Embed Size (px)

Citation preview

Transparency, Expectations Anchoring and the InflationTarget

Guido Ascari, University of Oxford Anna Florio, Polytechnic of MilanAlessandro Gobbi, Catholic University of Milan

XVII Annual Inflation Targeting SeminarBanco Central do Brasil, 20-22 May 2015

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 1

/ 35

MOTIVATION

“What we need to think about now is whether this could justifysetting a higher inflation target in the future. [...] Shouldpolicymakers therefore aim for a higher target inflation rate in normaltimes, in order to increase the room for monetary policy to react tosuch shocks? To be concrete, are the net costs of inflation muchhigher at, say, 4 percent than at 2 percent, the current target range?”Blanchard, Dell’Ariccia, and Mauro, (2010)

“In this context, raising the inflation objective would likely entailmuch greater costs than benefits. Inflation would be higher andprobably more volatile under such a policy, undermining confidence[...]. Inflation expectations would also likely become significantly lessstable”, Ben S. Bernanke, 2010 Jackson Hole Symposium.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 2

/ 35

MOTIVATION

“What we need to think about now is whether this could justifysetting a higher inflation target in the future. [...] Shouldpolicymakers therefore aim for a higher target inflation rate in normaltimes, in order to increase the room for monetary policy to react tosuch shocks? To be concrete, are the net costs of inflation muchhigher at, say, 4 percent than at 2 percent, the current target range?”Blanchard, Dell’Ariccia, and Mauro, (2010)

“In this context, raising the inflation objective would likely entailmuch greater costs than benefits. Inflation would be higher andprobably more volatile under such a policy, undermining confidence[...]. Inflation expectations would also likely become significantly lessstable”, Ben S. Bernanke, 2010 Jackson Hole Symposium.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 2

/ 35

MOTIVATION

What we now from the (New Keynesian) literature => price stabilityshould be the goal of monetary policy even taking into account theperils of hitting the zero lower bound (Coibion and Gorodnichenko,2010, and Schmitt-Grohè and Uribe, 2010)

but so far did not really address the Fed ex-Chairman’s concern: Doesa higher inflation target unanchor inflation expectations?

Important caveat: normal times, we abstract from ZLB

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 3

/ 35

MOTIVATION

What we now from the (New Keynesian) literature => price stabilityshould be the goal of monetary policy even taking into account theperils of hitting the zero lower bound (Coibion and Gorodnichenko,2010, and Schmitt-Grohè and Uribe, 2010)

but so far did not really address the Fed ex-Chairman’s concern: Doesa higher inflation target unanchor inflation expectations?

Important caveat: normal times, we abstract from ZLB

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 3

/ 35

MOTIVATION

What we now from the (New Keynesian) literature => price stabilityshould be the goal of monetary policy even taking into account theperils of hitting the zero lower bound (Coibion and Gorodnichenko,2010, and Schmitt-Grohè and Uribe, 2010)

but so far did not really address the Fed ex-Chairman’s concern: Doesa higher inflation target unanchor inflation expectations?

Important caveat: normal times, we abstract from ZLB

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 3

/ 35

Research Questions

Would it be more diffi cult for the central bank to stabilize inflationexpectations at higher values of the inflation target?

If yes, what monetary policy could do?

Reaction function => If the central bank targets a higher inflationlevel, does it need to respond more aggressively to inflation to stabilizeexpectations?

Communication strategy: transparency and opacity => Does a centralbank that fixes a higher level of inflation target need to be moretransparent?

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 4

/ 35

Research Questions

Would it be more diffi cult for the central bank to stabilize inflationexpectations at higher values of the inflation target?

If yes, what monetary policy could do?

Reaction function => If the central bank targets a higher inflationlevel, does it need to respond more aggressively to inflation to stabilizeexpectations?

Communication strategy: transparency and opacity => Does a centralbank that fixes a higher level of inflation target need to be moretransparent?

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 4

/ 35

Research Questions

Would it be more diffi cult for the central bank to stabilize inflationexpectations at higher values of the inflation target?

If yes, what monetary policy could do?

Reaction function => If the central bank targets a higher inflationlevel, does it need to respond more aggressively to inflation to stabilizeexpectations?

Communication strategy: transparency and opacity => Does a centralbank that fixes a higher level of inflation target need to be moretransparent?

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 4

/ 35

Research Questions

Would it be more diffi cult for the central bank to stabilize inflationexpectations at higher values of the inflation target?

If yes, what monetary policy could do?

Reaction function => If the central bank targets a higher inflationlevel, does it need to respond more aggressively to inflation to stabilizeexpectations?

Communication strategy: transparency and opacity => Does a centralbank that fixes a higher level of inflation target need to be moretransparent?

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 4

/ 35

Why transparency? Important component of the inflation targetingapproach

To the extent that it can explain its general approach, clarify its plansand objectives, and provide its assessment of the likely evolution ofthe economy, the central bank should be able to reduce uncertainty,focus and stabilize private-sector expectations”. Ben S. Bernanke,speech, March 2003.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 5

/ 35

Why transparency? Important component of the inflation targetingapproach

To the extent that it can explain its general approach, clarify its plansand objectives, and provide its assessment of the likely evolution ofthe economy, the central bank should be able to reduce uncertainty,focus and stabilize private-sector expectations”. Ben S. Bernanke,speech, March 2003.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 5

/ 35

INGREDIENTS

NK macromodel + trend inflation

Learning: What is the right conceptual framework for thinking aboutinflation expectations in the current context? [...] ... fit quitenaturally into the burgeoning literature on learning inmacroeconomics. [...] In a learning context, the concept of anchoredexpectations is easily formalized”Ben S. Bernanke, NBER MonetaryEconomics Workshop, July 2007.

E-stability and speed of convergence

We distinguish between transparency and opacity (Preston, 2006,Eusepi and Preston, 2010)

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 6

/ 35

INGREDIENTS

NK macromodel + trend inflation

Learning: What is the right conceptual framework for thinking aboutinflation expectations in the current context? [...] ... fit quitenaturally into the burgeoning literature on learning inmacroeconomics. [...] In a learning context, the concept of anchoredexpectations is easily formalized”Ben S. Bernanke, NBER MonetaryEconomics Workshop, July 2007.

E-stability and speed of convergence

We distinguish between transparency and opacity (Preston, 2006,Eusepi and Preston, 2010)

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 6

/ 35

INGREDIENTS

NK macromodel + trend inflation

Learning: What is the right conceptual framework for thinking aboutinflation expectations in the current context? [...] ... fit quitenaturally into the burgeoning literature on learning inmacroeconomics. [...] In a learning context, the concept of anchoredexpectations is easily formalized”Ben S. Bernanke, NBER MonetaryEconomics Workshop, July 2007.

E-stability and speed of convergence

We distinguish between transparency and opacity (Preston, 2006,Eusepi and Preston, 2010)

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 6

/ 35

INGREDIENTS

NK macromodel + trend inflation

Learning: What is the right conceptual framework for thinking aboutinflation expectations in the current context? [...] ... fit quitenaturally into the burgeoning literature on learning inmacroeconomics. [...] In a learning context, the concept of anchoredexpectations is easily formalized”Ben S. Bernanke, NBER MonetaryEconomics Workshop, July 2007.

E-stability and speed of convergence

We distinguish between transparency and opacity (Preston, 2006,Eusepi and Preston, 2010)

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 6

/ 35

Methodology

E ∗ => non-rational expectations formed on the basis of period t − 1information set

Adaptive learning => recursive least square E&H

Check E-stability by applying E&H machinery (PLM and ALM) andthe speed of convergence

Agents’perceived law of motion (PLM) coincides with the system’sMSV solution (no constant)

OP and TR of the rule as in Preston (2006) => under TR no need tolearn the policy rule

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 7

/ 35

The paper

1 Standard NK model + learning a là Evans and Honkapohja

2 Analyze the E-learnable region and the speed of convergence

3 Analyze the role of transparency vs opacity

4 Analytical results for the zero inflation case

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 8

/ 35

Related literature

No trend inflation

Bullard and Mitra (2002) => Euler equation learning a là Evans andHonkapohja

Preston (2006) and Eusepi and Preston (2010) => OP vs TR andinfinite horizon approach

Ferrero (2007) => speed of convergence under learning

Trend Inflation

Ascari and Ropele (2009) => determinacy

Kobayashi and Muto (2011), Kurozumi (2013) => learning

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 9

/ 35

Results

A higher inflation target tends to destabilize expectations:

both asymptotically: shrinks the E-stability regionand in the transition phase: lower speed of convergence

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 10

/ 35

Results

A higher inflation target tends to destabilize expectations:

both asymptotically: shrinks the E-stability region

and in the transition phase: lower speed of convergence

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 10

/ 35

Results

A higher inflation target tends to destabilize expectations:

both asymptotically: shrinks the E-stability regionand in the transition phase: lower speed of convergence

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 10

/ 35

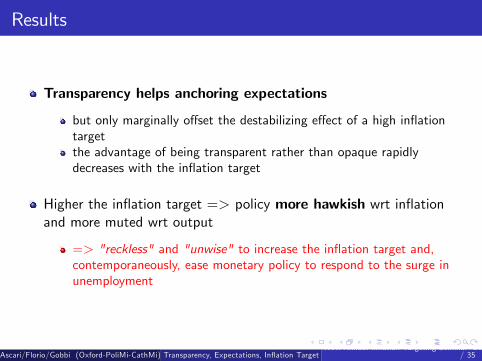

Results

Transparency helps anchoring expectations

but only marginally offset the destabilizing effect of a high inflationtargetthe advantage of being transparent rather than opaque rapidlydecreases with the inflation target

Higher the inflation target => policy more hawkish wrt inflationand more muted wrt output

=> "reckless" and "unwise" to increase the inflation target and,contemporaneously, ease monetary policy to respond to the surge inunemployment

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 11

/ 35

Results

Transparency helps anchoring expectations

but only marginally offset the destabilizing effect of a high inflationtarget

the advantage of being transparent rather than opaque rapidlydecreases with the inflation target

Higher the inflation target => policy more hawkish wrt inflationand more muted wrt output

=> "reckless" and "unwise" to increase the inflation target and,contemporaneously, ease monetary policy to respond to the surge inunemployment

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 11

/ 35

Results

Transparency helps anchoring expectations

but only marginally offset the destabilizing effect of a high inflationtargetthe advantage of being transparent rather than opaque rapidlydecreases with the inflation target

Higher the inflation target => policy more hawkish wrt inflationand more muted wrt output

=> "reckless" and "unwise" to increase the inflation target and,contemporaneously, ease monetary policy to respond to the surge inunemployment

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 11

/ 35

Results

Transparency helps anchoring expectations

but only marginally offset the destabilizing effect of a high inflationtargetthe advantage of being transparent rather than opaque rapidlydecreases with the inflation target

Higher the inflation target => policy more hawkish wrt inflationand more muted wrt output

=> "reckless" and "unwise" to increase the inflation target and,contemporaneously, ease monetary policy to respond to the surge inunemployment

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 11

/ 35

Results

Transparency helps anchoring expectations

but only marginally offset the destabilizing effect of a high inflationtargetthe advantage of being transparent rather than opaque rapidlydecreases with the inflation target

Higher the inflation target => policy more hawkish wrt inflationand more muted wrt output

=> "reckless" and "unwise" to increase the inflation target and,contemporaneously, ease monetary policy to respond to the surge inunemployment

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 11

/ 35

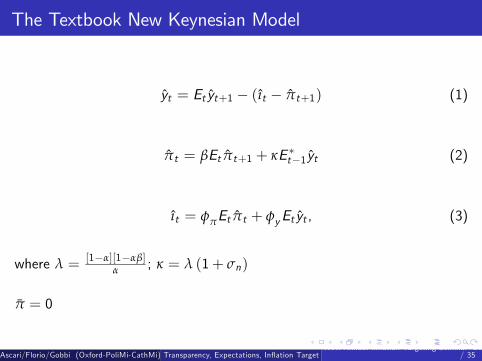

The Textbook New Keynesian Model

yt = Et yt+1 − (ıt − πt+1) (1)

πt = βEt πt+1 + κE ∗t−1yt (2)

ıt = φπEt πt + φyEt yt , (3)

where λ = [1−α][1−αβ]α ; κ = λ (1+ σn)

π = 0

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 12

/ 35

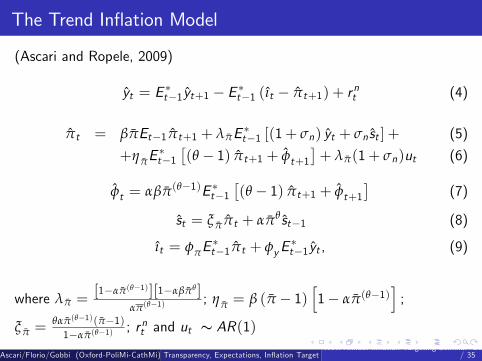

The Trend Inflation Model

(Ascari and Ropele, 2009)

yt = E ∗t−1yt+1 − E ∗t−1 (ıt − πt+1) + rnt (4)

πt = βπEt−1πt+1 + λπE ∗t−1 [(1+ σn) yt + σn st ] + (5)

+ηπE∗t−1[(θ − 1) πt+1 + φt+1

]+ λπ(1+ σn)ut (6)

φt = αβπ(θ−1)E ∗t−1[(θ − 1) πt+1 + φt+1

](7)

st = ξππt + απθ st−1 (8)

ıt = φπE∗t−1πt + φyE

∗t−1yt , (9)

where λπ =[1−απ(θ−1)][1−αβπθ]

απ(θ−1); ηπ = β (π − 1)

[1− απ(θ−1)

];

ξπ =θαπ(θ−1)(π−1)1−απ(θ−1)

; rnt and ut ∼ AR(1)

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 13

/ 35

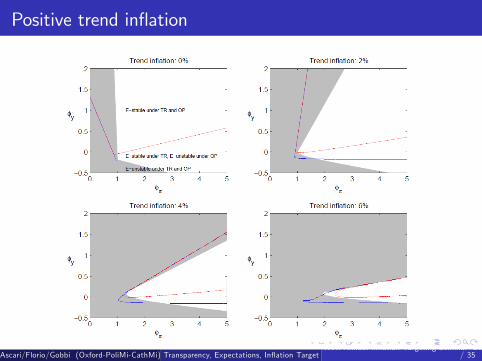

Positive trend inflation

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 14

/ 35

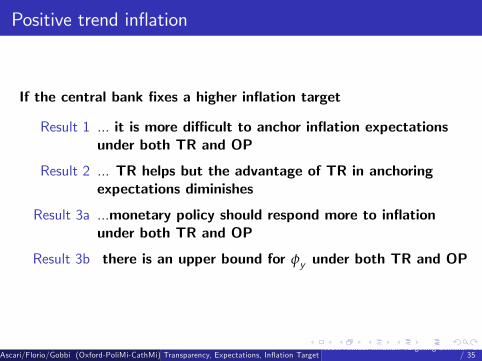

Positive trend inflation

If the central bank fixes a higher inflation target

Result 1 ... it is more diffi cult to anchor inflation expectationsunder both TR and OP

Result 2 ... TR helps but the advantage of TR in anchoringexpectations diminishes

Result 3a ...monetary policy should respond more to inflationunder both TR and OP

Result 3b there is an upper bound for φy under both TR and OP

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 15

/ 35

Speed of convergence

The speed of convergence matters

fast convergence => the economy always very close to the REEslow convergence => economy dynamics dominated by the transitionaldynamics under learning.

Conditional on E-stability => all eigenvalue of the T-map within theunit circle.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 16

/ 35

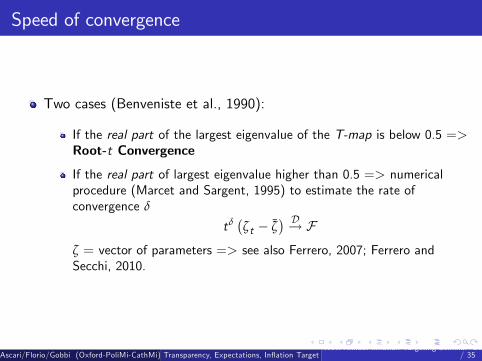

Speed of convergence

Two cases (Benveniste et al., 1990):

If the real part of the largest eigenvalue of the T-map is below 0.5 =>Root-t Convergence

If the real part of largest eigenvalue higher than 0.5 => numericalprocedure (Marcet and Sargent, 1995) to estimate the rate ofconvergence δ

tδ(ζt − ζ

) D→ Fζ = vector of parameters => see also Ferrero, 2007; Ferrero andSecchi, 2010.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 17

/ 35

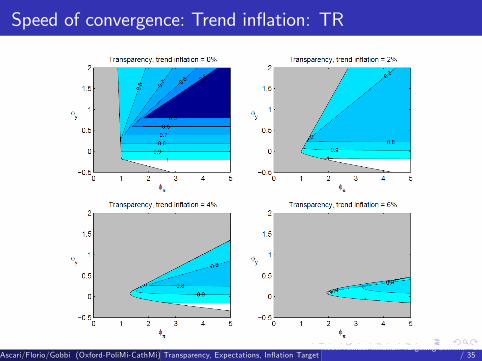

Speed of convergence: Trend inflation: TR

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 18

/ 35

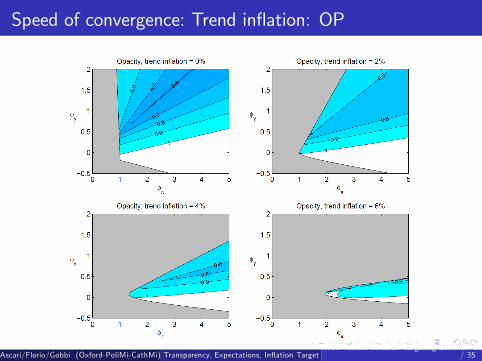

Speed of convergence: Trend inflation: OP

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 19

/ 35

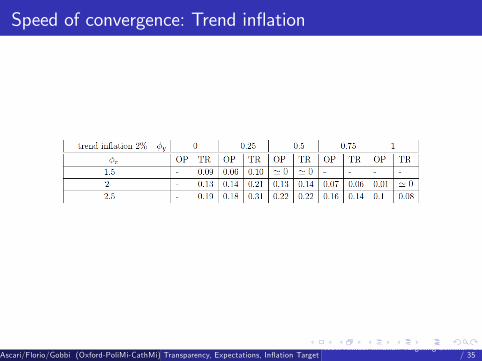

Speed of convergence: Trend inflation

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 20

/ 35

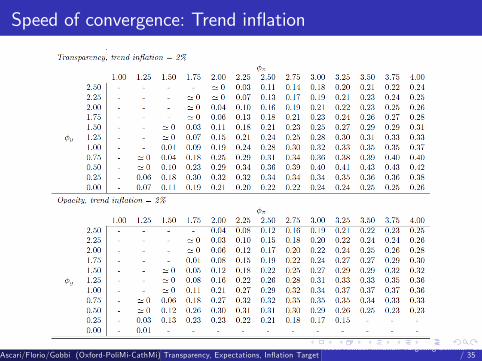

Speed of convergence: Trend inflation

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 21

/ 35

Conclusions

This paper supports the claim that a higher inflation targetunanchors expectations both asymptotically and in thetransition phase => Bernanke is right!

Transparency is an essential component of the inflationtargeting framework and helps in anchoring expectations

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 22

/ 35

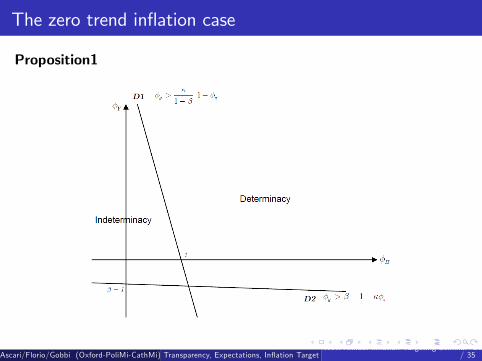

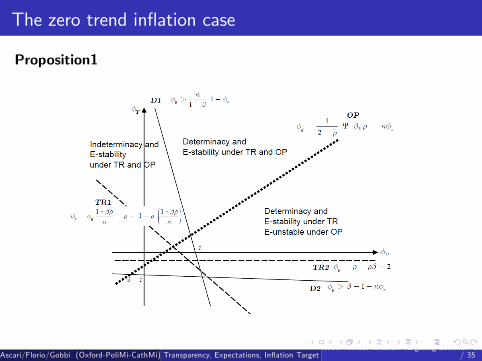

The zero trend inflation case

Proposition1

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 23

/ 35

The zero trend inflation case

Proposition1

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 24

/ 35

The zero trend inflation case

Proposition1

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 25

/ 35

The zero trend inflation case: TR and Policy

Result 1.1 Transparency helps anchoring inflation expectations.Let’s φπ, φy ≥ 0. If the rational expectation equilibrium isdeterminate, then it is always learnable under TR, while thisis not true under OP.

Result similar to Preston (2006) in a E&H environment

Result 1.2 A pure inflation targeting central bank needs to betransparent to anchor inflation expectations.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 26

/ 35

The zero trend inflation case: TR and Policy

Result 1.3 Under OP, monetary policy should respond to theoutput gap. Let’s φπ, φy ≥ 0. If the rational expectationequilibrium is determinate, it is learnable under OP iffφy >

1(2−ρ) (Ψ(β, ρ) + κφπ).

As in Eusepi and Preston (2010) an aggressive response to inflation coulddestabilize expectations under OPAgents do not anticipate the correct policy response => "too much toolate"Output is a more "leading indicator of inflation"

Result 1.4 The Taylor principle is not a necessary condition forE-stability neither under TR nor under OP.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 27

/ 35

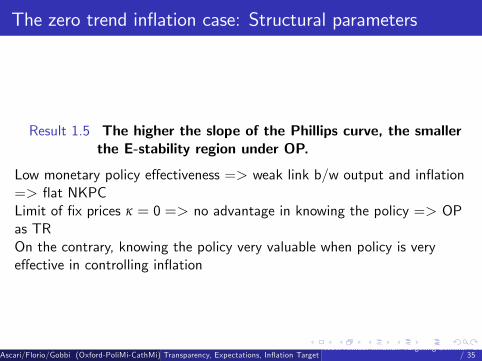

The zero trend inflation case: Structural parameters

Result 1.5 The higher the slope of the Phillips curve, the smallerthe E-stability region under OP.

Low monetary policy effectiveness => weak link b/w output and inflation=> flat NKPCLimit of fix prices κ = 0 => no advantage in knowing the policy => OPas TROn the contrary, knowing the policy very valuable when policy is veryeffective in controlling inflation

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 28

/ 35

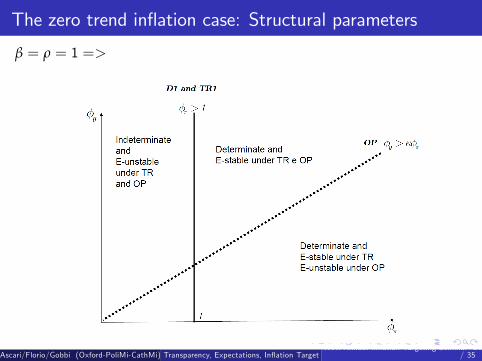

The zero trend inflation case: Structural parameters

β = ρ = 1 =>

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 29

/ 35

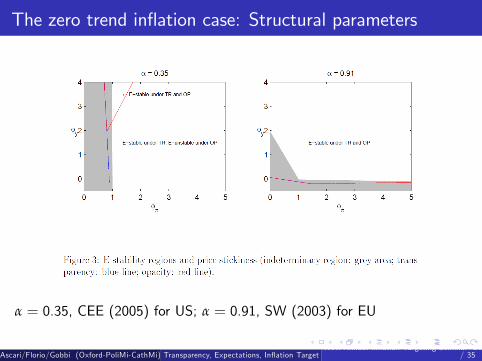

The zero trend inflation case: Structural parameters

α = 0.35, CEE (2005) for US; α = 0.91, SW (2003) for EU

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 30

/ 35

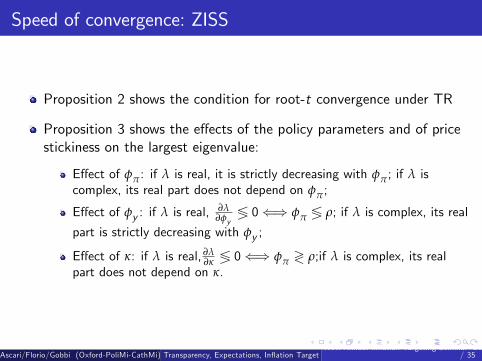

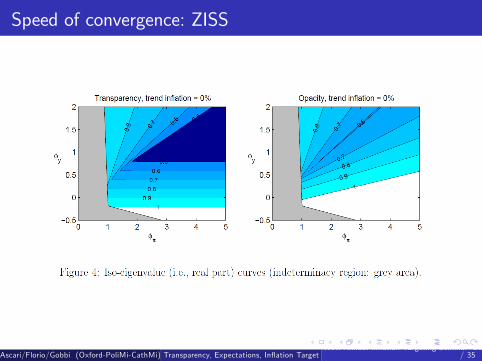

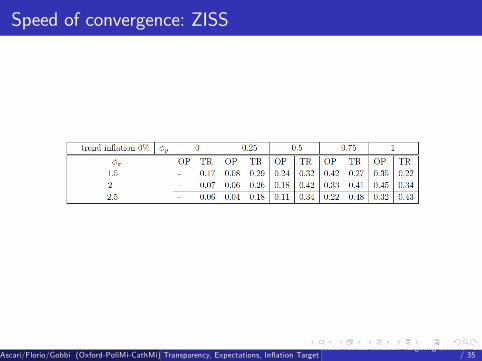

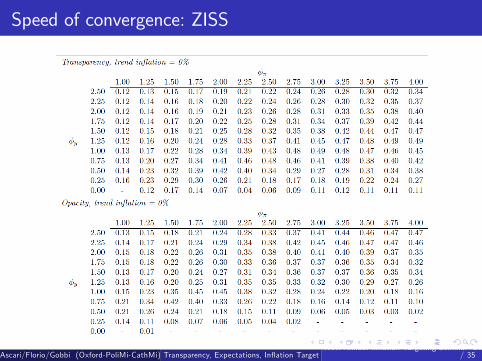

Speed of convergence: ZISS

Proposition 2 shows the condition for root-t convergence under TR

Proposition 3 shows the effects of the policy parameters and of pricestickiness on the largest eigenvalue:

Effect of φπ: if λ is real, it is strictly decreasing with φπ; if λ iscomplex, its real part does not depend on φπ;

Effect of φy : if λ is real, ∂λ∂φy

≶ 0⇐⇒ φπ ≶ ρ; if λ is complex, its real

part is strictly decreasing with φy ;

Effect of κ: if λ is real, ∂λ∂κ ≶ 0⇐⇒ φπ ≷ ρ;if λ is complex, its real

part does not depend on κ.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 31

/ 35

Speed of convergence: ZISS

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 32

/ 35

Speed of convergence: ZISS

Result 1.6 Transparency helps increase the speed of convergence.

Result 1.7 To increase the speed of convergence both φπ and φyhave to increase, both in the case of OP and TR.

Result 1.8 A pure inflation targeting central bank exhibits a verylow speed of convergence.

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 33

/ 35

Speed of convergence: ZISS

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 34

/ 35

Speed of convergence: ZISS

Ascari/Florio/Gobbi (Oxford-PoliMi-CathMi) Transparency, Expectations, Inflation TargetXVII Annual Inflation Targeting Seminar Banco Central do Brasil, 20-22 May 2015 35

/ 35