Embed Size (px)

Citation preview

Policy Research Working Paper 8533

Trade in Developing East Asia

How It Has Changed and Why It Matters

Cristina ConstantinescuAaditya MattooMichele Ruta

East Asia and the Pacific RegionDevelopment Research GroupMacroeconomics, Trade and Investment Global Practice July 2018

WPS8533P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

Produced by the Research Support Team

Abstract

The Policy Research Working Paper Series disseminates the findings of work in progress to encourage the exchange of ideas about development issues. An objective of the series is to get the findings out quickly, even if the presentations are less than fully polished. The papers carry the names of the authors and should be cited accordingly. The findings, interpretations, and conclusions expressed in this paper are entirely those of the authors. They do not necessarily represent the views of the International Bank for Reconstruction and Development/World Bank and its affiliated organizations, or those of the Executive Directors of the World Bank or the governments they represent.

Policy Research Working Paper 8533

East Asia, for long the epitome of successful engagement in trade, faces serious challenges: technological change that may threaten the very model of labor intensive industrial-ization and a backlash against globalization that may reduce access to important markets. A detailed analysis of the evo-lution of East Asia’s trade and trade policy in goods and services leads to the conclusion that how East Asia copes with these global challenges will depend on how it addresses three more proximate national and regional challenges. The first is the emergence of one East Asian country, China, as a global trade giant—accounting for nearly one-seventh of global exports and one-tenth of global imports—which

is fundamentally altering the trading patterns and oppor-tunities of its neighbors. The second is the asymmetric implementation of national reform—remarkable open-ness to goods trade and investment coexists with relative restrictiveness of services policies—which is affecting the evolution of comparative advantage and productivity in each country. The third is the divergence between the rela-tively shallow and fragmented agreements that regulate the region’s trade and investment and the growing importance of regional and global value chains as crucial drivers of productivity growth.

This paper is a product of the East Asia and the Pacific Region, Development Research Group, and the Macroeconomics, Trade and Investment Global Practice. It is part of a larger effort by the World Bank to provide open access to its research and make a contribution to development policy discussions around the world. Policy Research Working Papers are also posted on the Web at http://www.worldbank.org/research. The authors may be contacted at [email protected], [email protected], and [email protected]

Trade in Developing East Asia:

How It Has Changed and Why It Matters*

Cristina Constantinescu, Aaditya Mattoo, Michele Ruta**

Keywords: trade policy, goods trade, services trade, China, trade agreements, global value chains

JEL codes: F13, F14, F15, F63 * This study was prepared as a background paper for the East Asia Regional Flagship report, “A Resurgent East Asia: Navigating a Changing World,” and has benefited from valuable guidance and comments from Andrew Mason and Sudhir Shetty. We are also grateful for financial support from the World Bank’s Multi‐Donor Trust Fund for Trade and Development and Strategic Research Program. The findings in this paper do not necessarily represent the views of the World Bank’s Board of Executive Directors or the governments they represent. Any errors or omissions are the authors’ responsibility. ** World Bank, 1818 H Street, Washington, D.C. 20433.

2

1. INTRODUCTION

East Asia has for long been a paragon of successful engagement in trade. Dramatic growth in exports, stimulated by openness to foreign investment, has rapidly expanded incomes and shrunk poverty. Sustaining this success, however, faces challenges. Some of these are global, notably technological change that may threaten the very model of labor intensive industrialization, and a backlash against globalization that may reduce access to some of the most important markets. How East Asia copes with these global challenges will depend on how it addresses three more proximate national and regional challenges, which are the focus of this paper. The first is the emergence of one East Asian country, China, as a global trade giant ‐ accounting for nearly one‐seventh of global exports and one‐tenth of global imports ‐ which is fundamentally altering the trading patterns and opportunities of its neighbors. The second is the asymmetric implementation of national reform – remarkable openness to goods trade and investment that coexists with relative restrictiveness of services policies – which is affecting the evolution of comparative advantage and productivity in each country. The third is the divergence between the relatively shallow and fragmented agreements that regulate the region’s trade and investment and the growing importance of regional and global value chains as crucial drivers of productivity growth.

Developing East Asia’s trade growth has been impressive in the aggregate but uneven across countries and sectors and over time. The region today accounts for about 15 percent of world trade, up from 6 percent in 1995. China, of course, stands out, with a 70 percent share today of the group’s international trade. However, countries’ trade performance diverged in the 2000s. First China’s and then Vietnam and Cambodia’s impressive growth in manufacturing exports, contrasted with the slower growth of earlier dynamos, Malaysia, Thailand and Indonesia, and there are now signs that China’s manufacturing growth itself may be reaching a plateau. Mining products have dominated the trade growth of Mongolia and Myanmar (and to a lesser extent, Indonesia). Services trade growth has been impressive only in the Philippines, and services account on average for less than 20 percent of the region’s total exports.

Even though East Asia remains vulnerable to global developments, the stake in trade within the region is growing. East Asia outperformed the growth of the rest of the world, but the region has not been spared by the global trade slowdown that started in 2012. At the same time, regional trade among developing East Asian economies has progressively increased. Intra‐developing East Asia trade was about 5 percent in the early 1990s and is close to 20 percent today. This trend reflects the shift towards China as the center of gravity of trade for these economies. For countries in the region, the share of exports to China ranges between 10 and 30 percent, and for Mongolia it is as high as 80 percent.

The countries in the region have taken divergent paths in response to China’s emergence, depending on their stage of development and pattern of comparative advantage. Most of the relatively industrialized countries – Malaysia, Thailand, the Philippines and even Indonesia ‐ have been hurt by direct competition at home and abroad from China in manufactured goods. But countries have also benefited: from increased Chinese demand, especially for services (e.g.

3

Philippines, Thailand and the Lao People’s Democratic Republic) and commodities (Indonesia, Myanmar, Lao PDR, and Mongolia); from integration into China‐linked value chains (Malaysia, Vietnam); and from relocation of Chinese production (Vietnam and Cambodia). Going forward, further integration with China will increase competitive pressures in final goods markets, but also provide better access to imported inputs and a growing demand for commodities and services. Moreover, as Chinese manufacturing competitiveness declines due to higher labor costs, developing East Asian countries can be expected to gain market shares in third markets and see an increase in the relocation of production from China.

The paths taken by individual countries have also been determined by the pattern of national reform. In the most dynamic – China itself, as well as Vietnam and Cambodia – WTO accession induced a move away from state‐owned monopolies to more competitive private provision of telecommunications, financial, transport and a range of other services. Even though their services regimes are still not fully open, the radical reform has delivered dramatic improvements in services productivity and access, international connectivity and manufacturing productivity. In the less dynamic – Indonesia, Thailand, Myanmar, and even Malaysia and the Philippines – initial regimes were less closed but the approach to reform has been more lethargic. The irony is that countries that built their manufacturing success on the back of openness to FDI have resisted similar opening in services, sacrificing productivity not just in services but also in manufacturing. A key conclusion of this paper is that further services reform is vital for continued growth, because it will affect productivity in services and in other sectors, including by influencing the evolution of comparative advantage and participation in global value chains.

In fact, the increased fragmentation of production across the region has been an important factor in trade and productivity growth. Developing East Asian countries have the highest share in the world of foreign value added in gross exports ‐ a measure of backward specialization in global value chains. Traditionally, most of the intermediate inputs used in production would come from advanced economies. But today the increasing backward participation in global value chains by countries like Vietnam is in part the result of China’s growing exports of sophisticated intermediate inputs. The rise of both global and regional value chains has been an important driver of productivity growth for developing East Asian countries. The reason is that GVCs lead to technology spillovers, learning externalities, better inputs and a more efficient international division of labor. On average, a 10 percent increase in the backward GVC participation of manufacturing sectors has increased labor productivity by 1.4 percent.

Differently from other areas in the world such as Europe and North America, much of the rise of trade, investment and global value chains in East Asia took place despite the presence of relatively shallow trade agreements. These agreements lowered tariffs but led to relatively weak commitments in areas such as services, investment and intellectual property rights. All countries are now members of the World Trade Organization (WTO). The most recent accessions include Cambodia (2004), Vietnam (2007) and Lao PDR (2013). ASEAN ‐ the Association of East Asia Nations ‐ which includes all East Asian developing countries except for Mongolia and China ‐ has progressively widened its scope and signed new agreements with third countries such as Australia, New Zealand, India and the Republic of Korea in the 2000s. But these agreements are

4

still relatively shallow and efforts are underway to negotiate deeper trade rules on investment, services, competition, intellectual property rights protection, and government procurement, as in the context of the Comprehensive and Progressive Trans‐Pacific Partnership (CPTPP). A second key conclusion of this paper is that sustaining future growth in trade, investment and GVC participation, and hence productivity growth, will require deeper integration through a more coherent set of trade rules within the region and with the rest of the world.

The rest of the paper is organized as follows. Section 2 establishes stylized facts on the trade landscape of East Asian developing countries. Section 3 focuses on four issues: the rise of China and its economic rebalancing; asymmetric trade opening and restrictions on services trade; the rise of global value chains; and the importance of deep trade agreements. Section 4 concludes.

2. THE EVOLUTION OF DEVELOPING EAST ASIA’S TRADE

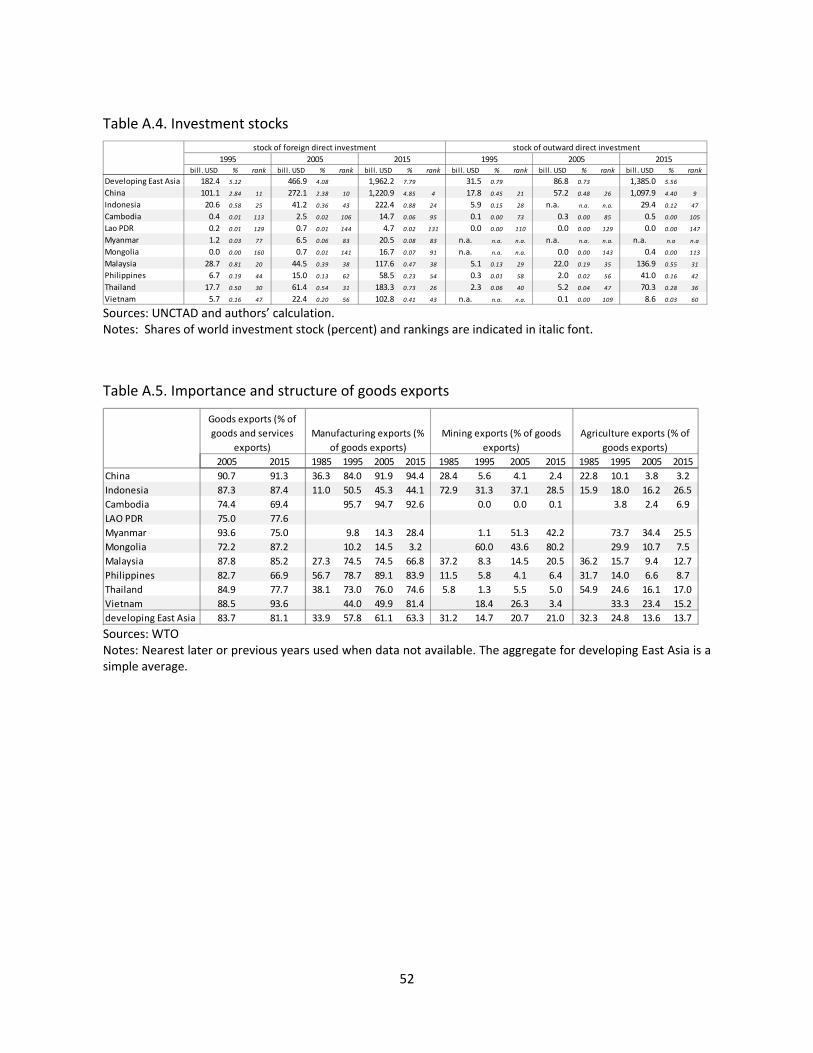

East Asia’s developing countries account today for about 15 percent of the world trade ‐ up from 6 percent in 1995 ‐ and for 8 percent of the global FDI stock ‐ up from 5 percent in 1995. There are currently 10 developing countries in the East Asia region, namely China, Mongolia, and eight of the Association of Southeast Asian Nations (ASEAN) members: Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, the Philippines, Thailand and Vietnam. These countries collectively traded 6.3 trillion USD in 2015 and absorbed almost 2 trillion USD of the global FDI stock, due in great part to the contribution of China which accounts for 70 percent of the international trade in goods and services of the developing East Asian group and for 62 percent of its FDI stock. The group’s dynamism over time is noteworthy, especially when it comes to exports of goods and services, which have tripled as a share of world trade since 1995.1

Developing East Asia’s trade shows considerable heterogeneity at the country level. The trading patterns and specialization focus of the countries in the region show divergent paths, depending on their stage of development, pattern of comparative advantage, and approach to reform. The big changes have been the emergence of China and the rise in global and regional value chains. In this section, we document these developments.

1 Developing East Asia includes some of the most active participants in trade and investment in the world. As indicated in tables A.1 through A.4, more than half of the developing East Asian countries are today among or close to the first 50 largest traders and FDI recipients in the world. Some of these countries (China, Indonesia, Malaysia, Philippines, Thailand) ranked highly in previous decades as well, while others have caught up, sometimes at impressive rates. For example, Vietnam has become the 25th largest merchandise importer by 2015, climbing up from the 82th and the 61th positions in 1980 and 1990, respectively. Among the developing East Asian countries, China is particularly noteworthy for its scale and dynamism in trade and investment. Accounting for almost 14 percent of world goods exports and 10 percent of world goods imports in 2015, China has stood out as the world’s largest exporter since 2009 (up from the 12th place in 1990), and the world’s second largest importer after the United States since 2009 (up from the 15th place in 1990). China has also ranked second and fifth in services imports, respectively, since 2013. In addition, it has been a preferred destination for FDI for many years. As of 2015, it hosted 5 percent of the global FDI. Particularly remarkable is the recent surge in China’s direct investment abroad. In 2015, China totaled 4 percent of the global outward direct investment, up from negligible shares in 2005 and before. In fact, China’s outward direct investment flows surpassed the FDI inflows for the first time in 2015.

5

a. Uneven trade growth

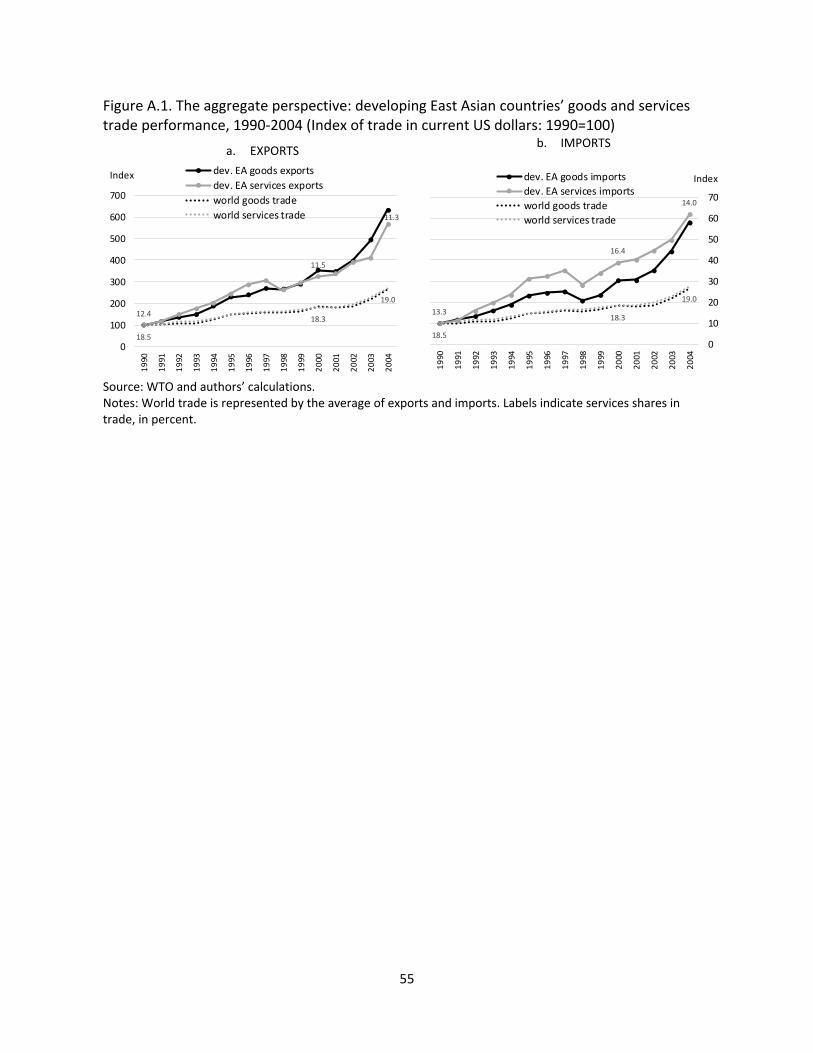

The trade performance of developing East Asian countries has been more dynamic than that of the rest of the world. The trends in the overall trade flows of developing East Asian countries reveal several specific features (Figure 1).

First, the group’s trade growth has generally outperformed global trade growth for the past 3 decades (see Figure A.1 for years prior to 2005).2

Second, the trade slowdown affecting global trade volumes since 2012 has not spared developing East Asia.3 The group’s trade volumes have slowed from a yearly average growth rate of 13 percent during 1987‐2007 to 3.8 percent since 2012. The decline is smaller, yet still apparent when China is excluded from the aggregate, with the growth rate falling from 9.8 percent during 1987‐2007 to 4 percent after 2012.

Third, developing East Asia’s exports of goods and trade in services have grown at comparable rates in the past decade. This is in contrast with the global trends, which point to a resilience of services trade growth relative to goods trade growth during the Great Recession and the recent trade slowdown. The gap between the growth in developing East Asia’s goods imports and services imports is mostly due to the recent growth in China’s travel imports.

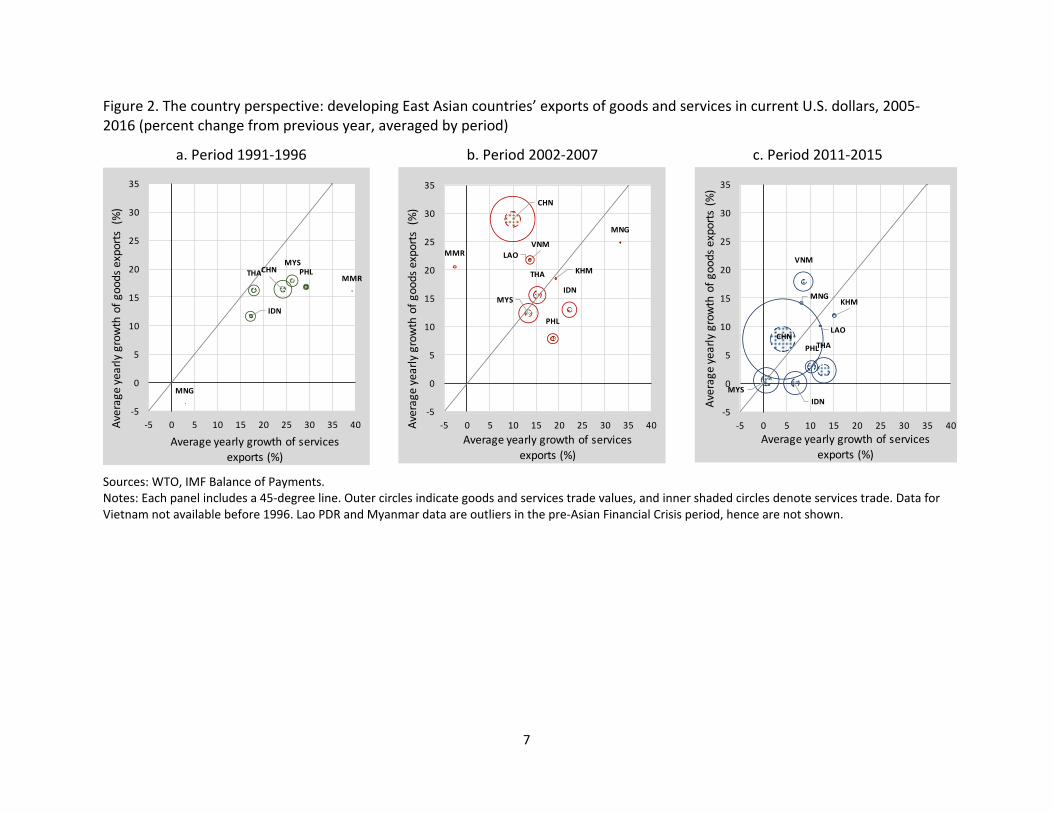

Three periods showing divergent paths can be identified in the growth experience of developing East Asian countries. An examination of the growth of goods and services export values by country and over time shows that developing East Asian countries followed different and often diverging routes for their exports, in part influenced by China’s emergence.

During the period that preceded the Asian Financial Crisis, goods exports were growing at comparable rates for most countries in the group (Figure 2a). Services exports were relatively more dynamic than goods exports, yet of significantly smaller magnitude (except in the cases of Thailand and the Philippines) and were mostly accounted for by travel exports (except for the Philippines, where other business services already had a significant contribution to services exports).

The 2000s brought a major split in the ranks (Figure 2b). China’s goods exports accelerated markedly, driven by rapid growth in manufacturing, and a switch in focus from apparel to electronic equipment. Vietnam followed in China’s footsteps, replicating its neighbor’s earlier emphasis on apparel. Cambodia, too, grew its exports based on apparel products. Thailand, Malaysia and Indonesia stayed broadly at the same levels of

2 Two notable exceptions are the period of the Asian Financial crisis and year 2015. In 2015, a combination of factors including sluggish external demand, the commodity price decline, and the macroeconomic rebalancing in China caused trade growth in East Asia to fall below the world aggregate (Constantinescu et al., 2016). 3 “The recent trade slowdown” refers to the post‐2012 sluggishness in the growth of global trade volume relative to the past rates and to real GDP growth. After bouncing back from the historic low of the Great Recession in 2010, world trade grew by 7.0 percent in 2011, slowed to 2.8 percent in 2012 and remained around 3 percent until 2016. This 3 percent is less than half the average yearly trade growth of 7 percent during period 1987‐2007. Moreover, it is in line with the GDP growth of the recent years, whereas before the crisis, and especially in the 1990s, trade was growing 2 and even 3 times faster than real GDP (Constantinescu et al., 2015).

6

growth, while the Philippines experienced a deceleration in the growth of its goods exports. Indonesia, Myanmar and Mongolia focused on commodity exports, reaping benefits from the rise of China’s imports. For most countries, goods exports growth increased relative to services exports growth. One notable exception is the Philippines, which continued its focus on other business services exports.

After the Great Recession, growth rates in export values throughout the region have been burdened by two situations (Figure 2c): the global trade slowdown and the decline in the commodity prices (particularly accelerated for fuels in 2014 and 2015). As a result, all points on the scatterplot appear closer to the origin. Yet many of the previous patterns remained and some accentuated: manufacturing exports grew faster in Vietnam and Cambodia, diverging significantly from the growth patterns of the old guard (Malaysia, Thailand, Indonesia). Export values of Indonesia, Myanmar and Mongolia were hit more severely by the commodity price shock. The Philippines continued to rely on services via other business services, while the services performance of Thailand, Cambodia, Myanmar and Lao PDR was tied to tourism.

Figure 1. The aggregate perspective: developing East Asian countries’ goods and services trade performance, 2005‐2016 (Index of trade in current US dollars: 2005=100)

a. EXPORTS b. IMPORTS

Source: World Trade Organization (WTO) and authors’ calculations. Notes: World trade is represented by the average of exports and imports. Labels indicate services shares in percent.

10.9

11.4

11.5

19.3

19.7

22.8

80

130

180

230

280

330

380

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

dev. EA goods exportsdev. EA services exportsworld goods tradeworld services trade

Index

13.5

13.4

20.3

19.3

19.7

22.8

80

13

18

23

28

33

38

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

dev. EA goods importsdev. EA services importsworld goods tradeworld services trade

Index

7

Figure 2. The country perspective: developing East Asian countries’ exports of goods and services in current U.S. dollars, 2005‐2016 (percent change from previous year, averaged by period)

a. Period 1991‐1996 b. Period 2002‐2007 c. Period 2011‐2015

Sources: WTO, IMF Balance of Payments. Notes: Each panel includes a 45‐degree line. Outer circles indicate goods and services trade values, and inner shaded circles denote services trade. Data for Vietnam not available before 1996. Lao PDR and Myanmar data are outliers in the pre‐Asian Financial Crisis period, hence are not shown.

CHN

IDN

KHM

LAO

MNG

MYS

PHLTHA

VNM

‐5

0

5

10

15

20

25

30

35

‐5 0 5 10 15 20 25 30 35 40

Average yearly growth of goo

ds exports (%)

Average yearly growth of services exports (%)

CHN

IDN

KHM

LAOMMR

MNG

MYS

PHL

THA

VNM

‐5

0

5

10

15

20

25

30

35

‐5 0 5 10 15 20 25 30 35 40Average

yea

rly growth of goo

ds exports (%)

Average yearly growth of services

exports (%)

CHN

IDN

MMR

MNG

MYSPHLTHA

‐5

0

5

10

15

20

25

30

35

‐5 0 5 10 15 20 25 30 35 40Average yearly growth of goo

ds expo

rts (%)

Average yearly growth of services exports (%)

8

b. Changing specialization

i. Goods trade

The specialization patterns within goods trade differ across countries (Figure 3). China, Malaysia, the Philippines, Thailand and Vietnam experienced increasing specialization in manufacturing – relative to the rest of the world ‐ over the previous decades. Mongolia and Myanmar continued to focus mostly on mining exports. For Indonesia, the share of manufacturing in total merchandise exports has increased from less than 10 percent in 1980 to more than 40 percent in 2015, yet mining products still dominate the country’s export basket. As indicated in Table A.5, manufacturing as a share of goods trade grew significantly during the 1980s and 1990s and then stayed broadly at the same level in countries like China, Indonesia, Malaysia, Philippines, and Thailand. In contrast, Vietnam experienced an increase of about 30 percentage points, between 2005 and 2015.

Figure 3. Share of manufacturing in goods exports (percent)

Sources: WTO Note: ISO3 country codes are indicated in labels. See Table 1 for country names.

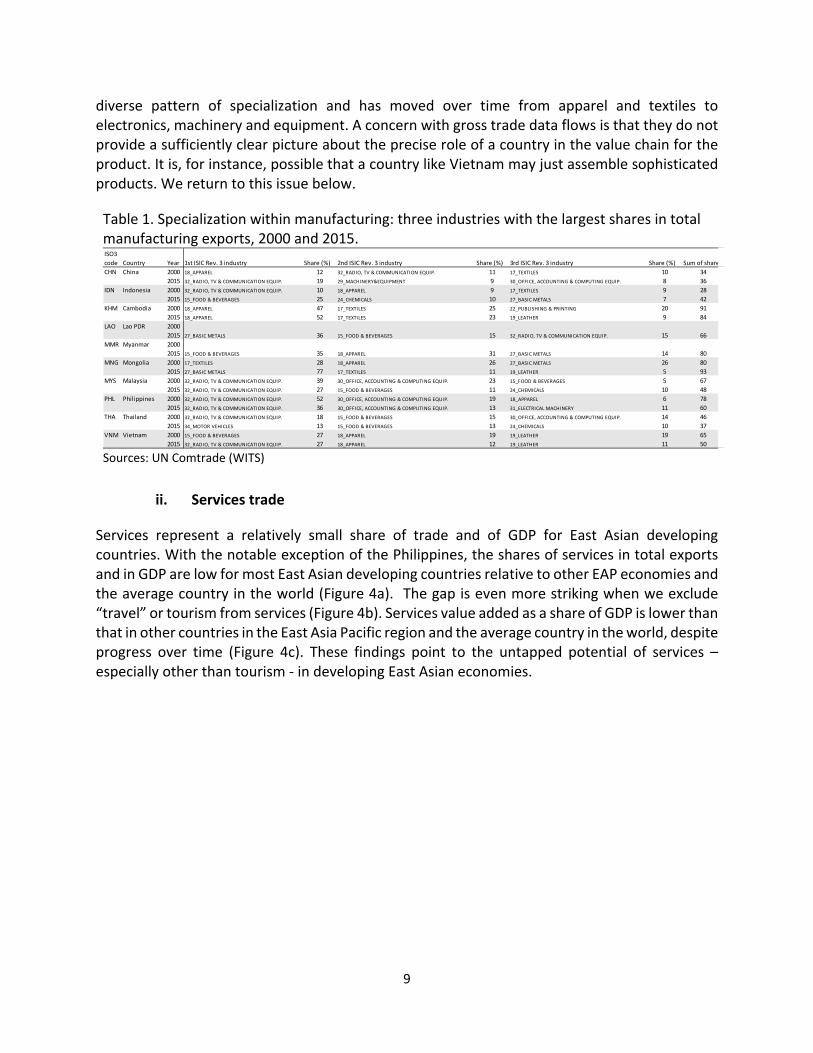

Within manufacturing, there is evidence of significant heterogeneity in exporting patterns across countries and over time (Table 1). Some countries have been and still are focused on light manufacturing (Cambodia) while others have started upgrading to more sophisticated manufacturing (Vietnam). Countries that began industrialization earlier are currently trading heavily in electronics and transport industries (Malaysia, Thailand, Philippines). China has a

IDN

MYS

PHL

THA

CHN

MMR

MNG

VNM

KHM

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

2015 or latest year with data

1980 or earliest year with data

9

diverse pattern of specialization and has moved over time from apparel and textiles to electronics, machinery and equipment. A concern with gross trade data flows is that they do not provide a sufficiently clear picture about the precise role of a country in the value chain for the product. It is, for instance, possible that a country like Vietnam may just assemble sophisticated products. We return to this issue below.

Table 1. Specialization within manufacturing: three industries with the largest shares in total manufacturing exports, 2000 and 2015.

Sources: UN Comtrade (WITS)

ii. Services trade

Services represent a relatively small share of trade and of GDP for East Asian developing countries. With the notable exception of the Philippines, the shares of services in total exports and in GDP are low for most East Asian developing countries relative to other EAP economies and the average country in the world (Figure 4a). The gap is even more striking when we exclude “travel” or tourism from services (Figure 4b). Services value added as a share of GDP is lower than that in other countries in the East Asia Pacific region and the average country in the world, despite progress over time (Figure 4c). These findings point to the untapped potential of services – especially other than tourism ‐ in developing East Asian economies.

ISO3

code Country Year 1st ISIC Rev. 3 industry Share (%) 2nd ISIC Rev. 3 industry Share (%) 3rd ISIC Rev. 3 industry Share (%) Sum of share

CHN China 2000 18_APPAREL 12 32_RADIO, TV & COMMUNICATION EQUIP. 11 17_TEXTILES 10 34

2015 32_RADIO, TV & COMMUNICATION EQUIP. 19 29_MACHINERY&EQUIPMENT 9 30_OFFICE, ACCOUNTING & COMPUTING EQUIP. 8 36

IDN Indonesia 2000 32_RADIO, TV & COMMUNICATION EQUIP. 10 18_APPAREL 9 17_TEXTILES 9 28

2015 15_FOOD & BEVERAGES 25 24_CHEMICALS 10 27_BASIC METALS 7 42

KHM Cambodia 2000 18_APPAREL 47 17_TEXTILES 25 22_PUBLISHING & PRINTING 20 91

2015 18_APPAREL 52 17_TEXTILES 23 19_LEATHER 9 84

LAO Lao PDR 2000

2015 27_BASIC METALS 36 15_FOOD & BEVERAGES 15 32_RADIO, TV & COMMUNICATION EQUIP. 15 66

MMR Myanmar 2000

2015 15_FOOD & BEVERAGES 35 18_APPAREL 31 27_BASIC METALS 14 80

MNG Mongolia 2000 17_TEXTILES 28 18_APPAREL 26 27_BASIC METALS 26 80

2015 27_BASIC METALS 77 17_TEXTILES 11 19_LEATHER 5 93

MYS Malaysia 2000 32_RADIO, TV & COMMUNICATION EQUIP. 39 30_OFFICE, ACCOUNTING & COMPUTING EQUIP. 23 15_FOOD & BEVERAGES 5 67

2015 32_RADIO, TV & COMMUNICATION EQUIP. 27 15_FOOD & BEVERAGES 11 24_CHEMICALS 10 48

PHL Philippines 2000 32_RADIO, TV & COMMUNICATION EQUIP. 52 30_OFFICE, ACCOUNTING & COMPUTING EQUIP. 19 18_APPAREL 6 78

2015 32_RADIO, TV & COMMUNICATION EQUIP. 36 30_OFFICE, ACCOUNTING & COMPUTING EQUIP. 13 31_ELECTRICAL MACHINERY 11 60

THA Thailand 2000 32_RADIO, TV & COMMUNICATION EQUIP. 18 15_FOOD & BEVERAGES 15 30_OFFICE, ACCOUNTING & COMPUTING EQUIP. 14 46

2015 34_MOTOR VEHICLES 13 15_FOOD & BEVERAGES 13 24_CHEMICALS 10 37

VNM Vietnam 2000 15_FOOD & BEVERAGES 27 18_APPAREL 19 19_LEATHER 19 65

2015 32_RADIO, TV & COMMUNICATION EQUIP. 27 18_APPAREL 12 19_LEATHER 11 50

10

Figure 4. The importances of services in developing East Asian countries’ trade and value added, according to the level of development a. Services exports

b. Non‐travel services exports

c. Services value added

Sources: WTO, World Bank World Development Indicators (WDI). Notes: GNI is in current US dollars calculated using the Atlas method. Vertical lines indicate thresholds for lower middle, upper middle and high income categories*. In panel b, countries with share of services in total exports greater than 40 percent are not shown: AFG, COM, CYP, DJI, GRC, LUX, KIR, CPV, CUB, MLT, IRL, LBN *https://datahelpdesk.worldbank.org/knowledgebase/articles/906519‐world‐bank‐country‐and‐lending‐groups.

CHNIDN

KHMLAO

MMR

MNG

MYSPHL THA

VNM

0

10

20

30

40

50

60

70

80

90

100

4 6 8 10 12

Share of services in total exports (percent)

Log of GNI per capita

2005

CHNIDN

KHM

LAOMMR

MNG MYS

PHL

THA

VNM

0

10

20

30

40

50

60

70

80

90

100

4 6 8 10 12

Share of services in total exports (percent)

Log of GNI per capita

2015

CHN

IDNKHMLAO

MMR

MNG

MYS

PHL

THA

VNM

0

5

10

15

20

25

30

35

40

4 6 8 10 12

Share of services (excl. travel) in total

exports (percent)

Log of GNI per capita

2005

CHNIDN

KHMLAO

MMRMNG MYS

PHL

THAVNM

0

5

10

15

20

25

30

35

40

4 6 8 10 12

Share of services (excl. travel) in total exports

(percent)

Log of GNI per capita

2015

CHNKHM

LAOMMR

MNG MYS

PHL THA

0

10

20

30

40

50

60

70

80

90

100

4 6 8 10 12

Share of services value ad

ded

in GDP

(percent)

Log of GNI per capita

2005

CHN

IDNKHMLAO

MMR

MNG MYS

PHLTHA

VNM

20

30

40

50

60

70

80

90

100

4 6 8 10 12

Share of services value ad

ded

in GDP

(percent)

Log of GNI per capita

2015

11

The composition of services exports in the developing East Asian economies varies by country and over time (Table 2). For most developing East Asian countries (Indonesia, Cambodia, Lao PDR, Myanmar, Malaysia, Philippines and Thailand), travel services exports are at around 50 percent of total services exports or more. This is not the case in China and the Philippines, where “other business services” exports are currently relatively larger than other services.

Table 2. Importance of services in trade and in GDP, and the structure of services exports

Sources: WTO Notes: Nearest later or previous years used when data not available for 2005 and 2015. The aggregate for developing East Asia is a simple average.

iii. Integration in global value chains

Developing East Asian countries are among the most integrated into global value chains (GVCs). Their integration is mostly occurring via backward participation in GVCs – that is, via using imported intermediate inputs in their exports (Figure 5a). Trade in value added (TiVA) data indicate that the share of foreign value added in gross exports in China and the other developing East Asian economies was higher than the aggregate for other regions during 1995‐2011.4 The levels of forward participation (intermediate exports used in other countries’ exports) are lower than backward participation and also lower than forward participation of other regions, except for the countries that have commodities as significant items in their export bundles, such as Indonesia (Figure 5b).

4 Based on EORA data, developing East Asia is one of the three groups of countries with the highest levels of backward participation, the other two being Western Europe and the industrialized East Asia. China’s share is lower because the EORA input output tables do not account for processing trade.

2005 2015 2005 2015 2005 2015 2005 2015 1985 1995 2005 2015

CHN China 9.3 8.7 19.8 17.8 37.6 20.8 25.6 50.3 29.4 33.7 41.3 50.2

IDN Indonesia 12.7 12.6 22.5 16.0 35.8 49.8 41.2 31.2 n.a. 41.1 40.3 46.5

KHM Cambodia 25.6 30.6 12.8 11.8 78.9 82.9 8.3 5.3 n.a. 35.6 41.2 42.3

LAO Lao PDR 25.0 22.4 19.8 8.5 75.4 85.1 4.8 6.4 n.a. 25.1 39.2 41.7

MMR Myanmar 6.4 25.0 45.7 11.6 25.8 55.3 19.2 25.4 n.a. n.a 35.8 38.7

MNG Mongolia 27.8 12.8 48.7 34.7 43.2 35.7 8.1 28.4 56.4 31.0 41.7 51.6

MYS Malaysia 12.2 14.8 20.7 11.6 45.0 50.9 33.4 30.2 40.5 45.6 45.8 55.1

PHL Philippines 17.3 33.1 10.9 6.7 26.6 18.2 62.1 74.9 40.4 46.3 53.5 59.0

THA Thailand 15.1 22.3 23.4 9.4 48.4 73.2 28.2 17.5 52.3 53.4 52.2 55.1

VNM Vietnam 11.5 6.4 27.6 21.9 54.3 66.2 18.1 12.0 n.a. n.a n.a 44.2

16.3 18.9 25.2 15.0 47.1 53.8 24.9 28.1 43.8 39.0 43.5 48.4

ISO3

code

dev. East Asia

Country

Travel services (% of

services exports)

Other services (% of

services exports) Services values added (% of GDP)

Services exports (% of

goods and services

exports)

Transport services (% of

services exports)

12

Figure 5. GVC participation of China and the other developing East Asia relative to the other regions of the world (percent of gross exports).

a. Backward participation in GVCs b. Forward participation in GVCs

Source: Authors’ calculations based on OECD Trade in Value Added (TiVA) Notes: Backward participation is measured as the share of foreign value added in the total gross exports of a country. Forward participation is a country’s domestic value added that is reexported by other countries, as a share of the country’s exports. *”Other East Asia” ‐ includes BRN, HKG, KOR, JPN, MAC, SGP, TWN; Other EAS ‐ East Asia and Pacific (all income levels) except East Asia; Other ECS ‐ Europe and Central Asia (all income levels) except Western Europe; LCN ‐ Latin America & the Caribbean (all income levels); MEA ‐ Middle East and North Africa (all income levels); SAS ‐ South Asia; SSF ‐ Sub‐Saharan Africa (all income levels).

There are important differences in GVC participation between developing East Asian countries (Figure 6). Within developing East Asia, the share of foreign value added in gross exports ranges from high for Malaysia to low for Indonesia (as well as Lao PDR and Myanmar, based on the EORA MRIO data). In terms of dynamism, interesting patterns emerge for three countries. Vietnam’s participation in GVCs has increased steadily overtime and especially in recent years, reflecting its deeper engagement into GVCs. In contrast, the Philippines saw a decline in the backward participation – possibly reflecting a retreat from GVCs, rather than an upgrade to more value added‐intensive activities. Finally, for China, the share of foreign value added in gross exports has been declining since the mid‐2000s, reflecting the substitution of imported inputs for domestically‐produced ones. At the same time, China has gradually increased its forward participation in global value chains with increasing exports of intermediate inputs.

5

10

15

20

25

30

35

40

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

China World

Other East Asia* Developing East Asia (excl. China)

Other ECS LCN (excl. Mex)

MEA North America (incl. Mex.)

Other EAS SAS

SSF Western Europe

5

10

15

20

25

30

35

40

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

China World

Other East Asia Developing East Asia (excl. China)

Other ECS LCN (excl. Mex)

MEA North America (incl. Mex.)

Other EAS SAS

SSF Western Europe

13

Figure 6. GVC participation of developing East Asian countries (percent of gross exports)

a. Backward participation in GVCs b. Forward participation in GVCs

Source: Authors’ calculations based on OECD TiVA Notes: Backward participation is measured as the share of foreign value added in the total gross exports of a country. Forward participation is a country’s domestic value added that is reexported by other countries, as a share of the country’s exports.

There is also important sectoral variation in GVC participation within East Asia. Figure 7 provides further illustration of the heterogeneous ways in which developing East Asian countries participate in GVCs. Indonesia is notable for its forward participation via commodities, Philippines for its forward participation via services, while Malaysia, Vietnam, Cambodia and Thailand for the backward participation via manufacturing. A comparison between 1995 and 2011 highlights the ascension of Vietnam and the decline of the Philippines as relates to the foreign value‐added content in gross manufacturing exports, and the increase in forward participation of Indonesia’s commodity sectors and of the Philippines’ services sector. The increase in the reexports of the Philippines’ domestic value added from manufacturing is driven by the electric equipment sector.

5

10

15

20

25

30

35

40

45

50

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

CHN IDN KHM MYS

PHL THA VNM

0

5

10

15

20

25

30

35

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

CHN IDN KHM MYS

PHL THA VNM

14

Figure 7. GVC participation in developing East Asia, by country and sector (percent of gross exports)

Source: Authors’ calculations based on OECD TiVA Notes: Backward participation is measured as the share of foreign value added (from commodities, manufacturing and services) in the total gross exports of a country. Forward participation is a country’s domestic value added (from commodities, manufacturing and services) that is reexported by other countries, as a share of the country’s exports.

0

5

10

15

20

25

commodities manufacturing services commodities manufacturing services

a. 1995

CHN IDN KHM MYS PHL THA VNM World

backward participation forward participation

0

5

10

15

20

25

commodities manufacturing services commodities manufacturing services

b. 2011

CHN IDN KHM MYS PHL THA VNM World

backward participation forward participation

15

c. Shifting partners

Close to 50 percent of developing East Asian countries’ trade is with countries outside the region (Figure 8). Several composition‐related trends are noteworthy. First, intra‐developing East Asian trade increased from around 5 percent in the early 1990s to 18 percent by 2016. Second, the share of other East Asian countries has gradually declined, notably since the late 2000s.5 Third, while trade with other advanced economies remained roughly stable, trade with other developing countries outside the region increased, particularly in the late 2000s.

Figure 8. Developing East Asia: bilateral trade (billion US dollars)

Source: IMF Direction of Trade Statistics (DOTS). Notes: trade is exports of goods plus imports of goods. *”Other East Asia” ‐ includes BRN, HKG, KOR, JPN, MAC, SGP, TWN; Other EAS ‐ East Asia and Pacific (all income levels) except East Asia; Other ECS ‐ Europe and Central Asia (all income levels) except Western Europe; LCN ‐ Latin America & the Caribbean (all income levels); MEA ‐ Middle East and North Africa (all income levels); SAS ‐ South Asia; SSF ‐ Sub‐Saharan Africa (all income levels).

The center of gravity for developing East Asian countries has shifted toward China. Figure 9 presents the regional trading patterns for the 10 developing East Asian countries in 1995 and 2015. The most striking development is the increase in exposure to China, both as an origin for goods imports and as a destination for goods exports. Other developing East Asian countries have also gained in importance as trading partners. Yet the opposite seems to be true of the other East Asia group. Even though the absolute traded values have generally expanded over time (there are exceptions, for example during crisis years), the goods trade of developing East Asian

5 Other East Asia includes Brunei; Hong Kong SAR, China; Korea; Japan; Macao SAR, China; Singapore; and Taiwan, China.

0

1

2

3

4

5

6

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

developing East Asia other East Asia*

Other EAS USA

Western Europe other ECS

LCN MEA

Canada and Mexico SAS

SSF

16

countries has been gradually shifting towards China (see trade values and more information on shares in Tables A.6 and A.7). In 2015, Mongolia and Lao PDR were the most exposed developing East Asian countries to intra‐regional trade. Mongolia sent 80 percent of its goods exports to China, while Lao PDR traded almost exclusively with developing East Asian countries, although within this group, it traded relatively less with China. Malaysia, Indonesia and Thailand were the least exposed to China, as they traded relatively more with other East Asia. Vietnam and Cambodia’s trading patterns suggest engagement in GVCs via triangular trade: importing from China and other developing East Asian countries and exporting overseas to the US and Western Europe.6

Figure 9. Bilateral trade in goods of developing East Asian countries, selected partners

a. Bilateral trade with China Exports to China (% of gross exports) Imports from China (% of gross imports)

6 Similar patterns emerge when examining bilateral trade in value added instead of bilateral gross trade.

AFG

AGO

AUS

CHL

COD

COG

GNQ

HKG

IRN

IRQ

KAZ

KOR

MAC

MLI

MRT

OMN

PER

SLB

TKM

URY

YEM

IDNKHM

LAO

MMR

MNG

MYS

PHL THA

VNM

0

10

20

30

40

50

60

70

80

90

0 10 20 30 40

2015

1995

AFG

ARE

AUSBGD

CHL COD

ETH GHA

GMB

HKG

IRQ JPN

KEN

KGZ

KOR

MAC

MRT

NERNGA

NPL

PAK

PER

SLB TGO

USAUZB

IDN

KHM

LAO

MMR

MNG

MYSPHL

THA

VNM

0

5

10

15

20

25

30

35

40

45

50

0 10 20 30 40

2015

1995

17

b. Bilateral trade with other developing East Asian countries (excl. China) Exports to dev. East Asia (% of gross exports) Imports from dev. East Asia (% of gross imports)

c. Bilateral trade with other East Asian countries Exports to other East Asia (% of gross exports) Imports from other East Asia (% of gross imports)

AUS

BEN

BFA

BRN

GNB

JPNKOR

MDV

MLI

OMN

SGP

TGO

ZMB

CHN

IDN

KHM

LAO

MMR

MNG

MYS

PHL

THA

VNM

0

10

20

30

40

50

60

0 10 20 30 40 50 60

2015

1995

AUS

BEN

BRN

DJI

GNB

IRQ

JPNLKA

MDV

NPL

NZLPAK

PNG

SGP

SLB

VUT

CHN

IDN

KHM

LAO

MMR

MNG

MYS

PHL

THA

VNM

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 602015

1995

ARE

AUS

BRN

CHL

COG

GNQ

IRN

JPN

KOR

KWT

MAC

MLT

MRT

NER

NZL

OMN

PNG QAT

SAU

SDNSGP

SLB

TON

USA

VUTYEMZMB

CHNIDN

KHM

LAO

MMR

MNG

MYS

PHL

THAVNM

0

10

20

30

40

50

60

70

80

0 20 40 60 80 100

2015

1995

AFGARE

AUS

BGD

BRN

CAFDJI

FJIGUY

HKG

KOR

LBR

LKAMAC

MDV

NPL

NZL

OMN

PNG

PRY

SDN

SGP

SLB

SYC

USA

VUT

WSM

CHN

IDN

KHM

LAO

MMR

MNG

MYS

PHL

THA

VNM

0

10

20

30

40

50

60

0 20 40 60 80

2015

1995

18

d. Bilateral trade with the U.S. and Western Europe Exports to the U.S. and Western Europe

(% of gross exports) Imports from the U.S. and Western Europe

(% of gross imports)

Source: IMF DOTS and authors’ calculations. Notes: 45‐degree line shown as dotted line. Labels indicate developing East Asian countries and other selected countries.

Much of the rise of China as a trade partner of developing East Asian countries has to do with its larger role in GVCs. Figure 10 depicts the Chinese foreign value added embodied in the other countries’ gross exports of goods and services, as well as the domestic value added produced in various countries that is re‐exported by China.7 Developing East Asian countries collaborate more closely with China on these two aspects of GVC participation relative to most other countries in the world, but different countries have different roles. Vietnam and Cambodia have a high content of Chinese value added in gross exports (Vietnam in its exports of electrical and optical equipment and Cambodia in its exports of garments), an indication of downstream positioning relative to China in a triangular trade to destinations overseas. Malaysia, Philippines and Thailand, which are not highly dependent on China in the bilateral gross trade charts, have more than 40 percent of their forward participation in the electrical equipment industry accounted for by China’s re‐exports. This suggests that the three countries are heavily integrated in global value chains, upstream of China, as its suppliers of parts and components.

7 Note that country availability is restricted to the coverage in the OECD TiVA Database. For example, Mongolia, a country with high gross trade exposure to China, is not included.

CHN

IDN

KHM

LAOMMR

MNG

MYS

PHLTHA

VNM

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100

2015

1995

CHN

IDN

K…LAO

MMR

MNG

MYS

PHLTHA

VNM

0

10

20

30

40

50

60

70

80

90

0 20 40 60 80

2015

1995

19

Figure 10a: China’s role in developing East Asia’s participation in GVCs China’s share in the total FVA embodied in a

country’s gross exports (percent) A country’s share in DVA embodied in China’s gross

exports (percent)

Source: OECD TiVA and authors’ calculations. Notes: 45‐degree line shown as dotted line. FVA stands for “foreign value added”; DVA stands for: “domestic value added.” Labels indicate developing East Asian countries and other selected countries. Note: Trade refers to both goods and services.

Figure 10b: China’s role in developing East Asia’s participation in GVCs: focus on the electrical and optical equipment industry China’s share in the total FVA embodied in a country’s gross exports of electrical and optical equip. (percent)

A country’s share in DVA from electrical equip. sector embodied in China’s gross exports (percent)

Source: OECD TiVA and authors’ calculations. Notes: 45‐degree line shown as dotted line. FVA stands for “foreign value added”; DVA stands for: “domestic value added.” Labels indicate developing East Asian countries and other selected countries.

AUS

BRA

BRNCOL

CZE

HKG

IND

JPN

KOR

MEX

PER

RUS

SGP

TWNUSA

IDN

KHM

MYS

PHL

THA

VNM

0

5

10

15

20

25

30

35

0 5 10 15 20

2011

1995

ARG

AUS

BRA

CANCHE

CHL

CRI

DEU

HKG

INDISR

JPN

KOR

NZL

PER

RUS

SAU

SGP

TWN

USA

ZAFIDN

KHM

MYS

PHL

THA

VNM

0

5

10

15

20

25

30

35

40

45

50

0 5 10 15 20 25 30

2011

1995

ARG

AUS

BRA

CAN

CHL

COLCZE

GBR

HKG

HUN

IND

JPN

KOR

MEX

NZL

PER

POLRUS

SGPTUR

TWN

USA

ZAF

IDN

KHM

MYS

PHL

THA

VNM

0

5

10

15

20

25

30

0 2 4 6 8 10 12 14

2011

1995

AUSCANCHE

CHL

CRI

DEU

ESP

FINFRA

GBRHKG

IND

IRL

ISR

JPN

KOR

LUX

MLT

NOR

NZL

ROU

ROW

RUS

SGP

SWE

TWN

USA

IDN

KHM

MYS

PHL

THA

VNM

0

10

20

30

40

50

60

0 5 10 15 20 25 30

2011

1995

20

As a source of final demand, the role of China in the region is still limited. Gross trade statistics show that developing Asian economies vary in their exposure to China, and that the exposure has been growing over time. Yet these indicators do not clarify whether a country is potentially exposed to shocks to Chinese domestic demand or to shocks to demand of other countries that are positioned downstream from China in an international supply chain. Examining the decomposed bilateral exports to China suggests that, among the developing East Asian countries for which we have the required data, the Philippines and Indonesia are relatively more exposed to Chinese demand. This exposure could reflect the fact that these two countries, with exports respectively dominated by services and natural resources, are different from the other East Asian countries which are linked to China through manufacturing value chains that ultimately serve third countries. In general, the exposure of East Asian economies to demand shocks in China is, however, not much higher than that of other economies (Figure 11).

Figure 11. Share of China in gross exports of goods and services, by type of value added, 2011

Source: OECD TiVA, Wang et al. (2013) and authors’ calculations. Note: Countries are sorted by the total domestic value added absorbed in China as a share of multilateral gross exports.

0

5

10

15

20

25

30

35

40

45

HKG

AUS

TWN

JPN

CHL

BRA

PHL*

KOR

ZAF

IDN*

SAU

MYS*

NZL

THA*

VNM*

RUS

ARG

SGP

IND

CRI

USA

DEU

COL

BRN

ISR

CHE

KHM*

CAN

Other

Foreign value added in gross exports to China

Domestic value added not absorbed in China

Domestic value added in intermediates absorbed in China

Domestic value added in final goods and services absorbed in China

% of multilateral gross exports

21

3. THE IMPLICATIONS OF AND THE POLICY RESPONSE TO THE CHANGING TRADE PATTERN

This section addresses four questions associated with the changing trade trends outlined in Section 2. The first pair of questions relates to China’s emergence and the appropriate national policy response. What are the trade effects of the growth of China on other developing East Asian countries? And how has the asymmetric opening of goods and services trade affected the productivity and comparative advantage of developing East Asian economies? The second pair relates to the emergence of GVCs and the appropriate response in terms of international cooperation. How does the increasing fragmentation of production across borders affect developing East Asian countries’ productivity? And how far are the international agreements negotiated by developing East Asia fostering the growth of GVCs and deeper international integration? We will investigate these issues in turn.

a. The heterogeneous impact of China

The inclusion of China in the global trade system has had a significant impact on developing East Asian countries. This section provides an assessment of the effect on trade flows. As discussed in Section 2, the rise of China as a major player in world trade has changed the nature of intra‐regional and extra‐regional trade for developing East Asian countries. China’s share of world exports increased between 1995 and 2015 from about 2 percent to 11 percent. In light of this change, a number of studies (most notably, Autor et al., 2013) have investigated the impact of the China (supply) shock on other countries. At the same time, China grew as an importer, notably of agricultural and mining products where its share of world imports increased from 2 percent in 1995 to 10 percent in 2015. This China (demand) shock also affected its trade partners, altering their trade patterns. China’s supply and demand shocks have contrasting effects on East Asian developing countries that ultimately depend on their production and trade structures and the similarity of their export destinations with China. An empirical investigation is required to quantify these various channels.

Econometric analysis points to a heterogeneous impact of China‐related trade shocks on exports of developing East Asian countries. Bastos (2018) examines empirically the effect of supply and demand shocks associated with China’s trade dynamics on multilateral exports of the Belt and Road Initiative (BRI) countries – a group that includes, but is not limited to developing East Asian countries ‐ and finds a significant overall effect and heterogeneous impacts by country and period, for both types of trade shocks.8,9 Table 1 presents the estimated coefficients obtained in

8 Intuitively, China‐related supply or competition shocks are associated with China’s rising global exports, and may pose a competition challenge especially for countries with an initial export structure that is similar to China’s. In contrast, China‐related demand shocks are associated with China’s rising imports, and may represent an opportunity for countries with initial export profiles matching China’s import structure. 9 The methodological approach in Bastos (2018) is built on insights by Autor et al. (2013). The estimation equation relates multilateral exports by country, sector and period to the China‐related supply and demand shocks, where the supply shock is computed as the product of the change in log of multilateral exports of China in a sector and period and the export similarity index between China and the exporting country and the same sector in 1995, while the demand shock is computed by the product of the change in log of multilateral imports of China in a sector and period and the similarity index between China’s imports and the country’s exports in the same sector in

22

Bastos (2018) for the average BRI country and for each developing East Asian country separately. The results suggest that China‐related supply shocks may have intensified in the last decade compared to the previous. Indeed, while competition pressures from China appear to have been innocuous for the multilateral exports of the developing East Asian countries during the period 1995‐2015, they have had a negative and significant impact for the exports of Indonesia, Malaysia, the Philippines, Thailand and Vietnam during period 2005‐2015. Demand shocks associated with the rise in China’s imports are found to have significantly boosted multilateral exports of Cambodia, Indonesia and Thailand, during 1995‐2015, and of Indonesia and Mongolia, during 2005‐2015.

The positive effects associated with the rise in Chinese imports may have offset China’s competition pressure on developing East Asian countries in external markets, but not consistently throughout the last two decades. The finding in Bastos (2018), that China‐driven supply shocks may have intensified in the last decade, holds for the entire group of BRI countries, as suggested by the changing magnitude of the estimate for the average BRI country (Table 3, last row). The implication is that up until 2005, China’s competition pressure in external markets, for countries in East Asia specifically, and for BRI countries in general, was offset by the positive effects associated with the increasing Chinese imports. This insight corroborates the findings in World Bank (2007) about the effect of the rise of China on the exports of East Asian countries during period 1985‐2004.10

1995. Regressions control for period effects (given that up to four 5‐year periods from the interval 1995‐2015 are being used) and panel fixed effects (either country‐industry level, for the regressions including all countries, or industry‐level, for the country‐specific regressions). Potential endogeneity concerns are addressed by employing 2SLS estimation, whereby the change in China’s multilateral exports is instrumented using changes in sectoral Chinese exports and imports to the top 10 destinations and sources. 10 Using a different methodology, the chapter on trade in World Bank (2007) finds that export growth to non‐China markets in industrial products was affected negatively by Chinese exports in the same products during period 1984‐2004 and more so during 2000‐2004. In addition, it finds that the negative effect was offset by the positive impact of China‐related demand shocks (with countries more seriously affected by the supply shocks also being the ones gaining from increased exports to China, notably Korea, Singapore, and Taiwan, China). The chapter further indicates that China appears to have been pushing other exporters up the value chain in parts and components, so that everyone ended up benefitting via specialization in specific tasks, and engagement in GVC and triangular trade.

23

Table 3. Impact of China shocks on exports of selected BRI countries.

Source: Bastos (2018). Notes: Robust standard errors clustered by country‐industry, *** p<0.01, ** p<0.05, * p<0.1. Reported coefficients are obtained using the 2SLS estimation method.

The China effect on trade depends on the complementarity of the trade structure of developing East Asian countries with China and the similarity of their export destinations with China. Bastos (2018) also offers an intuitive approach – validated by the previous econometric results ‐ on how to identify countries that are more likely to be impacted by China’s rise. First, countries that share a similarity of exports with China in both the exported products and the destination markets are likely to face competition pressure from China in the markets abroad (Figure 12a). Indeed, for Vietnam, Thailand, Malaysia and the Philippines, which have the highest similarity index among the BRI countries in 2015, the econometric analysis yields negative and significant supply shock coefficients in the regressions covering the period 2005‐2015. Second, countries whose exports are similar to China’s imports and who also have a large share of their exports going to China are likely to benefit from an increase in Chinese imports (Figure 12b). For Instance, Mongolia, a country in this category, is found to have a positive and significant demand shock effect during the period 2005‐2015. Third, countries that share a similarity of production structure (proxied by exports) with China and also have a large share of imports sourced from China are likely to be affected negatively in their domestic markets by Chinese competition (Figure 12c).

Country 1995-2015 2005-2015 1995-2015 2005-2015Cambodia 35.46 43.36 161.33*** 79.6

(31.89) (46.32) (27.40) (189.09)

Indonesia -12.87 -31.78* 39.76*** 36.97***

(9.82) (17.98) (15.02) (13.73)

Lao -63.83 -55.18 -189.1 59.5

(43.05) (44.35) (641.80) (363.26)

Malaysia 7.21 -83.48** 19.03 29.57*

(12.01) (40.64) (16.24) (16.19)

Myanmar -30.59 -35.05 21.16 -12.52

(49.83) (102.48) (15.78) (97.22)

Philippines -13.07 -70.54*** 40.7 61.96

(14.32) (24.35) (30.56) (38.34)

Thailand -1.34 -40.84** 32.35*** 6.79

(10.38) (17.74) (9.34) (23.90)

Vietnam -1.58 -36.92*** 38.18 4.23

(15.27) (11.04) (45.67) (13.05)

Mongolia 94.95 -129.03 126.42 512.76***

(66.45) (190.87) (104.73) (130.44)

Average BRI country -21.75*** -52.82*** 42.52*** 44.95***

(3.88) (8.31) (7.27) (16.94)

Supply shock Demand shock

24

Figure 12. Identifying opportunities and vulnerabilities associated with competition from China

a. Exposure to competition from China in third export markets: export similarity with China in products and markets, 2015

b. Exposure to demand shocks from China, 2015

c. Exposure to import competition from China in the domestic market, 2015

Source: Bastos (2018) Note: 45‐degree line shown as dotted line.

Further integration with China will affect developing East Asian countries differently and the extent of this impact will depend on the ongoing rebalancing of the Chinese economy.11 In recent years, China has been engaged in a number of regional processes, the Belt and Road Initiative (BRI) and the Regional Comprehensive Economic Partnership (RCEP), which are likely to further reduce trade costs within East Asia because of improved transport infrastructure and reduced

11 See Lardy (2012), Pettis (2014) and Constantinescu, Mattoo and Ruta (2016) for an analysis of the implications of China’s rebalancing.

0

0.05

0.1

0.15

0.2

0.25

0.3

VNM

THA

MYS

PHL

IND

SGP

HKG

IDN

CZE

POL

TUR

ISR

HUN

ROU

KHM

SVK

BGR

EST

SVN

LKA

LTU

PAK

BGD

LVA

GRC

HRV

EGY

SRB

ARE

BIH

MMR

UKR

NPL

RUS

MDA

JOR

BHR

ALB

MKD

LBN

BLR

GEO

LAO

SAU

OMN

ARM

QAT

KWT

MNE

KAZ

BRN

KGZ

IRN

SYR

MDV

MNG

AFG

UZB

YEM AZE

PSE

TJK

TLS

TKM BTN

IRQ

AFGALB

ARE

ARM

AZE

BHR

BGD

BLR

BTN

BIH

BRN

BGR

HRV

CZEEGY

ESTGEO

GRC

HKG

HUN

IND

IRN

IRQ

ISR

JOR

KAZ

KWT

KGZ

LVA

LBN

LTUMKD

MDVMDAMNE

NPL

OMN

PAK

PSE

POLQAT

ROU

RUS

SAU

SRB

SGP

SVKSVN

LKA

SYR

TJK

TLS

TURTKMUKR

UZB

YEM

KHM IDN

LAOMYS

MNG

MMR

PHLTHA

VNM

0

0.1

0.2

0.3

0.4

0.5

0.6

0 0.1 0.2 0.3 0.4 0.5

Share of im

ports sourced

from China

Similarity between country's exports and China's exports

AFGALB

ARE

ARM

AZEBHRBGD BLR

BTN BIHBRNBGR

HRV CZEEGYEST

GEO

GRC

HKG

HUNIND

IRN

IRQ

ISRJOR

KAZKWT

KGZ

LVALBN LTUMKD

MDV MDAMNENPL

OMN

PAK

PSE POL

QAT

ROU

RUS

SAU

SRB

SGP

SVKSVN

LKASYR

TJK

TLSTUR

TKM

UKR

UZB

YEM

KHMIDN

LAO

MYS

MNG

MMR

PHL

THA

VNM

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0 0.1 0.2 0.3 0.4

Share of exports to China

similarity between country's exports and China's imports

25

trade policy barriers. Based on this analysis, the impact of further integration with China will have asymmetric effects on developing East Asian countries.

Vietnam, Malaysia, the Philippines, Thailand and Indonesia source a large share of imports from China and have similar export structure and export destinations. For these countries, further integration with China will increase the competitive pressures in final goods markets. But firms involved in value chains with China will benefit from the access to cheaper inputs.

Myanmar and Mongolia source a sizable share of imports from China and have an export structure that differs from China. For these economies, further integration with China will have small effects on domestic competition, while these economies will benefit from further specialization according to their comparative advantage. The risk will be that they will be even more exposed to domestic economic and policy shocks in China.

At the same time, the gradual rebalancing of the Chinese economy, away from investment and industrial production and towards consumption and services, will imply that further integration in East Asia in the next decade may look quite different from the past decade. For instance, as Chinese competitiveness declines due to higher labor costs, countries like Vietnam, Cambodia and Indonesia will gain market shares in third markets. As Chinese demand for services increases, services export opportunities for countries like Malaysia (utilities and finance), the Philippines (business services) and Thailand (tourism and health) will surge. Resource exporters like Myanmar and Mongolia will still supply large shares of their exports to China and other industrializing countries, but probably not at the rising growth rates of past years.

b. Asymmetric market opening in services and goods

One striking aspect of East Asian reform is the contrasting attitude to the liberalization of goods and services trade which has meant foregone benefits. A region that has grown dramatically through manufacturing exports stimulated by foreign direct investment has shown a relative reluctance to be as open to foreign trade and investment in services. This reluctance is a puzzle because growth theories have for long emphasized that trade in intermediate goods and services generally improves the allocation of capital and labor across sectors and countries (Jones 2011).

There is also growing evidence that services reform, of which trade liberalization is one important component, can contribute significantly to inclusive growth. Services shape both overall economic performance and help people to engage productively in the modern economy. An efficient and well‐regulated financial sector leads to the efficient transformation of savings to investment, ensuring that resources are deployed wherever they have the highest returns, and facilitates better risk‐sharing in the economy. At the same time, improved access to finance improves household welfare and income growth, by allowing consumption smoothing and investment in assets that enhance longer‐term productivity. Improved efficiency in telecommunications allows the dissemination and diffusion of knowledge and connects firms and individuals to economic opportunity—witness the spread of the internet and the dynamism that that has lent to economies around the world. Similarly, transport services help goods to move where they are most wanted and people to where they are most productive. Business services

26

such as accounting and legal services are important in reducing transaction costs both for firms and individuals. Education and health services enhance the quality of lives and human capital, allowing people to engage productively in the modern economy.

In this section, we focus first on how services trade has an impact on two key aspects of economic performance: the growth of productivity and the evolution of comparative advantage. Improved access to finance, communications, transport, and other services, either through general reform or reform of trade and FDI policies, enhances firms’ productivity and other aspects of the performance of firms. The development of domestic services sectors and access to foreign services can also shift the pattern of comparative advantage. However, these benefits do not automatically follow from services liberalization, and a successful reform program will also need strengthened regulation and mechanisms to improve access to services, which is briefly discussed in the third part of this section.12

i. Asymmetric trade policy liberalization

Figure 13 depicts the asymmetric trade‐opening in goods and services in East Asia. On the horizontal axis is a measure of tariff protection, while on the vertical axis is a measure of services protection —as measured by the Services Trade Restrictions Index, which takes values from 0 for completely open regimes to 100 for completely closed. Apart from Cambodia and Mongolia, all the countries in the study inhabit the top left quadrant, signifying that their levels of tariff protection are lower than the global median while their levels of services protection are higher than the global median.

Even though many of the larger East Asian countries are now similarly situated, the pace of reform has been strikingly different over the last two decades. Even though their regimes are still not very open, in China, Vietnam and Cambodia, WTO accession induced a move away from state‐owned monopolies to more competitive private provision of telecommunications, financial, transport and a range of other services. In Indonesia, Thailand, Malaysia and the Philippines regimes at the turn of the century were less closed but the approach to reform has been more gradual and not always towards greater openness.

The World Bank Services Trade Restrictions Database reveals interesting policy patterns in East Asia. Although public monopolies are now rare, and few services markets are completely closed, numerous second‐generation restrictions remain on entry, ownership, and operations. Even where there is little explicit discrimination against foreign providers, market access is often unpredictable because the allocation of new licenses remains opaque and highly discretionary in many countries. Regulatory discretion is accentuated by a lack of accountability in a number of countries where regulators are not required to provide reasons for rejecting a license application or where foreign providers do not have the right to appeal regulatory decisions.

12Added urgency is lent to services reform by the deepening interlinkages between manufacturing and services sectors, manifested as the so‐called “servicification” of manufacturing, whereby services are increasingly embodied in manufactured goods. See Hallward‐Driemeier and Nayyar (2018) for a discussion of the trends and the implications of this phenomenon.

27

Figure 13. Protectionism in goods trade versus services trade

Sources: UNCTAD TRAINS (via WITS), World Bank Services Trade Restrictiveness database (Borchert et al. 2012) and authors’ calculations.

Bank sector policies in Thailand, Philippines, Malaysia, and Vietnam restrict greenfield entry and operations. In Thailand, the limit on foreign ownership in a “local bank” was 49 percent, and there was a limit on operations: the number of branches and ATMs allowed per subsidiary was 20. In the Philippines, greenfield entry was not possible since the license limit of 10 had been reached, and for acquisition, the foreign ownership limit was 60 percent. In Malaysia, with the enactment of the Financial Services Act 2013 and the Islamic Financial Services Act 2013 in June 2013, there was a comprehensive modernization and streamlining of Malaysia’s regime on licensing and foreign equity limits in the banking and insurance sector (conventional and Islamic). In both conventional and Islamic finance, application for a license is now based on the prudential and “best interest of Malaysia” criteria. Similarly, the acquisition of a significant foreign equity interest in Malaysian banks and insurance companies could be up to 100 percent, subject to meeting the aforementioned criteria. In the context of the TPP negotiations, Malaysia promised to phase‐in further liberalization in the financial sector. Vietnam allowed wholly foreign‐owned subsidiaries but imposed a limit on the acquisition of banks. To acquire existing banks, the foreign ownership limit was 30 percent for aggregate foreign investment and 20 percent for a single foreign credit institution.

Most developing East Asian countries limited foreign investment in fixed and mobile telecommunications services. The limit on foreign ownership was 49 percent in Indonesia and Malaysia, and 40 percent in the Philippines. But Malaysia is progressively removing foreign

ALBARG

ARM

AUSAUT

BDIBEL

BGD

BGR

BHR

BLR

BOL

BRA

BWA

CAN CHL

CIV CMR

COL

CRI

CZEDEU

DNK

DOM

DZA

ECU

EGY

ESP

FIN

FRA

GBR

GEO

GHA

GRC

GTM

HND

HUN

IND

IRL

IRN

ITA

JOR

JPN

KAZ

KEN

KGZ

KOR

KWT

LBN

LKA

LSO

LTU

MAR

MDG

MEXMLI

MOZMUS

MWI

NAM

NGA

NIC

NLD

NPL

NZL

OMN

PAK

PAN

PER

POL

PRT

PRY

QAT

ROU

RUS RWA

SAU

SEN

SWETTO

TUN

TUR

TZA

UGA

UKRURY

USA

UZB

VEN

YEM

ZAF

ZMB

ZWE

CHN

IDN

KHM

MNG

MYS

PHLTHA

VNM

0

10

20

30

40

50

60

70

80

0 2 4 6 8 10 12 14 16 18 20

Services Trade Restrictions Index (STR

I)

Average applied Most Favored Nation (MFN) tariff (percent)

28

equity limits in the telecom sector; currently the foreign equity limit is 70 percent for network facilities providers and 100 percent for applications service providers. The limit was a more relaxed 70 percent in Vietnam, but foreign majority control required government approval, and in Thailand foreign majority owned or controlled providers could only offer services on a resale basis. In the context of the TPP negotiations, Vietnam has promised to relax or eliminate foreign equity restrictions over the same time frame. A number of countries allowed full foreign ownership in private companies, but restricted foreign ownership in state‐owned telecom operators. Thus, the Philippines did not allow acquisition of a state‐owned entity, whereas Cambodia and Lao PDR allowed only a minority foreign share in state entities. In Vietnam, the state held a dominant share in telecommunications service providers with network infrastructure. However, in the context of the TPP, Vietnam has pre‐committed to further liberalization.

Transportation services were relatively restricted in developing East Asian countries as they were in other parts of the world. Thailand, Vietnam, Philippines, and Malaysia had restrictions on foreign ships carrying government cargo but no limitations on private cargo. On commercial presence (mode 3), for the types of transport covered by the survey (maritime, air, road, and rail), the majority of developing East Asian countries mentioned that the control must be held by local companies. In air transport, all ASEAN member states, including the developing East Asian countries (except Mongolia), signed the ASEAN Multilateral Agreement on Full Liberalization of Air Freight and Air Passenger services. It was difficult to assess how much more openness the regional air services agreements offered beyond the existing Bilateral Air Services Agreements (BASAs).

ii. Services openness and productivity

Research on several developing countries offers examples of the significant impact of openness to services on manufacturing productivity. Reforms in these countries visibly transformed services sectors, with greater openness and improved regulation leading to dramatic growth in domestic and foreign investment. Local manufacturing firms were no longer at the mercy of inefficient public monopolies but could now source services from a wide range of domestic and foreign providers operating in an increasingly competitive environment. As a result, they had access to better, newer, more reliable, and more diverse business services. These improvements enhanced firms’ ability to invest in new business opportunities and better production technology, to exploit economies of scale by concentrating production in fewer locations, to efficiently manage inventories, and to coordinate decisions with suppliers and customers.13

13 Several studies show that access to low‐cost and high‐quality (domestic or foreign) producer services can promote productivity and economic growth (Hoekman and Mattoo 2008). Arnold et al. (2016) collected detailed information on the pace of reform across Indian services sectors, with a focus on entry and operational restrictions. The results suggest that procompetitive reforms in banking, transport, insurance, and telecommunications boosted the productivity of both foreign and locally owned manufacturing firms. Using firm‐level data for the Czech Republic for 1998–2003, Arnold, Javorcik, and Mattoo (2011) find a positive effect on the productivity of domestic firms in downstream manufacturing as a result of services sector reforms leading to greater FDI. Using the annual manufacturing survey of Chilean firms, Fernandes and Paunov (2012) find a positive

29