Embed Size (px)

Citation preview

Trends in Employee BenefitsStraight Talk on where things are going….

Linda Smith & Jodi McMahon• 45 combined years of experience in Employee Benefits• Managing over $80M of 401k assets• Active member of our associations

• American Society of Pension Professionals and Actuaries• National Association of Plan Advisors• National Association of Health Underwriters

Linda Smith and Jodi McMahon are registered representatives and investment advisor representatives with Cambridge Investment Research, Inc. And Cambridge Investment Research Advisors, Inc. A Broker/Dealer, Member FINRA/SIPC. Branch office: 15 Lenox Pointe, Suite A - Atlanta Georgia 30306. 404-733-1350.

Cambridge and BenSource are not affiliates.

The information presented here is confidential. Topics are presented in summary format and are not intended as specific advise for attendees. Contents of this presentation are intended solely for attendees of this meeting and are not authorized for distribution.

Pursuant to IRS Circular 230, The information contained in this presentation is not intended to (and cannot) be used by anyone to avoid IRS penalties. This presentation supports the promotion and marketing of investment products. You should seek advice based on your particular circumstances from an independent tax or legal adviser.

Takeaways

PPACA – what you need to know and do nowHealthcare solutions – the trends and the

tricksWellness programs – do they work?Employee loyalty – what works, what doesn’t

work and what construction employees are seeking

How to ‘skin the cat’ on benefits and…..Dancing

PPACA - aka Obamacare

P atientP rotection andA ffordableC areA ct

PPACA – What you need to be doing NOW

Distributing the Notice of Coverage Options to new employees within 14 days of the employees’ start date.

Determining if your plan meets the minimum thresh hold of actuarial value – typically does if greater than 60%

Determining if you are a “large” employerLarge - employed an average of at least 50 full-time

equivalent (FTE) employees during the preceding calendar year.

Determining your Full-time, part time and seasonal employees and how they add up as fulltime equivalents .

Make your new-hire waiting period uniform – 90 day max Distribute SBCs at renewal and at least annually Examine payroll deductions no more than 9.5% of income for

cost of single coverage.

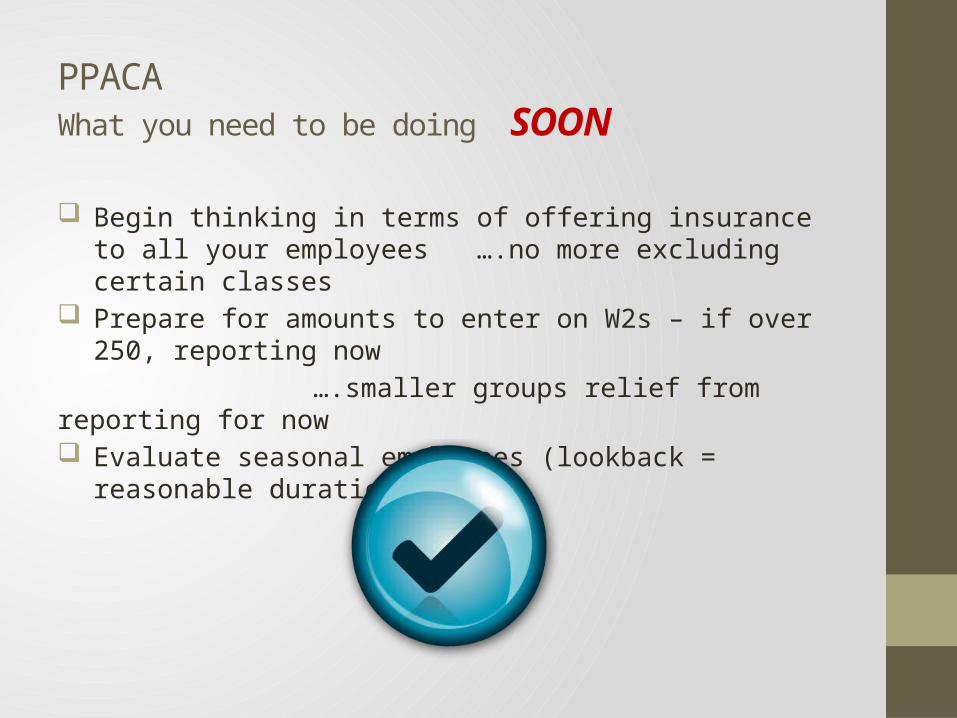

PPACA What you need to be doing SOON

Begin thinking in terms of offering insurance to all your employees ….no more excluding certain classes

Prepare for amounts to enter on W2s – if over 250, reporting now ….smaller groups relief from reporting for now Evaluate seasonal employees (lookback = reasonable duration)

Employer Mandate – aka “pay or play”

Requirement of ‘larger’ businesses to offer health plan with “minimum essential benefits “ or pay penalties. Penalties are based on:- number of full-time employees during the preceding calendar year; - if the firm offers coverage to fulltime employees (30 hours or more) - if coverage is “affordable” and meets “minimum value” - if one or more full-time employees qualify for a federal premium subsidy.

A full-time employee qualifies for a subsidy if :• household income is between 100 -400% of the FPL ($11,500 - $46,000) • employee’s share of the single premium exceeds 9.5% of taxable income. (Box 1, W-2 form) More than 50 FTE employees and the business offers insurance:If one or more full-time employees receives premium subsidies because their share of the self-only portion of the premium exceeds 9.5% of their income. The penalty is the lesser of $3,000 per subsidized FTE or $2,000 per full time employee (in excess of the first 30). More than 50 FTE employees and no insurance – If one or more full time employees receive premium subsidies, penalty is $2000 per employee (in excess of the first 30)

Access to employer-sponsored coverage that is both “affordable” andprovides “minimum value” disqualifies an individual from receiving the subsidy.

Checklist “Minimum essential benefits” (ACA compliant)

Offer coverage to fulltime employees (30 hrs or more)

Coverage is “affordable” (9.5% of income for “single”)

Coverage meets “minimum value” (60% or more)

One or more full-time employees qualify for a federal premium subsidy (will they?)

All ACA laws are subject to change

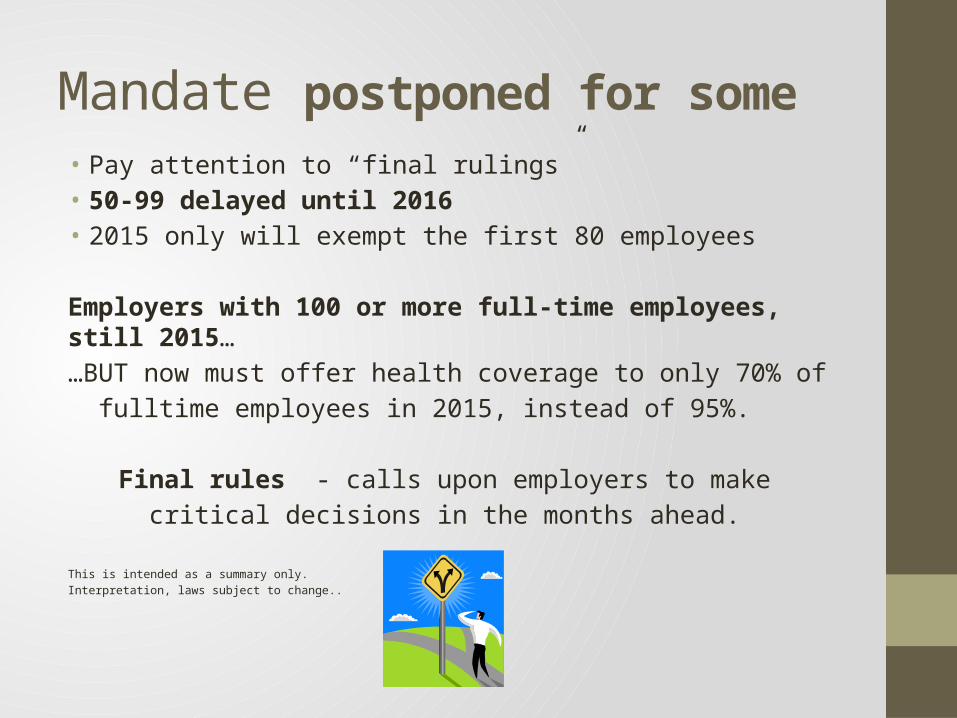

Mandate postponed for some• Pay attention to “final rulings”• 50-99 delayed until 2016• 2015 only will exempt the first 80 employees

Employers with 100 or more full-time employees, still 2015……BUT now must offer health coverage to only 70% of fulltime employees in 2015, instead of 95%.

Final rules - calls upon employers to make critical decisions in the months ahead.

This is intended as a summary only.Interpretation, laws subject to change..

The “under 50” game

Health insurance increases

Health benefit decreases

What PPACA did not change

Thirst

for cures

Costly research

and Innovatio

n

The increasing cost of health CARE

And if the cost of health CARE continues to increase …..

So where do we go from here?

Health insurance continuum

IndividualOff or on exchange

Single EmployerTraditional plans, Exchange plans

Multiple Employer

True MEP

Self InsuredPartially or Fully

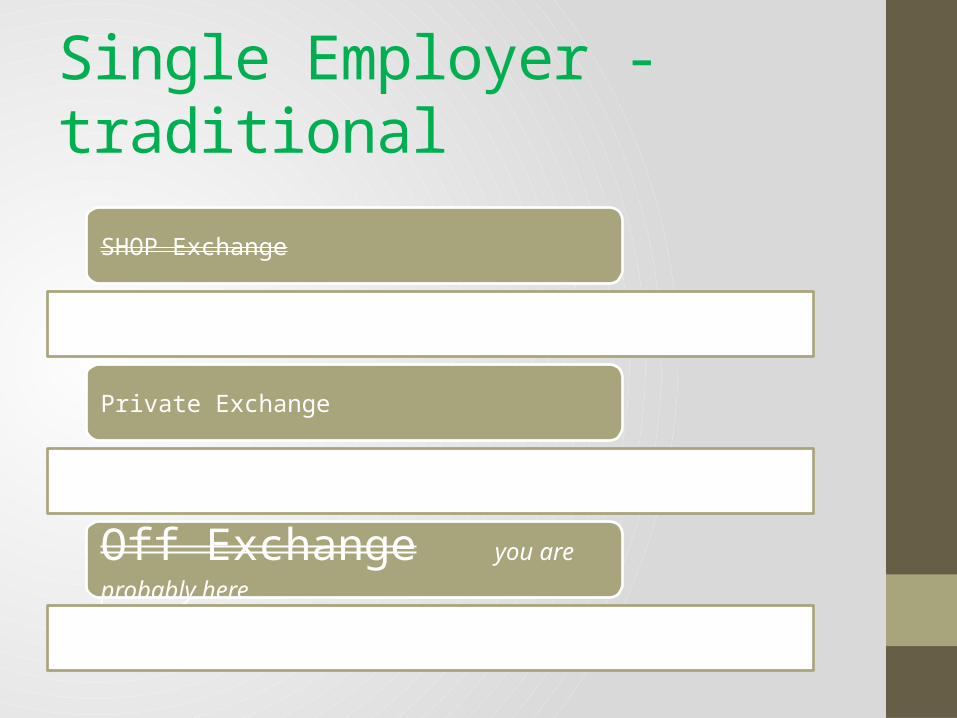

Single Employer - traditional

SHOP Exchange

Private Exchange

Off Exchange you are probably here

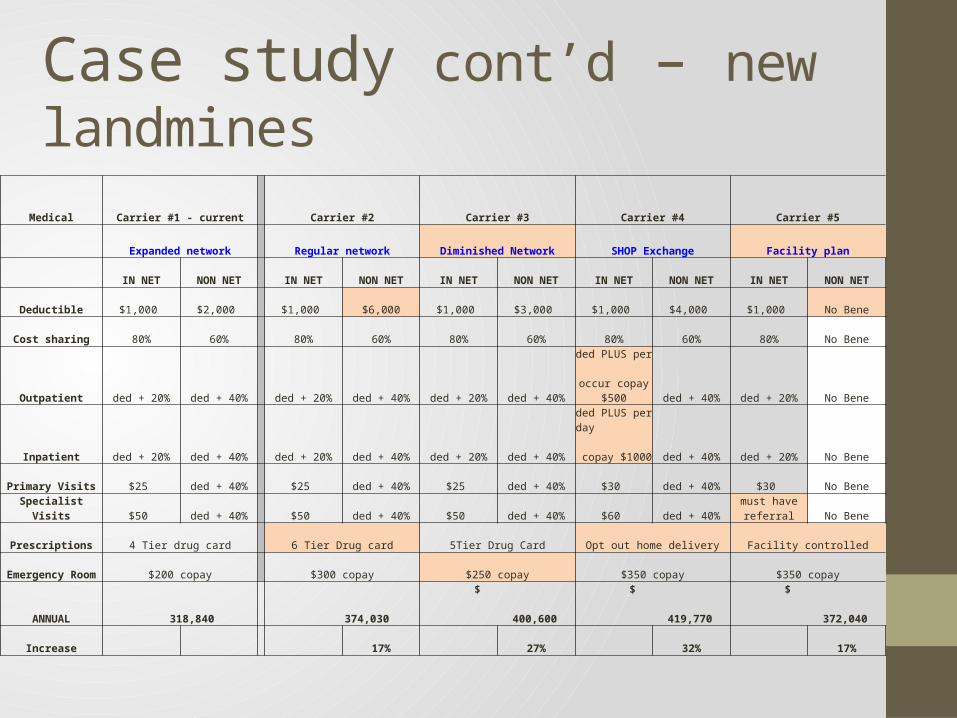

Case study cont’d – new landmines

Medical Carrier #1 - current Carrier #2 Carrier #3 Carrier #4 Carrier #5

Expanded network Regular network Diminished Network SHOP Exchange Facility plan

IN NET NON NET IN NET NON NET IN NET NON NET IN NET NON NET IN NET NON NET

Deductible $1,000 $2,000 $1,000 $6,000 $1,000 $3,000 $1,000 $4,000 $1,000 No Bene

Cost sharing 80% 60% 80% 60% 80% 60% 80% 60% 80% No Bene

Outpatient ded + 20% ded + 40% ded + 20% ded + 40% ded + 20% ded + 40%

ded PLUS per occur copay $500 ded + 40% ded + 20% No Bene

Inpatient ded + 20% ded + 40% ded + 20% ded + 40% ded + 20% ded + 40%

ded PLUS per day

copay $1000 ded + 40% ded + 20% No Bene

Primary Visits $25 ded + 40% $25 ded + 40% $25 ded + 40% $30 ded + 40% $30 No Bene

Specialist Visits $50 ded + 40% $50 ded + 40% $50 ded + 40% $60 ded + 40%must have

referral No Bene

Prescriptions 4 Tier drug card 6 Tier Drug card 5Tier Drug Card Opt out home delivery Facility controlled

Emergency Room $200 copay $300 copay $250 copay $350 copay $350 copay

ANNUAL 318,840

374,030

$ 400,600

$ 419,770

$ 372,040

Increase 17% 27% 32% 17%

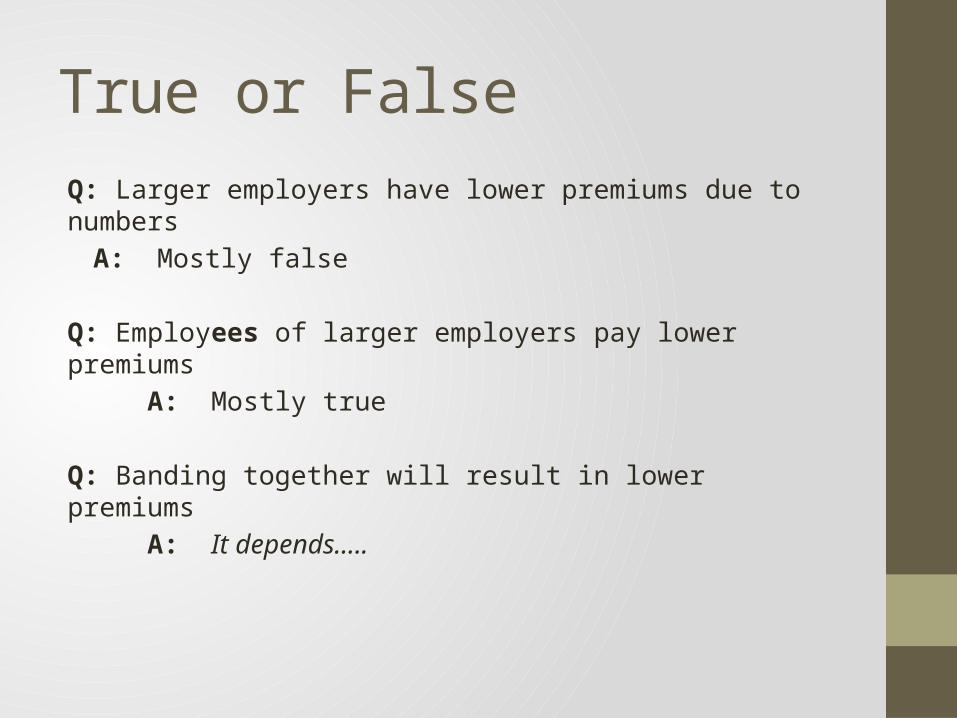

True or False

Q: Larger employers have lower premiums due to numbersA: Mostly false

Q: Employees of larger employers pay lower premiums A: Mostly true

Q: Banding together will result in lower premiums A: It depends…..

Shop Exchange

Where you must purchase your group plan if you intend to take advantage of the Federal Small Business Tax Credit.

Federal - Small business tax creditFor tax years beginning in 2014 or later:

- Max credit is 50% of premiums paid (35% for tax- exempt org)

- To be eligible:• Pay 50% of the single (not family) premium• Not have more than 25 FTE employees• Must purchase the plan from the Small Business

Health Options Program (SHOP) Marketplace just BCBS or Kaiser at this time

- Average salary cannot exceed $50k - $25k sweet spot

Georgia - State Tax Exemption

Opportunity Zone Credits

Enterprise Zone Credits (OCGA 36-88)Urban Redevelopment Law Benefits OCGA 36-61Job Tax Credit Program

NOT tied to SHOP Exchange

Single Employer - traditional

SHOP Exchange

Private Exchange

Off Exchange you are probably here

Private Exchange…..more choices

Can be sponsored by one carrier or can be an independent exchange containing several carriers

Plans are pre-selected - you don’t get to select You or your employees choose from what’s offered

Growing in popularity is….

Liazon technology and platform: - Defined contribution - Benefits administration, you just pay the bill - Ancillary benefits included - Intuitive shopping tool for employees - AGC of America

Single Employer Summary:SHOP Exchange – subsidies only

Private Exchange – same widget, employee choice

Off Exchange – traditional employer choice

Explore your options!

Health insurance continuum

IndividualOff or on exchange

Single EmployerTraditional plans, Exchange plans

Multiple Employer

True MEP

Self InsuredPartially or Fully

Wellness$6 Billion industry

Programs that give employers greater latitude in rewarding group health plan participants and their beneficiaries for healthy lifestyles through wellness programs that meet certain standards.

The limit on rewards or penalties is currently set at 30 percent of the cost of coverage.

Do they work?http://www.rand.org/pubs/research_reports/RR254.html

Smokers

Please stand up!

Survey: Why employees are being terminated….

62% Poor work ethic11% Employee skill gaps 5% Poor cultural fit17% Other

Source: Express Employment – largest privately held staffing company – Feb 2014 ‘America Employed’ campaign.

The “positive” cycle

Offer above the norm benefits

Attract and retain the best

employees

The best employees have the best work

ethic

Greater work ethic means

greater profitability

Other ‘benefits’ being sought

What other benefits will set an employer apart?• Soft benefits - respecting holiday time off• A growing bucket of paid time off with tenure• Sabbatical after long tenure

Source: Kimmel and Associates, national construction recruiting firm, interview March 2014

Rank the most important benefitsSurvey: 1500 people - employers, HR/hiring managers and employees

TOP THREE MOST IMPORTANT BENEFITS OFFERED BY EMPLOYERS:

(other than wages)

Management#1 – Healthcare plan (84%)#2 – Retirement plan (66%)#3 – Paid time off (62%)

Non-management#1 – Healthcare plan (83%)#2 – Retirement plan (73%)#3 – Paid time off (52%)

Source: Express Employment Professionals – America Employed Campaign - February 2014

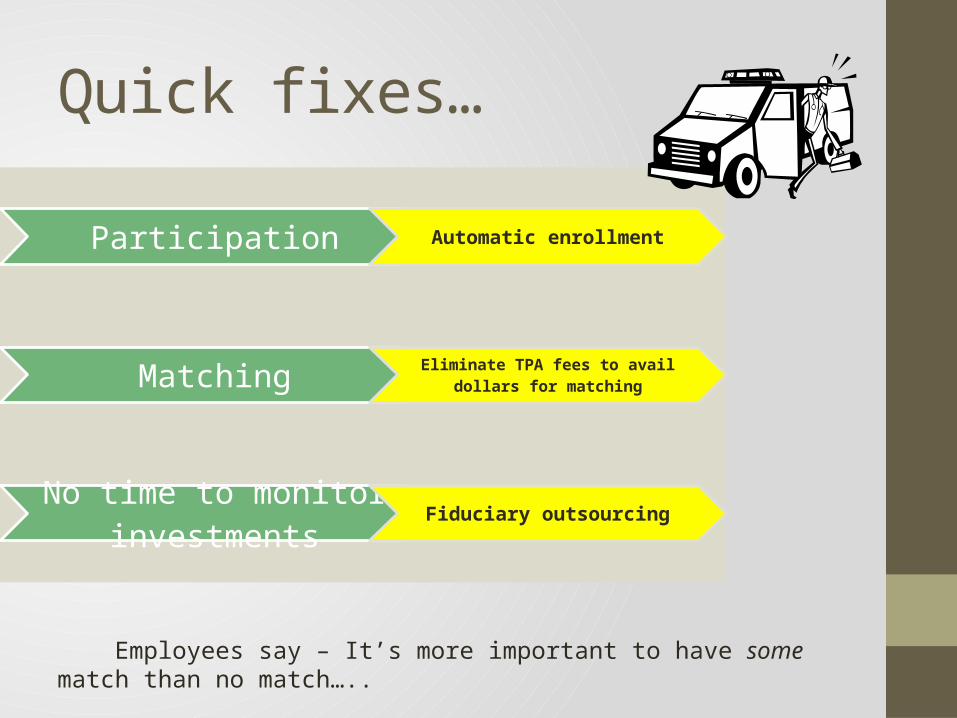

Quick fixes…

Participation Automatic enrollment

Matching Eliminate TPA fees to avail dollars for matching

No time to monitor investments Fiduciary outsourcing

Employees say – It’s more important to have some match than no match…..

PPACA - aka Obamacare

P atientP rotection andA ffordableC areA ct