Embed Size (px)

Citation preview

Development of the transportation sector in changing economic conditions

June 5, 2014

Igors Kasjanovs

Presentation outline

• The importance of the transportation sector in Latvia

• Latest data on transportation sector: are there any evidences of a

slowdown due to geopolitical risks?

• Forecasting of transportation sector: is it really possible?

The importance of the transportation sector in Latvia

GDP growth has been decelerating in the last quarters, however deceleration is mostly related to internal issues

3.8 4.4 4.6

3.6 2.8

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2013 Q1 Q2 Q3 Q4 2014 Q1*

GDP

Manufacturing

Construction

Trade

Transportation

Real estate

Professional services

Real GDP and largest sector growth rate, y-o-y, %

Source: Central statistical Bureau; * Flash estimate

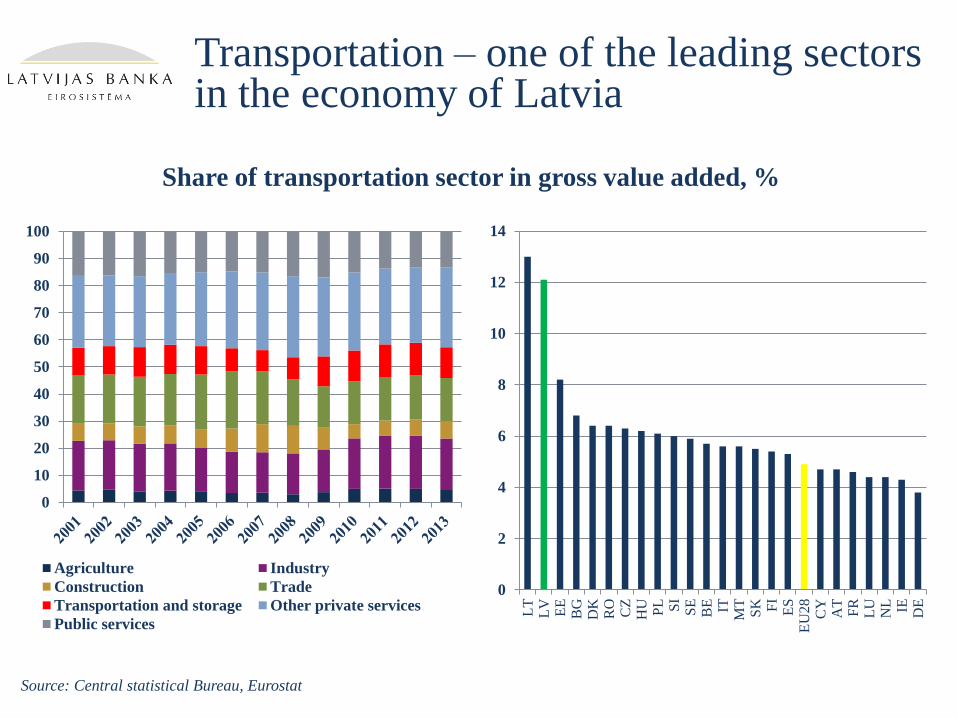

Transportation – one of the leading sectors in the economy of Latvia

0

10

20

30

40

50

60

70

80

90

100

Agriculture Industry

Construction Trade

Transportation and storage Other private services

Public services

0

2

4

6

8

10

12

14

LT

LV

EE

BG

DK

RO

CZ

HU PL SI

SE

BE IT

MT

SK FI

ES

EU

28

CY

AT

FR

LU

NL IE DE

Share of transportation sector in gross value added, %

Source: Central statistical Bureau, Eurostat

Transportation sector also plays a notable social role

Agriculture

Industry

Construction

Trade

Transportation

Other private

services

Public services 0

1

2

3

4

5

6

7

8

9

LV

EE

LT

LU

HU FI

CZ

SK

PL

BU

BE

DK SL

FR

MT

EU

-28

AT IE DE

NL

UK

CY IT

Employment structure of Latvia, % Share of employed persons in transportation sector, % of total employment

Source: Central Statistical Bureau

In 2013 transportation sector faced a deceleration, but the amount of investments points to further development

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

2008

Q1

Q3 2009

Q1

Q3 2010

Q1

Q3 2011

Q1

Q3 2012

Q1

Q3 2013

Q1

Q3

Total economy Transportation

0

2

4

6

8

10

12

14

16

18

20

0

200

400

600

800

1000

1200

1400

1600

Total economy Transportation Share, % (RHS)

Value added growth, y-o-y % Share of non-financial investments in total economy, %

Source: Central Statistica Bureau

Profitability rates have been higher than in total economy; the financial position is strong, however there are disparities among the sector

-8

-6

-4

-2

0

2

4

6

8

10

12

20

10

Q1

Q2

Q3

Q4

20

11

Q1

Q2

Q3

Q4

20

12

Q1

Q2

Q3

Q4

20

13

Q1

Q2

Q3

Q4

20

14

Q1

TOTAL Transportation and storage (H)

-100

-80

-60

-40

-20

0

20

40

60

Total economy

Transportation and storage

Land transport

Water transport

Air transport

Warehousing and support act.

Postal and courier activities

Profitability rate (net profit/turnover), % Share of equity capital in liabilities, %

Source: Central Statistical Bureau

Transportation sector is important player in service exports

0

100

200

300

400

500

600

700

800

900

1000

20

11Q

1

Q2

Q3

Q4

20

12Q

1

Q2

Q3

Q4

20

13Q

1

Q2

Q3

Q4

Government services, n.i.e.

Personal, cultural and recreational

servicesOther bussiness services

Royalties and licence fees

Computer and information services

Financial services

Insurance services

Construction services

Communication services

Travel

Transportation

Exports of services (millions EUR)

Source: Bank of Latvia

Latest data on transportation sector: are there any evidences of a slowdown due

to geopolitical risks?

Competition increases in the Baltic Sea region; Latvian ports loose their shares

0

10

20

30

40

50

60

70

80

2012 2013

Cargoes loaded and unloaded in Baltic sea ports, mln. tons

0

50

100

150

200

250

300

350

400

Baltic sea

region

+0.35%

Source: Klaipeda Seaport Authority

Further growth of cargo amount is observed in Port of Riga

0

5000

10000

15000

20000

25000

Small ports

Liepaja

Ventspils

Riga

Total

Cargo handled in ports of Latvia, thsd. tons

Source: Central Statistical Bureau

The diversification of ports of Latvia is still weak – two main cargo categories account for approx. 60%. Therefore ports are subject to specific demand risks.

0

10000

20000

30000

40000

50000

60000

70000

80000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Perishables

Grain and cereal products

Mineral building materials

Sugar

Other goods

Liquid chemicals

Metals and scrap

Timber and wood

Dry chemicals

Oil

Roll on/ roll off

Cargo in containers

Wood ships

Iron ore

Coal

Oil products

Handled cargos in ports of Latvia, thsd. tons

Source: Central Statistical Bureau

The Q1 increase in cargoes loaded and unloaded in ports is due to the significant increase in oil product cargoes at the Riga port

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2011

I

II III IV 2012

I

II III IV 2013

I

II III IV 2014

I

Goods in containers

Other

Metals

Wood

Oil

Coal

Grain

Total

Y-o-Y contributions of the main cargoe types and the change in overall cargoe turnover, percentage points

Source: Central Statistical Bureau

After a slight deceleration in 2013, cargo amount transported by rail rebounded in Q1 of 2014

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

2003

Q1

Q3 2004

Q1

Q2 2005

Q1

Q1 2006

Q1

Q4 2007

Q1

Q3 2008

Q1

Q2 2009

Q1

Q1 2010

Q1

Q4 2011

Q1

Q3 2012

Q1

Q2 2013

Q1

Q1

Internal traffic Transit Export Import

Cargo transported by rail, thsd. tons

Source: Central statistical Bureau

Geographically transportation sector highly relies on the economical and political situation in Russia

71%

21%

4%

3%

1% 0%

0%

Russia

Belarus

Kazakhstan

Lithuania

Ukraine

Estonia

Others

Import freight transport by rail, % (2012)

Source: Central statistical Bureau

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

National traffic Exports

Imports Transit

Structure of freight transport by rail, % (2012)

Cargo amount transported by road has been increasing steadily. However a drop in turnover has been observed in Q4 of 2013

0

500

1000

1500

2000

2500

3000

3500

4000

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

2005

1Q

3Q

2006

1Q

3Q

2007

1Q

3Q

2008

1Q

3Q

2009

1Q

3Q

2010

1Q

3Q

2011

1Q

3Q

2012

1Q

3Q

2013

1Q

3Q

2014

1Q

Freight traffic - total, thsd t

Freight turnover, mln tonne kilometres

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

06

Q1

Q3

20

07

Q1

Q2

20

08

Q1

Q1

20

09

Q1

Q4

20

10

Q1

Q3

20

11

Q1

Q2

20

12

Q1

Q1

20

13

Q1

Q4

Domestic traffic International traffic

Freight traffic by road Freight turnover, %

Source: Central statistical Bureau

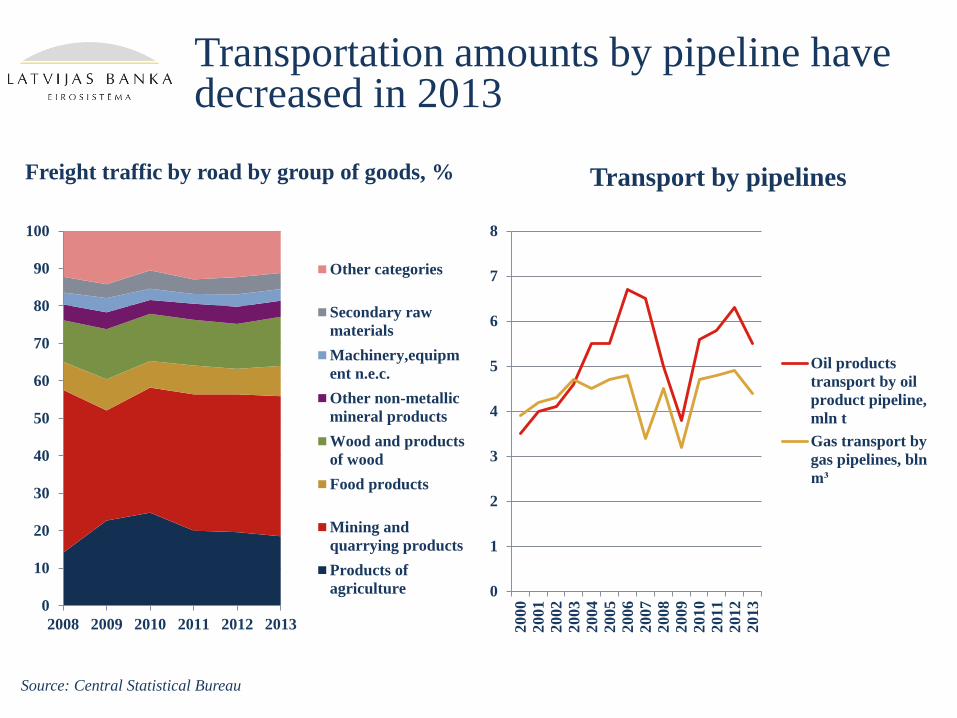

Transportation amounts by pipeline have decreased in 2013

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013

Other categories

Secondary raw

materials

Machinery,equipm

ent n.e.c.

Other non-metallic

mineral products

Wood and products

of wood

Food products

Mining and

quarrying products

Products of

agriculture 0

1

2

3

4

5

6

7

8

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Oil products

transport by oil

product pipeline,

mln t

Gas transport by

gas pipelines, bln

m³

Freight traffic by road by group of goods, % Transport by pipelines

Source: Central Statistical Bureau

Cargoes at ports and rail freight turnover figures suggest a successful Q1, but there are doubts about the sustainability of these results

-30

-20

-10

0

10

20

30

40

small ports

Liepaja port

Ventspils port

Riga port

Cargoes in ports

Rail freight turnover

Road freight turnover-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

2013'I II III

IV V VI

VII

VII

I

IX X XI

XII

2014'I II III

IV

Cargoes at ports

Rail freight turnover

Cargoes at ports, rail and road freight, % change Y-o-Y, and contributions to cargoes at ports by port, percentage points

Monthly cargoes loaded and unloaded at ports and freight turnover by rail, % change Y-o-Y

Source: Central Statistical Bureau

There was a slight pick-up in internal passenger traffic in 2013

0

10000

20000

30000

40000

50000

60000

70000

20

02 Q

1

Q3

20

03 Q

1

Q2

20

04 Q

1

Q1

20

05 Q

1

Q4

20

06 Q

1

Q3

20

07 Q

1

Q2

20

08 Q

1

Q1

20

09 Q

1

Q4

20

10 Q

1

Q3

20

11 Q

1

Q2

20

12 Q

1

Q1

20

13 Q

1

Q4

20

14 Q

1

Rail

Bus

Tram

Trolley-bus

Passenger traffic (thsd. passengers) by means of transport

Source: Central statistical Bureau

International passenger traffic is decreasing a bit on the back of consolidation of the largest air-carrier

0

200

400

600

800

1000

1200

1400

1600

1800

20

02

Q1

Q4

Q2

Q4

20

05

Q1

Q1

Q3

Q1

20

08

Q1

Q2

Q4

Q2

20

11

Q1

Q3

Q1

Q3

20

14

Q1

Non seasonaly adjusted Seasonaly adjusted

0

50

100

150

200

250

300

350

20

04

Q1

Q3

20

05

Q1

Q2

20

06

Q1

Q1

20

07

Q1

Q4

20

08

Q1

Q3

20

09

Q1

Q2

20

10

Q1

Q1

20

11

Q1

Q4

20

12

Q1

Q3

20

13

Q1

Q2

20

14

Q1

Non seasonaly adjusted Seasonaly adjusted

Passengers in airport “Riga”, thsd. pers. Passengers in port “Riga”, thsd. pers.

Source: Central statistical Bureau

Forecasting of transportation sector: is it really possible?

Forecasting of transportation sector is easy in case of central Europe, not the case in the Baltics

-15

-10

-5

0

5

10

15

2004 2005 2006 2007 2008 2009 2010 2011 2011

Manufacturing Trade Transportation

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

2004 2005 2006 2007 2008 2009 2010 2011 2012

Manufacturing Trade Transport

Transportation sector in EU-28 Transportation sector in Latvia

Source: Eurostat, Central Statistical Bureau

Top-down approach: econometrically possible, but have to rely on international environment forecasts which also contain an error

-20

-15

-10

-5

0

5

10

15

20

25

-20

-15

-10

-5

0

5

10

15

20

25

2001 Q

1

Q4

Q3

Q2

2004 Q

1

Q4

Q3

Q2

2007 Q

1

Q4

Q3

Q2

2010 Q

1

Q4

Q3

Q2

2013 Q

1

Q4

GDP of EU-28

Value added in transportation sector (LV)

Real imports of EU-28

-20

-15

-10

-5

0

5

10

15

20

25

-20

-15

-10

-5

0

5

10

15

20

25

2001

Q1

Q4

Q3

Q2

2004

Q1

Q4

Q3

Q2

2007

Q1

Q4

Q3

Q2

2010

Q1

Q4

Q3

Q2

2013

Q1

Q4

GDP of Russia

Value added in transportation sector (LV)

EU-28 GDP, real import and VA of transportation sector of Latvia, y-o-y, %

Russia GDP and VA of transportation sector of Latvia, y-o-y, %

Source: OECD, Central Statistical Bureau

However, life is not much easier in case of bottom-up approach

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Transportation sector value

added

Cargo by rail

Cargo in ports

Cargo by road

Passengers

Annual growth rates of transportation sub-sectors

Source: Central Statistical Bureau

However, there are some relations that can be used

0

10

20

30

40

50

60

70

80

90

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

20

06

I

III

20

07

I

III

20

08

I

III

20

09

I

III

20

10

I

III

20

11

I

III

20

12

I

III

20

13

I

III

20

14

I

Carbo by road Diesel oil

-60

-50

-40

-30

-20

-10

0

10

20

30

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Cargo by road Confidence indicator

Relation between consumption of diesel oil and cargo by road

Relation between confidence indicator of land transport sub-branch and cargo by road

Source: Central Statistical Bureau

Coal amount growth in ports can be easily forecasted as a lagged function of regional coal prices

-40

-30

-20

-10

0

10

20

30

40

50

60

-80

-60

-40

-20

0

20

40

60

80

100

120

Q3

Q4

20

09 Q

1

Q2

Q3

Q4

20

10 Q

1

Q2

Q3

Q4

20

11 Q

1

Q2

Q3

Q4

20

12 Q

1

Q2

Q3

Q4

20

13 Q

1

Q2

Q3

Q4

20

14 Q

1

Q2

Coal price

Coal cargo in ports

Coal price and coal handling amount y-o-y growth, %

Source: Bloomberg; Central Statistical Bureau

Closing remarks

• No hard data suggests any real problems or slowdown in the

transportation sector in Q1 of 2014;

• However, some forward looking indicators and operative statistics

point to a possible period of weaker results;

• The transportation sector remains highly vulnerable to external

demand shocks – both in terms of geographical exposures and

types of cargo;

• Forecasting of transportation sector of Latvia is highly problematic

– a lot of factors have to be taken into account;

• Still, the most important quote: “The success is in the details”