Embed Size (px)

Citation preview

TransCanada Corporation

Can We Make Energy Infrastructure

Great Again? Corey Goulet Senior Vice-President, Major Projects

University of Denver 2016 Pipeline Leadership Conference November 15, 2016

Forward-Looking Information

This presentation includes certain forward looking information to help current and potential investors understand management’s assessment of our future plans and financial outlook, and our future prospects overall. Statements that are forward-looking are based on certain assumptions and on what we know and expect today and generally include words like anticipate, expect, believe, may, will, should, estimate or other similar words. Forward-looking statements do not guarantee future performance. Actual events and results could be significantly different because of assumptions, risks or uncertainties related to our business or events that happen after the date of this presentation. Our forward-looking information is based on the following key assumptions: planned monetization of our U.S. Northeast power assets and a minority interest in our Mexican natural gas pipeline business, inflation rates, commodity prices and capacity prices, timing of financings and hedging, regulatory decisions and outcomes, foreign exchange rates, interest rates, tax rates, planned and unplanned outages and the use of our pipeline and energy assets, integrity and reliability of our assets, access to capital markets, anticipated construction costs, schedules and completion dates, acquisitions and divestitures.

Our forward looking information is subject to risks and uncertainties, including but not limited to: our ability to successfully implement our strategic initiatives and whether they will yield the expected benefits including the expected benefits of the acquisition of Columbia, timing and execution of our planned asset sales, the operating performance of our pipeline and energy assets, economic and competitive conditions in North America and globally, the availability and price of energy commodities and changes in market commodity prices, the amount of capacity sold and rates achieved in our pipeline businesses, the amount of capacity payments and revenues we receive from our energy business, regulatory decisions and outcomes, outcomes of legal proceedings, including arbitration and insurance claims, performance of our counterparties, changes in the political environment, changes in environmental and other laws and regulations, construction and completion of capital projects, labour, equipment and material costs, access to capital markets, interest and foreign exchange rates, weather, cyber security and technological developments. You can read more about these risks and others in our Quarterly Report to shareholders dated July 27, 2016 and 2015 Annual Report filed with Canadian securities regulators and the U.S. Securities and Exchange Commission (SEC) and available at www.transcanada.com.

As actual results could vary significantly from the forward-looking information, you should not put undue reliance on forward-looking information and should not use future-oriented information or financial outlooks for anything other than their intended purpose. We do not update our forward-looking statements due to new information or future events, unless we are required to by law.

This presentation contains reference to certain financial measures (non-GAAP measures) that do not have any standardized meaning as prescribed by U.S. generally accepted accounting principles (GAAP) and therefore may not be comparable to similar measures presented by other entities. These non-GAAP measures may include Comparable Earnings, Comparable Earnings per Share, Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA), Comparable EBITDA, Adjusted EBITDA, Earnings Before Interest and Taxes (EBIT), Comparable EBIT, Distributable Cash Flow, Comparable Distributable Cash Flow, Distributable Cash Flow per Share, Comparable Distributable Cash Flow per Share, Comparable Interest Expense, Comparable Interest Income and Other, Comparable Income Tax Expense, Comparable Net Income Attributable to Non-Controlling Interests, Comparable Net Income from Equity Investments, Comparable Depreciation and Amortization, and Funds Generated from Operations. Reconciliations to the most closely related GAAP measures are included in our Quarterly Report to shareholders dated July 27, 2016 filed with Canadian securities regulators and the SEC and available at www.transcanada.com.

TransCanada Corporation (TSX/NYSE: TRP)

One of North America’s Largest Natural Gas Pipeline Networks

• Operating 90,300 kms (56,100 miles) of pipelines

• Transports more than 25 per cent of continental demand

North America’s Largest Natural Gas Storage Operator

• More than 664 Bcf of capacity

Canada’s Largest Private Sector Power Generator

• 17 power facilities, 10,500 MW

• Diversified portfolio, including wind, hydro, nuclear, solar and natural gas

Premier Liquids Pipeline System

• Keystone Pipeline System: 4,300 km (2,700 miles), 545,000 bbl/d contracted capacity

• Safely delivered more than 1.3 billion barrels of Canadian oil to U.S. markets since 2010

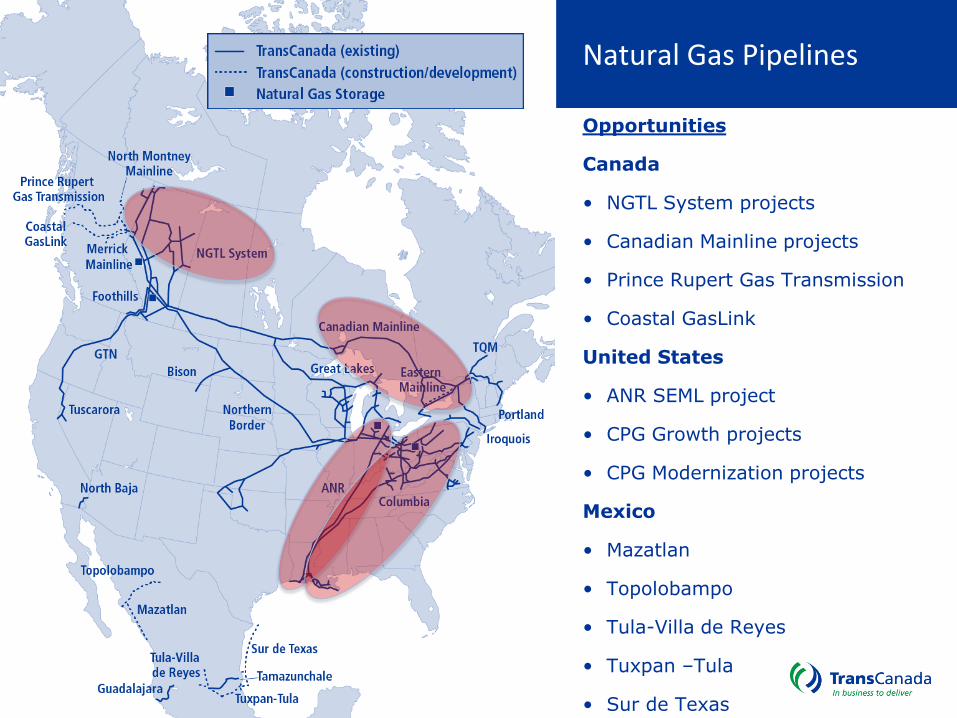

Natural Gas Pipelines

Opportunities

Canada

• NGTL System projects

• Canadian Mainline projects

• Prince Rupert Gas Transmission

• Coastal GasLink

United States

• ANR SEML project

• CPG Growth projects

• CPG Modernization projects

Mexico

• Mazatlan

• Topolobampo

• Tula-Villa de Reyes

• Tuxpan –Tula

• Sur de Texas

Liquids Pipelines

Opportunities

Canada

• Northern Courier

• Grand Rapids

• Energy East

• Heartland and TC Terminal

• Upland

United States

• Houston Lateral and Terminal

• Cushing Marketlink Receipt Facility

• Keystone XL

Committed to Responsible Development

• Safely delivering energy to meet North American demand in an economically, environmentally and socially responsible manner

• Receives recognition for Corporate Social Responsibility efforts from third-party investment rating agencies

• Visit csrreport.transcanada.com to learn more about our corporate social responsibility practices

Committed to Safety

• Top industry safety record

• Strive for zero safety incidents

• Investing heavily in research and development to enhance safety, integrity and quality of assets and improve standards industry-wide

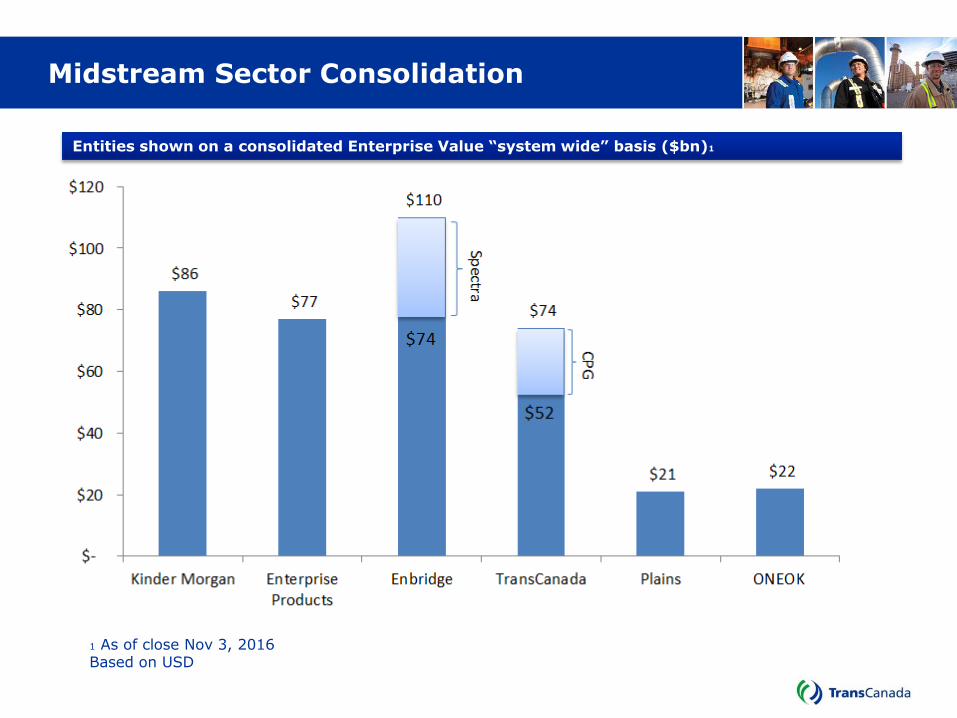

Midstream Sector Consolidation

Entities shown on a consolidated Enterprise Value “system wide” basis ($bn)1

1 As of close Nov 3, 2016 Based on USD

The MPL/Yield-Co Business Model is Being Questioned

“The model is now being questioned by investors. With double-digit yields, the ability for some MPLs to access the equity market on economic terms is impaired – at least for now” “Does the precedent cut of Kinder Morgan lead to many more dividend reductions or a trend toward much reduces dependence on capital markets (means much lower section distribution growth)” “Dividend and distribution cuts have become potential reality, which bags the question of, how do you value them?”

Acquisition Opportunities in Midstream and Power/Yield-Co Sectors

Well Positioned for Growing Equity Investor Risk Aversion

2

1 3

4 5

Market Shockwaves

WTI trades below US$40

Energy Transfer announces acquisition of Williams

Kinder Morgan lowers dividend growth guidance to 6-10% from 10%

Moody’s downgrades Kinder Morgan after it announces acquisition of majority interest in NGPL

5 1

2

3

4

TRP extends 8-10%annual dividend growth rate through 2020

TRP announces NCIB & private agreement to buy back up to 6.6 million shares

Strategic Rationale for Acquisition of Columbia Pipeline

• TransCanada to acquire Columbia Pipeline Group, Inc. (CPGX or Columbia) for US$25.50 per CPGX share in an all-cash deal

• Acquisition creates one of North America’s largest regulated natural gas transmission businesses

• Expected to be accretive to earnings per share in the first full year of ownership

• Premium natural gas pipeline and storage assets

• Extensive position in Marcellus and Utica basins

• FERC regulated assets generate stable and predictable earnings and cash flow

• US$7.3 billion portfolio of growth initiatives and modernization investments

• Complements our existing regulated natural gas pipeline and storage assets

• Long-term, fee-based contracts

• Diversified customer base

• Adds to basin diversification and access to large markets

Illustrates the configuration of material pipeline systems and

projects within TransCanada’s natural gas pipeline network

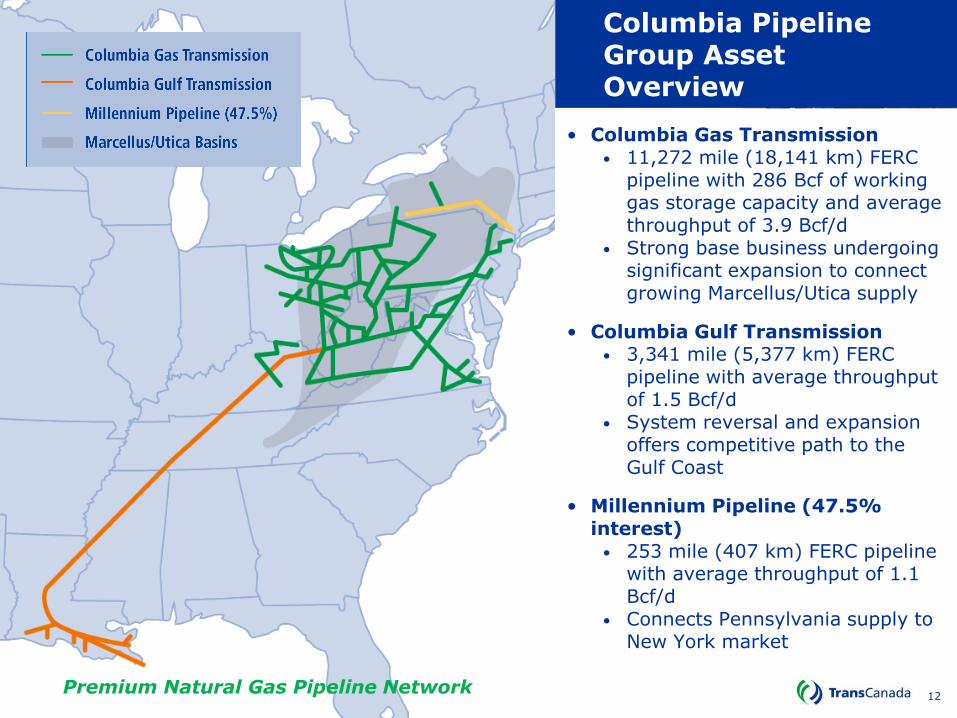

Columbia Pipeline Group Asset Overview

• Columbia Gas Transmission • 11,272 mile (18,141 km) FERC

pipeline with 286 Bcf of working gas storage capacity and average throughput of 3.9 Bcf/d

• Strong base business undergoing significant expansion to connect growing Marcellus/Utica supply

• Columbia Gulf Transmission • 3,341 mile (5,377 km) FERC

pipeline with average throughput of 1.5 Bcf/d

• System reversal and expansion offers competitive path to the Gulf Coast

• Millennium Pipeline (47.5% interest)

• 253 mile (407 km) FERC pipeline with average throughput of 1.1 Bcf/d

• Connects Pennsylvania supply to New York market

Premium Natural Gas Pipeline Network 12

13

CPG Acquisition - Timeline

Q1 2016 Q2 2016 Q3 2016

January – Inception • Negotiations

commenced between TransCanada and CPG

Mid-January to February • 40 day Due Diligence

March 17- Offer • TransCanada

announced merger agreement and purchase plans to acquire CPG

July 1- Closing • TransCanada

announced the completion of the transaction to acquire CPG for US$13 Billion

June 22 • Acquisition of CPG

receives stockholder support

May 16/17 • CFIUS clearance • Early termination of

waiting period under the HSR Act

1

Engage And Develop

Our Team

2

Strengthen Our Execution

Focus

3

Deepen Our Growth

Inventory

4

Enhance The Customer

Experience

Deliver

Results

CPG Integration Priorities

15

Engage & Develop our Team

•Realize integration synergies •Develop & implement our tactical plan •Sustainable, repeatable processes •Engage in Business Transformation

•Align our common values •Become a nimble, results-oriented organization •Consistently set and then meet or exceed expectations •Understand our role as part of the larger TransCanada family

•Attract and retain talent •Identify and mentor high performers •Further build bench strength and depth •Expand business acumen across the organization Build a Common Culture & Identity

Continue to Develop Our Team

Execute Transformative Change

Build

Develop

Execute

Deliver

Integration Resourcing Roadmap

On Track

BY JULY 1, 2016 Vice-President Level Organization Structure and Leadership Announced

BY JULY 29, 2016 Director-Level Organization Structure and Leadership Announced

BY SEPT 30, 2016 Organizational Changes and Personal Impacts Communicated at All Levels

BY MID-2017 Business Optimization completed

12 Day one 30 Days 100 days 12 months

17

Integration – HR, IS, Supply Chain & COE

Q4 2016 Q1 2017 Q2 2017 Q3-4 2017

FEB-APRIL SAP TRAINING

APRIL 3 SAP GO-LIVE

March to April • All TC HR practices and HR

policies take effect • SCM System integration : MRC

Global, Fieldglass • Assignment of ASL • Vendor, Supplier and Material

Master Data integration

BY DEC 31, 2016 • Plan for HR programs,

policies and practices communicated

• Technical COE priorities identified, plans approved

• Email roll-out complete

End of 2017 • COE

Implementation completed

• All Total TC rewards programs in place

Historical Issues facing the Industry

18

• Environmental interest in our industry is not new

• Opponents capitalized on three major events

1. Deepwater Horizon oil spill

2. Enbridge’s Kalamazoo oil spill

3. San Bruno explosion

• Fear and concern about the energy industry is now at the forefront

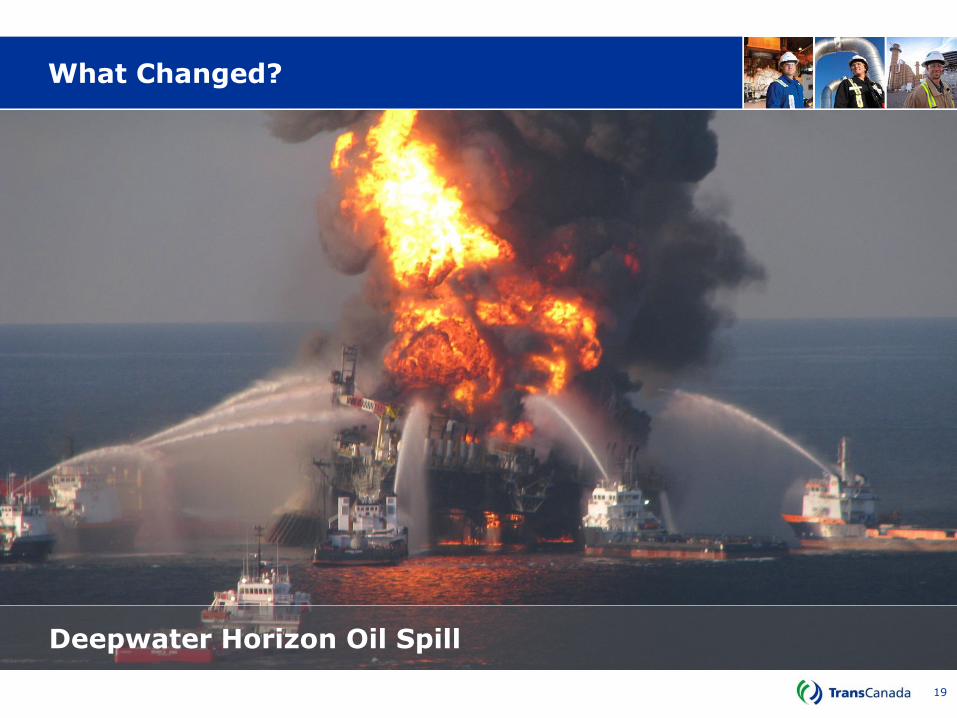

What Changed?

19

Deepwater Horizon Oil Spill

What Changed?

20

Kalamazoo Oil Spill

What Changed?

21

San Bruno Explosion

ENGO Activism

22

Source: Rockefeller Brothers Fund – The Tar Sands Campaign

Misguided Protest

23

Regulatory, Permitting Timelines & Costs Rising

Lack Of Deadline For Action

Increasing Risk Activists Have Learned That Delay = Denial

Dakota Access Pipeline Protest

Legitimate Concern

25

• Is the public’s concern legitimate? Absolutely!

• Our industry is committed to protecting the environment

• Doing everything possible to ensure these events don’t occur

• TransCanada has a goal of achieving zero incident rates

• Investing billions of dollars in new technology and processes to make these

systems as safe as possible

• Since 2001, liquid pipeline-related incidents have decreased by 62%

26

Calgary Herald Cartoon

THE MEDIA

?

Global Energy Demand

27

Global Energy Demand by Fuel (million tones of oil equivalent)

Source: IEA World Energy Outlook 2015, New Policies Case

0

1

2

3

4

5

6

Oil Coal Gas Bioenergy Nuclear Hydro Renewables

2040

2013

28

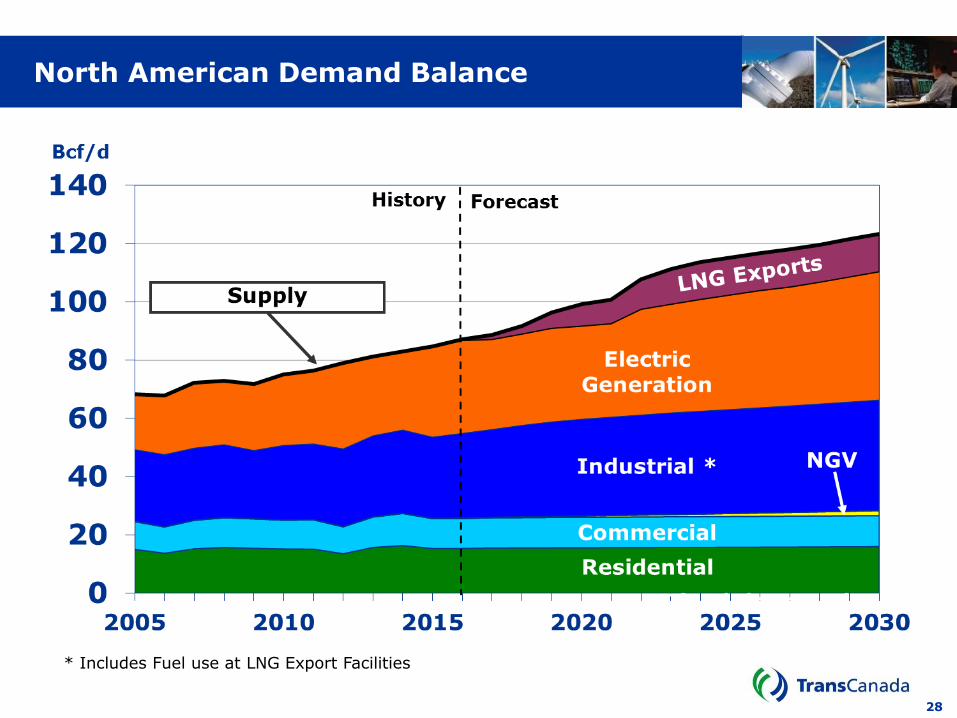

North American Demand Balance

* Includes Fuel use at LNG Export Facilities

North America’s Energy Infrastructure Requirements

29

$- $2 $4 $6 $8 $10 $12

North America

Europe

Pacific

Eastern Europe

Developing Asia

Middle East

Africa

Latin America

Inter-Regional Transport

Trillion

Coal

Oil

Gas

Power

Biofuels

Source: IEA World Energy Outlook 2012

Questions

30