPOs Represents Big Exits

1

6

4

4

6

1

1

2

2

4

1

3

6

1

1

4

4

2

1

1

2

2

1

1

1

1

1

2

2

1

2

1

2 2

1

1

1

1

# o

f B

ig E

xit

s

27

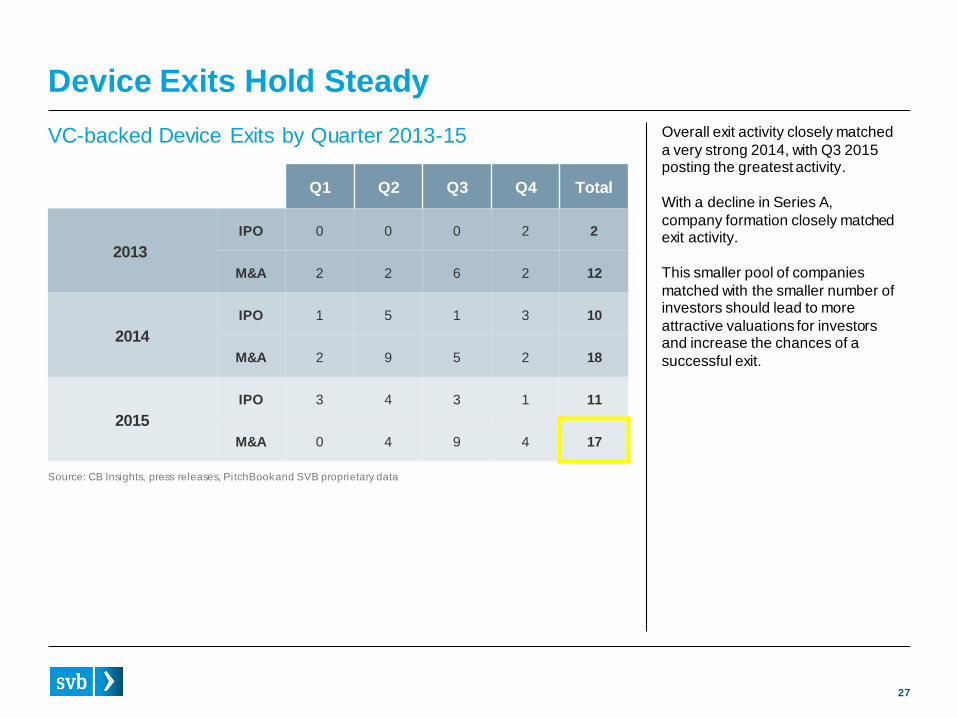

Device Exits Hold Steady

Q1 Q2 Q3 Q4 Total

2013

IPO 0 0 0 2 2

M&A 2 2 6 2 12

2014

IPO 1 5 1 3 10

M&A 2 9 5 2 18

2015

IPO 3 4 3 1 11

M&A 0 4 9 4 17

VC-backed Device Exits by Quarter 2013-15 Overall exit activity closely matched

a very strong 2014, with Q3 2015 posting the greatest activity.

With a decline in Series A,

company formation closely matched exit activity.

This smaller pool of companies

matched with the smaller number of investors should lead to more

attractive valuations for investors and increase the chances of a

successful exit.

Source: CB Insights, press releases, PitchBook and SVB proprietary data

28

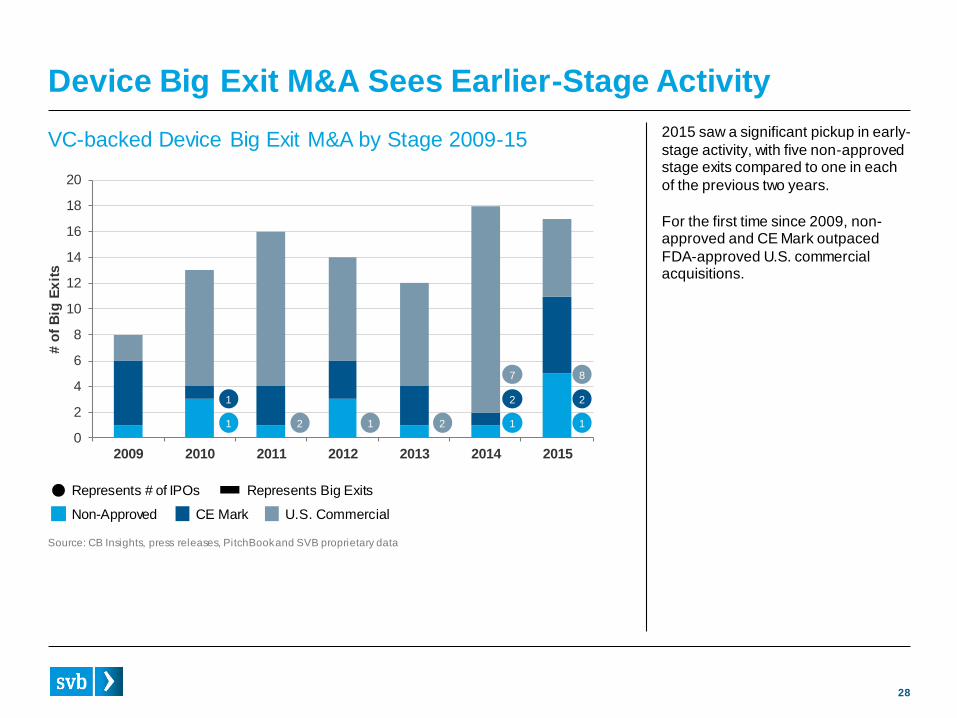

Device Big Exit M&A Sees Earlier-Stage Activity

Non-Approved CE Mark U.S. Commercial

Source: CB Insights, press releases, PitchBook and SVB proprietary data

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 2015

# o

f B

ig E

xit

s

Represents # of IPOs Represents Big Exits

1

1

2 1 2 1

2

7

1

2

8

VC-backed Device Big Exit M&A by Stage 2009-15 2015 saw a significant pickup in early-

stage activity, with five non-approved stage exits compared to one in each

of the previous two years.

For the first time since 2009, non-approved and CE Mark outpaced

FDA-approved U.S. commercial acquisitions.

29

0

2

4

6

8

10

12

14

16

18

20

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

# o

f E

xit

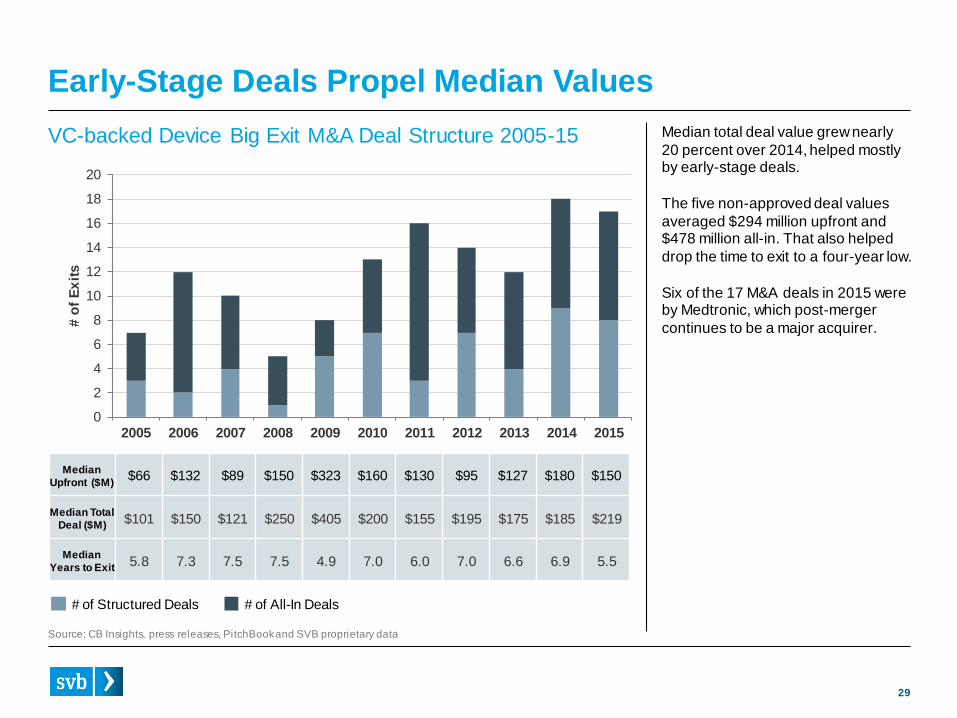

sEarly-Stage Deals Propel Median Values

Source: CB Insights, press releases, PitchBook and SVB proprietary data

VC-backed Device Big Exit M&A Deal Structure 2005-15 Median total deal value grew nearly

20 percent over 2014, helped mostly by early-stage deals.

The five non-approved deal values

averaged $294 million upfront and $478 million all-in. That also helped

drop the time to exit to a four-year low.

Six of the 17 M&A deals in 2015 were by Medtronic, which post-merger

continues to be a major acquirer.

Median

Upfront ($M)$66 $132 $89 $150 $323 $160 $130 $95 $127 $180 $150

Median Total

Deal ($M)$101 $150 $121 $250 $405 $200 $155 $195 $175 $185 $219

Median

Years to Exit5.8 7.3 7.5 7.5 4.9 7.0 6.0 7.0 6.6 6.9 5.5

# of Structured Deals # of All-In Deals

30

0

1

2

3

4

5

6

7

8

9

10

11

# o

f C

om

pa

nie

s

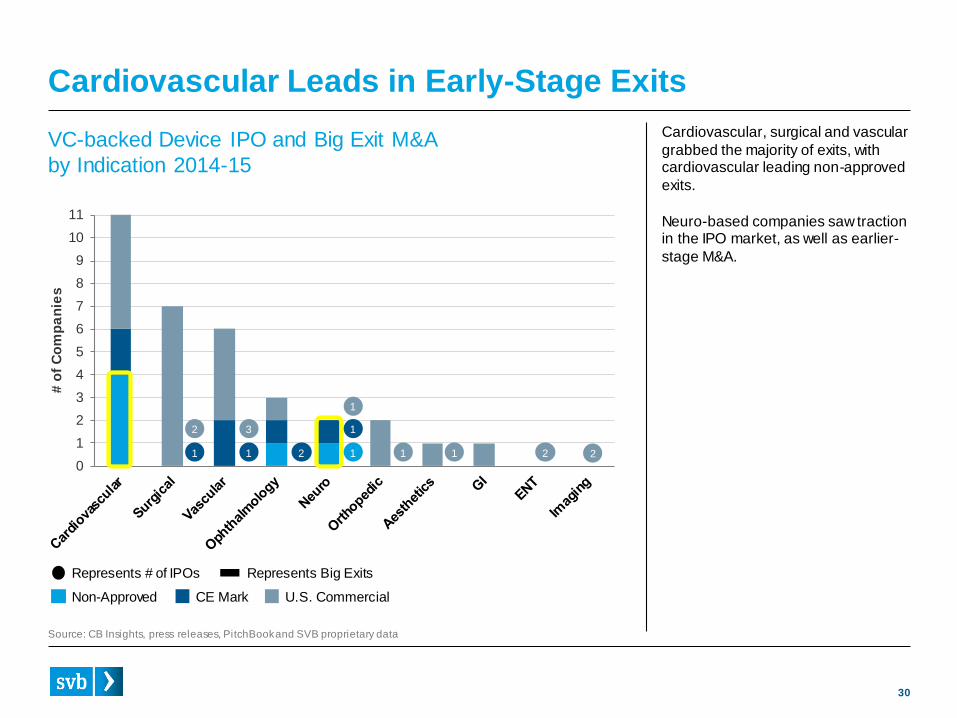

Cardiovascular Leads in Early-Stage Exits

VC-backed Device IPO and Big Exit M&A

by Indication 2014-15

Source: CB Insights, press releases, PitchBook and SVB proprietary data

1

2

Cardiovascular, surgical and vascular

grabbed the majority of exits, with cardiovascular leading non-approved

exits.

Neuro-based companies saw traction in the IPO market, as well as earlier-

stage M&A.

Non-Approved CE Mark U.S. Commercial

Represents # of IPOs Represents Big Exits

1

3

2 1

1

1

1 1 2 2

31

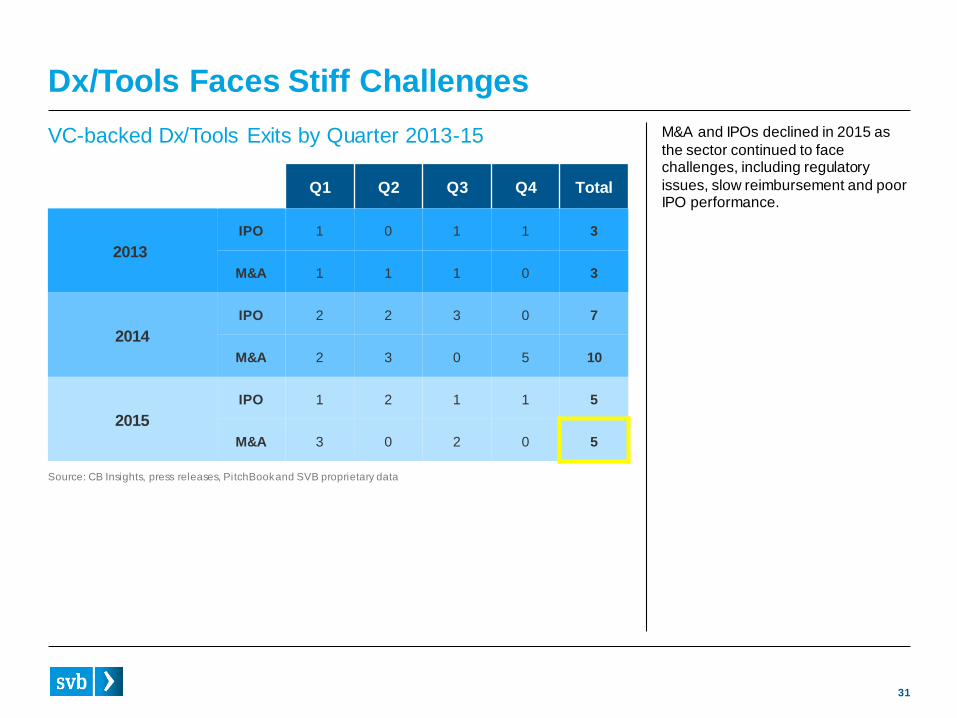

Dx/Tools Faces Stiff Challenges

Q1 Q2 Q3 Q4 Total

2013

IPO 1 0 1 1 3

M&A 1 1 1 0 3

2014

IPO 2 2 3 0 7

M&A 2 3 0 5 10

2015

IPO 1 2 1 1 5

M&A 3 0 2 0 5

VC-backed Dx/Tools Exits by Quarter 2013-15 M&A and IPOs declined in 2015 as

the sector continued to face challenges, including regulatory

issues, slow reimbursement and poor IPO performance.

Source: CB Insights, press releases, PitchBook and SVB proprietary data

32

0

1

2

3

4

5

6

7

8

9

10

2009 2010 2011 2012 2013 2014 2015

# o

f C

om

pa

nie

s

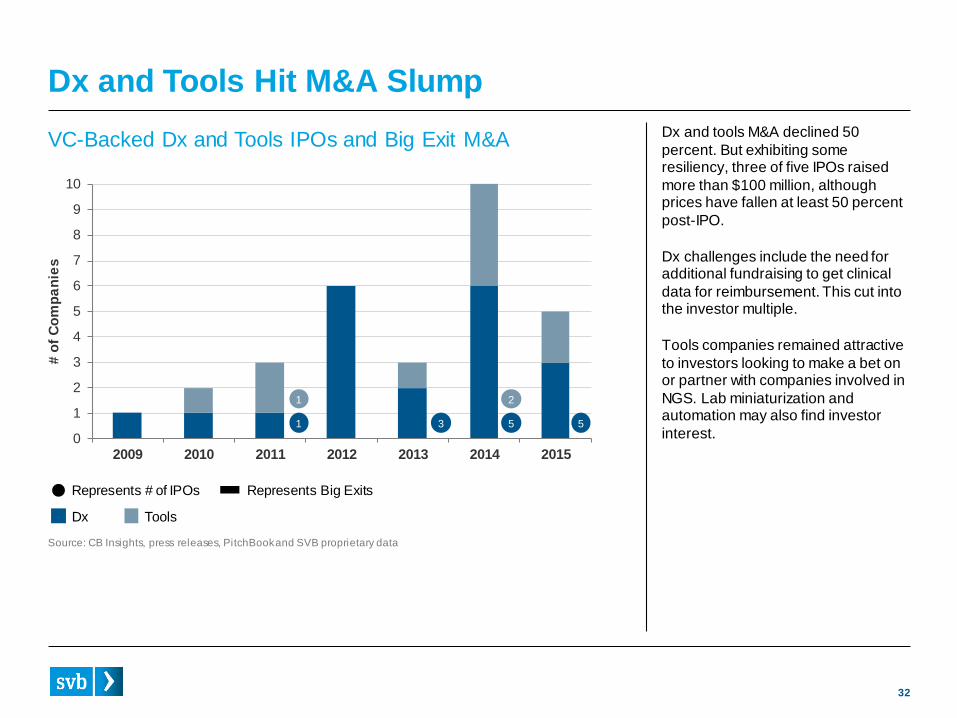

Dx and Tools Hit M&A Slump

Dx Tools

Source: CB Insights, press releases, PitchBook and SVB proprietary data

Represents # of IPOs Represents Big Exits

1

1

3 5

2

5

VC-Backed Dx and Tools IPOs and Big Exit M&A Dx and tools M&A declined 50

percent. But exhibiting some resiliency, three of five IPOs raised

more than $100 million, although prices have fallen at least 50 percent

post-IPO.

Dx challenges include the need for additional fundraising to get clinical

data for reimbursement. This cut into the investor multiple.

Tools companies remained attractive

to investors looking to make a bet on or partner with companies involved in

NGS. Lab miniaturization and automation may also find investor

interest.

33

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013 2014 2015

# o

f E

xit

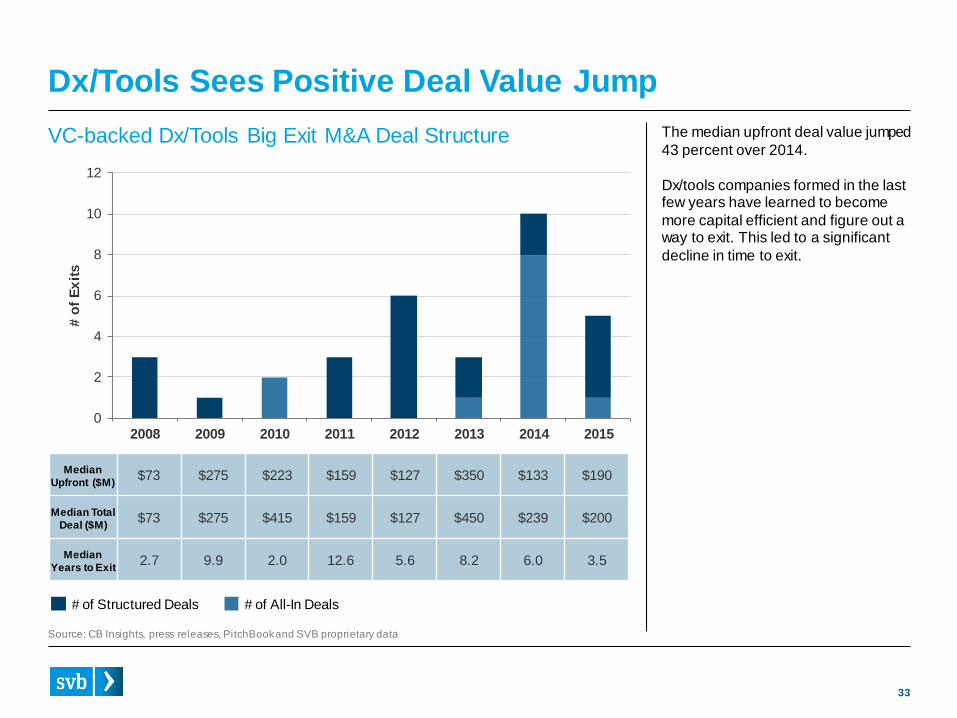

sDx/Tools Sees Positive Deal Value Jump

Source: CB Insights, press releases, PitchBook and SVB proprietary data

VC-backed Dx/Tools Big Exit M&A Deal Structure The median upfront deal value jumped

43 percent over 2014.

Dx/tools companies formed in the last few years have learned to become

more capital efficient and figure out a way to exit. This led to a significant

decline in time to exit.

Median

Upfront ($M)$73 $275 $223 $159 $127 $350 $133 $190

Median Total

Deal ($M)$73 $275 $415 $159 $127 $450 $239 $200

Median

Years to Exit2.7 9.9 2.0 12.6 5.6 8.2 6.0 3.5

# of Structured Deals # of All-In Deals

34

2016 Outlook: 2015 Will Be a Hard Act to Follow

As 2015 closed, we saw some decline in exit activity and investor interest that indicate things are slowing.

Here are our predictions for 2016:

• Investment levels are poised to decline as crossover investors pull back from involvement in large mezzanine

biopharma rounds and traditional investors slow their investment pace.

• Fundraising, too, will fall off as most investors in this “up-cycle” have already raised new funds.

• Series A investments in biopharma will drop slightly, but device may see an uptick to take advantage of the healthy

ratio of Series A companies to exits. Dx/tools likely will stabilize after a challenging 2015.

• The biopharma IPO window should remain open, but there will be fewer IPOs, about seven to eight per quarter in

2016. As a result, M&A will continue on pace as acquirers seek biopharma companies to replenish their pipeline,

and high-fliers from the IPO boom now become acquirers.

• Device IPO activity will decline. But as the pool of private device companies shrinks and acquirers look to innovate,

M&A activity will likely remain stable. We believe this will lead to increased deal values and returns to investors.

We anticipate continued acquisition flurries, similar to Q3 2015, as acquirers are pressured to innovate.

• Dx/tools IPO activity will be difficult given ongoing challenges. M&A should pick up, and will include a mix of

commercial stage companies without enough revenue to be IPO candidates and emerging tool companies that are

able to leverage NGS, lab miniaturization and automation innovations.

35

Glossary

Big Exit

Big Exits are defined as private, venture-backed merger and acquisition transactions in which the upfront payment is $75 million or more for biopharma deals and $50 million or more for device and dx/tools deals.

Initial Public Offering

IPO defined as venture-backed company raising IPO proceeds more than $25 million.

Deal Descriptions:

• Structured DealThis is a pay-for-performance system that pays some of the consideration upfront, but sets milestones in development that must be achieved before the full value of the transaction will be realized.

• All-in DealAll consideration for the deal is paid when deal closes.

• Big Exit Upfront PaymentsThe upfront payment refers to payments in a structured deal that are made at the close of the deal; it does not include milestones.

• Big Exit Milestones to be EarnedThe milestones to be earned refer to payments in a structured deal that are made after the pre-determined goals are met.

• Total Deal ValueThe total deal value of a structured deal includes both the upfront payment and the milestones to be earned.

Regulatory Definitions:

• Non-approvedNon-approved refers to a device company that has no regulatory approval for its product.

• CE MarkCE Mark refers to a device company that has a CE Mark-only product. CE Mark is a European Union designation that is less difficult to obtain than FDA approval, and the approval process typically has a faster timeline.

• U.S. CommercialCommercial refers to a device company that has an FDA-approved product, and typically is in commercial stage.

• Series ASeries A companies are defined as U.S. companies raising their first round greater than $2 million in equity or backed by institutional or corporate venture capital.

36

Paul Schuber

Paul Schuber is an associate with SVB Analytics leading valuation engagements

and specializing in the life sciences. Prior to SVB Analytics, Schuber facilitated

clinical trials on behalf of pharmaceutical sponsors and pre-clinical trials to

advance medical school research, which included writing and implementing IRB

and IACUC protocols. Schuber’s healthcare experience also consists of working

as an emergency medical technician and an electrocardiogram technician. He has

a background in technology as well, working in many roles, including chief

technology officer of an e-commerce company.

Schuber earned a master’s degree in the business of bioscience from Keck

Graduate Institute of Applied Life Sciences while also studying at Claremont

McKenna College at the Robert Day School of Economics and Finance.

Authors

Jonathan Norris

Jonathan Norris is a managing director for SVB's Healthcare practice. Norris

oversees business development efforts for banking and lending opportunities as

well as spearheading strategic relationships with many healthcare venture capital

firms. He also helps SVB Capital through sourcing and advising on limited

partnership allocations.

In addition, he speaks at major investor and industry conferences and authors

widely cited analyses of healthcare venture capital trends. Norris has more than

sixteen years of banking experience working with healthcare companies and

venture capital firms. Norris earned a bachelor's degree in business

administration from the University of California, Riverside and a juris doctorate

from Santa Clara University.

Managing Director,

Silicon Valley [email protected]

Valuations Associate,

37

About Silicon Valley Bank

For more than 30 years, Silicon Valley Bank (SVB) has helped innovative companies and their investors

move bold ideas forward, fast. SVB provides targeted financial services and expertise through its offices in

innovation centers around the world. With commercial, international and private banking services, SVB

helps address the unique needs of innovators. Forbes named SVB one of America’s best banks (2015)

and one of America’s best-managed companies (2014). Learn more at svb.com.

This material, including w ithout limitation to the statistical information herein, is provided for informational purposes only. The material is based in part on information from third-party sources that w e believe to be reliable, but w hich have not been independently verif ied by us and for this reason w e do not represent that the information is accurate or complete. The information should not be view ed as tax, investment, legal or other advice nor is it to be relied on in making an investment or other decision. You should obtain relevant and specif ic professional advice before making any investment decision. Nothing re lating to the material should be

construed as a solicitation, offer or recommendation to acquire or dispose of any investment or to engage in any other transaction.

©2016 SVB Financial Group. All rights reserved. Silicon Valley Bank is a member of FDIC and Federal Reserve System. SVB>, SVB Financial Group, and Silicon Valley Bank are registered trademarks.