Embed Size (px)

Citation preview

© 2017 Strategic Treasurer. All rights reserved. 1

TRANSFORMING A/P INTO A PROFIT CENTER

SYNOPSIS Accounts Payable (“A/P”) is rarely funded at a level that matches other finance areas. The moniker of “cost center” is hung around A/P’s neck and can be accompanied by limited resources. Treasury typically owns working capital and needs to help drive and support the right type of organizational emphasis on A/P. This is due to the fact that while A/P manages or influences several key levers of working capital, which can have disproportionate impact on the financial strength and flexibility of the firm, they do not occupy a seat at the executive table. By trying to make adjustments on their own, such as paying vendors late, A/P can destroy critical vendor relationships, costing the firm more than just money. A/P can be turned into a profit center while optimizing working capital usage, but they need a strong partner. Treasury is an ideal partner to help transform A/P into a profit center. In order to accomplish this, treasury must take a lead role in moving the levers with the right level of corporate support to ensure that the levers are not just pushed to one extreme or the other in a way that ignores key relationship elements.

Treasury’s Role in Transforming Accounts Payable Into a Profit Center

A white paper written & produced by

© 2017 Strategic Treasurer. All rights reserved. 2

TRANSFORMING A/P INTO A PROFIT CENTER

RECOGNIZING A/P’S PLIGHTIt is no secret that A/P departments are viewed as cost centers—operational and not strategic—a necessary administration function. Typically, this translates into organizations making a minimal investment in A/P, sufficient to keep it operating, in compliance, and out of trouble. If this negative perception surrounds an A/P department, it becomes particularly difficult for A/P leaders to get the level of attention and the investment required to make changes for a significant impact. When A/P seeks to move from being a cost center to a profit center, they may find themselves caught in the middle—trying to realize significant value for the organization, while being viewed as a necessary overhead.

ĵĵ Cost Center Label. That label reflects a relatively diminished view of the department compared to areas or divisions that generate revenue. A/P may be under-appreciated, overlooked, and therefore under- leveraged. This is a lost opportunity.

ĵĵ Historical Failure to Invest Beyond the Minimum. Investment in A/P is typically provided when it is necessary to comply with government rules, tax requirements, or to support new payment types. These required changes absorb all available funding. After compliance, the competition for additional funding is won by profit-generating areas and cost-reduction efforts.

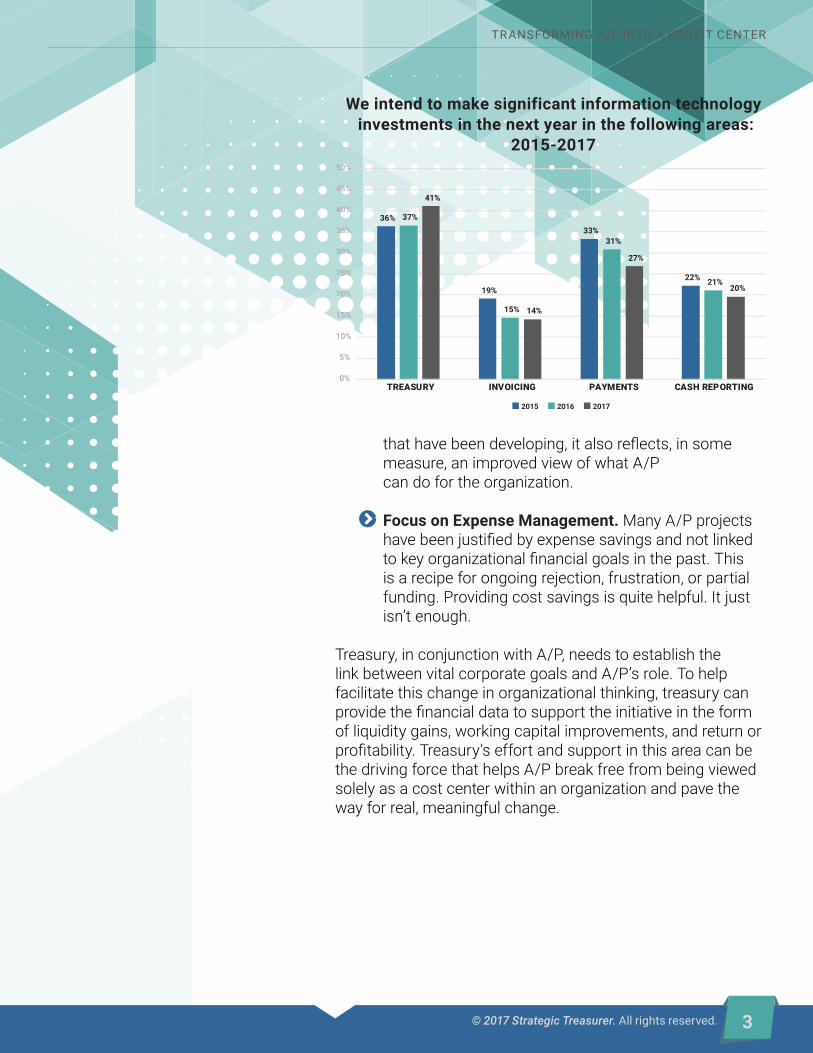

ĵĵ Intent to Spend. There is some good news that this attitude of minimal spending has been changing. Intent to spend significantly for payments remains elevated at 27%. While this certainly reflects new payment types

View as Cost

Center

Trying to Realize

Value for Organization

A/P

© 2017 Strategic Treasurer. All rights reserved. 3

TRANSFORMING A/P INTO A PROFIT CENTER

that have been developing, it also reflects, in some measure, an improved view of what A/P can do for the organization.

ĵĵ Focus on Expense Management. Many A/P projects have been justified by expense savings and not linked to key organizational financial goals in the past. This is a recipe for ongoing rejection, frustration, or partial funding. Providing cost savings is quite helpful. It just isn’t enough.

Treasury, in conjunction with A/P, needs to establish the link between vital corporate goals and A/P’s role. To help facilitate this change in organizational thinking, treasury can provide the financial data to support the initiative in the form of liquidity gains, working capital improvements, and return or profitability. Treasury’s effort and support in this area can be the driving force that helps A/P break free from being viewed solely as a cost center within an organization and pave the way for real, meaningful change.

36%

19%

33%

22%

37%

15%

31%

21%

41%

14%

27%

20%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

TREASURY INVOICING PAYMENTS CASH REPORTING

We intend to make significant information technology investments in the next year in the following areas: �

2015-2017

2015 2016 2017

© 2017 Strategic Treasurer. All rights reserved. 4

TRANSFORMING A/P INTO A PROFIT CENTER

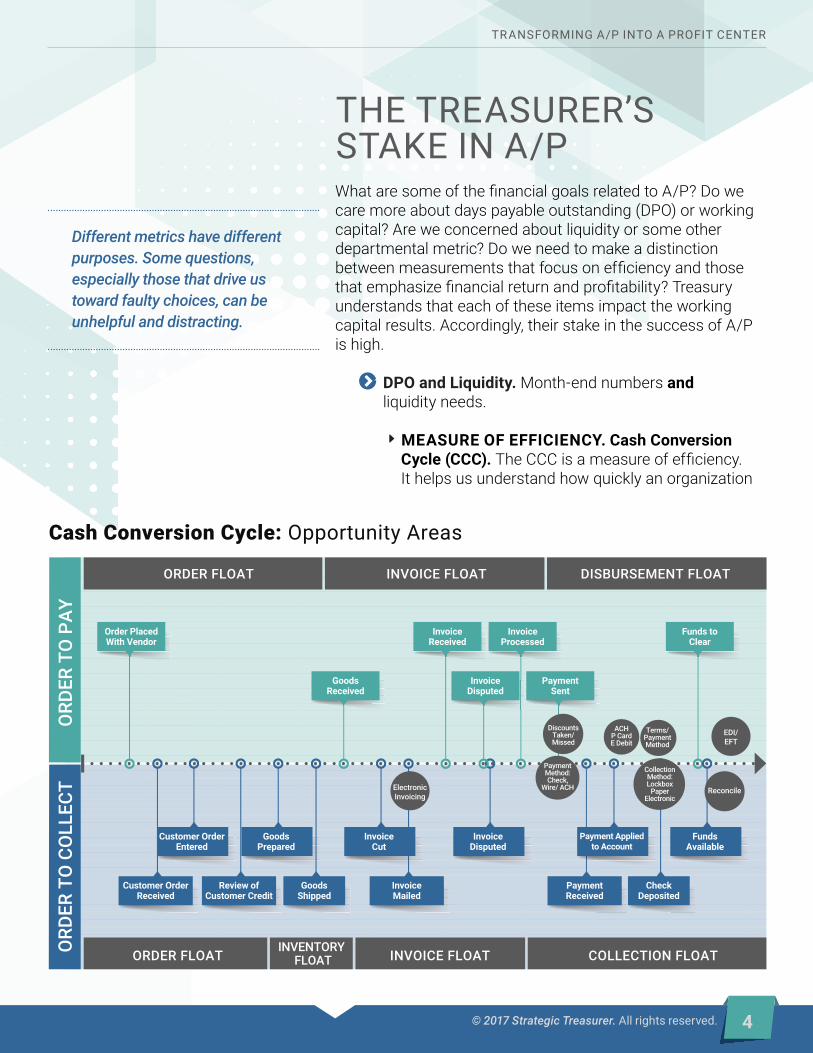

THE TREASURER’S STAKE IN A/PWhat are some of the financial goals related to A/P? Do we care more about days payable outstanding (DPO) or working capital? Are we concerned about liquidity or some other departmental metric? Do we need to make a distinction between measurements that focus on efficiency and those that emphasize financial return and profitability? Treasury understands that each of these items impact the working capital results. Accordingly, their stake in the success of A/P is high.

ĵĵ DPO and Liquidity. Month-end numbers and liquidity needs.

ĵEMEASURE OF EFFICIENCY. Cash Conversion Cycle (CCC). The CCC is a measure of efficiency. It helps us understand how quickly an organization

ORD

ER T

O P

AY

ORD

ER T

O C

OLL

ECT

ORDER FLOAT INVOICE FLOAT DISBURSEMENT FLOAT

ORDER FLOATINVENTORY

FLOAT INVOICE FLOAT COLLECTION FLOAT

Cash Conversion Cycle: Opportunity Areas

Order Placed With Vendor

InvoiceReceived

InvoiceProcessed

Funds toClear

Goods Received

Customer OrderEntered

GoodsPrepared

InvoiceCut

InvoiceDisputed

FundsAvailable

PaymentSent

Invoice Disputed

DiscountsTaken/Missed

PaymentMethod:Check,

Wire/ ACH

Customer OrderReceived

Review ofCustomer Credit

InvoiceMailed

PaymentReceived

GoodsShipped

CheckDeposited

ElectronicInvoicing

Reconcile

Collection Method:Lockbox

PaperElectronic

Terms/PaymentMethod

ACHP CardE Debit

EDI/EFT

Payment Appliedto Account

Different metrics have different purposes. Some questions, especially those that drive us toward faulty choices, can be unhelpful and distracting.

© 2017 Strategic Treasurer. All rights reserved. 5

TRANSFORMING A/P INTO A PROFIT CENTER

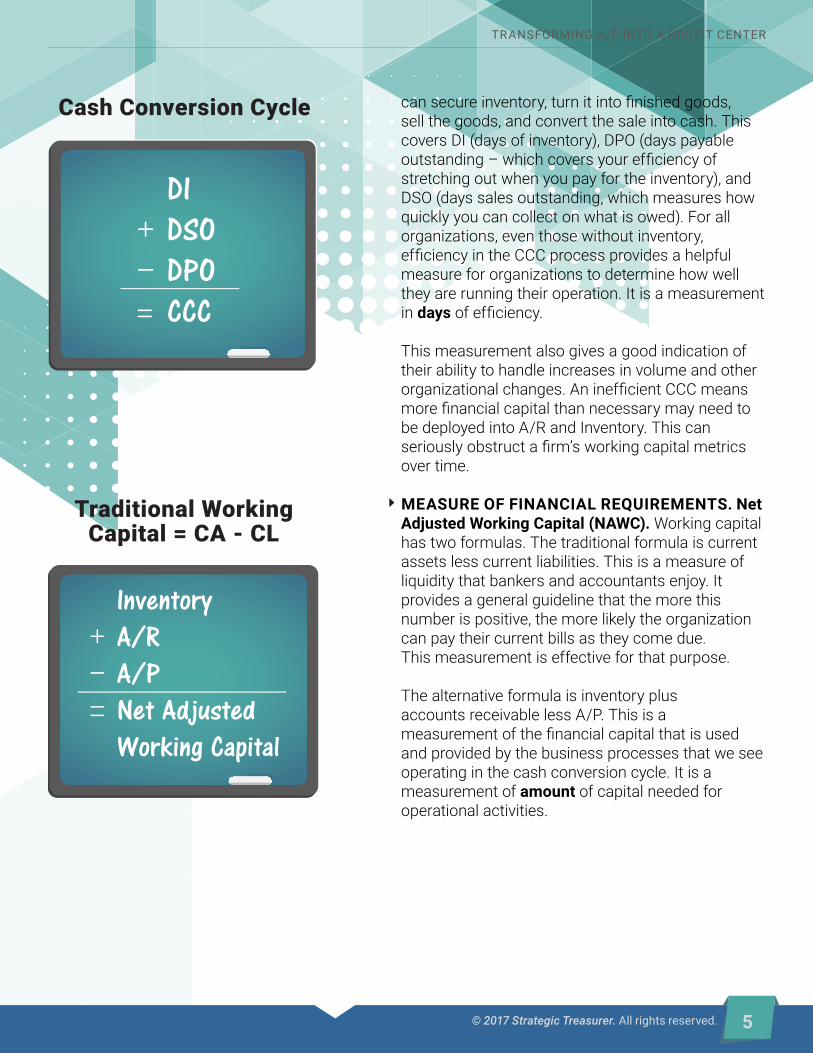

can secure inventory, turn it into finished goods, sell the goods, and convert the sale into cash. This covers DI (days of inventory), DPO (days payable outstanding – which covers your efficiency of stretching out when you pay for the inventory), and DSO (days sales outstanding, which measures how quickly you can collect on what is owed). For all organizations, even those without inventory, efficiency in the CCC process provides a helpful measure for organizations to determine how well they are running their operation. It is a measurement in days of efficiency. This measurement also gives a good indication of their ability to handle increases in volume and other organizational changes. An inefficient CCC means more financial capital than necessary may need to be deployed into A/R and Inventory. This can seriously obstruct a firm’s working capital metrics over time. ĵEMEASURE OF FINANCIAL REQUIREMENTS. Net

Adjusted Working Capital (NAWC). Working capital has two formulas. The traditional formula is current assets less current liabilities. This is a measure of liquidity that bankers and accountants enjoy. It provides a general guideline that the more this number is positive, the more likely the organization can pay their current bills as they come due. This measurement is effective for that purpose. The alternative formula is inventory plus accounts receivable less A/P. This is a measurement of the financial capital that is used and provided by the business processes that we see operating in the cash conversion cycle. It is a measurement of amount of capital needed for operational activities.

DIL DSOK DPO CCCKK

Cash Conversion Cycle

Traditional Working Capital = CA - CL

InventoryL A/RK A/P Net Adjusted Working CapitalKK

© 2017 Strategic Treasurer. All rights reserved. 6

TRANSFORMING A/P INTO A PROFIT CENTER

WHY THE PARTNERSHIP BETWEEN TREASURY & A/P MATTERSProblems can arise when an organization pits one KPI against another. Understanding the need to optimize working capital and liquidity requires that A/P and treasury work together. This is important when we consider how vital it is to both departments for A/P to succeed in linking their activities and projects to the organization’s strategic and tactical objectives. It is treasury’s partnership and influence that can create an environment where these A/P initiatives can be taken seriously.

Regarding A/P, there are important considerations for treasury that cannot be ignored:

ĵĵ DPO versus Liquidity. Month-end numbers and liquidity needs.

ĵEDPO. Month-End Numbers. The CCC numbers are provided as a measurement in the form of days. These numbers come from month-end financial reporting. DPO, for example is the payables outstanding at the end of the month (or, more commonly the average of the most recent month-end and the month prior). This does not show or reflect the actual payables outstanding every day of the month. Each CCC element (payables, inventory, and receivables) can have high

Understanding how measurements are made can help us understand what uninformed operational conclusions we need to avoid.

AccountsPayableDPO & I/S L B/S M KK

Number of Daysin a Period

Cost of Sales

INCOMESTATEMENTS

BALANCESHEET

© 2017 Strategic Treasurer. All rights reserved. 7

TRANSFORMING A/P INTO A PROFIT CENTER

or low points during the month. A/P and treasury may love the financial statement driven measurements for the purpose they were created. However, they are not created to measure liquidity needs directly.

ĵELIQUIDITY NEEDS. Continual View. The old joke that ends with the statement: “I can’t be out of money; I still have checks!” is a consumer- oriented example of the business situation that could be phrased as “We can’t have a liquidity issue on the 15th since our month-end working capital metrics are great!” A firm that has significant payments due on the 5th can run into liquidity problems even if their month-end accounts payables balances seem to provide significant working capital. The balance of cash (increased by collecting receivables and decreased when A/P makes the payment) can vary greatly throughout the month. Liquidity is the domain of treasury, and A/P has some important levers that impact liquidity on a daily basis.

$12.5 mm

$7.5 mm

TIME (DAYS OF MONTH)

MIL

LIO

NS

USD

$8

$10

$6

$12

$4

$14

$2

$16

1 3 6 9 12 15 242118 27 30

© 2017 Strategic Treasurer. All rights reserved. 8

TRANSFORMING A/P INTO A PROFIT CENTER

Optimizing working capital and liquidity needs to be front and center of any major A/P project or initiative to ensure it garners the right type of attention and support. This is an effective way to manage relationships and expectations while also providing significant value to the organization as a whole, including treasury. Treasury must not undervalue their role in this process and help make the case for A/P by highlighting the value their projects bring to the organization’s financial goals.

TRANSFORMING A/P INTO A PROFIT CENTERHow can a cost center like A/P become a profit center? The approach to optimizing A/P must be different from driving costs out of the department and the processes. Certainly, unneeded costs must continue to be exercised prudently, thoughtfully, and consistently over time. However, that is not enough. No matter what is done, costs cannot be driven below zero.

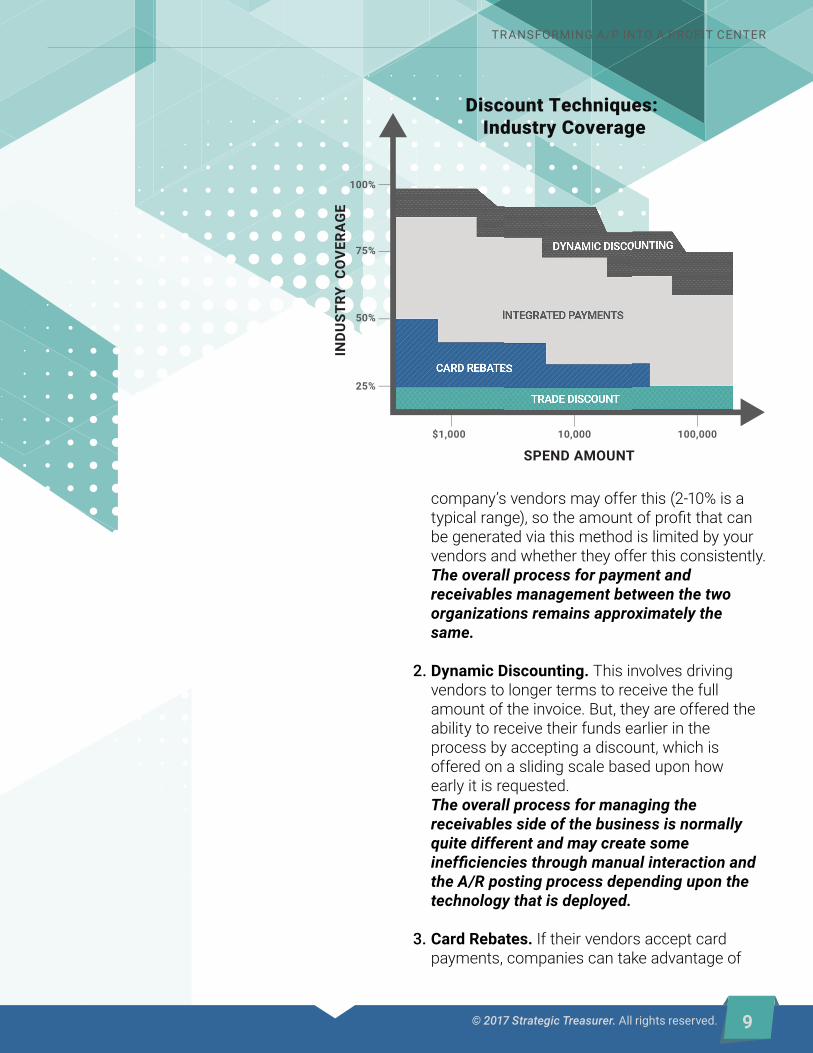

ĵĵ Examples of Generating Yield in A/P. Generating financial value that can exceed the cost of accounts payable.

ĵECOST OF CAPITAL. Extending payment terms frees up capital for other purposes. There is real, measurable financial value to the organization for this activity. This capital, if the change is long-term, can be valued as the weighted average cost of capital (WACC) or the cost of long-term debt. If the extension is not sustainable or is one-time in nature, then an overnight or short-term bond rate would need to be applied.

ĵEPUTTING CAPITAL TO WORK. There are several ways to generate discounts in A/P.

1. Accepting discount payment terms. (1/10, n/30) allows you to pay invoices earlier while realizing an effective 18% annual value for that action, which could be netted against a capital cost measure. Some percentage of the

A strategic approach to the payments process allows an organization to generate capital, payment rebates/discounts, and also allows A/P to generate profits in excess of their costs.

© 2017 Strategic Treasurer. All rights reserved. 9

TRANSFORMING A/P INTO A PROFIT CENTER

company’s vendors may offer this (2-10% is a typical range), so the amount of profit that can be generated via this method is limited by your vendors and whether they offer this consistently. The overall process for payment and receivables management between the two organizations remains approximately the same.

2. Dynamic Discounting. This involves driving vendors to longer terms to receive the full amount of the invoice. But, they are offered the ability to receive their funds earlier in the process by accepting a discount, which is offered on a sliding scale based upon how early it is requested. The overall process for managing the receivables side of the business is normally quite different and may create some inefficienciesthroughmanualinteractionand the A/R posting process depending upon the technology that is deployed.

3. Card Rebates. If their vendors accept card payments, companies can take advantage of

SPEND AMOUNT

INTEGRATED PAYMENTS

DYNAMIC DISCOUNTING

CARD REBATES

$1,000

25%

50%

75%

100%

10,000 100,000

IND

UST

RY C

OV

ERA

GE

Discount Techniques: Industry Coverage

TRADE DISCOUNT

© 2017 Strategic Treasurer. All rights reserved. 10

TRANSFORMING A/P INTO A PROFIT CENTER

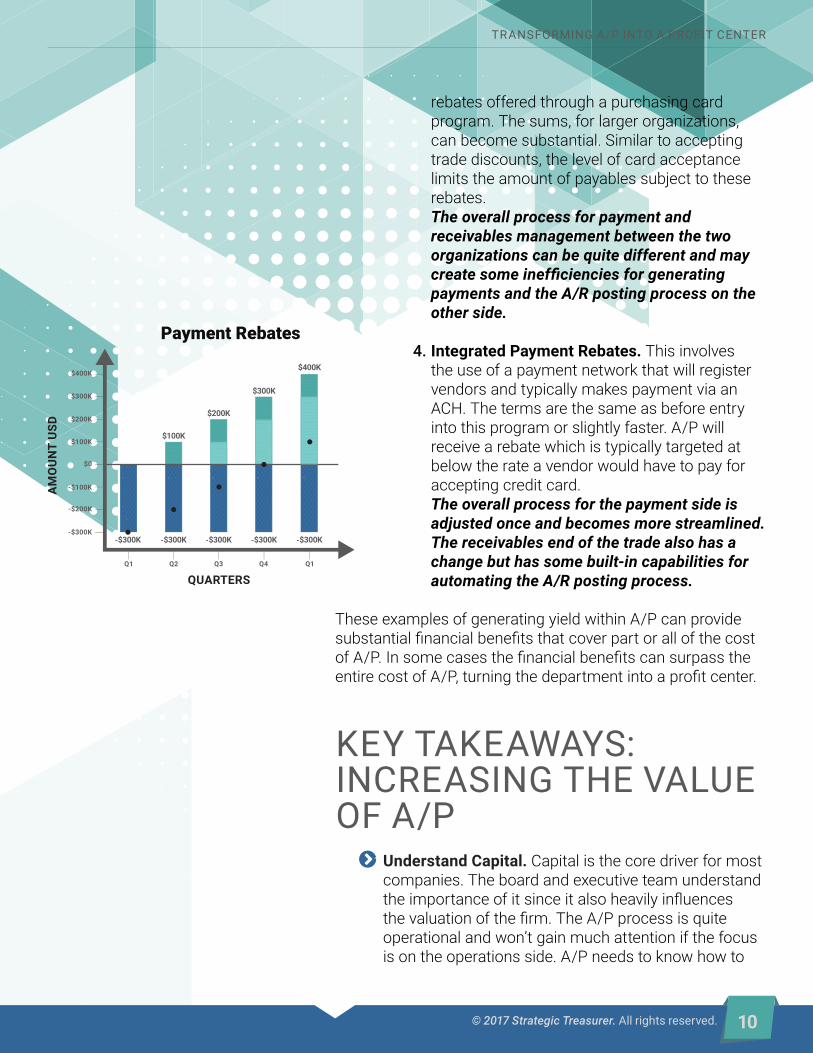

rebates offered through a purchasing card program. The sums, for larger organizations, can become substantial. Similar to accepting trade discounts, the level of card acceptance limits the amount of payables subject to these rebates. The overall process for payment and receivables management between the two organizations can be quite different and may createsomeinefficienciesforgenerating payments and the A/R posting process on the other side.

4. Integrated Payment Rebates. This involves the use of a payment network that will register vendors and typically makes payment via an ACH. The terms are the same as before entry into this program or slightly faster. A/P will receive a rebate which is typically targeted at below the rate a vendor would have to pay for accepting credit card. The overall process for the payment side is adjusted once and becomes more streamlined. The receivables end of the trade also has a change but has some built-in capabilities for automating the A/R posting process.

These examples of generating yield within A/P can provide substantial financial benefits that cover part or all of the cost of A/P. In some cases the financial benefits can surpass the entire cost of A/P, turning the department into a profit center.

KEY TAKEAWAYS: INCREASING THE VALUE OF A/P

ĵĵ Understand Capital. Capital is the core driver for most companies. The board and executive team understand the importance of it since it also heavily influences the valuation of the firm. The A/P process is quite operational and won’t gain much attention if the focus is on the operations side. A/P needs to know how to

QUARTERSQ1

$100K

-$300K -$300K -$300K -$300K -$300K

$200K

$300K

$400K

Q2 Q3 Q4 Q1

AM

OU

NT

USD

Payment Rebates

$0

$100K

-$100K

$200K

-$200K

$300K

-$300K

$400K

© 2017 Strategic Treasurer. All rights reserved. 11

TRANSFORMING A/P INTO A PROFIT CENTER

frame their plans and actions in a way that generates more excitement up the management chain. A/P can impact capital in positive and negative ways. Throwing around the word capital isn’t enough. Understand capital and how A/P initiatives and actions, or inactions, can have an impact, and you can get far better attention.

ĵĵ Recognize the Time Value of Money. Discounts missed and taken are terms largely unknown outside of A/P and some treasury circles. Few care about these things. But, this is just one example of how the time value of money intersects with working capital. The time value of money is a different way of recognizing the cost and value of capital. If A/P can move out payment terms on some clients, they can often free up enough cash to take all financially viable discounts. This allows A/P, in conjunction with treasury, to see where their levers add financial value— and, add to the profit center calculation. Offering the option to your vendors, or making it part of the business model, to get paid earlier at a discount, ensures you can leverage all or most of A/P instead of a small percentage of the payables universe.

ĵĵ Free Up Cash without Killing Your Trading Partners. Simply pushing out payment terms may seem like a sure way to push the capital-raising requirements out to your vendors. This can harm or imperil some vendors who may not have ready access to inexpensive capital. Making life difficult for key vendors can backfire creating a lose-lose situation. Instead, A/P can pay earlier at a discount or A/P can extend terms, while providing the flexibility of taking money earlier for those who need it. This flexibility can free up cash without killing your trading partners. The cash that is freed up, or the reduction in costs, all contribute to the profit center calculations.

Take these critical steps to help transform your A/P group into a profit center. The movement from cost center to profit center changes how the rest of the organization will look at and invest in A/P.

© 2017 Strategic Treasurer. All rights reserved. 12

TRANSFORMING A/P INTO A PROFIT CENTER

ABOUT BOTTOMLINE TECHNOLOGIESBottomline Technologies (NASDAQ: EPAY) helps businesses pay and get paid. We make complex business payments simple, secure and seamless. Businesses and banks rely on Bottomline for domestic and international payments, effective cash management tools, automated workflows for payment processing and bill review and state of the art fraud detection, behavioral analytics and regulatory compliance. Headquartered in Portsmouth, New Hampshire, we delight our customers through offices across the United States, Europe, and Asia-Pacific. Businesses around the world depend on Bottomline solutions to help them pay and get paid, including some of the world’s largest systemic banks, private and publicly traded companies and Insurers.

Every day, we help our customers by making complex business payments simple, secure and seamless. For more information, visit www.bottomline.com.

ABOUT BNY MELLON

BNY Mellon is a global investments company dedicated to helping its clients manage and service their financial assets throughout the investment lifecycle. Whether providing financial services for institutions, corporations or individual investors, BNY Mellon delivers informed investment management and investment services in 35 countries and more than 100 markets. As of March 31, 2017, BNY Mellon had $30.6 trillion in assets under custody and/or administration, and $1.7 trillion in assets under management. BNY Mellon can act as a single point of contact for clients looking to create, trade, hold, manage, service, distribute or restructure investments. BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation (NYSE: BK). Additional information is available on www.bnymellon.com. Follow us on Twitter @BNYMellon or visit our newsroom at www.bnymellon.com/newsroom for the latest company news.

+1 212.495.1784 ▪ +1 [email protected]

BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may be used as a generic term to reference the corporation as a whole and/or its various subsidiaries generally. This material and any products and services may be issued or provided under various brand names in various countries by duly authorized and regulated subsidiaries, affiliates, and joint ventures of BNY Mellon. The material contained in this white paper, which may be considered advertising, is for general information and reference purposes only and is not intended to provide or be construed as legal, tax, accounting, investment, financial or other professional advice on any matter, and is not to be used as such. This white paper is a financial promotion. This white paper, and the statements contained herein, are not an offer or solicitation to buy or sell any products (including financial products) or services or to participate in any particular strategy mentioned and should not be construed as such. This white paper is not intended for distribution to, or use by, any person or entity in any jurisdiction or country in which such distribution or use would be contrary to local law or regulation. Similarly, this white paper may not be distributed or used for the purpose of offers or solicitations in any jurisdiction or in any circumstances in which such offers or solicitations are unlawful or not authorized, or where there would be, by virtue of such distribution, new or additional registration requirements. Persons into whose possession this white paper comes are required to inform themselves about and to observe any restrictions that apply to the distribution of this document in their jurisdiction. To help us continually improve our service and in the interest of security, we may monitor and / or record telephone calls. The information contained in this white paper is for use by wholesale clients only and is not to be relied upon by retail clients. Any discussion of tax matters contained in this white paper is not intended to constitute tax advice and is not intended or written to be used, and cannot be used, for the purpose of avoiding tax or penalties imposed under the United States Internal Revenue Code or promoting, marketing or recommending to another party any transaction or matter. For tax advice, you should consult an independent tax advisor for advice based on your particular facts and circumstances. The contents may not be comprehensive or up-to-date, and BNY Mellon will not be responsible for updating any information contained within this white paper. Some information contained in this white paper has been obtained from third party sources and has not been independently verified. BNY Mellon makes no representation as to the accuracy or completeness of the information provided in this white paper. BNY Mellon recommends that professional consultation should be obtained before using any service offered by BNY Mellon. The views expressed within this white paper are those of the contributors only and not those of BNY Mellon or any of its subsidiaries or affiliates. BNY Mellon assumes no liability whatsoever (direct or consequential or any other form of liability) for any action taken in reliance on the information contained in this white paper, or for resulting from use of this white paper, its content, or services. Any unauthorized use of material contained in this white paper is at the user’s own risk. Reproduction, distribution, republication and retransmission of material contained in this white paper is prohibited without the prior consent of BNY Mellon. Trademarks, service marks and logos belong to their respective owners. Bottomline Technologies and the Bottomline Technologies logo are trademarks of Bottomline Technologies, Inc. which may be registered in certain jurisdictions. ©2017 The Bank of New York Mellon Corporation. All rights reserved.

TRANSFORMING A/P INTO A PROFIT CENTER

© 2017 Strategic Treasurer. All rights reserved.

ABOUT STRATEGIC TREASURER

Since 2004, Strategic Treasurer has helped hundreds of corporate clients face real world treasury issues. Our team of senior consultants is comprised of former practitioners with actual corporate treasury experience who have “hopped the desk” to support their former peers from the consulting side. Strategic Treasurer consultants are known not only for their expertise in the treasury space, but also for their responsiveness to client issues, thorough follow-through on each project, and general likability as temporary team members of your staff.

Our focus as a firm centers on maintaining true expertise in the treasury space. Through constantly refreshing our knowledge and intentionally learning about leading solutions, we ensure that our understanding is both global in scope and rich in detail.

525 Westpark Drive, Suite 130Peachtree City, GA 30269

+1 678.466.2220strategictreasurer.com

THE TIME IS NOW: TREASURY & AP DEPARTMENTS CAN COLLABORATE TO ACHIEVE PROFIT CENTER STATUSDiscover how 3 organizations use the Paymode-X payment network to elevate efficiency and improve the bottom line.

Read the case study ebook to learn how:

• A manufacturing company overcame its ERP integration and remittance delivery challenges to scale payment automation in response to growth demands

• A hospital finance team got out from under its pile of paper checks—and improved vendor relations

• A healthcare management company with 44 properties and 95 bank accounts reduced complexity and cut costs by more than $75,000

CLICK HERE TO READ MORE