Embed Size (px)

Citation preview

Transportation, Distribution and Logistics in Indiana

Reha Uzsoy, Ph.D., P.E.Director, Laboratory for Extended Enterprises at Purdue

Professor of Industrial Engineering

(765) 494-0829

Supported by the Central Indiana Corporate Partnership

Strengths in Indiana

• Location and infrastructure– Major interstates, crossroads of America

• Extensive industrial base that is used to operating in demanding TDL environments– JIT logistics for the auto companies

• Strong universities• Extensive network of regional campuses

and community colleges

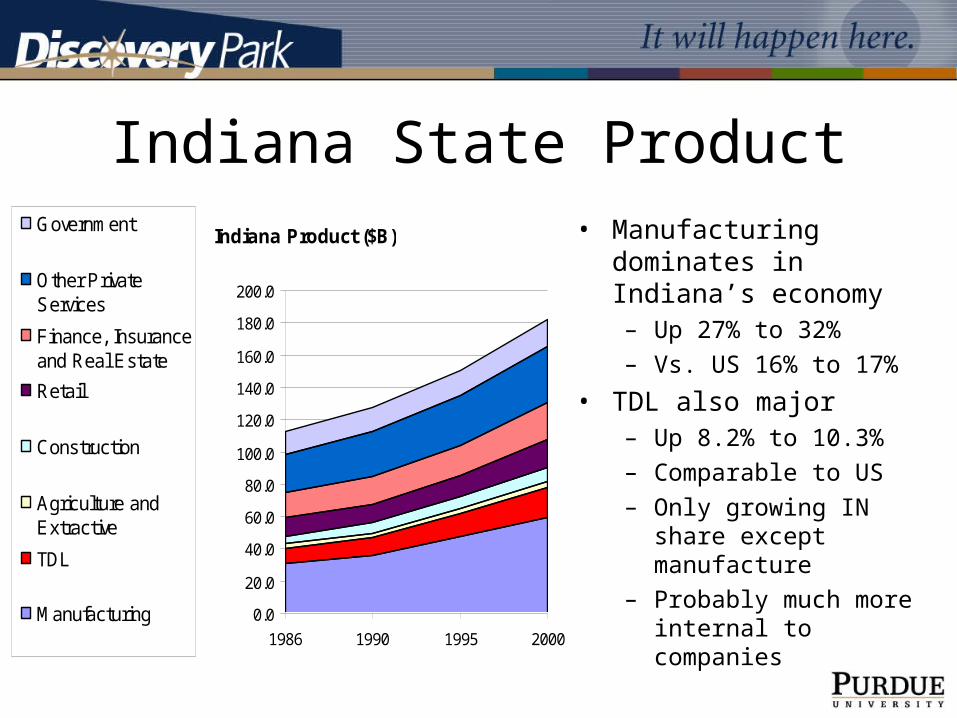

Indiana State Product• Manufacturing dominates in

Indiana’s economy– Up 27% to 32%

– Vs. US 16% to 17%

• TDL also major– Up 8.2% to 10.3%

– Comparable to US

– Only growing IN share except manufacture

– Probably much more internal to companies

Indiana Product ($B)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

1986 1990 1995 2000

Government

Other PrivateServices

Finance, Insuranceand Real Estate

Retail

Construction

Agriculture andExtractive

TDL

Manufacturing

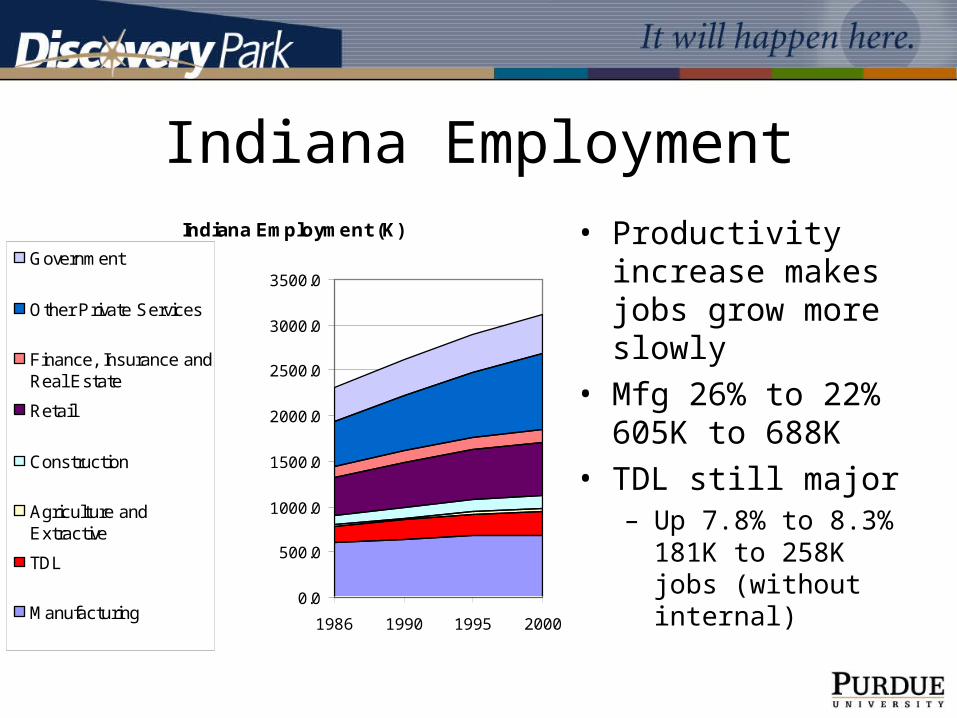

Indiana Employment• Productivity increase

makes jobs grow more slowly

• Mfg 26% to 22% 605K to 688K

• TDL still major– Up 7.8% to 8.3% 181K

to 258K jobs (without internal)

Indiana Employment (K)

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

1986 1990 1995 2000

Government

Other Private Services

Finance, Insurance andReal Estate

Retail

Construction

Agriculture andExtractive

TDL

Manufacturing

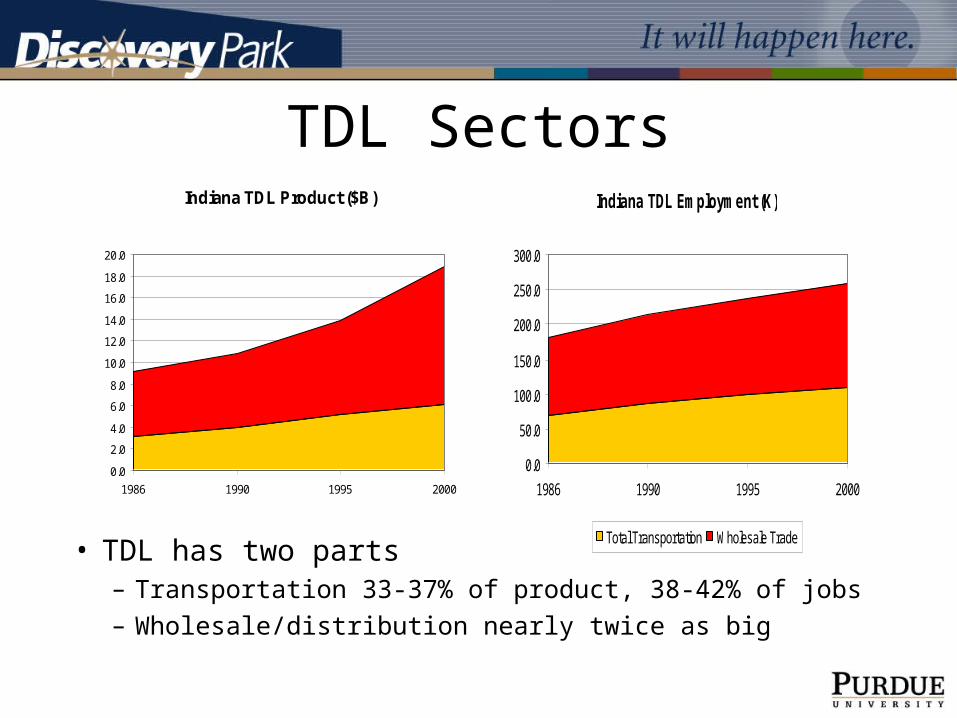

TDL SectorsIndiana TDL Product ($B)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

1986 1990 1995 2000

Indiana TDL Employment (K)

0.0

50.0

100.0

150.0

200.0

250.0

300.0

1986 1990 1995 2000

Total Transportation Wholesale Trade• TDL has two parts

– Transportation 33-37% of product, 38-42% of jobs– Wholesale/distribution nearly twice as big

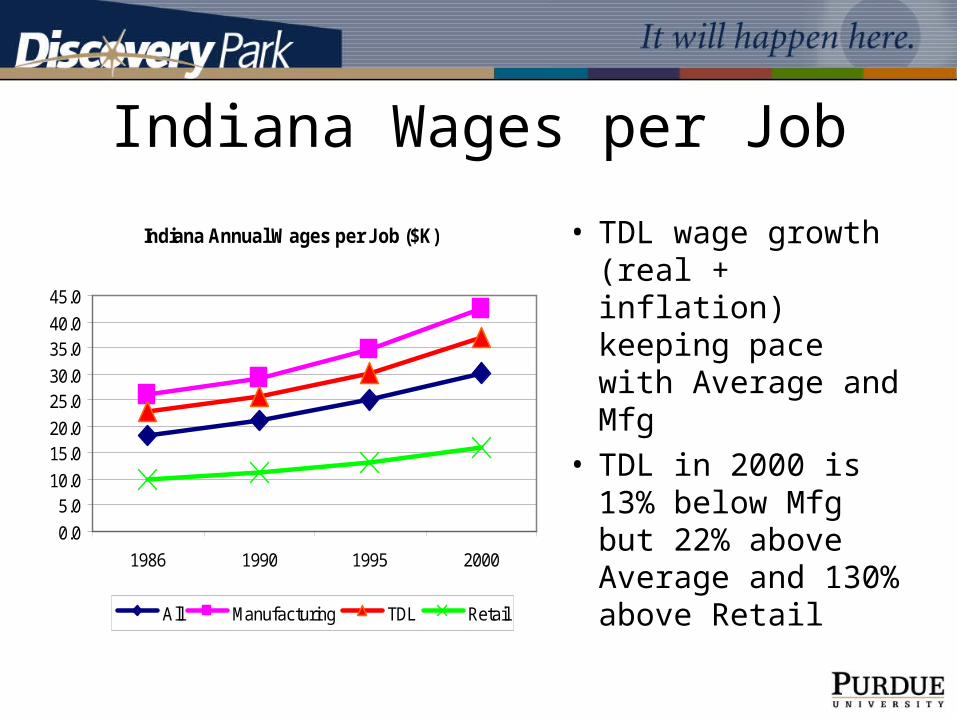

Indiana Wages per Job

Indiana Annual Wages per Job ($K)

0.0

5.010.0

15.020.0

25.030.0

35.040.0

45.0

1986 1990 1995 2000

All Manufacturing TDL Retail

• TDL wage growth (real + inflation) keeping pace with Average and Mfg

• TDL in 2000 is 13% below Mfg but 22% above Average and 130% above Retail

TDL Effects on Other Industries• Input-Output multipliers try to estimate the impact of

economic activity in one sector on the whole economy

• For purposes of this study we used Regional Input-Output Multipliers (RIMS II) information purchased from the U.S. Bureau of Economic Analysis (BEA)– Based on 1997 national benchmark data, in combination with 2000

regional and national output and employment estimates

– Separate values for Indiana alone, and whole United States

Two Directions

• We considered multiplier effects in two directions

• First, what is the full economic impact of TDL activity within different categories?– On total demand, wages, and employment

• Second, what would be the impact on TDL demand of expanded manufacturing activity, especially in high tech “Battelle” categories?

• Both done for all U.S. and for Indiana alone

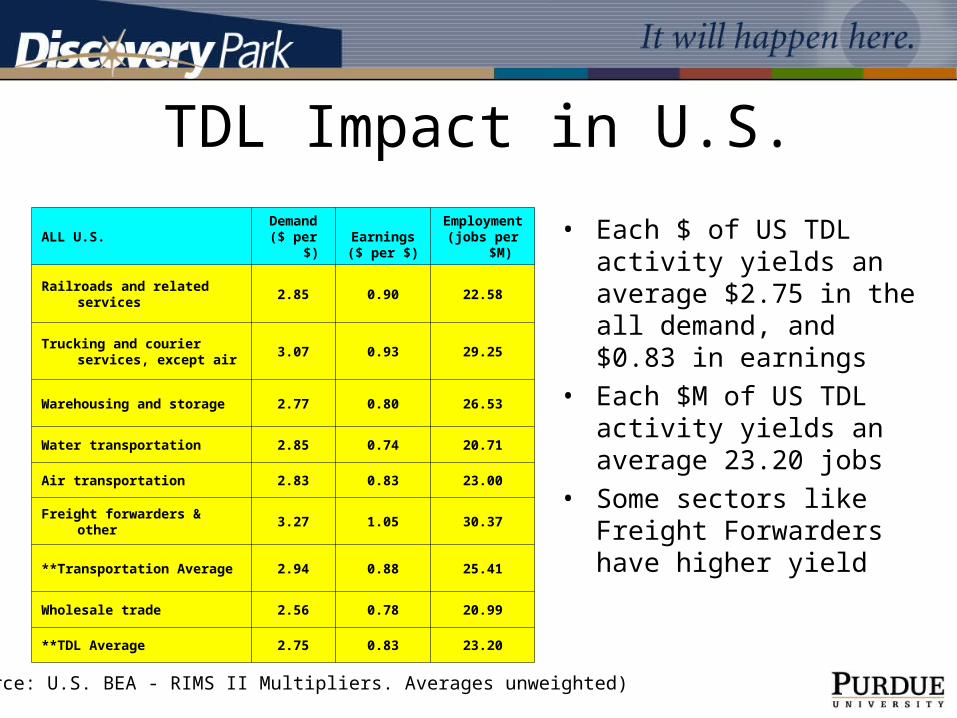

TDL Impact in U.S.

• Each $ of US TDL activity yields an average $2.75 in the all demand, and $0.83 in earnings

• Each $M of US TDL activity yields an average 23.20 jobs

• Some sectors like Freight Forwarders have higher yield

ALL U.S. Demand($ per $)

Earnings($ per $)

Employment(jobs per $M)

Railroads and related services 2.85 0.90 22.58

Trucking and courier services, except air

3.07 0.93 29.25

Warehousing and storage 2.77 0.80 26.53

Water transportation 2.85 0.74 20.71

Air transportation 2.83 0.83 23.00

Freight forwarders & other 3.27 1.05 30.37

**Transportation Average 2.94 0.88 25.41

Wholesale trade 2.56 0.78 20.99

**TDL Average 2.75 0.83 23.20

(Source: U.S. BEA - RIMS II Multipliers. Averages unweighted)

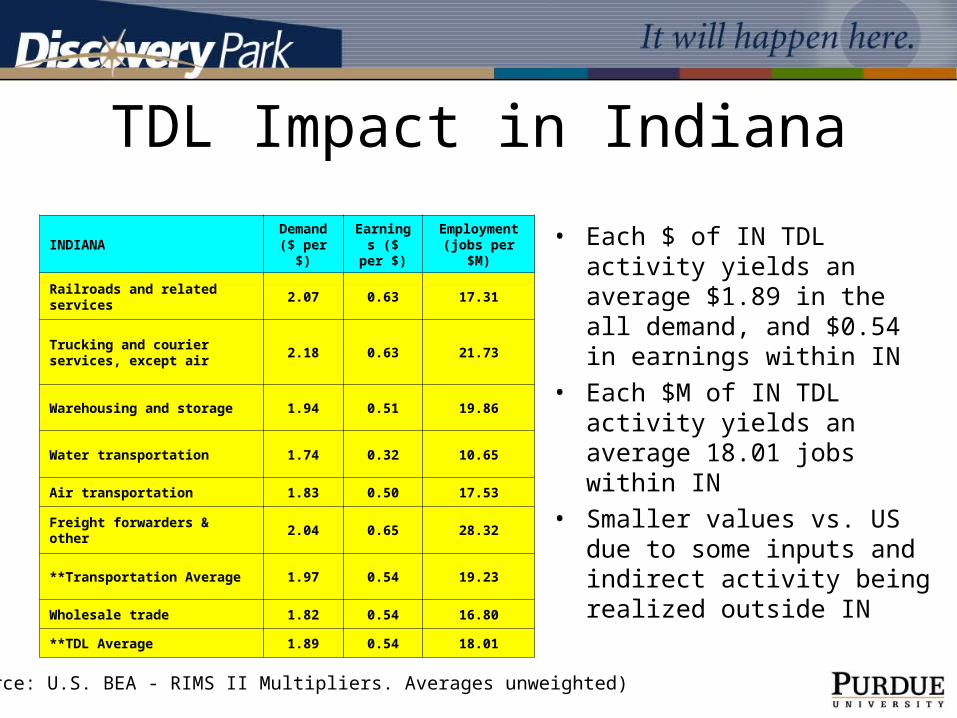

TDL Impact in Indiana

INDIANA Demand ($ per $)

Earnings ($ per $)

Employment (jobs per $M)

Railroads and related services 2.07 0.63 17.31

Trucking and courier services, except air

2.18 0.63 21.73

Warehousing and storage 1.94 0.51 19.86

Water transportation 1.74 0.32 10.65

Air transportation 1.83 0.50 17.53

Freight forwarders & other 2.04 0.65 28.32

**Transportation Average 1.97 0.54 19.23

Wholesale trade 1.82 0.54 16.80

**TDL Average 1.89 0.54 18.01

• Each $ of IN TDL activity yields an average $1.89 in the all demand, and $0.54 in earnings within IN

• Each $M of IN TDL activity yields an average 18.01 jobs within IN

• Smaller values vs. US due to some inputs and indirect activity being realized outside IN

(Source: U.S. BEA - RIMS II Multipliers. Averages unweighted)

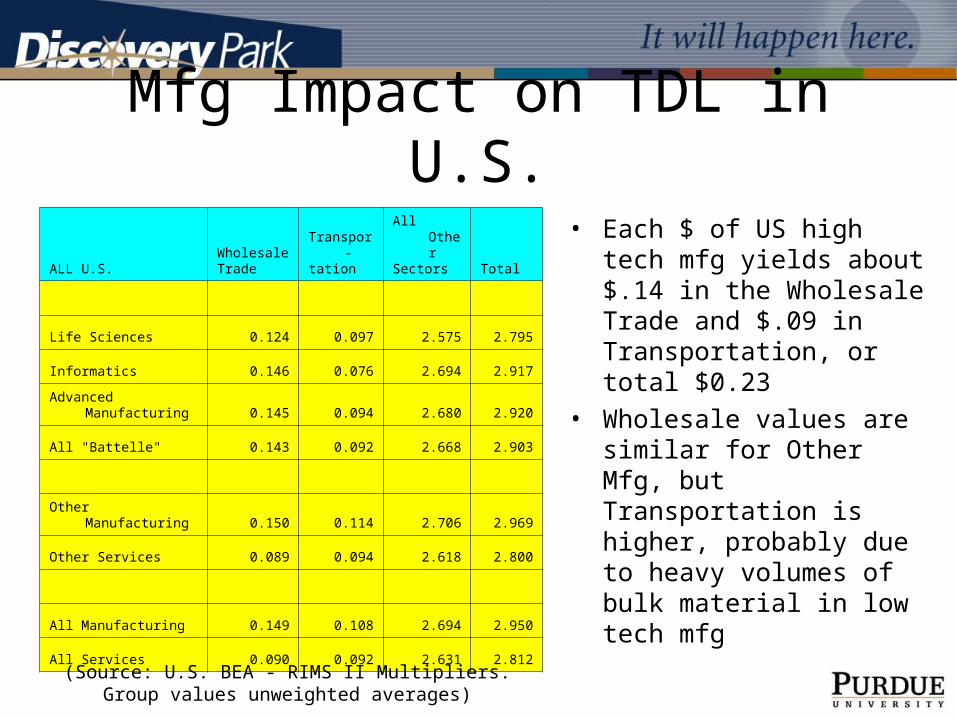

Mfg Impact on TDL in U.S.

• Each $ of US high tech mfg yields about $.14 in the Wholesale Trade and $.09 in Transportation, or total $0.23

• Wholesale values are similar for Other Mfg, but Transportation is higher, probably due to heavy volumes of bulk material in low tech mfg

ALL U.S.WholesaleTrade

Transpor-tation

All OtherSectors Total

Life Sciences 0.124 0.097 2.575 2.795

Informatics 0.146 0.076 2.694 2.917

Advanced Manufacturing 0.145 0.094 2.680 2.920

All "Battelle" 0.143 0.092 2.668 2.903

Other Manufacturing 0.150 0.114 2.706 2.969

Other Services 0.089 0.094 2.618 2.800

All Manufacturing 0.149 0.108 2.694 2.950

All Services 0.090 0.092 2.631 2.812

(Source: U.S. BEA - RIMS II Multipliers.Group values unweighted averages)

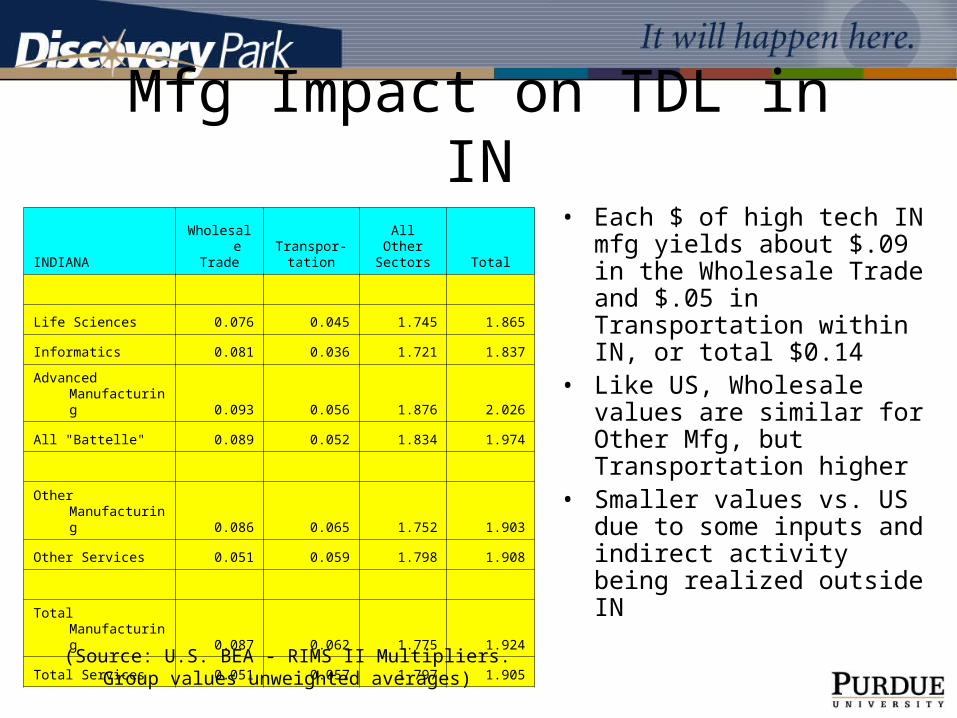

Mfg Impact on TDL in IN

INDIANAWholesale

TradeTranspor-

tation

AllOther

Sectors Total

Life Sciences 0.076 0.045 1.745 1.865

Informatics 0.081 0.036 1.721 1.837

Advanced Manufacturing 0.093 0.056 1.876 2.026

All "Battelle" 0.089 0.052 1.834 1.974

Other Manufacturing 0.086 0.065 1.752 1.903

Other Services 0.051 0.059 1.798 1.908

Total Manufacturing 0.087 0.062 1.775 1.924

Total Services 0.051 0.057 1.797 1.905

• Each $ of high tech IN mfg yields about $.09 in the Wholesale Trade and $.05 in Transportation within IN, or total $0.14

• Like US, Wholesale values are similar for Other Mfg, but Transportation higher

• Smaller values vs. US due to some inputs and indirect activity being realized outside IN

(Source: U.S. BEA - RIMS II Multipliers.Group values unweighted averages)

And So…

• Case for TDL as an important part of the Indiana economy appears pretty solid

• Potential for significant growth in the future

• Significant effects on other industries in the state as well as employment

• Many advantages in Indiana!– Even the competition says so!

Vision

• Indiana as the home of an innovative, world-class TDL sector supported by creative public-private partnerships, innovative technology firms and enlightened, informed economic policies developed with the participation of all stakeholders

Role of Higher Education

• Provide intellectual capital through federal and industrial research

• Work with stakeholders to support economic policy decisions

• Significant role in workforce development

• We are all in this together!!

Current Status

• TDL initiative located in Purdue’s Center for Advanced Manufacturing

• 21st century proposal submitted with significant industrial, academic support– Not successful

• Currently reworking concepts, seeking industrial and academic partners