Embed Size (px)

Citation preview

Trade, Inequality, and Populism

Caroline FreundDirector of Macro, Trade and Investment

Global Lecture

The Vienna Institute for International Economic Studies

October 1, 2018

Themes from research on trade, growth, and inequality

• Trade and Inequality• Trade and poverty reduction

• Trade and the middle class

• Superstar firms, trade, and extreme wealth creation

• Backlash against globalization• Policy

• Identity politics

Common narrative on trade and inequality

• Globalization allowed poor countries to export more labor intensive goods

• Less skilled workers in rich countries lost their jobs

• Bottoming out of the middle class and rise in inequality

• Leading to a backlash against globalization

• Suggests development of poor countries has come at the expense of low skilled workers in developed countries

3

True narrative is more nuanced

• Trade contributed significantly to drop in global inequality• Trade helps poor countries grow, as resources shift to productive uses

• Less evidence that trade contributed significantly to increase in within-country income inequality• Trade helped create a class of superrich, but also lowers prices

disproportionately helping the poor

• Populism/Protectionism responds to confluence of factors, among which rhetoric on trade exceeds the reality

4

Trade helped poor countries grow

5

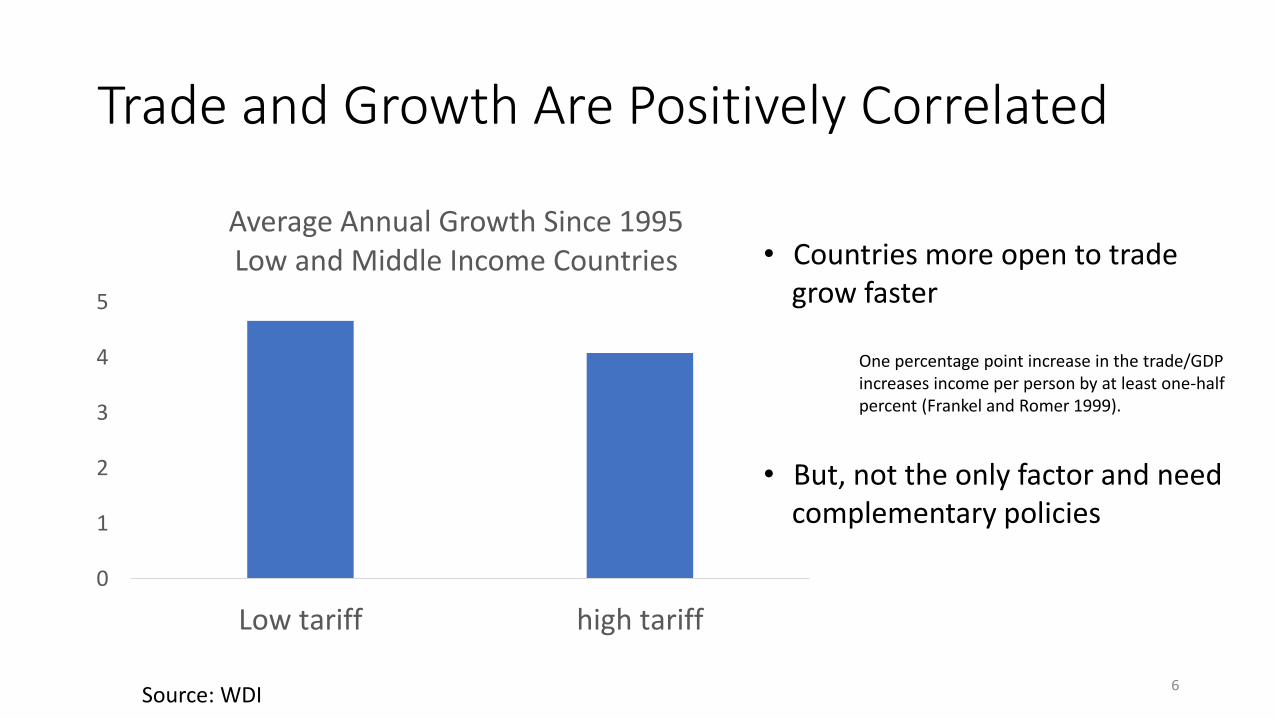

Trade and Growth Are Positively Correlated

0

1

2

3

4

5

Low tariff high tariff

Average Annual Growth Since 1995 Low and Middle Income Countries • Countries more open to trade

grow faster

One percentage point increase in the trade/GDP increases income per person by at least one-half percent (Frankel and Romer 1999).

• But, not the only factor and need complementary policies

Source: WDI6

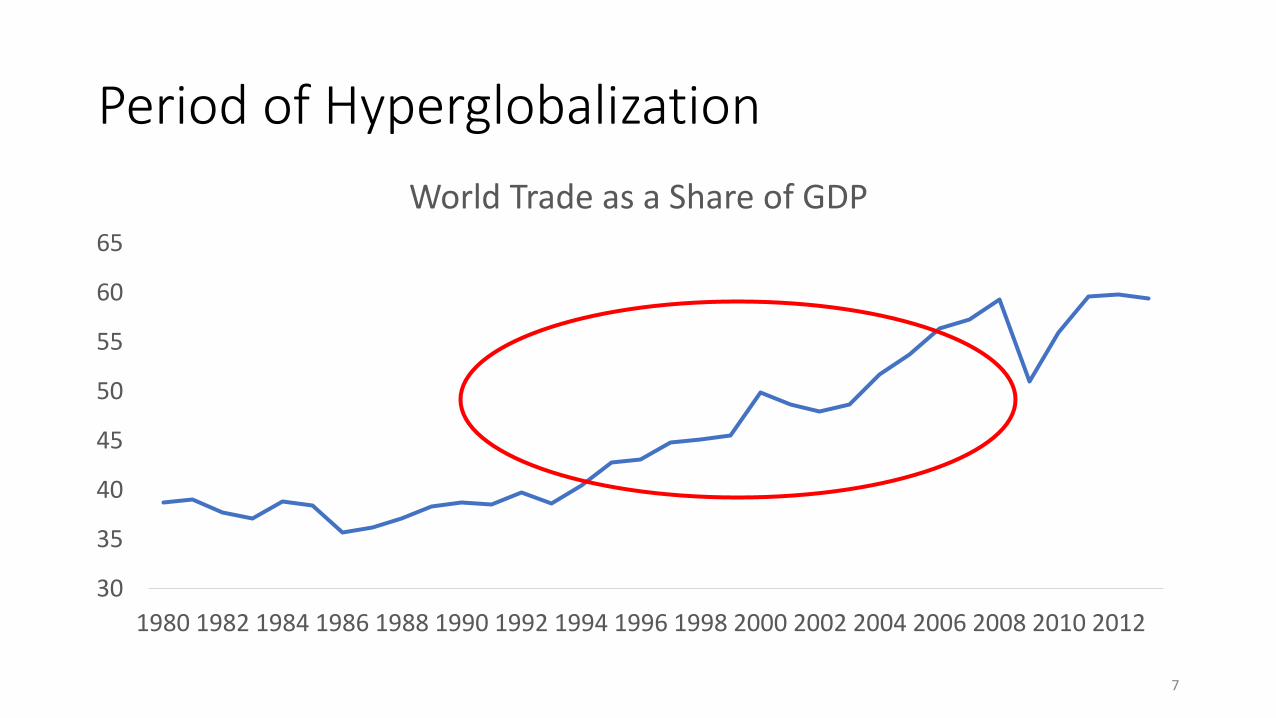

Period of Hyperglobalization

30

35

40

45

50

55

60

65

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

World Trade as a Share of GDP

7

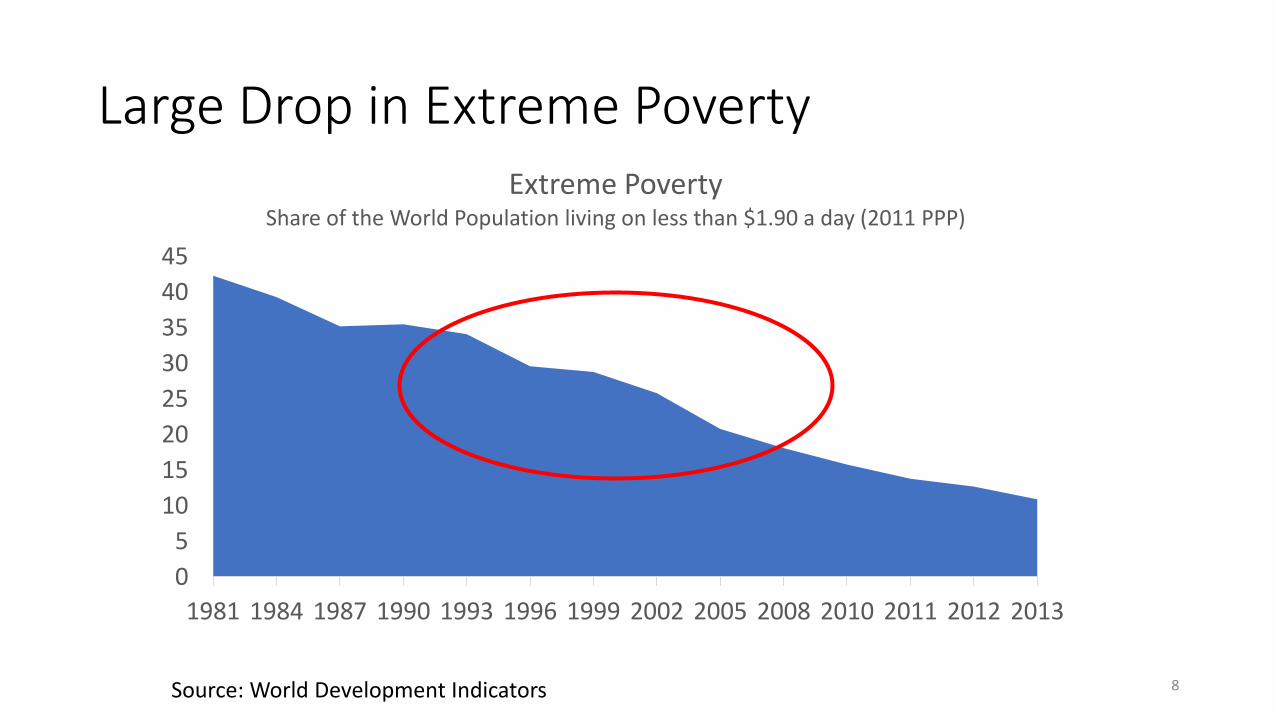

Large Drop in Extreme Poverty

0

5

10

15

20

25

30

35

40

45

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2010 2011 2012 2013

Extreme PovertyShare of the World Population living on less than $1.90 a day (2011 PPP)

Source: World Development Indicators 8

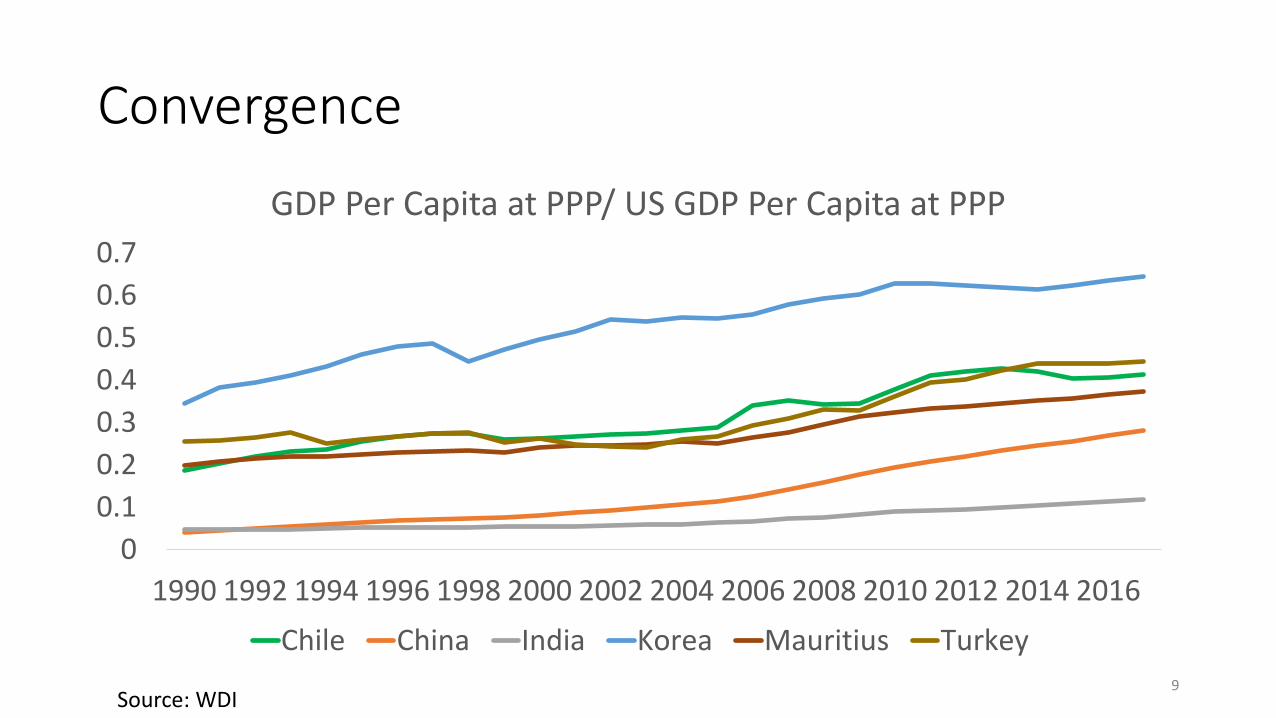

Convergence

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

GDP Per Capita at PPP/ US GDP Per Capita at PPP

Chile China India Korea Mauritius Turkey

Source: WDI9

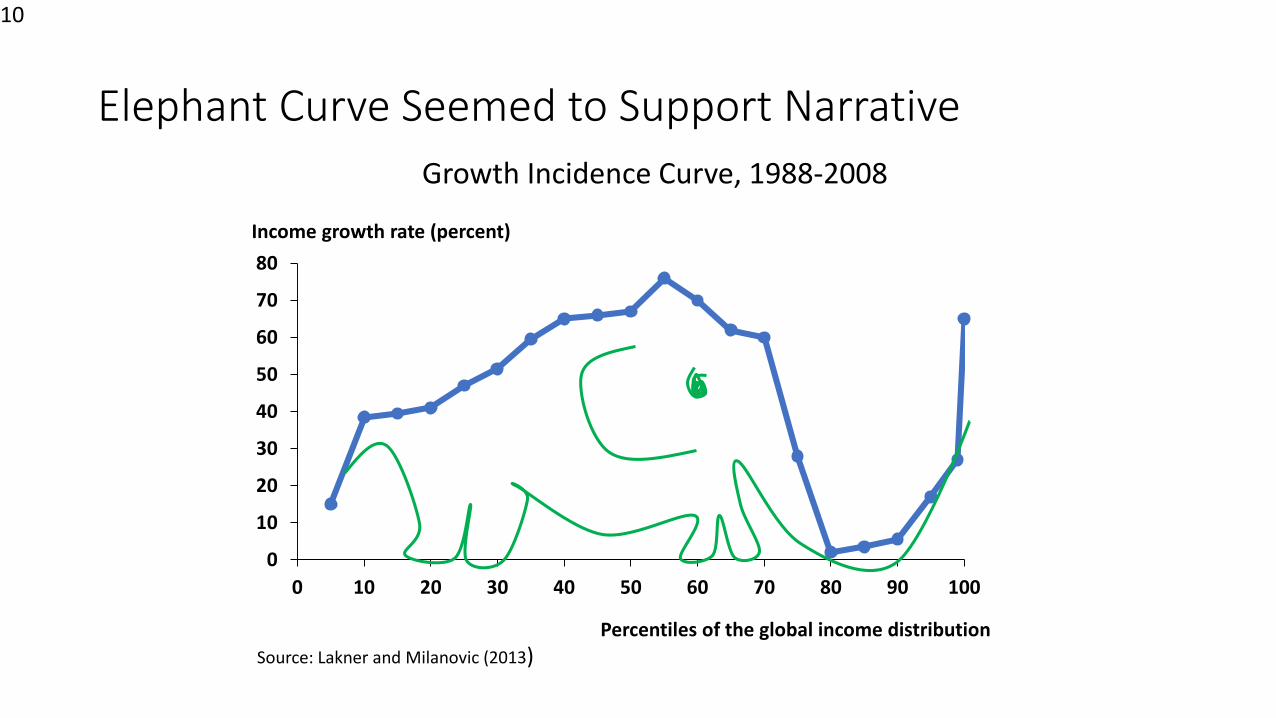

Elephant Curve Seemed to Support Narrative

10

Source: Lakner and Milanovic (2013)

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 60 70 80 90 100

Percentiles of the global income distribution

Income growth rate (percent)

Growth Incidence Curve, 1988-2008

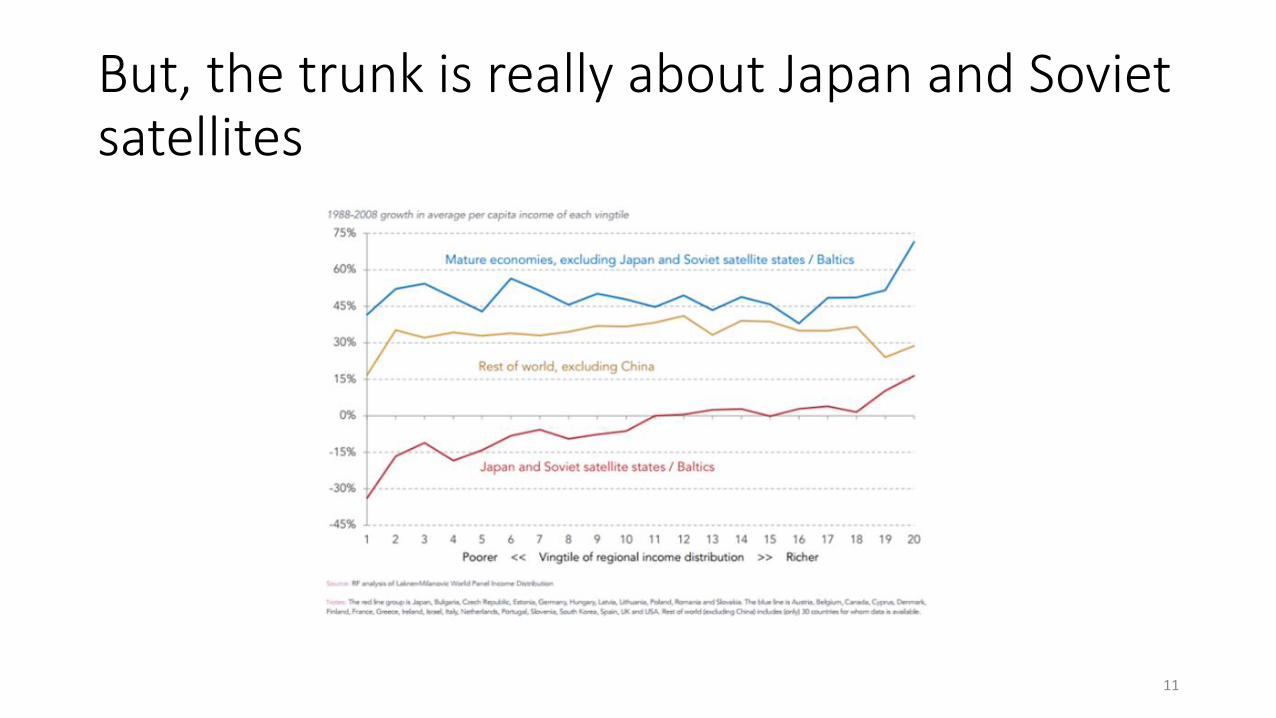

But, the trunk is really about Japan and Soviet satellites

11

What about within-country inequality?

12

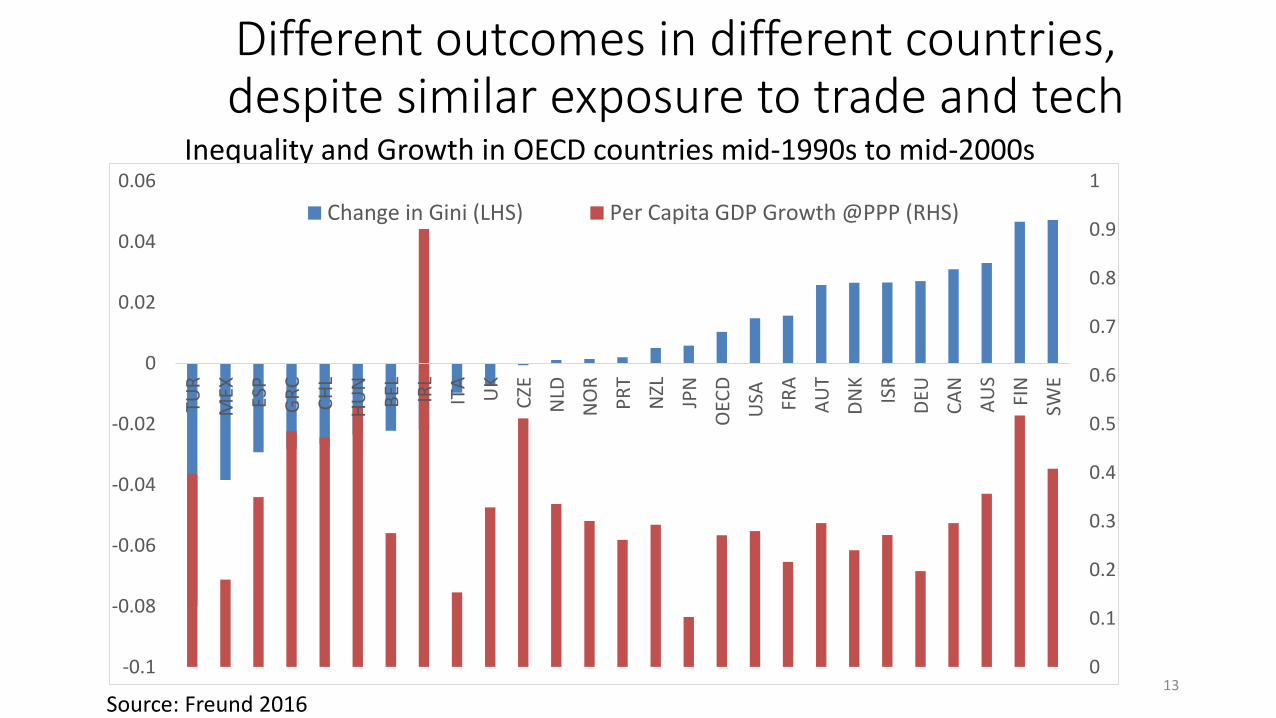

Different outcomes in different countries, despite similar exposure to trade and tech

Inequality and Growth in OECD countries mid-1990s to mid-2000s

13

Source: Freund 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06TU

R

MEX ES

P

GR

C

CH

L

HU

N

BEL IR

L

ITA

UK

CZE

NLD

NO

R

PR

T

NZL

JPN

OEC

D

USA FR

A

AU

T

DN

K

ISR

DEU

CA

N

AU

S

FIN

SWE

Change in Gini (LHS) Per Capita GDP Growth @PPP (RHS)

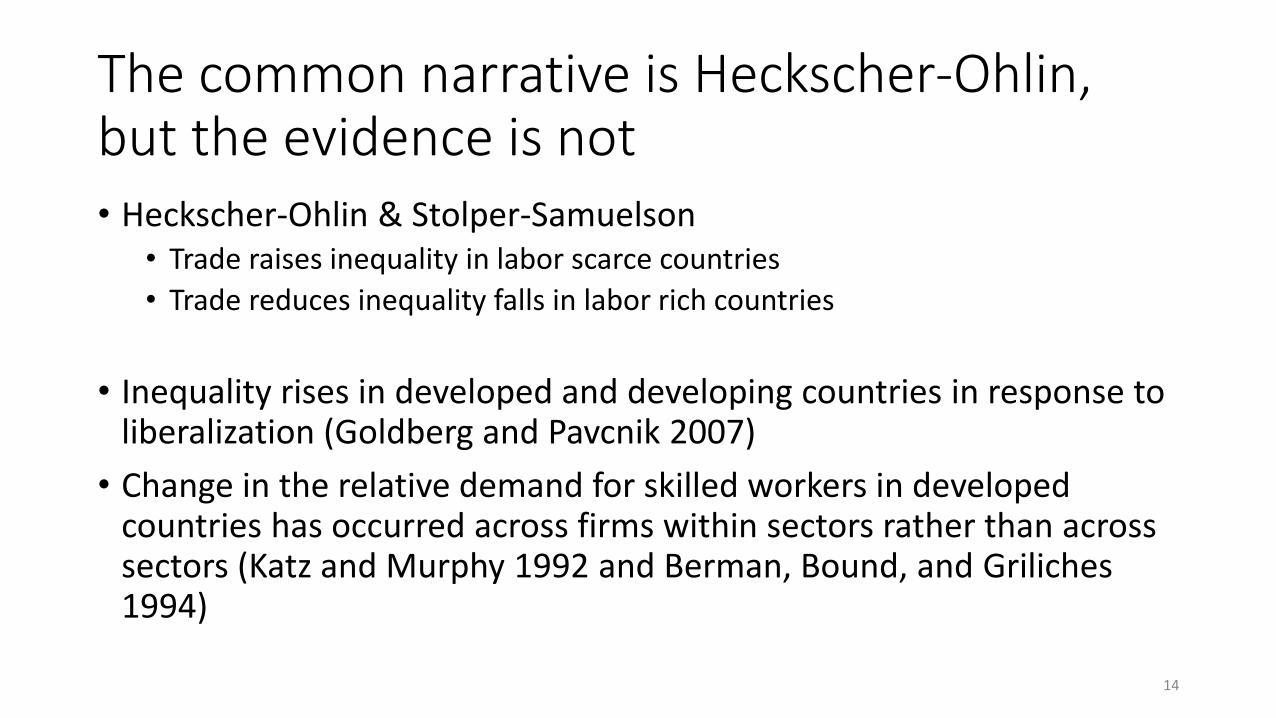

The common narrative is Heckscher-Ohlin, but the evidence is not• Heckscher-Ohlin & Stolper-Samuelson

• Trade raises inequality in labor scarce countries

• Trade reduces inequality falls in labor rich countries

• Inequality rises in developed and developing countries in response to liberalization (Goldberg and Pavcnik 2007)

• Change in the relative demand for skilled workers in developed countries has occurred across firms within sectors rather than across sectors (Katz and Murphy 1992 and Berman, Bound, and Griliches1994)

14

The Role of Superstar Firms

15

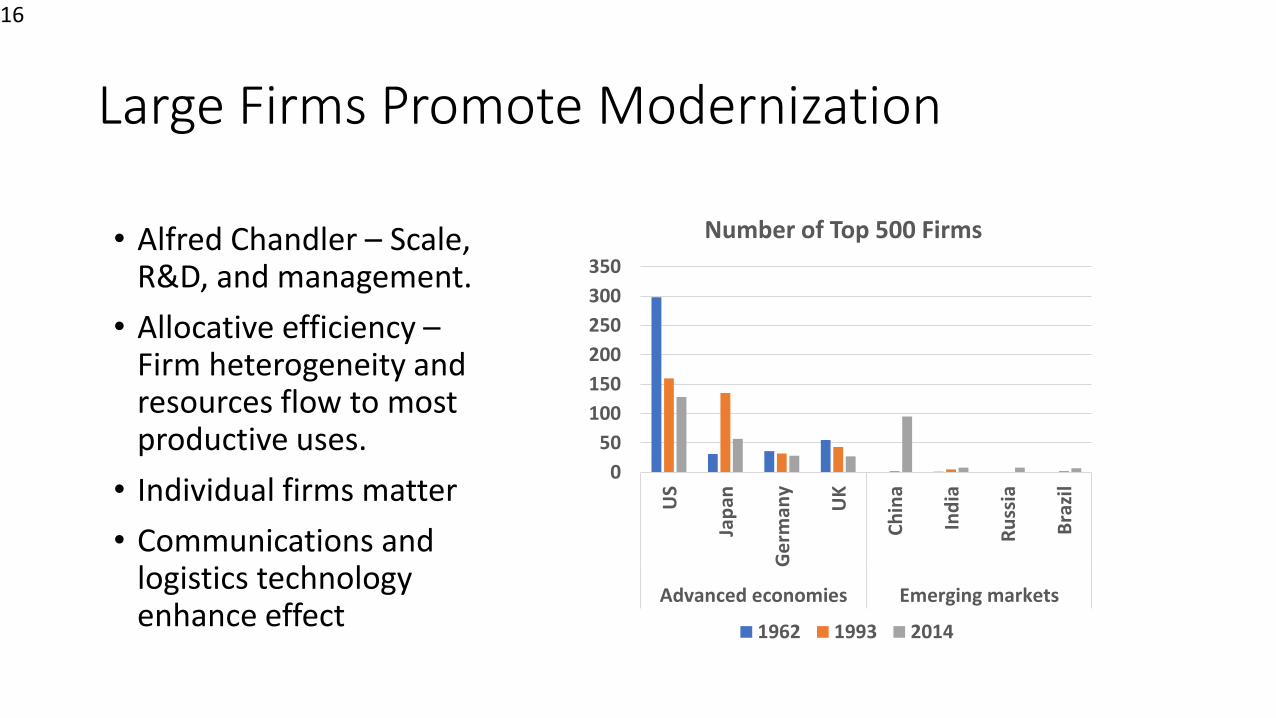

Large Firms Promote Modernization

• Alfred Chandler – Scale, R&D, and management.

• Allocative efficiency –Firm heterogeneity and resources flow to most productive uses.

• Individual firms matter

• Communications and logistics technology enhance effect

16

0

50

100

150

200

250

300

350

US

Jap

an

Ge

rman

y

UK

Ch

ina

Ind

ia

Ru

ssia

Bra

zil

Advanced economies Emerging markets

Number of Top 500 Firms

1962 1993 2014

Allocative Efficiency

• Trade affects productivity through reallocation across firms• As market access abroad expands, most efficient firms export more and grow

• As openness to imports expands, least efficient firms exit

• As countries trade and grow, superstar firms are created

• Increasing trades raises incomes, especially in poor countries, with inefficient allocation of resources

• Increasing trade also creates a class of superrich

17

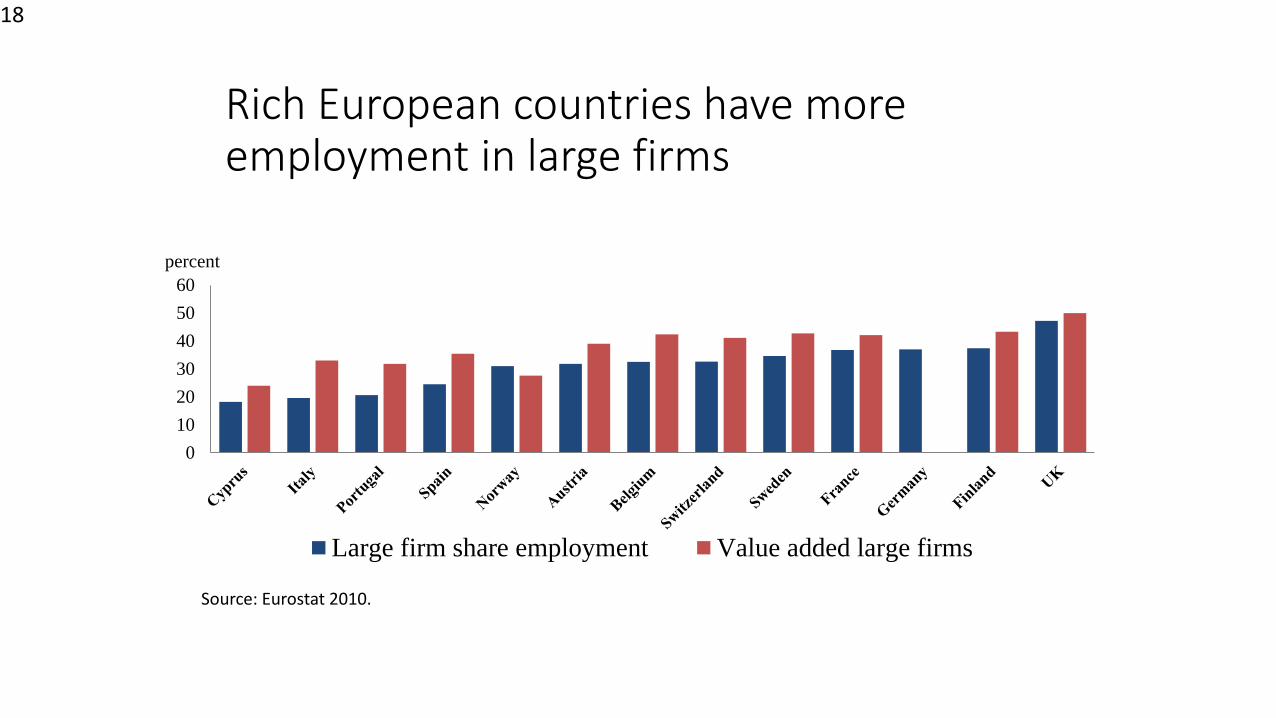

Rich European countries have more employment in large firms

0

10

20

30

40

50

60

percent

Large firm share employment Value added large firms

18

Source: Eurostat 2010.

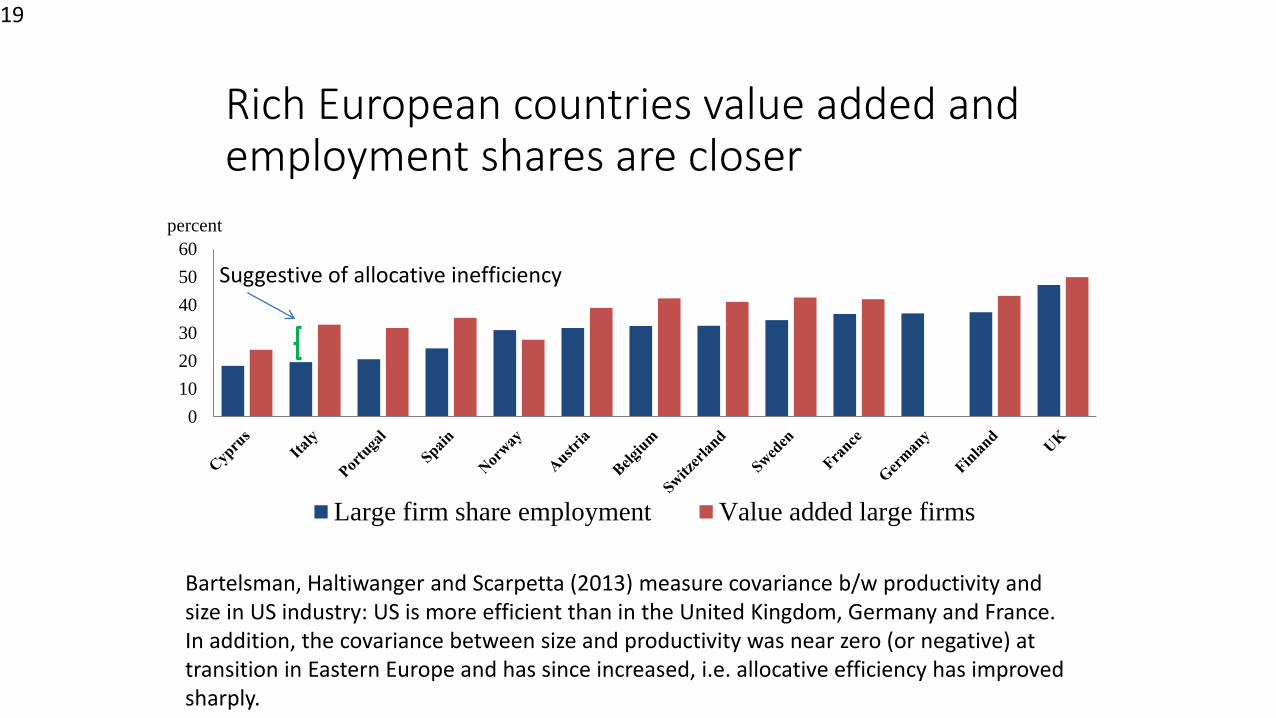

Rich European countries value added and employment shares are closer

0

10

20

30

40

50

60

percent

Large firm share employment Value added large firms

19

Suggestive of allocative inefficiency

Bartelsman, Haltiwanger and Scarpetta (2013) measure covariance b/w productivity and size in US industry: US is more efficient than in the United Kingdom, Germany and France. In addition, the covariance between size and productivity was near zero (or negative) at transition in Eastern Europe and has since increased, i.e. allocative efficiency has improved sharply.

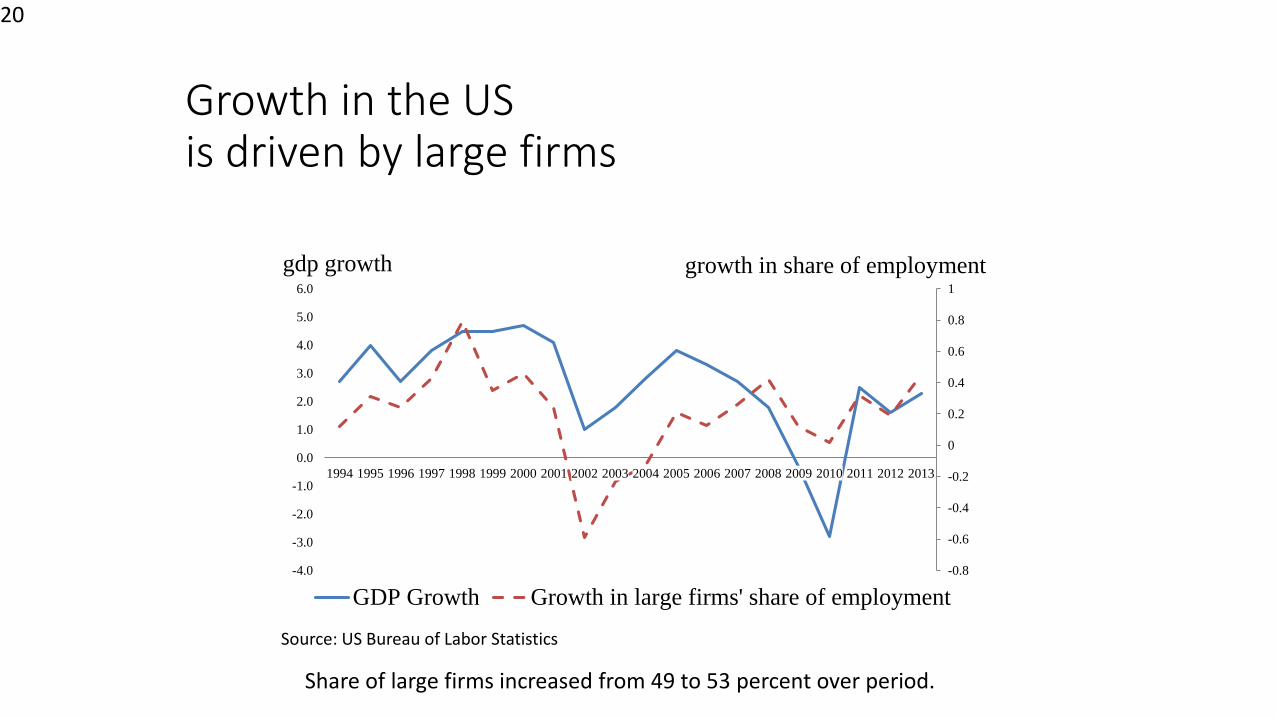

Growth in the US is driven by large firms

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

growth in share of employmentgdp growth

GDP Growth Growth in large firms' share of employment

20

Share of large firms increased from 49 to 53 percent over period.

Source: US Bureau of Labor Statistics

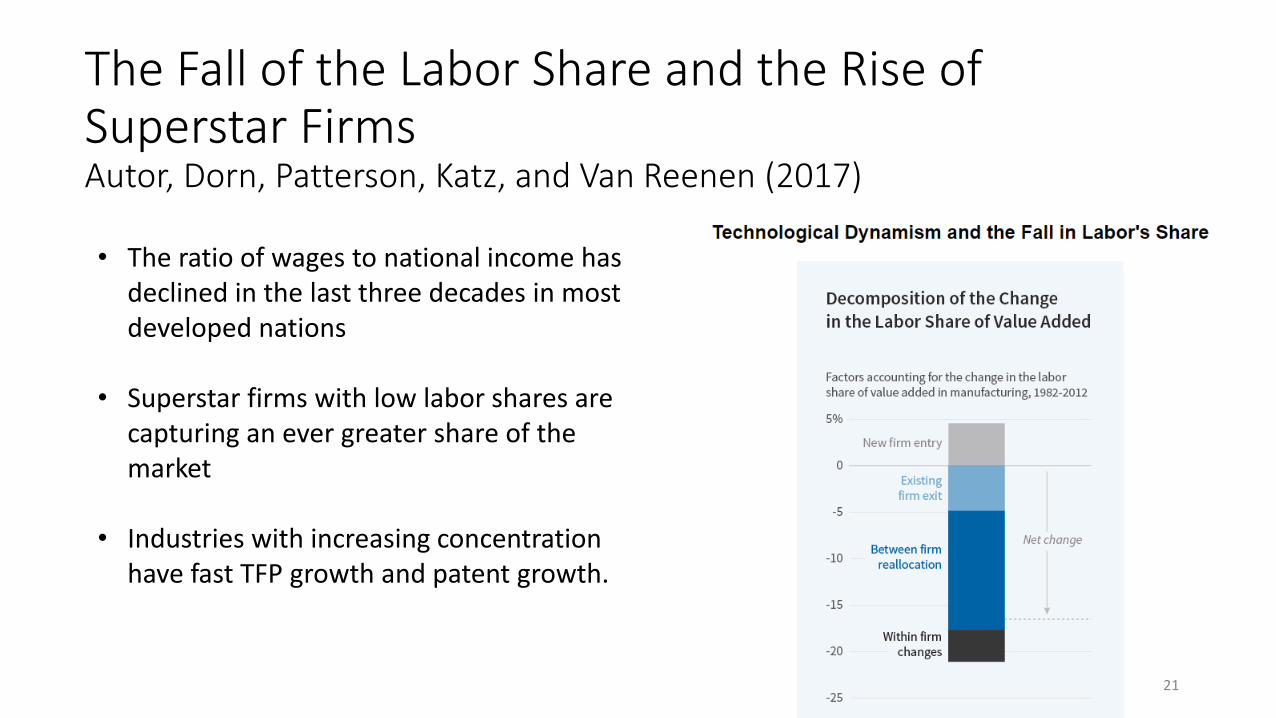

The Fall of the Labor Share and the Rise of Superstar FirmsAutor, Dorn, Patterson, Katz, and Van Reenen (2017)

• The ratio of wages to national income has declined in the last three decades in most developed nations

• Superstar firms with low labor shares are capturing an ever greater share of the market

• Industries with increasing concentration have fast TFP growth and patent growth.

21

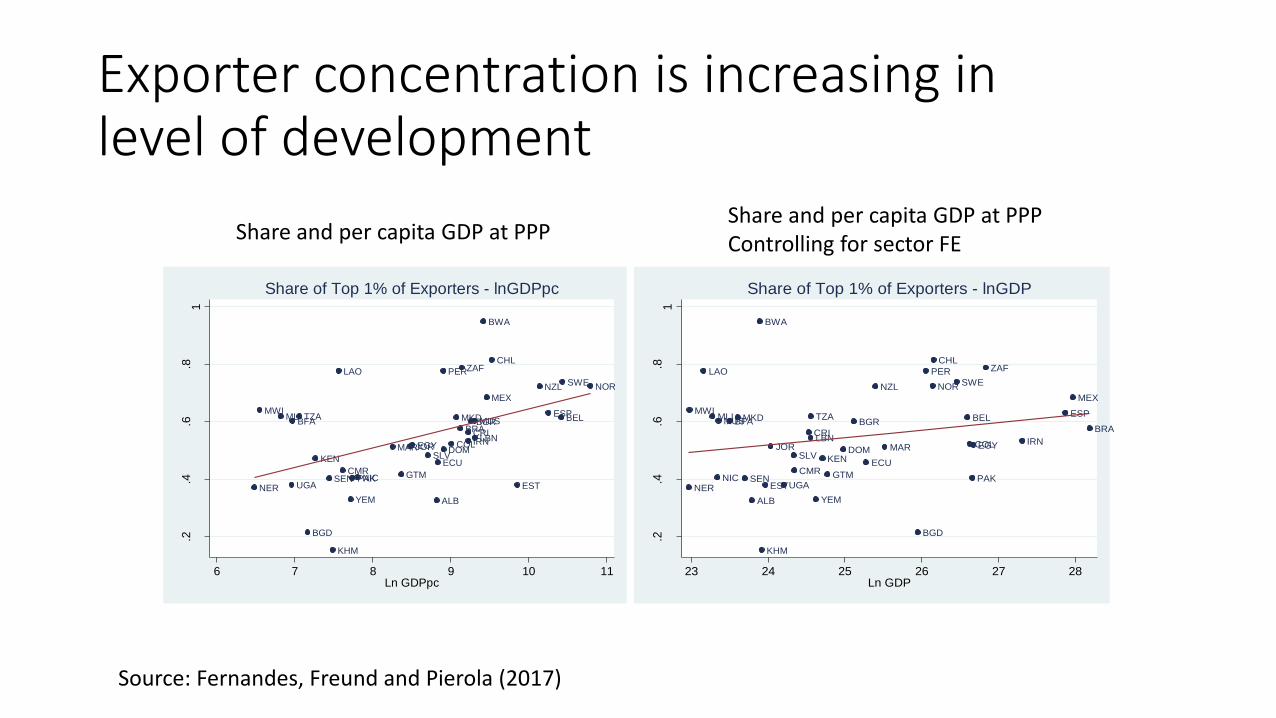

Exporter concentration is increasing in level of development

ALB

BELBFA

BGD

BGRBRA

BWA

CHL

CMR

COL

CRI

DOM

ECU

EGY

ESP

EST

GTM

IRNJOR

KEN

KHM

LAO

LBNMAR

MEX

MKDMLIMUS

MWI

NERNIC

NORNZL

PAK

PER

SEN

SLV

SWE

TZA

UGA

YEM

ZAF

.2.4

.6.8

1

Sh

are

Top

1%

6 7 8 9 10 11Ln GDPpc

Share of Top 1% of Exporters - lnGDPpc

ALB

BELBFA

BGD

BGRBRA

BWA

CHL

CMR

COL

CRI

DOM

ECU

EGY

ESP

EST

GTM

IRNJOR

KEN

KHM

LAO

LBNMAR

MEX

MKDMLIMUS

MWI

NERNIC

NORNZL

PAK

PER

SEN

SLV

SWE

TZA

UGA

YEM

ZAF

.2.4

.6.8

1

Sh

are

Top

1%

23 24 25 26 27 28Ln GDP

Share of Top 1% of Exporters - lnGDP

Share and per capita GDP at PPPShare and per capita GDP at PPPControlling for sector FE

Source: Fernandes, Freund and Pierola (2017)

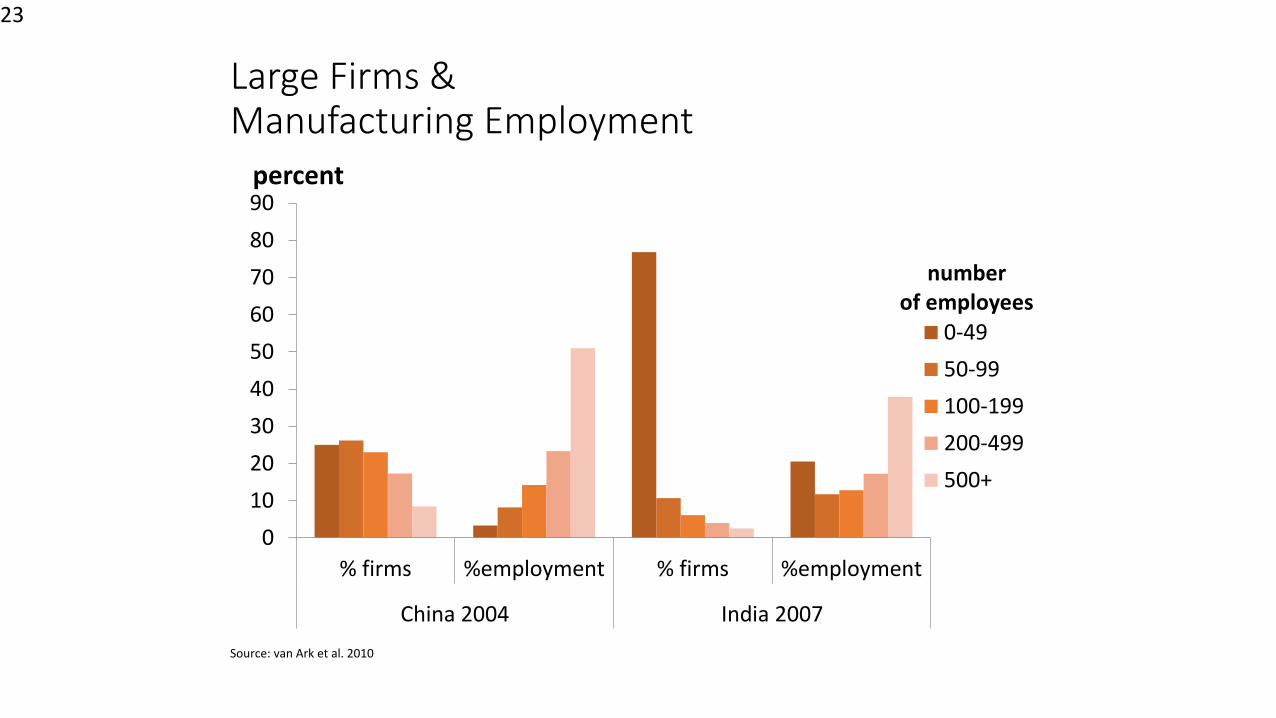

Large Firms & Manufacturing Employment

0

10

20

30

40

50

60

70

80

90

% firms %employment % firms %employment

China 2004 India 2007

number of employees

percent

0-49

50-99

100-199

200-499

500+

23

Source: van Ark et al. 2010

Research confirms importance of large firms

• Cross country research: Average firm size increases with development: 10 percent increase in per capita income associated with a 2.6 percent increase in average firm size. (Bento and Restuccia 2014).

• The myth of the missing middle--Large firms have higher average productivity and that the fraction of missing firms is increasing in firm size (Hsieh and Olken 2014).

• Developing countries export less because they are missing the largest superproductive firms—the firm-size distribution is truncated at the top. Fernandes, Freund, and Pierola (2015).

24

Superstar firms are good for growth, but create extreme wealth

The force of trade is present in North & South

25

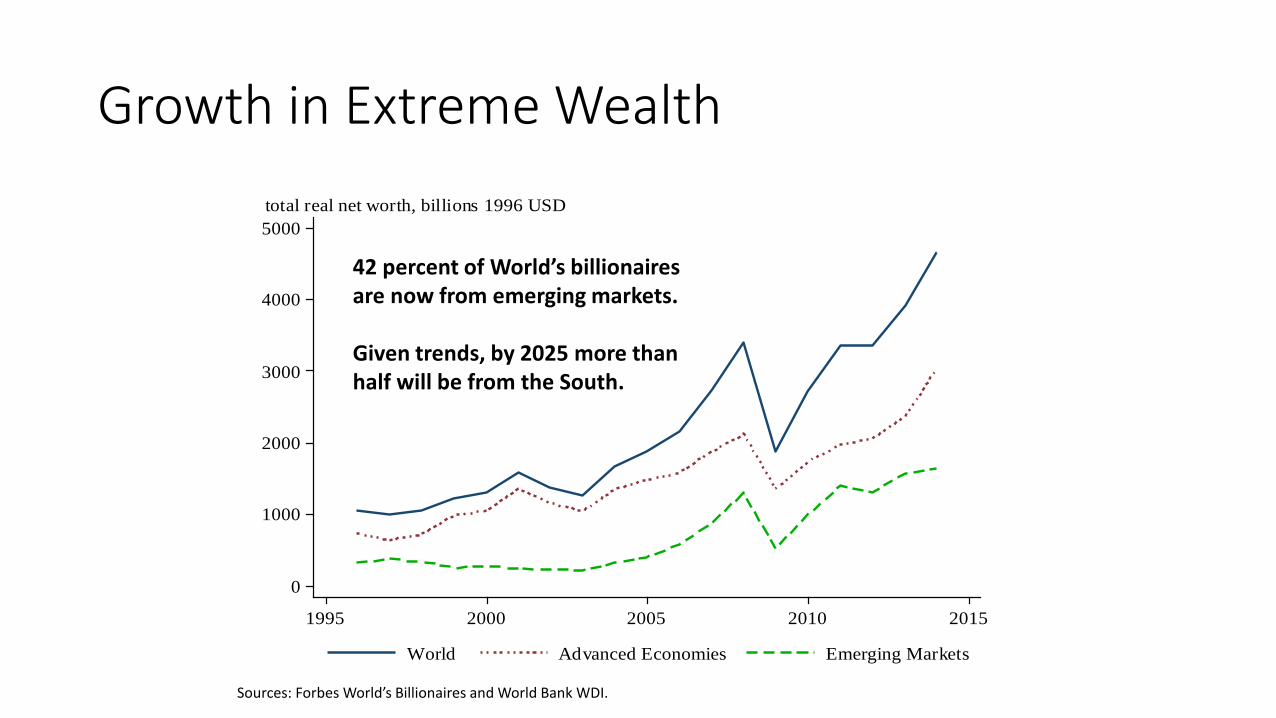

Growth in Extreme Wealth

0

1000

2000

3000

4000

5000

1995 2000 2005 2010 2015

World Advanced Economies Emerging Markets

total real net worth, billions 1996 USD

42 percent of World’s billionaires are now from emerging markets.

Given trends, by 2025 more than half will be from the South.

Sources: Forbes World’s Billionaires and World Bank WDI.

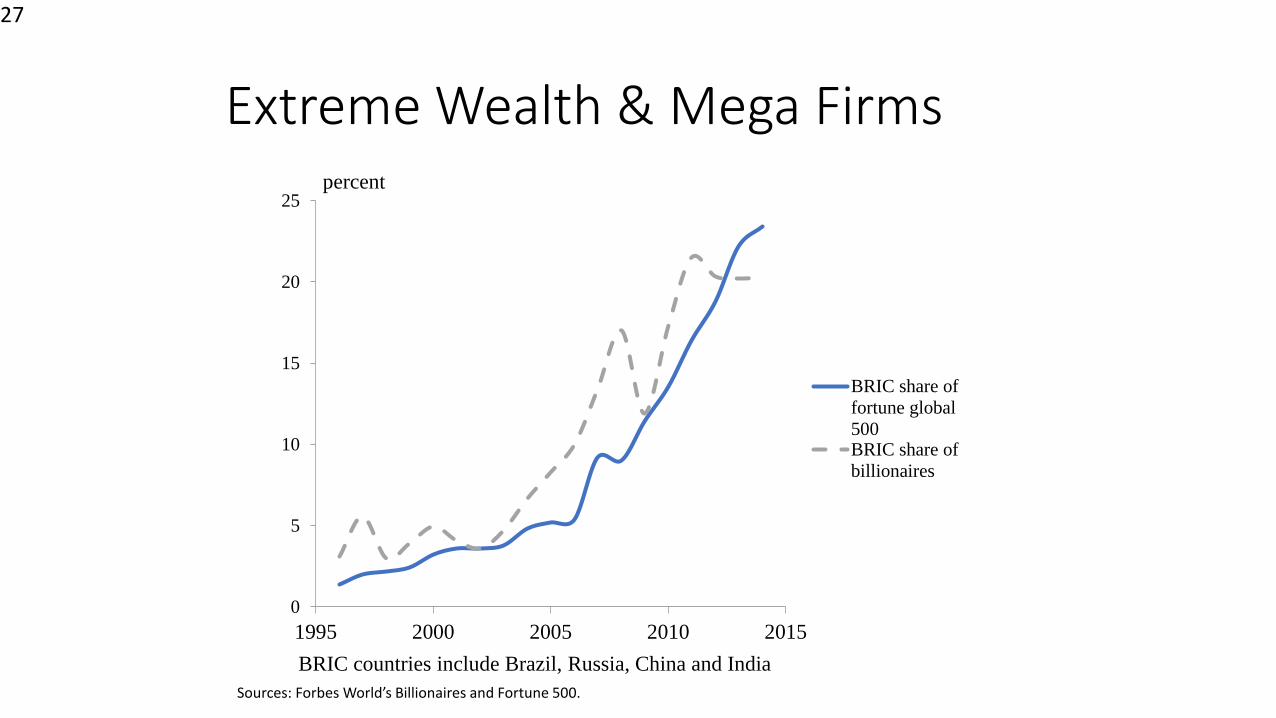

Extreme Wealth & Mega Firms

27

0

5

10

15

20

25

1995 2000 2005 2010 2015

percent

BRIC share of

fortune global

500BRIC share of

billionaires

BRIC countries include Brazil, Russia, China and India

Sources: Forbes World’s Billionaires and Fortune 500.

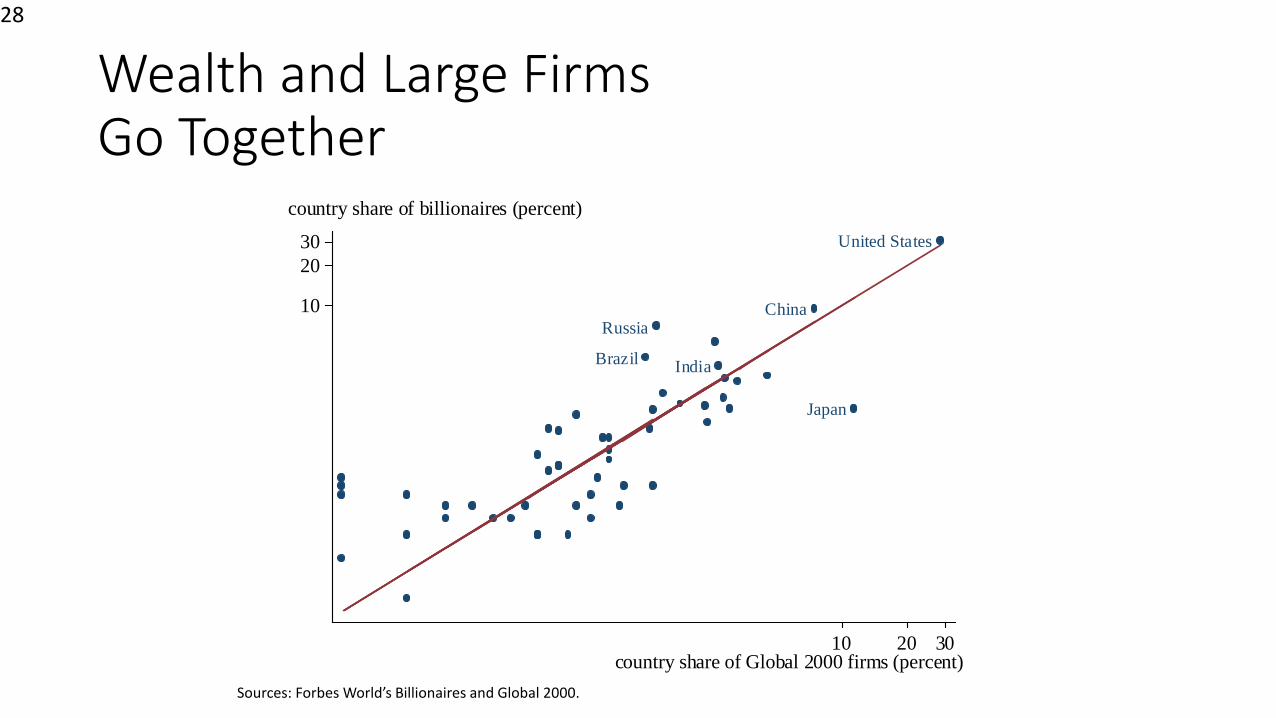

Wealth and Large Firms Go Together

28

Brazil

China

India

Japan

Russia

United States

10

20

30

10 20 30country share of Global 2000 firms (percent)

country share of billionaires (percent)

Sources: Forbes World’s Billionaires and Global 2000.

Where does extreme wealth come from?

29

Who are the Superrich?

• Inheritors

• Self-made• Company founders

• Executives

• Politically connected/resource based

• Finance/real estate

30

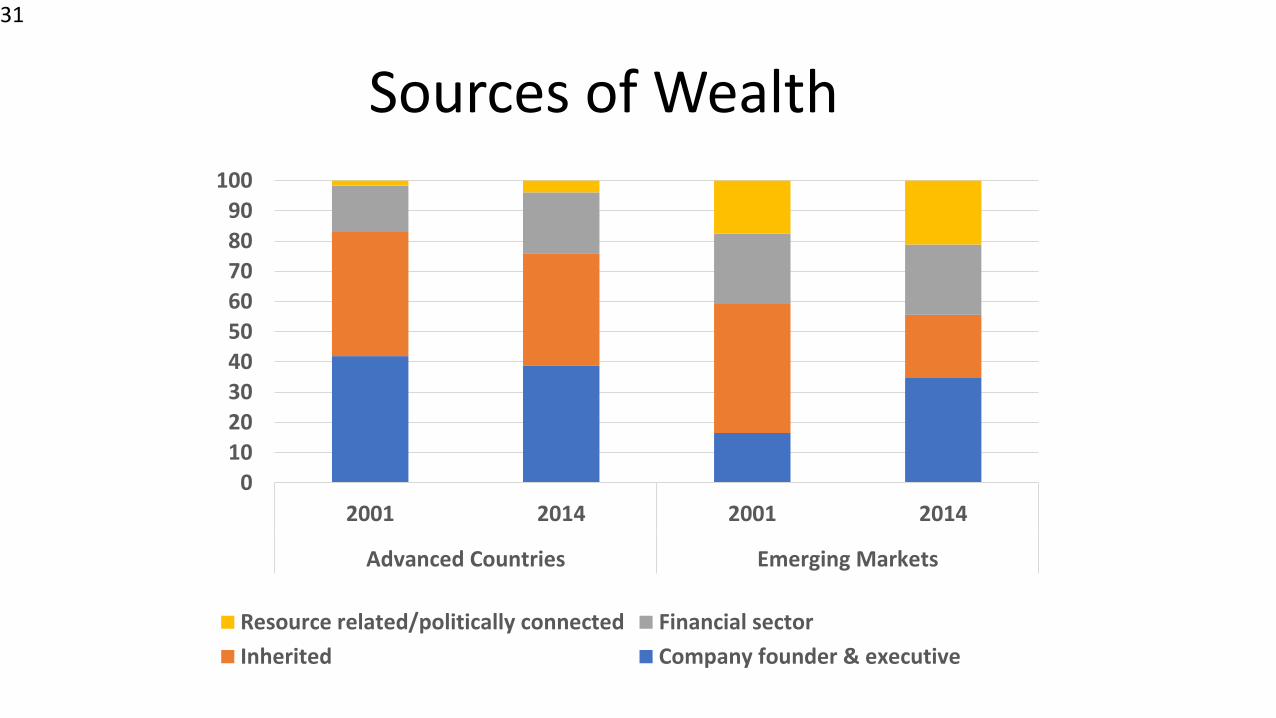

Sources of Wealth

31

0

10

20

30

40

50

60

70

80

90

100

2001 2014 2001 2014

Advanced Countries Emerging Markets

Resource related/politically connected Financial sector

Inherited Company founder & executive

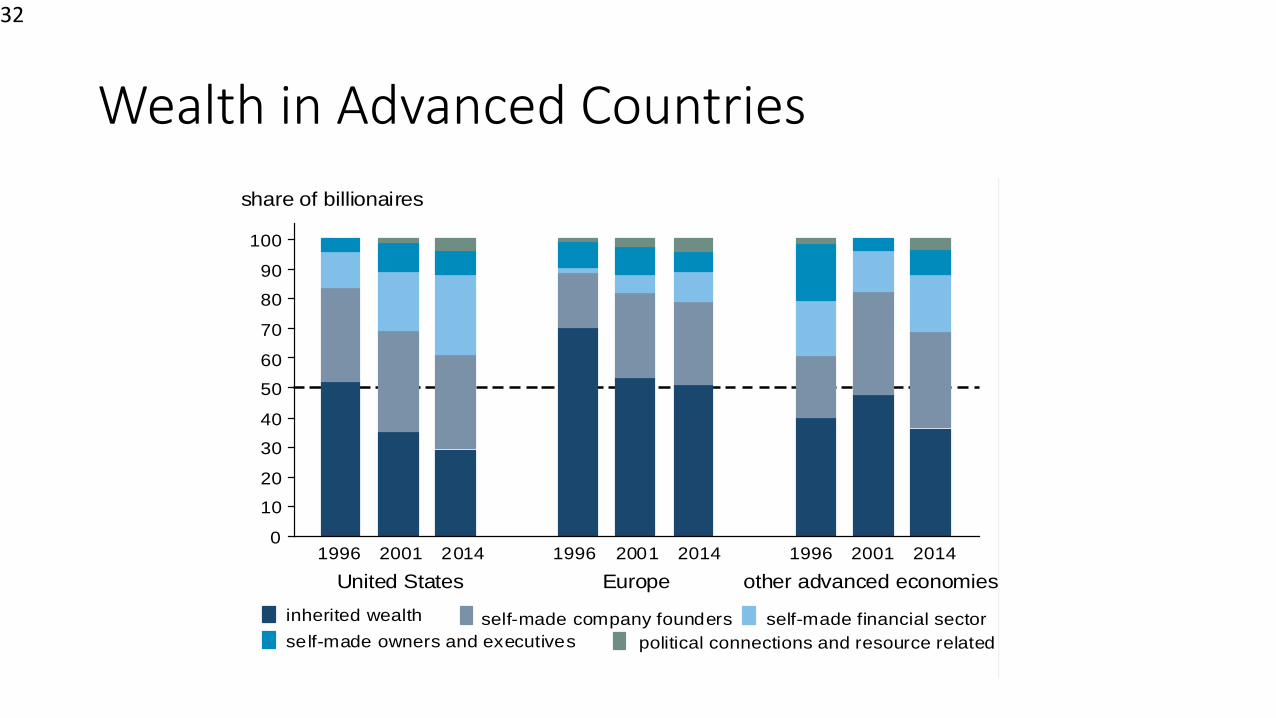

Wealth in Advanced Countries

32

0

10

20

30

40

50

60

70

80

90

100

United States Europe other advanced economies

1996 2001 2014 1996 2001 2014 1996 2001 2014

share of billionaires

inherited wealth self-made company founders self-made financial sector

self-made owners and executives political connections and resource related

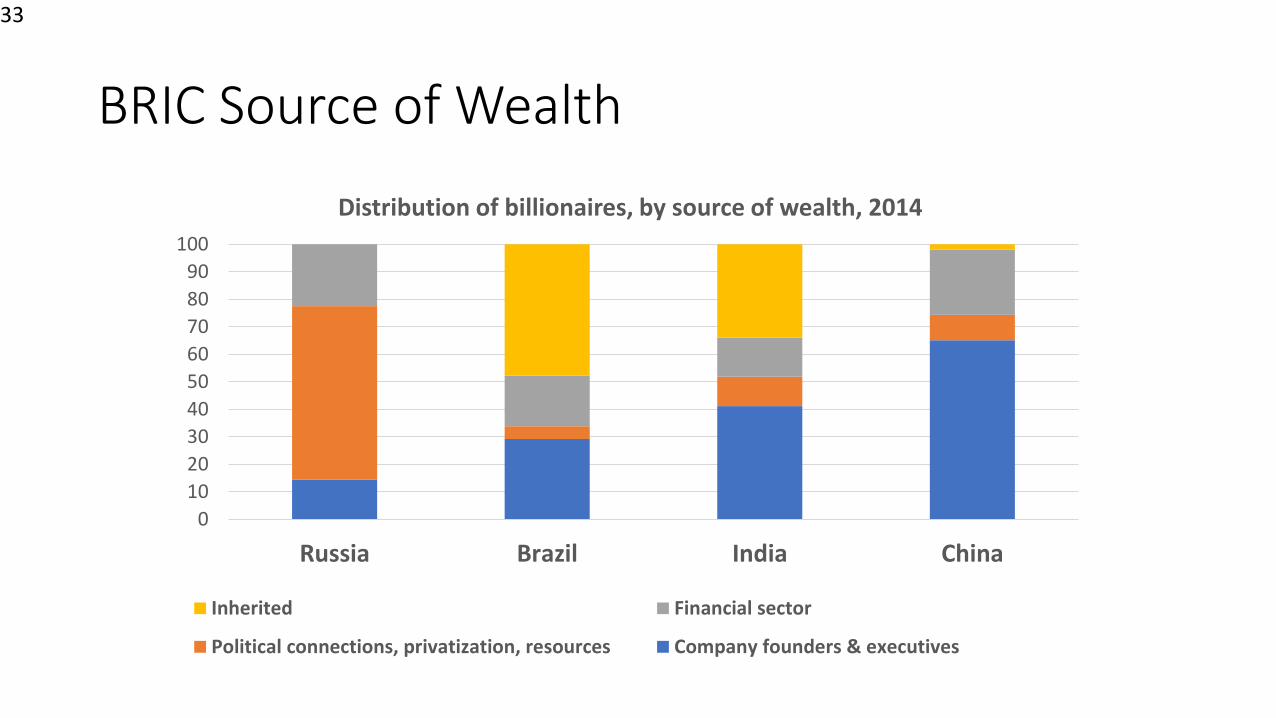

BRIC Source of Wealth

33

0

10

20

30

40

50

60

70

80

90

100

Russia Brazil India China

Distribution of billionaires, by source of wealth, 2014

Inherited Financial sector

Political connections, privatization, resources Company founders & executives

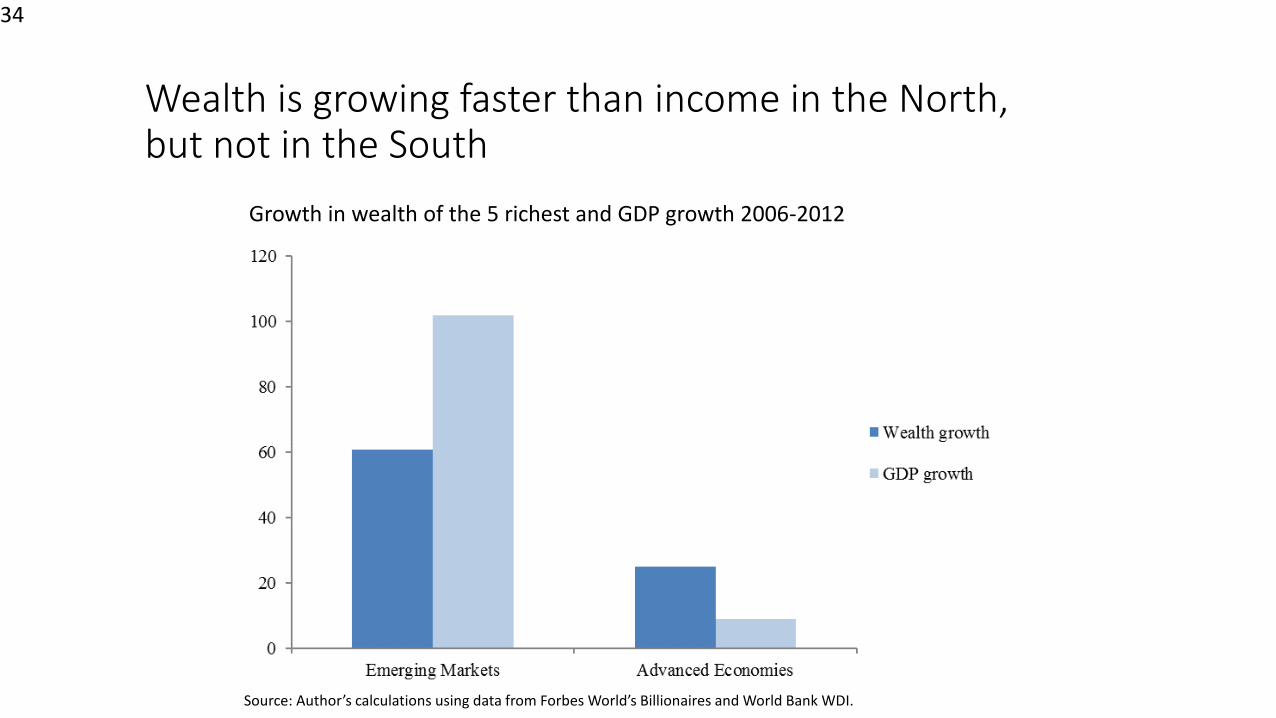

Wealth is growing faster than income in the North, but not in the South

34

Growth in wealth of the 5 richest and GDP growth 2006-2012

Source: Author’s calculations using data from Forbes World’s Billionaires and World Bank WDI.

Policy Implications

• Promote entrepreneurship • Property rights, free entry and openness to trade and foreign investment

• Limit cronyism • Transparent privatization & government procurement, competition policy

• Tax more heavily less productive sources of wealth• Inheritance & (some) finance

35

Why the backlash against globalization now?

36

The backlash can’t be only about trade

• Inequality and jobs in advanced countries

• Same shocks, trade and technology, but inequality not up everywhere

• Timing—trade surged from 1995-2005 and then stagnated

• Post financial crisis slowdown

• The rise of China

• New issues—subsidies, investment, SOEs, technology

Other pressures on inequality in Anglo countries• Policies: Tax cuts, deregulation, de-unionization, rise of finance,

lower spending on labor adjustment

• Social: Assortative mating, private schools, tutoring

• Fear around immigration and terrorism

38

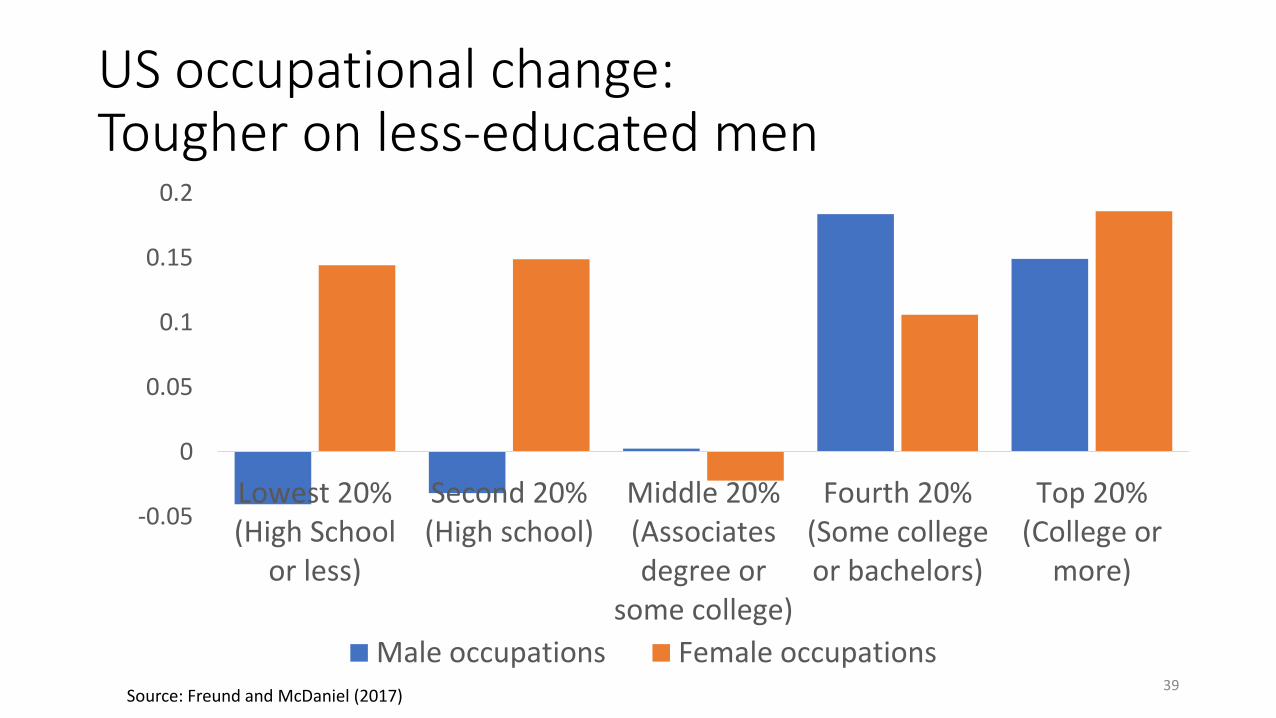

US occupational change: Tougher on less-educated men

-0.05

0

0.05

0.1

0.15

0.2

Lowest 20%(High School

or less)

Second 20%(High school)

Middle 20%(Associatesdegree or

some college)

Fourth 20%(Some collegeor bachelors)

Top 20%(College or

more)

Male occupations Female occupationsSource: Freund and McDaniel (2017)

39

Structural change is difficult

Discontent among workers

But, do workers really blame trade?

40

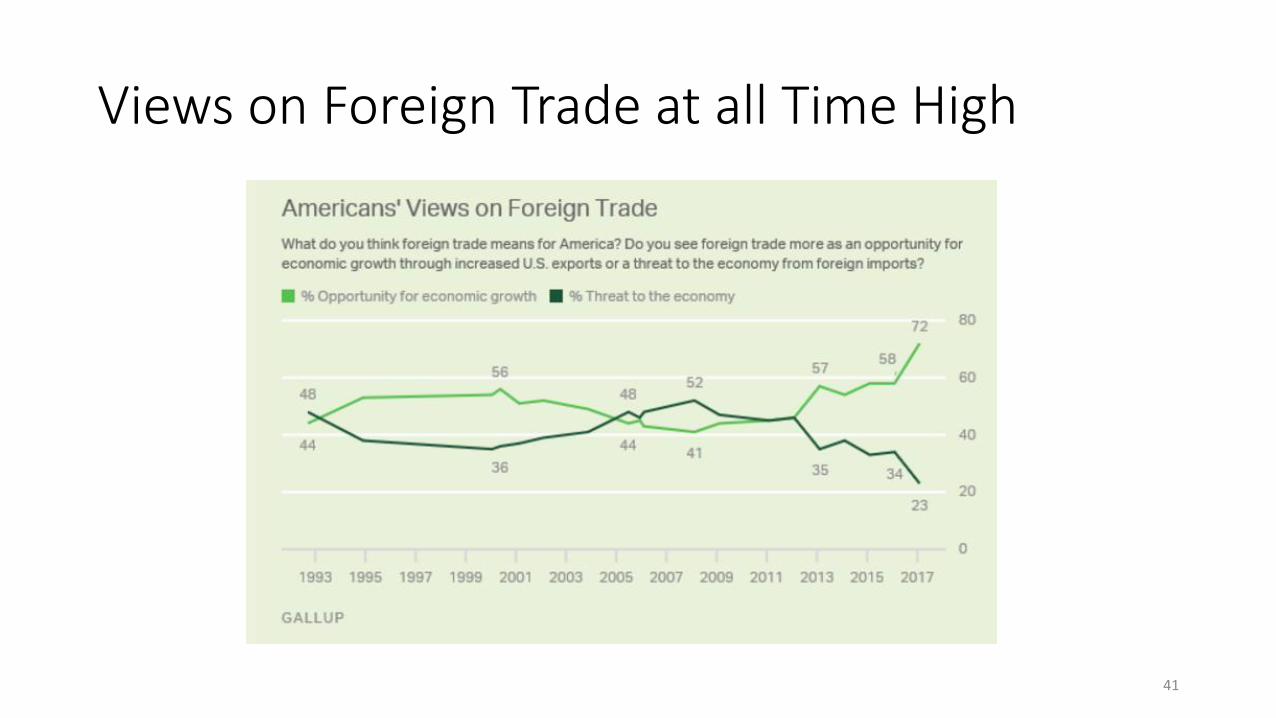

Views on Foreign Trade at all Time High

41

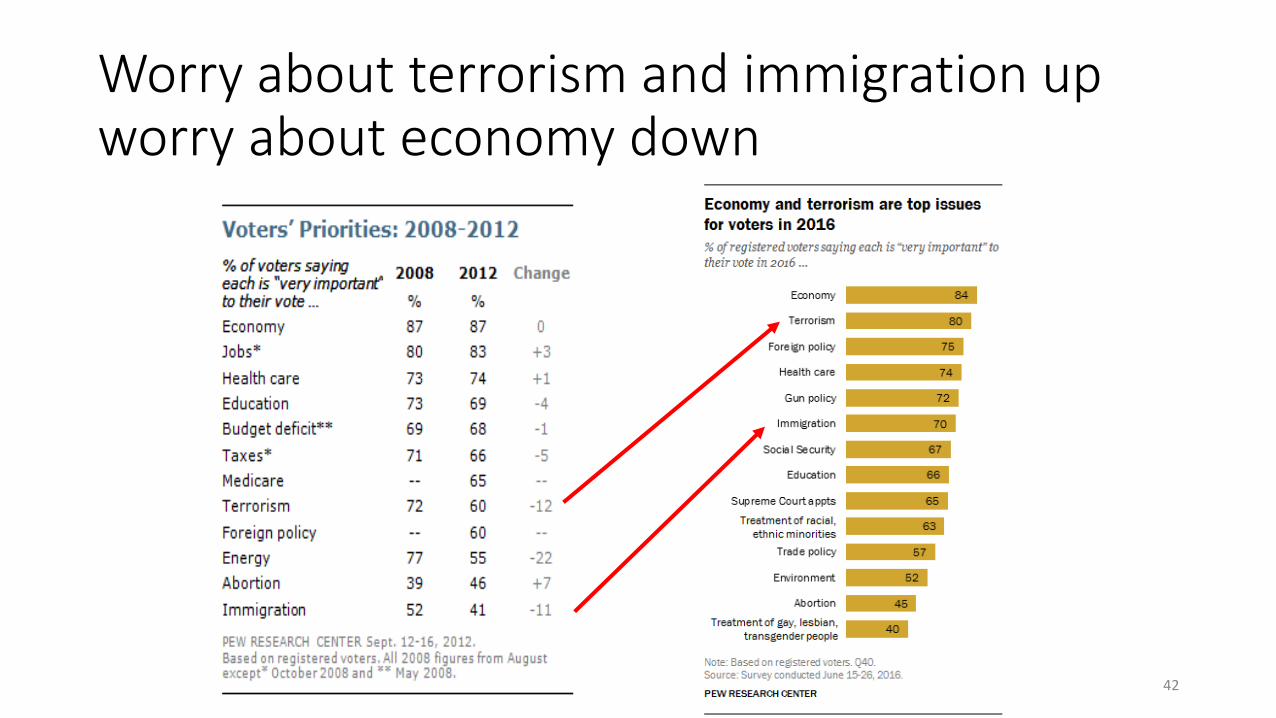

Worry about terrorism and immigration up worry about economy down

42

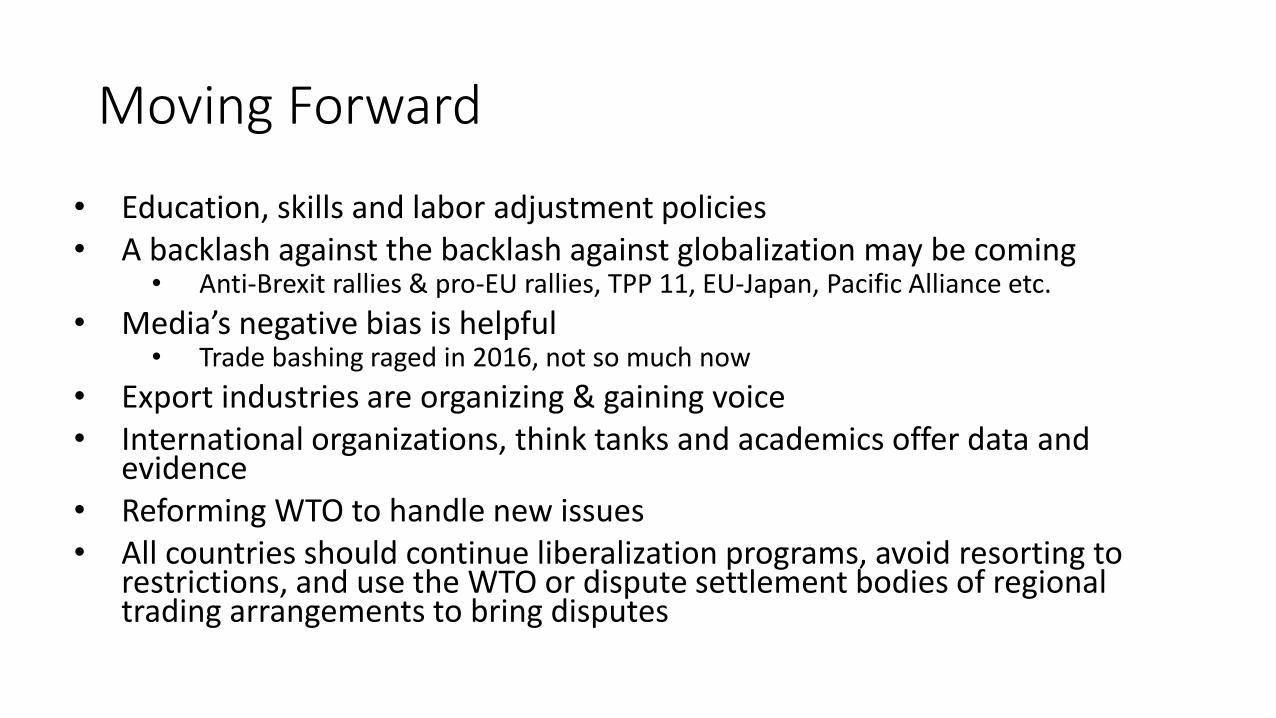

Moving Forward

• Education, skills and labor adjustment policies• A backlash against the backlash against globalization may be coming

• Anti-Brexit rallies & pro-EU rallies, TPP 11, EU-Japan, Pacific Alliance etc.

• Media’s negative bias is helpful• Trade bashing raged in 2016, not so much now

• Export industries are organizing & gaining voice• International organizations, think tanks and academics offer data and

evidence• Reforming WTO to handle new issues• All countries should continue liberalization programs, avoid resorting to

restrictions, and use the WTO or dispute settlement bodies of regional trading arrangements to bring disputes

Thank you!

Follow me on twitter

@carolinefreund

44

Extras…

45

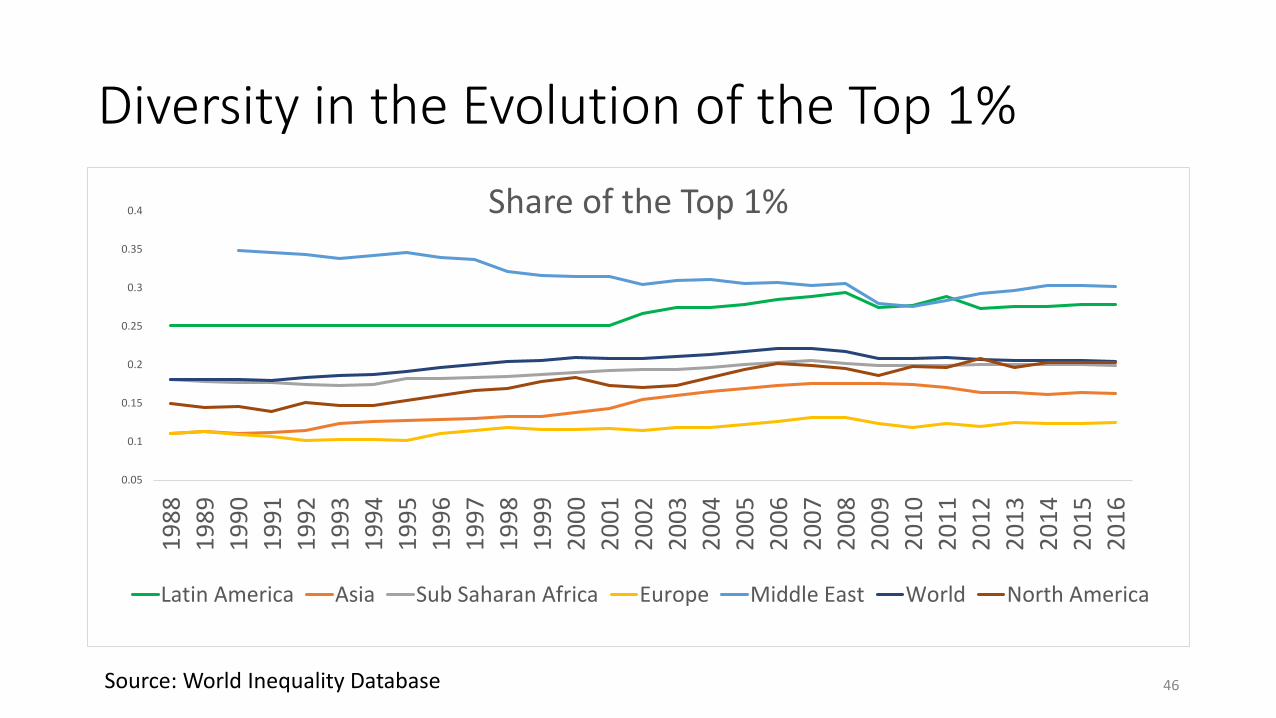

Diversity in the Evolution of the Top 1%

Source: World Inequality Database

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Share of the Top 1%

Latin America Asia Sub Saharan Africa Europe Middle East World North America

46

0

0.05

0.1

0.15

0.2

0.25

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

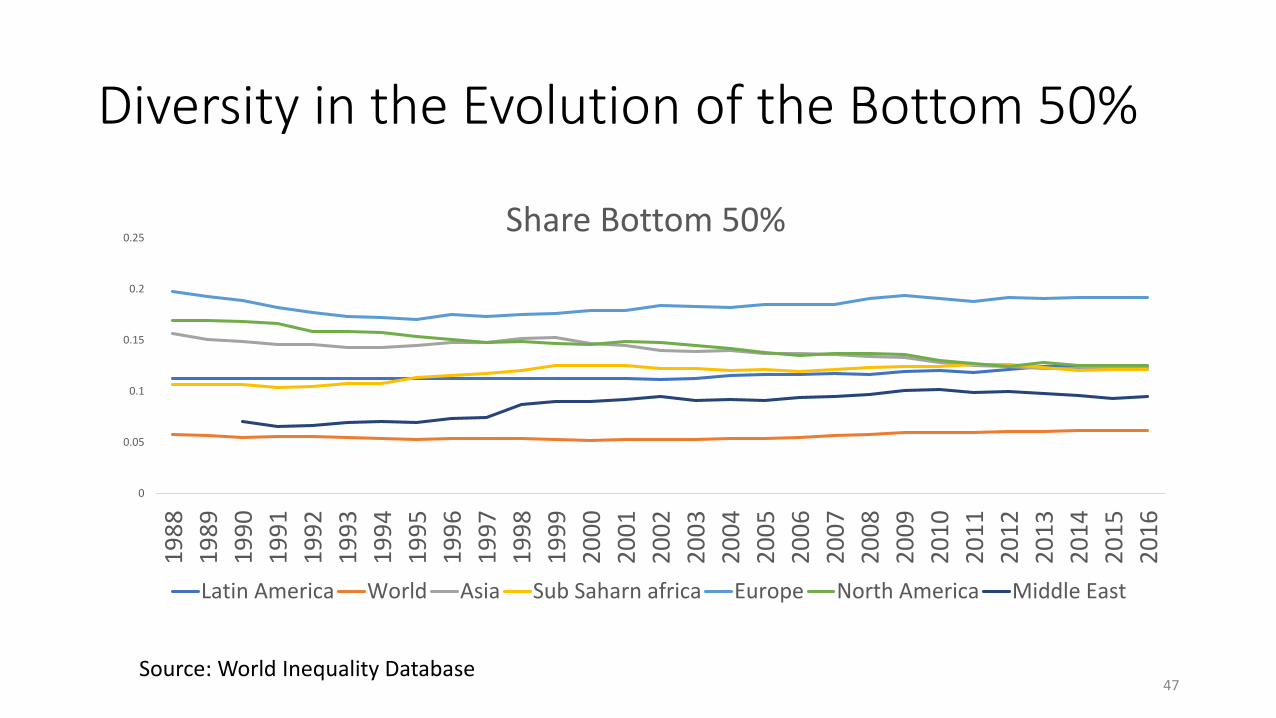

Share Bottom 50%

Latin America World Asia Sub Saharn africa Europe North America Middle East

Diversity in the Evolution of the Bottom 50%

Source: World Inequality Database47

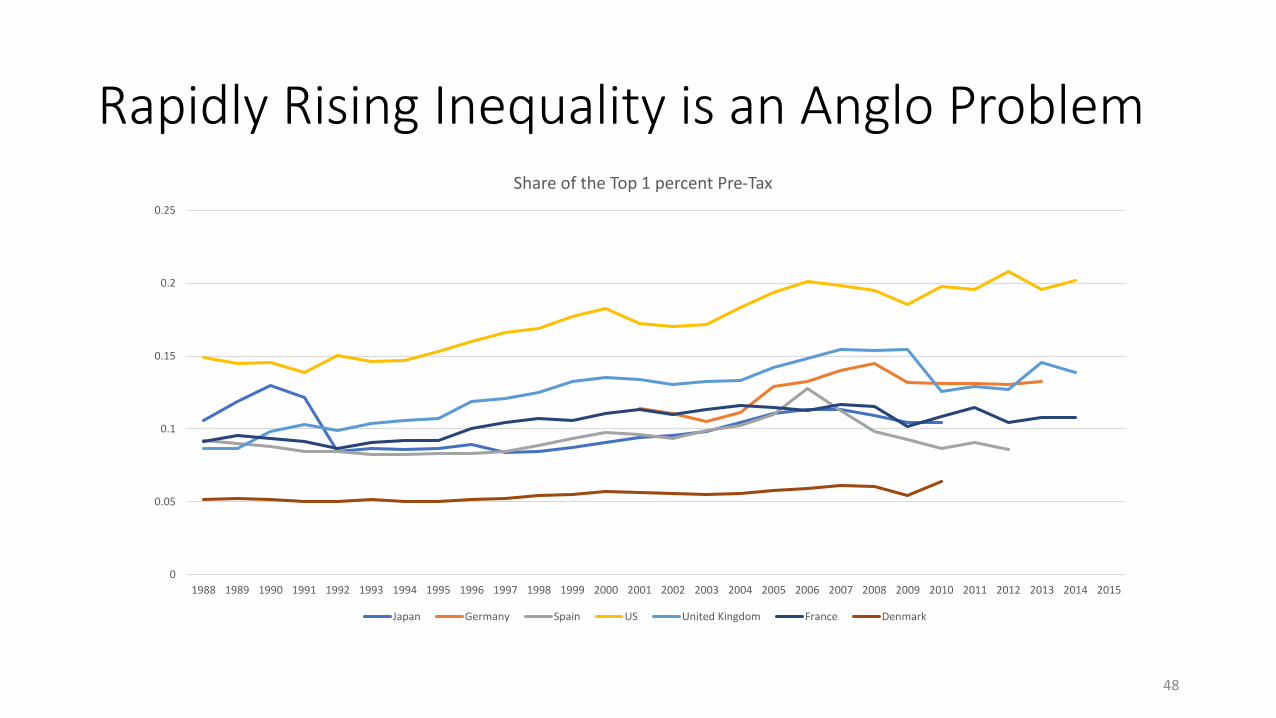

Rapidly Rising Inequality is an Anglo Problem

0

0.05

0.1

0.15

0.2

0.25

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Share of the Top 1 percent Pre-Tax

Japan Germany Spain US United Kingdom France Denmark

48