Embed Size (px)

Citation preview

Trade and Climate Change in Emerging Economies: Trade and Climate Change in Emerging Economies: The Competitiveness, Technology, and Intellectual Property Rights DimensionThe Competitiveness, Technology, and Intellectual Property Rights DimensionInformal Dialogue organised by ICTSD in collaboration with RIS Informal Dialogue organised by ICTSD in collaboration with RIS

Trade Flows, Trade-Barriers and Market Drivers in Trade Flows, Trade-Barriers and Market Drivers in Climate-Friendly Technologies and Associated Climate-Friendly Technologies and Associated Goods: Where do Emerging Economies Stand?Goods: Where do Emerging Economies Stand?

RenRenéé Vossenaar Vossenaar

2ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

BACKGROUNDBACKGROUND

BackgroundBackground• The deployment of renewable energy (RE) technologies and the The deployment of renewable energy (RE) technologies and the

promotion of energy efficiency (EE) are crucial for climate promotion of energy efficiency (EE) are crucial for climate mitigation and provide opportunities for sustainable development mitigation and provide opportunities for sustainable development and trade gains. and trade gains.

• Trade can contribute to the diffusion of climate-friendly Trade can contribute to the diffusion of climate-friendly technologies:technologies:− Trade liberalisation (reducing costs of technologies/components). Trade liberalisation (reducing costs of technologies/components). − Market transformation. Market transformation.

This presentationThis presentation• Linking technology deployment with international tradeLinking technology deployment with international trade

− ICTSD studiesICTSD studies− Trade flowsTrade flows− Trade barriersTrade barriers− Market driversMarket drivers

• Some lessons learned for EGS negotiationsSome lessons learned for EGS negotiations

3ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

ICTSD STUDIESICTSD STUDIES

Issues covered in ICTSD project:Issues covered in ICTSD project:• Mapping of climate friendly Mapping of climate friendly

technologies technologies − Renewable energy (RE) Renewable energy (RE) − Energy efficiency (EE) Energy efficiency (EE)

• Identification of (internationally-traded) Identification of (internationally-traded) products and components associated products and components associated with these technologies, including HS with these technologies, including HS codescodes

• Drivers of technology deployment, tradeDrivers of technology deployment, trade• Trade, tariff and NTB analysisTrade, tariff and NTB analysis

− Market access conditionsMarket access conditions− Market opportunities that arise from Market opportunities that arise from

the deployment of such the deployment of such technologies, especially for technologies, especially for producers in emerging countriesproducers in emerging countries

• Policy conclusionsPolicy conclusions

Three sectors:Three sectors:• Renewable energy Renewable energy

supplysupply• Residential and Residential and

commercial buildingscommercial buildings• Transport Transport

Trade analysis can be Trade analysis can be linked to only part of linked to only part of the technology options the technology options identified in the identified in the mapping studiesmapping studies

4ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

CONCLUSIONSCONCLUSIONS

• The deployment of RE technologies and investment in EE are The deployment of RE technologies and investment in EE are largely driven by policy targets, regulations and incentives.largely driven by policy targets, regulations and incentives.

• Tariff liberalisation alone likely to have relatively little impact.Tariff liberalisation alone likely to have relatively little impact.• Need to look into NTBs and subsidies and how they affect Need to look into NTBs and subsidies and how they affect

opportunities for developing country producers to participate in opportunities for developing country producers to participate in global supply chains global supply chains

• Trade can help promote market transformation (beyond EGS Trade can help promote market transformation (beyond EGS negotiations).negotiations).

• Integrated packages are needed to stimulate the successful Integrated packages are needed to stimulate the successful deployment of RE and EE technologies in emerging economies.deployment of RE and EE technologies in emerging economies.

• The uptake of RE and EE technologies in many developing The uptake of RE and EE technologies in many developing countries will require a broad array of support measures (e.g. countries will require a broad array of support measures (e.g. sharing knowledge of the technologies and their components, sharing knowledge of the technologies and their components, financing and capacity-building).financing and capacity-building).

5ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

METHODOLOGICAL ISSUESMETHODOLOGICAL ISSUES

• HS codes often not specific enough to capture climate-friendly technologies: unrelated goods get included (“ex-out” items).

• Multiple-use: including non-environmental.

• Energy efficiency: in most cases tariff classifications cannot identify relatively energy-efficient products

• A good match between RE A good match between RE technologies and HS exists in technologies and HS exists in only very few cases. only very few cases. − In several proposed definitions In several proposed definitions

of (potential) EG, multiple-use of (potential) EG, multiple-use products represent around 80 products represent around 80 per cent of world imports.per cent of world imports.

• Consulting more detailed tariff schedules may sometimes be useful, but conclusions cannot be generalized.

• In most cases, expert opinions and industry surveys are needed to assess whether the deployment of climate-friendly technologies is a driver of trade− USITC study on US wind

industry

“Ex-outs”• Where multiple use is intrinsic

to the product, creating “ex-outs” is not a viable option.

6ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

MAPPING TECHNOLOGIES: RE SUPPLYMAPPING TECHNOLOGIES: RE SUPPLY

Key technologies:Key technologies:• Solar energySolar energy

− Concentrating solar power Concentrating solar power (CSP)(CSP)

− Solar heating and cooling Solar heating and cooling − Photovoltaic (PV) Photovoltaic (PV)

• Wind energyWind energy− OnshoreOnshore− OffshoreOffshore

• HydropowerHydropower• BiomassBiomass

− EquipmentEquipment− BiofuelsBiofuels

• Ocean energyOcean energy• Geothermal energyGeothermal energy

Trade analysis Trade analysis (largest number of products)(largest number of products)

• Single environmental useSingle environmental use− Finished products (examples)Finished products (examples)

• Solar PV panels (Ex Solar PV panels (Ex 8541.40)8541.40)

• SWH equipment (Ex SWH equipment (Ex 8419.19)8419.19)

• Wind-energy turbines Wind-energy turbines (850231)(850231)

− Hydraulic turbines (HS 8410)Hydraulic turbines (HS 8410)− Biofuels Biofuels

• Ex 2207Ex 2207• Ex 382490Ex 382490

• ComponentsComponents− Participation in supply chainsParticipation in supply chains

− Multiple use issues (and “ex-Multiple use issues (and “ex-out” issues)out” issues)

7ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

MAPPING TECGNOLOGIES: BUILDINGSMAPPING TECGNOLOGIES: BUILDINGS

Key technologies:Key technologies:• Improving energy efficiency (EE) Improving energy efficiency (EE)

in new and existing buildingsin new and existing buildings− Insulation materials Insulation materials − Efficient lightingEfficient lighting− Energy-efficient HVAC-R, hot Energy-efficient HVAC-R, hot

water, applianceswater, appliances

• Increasing renewable energy Increasing renewable energy (RE) use in buildings(RE) use in buildings − Active collection and Active collection and

transformation of solar energy transformation of solar energy − RE heating and cooling (REHC), RE heating and cooling (REHC),

such as geothermal heat pumps such as geothermal heat pumps and wood-pellet stovesand wood-pellet stoves

overlap with RE supplyoverlap with RE supply

Trade analysisTrade analysis

• Certain insulation materialsCertain insulation materials− excl multiple-use materialsexcl multiple-use materials

• Efficient lightingEfficient lighting− HS 8531.39HS 8531.39

• EE componentsEE componentse.g. control instruments e.g. control instruments (such as thermostats)(such as thermostats)

• Solar PV panels Solar PV panels − HS 8541.40 (includes LED)HS 8541.40 (includes LED)

• Solar water heatersSolar water heaters− HS Ex 8419.19HS Ex 8419.19

• Heat pumpsHeat pumps− HS Ex 8418.61HS Ex 8418.61

8ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

MAPPING TECHNOLOGIES: ROAD MAPPING TECHNOLOGIES: ROAD TRANSPORTTRANSPORT

Key technologies:Key technologies:

• More efficient petroleum-powered More efficient petroleum-powered vehiclesvehicles− Improvements to gasoline and diesel Improvements to gasoline and diesel

internal-combustion engines (ICE) internal-combustion engines (ICE) − Non-engine technologies; e.g. lighting Non-engine technologies; e.g. lighting

and air conditioning, rolling-resistant tyres and air conditioning, rolling-resistant tyres − Lightweight materials Lightweight materials

• Larger market penetration of alternative, Larger market penetration of alternative, low-carbon vehicles such as hybrid cars, low-carbon vehicles such as hybrid cars, plug-in hybrids and electric carsplug-in hybrids and electric cars− Electric carsElectric cars− Battery technologiesBattery technologies− Fuel cells Fuel cells

• Increased consumption of biofuelsIncreased consumption of biofuels

Trade analysisTrade analysis

• Electric carsElectric cars• Ex 8703.90Ex 8703.90• BatteriesBatteries

− Ex 8506.80Ex 8506.80− Ex 8507.80Ex 8507.80

• Fuel cellsFuel cells

• BiofuelsBiofuels− Ex 2207.10Ex 2207.10− Ex 2207.20Ex 2207.20− Ex 3824.90Ex 3824.90

9ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TRADE IN CLIMATE-FRIENDLY TRADE IN CLIMATE-FRIENDLY TECHNOLOGIES/PRODUCTSTECHNOLOGIES/PRODUCTS

Based on ICTSD studies:Based on ICTSD studies:

• Although trade in products and components (that may be) Although trade in products and components (that may be) associated with climate-friendly technologies is significantly associated with climate-friendly technologies is significantly overestimated due to “ex-out” and multiple-use issues, it overestimated due to “ex-out” and multiple-use issues, it represents only around 2% of total world trade or around 3% of represents only around 2% of total world trade or around 3% of world trade in industrial products (HS 28-97). world trade in industrial products (HS 28-97).

• Developing country share in world exports (excluding intra-EU Developing country share in world exports (excluding intra-EU trade) increased from 32% in 2004 to 42% in 2008, in value trade) increased from 32% in 2004 to 42% in 2008, in value terms. terms.

• Very strong increase developing country share wind and solar Very strong increase developing country share wind and solar energy.energy.

• Their share in world imports remained stable at around 60%. Their share in world imports remained stable at around 60%. • The share in total developing country exports of industrial The share in total developing country exports of industrial

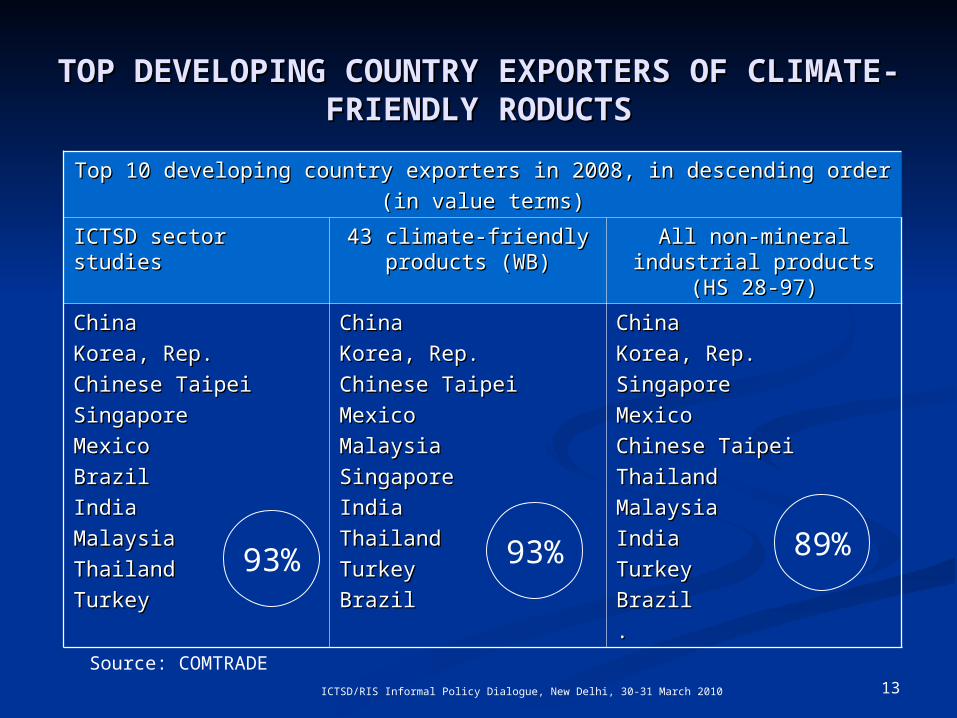

products increased gradually from 2% in 2004 to 3% in 2008.products increased gradually from 2% in 2004 to 3% in 2008.• Top developing country exporters of products and components Top developing country exporters of products and components

associated with climate-friendly technologies are no different from associated with climate-friendly technologies are no different from top exports of industrial products in general.top exports of industrial products in general.

Trade flows

10ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

SHARES IN WORLD EXPORTS OF RE SHARES IN WORLD EXPORTS OF RE TECHNOLOGIES/GOODSTECHNOLOGIES/GOODS

Shares in world exports (excluding intra-EU trade)Shares in world exports (excluding intra-EU trade)

20042004 20052005 20062006 20072007 20082008

Brazil, China, India and South AfricaBrazil, China, India and South Africa 1313 1515 1818 2020 2323

- ChinaChina 1111 1212 1515 1717 1919

- Brazil, India and South Africa- Brazil, India and South Africa 22 33 44 44 44

Other developing countriesOther developing countries 1818 1818 1818 1919 1818

Rest of the worldRest of the world 6969 6767 6464 6060 5959

TotalTotal 100100 100100 100100 100100 100100

Large emerging economies increased their share (in value terms) in world exports of goods and components associated with RE technologies during the period 2004-2008 (at the expense of developed countries)

Source: COMTRADE and ICTSD studies

11ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

DEVELOPING COUNTRY SHARE IN EXPORTS OF DEVELOPING COUNTRY SHARE IN EXPORTS OF WIND TURBINES UP SHARPLYWIND TURBINES UP SHARPLY

Top exportersTop exporters Exports (in US$ values)Exports (in US$ values)

20020044

20052005 20020066

20020077

20082008

WorldWorld 10710744

19161916 30930966

38638666

53925392

GermanyGermany 9797 590590 832832 969969 20042004

DenmarkDenmark 888888 998998 11811822

16716733

11861186

IndiaIndia 11 2424 199199 336336 651651

SpainSpain 3737 182182 327327 198198 479479

JapanJapan 00 88 143143 354354 469469

ChinaChina 00 00 00 33 211211

Developing countriesDeveloping countries 2020 6666 285285 525525 10101010

World World (excl-intra EU)(excl-intra EU) 561561 11041104 24624677

28028033

33353335

Share (%)Share (%) 44 66 1212 1919 3030

0

500

1000

1500

2000

2500

2004 2005 2006 2007 2008

Other exporters

Developing country exporters

Source: COMTRADE

12ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

EXPORTS OF PV CELLS AND MODULESEXPORTS OF PV CELLS AND MODULES

• Developing country share in world exports Developing country share in world exports (excl. intra-EU trade) of solar PV cells and (excl. intra-EU trade) of solar PV cells and modules has increased sharply in recent modules has increased sharply in recent yearsyears

• Chinese and Indian exports increased, Chinese and Indian exports increased, largely in response to rapidly increasing largely in response to rapidly increasing EU imports (in particular Spain and EU imports (in particular Spain and Germany) Germany)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2003 2004 2005 2006 2007 2008

World exports excl. intra-EU

Developing country exports

Exports by other countries

Developing country share (%)Developing country share (%)

20032003 20042004 20052005 20062006 20072007 20082008

2525 3535 3939 4646 5555 6464

Developing country exports of solar PV Developing country exports of solar PV cells/modules ($m)cells/modules ($m)

20042004 20052005 20062006 20072007 20082008

ChinaChina 644644 12581258 24602460 52525252 1174511745

IndiaIndia 8787 9494 134134 213213 529529

OtherOther 28812881 32783278 41974197 53425342 71857185

Source: COMTRADE

13ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TOP DEVELOPING COUNTRY EXPORTERS OF TOP DEVELOPING COUNTRY EXPORTERS OF CLIMATE-FRIENDLY RODUCTSCLIMATE-FRIENDLY RODUCTS

Top 10 developing country exporters in 2008, in descending orderTop 10 developing country exporters in 2008, in descending order

(in value terms)(in value terms)

ICTSD sector studiesICTSD sector studies 43 climate-friendly 43 climate-friendly products (WB)products (WB)

All non-mineral industrial All non-mineral industrial products (HS 28-97)products (HS 28-97)

ChinaChina

Korea, Rep.Korea, Rep.

Chinese TaipeiChinese Taipei

SingaporeSingapore

MexicoMexico

BrazilBrazil

IndiaIndia

Malaysia Malaysia

ThailandThailand

Turkey Turkey

ChinaChina

Korea, Rep.Korea, Rep.

Chinese TaipeiChinese Taipei

MexicoMexico

MalaysiaMalaysia

Singapore Singapore

IndiaIndia

ThailandThailand

Turkey Turkey

BrazilBrazil

ChinaChina

Korea, Rep.Korea, Rep.

SingaporeSingapore

Mexico Mexico

Chinese TaipeiChinese Taipei

ThailandThailand

MalaysiaMalaysia

IndiaIndia

Turkey Turkey

BrazilBrazil

. .

93% 93% 89%

Source: COMTRADE

14ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

WHAT ARE THE IMPORTANT BARRIERS?WHAT ARE THE IMPORTANT BARRIERS?

• Tariffs are, in general, less significant as an explanatory variable Tariffs are, in general, less significant as an explanatory variable for increased exports or imports of RE equipment and components for increased exports or imports of RE equipment and components compared to other variables. compared to other variables. − However, bio-ethanol tariffs have significant impacts on trade (bio-However, bio-ethanol tariffs have significant impacts on trade (bio-

ethanol is an agricultural product).ethanol is an agricultural product). • WRI study on the wind-energy industry: non-tariff barriers (NTBs) WRI study on the wind-energy industry: non-tariff barriers (NTBs)

and formal and informal barriers that distort firms’ investment and formal and informal barriers that distort firms’ investment decisions (rather than import tariffs) are the principal obstacles to decisions (rather than import tariffs) are the principal obstacles to global integration.global integration.

• NTBs, subsidies and their effects on opportunities for developing NTBs, subsidies and their effects on opportunities for developing country producers to participate in global supply chains.country producers to participate in global supply chains.

The markets for RE technologies are distorted by subsidies, The markets for RE technologies are distorted by subsidies, preferential procurement policies, local-content provisions, tied preferential procurement policies, local-content provisions, tied aid and projects offering tariff and other concessionsaid and projects offering tariff and other concessions

Trade barriers

15ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TARIFFS IN LARGE EMERGING ECONOMIESTARIFFS IN LARGE EMERGING ECONOMIES

Sample of products that may be associated with climate-friendly Sample of products that may be associated with climate-friendly technologies:technologies:

• China: MFN applied tariffs are mostly in the 8-12% range China: MFN applied tariffs are mostly in the 8-12% range − Simple average close to 10%. Simple average close to 10%.

• India: Most MFN applied tariffs are either 7.5 or 10% India: Most MFN applied tariffs are either 7.5 or 10% − Simple average of slightly above 8%. Simple average of slightly above 8%.

• Brazil: simple average of MFN applied rates around 14%. Brazil: simple average of MFN applied rates around 14%. • In South Africa, most tariffs are in the 0-15% range In South Africa, most tariffs are in the 0-15% range

− Simple average of around 5%Simple average of around 5%

• Solar PV cells and panels (part of HS 8541.40) enter most markets Solar PV cells and panels (part of HS 8541.40) enter most markets (including China, India and South Africa) duty-free. 99.5% per cent of (including China, India and South Africa) duty-free. 99.5% per cent of 2008 world imports of (in value terms, excluding intra-EU trade) 2008 world imports of (in value terms, excluding intra-EU trade) enjoyed zero MFN applied rates (for developing country importers: enjoyed zero MFN applied rates (for developing country importers: 98.5%).98.5%).− In Brazil: MFN applied rate of 12%In Brazil: MFN applied rate of 12%

• In many developing countries MFN applied rates for solar water heaters In many developing countries MFN applied rates for solar water heaters (part of HS 8419.19) are rather high (20% in Brazil and 35% in China).(part of HS 8419.19) are rather high (20% in Brazil and 35% in China).

16ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TARIFF LIBERALISATION: SOME ISSUESTARIFF LIBERALISATION: SOME ISSUES

• It is sometimes suggested that tariff liberalisation could focus on It is sometimes suggested that tariff liberalisation could focus on finished products with predominantly single environmental use (to finished products with predominantly single environmental use (to minimise concerns related to multiple-use products).minimise concerns related to multiple-use products).− Preferred option for smaller developing countries? Preferred option for smaller developing countries? − Focusing liberalisation on finished products only might, in theory, affect Focusing liberalisation on finished products only might, in theory, affect

tariff structures and, in some cases, result in negative protection. tariff structures and, in some cases, result in negative protection.

• Developing countries with sufficiently large markets seek to develop Developing countries with sufficiently large markets seek to develop local manufacturing capacities and attract FDI. local manufacturing capacities and attract FDI. − Examples: wind energy in Brazil and China, National Solar Mission in India Examples: wind energy in Brazil and China, National Solar Mission in India

and SWH in South Africa.and SWH in South Africa.− Infant-industry arguments for tariff protection (but avoiding inefficiency)? Infant-industry arguments for tariff protection (but avoiding inefficiency)? − Liberalising key intermediate products (despite multiple-use issues)? Liberalising key intermediate products (despite multiple-use issues)?

• Some countries may have relatively high tariffs at the border, but Some countries may have relatively high tariffs at the border, but provide for significant fiscal incentives (e.g. internal tax reductions or provide for significant fiscal incentives (e.g. internal tax reductions or exemptions. Example: Brazilian incentives for solar and wind-energy exemptions. Example: Brazilian incentives for solar and wind-energy products) products)

17ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TARIFFS, WIND ENERGY: TARIFFS, WIND ENERGY: FINISHED PRODUCTS AND COMPONENTSFINISHED PRODUCTS AND COMPONENTS

BrazilBrazil ChinaChina IndiaIndia South Africa South Africa

ApplieAppliedd

(2009)(2009)

BoundBound AppliedApplied

(2008)(2008)BoundBound ApplieApplie

dd

(2008(2008))

BoundBound ApplieAppliedd

(2007(2007))

BoundBound

Wind turbinesWind turbines 00

(14)(14)3535 88 88 88 2525 0 0 2020

ComponentsComponents

TowersTowers

BladesBlades

Ball bearingsBall bearings

GearboxesGearboxes

GeneratorsGenerators

Motor partsMotor parts

1414

1414

1616

1414

1414

1414

3535

3535

25-3525-35

25-3525-35

3535

3030

8.48.4

2-82-8

88

88

5.8-105.8-10

3-123-12

8.48.4

2-82-8

88

88

5.8-105.8-10

3-123-12

1010

88

88

88

88

88

4040

2525

4040

4040

4040

4040

7.57.5

00

00

00

00

5-155-15

1515

1515

3030

1010

3030

1515

Source: WTO Tariff Download Facility

18ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

INCENTIVES AND NTBsINCENTIVES AND NTBs

Incentives and subsidiesIncentives and subsidies− Incentives based on Government interventions (such as Feed-Incentives based on Government interventions (such as Feed-

in Tariffs) in Tariffs) − Governments subsidies (e.g. installation subsidies, tax credits, Governments subsidies (e.g. installation subsidies, tax credits,

preferential loans)preferential loans)− Manufacturing subsidies (e.g. section 48C of the American Manufacturing subsidies (e.g. section 48C of the American

Recovery and Reinvestment Act (ARRA))Recovery and Reinvestment Act (ARRA))

WRI study on wind-energy sector: NTBs more important than WRI study on wind-energy sector: NTBs more important than tariffs: tariffs:

− Local content requirements (in developed and developing countries)

− Different industrial standards and certification requirements.− Political quid-pro-quo expectations

19ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

KEY DRIVERS, POLICIES AND MEASURESKEY DRIVERS, POLICIES AND MEASURES

DriversDrivers• Climate change (in particular in developed countries) Climate change (in particular in developed countries) • Energy shortage, access to energy (in particular in developing Energy shortage, access to energy (in particular in developing

countries)countries)

Policies and measures (examples)Policies and measures (examples)

RE technologiesRE technologies• Renewable portfolio standards (which require electricity providers to obtain a Renewable portfolio standards (which require electricity providers to obtain a

minimum percentage of their power from RE resources by a certain date). minimum percentage of their power from RE resources by a certain date). • Feed-in tariffs to encourage the deployment of RE technologies for electricity Feed-in tariffs to encourage the deployment of RE technologies for electricity

generation.generation.

BuildingsBuildings • EE requirements in building codes, incentives for renovationsEE requirements in building codes, incentives for renovations• Minimum energy performance standards (MEPS) and labellingMinimum energy performance standards (MEPS) and labelling

TransportTransport•• Fuel-economy or CO2 emissions standards. Fuel-economy or CO2 emissions standards.

•• Blending mandatesBlending mandates

Market drivers

20ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

DRIVERS OF TRADEDRIVERS OF TRADE

DriversDrivers• Capacity additions are often an important driver of international trade.Capacity additions are often an important driver of international trade. • Nine of the 10 countries that most expanded their wind-energy Nine of the 10 countries that most expanded their wind-energy

capacity in 2008 are also among the top 20 importers of wind turbines capacity in 2008 are also among the top 20 importers of wind turbines (India being the exception). (India being the exception).

• USITC study: from 1998 to 2005 changes in US imports of wind USITC study: from 1998 to 2005 changes in US imports of wind turbines were closely correlated with changes in annual wind-turbine turbines were closely correlated with changes in annual wind-turbine installations.installations.

• Large additions in installed PV solar capacity in Spain and Germany (in Large additions in installed PV solar capacity in Spain and Germany (in particular in 2008) resulted in significant increases of imports. particular in 2008) resulted in significant increases of imports. − Chinese exports of solar PV modules jumped from $5.3 billion in 2007 to Chinese exports of solar PV modules jumped from $5.3 billion in 2007 to

$11.7 billion in 2008 with exports to Spain and Germany together $11.7 billion in 2008 with exports to Spain and Germany together accounting for almost 70 per cent of this increase. accounting for almost 70 per cent of this increase.

Developing country advantagesDeveloping country advantages• Abundant renewable resourcesAbundant renewable resources• Lower production costs (equipment, components) Lower production costs (equipment, components)

21ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

THE SOLAR PV MARKET: TRADE GENERATION THE SOLAR PV MARKET: TRADE GENERATION

• World solar PV market of 5.95 GW in 2008 World solar PV market of 5.95 GW in 2008 • Increase of 110% over 2007 (285% growth in Spain)Increase of 110% over 2007 (285% growth in Spain)

− A large part of demand was met by imports (from China, India)A large part of demand was met by imports (from China, India)

• Market grew 5% to 6.37 GW in 2009 (i.e. in terms of new capacity Market grew 5% to 6.37 GW in 2009 (i.e. in terms of new capacity installations; price decreases may have resulted in lower market installations; price decreases may have resulted in lower market values) values) − Negative factors: Negative factors: new installed capacity eligible for FiT capped to 500 new installed capacity eligible for FiT capped to 500

MW in Spain and recession MW in Spain and recession − Positive factors: New incentives (China, Japan) and strong demand Positive factors: New incentives (China, Japan) and strong demand

growth in Germany in anticipation of reduction of FiTgrowth in Germany in anticipation of reduction of FiT

• In 2008, PV market of 5.95 GW generated $30.5b of world trade.In 2008, PV market of 5.95 GW generated $30.5b of world trade.• Subsidies/FiT (which suddenly change) contributing to market Subsidies/FiT (which suddenly change) contributing to market

fluctuations fluctuations • Ambitious targets to strengthen the domestic market (e.g. India) Ambitious targets to strengthen the domestic market (e.g. India)

22ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

THE WIND-ENERGY MARKET: THE WIND-ENERGY MARKET: TRADE GENERATIONTRADE GENERATION

• World wind-energy market: 37.5 GW in 2009 World wind-energy market: 37.5 GW in 2009 • In 2009, China added more capacity (13.9 GW) than any other In 2009, China added more capacity (13.9 GW) than any other

country. country. • Imports into the US market have been key driver of Imports into the US market have been key driver of

international tradeinternational trade• In 2008: wind-energy market of 27.1 GW generated $3.3b of In 2008: wind-energy market of 27.1 GW generated $3.3b of

world imports of wind turrbines.world imports of wind turrbines. Annual wind-energy capacity additions (MW), 2004-2009 Annual wind-energy capacity additions (MW), 2004-2009

20042004 20052005 20062006 20072007 20082008 20092009

ChinaChina 197197 496496 13391339 33113311 63006300 1300013000

EU27EU27 57735773 61406140 75187518 85028502 84178417 1016310163

United StatesUnited States 353353 24242424 24262426 52495249 83468346 99229922

IndiaIndia 875875 14301430 18401840 15751575 18001800 12711271

WorldWorld 82078207 1153111531 1524515245 1986519865 2705127051 3746637466

Source: Global Wind Energy Council

23ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TRADE INTENSITY MAY DIMINISHTRADE INTENSITY MAY DIMINISH

• Future capacity may generate less trade per MW Future capacity may generate less trade per MW

• The correlation between additions to RE installations and imports The correlation between additions to RE installations and imports may weaken over time, as local content increases: may weaken over time, as local content increases: − As (larger) countries add more installed capacity, domestic As (larger) countries add more installed capacity, domestic

industry will develop more capacity to supply RE equipment industry will develop more capacity to supply RE equipment and components.and components.

− Leading manufacturers may target growing markets through FDI (e.g. subsidiaries or joint ventures) rather than exports (e.g. subsidiaries or joint ventures) rather than exports (wind-industry)(wind-industry)

− Governments which play a key role in stimulating the take-off of RE capacity by providing incentives may seek to ensure maximum benefit for local (domestic and foreign-owned) firms and employment, in particular when incentives are provided through stimulus packages. This is done through This is done through formal local content requirements or political pressure.formal local content requirements or political pressure.

24ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

US: ANNUAL WIND CAPACITY ADDITIONS US: ANNUAL WIND CAPACITY ADDITIONS AND IMPORTS OF WIND TURBINESAND IMPORTS OF WIND TURBINES

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Annual wind-energy capacity additions

Imports of wind turbines(US$ values)

(10 GW)

(US$2.3b)

Source: USITC, updated

25ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

LESSONS LEARNED FOR EGS LESSONS LEARNED FOR EGS NEGOTIATIONSNEGOTIATIONS

• EGS liberalisation may be relevant for only part of the technology EGS liberalisation may be relevant for only part of the technology options identified by IPCC.options identified by IPCC.

• Tariff policies only a small part of policy options and unlikely to have a Tariff policies only a small part of policy options and unlikely to have a significant impact if not supporting other (more targeted/efficient) significant impact if not supporting other (more targeted/efficient) policies. policies.

• Difficult to agree on which products to include in definition of EG. Difficult to agree on which products to include in definition of EG. • Only a limited number of products may have a clear environmental Only a limited number of products may have a clear environmental

benefit. benefit. • Most products involve multiple use and “ex-out” issues, with Most products involve multiple use and “ex-out” issues, with

environmental benefit, if any, depending on many factors. environmental benefit, if any, depending on many factors. − In countries where there are no strong RE and EE policies, 6-digit HS codes In countries where there are no strong RE and EE policies, 6-digit HS codes

are not likely to significantly include EG are not likely to significantly include EG

• Liberalising trade in a certain multiple-use products may be useful, Liberalising trade in a certain multiple-use products may be useful, but fast-tracking under paragraph 31(iii) may be difficult to justify.but fast-tracking under paragraph 31(iii) may be difficult to justify.

• Positive outcome of EGS negotiations may be important, politically. Positive outcome of EGS negotiations may be important, politically. • Developing countries need flexibility (e.g. through request and offer) Developing countries need flexibility (e.g. through request and offer)

to harness real possibilities for environmental and developmental to harness real possibilities for environmental and developmental gains.gains.

Lessons learned

26ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

THANK YOUTHANK YOU

27ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TRADE BALANCES (2008)TRADE BALANCES (2008)ICTSD STUDIESICTSD STUDIES

NET EXPORTERSNET EXPORTERS $ $ millionsmillions

NET IMPORTERSNET IMPORTERS $ $ millionsmillions

ChinaChina 2067420674 United StatesUnited States -13762-13762

JapanJapan 2058620586 Hong Kong, ChinaHong Kong, China -11168-11168

EU (excluding intra-EU)EU (excluding intra-EU) 1061710617 Russian FederationRussian Federation -5144-5144

IsraelIsrael 21562156 CanadaCanada -3980-3980

Chinese TaipeiChinese Taipei 905905 United Arab EmiratesUnited Arab Emirates -3778-3778

SwitzerlandSwitzerland 885885 AustraliaAustralia -3001-3001

BrazilBrazil 882882 MexicoMexico -1766-1766

South Africa, RepublicSouth Africa, Republic -1276-1276

IndiaIndia -1150-1150

Developing countriesDeveloping countries -17017-17017Source: COMTRADE

ANNEX

28ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TRADE BALANCES (2008)TRADE BALANCES (2008) 43 CLIMATE-FRIENDLY GOODS (WB) 43 CLIMATE-FRIENDLY GOODS (WB)

NET EXPORTERSNET EXPORTERS $ $ millionsmillions

NET IMPORTERSNET IMPORTERS $ $ millionsmillions

JapanJapan 1406214062 United StatesUnited States -5546-5546

EU27 (excl. intra-EU EU27 (excl. intra-EU trade)trade)

87818781 Hong Kong, ChinaHong Kong, China -4827-4827

ChinaChina 49124912 Russian FederationRussian Federation -3365-3365

Chinese TaipeiChinese Taipei 28102810 CanadaCanada -2534-2534

Korea, RepublicKorea, Republic 878878 TurkeyTurkey -2388-2388

MalaysiaMalaysia 798798 United Arab EmiratesUnited Arab Emirates -2329-2329

MexicoMexico 323323 AustraliaAustralia -1956-1956

SingaporeSingapore 181181

BrazilBrazil -1118-1118

South Africa, RepublicSouth Africa, Republic -845-845

IndiaIndia -431-431

Developing countriesDeveloping countries -14281-14281Source: COMTRADE

29ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

TRADE BALANCES (2008)TRADE BALANCES (2008)ICTSD STUDIES: PREDOMINANTLY SINGLE USEICTSD STUDIES: PREDOMINANTLY SINGLE USE

NET EXPORTERSNET EXPORTERS $ $ millionsmillions

NET IMPORTERSNET IMPORTERS $ $ millionsmillions

ChinaChina 1156911569 United StatesUnited States -4453-4453

JapanJapan 56895689 EU (excluding intra-EU)EU (excluding intra-EU) -4200-4200

Chinese TaipeiChinese Taipei 31673167 Hong KongHong Kong -2160-2160

IndiaIndia 714714 Korea, Rep.Korea, Rep. -1600-1600

BrazilBrazil -306-306

South AfricaSouth Africa -116-116

Developing countriesDeveloping countries 1015110151Source: COMTRADE

30ICTSD/RIS Informal Policy Dialogue, New Delhi, 30-31 March 2010

SELECTED PRODUCTS (12) WITH SELECTED PRODUCTS (12) WITH PREDOMINANTLY ENVIRONMENTAL USEPREDOMINANTLY ENVIRONMENTAL USE

Exports in 2008 (3 principal Exports in 2008 (3 principal products)products)

Imports in 2008 (3 principal Imports in 2008 (3 principal products) products)

HSHS ProductProduct $millio$millionn

HSHS ProductProduct $million$million

BrazilBrazil 117117 BrazilBrazil 424424841090841090 Hydraulic turbines, partsHydraulic turbines, parts 7272 853931853931 Fluorescent, hot cathode Fluorescent, hot cathode

lampslamps136136

853931853931 Fluorescent, hot cathode Fluorescent, hot cathode lampslamps

1515 850231850231 Wind turbinesWind turbines 122122

850231850231 Wind turbinesWind turbines 1414 854140854140 Solar PV cells and panelsSolar PV cells and panels 115115

ChinaChina 1608616086 ChinaChina 45174517854140854140 Solar PV cells and panelsSolar PV cells and panels 1174511745 854140854140 Solar PV cells and panelsSolar PV cells and panels 37443744

853931853931 Fluorescent, hot cathode Fluorescent, hot cathode lampslamps

47344734 841861841861 Heat pumpsHeat pumps 339339

850231850231 Wind turbinesWind turbines 211211 850231850231 Wind turbinesWind turbines 189189

IndiaIndia 12441244 IndiaIndia 530530850231850231 Wind turbinesWind turbines 651651 854140854140 Solar PV cells and panelsSolar PV cells and panels 422422

854140854140 Solar PV cells and panelsSolar PV cells and panels 529529 853931853931 Fluorescent, hot cathode Fluorescent, hot cathode lampslamps

3333

853931853931 Fluorescent, hot cathode Fluorescent, hot cathode lampslamps

2929 841090841090 Hydraulic turbines, partsHydraulic turbines, parts 1919

South AfricaSouth Africa 187187 South AfricaSouth Africa 304304854140854140 Solar PV cells and panelsSolar PV cells and panels 175175 854140854140 Solar PV cells and panelsSolar PV cells and panels 161161

841861841861 Heat pumpsHeat pumps 44 853931853931 Fluorescent, hot cathode Fluorescent, hot cathode lampslamps

5757

680610680610 Slag wool Slag wool 33 841861841861 Heat pumpsHeat pumps 3838

Source: COMTRADE