Embed Size (px)

Citation preview

t. +44 7775 230 499 e. [email protected] e. . [email protected]

TravelViewIQ: COVID Recovery (Travel)

Summary of industry conferences, events and opinion

Q4 2020

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Richard is a Sales, Sales Operations and Strategy specialist

• 20 years of experience in driving revenue and share performance• 10 years British Airways

• 7 years Travelport GDS

• 2 years Etihad Airways

• Experience North America / Africa / Europe / Asia / Middle East

• MBA 1998

• Founder, TravelViewIQ

• Richard is currently located between the UK and Singapore.

Introduction

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Post-COVID recovery outlook

• International and domestic key travel trends

• Industry analysis and opinion• Aviation

• Online Travel Agencies – next step

• Airline industry – specific airline deep divBl

Information sources OAG / CAPA Conferences / IATA / Bloomberg.

Agenda

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Post 2020 Landscape

Fewer airlines, reduced capacity, fewer routes, consolidation – innovation is key

Government subsidies leading to protectionism –inconsistently applied – particularly intercontinental

Market sectors returning quickest are likely to be the most price sensitive – domestic / SH leisure

Brain-drain from the industry as furlough schemes expire and employees are forced to other sectors

Asset values will decline, debt will become more expensive, sector investment will dry up

Huge pressure on full service premium focus network operation airlines who relied on corporate travel

Huge opportunity to wean airlines from legacy technology which has been a barrier to innovation

Costs can dramatically decrease and retailing can be dramatically enhanced using APIs

The demands of travellers will evolve, and they ways of selling to them will need to adapt

With downward pressure on demand and yield, airlines will need to radically optimize retailing opportunities

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• In 2009 – 0.4% drop in Pax numbers (GFC)

• In 2020 – forecasted to be a 60% pax number drop

• In a good year, the industry will make c.$35bn profit (50% of that is domestic USA)

• 40% of full service carrier revenue (FSC) is business / corporate travel. As of October 2020 that is down 95% YoY

• Assumption this will return to c. 40% by the end of the year 2021 (back-end loaded)

• LCC market share increased by 2%-5% YoY; less so in South East Asia as international travel has stopped

2020 in context

Source: IATA

60% widebody fleets – Grounded

t. +44 7775 230 499 e. [email protected] e. . [email protected]

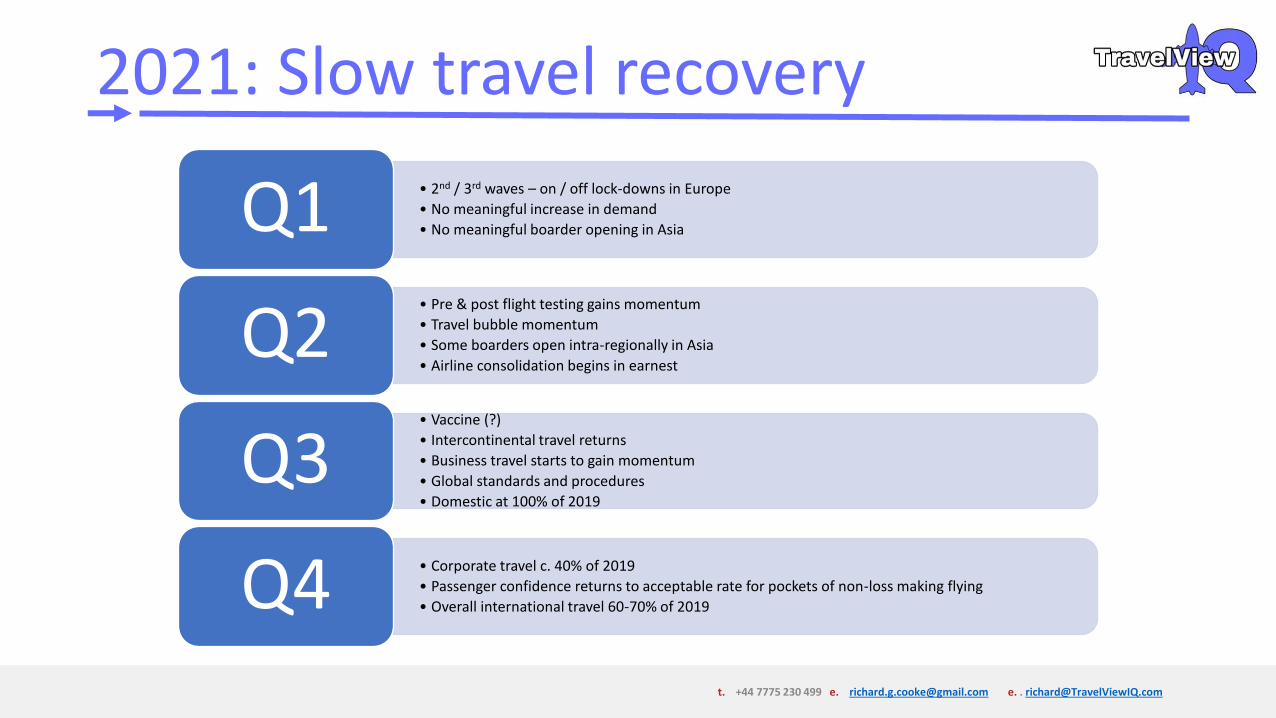

• 2nd / 3rd waves – on / off lock-downs in Europe

• No meaningful increase in demand

• No meaningful boarder opening in AsiaQ1• Pre & post flight testing gains momentum

• Travel bubble momentum

• Some boarders open intra-regionally in Asia

• Airline consolidation begins in earnestQ2

• Vaccine (?)

• Intercontinental travel returns

• Business travel starts to gain momentum

• Global standards and procedures

• Domestic at 100% of 2019

Q3• Corporate travel c. 40% of 2019

• Passenger confidence returns to acceptable rate for pockets of non-loss making flying

• Overall international travel 60-70% of 2019Q4

2021: Slow travel recovery

t. +44 7775 230 499 e. [email protected] e. . [email protected]

China Domestic Capacity

Source: OAG

- 100% domestic capacity by Sept 2020

- Yields?

t. +44 7775 230 499 e. [email protected] e. . [email protected]

USA Domestic Capacity

- 50% domestic capacity by Sept 2020

Source: OAG

t. +44 7775 230 499 e. [email protected] e. . [email protected]

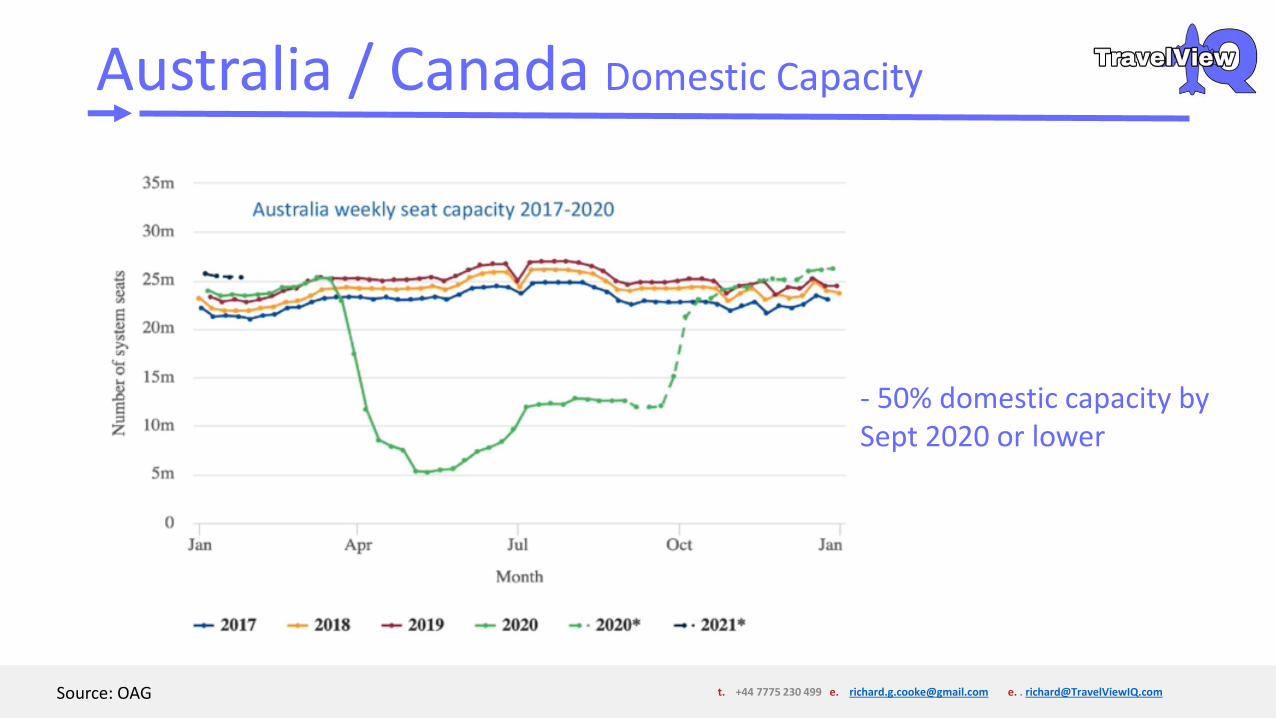

Australia / Canada Domestic Capacity

- 50% domestic capacity by Sept 2020 or lower

Source: OAG

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Airline Industry Debt

Source: Bloomberg

- This graph does not include $47bn in bonds (Bloomberg)

- Credit ratings have changed meaning that interest payments higher

- Where’s the money going to come from?

t. +44 7775 230 499 e. [email protected] e. . [email protected]

‘TOP’ Airline credit ratings

Source: IATA Economics

- 60% of worlds leadingairlines are:

- Highly speculative- Extremely speculative- Little prospect of recovery

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Regional Outlooks – YoY August & October

Source: OAG / CAPA

Overall View - October

International Capacity

2019 2020 August

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Most governmental support and airline restructuring were based on stability by end of 2020 – this now will not happen

• Cash will run out in 6 months – what will happen next?• Phase 1 = Travel corridors (bilateral bubbles)• Phase 2 = Intra regional short haul• Phase 3 = Governmentally supported Long haul (because business travel will

not recover for years)

• A new customer profile:• Books closer to travel• More price sensitive• More demanding in terms of safety• Duty of care for corporate travel

Low yield returns quicker

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Latin America: Traffic bottomed out in April. Still large COVID cases – very slight traffic increases over the last few months (e.g. Peru / Columbia domestic). Brazil did not fully cease; 60%-80% resumption by year end for 2 of the largest Brazilian carriers.

LATAM, AeroMexico, Aviana – filed for bankruptcy. Resizing activity

North America: Profitable business travel normally resumes in September however obviously this year it will not, causing airlines to brace for particularly challenging end of 2020

• Between May / August down c.70%. US is slightly better than Canada

• 65% of fleet ‘active’ by end September YoY

• US Domestic 40-50% by end of year, International c.10%

50% of aircraft in service are operating

Delta – quoted that the airline has only obtained 25% of pre-COVID revenues

Furlough initiatives are ending meaning sizable job cuts over autumn

Regional Outlook: Americas

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Europe: Like elsewhere, March / April RPKs down -90% YoY. Most European carriers do not now report monthly pax numbers

A higher share of LCC carriers have returned to operations vs. Full Service Carriers

Ryanair July – 60% down in capacity and 70% down in pax numbers – anticipated to be lower in November due to lockdowns

• Confusion and return of travel restrictions

• Russian Domestic market has returned at a faster level than others meaning it’s a much higher proportion of overall European capacity than it was in 2019

• Western Europe leads the way in terms of international capacity (mainly intra Europe) at -60% YoY

• LCCs have brought aircraft back quicker than Full Service (driven by RyanAir and Wizz)

August – Seat numbers -55% YoY – has been for some weeks – however this is -61% in October

Stagnation – due to second waves

Regional Outlook: Europe

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Could be below 30% by the end of November

• Load factors <50%

• Not all carriers are getting bail-outs

• Europe – US <70%

• Politicized – no common approach to testing or quarantine

• Pre & post testing – no success on testing protocol

Europe Mid Oct 2020 position:

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Fragile led by China and Japan

China: Lowest point in Feb, now at 72% of 2019 totals (domestic at 90% and full recovery by end of year)

Domestic routes generate most profits, stimulation of market through heavy discounting

Japan: Huge domestic market and government stimulation. Resumed domestic travel could mean the industry return to profitability in Japan

Refocus on Cargo due to rush orders for PPE etc.

‘Sightseeing’ flights

Taiwan / South Korea: Very small domestic markets however success at COVID suppression based on experience of previous pandemics

South Korea – much more competitive market than Taiwan leading to liquidity issues for airlines even before COVID

Regional Outlook: North Asia

t. +44 7775 230 499 e. [email protected] e. . [email protected]

One of the most impacted regions. RPKs and ASKs (extremely low load factors even compared to global average)

Very limited domestic markets (other than Saudi Arabia)

All airlines largely shut down, other than Qatar Airway which did not reduce operations to the extent of others, focusing on re-patriations

• Largest A380 operator – aircraft economics were shaky before 2020 but now accelerated by COVID

• Moving from 777 to 787 aircraft orders (more than 100 seats lower per aircraft)

Emirates stating they want to serve all previous destinations by mid-2021 (lower capacity)

IATA: Job losses in region could be 1.5m (over half employed in aviation related industries) – and $85% of associated GDP

Regional Outlook: Middle East

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Been successful in obtaining financing. 4000 staff cuts and has deemed 26 aircraft surplus aircraft (1/3rd A380s phased out & older 777. Aircraft order deferral

SIA: no domestic network, boarder closures. Anticipate 16% pre-COVID levels by year end.

• 8500 role reductions, existing staff have been asked to take revised terms. Dragonair will merge into CX

CX: Key focus is restructuring, workforce re-alignment.

• ‘Plan B’ is to shut down the company and re-start under a subsidiary brand such as Firefly (now turboprop but likely to move to MH’s 737s)

MH: ‘Plan A’: Rescue plan being attempted based on debt restructuring.

AirAsia X: may have to liquidate if unsecured debt is not waived

TG: Rehabilitation plan in bankruptcy court. Selling 34 aircraft. 5000 employees early retirement

NOK also going through bankruptcy court

NOK Scoot shut down in June

Regional Outlook: SEA

t. +44 7775 230 499 e. [email protected] e. . [email protected]

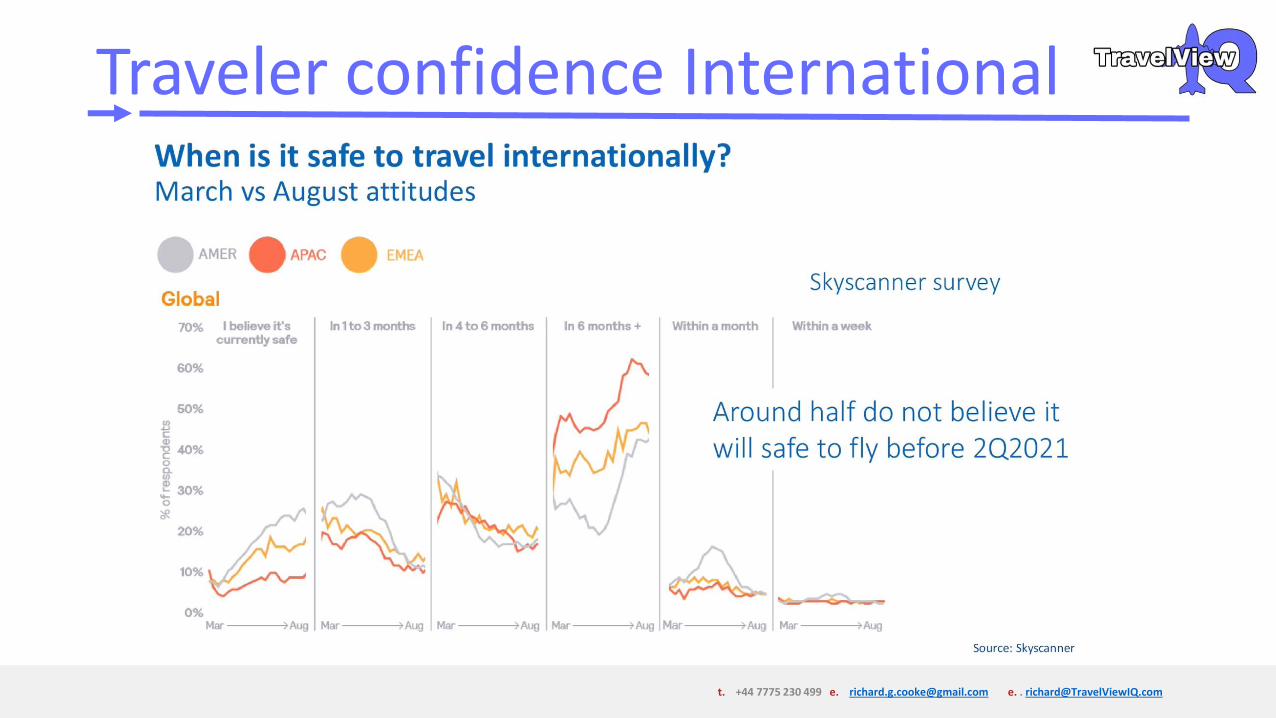

SkyScanner Insights: Traveler Pulse

When will it be safe to travel internationally?

• Now = 19% (going DOWN week on week)

• +6 months = 47%

Regional Outlook

• Asia = 8% - however interestingly 61% at +6 months

• Europe = 24%

• North America = 17%

Source: SkyScanner Pulse

t. +44 7775 230 499 e. [email protected] e. . [email protected]

China Deep-dive

Effective Suppression – but setbacks

Revenge Travel – world’s largest domestic market

Passenger Confidence – QR Codes and Tracking

Govt Sponsored Seat Sales & travel passes

Governmental support

Source: SkyScanner Pulse

t. +44 7775 230 499 e. [email protected] e. . [email protected]

•Huge numbers of redundancies throughout global aviation and associated industries have made this even more unlikely

•There will be a huge number of consultants vying for business amongst the airlines that survive, but many of these consultants will not have industry experience and background

Many traditional airlines do not have the in-house expertise to thrive in the post-COVID market conditions

•Desperate times call for desperate measures. Blockers to model change simply cannot be viable

There are a huge number of efficiencies that global aviation can achieve, but this will need to be a coordinated approach

•Proven commercial leaders, with a track record of success from within airlines and within technology players, are ideally suited to help airlines navigate the post COVID landscape

Very few airlines optimize profit seeking strategies e.g. merchandising and ancillary sales

What we knew before COVID and the data that was captured may be of limited use

•2020 = -90%

•2021 = -50% to –75%

•2022 = -25% to –50%

Large corporate travel budgets will reduce for the forseeable future (from 2019 levels)

•however there will be a long lead time for a vaccine to be rolled out in a way that will make travel safe

Vaccine and testing will have dramatic impact on consumer confidence

•however the temptation to discount to win volume and share will be too much – as that was the 'old normal'

Airlines to raise prices, and to improve the profitability per passenger, taking advantage of low fuel prices

Top Line Opinion - TravelViewIQ

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Low cost – not only in terms of fares but cost base

• Work assets harder (e.g. average aircraft flying time / m2 utilization)

• 2nd tier airports / labor costs / better ancillary sales / fewer higher expense items (e.g. catering)

• Less of a proposition for business travellers, more of a proposition for VFR (Visiting Friends & Relatives) and Leisure

• Which market segments are likely to return quickest?

• Low cost carriers – traditionally higher liquidity

• Cost effective ‘value models’

LCCs vs. FSCs

t. +44 7775 230 499 e. [email protected] e. . [email protected]

A new airline model?

• Demand likely to be reduced / network sizes likely to be consolidated to profitable routes

Airlines likely to be smaller and leaner post-COVID (e.g. Air New Zealand / VS).

• LCC model has performed better historically after crises (Bill Franke)

• Ryanair states it has $4bn cashflow and are ‘relaxed’ about losing $200m in Q2 2020

• LCCs nimble, agile and flexible – will be best positioned to adapt

• LCCs rely heavily on fast turn-around (fast boarding and cleaning) onboard ancillary sales, and often bussing gates, which will all be more challenging)

• Traditional airlines need to radically restructure themselves around profitability

• Traditional airlines will need to be much better retailers on a much lower cost base

• COVID needs to be the opportunity to break-down persistent blockers to efficiency

LCC business model generates cash, 30% lower cost. Traditional airlines burn cash

• Reduced ‘shelf space’ on aircraft – airlines need to maximise their ‘revenue per square metre’

Bigger aircraft with ‘bargain’ economy seats will retire (A340 / 747 / even A380 and older 777)

• Long haul international only likely to pick up significantly post vaccine

Domestic and Regional operations likely to be the only sources of cash in the near term

Hub strategy will be revised (e.g. Gatwick in the UK)

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Some airlines won’t survive (c.30%)• These will be airlines:

• focusing on International• with low levels of liquidity (or no-loan assets to borrow against)• operating in more ‘closed’ regions such as Asia• unable to secure loans or Govt subsidies• unable to squeeze revenue opportunities (such as ancillaries)• unable to unbundle• over-reliant on business travel (not historic but future)• unable to generate higher yields• unable to convert to LCC principles• no other ‘diversified portfolio’ e.g. Freight / loyalty / etc. (Alan Joyce / QF)• can’t reinvest in new business models post COVID – eg embracing technology• lean fleet allowing P2P rather than 6th freedom• unable to enforce capacity discipline (RASK)

Which airlines are at risk?

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Corporate travel down approx. 95%

• Ways to protect TMCs• Less reliance on debt

• Reduced fixed cost

• Technology in house

• Diversified client base (including Government travel / Domestic / Primary to Tertiary industries)

Corporate Travel Outlook

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• No Asian countries in the ‘Hot Spots’

• Perhaps due to effective suppression thanks to experience with previous outbreaks

• Certain countries have been impacted more – likely due to a mixture of size, population movements and governmental response

Pandemic Hot-Spots

t. +44 7775 230 499 e. [email protected] e. . [email protected]

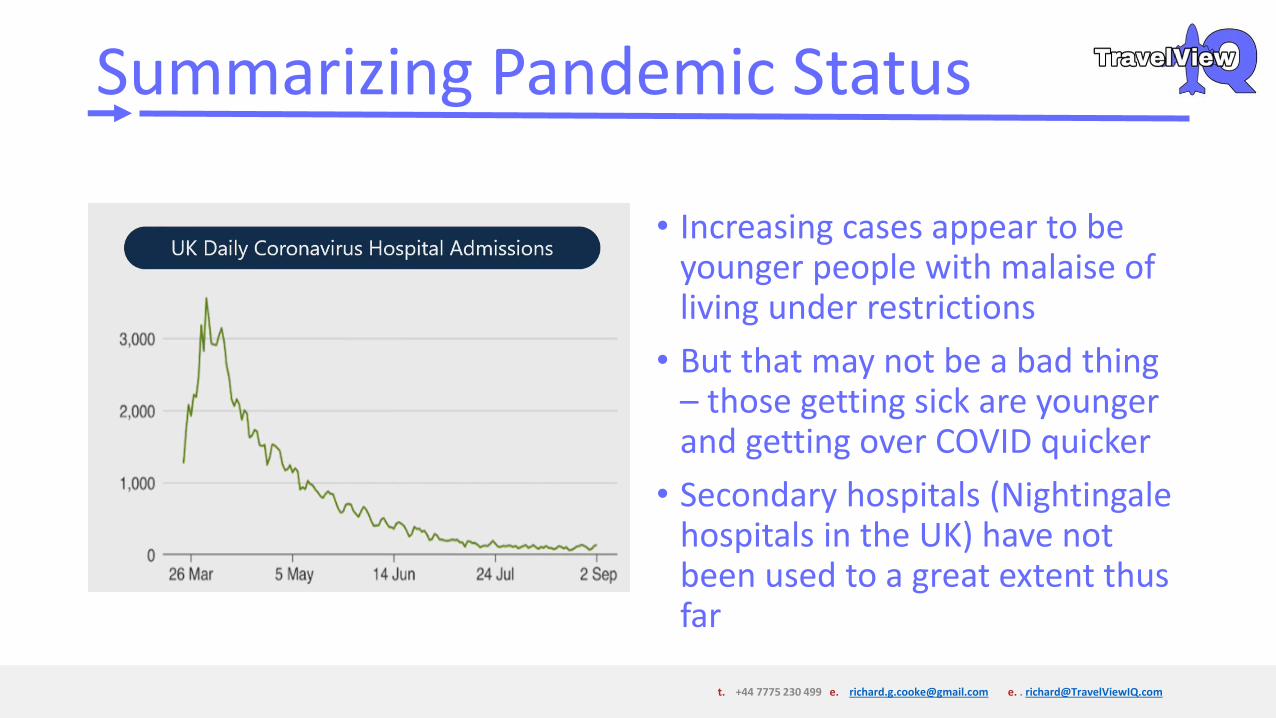

• Increasing cases appear to be younger people with malaise of living under restrictions

• But that may not be a bad thing – those getting sick are younger and getting over COVID quicker

• Secondary hospitals (Nightingale hospitals in the UK) have not been used to a great extent thus far

Summarizing Pandemic Status

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Currently around 3k clinical trials

• 600 pipeline drugs (Therapeutics & Vaccines)• Re-purposed drugs• Specific anti-virals• Prophylatics

• Only <10% of trials have been completed

• Clinical trials are following the virus hotspots

• 200 vaccines in development

• 30 in clinical trials

• Huge pace and collaboration across the industry

Vaccine R&D

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Pre-travel to avoid quarantine essential to improve confidence to travel and to provide governmental confidence to loosen restrictions on travel

• False positive rates appear very low <1%

• Correct identification of COVID cases >95%

• Significant innovation ongoing – very low rates of false positives and false negatives

Rapid Testing efficacy

t. +44 7775 230 499 e. [email protected] e. . [email protected]

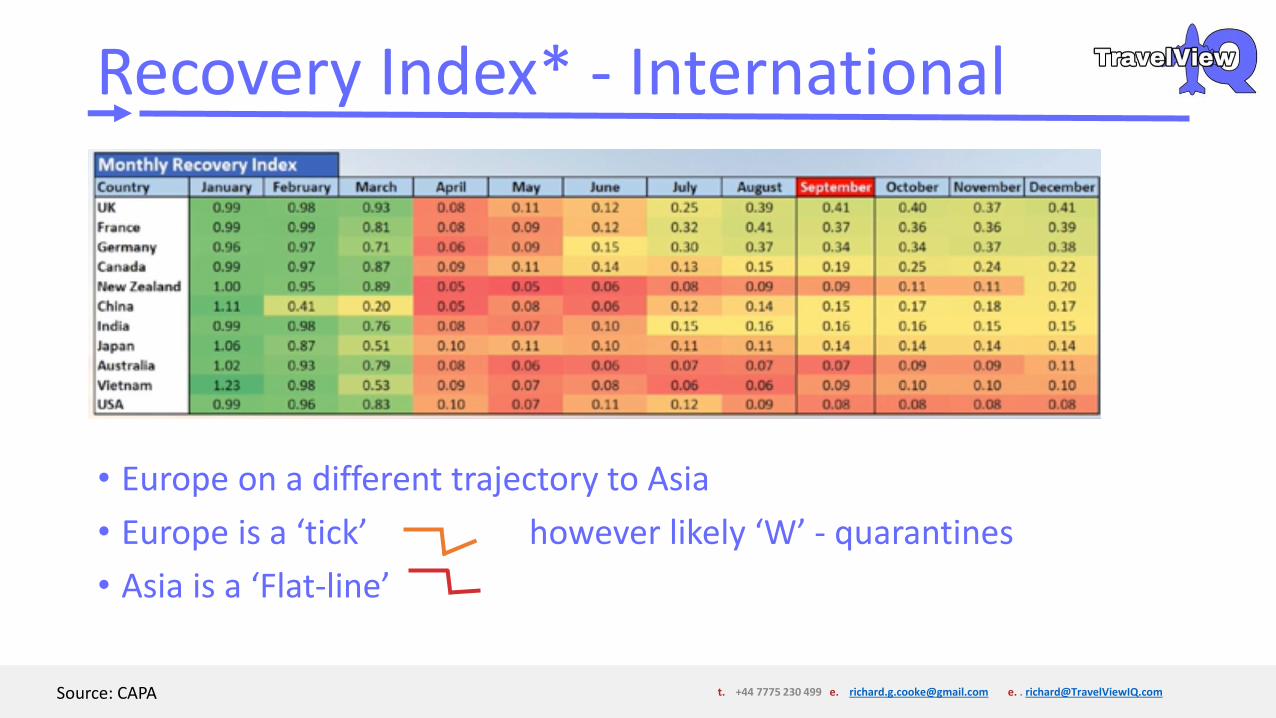

• Europe on a different trajectory to Asia

• Europe is a ‘tick’ however likely ‘W’ - quarantines

• Asia is a ‘Flat-line’

Recovery Index* - International

Source: CAPA

t. +44 7775 230 499 e. [email protected] e. . [email protected]

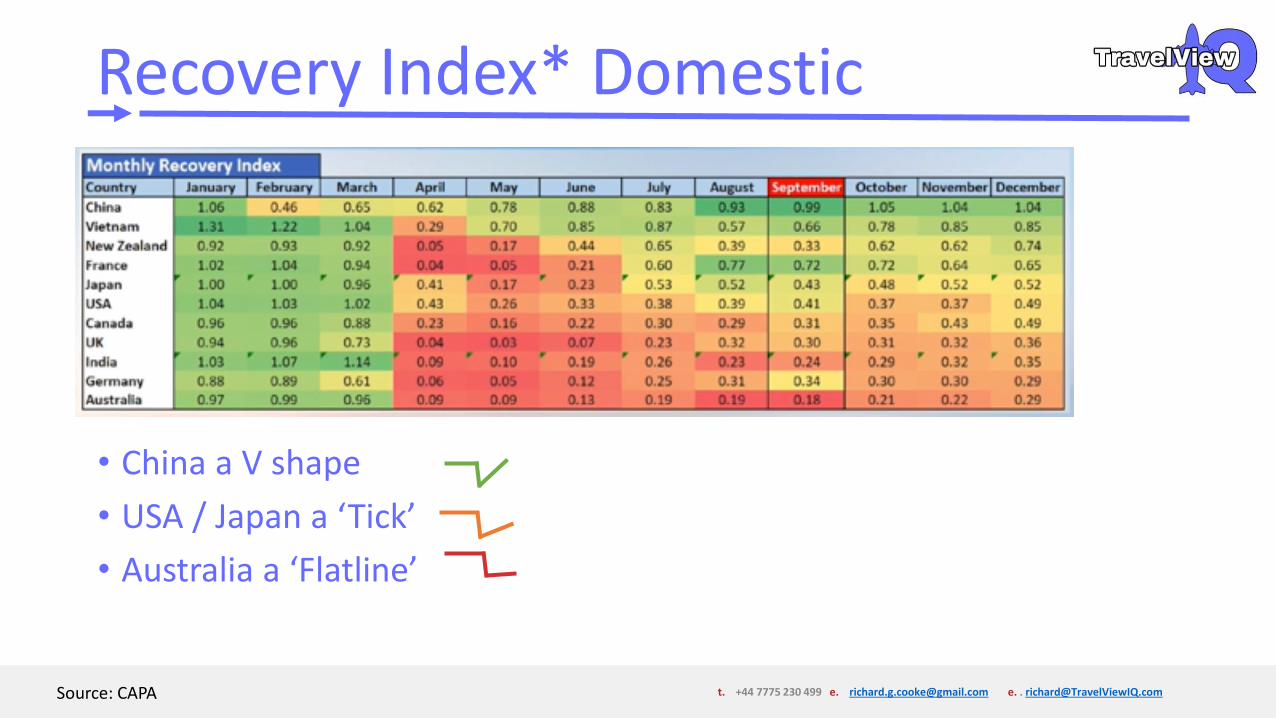

• China a V shape

• USA / Japan a ‘Tick’

• Australia a ‘Flatline’

Recovery Index* Domestic

Source: CAPA

t. +44 7775 230 499 e. [email protected] e. . [email protected]

China Domestic Recovery

Source: CAPA

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Vietnam Domestic Double Dip

Source: CAPA

t. +44 7775 230 499 e. [email protected] e. . [email protected]

Airline CEO & Industry expert Interview Summary

CAPA & Skift Conferences H2 2020

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Great success in smaller destinations domestic USA (more of these have a leisure orientation)

• Commitment to the 737 – previously couldn’t get enough aircraft (due to the 737 Max issue) but now this strategy can fast-forward

• Not turning into a hub carrier, although during pandemic 35% pax are connecting

• Losing c.$10m / day, no end in sight, 20% overstaffed, costing $1bn yearly. In conversations with unions for concessions

• We don’t know if there’s going to be a structural change in the way people travel in the future – on the whole I believe ‘this too will pass’ and people are looking forward to getting back to normal life. However it will take a while.

• Business travel in every recession took 5 years to get back to pre-crisis levels. Southwest well positioned for both business and leisure

• Industry back to normal levels by 2024 – however that’s a ‘wild guess’

Gary Kelly – Southwest CEO (Nov 20)

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Rex: Biggest dedicated regional airline in AU

• No free travel between the states in Australia – REX = most flights are intra-states so not so badly impacted by the states boarder closure (e.g. Queensland 90% of pre-COVID) but Victoria / NSW sizeable impact of boarder closures – which equated to c.65% of REX pre-COVID pax

• REX: expanding out into 737: Trunk routes: Different services and different aircraft type (picking up aircraft from Virgin Australia). Taken delivery of first aircraft, currently in pilot training. Signed leases for 6 aircraft – initial launch in March (operating 5), will start increasing the fleet gradually if this works (one aircraft every month / six weeks after that)

• There will be some synergy between the domestic and regional operations in terms of feed, but also more importantly in terms business operations

• Offering business class & lounges – pitched at the JetStar prices (however an enhanced product); hence attractive to SME

• Aiming for a lower cost base than competitors – extremely tight focus on cost

• SYD – MEL (9 return services initially) will be first, then BRI, then expanding out to the state capitals.

• “Use it or lose it” slot policy. Therefore if airlines are 35% down by March 2021 and give up these slots, then new entrants can take those slots and have grandfather rights for those slots moving forward. (Rex only require 10% of slots for their expansion plans)

• Concern over anti-competitive practices by incumbents to keep the flights to ensure carriers aren’t flying empty planes to keep the slots. Governmental review of slot scheme. Can’t operate services without commercial return, particularly as airlines are receiving govt. funding

• Some things will be outsourced (eg 737 engineering and maintenance) will be outsourced, however overarching view is that outsourcing is giving up profit

Lim Kim Hai – Regional Express (REX) CEO Nov 20

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• $7bn from French Govt, $3.5bn from NL government, but conditions include decreasing environmental footprint and becoming more competitive, therefore focus on strengthening balance sheet.

• VFR traffic after 1st lockdown resumed very quickly

• Importance of a balanced network, including domestic (but this has environmental connotations) – working hand in hand with SNCF

• Network needs to be profoundly changed (pressure from LCCs) – growing Transavia to compete with LCCs

• Decided before crisis to phase out the A380 (& A340) – replacing with A350 and short haul A320

• Commitment to First class in the long term (in a cost-effective way)

• Certain aircraft have ‘quick change’ – can change configuration; however VFR doesn’t necessarily mean less premium cabins, as many premium pax are travelling for leisure

• Business traffic to return to 2019 levels to 2024, however different types of travel e.g. bleisure

• The crisis is a catalyst for business transformation

Anne Rigail CEO Air France Nov 20

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• RyanAir had a positive summer when restrictions were lifted (c. 70% load factors) however Nov is a hard month generally, plus lockdowns / restrictions across Europe, Nov 20 c. 40% of Nov 19

• RyanAir supportive of stimulus but not supportive of Govt bail-outs across Europe which will be c.$30bn; poorly capitalized airlines will be swamped with debt; RyanAir in legal proceedings which could take c.3 years

• Fares will be very low to stimulate the market, however these will be discounted fares (RyanAir) vs. subsidized fares (FSCs)

• RyanAir = lowest unit costs in Europe, Wizz c. 25% higher, EasyJet c. 70% higher• These will be exacerbated by 737 Max, 8% extra seats, 16% less fuel• 210 737 Max orders – the most tested plane in aircraft history

• RyanAir will be well placed to succeed because:• Not saddled with debt• Deals on Staff (reduced salaries)• Deals on Airports – working with airports to generate demand – creation of markets through lower pricing• Deals on Aircraft ownership and maintenance (exacerbated by the 737 Max)

• No plans to fly transatlantic, aircraft utilization / don’t know the market / business travellers don’t go to secondary airports. LC LH hasn’t worked

Eddie Wilson CEO RyanAir Nov 20

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• “Delta has done a great job pivoting on the fly about what’s important to the customer. Before it was schedule and price. Now it’s about social distancing and aircraft cleanliness”. • Bill Lentsch: Chief Customer Experience Officer, Delta: Nov 20

• “Recovering traffic through testing at airports can’t work. It’s just headline grabbing. Look at the disruption when there were changes in security due to liquids – it was chaos!”• Eddie Wilson, Ryanair

• Health insurance incorporated into Emirates offering – Governmental mandate, to give customers confidence of treatment when visiting Dubai

• Dubai welcomed tourism July 7th 2020 due to economic consequences & one of the first countries allowing transiting while ensuring the highest level of safety being implemented across the passenger journey• Adel Al Redha: COO Emirates Nov 2020

Skift Forum: 19 November 2020

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Flat demand seen between Oct & Nov 2020 – no rebound yet

• QR in a strong position due to a variety of reasons:• Less focus on A380 and more focus on 787 and A350 (now the world’s biggest operator of the

A350)• Agility with fleet – twin engine, lower operating costs, higher frequency, good cargo capacity• Agility with destinations based on ever changing govt. regulations / quarantines etc. • Staying in touch with the trade• Monitoring the flows (which are changing regularly and rapidly – was AU, then Americas,

now Pakistan / Iran / Afghanistan etc.)• Cargo – to cover costs, passenger additions as a ‘top-up’• Investment in quality (HIA / Skytrax awards)• Blockade by UAE / KSA in 2017 forced a cutting of destinations, however this provided

resiliency in the QR business, hence has seen growth at a higher rate (2019/2020 double digit) than ME competitors, and although high $ losses, as investment in the future• Associated to this QR is suing for $5bn losses

• FIFA World Cup 2022

Thierry Antinori – CCO QR Nov 20

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Delta isn’t selling 1/3rd of it’s seats so it’s not well positioned until at least March, American ‘a better investment bet’ in part due to the younger fleet

• As things are going, American can last with cash for 9 more months if nothing changes

• Domestic China and Russia are back – there is pent up demand and people will travel

• Low-cost model will outperform the network model in the next 5 years

• I think business travel will come back – 75% of the way back in 3 years

• Wizz and Ryanair = great airlines with great balance sheet

• Copa – great management team

Helane Becker (Cowen) - Nov 2020

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• US: Only 20m doses (both are 2 shot) so this year only enough for 10m each. That isn’t even the frontline healthcare workforce

• Will be well into next year before enough vaccines available to stimulate short term bookings (based on vaccines and availability)

• Vaccine – we don’t know how this plays out in the long term – so policies will be fluid as we find out more

• Immunity passports – complexity around this

• Transmission on planes – very complex environments (e.g. wearing masks properly, if there are more than 1 person infected on a flight)

• Risk perception & awareness: People have different behaviors (mask wearing, social distancing, use of sanitizers) on the plane vs. off the plane (e.g. boarding)

Dr. Angela Rasmussen / Dr Saskia Popescu: Nov20

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Tim Clark does not buy into a ‘new normal’ whereby demand for travel is suppressed for a very long term –believes demand will increase quickly

• “Memories are short” – does not buy into the fact that travel will only return by 2025/6• Underlined the importance of network operation as many routes wouldn’t survive without network operations, e.g. Africa to

Europe / US

• Frustration about lack of consistency of standards, continual changes to quarantines / boarders and metrics being unobtainable

• Key problems in the industry are• Huge debts / governmental involvement / smaller demand / more protectionism / inconsistent subsidies

• Cargo demand huge, repurposing aircraft to carry cargo, returning route operation largely due to cargo economics

• Positive contribution and a reduction of cash-burn

• Not optimistic about pre-flight testing being accepted by many governments (e.g. EU / Europe)

• Even countries such as S. Korea with pandemic experience and effective track and trace have not opened up boarders

• On board showers & bars starting to open (due to brand pressures & stimulation of confidence)

• Environmental issues: other industries have reduced emissions by more, but it’s because they can. Huge advances in aircraft efficiencies but very little alternative to flights for non domestic / non regional travel

Emirates CEO outlook (Oct 20)

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Initial optimism – but continual let-down • South East Asia boarders closed

• Nothing much going to improve in 2020 – hopefully 2021

• Driven by domestic politics & isolationism• Opening based on familiarity and political ties & ‘Trust’

• Rapid cheap & effective testing• Heathrow testing

• Big blockers are not only safety but the practicality of having to quarantine

• This is a ‘good time to be an LCC’ -• Leisure & VFR - Not reliant on business class

• Serve regional destinations – which will likely return first

• Point to Point – don’t require hub dynamics

• ‘Lower Touch’

• In Asia there isn’t the competition of land based travel like there is in Europe & North America

• Although demand and capital isn’t there – aircraft don’t go away• Aircraft are cheap

• Fuel is cheap

• Staff are available

• Borrowing is cheap

• In ASEAN – discussions with Japan / China / Indonesia / Malaysia for travel corridors – the ‘ingredients are there but not the appetite’

Scoot CEO outlook (Sep 20)

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Largest international airline in the world in mid-2020

• Repatriation & Cargo operator – largest cargo operator in the world behind FedEx and UPS

• No uniformity / rules & regulations – making it very difficult for airlines to meet each of the requirements to operate

Qatar Airways CEO outlook (Sep 20)

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• No substantial flying until July 2021 – Long Tail Recovery

• 50% pre-COVID

• A380s parked for 3 years – until 2023 / 2024

• Cash-burn $40m/ week• This was very low compared to some Asian / US carriers >$100m/week

• Testing & Tracing– travel corridors (travel bubbles in Asia)• 15 min vaccine in testing – negate the need for quarantine

• Earlier – Vaccine dependent – however these needs to have standards defined• Without international governmental corporation boarders will stay closed• Bilaterals easier than bubbles

• 35% of all credit card spend in AU is on a Qantas branded credit card• FFP: $500m earnings by 2024

• “The demand is there” – Jetstar had the biggest seat sale in it’s history post-COVID, c. 250 tickets / minute –however only at extremely low yields

• However this was very low yield

• Qantas spent a lot of time and money on distribution strategy• Added value though customized, different offerings directly to individuals – will be a big part of profitability

Qantas CEO outlook (Oct 20)

t. +44 7775 230 499 e. [email protected] e. . [email protected]

• Before the industry experienced ‘short sharp shocks’

• The current TMC business model is 2/3rds funded by suppliers – this will undoubtedly change: business models are unsustainable

• All players in TMC ecosystem have been in survival mode; future travel state likely to be less $ in the ecosystem, particularly as airlines move to TMC

• Airlines = less capacity, lower load factor, lower yield (mix of customers and mix of routes); levers won’t work the same way (e.g. lowering prices won’t necessarily increase load factor).

• If all these are lower then there will be a compounding effect.• Therefore huge cost focus and a requirement to be more nimble to take advantage of business opportunities. Who are the pax (e.g. VFR vs.

Corporate)? Where are they going? How are they buying?

• GDS = transaction based businesses therefore reduced volume, airlines looking to reduce sector fees

• TMCs = impacted by volume reductions and the reduction of supplier revenues because less $ in the ecosystem; therefore if revenues are not coming in elsewhere, TMCs may need to increase prices or fundamentally change business models.

• TMCs need to better communicate their value to control corporate travel costs and negotiate value on behalf of the corporate.• Need to redefine their value proposition. TMCs have perhaps less of a role in domestic, which is going to be a higher proportion of traffic• Post-COVID will be huge amounts of ‘admin’ – an area that the TMC can add value prop

• Each industry segment will be taking a financial hit on multiple fronts.

• Direct sales aren’t that cheap – there is a value of the agent, especially if airlines don’t have marketing budgets anymore

• Can TMCs start focusing on diversifying to other revenue streams such as leisure? Where are the areas they can add value (reporting, expense management, easing admin burden, payments etc.)

Future role of TMC (Panel CAPA Nov 20)