Embed Size (px)

Citation preview

Transformation 2.0:Creating the Narrative for

Employment Success

PERSON-CENTERED, SYSTEM-WIDE

#Transformation2.0

Transformation 2.0

Changing Business Models

September and November 2016

Presented by

Laurie A. Kelley and Allan Blum

for NYSRA

Agenda

Overview

Effect of Funding Environment

OPWDD’s Integrated Business Model

Considerations for Existing Business with Program

Structure Change

Considerations for a New Business Venture

4-Special Needs/16 Pres/3088h17lk_Transformation2

Effect of Funding Environment

GOOD TIMES

In times of growth money is free-flowing

Banks provide loans

States provide more funding

Agencies grow

4-Special Needs/16 Pres/3088h17lk_Transformation3

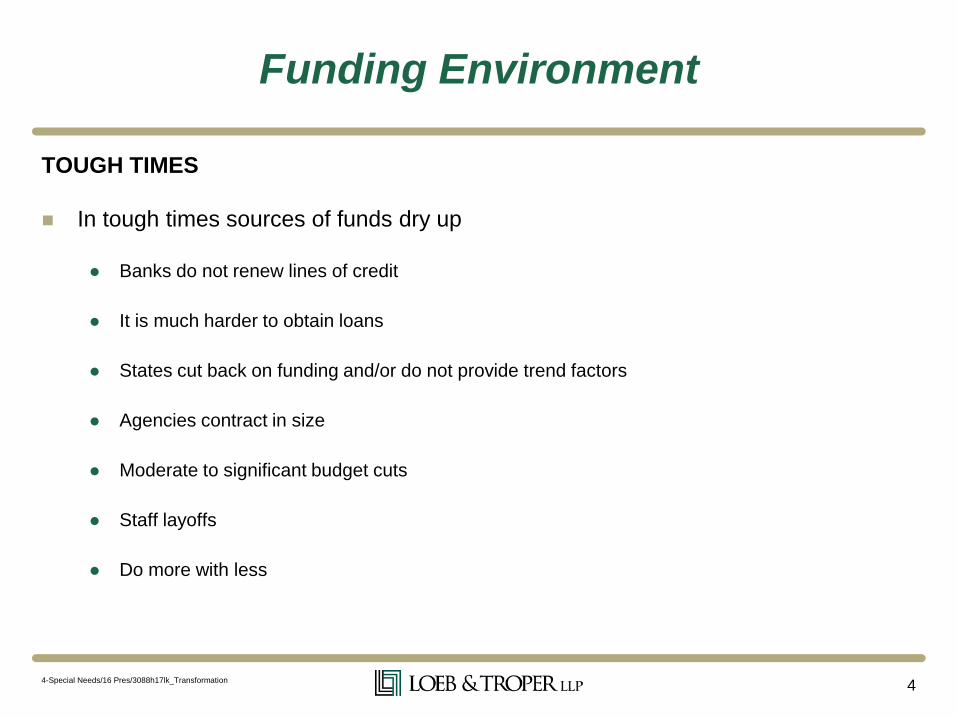

Funding Environment

TOUGH TIMES

In tough times sources of funds dry up

Banks do not renew lines of credit

It is much harder to obtain loans

States cut back on funding and/or do not provide trend factors

Agencies contract in size

Moderate to significant budget cuts

Staff layoffs

Do more with less

4-Special Needs/16 Pres/3088h17lk_Transformation4

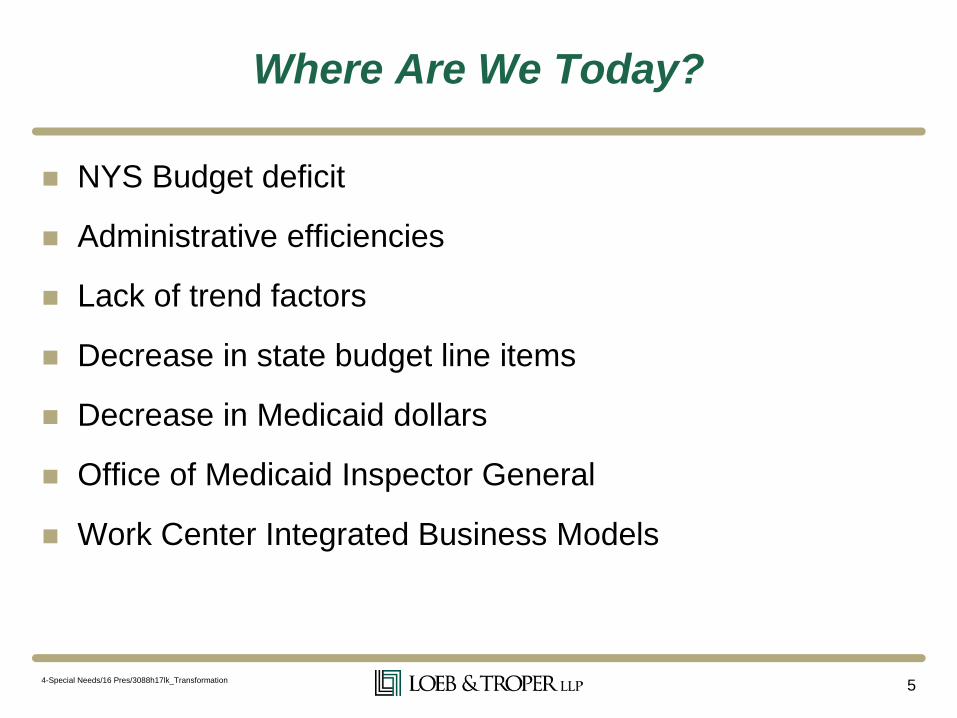

Where Are We Today?

NYS Budget deficit

Administrative efficiencies

Lack of trend factors

Decrease in state budget line items

Decrease in Medicaid dollars

Office of Medicaid Inspector General

Work Center Integrated Business Models

4-Special Needs/16 Pres/3088h17lk_Transformation5

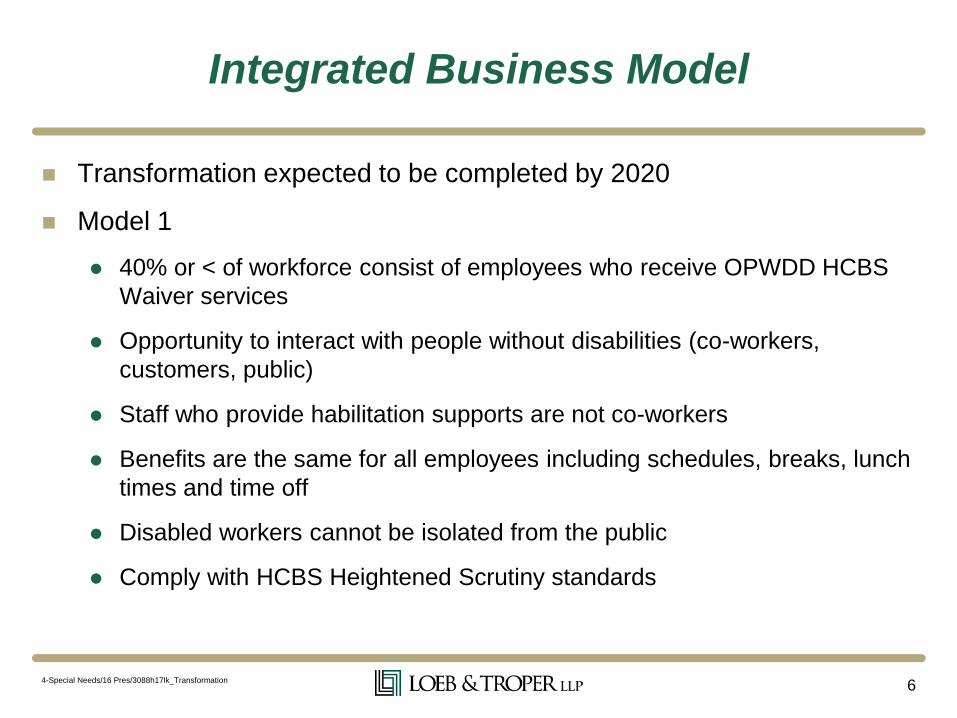

Integrated Business Model

Transformation expected to be completed by 2020

Model 1

40% or < of workforce consist of employees who receive OPWDD HCBS

Waiver services

Opportunity to interact with people without disabilities (co-workers,

customers, public)

Staff who provide habilitation supports are not co-workers

Benefits are the same for all employees including schedules, breaks, lunch

times and time off

Disabled workers cannot be isolated from the public

Comply with HCBS Heightened Scrutiny standards

4-Special Needs/16 Pres/3088h17lk_Transformation6

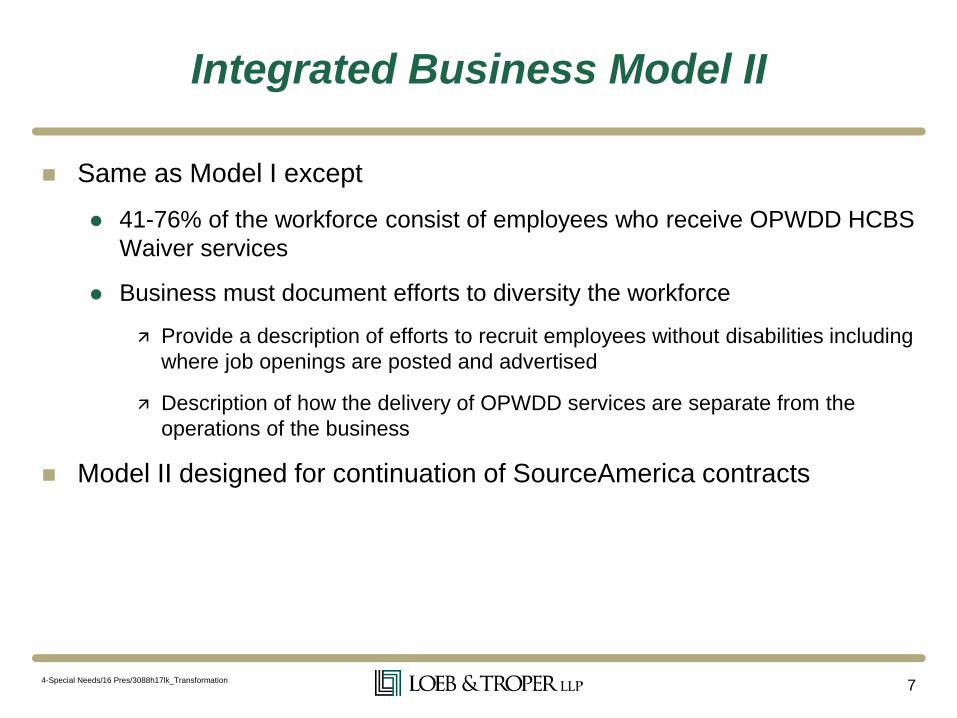

Integrated Business Model II

Same as Model I except

41-76% of the workforce consist of employees who receive OPWDD HCBS

Waiver services

Business must document efforts to diversity the workforce

Provide a description of efforts to recruit employees without disabilities including

where job openings are posted and advertised

Description of how the delivery of OPWDD services are separate from the

operations of the business

Model II designed for continuation of SourceAmerica contracts

4-Special Needs/16 Pres/3088h17lk_Transformation7

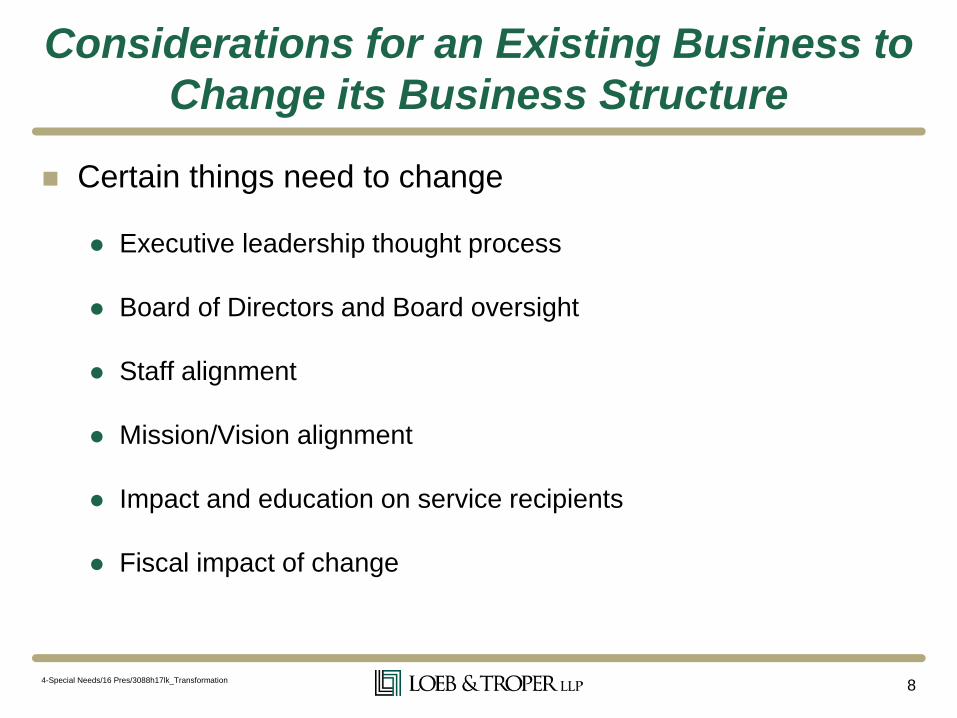

Certain things need to change

Executive leadership thought process

Board of Directors and Board oversight

Staff alignment

Mission/Vision alignment

Impact and education on service recipients

Fiscal impact of change

4-Special Needs/16 Pres/3088h17lk_Transformation8

Considerations for an Existing Business to

Change its Business Structure

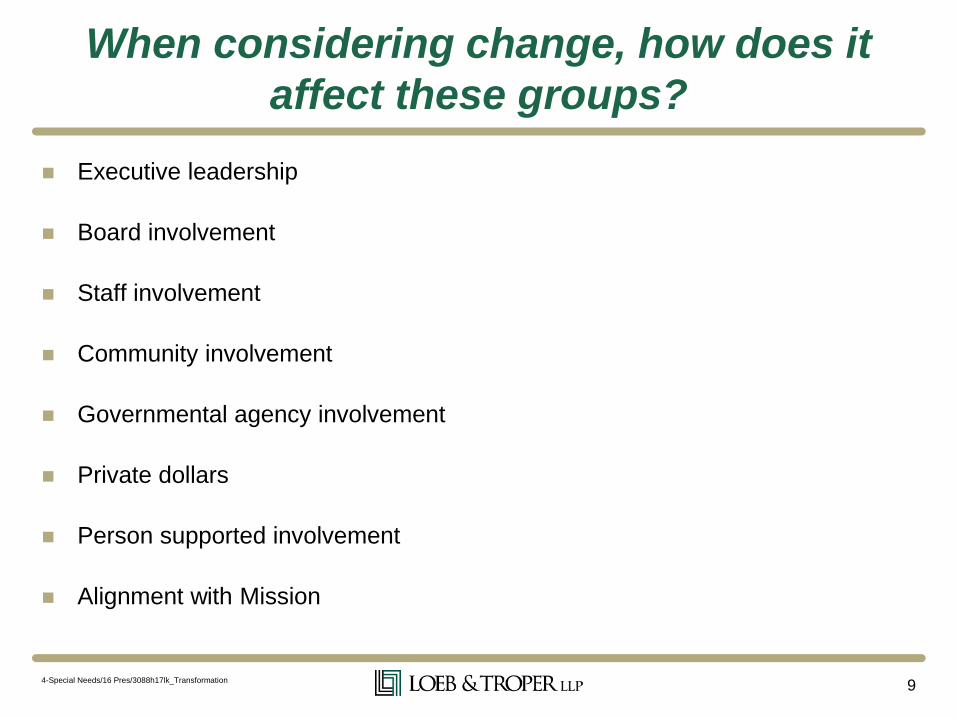

When considering change, how does it

affect these groups?

Executive leadership

Board involvement

Staff involvement

Community involvement

Governmental agency involvement

Private dollars

Person supported involvement

Alignment with Mission

4-Special Needs/16 Pres/3088h17lk_Transformation9

Business Plan

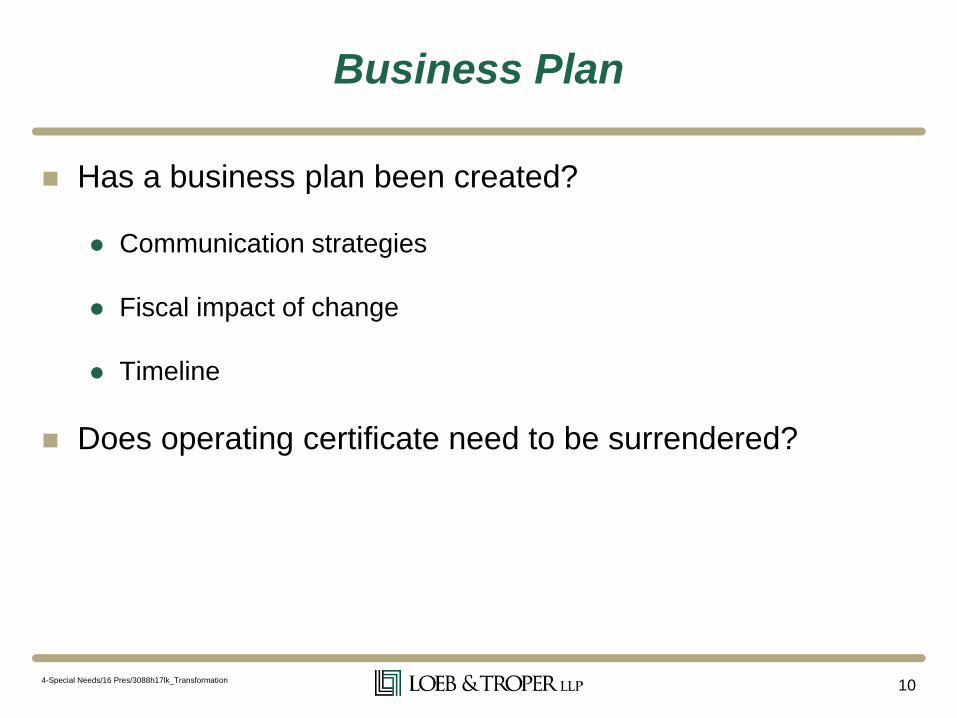

Has a business plan been created?

Communication strategies

Fiscal impact of change

Timeline

Does operating certificate need to be surrendered?

4-Special Needs/16 Pres/3088h17lk_Transformation10

Process for Change

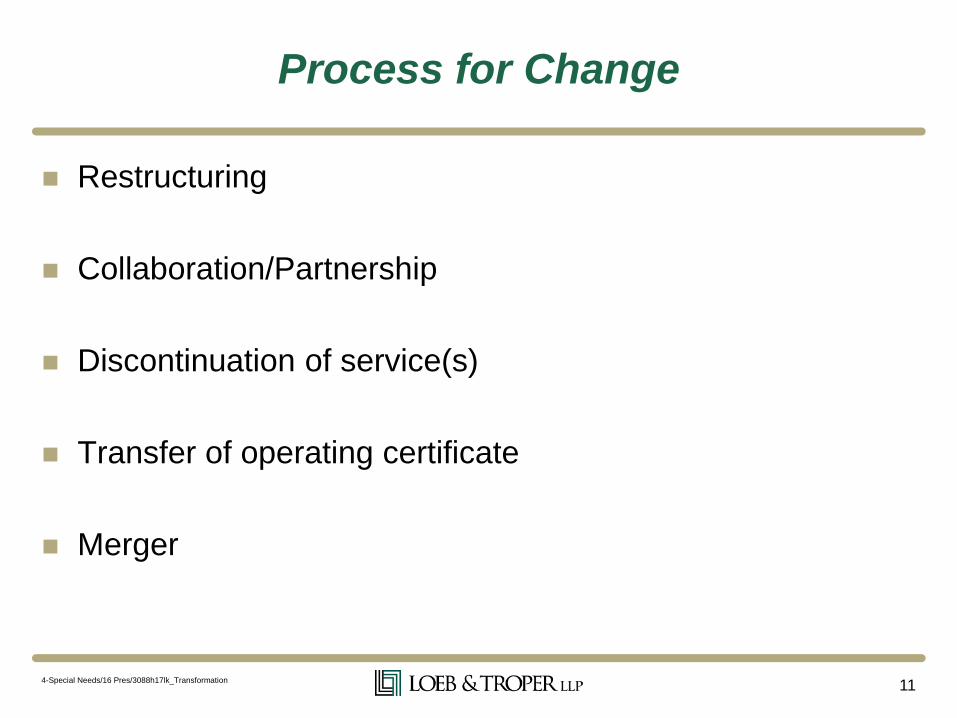

Restructuring

Collaboration/Partnership

Discontinuation of service(s)

Transfer of operating certificate

Merger

4-Special Needs/16 Pres/3088h17lk_Transformation11

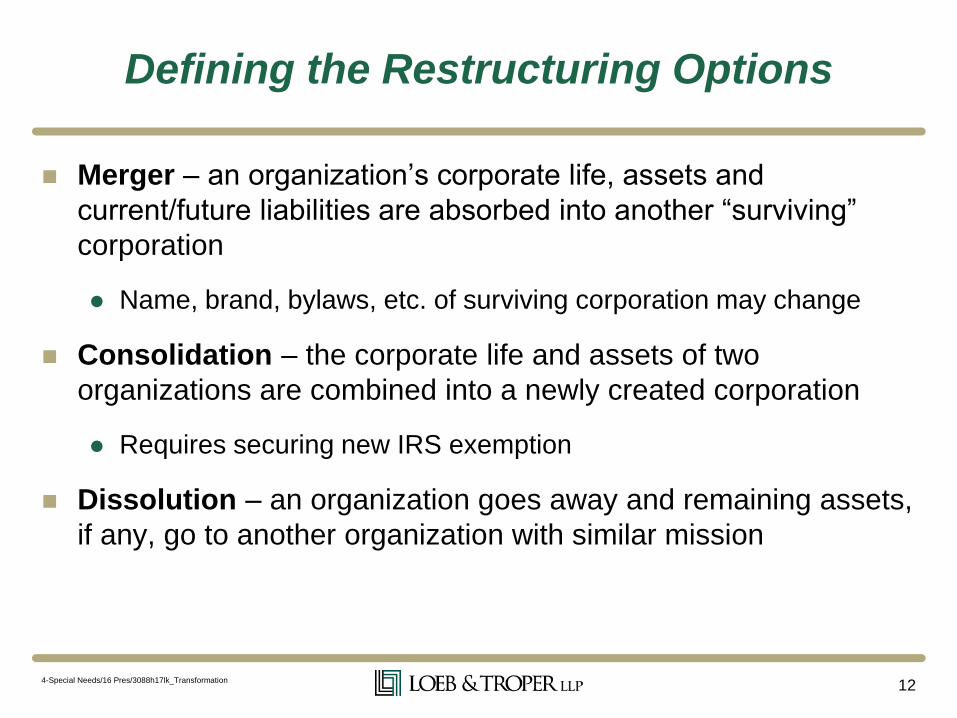

Defining the Restructuring Options

Merger – an organization’s corporate life, assets and

current/future liabilities are absorbed into another “surviving”

corporation

Name, brand, bylaws, etc. of surviving corporation may change

Consolidation – the corporate life and assets of two

organizations are combined into a newly created corporation

Requires securing new IRS exemption

Dissolution – an organization goes away and remaining assets,

if any, go to another organization with similar mission

4-Special Needs/16 Pres/3088h17lk_Transformation12

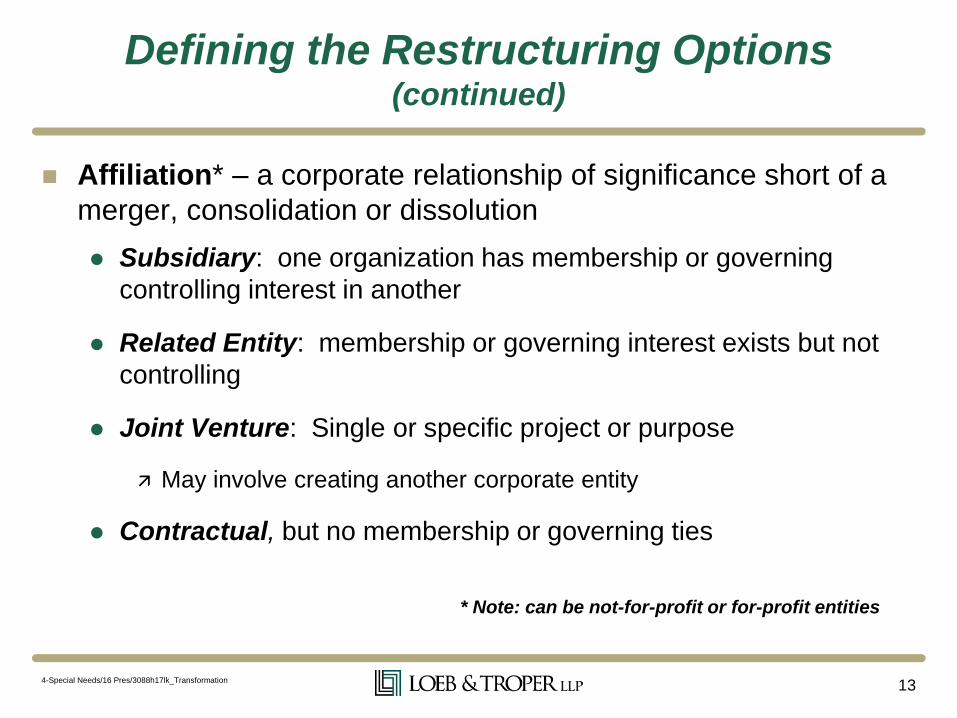

Defining the Restructuring Options (continued)

Affiliation* – a corporate relationship of significance short of a

merger, consolidation or dissolution

Subsidiary: one organization has membership or governing

controlling interest in another

Related Entity: membership or governing interest exists but not

controlling

Joint Venture: Single or specific project or purpose

May involve creating another corporate entity

Contractual, but no membership or governing ties

4-Special Needs/16 Pres/3088h17lk_Transformation13

* Note: can be not-for-profit or for-profit entities

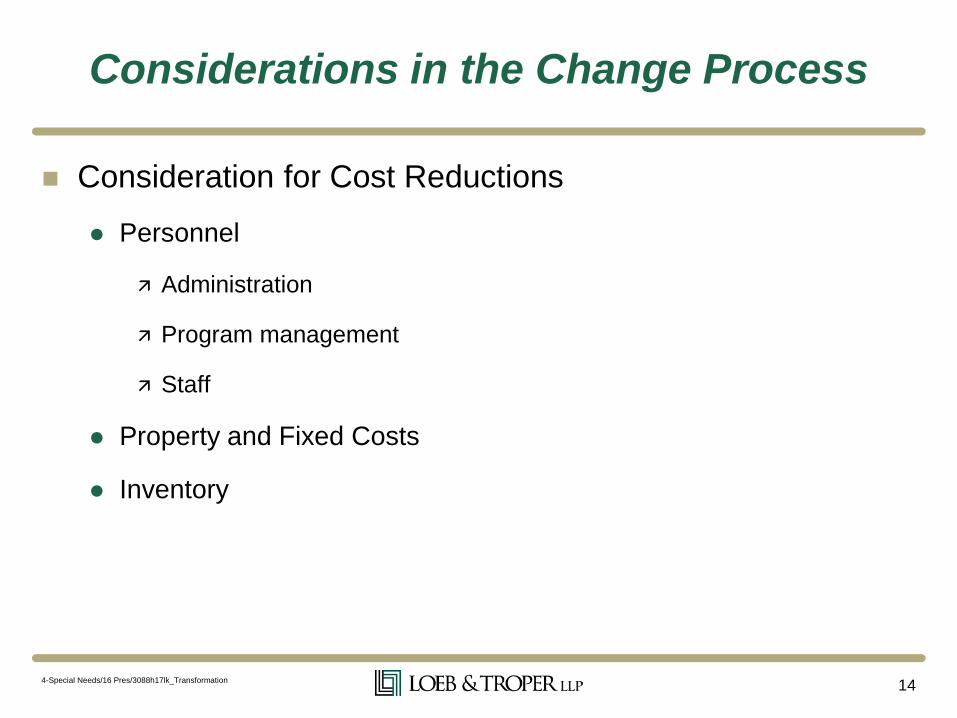

Considerations in the Change Process

Consideration for Cost Reductions

Personnel

Administration

Program management

Staff

Property and Fixed Costs

Inventory

4-Special Needs/16 Pres/3088h17lk_Transformation14

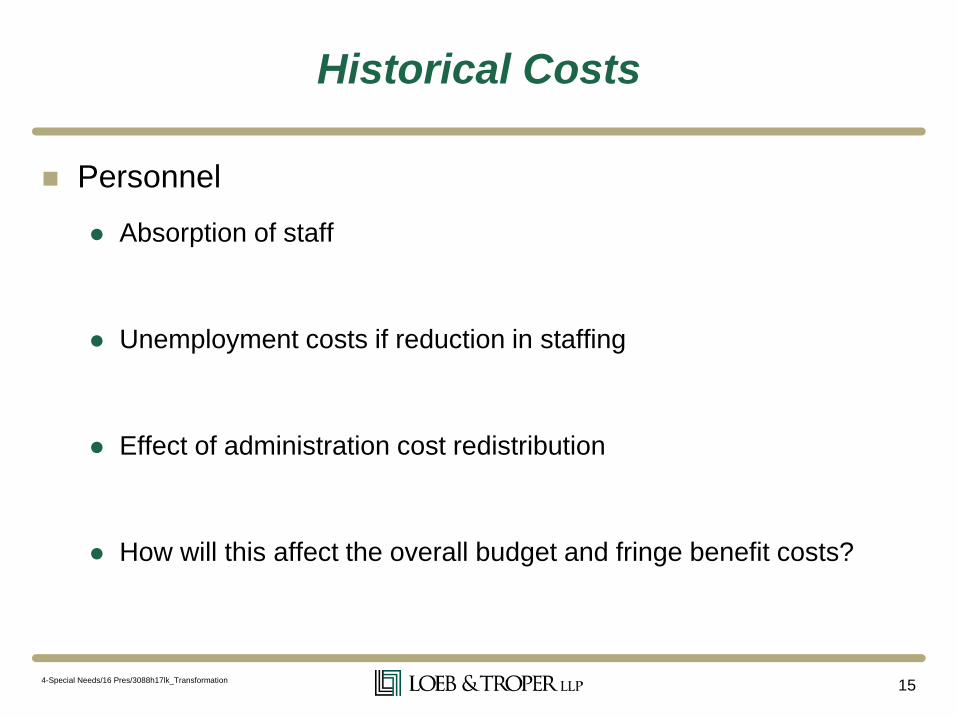

Historical Costs

Personnel

Absorption of staff

Unemployment costs if reduction in staffing

Effect of administration cost redistribution

How will this affect the overall budget and fringe benefit costs?

4-Special Needs/16 Pres/3088h17lk_Transformation15

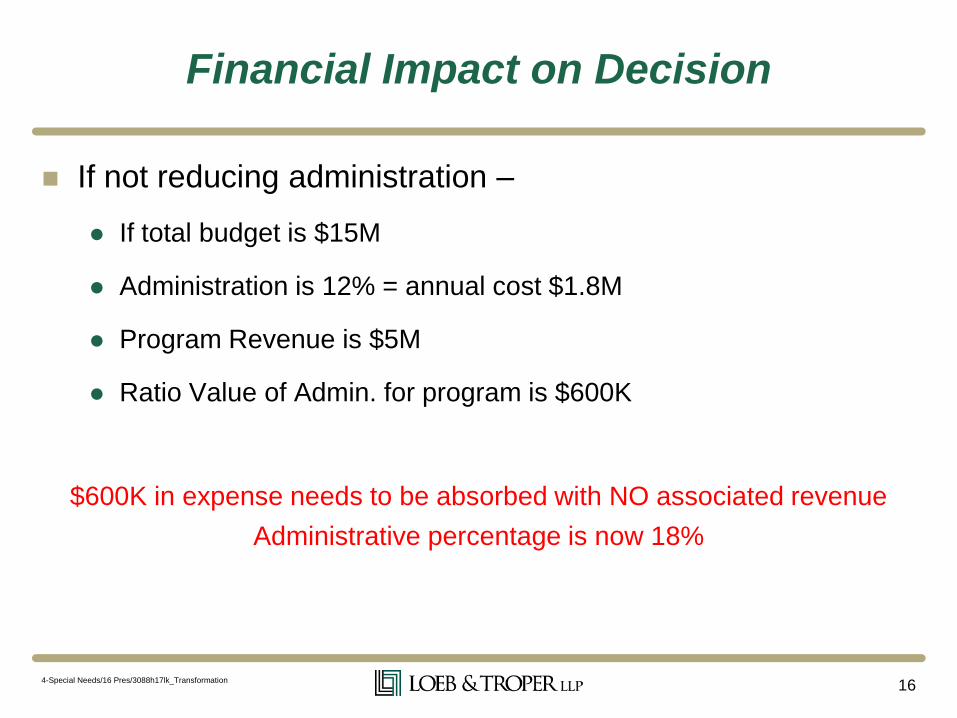

Financial Impact on Decision

If not reducing administration –

If total budget is $15M

Administration is 12% = annual cost $1.8M

Program Revenue is $5M

Ratio Value of Admin. for program is $600K

$600K in expense needs to be absorbed with NO associated revenue

Administrative percentage is now 18%

4-Special Needs/16 Pres/3088h17lk_Transformation16

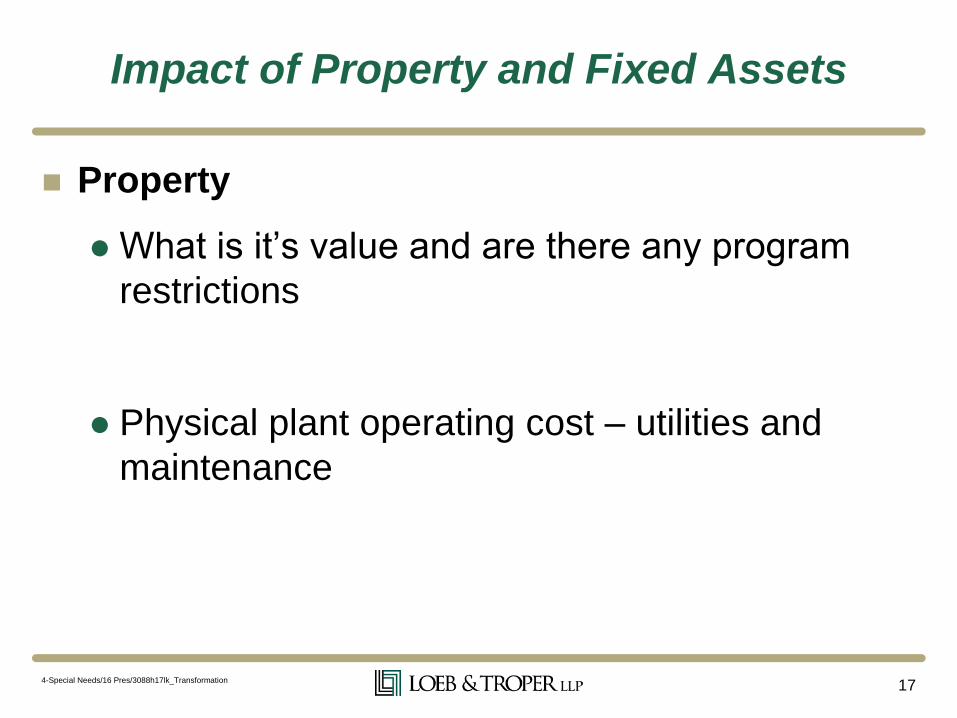

Impact of Property and Fixed Assets

Property

What is it’s value and are there any program

restrictions

Physical plant operating cost – utilities and

maintenance

4-Special Needs/16 Pres/3088h17lk_Transformation17

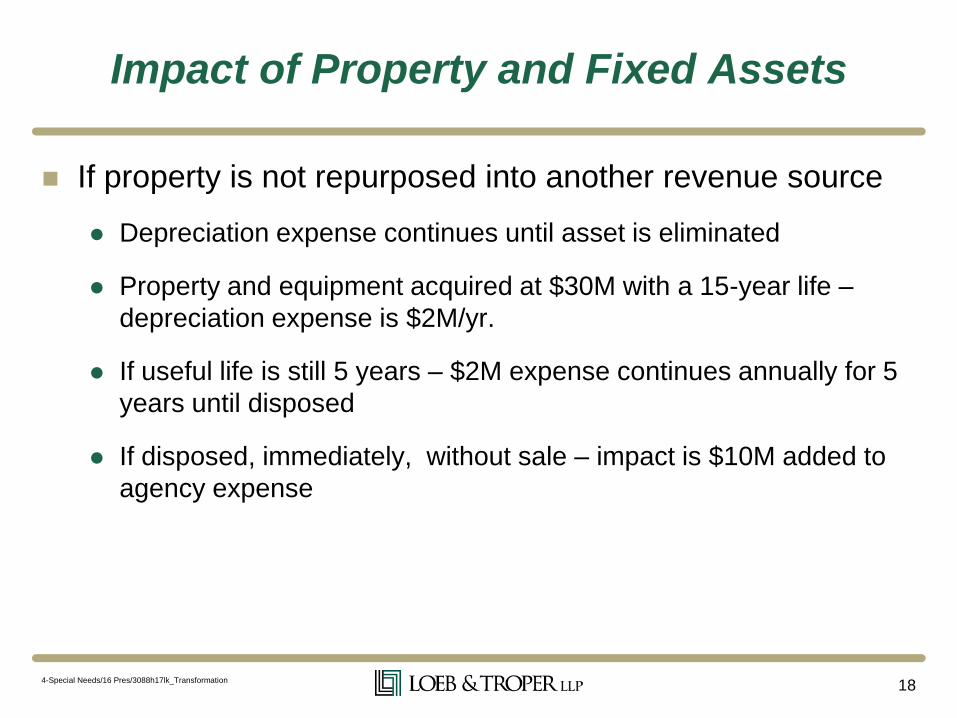

Impact of Property and Fixed Assets

If property is not repurposed into another revenue source

Depreciation expense continues until asset is eliminated

Property and equipment acquired at $30M with a 15-year life –

depreciation expense is $2M/yr.

If useful life is still 5 years – $2M expense continues annually for 5

years until disposed

If disposed, immediately, without sale – impact is $10M added to

agency expense

4-Special Needs/16 Pres/3088h17lk_Transformation18

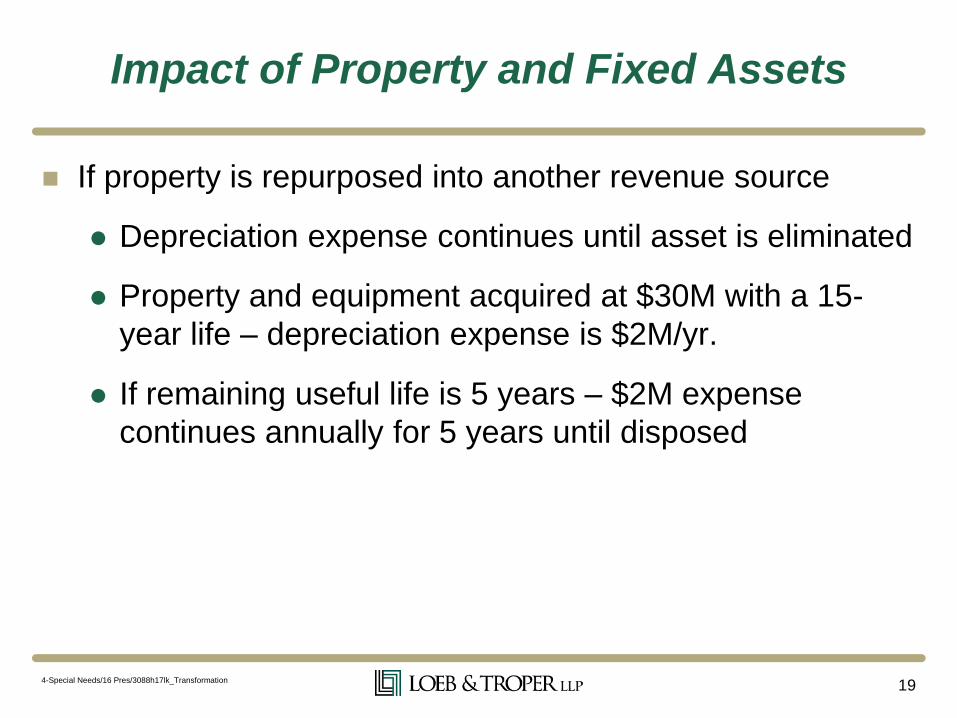

Impact of Property and Fixed Assets

If property is repurposed into another revenue source

Depreciation expense continues until asset is eliminated

Property and equipment acquired at $30M with a 15-

year life – depreciation expense is $2M/yr.

If remaining useful life is 5 years – $2M expense

continues annually for 5 years until disposed

4-Special Needs/16 Pres/3088h17lk_Transformation19

Inventory – Cost of Goods Sold

Determine cost of inventory

Can it be sold?

Does a write off for inventory need to occur?

4-Special Needs/16 Pres/3088h17lk_Transformation20

Other Considerations

Potential unrealized liabilities

A/R and potential write offs from subcontract vendors

Debt covenant requirements

Ability to repurpose fixed assets

Maintaining financial ratios

4-Special Needs/16 Pres/3088h17lk_Transformation21

Considerations for Work Center in New

Organizational Structure

Access to capital

Purchasing and A/P functions

Cost and transferability of employee benefits

Working capital

4-Special Needs/16 Pres/3088h17lk_Transformation22

Considerations for the New Business

Venture

Successful For-Profit business have several

common traits

Focus on profitability

Eliminate waste and inefficiency

Ability to change as necessary (strategically)

Funding (capital)

Clear business model

Low fixed costs

4-Special Needs/16 Pres/3088h17lk_Transformation23

Questions

Laurie A Kelley

Allan Blum

4-Special Needs/16 Pres/3088h17lk_Transformation24

4-Special Needs/16 Pres/3088h17lk_Transformation25

#Transformation2.0

Keep Board Members on Board!

Join Laurie & Allan

Next Week!

Thursday, September 15th

12:00 pm – 1:30 pm