Embed Size (px)

Citation preview

A collection of transfer pricing summaries of countries in the

Asia Pacific region

Transfer Pricing | 2015

2 | Transfer Pricing 2015 - AGN Asia Pacific Region

“This publication has been prepared for the purpose of quick information dissemination. Its contents should not be used as a basis for advice or formulating decisions under any circumstances.”

Agn International - Europe Limited

Transfer Pricing | 2015 The AGN Asia Pacific conducts Transfer Pricing Surveys of the following countries:

Index

Australia 3

Hong Kong 5

Japan 7

Korea 9

Malaysia 11

New Zealand 13

Pakistan 15

Singapore 17

Thailand 19

3 | Transfer Pricing 2015 - AGN Asia Pacific Region

AUSTRALIA 2015 TRANSfeR PRIcING

1.TP legislation/guidelines

Australia’s TP legislation is detailed in Division 815 Income Tax Assessment Act 1997: Cross-border transfer pricing. The Commissioner of Taxation (“Commissioner”) has issued various rulings outlining the policy and practical operation of Australia’s TP legislation, specifically TR 97/20 Income tax: arm’s length transfer pricing methodologies for international dealings and TR 98/11 Income tax: documentation and practical issues associated with setting and reviewing transfer pricing in international dealings.

Generally the Commissioner seeks to apply the Australian legislation in accordance with OECD TP principles and recent amendments to Australia’s transfer pricing rules seek to further align Australia’s domestic regime with OECD practices.

Those amendments have introduced significant changes, including:

(a) Expressly allowing the use of specified OECD guidelines in the legislation and regulations to interpret if an entity obtains a transfer pricing benefit;

(b) Introducing a self-executing regime (Commissioner no longer required to make a determination before a tax shortfall arises);

(c) The Commissioner has reconstruction power to look at economic substances and construct a hypothetical transaction; and

(d) Without contemporaneous TP documentation with support for pricing methodology used, taxpayers are subject to minimum penalties of 25% on any shortfall arising from a transfer pricing benefit.

2.TP documentation required to be filed with tax return

While no TP documentation is required to be filed with the income tax return, disclosure is required as part of the income tax return setting out a taxpayer’s dealings with international related parties and pricing methodology applied to such dealings where they exceed $2M per year (including balance of loans).

Taxpayers should therefore maintain contemporaneous documentation supporting the basis for the arm’s length price adopted. Documentary requirements for compliance purposes would vary depending on the nature of the international transactions carried out by the taxpayer and the size of the taxpayer, with larger taxpayers requiring more detailed and robust TP documentation.

3. TP audits done by tax authority

The Australian Taxation Office (ATO) regularly conducts compliance activities at all levels in this area and although it has been largely unsuccessful to date, will pursue TP matters to court as required.

4 | Transfer Pricing 2015 - AGN Asia Pacific Region

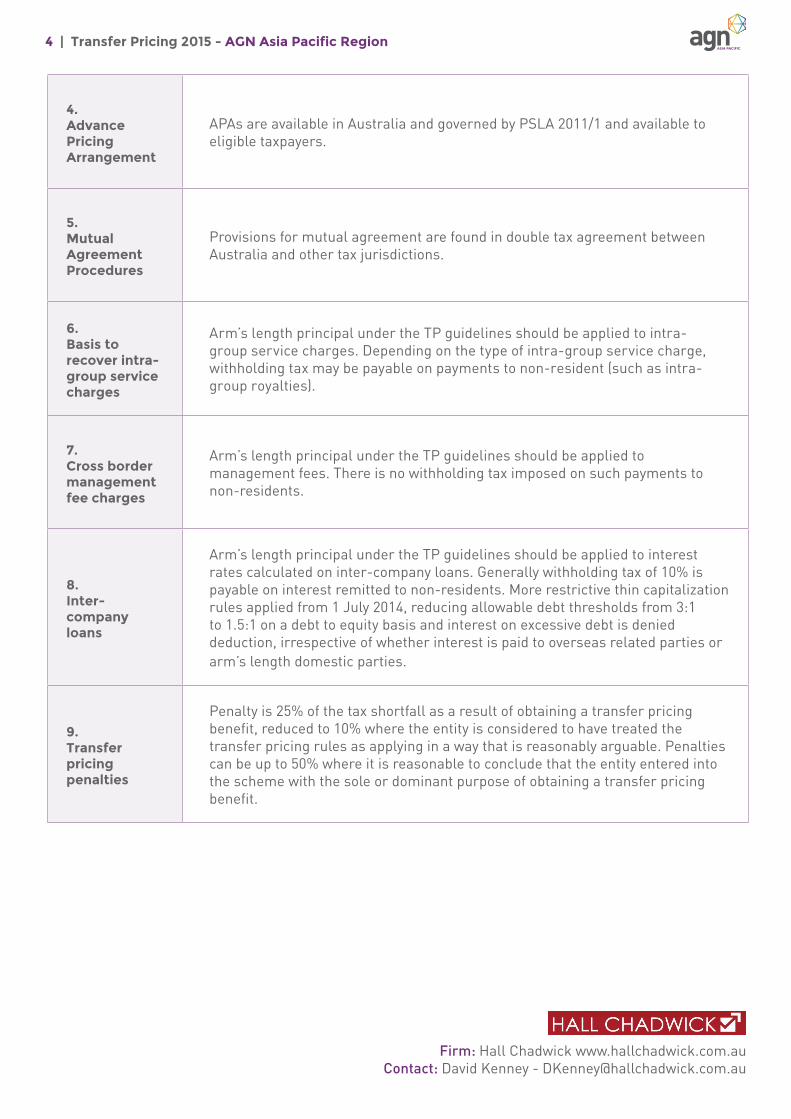

4.Advance Pricing Arrangement

APAs are available in Australia and governed by PSLA 2011/1 and available to eligible taxpayers.

5.Mutual Agreement Procedures

Provisions for mutual agreement are found in double tax agreement between Australia and other tax jurisdictions.

6.Basis to recover intra-group service charges

Arm’s length principal under the TP guidelines should be applied to intra-group service charges. Depending on the type of intra-group service charge, withholding tax may be payable on payments to non-resident (such as intra-group royalties).

7.cross border management fee charges

Arm’s length principal under the TP guidelines should be applied to management fees. There is no withholding tax imposed on such payments to non-residents.

8.Inter-company loans

Arm’s length principal under the TP guidelines should be applied to interest rates calculated on inter-company loans. Generally withholding tax of 10% is payable on interest remitted to non-residents. More restrictive thin capitalization rules applied from 1 July 2014, reducing allowable debt thresholds from 3:1 to 1.5:1 on a debt to equity basis and interest on excessive debt is denied deduction, irrespective of whether interest is paid to overseas related parties or arm’s length domestic parties.

9.Transfer pricing penalties

Penalty is 25% of the tax shortfall as a result of obtaining a transfer pricing benefit, reduced to 10% where the entity is considered to have treated the transfer pricing rules as applying in a way that is reasonably arguable. Penalties can be up to 50% where it is reasonable to conclude that the entity entered into the scheme with the sole or dominant purpose of obtaining a transfer pricing benefit.

Firm: Hall Chadwick www.hallchadwick.com.auContact: David Kenney - [email protected]

5 | Transfer Pricing 2015 - AGN Asia Pacific Region

Hong Kong 2015 TRANSfeR PRIcING

1.TP legislation/guidelines

In December 2009, the Inland Revenue Department (“IRD”) issued the Departmental Interpretation and Practice Notes (“DIPN”) No. 46 “Transfer Pricing Guidelines – Methodologies and Related Issues). In the DIPN No. 46, the Commissioner of the IRD confirms that they would in general seek to apply the arm’s length principles expressed in OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations.

2.TP documentation required to be filed with tax return

There is no specific TP documentation requirement, and only limited disclosure in profits tax return concerning whether or not there is transaction with a closely connected non-resident person is required. In addition, related party transactions have to be disclosed in audited accounts in accordance with accounting standards.

3. TP audits done by tax authority

No major TP audits have been done and published by the IRD so far.

4.Advance Pricing Arrangement

A Departmental Interpretation & Practice Note No. 48 “Advance Pricing Arrangement” was issued by the Hong Kong Tax Department in March 2012 provide guidance to enterprises seeking an Advance Pricing Arrangement (APA). It explains the APA process and the terms and conditions of the APA process prescribed by the Hong Kong Tax Department. However, the Hong Kong Tax Department will only consider bilateral or multilateral APA applications.

5.Mutual Agreement Procedures (MAP)

Provisions for mutual agreement are found in double tax agreements between Hong Kong and other tax jurisdictions. Request for resolving of the double taxation issues by the tax treaty partners can be made in writing to the “The Hong Kong Competent Authority of 36/F, Revenue Tower, 5 Gloucester Road, Wanchai, Hong Kong” or by email at [email protected]. For MAP request made by Hong Kong resident a form IR.1454 should be completed and returned to the “Hong Kong Competent Authority”.

6.Basis to recover intra-group service charges

There is no specific requirement. Intra-group service charges are subject to the general deduction rules under Hong Kong tax laws. There is no withholding tax imposed on such payment to non-resident.

6 | Transfer Pricing 2015 - AGN Asia Pacific Region

7.cross border management fee charges

There is no specific requirement. Management fee charges are subject to the general deduction rules under Hong Kong tax laws. There is no withholding tax imposed on such payment to non-resident.

8.Inter-company loans

Interest received / charged on Inter-Company loans are subject to the general tax rules under Hong Kong Tax Law. There is no thin capitalization rule.

9.Transfer pricing penalties

There is no specific penalty rule for TP arrangements. However, the general penalty rule may apply and penalty of up to three times of tax underpaid may be imposed on those cases that transfer pricing primarily used in the context of tax avoidance and tax evasion.

Firm: Yong Zheng CPA Limited - www.yongzhengcpa.comContact: Ms Pinky Chan - [email protected]

7 | Transfer Pricing 2015 - AGN Asia Pacific Region

JAPAn 2015 TRANSfeR PRIcING

1.TP legislation/guidelines

Japanese Tax Bureau has issued TP rulings. They have been in practice since 1986.

2.TP documentation required to be filed with tax return

Not required, but tax payer is obliged to maintain such documents and provide to tax authority when required.

3. TP audits done by tax authority

There is no fixed rule how they decide a tax payer to carry tax audit, but once chosen it may last minimum a year, and put a considerable burden to the company.TP Tax audit used to be for larger companies, but it is getting popular that medium/smaller sized companies are also scrutinized.

4.Advance Pricing Arrangement

Available but have to wait for a long time. Informal consultation with the tax authority is recommended before officially apply for the APA.

5.Mutual Agreement Procedures

Mutual Agreement Procedures are available only with the countries tax treaty has been concluded.

6.Basis to recover intra-group service charges

As a practice, 5% to 7% mark up rate is accepted to intra-group services, especially when Japanese company is a receiving side. When a Japanese company is a paying side, there is no such standard and have to be verified to satisfy the Bureau.

8 | Transfer Pricing 2015 - AGN Asia Pacific Region

7.cross border management fee charges

Only on the basis of arm’s transaction, the charges are deductible. As Management fee charge arrangement will be investigated in full, not only the documentation, but economic and logical good reason for that need to be substantiated.

8.Inter-company loans

Terms and conditions of the loan have to be commercial and on an arm’s length basis. The transaction could be caught by Thin capitalization rule, regardless of the TP rule.

9. Transfer pricing penalties

General tax penalty rule applies, and no extra penalty tax rule exists.Penalty tax rate applicable is either 20% or 40%, of the amended tax liabilities.However, as referred to in 3 above, in general as the investigation may takes years until the end, if there are additional TP tax liabilities, interest penalty at a rate of 13.6% per annum for delayed payment sometimes reaches to an enormous amount.

Firm: Hor-u Group | www.hor-u.jpContact: Fumiaki Masulo | [email protected]

9 | Transfer Pricing 2015 - AGN Asia Pacific Region

KOReA 2015 TRANSfeR PRIcING

1.TP legislation/guidelines

International Tax Adjustment Act

2.TP documentation required to be filed with tax return

(1) Various related contracts concerning the transfer and acquisition of assets.

(2) Product Pricing table(3) Manufacturing cost specification(4) Transactions each item description (to be identified separately from

transactions with related parties)(5) If provide the services or other transactions, (1) to (4) similar to the

document(6) Corporate organization and working-allotment table(7) International trade pricing data(8) Internal guidance on the pricing of the parties that have a special

relationship(9) Accounting principles and methods associated with the transaction(10) Business activities of the person associated with the transaction(11) Cross-shareholding status of the people in related parties(12) Income tax forms or missing items(13) Data to identify the service transaction made by the normal price(14) Cost-sharing agreements, etc.(15) Other appropriate data for Pricing.

3. TP audits done by tax authority

Yes

4.Advance Pricing Arrangement

Residents may apply for approval to the end of the first tax year in which want to apply th method for calculating the normal value.

5.Mutual Agreement Procedures

Reason for request To whom

If there is a necessity to discussion about the application and interpretation of tax treaties. Minister of strategy and Finance

If there is a possibility that taxes levied or imposed that do not comply with the

provisions of the tax treatyNTS commissioner

If need a tax adjustment in accordance with tax treaty between countries NTS commissioner

10 | Transfer Pricing 2015 - AGN Asia Pacific Region

6.Basis to recover intra-group service charges

According to Korean tax laws, there is no specific requirement. Intra-group service charges are subject to the general deduction rules.

7.cross border management fee charges

If satisfy all of the following conditions, the transaction cast is recognized as the normal price.(1) The service provider has signed an agreement in advance, and will actually

provide the services.(2) The party receiving the services will be additional revenue generation or cost

savings.(3) The cost of receiving services will be calculated in accordance with the

relevant laws and regulations.(4) Keep documents that proves

8.Inter-company loans

In the following cases, paid interest on the excess debt of a domestic company is not recognized.

A + B > C * D

A : The amount borrowed directly from foreign controlling shareholderB : The amount borrowed from a third party by guarantees of the foreign controlling shareholderC : The amount of equity invested in foreign controlling shareholderD : Usually 3 times (if the finance company, applied 6 times)

9.Transfer pricing penalties

(1) Submission breach

The imposed criteria The amount

‘2. TP document- (12) ‘is missing or false submission 70 million won

‘2. TP document- (6),(10),(11) ‘is missing or false submission 30 million won

Others 50 million won

(2) Penalties under-reported : 10% of under-reporting pay tax

Firm: Seoil & Company | www.seoilacc.co.krContact: Jin-Hyuk Joo | [email protected]

11 | Transfer Pricing 2015 - AGN Asia Pacific Region

MALAySIA 2015 TRANSfeR PRIcING

1.TP legislation/guidelines

Inland Revenue Board (IRB) issued its first TP Guidelines on 8 July 2003. A revised version of TP Guidelines was issued in July 2012. Legislation has been introduced effective from 1 Jan 2009.

2.TP documentation required to be filed with tax return

Taxpayer who enters into controlled transactions with related companies is required to prepare and maintain contemporaneous TP documentation. It is mandatory to prepare but not required to be filed together with the tax return.

3. TP audits done by tax authority

IRB has issued TP Audit Framework (TPAF) with effective from 1/4/2013. TP audits generally cover a period of 3 to 6 years of assessment depending on the TP issues.

However, with effect from 1 January 2014, the years of assessment to be covered will be restricted up to 5 years of assessment. The selection of cases for audit is determined by the significance in amount of controlled transactions between related companies, before a detailed risk analysis is carried out.

The Director General is allowed to have a 7 years time bar period for raising an assessment or additional assessment in respect of TP adjustment for a transaction entered into between associated persons not at arms length.

4.Advance Pricing Arrangement

Taxpayers are allowed to apply for APAs with effect from 1 January 2009.

5.Mutual Agreement Procedures

Taxpayers residing in Malaysia can apply for assistance from the competent authorities in Malaysia through the MAP, on issues arising from TP audit adjustments affecting cross-border transactions with related companies in any treaty partner country.

12 | Transfer Pricing 2015 - AGN Asia Pacific Region

6.Basis to recover intra-group service charges

Under the TP Guideline, taxpayer must apply arm’s length principle for intra-group services, it is necessary to consider the nature, value, cost and functions of the service from the perspective of both the provider and recipient of the service.

7.cross border management fee charges

Taxpayers are allowed deduction for such charges from overseas holding company or head office provided they are charged on arm’s length basis that is commensurate with the services provided.

10% withholding tax would apply if such services are rendered in Malaysia subject to tax treaty provisions.

8.Inter-company loans

IRB has introduced thin capital rules. Lender must determine and charge at arm’s length interest rate. Interest expense is deductible provided arm’s length and thin capitalization rules are satisfied.

15% withholding tax applicable on interest payments made to non-residents, subject to lower rates applicable under tax treaty provisions.

Nevertheless, the Government has deferred the implementation of thin capital rules until further notice.

9.Transfer pricing penalties

If it is discovered during a TP audit that there has been an understatement or omission of income, a penalty will be imposed equals to the amount of tax undercharged (100%) accordingly.

A concessionary penalty rate may be imposed in a case where the taxpayer makes a voluntary disclosure. Upon voluntary disclosure, the taxpayer is still required to prepare the TP documentation.

Contact Person: Mr Foong Kok KeongE-mail: [email protected]

13 | Transfer Pricing 2015 - AGN Asia Pacific Region

New ZeALANd 2015 TRANSfeR PRIcING

1.TP legislation/guidelines

New Zealand’s current transfer pricing provisions are contained in ss GB and GC – to GC 14 on the Income Tax Act 2007. The transfer pricing legislation closely follows the current OECD Guidelines and the United States s 482 regulations. Other features of the legislation are as follows:

- The rules are based on the arm’s length principle, as defined by the OECD Guidelines, using five permitted pricing methods (ie, comparable uncontrolled price (CUP), resale price, cost plus, profit split and comparable profits methods).

- The arm’s length amount of consideration must be determined by applying whichever method or combination of methods will produce the most reliable measure of the amount completely independent parties would have agreed upon after real and fully adequate bargaining.

- The substitution of an arm’s length price applies only so as to increase New Zealand’s tax base (ss GC 7 & GC 8). The burden of proof as to the arm’s length nature of consideration rests with the Commissioner of the Inland Revenue unless the commissioner can show the taxpayer has not cooperated or can demonstrate another amount to be a more reliable measure of an arm’s length amount

- There are specific powers, in addition to those in the double tax agreements (DTA’s), to allow compensating adjustments and corresponding adjustments.

2.TP documentation required to be filed with tax return

There is no specific statutory requirement for New Zealand taxpayers to prepare transfer pricing documentation in relation to their international associated party transactions. However, TP documentation is central to the process if justifying and explaining the arm’s length nature of a taxpayers pricing of cross border associated party transactions. A taxpayers main purpose in preparing and maintaining documentation should be to place itself in the position where it can readily demonstrate to the IRD that its transfer prices are consistent with the arm’s length principle.

3. TP audits done by tax authority

The IRD regularly reviews arrangements where it becomes aware of them, usually through a GST audit or something similar. The client should have high quality documentation which should satisfy any IRD audit enquiry. However, questionnaires remain central to the IRD’s transfer pricing compliance programme. The questionnaire is a high level risk review, in which taxpayers are requested to disclose details of their financial performance, the worldwide group’s financial performance, the type and amounts of cross border associated party transactions, the method or methods used to test the transactions and whether documentation exists to substantiate the transfer prices.

14 | Transfer Pricing 2015 - AGN Asia Pacific Region

4.Advance Pricing Arrangement

APA’s are available in New Zealand. They are negotiated in a cooperative environment in which the IRD and the taxpayer agree on a transfer pricing methodology that will result in an appropriate allocation of income and expenses between the related parties. A concluded APA generally lasts for 3 to 5 years and may be renewed on an ongoing basis.

5.Mutual Agreement Procedures

Provisions for mutual agreement procedures are found in double tax agreements between New Zealand and other tax jurisdictions.

6.Basis to recover intra-group service charges

Intra-group service changes are subject to the general deduction rules under New Zealand tax law. Depending on the type of intra-group service charge, withholding tax may be payable on payments to a non-resident (such as interest and intra-group royalties).

7.cross border management fee charges

Management fees are subject to general deduction rules under New Zealand tax law. There is no withholding tax imposed on such payments to non-residents.

8.Inter-company loans

Cross border financing form a substantial part of the total associated party dealings by New Zealand members of multinational groups. Key issues arising include the pricing of interest and guarantee fees at market rates and capital structuring within New Zealand’s thin capitalization rules. New Zealand owned multinationals also need to account for the very same issues in their outbound financing activities. The IRD endeavours to strike a balance between protecting the tax base and containing compliance costs.

9.Transfer pricing penalties

New Zealand’s tax legislation specified penalties that may be applied to adjustments arising from TP issues. Determination of the penalties focuses on culpability. The shortfall penalties are; - Not taking reasonable care – 20% of tax shortfall. - Unacceptable interpretation – 20% of tax shortfall. - Gross carelessness – 40% of tax shortfall - Abusive tax avoidance – 100% of tax shortfall Evasion – 150% of tax shortfall.Any penalties are likely to be met with an interest charge as well.

Firm: HFK Limited Chartered Accountants | www.hfk.co.nzContact: Greg Cowles | [email protected]

15 | Transfer Pricing 2015 - AGN Asia Pacific Region

PAKIsTAn2015 TRANSfeR PRIcING

1.TP legislation/guidelines

There is no specific TP legislation except section 108 of the Income Tax Ordinance, 2001 which emphasis TP to be on an arm’s length basis. The Income Tax rules identify four methods for determining the arm’s length transaction viz., Comparable Uncontrolled Price Method; Re-sale Price Method, Cost-Plus Method & Profit Split Method with powers to Commissioner to adopt any method.

2.TP documentation required to be filed with tax return

The Law in Pakistan does not provide with any specific documents to be filed with tax return related to TP.

3. TP audits done by tax authority

There is no specific audit requirement. The Commissioner, during the course of regular audit proceedings, has the powers to ask for the TP related transactions.

4.Advance Pricing Arrangement

Pakistan does not have an advance pricing arrangement regime.

5.Mutual Agreement Procedures

No specific procedure has been defined it depend upon the mutual agreements.

6.Basis to recover intra-group service charges

There is no specific requirement. Depending on the type of transactions withholding tax provisions apply.

16 | Transfer Pricing 2015 - AGN Asia Pacific Region

7.cross border management fee charges

Cross border management fee are covered under the Double Taxation agreements between Pakistan & other countries

8.Inter-company loans

Inter-company loans require special approval under section 208 the Companies Ordinance, 1984 and restrict inter-company loans on softer terms.

9.Transfer pricing penalties

Transfer pricing penalties are not specifically defined under the Income Tax Ordinance, 2001.

Firm: Riaz Ahmad, Saqib, Gohar & Co. | www.rasgco.comContact: Gohar Manzoor | [email protected]

17 | Transfer Pricing 2015 - AGN Asia Pacific Region

SINGAPORe2015 TRANSfeR PRIcING

1.TP legislation/guidelines

Inland Authority of Singapore (“IRAS”) has updated the TP guidelines on 6 January 2015. Section 34D of the Singapore Income Tax Act has enacted the requirement for compliance for related party transactions to be conducted on arm’s length basis.

2.TP documentation required to be filed with tax return

Taxpayer should maintain TP documentation. However, it is not required to be filed with the tax return. Following taxpayers are excluded from the preparation of transfer pricing documentation if they meet the following exemptions or thresholds:

• Domestic transactions for services, royalties and trades as long as both parties are at the same tax rate

• Domestic loans between Singapore entities that are not in the business of borrowing or lending money as interest restriction will apply

• Recovery of routine support services that are recovered at cost plus 5% mark up

• Related parties that have entered into Advance Pricing Arrangement

For all other related party transactions (“RPT”) the following thresholds apply:

Category of RPT Threshold (S$) per financial year

Sale of goods 15 million

Purchase of goods 15 million

Loans provided to related parties 15 million

Loans received from related parties 15 million

All other transactions (service income/expense, royalty income/expense, rental

income/expense)1 million per category of transaction

3. TP audits done by tax authority

IRAS, under the TP consultation process, may target taxpayers with substantial cross border related party transactions as well as taxpayers making continues losses. IRAS will assess the adequacy of the taxpayer’s compliance with the arm’s length principles for intra-group transactions and may make adjustments if profits are not at arm’s length.

4.Advance Pricing Arrangement

IRAS issued the Supplementary Guidance on Advance Pricing Arrangement (“APA”) on 20 Oct 2008. Taxpayers can avail themselves to APA’s where appropriate.

18 | Transfer Pricing 2015 - AGN Asia Pacific Region

5.Mutual Agreement Procedures

Singapore as a treaty partner to more than 70 double tax treaties subscribes to the mutual agreement procedures generally as prescribed under Article 25 of the OECD model tax convention.

6.Basis to recover intra-group service charges

IRAS accepts the cost plus 5% mark up as an arm’s length service fee charge for routine support services rendered between intra-group and related companies.

IRAS expects non-routine support services to be charged and recovered on arm’s length basis that is commensurate with the industry practice and/or substantiated by proper bench marking studies or analysis.

7.cross border management fee charges

Taxpayers are allowed deduction for such charges from overseas holding company or head office provided they are charged on arm’s length basis that is commensurate with the services provided. There is a 17% withholding tax if such services are rendered in Singapore subject to tax treaty provisions.

8.Inter-company loans

Lenders can extend inter-company loans within Singapore interest free subject to interest restriction on their non-income producing and/or non-trade balances.

However, with effect from 1 January 2011, cross border inter-company loans will be required to be charged an arm’s length interest rate. There is a 15% withholding tax on interest payment to non-residents, subject to tax treaty provisions.

There is no thin capital rule.

9.Transfer pricing penalties

The general penalty rules in the Income Tax Legislation will apply.

Firm: BSL Tax Services Pte Ltd | www.bslpac.com.sgContact: N Vimala Devi | [email protected]

19 | Transfer Pricing 2015 - AGN Asia Pacific Region

THAILANd2015 TRANSfeR PRIcING

1.TP legislation/guidelines

Thailand’s transfer pricing rules are contained in its Revenue Code, in order toprevent the evasion of taxation caused by manipulated transfer pricing within the MNEs, tax authorities can price goods and services by applying the provisions of Section 65 bis (4) and (7), Section 65 ter, and Section 70 ter under the Revenue Code, Double Tax Agreements between Thailand and other countries, as well as Standard Accounting No. 37 and 47. Moreover, the Revenue Department recently issued Departmental Instruction No. Paw 113/2545, Subject : Corporate IncomeTax - The Determination of Transfer Price based on the Market Price, issued on16th May 2002, which is a guideline on how to Thai taxpayers should apply thearm’s length principle.

2.TP documentation required to be filed with tax return

There is no specific TP documentation requirement.

3. TP audits done by tax authority

No major TP audits have been done by the TRD.

4.Advance Pricing Arrangement

According to, Departmental Instruction No. Paw 113/2545 (Clause 5), APAs areavailable. However, based on current practice, the Thai Revenue Department isnot willing to accept applications for unilateral APAs. Bilateral agreements may be applied for under the mutual agreement procedure of treaties. The Thai Revenue Department has issued a booklet including guidance for bilateral APAs

5.Mutual Agreement Procedures

In order to prevent the evasion of taxation caused by manipulated transfer pricing within the MNEs, it should be followed with the Departmental Instruction No. Paw 113/2545. Basis of calculation income should be market price which acceptable by Revenue Department (See no.6)

20 | Transfer Pricing 2015 - AGN Asia Pacific Region

6.Basis to recover intra-group service charges

Market price would be charged between independent parties at the date of transactionfor the sale of assets, provision of services or lending of funds under the same circumstances.Pricing methods that the Revenue Department accepts are as follows:• Comparable Uncontrolled Price Method• Resale Price Method• Cost Plus Method• Other methods if any of the above methods cannot be applied, includingprofit based methods adopted by OECD such as profit-split method, transactional net margin method and any other methods that are internationally accepted.

7.cross border management fee charges

Management fee charges is based on market pricing methods according to No.6,withholding tax related with this charges should be considered to the DTA.

8.Inter-company loans

No interest rate is specified on inter-company loans.

9.Transfer pricing penalties

There is no specific penalty for transfer pricing assessments. However, the general corporate tax penalty regime applies. A penalty of up to 100 percent of the additional corporate tax and interest surcharges of 1.5 percent per month may apply on outstanding tax.

Contact person: Mr. Krit SummacaravaE-mail: [email protected]

www.agn.org

For further information, or become involved, please contact:

AGN InternationalEmail: [email protected] | Office: +44 (0)20 7971 7373 | Web: www.agn.org

AGN International Ltd is a company limited by guarantee registered in England & Wales, number 3132548, registered office 24 Greville Street, London EC1N 8SS, United Kingdom. AGN International Ltd (and its regional affiliates; together “AGN”) is a not-for-profit worldwide membership association of separate and independent accounting and advisory businesses. AGN does not provide and is not responsible for services to the clients of its members. Members provide services to their clients under their own local agreements with those clients. Members are not in partnership together, they are neither agents of nor obligate one another, and are not responsible for the services of other members. 04

74 A

sia

Tran

sfer

Pri

cing