Embed Size (px)

Citation preview

Transaction Advisory Services

Transaction TrendsNorwegian M&A update – Q4 2018

Norwegian M&A activity resilient to geopolitical turmoil – for now

Transaction Trends, published by EY Transaction Advisory Services, is a quarterly publication that aims to identify trends in the Norwegian transactions market. Data presented in this newsletter cover all transactions where the 500 largest companies in Norway have participated as either target, buyer or vendor. This makes Transaction Trends the most comprehensive transaction newsletter available for the Norwegian market.

Also in this edition:

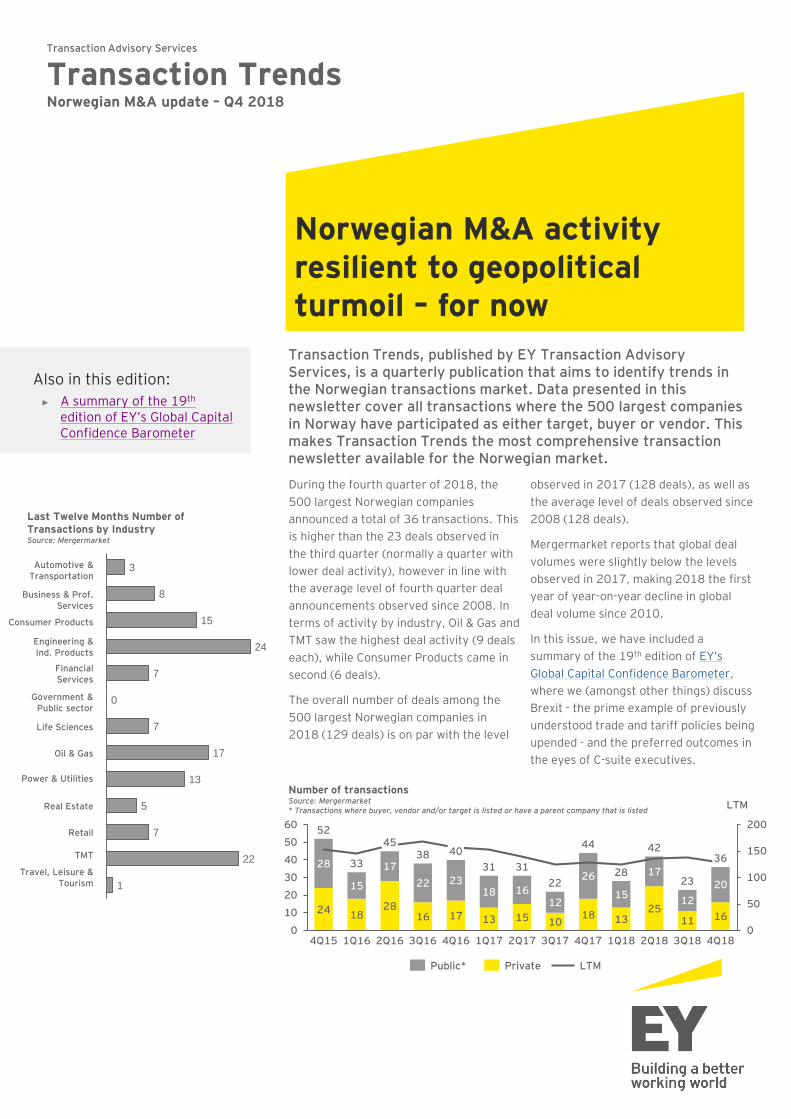

Number of transactionsSource: Mergermarket* Transactions where buyer, vendor and/or target is listed or have a parent company that is listed

During the fourth quarter of 2018, the

500 largest Norwegian companies

announced a total of 36 transactions. This

is higher than the 23 deals observed in

the third quarter (normally a quarter with

lower deal activity), however in line with

the average level of fourth quarter deal

announcements observed since 2008. In

terms of activity by industry, Oil & Gas and

TMT saw the highest deal activity (9 deals

each), while Consumer Products came in

second (6 deals).

The overall number of deals among the

500 largest Norwegian companies in

2018 (129 deals) is on par with the level

observed in 2017 (128 deals), as well as

the average level of deals observed since

2008 (128 deals).

Mergermarket reports that global deal

volumes were slightly below the levels

observed in 2017, making 2018 the first

year of year-on-year decline in global

deal volume since 2010.

In this issue, we have included a

summary of the 19th edition of EY’s

Global Capital Confidence Barometer,

where we (amongst other things) discuss

Brexit - the prime example of previously

understood trade and tariff policies being

upended - and the preferred outcomes in

the eyes of C-suite executives.

► A summary of the 19th

edition of EY’s Global Capital Confidence Barometer

3

8

15

24

7

7

17

13

5

7

22

1

0

Last Twelve Months Number of Transactions by IndustrySource: Mergermarket

Automotive & Transportation

Business & Prof. Services

Consumer Products

Financial Services

Government & Public sector

Power & Utilities

Real Estate

TMT

Travel, Leisure & Tourism

Oil & Gas

24 1828

16 17 13 15 1018 13

2511 16

28

15

17

22 2318 16

12

26

15

17

12

20

0

50

100

150

200

0

10

20

30

40

50

60

LTM

4238

4Q16 1Q182Q174Q15 1Q16

44

2Q16 1Q17

52

3Q16

36

3Q17 4Q17 2Q18

33

3Q18

4540

3131

2228

23

4Q18

Public* LTMPrivate

Engineering & Ind. Products

Life Sciences

Retail

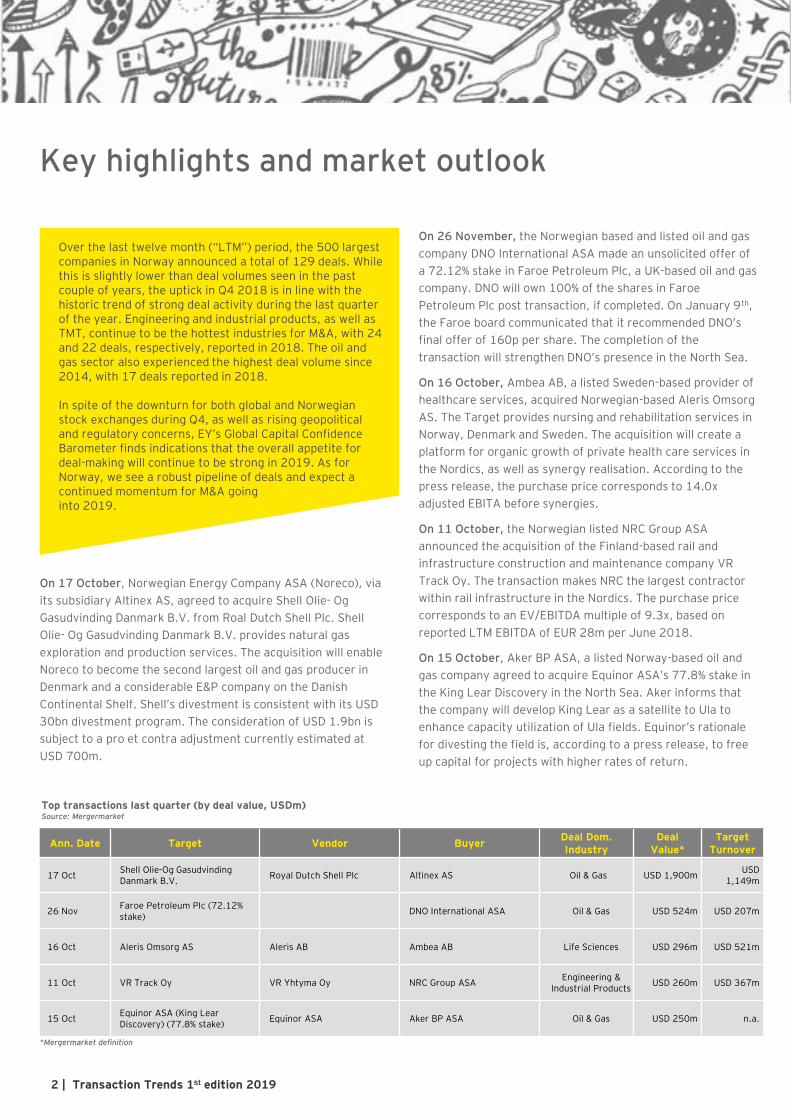

On 26 November, the Norwegian based and listed oil and gas

company DNO International ASA made an unsolicited offer of

a 72.12% stake in Faroe Petroleum Plc, a UK-based oil and gas

company. DNO will own 100% of the shares in Faroe

Petroleum Plc post transaction, if completed. On January 9th,

the Faroe board communicated that it recommended DNO’s

final offer of 160p per share. The completion of the

transaction will strengthen DNO’s presence in the North Sea.

On 16 October, Ambea AB, a listed Sweden-based provider of

healthcare services, acquired Norwegian-based Aleris Omsorg

AS. The Target provides nursing and rehabilitation services in

Norway, Denmark and Sweden. The acquisition will create a

platform for organic growth of private health care services in

the Nordics, as well as synergy realisation. According to the

press release, the purchase price corresponds to 14.0x

adjusted EBITA before synergies.

On 11 October, the Norwegian listed NRC Group ASA

announced the acquisition of the Finland-based rail and

infrastructure construction and maintenance company VR

Track Oy. The transaction makes NRC the largest contractor

within rail infrastructure in the Nordics. The purchase price

corresponds to an EV/EBITDA multiple of 9.3x, based on

reported LTM EBITDA of EUR 28m per June 2018.

On 15 October, Aker BP ASA, a listed Norway-based oil and

gas company agreed to acquire Equinor ASA’s 77.8% stake in

the King Lear Discovery in the North Sea. Aker informs that

the company will develop King Lear as a satellite to Ula to

enhance capacity utilization of Ula fields. Equinor’s rationale

for divesting the field is, according to a press release, to free

up capital for projects with higher rates of return.

Key highlights and market outlook

On 17 October, Norwegian Energy Company ASA (Noreco), via

its subsidiary Altinex AS, agreed to acquire Shell Olie- Og

Gasudvinding Danmark B.V. from Roal Dutch Shell Plc. Shell

Olie- Og Gasudvinding Danmark B.V. provides natural gas

exploration and production services. The acquisition will enable

Noreco to become the second largest oil and gas producer in

Denmark and a considerable E&P company on the Danish

Continental Shelf. Shell’s divestment is consistent with its USD

30bn divestment program. The consideration of USD 1.9bn is

subject to a pro et contra adjustment currently estimated at

USD 700m.

2 | Transaction Trends 1st edition 2019

Top transactions last quarter (by deal value, USDm)Source: Mergermarket

Ann. Date Target Vendor BuyerDeal Dom.Industry

DealValue*

TargetTurnover

17 OctShell Olie-Og GasudvindingDanmark B.V.

Royal Dutch Shell Plc Altinex AS Oil & Gas USD 1,900mUSD

1,149m

26 NovFaroe Petroleum Plc (72.12% stake)

DNO International ASA Oil & Gas USD 524m USD 207m

16 Oct Aleris Omsorg AS Aleris AB Ambea AB Life Sciences USD 296m USD 521m

11 Oct VR Track Oy VR Yhtyma Oy NRC Group ASAEngineering &

Industrial ProductsUSD 260m USD 367m

15 OctEquinor ASA (King Lear Discovery) (77.8% stake)

Equinor ASA Aker BP ASA Oil & Gas USD 250m n.a.

*Mergermarket definition

Over the last twelve month (“LTM”) period, the 500 largest companies in Norway announced a total of 129 deals. While this is slightly lower than deal volumes seen in the past couple of years, the uptick in Q4 2018 is in line with the historic trend of strong deal activity during the last quarter of the year. Engineering and industrial products, as well as TMT, continue to be the hottest industries for M&A, with 24 and 22 deals, respectively, reported in 2018. The oil and gas sector also experienced the highest deal volume since 2014, with 17 deals reported in 2018.

In spite of the downturn for both global and Norwegian stock exchanges during Q4, as well as rising geopolitical and regulatory concerns, EY’s Global Capital Confidence Barometer finds indications that the overall appetite for deal-making will continue to be strong in 2019. As for Norway, we see a robust pipeline of deals and expect a continued momentum for M&A going into 2019.

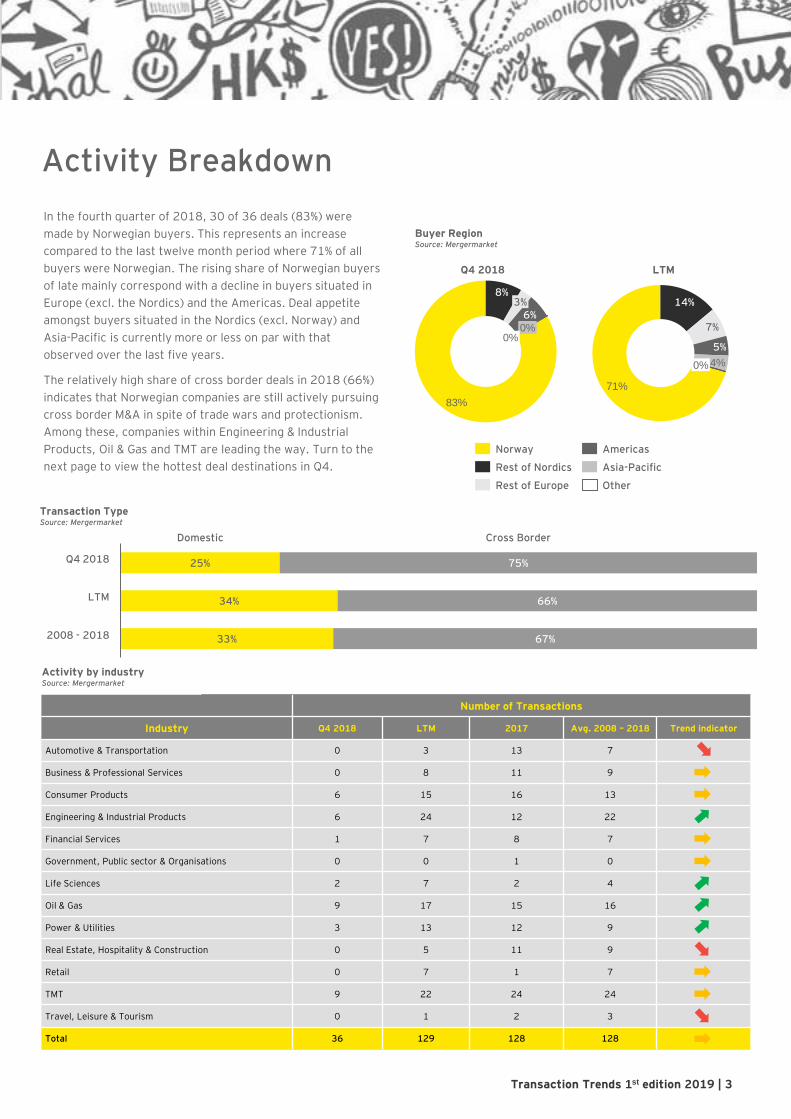

Transaction TypeSource: Mergermarket

Buyer RegionSource: Mergermarket

Activity Breakdown

In the fourth quarter of 2018, 30 of 36 deals (83%) were

made by Norwegian buyers. This represents an increase

compared to the last twelve month period where 71% of all

buyers were Norwegian. The rising share of Norwegian buyers

of late mainly correspond with a decline in buyers situated in

Europe (excl. the Nordics) and the Americas. Deal appetite

amongst buyers situated in the Nordics (excl. Norway) and

Asia-Pacific is currently more or less on par with that

observed over the last five years.

The relatively high share of cross border deals in 2018 (66%)

indicates that Norwegian companies are still actively pursuing

cross border M&A in spite of trade wars and protectionism.

Among these, companies within Engineering & Industrial

Products, Oil & Gas and TMT are leading the way. Turn to the

next page to view the hottest deal destinations in Q4.

83%

8%

6%3%

0%0%

Norway

Other

Rest of Nordics

Rest of Europe

Americas

Asia-Pacific

LTM

71%

14%

7%

5%

4%0%

Q4 2018

25%

34%

33%

75%

66%

67%

Domestic Cross Border

LTM

2008 - 2018

Q4 2018

Activity by industrySource: Mergermarket

Number of Transactions

Industry Q4 2018 LTM 2017 Avg. 2008 – 2018 Trend indicator

Automotive & Transportation 0 3 13 7

Business & Professional Services 0 8 11 9

Consumer Products 6 15 16 13

Engineering & Industrial Products 6 24 12 22

Financial Services 1 7 8 7

Government, Public sector & Organisations 0 0 1 0

Life Sciences 2 7 2 4

Oil & Gas 9 17 15 16

Power & Utilities 3 13 12 9

Real Estate, Hospitality & Construction 0 5 11 9

Retail 0 7 1 7

TMT 9 22 24 24

Travel, Leisure & Tourism 0 1 2 3

Total 36 129 128 128

Transaction Trends 1st edition 2019 | 3

5%

Transaction ArenaSource: Mergermarket

4%

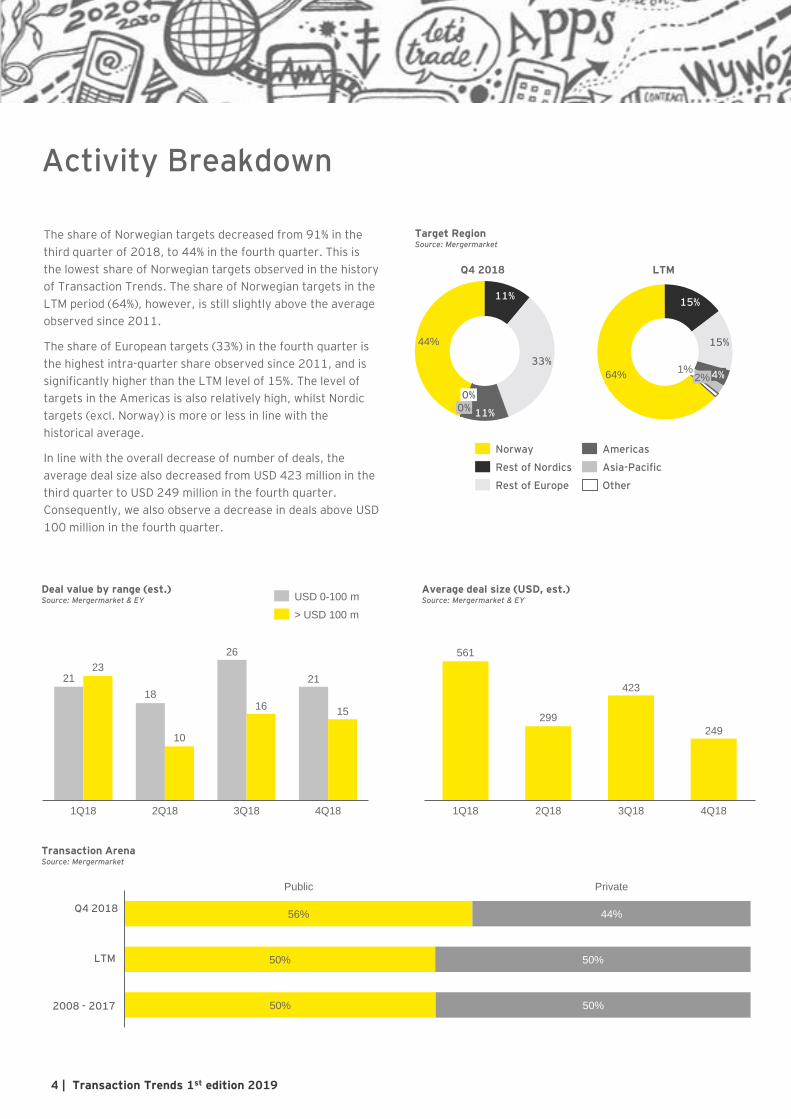

The share of Norwegian targets decreased from 91% in the

third quarter of 2018, to 44% in the fourth quarter. This is

the lowest share of Norwegian targets observed in the history

of Transaction Trends. The share of Norwegian targets in the

LTM period (64%), however, is still slightly above the average

observed since 2011.

The share of European targets (33%) in the fourth quarter is

the highest intra-quarter share observed since 2011, and is

significantly higher than the LTM level of 15%. The level of

targets in the Americas is also relatively high, whilst Nordic

targets (excl. Norway) is more or less in line with the

historical average.

In line with the overall decrease of number of deals, the

average deal size also decreased from USD 423 million in the

third quarter to USD 249 million in the fourth quarter.

Consequently, we also observe a decrease in deals above USD

100 million in the fourth quarter.

4 | Transaction Trends 1st edition 2019

Target RegionSource: Mergermarket

Activity Breakdown

44%

11%

33%

11%0%0%

Rest of Europe

Norway Americas

Rest of Nordics Asia-Pacific

Other

Q4 2018

64%

15%

15%

4%2%1%

LTM

56%

50%

50%

44%

50%

50%

PrivatePublic

LTM

2008 - 2017

Q4 2018

21

18

26

2123

10

1615

3Q181Q18 2Q18 4Q18

> USD 100 m

USD 0-100 mDeal value by range (est.) Source: Mergermarket & EY

Average deal size (USD, est.) Source: Mergermarket & EY

561

299

423

249

4Q181Q18 3Q182Q18

Public Market Update

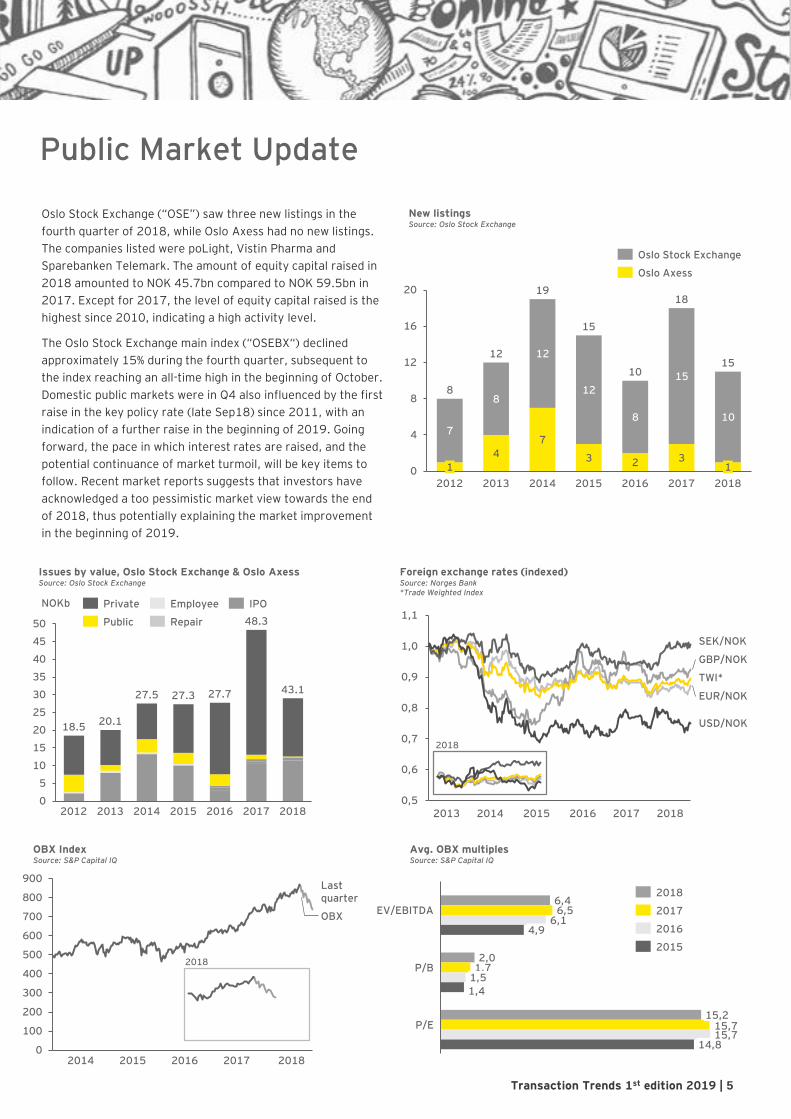

Oslo Stock Exchange (“OSE”) saw three new listings in the

fourth quarter of 2018, while Oslo Axess had no new listings.

The companies listed were poLight, Vistin Pharma and

Sparebanken Telemark. The amount of equity capital raised in

2018 amounted to NOK 45.7bn compared to NOK 59.5bn in

2017. Except for 2017, the level of equity capital raised is the

highest since 2010, indicating a high activity level.

The Oslo Stock Exchange main index (“OSEBX“) declined

approximately 15% during the fourth quarter, subsequent to

the index reaching an all-time high in the beginning of October.

Domestic public markets were in Q4 also influenced by the first

raise in the key policy rate (late Sep18) since 2011, with an

indication of a further raise in the beginning of 2019. Going

forward, the pace in which interest rates are raised, and the

potential continuance of market turmoil, will be key items to

follow. Recent market reports suggests that investors have

acknowledged a too pessimistic market view towards the end

of 2018, thus potentially explaining the market improvement

in the beginning of 2019.

New listings Source: Oslo Stock Exchange

4

7

3 2 3

7

8

12

12

8

15

10

0

4

8

12

16

20

1

2014

1

2012 20172013 2015 2016 2018

8

12

19

15

10

18

15

Oslo Stock Exchange

Oslo Axess

Issues by value, Oslo Stock Exchange & Oslo AxessSource: Oslo Stock Exchange

Avg. OBX multiples Source: S&P Capital IQ

Transaction Trends 1st edition 2019 | 5

5%4%

0

5

10

15

20

25

30

35

40

45

50

20142013

20.1

NOKb

2012 20162015 2017 2018

27.7

18.5

27.5 27.3

48.3

43.1

EmployeePrivate

RepairPublic

IPO

14,8

EV/EBITDA

2,0P/B

P/E

4,96,1

15,7

6,56,4

1,71,5

1,4

15,215,7

2018

2017

2016

2015

OBX Index Source: S&P Capital IQ

0

100

200

300

400

500

600

700

800

900Last quarter

OBX

2018

2014 2015 2016 2017 2018

Foreign exchange rates (indexed) Source: Norges Bank*Trade Weighted Index

5%4%

2013 2014 2015 2016 2017 2018

1,1

0,9

0,5

1,0

0,6

0,8

0,7

EUR/NOK

GBP/NOK

TWI*

SEK/NOK

USD/NOK

2018

Capital Confidence BarometerEY’s Global Capital Confidence Barometer is a bi-annual survey of senior executives from large companies around the world conducted by Euromoney Institutional Investor Thought Leadership (EIITP). The independent EIITP panel consists of more than 2,600 senior executives and selected EY clients and contacts, representing 14 sectors across 45 countries, including some 1,800 CEOs, CFOs and other C-level executives. The 19th Barometer provides a snapshot of our findings, measuring corporate confidence in the economic outlook and identifies boardroom trends and practices in the capital management. Click here to view the full report.

Key findings

Macroeconomic and external environmentStrong corporate earnings and open credit markets point to a continued upswing in equity markets.

Buy and integrate

Major M&A themes

Executives see the M&A cycle continuing at elevated levels. While some executives look to pause deal-making, for others M&A remains an imperative. Identification and realisation of synergies are at the centre of M&A value creation.

Trade and tariff issues are compelling some executives to pause M&A plans. PE is seen to be a major influence in the near-term deal making, and cross-border deal making is on the rise as companies seek to mitigate the negative impact from trade and tariff uncertainty, and secure market access and supply chains.

of executives see the globaleconomy as improving

of companies see corporateearnings improving

80%of executives expect the M&Amarket to improve

90%

Confidence in the M&A market remains near record highs supported by a positive economic environment that’s boosting corporate earnings. On the other hand, rising geopolitical and regulatory concerns are perceived as a growing impediment, and trade and tariff issues – from the renegotiation of NAFTA, to Brexit, and beyond – are compelling some executives to pause their own M&A plans. For deals in process, however,integration is front and centre as executives recognise the opportunity to achieve greater synergies.

of executives expect to actively pursue acquisitions in the next year – the lowest in four years

46%of executives are starting integration planning earlier

49%of companies say they achieved lower synergies than anticipatedin their most recent deal

49%

of respondents cite regulation and policy uncertainty as the biggest potential risks to deal-making

46%of executives say due to changes in trade and tariff policy, they are refocusing on cross-border M&A

20%of companies expect increasing competition for assets from PE buyers

20%

85%

Transaction Trends 1st edition 2019 | 6

Brexit

What do you think should be the preferred outcome of the UK and EU Brexit negotiations?*

Executives want familiarity, not uncertainty, over trade post-Brexit

*Refer to the below definitions.

Capital Confidence Barometer

The Norway model – the European Economic Area option: access to single market for most goods and services; power to strike free-trade deals; UK must accept free movement of people and make EU contributionsRevert to WTO rules – acceptance of EU tariffs on goods exported to single market; UK halts EU contributions and free movement of peopleThe Canada and Japan model – the Free-Trade Agreement option: tariff-free access for most goods – services not necessarily included – but custom controls in place; UK does not need to accept free movement of peopleThe UK White Paper Option – UK part of a free-trade area for goods but different rules for services; shared EU-UK customs border but with the right to diverge on tariffs and strike own FTAs; free movement of people to be replaced by mobility scheme with preferential access for EU citizensThe Switzerland model – the Economic Free-Trade Agreement option: bilateral agreement with EU affording UK select access to single market for goods but not services; UK must accept free movement of people and make specific contributionsA second referendum in the UK – Article 50 to be halted

*Definitions for the possible outcome of the UK and EU Brexit negotiations:

Brexit is the prime example of previously understood trade and tariff policy being upended. Executives are clearly signalling they would prefer a known framework to replace the existing UK/EU trading relationship.

The preferred options for respondents are ones built on familiar frameworks. Existing EU trade relationships, whether Swiss, Norwegian or Canadian, can be modelled into companies’ plans and operations.

Less favoured is the UK’s current White Paper, otherwise known as the Chequers plan. This will be an unfamiliar framework, which may pose new challenges to companies, especially where trade in goods and services is intertwined.

What executives signal they do not want is the continuation of uncertainty that a second referendum in the UK will entail or a fall-back to World Trade Organization (WTO) rules. The “hard Brexit” would be problematic for many companies, as the UK is yet to agree its own position with regard to the WTO and the conditions of its independent membership.

Q:

The Switzerland model

41% 41% 38%

The Norway model

16% 23% 27%

The Canada and Japan model

23% 17% 24%

The UK White Paper Option

Revert to WTO rules

A second referendum

Rest of World European Union UK

3%5%6%

7%9%8%

1%5%5%

Transaction Trends 1st edition 2019 | 7

Executives look to establish frameworks as the preferred outcome to UK and EU negotiations.

Transaction Support

Contact list - EY Transaction Advisory Services

Strategy and Operations

Sell-side services Vendor due diligence IPO due diligence SPA support Sell-side M&A advisory Carve-out planning Exit readiness

Complete and integrated services covering preparation to closing

EY Transaction Advisory Services

Buy-side services Financial due diligence Commercial and

operational due diligence Tax and legal due

diligence SPA support Buy-side M&A advisory Integration support

Other services Valuation and modelling Tax structuring Legal support Restructuring

Global reach and local presence with 10,000 transaction professionals

M1

60

02

no

rdic

Vegard Stevning

+47 916 83 692

Oslo

Trond Olberg

+47 997 35 554

Oslo

Bjørn Tore Foss

+47 970 25 021

Oslo

Ole Conrad Siem

+47 971 16 869

Oslo

Erik Haagensen

+47 905 66 778

Oslo

Cecilie Rasmussen

+47 984 89 439

Stavanger

Cato Rognli

+47 982 06 499

Oslo

Nils Kristian Bø

+47 971 66 567

Oslo

Kjell Stenersen

+47 982 06 678

Stavanger

Espen Norheim

+47 928 02 095

Stavanger

Merete Skage

+47 982 06 499

Bergen

Helge Fredheim

+47 913 47 741

Oslo

Njaal Arne Høyland

+47 928 81 430

Oslo

Henning Raa

+47 917 86 479

Oslo

Valuation & Business Modeling

Sigurd Garmann Tuntland

+47 901 06 610

Oslo

Corporate Finance

Transaction Tax

Transaction Trends 1st edition 2019 | 8

Marit Dokka Holthe

+47 917 14 900

Oslo

About this publication

Transaction Trends is a quarterly publication that aims to identify trends in the

Norwegian transactions market. Transactions covered in this publication are

public and private transactions announced by the 500 largest Norwegian

companies (DN500), defined as a transaction where either the buyer, target or

vendor company is a Norwegian based company. Public transactions are defined

as transactions where either the buyer, target or vendor company is listed on a

public stock exchange. All other transactions have been classified as private.

Domestic transactions are defined as transactions conducted within a national

boundary, i.e. deals involving two or more incumbent nationals, while cross

border transactions involve companies from at least two different nationalities.

Deal Value is taken as the sum of the consideration paid by the acquirer for the

equity stake in the target plus the value of the net debt in the target, where

applicable. Inclusion of net debt in the deal value will depend on the stake

acquired or the target company type.

Transaction Statistics are based on Mergermarket and EY data. Public market

data are sourced from S&P Capital IQ and Oslo Stock Exchange.

Transaction Trends is published by EY Transaction Advisory Services.

Contact information

For further enquiries, or to add your name to the mailing list for this publication,

please send an e-mail to [email protected].

About EYEY is a global leader in assurance, tax,transaction and advisory services. Theinsights and quality services we deliverhelp build trust and confidence in thecapital markets and in economies theworld over. We develop outstandingleaders who team to deliver on ourpromises to all of our stakeholders. In sodoing, we play a critical role in building abetter working world for our people, forour clients and for our communities.

EY refers to the global organization,and may refer to one or more, of themember firms of Ernst & Young GlobalLimited, each of which is a separate legalentity. Ernst & Young Global Limited, aUK company limited by guarantee, doesnot provide services to clients. For moreinformation about our organization, pleasevisit ey.com.

© 2019 EYGM Limited.

All Rights Reserved.

This material has been prepared for general

informational purposes only and is not intended to

be relied upon as accounting, tax, or other

professional advice. Please refer to your advisors

for specific advice.

ey.com

EY | Assurance | Tax | Transactions | Advisory