Embed Size (px)

Citation preview

2015

www.dunedinkindergartens.org.nz

Treasurers Guide

2

3

Contents

1. Job Description

2. Weekly Tasks

3. Monthly Tasks

4. Annual Tasks

5. Miscellaneous

6. Forms

4

1. JOB DESCRIPTION

Control

The Committee is legally responsible for control of the Kindergarten finances. They should ensure the Treasurer is competent to do the job and is prepared to attend any training provided by Dunedin Kindergartens (DK)

Decisions on how the money should be spent and how money should be raised is a Committee decision; the treasurer’s role is to record all transactions and provide reports to the DK office for GST returns (20th January, March, May, July, September, November) and annual review (January).

It is important to remember that the Treasurer is appointed by, and is responsible to, the parents of the kindergarten. Compliance with the rules and regulations of the DK Constitution, DK Financial Policy (see policy and procedure manual), and the Ministry of Education is required.

A Reviewer will be appointed in January by DK to do an annual review of each kindergarten’s financial records. This forms part of the annual financial audit of Dunedin Kindergartens in February and your documents will requested to be delivered to the DK admin office by January 20th each year. (See checklist at the end of this guide for documents that will be needed).

Please remember that you are not on your own - help is only a phone call away - contact DK phone 455-8892, or call at the Administration Offices at 81 Forbury Road.

Authorisation of Expenditure

All expenditure must be approved by the Committee and minuted. This should be done at the monthly meeting and in advance of payment being made.

Only people who are authorised by the committee may incur expenditure. This means a decision has been recorded in the minutes to delegate authorisation to a particular person (or persons) to make purchases for a specific purpose; a limit to cost should be included in the minutes.

On occasion, it is necessary to approve a payment by gaining approval from a quorum of the Committee (ie 4 committee members).

If expenditure is incurred through an ongoing project, the expenditure is usually approved well in advance by acceptance of a quote or approval to have work done or expenditure incurred. Therefore, you can often go ahead and pay accounts when due without waiting for a meeting.

If in doubt, check with your President or Secretary as to what was decided before making payment (one of them has to co-sign anyway). Contact the DK office if any further queries arise.

Treasurers Supplies

Folders, receipt books, and other stationery that you require should be supplied by the committee. It is likely that the treasurer will inherit most supplies from their predecessor, but ongoing needs should be met from committee funds.

DK will provide an Excel spreadsheet that is used to record all financial transactions. It contains macros and formulas that must be retained in the file, so it is not possible to utilise software other than Excel. All kindergartens have the Microsoft Office suite loaded on their computers and use of one of their computers is available to you, if required.

The basics of your supplies are: A ring binder for each month’s documents: bank statements, invoices, correspondence; to have these filed in month order is helpful Bank deposit book Cheque book

5

2. WEEKLY TASKS

Receipting and Banking Monies

It is the Treasurer’s responsibility to receipt and bank money collected. In the case of cash, good practice is to count in the presence of the person giving it to you so that you can agree on the amount.

Where a large amount of cash ($500+) is being received at a function or fundraising project, it is recommended that two people should agree the amount and sign the receipt.

Always write a receipt as soon as cash or cheques are received. The receipt should state: - the name of the person/organisation from whom received - nature of the receipt (e.g. raffle) - the sum received in words and numbers - signature of Treasurer. - name of kindergarten.

You must receipt different types of income, i.e. fundraising/donations/ separately - a different receipt for each type of income. Receipt Book

This should be in duplicate, consecutively numbered and STAMPED WITH THE NAME OF THE KINDERGARTEN. Whenever money is received a receipt must be written out, the carbon copy remaining in the book as the Treasurer’s record. This must be done whether or not the person paying the money requires a receipt. If it’s necessary to cancel a receipt, leave both copies in the receipt book and draw two lines diagonally across the receipt with “Cancelled” written between. Deposit Book

Westpac Bank deposit book should be used for each deposit. It is acceptable for an automated bank deposit machine to be used when depositing 1-2 cheques providing the receipt with the image of the cheques on the reverse is kept with your records. All monies received should be banked within a few days of receipt; banking once a week is usually appropriate. Banking should include a complete group of receipts (e.g. numbers 22-27 inclusive) and the total of the banking and the date should be entered at the foot of the bottom copy of the last receipt in the group. This should match the banked total in deposit book, on bank statement and in the cash book.

Collect Bills and Correspondence

There should be a place in the kindergarten office – rather than the “public” area of the kindergarten - for all bills and other items for the Treasurer. This should be cleared at least once a week.

Correspondence

Action/reply as soon as possible; make two copies of any written reply - one for your records and one for the Secretary – this applies to email correspondence also; cc to the Secretary for committee records.

6

Invoices (bills to pay)

Bills - ensure the kindergarten received the goods/service (the person responsible, i.e. teacher who ordered puzzles, etc must sign invoice); file the account ready for payment/approval at the next committee meeting.

If funds are given to teachers for resources, copies of supplier’s invoices must be obtained and filed with other invoices. GST should be claimed for funds given to teachers, providing a supporting invoice can be obtained. If no invoice is available, funds given to the teaching team should be recorded in the cashbook with ‘no’ in the gst column. Almost all fundraising income attracts GST, and it is sensible to mitigate this cost by ensuring GST can be reclaimed when purchase of goods is made.

a) Fundraising that does not attract GST:

- Ventures for which the time and materials used in the fundraising have been donated to the kindergarten, e.g. cake stalls and garage sales.

- Proceeds from stalls at kindergarten fairs where all goods are donated, this could be a cake stall, for example. Income from this stall must be kept

separate and recorded separately in the cashbook.

- Cash-back promotions

- Stocktakes – providing the retailer confirms they are making a donation for your labour

b)Fundraising that does attract GST

- Goods used in fundraising have been purchased, e.g. selling pies that you have purchased (rather than pies that were donated), chocolate sales,

photography fundraisers etc.

- All raffles

- Craft nights

- Stall money, except example above

- Quiz night income

7

3. MONTHLY TASKS

Cash Book

Recording Cash Book Transactions The cashbook is an Excel file, provided by the DK admin office at conclusion of the annual review. It is emailed to the Treasurer with opening balances endorsed by the reviewer. Note: the cashbook must be printed and filed with your records each month – this is an audit requirement. Cash Book Guide A full description of using the spreadsheet is included at the end of this guide, the various functions of the cashbook are described below:

1. Income or expenditure types are selected from the drop-down list, and are totaled in the annual income and expenditure report, so accuracy is important.

2. GST choice is recorded as ‘Y/N’ from a drop-down choice option

3. GST return is updated automatically from the income / expenditure table, based on ‘Y/N’ chosen in the GST column

4. Treasurer’s report is also automatically updated; there are fields available for detailing information for your committee

5. Unpresented cheques or banking section is manually updated with transactions that are listed on the income and expenditure table, but do not appear on your bank statement at the end of the month.

6. Bank reconciliation is automatically updated; there is a field where manual entry of the closing balance must be entered from the end-of-month bank statement. If this figure does not equal the spreadsheet calculation, an ‘Error’ message will be displayed – check amounts entered in the income & expenditure table if this is the case.

7. There is a section to list upcoming expenses for acceptance by the committee

8. Fundraising summary is automatically updated monthly with a net figure (income less expenditure). Some Treasurer’s choose to track net fundraising by event separately, for reporting to the committee

9.

Prepare a report to the committee

Once a month, the committee must receive a WRITTEN report from the Treasurer (in person where possible) on the last completed month (i.e. report on April in May) Items 4-7 form the Treasurer’s Report. A formal motion to have these approved must be put (i.e. specific bills and amounts to be paid), passed and written into the minutes. If your committee meets late in the month, it may be appropriate to add an updated balance of funds. It does not matter, however if your report is not completely ‘up to the minute’. It is, in fact, more helpful to report at regular intervals (i.e. each calendar month). This makes year by year and kindergarten to kindergarten comparisons possible and requires only one set of figures to be done each month. A periodic check of your actual position against what you budgeted should be helpful and may allow you to avoid financial difficulties, if your committee is in the habit of preparing an annual budget.

8

Recommendation: That the President signs your financial statement to indicate its acceptance and approval by the Committee, just as he/she signs the minutes of the previous meeting. This provides added protection for you. Bank Reconciliation

Every month, the treasurer must reconcile the cash book with the bank statement. The final figures must match. This is proof that your cash book is accurate. The Auditor will not do the audit until he sees the final bank reconciliation for the year (year to date to 31 December). This is a “proof” of your cash book and your cheque book, so you know they are correct (or pick any errors - yours or the bank’s - quickly) and can check how much money you have. Watch for additional entries on the bank statement to enter into the cash book, e.g. cheque book fees, Community Trust grants, automatic payments and direct credits. You may have the bank send your statement at any time/frequency you require. It is recommended that you have it prepared following the end of each calendar month, so it matches your monthly report and the monthly totals in your cash book.

Pay Bills

Accounts for payment - must be signed by the person receiving the goods/service before being submitted to the Committee for approval. They should be approved at a Committee meeting before payment and a list of accounts so approved should be incorporated in the minute book (in your statement). NOTE: Accounts are usually paid on 20th of the month following the expenditure being incurred. Where accounts are paid by cheque, the cheque must be signed by two of the authorised signatories. The cheque butt should record:

1. date of payment

2. name of person/organisation to be paid

3. reason for payment

4. amount

5. opening/closing balances.

6. Invoices must be filed in cheque number order,

Online Banking can be used for payments

A signed letter from the committee approving the facility is required by the bank

The bank will set up business online banking.

Payments will require the authorization of two people – usually the same signatories that can sign cheques are loaded for online banking.

All payments made must be confirmed by the committee before using online banking.

Record the transaction number in the cash book

Cheque and online banking signatories The following personnel should be authorized to sign cheques or authorize online payments:

President Vice President Treasurer Secretary

9

Contributions to Teachers’ funds are often made by committees. These payments are a ‘yes’ for gst only when copies of the invoices for which committee funds are used are made available. Otherwise all payments to teachers are ‘no’ for gst. GST Return is completed two monthly (due dates, 1. Control) and sent to DK, who condenses the information into a single return. It is very important that a return is filed every time when due as if there are amounts owing, penalties could be incurred. Kindergarten IRD Number: 10-357-268. (DK is our “umbrella” organisation for GST and files a group return for all 24 kindergartens, so we share the same number). Refunds will be direct credited to your bank account. If you have GST to pay, you will be sent an invoice - pay on that advice.

10

4. ANNUALLY

Financial Statements

The financial statement is made up to 31 December each year.

Remember, at your last committee meeting for the year to get permission to pay any outstanding accounts before that date (and to pay January accounts payable before your first meeting in the New Year).

Buildings and land do not appear as part of your annual accounts, as all kindergarten land and buildings are either owned by the Government or are vested in Dunedin Kindergartens. They are, therefore, shown as part of the Association Annual Accounts.

Audit

The 24 kindergartens of Dunedin Kindergartens and the Association itself will be group-audited in late January/early February. Books need to be at the Administration offices in early January for pre-audit checks. The board will appoint and pay the auditor and advise committees of times and what is required. The treasurer should present to the auditor all of the following:

1. The previous year’s original audit report (a copy is kept in the Charter Information folder –it may be convenient to also keep a copy with your Treasurers records).

2. Reconciled cash book.

3. Receipt books for the whole year.

4. Treasurer’s monthly reports for the whole year.

5. Statement of Receipts and Payments for the year to be audited (part of the cashbook spreadsheet file).

6. Bank statements for the whole year with bank reconciliations completed. Ensure these cover the end of the financial year. If there are large outstanding cheques as at year-end, also include January statement to show they were presented.

7. Bank deposit book(s)

8. Cheque butts.

9. Paid accounts in cheque order, most recent at the top. Ensure all cheques have documentation.

10. The minutes of the committee for the year. Ensure that minutes for every month have an original signature indicating their acceptance by the committee, except December, which would not yet have been approved.

All of these will be returned with the Audit Report. The Report will include a disclaimer, indicating that he/she cannot verify what monies were received before they were receipted. Provided everything is supplied to the auditor (well-organised, balanced, reconciled and complete), the audit should take 1-2 weeks. A checklist to help prepare for this is included in section 6.

Store old records

After the audit has been completed, pack up and store records separately as follows: 1. Minutes, cashbook, annual financial statements 2. Bank statements, GST returns, correspondence, cheque butts & deposit books 3. Invoices

11

Put them into an envelopes/small box and label the container clearly as to what is inside and what year it is from. You need to keep the past years’ records for reference. Retain records at the kindergarten in a dry, safe place (not the garden shed) for seven years. After seven years, send documents (1) to the Hocken Library (at University of Otago), documents (2) and (3) may be destroyed

Cheque Signing Authority

Once the new Committee is formed after your AGM, new cheque signing authorities must be filled out and returned to your branch of Westpac Trust. Online banking authorities must also be updated Visit your Westpac branch for the forms required.

12

5. MISCELLANEOUS

Fundraising

Checking Monies Received Fundraising organisers should give you the money already counted. You should check it with them to ensure you agree. In the case of large amounts (i.e. over $500), it is a useful safeguard for both to sign the receipt. Suggestion: If there are several parts to the event (e.g. stalls at a craft evening), you may wish to keep the money for each separate. This allows you to see where best profits are made and split GST inclusive/exclusive items.

Floats (Cash used as change at a fundraising event) If a float is required, cash a cheque. You may specify what amount of each denomination if required. This cheque is entered in your cash book as a fundraising expense (gst is ‘yes’). Documentation should be kept with your invoices which states: cheque number amount date what it is for, e.g. float for stall. As a safeguard to show it is a legitimate expense, both Treasurer and Chairperson should sign this page.

Expenditure Despite the temptation to do so, fundraising expenditure MUST NOT be reimbursed from cash income from a fundraising event; e.g. a committee member is collecting and paying for the cheese for making cheese rolls. He/she must obtain a cheque or be paid through online banking to reimburse their expense, and must provide an invoice to evidence their expense. He/she may NOT use cash received from orders of the cheese rolls to pay for the cheese. General Rule: Any fundraising activity where you purchase goods/services to re-sell to the community ALWAYS has GST included in both income and expenditure:

Some grants are GST exclusive, for example, Community Trust of Otago, KOCCT,NZCT, Bendigo, Pub Charity.

All games of chance at fairs/fetes such as chocolate wheels, lucky dips etc are GST inclusive as they are like raffles - you are buying a chance to win. It doesn’t matter if the prizes are donated or not.

.

RAFFLES - are all GST inclusive (because when you buy a raffle ticket you buy a chance to win - regardless of whether the prizes are donated or bought).

13

Investment with DK/Realising Investments

DK recommends that no more than $2,000 be kept in the kindergarten cheque account. All excess money must be invested in the Association Investment Fund to ensure that it is invested with a 100% secure depositor. As DK invests in bulk, they are able to get better interest rates than individual kindergartens. All that is required is that you send a cheque, with a letter indicating that you wish it to be invested (See section 6 for letter example). A deposit may be made direct to the DK account, and the letter sent to DK – please call the admin office to arrange if you intend to use this option. Withdrawals can be available within three working days of receipt of a letter requesting money from your investment. This letter must be signed by three office bearers of your committee (See section 6). Investments can be paid directly into your committee bank accounts. Interest on Investments is paid out February/March each year by DK .

Subsidies/Grants

Kindergartens can apply for Grants from many outside organisations. Community Trust grants money to many kindergartens every year (applications may be made at any time and are available at any Westpac Trust branch). Pub charities are another good source of funds often financed by ‘pokie’ machines. Many pubs are very willing to give to local causes. You don’t know until you ask. Kindergartens cannot obtain money from the Hilary Commission, as we are Government funded. There is a booklet outlining what grants are available from the Community Development Group (Internal Affairs), Moray Place, Dunedin, Phone 477-1274, www.dia.govt.nz.. When the Ministry of Education has “surplus” funds available, they announce a round of ‘discretionary grants’. All manner of early childhood centres can apply for the same funds as kindergartens. There is usually three to four times as much money applied for as is available, so we are very fortunate to receive a grant. Applications are graded, with particular criteria, e.g. health and safety given priority. Application is made through the DK. Due Dates

GST Return to DK 20th of March, May, July, Sept, Nov and Jan Annual accounts to DK for audit Mid January Annual financials & treasurer’s report for AGM Mid February Bank Reconciliation Monthly, as bank statements are received Meeting Report Monthly

Stale/Unpresented Cheques

A cheque is ‘stale’ when it has not been banked six months after its date of issue. Then, in theory it should not be honoured by the bank and should be returned to you for re-dating. However, it has been known for banks to honour stale cheques. You may, therefore, wish to cancel it after six months. There is a charge by the bank for a Stop Payment. Should you have an outstanding stale cheque when doing the December bank reconciliation, it is written back into expenditure as a reversal, i.e. entered as ‘sundry income’ which will result in a deduction from the total, thereby cancelling the original entry. This occurs regardless of the financial year the payment was made.

14

Cancelled Cheques

Cut out serial number on cheque and attach it to cheque butt - mark “cancelled”. Destroy the cheque. Insurance

All NZK kindergartens are collectively insured with a Wellington broker. The excess on our policy is $250.Claims under this amount cannot be made. If your kindergarten is broken into or vandalised, the Police and DK must be informed immediately.

All claims will be processed by DK. Kindergarten resourcing (not paid by DK)

DK covers costs of all utilities, cleaning, insurance and cyclical maintenance. Also covered are most IT maintenance expenses for computers and IT hardware purchased by DK for administration purposes.

There are only two on-going expenses that are the responsibility of the committee:

One wheelie-bin empty per week is paid by DK; any additional bins at the curb for collection will be billed to the kindergarten committee at the end of each term.

Printer purchase / lease and printing consumables are the responsibility of the teaching team and committee. This expense is often covered by the committee through fundraising efforts, or parent donations, or is shared between teaching team funding and the committee.

15

6 FORMS

a) Making an Investment - Letter

b) Realising an Investment - Letter

c) Annual Budget – (Income & Expenditure by month)

d) Audit - Financial Checklist of documents to return to DK in January

16

6 a Making an Investment - Form Letter ___________________________ Kindergarten ___________________________ (Address) Dunedin _______________ (Date) Dunedin Kindergartens P O Box 3076 Caversham 9045 DUNEDIN Please find enclosed $__________ to be invested with the association on behalf of _________________________ Kindergarten. Yours sincerely,

___________________ (Treasurer)

17

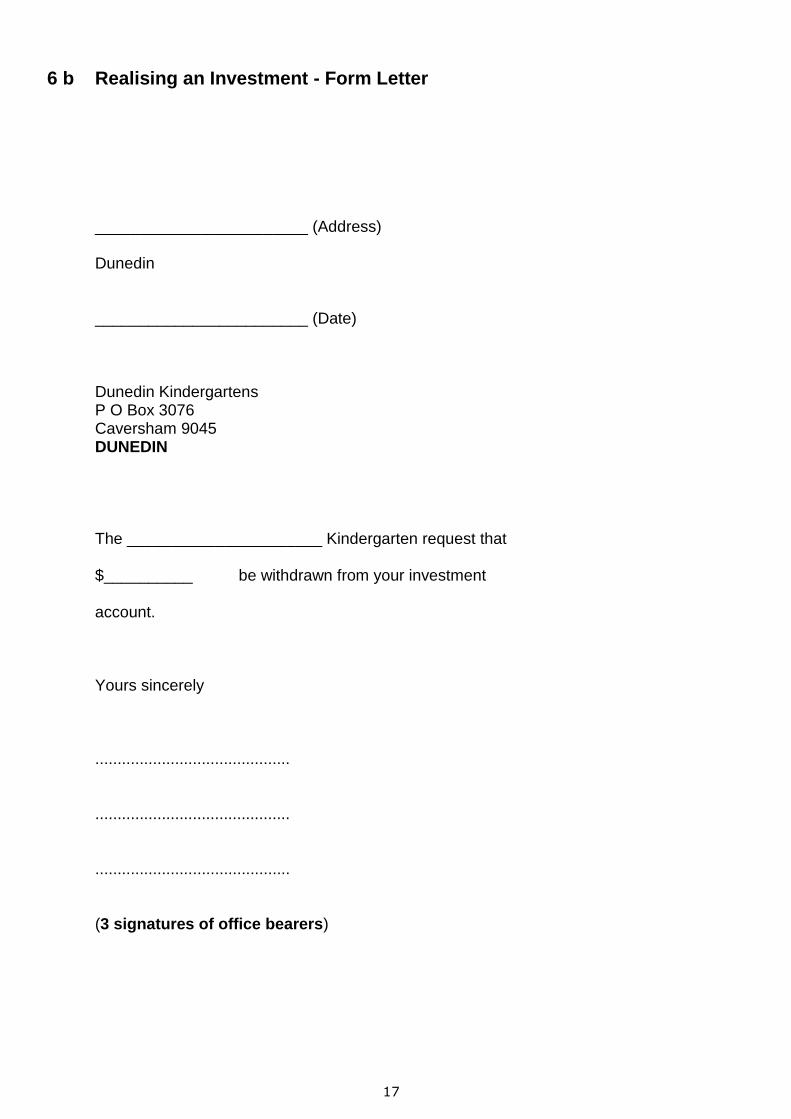

6 b Realising an Investment - Form Letter ________________________ (Address) Dunedin ________________________ (Date) Dunedin Kindergartens P O Box 3076 Caversham 9045 DUNEDIN The ______________________ Kindergarten request that $__________ be withdrawn from your investment account. Yours sincerely ............................................ ............................................ ............................................ (3 signatures of office bearers)

18

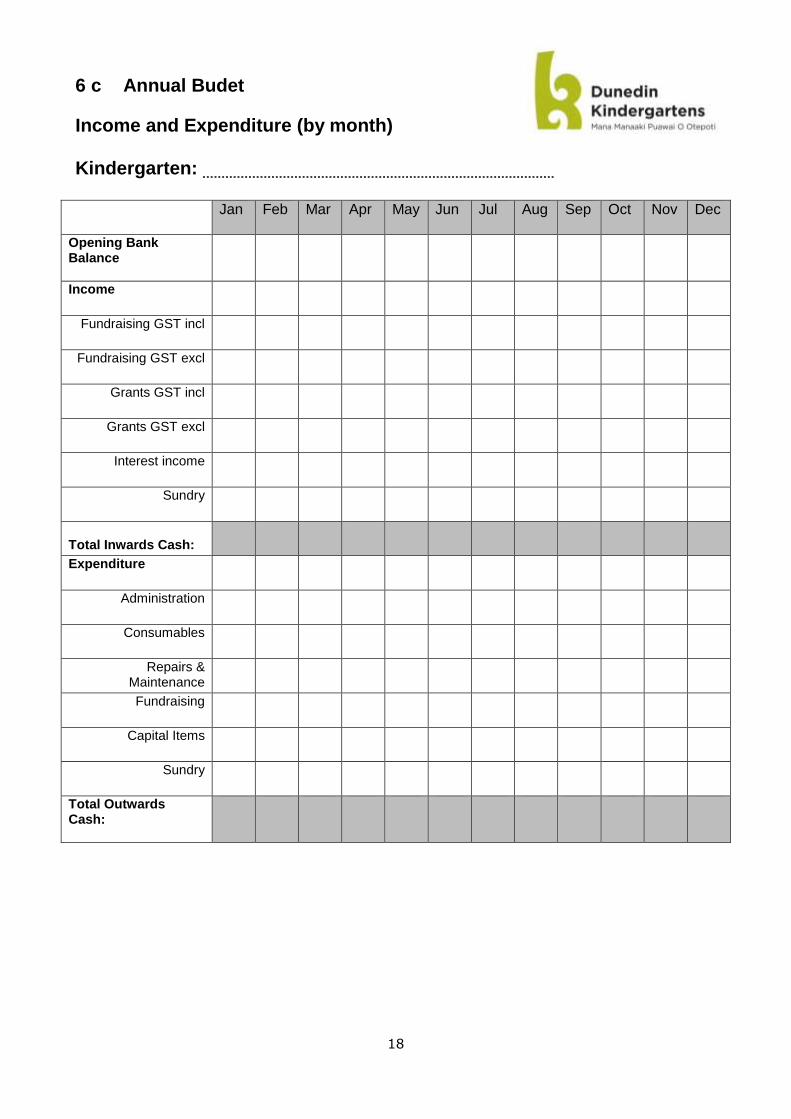

6 c Annual Budet

Income and Expenditure (by month) Kindergarten:

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening Bank Balance

Income

Fundraising GST incl

Fundraising GST excl

Grants GST incl

Grants GST excl

Interest income

Sundry

Total Inwards Cash:

Expenditure

Administration

Consumables

Repairs & Maintenance

Fundraising

Capital Items

Sundry

Total Outwards Cash:

19

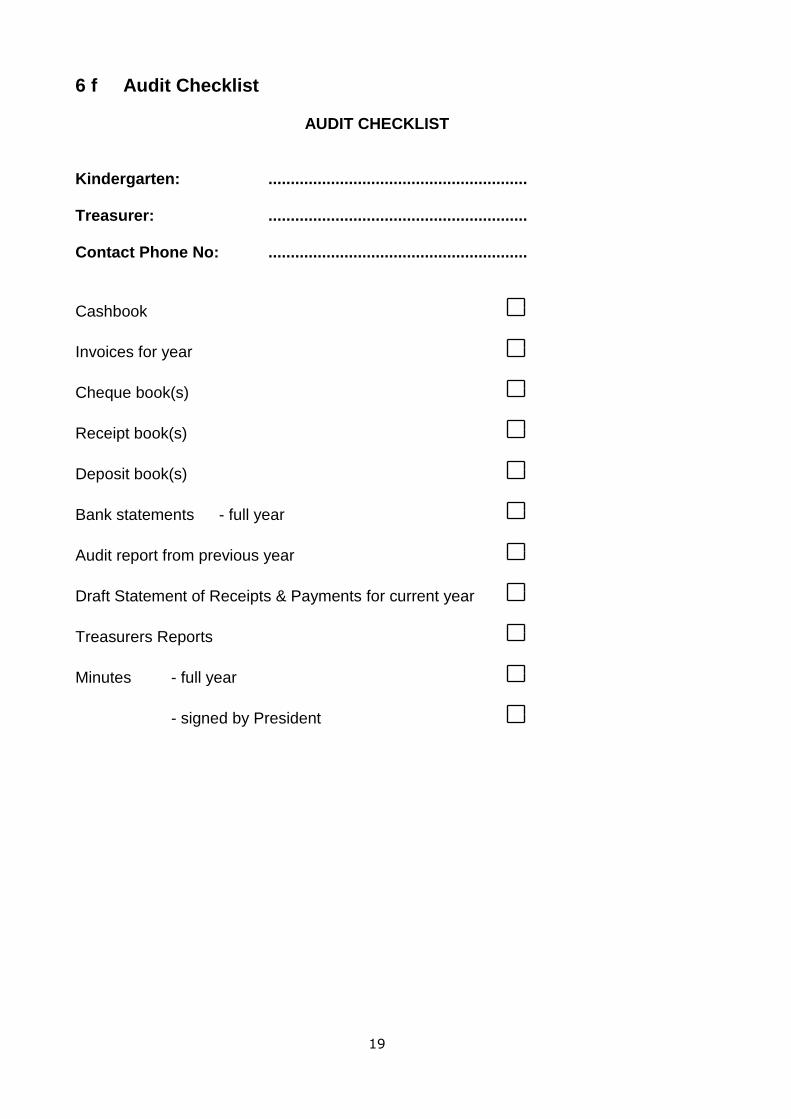

6 f Audit Checklist

AUDIT CHECKLIST

Kindergarten: .......................................................... Treasurer: .......................................................... Contact Phone No: ..........................................................

Cashbook

Invoices for year

Cheque book(s)

Receipt book(s)

Deposit book(s)

Bank statements - full year

Audit report from previous year

Draft Statement of Receipts & Payments for current year

Treasurers Reports

Minutes - full year

- signed by President

20

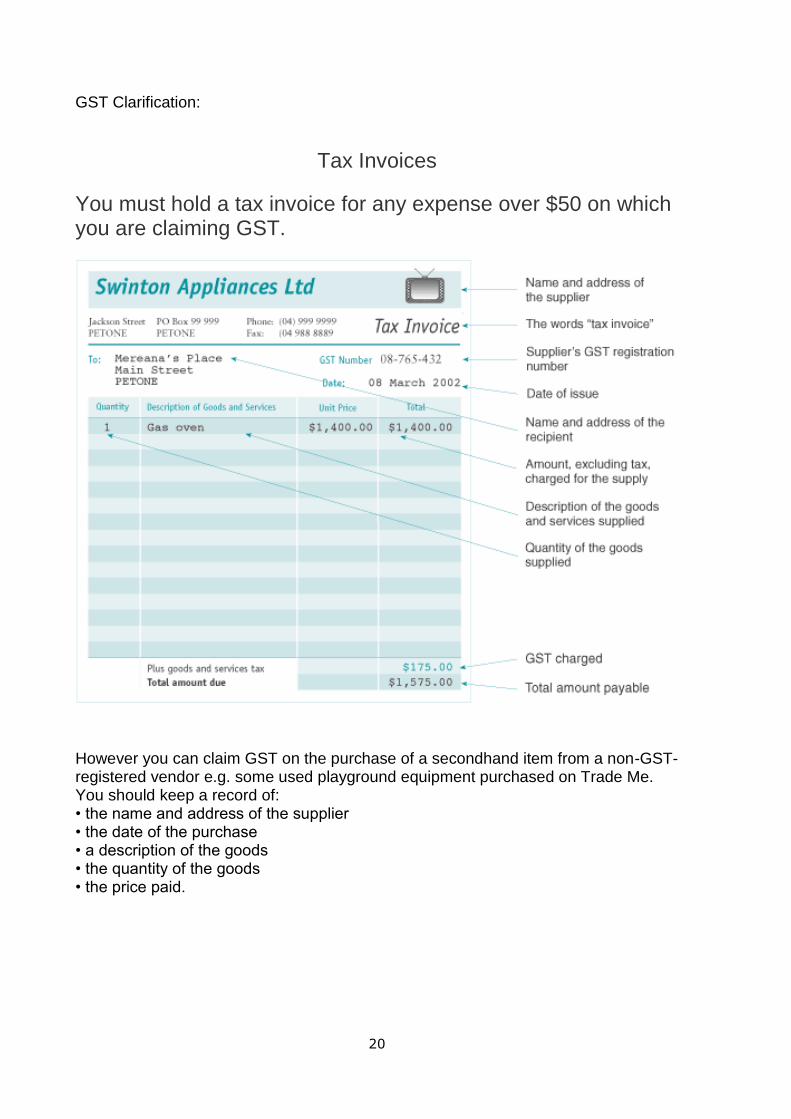

GST Clarification:

Tax Invoices

You must hold a tax invoice for any expense over $50 on which you are claiming GST.

However you can claim GST on the purchase of a secondhand item from a non-GST-registered vendor e.g. some used playground equipment purchased on Trade Me. You should keep a record of: • the name and address of the supplier • the date of the purchase • a description of the goods • the quantity of the goods • the price paid.

21

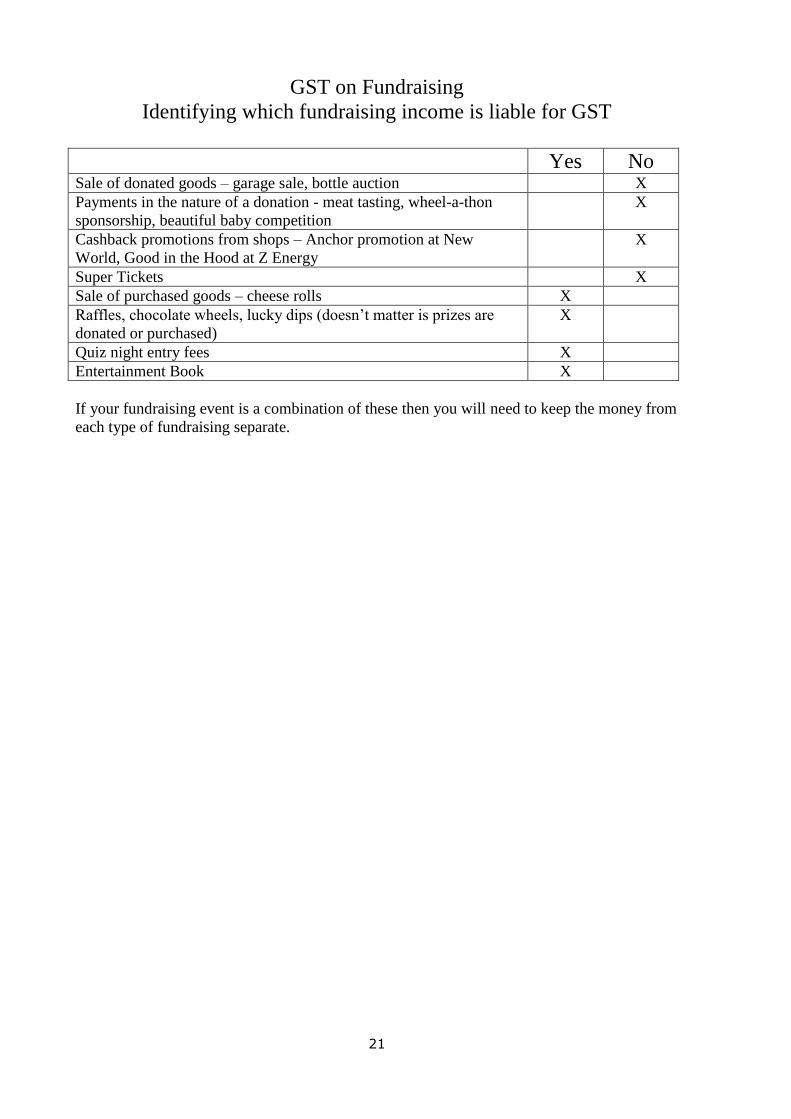

GST on Fundraising

Identifying which fundraising income is liable for GST

Yes No Sale of donated goods – garage sale, bottle auction X

Payments in the nature of a donation - meat tasting, wheel-a-thon

sponsorship, beautiful baby competition

X

Cashback promotions from shops – Anchor promotion at New

World, Good in the Hood at Z Energy

X

Super Tickets X

Sale of purchased goods – cheese rolls X

Raffles, chocolate wheels, lucky dips (doesn’t matter is prizes are

donated or purchased)

X

Quiz night entry fees X

Entertainment Book X

If your fundraising event is a combination of these then you will need to keep the money from

each type of fundraising separate.