Embed Size (px)

Citation preview

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT

POLICY ISSUES IN INTERNATIONAL TRADE AND COMMODITIES

STUDY SERIES No. 19

TRADE IN SERVICES – MARKET ACCESS OPPORTUNITIES AND THE BENEFITS OF LIBERALIZATION FOR DEVELOPING

ECONOMIES

by

Greg McGuire

Senior Economist Economic Insights Pty Ltd.

1st Floor, 50 Leichhardt St., Spring Hill Brisbane, Queensland, 4000

Australia

UNITED NATIONS

New York and Geneva, 2002

ii

NOTE

The views expressed in this study are those of the author and do not necessarily reflect the views of the United Nations.

The designations employed and the presentation of the material do not imply the expression of any opinion whatsoever on the part of the United Nations Secretariat concerning the legal status of any country, territory, city or area, or of its authorities, or concerning the delimitation of its frontiers or boundaries.

Material in this publication may be freely quoted or reprinted, but acknowledgement is requested, together with a reference to the document number. A copy of the publication containing the quotation or reprint should be sent to the UNCTAD secretariat:

Chief Trade Analysis Branch

Division on International Trade in Goods and Services, and Commodities United Nations Conference on Trade and Development

Palais des Nations CH-1211 Geneva

UNCTAD/ITCD/TAB/20

UNITED NATIONS PUBLICATION

Sales No. E.02.II.D.9

ISBN 92-1-112556-1

ISSN 1607-8291

© Copyright United Nations 2002 All rights reserved

iii

ABSTRACT

The service sector is the most important sector for most developing economies. It is the largest contributor to gross domestic product, production and employment. Since it is such an important sector, developing economies need to identify their comparative advantage in services and potential export markets.

Developing economies have a comparative advantage in labour services. They have an

abundance of low and semi-skilled labour that is a major input into tourism, construction and transport services. New potential export opportunities are also emerging in communications and computer services. However, the export of many of these services is limited by many restrictions on the temporary movement of labour imposed by their trading partners through domestic regulation. Developing economies can improve their export revenues by specifically identifying these restrictions and, where a movement of labour is required, promote the benefits to potential export markets of services trade liberalization.

Developing economies are projected to be better off by US$ 130 billion from services

trade liberalization. Consistent with similar modelling exercises for trade in goods, while there are some benefits from improving market access to foreign markets, most of the benefits come for liberalizing one’s own market. As developing economies remove their restrictions, their service sectors develop, primarily funded by foreign direct investment, and they become major exporters of services. The main restrictions on service suppliers that are preventing developing economies from realizing these benefits are limits on foreign direct investment, stringent licensing requirements and restrictions on expanding operations.

iv

ACKNOWLEDGEMENTS

I would like to thank UNCTAD for inviting me to write a paper on a topic that is a major issue for developing economies in the new round of WTO negotiations. I am grateful to UNCTAD for their valuable comments, particularly Sam Laird, and Jenifer Tacardon-Mercado for organizing the final publication of the paper. Dr. John Fallon from Economic Insights Pty Ltd also provided some extremely useful comments. I originally presented the paper at the Workshop on Market Access at the United Nations in New York on 8-9 January 2002 and the comments provided by the participants are also gratefully acknowledged.

The paper draws heavily on the work of the Australian Productivity Commission who, in recent years, have been at the forefront in measuring and modelling the benefits of services trade liberalization.

v

CONTENTS

INTRODUCTION............................................................................................................1 I. AN OVERVIEW OF INTERNATIONAL TRADE IN SERVICES...................2 II. MARKET ACCESS FOR DEVELOPING ECONOMIES.................................4 A. Developing economies and comparative advantage ........................................4

B. Market access and the movement of natural persons ......................................4 C. Market access and tourism services................................................................6 D. Market access and new export opportunities ..................................................7

III. WHAT’S AT STAKE FOR DEVELOPING ECONOMIES?............................9 IV. WHAT ARE THE RESTRICTIONS AND THEIR EFFECTS?......................13

A. Measuring restrictions on trade in services ...................................................13 1. Trade restrictiveness index results for developing economies...............16 2. Restrictions on services and GDP per capita .......................................19 B. The effect of restrictions on the price and cost of services ............................21 1. Results from price and cost estimations...............................................22 2. Benefits of removing restrictions on market access..............................26 V. LIBERALIZATION, EFFICIENCY AND THE DOMESTIC SERVICE SECTOR...........................................................................................27 A. The importance of the financial services sector.............................................30 B. Unilateral and multilateral liberalization........................................................31 VI. CONCLUSION...................................................................................................32 REFERENCES ..............................................................................................................33

vi

Tables

1. Effects of liberalizing trade in services...................................................................10 2. Effects of partial liberalization on world real income .............................................11 3. An example of classifying trade restrictions on banking services ............................14 4. Price and cost raising effect of restrictions for developing economies ....................24 5. Price and cost raising effect of restrictions for developed economies .....................25

Figures 1. World exports and imports of services for selected regions, 2000............................2 2. An illustration of the results from the trade restrictiveness index............................15 3. Banking services ...................................................................................................16 4. Distribution services..............................................................................................17 5. Maritime services..................................................................................................18 6. Professional services .............................................................................................19 7. Telecommunications services ................................................................................20 8. GDP per capita at PPP and average foreign trade restrictiveness index scores for the service sector ..................................................................................21 9. GDP per capita at PPP and foreign trade restrictiveness index scores for banking services ..............................................................................................22 10. GDP per capita at PPP and foreign trade restrictiveness index scores for telecommunications services............................................................................23

Boxes

1. How are services traded? ........................................................................................3 2. Developing economies, market access and the GATS..............................................7 3. Foreign direct investment and developing economies.............................................29

1

The economic and trade performanceof an economy is dependent on the efficiencyof its service sector. Not only do economiesderive the bulk of their employment and in-come from the service sector, but also manyservices � financial, telecommunicationsand transport � are vital intermediate inputsfor other sectors. The international competi-tiveness of traditional sectors of developingeconomies is heavily dependent on access toservices at world prices. The best guaranteethat services will be supplied at world pricesis to open an economy to the pressures andopportunities of international competition ortrade and investment liberalization.

Developing economies benefit fromliberalization by gaining market access andexporting those services in which they havea relative strength or comparative advantage.Access to foreign services markets is impor-tant for developing countries to enable themto improve their export earnings and the em-ployment opportunities of their nationals, aswell as increase the efficiency in their owneconomies so as to mobilize resources fordevelopment. Global economic integrationand technological developments have in-creased international trade in services and areproviding many export opportunities for de-veloping economies.

Developing economies have the po-tential to reap greater benefits from liberali-zation than developed economies, primarilyby liberalizing their own service sector. Do-mestic liberalization permits resources to beallocated to their most efficient uses. A moreefficient allocation of resources improves the

price, choice and quality of services, andoverall economic capacity, which facilitatestrade in agriculture and manufacturing � atraditional export earner for developingeconomies. Central to building economiccapacity and progressing development is anefficient financial services sector. Liberal andappropriately regulated financial servicessectors efficiently mobilize savings for in-vestment, provide payment mechanisms forbusiness transactions and improve the stabil-ity of financial institutions.

Sophisticated general equilibriummodelling of liberalizing trade in servicesprovide insights into the projected real-in-come gains from a more efficient allocationof resources for development. The resultsestablish a framework for negotiating priori-ties when the gains from liberalizing tradein services are compared with those for agri-culture and manufacturing. They also providevaluable information to negotiators andpolicy makers on the potential gains fromimproved market access as well as on ap-proaches to liberalization.

The greatest benefits will come fromliberalizing all services markets � domesticand foreign. Politically, this is extremely dif-ficult, but a multilateral framework thatachieves market access in foreign marketscan be an impetus for liberalizing one�s ownmarket. While this paper covers market ac-cess in foreign markets, results from empiri-cal research indicate that most of the gainsare from domestic liberalization � what youdo for yourself is more important than whatothers do for you.

INTRODUCTION

2

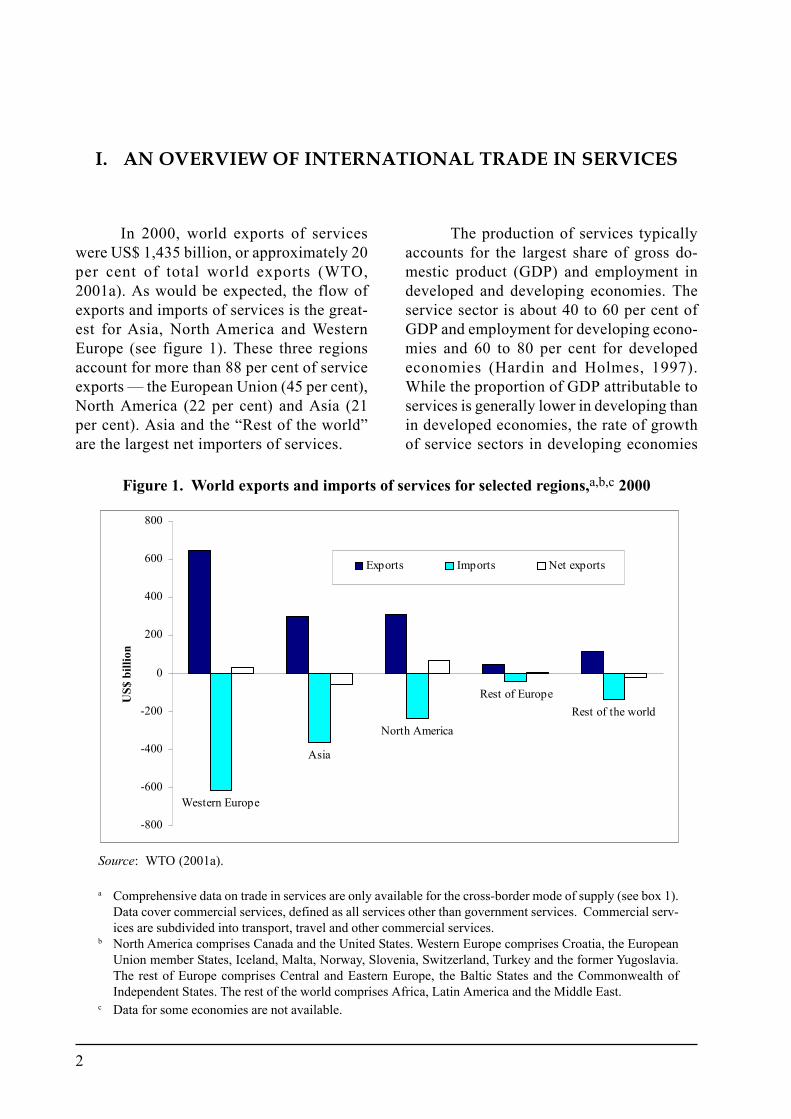

In 2000, world exports of serviceswere US$ 1,435 billion, or approximately 20per cent of total world exports (WTO,2001a). As would be expected, the flow ofexports and imports of services is the great-est for Asia, North America and WesternEurope (see figure 1). These three regionsaccount for more than 88 per cent of serviceexports � the European Union (45 per cent),North America (22 per cent) and Asia (21per cent). Asia and the �Rest of the world�are the largest net importers of services.

The production of services typicallyaccounts for the largest share of gross do-mestic product (GDP) and employment indeveloped and developing economies. Theservice sector is about 40 to 60 per cent ofGDP and employment for developing econo-mies and 60 to 80 per cent for developedeconomies (Hardin and Holmes, 1997).While the proportion of GDP attributable toservices is generally lower in developing thanin developed economies, the rate of growthof service sectors in developing economies

I. AN OVERVIEW OF INTERNATIONAL TRADE IN SERVICES

Figure 1. World exports and imports of services for selected regions,a,b,c 2000

Source: WTO (2001a).

a Comprehensive data on trade in services are only available for the cross-border mode of supply (see box 1).Data cover commercial services, defined as all services other than government services. Commercial serv-ices are subdivided into transport, travel and other commercial services.

b North America comprises Canada and the United States. Western Europe comprises Croatia, the EuropeanUnion member States, Iceland, Malta, Norway, Slovenia, Switzerland, Turkey and the former Yugoslavia.The rest of Europe comprises Central and Eastern Europe, the Baltic States and the Commonwealth ofIndependent States. The rest of the world comprises Africa, Latin America and the Middle East.

c Data for some economies are not available.

Western Europe

Asia

North America

Rest of EuropeRest of the world

-800

-600

-400

-200

0

200

400

600

800

US$

bill

ion

Exports Imports Net exports

3

is faster than that in developed economies(OECD, 1999).

The importance of services to aneconomy is even greater than that reflectedin direct sectoral shares of GDP and employ-ment because services are important inputsfor all aspects of processing and production.The growth of an economy�s service sectoris strongly associated with product speciali-zation, income growth and economic mod-ernization. Services provide much of the nec-essary infrastructure for investment and eco-nomic growth, ensuring that their efficientdelivery is an important means of improvingan economy�s overall productivity.

Global economic integration and tech-nological developments have led to a con-tinual expansion of a range of traded serv-ices which are defined as including bothtransactions between residents and non-resi-dents, and transactions across geographicalborders. International transactions, which inearlier times would have been impossible orprohibitively expensive, have now becomecommonplace because of the ease with whichpeople can move and communicate acrossinternational borders. For example, the fallin the cost of international air services in re-cent decades has made many tourist servicestradable. These services were previouslyavailable only to domestic consumers. Box1 outlines how services are traded.

The major distinction between interna-tional trade in goods and international trade inservices lies in the movement of the factors ofproduction � mainly, labour and capital. Fortrade in goods, the factors of production aretypically fixed in a specific location and theproduct is transported to the foreign market.For example, a motor vehicle manufacturingplant is usually located in the domestic marketand motor vehicles are transported to the for-eign market.

For trade in services, the factors of pro-duction move such that services can be sup-plied in four ways. The World Trade Organi-zation�s General Agreement on Trade in Serv-ices (GATS) describes the four ways or modesof supply for trade in services � cross-border,consumption abroad, commercial presence andthe movement of people.

Mode 1: Cross-borderIn the same way as goods are traded, servicescan be traded across borders. There is thus aclear geographical separation between thebuyer and the seller. For example, a UnitedStates stockbroking firm may buy or sell sharesfor a Japanese resident over the Internet. TheUnited States is exporting financial servicesacross the border to Japan and Japan is import-ing financial services from the United States.

Mode 2: Consumption abroadServices can be traded by the consumer mov-ing or travelling to the foreign market. For ex-ample, a United States fee-paying student maytravel to Japan to study at a Japanese univer-sity. Japan is exporting its education servicesto the United States and the United States isimporting education services from Japan.

Mode 3: Commercial presenceServices can be traded by the capital of theexporter moving to the foreign market. For ex-ample, a United States telecommunicationscompany may establish a company in Japan.The sale of telecommunications services inJapan is an export from the United States toJapan and Japan is importing telecommunica-tions services from the United States. Mostservices are traded in this way.

Mode 4: Presence of natural persons (or move-ment of people)Services can be traded by the producer or serv-ice supplier moving to the foreign market. Forexample, an accountant who is a United Statescitizen may temporarily work for a Japanesecompany in Japan. The United States account-ant is exporting professional services to Japanand Japan is importing professional servicesfrom the United States.

Box 1. How are services traded?

4

Market access in services is inherentlymore complex than market access for tradein goods. For trade in goods, market accessis about reducing mainly border measuressuch as tariffs that are imposed on goods asthey enter a market. For trade in services,market access is about reducing governmentpolicy interventions which are less visibleand may be applied after a service supplierhas entered the market. These measures takethe form of government regulations that areusually aimed at domestic policy objectivesrather than trade policy objectives. There isusually little consideration of the effects ofsuch measures on trade and market accessfor foreign service suppliers.

Exploiting market access in services,as for trade in goods, requires identificationof the relative strength or comparative ad-vantage and specialization in the productionand export of those services. Developingeconomies can assess comparative advantageindependently of others, but maximizing theirexport revenues requires identification ofrestrictions in foreign markets and skillfulnegotiation of their reduction or removal.

A. Developing economies and compara-tive advantage

The modern economy fundamentallydepends on specialization and trade betweeneconomies. The principle of comparativeadvantage is the fundamental analytical ex-planation of the �gains from trade�. Thetheory states that an economy should special-ize in the production and export of servicesin which it has a relative advantage and im-port services in which it has a relative disad-

vantage. International trade on this basis willmean that services will be produced by therelatively least cost world producer and thequantity of services consumed will be opti-mal.

The determinants of an economy�scomparative advantage are the endowmentsof the factors of production and technology.Factor endowment is the amount of resources� land, labour or capital � held by aneconomy that can be used for production.Technology entails the productive use of re-sources. An economy may have abundantfactor endowments of unskilled labour and acomparative advantage in labour-intensiveservices � construction and tourism serv-ices. On the other hand, an economy mayhave a small quantity of highly skilled laboursuch that it has a comparative advantage inlegal services.

Developing economies clearly have acomparative advantage in labour services orservices where labour is a major input, suchas tourism. Some developing economies alsohave a comparative advantage in construc-tion and transport services, although this ismore variable between economies. New ex-port opportunities are also emerging for de-veloping economies in communications andcomputer services.

B. Market access and the movement ofnatural persons

Developing economies� comparativeadvantage and the export potential of theirservices predominantly lie in the movementof low- and semi-skilled labour services or

II. MARKET ACCESS FOR DEVELOPING ECONOMIES

5

the movement of people. Statistics on themovement of people, although imperfect,suggest that developing economies are netexporters and developed economies are netimporters of labour services (WTO, 2001b).

Trade conditions for the movement ofpeople tend to be more restrictive than forany other mode of supply (Drabek and Laird,2001). Many developed economies are capi-tal-intensive and permit the entry of highlyskilled labour, but not the entry of low-skilledworkers from labour-abundant developingeconomies. Developed economies permit theentry of highly skilled personnel and profes-sionals for a limited duration but not the en-try of unskilled and low-skilled workers suchas construction workers (Stewart, 1993).

The restrictiveness of this mode ofsupply is also reflected in GATS commit-ments. Market access conditions tend to besignificantly more restrictive for the move-ment of natural persons mode of supply thanfor any other mode (WTO, 2001b). Most ofthe commitments apply to all service sectors;and, rather than aiming to expand marketaccess, commitments are usually less than thestatus quo. Commitments also specify thetype of person that can enter a market � ex-ecutive, manager or specialist � and the pur-pose of the entry � business networking, ne-gotiating sales or establishing a commercialpresence.

There are many constraints on thetemporary migration of labour that are im-posed through domestic regulations, and aremainly administrative in nature. There arefour main types of restrictions on the move-ment of natural persons:

� Immigration regulation on the entry.These restrictions include eligibility con-ditions for the granting of work permits,cumbersome application procedures, andlimitations on the length of stay andtransferability of employment.

� Regulation on the recognition of quali-fications, work experience and training.Recognition requirements prevent mar-ket access for foreign service suppliersor limit the scope of work that can beperformed. There is also some discretionin granting recognition for certificationor licensing of foreign persons.

� Differential treatment of domestic andforeign service personnel. There are usu-ally stringent qualification and eligibil-ity conditions � citizenship or residencyrequirements � imposed on foreign serv-ice suppliers.

� Entry conditional on commercial pres-ence. The entry of foreign personnel isusually conditional on some form of es-tablishment. Developing economies usu-ally have limited resources to enterthrough commercial presence and arethus, unable to provide labour services.

Improved market access for develop-ing economies will increase export earningsand improve employment opportunities fortheir nationals. The temporary nature of tradein the movement of people also improvesdomestic human capital. People returningfrom a foreign services market have acquireda new range of skills and knowledge that canbe used to build capacity in the domesticeconomy.

In gaining market access, primarilyfrom developed economies, developingeconomies need to promote the benefits andaddress the concerns of such trade for devel-oping economies. Developed economies canacquire similar skills and knowledge fromless expensive foreign personnel, which canalleviate pressures on inflation through de-mands from nationals for higher wages.Wages are around 80 per cent of the cost ofproduction and lower labour costs providedeveloped economy firms with larger profitmargins, which in a competitive market couldbe reinvested in research and developmentto produce more innovative products.

6

Economies often have many, mainlypolitical, concerns about the liberalization oftheir labour services markets. It is difficultfor Governments to embrace the benefits ofimporting less expensive labour in the faceof vocal domestic lobby groups describingsuch a policy as a �threat� to domestic jobs.The fears of a few from the importing Gov-ernment need to be weighed against the sub-stantial benefits for the overall economy.Governments and lobby groups may need tobe educated about the benefits. As in the caseof any liberalization, short-term adjustmentcosts will also occur as resources in a previ-ously protected labour market are reallocated,but in the long term substantial benefits willaccrue to the economies importing (and ex-porting) labour services.

Governments and lobby groups alsoraise concerns about employment and per-manent migration. Measures affecting natu-ral persons seeking access to the employmentmarket or measures regarding citizenship,residence or employment on a permanentbasis are not covered under the GATS. Thelatter aims to promote liberalization of la-bour services but at the same time gives WTOMembers the freedom to regulate the entryand temporary stay of natural persons, whichincludes the implementation of measuresnecessary to protect the integrity and ensurethe orderly movement of natural personsacross their borders.

Restrictions on the movement of peo-ple in some economies may prohibit the en-try of foreign persons. However, market ac-cess can still be achieved by switching to thenext best alternative, and usually less effi-cient, mode of supply. In recent years, Indiahas developed a growing software servicesindustry that delivers services over theInternet or via the cross-border mode of sup-ply. The industry competes internationallyeven though developed economies continueto impose restrictions on the movement ofIndian nationals (Chadha, 2001). Developedeconomies may also be more amenable with

labour being embodied in a service suppliedto the domestic market rather than labourentering directly and supplying a servicewithin the domestic market.

The GATS also provides provisionsaimed at enhancing market access for devel-oping economies (see box 2).

C. Market access and tourism services

Tourism generates the largest exportrevenues for developing economies. It is oneof the largest and fastest-growing servicesectors, accounting for over 35 per cent ofworld services exports (WTO, 2001b). It ishighly labour-intensive and is an importantemployer in developing economies.

Natural attractions and inexpensivedestinations are the determinants of compara-tive advantage in tourism for developingeconomies. Foreigners are drawn to devel-oping economies by their differences in termsof natural attractions and culture. Most of thelargest exporters of tourist services are smallisland nations. Foreigners from developedeconomies also find visiting a developingeconomy relatively inexpensive and a �valuefor money� holiday.

Market access for tourist services isprimarily the responsibility of a developingeconomy. Tourists travel to the foreign (orexport) market to consume such services.Market access for tourist services is aboutpermitting foreign persons� access to thecountry. Measures imposed by developingeconomies that limit their ability to maximizetheir export revenues from tourism are re-strictions on the issuing and length of visasand currency movements for individual tour-ists.

Maximizing export revenues fromtourism is very dependent on the necessaryand efficient infrastructure being in place.Tourists rely on efficiently operating trans-

7

port, telecommunications and financial serv-ices. The domestic economy requires reliabletransport services for tours and sightseeing,telecommunications services for organizingtours and financial services for currency ex-change. Many developing economies need todevelop these essential input services for thebenefit of tourism and other sectors.

D. Market access and new export oppor-tunities

Developing economies also have anopportunity to expand their service exportbases. These include semi-skilled knowl-edge-based services in a range of communi-cation and computer services. Advances ininformation technology and electronic com-merce have created these opportunities. Forexample, India has in recent years developeda high-quality and low-cost software devel-opment industry (Chadha, 2001).

Potential comparative advantage fordeveloping economies lies in a number ofbusiness services. These include a wide rangeof:

� Computer services, including softwareprogramming, database management,online support services, and Internet sitedesign and management;

� Professional services, including low-costarchitecture, consulting engineering, le-gal research and market research serv-ices;

� Technical assistance for other develop-ing economies, including low-tech andmedium-tech production processes, in-dustrial engineering, industrial design,and research and development; and

� Cultural or linguistic services, includingmultilingual offshore call centre services(UNCTAD, 1998, 2001).

The General Agreement on Trade inServices (GATS) is the first multilateral legallyenforceable agreement on international tradein services. Its objective is progressive liber-alization of international trade in servicesthrough successive rounds of negotiations.Generally, the GATS covers all services (ex-cept those provided by a governmental author-ity), services delivered through the four modesof supply (see box 1) and all measures affect-ing trade in services. The important principlesin the GATS, as in other WTO agreements, aremost-favoured-nation, transparency, market ac-cess and national treatment.

Developing economies can use theGATS to help them gain market access. UnderArticle IV, the GATS aims to increase the par-ticipation of developing economies in theworld trading system. Developing economiescan request developed economies to providethem with opportunities for their service ex-ports. Article IV requires WTO Members to

increase the participation of developing econo-mies in the world trade by:

� Strengthening the domestic services capac-ity of developing economies and its effi-ciency and competitiveness through accessto technology on a commercial basis;

� Improving their access to distributionchannels and information networks; and

� Liberalizing market access in services thatare of export interest to developing econo-mies.

WTO Members were also requested toestablish contact points for service suppliersfrom developing economies in order to facili-tate access to information about supplyingservices in developed economies. Special pri-ority is to be given to market access and infor-mation requests from least developed econo-mies.

Box 2. Developing economies, market access and the GATS

8

Developing economies have a poten-tial comparative advantage in these services� as in many other services � because oftheir low-cost labour services, and thus mar-ket access is dependent on the movement ofpeople. These new opportunities are also sub-stantial generators of new employment.There are worldwide labour shortages insome of these services, in particular software

development. Restrictions on work permitsand visas limit the ability of the shortages tobe addressed via the importation of labourfrom developing economies (WTO, 1998).As mentioned above, developing economiescan take advantage, to a lesser extent, of someof these opportunities by supplying theseservices via a mode of supply other than themovement of people.

9

Measuring the economy-wide impactof trade liberalization requires a global gen-eral equilibrium framework, which capturesintersectoral effects for an economy and linksbetween economies. This enables an assess-ment to be made of the impact of sector-spe-cific policies on an economy as a whole.

Numerous general equilibrium stud-ies analyse the economic impacts of policiesaffecting trade in goods, but relatively littlework has been completed on assessing thepotential gains from alternative liberalizationscenarios in services. The past difficultiesarise from inadequate information about in-ternational service transactions and a lack ofcomprehensive measures of restrictions ontrade in services. Modelling of services tradealso requires the development of a differentmodelling structure from that used for goodstrade in order to incorporate the variousmodes through which services are supplied,that is, to account for the movement of fac-tors of production (OECD, 2000a, 2000b).

A significant amount of methodologi-cal thinking is still required on modellingservices trade liberalization, but a number ofstudies have analyzed the effects (Benjaminand Diao, 1998, 2000; Brown et al., 1996;Chadha, 2001; Chadha et al., 2000; Dee andHanslow, 2000; DFAT, 1999; Hertel et al.,1999; and Robinson et al., 1999). The resultsare similar in a number of respects:

� There are always substantial global real-income gains from services liberaliza-tion. In many studies, the gains in termsof real income are similar to or greaterthan those derived from liberalization oftrade in agriculture and manufacturingcombined.

� Developing economies gain more thandeveloped economies. Economies withgreater restrictions or, mainly, develop-ing economies reap the greatest benefitsfrom liberalization.

� Liberalization of trade in services haspowerful impacts on agriculture andmanufacturing through intersectoral link-ages in an economy. Services are essen-tial inputs to other sectors, and substan-tial productivity gains accrue to othersectors when liberalization improves theefficiency of the service sector.

Dee and Hanslow (2000) use one ofthe most sophisticated general equilibriummodels to analyse the effects of liberalizingtrade in services. The model simulates thebenefits of liberalizing restrictions on allservices and indirectly incorporates the ben-efits from liberalizing restrictions on themovement of natural persons. It also has thecapability to simulate the effect of removingcertain types of restrictions. It can examinethe impact of full and partial multilateral lib-eralization of services trade. It is a 19-region(covering Asia, North and South America andthe European Union) by 3-sector (agriculture,manufacturing and services) computable gen-eral equilibrium model of the world economyknown as the FTAP model. It was developedfrom the Global Trade Analysis Project(GTAP) model (Hertel, 1997), with the ad-dition of the structure necessary to supportthe analysis of services liberalization.

One of the distinguishing features ofFTAP is the inclusion of foreign direct in-vestment (FDI). The treatment of FDI allowsfor examination of the comprehensive re-moval of restrictions on all modes of service

III. WHAT�S AT STAKE FOR DEVELOPING ECONOMIES?

10

supply, including restrictions on servicesdelivered via FDI. Hanslow et al. (1999) fullydocuments the structure of the FTAP model.

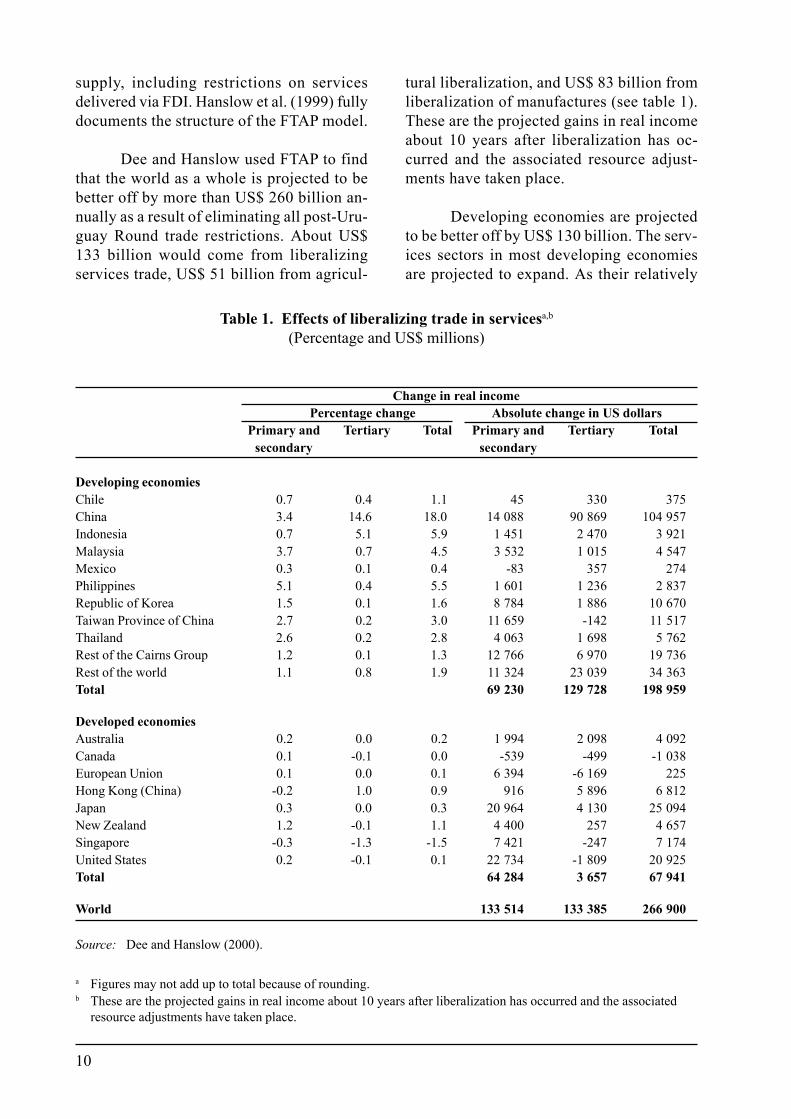

Dee and Hanslow used FTAP to findthat the world as a whole is projected to bebetter off by more than US$ 260 billion an-nually as a result of eliminating all post-Uru-guay Round trade restrictions. About US$133 billion would come from liberalizingservices trade, US$ 51 billion from agricul-

tural liberalization, and US$ 83 billion fromliberalization of manufactures (see table 1).These are the projected gains in real incomeabout 10 years after liberalization has oc-curred and the associated resource adjust-ments have taken place.

Developing economies are projectedto be better off by US$ 130 billion. The serv-ices sectors in most developing economiesare projected to expand. As their relatively

Change in real incomePercentage change Absolute change in US dollars

Primary and Tertiary Total Primary and Tertiary Totalsecondary secondary

Developing economiesChile 0.7 0.4 1.1 45 330 375China 3.4 14.6 18.0 14 088 90 869 104 957Indonesia 0.7 5.1 5.9 1 451 2 470 3 921Malaysia 3.7 0.7 4.5 3 532 1 015 4 547Mexico 0.3 0.1 0.4 -83 357 274Philippines 5.1 0.4 5.5 1 601 1 236 2 837Republic of Korea 1.5 0.1 1.6 8 784 1 886 10 670Taiwan Province of China 2.7 0.2 3.0 11 659 -142 11 517Thailand 2.6 0.2 2.8 4 063 1 698 5 762Rest of the Cairns Group 1.2 0.1 1.3 12 766 6 970 19 736Rest of the world 1.1 0.8 1.9 11 324 23 039 34 363Total 69 230 129 728 198 959

Developed economiesAustralia 0.2 0.0 0.2 1 994 2 098 4 092Canada 0.1 -0.1 0.0 -539 -499 -1 038European Union 0.1 0.0 0.1 6 394 -6 169 225Hong Kong (China) -0.2 1.0 0.9 916 5 896 6 812Japan 0.3 0.0 0.3 20 964 4 130 25 094New Zealand 1.2 -0.1 1.1 4 400 257 4 657Singapore -0.3 -1.3 -1.5 7 421 -247 7 174United States 0.2 -0.1 0.1 22 734 -1 809 20 925Total 64 284 3 657 67 941

World 133 514 133 385 266 900

Source: Dee and Hanslow (2000).

a Figures may not add up to total because of rounding.b These are the projected gains in real income about 10 years after liberalization has occurred and the associated

resource adjustments have taken place.

Table 1. Effects of liberalizing trade in servicesa,b

(Percentage and US$ millions)

11

high restrictions on entry are removed, theirservices sectors develop, primarily funded byFDI, and they become major exporters ofservices. China is expected to benefit by US$91 billion from the removal of particularlystringent restrictions.

While developing economies will re-ceive a greater share of the expanding globalservices market, services sectors in econo-mies with moderate restrictions will expandbut their share of the global services mar-kets in the long run will be smaller. Australia,New Zealand, Canada and the United States,as well as the European Union, are expectedto gain but relatively less than developingeconomies. In part, this is because of in-creased competition via cross-border tradefrom the newly expanded Asian service sec-tors.

For some economies � the EuropeanUnion, the United States, Canada, Singaporeand the Taiwan Province of China � thecontribution of multilateral services trade lib-eralization is expected to be negative (Deeand Hanslow, 2000). There are a number ofreasons that contribute to this result, but oneof the more interesting insights is the effectsof liberalization on foreign direct investment(Productivity Commission and the Austral-ian National University, 2000). FDI can lead

to an expansion or contraction in the capitalstock located within a region, leading to apositive or negative contribution to incomegenerated within a region from this changein national endowments. For many countries,after the restrictions on FDI in foreign econo-mies are removed, the owners of the foreigncapital receive a lower return.

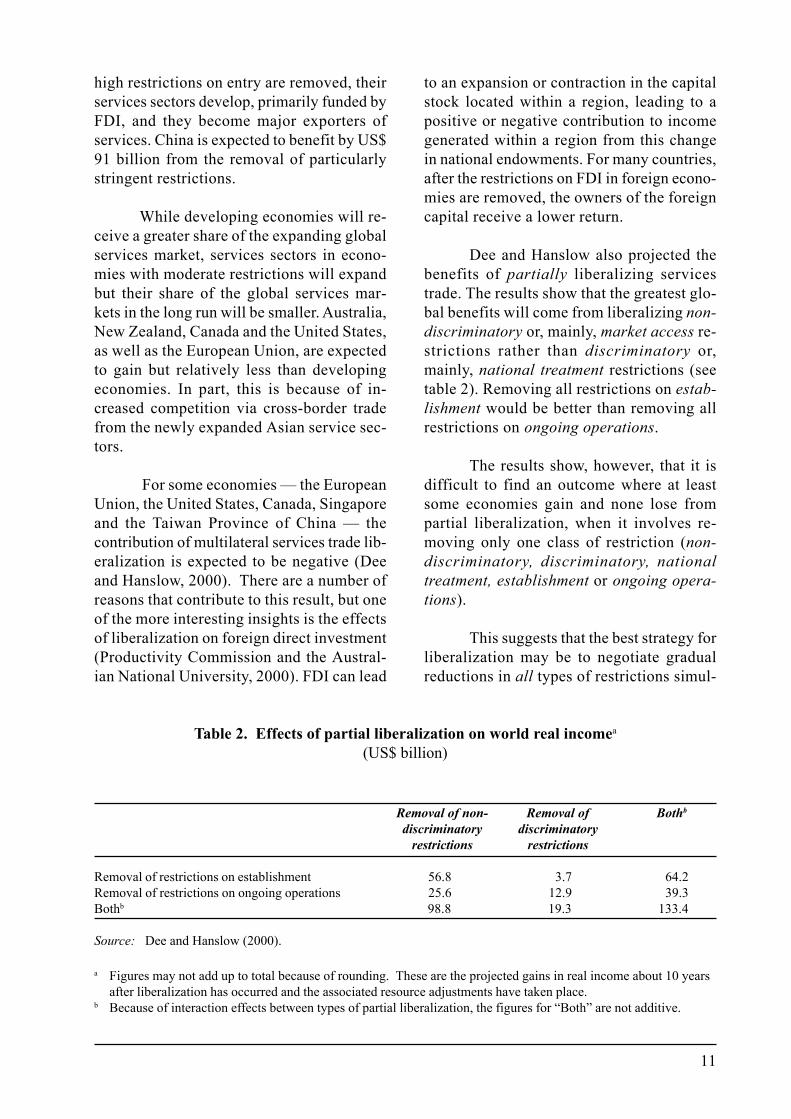

Dee and Hanslow also projected thebenefits of partially liberalizing servicestrade. The results show that the greatest glo-bal benefits will come from liberalizing non-discriminatory or, mainly, market access re-strictions rather than discriminatory or,mainly, national treatment restrictions (seetable 2). Removing all restrictions on estab-lishment would be better than removing allrestrictions on ongoing operations.

The results show, however, that it isdifficult to find an outcome where at leastsome economies gain and none lose frompartial liberalization, when it involves re-moving only one class of restriction (non-discriminatory, discriminatory, nationaltreatment, establishment or ongoing opera-tions).

This suggests that the best strategy forliberalization may be to negotiate gradualreductions in all types of restrictions simul-

Table 2. Effects of partial liberalization on world real incomea

(US$ billion)

Removal of non- Removal of Bothb

discriminatory discriminatoryrestrictions restrictions

Removal of restrictions on establishment 56.8 3.7 64.2Removal of restrictions on ongoing operations 25.6 12.9 39.3Bothb 98.8 19.3 133.4

Source: Dee and Hanslow (2000).

a Figures may not add up to total because of rounding. These are the projected gains in real income about 10 yearsafter liberalization has occurred and the associated resource adjustments have taken place.

b Because of interaction effects between types of partial liberalization, the figures for �Both� are not additive.

12

taneously. Non-discriminatory restrictions onall service suppliers should be reduced oreliminated before the removal of discrimi-natory restrictions on foreign service suppli-ers. Dee et al. (2000) argue that reducing non-discriminatory restrictions on all service sup-pliers is a better approach than only reduc-ing discriminatory restrictions on foreignservice suppliers. Reducing discriminatoryrestrictions on foreigners alone can have anegative impact on the level of services sup-plied by domestic firms. This will result inlower prices and higher total sales, but do-mestic service suppliers will end up with asmaller share of the service sector. However,if restrictions that affect foreign and domes-tic service suppliers equally are reduced, allservice suppliers will have the same oppor-

tunities to increase the amount of servicesthey supply in an expanding market.

Verikios and Zhang (2001) also usedthe FTAP model to analyse the sectoral im-pacts of removing all restrictions on trade infinancial and communications services. Theyfound that the total gain in world incomefrom liberalizing both sectors is US$ 48 bil-lion. About US$ 24 billion of this wouldcome from liberalizing communications serv-ices, with most of the gains coming from re-moving non-discriminatory restrictions. US$24 billion is likely to accrue to financial serv-ices, with almost all the gains coming fromremoving discriminatory restrictions. How-ever, the gains from most regions are thehighest when all restrictions are removed.

13

The modelling results show greaterbenefits from liberalization for developingeconomies than for developed economies.Most of these gains arise from liberalizingthe domestic service sector, not from seek-ing better market access to foreign servicesmarkets. This raises the question of the na-ture and extent of restrictions on trade inservices that are preventing developingeconomies from achieving these gains.

Identifying and measuring restrictionsshows the extent of restrictiveness of differ-ent economies and which economies, poten-tially, have the most to gain. Convertingqualitative information on restrictions to aquantitative index measure of trade restric-tiveness, based on coverage and some initialjudgements about the relative stringency ofthe different sorts of restrictions, provides forease of comparison for economies. Theseresults can then be used to estimate the ef-fect of restrictions on the prices and costs ofservices.

Measuring the effects of restrictionson trade in services has, until recently, beenconsidered too difficult. This has mainly beenbecause of the difficulty in identifying restric-tions on services. Restrictions on trade ingoods usually take the form of a tariff, whilerestrictions on trade in services usually takethe form of government regulation and a cer-tain level of regulation is usually justified formeeting regulatory objectives. These diffi-culties have, to a certain extent, been over-come with advances in economic thinkingand the collection of information on restric-tions. In recent years, researchers have de-veloped a methodology that generally in-volves:

� Measuring how restrictive a service sec-tor is in an economy by using a trade re-strictiveness index; and

� Estimating the effect of restrictions, asmeasured by the trade restrictiveness in-dex, on the economic performance �price, cost and/or price-cost margins �of service suppliers (McGuire, 2000).

These estimates of the effects on re-strictions can be used to project the economy-wide and global benefits of removing restric-tions on services using a computable generalequilibrium model. Dee and Hanslow (2000)used some of these measures to model thebenefits of liberalizing trade in services.

A. Measuring restrictions on trade inservices

Restrictions on trade in services canbe measured using a trade restrictiveness in-dex. This index is a sophisticated frequencymeasure that estimates the restrictiveness ofan economy�s trading regime for services onthe basis of the number and severity of re-strictions.

Information on restrictions is firstgathered and then classified. The informa-tion on restrictions is drawn from a numberof sources, including material produced byAsia-Pacific Economic Cooperation (APEC),the OECD, the WTO and the United StatesTrade Representative. A comprehensive da-tabase of restrictions can be compiled fromthese sources, but it is possible that someservice sector regulation and developmentsare not captured. That said, the information

IV. WHAT ARE THE RESTRICTIONS AND THEIR EFFECTS?

14

compiled on restrictions is significantly morecomprehensive than that provided in theGATS schedules of WTO Members. Theprocess also highlights the types of restric-tions that are imposed on services which isvery helpful for negotiators.

Restrictions can be classified in twoways. The first is by whether a restrictionapplies to:

� Establishment � the ability of servicesuppliers to establish physical outlets inan economy and supply services throughthose outlets; or

� Ongoing operations � the operations ofa service supplier after it has entered themarket.

Restrictions on establishment ofteninclude licensing requirements for servicesuppliers or firms, restrictions on direct in-vestment in existing firms and restrictions onthe permanent movement of people. Restric-tions on ongoing operations often includerestrictions on firms conducting their corebusiness, the pricing of services and the tem-porary movement of people.

The second way a restriction can beclassified is by whether it is:

� Non-discriminatory � restricting do-mestic and foreign service suppliersequally; or

� Discriminatory � restricting only for-eign service suppliers.

This two-by-two classification is simi-lar to that used in the GATS schedules ofcommitments (WTO, 1994). Restrictions onestablishment (or commercial presence) in-clude those affecting services delivered viaFDI. Restrictions on ongoing operations canaffect services delivered by cross-border sup-ply, consumption abroad or the presence ofnatural persons (other modes of supply rec-ognized under the GATS). Non-discrimina-tory restrictions are similar to the GATS limi-tations on market access and discriminatoryrestrictions are similar to limitations on na-tional treatment. Table 3 provides an exam-ple of how trade restrictions on banking serv-ices are classified.

The trade restrictiveness index scoreis calculated for each economy using a meth-odology of weights and scores (McGuire etal., 2000). Scores are assigned for each re-striction on the basis of a judgement abouthow stringent it is. The more stringent therestriction, the higher the score. For exam-ple, an economy that restricts the number of

Table 3. An example of classifying trade restrictions on banking services

Establishment Ongoing operations(commercial presence (cross-border, consumption abroad and

mode of supply) movement of natural persons modes of supply)

Non- The number of banking licences is Banks are restricted regarding the manner indiscriminatory restricted. which they can raise funds.

Discriminatory The number of foreign bank Foreign banks are restricted regarding thelicenses is restricted. manner in which they can raise funds.

Source: McGuire (2000).

15

banking licences is assigned a higher scorethan an economy that issues new banking li-cences with only prudential requirements.

The restriction categories are thenweighted together according to a judgementabout their relative economic cost subject toreasonably available information. For exam-ple, restrictions on banking licences areweighted more heavily than restrictions onthe temporary movement of people. Theweights are generally chosen so that the to-tal restrictiveness index score ranges from 0to 1.

In calculating an overall economyscore, it is not determined which restrictionsmight be justified for enhancing the effi-ciency of a service sector and which mightnot. In general, trade restrictions, by reduc-ing competition in a services market, willreduce the efficiency of that market. How-ever, sometimes regulation which limits com-petition is necessary to deal with �marketfailure� and to meet particular social objec-tives. No assessment is made of the meritsor otherwise of the restrictions covered by

the trade restrictiveness index. It is extremelydifficult to make an assessment about themerits of regulation for economies with dif-ferent regulatory objectives and structures.Furthermore, multilateral trading agree-ments, such as the GATS, aim to reduce re-strictions while recognizing the freedom oftrading agreement members to regulate tomeet national policy objectives. Govern-ments generally set their own regulation ob-jectives � efficiency, transparency, stabilityand adequate disclosure.

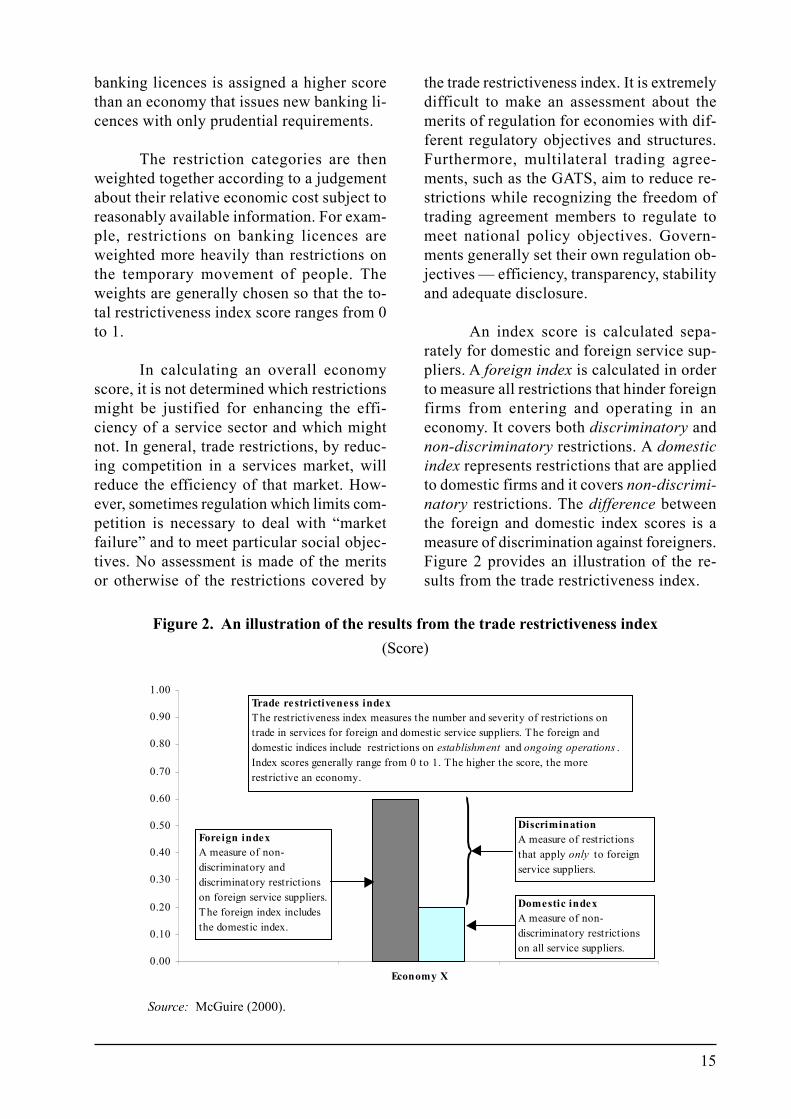

An index score is calculated sepa-rately for domestic and foreign service sup-pliers. A foreign index is calculated in orderto measure all restrictions that hinder foreignfirms from entering and operating in aneconomy. It covers both discriminatory andnon-discriminatory restrictions. A domesticindex represents restrictions that are appliedto domestic firms and it covers non-discrimi-natory restrictions. The difference betweenthe foreign and domestic index scores is ameasure of discrimination against foreigners.Figure 2 provides an illustration of the re-sults from the trade restrictiveness index.

Figure 2. An illustration of the results from the trade restrictiveness index(Score)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Economy X

Trade restrictiveness indexThe restrictiveness index measures the number and severity of restrictions on trade in services for foreign and domestic service suppliers. The foreign and domestic indices include restrictions on establishment and ongoing operations . Index scores generally range from 0 to 1. The higher the score, the more restrictive an economy.

Foreign indexA measure of non-discriminatory and discriminatory restrictions on foreign service suppliers. The foreign index includes the domestic index.

Domestic indexA measure of non-discriminatory restrictions on all service suppliers.

DiscriminationA measure of restrictions that apply only to foreign service suppliers.

Source: McGuire (2000).

16

1. Trade restrictiveness index results fordeveloping economies

The results from the trade restrictive-ness indices show that developing economiestend to have higher trade restrictiveness in-dex scores than developed economies. Manyof the economies experiencing financial dif-ficulties in recent years, mainly Asian andSouth American economies, have medium tohigh restrictiveness index scores. Theseeconomies were also found to be the mostdiscriminatory against foreign service sup-pliers.

Figures 3 to 7 show the results for se-lected service sectors from the trade restric-tiveness indices for low- and middle-incomeeconomies (LMIEs) (or developing econo-mies) and the average for high-incomeeconomies (HIEs) (or developed economies).The World Bank (2001) provides the group-ings for LMIEs and HIEs.

The Productivity Commission (2001a)provides data for each service sector with

greater economy coverage and data disaggre-gation for the trade restrictiveness indices.Insufficient information is available for cal-culating trade restrictiveness indices for anumber of developing economies.

The commentary on each service sec-tor for each economy provides an overviewof the type of restrictions imposed. Morespecific details are available from the rel-evant identified papers.

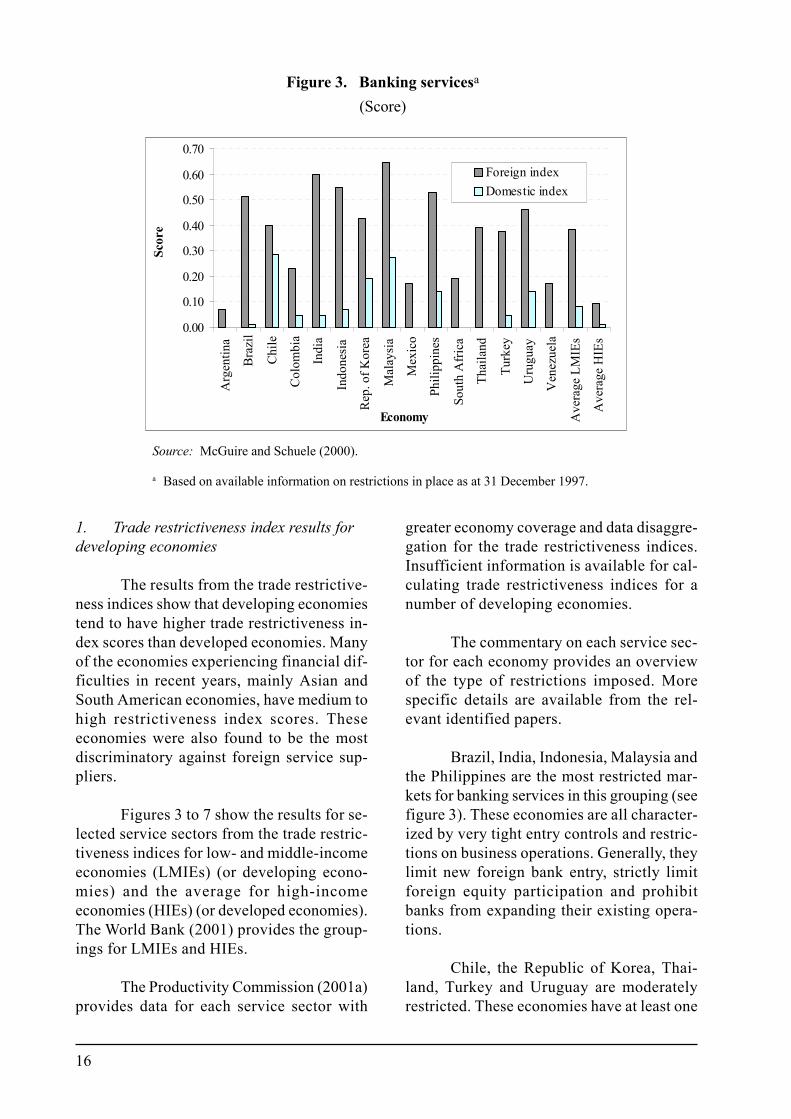

Brazil, India, Indonesia, Malaysia andthe Philippines are the most restricted mar-kets for banking services in this grouping (seefigure 3). These economies are all character-ized by very tight entry controls and restric-tions on business operations. Generally, theylimit new foreign bank entry, strictly limitforeign equity participation and prohibitbanks from expanding their existing opera-tions.

Chile, the Republic of Korea, Thai-land, Turkey and Uruguay are moderatelyrestricted. These economies have at least one

Figure 3. Banking servicesa

(Score)

Source: McGuire and Schuele (2000).

a Based on available information on restrictions in place as at 31 December 1997.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Arg

entin

a

Bra

zil

Chi

le

Col

ombi

a

Indi

a

Indo

nesi

a

Rep

. of K

orea

Mal

aysi

a

Mex

ico

Phili

ppin

es

Sout

h A

fric

a

Thai

land

Turk

ey

Uru

guay

Ven

ezue

la

Ave

rage

LM

IEs

Ave

rage

HIE

s

Economy

Scor

eForeign indexDomestic index

17

significant restriction that limits foreign ac-cess to their markets. This includes either arestriction on licensing foreign equity par-ticipation in domestic banks or restrictionson their operations, such as opening newoutlets and street branches.

Argentina, Colombia, South Africaand Venezuela are the least restricted in thisgrouping. They have fewer restrictions onlicensing, and foreign equity participation.

Brazil, India and Indonesia have themost discriminatory restrictions against for-eigners for banking services as measured bythe large difference between the foreign anddomestic index scores.

India, Indonesia, Malaysia, the Phil-ippines, the Republic of Korea and Thailandare the most restricted markets for distribu-tion services (see figure 4). Some of theseeconomies are characterized by one or moreof the following � foreign firms being pro-hibited from participating in retail distribu-tion, limits on the number of import licences

granted to foreigners, and limits and perform-ance requirements on foreign equity partici-pation in domestic firms. The Republic ofKorea imposes on all distributors non-dis-criminatory restrictions that limit the avail-ability of land and the ability of firms to es-tablish large-scale stores.

Brazil, Chile, Colombia and Turkeyare moderately restricted. These economieshave a number of restrictions on ongoingoperations. They typically impose restrictionson opening hours and promotional activities,impose licensing requirements on manage-ment and restrict the movement of people.

Argentina, Mexico, South Africa andUruguay are the least restricted. They requirescreening of foreign investment and licens-ing of management.

Malaysia, the Philippines and Thai-land have the most discriminatory restrictionsagainst foreigners with regard to distributionservices.

Figure 4. Distribution servicesa

(Score)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Arg

entin

a

Bra

zil

Chi

le

Col

ombi

a

Indi

a

Indo

nesi

a

Rep

. of K

orea

Mal

aysi

a

Mex

ico

Phili

ppin

es

Sout

h A

fric

a

Thai

land

Turk

ey

Uru

guay

Ven

ezue

la

Ave

rage

LM

IEs

Ave

rage

HIE

s

Economy

Scor

e

Foreign indexDomestic index

Source: Kalirajan (2000).

a Based on the available information on restrictions in place as at 30 June 1999.

18

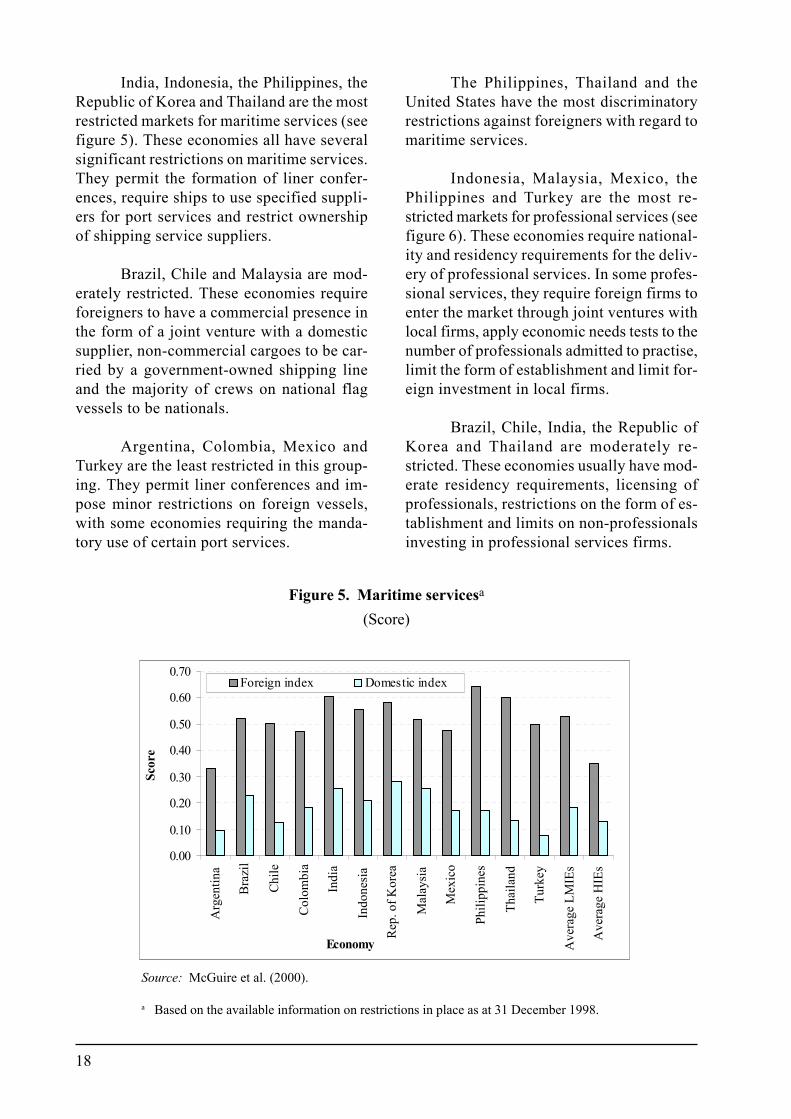

India, Indonesia, the Philippines, theRepublic of Korea and Thailand are the mostrestricted markets for maritime services (seefigure 5). These economies all have severalsignificant restrictions on maritime services.They permit the formation of liner confer-ences, require ships to use specified suppli-ers for port services and restrict ownershipof shipping service suppliers.

Brazil, Chile and Malaysia are mod-erately restricted. These economies requireforeigners to have a commercial presence inthe form of a joint venture with a domesticsupplier, non-commercial cargoes to be car-ried by a government-owned shipping lineand the majority of crews on national flagvessels to be nationals.

Argentina, Colombia, Mexico andTurkey are the least restricted in this group-ing. They permit liner conferences and im-pose minor restrictions on foreign vessels,with some economies requiring the manda-tory use of certain port services.

The Philippines, Thailand and theUnited States have the most discriminatoryrestrictions against foreigners with regard tomaritime services.

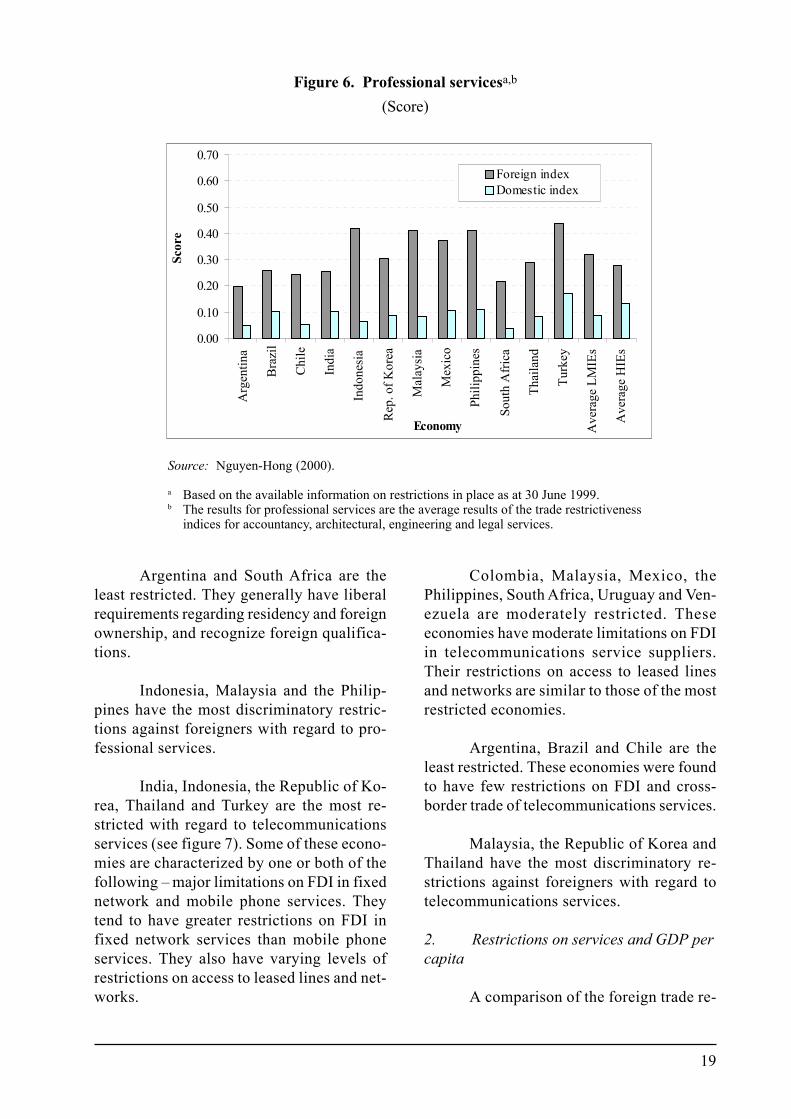

Indonesia, Malaysia, Mexico, thePhilippines and Turkey are the most re-stricted markets for professional services (seefigure 6). These economies require national-ity and residency requirements for the deliv-ery of professional services. In some profes-sional services, they require foreign firms toenter the market through joint ventures withlocal firms, apply economic needs tests to thenumber of professionals admitted to practise,limit the form of establishment and limit for-eign investment in local firms.

Brazil, Chile, India, the Republic ofKorea and Thailand are moderately re-stricted. These economies usually have mod-erate residency requirements, licensing ofprofessionals, restrictions on the form of es-tablishment and limits on non-professionalsinvesting in professional services firms.

Figure 5. Maritime servicesa

(Score)

Source: McGuire et al. (2000).

a Based on the available information on restrictions in place as at 31 December 1998.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Arg

entin

a

Bra

zil

Chi

le

Col

ombi

a

Indi

a

Indo

nesi

a

Rep

. of K

orea

Mal

aysi

a

Mex

ico

Phili

ppin

es

Thai

land

Turk

ey

Ave

rage

LM

IEs

Ave

rage

HIE

s

Economy

Scor

e

Foreign index Domestic index

19

Argentina and South Africa are theleast restricted. They generally have liberalrequirements regarding residency and foreignownership, and recognize foreign qualifica-tions.

Indonesia, Malaysia and the Philip-pines have the most discriminatory restric-tions against foreigners with regard to pro-fessional services.

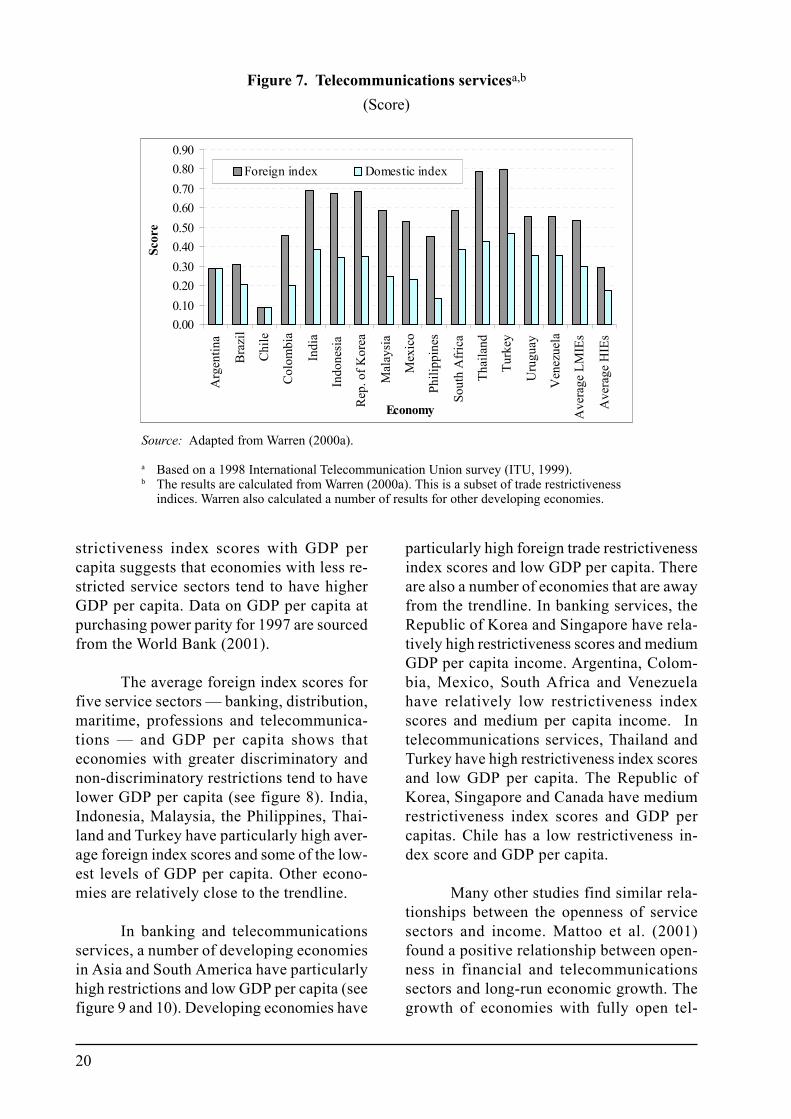

India, Indonesia, the Republic of Ko-rea, Thailand and Turkey are the most re-stricted with regard to telecommunicationsservices (see figure 7). Some of these econo-mies are characterized by one or both of thefollowing � major limitations on FDI in fixednetwork and mobile phone services. Theytend to have greater restrictions on FDI infixed network services than mobile phoneservices. They also have varying levels ofrestrictions on access to leased lines and net-works.

Colombia, Malaysia, Mexico, thePhilippines, South Africa, Uruguay and Ven-ezuela are moderately restricted. Theseeconomies have moderate limitations on FDIin telecommunications service suppliers.Their restrictions on access to leased linesand networks are similar to those of the mostrestricted economies.

Argentina, Brazil and Chile are theleast restricted. These economies were foundto have few restrictions on FDI and cross-border trade of telecommunications services.

Malaysia, the Republic of Korea andThailand have the most discriminatory re-strictions against foreigners with regard totelecommunications services.

2. Restrictions on services and GDP percapita

A comparison of the foreign trade re-

Figure 6. Professional servicesa,b

(Score)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Arg

entin

a

Bra

zil

Chi

le

Indi

a

Indo

nesi

a

Rep

. of K

orea

Mal

aysi

a

Mex

ico

Phili

ppin

es

Sout

h A

fric

a

Thai

land

Turk

ey

Ave

rage

LM

IEs

Ave

rage

HIE

s

Economy

Scor

eForeign indexDomestic index

Source: Nguyen-Hong (2000).

a Based on the available information on restrictions in place as at 30 June 1999.b The results for professional services are the average results of the trade restrictiveness

indices for accountancy, architectural, engineering and legal services.

20

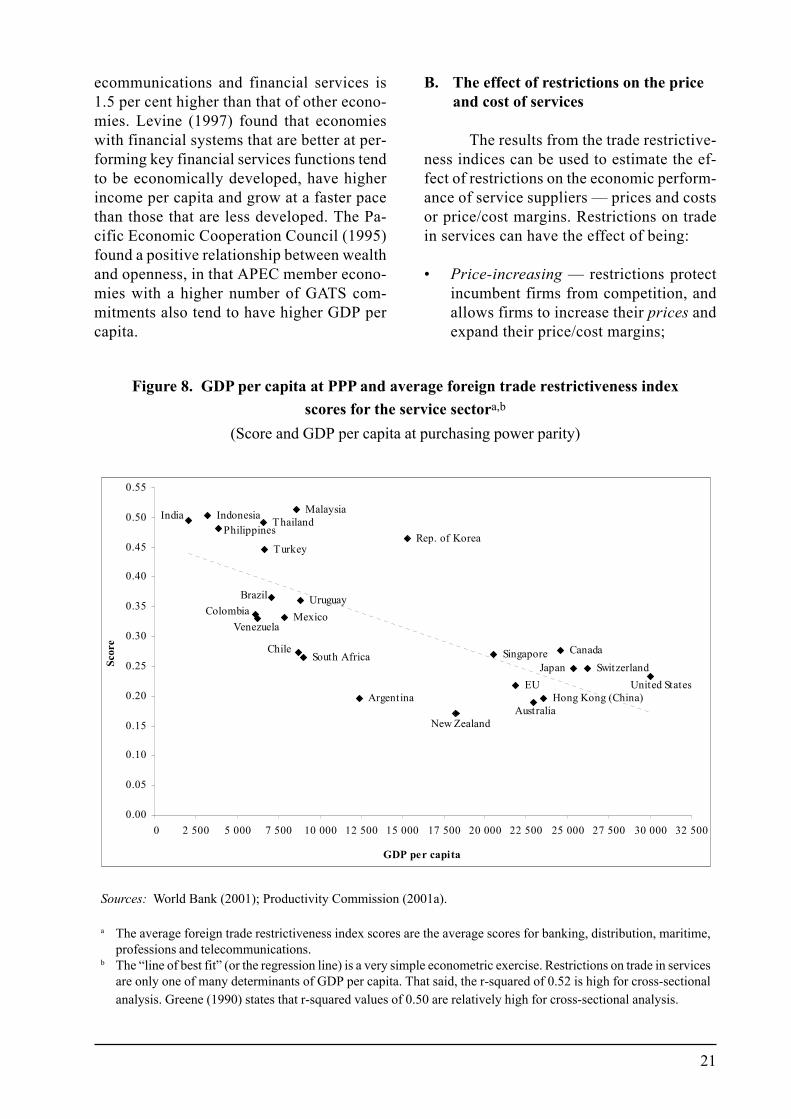

strictiveness index scores with GDP percapita suggests that economies with less re-stricted service sectors tend to have higherGDP per capita. Data on GDP per capita atpurchasing power parity for 1997 are sourcedfrom the World Bank (2001).

The average foreign index scores forfive service sectors � banking, distribution,maritime, professions and telecommunica-tions � and GDP per capita shows thateconomies with greater discriminatory andnon-discriminatory restrictions tend to havelower GDP per capita (see figure 8). India,Indonesia, Malaysia, the Philippines, Thai-land and Turkey have particularly high aver-age foreign index scores and some of the low-est levels of GDP per capita. Other econo-mies are relatively close to the trendline.

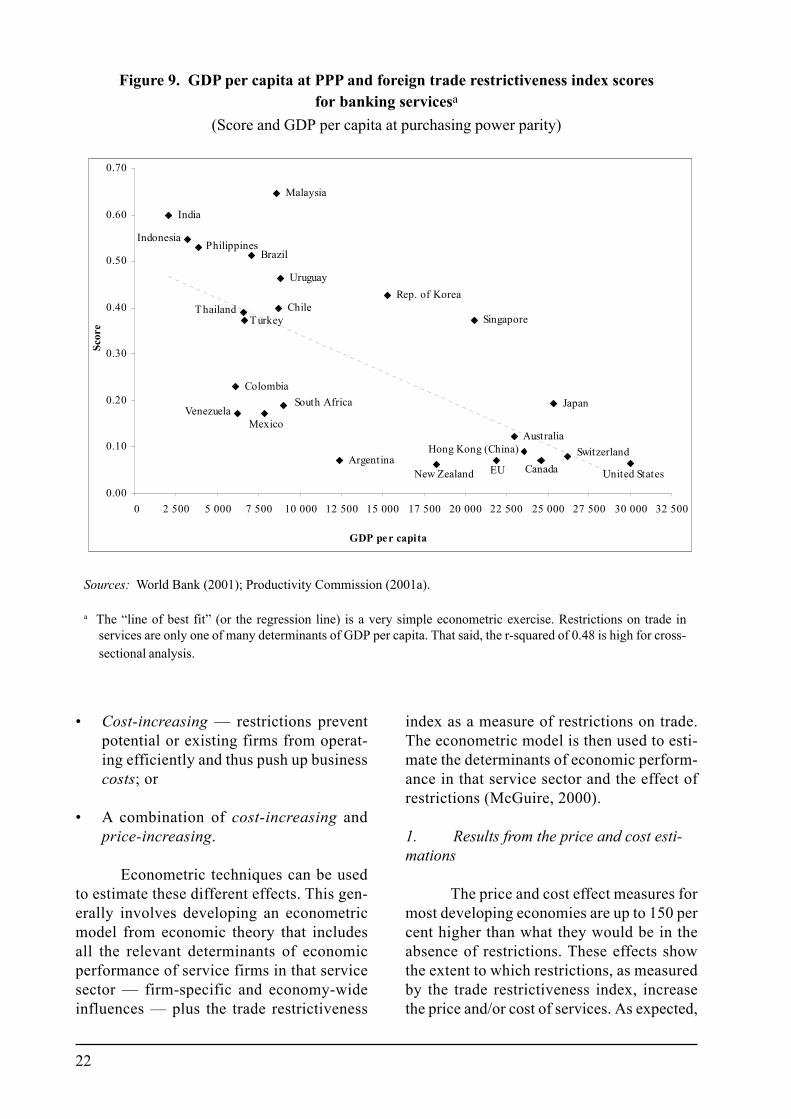

In banking and telecommunicationsservices, a number of developing economiesin Asia and South America have particularlyhigh restrictions and low GDP per capita (seefigure 9 and 10). Developing economies have

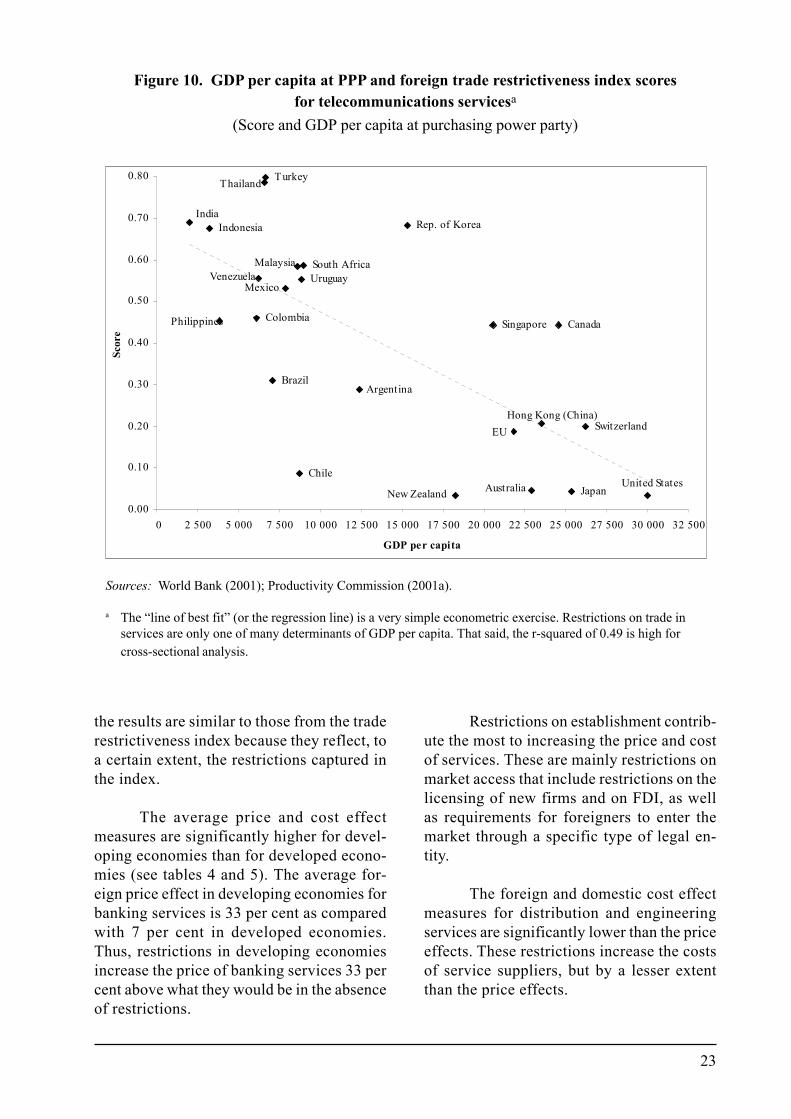

particularly high foreign trade restrictivenessindex scores and low GDP per capita. Thereare also a number of economies that are awayfrom the trendline. In banking services, theRepublic of Korea and Singapore have rela-tively high restrictiveness scores and mediumGDP per capita income. Argentina, Colom-bia, Mexico, South Africa and Venezuelahave relatively low restrictiveness indexscores and medium per capita income. Intelecommunications services, Thailand andTurkey have high restrictiveness index scoresand low GDP per capita. The Republic ofKorea, Singapore and Canada have mediumrestrictiveness index scores and GDP percapitas. Chile has a low restrictiveness in-dex score and GDP per capita.

Many other studies find similar rela-tionships between the openness of servicesectors and income. Mattoo et al. (2001)found a positive relationship between open-ness in financial and telecommunicationssectors and long-run economic growth. Thegrowth of economies with fully open tel-

Figure 7. Telecommunications servicesa,b

(Score)

0.000.100.200.300.400.500.600.700.800.90

Arg

entin

a

Bra

zil

Chi

le

Col

ombi

a

Indi

a

Indo

nesi

a

Rep

. of K

orea

Mal

aysi

a

Mex

ico

Phili

ppin

es

Sout

h A

fric

a

Thai

land

Turk

ey

Uru

guay

Ven

ezue

la

Ave

rage

LM

IEs

Ave

rage

HIE

s

Economy

Scor

eForeign index Domestic index

Source: Adapted from Warren (2000a).

a Based on a 1998 International Telecommunication Union survey (ITU, 1999).b The results are calculated from Warren (2000a). This is a subset of trade restrictiveness

indices. Warren also calculated a number of results for other developing economies.

21

ecommunications and financial services is1.5 per cent higher than that of other econo-mies. Levine (1997) found that economieswith financial systems that are better at per-forming key financial services functions tendto be economically developed, have higherincome per capita and grow at a faster pacethan those that are less developed. The Pa-cific Economic Cooperation Council (1995)found a positive relationship between wealthand openness, in that APEC member econo-mies with a higher number of GATS com-mitments also tend to have higher GDP percapita.

B. The effect of restrictions on the priceand cost of services

The results from the trade restrictive-ness indices can be used to estimate the ef-fect of restrictions on the economic perform-ance of service suppliers � prices and costsor price/cost margins. Restrictions on tradein services can have the effect of being:

� Price-increasing � restrictions protectincumbent firms from competition, andallows firms to increase their prices andexpand their price/cost margins;

Figure 8. GDP per capita at PPP and average foreign trade restrictiveness indexscores for the service sectora,b

(Score and GDP per capita at purchasing power parity)

Sources: World Bank (2001); Productivity Commission (2001a).

a The average foreign trade restrictiveness index scores are the average scores for banking, distribution, maritime,professions and telecommunications.

b The �line of best fit� (or the regression line) is a very simple econometric exercise. Restrictions on trade in servicesare only one of many determinants of GDP per capita. That said, the r-squared of 0.52 is high for cross-sectionalanalysis. Greene (1990) states that r-squared values of 0.50 are relatively high for cross-sectional analysis.

United StatesSwitzerlandJapan

Canada

Hong Kong (China)Australia

EU

Singapore

New Zealand

Rep. of Korea

Argentina

South AfricaChile

Malaysia

UruguayBrazil

Turkey

India IndonesiaPhilippines

VenezuelaColombia Mexico

Thailand

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0 2 500 5 000 7 500 10 000 12 500 15 000 17 500 20 000 22 500 25 000 27 500 30 000 32 500

GDP per capita

Scor

e

22

� Cost-increasing � restrictions preventpotential or existing firms from operat-ing efficiently and thus push up businesscosts; or

� A combination of cost-increasing andprice-increasing.

Econometric techniques can be usedto estimate these different effects. This gen-erally involves developing an econometricmodel from economic theory that includesall the relevant determinants of economicperformance of service firms in that servicesector � firm-specific and economy-wideinfluences � plus the trade restrictiveness

index as a measure of restrictions on trade.The econometric model is then used to esti-mate the determinants of economic perform-ance in that service sector and the effect ofrestrictions (McGuire, 2000).

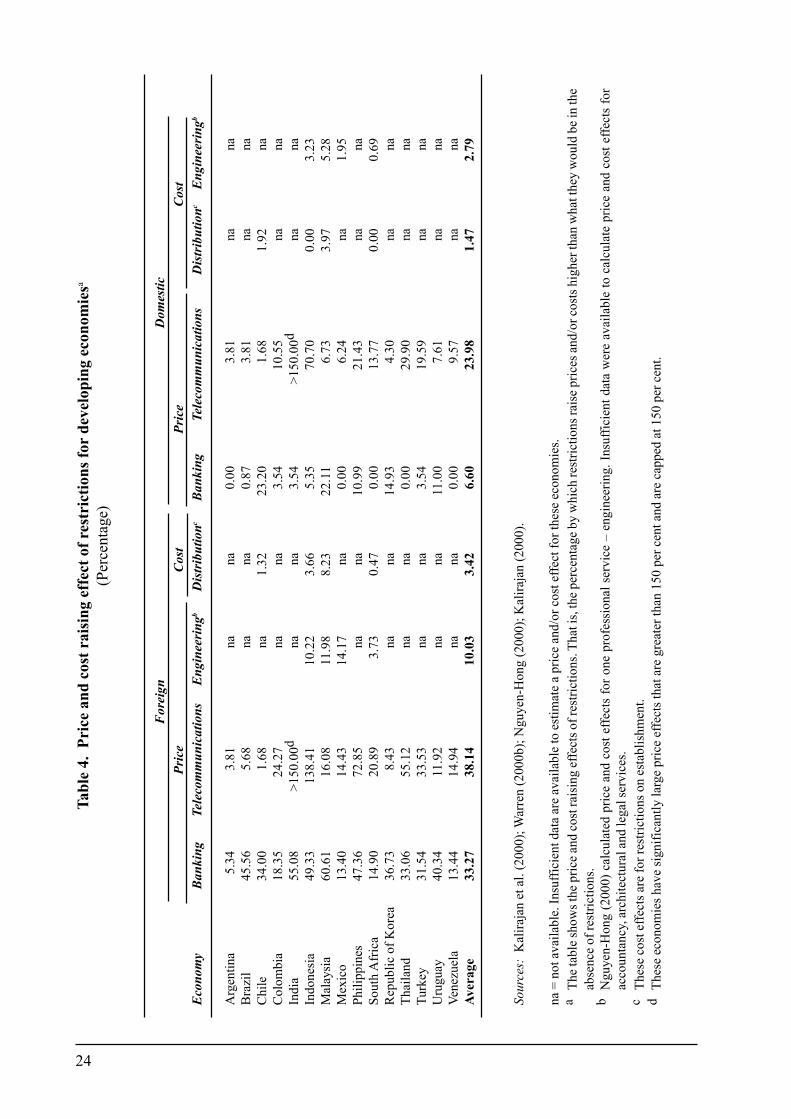

1. Results from the price and cost esti-mations

The price and cost effect measures formost developing economies are up to 150 percent higher than what they would be in theabsence of restrictions. These effects showthe extent to which restrictions, as measuredby the trade restrictiveness index, increasethe price and/or cost of services. As expected,

Figure 9. GDP per capita at PPP and foreign trade restrictiveness index scoresfor banking servicesa

(Score and GDP per capita at purchasing power parity)

Sources: World Bank (2001); Productivity Commission (2001a).

a The �line of best fit� (or the regression line) is a very simple econometric exercise. Restrictions on trade inservices are only one of many determinants of GDP per capita. That said, the r-squared of 0.48 is high for cross-sectional analysis.

Singapore

New Zealand

Rep. of Korea

Argentina

India

IndonesiaPhilippines

Colombia

Venezuela

TurkeyThailand

Brazil

Mexico

South Africa

Chile

Uruguay

Malaysia

EU

AustraliaHong Kong (China)

Canada

Japan

Switzerland

United States

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0 2 500 5 000 7 500 10 000 12 500 15 000 17 500 20 000 22 500 25 000 27 500 30 000 32 500

GDP per capita

Scor

e

23

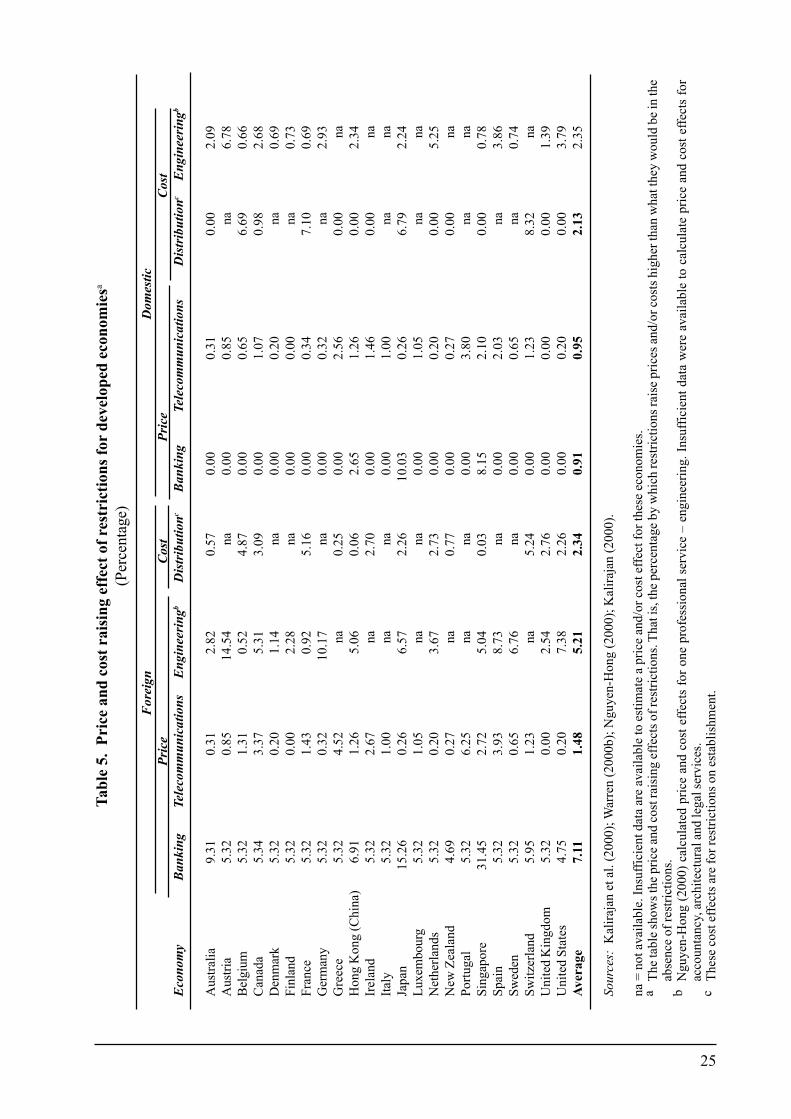

the results are similar to those from the traderestrictiveness index because they reflect, toa certain extent, the restrictions captured inthe index.

The average price and cost effectmeasures are significantly higher for devel-oping economies than for developed econo-mies (see tables 4 and 5). The average for-eign price effect in developing economies forbanking services is 33 per cent as comparedwith 7 per cent in developed economies.Thus, restrictions in developing economiesincrease the price of banking services 33 percent above what they would be in the absenceof restrictions.

Restrictions on establishment contrib-ute the most to increasing the price and costof services. These are mainly restrictions onmarket access that include restrictions on thelicensing of new firms and on FDI, as wellas requirements for foreigners to enter themarket through a specific type of legal en-tity.

The foreign and domestic cost effectmeasures for distribution and engineeringservices are significantly lower than the priceeffects. These restrictions increase the costsof service suppliers, but by a lesser extentthan the price effects.

Figure 10. GDP per capita at PPP and foreign trade restrictiveness index scoresfor telecommunications servicesa

(Score and GDP per capita at purchasing power party)

IndiaIndonesia

Philippines Colombia

United States

EU

Australia

Venezuela

TurkeyThailand

South AfricaMalaysiaUruguay

Mexico

Brazil

Chile

Argentina

Rep. of Korea

New Zealand

Singapore

Hong Kong (China)

Canada

Switzerland

Japan

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0 2 500 5 000 7 500 10 000 12 500 15 000 17 500 20 000 22 500 25 000 27 500 30 000 32 500

GDP per capita

Scor

e

Sources: World Bank (2001); Productivity Commission (2001a).

a The �line of best fit� (or the regression line) is a very simple econometric exercise. Restrictions on trade inservices are only one of many determinants of GDP per capita. That said, the r-squared of 0.49 is high forcross-sectional analysis.

24

Tabl

e 4.

Pri

ce a

nd c

ost r

aisi

ng e

ffec

t of r

estr

ictio

ns fo

r de

velo

ping

eco

nom

iesa

(Per

cent

age)

Fore

ign

Dom

estic

Pric

eCo

st

Pric

eCo

stEc

onom

yBa

nkin

gTe

leco

mm

unic

atio

ns E

ngin

eerin

gbD

istrib

utio

ncBa

nkin

gTe

leco

mm

unic

atio

nsD

istrib

utio

ncEn

gine

erin

gb

Arg

entin

a5.

343.

81na

na0.

003.

81na

naB

razi

l45

.56

5.68

nana

0.87

3.81

nana

Chi

le34

.00

1.68

na1.

3223

.20

1.68

1.92

naC

olom

bia

18.3

524

.27

nana

3.54

10.5

5na

naIn

dia

55.0

8>1

50.0

0dna

na3.

54>1

50.0

0dna

naIn

done

sia

49.3

313

8.41

10.2

23.

665.

3570

.70

0.00

3.23

Mal

aysi

a60

.61

16.0

811

.98

8.23

22.1

16.

733.

975.

28M

exic

o13

.40

14.4

314

.17

na0.

006.

24na

1.95

Phili

ppin

es47

.36

72.8

5na

na10

.99

21.4

3na

naSo

uth

Afr

ica

14.9

020

.89

3.73

0.47

0.00

13.7

70.

000.

69R

epub

lic o

f Kor

ea36

.73

8.43

nana

14.9

34.

30na

naTh

aila

nd33

.06

55.1

2na

na0.

0029

.90

nana

Turk

ey31

.54

33.5

3na

na3.

5419

.59

nana

Uru

guay

40.3

411

.92

nana

11.0

07.

61na

naVe

nezu

ela

13.4

414

.94

nana

0.00

9.57

nana

Aver

age

33.2

738

.14

10.0

33.

426.

6023

.98

1.47

2.79

Sour

ces:

Kal

iraja

n et

al.

(200

0); W

arre

n (2

000b

); N

guye

n-H

ong

(200

0); K

alira

jan

(200

0).

na =

not

ava

ilabl

e. In

suffi

cien

t dat

a ar

e av

aila

ble

to e

stim

ate

a pr

ice

and/

or c

ost e

ffect

for t

hese

eco

nom

ies.

aTh

e tab

le sh

ows t

he p

rice a

nd co

st ra

isin

g ef

fect

s of r

estri

ctio

ns. T

hat i

s, th

e per

cent

age b

y w

hich

rest

rictio

ns ra

ise p

rices

and/

or co

sts h

ighe

r tha

n w

hat t

hey

wou

ld b

e in

the

abse

nce

of re

stric

tions

.b

Ngu

yen-

Hon

g (2

000)

cal

cula

ted

pric

e an

d co

st e

ffect

s fo

r one

pro

fess

iona

l ser

vice

� e

ngin

eerin

g. In

suffi

cien

t dat

a w

ere

avai

labl

e to

cal

cula

te p

rice

and

cost

effe

cts

for

acco

unta

ncy,

arc

hite

ctur

al a

nd le

gal s

ervi

ces.

cTh

ese

cost

effe

cts a

re fo

r res

trict

ions

on

esta

blis

hmen

t.d

Thes

e ec

onom

ies h

ave

sign

ifica

ntly

larg

e pr

ice

effe

cts t

hat a

re g

reat

er th

an 1

50 p

er c

ent a

nd a

re c

appe

d at

150

per

cen

t.

25

Tabl

e 5.

Pri

ce a

nd c

ost r

aisi

ng e

ffec

t of r

estr

ictio

ns fo

r de

velo

ped

econ

omie

sa

(Per

cent

age)

Fore

ign

Dom

estic

Pric

eCo

stPr

ice

Cost

Econ

omy

Bank

ing

Tele

com

mun

icat

ions

Engi

neer

ingb

Dist

ribut

ionc

Bank

ing

Tele

com

mun

icat

ions

Dist

ribut

ionc

Engi

neer

ingb

Aus

tralia

9.31

0.31

2.82

0.57

0.00

0.31

0.00

2.09

Aus

tria

5.32

0.85

14.5

4na

0.00

0.85

na6.

78B

elgi

um5.

321.

310.

524.

870.

000.

656.

690.

66C

anad

a5.

343.

375.

313.

090.

001.

070.

982.

68D

enm

ark

5.32

0.20

1.14

na0.

000.

20na

0.69

Finl

and

5.32

0.00

2.28

na0.

000.

00na

0.73

Fran

ce5.

321.

430.

925.

160.

000.

347.

100.

69G

erm

any

5.32

0.32

10.1

7na

0.00

0.32

na2.

93G

reec

e5.

324.

52na

0.25

0.00

2.56

0.00

naH

ong

Kon

g (C

hina

)6.

911.

265.

060.

062.

651.

260.

002.

34Ir

elan

d5.

322.

67na

2.70

0.00

1.46

0.00

naIta

ly5.

321.

00na

na0.

001.

00na

naJa

pan

15.2

60.

266.

572.

2610

.03

0.26

6.79

2.24

Luxe

mbo

urg

5.32

1.05

nana

0.00

1.05

nana

Net

herla

nds

5.32

0.20

3.67

2.73

0.00

0.20

0.00

5.25

New

Zea

land

4.69

0.27

na0.

770.

000.

270.

00na

Portu

gal

5.32

6.25

nana

0.00

3.80

nana

Sing

apor

e31

.45

2.72

5.04

0.03

8.15

2.10

0.00

0.78

Spai

n5.

323.

938.

73na

0.00

2.03

na3.

86Sw

eden

5.32

0.65

6.76

na0.

000.

65na

0.74

Switz

erla

nd5.

951.

23na

5.24

0.00

1.23

8.32

naU

nite

d K

ingd

om5.

320.

002.

542.

760.

000.

000.

001.

39U

nite

d St

ates

4.75

0.20

7.38

2.26

0.00

0.20

0.00

3.79

Aver

age

7.11

1.48

5.21

2.34

0.91

0.95

2.13

2.35

Sour

ces:

Kal

iraja

n et

al.

(200

0); W

arre

n (2

000b

); N

guye

n-H

ong

(200

0); K

alira

jan

(200

0).

na =

not

ava

ilabl

e. In

suffi

cien

t dat

a ar

e av

aila

ble

to e

stim

ate

a pr

ice

and/

or c

ost e

ffect

for t

hese

eco

nom

ies.