Embed Size (px)

Citation preview

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 1/24

Export DocumentationAn Overview

Compiled by Ca V.V.S. Rao, Bangalore, [email protected]

Compiled by Ca V.V.S. Rao, Bangalore, [email protected]

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 2/24

I hear and I forget

I see and I remember

I do and I understand

Confucius(551 BC ² 479 BC)

The great Chinese Thinker & Philosopher

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 3/24

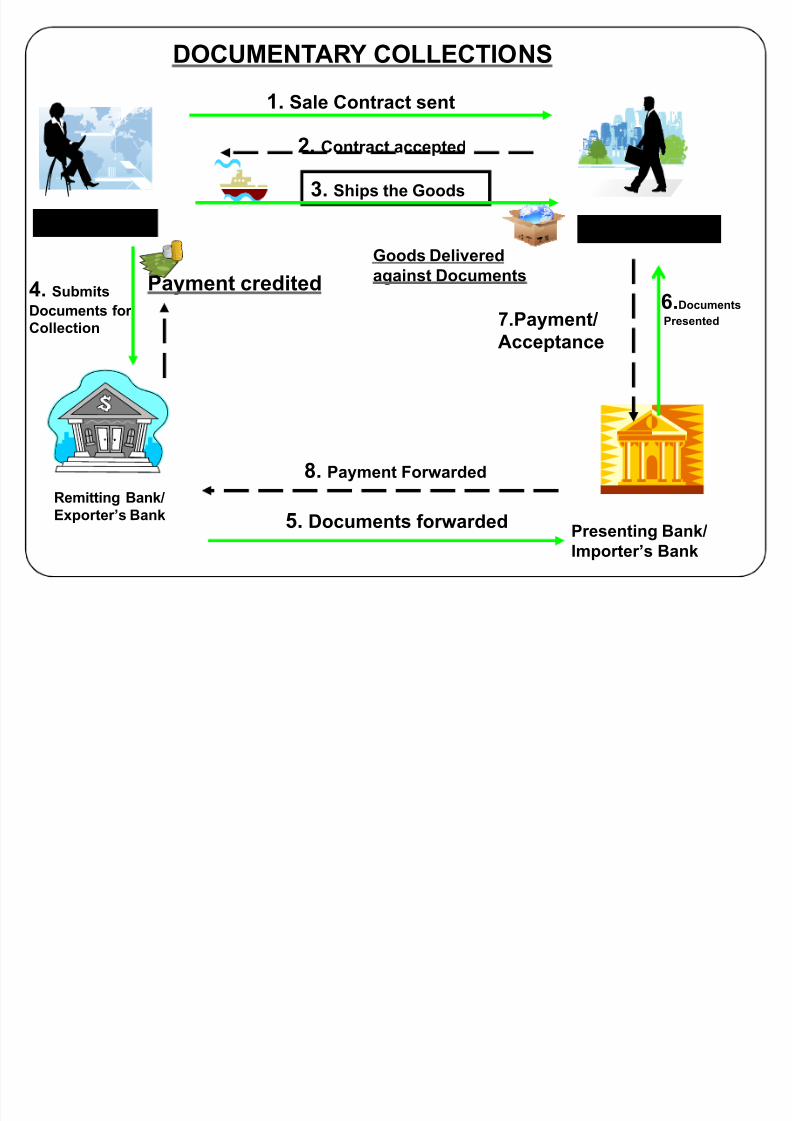

Exporter Importer

1. Sale Contract sent

4. Submits

Documents for

Collection

Remitting Bank/

Exporter¶s Bank 5. Documents forwardedPresenting Bank/

Importer¶s Bank

6.Documents

Presented

DOCUMENTARY COLLECTIONS

3. Ships the Goods

2. Contract accepted

Goods Delivered

against Documents

7.Payment/

Acceptance

8. Payment Forwarded

Payment credited

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 4/24

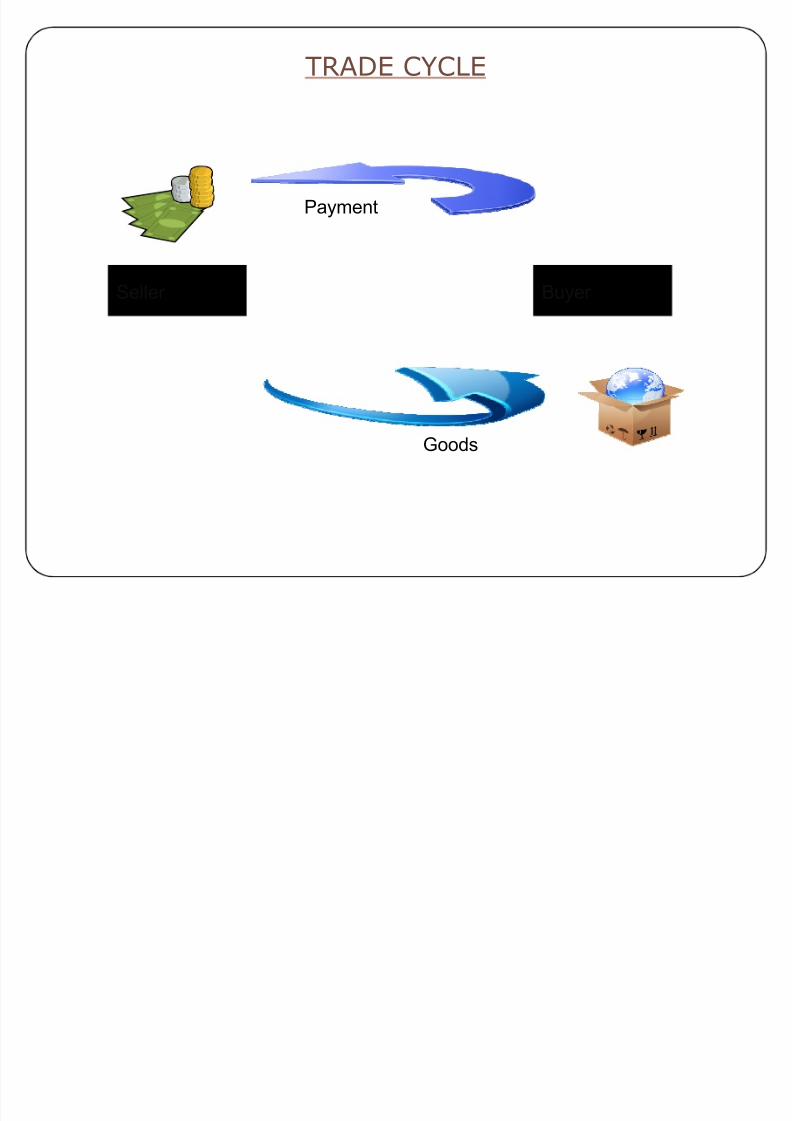

TRADE CYCLE

Seller Buyer

Goods

Payment

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 5/24

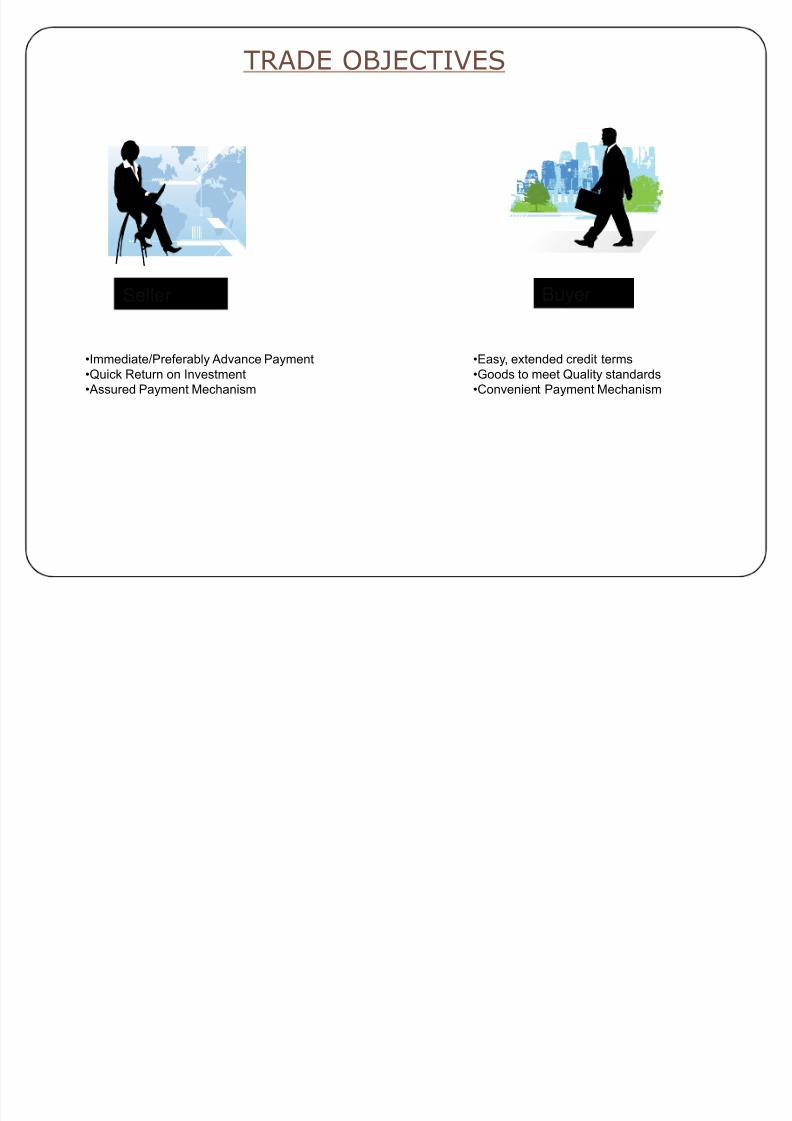

TRADE OBJECTIVES

Seller Buyer

Immediate/Preferably Advance PaymentQuick Return on InvestmentAssured Payment Mechanism

Easy, extended credit termsGoods to meet Quality standardsConvenient Payment Mechanism

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 6/24

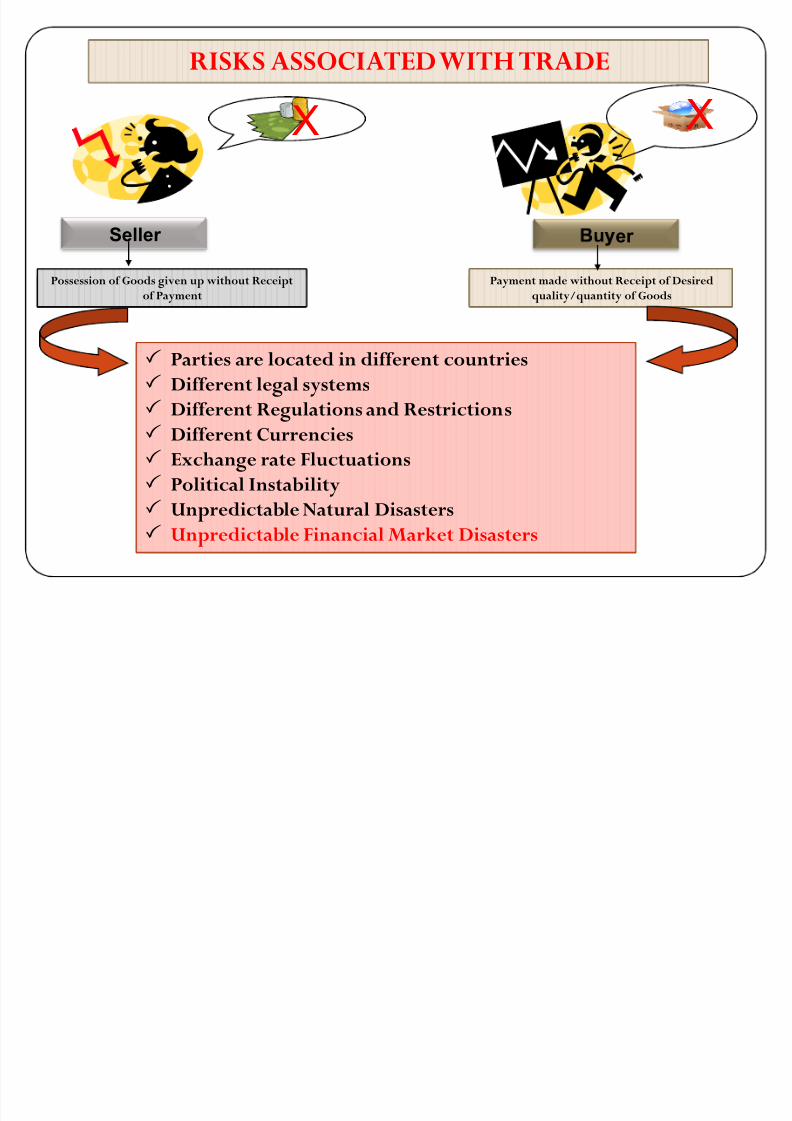

RISKS ASSOCIATED WITH TRADE

RISKS ASSOCIATED WITH TRADE

Seller er

Payment made without Receipt of Desiredquality/quantity of Goods

Payment made without Receipt of Desiredquality/quantity of Goods

XX

Possession of Goods given up without Receiptof Payment

Possession of Goods given up without Receiptof Payment

Parties are located in different countries Different legal systems

Different Regulations and Restrictions Different Currencies Exchange rate Fluctuations Political Instability Unpredictable Natural Disasters Unpredictable Financial Market Disasters

Parties are located in different countries Different legal systems

Different Regulations and Restrictions Different Currencies Exchange rate Fluctuations Political Instability Unpredictable Natural Disasters Unpredictable Financial Market Disasters

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 7/24

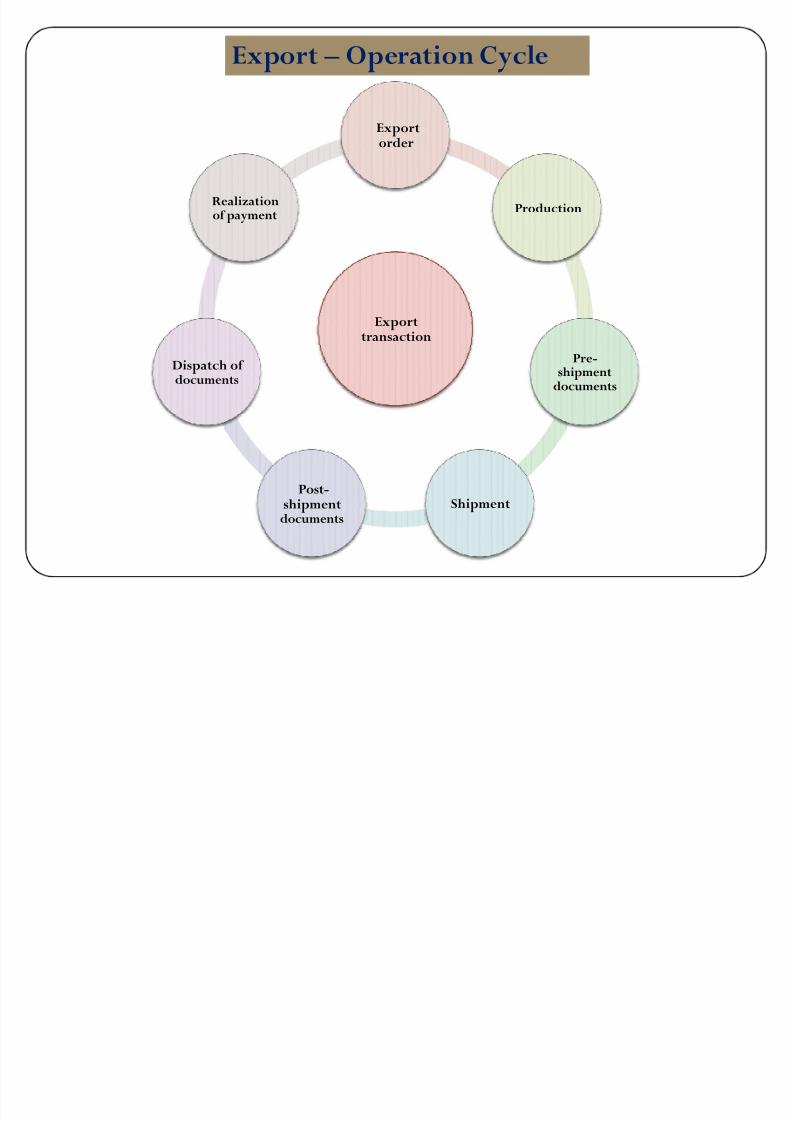

Exporttransaction

Exportorder

Production

Pre-shipment

documents

ShipmentPost-

shipmentdocuments

Dispatch of documents

Realizationof payment

Export ² Operation Cycle

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 8/24

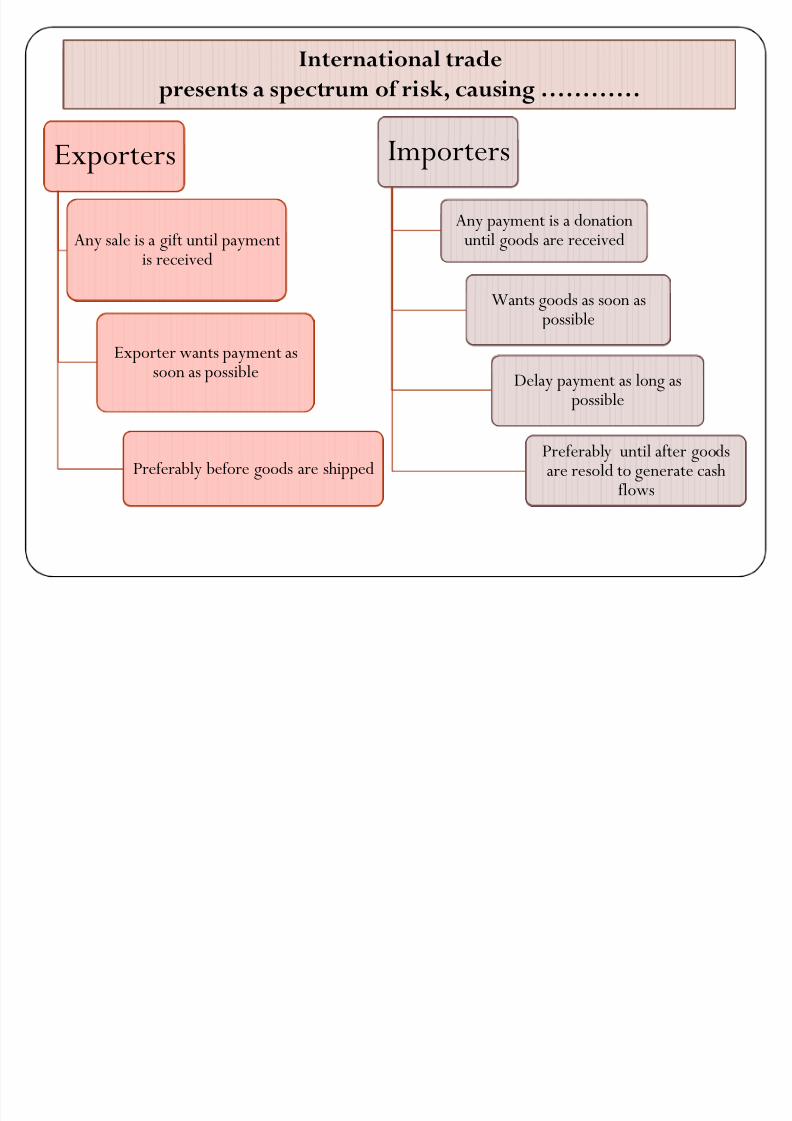

International tradepresents a spectrum of risk, causing ««««

International tradepresents a spectrum of risk, causing ««««

ExportersExporters

Any sale is a gift until paymentis received

Any sale is a gift until paymentis received

Exporter wants payment assoon as possible

Exporter wants payment assoon as possible

Preferably before goods are shippedPreferably before goods are shipped

ImportersImporters

Any payment is a donationuntil goods are received

Any payment is a donationuntil goods are received

Wants goods as soon aspossible

Wants goods as soon aspossible

Delay payment as long aspossible

Delay payment as long aspossible

Preferably until after goodsare resold to generate cash

flows

Preferably until after goodsare resold to generate cash

flows

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 9/24

Various Methods of PaymentVarious Methods of Payment

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 10/24

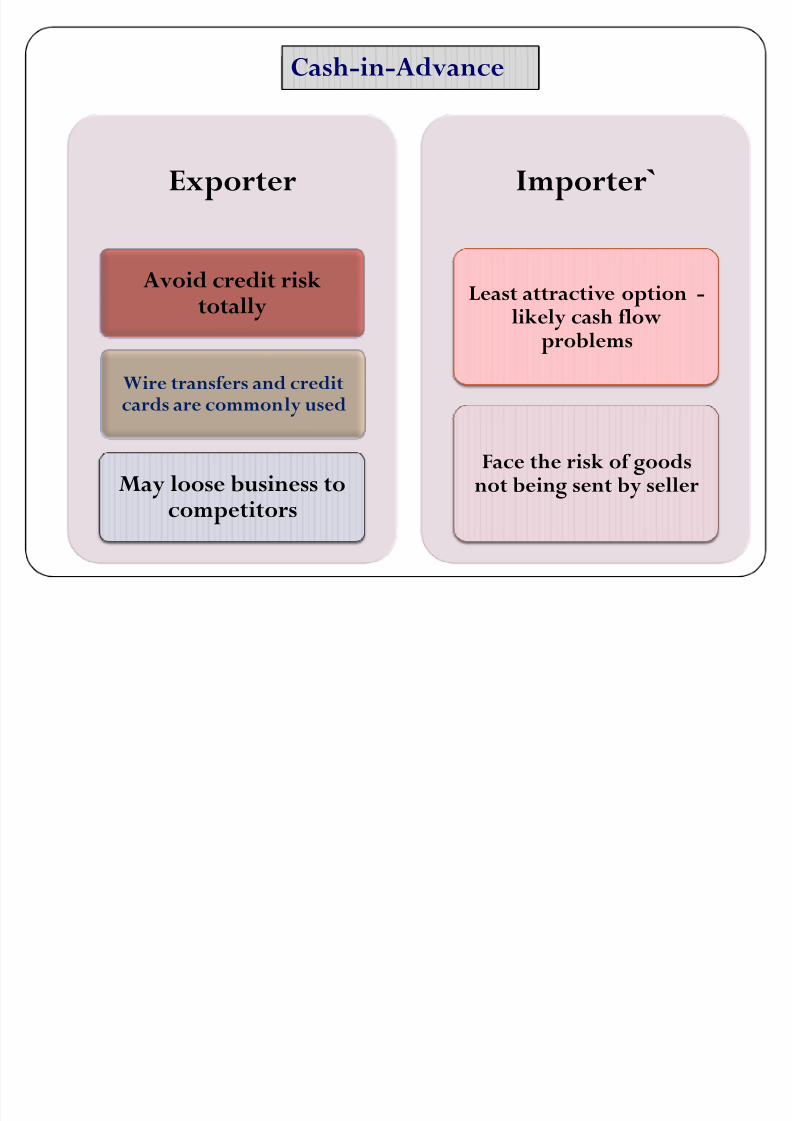

Cash-in-AdvanceCash-in-Advance

Exporter

Avoid credit risktotally

Wire transfers and credit

cards are commonly used

May loose business tocompetitors

Importer`

Least attractive option -likely cash flow

problems

Face the risk of goodsnot being sent by seller

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 11/24

11

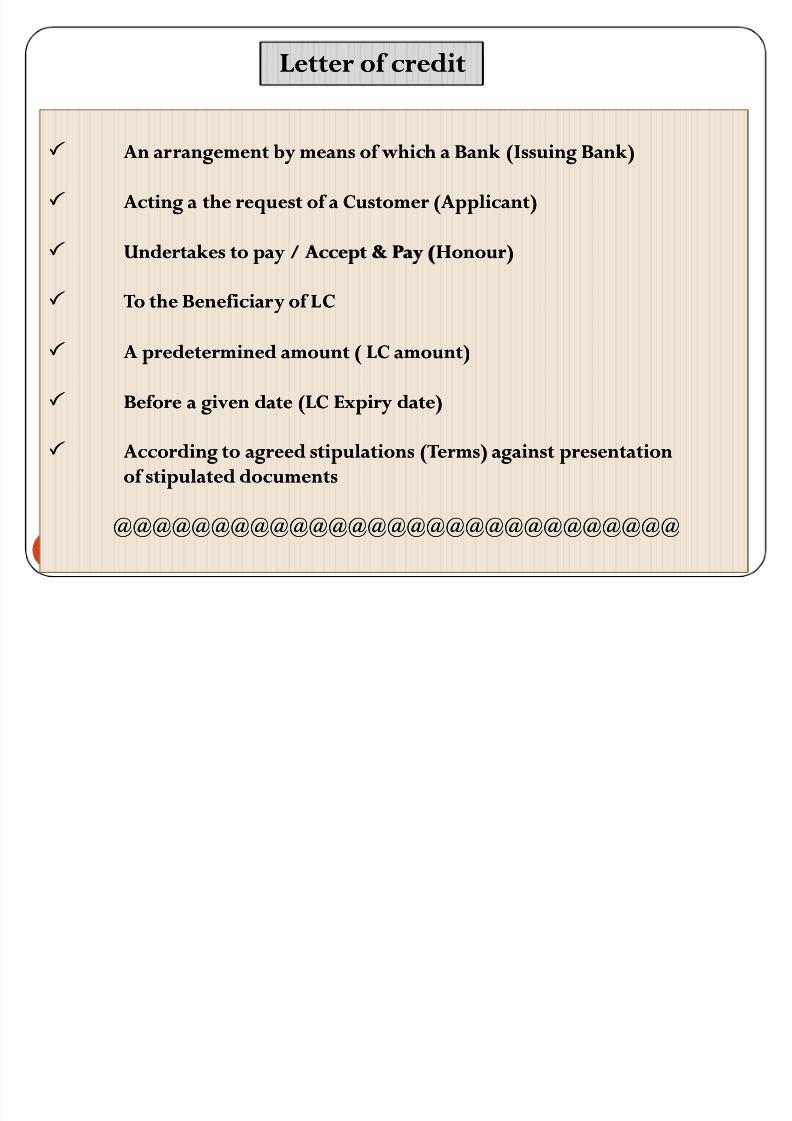

An arrangement by means of which a Bank (Issuing Bank)An arrangement by means of which a Bank (Issuing Bank)

Acting a the request of a Customer (Applicant)Acting a the request of a Customer (Applicant)

Undertakes to pay / Accept & Pay (Undertakes to pay / Accept & Pay (HonourHonour))

To the Beneficiary of LCTo the Beneficiary of LC

A predetermined amount ( LC amount)A predetermined amount ( LC amount)

Before a given date (LC Expiry date)Before a given date (LC Expiry date)

According to agreed stipulations (Terms) against presentationAccording to agreed stipulations (Terms) against presentationof stipulated documentsof stipulated documents

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

An arrangement by means of which a Bank (Issuing Bank)An arrangement by means of which a Bank (Issuing Bank)

Acting a the request of a Customer (Applicant)Acting a the request of a Customer (Applicant)

Undertakes to pay / Accept & Pay (Undertakes to pay / Accept & Pay (HonourHonour))

To the Beneficiary of LCTo the Beneficiary of LC

A predetermined amount ( LC amount)A predetermined amount ( LC amount)

Before a given date (LC Expiry date)Before a given date (LC Expiry date)

According to agreed stipulations (Terms) against presentationAccording to agreed stipulations (Terms) against presentationof stipulated documentsof stipulated documents

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

Letter of creditLetter of creditLetter of creditLetter of credit

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 12/24

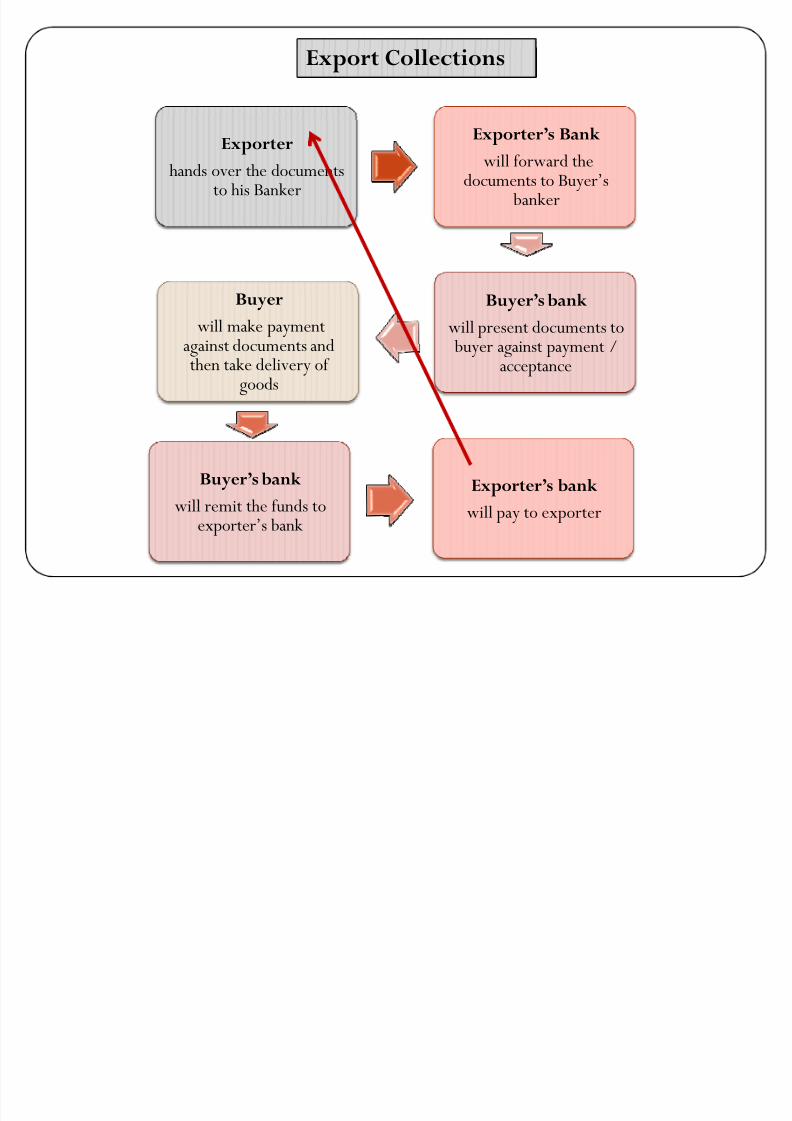

Exporterhands over the documents

to his Banker

Exporter·s Bankwill forward the

documents to Buyer·s banker

Buyer·s bank

will present documents to buyer against payment /

acceptance

Buyer

will make paymentagainst documents andthen take delivery of

goods

Buyer·s bank

will remit the funds toexporter·s bank

Exporter·s bank

will pay to exporter

Export CollectionsExport Collections

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 13/24

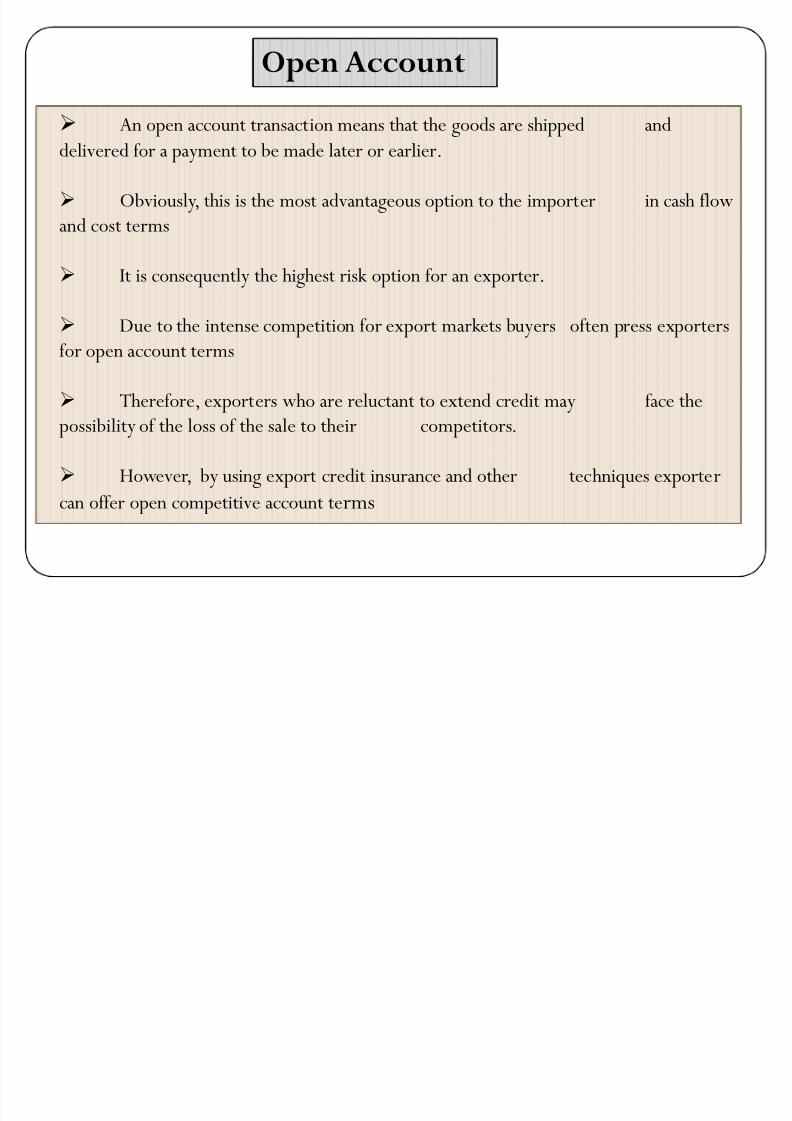

An open account transaction means that the goods are shipped and

delivered for a payment to be made later or earlier.

Obviously, this is the most advantageous option to the importer in cash flow

and cost terms

It is consequently the highest risk option for an exporter.

Due to the intense competition for export markets buyers often press exporters

for open account terms

Therefore, exporters who are reluctant to extend credit may face the

possibility of the loss of the sale to their competitors.

However, by using export credit insurance and other techniques exporter

can offer open competitive account terms

An open account transaction means that the goods are shipped and

delivered for a payment to be made later or earlier.

Obviously, this is the most advantageous option to the importer in cash flow

and cost terms

It is consequently the highest risk option for an exporter.

Due to the intense competition for export markets buyers often press exporters

for open account terms

Therefore, exporters who are reluctant to extend credit may face the

possibility of the loss of the sale to their competitors.

However, by using export credit insurance and other techniques exporter

can offer open competitive account terms

Open AccountOpen Account

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 14/24

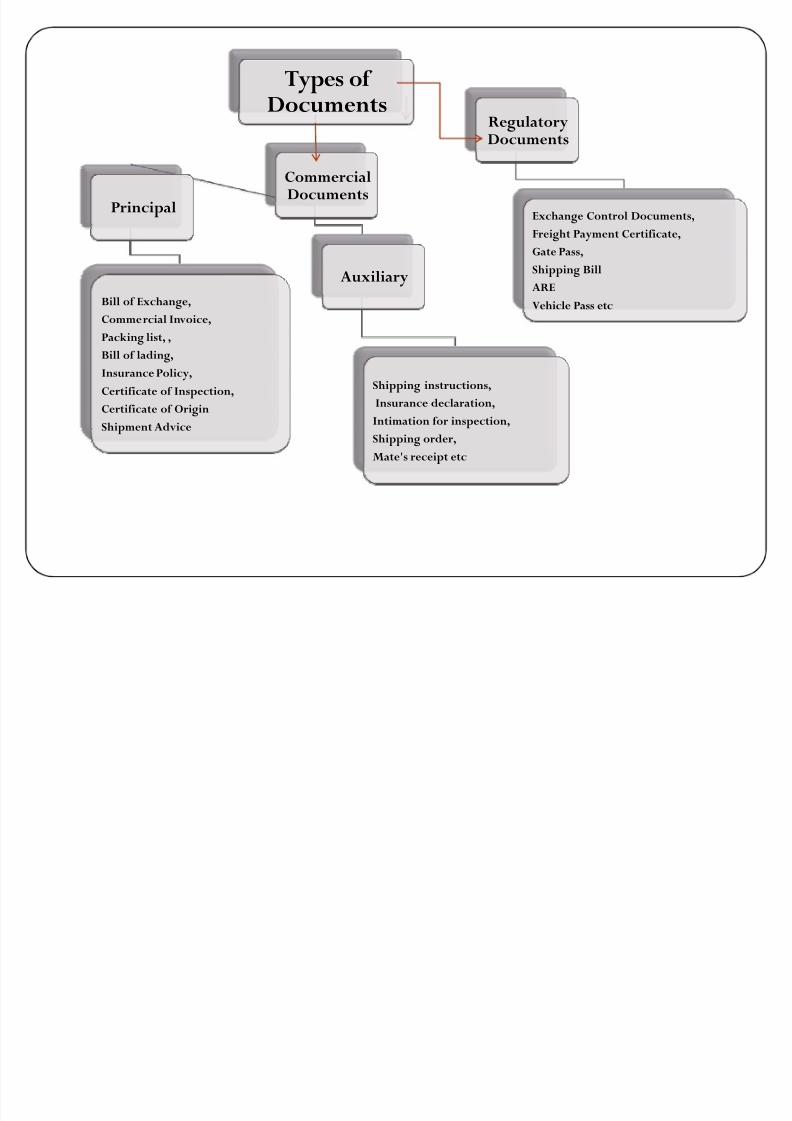

Types of Documents

CommercialDocuments

Principal

Bill of Exchange,

Commercial Invoice,

Packing list, ,

Bill of lading,

Insurance Policy,

Certificate of Inspection,

Certificate of OriginShipment Advice

Auxiliary

Shipping instructions,

Insurance declaration,

Intimation for inspection,

Shipping order,

Mate's receipt etc

Regulatory

Documents

Exchange Control Documents,

Freight Payment Certificate,

Gate Pass,

Shipping Bill

ARE

Vehicle Pass etc

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 15/24

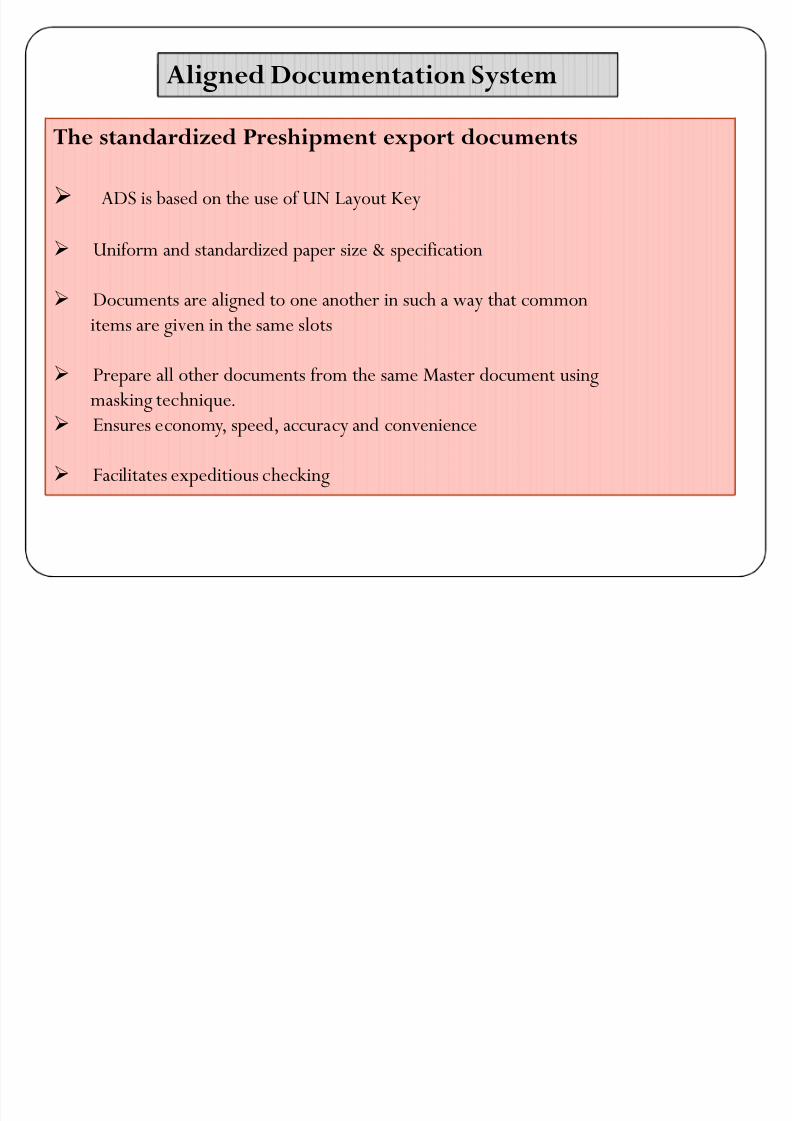

Aligned Documentation SystemAligned Documentation System

The standardized Preshipment export documents

ADS is based on the use of UN Layout Key

Uniform and standardized paper size & specification

Documents are aligned to one another in such a way that common

items are given in the same slots

Prepare all other documents from the same Master document using

masking technique.

Ensures economy, speed, accuracy and convenience

Facilitates expeditious checking

The standardized Preshipment export documents

ADS is based on the use of UN Layout Key

Uniform and standardized paper size & specification

Documents are aligned to one another in such a way that common

items are given in the same slots

Prepare all other documents from the same Master document using

masking technique.

Ensures economy, speed, accuracy and convenience

Facilitates expeditious checking

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 16/24

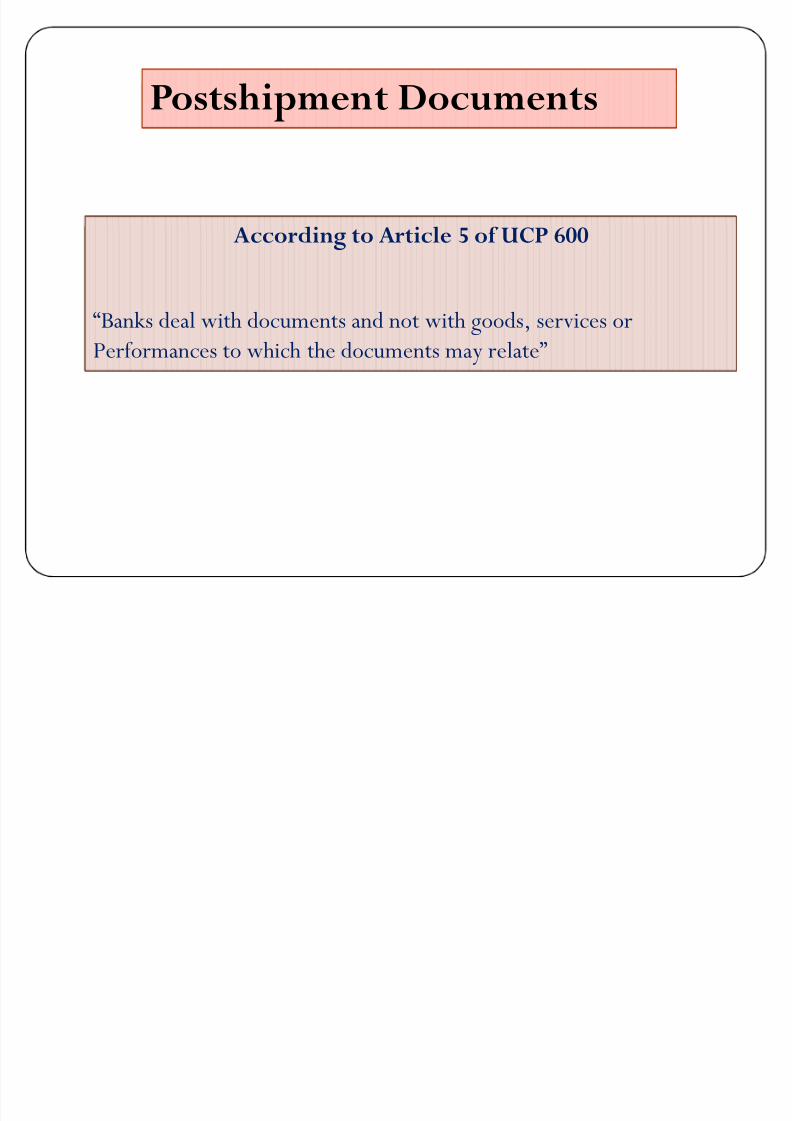

According to Article 5 of UCP 600

´Banks deal with documents and not with goods, services or

Performances to which the documents may relateµ

According to Article 5 of UCP 600

´Banks deal with documents and not with goods, services or

Performances to which the documents may relateµ

Postshipment DocumentsPostshipment Documents

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 17/24

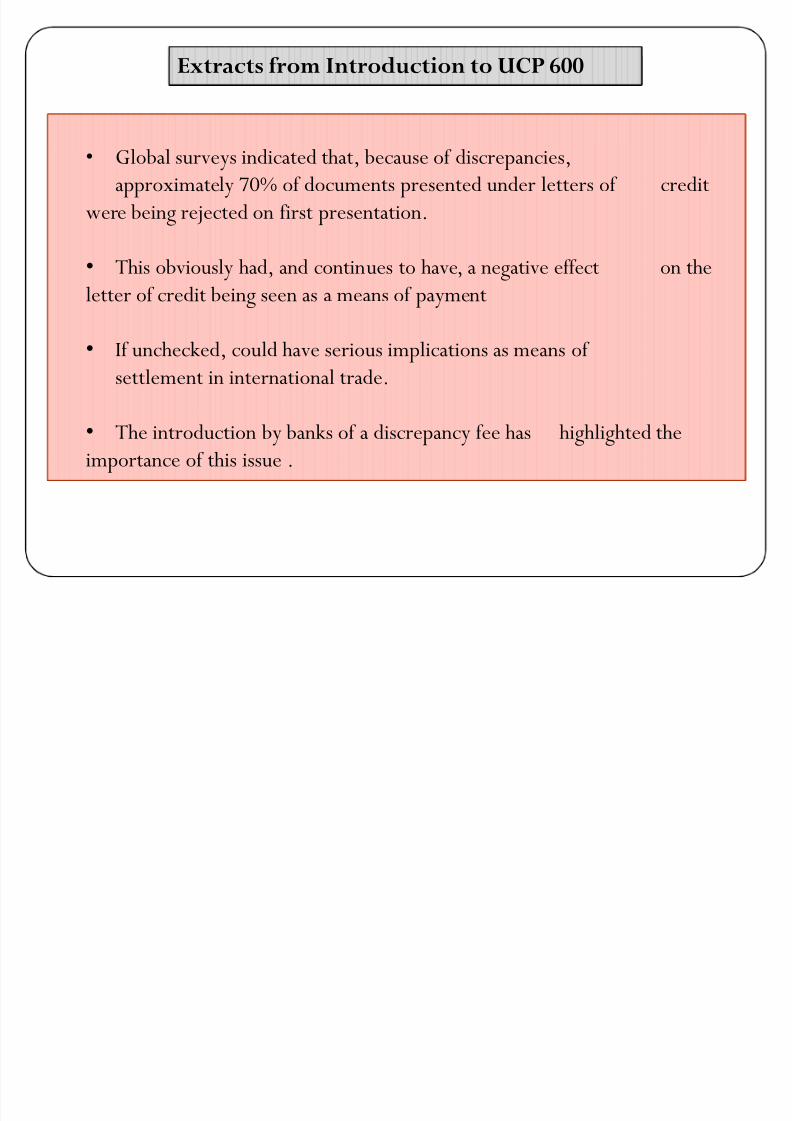

Global surveys indicated that, because of discrepancies,

approximately 70% of documents presented under letters of credit

were being rejected on first presentation.

This obviously had, and continues to have, a negative effect on theletter of credit being seen as a means of payment

If unchecked, could have serious implications as means of

settlement in international trade.

The introduction by banks of a discrepancy fee has highlighted the

importance of this issue .

Global surveys indicated that, because of discrepancies,

approximately 70% of documents presented under letters of credit

were being rejected on first presentation.

This obviously had, and continues to have, a negative effect on theletter of credit being seen as a means of payment

If unchecked, could have serious implications as means of

settlement in international trade.

The introduction by banks of a discrepancy fee has highlighted the

importance of this issue .

Extracts from Introduction to UCP 600Extracts from Introduction to UCP 600

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 18/24

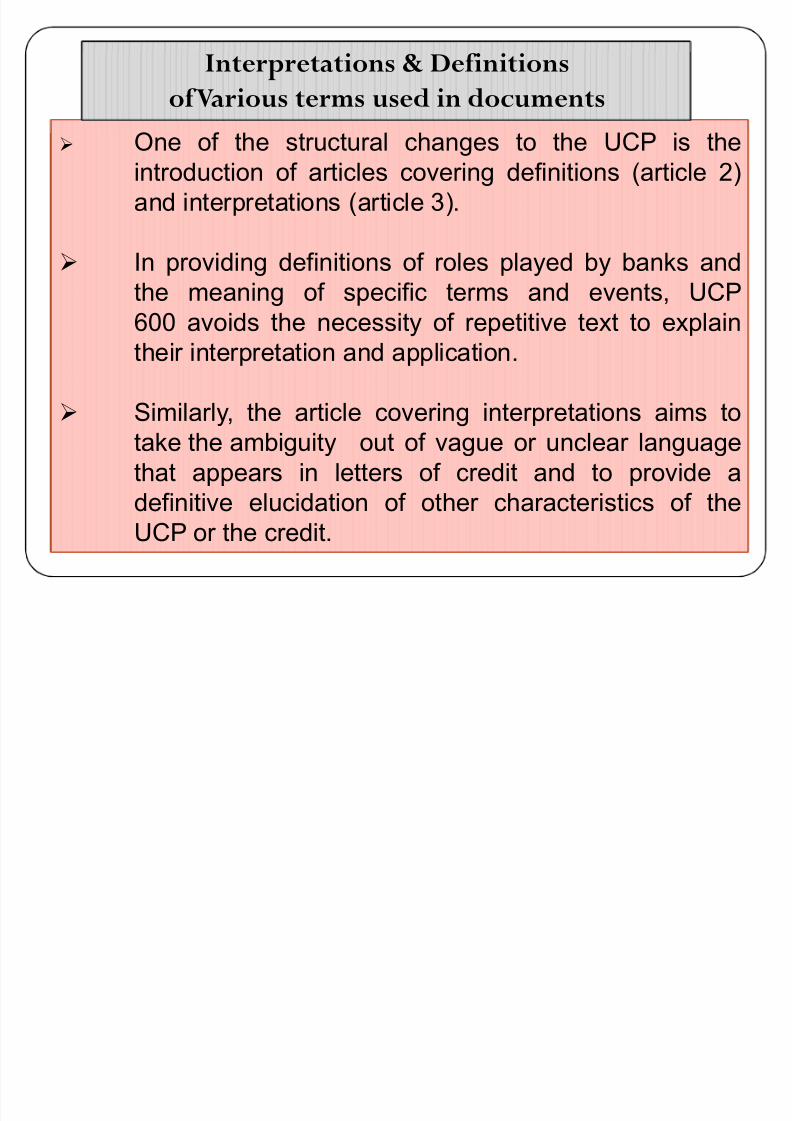

ne of the structural changes to the UCP is theintroduction of articles covering definitions (article 2)and interpretations (article 3).

In providing definitions of roles played by banks andthe meaning of specific terms and events, UCP600 avoids the necessity of repetitive text to explaintheir interpretation and application.

Similarly, the article covering interpretations aims totake the ambiguity out of vague or unclear languagethat appears in letters of credit and to provide adefinitive elucidation of other characteristics of theUCP or the credit.

One of the structural changes to the UCP is theintroduction of articles covering definitions (article 2)and interpretations (article 3).

In providing definitions of roles played by banks andthe meaning of specific terms and events, UCP600 avoids the necessity of repetitive text to explaintheir interpretation and application.

Similarly, the article covering interpretations aims totake the ambiguity out of vague or unclear languagethat appears in letters of credit and to provide adefinitive elucidation of other characteristics of theUCP or the credit.

Interpretations & Definitionsof Various terms used in documents

Interpretations & Definitionsof Various terms used in documents

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 19/24

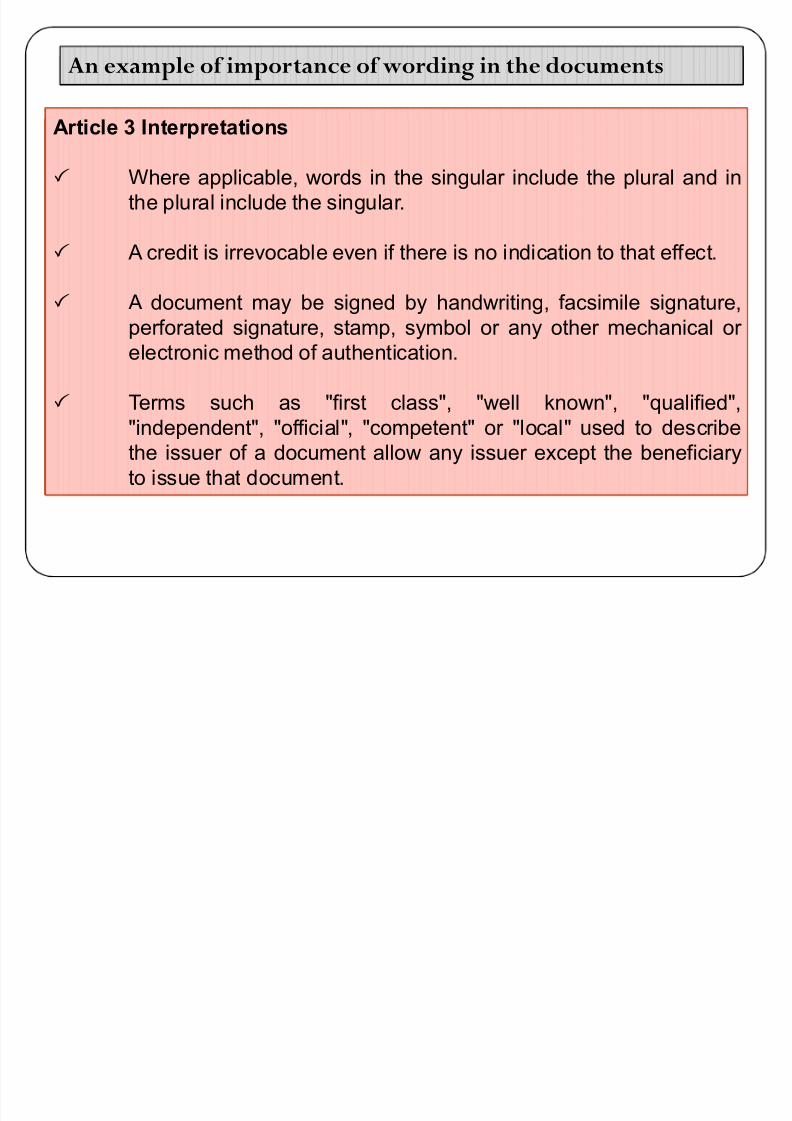

Article 3 Interpretations

Where applicable, words in the singular include the plural and inthe plural include the singular.

A credit is irrevocable even if there is no indication to that effect.

A document may be signed by handwriting, facsimile signature,perforated signature, stamp, symbol or any other mechanical or electronic method of authentication.

Terms such as "first class", "well known", "qualified","independent", "official", "competent" or "local" used to describethe issuer of a document allow any issuer except the beneficiaryto issue that document.

Article 3 Interpretations

Where applicable, words in the singular include the plural and inthe plural include the singular.

A credit is irrevocable even if there is no indication to that effect.

A document may be signed by handwriting, facsimile signature,perforated signature, stamp, symbol or any other mechanical or electronic method of authentication.

Terms such as "first class", "well known", "qualified","independent", "official", "competent" or "local" used to describethe issuer of a document allow any issuer except the beneficiaryto issue that document.

An example of importance of wording in the documentsAn example of importance of wording in the documents

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 20/24

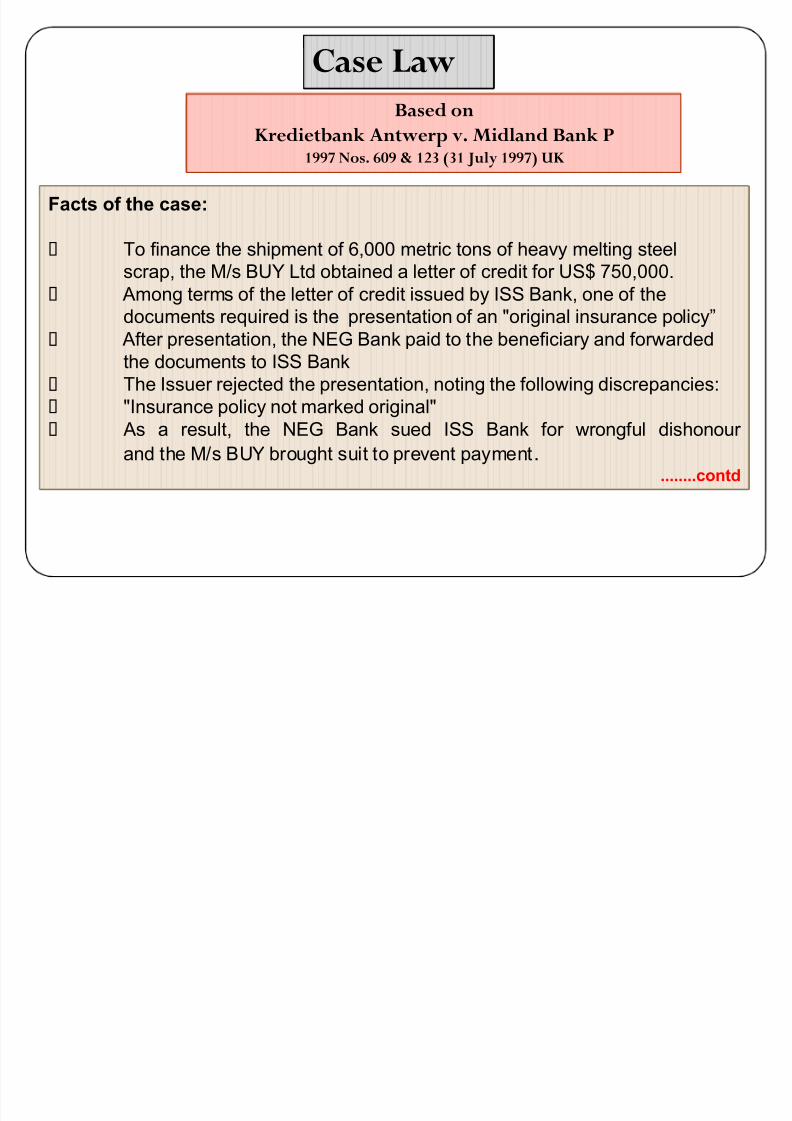

Facts of the case:

To finance the shipment of 6,000 metric tons of heavy melting steel

scrap, the M/s BUY Ltd obtained a letter of credit for US$ 750,000. Among terms of the letter of credit issued by ISS Bank, one of thedocuments required is the presentation of an "original insurance policy´

After presentation, the NEG Bank paid to the beneficiary and forwardedthe documents to ISS Bank

The Issuer rejected the presentation, noting the following discrepancies: "Insurance policy not marked original" As a result, the NEG Bank sued ISS Bank for wrongful dishonour

and the M/s BUY brought suit to prevent payment.........contd

Facts of the case:

To finance the shipment of 6,000 metric tons of heavy melting steel

scrap, the M/s BUY Ltd obtained a letter of credit for US$ 750,000. Among terms of the letter of credit issued by ISS Bank, one of thedocuments required is the presentation of an "original insurance policy´

After presentation, the NEG Bank paid to the beneficiary and forwardedthe documents to ISS Bank

The Issuer rejected the presentation, noting the following discrepancies: "Insurance policy not marked original" As a result, the NEG Bank sued ISS Bank for wrongful dishonour

and the M/s BUY brought suit to prevent payment.........contd

Case LawCase LawBased on

Kredietbank Antwerp v. Midland Bank P1997 Nos. 609 & 123 (31 July 1997) UK

Based on

Kredietbank Antwerp v. Midland Bank P1997 Nos. 609 & 123 (31 July 1997) UK

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 21/24

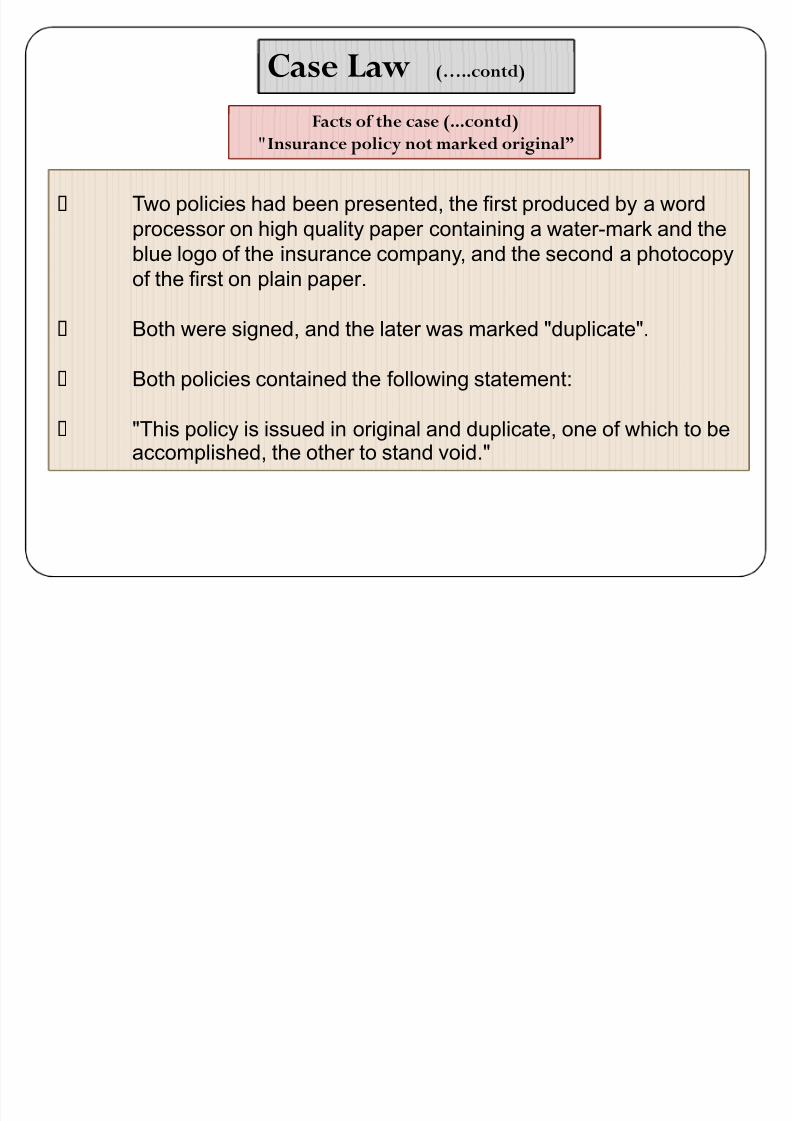

Two policies had been presented, the first produced by a wordprocessor on high quality paper containing a water-mark and theblue logo of the insurance company, and the second a photocopy

of the first on plain paper.

Both were signed, and the later was marked "duplicate".

Both policies contained the following statement:

"This policy is issued in original and duplicate, one of which to beaccomplished, the other to stand void."

Two policies had been presented, the first produced by a wordprocessor on high quality paper containing a water-mark and theblue logo of the insurance company, and the second a photocopy

of the first on plain paper.

Both were signed, and the later was marked "duplicate".

Both policies contained the following statement:

"This policy is issued in original and duplicate, one of which to beaccomplished, the other to stand void."

Facts of the case (...contd)

"Insurance policy not marked originalµ

Facts of the case (...contd)

"Insurance policy not marked originalµ

Case Law («..contd)Case Law («..contd)

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 22/24

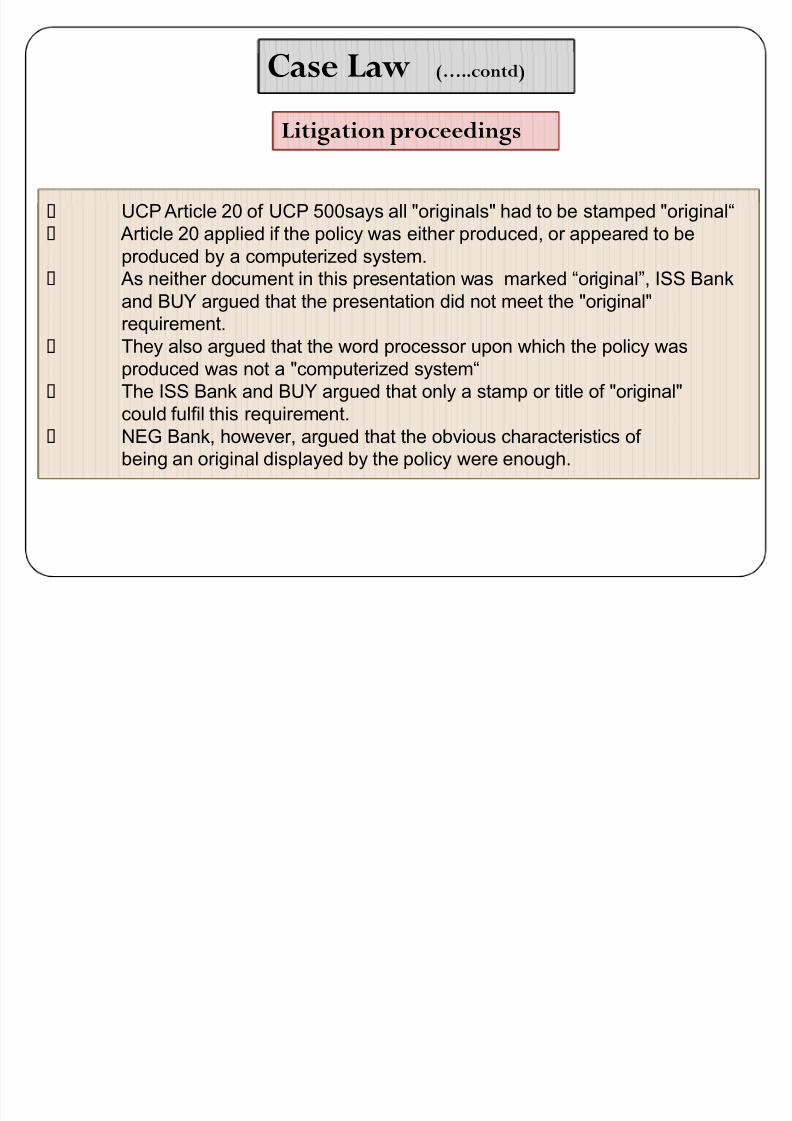

UCP Article 20 of UCP 500says all "originals" had to be stamped "original³ Article 20 applied if the policy was either produced, or appeared to be

produced by a computerized system.

As neither document in this presentation was marked ³original´, ISS Bankand BUY argued that the presentation did not meet the "original"requirement.

They also argued that the word processor upon which the policy wasproduced was not a "computerized system³

The ISS Bank and BUY argued that only a stamp or title of "original"

could fulfil this requirement. NEG Bank, however, argued that the obvious characteristics of

being an original displayed by the policy were enough.

UCP Article 20 of UCP 500says all "originals" had to be stamped "original³ Article 20 applied if the policy was either produced, or appeared to be

produced by a computerized system.

As neither document in this presentation was marked ³original´, ISS Bankand BUY argued that the presentation did not meet the "original"requirement.

They also argued that the word processor upon which the policy wasproduced was not a "computerized system³

The ISS Bank and BUY argued that only a stamp or title of "original"

could fulfil this requirement. NEG Bank, however, argued that the obvious characteristics of

being an original displayed by the policy were enough.

Litigation proceedingsLitigation proceedings

Case Law («..contd)Case Law («..contd)

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 23/24

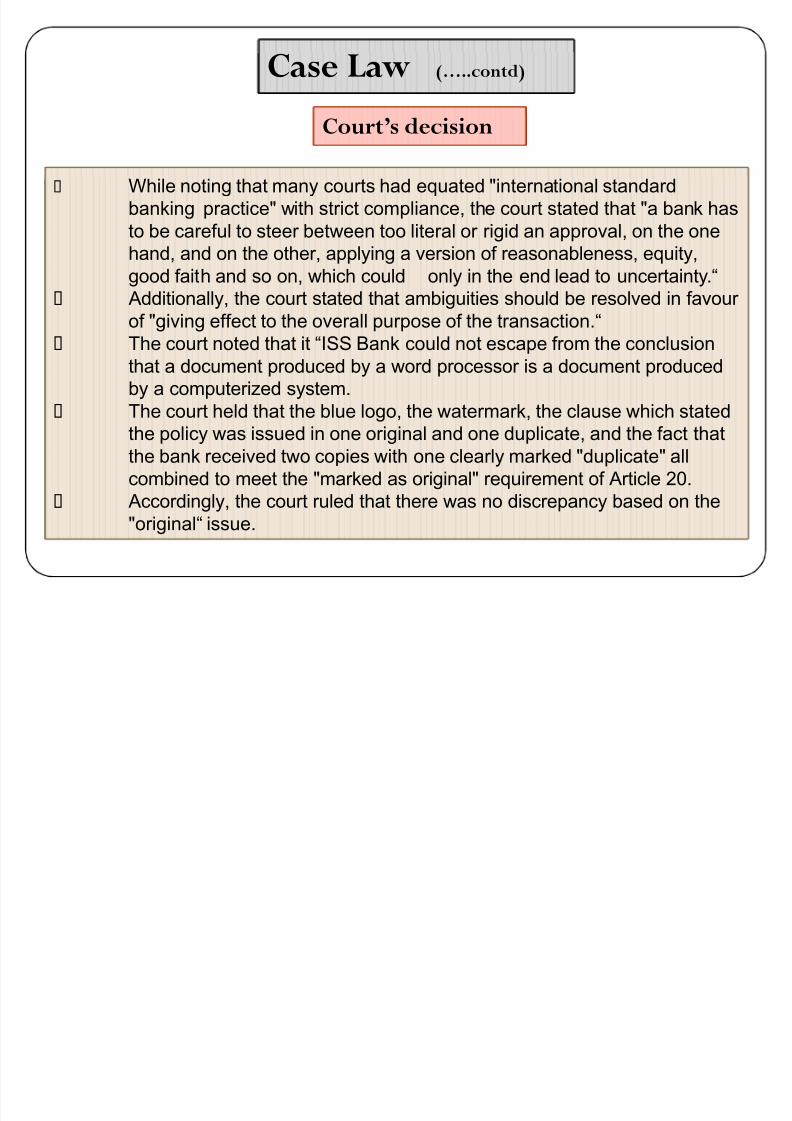

While noting that many courts had equated "international standardbanking practice" with strict compliance, the court stated that "a bank hasto be careful to steer between too literal or rigid an approval, on the onehand, and on the other, applying a version of reasonableness, equity,

good faith and so on, which could only in the end lead to uncertainty.³ Additionally, the court stated that ambiguities should be resolved in favour

of "giving effect to the overall purpose of the transaction.³ The court noted that it ³ISS Bank could not escape from the conclusion

that a document produced by a word processor is a document producedby a computerized system.

The court held that the blue logo, the watermark, the clause which statedthe policy was issued in one original and one duplicate, and the fact thatthe bank received two copies with one clearly marked "duplicate" allcombined to meet the "marked as original" requirement of Article 20.

Accordingly, the court ruled that there was no discrepancy based on the"original³ issue.

While noting that many courts had equated "international standardbanking practice" with strict compliance, the court stated that "a bank hasto be careful to steer between too literal or rigid an approval, on the onehand, and on the other, applying a version of reasonableness, equity,

good faith and so on, which could only in the end lead to uncertainty.³ Additionally, the court stated that ambiguities should be resolved in favour

of "giving effect to the overall purpose of the transaction.³ The court noted that it ³ISS Bank could not escape from the conclusion

that a document produced by a word processor is a document producedby a computerized system.

The court held that the blue logo, the watermark, the clause which statedthe policy was issued in one original and one duplicate, and the fact thatthe bank received two copies with one clearly marked "duplicate" allcombined to meet the "marked as original" requirement of Article 20.

Accordingly, the court ruled that there was no discrepancy based on the"original³ issue.

Case Law («..contd)Case Law («..contd)

Court·s decisionCourt·s decision

8/8/2019 Trade Finance Documentation Framework

http://slidepdf.com/reader/full/trade-finance-documentation-framework 24/24