Embed Size (px)

Citation preview

Training Report on

Workshops conducted

for WASC

HRM, Financial Management, Procurement Management,

Monitoring & Evaluation

Developed by:

1. Mr. Hussain Saqib, Financial Management Expert

2. Brig. Uzair Ahmad, Procurement Management Expert

3. Dr. Attiq-ur-Rehman, M&E Expert

4. Syed Hussain Haider, HRM Expert

ASP RSPN,

Islamabad

2

Contents

ACRONYMS .............................................................................................................................................. 3

TRAINING REPORT ...................................................................................................................................... 5

Background of the Project ........................................................................................................................... 5

Introduction to WAPDA Administrative Staff College ................................................................................... 6

Vision of WASC ........................................................................................................................................ 6

Training Objectives .................................................................................................................................. 6

Training Conducted by ASP-RSPN Consultants for WASC / WAPDA .......................................................... 6

Training Report on Financial Management Training Modules at WASC and TOT for 48th SMC at WASC,

Islamabad ................................................................................................................................................... 7

Training Report on Human Resource Management Workshop for 47th Cadre SMC at WAPDA

Administrative Staff College, Islamabad....................................................................................................... 9

Training Report on Procurement Management to 93rd MMC at WAPDA Administrative Staff College,

Islamabad ................................................................................................................................................. 11

Training Report on Monitoring & Evaluation 93rd MMC, WAPDA Administrative Staff College, Islamabad . 13

List of Participants in MMC Workshops .................................................................................................... 14

List of Participants in SMC Workshops ..................................................................................................... 15

List of Participants in SMC Workshops ..................................................................................................... 16

Presentation on Procurement Management ................................................................................................ 17

Presentation on Financial Management...................................................................................................... 35

Presentation on Human Resource Management ......................................................................................... 62

Presentation on Monitoring and Evaluation ............................................................................................. 102

Group Photo of Human Resource Management ....................................................................................... 122

Class Room Photo of Human Resource Management Workshop ............................................................. 123

Class Room Photos of Monitoring and Evaluation Workshop .................................................................. 124

Group Photo of Procurement Management .............................................................................................. 125

3

ACRONYMS

AEDB Alternative Energy Development Board

AJK Azad Jammu Kashmir

ASP Assessment Strengthening Program

BER Baseline Evaluation Report

CBI Capacity Building Initiative

CBP Capacity Building Program

DA Daily Allowance

DISCO Distribution Companies

ERP Enterprise Resource Planning

FGD Focus Group Discussion

FM Financial Management

GENCO Generation Companies

GEPCO Gujranwala Electric Power Company

GRP Group Research Project

HESCO Hyderabad Electric Supply Company

HRM Human Resource Management

IESCO Islamabad Electric Supply Company

IRP Individual Research Project

JMC Junior Management Course

LESCO Lahore Electric Supply Company

LNA Learning Need Analysis

LUMS Lahore University of Management Sciences

MCQ Multiple Choice Questions

MEPCO Multan Electric Supply Company

MMC Middle Management Course

4

NEPRA National Electric Power Regulatory Authority

NIPA National Institute of Public Administration

NTDC National Transmission & Dispatch Company

PC Personal Computer

PESCO Peshawar Electric Supply Company

PDER Preliminary Draft Evaluation Report

PEPCO Pakistan Electric Power Company

PEPRA Public Procurement Regulatory Authority

PM Procurement Management

PPIB Private Power Infrastructure Board

PPRA Public Procurement Regulatory Authority

PSTI Public Sector Training Institutions

RSPN Rural Support Program Network

SMC Senior Management Course

T&D Training & Development

TESCO Tribal Electric Supply Company

TA Traveling Allowance

TOR Terms of Reference

UPS Uninterrupted Power Supply

WAPDA Water & Power Development Authority

WASC WAPDA Administrative Staff College

5

TRAINING REPORT

Background of the Project

Pakistan‟s local institutions, both in the public and private sector, face institutional capacity

issues and overall weaknesses in their management systems. The degree of weakness varies

across different individual organizations. However, weak institutional capacity has been a

predominant factor, thereby leading to a higher degree of risk, inadequacies in outcomes and

hampered development, despite the provision of international aid.

Assessment and Strengthening Program (ASP) – Rural Support Program Network‟s (RSPN)

capacity building role has been mandated through United States Agency for International

Development (USAID). USAID aims to implement a substantial portion of its development

portfolio through public sector partner organizations and ASP is designed to help utilize this aid

effectively by helping strengthen various financial, human resource, procurement, internal

control and absorptive capacity system in these organizations.

The current energy deficiencies within Pakistan, pose huge challenges to the country‟s growth

and economic prosperity. Given Pakistan‟s substantial hydro electrical potential there is a dire

need to help strengthen organizations such as WAPDA, which can play a tremendous role to help

improve energy deficiency. Furthermore given the fact that currently and in the past, USAID has

been WAPDA‟s active development partner, helping build WAPDA‟s capacity will further

cement this relationship. After various interactions and feedback WAPDA Administrative Staff

College (WASC) has been identified as a suitable area for intervention in capacity building

whereby the WAPDA Associated Companies become equipped with globally attuned

professional Human Resource.

Public sector employees require a continuous infusion of new skills, tools and methods in the existing public service delivery mechanism to make them more response driven to public needs.

Public sector employees not only provide key input in policy formulation but also are also

responsible for implementing such policies. Given this extraordinary role in policy formulation

and implementation, training and capacity development of public officials becomes critical and

PSTIs owe the responsibility to address emerging challenges by continuously reviewing, revising

and improving their training programs. Further to this, impact assessment of these programs in

terms of outcomes and outputs is also very important for improving the design, content and

scope of trainings.

WASC being an important PSTI plays an important role in management training and capacity

development of WAPDA‟s staff and is integral to its human resource management system.

However WASC is currently facing problems in effective service delivery due to weaknesses in

its training development, design and delivery system and lack of capacity development of its

core staff members. ASP aims to fill the existing institutional and staff related capacity gaps and

transform WASC into an important PSTI that not only helps build the capacity of WAPDA‟s

staff but that of officials related to the energy sector in general and its further utilization and

efficacy in the WAPDA associated companies.

6

Introduction to WAPDA Administrative Staff College

Purpose / Mission Statement of WAPDA Administrative Staff College

“To intensify the leadership quality of both “individual” and “client” organizations through

interactive learning models that immerse managers into a transformational experience which

fosters professional, intellectual and personal development. This is achieved through presenting

programs that challenge executives to grow as leaders, to shape powerful ideas into decisive

action-plans and to think and behave differently in a challenging business world”.

Vision of WASC

“To provide state of the art learning environment for nation building activities with

organizational success through enhanced performance skills.

To be acknowledged as the nations‟ best in the field, to eventually also earn unaffiliated (self-

recognized) status of university at masters level”

Training Objectives

There are two main objectives of the training courses held at WASC. One is to enhance the

presentation skills of the participants and other is to inculcate latest professional / management

knowledge through lectures by in house / visiting faculty.

Another important objective of the trainings is to prepare the participants for practical work to

contribute positively in solving the current confronting water and power issues of WAPDA /

PEPCO. In order to achieve this objective capacity building is conducted at all levels of training.

Currently WASC is managing following training courses for their staff: -

- Senior Management Courses - Middle Management Courses

- Junior Management Courses

- Engineering Management Post Graduate Certificate

Nearly 25 years ago, Management Courses for Senior, Middle & Junior levels were prepared

with the technical assistance of USAID training program, in consonance with the management

requirements of WAPDA. These courses went through certain modifications keeping in view, the

changing scenario and innovation of modern management techniques. At present, WASC is

linked with leading management and social science institutes of Pakistan. Suggestions received

from stakeholders i.e. PEPCO, DISCOs & WAPDA are given due consideration and

improvements are incorporated in the WASC syllabus.

WASC has 13 permanent and 10 visiting faculty members having 10-30 years field as well as

training experience. During the last five years WASC has conducted more than 97 trainings in

which approximately 2600 staff members have been trained.

Training Conducted by ASP-RSPN Consultants for WASC / WAPDA

After the approval of revised curriculum of HRM, Procurement Management, Financial Management and

M &E, the consultants executed customized trainings according to the revised curriculum at WASC for the

senior officers of Wapda and its associated companies. The trainings were conducted for 3 different

batches of SMC and MMC. The individual reports of the consultant are enclosed.

7

Training Report on Financial Management Training Modules at WASC and

TOT for 48th SMC at WASC, Islamabad

By: Mr. Hussain Saqib

As per contract deliverables, the consultants are required to deliver training modules

developed for various courses at WAPDA Administrative Staff College (WASC)

themselves in such a way that the in-house faculty can independently deliver these

modules subsequently. In line with this requirement, all the modules developed for

SMC were delivered to on-going course from 29 Dec to 31 Dec, 2014. Following

modules were delivered:

a) Corporate Environment

b) Understanding Financial Information

c) Business Planning and the Budget

d) Using financial tools for making better decisions

e) Pricing decisions and Power sector Regulatory Framework

Modules at (b) and (e) were proposed to be delivered by the experts through

extension lecture. Time allotted to Modules (a), (b) and (e) was two hours each and

time for each module at (c) and (d) was 4 hours. Proper exercises and case studies

were developed and included in Trainers’ Manual.

The modules were developed for general and specific learning objectives in order to

enable the participants to:

Understand the corporate environment including corporate governance,

company structure, objectives and accountability mechanism,

Successfully depart from legacy system of accounting and finance and

understand the impact of their day-to-day decisions of the profitability of their

respective entities,

Understand their role to assist management take decisions regarding financial

planning, financing and acquisition of assets,

Understand the role of Power sector regulator, the financial components of

electricity tariff and the guidelines for tariff-setting issued by the government,

and

Understand the system of taxation in Pakistan and the obligations of corporate

entities regarding various taxes.

8

The following methodology was proposed to be adopted for module delivery:

Pre-training methodology was restricted to course design where a wide range

of top-level executives were consulted.

During-training methodology is class-room lectures followed by discussions,

lectures by eminent expert in specialized areas and case studies. The contents

were to be delivered in an interactive format to engage the trainees, use of

multi-media presentations and development of training manuals.

Post training methodology, for improvement in the content and delivery,

includes evaluation by trainees themselves and the end-users.

The overall report can be summed up as successful and effective conduct of training

as acknowledged by the participants and WASC management and faculty. Following

is the detailed feedback:

a) GM (Training) at WAPDA House had informed to have allocated three days

slot for SMC course. The slot was originally allotted to Member (Finance) for

the legacy course. However, the consultant was requested to deliver the newly

developed course modules in this time-frame.

b) It was originally proposed that a part of Module (b) and whole of Module (e)

should be delivered by the experts in the relevant field. The consultant was

informed that he will have to deliver these modules himself because of sudden

allocation of training slot for the new course. The modules were successfully

delivered.

c) The course duration originally proposed seemed adequate.

d) The course modules in this format and with these learning objectives were

delivered for the first time. Informal feedback indicated that the modules were

relevant, interesting and useful for the target audience.

e) General and specific learning objectives were achieved more effectively than

intended.

f) Exercises and case studies engaged the participants fully in the training.

g) In the light of queries and questions, the Manual developed is being further

updated by the consultant voluntarily though it’s not a deliverable.

9

Training Report on Human Resource Management Workshop for 47th

Cadre SMC at WAPDA Administrative Staff College, Islamabad.

By: Syed Hussain Haider

Human Resource Management Training was scheduled for 47th SMC on 8-9 Sep,

2014. Coordination was made with Course Director Mr. Anwar for the subject

training 2 weeks prior. Accordingly, on 8th Sep 2014, after initial an session with

Principal/Chief Engineer, WASC, Mr. Riaz Hussain and Mr. Muhammad Yusaf Aziz

DG (Training), Mr. Anwar led the resource person to the class and introduced to all

the participants.

The faculty of WASE and Principal WASC, remained in class throughout the various

sessions. First session commenced at 10:00 hrs and it continued till 11:15 hrs.

Following were covered in first session:-

1. Personal introduction

2. Class introduction

3. Detailed Overview of HRM and its elements.

The second session commenced at 11:45 hrs. DG training, Mr. Yousaf, accompanied

me to the class. In this session, following were covered:-

1. Strategic Role of HRM

2. Model of SHRM

3. Changing Roles of HRM Mangers

4. Ulrich Model

5. Knowledge Based Economy and Learning Organizations

6. WPADA and its new role in the context of HRM

The class comprised 25 SMC participants. It was observed that class was having a

basic knowledge of HRM. The class showed a lot of interest, which was visible from

their constant questioning throughout the session. Two additional hours were taken

to complete the discussion post lunch.

In the evening, the resource person spent another 3 hours informally, addressing the

questions related to HRM and the real life issues of WAPDA and its associated

companies.

10

On the second day the workshop commenced at 9am and continued till 1:30 pm. The

topic covered were as follows:

1. HRM and Leadership Development

2. Performance Management

3. Improving Performance through Empowerment, Team work and

Communication

4. Importance of Capacity Building & Training for Wapda associated companies

5. Case Study on Training and Development – Developing a holistic training

Strategy

During and after lunch an informal Q & A session continued for over 2 additional

hours. Subsequently an HRM multiple choice paper was also developed and

provided to WASC for the SMC exam.

It was the considered opinion of all the concerned stakeholders that two days are

very less time to complete the training of Human Resource Management. Therefore,

three days would be sufficient in future to complete the training of Human Resource

management. The training ended on a note of thanks. The Principal presented a letter

of thanks to the resource person in this context and also discussed about the context

of the presentations. List of students and photos are attached with the report.

11

Training Report on Procurement Management to 93rd MMC at WAPDA

Administrative Staff College, Islamabad

By: Ozair Ahmed

Procurement Management Training was scheduled to Sr#93 MMC on 22nd January,

2015. Coordination was made with Course Director Mr. Anwar for the subject

training a day prior. Accordingly, on 22nd January 2015, after initial session with

Principal/Chief Engineer, Mr. Shah Mulk, and GM Training Headquarter WAPDA

Lahore, Mr. Anwar led the resource person to the class and introduced him.

Mr. Hassaan, the Deputy Course Director, remained in class throughout the session.

First session commenced at 10:00 hrs and it continued till 11:15 hrs. Following were

covered in first session:-

4. Personal introduction

5. Class introduction

6. Difference between procurement and purchasing

7. Essentials of PPR(Public Procurement Rules)

The second session commenced at 11:45 hrs. DG training, Mr. Yousaf, accompanied

the resource person to the class. In this session, following were covered:-

7. Detailed process of Procurement Cycle

8. Understanding the ethics of procurement code of conduct

9. Gaps in procurement

10. Discussion of case study and group work

11. A brief introduction of Draft E-strategy for procurement 2014

The class comprised 24 students including 2 female officers. It was observed that

class was having a basic knowledge of procurement. The class showed a lot of

interest, which was visible from their constant questioning throughout the session.

An additional hour was taken to complete the discussion. The session was concluded

at 14:05 hrs instead of 13:00 hrs.

Mr. Ozair Ahmed and the participants were of the view that one day is very less time

to complete the training of procurement management. Therefore, two days will be

sufficient in future to complete training of procurement management, if possible. The

12

training ended on a note of thanks. The principal presented a letter of thanks to the

resource person in this regard.

Copy of presentation attached with a group photo, which was taken at the end of the

session.

13

Training Report on Monitoring & Evaluation 93rd MMC, WAPDA

Administrative Staff College, Islamabad

By: Atiqur Rehman

Training session started at 9.45 am, today (23 January, 2015). The Day Course

Coordinator introduced the resource person in the class. There were 24 participants

available in the training room. First session lasted for about 90 m.

During initial interaction with the participants, it was realized that many of them

were not much familiar with even basic concept of M&E, hence, the session began

with basic concepts, then gradually leading to advanced concepts, tools, techniques

and application of M&E.

During first session following themes were covered:

Concepts of M&E

Need for M&E

Difference between monitoring and evaluation

M&E system of Government of Pakistan

o Positioning of M&E in generic project cycle

o PC-III proforma;

o PC-IV proforma; and

o PC-V proforma

Framework of M&E

After a break of about 20 minutes, second session commenced at 11.35. During

second session following themes were covered:

Inputs, outputs, outcomes and impact indicators

Earned Value Analysis (EVA)

Interpreting values of CV, SV, CPI and SPI

Use of M&E data in decision making

In the second session, three exercises (relating to EVA) were also introduced in the

class. The session concluded at 1.00 pm, just half an hour before the jumma prayer.

On overall basis, the both sessions went very well. The participants actively

participated in the discussions and the exercises. However, they all realized that time

available for the M&E was inadequate.

14

List of Participants in MMC Workshops

LIST

Sr.

No.

Name Designation

01 Mr.Mehar Muhammad

Yousaf Khan Sr.Engineer, PEPCO

02 Mr. Khalid Javed Khan Sr.Engineer, Mepco

03 Mr. Farooq Rashid Sr.Engineer, Hesco

04 Mr. Muhammad Akhtar

Qureshi Sr.Engineer, Hesco

05 Mr. Muhammad Umer Lodhi Sr.Engineer, Mepco

06 Mr. Mehood ul Hassan Qamar Dy. Director Computer Fesco

07 Mr. Muhammad Fiaz Awan Dy. Director Computer Pepco

08 Mr. Muhammad Naeem Ullah Sr.Engineer,Qesco

09 Mr. Tariq Mehmood Dy Manager costing Pepco

10 Malik Jamil Ahmad Addl Se(Civil) GSO NTDC Islamabad

11 Raja Tariq Nawaz Khan Addl Se(Civil) satpara Dam

12 Mr. Muhammad Azam Joya Addl Se(Civil) Wapda House

13 Mr.Safdar Ali Khan Addl Se(Civil) CDO

14 Dr. Abida Mumtaz Lady Sr. Medical Officer Lahore

15 Dr. Farhat Hussain Shah Sr. Medical Officer Rwalpindi

16 Mr. Malieha Aftab Dy.Director PR Wapda House

17 Mr. Muhammad Hassan Addl Se(Electrical) Gazi bortha

18 Mr. Muhammad Khalid Addl Se(Electrical) Gazi bortha

19 Munrwar Hussain Abbasi Xen NTDC

20 Mr. Muhammad Hayat Director Electricity Azad Kashmir

21 Mr. Muhammad Rafique

Rana Addl Manager CS Fesco

22 Mr. Abdul Qavi Sheikh Xen NTDC

23 Mr. Gul Munir Surahio Xen Hesco

24 Mr. Ashfaq Ahmad Sr.Engineer,Fesco

15

List of Participants in SMC Workshops

16

List of Participants in SMC Workshops

17

Presentation on Procurement Management

18

Slide 1

PROCUREMENT MANAGEMENT

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 2

2

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 3

What is procurement and purchasing?

Essentials of PPR

Procurement cycle

Understanding the Procurement Code of Conduct

Gaps in procurement

3

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

19

Slide 4

4

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 5 “Procurement” is the overarching function that describes the

activities and processes to acquire goods and services.

Importantly, and distinct from “purchasing”, procurement

involves the activities involved in establishing fundamental

requirements, sourcing activities such as market research and

vendor evaluation and negotiation of contracts. It can also include

the purchasing activities required to order and receive goods.

“Purchasing” refers to the process of ordering and receiving

goods and services. It is a subset of the wider procurement

process. Generally, purchasing refers to the process involved in

ordering goods such as request, approval, creation of a purchase

order record (a Purchase Order or P.O.) and the receipting of

goods.5

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 6 The process of procurement is often part of

a company's strategy because the ability to purchase

certain materials will determine if operations will continue.

A business will not be able to survive if it's price of procurement

is more than the profit it makes on selling the actual product.

6

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

20

Slide 7

ESSENTIALS OF

PUBLIC PROCUREMENT

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 8 Essentials of Public Procurement Rules

Public Procurement Regulatory Authority Ordnance 2002.

Public Procurement Rules 1/2004 amended vide Cabinet Division

in year 06, 08, 09, 10 & 11.

General Provisions

Definitions

Emergency.

Lowest evaluated bid.

Repeat orders.

Value for money.

Scope and Applicability

Proc Agency of Fed Govt.

Within or outside Pak. 8

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 9 Essentials of Public Procurement Rules

Principles of Procurement

Fair and transparent.

Value for money.

Efficient and economic.

Language

Integrity Pact

Specifications

Generic.

Shall not favor or put others at disadvantage. 9

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

21

Slide 10 Essentials of Public Procurement Rules

Advertisement

Rs .1 M to Rs 2 M (PPRA website).

Print media optional.

Rs .5 M amended in 2006 as lowest financial limit for ad on

authority website (rule 42 clause b) subject to approval of

respective board of autonomous body.

15 and 30 days.

No time limit.

Exceptions in ad. 10

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 11 Essentials of Public Procurement Rules

Pre-qualification (Rule-15)

How to determine price of pre-qualification documents?

Communication with pre-qualified and those who are not

qualified.

Communication on having credible reasons for or prima

facie evidence whether pre-qualified or not qualified.

Disqualification at any stage (Rule 17).

Blacklisting after adequate opportunity of being heard

(Rule 18). 11

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 12 Essentials of Public Procurement Rules

Bid Security (Rule-25). Not exceeding 5% of the bid price.

Bid Validity (Rule-26). As agreed. Extension not more than of

original period.

Rejection of Bid (Rule-33). Upon request, grounds for rejection

be communicated but not required to justify those grounds.

Negotiations. With lowest bidder not allowed (Rule 40). Rule

being considered for amendment.

Single Stage – One / Two Envelope Procedures.

First Stage and Second Stage. Complex contracting.

Two Stage Two Envelope Bidding. Alternate technical

proposals are possible. 12

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

22

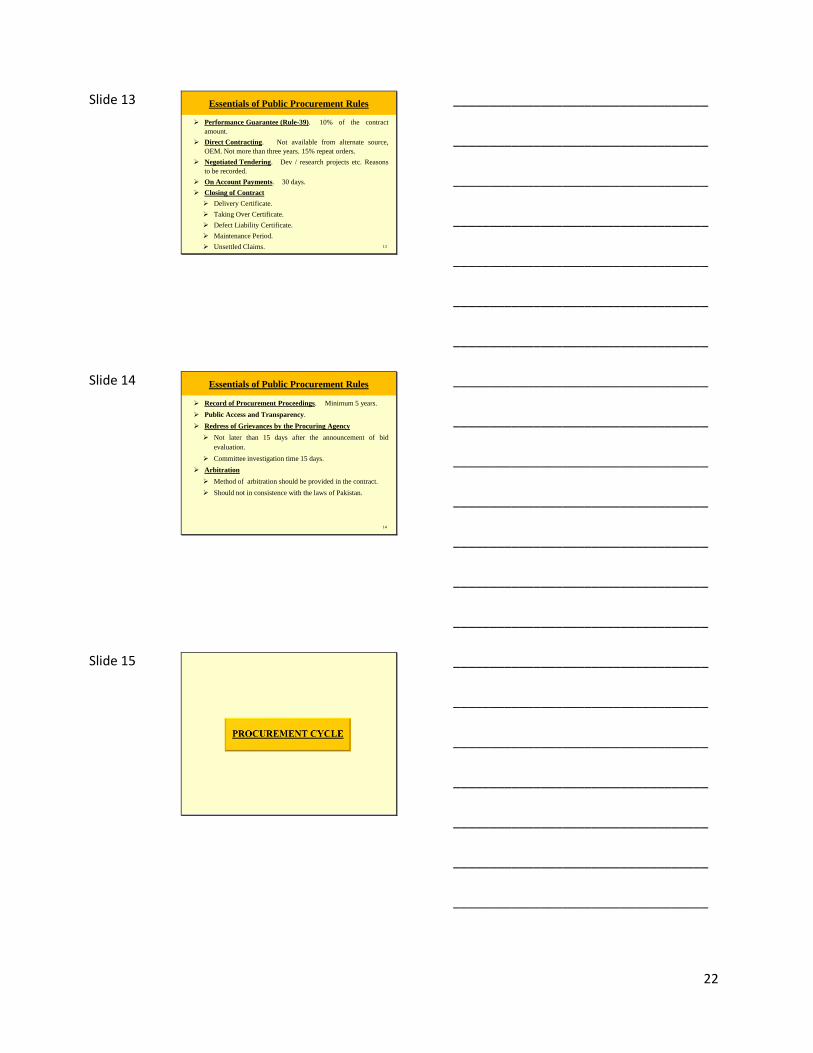

Slide 13 Essentials of Public Procurement Rules

Performance Guarantee (Rule-39). 10% of the contract

amount.

Direct Contracting. Not available from alternate source,

OEM. Not more than three years. 15% repeat orders.

Negotiated Tendering. Dev / research projects etc. Reasons

to be recorded.

On Account Payments. 30 days.

Closing of Contract

Delivery Certificate.

Taking Over Certificate.

Defect Liability Certificate.

Maintenance Period.

Unsettled Claims. 13

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 14 Essentials of Public Procurement Rules

Record of Procurement Proceedings. Minimum 5 years.

Public Access and Transparency.

Redress of Grievances by the Procuring Agency

Not later than 15 days after the announcement of bid

evaluation.

Committee investigation time 15 days.

Arbitration

Method of arbitration should be provided in the contract.

Should not in consistence with the laws of Pakistan.

14

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 15

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

23

Slide 16

16

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 17

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 18 Planning

18

Ideally, the beginning should be with the preparation of the

specifications (for goods and works) and terms of reference (for

services). This is really the beginning of the process and should

be calculated in such a manner that the completion of this stage

can be determined.

The preparation of specifications and terms of reference is crucial

and sometimes presents a bottleneck because only someone with

experience can ideally estimate the time it will take to prepare the

specifications or terms of reference of a particular requirement

due to its complexity and uniqueness.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

24

Slide 19 Planning

19

This is important because if this period is not calculated correctly

the whole plan can be thrown off. So carefully calculate this

period so that it encompasses the commencement and completion

of the specifications and terms of reference.

We know that very seldom are plans carried out strictly according

to what was foreseen and procurement plans are no exception.

This is primarily because when planning we are actually guessing

how much time things will take based on past experience and

given that there are uncertainties, any missed milestones can result

in delays in the plan.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 20

20

It’s important to keep delays in the execution of the procurement

plan to a minimum, because such delays can have an impact on

contract award and completion, which directly affects service

delivery. That’s why the periodic update of procurement plans

cannot be overstated.

Specification catalogue help in generating the demand / counter

check corrections where required. Therefore, the uniformity

prevails all over. It should be regularly updated with lead time

from demand to receipt of store.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 21

21

Placement of approximate budget against a project is essential for

procurement that’s why a word AFE (Approval for Expenditures)

is included in procurement planning.

For procurement against major / mega projects the planning has to

be at least a year ahead of actual procurement

Planning

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

25

Slide 22

Procurement

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 23 Sourcing

23

A procuring agency prior to the floating of tenders, invitation to

proposals or offers in procurement proceedings, may engage in

pre-qualification of bidders in case of services, civil works,

turnkey projects and in case of procurement of expensive and

technically complex equipment to ensure that only technically and

financially capable firms having adequate managerial capability

are invited to submit bids.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 24 Sourcing

24

A procuring agency while engaging in pre-qualification may take

into consideration the following factors, namely:-

Relevant experience and past performance.

Capabilities with respect to personnel, equipment, and plant.

Financial position.

Appropriate managerial capability.

Any other factor that a procuring agency may deem relevant,

not inconsistent with these rules.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

26

Slide 25 Sourcing

25

For pre-qualification of mega projects, elaborate criteria

has been set by PEC as well as various donors agencies.

One such example is of sample document formulized by

World Bank. The document comprised of two parts.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 26 Sourcing

26

PART 1 – PREQUALIFICATION PROCEDURES

Section I. Instructions to Applicants (ITA). This section

specifies the procedures to be followed by Applicants in the

preparation and submission of their Applications for Prequalification

(AFPs). Information is also provided on evaluation of AFPs.

Section II. Prequalification Data Sheet (PDS). This section

consists of provisions that are specific to each prequalification, and

supplements the information or requirements included in Section I,

Instructions to Applicants.

Section III. Qualification Criteria and Requirements. This

section contains the methods, criteria, and requirements to be used to

determine how Applicants shall be prequalified and later invited to

bid.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 27 Sourcing

27

Section IV. Application Forms. This section contains the forms

for the Application Submission Form and all the forms required to be

submitted with the Application.

Section V. Eligible Countries. This section states the country

eligibility policy and provides lists of ineligible countries.

PART 2. SERVICE REQUIREMENTS

Section VI. Scope of Services. This section includes a summary

description of the terms of reference of the services that are the

subject of this prequalification, as well as a summary description,

technical specifications and drawings of the system for which the

management services are being sought.

Annex: Sample Format of Invitation for Prequalification

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

27

Slide 28 Sourcing

28

Procurement Methods

Open Competitive Bidding (National and International). It should

be adopted as principal bidding method. The conditions between

national / international bidding do not change except more time is

required for international bidding.

Restricted or Limited Bidding. This method is adopted due in

special circumstances when time for the procurement is compressed.

Single Source / Propriety / Direct Contracting. It is only adopted

when only one supplier has the exclusive right to the manufacture of the

goods, carryout the work or performs the services to be procured and no

suitable alternative is available.

Request for Quotations (RFQ) / Shopping. This is also known as

“shopping” and is based on comparing price quotations obtained from

several suppliers, usually at least three, to ensure competitive prices.

Shopping method is appropriate for procuring readily available off-the-

shelf goods or standard specification commodities that are small in

value.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 29 Sourcing

29

Methods of Selection and Employing Consultants. The procurement

of consultant services is a specialized form of procurement requiring

bidding procedures and documents which are very different to those for

standard goods and works. Method of Procurement of Consultancy

Services depends upon nature, size and complexity of works, goods or

other tasks for which Services are required. Following common methods

should be used considering quality, time and other aspects:-

Quality and Cost Based Selection (QCBS)

Quality Base Selection (QBS)

Fixed Budget Selection (FBS)

Least Cost Selection (LCS)

Single Source Selection

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 30

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

28

Slide 31 Tendering

31

Company / firm name with logo if available

Tender description

Tender number

Bidding procedure

Percentage of earnest money

Tender collection start date

Tender collection end date

Tender submission date and time

Technical bid date / opening time

Commercial bid date / time to technically qualified bidder only

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 32 Tendering

32

Tender fee in form of PO / DD

Various documents required including taxation papers along with

the address and time to be deposited

Proof regarding past experience of similar works and financial

strength to accomplish the assigned task

Exact location to drop the tender

Additional notes if required

Minimum 15 days for local and 30 days for international tender

Depending upon the quantum of project it should have print /

electronic wide publicity

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 33

33

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

29

Slide 34

34

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 35 Bid Evaluation

35

Bid Opening Record

Bid Validity

Verification

Eligibility

Bid Security

Completeness of Bid

Major and Minor deviations

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 36

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

30

Slide 37 Contract Award

37

Contract review is an essential step in the contracting process. It

provides for independent written advice on the acceptability of the

procurement process undertaken and the proposed commitment of

funds by the procurement unit or officer with the appropriate

delegated authority, through contracts or purchase orders

(awarding authority).

Award is the formal decision and approval to establish a contract,

e.g. services contract or purchase order, or an LTA, with a

successful supplier, based on independent review of the

procurement process within the limits of awarding authority. The

award phase marks the:-

• Successful conclusion of the procurement process

• Starting point for contract finalization and execution

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 38

38

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 39

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

31

Slide 40 Contract Management

40

Contract Management is a process that enables both parties (the

Service and the Supplier/Contractor) to ensure that a contract fully

meets their respective obligations as efficiently and effectively as

possible, in order to deliver the business and operational

objectives required from the contract as well as providing value

for money.

A contract is a legally binding agreement between two parties, it

can be as simple as buying something from a shop – you place the

order and the shop provides the goods, or it can become

progressively more complex. Essentially the two sides to the

agreement are the offer (returned tender) and the acceptance

(preferred supplier’s submission).

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 41 Contract Management

41

There are many post-contract issues that need to be dealt with,

monitored and resolved before the contract reaches its conclusion

including:-

Contract effectiveness.

Delivery and inspections of goods

Payments to the consultant, supplier or contractor.

Performance monitoring for services and works.

Contractual disputes.

Delays in performance.

Claims for damages.

Installation and commissioning of equipment.

Acceptance of deliverables.

Takeover of construction works.

Contract closure.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 42

Understanding the

Procurement Code

of Conduct

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

32

Slide 43 Understanding the Procurement Code of Conduct

43

Revealing confidential or “inside information” either directly or

indirectly to any bidder or prospective bidder.

Discussing a procurement with any bidder or prospective bidder

outside the official rules and procedures for conducting

procurements.

Favoring or discriminating against any bidder or prospective

bidder in the drafting of technical specifications or standards or

the evaluation of bids.

Destroying, damaging, hiding, removing, or improperly changing

any official procurement document.

Accepting or requesting money, travel, meals, entertainment,

gifts, favors, discounts or anything of material value from bidders

or prospective bidders.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 44 Understanding the Procurement Code of Conduct

44

Discussing or accepting future employment with a bidder or

prospective bidder.

Requesting any other public servant or government official

representing the Company in procurement to violate the public

procurement rules or procedures.

Ignoring illegal or unethical activity by bidders or prospective

bidders, including any offer of personal inducements or rewards.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 45 Reasons / Measures for Preventing Corruption

45

Impairs economic development.

Leads to economic waste, inefficiency and reduction in

productivity.

Generates administrative inefficiency and ineffectiveness.

Promotes nepotism.

Frustrates competent and honest suppliers/contractors.

To deter corruption in procurement it is necessary to:-

Perform internal audit to monitor the process.

Institute checks in the various stages of the procurement cycle.

Require strict observance of procurement regulations.

Disqualify bidders who engage in any form of canvassing.

Penalize all those found guilty, blacklisting errant suppliers,

and to sanction staff and procurement unit members by

disciplinary action.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

33

Slide 46

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 47 Gaps in Procurement

47

Competency and availability of requisite staff

Updated procurement manuals

Regular training

Specification and its updation including lead time calculation

Timely preparation of demands

Timely availability of budget

Comprehensive tendering

Unusual delays

Political / bureaucratic pressures

Weak M&E

Delayed payments

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 48 Conclusion

48

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

34

Slide 49

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 50

50

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 51

51

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

35

Presentation on Financial Management

36

Slide 1

• F I N A N C I A L F O R E C A S T I N G

• P R E P A R A T I O N O F B U D G E T E D F I N A N C I A L S T A T E M E N T S

• C A S H B U D G E T

• M A N A G E M E N T O F W O R K I N G C A P I T A L

Budgeting and Corporate Planning

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 2

A T T H E E N D O F T H E L E C T U R E , T H E P A R T I C I P A N T S W I L L B E A B L E T O :• D E P A R T F R O M T R A D I T I O N A L C O N C E P T O F

B U D G E T I N G , • U N D E R S T A N D H O W C O R P O R A T E E N T I T I E S

P L A N F O R F U T U R E A N D A S S I G N F I N A N C I A L N U M B E R S T O T H E I R P L A N S ,

• U N D E R S T A N D H O W T O M A N A G E W O R K I N G C A P I T A L , A N D

• H O W T O P L A N C A S H R E C E I P T S A N D E X P E N D I T U R E .

Learning Objectives

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 3 Corporate Planning

Corporate Planning is:

A multi-tiered approachthat represents a company's goals, objectives andfuture work activities.

The plan expresses the strategies, milestones anddesired outcomes for the company, alongwith progress review practices and changemanagement policies.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

37

Slide 4 Corporate Planning Process

Establishing Mission and Objectives:

Top management formulate policies and strategies and communicates them downward for implementation.

Preparation of mission (purpose of existence), goals and objectives (measureable targets).

Corporate image to the customers and provides direction for the employees.

Situation Analysis

Plan to achieve objectives in accordance to its current situation. The changes in the environment provide newer ways to reach them.

The organization conducts an environmental analysis to assess available opportunities and identify its limitations and capabilities.

Two types of environmental analysis are usually conducted by organizations: external and internal. External analysis comprises macro and micro aspects.

Macro environment analysis consists of analyzing political, economic, social and technological aspects. Micro environment analysis is the study of the industry in which the firm operates or is considering operating in.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 5 Corporate Planning Process …..Cont

Internal analysis is analyzing the organization's culture, structure, image, capacity, resources and access of key staff. Also the organization's position on the experience curve is calculated. The operational efficiency and capacity are measured. The firm's patents, market share, finances and contracts are studied.

With the external and internal analysis, the organization can conduct a SWOT analysis.

Strategy Formulation and Implementation: Three generic strategies that are considered while formulating strategy are cost leadership, differentiation and focus. Only one of the three should be used for any product.

Control: The implemented strategies are continuously considered and appraised. Modifications are made from time to time to avoid deviations on the plan. The standards of performance are set, performance is monitored and necessary action is taken to guarantee success.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 6 Budgeting

A budget is an allocation of money for some purpose Company budgets give financial expression to strategy, motivate managers to achieve commonly understood

targets and provide a coherent framework for the analysis of results.

Poorly conceived or inefficient budgeting processes do not stimulate achievement of targets and are of little value for operational management

Corporate budgets limit expenditures, predict income, profits, and returns on investment a year ahead.

Budgets have evolved into tools of control and are also used as a means of determining such rewards as profit-sharing and bonuses.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

38

Slide 7 Budgetary Process

A collective process in which operating units prepare their plans in conformity with corporate goals published by top management.

Each unit plan is intended to contribute to the achievement of the corporate goals.

Unit managers prepare projections of sales, operating costs, overhead costs, and capital requirements. They calculate operating profits and returns on the investment they intend to use.

The budget itself is the projection of these values for the next period. As part of this process, each unit presents its plans and budget to a reviewing upper management panel and may, thereafter, make whatever changes result from instructions from or negotiations with the higher level.

Budget approved by BoD becomes the road-map for operations in the coming year.

Budget can be revised through periodic reviews and also serves as a measure to judge performance

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 8 Budget Types

Traditional budgeting: based on a review of historical performance and then the projection of such findings to the future with modifications. Inflation-adjusted cost trends, projected sales growth, new sales from planned new product introductions.

Zero-based budgeting: creation of a completely new budget from the ground up—as if no history existed. The operation must justify and document every item of expenditure and income anew. Brand-new operations will utilize zero-based methods.

Performance budgeting: the budget is fixed at the outset. The planning activity is to determine exactly what activities will be carried out using the allocated funds. Performance budgeting is sometimes used in the corporate setting when the advertising budget is arbitrarily set as such-and-such a percent to projected sales.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 9 Major Subsidiary Budgets

Operational budget - It forecasts and predicts yearly revenue and expenses for a business. This budget can be updated with actual figures on a monthly basis and then you can revise your figures for the year, if needed.

Cash budget - A cash budget details the amount of cash you collect and pay out. This is generally tallied on a monthly basis, but some businesses tabulate this weekly. In this budget, you track your sales and other receivables from income sources and contrast those against how much you pay to suppliers and in expenses. A positive cash flow is essential to grow your business.

Capital budget - The capital budget helps you figure out how much money you need to put in place new equipment or procedures to launch new products or increase production or services. This budget estimates the value of capital purchases you need for your business to grow and increase revenues.

Others include Sales Budget, production budget, raw material budget, labor and overhead budgets etc. in case of manufacturing units.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

39

Slide 10 Forecasting Income Statement

Major Items of Income Statement Sales: Simply multiply estimated unit sales by expected unit price for each

period. Or forecast the total market and the company’s market share in order to determine unit sales. Or use regression analysis to fit a trend line through historical data to forecast future unit sales.

Cost of Goods Sold is projected as a percentage of sales based on historical experience and/or expected direct unit production costs.

Operating Expenses: Identify categories of expense relevant to business (e.g. salaries, maintenance, depreciation,

utilities, marketing, rent, etc.). Some expense categories might be projected as a percentage of sales based on historical

experience and or budget targets. Others, such as utilities, might be based on an annual percentage increase. Depreciation expenses can be determined from depreciation schedules for existing assets

and assets to be acquired in the future. Future rental expenses might be projected based on existing rental or lease contracts.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 11 Forecasting Balance Sheet

Cash: Future end-of-period cash balances are normally projected on the cash flow statement or statement of changes in financial position.

Accounts Receivable: Once the sales forecast has been prepared on the income statement, assumptions can be made about when each month’s sales will be collected. The appropriate percentages for each business will vary depending upon such considerations as experience in collecting receivables and/or credit policy.

Inventory: Closing or ending inventory for each future balance sheet date is normally projected using the following equation: Closing Inventory = Opening Inventory + Additions to Inventory - Cost of

Goods Sold

Property: Any existing property owned by a company will be carried forward on projected future balance sheets at the historical cost of the land. If land acquisitions are planned in the future the future acquisition cost will have to be estimated and added to the value of any existing property from that point forward.

Plant and Equipment: Net value less future depreciation.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 12 Forecasting Balance Sheet (…contd)

Accounts Payable: Total purchases for the period can be converted to average purchases per day by dividing by the number of days in the period. The average purchases per day can then be multiplied by the average age of payables (based on supplier credit terms e.g. 30, 60 days etc.).

Short Term Debt: Short-term debt can be projected based on known future short term borrowing requirements. In the case of an operating line of credit, the balance owing at the end of each period can be determined form the cash budget. If the projected cash balance at the end of a period is positive, the balance owing on the line of is zero. If the projected cash balance were negative, the amount would be the projected balance owing on the line of credit.

Long-Term Debt: Projected long-term debt liability can be determined from loan amortization schedules for existing and planned future borrowings.

Shareholder’s Equity: Projected share capital will be based on any existing share capital that has been provided by investors in the company and any planned future equity infusions.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

40

Slide 13

Exercise

C A S H B U D G E T

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 14

Management of Working Capital

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 15 Working Capital

Working capital is operating liquidity available to a business, organization or other entity.

Along with fixed assets such as plant and equipment, working capital is considered a part of operating capital.

Gross working capital equals to current assets. Working capital is calculated as current assets minus current liabilities.

If current assets are less than current liabilities, an entity has a working capital deficiency, also called a working capital deficit.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

41

Slide 16 Working Capital Cycle

The working capital cycle (WCC) is the amount of time it takes to turn the net current assets and current liabilities into cash.

The longer the cycle is, the longer a business is tying up capital in its working capital without earning a return on it.

Companies strive to reduce their working capital cycle by collecting receivables quicker or sometimes stretching accounts payable.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 17 Working Capital Management

Decisions relating to working capital and short term financing are referred to as working capital management.

Managing the relationship between a firm's short-term assets and its short-term liabilities.

The goal of working capital management is to ensure that the firm is able to continue its operations and that it has sufficient cash flow to satisfy both maturing short-term debt and upcoming operational expenses.

A managerial accounting strategy focusing on maintaining efficient levels of both components of working capital, current assets and current liabilities, in respect to each other.

Working capital management ensures a company has sufficient cash flow in order to meet its short-term debt obligations and operating expenses.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 18 Factors of Working Capital Management

One measure of cash flow is provided by the cash conversion cycle—the net number of days from the outlay of cash for raw material to receiving payment from the customer.

Decisions relating to inventories, accounts receivable and payable, and cash are thus, inter-related.

Return on capital (ROC) increases with efficient working capital management.

Credit policy of the firm includes buying of raw material and selling of finished goods either in cash or on credit.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

42

Slide 19 Working Capital Management-Policies and Techniques

Cash management. Identify the cash balance which allows for the business to meet day to day expenses, but reduces cash holding costs.

Inventory management. Identify the level of inventory which allows for uninterrupted production but reduces the investment in raw materials—and minimizes reordering costs—and hence increases cash flow. Besides this, the lead times in production should be lowered to reduce Work in Process (WIP) and similarly, the Finished Goods should be kept on as low level as possible to avoid over production—see Supply chain management; Just In Time (JIT); Economic order quantity (EOQ); Economic quantity

Debtors’ management. Identify the appropriate credit policy, i.e. credit terms which will attract customers, such that any impact on cash flows and the cash conversion cycle will be offset by increased revenue and hence Return on Capital (or vice versa); see Discounts and allowances.

Short-term financing. Identify the appropriate source of financing, given the cash conversion cycle: the inventory is ideally financed by credit granted by the supplier; however, it may be necessary to utilize a bank loan (or overdraft), or to "convert debtors to cash" through "factoring".

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

43

Slide 1

CORPORATE ENVIRONMENTHOW THE COMPANIES ARE FORMED?HOW THE COMPANIES ARE GOVERNED?HOW THE COMPANIES ARE MADE ACCOUNTABLE?

H U S S A I N S AQ I B

D E C 2 9 , 2 0 1 4

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 2 LEARNING OBJECTIVES

At the end of the module, the participants will be able to understand:

• how corporate entities come into being,

• how these are organized and governed, and

• how the owners of a business exercise their control through their presence on the board of directors and audit committees.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 3 HOW THE COMPANIES ARE FORMED?

Companies are formed for varyingobjectives and by various individual andgroups. Consequently each company isestablished on a specific format withdifferent requirements of capital, businessregulations, liabilities and taxation. Aspecific form to establish a company ischosen keeping all these factors in view.

___________________________________

___________________________________

___________________________________

___________________________________