Embed Size (px)

Citation preview

CYPRUS www.bakertillyklitou.com

Transfer Pricing in Cyprus

CYPRUS www.bakertillyklitou.com

New Transfer Pricing Considerations

The philosophy of the new tax-pricing regime is based on the

arm's length principle, as set out in Article 9 of the OECD Model

Tax Convention on Income and on Capital.

This principle is the international standard adopted by OECD

member states for the purpose of determining the transfer prices

between related entities conducting cross-border transactions and

it aims to ensure that the prices of transactions conducted between

affiliated entities, are those that would have been agreed between

independent entities under comparable conditions.

In order to ensure the appropriate application of this principle, the

OECD has developed regularly updated guidelines to be observed

by multinational enterprises when conducting intra-group

transactions, as well as by tax administrations when conducting tax

audits.

CYPRUS www.bakertillyklitou.com

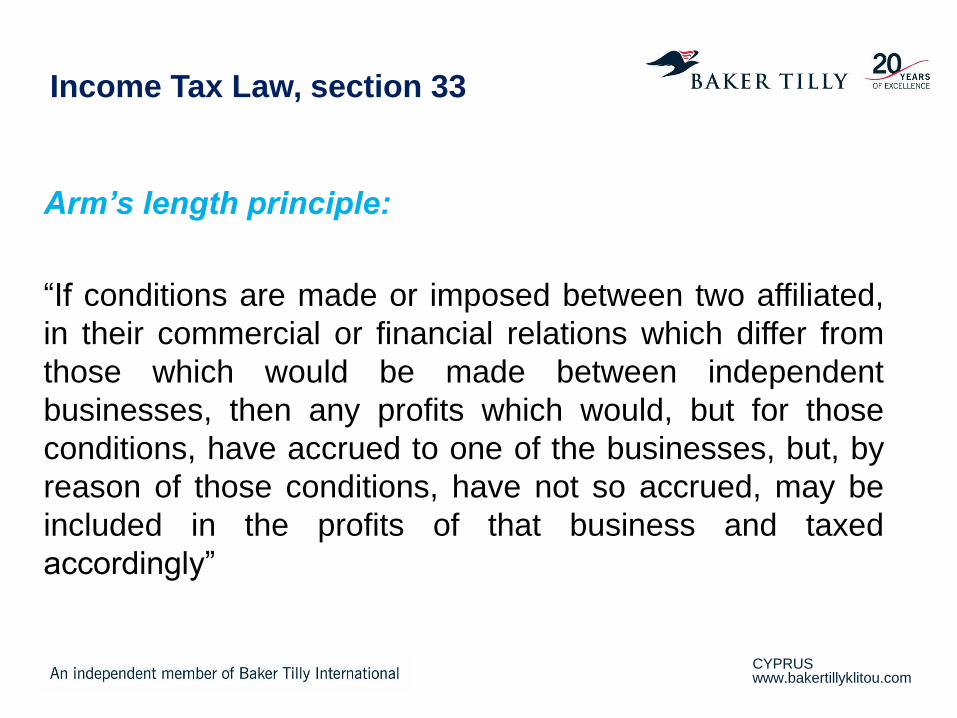

Income Tax Law, section 33

Arm’s length principle:

“If conditions are made or imposed between two affiliated,

in their commercial or financial relations which differ from

those which would be made between independent

businesses, then any profits which would, but for those

conditions, have accrued to one of the businesses, but, by

reason of those conditions, have not so accrued, may be

included in the profits of that business and taxed

accordingly”

CYPRUS www.bakertillyklitou.com

Adjustments by the tax authorities (I)

[4]

Tax authorities are allowed to adjust transactions concluded

between related parties on terms that deviate from those that

would apply in similar transactions carried out between

independent enterprises, in accordance with the arm’s length

principle.

Where the Commissioner of Taxes increases the profits of a

resident business because its transactions or its financial

relations with another resident business were not at arm’s

length, a corresponding credit is granted to the other

business.

CYPRUS www.bakertillyklitou.com

Adjustments by the tax authorities (II)

[5]

Downward adjustments apply as corresponding adjustments

to cases where the taxable profits of a resident business

resulting from a transaction with another resident business

are decreased to reflect an arm’s length price.

Compensating adjustments are also accepted.

Compensating adjustment = the taxpayer propose a transfer

price that is an arm’s length price, even tough this price

differs from the one actually charged.

CYPRUS www.bakertillyklitou.com

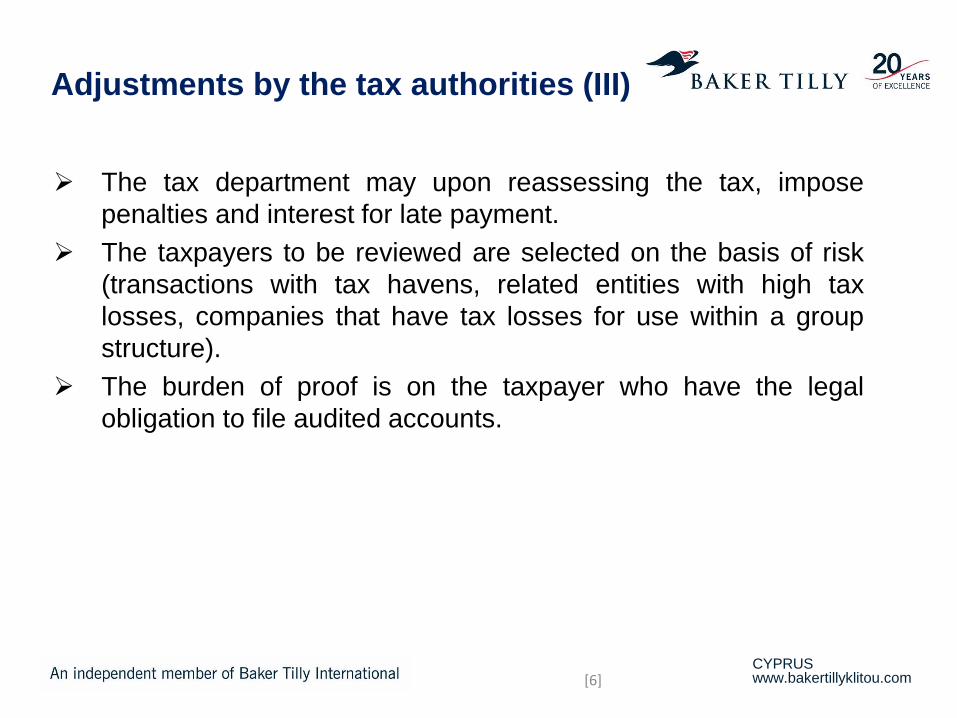

Adjustments by the tax authorities (III)

[6]

The tax department may upon reassessing the tax, impose

penalties and interest for late payment.

The taxpayers to be reviewed are selected on the basis of risk

(transactions with tax havens, related entities with high tax

losses, companies that have tax losses for use within a group

structure).

The burden of proof is on the taxpayer who have the legal

obligation to file audited accounts.

CYPRUS www.bakertillyklitou.com

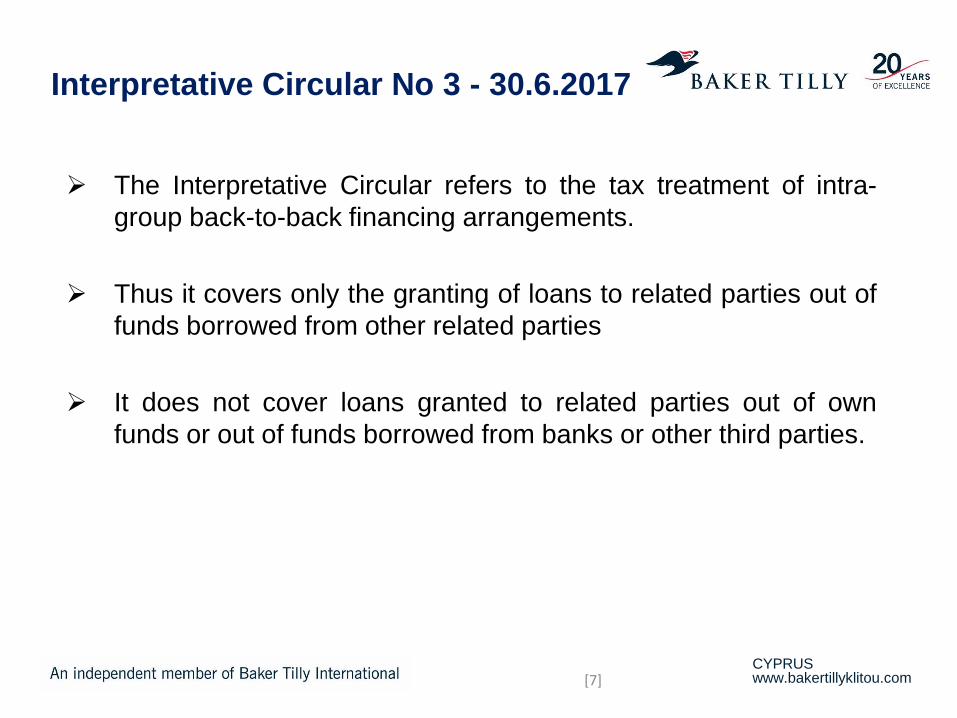

Interpretative Circular No 3 - 30.6.2017

[7]

The Interpretative Circular refers to the tax treatment of intra-

group back-to-back financing arrangements.

Thus it covers only the granting of loans to related parties out of

funds borrowed from other related parties

It does not cover loans granted to related parties out of own

funds or out of funds borrowed from banks or other third parties.

CYPRUS www.bakertillyklitou.com

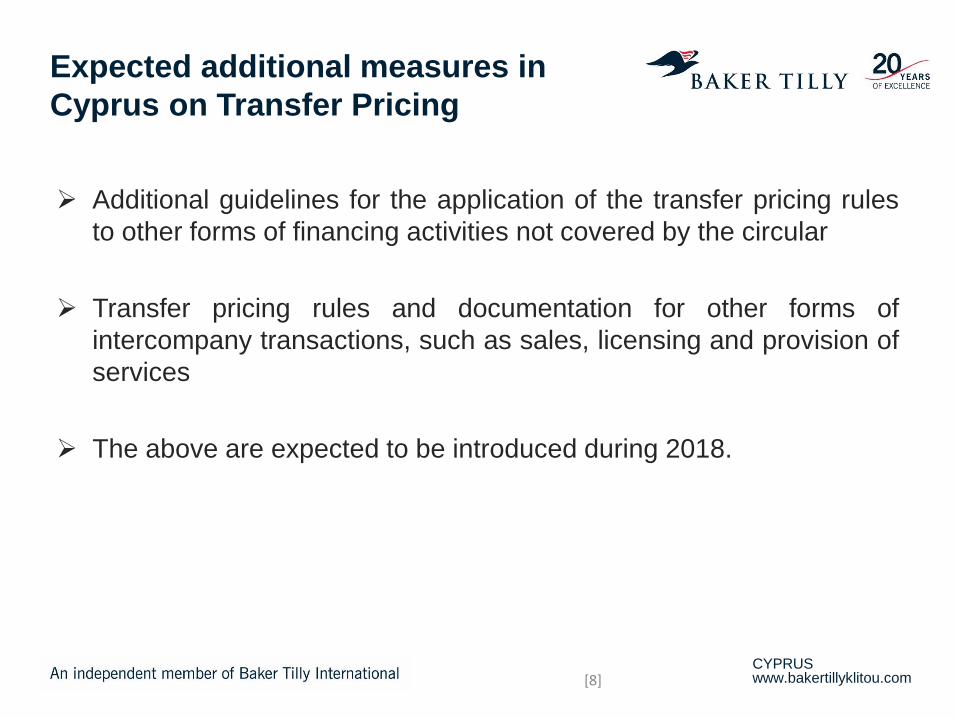

Expected additional measures in

Cyprus on Transfer Pricing

Additional guidelines for the application of the transfer pricing rules

to other forms of financing activities not covered by the circular

Transfer pricing rules and documentation for other forms of

intercompany transactions, such as sales, licensing and provision of

services

The above are expected to be introduced during 2018.

[8]

CYPRUS www.bakertillyklitou.com

What can Baker Tilly do for you on

Transfer Pricing

Providing information about Cypriot, Greek, Bulgarian, and Romanian Transfer Pricing regulations

Preparing / advising on the transfer pricing documentation

Assessing tax risks of transfer prices and performing transfer pricing diagnosis

Advising on appropriate pricing for transactions with associated companies,

Preparing transfer pricing studies for intercompany loans

Negotiation of a group’s transfer pricing policies with national authorities

Assisting on the issuance of Tax Rulings and of Advanced Pricing Arrangements

Guiding on transfer pricing issues on a business restructuring

[9]

CYPRUS www.bakertillyklitou.com

Transfer Pricing under

OECD and EU rules

CYPRUS www.bakertillyklitou.com

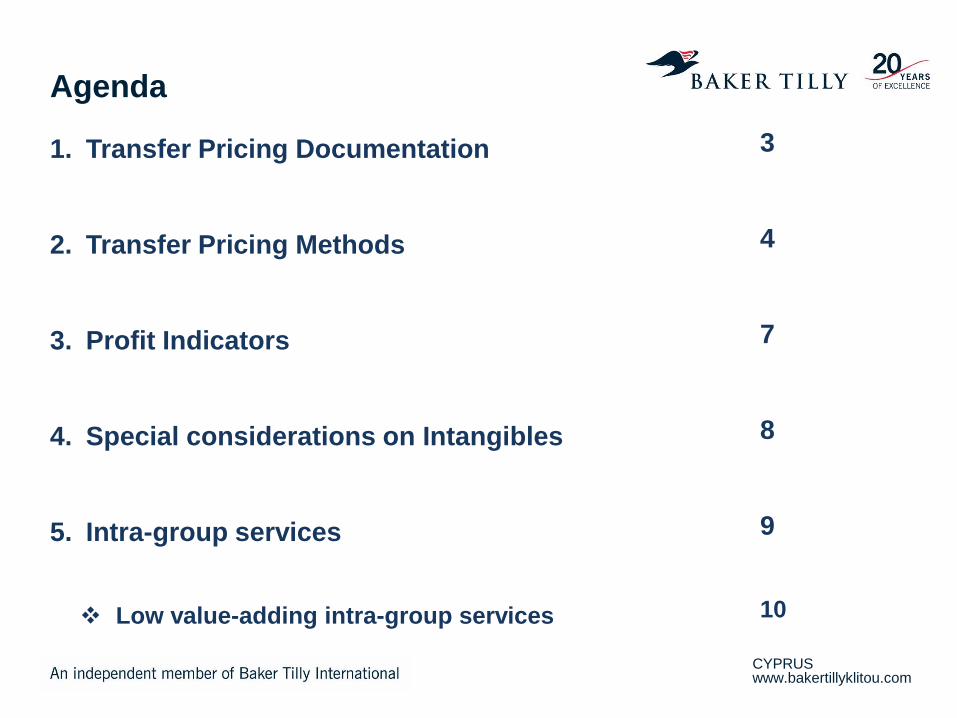

Agenda

1. Transfer Pricing Documentation

2. Transfer Pricing Methods

3. Profit Indicators

4. Special considerations on Intangibles

5. Intra-group services

Low value-adding intra-group services

3

4

7

8

9

10

CYPRUS www.bakertillyklitou.com

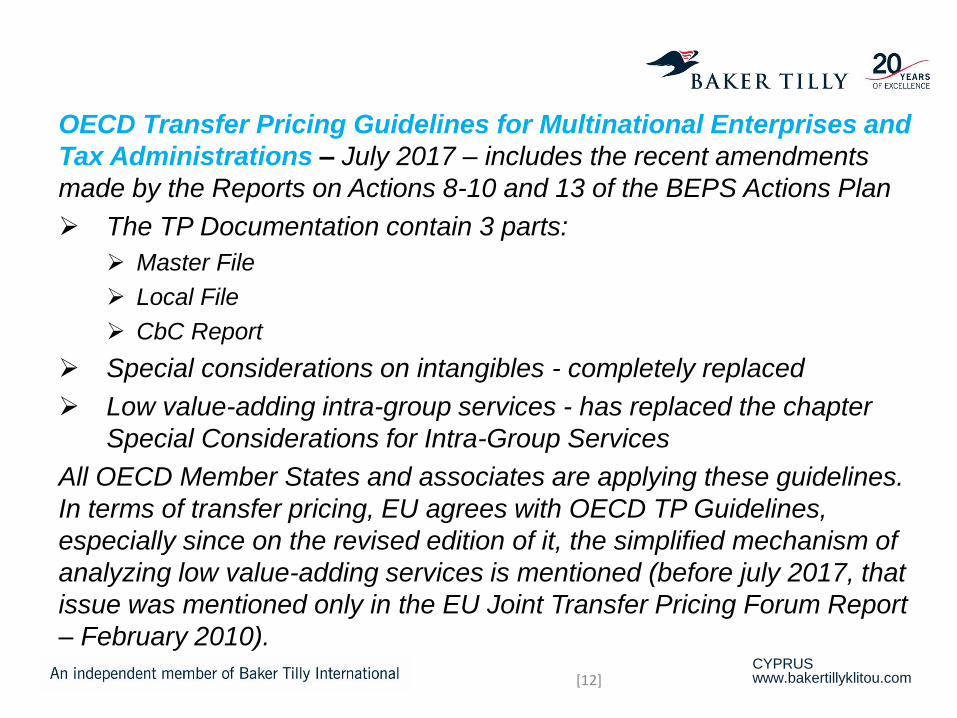

OECD Transfer Pricing Guidelines for Multinational Enterprises and

Tax Administrations – July 2017 – includes the recent amendments

made by the Reports on Actions 8-10 and 13 of the BEPS Actions Plan

The TP Documentation contain 3 parts:

Master File

Local File

CbC Report

Special considerations on intangibles - completely replaced

Low value-adding intra-group services - has replaced the chapter

Special Considerations for Intra-Group Services

All OECD Member States and associates are applying these guidelines.

In terms of transfer pricing, EU agrees with OECD TP Guidelines,

especially since on the revised edition of it, the simplified mechanism of

analyzing low value-adding services is mentioned (before july 2017, that

issue was mentioned only in the EU Joint Transfer Pricing Forum Report

– February 2010).

[12]

CYPRUS www.bakertillyklitou.com

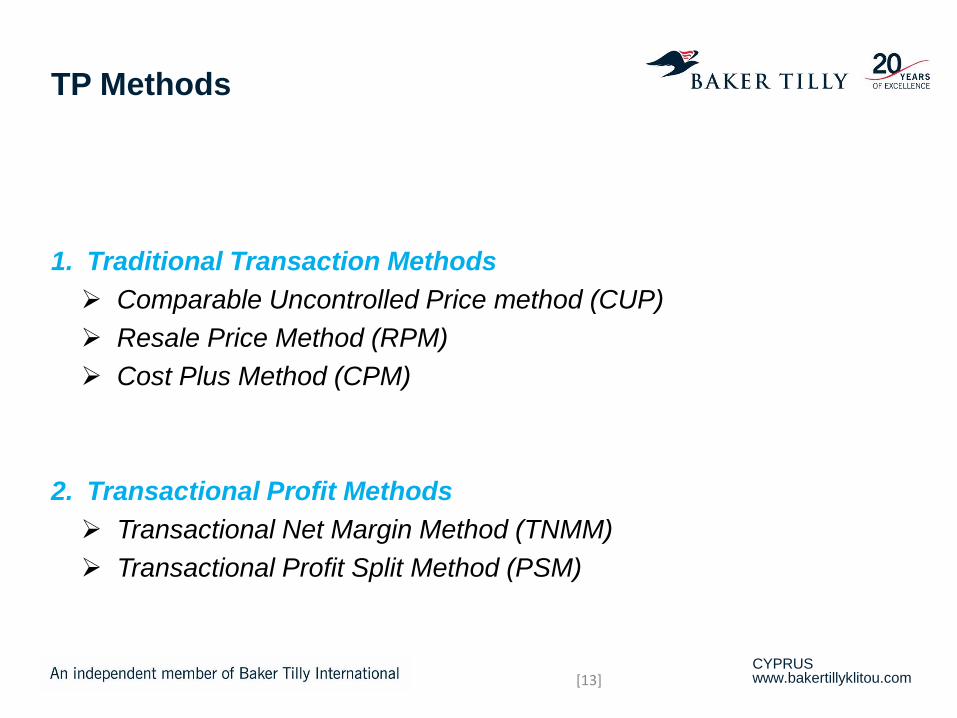

TP Methods

[13]

1. Traditional Transaction Methods

Comparable Uncontrolled Price method (CUP)

Resale Price Method (RPM)

Cost Plus Method (CPM)

2. Transactional Profit Methods

Transactional Net Margin Method (TNMM)

Transactional Profit Split Method (PSM)

CYPRUS www.bakertillyklitou.com

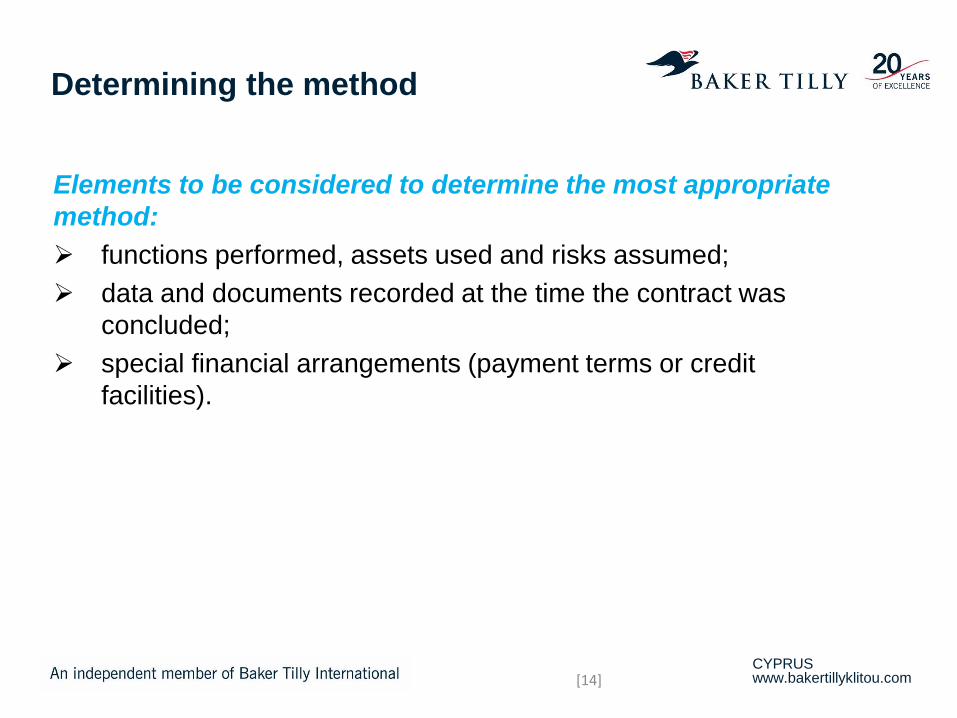

Determining the method

[14]

Elements to be considered to determine the most appropriate

method:

functions performed, assets used and risks assumed;

data and documents recorded at the time the contract was

concluded;

special financial arrangements (payment terms or credit

facilities).

CYPRUS www.bakertillyklitou.com

Determining the method

[15]

Specifically, we should consider:

Transactions with goods and services: Typology of traded goods

/ services, market conditions on which goods / services are

provided, activities carried out and stages in the production and

distribution chain of the entities involved, payment deadlines,

discounts, etc.

Financial transactions: the amount and duration of the loan, the

nature and purpose of the loan, the guarantee involved, the

foreign currency involved, the foreign exchange risks and the

costs of exchange rate insurance measures, as well as other

circumstances of the loan.

CYPRUS www.bakertillyklitou.com

Most used profit indicators

[16]

Return on Sales (ROS) = Net profit / Sales

Used for trade activities. Attention must be paid to discounts and

rebates.

Return on Total Costs (ROTC) = Net profit / Costs (Directly or

indirectly related)

Used when costs are a relevant indicator of functions performed,

assets used and risks assumed by the tested party. Most commonly

used for manufacturers or service providers.

Return on Assets (ROA) = Net profit / Assets (operating ones)

Used in cases where assets are a better indicator of the value added

by the tested party (certain manufacturing or other asset-intensive

activities and in capital-intensive financial activities. The denominator

can also be capital, instead of assets. Operating assets should be

used, but not trade payables. Investments and cash balances are

generally not operating assets outside the financial industry sector.

CYPRUS www.bakertillyklitou.com

Special considerations on

intangibles

[17]

Identifying intangibles

• Intangibles that are important to consider for transfer pricing

purposes are not always recognized as intangible assets for

accounting purposes

Categories of intangibles

• trade and marketing

• soft and hard

• routine and no-routine

• unique and valuable

Examples: patents, know-how and trade secrets, trademarks, trade

names and brands, rights under contracts and government licences,

licences and similar limited rights in intangibles, goodwill and

ongoing concern value, group synergies, market specific

characteristics.

CYPRUS www.bakertillyklitou.com

Intra-group services

[18]

An intra-group service is considered to be provided if the activity

provides the respective member of the group plus commercial and

economic value to obtain a commercial position on the market.

Elements to be considered in the analysis of intra-group services:

The economic motivation of the transaction - the benefit to the

company;

Cost base allocated to the beneficiary;

Profit margin applied to assigned costs.

Would the company have purchased such services from an

independent supplier?

CYPRUS www.bakertillyklitou.com

Low value-adding intra-group

services

[19]

Simplified methodology of analysis is applicable: costs + 5%, without

having to conduct a benchmark.

Conditions to be met:

are of a supporting nature

are not part of the core business of the MNE group

do not require the use of unique and valuable intangibles

do not involve the assumption or control of substantial and

significant risks by the provider

CYPRUS www.bakertillyklitou.com

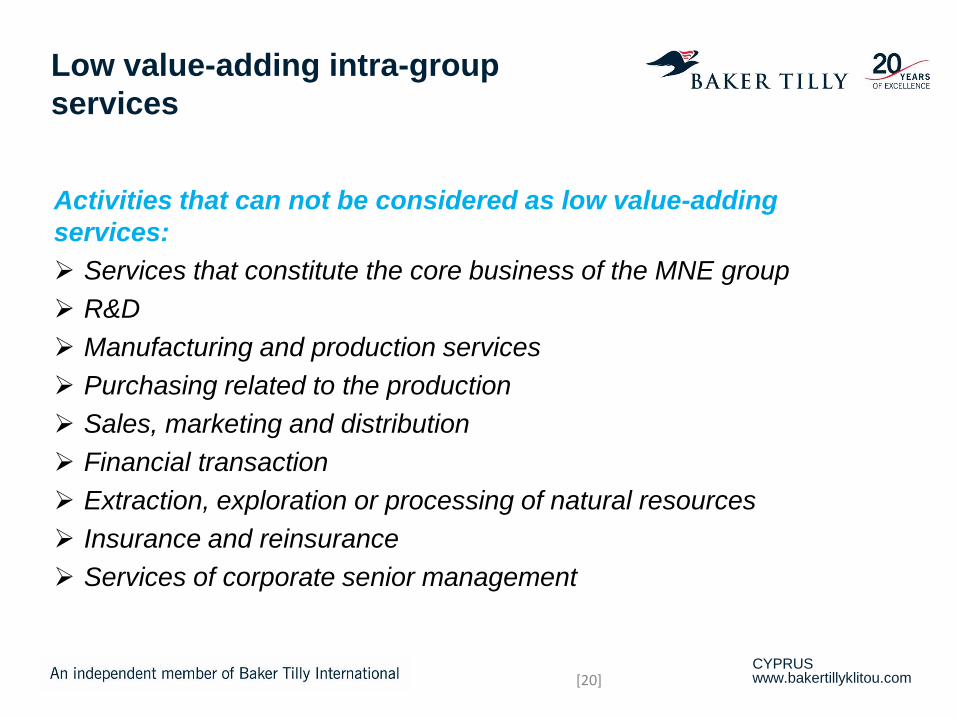

Low value-adding intra-group

services

[20]

Activities that can not be considered as low value-adding

services:

Services that constitute the core business of the MNE group

R&D

Manufacturing and production services

Purchasing related to the production

Sales, marketing and distribution

Financial transaction

Extraction, exploration or processing of natural resources

Insurance and reinsurance

Services of corporate senior management

CYPRUS www.bakertillyklitou.com

Transfer Pricing and

Back – to Back Financing

Arrangements

CYPRUS www.bakertillyklitou.com

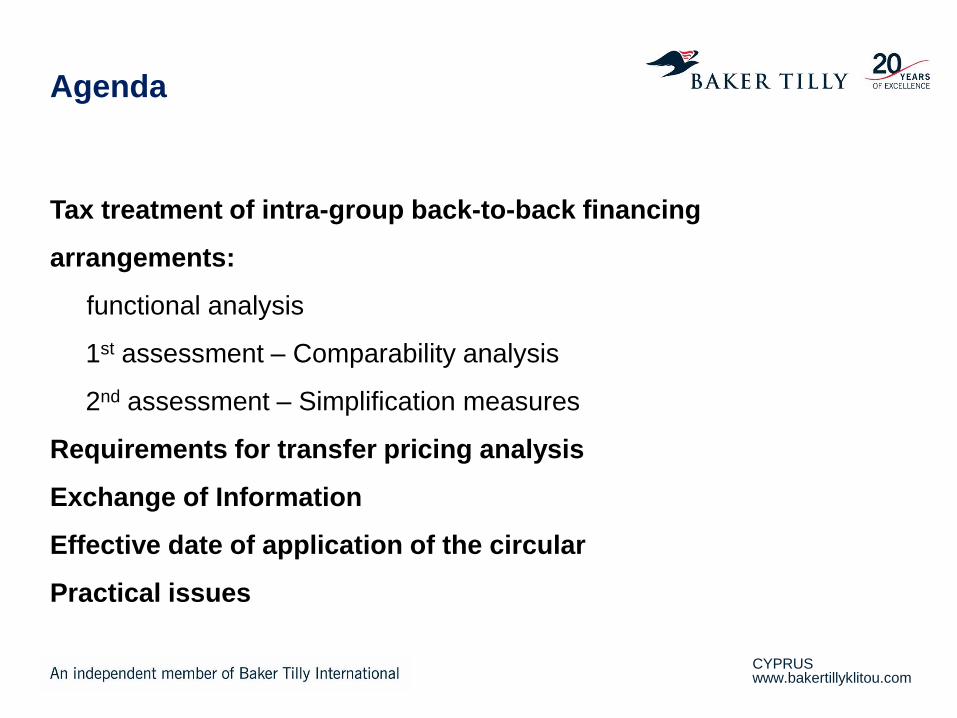

Agenda

Tax treatment of intra-group back-to-back financing

arrangements:

functional analysis

1st assessment – Comparability analysis

2nd assessment – Simplification measures

Requirements for transfer pricing analysis

Exchange of Information

Effective date of application of the circular

Practical issues

CYPRUS www.bakertillyklitou.com

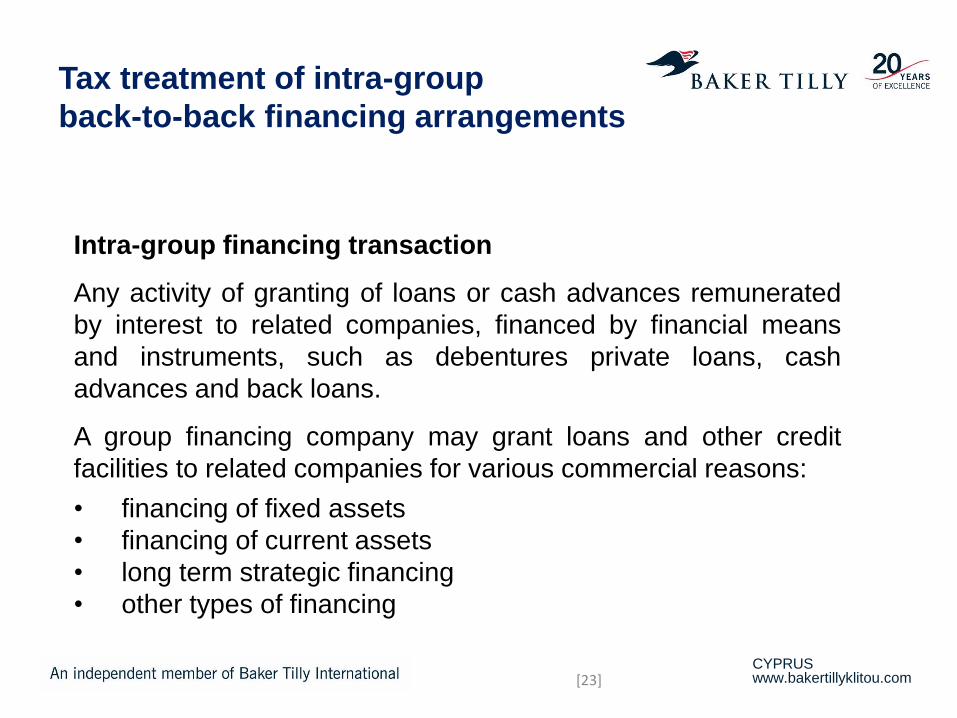

Tax treatment of intra-group

back-to-back financing arrangements

[23]

Intra-group financing transaction

Any activity of granting of loans or cash advances remunerated

by interest to related companies, financed by financial means

and instruments, such as debentures private loans, cash

advances and back loans.

A group financing company may grant loans and other credit

facilities to related companies for various commercial reasons:

• financing of fixed assets

• financing of current assets

• long term strategic financing

• other types of financing

CYPRUS www.bakertillyklitou.com

Functional analysis (I)

[24]

An analysis of the functions performed (taking into account

assets used and risks assumed) by associated enterprises in

controlled transactions and by independent enterprises in

comparable uncontrolled transactions.

The functions carried out (taking into account the assets used

and the risks assumed) will determine to some extent the

allocation of risks between the parties, and therefore the

conditions each party would expect in arm’s length transactions.

The functions analyzed include decision-making, in particular in

terms of corporate strategy and risks => it is necessary to

determine the legal rights and obligations of each party when

performing said functions.

CYPRUS www.bakertillyklitou.com

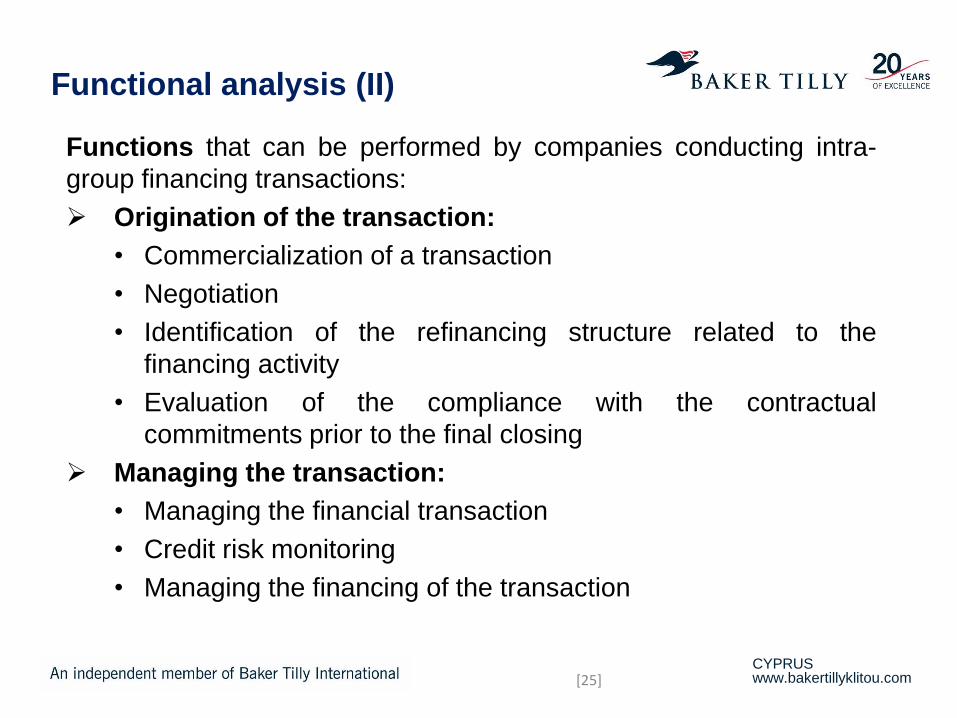

Functional analysis (II)

[25]

Functions that can be performed by companies conducting intra-

group financing transactions:

Origination of the transaction:

• Commercialization of a transaction

• Negotiation

• Identification of the refinancing structure related to the

financing activity

• Evaluation of the compliance with the contractual

commitments prior to the final closing

Managing the transaction:

• Managing the financial transaction

• Credit risk monitoring

• Managing the financing of the transaction

CYPRUS www.bakertillyklitou.com

Functional analysis (III)

[26]

Risks

In order to assess the borrower-related risk, financial

establishments verify whether guarantees exist, they analyze the

purpose and duration of credit, as well as any other important

factors. On the open market, higher risk generally induces higher

remuneration.

A group financing company assume the risk if it has access to

funding necessary in order to take on or avoid the risk, to pay for

the risk mitigation actions, and to bear its consequences if the

risk occurs.

CYPRUS www.bakertillyklitou.com

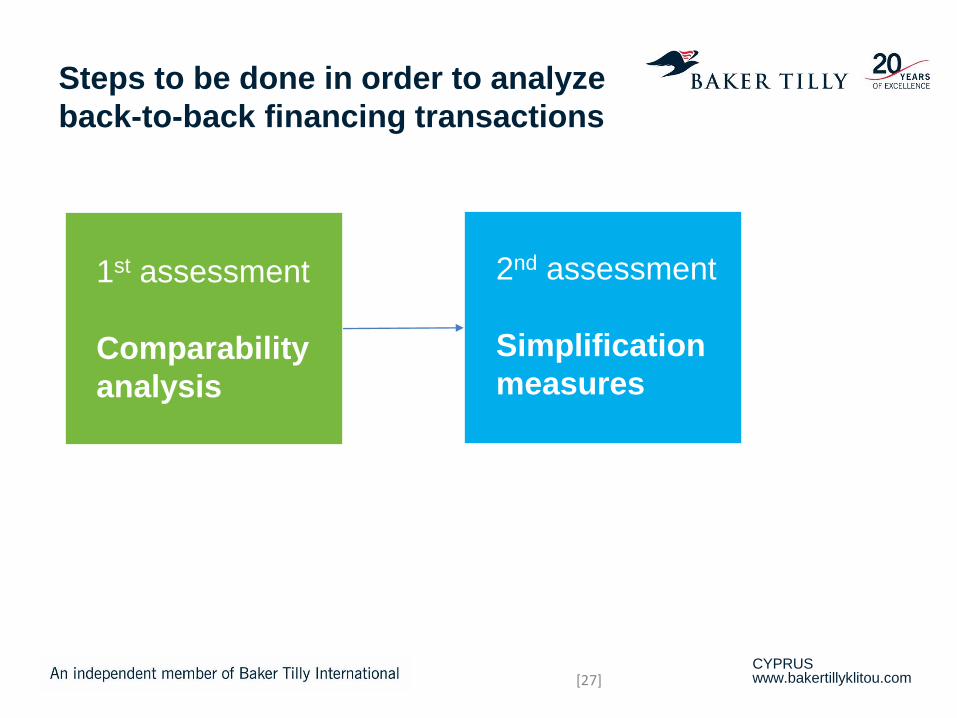

Steps to be done in order to analyze

back-to-back financing transactions

[27]

1st assessment

Comparability

analysis

2nd assessment

Simplification

measures

CYPRUS www.bakertillyklitou.com

1st assessment:

Comparability analysis

[28]

An appropriate comparability analysis must be carried out in order to

determine whether transactions between related entities are

comparable to transactions between independent entities.

The comparability analysis should consist of two main parts:

a. identification of commercial or financial relationship between

related entities and determination of the conditions and

economically relevant circumstances attaching to those relations;

b. comparison of the as accurately delineated conditions and

economically relevant circumstances of the controlled transaction

with those of comparable transactions between independent entities (determination of arm’s length remuneration).

CYPRUS www.bakertillyklitou.com

Identification of transactions,

conditions and circumstances (I)

[29]

For the comparability analysis it is not relevant whether or not

the transaction is formalized in writing. The actual conduct of the

parties must be taken into account while delineating the

transaction.

In order to accurately delineate a controlled financing

transaction, it is necessary to determine its characteristics, such

as its terms and functions, the assets used and the risks

assumed by the related entities.

CYPRUS www.bakertillyklitou.com

Identification of transactions,

conditions and circumstances (II)

[30]

The extent to which the comparability factors are economically

significant for a particular transaction depends on the extent to

which it would be taken into consideration by independent

entities assessing the terms of the same transaction.

There are some transactions that cannot be observed in the

open market, or are devoid of any commercial rationale, in a way

that independent parties would not have agreed to conclude

these transactions under the same conditions. Such

transactions, together with the associated tax consequences

must be disregarded to ensure full compliance with the arm’s

length principle.

CYPRUS www.bakertillyklitou.com

Determination of arm’s

length remuneration

[31]

The arm’s length remuneration is the remuneration that would

have been agreed under comparable conditions on the open

market.

The process of identification of potential comparable

transactions must be transparent, systematic and verifiable.

The search should be conducted using all sources of information

available at the time of the undertaking of the transaction.

Comparability adjustments may be performed based on

internationally recognized standards in this field, if it appears

necessary for improving the reliability and quality of the

comparability analysis.

For intra-group financing companies with a functional

profile similar to that of a regulated financial undertaking,

an after-tax return on equity equal to 10% is considered at

arm’s length.

CYPRUS www.bakertillyklitou.com

2nd assessment:

Simplification measures (I)

[32]

The transactions carried out by a Cypriot tax resident group

financing company, which pursues a purely intermediary activity, (i.e.

it grants loans or advances to related companies, which are

refinanced by loans or advances obtained from related companies),

are deemed to comply with the arm’s length principle, if the company

receives in relation to its controlled transactions under analysis, a

minimum after tax return 2% on the assets (i.e. 2.3% on assets).

CYPRUS www.bakertillyklitou.com

2nd assessment:

Simplification measures (II)

[33]

The company must prove that it acts as a purely intermediary

company i.e. performing reduced functions, assets deployed for

that purpose are very few and the risks associated with the

transactions analyzed are low.

The transfer pricing study should initially include only a

functional analysis.

If the functions do not prove that the assumed risks are reduced,

then a full economic transfer pricing analysis is required.

CYPRUS www.bakertillyklitou.com

2nd assessment:

Simplification measures(III)

[34]

The simplification procedures can only be used by a group financing

company which meets the criteria for substance - it is imperative that

the company must have an actual presence in Cyprus.

Criteria to be observed:

• The number of board of Directors members of the company that are

Cyprus tax residents;

• The number of board of Directors meetings held in Cyprus and the

main management and commercial decisions taken in Cyprus;

• The number of shareholders’ meetings taking place in Cyprus.

The group financing company must have the qualified personnel to

control the transactions performed.

(The company may subcontract functions that do not have a

significant impact on risk control).

CYPRUS www.bakertillyklitou.com

2nd assessment:

Simplification measures (IV)

[35]

The minimum percentage of 2% on assets cannot be used

without a transfer pricing analysis in order to determine arm’s

length remuneration for intra-group financing transactions which

are different from those transactions covered by the relevant

circular.

If the minimum substance criteria are not met, it should be

expected that the minimum margin acceptable under the transfer

pricing study would be higher than the 2%.

However a transfer pricing study for companies which meet all

the requirements on substance, credit risk assessment and other

considerations may result in an acceptable margin below 2%.

CYPRUS www.bakertillyklitou.com

Requirements for transfer pricing

analysis (I)

[36]

Minimum requirements:

description of the computation of equity allocation required to

assume the risks;

description of the group and the inter-linkages between the

functions performed by the entities participating in the controlled

transactions and the rest of the group, together with a

description of the value creation in the broad sense;

the precise scope of the transactions analyzed;

a complete list of the searched potentially comparable

transactions;

CYPRUS www.bakertillyklitou.com

Requirements for transfer pricing

analysis (II)

[37]

Minimum requirements (contd.):

a rejection matrix (with the rejection reasons/justifications);

the final list of comparable transactions accurately delineated;

a general description of market conditions;

a list of all previous agreements on TP concluded with other

countries in relation to the transactions analyzed;

a list of all previous agreements concluded with the entities

under analysis which are still in effect at the time of the

submission of the request;

a projection of the income statements for the years covered by

the request.

CYPRUS www.bakertillyklitou.com

Preparation of TP Analysis

[38]

The TP Analysis should be prepared by a Transfer Pricing

Expert. The TP Analysis must be submitted to the Cypriot Tax

Department by a person who has a license to act as an auditor

of a company according to the Cyprus Company Law and is

required to carry an assurance control confirming the quality of

the Transfer Pricing Analysis.

The TP Analysis will only be submitted to the tax authorities only

upon request or in the case of applying for an advance tax

ruling.

The tax return filed by the company (Form IR4) is expected to be

amended in order to indicate whether:

(a) the simplification procedure has been applied

(b) a transfer pricing study exists

CYPRUS www.bakertillyklitou.com

Exchange of Information

The issue of tax rulings for the conclusion of Advanced Pricing

Arrangements, as well as the use of the simplification measures,

(whether applied upon the issue of a tax ruling or not), are subject to

the exchange of information rules under the applicable procedures

(within EU member states).

[39]

CYPRUS www.bakertillyklitou.com

Effective date of application of the

circular

The Circular applies with effect from 1 July 2017, for all

existing and future transactions, irrespective of the date of

entering into the relevant transactions and irrespective of any

tax rulings issued prior to the said date.

Any tax rulings issued on transactions within the scope of this

circular, which were issued prior the 1 July, 2017 will no

longer be valid for tax periods after 1 July 2017.

If the intra group financing transactions effected prior to 1 July

2017 are still ongoing post 1 July 2017 and they were

supported by a transfer pricing study, this transfer pricing

study must comply with the provisions of this circular.

[40]

CYPRUS www.bakertillyklitou.com

Practical issues

It is not necessary to amend legally existing loan agreements in

order to amend the interest rates. An adjustment to the tax

computations to include the additional interest necessary for the

acceptable margin would be sufficient.

If no transfer pricing study is prepared, the simplification procedures

cannot be applied and the company adopts an arbitrary interest rate

margin on back to back intercompany loans, then the Cypriot tax

authorities have the right to impute additional income when they

examine the company’s tax returns by adopting a different interest

rate and thus levy additional taxes and penalties.

[41]

CYPRUS www.bakertillyklitou.com

Other current tax developments

in Cyprus and internationally

CYPRUS www.bakertillyklitou.com

Issues to be covered

Country by Country Reporting

New tax residency rules for individuals

Payment of overdue taxes

Substance requirements in the context of exchange of

information

Beneficial ownership of income with particular emphasis on

Russia

CYPRUS www.bakertillyklitou.com

Country by Country Reporting

CbC Reporting requires large multinational enterprises (“MNE”) to file a CbC Report that will provide a breakdown of the amount of revenue, profits, taxes and other indicators of economic activities for each tax jurisdiction in which the MNE group does business. CbC Reporting only applies to MNE groups with annual consolidated group revenue of €750 million or more in the preceding fiscal year (“MNE Groups”).

CbC Reporting requirements apply in Cyprus for fiscal years beginning on or after 1 January 2016.

The following constituent entities will be required to file CbC Reports in Cyprus with respect to fiscal years beginning on or after 1 January 2016:

(i) a Cyprus tax resident ultimate parent entity of an MNE Group;

(ii) a Cyprus tax resident surrogate parent entity of an MNE Group (a surrogate parent entity can only be appointed in specific circumstances).

[44]

CYPRUS www.bakertillyklitou.com

CbC notification requirement

An annual notification to be made to the Tax Department by the last day of the fiscal year to which the CbC report relates to, as follows:

For ultimate parent entities resident in Cyprus, the entities must electronically notify the Tax Department confirming that they are the CbC reporting entity of the Group.

For surrogate parent entities resident in Cyprus, the entities must electronically notify the Tax Department confirming that they are the CbC reporting entity for the Group and also provide the identity and tax residence of the Group’s ultimate parent entity.

For domestic constituent entities resident in Cyprus, the entities must electronically notify the Tax Department confirming the identity and tax residence of the CbC reporting entity of the Group and also provide the identity and tax residence of the Group’s ultimate parent entities (if different from the reporting entity).

For 2016, the deadline for first notification has been extended to 20 October 2017.

[45]

CYPRUS www.bakertillyklitou.com

What information should a CbC

Report contain?

A CbC report for an MNE Group must contain the following information on an aggregate basis in respect of each jurisdiction in which the MNE Group operates:

amount of unrelated party revenue, related party revenue and total revenue;

amount of profit or loss before income tax;

amount of income tax paid;

amount of income tax accrued;

amount of stated capital,

amount of accumulated earnings,

number of employees, and

value of tangible assets other than cash or cash equivalents

[46]

CYPRUS www.bakertillyklitou.com

New rules on tax residency for

individuals (I)

The Cyprus Income Tax Law has been amended so that an individual,

who does not remain in any other state for one or more periods which

altogether exceed 183 days in the same tax year and who is not tax

resident in any other state for the same tax year, be considered to

be a tax resident of Cyprus, provided that the following conditions are

cumulatively met:

he should remain in Cyprus for at least 60 days during the tax year

he should pursue any business in Cyprus and / or to work in Cyprus

and / or to be a director in a company resident in Cyprus at any time

during the tax year

he should maintain a permanent residence in Cyprus, which can be

either owned or rented by him

[47]

CYPRUS www.bakertillyklitou.com

New rules on tax residency for

individuals (II)

An individual who cumulatively fulfils the above conditions is not considered as tax resident of Cyprus in the tax year, if in that year the exercise of any business and / or employment in Cyprus and / or the holding of a post to a taxable person of Cyprus have ceased.

For the purposes of calculating the days of stay in Cyprus:

(a) the day of departure from Cyprus is considered as a day outside Cyprus

(b) the day of arrival in Cyprus is considered as a day in Cyprus

(c) arrival in Cyprus and departure from Cyprus within the same day is counted as one day in Cyprus

(d) departure from Cyprus and return to Cyprus within the same day is counted as one day outside Cyprus.

[48]

CYPRUS www.bakertillyklitou.com

New rules on tax residency for

individuals (III)

It is noted that for employment purposes in Cyprus with earnings in

excess of Euro 100,000, an individual is allowed for an exemption

from tax of 50% of the salary for a period of 10 years, which

significantly reduces his income tax liability.

At the same time, an individual is granted exemption from income

tax or defense tax on dividends and interest received either in

Cyprus or abroad, provided that such individual is considered as

non - dom in Cyprus.

[49]

CYPRUS www.bakertillyklitou.com

Settlement of overdue taxes (I)

The law on the procedure for settling tax arrears, which covers the following taxes:

Income tax

Special contribution for the defense

Immovable property tax

Capital gains tax

Inheritance tax

Special contribution for employed, retired and self-employed in the private sector

Special contribution for refugees

Stamp duties

Value Added Tax

[50]

CYPRUS www.bakertillyklitou.com

Settlement of overdue taxes (II)

This regulation relates to the following tax liabilities:

All taxes in arrears up to and including 31 December 2015 which at the date of the application have been assessed by the Tax Department of Taxation and appear as payable, irrespective of the manner in which they are repaid either by agreement with the Tax Department or pursuant court order .

Amounts which become payable as a result of the submission of a self-assessment in respect of tax years up to 31 December 2015 where the tax returns for the relevant tax year have already been submitted by 3 July 2017, but without payment of the tax due.

Tax liabilities which are assessed after 3 July 2017 by the Tax Commissioner relating to tax years until 31 December 2015. In such a case, an application for regulation shall be made within three months from the date on which the tax becomes payable, on the basis of the tax assessment which has been issued.

[51]

CYPRUS www.bakertillyklitou.com

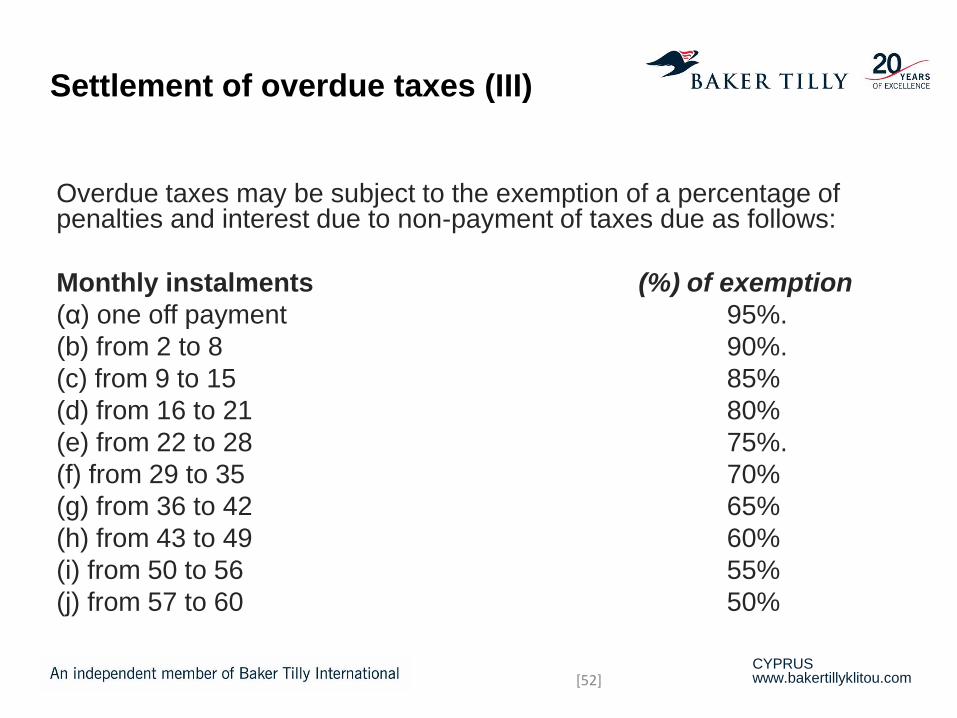

Settlement of overdue taxes (III)

Overdue taxes may be subject to the exemption of a percentage of penalties and interest due to non-payment of taxes due as follows:

Monthly instalments (%) of exemption

(α) one off payment 95%.

(b) from 2 to 8 90%.

(c) from 9 to 15 85%

(d) from 16 to 21 80%

(e) from 22 to 28 75%.

(f) from 29 to 35 70%

(g) from 36 to 42 65%

(h) from 43 to 49 60%

(i) from 50 to 56 55%

(j) from 57 to 60 50%

[52]

CYPRUS www.bakertillyklitou.com

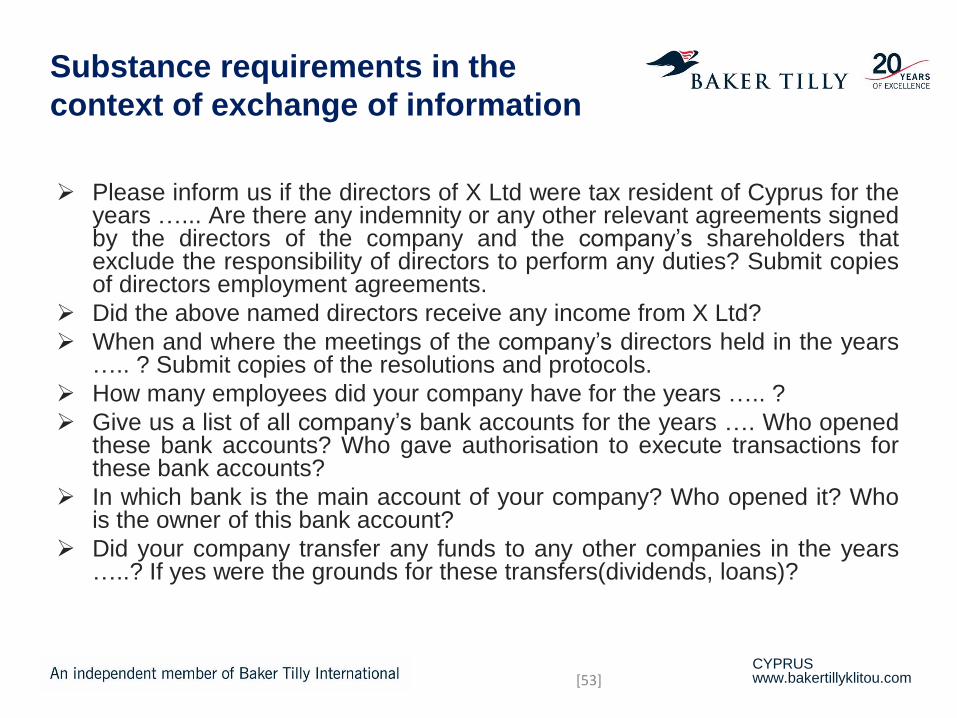

Substance requirements in the

context of exchange of information

Please inform us if the directors of X Ltd were tax resident of Cyprus for the years …... Are there any indemnity or any other relevant agreements signed by the directors of the company and the company’s shareholders that exclude the responsibility of directors to perform any duties? Submit copies of directors employment agreements.

Did the above named directors receive any income from X Ltd?

When and where the meetings of the company’s directors held in the years ….. ? Submit copies of the resolutions and protocols.

How many employees did your company have for the years ….. ?

Give us a list of all company’s bank accounts for the years …. Who opened these bank accounts? Who gave authorisation to execute transactions for these bank accounts?

In which bank is the main account of your company? Who opened it? Who is the owner of this bank account?

Did your company transfer any funds to any other companies in the years …..? If yes were the grounds for these transfers(dividends, loans)?

[53]

CYPRUS www.bakertillyklitou.com

Beneficial ownership of income with

particular emphasis on Russia

Decision No. 15АП-17143/2016 of 13 March 2017 issued by the 15th Appellate Arbitrazh Court1

This involves a Cypriot company (“CYCO”) that is the sole shareholder of a Russian tax resident entity. CYCO satisfied all formal requirements confirming that it acts as a tax resident of Cyprus, as well as met the minimum capital contribution required to apply the reduced tax rate in the dividends article of the Russia-Cyprus DTT. However, the court stated that these criteria were insufficient for applying the reduced tax rate, because CYCO was not a beneficial owner of the income.

In this case, the Russian refinery did not actually transfer the dividends to the Cypriot company, but remitted them to the company’s Russian branch. The cash was then converted to foreign currency and moved out of Russia to a third-party foreign company resident in an offshore jurisdiction (the Isle of Man) that has no DTT with Russia.

The court dismissed the tax authorities’ position that the Russia-Cyprus DTT does not apply in this case, because the income was paid not to the Cypriot company but to its PE, as there were no evidence that the dividends were paid to the branch directly in connection to its Russian business operations.

[54]

CYPRUS www.bakertillyklitou.com

Beneficial ownership of income with

particular emphasis on Russia

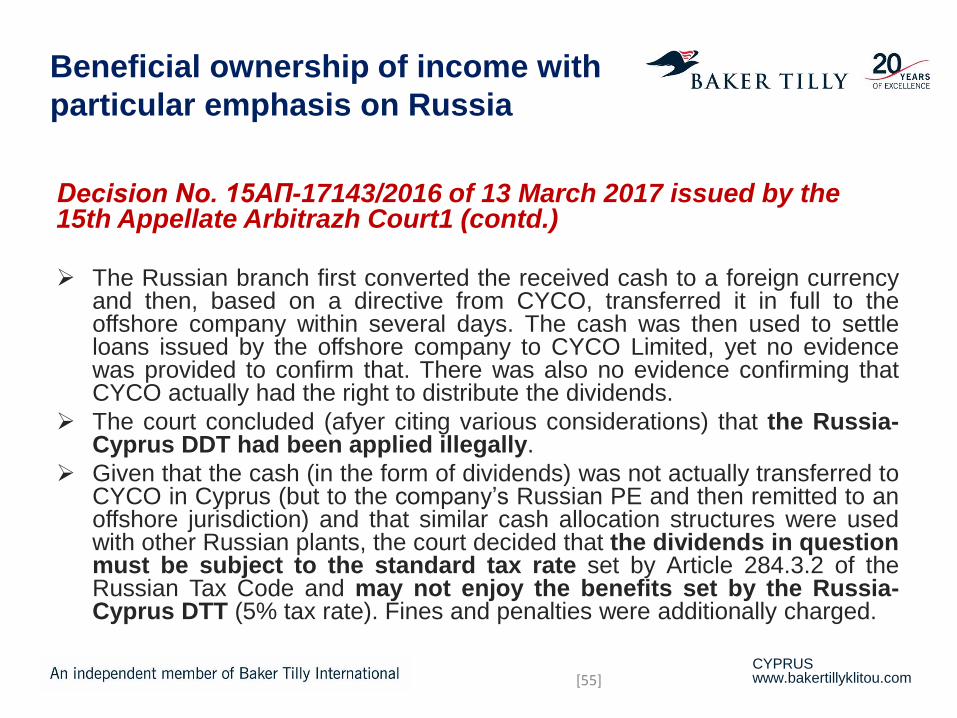

Decision No. 15АП-17143/2016 of 13 March 2017 issued by the 15th Appellate Arbitrazh Court1 (contd.)

The Russian branch first converted the received cash to a foreign currency and then, based on a directive from CYCO, transferred it in full to the offshore company within several days. The cash was then used to settle loans issued by the offshore company to CYCO Limited, yet no evidence was provided to confirm that. There was also no evidence confirming that CYCO actually had the right to distribute the dividends.

The court concluded (afyer citing various considerations) that the Russia-Cyprus DDT had been applied illegally.

Given that the cash (in the form of dividends) was not actually transferred to CYCO in Cyprus (but to the company’s Russian PE and then remitted to an offshore jurisdiction) and that similar cash allocation structures were used with other Russian plants, the court decided that the dividends in question must be subject to the standard tax rate set by Article 284.3.2 of the Russian Tax Code and may not enjoy the benefits set by the Russia-Cyprus DTT (5% tax rate). Fines and penalties were additionally charged.

[55]

CYPRUS www.bakertillyklitou.com

Applying the concept of the beneficial

ownership: Russian Federal Tax

Service (“FTS”) explanations (I)

In a recent letter the FTS explained its approach to interpreting the

concept of the beneficial ownership of income in applying DTT

provisions.

The position taken by the FTS is in line with how court practice is

currently shaping up.

The letter addressed four issues:

[56]

CYPRUS www.bakertillyklitou.com

Applying the concept of the beneficial

ownership: Russian Federal Tax

Service (“FTS”) explanations (II)

(1) Can OECD documents be used as a guideline for interpreting DTT provisions?

The Russian FTS notes that the courts may refer to the official Commentary on the OECD Model Tax Convention on Income and on Capital when making judgements (citing certain references). Notably, the Russian Ministry of Finance also refers to OECD commentary for guidance on interpreting DTT provisions.

The Russian FTS notes that both primary sources and secondary sources may be used when interpreting DTT provisions. The commentaries to the Model Convention constitute a secondary source in this context. They can be used in the absence of a bilateral agreement between countries on a particular issue, or in the absence of clauses that state the express position of a country toward a certain provision.

[57]

CYPRUS www.bakertillyklitou.com

Applying the concept of the beneficial

ownership: Russian Federal Tax

Service (“FTS”) explanations (III)

(2) Does the beneficial ownership concept apply ONLY to interest, dividends and royalties?

The Russian FTS states that the articles on dividends, interest, and royalties in DTTs use the concept of the beneficial ownership. At the same time, the FTS accepts that the concept can be applied to “various types of income paid by foreign entities”.

The Russian FTS also referred to court decisions confirming this approach by indicating a recent case involving another Cypriot tax resident company, where the concept was applied to the disposal of shares in a Russian company.

[58]

CYPRUS www.bakertillyklitou.com

Applying the concept of the beneficial

ownership: Russian Federal Tax

Service (“FTS”) explanations (IV)

(3) What are the criteria for determining whether a party is the beneficial owner of income? Russian tax law does not contain any specific beneficial owner test. Instead, the general provisions of the Russian Tax Code and DTTs on this matter have been explained by way of Ministry of Finance letter.

Companies that receive income must:

Have an economic presence in their country of residence;

Have wide authority to dispose of the income;

Use the income in their business activities;

Take independent decisions through their officials;

Show signs of performing business operations (office, hired staff, general business expenses);

Receive economic benefit from the income;

Bear individual risks pertaining to assets;

Have no legal or actual obligations to transfer the income to third parties (specifically parties not entitled to DTT benefits).

[59]

CYPRUS www.bakertillyklitou.com

Applying the concept of the beneficial

ownership: Russian Federal Tax

Service (“FTS”) explanations (V)

(4) Is it necessary to identify the beneficial owner in order to deny the first recipient right to apply tax treaty benefits?

The Russian FTS announced that the tax authorities do not have to identify the beneficial owner of income. The application of benefits can be denied on the grounds that the first recipient is not the beneficial owner of income. In such cases, regular Russian tax rates shall apply.

In fact, the non-recognition of a party as beneficial owner is a separate tool for preventing the abuse of DTTs.

As it follows from the letter, the tax authorities must take account of documents that confirm a party’s actual right to the income in the course of a tax audit, if the confirmation had been provided before the ultimate resolution regarding the audit was issued.

[60]

CYPRUS www.bakertillyklitou.com

This presentation has been prepared for general guidance on matters of interest only, and does not constitute professional advice. Do not act upon the

information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as

to the accuracy or completeness of the information contained in this publication. Τo the extent permitted by law, Baker Tilly Klitou and Partners Ltd, its

members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of anyone acting, or

refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2016 Baker Tilly Klitou and Partners Ltd. All rights reserved. In this document, “Baker Tilly” or “Baker Tilly Klitou” refers to Baker Tilly Klitou and

Partners Ltd, registered in Cyprus, which is an independent member of Baker Tilly International, a worldwide network of accounting firms. “Baker Tilly”

is a trademark of Baker Tilly UK Group LLP, used under license.

Contact us

NEOFYTOS NEOFYTOU

Head of Tax

South East Europe

Baker Tilly Klitou

Tel. +357 22 458 500, Fax. +357 22 751 648

Email: [email protected]

CYPRUS www.bakertillyklitou.com

[62]