Embed Size (px)

Citation preview

TransparencyReport 2017

EY Sweden

Transparency Report 2017: EY Sweden 2

ContentsMessage from the Chief Executive Officer ....................................................................................................................... 3

About us ...................................................................................................................................................................... 5

Legal structure, ownership and governance ................................................................................................................. 5

Network arrangements .............................................................................................................................................. 6

Commitment to quality .................................................................................................................................................. 8

Infrastructure supporting quality................................................................................................................................. 8

Instilled professional values ........................................................................................................................................ 9

Internal quality control system .................................................................................................................................. 10

Client acceptance and continuance ............................................................................................................................ 11

Performance of audits ............................................................................................................................................. 11

Review and consultation .......................................................................................................................................... 13

Audit partner rotation .............................................................................................................................................. 14

Audit quality reviews ............................................................................................................................................... 14

External quality assurance review ............................................................................................................................. 15

Compliance with legal requirements .......................................................................................................................... 15

Independence practices ............................................................................................................................................... 16

Continuing education of audit professionals .................................................................................................................. 18

Revenue and remuneration .......................................................................................................................................... 19

Financial information ............................................................................................................................................... 19

Partner remuneration .............................................................................................................................................. 19

Declaration from the Board of Directors ....................................................................................................................... 21

Appendix 1 ................................................................................................................................................................. 22

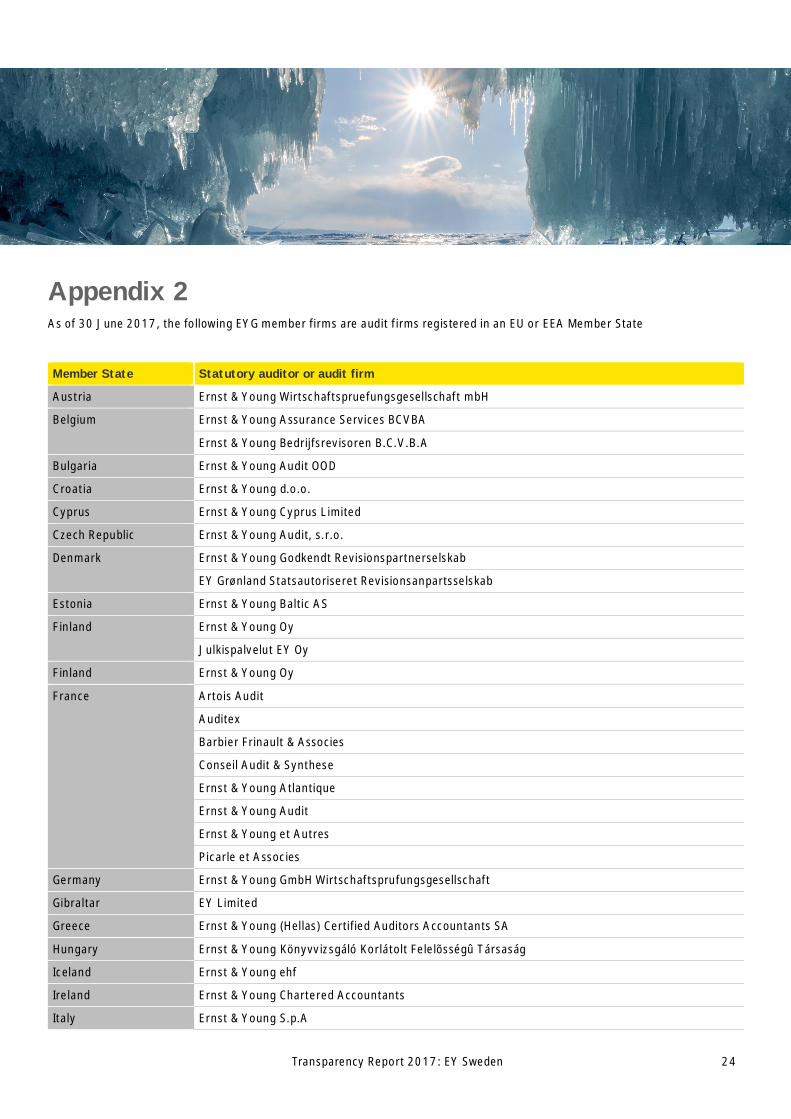

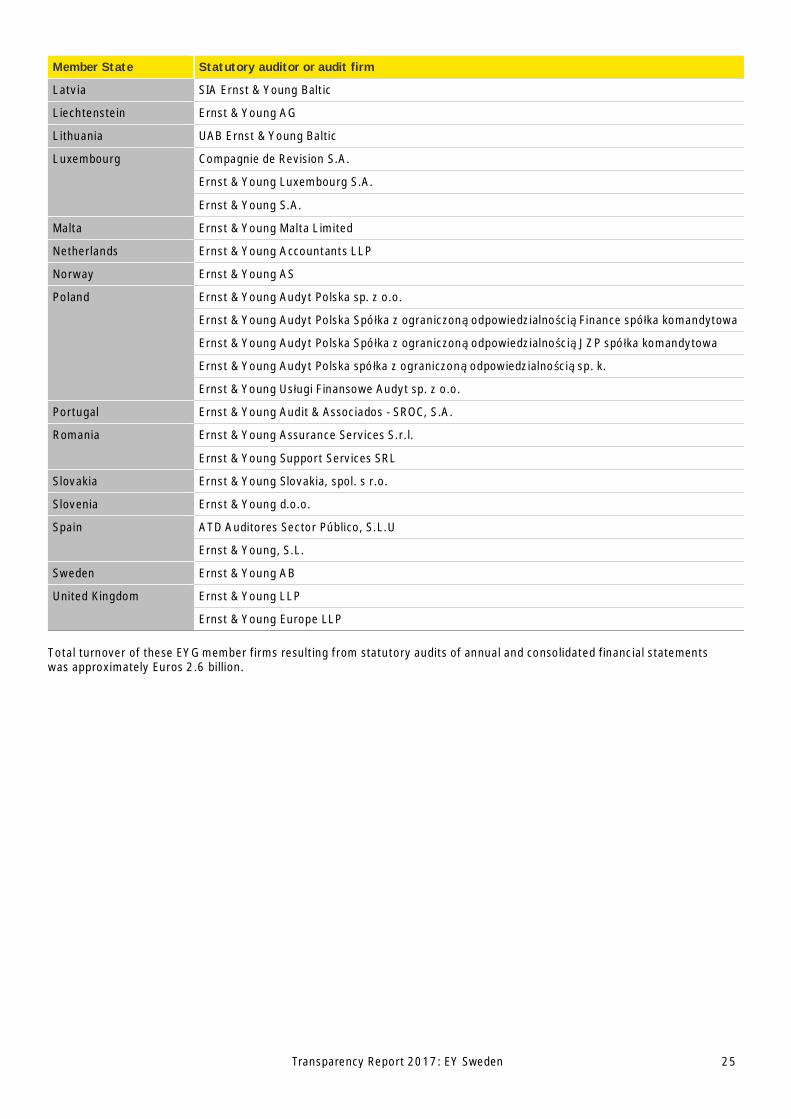

Appendix 2 ................................................................................................................................................................. 24

More information about EY can be found at ey.com.

Transparency Report 2017: EY Sweden 3

Message from the Chief Executive Officer

Welcome to the 2017 Transparency Report of Ernst & Young AB (EY Sweden). We appreciate that our stakeholders want tounderstand how we advance audit quality, manage risk and maintain our independence as auditors. Regular dialogue is importantto us, and this report is one of the ways in which we advise our stakeholders on what we are doing in each of these areas.

Executing high-quality audits continues to be our top priority and is at the heart of our commitment to serve the public interest.It enables us to grow the global EY network successfully and responsibly, while achieving our purpose of building a better workingworld. Auditors play a vital role in the functioning of capital markets by promoting transparency and supporting investorconfidence. Companies, regulators and other stakeholders count on us to deliver excellence in every engagement.

We are focused on investing in tools to improve what we do, creating the highest-performing teams, and building trust andconfidence in the audits we perform.

EY Sweden’s reputation is based on and grounded in providing high-quality professional audit services objectively and ethically toevery company we audit.

We continue to embrace the transparency objectives of the European Union’s 8th Company Law Directive and Article 13 of theRegulation (EU) 537/2014 of the European Parliament and of the Counsel of 16 April 2014 which require Sweden’s statutoryauditors of public interest entities (PIEs) to publish annual transparency reports.

The 2017 EY Sweden Transparency Report complies with the directive, and covers the fiscal year ending June 30, 2017. In thisreport, you can learn more about our internal quality control system: how we instill professional values, how we perform an audit,our review and consultation processes, our approach to audit quality reviews, and our independence practices.

EY Sweden is focused on enhancing audit quality and upholding our independence, informed by several matters includingexternal and internal inspection results. Continuous improvement of audit quality requires us to challenge approaches to auditexecution, and we focus on this by evaluating all inspection findings and taking responsive actions.

EY Sweden is an integral part of our global Sustainable Audit Quality (“SAQ”) effort to support the highest quality audits asdescribed in more detail on page 10. The six focus areas of SAQ are; tone at the top, people; simplification; transformation andinnovation; enablement; quality support and monitoring; and accountability. The enhanced Global Audit Methodology (EY GAM),our new documentation tool (EY Canvas), upgrading of data analytics tools, augmented forms and templates and increasedtraining all form part of the SAQ effort and were introduced two years ago. Even if it is early days we note some generalimprovements in the outcome from external and internal inspection results over time. Our Sustainable Audit Quality commitmentis the way we work on a daily basis to learn, develop and achieve high-quality audit services.

The EU audit reform has during 2016/2017 been in force for the first time. The reform includes legal definitions of PublicInterest Entities, new audit reporting requirements, reinforcement of auditors independence and objectivity, mandatory firmrotation rules, non-audit services (NAS ) restrictions, increased interaction with the audit committees and also regulations for thePIE audit committees.

Sweden opted to implement the mandatory firm rotation requirements of the EU Audit Regulation as follows:

Transparency Report 2017: EY Sweden 4

• For PIEs with securities traded on a regulated market the maximum audit firm retention period is ten years plus anadditional ten years if a tender process results in a decision by the shareholders to retain the auditor or 14 years if thetender process results in a decision to simultaneously engage an additional statutory auditor or audit firm.

• For PIEs within the financial sector the audit firm retention period is limited to ten years. No extension is allowed.

At EY Sweden, we were subject to a joint inspection by the US Public Companies Accounting Oversight Board (“PCAOB”) and theSwedish Inspectorate of Auditors (Revisorsinspektionen, “RI”) during spring last year. The PCAOB issued their report onDecember 15, 2016 which was published during the first half of 2017. The RI issued and published their report at the end ofJanuary, 2017. We were also subject to an inspection performed by the Institute of Public Accountants (FAR) of private entitieson behalf of the RI. The FAR’s report is not publicly available. We are pleased with the results from the inspections and willcontinue to embrace the issues raised as elements of our continuous effort to maintain and improve audit quality.

We continue to contribute to the development of audit quality via the FAR. FAR assumes an important role in informing themarket of the development in the profession and in the work for improving efficiency and quality of the auditors work. EY Swedenis represented in FAR’s three policy groups (assurance, accounting and ethics) and other working groups at FAR also this year.The Interaction with the RI, our regulator, has increased during the year. For example we have participated in several seminarsheld by our audit regulator and met them to discuss the developments in our profession.

EY is the only Big 4 audit firm which has developed a truly integrated Nordic organization, which allows a better utilization ofresources and competence from our Nordic organization for the benefit of our Nordic customers. Globally we are the mostintegrated Big 4 firm. We have developed global industry/sector groups and competency centres, ensuring that our clientsreceive relevant insight and knowledge.

During the year EY played an active role in many networks and events. We see this as a good way of contributing to building abetter working world. We have arranged regular seminars, networking events and training courses for our clients – some hostedby ourselves, some in cooperation with third parties. For the twelfth consecutive year EY were present in Almedalen, takingactive part in the public debate and discussed challenges and opportunities in today’s society. Sustainability, entrepreneurship,taxes, infrastructure and the financial sector were some of the topics on the agenda during the week. We were also active in theannual Swedish American Life Science Summit.

For the second consecutive year business students in the Nordics have ranked us number one in Most Attractive EmployersNordic 2016.

We encourage all our stakeholders — including investors, audit committee members, companies and regulators — to continue toengage with us on our strategy as well as any of the matters covered in this report.

Jesper NilssonChief Executive OfficerErnst & Young AB

EY’s purpose: building a better working worldEY is committed to doing its part in building a better working world.

The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the worldover. We develop outstanding leaders who team to deliver on our promises to stakeholders. In so doing, we play a critical rolein building a better working world for our people, our clients and our communities.

Transparency Report 2017: EY Sweden 5

About usLegal structure, ownership andgovernanceThe company preparing and issuing this report is Ernst &Young AB which is the company where our audit practice isperformed. Ernst & Young AB is a wholly-owned subsidiaryof Ernst & Young Sweden AB.

Ernst & Young Sweden AB is a limited company organized inStockholm and is a member firm of Ernst & Young GlobalLimited, a UK company limited by guarantee (EYG). In thisreport, we refer to ourselves as “EY Sweden,” “we,” “us” or“our.” EY refers collectively to the global organization of themember firms of EYG.

Ernst & Young Sweden AB is owned by 156 partners whoare active in the business, representing an ownership ofapprox. 89% (46% voting rights). The remaining shares areowned by Ernst & Young Europe LLP (EY Europe).

EY Sweden has 54 offices and 2,240 employees.

During the fiscal year 2016/2017 the Board of Directors forEY Sweden was constituted as follows:

Chairman of the Board: Jonas Svensson

Chief Executive Officer: Jesper Nilsson (November 16,2016 -) Hamish Mabon (– November15, 2016)

Board Members: Erik Mamelund, Åsa Lundvall (November16, 2016 - ), Helena Robertsson (November 16, 2016 -),Stefan Persson (- November 15, 2016), Hamish Mabon (-November 15, 2016)

Employee representatives: Monica Sennfors, Fredrik Hertz

Nordic Leadership Team:

Regional Managing Partner for the Nordic region: ErikMamelund

Country Managing Partner Sweden: Lars Weigl

Chief Operating Officer: Mette Storm

Nordic Service Line Leaders Assurance: Jesper Koefoed(Big Cities), Asbjørn Ler (Local Regions)

Nordic Service Line Leader TAX: Christin Erichsen Bøsterud

Nordic Service Line Leader TAS: Jesper Almström

Nordic Service Line Leader Advisory: Terje Andersen

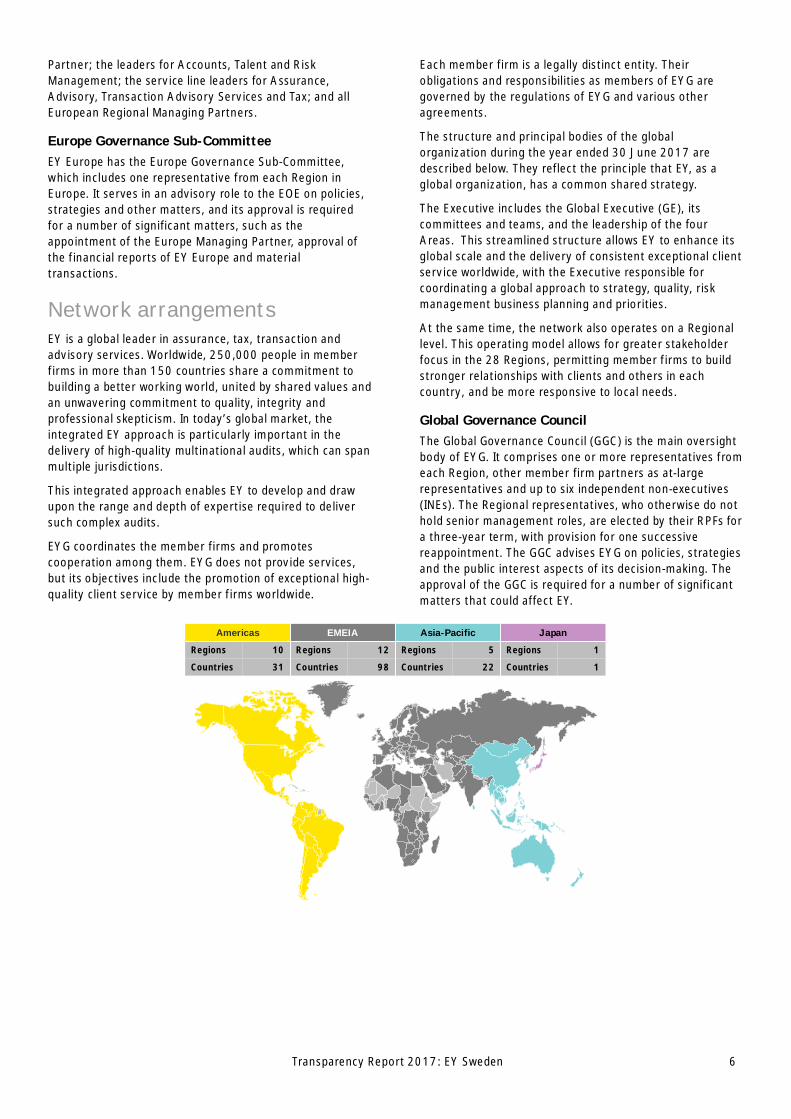

EYG member firms are grouped into four geographic Areas:Americas; Asia-Pacific; Europe, Middle East, India andAfrica (EMEIA); and Japan. The Areas comprise a number ofRegions, which consist of member firms or sections of thosefirms.

EY Sweden is part of the EMEIA Area, which comprises EYGmember firms in 98 countries in Europe, the Middle East,India and Africa. Within the EMEIA Area, there were 12Regions and from 1 July 2017 the number has reduced to11 Regions.

Ernst & Young (EMEIA) Limited (“EMEIA Limited”), anEnglish company limited by guarantee, is the principalcoordinating entity for the EYG member firms in the EMEIAArea. EMEIA Limited facilitates the coordination of thesefirms and cooperation between them, but it does notcontrol them. EMEIA Limited is a member firm of EYG, hasno financial operations and does not provide anyprofessional services.

Each Region elects a Regional Partner Forum (RPF), whoserepresentatives advise and act as a sounding board toRegional leadership. The partner elected as PresidingPartner of the RPF also serves as the Region’srepresentative on the Global Governance Council (see page6).

In Europe, a holding entity, Ernst & Young Europe LLP(“EY Europe”), was formed in conjunction with EMEIALimited. EY Europe is an English limited liability partnership,owned by partners of the EYG member firms operating inEurope. It is an audit firm registered with the Institute ofChartered Accountants in England and Wales (ICAEW), butit does not carry out audits or provide any professionalservices. To the extent permitted by local legal andregulatory requirements, EY Europe has acquired or willacquire voting control of the EYG member firms operatingin Europe. EY Europe is a member firm of both EYG andEMEIA Limited.

EY Europe acquired voting control of EY Sweden asof January 18, 2010.

EY Europe’s principal governing bodies are:

Europe Operating ExecutiveThe Europe Operating Executive (EOE) operates as theboard of EY Europe. It has authority and accountability forstrategy execution and management of EY Europe’soperations. The EOE comprises: the Europe Managing

Transparency Report 2017: EY Sweden 6

Partner; the leaders for Accounts, Talent and RiskManagement; the service line leaders for Assurance,Advisory, Transaction Advisory Services and Tax; and allEuropean Regional Managing Partners.

Europe Governance Sub-CommitteeEY Europe has the Europe Governance Sub-Committee,which includes one representative from each Region inEurope. It serves in an advisory role to the EOE on policies,strategies and other matters, and its approval is requiredfor a number of significant matters, such as theappointment of the Europe Managing Partner, approval ofthe financial reports of EY Europe and materialtransactions.

Network arrangementsEY is a global leader in assurance, tax, transaction andadvisory services. Worldwide, 250,000 people in memberfirms in more than 150 countries share a commitment tobuilding a better working world, united by shared values andan unwavering commitment to quality, integrity andprofessional skepticism. In today’s global market, theintegrated EY approach is particularly important in thedelivery of high-quality multinational audits, which can spanmultiple jurisdictions.

This integrated approach enables EY to develop and drawupon the range and depth of expertise required to deliversuch complex audits.

EYG coordinates the member firms and promotescooperation among them. EYG does not provide services,but its objectives include the promotion of exceptional high-quality client service by member firms worldwide.

Each member firm is a legally distinct entity. Theirobligations and responsibilities as members of EYG aregoverned by the regulations of EYG and various otheragreements.

The structure and principal bodies of the globalorganization during the year ended 30 June 2017 aredescribed below. They reflect the principle that EY, as aglobal organization, has a common shared strategy.

The Executive includes the Global Executive (GE), itscommittees and teams, and the leadership of the fourAreas. This streamlined structure allows EY to enhance itsglobal scale and the delivery of consistent exceptional clientservice worldwide, with the Executive responsible forcoordinating a global approach to strategy, quality, riskmanagement business planning and priorities.

At the same time, the network also operates on a Regionallevel. This operating model allows for greater stakeholderfocus in the 28 Regions, permitting member firms to buildstronger relationships with clients and others in eachcountry, and be more responsive to local needs.

Global Governance CouncilThe Global Governance Council (GGC) is the main oversightbody of EYG. It comprises one or more representatives fromeach Region, other member firm partners as at-largerepresentatives and up to six independent non-executives(INEs). The Regional representatives, who otherwise do nothold senior management roles, are elected by their RPFs fora three-year term, with provision for one successivereappointment. The GGC advises EYG on policies, strategiesand the public interest aspects of its decision-making. Theapproval of the GGC is required for a number of significantmatters that could affect EY.

Americas EMEIA Asia-Pacific Japan

Regions 10 Regions 12 Regions 5 Regions 1

Countries 31 Countries 98 Countries 22 Countries 1

Transparency Report 2017: EY Sweden 7

Independent Non-ExecutivesUp to six Independent Non-Executives (INEs) are appointedfrom outside EY. The INEs are senior leaders from both thepublic and private sectors, and reflect diverse geographicand professional backgrounds. They bring to the globalorganization, and the GGC, the significant benefit of theirvaried perspectives and depth of knowledge. The INEs alsoform a majority of the Public Interest Sub-Committee of theGGC, which addresses public interest matters, includingstakeholder dialogue. The INEs are nominated by adedicated committee.

Global ExecutiveThe Global Executive (GE) brings together EY’s leadershipfunctions, services and geographies. It is chaired by theChairman and CEO of EYG, and includes its Global ManagingPartners of Client Service and Business Enablement; theArea Managing Partners; the global functional leadershipfor Talent and Finance; the leaders of the global servicelines — Assurance, Advisory, Tax and Transaction AdvisoryServices; the Global Leader for Public Policy; and one EYGmember firm partner on rotation.

The GE also includes the Chair of the Global AccountsCommittee and the Chair of the Emerging MarketsCommittee, as well as a representative from the EmergingMarkets practices.

The GE and the GGC approve nominations for the Chairmanand CEO of EYG, and ratify appointments of the GlobalManaging Partners. The GE also approves appointments ofGlobal Vice Chairs. The GGC ratifies the appointments ofany Global Vice Chair who serves as a member of the GE.

The GE’s responsibilities include the promotion of globalobjectives and the development, approval, and, whererelevant, implementation of:

• Global strategies and plans• Common standards, methodologies and policies to be

promoted within member firms• People initiatives, including criteria and processes for

admission, evaluation, development, reward andretirement of partners

• Quality improvement and protection programs• Proposals regarding regulatory matters and

public policy• Policies and guidance relating to member firms’ service

of international clients, business development, marketsand branding

• EY’s development funds and investment priorities• EYG’s annual financial reports and budgets• GGC recommendations

The GE also has the power to mediate and adjudicatedisputes between member firms.

GE committeesEstablished by the GE and bringing together representativesfrom the four Areas, the GE committees are responsible formaking recommendations to the GE. In addition to theGlobal Audit Committee, there are committees for GlobalMarkets and Investments, Global Accounts, EmergingMarkets, Talent, Risk Management, Assurance, Advisory,Tax, and Transaction Advisory Services.

Global Practice GroupThis group brings together the members of the GE, GEcommittees and Regional leaders. The Global PracticeGroup seeks to promote a common understanding of EY’sstrategic objectives and consistency of execution across theorganization.

EYG member firmsUnder the regulations of EYG, member firms committhemselves to pursue EY’s objectives, such as the provisionof high-quality service worldwide. To that end, the memberfirms undertake the implementation of global strategies andplans, and to maintain the prescribed scope of servicecapability. They are required to comply with commonstandards, methodologies and policies, including thoseregarding audit methodology, quality and risk management,independence, knowledge sharing, human resources, andtechnology.

Above all, EYG member firms commit to conducting theirprofessional practices in accordance with applicableprofessional and ethical standards, and all applicablerequirements of law. This commitment to integrity anddoing the right thing is underpinned by the EY Global Codeof Conduct and EY values (see page 10).

Besides adopting the regulations of EYG, member firmsenter into several other agreements covering aspects oftheir membership in the EY organization, such as the rightand obligation to use the EY name, and the sharing ofknowledge.

Member firms are subject to reviews that evaluate theiradherence to EYG requirements and policies governingissues such as independence, quality and risk management,audit methodology, and human resources. Member firmsunable to meet the quality commitments and other EYGmembership requirements may be subject to separationfrom the EY organization.

Transparency Report 2017: EY Sweden 8

Commitment to qualityInfrastructure supportingqualityQuality in our service linesVision 2020+, which sets out EY’s purpose, ambition andstrategy, calls for EYG member firms to provide exceptionalclient service worldwide. This is supported by anunwavering commitment to quality and service that isprofessionally and globally consistent, and means servicethat is based on objectivity, professional skepticism, andadherence to EY and professional standards.

EYG member firms and their service lines are accountablefor delivering quality engagements. EY service linesmanage the overall process for quality reviews of completedengagements and input for the quality of in-processengagements, which helps achieve compliance withprofessional standards and EY policies.

Vision 2020 has reinforced the ownership of qualityby the service lines, including audit. It has alsoresulted in increased clarity around the role of riskmanagement in policies and practices that support andimprove quality audit.

The Global Vice Chair of Assurance coordinates memberfirms’ compliance with EY policies and procedures forassurance services.

Professional PracticeThe Global Vice Chair of Professional Practice, referred toas the Global Professional Practice Director (PPD), isoverseen by the Global Vice Chair of Assurance and worksto establish global audit quality control policies andprocedures. Each of the Area PPDs is overseen by theGlobal PPD and the related Area Assurance Leader. Thishelps provide greater assurance as to the objectivity ofaudit quality and consultation processes.

The Global PPD also leads and oversees the GlobalProfessional Practice group. This is a global network oftechnical subject matter specialists in accounting andauditing standards, who consult on accounting, auditingand financial reporting matters, and perform variouspractice monitoring and risk management activities.

The Global PPD oversees development of the EY GlobalAudit Methodology (EY GAM) and related technologies sothat they are consistent with relevant professionalstandards and regulatory requirements. The GlobalProfessional Practice group also oversees the developmentof the guidance, training and monitoring programs andprocesses used by member firm professionals to executeaudits consistently and effectively. The Global, Area andRegion PPDs, together with other professionals who workwith them in each member firm, are knowledgeable aboutEY people, clients and processes, and they are readilyaccessible for consultation with audit engagement teams.

Additional resources often augment the Global ProfessionalPractice group, including networks of professionals focusedon:

• Internal-control reporting and related aspects of the EYaudit methodology

• Accounting, auditing and risk issues for specificindustries and sectors

• Event-specific issues involving areas of civil andpolitical unrest; or sovereign debt and relatedaccounting, auditing, reporting and disclosureimplications

• General engagement issues and how to work effectivelywith audit committees

Risk managementResponsibility for the delivery of high-quality service andownership of the risks associated with quality is placed withthe member firms. Among other things, the Global RiskManagement Leader helps oversee the management ofthese risks by the member firms, as well as other risksacross the organization as part of the broader EnterpriseRisk Management framework.

Member firm partners are appointed to lead riskmanagement initiatives in both the service lines andmember firms, supported by other staff and professionals.The Global Risk Management Leader is responsible forestablishing globally consistent risk management executionpriorities and enterprise-wide risk management. Thesepriorities cascade to member firms, and their execution ismonitored through an Enterprise Risk Managementprogram.

Transparency Report 2017: EY Sweden 9

Global confidentiality policyProtecting confidential information is ingrained in theeveryday activities of EYG member firms. Respect forintellectual capital and all other sensitive and restrictedinformation is required by the Global Code of Conduct,which provides a clear set of principles to guide thebehaviors expected of all EY people. The GlobalConfidentiality Policy further details this approach toprotecting information and reflects the ever-increasing useof restricted data. This policy provides added clarity for EYpeople and forms the fundamental element of broaderguidance that includes key policies on conflicts of interest,personal data privacy and records retention. Otherguidance includes:

• Social media guidance• Information-handling requirements• Knowledge-sharing protocols

Components of the audit quality control programIn the following sections, we describe the principalcomponents of the EY Sweden audit quality controlprogram:

• Instilled professional values• Internal quality control system• Client acceptance and continuance• Performance of audits• Review and consultation• Audit partner rotation• Audit quality reviews• External quality-assurance reviews• Compliance with legal requirements

Instilled professional valuesSustainable Audit QualityQuality is the foundation for exceptional client service. It iswhat we pride ourselves on. It is integral to our work andcentral to our responsibility to provide confidence to thecapital markets. Delivering quality is at the heart of all wedo and supports our purpose of building a better workingworld for our people, our clients and our communities. Thisis reflected in the Sustainable Audit Quality (SAQ) program,which is the highest priority for our Assurance practice.

Each member firm that makes up our global structure iscommitted to providing high-quality audits. In 2015, welaunched the SAQ initiative throughout our Assurancepractices. SAQ establishes a governance structure and isfocused on continuously improving our audit process.

We use the word “sustainable” in SAQ to demonstrate thatthis is not a one-off short-term initiative, but an ongoingprocess of improvement. EY has had a common auditmethodology for some time; now we have a commonlanguage and processes regarding audit quality.

There are six components to SAQ: tone at the top,strengthening people capabilities, simplification, audittechnology and digital, enablement and quality support,

and accountability. SAQ is implemented by each memberfirm, and is coordinated and overseen globally.

We constantly reinforce the importance of the sixcomponents, and discuss them with every RegionalAssurance leader and every partner. Audit quality and thekey elements of SAQ are something every senior manager,manager and team member must understand and becommitted to implementing locally. SAQ is essential to allour goals and ambitions.

We have made significant progress through SAQ. EY’sinternal and external inspection findings globally areshowing improvement, and we are producing greaterconsistency in execution.

We have deployed world-class tools that enhance thequality and value of our audits. Our ability to deliverconsistency is based in part on the use of EY Canvas, ouronline audit platform. EY Canvas was broadly deployedbeginning in 2015 and is now used globally. It bettersupports audit execution, streamlines communications andenables us to provide a seamless audit.

We recently launched the EY Canvas Client Portal, whichadds to the leading-edge tools already offered to ourauditors. In addition, we have deployed the 2017 AuditMilestones Program globally, which establishes the use ofMilestones on selected PIE audits as one important step toimproving results and sustaining quality acrossengagements.

In 2016, EY developed a network of Quality EnablementLeaders (QELs) and created a Global Audit QualityCommittee.These and other SAQ initiatives have helped us to continueto drive quality improvements. They demonstrate that auditquality is the single most important factor in our decision-making and the key measure on which our professionalreputation stands.

Tone at the topSenior EY and EY Sweden leadership are responsible forsetting the right tone at the top and demonstrating EY’scommitment to building a better working world throughbehavior and actions. While the tone at the top is vital, ourpeople also understand that quality and professionalresponsibility start with them. Our shared values, whichinspire our people and guide them to do the right thing, andour commitment to quality are embedded in who we are andin everything we do.

The EY approach to business ethics and integrity iscontained in the EY Global Code of Conduct and otherpolicies, and is embedded in the EY culture of consultation,training programs and internal communications. Seniormanagement regularly reinforces the importance ofperforming quality work, complying with professionalstandards, adhering to our policies, leading by example andthrough various communications. Also, EY’s quality reviewprograms assess professional service as a key metric inevaluating and rewarding all professionals.

The EY culture strongly supports collaboration and placesspecial emphasis on the importance of consultation in

Transparency Report 2017: EY Sweden 10

dealing with complex or subjective accounting, auditing,reporting, regulatory and independence matters. We believeit is important to determine that engagement teams andclients correctly follow consultation advice, and weemphasize this when necessary.

The consistent stance of EY Sweden has been that noclient is more important than our professionalreputation — the reputation of EY Sweden and thereputation of each of our professionals.

Code of conductWe promote a culture of integrity among our professionals.The EY Global Code of Conduct provides a clear set ofprinciples that guide our actions and our business conduct,and are to be followed by all EY personnel. The Code ofConduct is divided into five categories:

• Working with one another• Working with clients and others• Acting with professional integrity• Maintaining our objectivity and independence• Respecting intellectual capital

Through our procedures to monitor compliance withthe EY Global Code of Conduct, and through frequentcommunications, we strive to create an environment thatencourages all personnel to act responsibly, includingreporting misconduct without fear of retaliation.

The EY Ethics Hotline provides our people, clients andothers outside of the organization with a meansconfidentially to report activity that may involve unethicalor improper behavior and that may be in violation ofprofessional standards or otherwise inconsistent with theEY Global Code of Conduct. The hotline is operated by anexternal organization that provides confidential and, ifdesired, anonymous hotline reporting services forcompanies worldwide.

When a report comes into the EY Ethics Hotline, either byphone or internet, it receives prompt attention. Dependingon the content of the report, appropriate individuals fromRisk Management, Talent, Legal or other functions areinvolved to address the report. The same procedures arefollowed for matters that are reported outside of the EYEthics Hotline.

Our values: who we are

People who demonstrate integrity, respect and teaming

People with energy, enthusiasm and the courage to lead

People who build relationships based on doing theright thing

Internal quality control systemEY Sweden’s reputation for providing high-qualityprofessional audit services independently, objectively andethically is fundamental to our success as independentauditors. We continue to invest in initiatives to promoteenhanced objectivity, independence and professionalskepticism. These are fundamental attributes of ahigh-quality audit.

At EY Sweden, our role as auditors is to provide assuranceon the fair presentation of the financial statements of thecompanies we audit. We bring together qualified teams toprovide our services, drawing on our proven experienceacross industry sectors and services. We continually striveto improve our quality and risk management processes sothat the quality of our service is at a consistently high level.

We recognize that in today’s environment — characterizedby continuing globalization and the rapid movement ofcapital — the quality of our audit services has never beenmore important. As part of EY Vision 2020+, we continueto invest heavily in developing and maintaining our auditmethodology, tools and other resources needed tosupport quality service delivery.

While the market and stakeholders continue to demandhigh-quality audits, they also demand increasingly efficientand effective delivery of audit services. In addition to theinvestment mentioned, EY continues to seek ways toimprove the effectiveness and efficiency of its auditmethodology and processes, while improving audit quality.

We work to understand where our audit quality may not beup to our own expectations and those of stakeholders,including external audit firm regulators. We seek to learnfrom external and internal inspection activities and toidentify root causes of adverse quality occurrences toenable us continually to improve audit quality, and webelieve that taking effective and appropriate actions toimprove quality is important.

Effectiveness of the quality control systemEY has designed and implemented a comprehensive set ofglobal audit quality control policies and practices. Thesepolicies and practices meet the requirements of theInternational Standards on Quality Control issued by theInternational Auditing and Assurance Standards Board(IAASB). EY Sweden has adopted these global policies andprocedures, and has supplemented them as necessary tocomply with local laws and professional guidelines, and toaddress specific business needs.

We also execute the EY Audit Quality Review (AQR) programto evaluate whether our system of audit quality control hasoperated effectively so as to provide reasonable assurancethat EY Sweden and our people comply with applicableprofessional and internal standards and with regulatoryrequirements.

Transparency Report 2017: EY Sweden 11

The results of the AQR program and external inspectionsare evaluated and communicated within EY Sweden toprovide the basis for continual improvement in audit quality,consistent with the highest standards in the profession.

The GE is responsible for implementing quality improvementand protection programs across EY. As such, it reviews theresults of our internal AQR program and external regulatoryreviews, as well as any key actions designed to addressareas for improvement.

The recent results of such monitoring, together with therecent feedback from independent regulatory inspectionvisits, provide EY Sweden with a basis to conclude that ourinternal control systems are designed appropriately and areoperating effectively.

Client acceptance andcontinuanceEY policyThe EY Global Client Acceptance and Continuance Policysets out principles for member firms to determine whetherto accept a new client or a new engagement, or to continuewith an existing client or engagement. These principles arefundamental to maintaining quality, managing risk,protecting our people and meeting regulatoryrequirements. The objectives of the policy are to:

• Establish a rigorous process for evaluating risk andmaking decisions to accept or continue clients orengagements

• Meet applicable independence requirements• Identify and deal appropriately with any conflicts

of interest• Identify and decline clients or engagements that pose

excessive risk• Require consultation with designated professionals to

identify additional risk management procedures forspecific high-risk factors

• Comply with legal, regulatory and professionalrequirements

In addition, the EY Global Conflicts of Interest Policy definesglobal standards for addressing categories of potentialconflicts of interest and a process for identifying them. Italso includes provisions for managing potential conflicts ofinterest as quickly and efficiently as possible through theuse of appropriate safeguards. Such safeguards range fromobtaining a client’s consent for EYG member firms to act fortwo or more clients to declining an engagement to avoid anidentified conflict.

The EY Global Conflicts of Interest Policy and associatedguidance were updated in early 2015. The updates take intoaccount the increasing complexity of engagements andclient relationships, and the need for speed and accuracy inresponding to clients. They also align with the latestInternational Ethics Standards Board for Accountants(IESBA) standards.

Putting policy into practiceWe use the EY Process for Acceptance of Clients andEngagements (PACE), a new intranet-based system, forefficiently coordinating client and engagement acceptanceand continuance activities in line with global, service lineand member firm policies. PACE takes users through theacceptance and continuance requirements, and identifiesthe policies and references to professional standardsneeded to assess both business opportunities andassociated risks.

As part of this process, we carefully consider the riskcharacteristics of a prospective client or engagement andseveral due diligence procedures. Before we take on a newengagement or client, we determine whether we cancommit sufficient resources to deliver quality service,especially in highly technical areas, and if the services theclient wants are appropriate for us to provide. The approvalprocess is rigorous, and no new audit engagement may beaccepted without the approval of our PPD.

In our annual client continuance process, we review ourservice delivery and ability to continue to provide qualityservice, and confirm that clients share EY Sweden’scommitment to quality and transparency in financialreporting. The partner in charge of each audit, togetherwith our Assurance leadership, annually reviews ourrelationship with the audit client to determine whethercontinuance is appropriate.

As a result of this review, certain audit engagements areidentified as requiring and are then subjected to additionaloversight procedures during the audit (close monitoring),and some audit clients are discontinued. As with the clientacceptance process, our Country PPD is involved in theclient continuance process and must agree with thecontinuance decisions.

Both client acceptance and client continuance decisionsconsider the engagement team’s assessment of whetherthe company’s management could pressure us to acceptinappropriate accounting, auditing and reportingconclusions to undermine quality. Considerations andconclusions on the integrity of management are essentialto acceptance and continuance decisions.

Performance of auditsAs part of EY Vision 2020+, EY has invested significantly inimproving audit methodologies and tools, with the goal ofperforming the highest-quality audits in the profession. Thisinvestment is consistent with EY’s goal to have the leadingaudit practices in the profession by 2020 and reflects thecommitment to building trust and confidence in the capitalmarkets and in economies the world over.

Audit methodologyEY GAM provides a global framework for delivering high-quality audit services through the consistent application ofthought processes, judgments and procedures in all auditengagements.

Transparency Report 2017: EY Sweden 12

Making risk assessments, reconsidering and modifyingthem as appropriate, and using these assessments todetermine the nature, timing and extent of audit proceduresare fundamental to EY GAM. The methodology alsoemphasizes applying appropriate professional skepticismin the execution of audit procedures. EY GAM is based onInternational Standards on Auditing (ISAs) and issupplemented in Sweden to comply with the localSwedish auditing standards and regulatory or statutoryrequirements.

An EY auditor is presented with a version of EY GAMorganized by topic and designed to focus the audit strategyon the financial statement risks, and the design andexecution of the appropriate audit response to those risks.EY GAM consists of two key components: requirements andguidance, and supporting forms and examples. Therequirements and guidance reflect both audit standards andEY policies. The forms and examples include leadingpractice illustrations, and assist in performing anddocumenting audit procedures.

Using technology, EY GAM can be “profiled” or tailored topresent the relevant requirements and guidance, dependingon the nature of the entity being audited. For example,there are profiles for listed entities and for those considerednon-complex entities.

Enhancements to the audit methodology are made regularlyto address new standards, emerging auditing issues andmatters, implementation experiences, and external andinternal inspection results. In 2016, EY GAM was updated toinclude the new and revised ISAs dealing with auditorreporting, other information included in an annual reportand financial statement disclosures. EY GAM was alsoenhanced by adding guidance to address common questionsfrom audit teams and issues arising from inspections.

In addition, we monitor current and emerging developmentscontinually, and issue timely audit planning and otherreminders. These reminders emphasize areas noted duringinspections as well as other key topics of interest to ourregulators, including the International Forum ofIndependent Audit Regulators (IFIAR). These topics includeprofessional skepticism, group audits, revenue recognitionand engagement quality reviews.

EY GAM requires compliance with relevant ethicalrequirements, including independence from the companywe audit.

TechnologyOur audit engagement teams use technology to assist inexecuting and documenting the work performed inaccordance with EY GAM.

Beginning in late fiscal year 2015, we launched EY Canvas,our global audit platform that lies at the heart of the auditand enables us to provide a high-quality audit. This waslaunched on a phased basis across EYG member firmsglobally, with deployment completed in 2017. EY Canvas isbuilt using HTML5, state-of-the-art technology for webapplications. This allows us to provide heightened data

security and to evolve our software to respond to changesin the accounting profession and regulatory environment.

Through the use of profile questions, audit engagements inEY Canvas are automatically configured with informationrelevant to the company’s listing requirements and industry.This helps to keep our audit plans customized and up-to-date, and provides direct linkage to our audit guidance,professional standards and documentation templates. EYCanvas is built with a fresh, clear design and user interfacethat allows users to visualize risks and their relationship toour planned response and work performed in key areas. Italso enables a linkage for our group audit teams tocommunicate inter-office risks and instructions so that theprimary audit team can direct execution and monitorperformance of the group audit. The predecessor auditsupport tool, GAMx, will be decommissioned in our 2018fiscal year.

EY Canvas includes a Client Portal, released in April 2017,to assist teams in communicating with clients andstreamline their client requests. Mobile applications,integrated with EY Canvas, were released in fiscal year2017 that assist our people in their audit work; forexample, in monitoring the status of the audit, capturingaudit evidence securely and performing inventoryobservations.

Audit engagement teams use other software applications,forms and templates during various phases of an audit toassist in executing procedures, making and documentingaudit conclusions, and performing analysis.

EY Helix is our suite of data analytic tools for use in audits.Analytics is transforming the audit by analyzing largerpopulations of audit-relevant data, identifying unseenpatterns and trends in that data, and helping to direct ouraudit efforts. The use of analytics also allows us to obtainbetter perspectives, richer insights and a deeperunderstanding of transactions and areas of risk.

We have developed analytics that cover our clients’ end-to-end business operating cycles, supported by analytics-based audit programs to aid their application.

Using our analytics, our engagement teams can enhancetheir audit risk assessment, enabling the audit of higher-risktransactions, and assisting our people in asking betterquestions about audit findings and evaluating theoutcomes.

Formation of audit engagement teamsEY Sweden policies require an annual review of partnerassignments by our Assurance leadership and Country PPDto make sure that the professionals leading listed-companyaudits possess the appropriate competencies (i.e., theknowledge, skills and abilities) to fulfill their engagementresponsibilities, and are in compliance with applicableauditor rotation regulations.

The assignment of professionals to an audit engagement isalso made under the direction of our Assurance leadership.Factors considered when assigning people to audit teamsinclude engagement size and complexity, specialized

Transparency Report 2017: EY Sweden 13

industry knowledge and experience, timing of work,continuity, and opportunities for on-the-job training. Formore complex engagements, consideration is given towhether specialized or additional expertise is needed tosupplement or enhance the audit engagement team.

In many situations, internal specialists are assigned as partof the audit engagement team to assist in performing auditprocedures and obtaining appropriate audit evidence. Theseprofessionals are used in situations requiring special skillsor knowledge, such as information systems, asset valuationand actuarial analysis.

Review and consultationReviews of audit workEY policies describe the requirements for timely and directsenior professional participation, as well as the level ofreview required for the work performed. Supervisorymembers of an audit engagement team perform a detailedreview of the audit documentation for accuracy andcompleteness. Senior audit executives and engagementpartners perform a second-level review to determineadequacy of the audit work as a whole, and the relatedaccounting and financial statement presentation. A taxprofessional reviews the significant tax and other relevantworking papers. For listed and certain other companies, anengagement quality reviewer (described below) reviewsimportant areas of accounting, financial reporting and auditexecution, as well as the financial statements of thecompany we audit and our audit report.

The nature, timing and extent of the reviews of audit workdepend on many factors, including:

• The risk, materiality, subjectivity and complexity of thesubject matter

• The ability and experience of the audit team memberspreparing the audit documentation

• The level of the reviewer’s direct participation in theaudit work

• The extent of consultation employed

Our policies also describe the roles and responsibilities ofeach audit engagement team member for managing,directing and supervising the audit, as well as therequirements for documenting their work and conclusions.

Consultation requirementsOur consultation policies are built upon a culture ofcollaboration, whereby audit professionals are encouragedto share perspectives on complex accounting, auditing andreporting issues. Consultation requirements and relatedpolicies are designed to involve the right resources so thataudit teams reach appropriate conclusions.

Consultation is built into the decision-making process;it is not just a process to provide advice.

For complex and sensitive matters, we have a formalprocess requiring consultation outside of the auditengagement team with other personnel who have more

experience or specialized knowledge, primarily ProfessionalPractice and Independence personnel. In the interests ofobjectivity and professional skepticism, our policies requiremembers of Professional Practice, Independence andcertain others to withdraw from a consultation if theycurrently serve, or have recently served, the client to whichthe consultation relates.

Our policies also require that we document allconsultations, including written concurrence from theperson or persons consulted, in order to demonstrate theirunderstanding of the matter and its resolution.

Engagement quality reviewsEngagement quality reviews are performed by auditpartners in compliance with professional standards foraudits of all listed companies and those considered higherrisk. Engagement quality reviewers are experiencedprofessionals with significant subject matter knowledge.They are independent of the engagement team and ableto provide objective evaluation of significant accounting,auditing and reporting matters. In no circumstances maythe responsibility of the engagement quality reviewer bedelegated to another individual.

The engagement quality review spans the entireengagement cycle, including planning, risk assessment,audit strategy and execution. Policies and procedures forthe performance and documentation of engagement qualityreviews provide specific guidelines on the nature, timingand extent of the procedures to be performed, and therequired documentation evidencing their completion. OurCountry PPD approves all engagement quality reviewassignments for listed companies and those consideredhigher risk.

Audit engagement team resolution process fordifferences of professional opinionEY has a collaborative culture that encourages and expectspeople to speak up, without fear of reprisal, if a differenceof professional opinion arises or if they are uncomfortableabout a matter relating to a client engagement. Policiesand procedures are designed to empower members of anaudit engagement team to raise any disagreements relatingto significant accounting, auditing or reporting matters.

These policies are made clear to people as they join EY, andwe continue to promote a culture that reinforces a person’sresponsibility and authority to make their own views heard,and seek out the views of others.

Differences of professional opinion that arise during anaudit are generally resolved at the audit engagement teamlevel. However, if any person involved in the discussion of anissue is not satisfied with the decision, they refer it to thenext level of authority until agreement is reached or a finaldecision is made.

Furthermore, if the engagement quality reviewer makesrecommendations that the engagement partner does notaccept or the matter is not resolved to the reviewer’ssatisfaction, the audit report is not issued until the matter is

Transparency Report 2017: EY Sweden 14

resolved. EY policies require documentation ofdisagreements and their resolution.

Audit partner rotationEY supports mandatory audit partner rotation to helpstrengthen auditor independence. EY Sweden complies withthe audit partner rotation requirements of the code of theIESBA, Regulation (EU) 537/2014 of the EuropeanParliament and of the Counsel of 16 April 2014, differentSwedish Companies Acts applicable for PIEs, as well as theU.S. Securities and Exchange Commission (SEC), whererequired. In addition Sweden has elected to implementmandatory audit partner rotation for certain companies inthe financial sector even if those are not Public InterestEntities. EY Sweden supports audit partner rotationbecause it provides a fresh perspective and promotesindependence from company management, while retainingexpertise and knowledge of the business. Audit partnerrotation, combined with independence requirements,enhanced systems of internal quality controls andindependent audit oversight, helps strengthenindependence and objectivity, and are important safeguardsof audit quality.

For PIEs where rotation of the audit partner is notmandated by local independence regulation or is lessrestrictive than the IESBA or EU 537/2014 requirements,the EY Global Independence Policy requires the leadengagement partner and the engagement quality reviewerto be rotated after seven years. For a new PIE (including anewly listed company) client, the lead engagement partnerand the engagement quality reviewer may remain in placefor an additional two years before rotating off the team, ifthey have served the client for six or more years prior to thelisting. Following rotation, the partner may not resume thelead or engagement quality review role until at least twoyears have elapsed.

We employ tools to track partner rotation that enableeffective monitoring of compliance with requirements.We have also implemented a process for partner rotationplanning and decision-making that involves consultationwith, and approvals by, our Professional Practice andIndependence professionals.

Audit quality reviewsThe EY Global AQR program is the cornerstone of the EYprocess to monitor audit quality. EY Sweden executes theGlobal AQR program, reports results and developsresponsive actions plans. The primary goal of the programis to determine whether systems of quality controls,including those of EY Sweden, are appropriately designedand followed in the execution of audit engagements toprovide reasonable assurance of compliance with policiesand procedures, professional standards, and regulatoryrequirements. The Global AQR program complies withguidelines in the International Standard on Quality ControlNo. 1 (ISQC No. 1), as amended, and is supplementedwhere necessary to comply with Swedish professional

standards and regulatory requirements. It also aids EYSweden’s continual efforts to identify areas where we canimprove our performance or enhance our policies andprocedures.

Implemented annually, the program is coordinated andmonitored by representatives of the Global PPD network,with oversight by Global Assurance leadership.

The engagements reviewed each year are selected on a risk-based approach, emphasizing audit engagements that arelarge, complex or of significant public interest. The GlobalAQR program includes detailed risk-focused file reviewscovering a large sample of listed and non-listed auditengagements to measure compliance with internal policiesand procedures, EY GAM requirements, and relevant localprofessional standards and regulatory requirements. It alsoincludes reviews of a sample of non-audit engagements.These measure compliance with the relevant professionalstandards and internal policies and procedures that shouldbe applied in executing non-audit services. In addition,practice-level reviews are performed to assess compliancewith quality control policies and procedures in thefunctional areas set out in ISQC No. 1. The Global AQRprogram complements external practice monitoring andinspection activities, such as regulatory inspectionprograms and external peer reviews.

AQR reviewers and team leaders are selected for their skillsand professional competence in accounting and auditing, aswell as their industry specialization; they often work in theGlobal AQR program for a number of years and are highlyskilled in the execution of the program. Team leaders andreviewers are assigned to inspections outside of their homelocation and are independent of the audit teams reviewed.

The results of the Global AQR program, external practice-monitoring and inspection activities are evaluated andcommunicated to improve quality. Any quality improvementplans describe the follow-up actions to be taken, the peopleresponsible, the timetable and deadlines, and sign-off oncompleted actions. Measures to resolve audit qualitymatters noted from the Global AQR program, regulatoryinspections and peer reviews are addressed by Assuranceleadership and our PPD. The actions are monitored by ourPPD and Assurance leadership. These programs provideimportant practice monitoring feedback for our continuingquality improvement efforts.

In 2016 29 (25) larger audit engagements were subject toGlobal AQR whereof 8 (10) were PIE audit engagements. 7(10) of the PIE engagements inspected internally by EYGwere rated as having no material findings or deficiencies. Inthe engagement with significant findings, the main areaswere connected to IT and tax. In accordance with ourSustainable Audit Quality program a root cause analysis wasprepared and remedial action plans put in place. Coachingresources were established to support the team to re-establish good quality and learn from the inspectionfindings.

In addition to the Global AQR we also perform a Nordic AQRtailored for our smaller audit clients. Results in the non-PIEquality controls were, as last year, considerably better than

Transparency Report 2017: EY Sweden 15

in former years. However, there is potential forimprovement for certain engagements and we are workingon actions to improve audit quality in the engagements inquestion. In our continuous work with the Sustainable AuditQuality program, on engagement level significant findingsare followed-up and remedial action plans are put in placeand monitored.

External qualityassurance reviewEY Sweden’s audit practice and our registered statutoryauditors of Public Interest Entities are subject to inspectionevery three years by the Swedish Inspectorate of Auditors(Revisorsinspektionen, hereinafter “RI”). The regulator hasduring this year changed its name from the SupervisoryBoard of Public Accountants (Revisorsnämnden). We arealso subject to inspection by the Public CompanyAccounting Oversight Board (hereinafter “PCAOB”), asapplicable. In addition, we were subject to an inspectionperformed by the Institute of Public Accountants (“FAR”) ofprivate companies on behalf of the RI.

The last quality assurance inspection by the RI and thePCAOB took place in 2016. The final reports on theinspection were issued by the PCAOB on December 15,2016 and by the RI on January 24, 2017. The FAR reportwas issued on February 15, 2017.

We respect and benefit from all inspection processes. Wethoroughly evaluate points raised during the inspection inorder to identify areas where we can improve audit quality.Together with our AQR process, external inspections aid usin making our audits and related control processes of thehighest quality in the interests of investors and otherstakeholders.

The inspection performed by the PCAOB was comprised of apractice level inspection and inspection of three auditengagements. No findings were reported in the issuedreport from PCAOB from the inspection.

The Inspection performed by the RI also comprised of apractice level inspection and inspection of seven PIE auditengagements. The issued report by RI did not report anyfindings regarding the practice level inspection. Regardingthe engagement inspection the report containsrecommendations on areas such as documentation,analytical procedures, inventory and communication andreporting. No area covered by the recommendations wasdeemed significant enough to require immediate actions. Asrequested we have responded with an action plan to therecommendations in the report which received approvalfrom RI. The overall result from RI’s inspection showsimprovements in our audit quality compared to the latestinspection three years ago.

The FAR inspection contained the same elements as theother two and reported no significant or material findings.

Information on the above-mentioned regulators along withpublicly available inspection reports can be found at:

www.revisorsnamnden.se and www.pcaobus.org. The FARreport is not publicly available.

Compliance with legalrequirementsThe EY Global Code of Conduct provides a clear set ofstandards that guide our actions and business conduct.EY Sweden complies with applicable laws and regulations,and EY’s values underpin our commitment to doing theright thing. This important commitment is supported by anumber of policies and procedures, explained in theparagraphs below.

Anti-briberyThe EY Global Anti-bribery Policy provides EY people withdirection around certain unethical and illegal activities. Itemphasizes the obligation to comply with anti-bribery lawsand provides greater definition of what constitutes bribery.It also identifies reporting responsibilities when bribery isdiscovered. In recognition of the growing global impact ofbribery and corruption, efforts have been increased toembed anti-bribery measures across EY.

Insider tradingThe EY Global Insider Trading Policy reaffirms the obligationof our people not to trade in securities with insiderinformation, provides detail on what constitutes insiderinformation and identifies with whom our people shouldconsult if they have questions regarding theirresponsibilities.

Trade sanctionsIt is important that we are aware of the ever-changingsituation with respect to international trade sanctions. EYmonitors sanctions issued in multiple geographies andprovides guidance to our people on impacted activities.

Data privacyThe EY Global Personal Data Privacy Policy sets out theprinciples to be applied to the use and protection ofpersonal data, including that relating to current, past andprospective personnel, clients, suppliers, and businessassociates. This policy is consistent with applicable laws andregulations concerning data protection and privacy formaintaining and processing personal data. Furthermore, wehave a policy to address our specific Swedish data privacyrequirements and business needs.

Document retentionEY Sweden’s record retention policy applies to allengagements and personnel. This policy addressesdocument preservation whenever any person becomesaware of any actual or reasonably anticipated claim,litigation, investigation, subpoena or other governmentproceeding involving us or one of our clients that may relateto our work. It also addresses Swedish legal requirementsapplicable to the creation and maintenance of workingpapers relevant to the work performed.

Transparency Report 2017: EY Sweden 16

Independence practicesEY Global Independence policies require EY Sweden and ourpeople to comply with the independence standardsapplicable to specific engagements, including, for example,the Code of Ethics of the IESBA and the Auditor’s Act.

We consider and evaluate independence from severalperspectives, including our financial relationships and thoseof our people; employment relationships; businessrelationships; the permissibility of non-audit services weprovide to audit clients; applicable firm and partner rotationrequirements; fee arrangements; audit committee pre-approval, where applicable; and partner remuneration andcompensation.

Failure to comply with applicable professionalindependence requirements will factor into decisionsrelating to a person’s promotion and compensation,and may lead to other disciplinary measures, includingseparation from EY Sweden.

EY Sweden has implemented EY’s global applications, toolsand processes to support us, our professionals and otheremployees in complying with independence policies.

EY Global Independence PolicyThe EY Global Independence Policy contains theindependence requirements for member firms,professionals and other personnel. It is a robust policypredicated on the IESBA Code of Ethics and supplementedby more stringent requirements where prescribed by agiven regulator. The policy also contains guidance to helppeople apply the independence rules. The EY GlobalIndependence Policy is readily accessible and easilysearchable on the EY intranet.

Global Independence System (GIS)The GIS is an intranet-based tool that helps EY professionalsidentify the listed entities from which independence isrequired and the independence restrictions that apply. Mostoften, these are listed audit clients and their affiliates, butthey can be other types of attest or assurance clients too.The tool includes family-tree data relating to affiliates oflisted audit clients and is updated by client-servingengagement teams. The entity data includes notations thatindicate the independence rules that apply to each entity,helping our people determine the type of services that can

be provided or other interests or relationships that can beentered into.

Global Monitoring System (GMS)The GMS is another important global tool that assists inidentifying proscribed securities and other impermissiblefinancial interests. Professionals ranked as manager andabove are required to enter details about all securities theyhold, or those held by their immediate family, into the GMS.When a proscribed security is entered or if a security theyhold becomes proscribed, professionals receive a notice,and are required to dispose of the security. Identifiedexceptions are reported through the Global IndependenceIncident Reporting System (GIIRS) for regulatory matters.

GMS also facilitates annual and quarterly confirmation ofcompliance with independence policies, as described below.

Independence complianceEY has established a number of processes and programsaimed at monitoring the compliance with independencerequirements of EY member firms and their people. Theseinclude the following activities, programs and processes.

Independence confirmations

Annually, EY Sweden is included in an Area-wide process toconfirm compliance with the EY Global Independence Policyand process requirements, and to report identifiedexceptions, if any.

All EY professionals, and certain others, based on their roleor function, are required to confirm compliance withindependence policies and procedures at least once a year.All partners are required to confirm compliance quarterly.

Global independence compliance reviews

EY conducts internal procedures to assess member firmcompliance with independence matters. These reviewsinclude aspects of compliance related to non-audit services,business relationships with the companies we audit andfinancial relationships of member firms.

Transparency Report 2017: EY Sweden 17

Personal independence compliance testing

Each year, the EY Global Independence team establishes aprogram for testing compliance with personal independenceconfirmation requirements and with reporting ofinformation into GMS. For the 2016 testing cycle, EYSweden tested more than 90 partners and other personnel.

Non-audit services

We monitor compliance with professional standardsgoverning the provision of non-audit services to auditclients through a variety of mechanisms. These include theuse of tools, such as PACE (see page 11) and ServiceOffering Reference Tool (see below), and training andrequired procedures completed during the performance ofaudits and internal inspection processes.

Global independence learning

EY develops and deploys a variety of independence learningprograms. All professionals and certain other personnelare required to participate in annual independence learningto help maintain our independence from the companieswe audit.

The goal is to help EY people understand theirresponsibility and to enable each of them, and theirmember firms, to be free from interests that might beregarded as incompatible with objectivity, integrity andimpartiality in serving an audit client.

The annual independence learning program coversindependence requirements focusing on recent changes topolicy, as well as recurring themes and topics ofimportance. Timely completion of annual independencelearning is required and is monitored closely.

In addition to the annual learning program, independenceawareness is promoted through a number of events andmaterials, including new-hire programs, milestone programsand core service line curricula.

Service Offering Reference Tool (SORT)

We assess and monitor our portfolio of services on anongoing basis to confirm that they are permitted by law andprofessional standards, and to make sure that we have theright methodologies, procedures and processes in place asnew service offerings are developed. We restrict servicesfrom being provided that could present undueindependence or other risks. SORT provides EY people withinformation about EY service offerings. It includes guidancearound which services can be delivered to audit and non-audit clients, as well as independence and other riskmanagement issues.

Business Relationship Evaluation Tool (BRET)

The BRET process helps to support compliance withindependence requirements. Our people are required to useBRET in many circumstances to identify, evaluate andobtain advance approval of a potential business relationshipwith an audit client.

Audit committees and oversight of independenceWe recognize the important role audit committees andsimilar corporate governance bodies undertake in theoversight of auditor independence. Empowered andindependent audit committees perform a vital role on behalfof shareholders in protecting independence and preventingconflicts of interest. We are committed to robust andregular communication with audit committees or thosecharged with governance. Through EY quality reviewprograms, we monitor and test compliance with EYstandards for audit committee communications, as well asthe pre-approval of non-audit services, where applicable.

Transparency Report 2017: EY Sweden 18

Continuing education ofaudit professionalsProfessional developmentThe EY career development framework, EYU, provides ourpeople with opportunities for the right experiences, learningand coaching to help them grow and achieve their potential.

The learning component of EYU is based on an extensiveand globally consistent learning curriculum that helps all EYpeople develop the right technical and personal leadershipskills, wherever they are located around the world. Coreaudit training courses are supplemented by learningprograms that are developed in response to changes inaccounting and reporting standards, independence andprofessional standards, and emerging practice issues.

EY has redesigned its core audit training into “The AuditAcademy” — a curriculum for learning. This high-impact andaward-winning learning combines interactive classroom-based simulations and “on-demand” e-learning moduleswith relevant reinforcement and application support.

Where an EYG member firm audits and reviewsInternational Financial Reporting Standards (IFRS) financialstatements, relevant team members undertake learning tobecome IFRS-accredited.

EY Sweden requires our audit professionals to obtain atleast 20 hours of continuing professional education eachyear and at least 120 hours over a three-year period. Ofthese hours, 40% (eight hours each year and 48 hours overa three-year period) must cover technical subjects relatedto accounting and auditing. This is more than the SwedishInspectorate of Auditors’ (Revisorsinspektionen)requirements of 100 hours verifiable continuingprofessional education over a five-year period.

In addition to formal learning, professional developmentoccurs through coaching and experiences our professionalsreceive on the job. Coaching helps to transform knowledgeand experience into practice.

Experienced professionals are expected to coach anddevelop less-experienced personnel to create a continuallearning environment. We also manage the assignment ofour people to particular engagements in a systematic waythat helps provide them exposure to a range of experiencesas part of their own development.

Knowledge and internal communicationsIn addition to professional development and performancemanagement, we understand the importance of providingclient engagement teams with up-to-date information tohelp them perform their professional responsibilities. EYmakes significant investments in knowledge andcommunication networks to enable the rapid disseminationof information to help people collaborate and share bestpractices. Examples include:

• EY Atlas, which includes local and internationalaccounting and auditing standards, as well asinterpretive guidance; replacement for GlobalAccounting and Auditing Information Tool (GAAIT)since the fiscal year 2017

• Publications such as International GAAP, IFRSdevelopments and illustrative financial statements

• Global Accounting and Auditing News, a weekly updatecovering assurance and independence policies,developments from standard setters and regulators, aswell as internal commentary thereon

• Practice alerts and webcasts covering a range of globaland country-specific matters designed for continuousimprovement in member firms’ Assurance practices

Performance managementA comprehensive performance management processrequires our people to set goals, have clear workexpectations, receive feedback and talk about theirperformance. The Performance Management andDevelopment Process (PMDP) is designed to help our peoplegrow and succeed in their careers.

Under the PMDP, periodic job performance reviews arecombined with annual self-appraisal and reviews. As part ofthe annual review process, each professional, in conjunctionwith their counselor (an assigned, more experiencedprofessional), identifies opportunities for furtherdevelopment. Professionals and their counselors are guidedby a set of expectations that articulate the knowledge, skillsand behaviors that should be maintained and developed fortheir respective ranks. These expectations are derived from,and align with, the EY Global strategy and values.

Transparency Report 2017: EY Sweden 19

Revenue andremunerationFinancial informationRevenue represents combined, not consolidated, revenuesand includes expenses billed to clients and revenues relatedto billings to other EYG member firms. Revenue amountsdisclosed in this report include revenues from both auditand non-audit clients.

Revenue is presented in accordance with the AnnualAccounts Act and included for:

1. Revenues from the statutory audit of annual andconsolidated financial statements of PIEs, and entitiesbelonging to a group of undertakings whose parentundertaking is a PIE

2. Revenues from the statutory audit of annual andconsolidated financial statements of other entities

3. Revenues from permitted non-audit services to entitiesthat are audited by the statutory auditor or the auditfirm

4. Revenues from non-audit services to other entities

Financial information for the period ended 30 June2017 expressed in SEK million

Service Revenue Percent

Statutory audits anddirectly related servicesfor PIEs

392 9,9%

Other audit services anddirectly related servicesfor non-PIEs

1,482 37,5%

Non-audit servicesprovided to audit clients 935 23,7%

Non-audit servicesprovided to other entities 1,143 28,9%

Total revenue 3,953 100,0%

Partner remunerationQuality is at the center of the EY strategy and is a keycomponent of EY performance management systems. EYSweden’s partners and other professionals are evaluatedand compensated on the basis of criteria that includespecific quality and risk management indicators, coveringboth actions and results.

Global performance management processes cover partnersin EYG member firms around the world. They reinforce theglobal business agenda by linking performance to widergoals and values. These ongoing cyclical processes includegoal setting, personal development planning andperformance review, and are tied to partners’ recognitionand reward. Documenting partners’ goals and performanceis the cornerstone of the evaluation process. A partner’sgoals are required to reflect various global priorities, one ofwhich is quality.