Embed Size (px)

Citation preview

A

training needs analysis and quality assurance for smes

WESTERN BALKANS AND TURKEY´S SMALL BUSINESS COMMUNITY EXPERIENCE

The European Union’s IPA Multi – beneficiary Programme

Co-funded by the

European Union

This project is implemented by

SEECEL

B training needs analysis

1

entrepreneurial learning

Training Needs Analysis and Quality Assurance for SMEs

Western Balkans and Turkey’s small business community experience

2 training needs analysis

published bySouth East European Centre for Entrepreneurial LearningSelska 217/IVZagreb, 10000Croatia

for the publisherSandra RončevićSonja Šegvić

©South East European Centre for Entrepreneurial Learning, 2015. All rights reserved.

authorsStjepan Srhoj Efka HederMaja Ljubić

ISBN 978-953-8084-03-4

Copies of this book are available at the SEECEL website at www.seecel.hr

Printed in Zagreb, Croatia 2015Printed by Magnus Gubernator d.o.o.Design & Layout by Jelenko Hercog

A CIP catalogue record for this book is available from the National and University Library in Zagreb under 000913828

3Organisational Profile

The South East European Centre for Entrepreneurial Learning (SEECEL) is a regional think tank for human capital development and lifelong entrepreneurial learning (LLEL).

SEECEL’s mission is to work on the systematic development of LLEL, on entrepreneurship as a key competence, and on the alignment of policies and practices with those of the European Union (EU) by strengthening structural regional cooperation. SEE-CEL’s vision is to build entrepreneurially literate so-cieties by strengthening entrepreneur-friendly envi-ronments and entrepreneurial mind-sets that lead to sustainable economic growth and development.

SEECEL originated from the jointly expressed in-terest of the South East European countries to work on the institutionalisation of regional dialogue and targeted cooperation in the area of lifelong entre-preneurial learning in line with EU policy essentials, particularly within the Small Business Act for Europe (SBA), under Principles 1 and 8.

SEECEL was established in 2009 in Zagreb, Croatia at the initiative of eight pre-accession countries and with the support of the Government of the Republic of Croatia, which took the lead in founding SEECEL with two co-founders: the Ministry of Economy, Labour and Entrepreneurship (today the Ministry of Entrepreneurship and Crafts) and the Croatian Cham-ber of Economy. SEECEL enjoys the full support of all its Member States: Albania, Bosnia and Herzegovina, Croatia, Kosovo*, the former Yugoslav Republic of Macedonia, Montenegro, Serbia and Turkey, and of the European Commission, in particular the Directo-rate General (DG) for Enlargement (recently renamed

the DG Neighbourhood and Enlargement Negotia-tions). SEECEL is governed by an International Steer-ing Committee composed of two representatives of each SEECEL member state – one from the ministry of education and one from the ministry in charge for the implementation of the SBA. This structure ensures policy dialogue between the world of edu-cation and economy, participation in institutional strategic development as well as full ownership of the developments achieved.

SEECEL also closely cooperates with the European Commission, especially with the Directorates General for Neighbourhood and Enlargement Negotiations; Internal Market, Industry, Entrepreneurship and SMEs (DG GROW); Education and Culture (EAC); Re-gional and Urban Policy (REGIO), and Employment, Social Affairs and Inclusion (EMPL) and organisations like the European Training Foundation (ETF), the Or-ganisation for Economic Cooperation and Develop-ment (OECD) and the Regional Cooperation Council (RCC).

SEECEL was the first institution derived from the implementation of the SBA. It shares its develop-ments with all national and regional stakeholders, European and international institutions and agen-cies, EU Member States and other interested parties. Its methodology is based on the Evidence-Based

* This designation is without prejudice to positions on status,

and is in line with UNSCR 1244 and the ICJ Opinion on the

Kosovo Declaration of independence

4 training needs analysis

Policy Making (EBPM) and the Open Method of Co-ordination (OMC). SEECEL’s operations are either in-tegral or complementary part of the following key policy documents: South East Europe 2020 Strategy (SEE 2020 Strategy), the EU Strategy for the Danube Region (EUSDR), the EU Strategy for the Adriatic and Ionian Region (EUSAIR) and the Europe 2020 Strategy.

SEECEL is financially supported primarily by the EU through the Multi-beneficiary Programmes under the Instrument for Pre-Accession Assistance (IPA), the national budget of Croatia, through the Ministry of Entrepreneurship and Crafts and SEECEL member states. In 2011, SEECEL expanded its activities to sup-port the development of women’s entrepreneurship.

Although still quite a young institution, SEECEL has achieved international recognition and awards from the Knowledge Economy Network, the European Commission, the RCC, the European Project Awards, and just recently “Creators for Centuries”, includ-ing the European Commission’s European Enterprise Promotion Award (EEPA) as National Winners in 2014. SEECEL has also been recognised by the European Commission as the best practice for good conceptual solutions in the field of entrepreneurial learning and strategic regional cooperation. As such, SEECEL’s work is featured in numerous European Commission reports and SEECEL participates in high-level work-ing groups on entrepreneurial learning in Europe.

5Organisational Profile

Small and medium sized enterprises (SMEs) are seen as engine for job creation and the overall eco-nomic and social development. The largest number of enterprises in the economy are SMEs, and they contribute significantly in terms of providing a wide variety of jobs in SEECEL member states. At the same time they face unique challenges in the business environment. By their nature, SMEs have more lim-ited human, material and financial resources when compared to large enterprises, so in order to survive and grow in an economically challenging world, SMEs need to be able to change and adapt as inter-nal and external challenges arise.

The development of human capital is increas-ingly seen as key to ensuring competitive advan-tage for long-term labour market productivity and for integrated, inclusive, smart and sustainable growth and economic development. Education and training systems obviously play a crucial role in the increase of human capital, and they should remain flexible and respond accurately to the demands of the labour market. However, the development of human capital within SME’s through up-skilling of entrepreneurs and their employees is of equal importance to foster their competitiveness. And SME skills can neither be equated with skills-needs on the labour market in general nor with the skills needs of large enterprises. Namely, due to specifi-cities in terms of their environment, strategy, struc-ture, technology and culture, SMEs differ markedly from large enterprises with regard to their training and development needs and their resources and capabilities (Roy and Raymond, 2008).

Despite the importance of training for SMEs, insuf-ficient participation in training by SMEs is a Europe-wide problem, as noted by the European Commis-sion:

“Today more than ever before, the skills, motivation and activation of employees are crucial precondi-tions for the sustainable success, productivity and innovation of enterprises. However, the situation of SMEs with regard to training is characterised by a paradox. On the one hand, continuous training and lifelong learning (both for workers and mana-gerial staff) are regarded as crucial elements of competitiveness against the backdrop of globali-sation. On the other hand however, statistics show that continuous training and qualification are less likely to be available to employees working in SMEs than to those in large enterprises.” EC DG Employment, Social Affairs and Equal Opportunities: SME Training Guide, June 2009, p. 3

In SEECEL member states, the development of SME competences has consistently been highlighted in national SME strategies, programmes and action plans among the countries’ economic priorities. However, training and development planning is not always approached in a structured or strategic manner and is rather initiated in response to spe-cific problems. This can be particularly valid for SMEs where the lack of a training function combined with the scarcity of resources often results in ‘ad hoc’ ap-proach that enterprises opt for in the provision of

6 training needs analysis

trainings. Strategic planning can identify the ‘criti-cal success factors’ and specific human capital that enable SMEs to gain competitive advantage in the market (Healy, Ryan, Stewart and Stewart, 2002).

Accurate and relevant data on SME training needs at the national level present the foundation for adopting strategic approach to developing hu-man capital among SMEs. For this reason, SEECEL has been working since 2010 on developing tools for analysing specific training needs of SMEs in the countries of South East Europe and Turkey. In this publication, which presents the second generation of the regional Training Needs Analysis (TNA), the focus is on micro and small enterprises in three sectors: the food and beverage processing and tourism sectors (both of which were identified in the SEE 2020 Strategy as high-potential sectors for the region) and the manufacturing sector.

This publication presents the results and the recommended process which we call the Training Navigation System. It is based on comprehensive regional research (TNA) and current best practice, and is derived from engagement with micro and small enterprises from the three selected sectors. The process is adaptable to a range of scenarios and can be scaled up to include different stakeholders and roles.

A well supported and carefully planned Train-ing Navigation System with the TNA as a baseline is a significant step towards providing SME’s human capital development in the SEECEL member state that is strategic, coordinated, timely, cost-effective and based on real needs.

7Foreword

This document is the result of a broad and com-plex SEET effort to promote economic cooperation and foster the competitiveness of SMEs through the Training Needs Analysis as a key element of inte-grated, inclusive, smart and sustainable growth. It has been a team endeavour.

We would like to thank the governments of:

• Albania, • Bosnia and Herzegovina, • Croatia, • Kosovo, • the former Yugoslav Republic of Macedonia, • Montenegro, • Serbia, • Turkey.

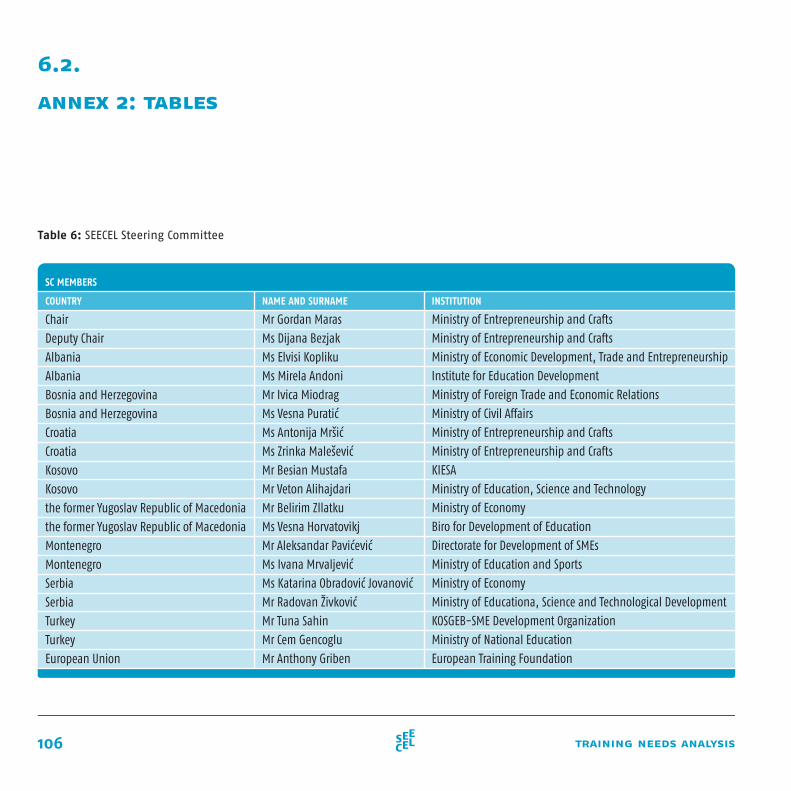

We would like to express our gratitude to SEECEL member states, represented by their respective ministry of education and ministry in charge of SBA (Table 6, in Annex), for their full support and coop-eration, without which this step forward would not have been possible.

We would especially like to thank the European Commission and the Government of the Republic of Croatia represented by the Ministry of Entrepreneur-ship and Crafts for their financial support.

These developments would not have been pos-sible without the contribution, expertise and knowledge of national and international experts. We would therefore like to thank the experts and institutions that form the SEECEL Development and Advisory Network for Enterprises Training (DANET). We

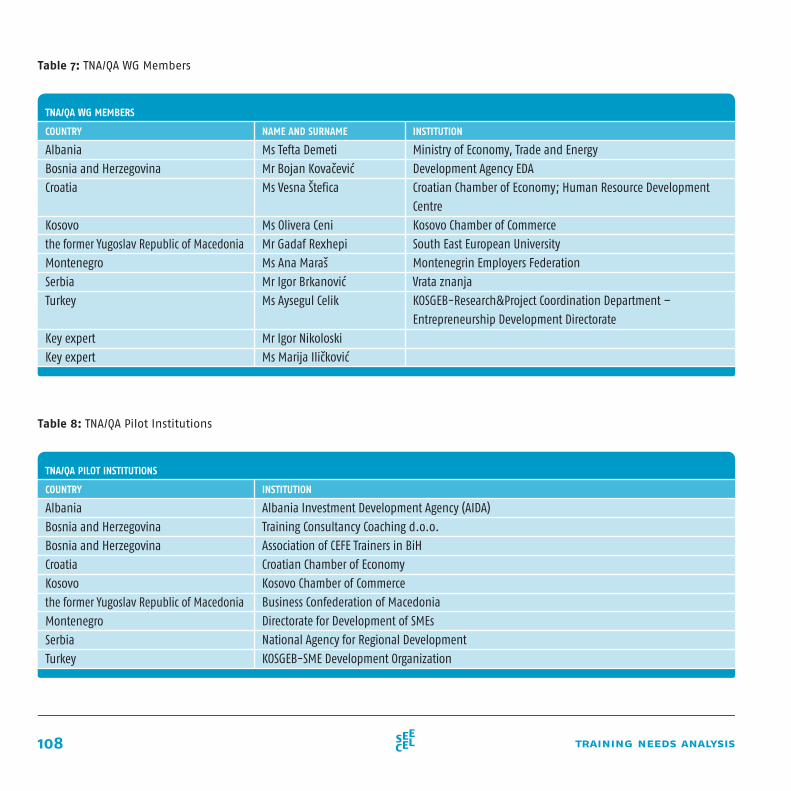

express our gratitude and appreciation to all DANET members for contributing their knowledge and ex-perience: Albanian Investment Development Agency, Training Consultancy Coaching Ltd from Bosnia and Herzegovina, Association of CEFE Trainers in Bosnia and Herzegovina, Croatian Chamber of Economy, Ko-sovo Chamber of Commerce, Business Confederation of Macedonia, Directorate for Development of SMEs, National Agency for Regional Development from Serbia and KOSGEB from Turkey, as well as Ms Tefta Demeti, Ms Sonila Hysi, Ms Edita Perić, Ms Aida Dolić, Mr Zoran Kulundžija, Ms Lenka Radišić, Ms Tajana Kesić Šapić, Ms Vesna Štefica, Ms Olivera Ceni, Ms Gabriela Kostovska Bogoeska, Mr Gadaf Rexhepi, Mr Mile Boškov, Ms Anđela Pušonjić, Ms Ana Maraš, Mr Igor Brkanović, Mr Vladimir Jovanović and Ms Aysegul Celik. Our special thanks go to our two international Key Experts who led and coordinated the work of the working group, Ms Marija Iličković and Mr Igor Nikoloski (Table 7 and Table 8, in Annex).

Finally, we would like to extend our deepest gratitude and acknowledge the invaluable contri-butions of all entrepreneurs and employees who participated in the survey.

8 training needs analysis

BSO – Business Support Organisation COP – Community of Practice DANET - Development and Advisory Network for Enterprises

Training EL – Entrepreneurial Learning EU – European Union EC – European Commission ETF – European Training Foundation FBP – Food and Beverages Processing ICT – Information and Communication Technology LLEL – Lifelong Entrepreneurial Learning NACE – ‘Nomenclature Generale des Activites Economiques

dans I`Union Europeenne’ (General Name for Economic Activities in the European Union)

OECD – Organisation for Economic Development and Cooperation

OMC – Open Method of Coordination RCC – Regional Cooperation Council SBA – The Small Business Act for Europe SEE – South East Europe SEECEL – South East European Centre for Entrepreneurial Learning SEET – South East Europe and Turkey SME – Small and Medium Enterprises TNA – Training Needs Analysis TNAS – Training Needs Analysis System WETNAS – Women Entrepreneurs Training Needs Analysis System WG – Working Group

list of abbreviations

9Table of Contents

contents

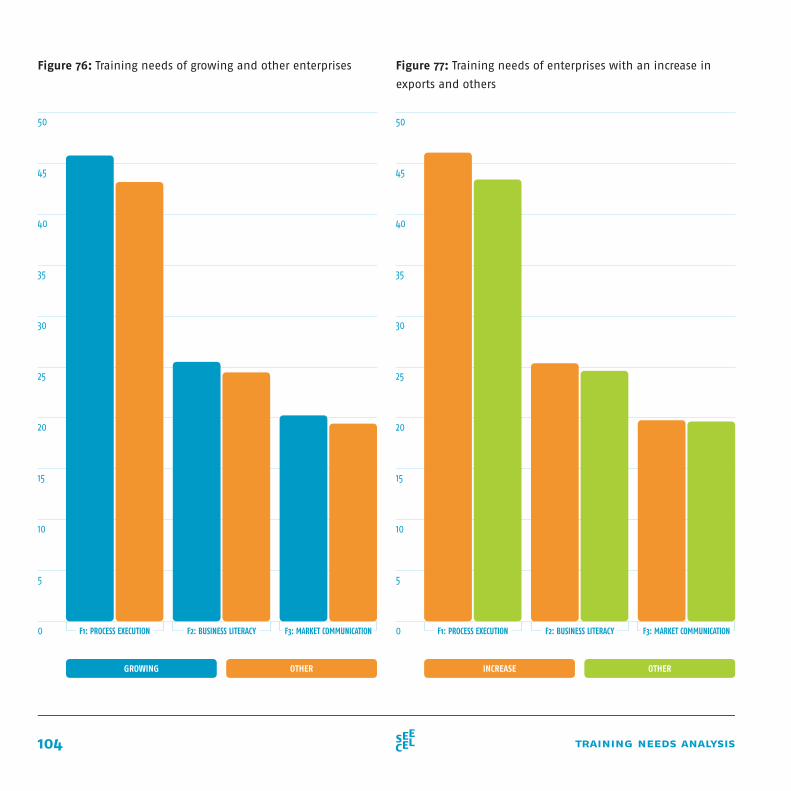

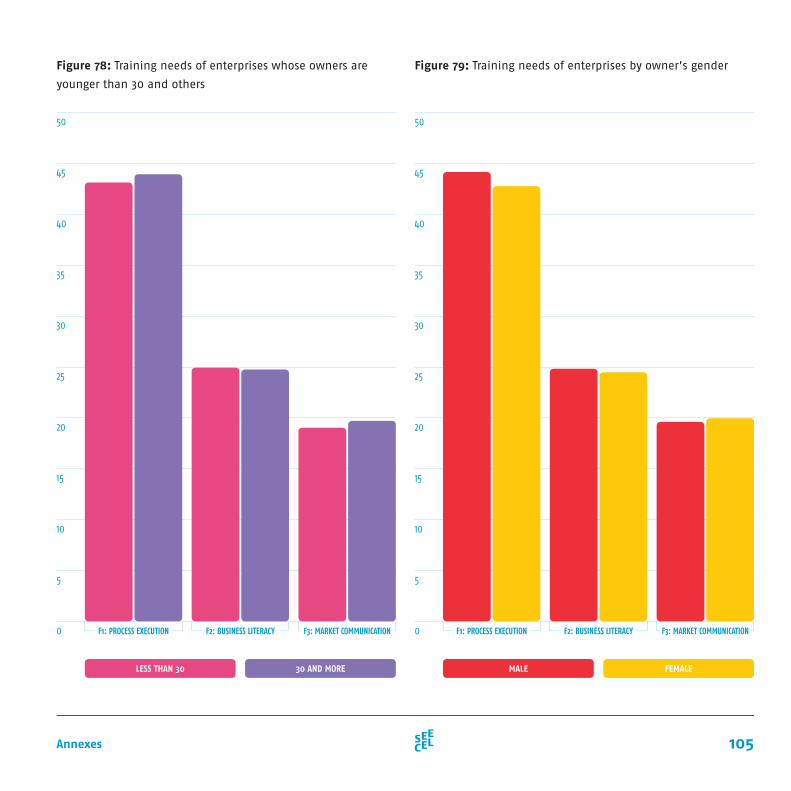

3.9. Regression Results 54 3.10. Focus on Job Creators 57 3.10.1. Growing Enterprises 58 3.10.2. Enterprises with Increase in Exports 60 3.10.3. Enterprises Owned by Entrepreneurs

Younger than 30 62 3.10.4. Female-owned Enterprises 64 3.11. Developing the Model of Human

Capital Intervention 66 3.11.1. Training Navigation System 72

4. quality assurance criteria framework 75

5. way forward 81

6. annexes: 84 6.1. Annex 1: Figures 85 6.2. Annex 2: Tables 106 6.3. Annex 3: Questionnaire 121

7. indexes: 145 7.1. Index of Figures 146 7.2. Index of Tables 149

8. bibliography 150

Organisational Profile 2 Foreword 4 Acknowledgements 6 List of Abbreviations 8

1. development context 10 1.1. EU Policy Framework 11 1.2. State of Play in the Region 13

2. tna - methodology and objectives 16

3. findings 21 3.1. Information on the Sample 23 3.2. Perceived Business Environment and

Business Trends in Enterprises 30 3.3. Access to Finance 32 3.4. Networking and Business Partnership 33 3.5. Human Resources and Training 35 3.6. Challenges Influencing Small Business

Community 36 3.7. Trainings Needs of the Small Business

Community 45 3.8. Organisational Benefits Acquired

Through Training 50

10 training needs analysis

11Development Context

The recent global economic developments presented an opportunity for Europe to grow stronger, and promote smart, sustainable and inclusive growth. In order to take advantage of this opportunity, the Eu-rope 2020 Strategy outlined steps which set the tar-gets and key priorities and initiatives. Recognizing that Europe can “count on the talent and creativity of [its] people”, the EU 2020 strategy places a great focus on the development of Europe’s human capi-tal. In particular, it stipulates that promoting smart growth driven by knowledge and innovation ne-cessitates reforms which should improve the qual-ity of education and training, and reforms should contribute to “ensuring that innovative ideas can be turned into new products and services that create growth, quality jobs and help address European and global societal challenges. But, to succeed, this must be combined with entrepreneurship, finance and a focus on user needs and market opportunities.”

In the development of human capital, special fo-cus should be put on the development of a lifelong learning system that supports individuals through

education and training – as defined in the Edu-cation and Training 2020 strategic framework. The basis for this system in Europe is a set of eight key competences that define knowledge, skills and at-titudes necessary for successful life in the knowledge society.

The implementation of the lifelong learning pro-cess was further elaborated in the European Council conclusions on the role of education and training in the implementation of the ‘Europe 2020’ strategy. The conclusion emphasises that: “education and training have a fundamental role to play in achiev-ing the ‘Europe 2020’ objectives of smart, sustain-able and inclusive growth, notably by equip-ping citizens with the skills and competences which the European economy and European society need in order to remain competitive and innovative”. In particular, the ‘An Agenda for new skills and jobs’ initiative “should improve the identification of training needs, increase the labour market relevance of education and training, facilitate individuals’ ac-cess to lifelong learning opportunities and guidance,

1.1.

eu policy framework

12 training needs analysis

and ensure smooth transitions between the world of education, training and employment.” The ini-tiative concludes that: “there is a need to ensure a better long-term match between skills supply and labour market demand.” In ensuring better match between training and labour market needs, busi-nesses should be actively involved in “forecasting skills needs, through an employers survey tool and qualitative studies on the skills needs of business, notably SMEs”.

EU 2020 Strategy and other relevant documents recognize the impact that entrepreneurship has on economy and society and consequently support hu-man capital development in the SME sector as a key driver of competitiveness. This message was further reinforced with the Entrepreneurship 2020 Action Plan. Developing the human capital of SMEs has its roots in a range of policy documents, with the most recent and relevant, the SBA. The SBA builds on Com-mission and Member States policy achievements and creates a new policy framework that integrates the existing SME policy instruments. SBA also promotes

growth of SMEs by helping them tackle the remain-ing problems which hamper their development. The SBA is the policy framework for SMEs for EU Mem-ber States and pre-accession countries alike, and it is composed of ten principles with indicators. The eighth principle focuses on “Enterprise skills and in-novation” and one of its objectives is the establish-ment of a “national policy and support framework to ensure a better fit between supply and demand for training in small enterprises.” As outlined by the principle, it is important to focus on the develop-ment of TNA, which is defined as the “identification of training requirements and the most cost-effective means of meeting those requirements.”

13Development Context

SMEs - the backbone of economies in pre-accession countries - are a priority in all policy documents. As a part of their accession process, countries are fully implementing the SBA for Europe and regularly reporting to the European Commission. Their par-ticipation in the process began in 2003 when they signed the agreement to implement the European Charter for Small Enterprises. The countries took a step further and requested a more strategic approach towards reporting on the implementation of the Eu-ropean Charter for Small Enterprises for the Western Balkans. Following that request, policy indicators were developed and are used as a planning instru-ment for pre-accession countries in their EU acces-sion process. Indicators, otherwise known as the SME Policy Index, were developed jointly by the European Commission, European Training Foundation, SEECEL, European Bank for Reconstruction and Development and OECD, together with National SBA coordinators.

This strong cooperation on a regional level has further resulted in the signing of “A Charter for En-trepreneurial Learning: the Keystone for Growth and

Jobs” (SEECEL, 2012a) – signed at the Entrepreneur-ship-Education Regional Summit, hosted by the Min-istry of Entrepreneurship and Crafts and the SEECEL, in Zagreb on 23 October 2012. The Charter builds on an existing co-operation framework provided by the SEECEL, where each country’s education and economy/entrepreneurship ministries are represented. By sign-ing the Charter, the participating parties reconfirmed their full support to the systematic development of the life-long entrepreneurial learning as a key com-petence through continued policy improvement, good practise sharing and regional cooperation.

All SEECEL member states are making progress towards the development of a national TNA as part of their efforts to develop more efficient national policies and support systems for the training of SMEs following the principles of the SBA. Respecting the OMC and peer learning principle, all SEECEL member states decided to cooperate on system development in this field, through SEECEL activities for the region as a whole that supports national developments. In the development of a regional TNA, it was very important

1.2.

state of play in the region

14 training needs analysis

to account for all differences between SEECEL member states (for example, territory size, population, natural resources, etc.) as this does not present an obstacle to the development but enriches the process.

The key macro-regional and regional strategies relevant to South East Europe and Turkey include an emphasis on human capital development and on developing SME skills. The EU Strategy for the Danube Region covers human capital development through its “Building Prosperity” pillar, whilst in the EU Strategy for the Adriatic Ionian Region a cross-cutting theme of “Strengthening R&D, Innovation and SMEs” is present across four key pillars of the strategy. Furthermore, with the SEE 2020 Strategy– Jobs and Prosperity in a European Perspective, the governments of Albania, Bosnia and Herzegovina, Kosovo, the former Yugoslav Republic of Macedonia, Montenegro and Serbia have embraced the policy approach required to attain the levels of socioeco-nomic growth necessary to improve the prosperity of all its citizens and to facilitate eventual integration with the EU. The Smart Growth Pillar and its Dimen-sion D – Education and Competences within the SEE 2020 Strategy looks at ways to ‘ensure education and training systems better meets economic and labour market needs (and provide learners with labour market relevant skills)’ (RCC, 2013, p. 19).

Pre-accession countries are facing the conse-quences of the global economic crisis that are es-pecially unfavourable for SMEs. In response to the challenges posed by the crisis, countries defined human capital development as one of the key ar-eas for fostering the competitiveness of SMEs which

would represent the basis for sustainable growth. A systematic approach to developing human capi-tal requires the identification of training needs of SMEs through TNA. The New Skills for News Jobs in the Western Balkans position paper highlights that there is an identified need for a region-wide all-encompassing analysis (supply-demand; compe-tences-gaps; current-future needs). Hence, the benefits of a regional TNA is that it identifies the similarities, differences and training needs of SMEs on the SEE level, all of which benefits the home and host countries alike. In order to ensure the success of international SME operations, SMEs need specific training and advisory services.

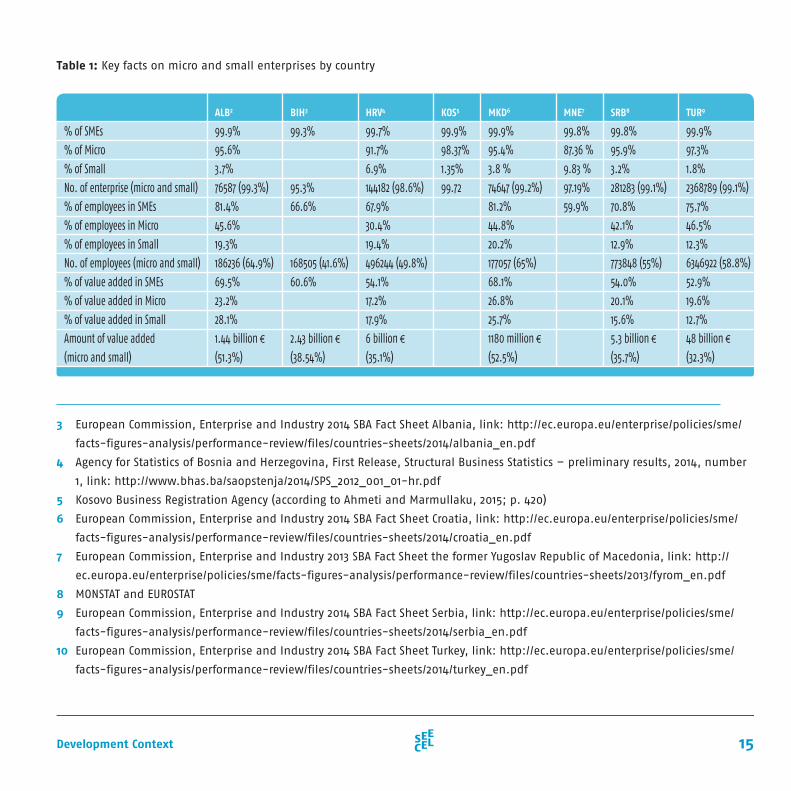

As it is visible from the Table 1, Bosnia and Her-zegovina has the lowest percentage of micro and small enterprises out of total number of enterprises amounting to 95.3%. On the other side, Albania has the highest percentage of micro and small enter-prises, 99.3%. Looking at the total number of micro and small enterprises it is obvious that Turkey takes the lead with 2,368,789 enterprises1. Whilst the exact number of enterprises was not available for Monte-negro, previous studies point to less than 24,0002 of micro and small enterprises.

1 European Commission, Enterprise and Industry 2014 SBA

Fact Sheet Turkey, link: http://ec.europa.eu/enterprise/poli-

cies/sme/facts-figures-analysis/performance-review/files/

countries-sheets/2014/turkey_en.pdf

2 Statistical Office, Montenegro, August 2012

15Development Context

Table 1: Key facts on micro and small enterprises by country

3 European Commission, Enterprise and Industry 2014 SBA Fact Sheet Albania, link: http://ec.europa.eu/enterprise/policies/sme/

facts-figures-analysis/performance-review/files/countries-sheets/2014/albania_en.pdf

4 Agency for Statistics of Bosnia and Herzegovina, First Release, Structural Business Statistics – preliminary results, 2014, number

1, link: http://www.bhas.ba/saopstenja/2014/SPS_2012_001_01-hr.pdf

5 Kosovo Business Registration Agency (according to Ahmeti and Marmullaku, 2015; p. 420)

6 European Commission, Enterprise and Industry 2014 SBA Fact Sheet Croatia, link: http://ec.europa.eu/enterprise/policies/sme/

facts-figures-analysis/performance-review/files/countries-sheets/2014/croatia_en.pdf

7 European Commission, Enterprise and Industry 2013 SBA Fact Sheet the former Yugoslav Republic of Macedonia, link: http://

ec.europa.eu/enterprise/policies/sme/facts-figures-analysis/performance-review/files/countries-sheets/2013/fyrom_en.pdf

8 MONSTAT and EUROSTAT

9 European Commission, Enterprise and Industry 2014 SBA Fact Sheet Serbia, link: http://ec.europa.eu/enterprise/policies/sme/

facts-figures-analysis/performance-review/files/countries-sheets/2014/serbia_en.pdf

10 European Commission, Enterprise and Industry 2014 SBA Fact Sheet Turkey, link: http://ec.europa.eu/enterprise/policies/sme/

facts-figures-analysis/performance-review/files/countries-sheets/2014/turkey_en.pdf

ALB2 BIH3 HRV4 KOS5 MKD6 MNE7 SRB8 TUR9

% of SMEs

% of Micro

% of Small

No. of enterprise (micro and small)

% of employees in SMEs

% of employees in Micro

% of employees in Small

No. of employees (micro and small)

% of value added in SMEs

% of value added in Micro

% of value added in Small

Amount of value added

(micro and small)

99.9%

95.6%

3.7%

76587 (99.3%)

81.4%

45.6%

19.3%

186236 (64.9%)

69.5%

23.2%

28.1%

1.44 billion €

(51.3%)

99.3%

95.3%

66.6%

168505 (41.6%)

60.6%

2.43 billion €

(38.54%)

99.7%

91.7%

6.9%

144182 (98.6%)

67.9%

30.4%

19.4%

496244 (49.8%)

54.1%

17.2%

17.9%

6 billion €

(35.1%)

99.9%

98.37%

1.35%

99.72

99.9%

95.4%

3.8 %

74647 (99.2%)

81.2%

44.8%

20.2%

177057 (65%)

68.1%

26.8%

25.7%

1180 million €

(52.5%)

99.8%

87.36 %

9.83 %

97.19%

59.9%

99.8%

95.9%

3.2%

281283 (99.1%)

70.8%

42.1%

12.9%

773848 (55%)

54.0%

20.1%

15.6%

5.3 billion €

(35.7%)

99.9%

97.3%

1.8%

2368789 (99.1%)

75.7%

46.5%

12.3%

6346922 (58.8%)

52.9%

19.6%

12.7%

48 billion €

(32.3%)

16 training needs analysis

17TNA - Methodology and Objectives

The second generation of the TNA instrument is de-veloped by the working group (WG) representatives via the Community of Practice and in vivo discus-sions during the WG meetings in Zagreb, Croatia on 22 October 2013 and in Ankara, Turkey from 3 to 5 March 2014. The TNA instrument has underpinnings in national and EU policy documents, theoretical knowledge, previous SEECEL experience with devel-oping TNA (SEECEL, 2012) and WETNAS (SEECEL, 2014) as well as national expertise of the WG members. The instrument’s main objective is to identify the training needs and challenges of micro and small enterprises from three strategic sectors from eight countries (Albania, Bosnia and Herzegovina, Croatia, Kosovo, the former Yugoslav Republic of Macedonia, Montenegro, Serbia and Turkey). Three strategic sec-tors were predefined, two out of three originally coming from the SEE 2020 strategy and the third sec-tor was agreed upon by consensus of the national experts during the TNA/QA WG in Zagreb. The target sectors were tourism, manufacturing and food and beverages processing (FBP) sector.

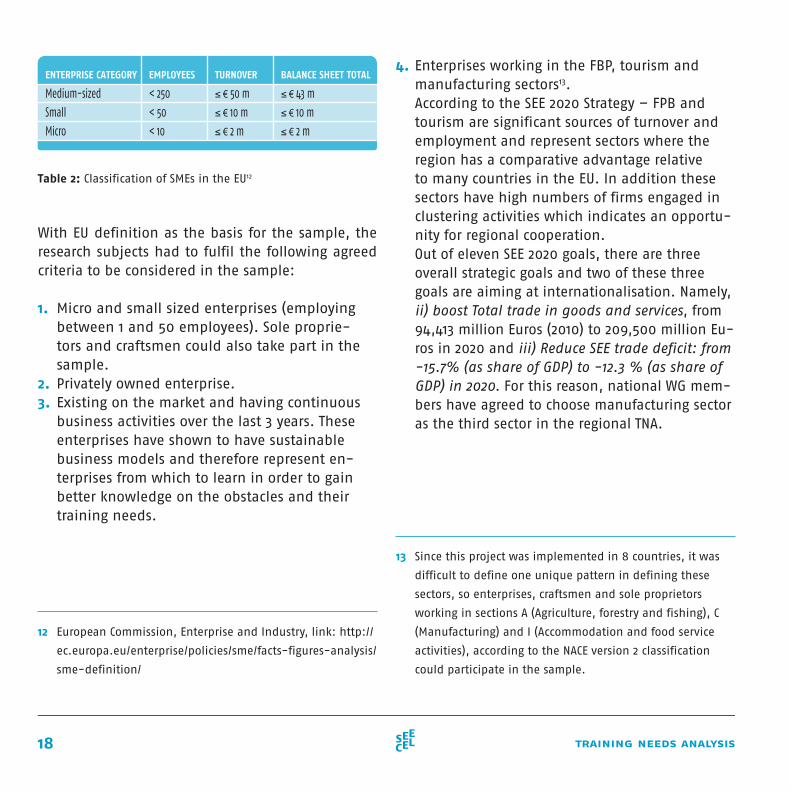

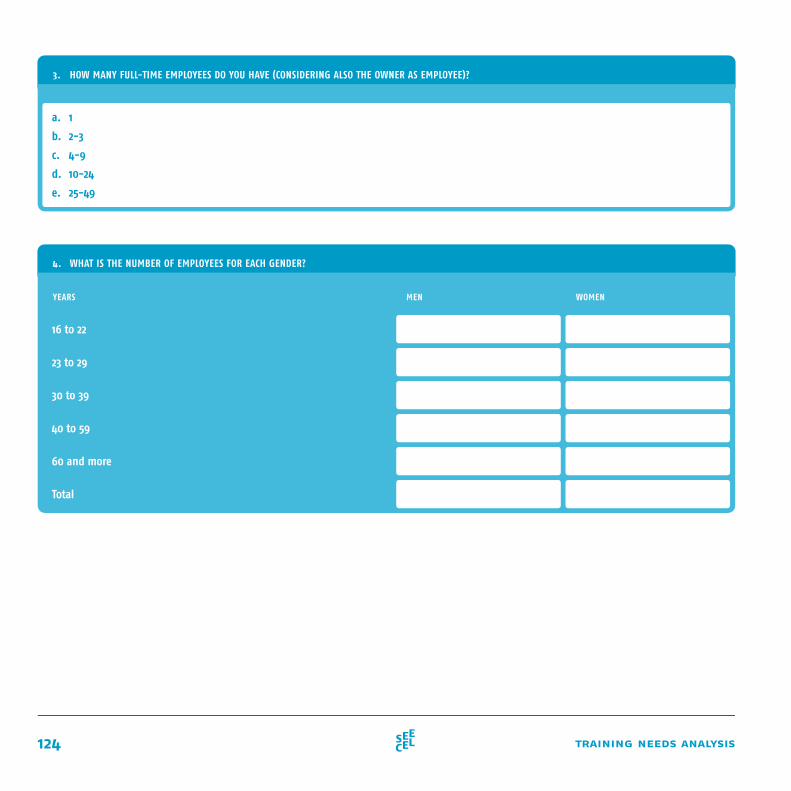

Since more than 95%11 of the total number of en-terprises in all SEECEL Member States are micro and small enterprises, the main selection criterion for the survey enterprises was the number of employ-ees. Furthermore, the EU definition in regards to the number of employees is applied in all SEECEL coun-tries, however, the same definition is not applied in all SEECEL countries when it comes to the turnover or balance sheet. According to the EU definition, micro enterprises employ up to 10 and small enterprises up to 50 employees (Table 2).

11 Based on the SBA Fact Sheets, see Table 1

18 training needs analysis

4. Enterprises working in the FBP, tourism and manufacturing sectors13. According to the SEE 2020 Strategy – FPB and tourism are significant sources of turnover and employment and represent sectors where the region has a comparative advantage relative to many countries in the EU. In addition these sectors have high numbers of firms engaged in clustering activities which indicates an opportu-nity for regional cooperation. Out of eleven SEE 2020 goals, there are three overall strategic goals and two of these three goals are aiming at internationalisation. Namely, ii) boost Total trade in goods and services, from 94,413 million Euros (2010) to 209,500 million Eu-ros in 2020 and iii) Reduce SEE trade deficit: from -15.7% (as share of GDP) to -12.3 % (as share of GDP) in 2020. For this reason, national WG mem-bers have agreed to choose manufacturing sector as the third sector in the regional TNA.

13 Since this project was implemented in 8 countries, it was

difficult to define one unique pattern in defining these

sectors, so enterprises, craftsmen and sole proprietors

working in sections A (Agriculture, forestry and fishing), C

(Manufacturing) and I (Accommodation and food service

activities), according to the NACE version 2 classification

could participate in the sample.

Table 2: Classification of SMEs in the EU12

With EU definition as the basis for the sample, the research subjects had to fulfil the following agreed criteria to be considered in the sample:

1. Micro and small sized enterprises (employing

between 1 and 50 employees). Sole proprie-tors and craftsmen could also take part in the sample.

2. Privately owned enterprise.3. Existing on the market and having continuous

business activities over the last 3 years. These enterprises have shown to have sustainable business models and therefore represent en-terprises from which to learn in order to gain better knowledge on the obstacles and their training needs.

12 European Commission, Enterprise and Industry, link: http://

ec.europa.eu/enterprise/policies/sme/facts-figures-analysis/

sme-definition/

EMPLOYEES ENTERPRISE CATEGORY TURNOVER BALANCE SHEET TOTAL

Medium-sized

Small

Micro

< 250

< 50

< 10

≤ € 50 m

≤ € 10 m

≤ € 2 m

≤ € 43 m

≤ € 10 m

≤ € 2 m

19TNA - Methodology and Objectives

Previously mentioned criteria enable the analysis to reach the data for specific target group and thus assist in making a tailor made analysis. The ques-tionnaire was developed by the DANET members. Building on the previous TNA experience, the brain-storming method was used during the in vivo WGs in order to cover as many human capital-related questions and training sub areas as possible. In the time between the WGs, the delphi method was used via the CoP in order to get further details, new ideas and improvements of the questionnaire. Once the methodology and the questionnaire were finalised, the procedures on the implementation of next ac-tivities were also defined. Given that an indirect goal is to increase the overall digital competencies, it was decided to use online system to conduct the research. Along this line, an electronic online system for data collection has been created, and in order to participate in the survey, entrepreneurs14 had to visit the website where the questionnaire was posted. After the English version of the platform and questionnaire was agreed and approved by all the parties, the WG members translated the question-naire and necessary website features. The platform and the questionnaire were therefore translated into all languages of the participating countries. Before the full scale implementation, online ques-tionnaire was tested and subsequently standardised

14 The word entrepreneur is used in this study synonymously

for both male and female entrepreneurs

and objectivised. The overall process of implemen-tation of the survey was supported and supervised by the predefined business support organisation (BSO) in each country. Each organisation has received 1000 unique survey codes that were disseminated among the enterprises so they could participate in the project. Before accessing the questionnaire, the entrepreneurs had to enter the given code by the or-ganisation. Once the code was accepted the process of answering the questions could begin. Introducing the codes for each enterprise provided additional information to the BSOs regarding the enterprises’ participation rate in the survey per country, but it also reduced the risks of misusing the survey. Ad-ditionally, respondents’ unintentional mistakes were minimised because the system did not allow successful completion of the survey if some of the fields were empty or if there was a logical mismatch between two answers.

The questionnaire is composed of five chapters:

A. General and Personal Information, showing insight in general information about the enter-prises’ sectors of operation and their background and experience;

B. Networking and business partnership, gather-ing information regarding the networking and cooperation and collaboration activities and possibilities;

C. Enterprise Information, collecting data regarding the business performance, demographic struc-ture and market success;

D. Access to finance, gathering information regard-

20 training needs analysis

ing the perception of availability and the us-age of the basic and the alternative financial instruments, as well as regarding the sources of information; and

E. Human resources and training is the main part of the survey, collecting data regarding the car-ried on activities, plans and budget for train-ing, education and skills development, for both managerial and non-managerial staff.

Questions were analysed by using descriptive sta-tistics, factorial analysis (Principal Axes Factoring), inferential statistics (one-way ANOVA) and hierarchi-cal multiple regression. The factor analysis examines the interdependency among a large number of vari-ables, and it tries to explain these variables through a small number of common characteristics. Thus, the purpose of the factor analysis is to summarise a large pool of information into a small number of common characteristics with minimum loss of information, allowing a better understanding among variables. On the other hand, regression can be explained as a statistical measure that attempts to determine the strength of the relationship between one dependent variable and a series of other independent variables. The factor analysis and regression are featured in the section 3, Findings.

Having in mind the differences in countries’ size and the number of enterprises (ranging from ap-

proximately 24,00015 in Montenegro to 2 386 92116 in Turkey) respectively, the sample size for this ac-tion has been set to a minimum of 300 fully filled in questionnaires per country. The sample size was decided based on previous TNA experiences (SEECEL, 2012), as well as WETNAS experience (SEECEL, 2014) where BSOs collected 200 questionnaires filled in by women entrepreneurs only. Therefore, it was reasonable that the BSOs will be able to collect the target sample of 300 micro and small enterprises in tourism, manufacturing and FBP sectors.

15 Analysis of number and structure of business entities in

Montenegro for the second quarter 2012 year, Statistics Of-

fice, Montenegro, August 2012

16 European Commission, Enterprise and Industry 2014 SBA

Fact Sheet Turkey, link: http://ec.europa.eu/enterprise/poli-

cies/sme/facts-figures-analysis/performance-review/files/

countries-sheets/2014/turkey_en.pdf

21Findings

22 training needs analysis

In the following section of the publication, all de-tailed statistical explanations are given in blue boxes. The explanations are extracted because the target audience of the publication comprises a wide range of stakeholders. As such, the goal was to write up the findings in a more popular manner.

23Findings

The sample used in this large scale study included 2557 participants from eight countries, with more than 300 participants from each country (Figure 1). All the enterprises participating in the survey are relatively new enterprises, established in the last 6 years (Figure 42, in Annex), whilst 330 out of 2557 enterprises were established three years ago. It was expected that enterprises younger than three years would not be presented, as one of the prerequisites for the survey participation was for an enterprise to be active a minimum of three years.

The sample is characterized with relatively propor-tionate number of participants from enterprises that belong to each of the three sectors of operation: (1) food products, beverages and herbs production and processing (FBP); (2) manufacturing; and (3) tour-ism and complementary services. Turkey and Kosovo have somewhat larger number of participants from the manufacturing enterprises (Figure 2). Turkey is represented by the most manufacturing enterprises which is in line with the strong manufacturing sector in their economy. In general, participants from the

two specific areas of manufacturing (manufacture of wood and paper products and printing and manu-facture of textiles, apparel, leather, footwear and related products) filled somewhat larger number of the overall questionnaires. The most questionnaires from the manufacture of wood and paper products and printing were submitted in Kosovo, Montenegro and Turkey (Figure 43, in Annex), whilst the most questionnaires from the manufacture of textiles, apparel, leather, footwear and related products were submitted in Albania, Turkey and the former Yugoslav Republic of Macedonia. In every country, the number of questionnaires from the tourism sec-tor differs according to the specific tourism areas. For example, enterprises in the catering and restaurant business filled the largest number of questionnaires within the tourism sector in Bosnia and Herzego-vina and Albania. In Croatia, hotels filled the largest number of questionnaires (Figure 44, in Annex).

3.1.

information on the sample

24 training needs analysis

Figure 1: Study participants by country Figure 2: Participants from different sector of operation by

country

360

350

340

330

320

310

300

290

280 TURSRBMNEMKDKOS*BIH HRVALB

100

90

80

70

60

50

40

30

20

10

0

TOURISM AND COMPLEMENTARY SERVICES

MANUFACTURING

FOOD PRODUCTS, BEVERAGES AND HERBS PRODUCTION AND PROCESSING

TURSRBMNEMKDKOS*BIH HRVALB

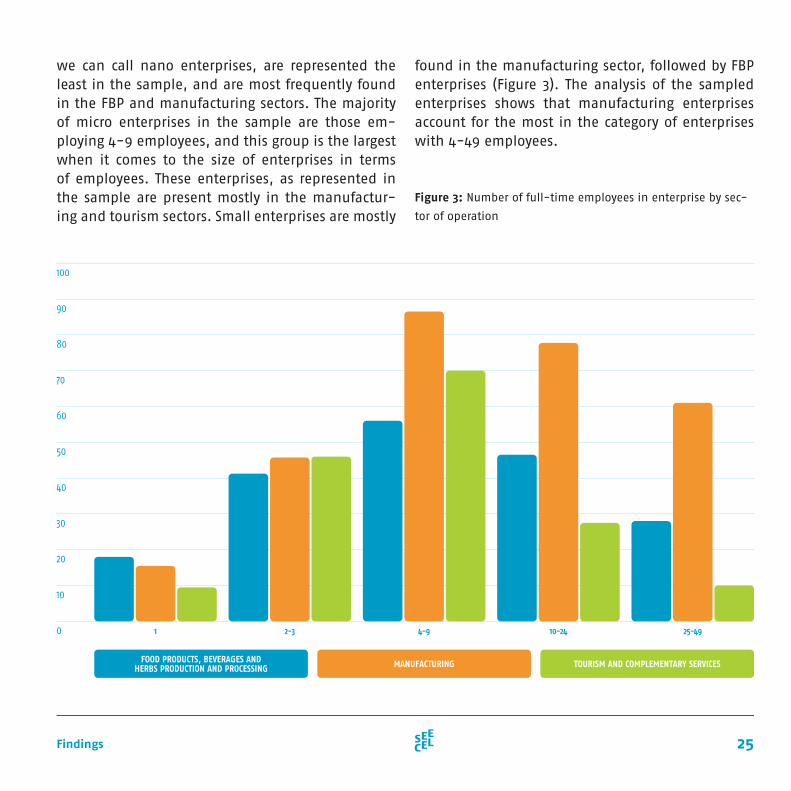

One of the key determinants of the size of an enter-prise is often the number of employees17. Building

17 As depicted in the Section 2, this is not the only criterion for the size of an enterprise, however, it is often used in literature because it is difficult to collect precise financial information.

on the previously explained disaggregation of en-terprises into micro, small and medium sized enter-prise, Figure 3 provides an analysis of the size of en-terprise in the sample by further breakdown of the number of employees. Following the structures of the eight economies, the sample has a higher pro-portion of micro when compared to small enterpris-es. Enterprises with one full time employee, which

25Findings

we can call nano enterprises, are represented the least in the sample, and are most frequently found in the FBP and manufacturing sectors. The majority of micro enterprises in the sample are those em-ploying 4-9 employees, and this group is the largest when it comes to the size of enterprises in terms of employees. These enterprises, as represented in the sample are present mostly in the manufactur-ing and tourism sectors. Small enterprises are mostly

Figure 3: Number of full-time employees in enterprise by sec-

tor of operation

found in the manufacturing sector, followed by FBP enterprises (Figure 3). The analysis of the sampled enterprises shows that manufacturing enterprises account for the most in the category of enterprises with 4-49 employees.

100

90

80

70

60

50

40

30

20

10

0 1 2-3 4-9 10-24 25-49

FOOD PRODUCTS, BEVERAGES AND HERBS PRODUCTION AND PROCESSING MANUFACTURING TOURISM AND COMPLEMENTARY SERVICES

26 training needs analysis

Employees aged up to 39 years old jointly represent 67.38% of the overall employees in the sample. However, when we analyse the groups as given in the Figure 4, employees aged 40-59 represents the second largest category (28.71%), after employees aged 30-39. Women older than 60 years belong to the least frequent group of employees in the sam-pled regional small business community, whilst women aged 30-39 are represented the most. The proportion of female employees is increasing stead-ily from the group of employees 16-22 year old to the group 23-29 and peaks in the age group 30-39, after Figure 4: Employees by age and gender

3500

3000

2500

2000

1500

1000

500

0

which it starts declining in the age group 40-59, de-clining further in the category 60 and older. Men are overrepresented in the category 16-22 years old, and this overrepresentation decreases in the category 23-29, declining further in the category 30-39 years old. Afterwards, ratio of women decreases in the category 40-59 reaching its lowest point in the category of 60 and older.

FEMALE

MALE

16-22 23-29 30-39 40-49 60 AND MORE

27Findings

2500

2000

1500

1000

500

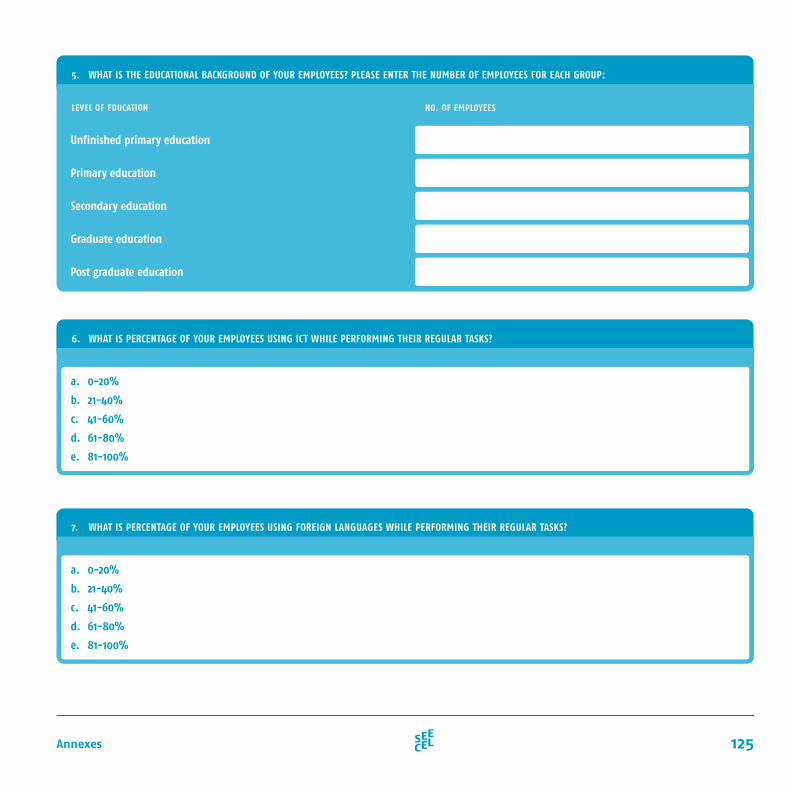

0 PRIMARY EDUCATIONUNFINISHED PRIMARY EDUCATION SECONDARY EDUCATION GRADUATE EDUCATION POST GRADUATE EDUCATION

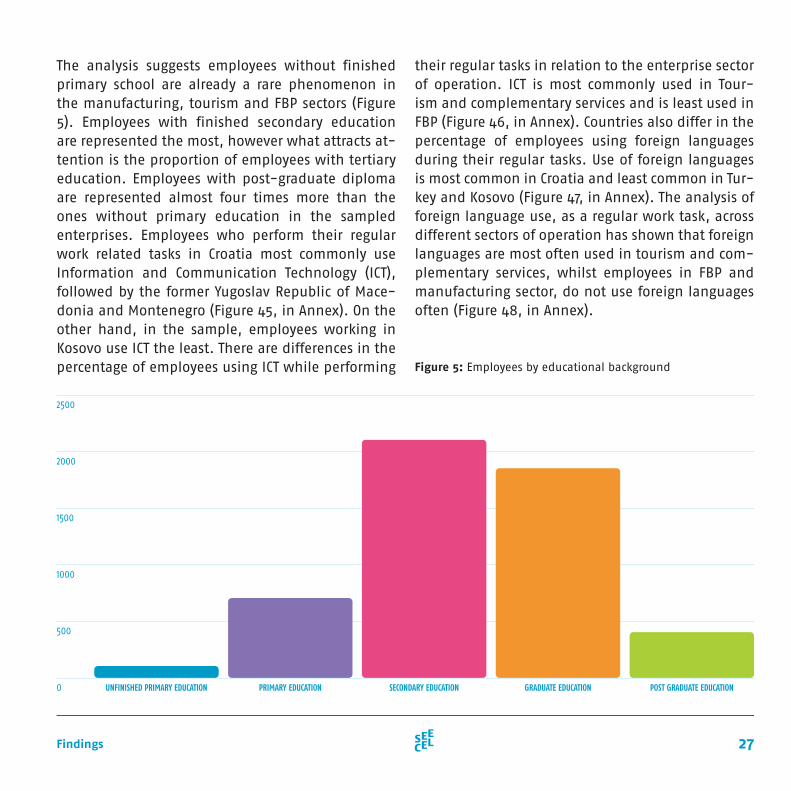

The analysis suggests employees without finished primary school are already a rare phenomenon in the manufacturing, tourism and FBP sectors (Figure 5). Employees with finished secondary education are represented the most, however what attracts at-tention is the proportion of employees with tertiary education. Employees with post-graduate diploma are represented almost four times more than the ones without primary education in the sampled enterprises. Employees who perform their regular work related tasks in Croatia most commonly use Information and Communication Technology (ICT), followed by the former Yugoslav Republic of Mace-donia and Montenegro (Figure 45, in Annex). On the other hand, in the sample, employees working in Kosovo use ICT the least. There are differences in the percentage of employees using ICT while performing

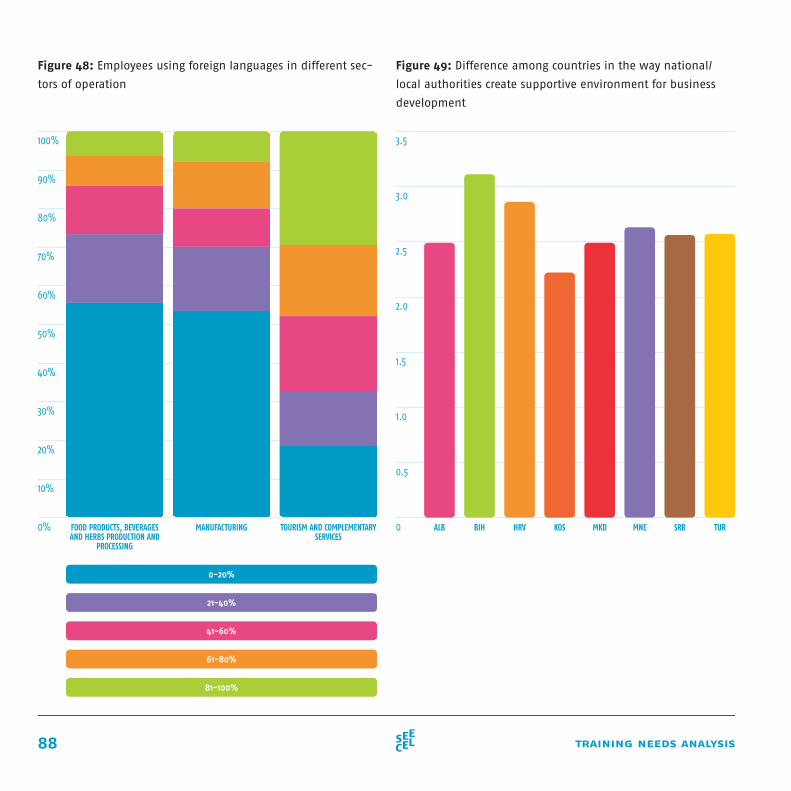

their regular tasks in relation to the enterprise sector of operation. ICT is most commonly used in Tour-ism and complementary services and is least used in FBP (Figure 46, in Annex). Countries also differ in the percentage of employees using foreign languages during their regular tasks. Use of foreign languages is most common in Croatia and least common in Tur-key and Kosovo (Figure 47, in Annex). The analysis of foreign language use, as a regular work task, across different sectors of operation has shown that foreign languages are most often used in tourism and com-plementary services, whilst employees in FBP and manufacturing sector, do not use foreign languages often (Figure 48, in Annex).

Figure 5: Employees by educational background

28 training needs analysis

Shifting from employees to employers, most of the enterprise owners have completed tertiary educa-tion, one third of the enterprise owners who hold a graduate degree have completed economic studies, whilst two thirds come from other disciplines (Figure 6). Entrepreneurs who finished only primary educa-tion are rare, representing less than 4% of the total sample. A considerable portion of entrepreneurs have secondary education as their highest education acquired, whereby more than 60% of entrepreneurs have finished VET schools, whilst others have final-ised general studies e.g. gymnasiums. Figure 6: Owner’s educational background

PRIMARYEDUCATION

SECONDARYEDUCATION

GRADUATEEDUCATION

POST GRADUATEEDUCATION

VOCATIONAL TECHNICAL STUDIES

GENERALSTUDIES

ECONOMICSTUDIES

ECONOMICSTUDIES

NON ECONOMICSTUDIES

NON ECONOMICSTUDIES

900

800

700

600

500

400

300

200

100

0

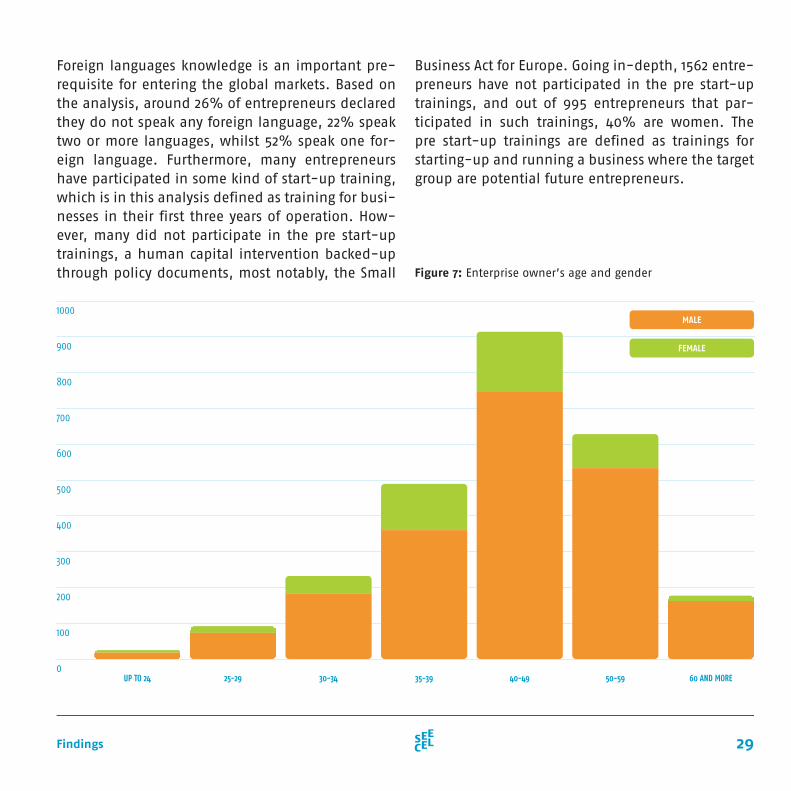

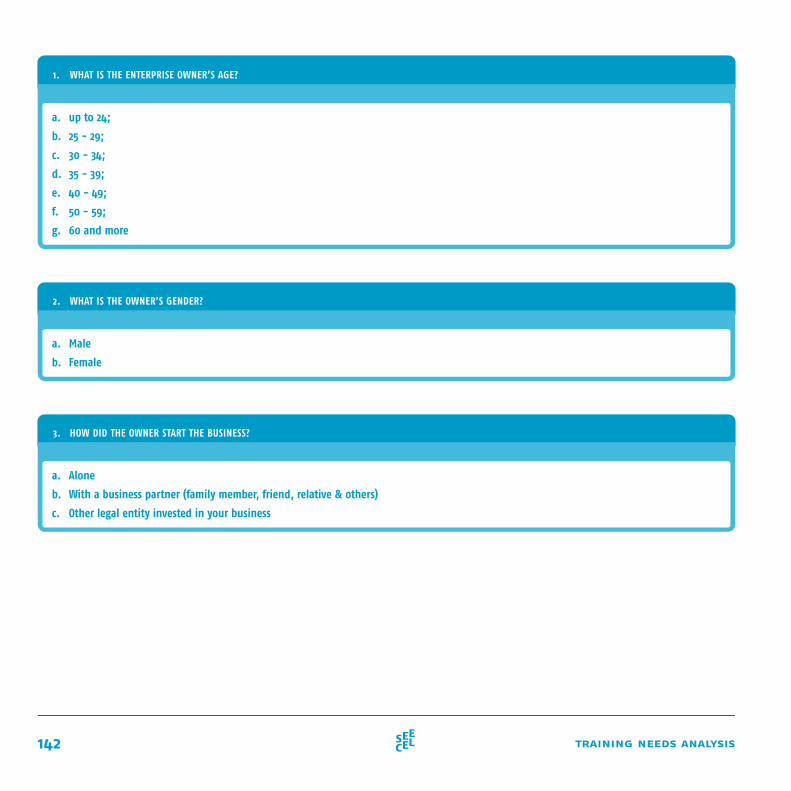

Most of the enterprise owners from the sample are men, and they most frequently belong to the age categories 40-49 and 50-59 (Figure 7). The analysis also shows that enterprises are established by sole effort of one entrepreneur, rather than in partner-ship. Deeper analysis shows that for 66% of entre-preneurs their current enterprise is their first entre-preneurial experience, for 25% second and for the rest of them third or subsequent experience.

29Findings

Foreign languages knowledge is an important pre-requisite for entering the global markets. Based on the analysis, around 26% of entrepreneurs declared they do not speak any foreign language, 22% speak two or more languages, whilst 52% speak one for-eign language. Furthermore, many entrepreneurs have participated in some kind of start-up training, which is in this analysis defined as training for busi-nesses in their first three years of operation. How-ever, many did not participate in the pre start-up trainings, a human capital intervention backed-up through policy documents, most notably, the Small

Business Act for Europe. Going in-depth, 1562 entre-preneurs have not participated in the pre start-up trainings, and out of 995 entrepreneurs that par-ticipated in such trainings, 40% are women. The pre start-up trainings are defined as trainings for starting-up and running a business where the target group are potential future entrepreneurs.

1000

900

800

700

600

500

400

300

200

100

0

Figure 7: Enterprise owner’s age and gender

UP TO 24 25-29 30-34 35-39 40-49 50-59 60 AND MORE

FEMALE

MALE

30 training needs analysis

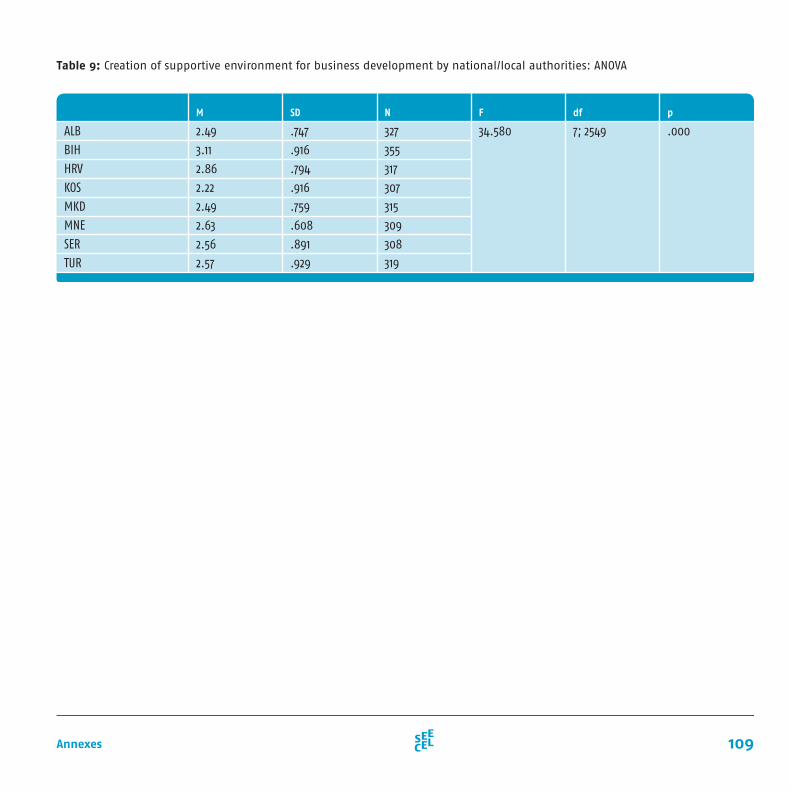

Perceived business support and the difference among countries are given in the Figure 49 (in An-nex). The question revolved around perceived way national/local authorities create supportive envi-ronment for business development. The environ-ment for business development is evaluated on the 4 point scale, where lower score suggests higher support for business development. The highest perceived support given to business development is experienced by enterprises in Kosovo, Albania and the former Yugoslav Republic of Macedonia. In ad-dition, the analysis of variance (Table 9, in Annex) showed differences between countries, F(7,2549) = 34.580, p = 0.000. Business support is perceived as the least conducive in Bosnia and Herzegovina and Croatia.

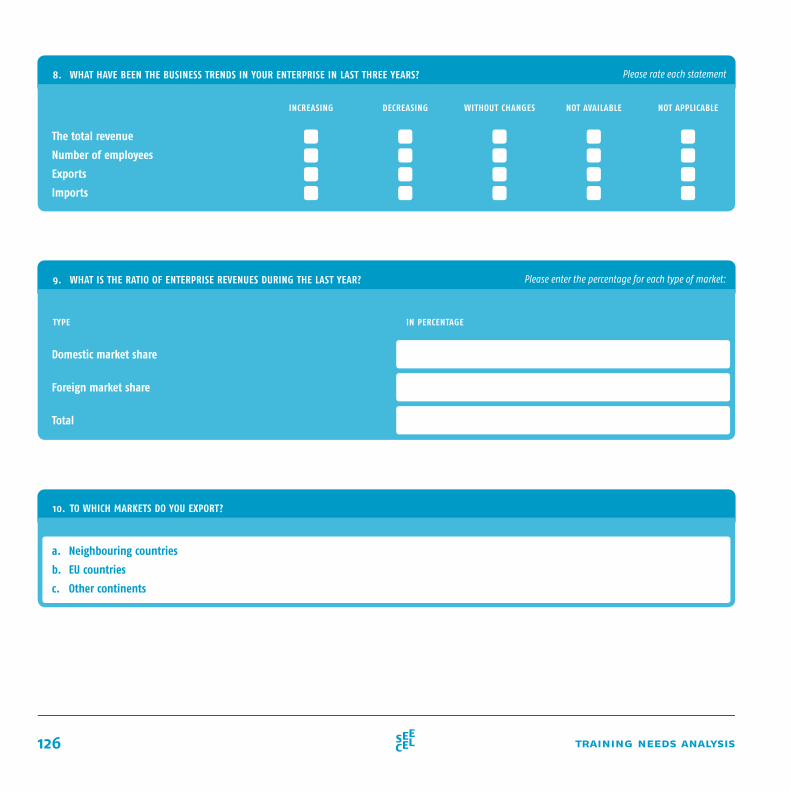

In order to determine the business trends of the participating enterprises, the following parameters were analysed: total revenue, number of employ-ees, export and imports linked to the country of enterprise origin as well as the main sector of op-eration. An analysis of variance showed differences

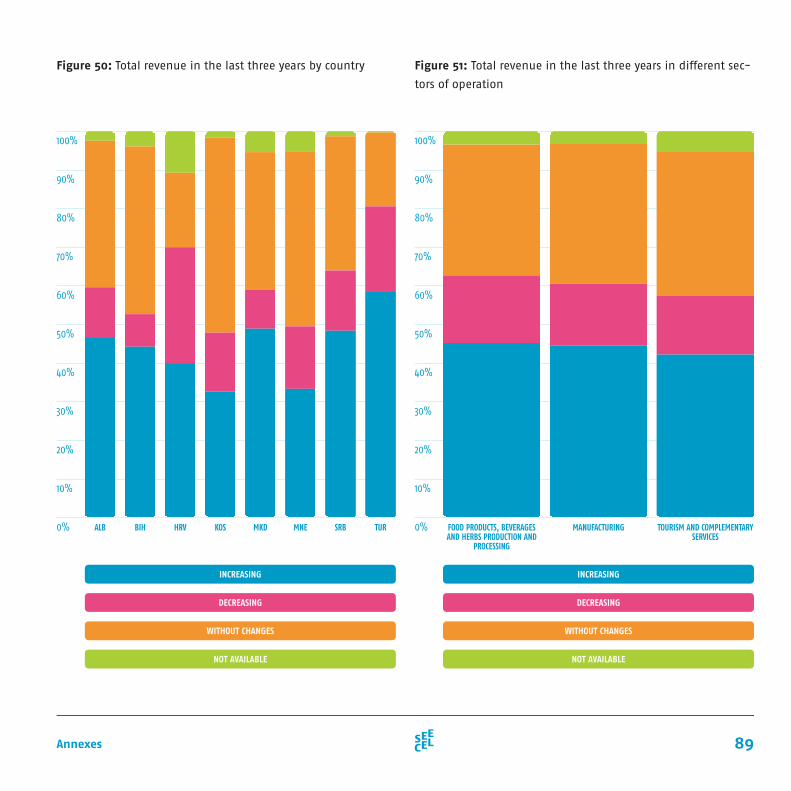

between countries regarding total revenue, num-ber of employees and both exports and imports. The detailed data are presented through figures and statistical data. Furthermore, there are visible differences in total revenue trends reported in the last three years in relation to the country (Figure 50, in Annex). The country with the highest per-centage of enterprises which reported an increase in the total revenue is Turkey (approximately 60% of enterprises), whilst the country with the highest percentage of enterprises which reported decrease in the total revenue is Croatia (approximately 30% of enterprises).

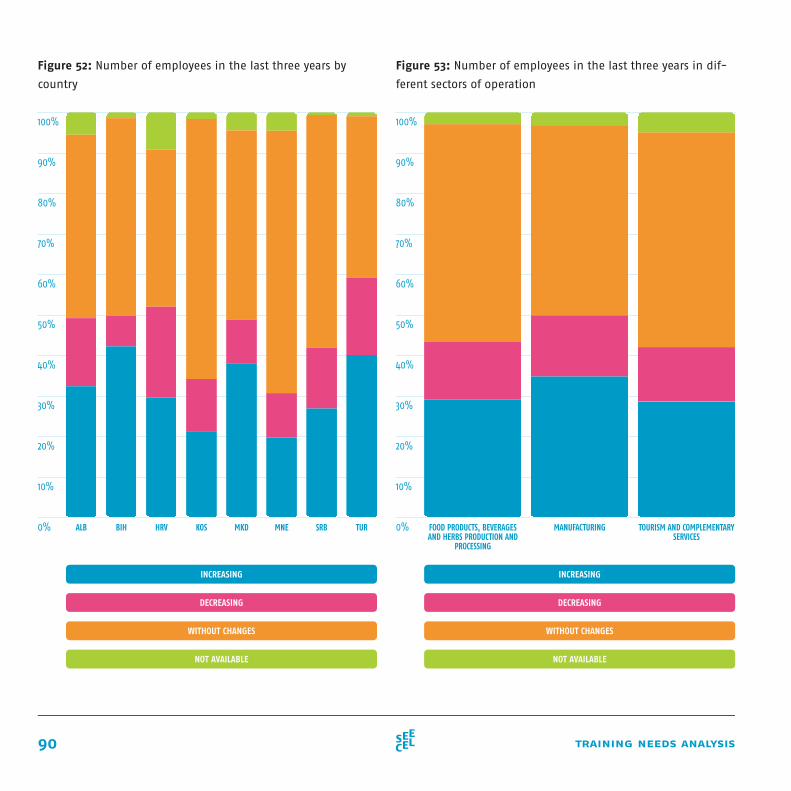

In terms of sectors of operation and revenues, the most enterprises which stated an increase in total revenues come from the manufacturing sec-tor (510), followed by FBP (343) and tourism (275), however, it should be noted that manufacturing enterprises make up for the largest part of the sam-ple (Figure 51, in Annex). Furthermore, there were some differences in the number of employee trends in the last three years from country to country. The

3.2

the business environment and business trends in

enterprises

31Findings

largest increase in number of employees is expe-rienced in enterprises in Bosnia and Herzegovina (around 40% of enterprises). The largest decrease in number of employees is experienced by enterprises in Croatia (around 20% of enterprises) (Figures 52, in Annex). When comparing the differences in the number of employees by different sector of opera-tion, approximately 35% of manufacturing enter-prises are experiencing an increase in the number of employees in the last three years. At the same time, around 15% of manufacturing enterprises have a decrease in the number of employees. Moreover, a very similar share of enterprises in FBP and tourism are experiencing increase, decrease and no changes in the number of employees (Figure 53, in Annex).

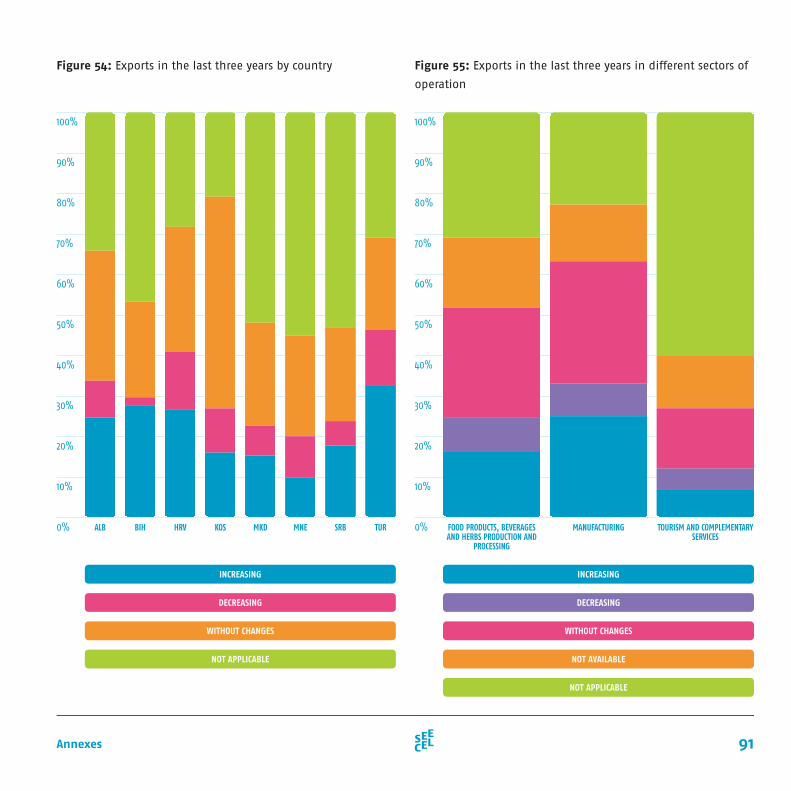

The largest increase in exports is visible in Bosnia and Herzegovina, Turkey, Albania and Croatia. At the same time, information on exports is not applicable to approximately 50% of enterprises in the former Yugoslav Republic of Macedonia and Serbia, imply-ing that these enterprises might not export (Figure 54, in Annex). Comparing these trends to the sector of operation, the largest percentage of enterprises, which have an increase of exports are manufactur-ing enterprises, followed by FBP enterprises. Tourism and complementary services is a sector of operation where data on exports are most often not applicable (Figure 55, in Annex). Analysing the import trends in the last three years, a high percentage of enter-prises have stable imports data for the last three years. The largest percentage of enterprises that did not have any changes in import are from Kosovo. Analysing different operating sectors, import data

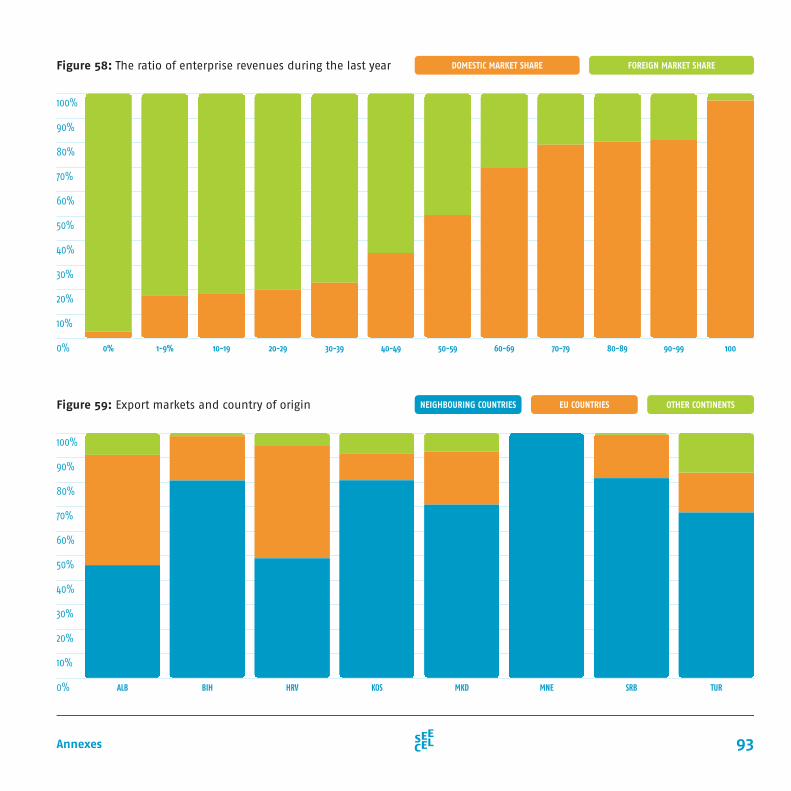

are not applicable for almost 80% of enterprises in tourism sector, other two sectors are characterized with rather high percentage of enterprises (approxi-mately 30% of enterprises) with stable import data for the last three years, with manufacturing sector having the most enterprises that have an increase in imports (Figures 56 and 57, in Annex). Most of the survey participants (N=1474) earned 100% of their enterprise revenues on the local market, whilst only 43 participants earned 100% of the enterprise rev-enue on the foreign market share. However, many enterprises operate both on domestic and foreign markets (Figure 58, in Annex).

Out of those enterprises that export, Albania and Croatia have the highest percentage (approximately 45%) of enterprises which export their goods to the EU countries. Enterprises in the Montenegrin sam-ple are exporting their goods only to neighbouring countries. Exporting goods to neighbouring coun-tries is typical for 80% of enterprises in Bosnia and Herzegovina, Kosovo and Serbia. Almost 15% of en-terprises in Turkey export their goods to other con-tinents, which is accompanied with another 15% of export to the EU countries (Figure 59, in Annex).

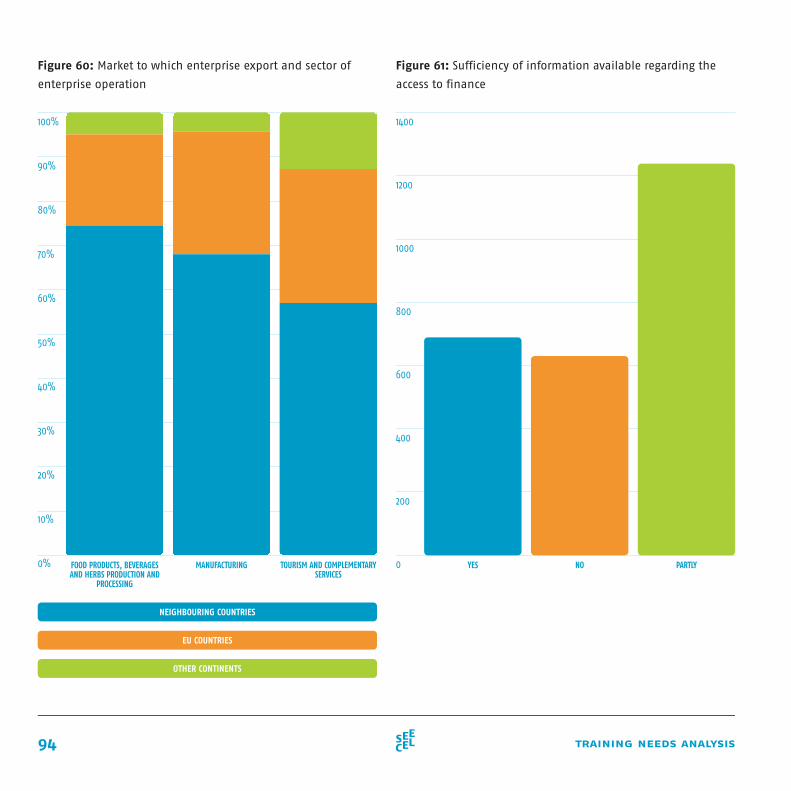

Furthermore, when analysing exports by operat-ing sector (Figure 60, in Annex) it is obvious that neighbouring countries are the most frequent ex-port markets, followed by the EU countries. Out of the three sectors, manufacturing sector exports to the EU the most, in absolute terms of the enter-prises, whilst when looking at the relative terms, tourism sector exports the most to the EU countries and other continents.

32 training needs analysis

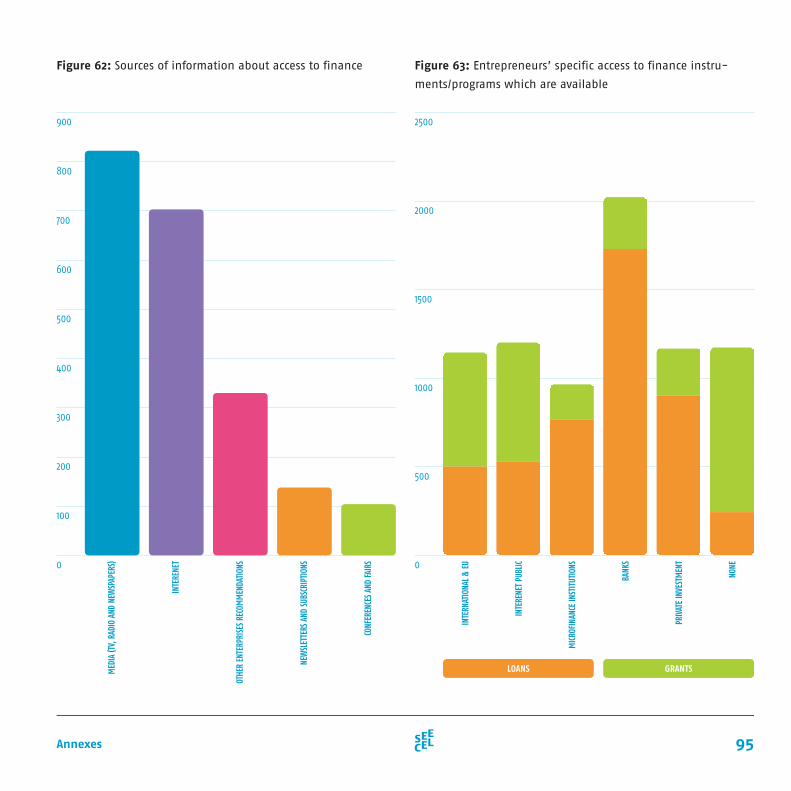

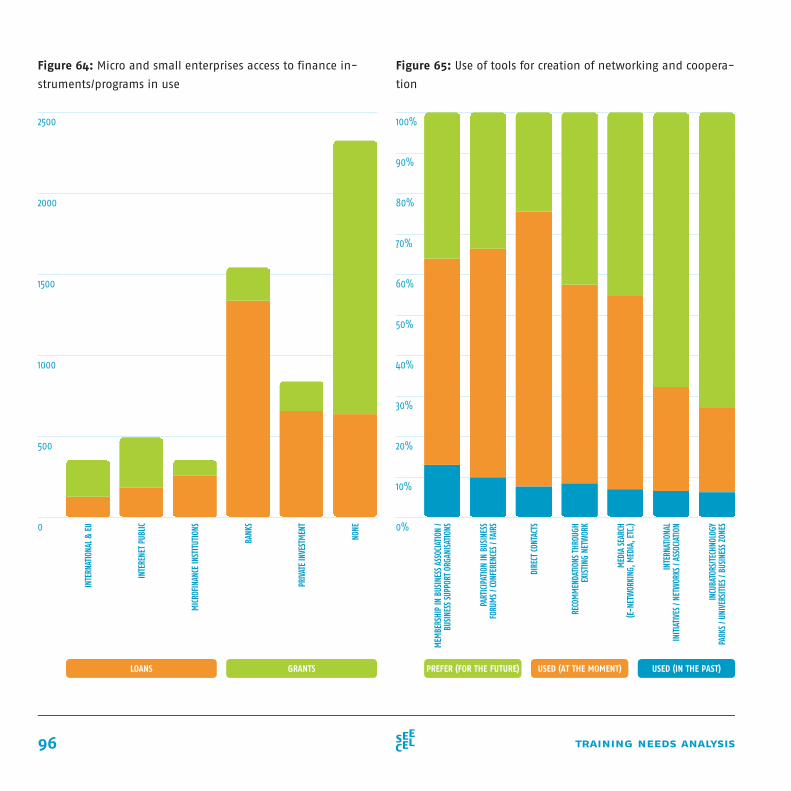

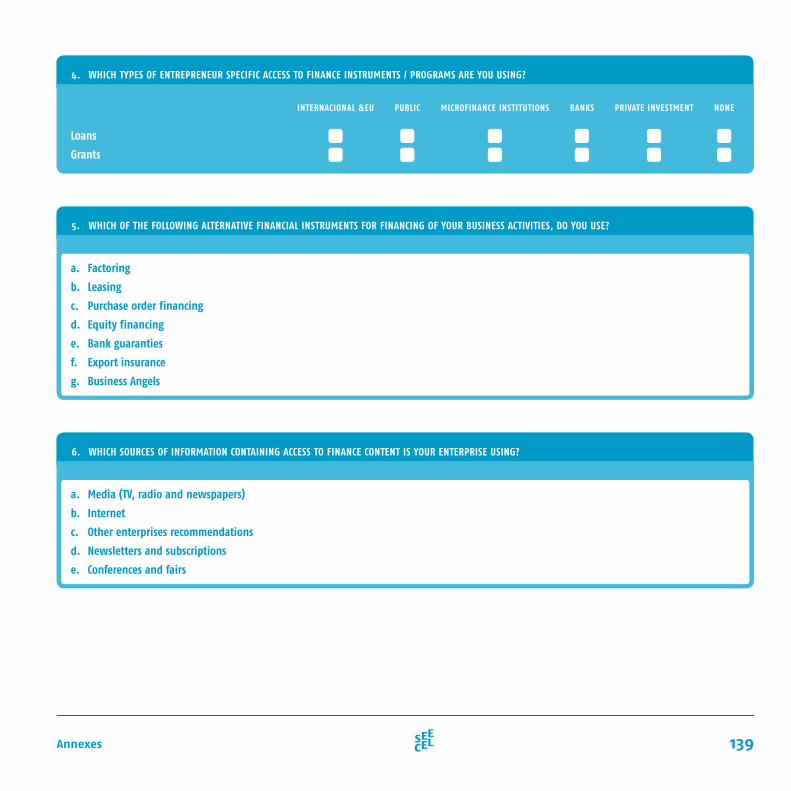

Access to finance has been widely recognised as one of the problems of SMEs in general. Therefore, this section tries to give a brief overview of the access to finance in the micro and small enterprises of the region. Out of the total sample, 1228 entrepre-neurs have stated they are partly satisfied with the availability of information about access to finance, 630 are not satisfied at all and 689 entrepreneurs are satisfied. Furthermore, entrepreneurs from the sampled enterprises, gather information on the ac-cess to finance mostly via media and internet, and then through recommendations. Entrepreneurs who participated in this survey used newsletters, confer-ences and fairs least commonly as a source of in-

formation covering access to finance (Figure 61 and Figure 62, in Annex).

Entrepreneurs were also asked to respond to two different issues, the actual usage and perceived availability of finance instruments. Micro financ-ing institutions, as sources of access to financing, are least used, followed by the international and EU funds and public funds. On the other hand, banks are most frequently used by micro and small en-terprises in the region. Analysing the perception of the availability of instruments, micro financing in-stitutions are perceived as the least available in the region (Figure 63 and Figure 64, in Annex).

3.3.

access to finance

33Findings

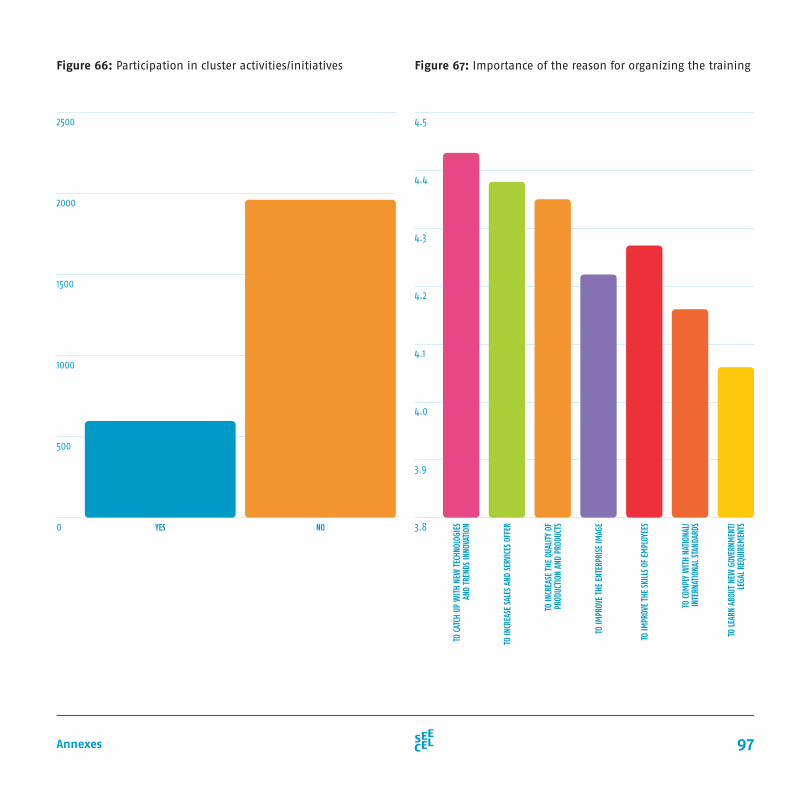

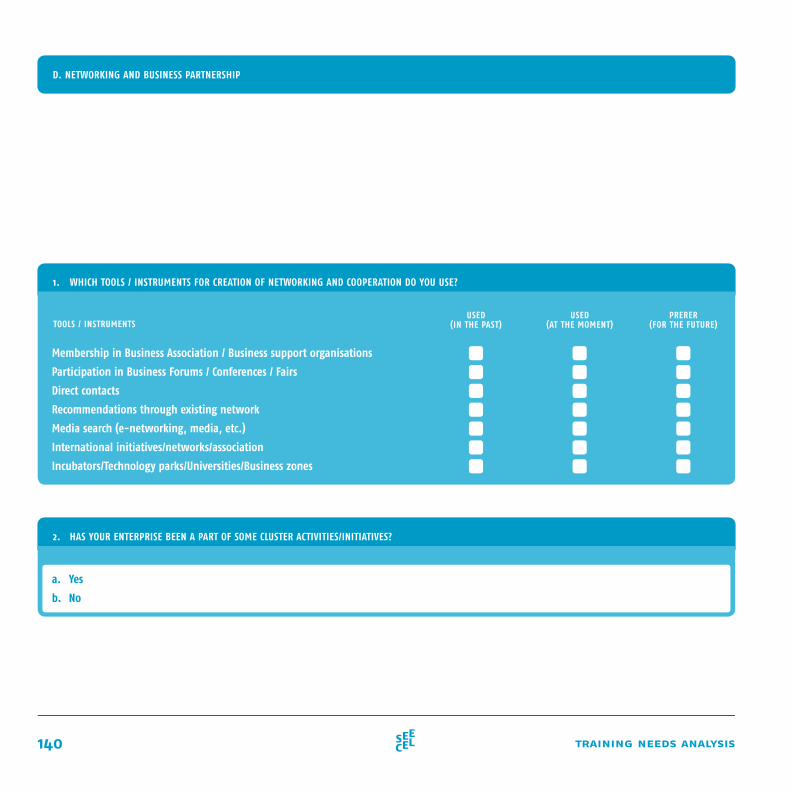

This section gives an overview of the ways micro and small enterprise owners build their networks. Almost 70 percent of enterprises currently use direct contact for networking and cooperation (Figure 65, in An-nex). The second most commonly used networking tool, used by more than 55% of enterprises, is par-ticipation in business forums, conferences and fairs. The least used tool in the past and at the moment is incubators, technology parks/universities and busi-ness zones. At the same time, survey participants recognize this tool the most desirable instrument for creation of networking and cooperation in the future (Figure 65, in Annex). Survey data indicate relatively

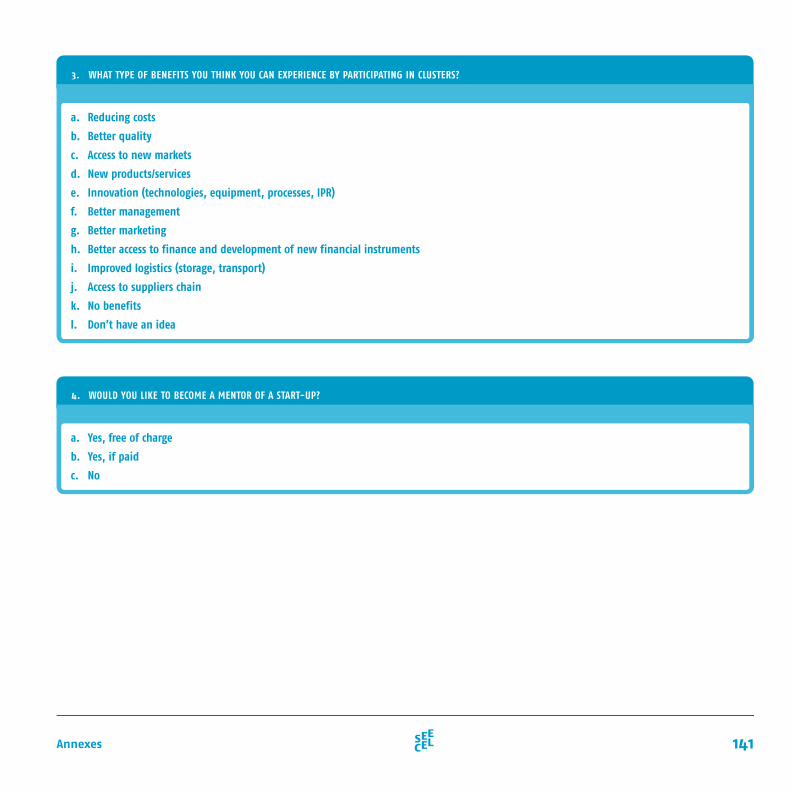

low participation in cluster activities and/or initia-tives (Figure 66, in Annex). Nevertheless, additional data suggest that business owners are aware of possible benefits of participation in clusters. As pre-sented in the Figure 8, the most commonly perceived benefits from participation in clusters are: access to new markets, cost reduction and new products and/or services. The least commonly perceived benefits are: improved logistics and access to supply chain. Survey participants rarely believe there are no ben-efits from participating in clusters.

3.4.

networking and business partnership

34 training needs analysis

Figure 8: Possible benefits of participating in clusters The 49% of the sampled entrepreneurs are not will-ing to become a start-up mentor (Figure 9). Addi-tionally, 28% of entrepreneurs have indicated they would be mentors to a start-up if they were paid for it, whilst 23% of entrepreneurs have indicated they would mentor new enterprise free of charge. This is a substantial negative trend when compared to the previous TNA (SEECEL, 2012), where more entrepre-neurs were willing to become mentors. There are many policy documents (e.g. European Commission, 2013) aiming at support and mentoring schemes, however, we can assume that the crisis and living in condition related to crisis left no margin for this type of activity.

Figure 9: Willingness to become a mentor of a start-up

ACCE

SS TO

NEW

MAR

KETS

REDU

CING

COST

S

NEW

PRO

DUCT

S/SE

RVIC

ES

BETT

ER Q

UALIT

Y

DON’

T HA

VE A

N ID

EA

BETT

ER M

ARKE

TING

INNO

VATI

ON (T

ECHN

OLOG

IES,

EQU

IPM

ENT,

PROC

ESSE

S)

BETT

ER M

ANAG

EMEN

T

BETT

ER A

CESS

TO F

INAN

CE A

ND D

EVEL

OPM

ENT

OF N

EW

ACCE

SS TO

SUP

PLIE

RS C

HAIN

IMPR

OVED

LOGI

STIC

S (S

TORA

GE, T

RANS

PORT

)

NO B

ENEF

ITS

1200

1000

800

600

400

200

0

1400

1200

1000

800

600

400

200

0 YES, FREE OF CHARGE YES, IF PAID NO

35Findings

This section provides an overview of the previous trainings delivered in sampled micro and small enterprises in the region. Furthermore, the sec-tion gives an overview of the responsibility for human resource management, important training areas and reasons for organising trainings. Gener-ally speaking, both theory and practice suggest that with the increase of the firm and/or its number of employees there is a need for more systematic and more comprehensive human resource man-

3.5.

human resources and training

agement, implying that in larger firms, develop-ment and training of human resources is in charge of particular persons and/or special departments (units) established for these activities solely (SEECEL, 2012b, p. 46). In the sampled enterprises, owners are most commonly in charge of human resource development (Figure 10). As expected, enterprises with more employees usually have human resource departments or directors, who are in charge of hu-man resource development.

36 training needs analysis

Figure 10: Human resource development activities by enter-

prise size

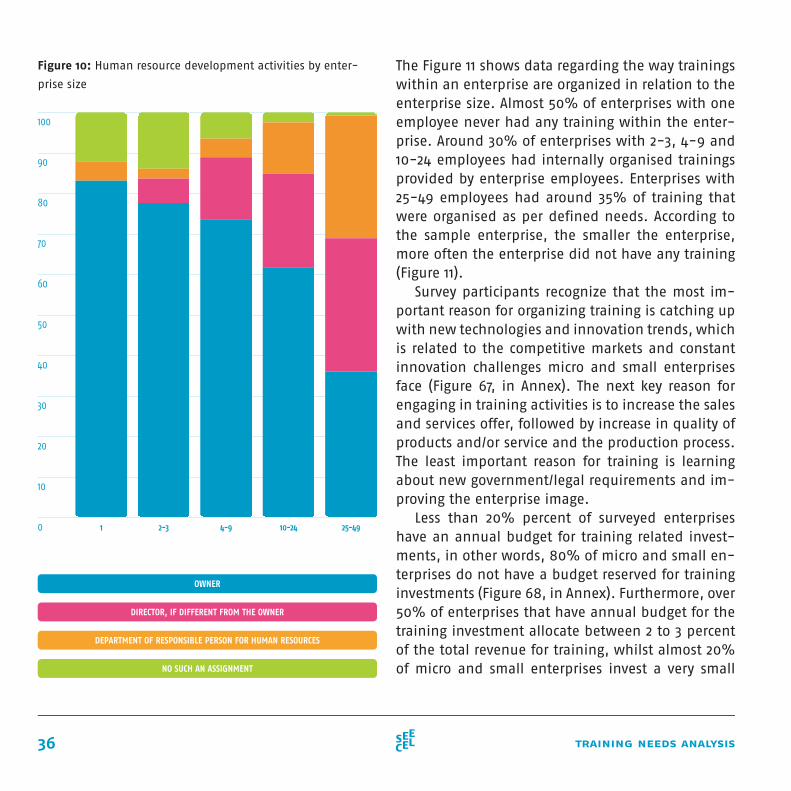

The Figure 11 shows data regarding the way trainings within an enterprise are organized in relation to the enterprise size. Almost 50% of enterprises with one employee never had any training within the enter-prise. Around 30% of enterprises with 2-3, 4-9 and 10-24 employees had internally organised trainings provided by enterprise employees. Enterprises with 25-49 employees had around 35% of training that were organised as per defined needs. According to the sample enterprise, the smaller the enterprise, more often the enterprise did not have any training (Figure 11).

100

90

80

70

60

50

40

30

20

10

0 1 2-3 4-9 10-24 25-49

NO SUCH AN ASSIGNMENT

DEPARTMENT OF RESPONSIBLE PERSON FOR HUMAN RESOURCES

DIRECTOR, IF DIFFERENT FROM THE OWNER

OWNER

Survey participants recognize that the most im-portant reason for organizing training is catching up with new technologies and innovation trends, which is related to the competitive markets and constant innovation challenges micro and small enterprises face (Figure 67, in Annex). The next key reason for engaging in training activities is to increase the sales and services offer, followed by increase in quality of products and/or service and the production process. The least important reason for training is learning about new government/legal requirements and im-proving the enterprise image.

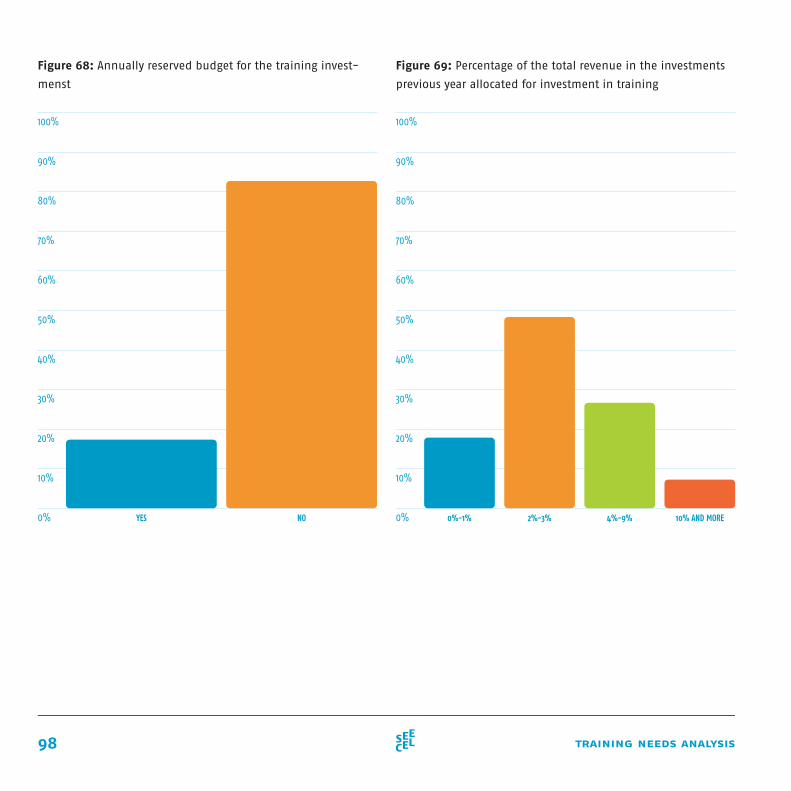

Less than 20% percent of surveyed enterprises have an annual budget for training related invest-ments, in other words, 80% of micro and small en-terprises do not have a budget reserved for training investments (Figure 68, in Annex). Furthermore, over 50% of enterprises that have annual budget for the training investment allocate between 2 to 3 percent of the total revenue for training, whilst almost 20% of micro and small enterprises invest a very small

37Findings

Figure 11: The way in which training within the enterprise is

organised and enterprise size

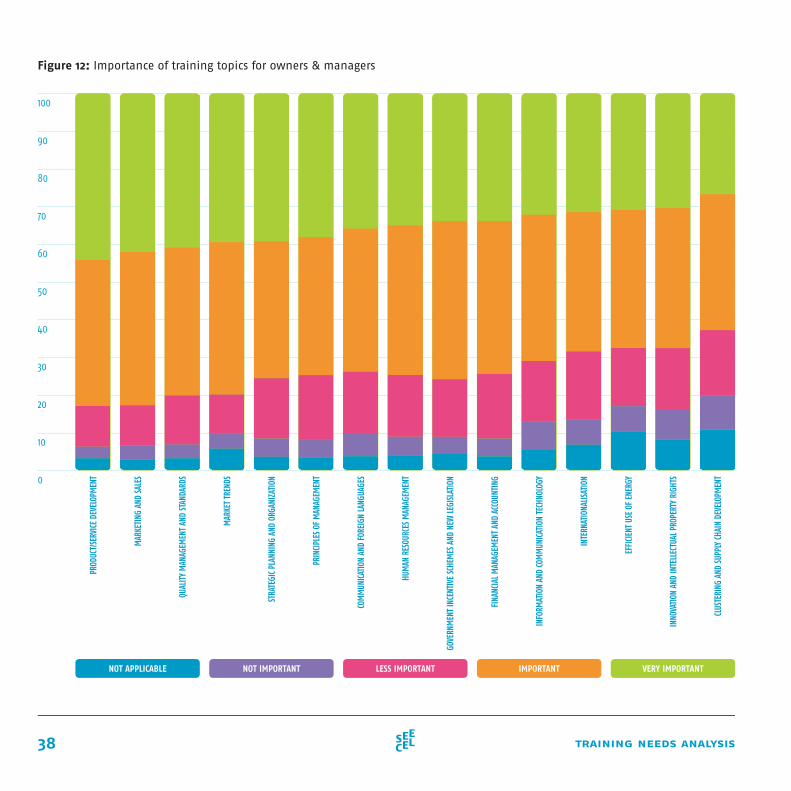

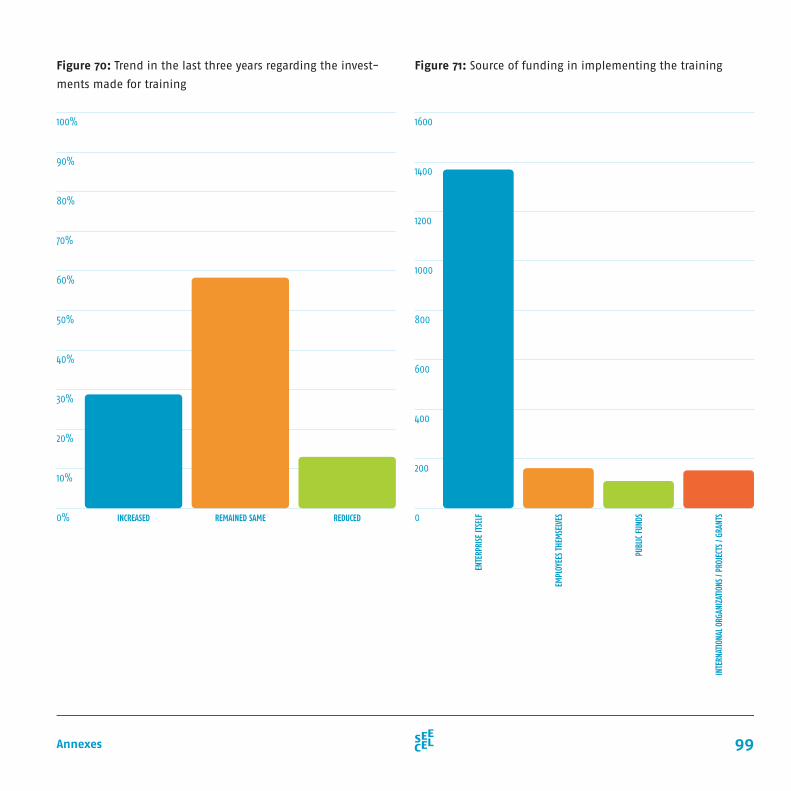

portion of their total revenues in training activities, ranging somewhere between 0 and 1 percent (Figure 69, in Annex). Training investment trends have re-mained the same in the last three years for almost 60% of the sampled micro and small enterprises, whilst around 10% of enterprises have reduced their budget in the last three years. On the other hand, almost 25% of the enterprises in the sample have increased their budget for investments in trainings (Figure 70, in Annex). The most common source of funding for implementation of training is enterprise itself (Figure 71, in Annex). Other sources of funding, such as employees themselves, public funds and international organisations, projects and grants are equally used. It is possible to speculate that majority of the enterprises are not familiar with the avail-able options for training funding. According to the data presented in the Figure 12, the most important training topics for owners and managers are:

• product/service development, • marketing and sales, • quality managements and standards, and • following market trends.

At the same time topics recognized as less important are:

• clustering and supply chain development, • innovation and intellectual property rights, • efficient use of energy, and • internationalization.

100

90

80

70

60

50

40

30

20

10

0 1 2-3 4-9 10-24 25-49

WE NEVER HAD ANY TRAINING WITHIN ENTERPRISE

COMBINED AS PER DEFINED NEEDS

OUTSOURCED - TRAININGS, SEMINARS, CONSULTANCY WITHIN ENTERPRISE

OUTSOURCED - TRAININGS, SEMINARS, CONFERENCES, CONSULTANCY OUTSIDE THE ENTERPRISE

INTERNALLY - PROVIDED BY ENTERPRISE’S EMPLOYEES

38 training needs analysis

Figure 12: Importance of training topics for owners & managers

NOT APPLICABLE NOT IMPORTANT LESS IMPORTANT IMPORTANT VERY IMPORTANT

CLUS

TERI

NG A

ND S

UPPL

Y CH

AIN

DEVE

LOPM

ENT

INNO

VATI

ON A

ND IN

TELL

ECTU

AL P

ROPE

RTY

RIGH

TS

EFFI

CIEN

T US

E OF

ENE

RGY

INTE

RNAT

IONA

LISAT

ION

INF

ORM

ATIO

N AN

D CO

MM

UNIC

ATIO

N TE

CHNO

LOGY

FINA

NCIA

L MAN

AGEM

ENT

AND

ACCO

UNTI

NG

GOVE

RNM

ENT

INCE

NTIV

E SC

HEM

ES A

ND N

EW LE

GISL

ATIO

N

HUM

AN R

ESOU

RCES

MAN

AGEM

ENT

COM

MUN

ICAT

ION

AND

FORE

IGN

LANG

UAGE

S

PRIN

CIPL

ES O

F M

ANAG

EMEN

T

STRA

TEGI

C PLA

NNIN

G AN

D OR

GANI

ZATI

ON

MAR

KET

TREN

DS

PROD

UCT/

SERV

ICE

DEVE

LOPM

ENT

MAR

KETI

NG A

ND S

ALES

QUAL

ITY M

ANAG

EMEN

T AN

D ST

ANDA

RDS

100

90

80

70

60

50

40

30

20

10

0

39Findings

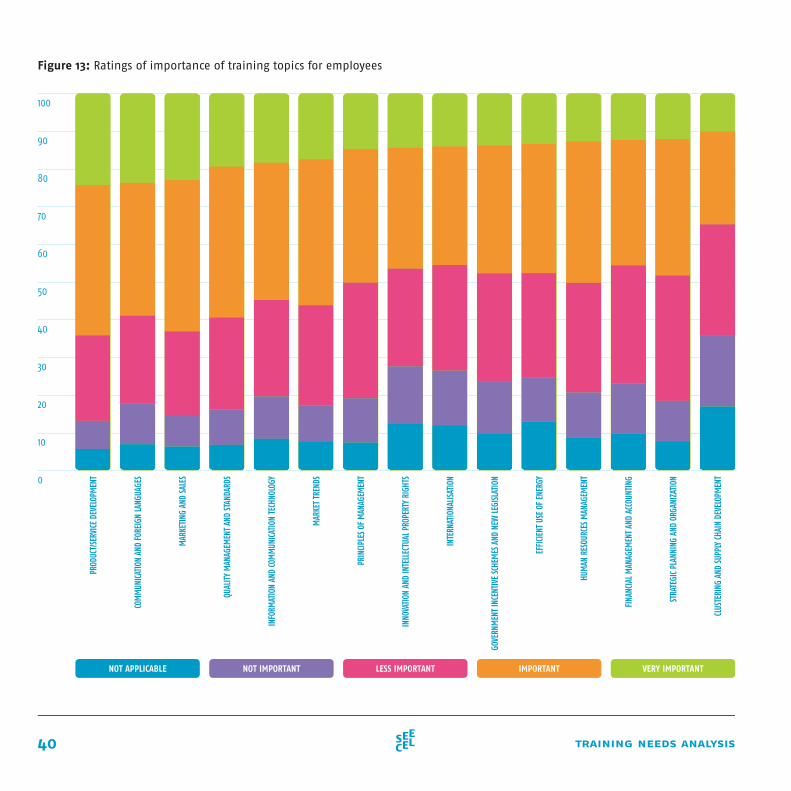

Moving from employers to employees, training top-ics which are recognized as the most important for training of employees are:

• product/service development, • communication and foreign languages, • marketing, and • quality management and standards.

The least important topics are:

• clustering and supply chain development • strategic planning and organization, and • financial management and accounting (Figure 13).

Notably, human resource management is not per-ceived as an important training topic for employees. Although human resource management is important per se, entrepreneurs have stressed the importance of obtaining technical knowledge, process manage-ment and marketing skills for their employees. This could be due to the fact that entrepreneurs them-selves are mostly in charge of human resource man-agement.

40 training needs analysis

Figure 13: Ratings of importance of training topics for employees

100

90

80

70

60

50

40

30

20

10

0

PROD

UCT/

SERV

ICE

DEVE

LOPM

ENT

COM

MUN

ICAT

ION

AND

FORE

IGN

LANG

UAGE

S

MAR

KETI

NG A

ND S

ALES

QUAL

ITY M

ANAG

EMEN

T AN

D ST

ANDA

RDS

INFO

RMAT

ION

AND

COM

MUN

ICAT

ION

TECH

NOLO

GY

MAR

KET

TREN

DS

PRIN

CIPL

ES O

F M

ANAG

EMEN

T

INNO

VATI

ON A

ND IN

TELL

ECTU

AL P

ROPE

RTY

RIGH

TS

INTE

RNAT

IONA

LISAT

ION

GOVE

RNM

ENT

INCE

NTIV

E SC

HEM

ES A

ND N

EW LE

GISL

ATIO

N

EFFI

CIEN

T US

E OF

ENE

RGY

HUM

AN R

ESOU

RCES

MAN

AGEM

ENT

FINA

NCIA

L MAN

AGEM

ENT

AND

ACCO

UNTI

NG

STRA

TEGI

C PLA

NNIN

G AN

D OR

GANI

ZATI

ON

CLUS

TERI

NG A

ND S

UPPL

Y CH

AIN

DEVE

LOPM

ENT

NOT APPLICABLE NOT IMPORTANT LESS IMPORTANT IMPORTANT VERY IMPORTANT

41Findings

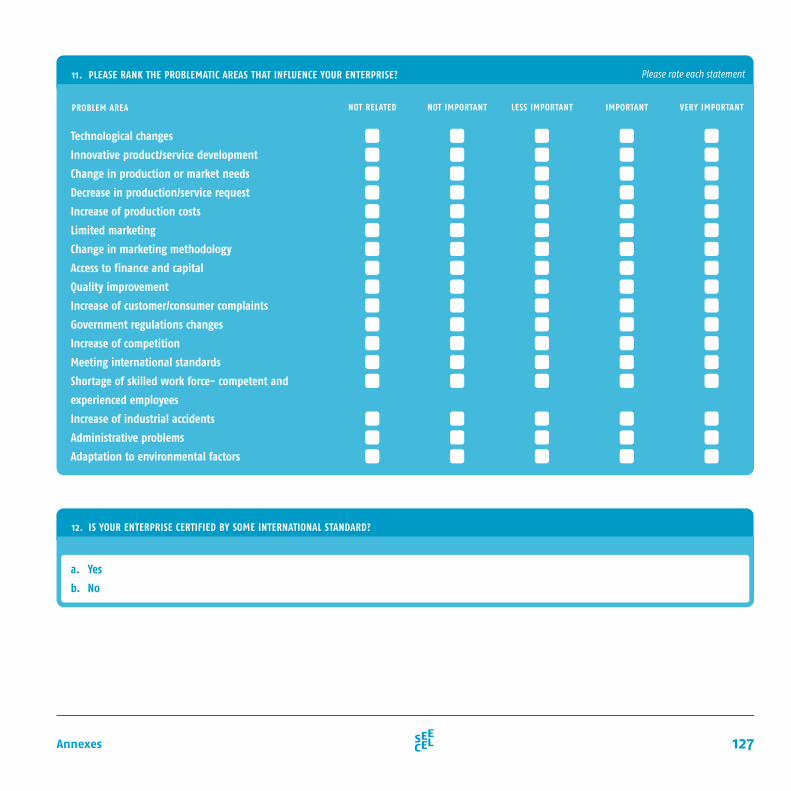

Every year, in every economy, new businesses are be-ing set up, some enterprises are growing, whilst the other are declining, and some cease to exist. The more productive ones take place of the less productive ones, which is often explained with the popular term of ‘creative destruction’ (Schumpeter, 1934). The dynam-ics of the market with new enterprises emerging can affect the economy through enhancing the level of innovation. In parallel, by understanding the barri-ers faced by the existing small business community, governments can enterprises grow with different forms of interventions, and thus assist the future new en-terprises. In line with the previously said, this chapter tries to give a deeper, statistically more rigorous analy-sis of the challenges micro and small enterprises face.

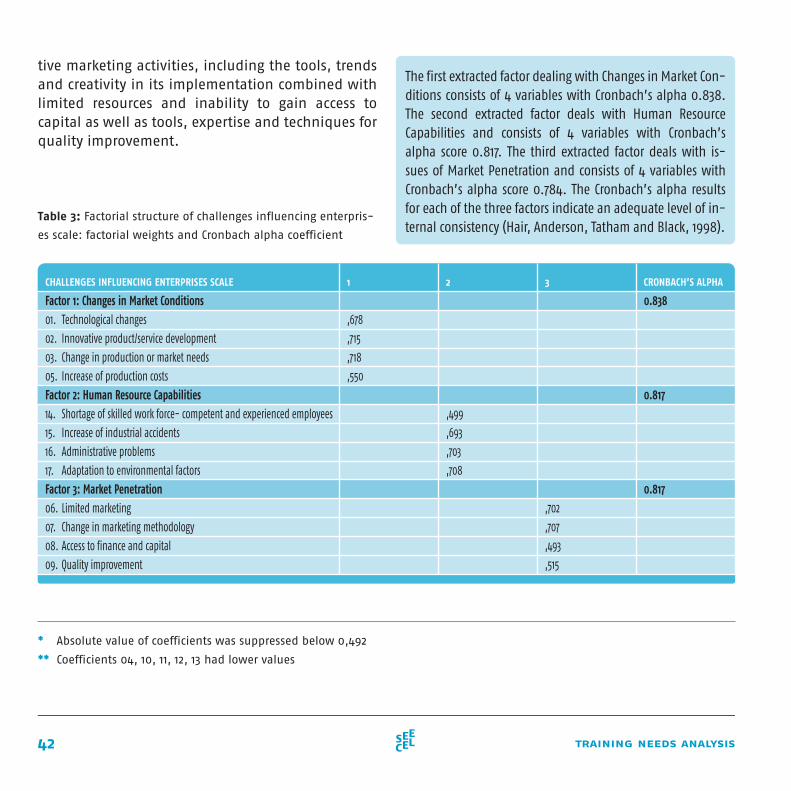

The scale of challenges influencing enterprises consisted of 17 questions. Exploratory factorial anal-ysis was conducted by using principal axis factoring and revealed three factors (Table 3), which account for 50.47% of the common variance. Out of the 17 items, overall 12 items are grouped in three different factors, namely:

• Factor 1: Changes in Market Conditions, • Factor 2: Human Resource Capabilities, and • Factor 3: Market Penetration.

Factor 1: Changes in Market Condition represents the challenges micro and small enterprises face, which occur as a result of constant velocity of changes in meeting customer needs, adjustments to the tech-nological advancements related to the sector, as well as the requirement to constantly make incre-mental innovations and keep track of the innovative achievements of the competitors in the market. Factor 2: Human Resource Capabilities represents the challenges micro and small enterprises face, which occur in relation to employees’ abilities to absorb the administrative requirements towards the state institutions and the enterprise’s clients.

Factor 3: Market Penetration represents the chal-lenges micro and small enterprises face, which occur as a result of limited knowledge in conducting effec-

3.6.

challenges influencing small business community

42 training needs analysis

tive marketing activities, including the tools, trends and creativity in its implementation combined with limited resources and inability to gain access to capital as well as tools, expertise and techniques for quality improvement.

The first extracted factor dealing with Changes in Market Con-ditions consists of 4 variables with Cronbach’s alpha 0.838. The second extracted factor deals with Human Resource Capabilities and consists of 4 variables with Cronbach’s alpha score 0.817. The third extracted factor deals with is-sues of Market Penetration and consists of 4 variables with Cronbach’s alpha score 0.784. The Cronbach’s alpha results for each of the three factors indicate an adequate level of in-ternal consistency (Hair, Anderson, Tatham and Black, 1998).

Table 3: Factorial structure of challenges influencing enterpris-

es scale: factorial weights and Cronbach alpha coefficient

* Absolute value of coefficients was suppressed below 0,492

** Coefficients 04, 10, 11, 12, 13 had lower values

CHALLENGES INFLUENCING ENTERPRISES SCALE 1 2 3 CRONBACH’S ALPHA

Factor 1: Changes in Market Conditions01. Technological changes

02. Innovative product/service development

03. Change in production or market needs

05. Increase of production costs

Factor 2: Human Resource Capabilities14. Shortage of skilled work force- competent and experienced employees

15. Increase of industrial accidents

16. Administrative problems

17. Adaptation to environmental factors

Factor 3: Market Penetration06. Limited marketing

07. Change in marketing methodology

08. Access to finance and capital

09. Quality improvement

,678

,715

,718

,550

0.838

0.817

0.817

,499

,693

,703

,708

,702

,707

,493

,515

43Findings

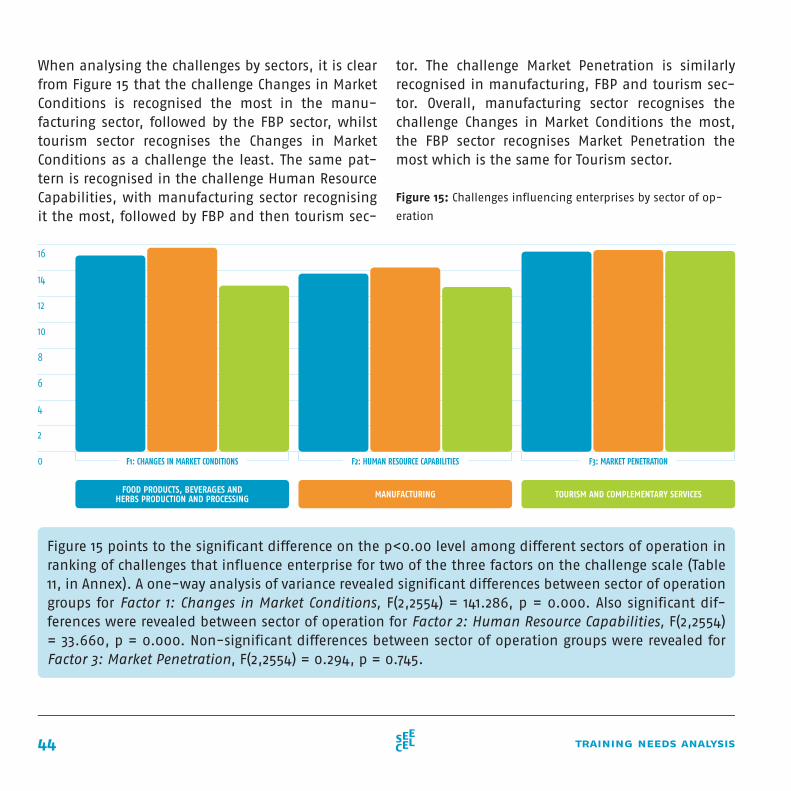

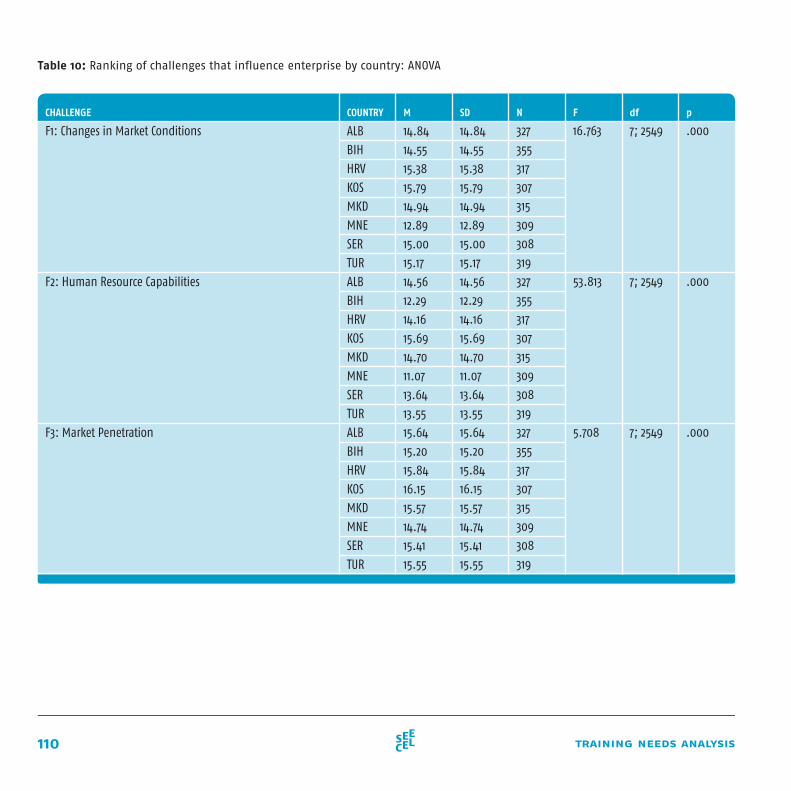

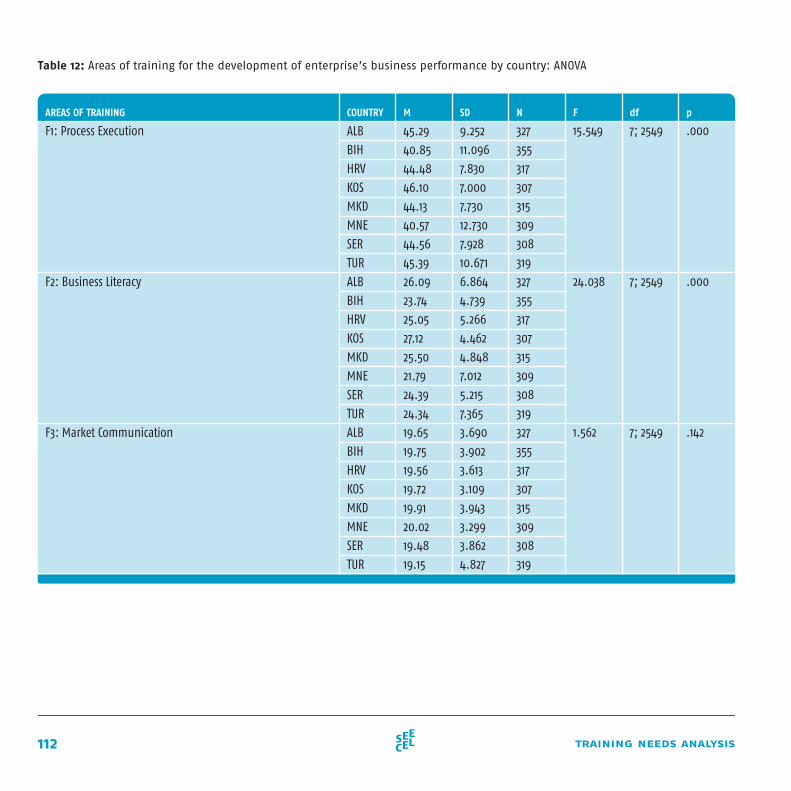

In comparison to the degree of challenges recognition within countries it can be noted that Factor 3: Market Penetration represents the most recognised challenge in all countries and it is followed by the Factor 1: Changes in Market Conditions in all countries, which is in second place. Factor 2: Human Resource Capabili-ties is recognised the least in all countries (Table 10, in Annex). The challenge Changes in Market Conditions is recognised the least in sampled enterprises from Montenegro and the most in sampled enterprises

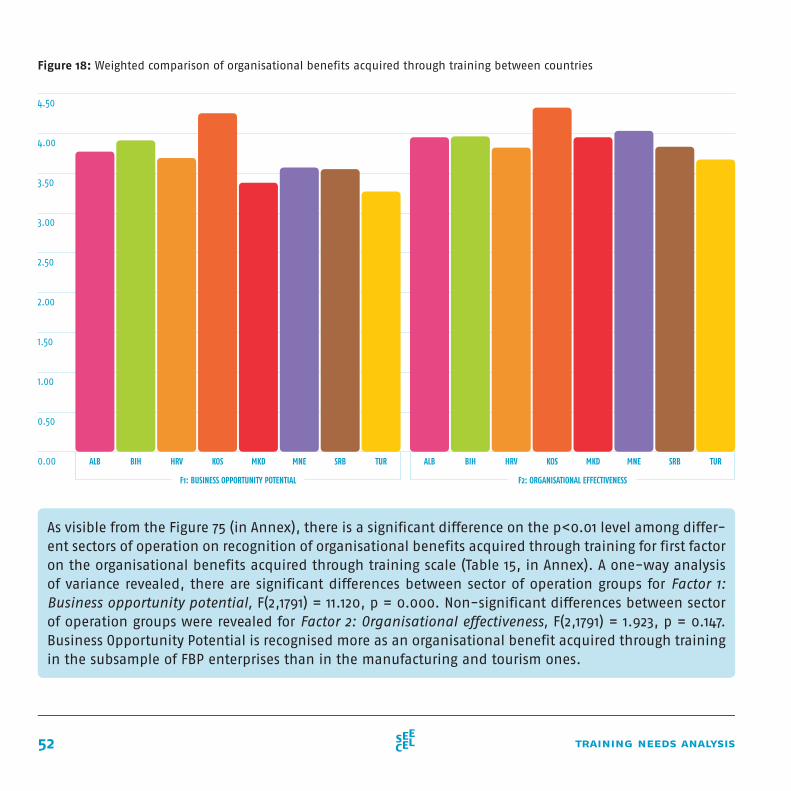

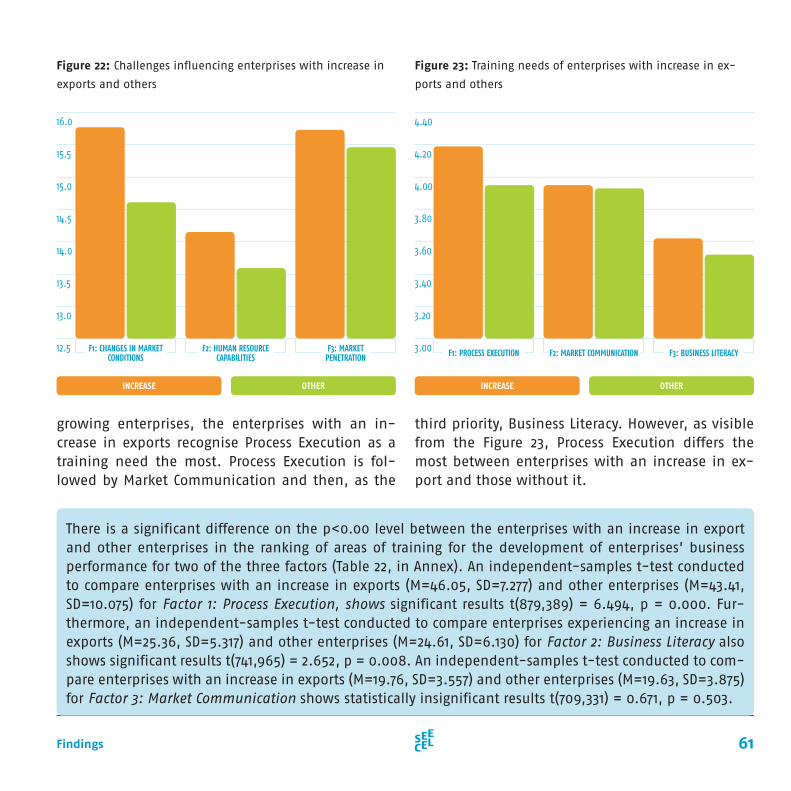

As visible from Figure 14, there is a significant difference on the p<0.01 level among the countries in rank-ing of challenges that influence enterprises for each of the three factors on the challenge scale (Table 10, in Annex). A one-way analysis of variance revealed significant differences between countries for Factor 1: Changes in Market Conditions, F(7,2549) = 16.763, p = 0.000. Furthermore, significant differences between countries were revealed for Factor 2: Human Resource Capabilities, F(7,2549) = 53.813, p = 0.000 and for Factor 3: Market Penetration, F(7,2549) = 5.708, p = 0.000.

from Kosovo. The challenge Human Resource Capa-bilities is recognised the least in Montenegro, whilst it is recognised the most in Kosovo and the former Yugoslav Republic of Macedonia. Challenge Market Penetration is recognised the least in Montenegro and Bosnia and Herzegovina, whilst entrepreneurs from Kosovo, Croatia and Albania have recognised Market Penetration as a challenge the most (Figure 14).

Figure 14: Challenges influencing enterprises by country

18

16

14

12

10

8

6

4

2

0 TURSRBMNEMKDKOSBIH HRVALB TURSRBMNEMKDKOSBIH HRVALB TURSRBMNEMKDKOSBIH HRVALB

F1: CHANGES IN MARKET CONDITIONS F2: HUMAN RESOURCE CAPABILITIES F3: MARKET PENETRATION

44 training needs analysis

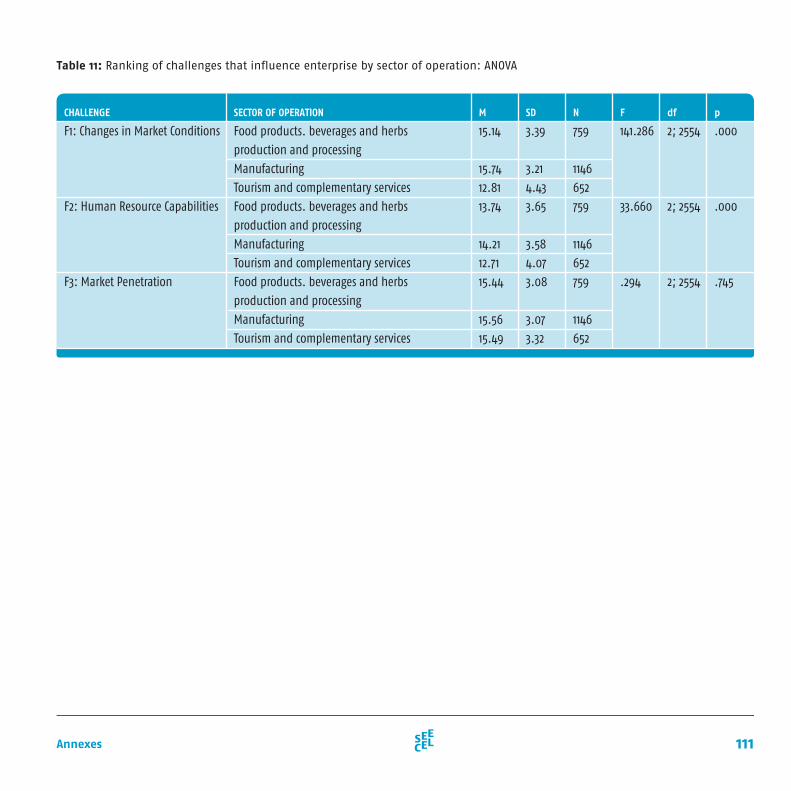

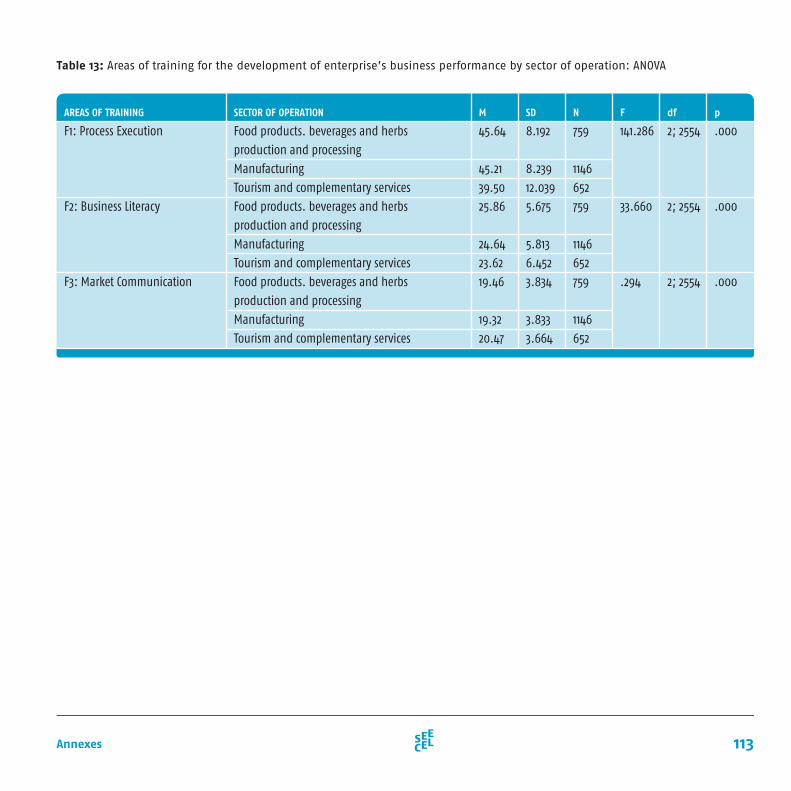

Figure 15 points to the significant difference on the p<0.00 level among different sectors of operation in ranking of challenges that influence enterprise for two of the three factors on the challenge scale (Table 11, in Annex). A one-way analysis of variance revealed significant differences between sector of operation groups for Factor 1: Changes in Market Conditions, F(2,2554) = 141.286, p = 0.000. Also significant dif-ferences were revealed between sector of operation for Factor 2: Human Resource Capabilities, F(2,2554) = 33.660, p = 0.000. Non-significant differences between sector of operation groups were revealed for Factor 3: Market Penetration, F(2,2554) = 0.294, p = 0.745.

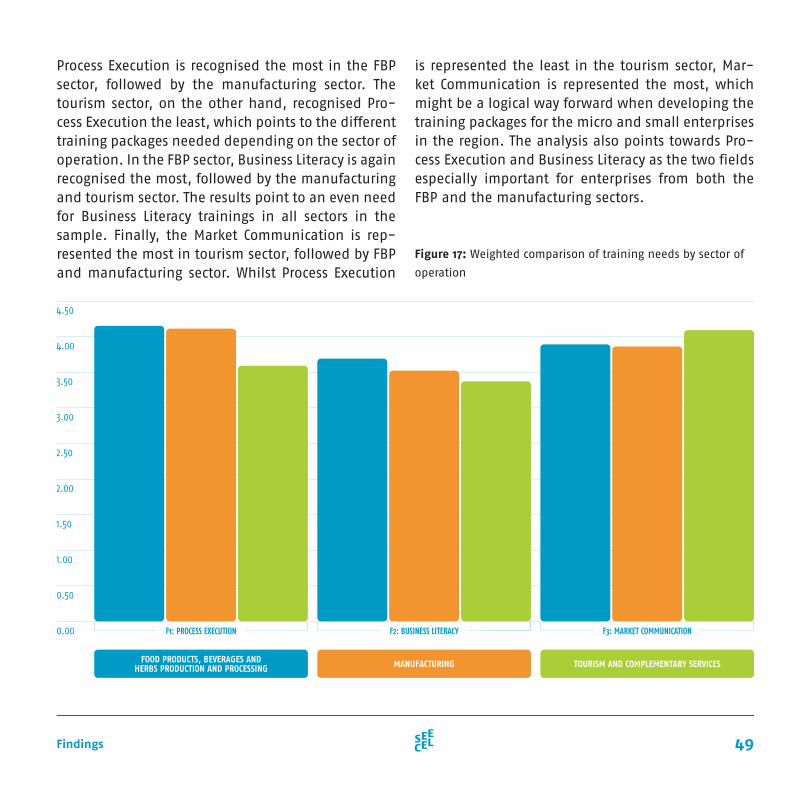

tor. The challenge Market Penetration is similarly recognised in manufacturing, FBP and tourism sec-tor. Overall, manufacturing sector recognises the challenge Changes in Market Conditions the most, the FBP sector recognises Market Penetration the most which is the same for Tourism sector.

Figure 15: Challenges influencing enterprises by sector of op-

eration

16

14

12

10

8

6

4

2

0

FOOD PRODUCTS, BEVERAGES AND HERBS PRODUCTION AND PROCESSING MANUFACTURING TOURISM AND COMPLEMENTARY SERVICES

F1: CHANGES IN MARKET CONDITIONS F2: HUMAN RESOURCE CAPABILITIES F3: MARKET PENETRATION

When analysing the challenges by sectors, it is clear from Figure 15 that the challenge Changes in Market Conditions is recognised the most in the manu-facturing sector, followed by the FBP sector, whilst tourism sector recognises the Changes in Market Conditions as a challenge the least. The same pat-tern is recognised in the challenge Human Resource Capabilities, with manufacturing sector recognising it the most, followed by FBP and then tourism sec-

45Findings

This chapter attempts to give an overview of the trainings entrepreneurs from the sampled enterpris-es in eight countries perceive as the most needed. It is these needs that are the voice of the entrepre-neurs for the measures of support but also for the consultants to act upon them.

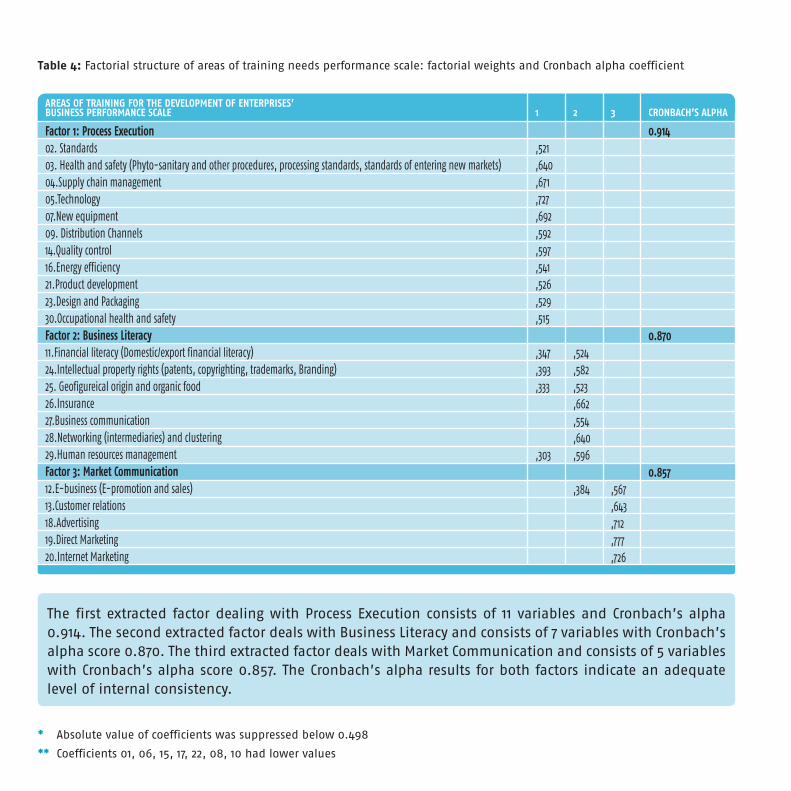

The areas of training for the development of enterprise’s business performance scale consisted of 30 questions. Exploratory factorial analysis was conducted by using the principal axis factoring and revealed three factors (Table 4), which account for 52.48% of the common variance. Out of the 30 items, 23 have a common denominator in the fol-lowing three factors,

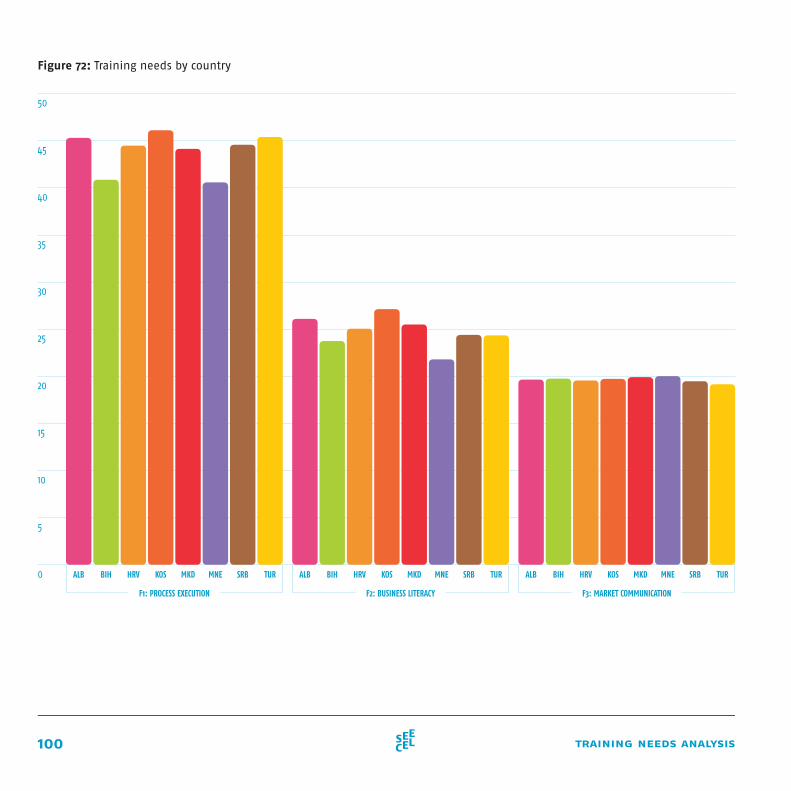

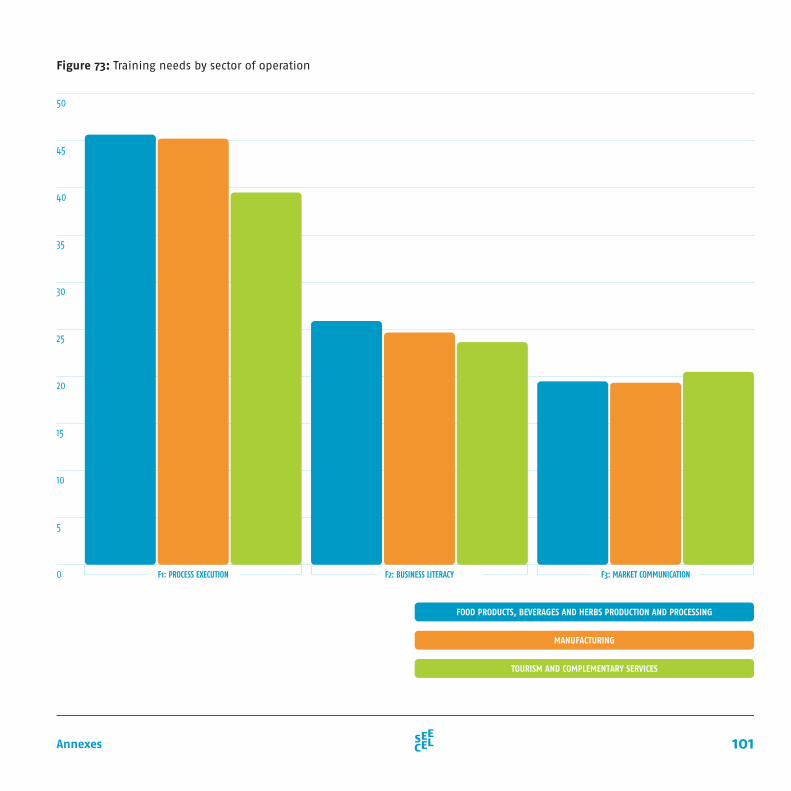

• Factor 1: Process Execution, • Factor 2: Business Literacy, and • Factor 3: Market Communication.

Factor 1: Process Execution refers to the trainings that include acquiring practical skills and tech-niques in using the technology and equipment for the increase of productivity levels, design think-

ing and customer development, management of the supply chain and step by step implementation of standards as well as health and safety require-ments.

Factor 2: Business Literacy represents trainings that feature the overall knowledge needed to run a busi-ness professionally and understand the general en-vironment in which the entrepreneur is operating; this refers to understanding financial instruments, intellectual property rights, professional business correspondence, leading and motivating as well as effective networking strategies.

Factor 3: Market Communication represents trainings for effective market positioning of micro and small enterprises, and it refers to business to business as well as business to customer marketing, effective use of internet marketing tools and how to extract valu-able information from and lock in the customers.

3.7.

trainings needs of the small business community

AREAS OF TRAINING FOR THE DEVELOPMENT OF ENTERPRISES’ BUSINESS PERFORMANCE SCALE 1 2 3 CRONBACH’S ALPHA

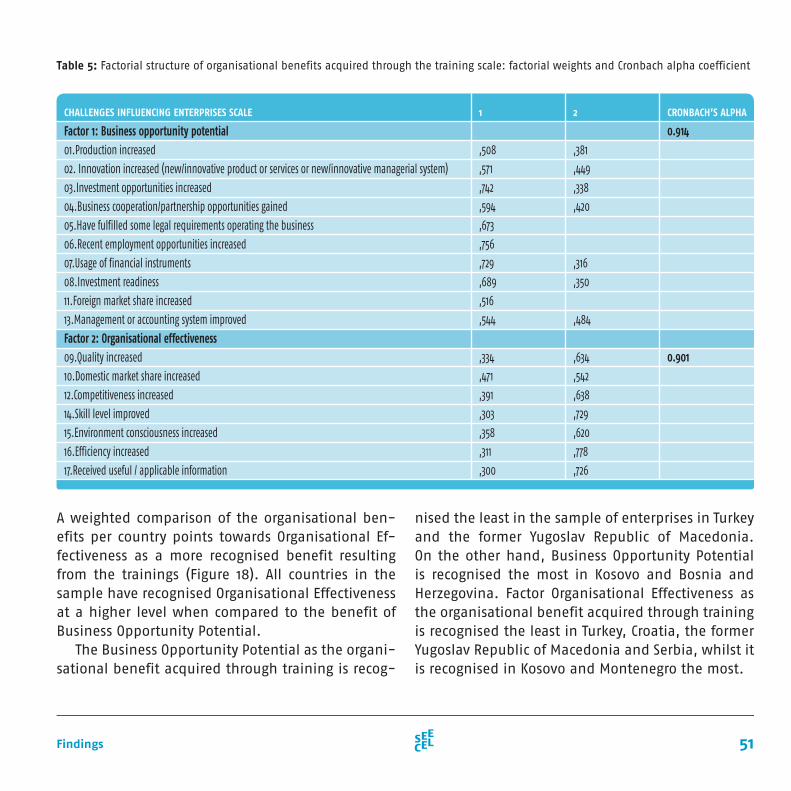

Factor 1: Process Execution 02. Standards03. Health and safety (Phyto-sanitary and other procedures, processing standards, standards of entering new markets)04.Supply chain management05.Technology07.New equipment09. Distribution Channels14.Quality control16.Energy efficiency21.Product development23.Design and Packaging30.Occupational health and safetyFactor 2: Business Literacy11.Financial literacy (Domestic/export financial literacy)24.Intellectual property rights (patents, copyrighting, trademarks, Branding)25. Geofigureical origin and organic food26.Insurance27.Business communication28.Networking (intermediaries) and clustering29.Human resources managementFactor 3: Market Communication12.E-business (E-promotion and sales)13.Customer relations18.Advertising19.Direct Marketing20.Internet Marketing

,521 ,640 ,671 ,727 ,692 ,592 ,597 ,541 ,526 ,529 ,515

0.914

0.870

0.857

,524,582,523 ,662 ,554 ,640,596

,384

,347 ,393 ,333

,303

,567,643,712,777,726

* Absolute value of coefficients was suppressed below 0.498

** Coefficients 01, 06, 15, 17, 22, 08, 10 had lower values

Table 4: Factorial structure of areas of training needs performance scale: factorial weights and Cronbach alpha coefficient

The first extracted factor dealing with Process Execution consists of 11 variables and Cronbach’s alpha 0.914. The second extracted factor deals with Business Literacy and consists of 7 variables with Cronbach’s alpha score 0.870. The third extracted factor deals with Market Communication and consists of 5 variables with Cronbach’s alpha score 0.857. The Cronbach’s alpha results for both factors indicate an adequate level of internal consistency.

47Findings

Items that have not been grouped in the previous three factors are legislation, franchising, new ser-vice development, market research, environmental management, investment and finance management and risk management.

Financial literacy and human resource manage-ment are the only two items that have loaded in all three factors (Table 4). Therefore, we can state that financial literacy, an integral part of the en-trepreneurial learning in the SEECEL Member States, is given substantial importance. The issue of lack of financial literacy and need for further improvement in this area could be addressed by full scale imple-mentation of the entrepreneurship as a key compe-tence in the education systems of the SEECEL Member States, starting from primary level all the way to the tertiary level of education.