Embed Size (px)

Citation preview

Reviewing the Europeanexcellence model from amanagement control view

Su Mi Dahlgaard-ParkInstitute of Service Management, Lund University, Sweden

Abstract

Purpose – The purpose of this paper is to review and identify the dominating paradigms withinmanagement control theories in order to investigate adoptability of the European excellence model(EEM) as an alternative management control model or a framework.

Design/methodology/approach – The paper has conceptual character based on a literaturesurvey.

Findings – The six dominating paradigms are identified within management control theories andbased on the analysis it is concluded that EEM can be adapted as a management control model if itslimitations are supplemented with other ideas or frameworks.

Originality/value – This is the first study which investigates adaptability and adoptability of EEMas a management control model.

Keywords Control, European quality model, Control systems, Evolution, Management activities

Paper type Conceptual paper

1. IntroductionSince the beginning of the twentieth century, where early management theoreticianssuch as Taylor, Emerson, and Church introduced the basic ideas of control, theconcepts and frameworks of management control theory changed constantly. As Berryet al. (1998) point it out, the early study of management control seems to be rooted in afunctionalistic and rather mechanical paradigm[1] in line with other generalmanagement and organization theories, which were dominating in the same period.However, the literature study on the subject shows that during the last several decades,various alternative viewpoints based on different sets of conceptions and assumptionshave been presented.

Quality management (QM) is a management philosophy, which has evolved from arather narrow and mechanistic approach known as statistical quality controlintroduced by Shewhart to a more holistic and humanistic approach under the termtotal quality management (TQM) and business excellence (Dahlgaard-Park et al., 2001).During the last five decades the basic assumptions and paradigms of quality haveconstantly changed parallel with the general changes of paradigms in societies andglobal environments. These changes are not unique within the quality field but more orless in line with changes within other management fields including organizationaltheory and management control theory (Dahlgaard-Park, 1999).

Despite the increasing focus on QM during the 1980s and 1990s, and despite the factthat quality became a central agenda for top managers, there have been relativelylimited attempts on searching, reflecting and analysing its framework seen from a

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1754-2731.htm

TQM20,2

98

The TQM JournalVol. 20 No. 2, 2008pp. 98-119q Emerald Group Publishing Limited1754-2731DOI 10.1108/17542730810857345

broader theoretical perspective (Scott and Cole, 1999). In fact, this was also one of themajor criticisms, which the quality movement often received from varioustheoreticians during the middle and last part of the 1990s in particular fromorganization theorists (Dahlgaard-Park, 2006).

This criticism has been received in the quality research field with some surprise. Oneof the reasons is that the development of the QM philosophy and in particular TQM wasbased on an emergent need for a new management philosophy and a holistic/integrativemanagement model, which had an emphasis on quality as the main strategy forimproving competitiveness. The need for improving quality and thereby strengthencompetitiveness was perceived as an emergent task for major European and NorthAmerican companies, which were confronted with serious challenges from Japanesecompanies. The Japanese companies had become “masters” in practicing company widequality control (CWQC) and in this way they gained a competitive advantage comparedto most western companies. This company wide approach to quality was unknown formost Western companies until the 1980s, when it was understood what had happened inJapan, and why a new management philosophy was needed. The huge interest towardTQM during the last part of the 1980s and the 1990s should be understood with thesecontextual factors as a background. The existing theories and models of organizationand management could not provide the necessary principles, tools and systems to meetthese new challenges and problems. For practitioners, the majority of the existingmanagement theories were considered to be either too theoretical or too fragmental.

As “insiders” in the quality field we find that much of the criticisms fromorganization or management theorists are unreasonable, because those critics are oftenbased on insufficient knowledge on the quality movement and the “becoming process”of TQM (Dahlgaard-Park, 2006). For instance “lack of a generally agreed definition”was one of major criticisms toward quality management. However when I investigatedin several other management fields such as knowledge management, human resourcemanagement, strategic management etc. it became clear for me that the phenomena of“lacking generally agreed definition” was a common characteristic of those investedmanagement fields. This does not mean that all criticisms toward quality managementare irrelevant! I am more than critical for quality professionals intended or not intended“blindness” to enlighten the difficulties in relationship with implementation of quality.Especially the dilemma in terms of political, psychological, cultural and behaviourresistances in organisations are most frequent obstacles when implementing qualityand hence there are strong needs for more focus on these uncovered or “ignored” areas.I believe that other management theories can be used in reflecting and analysing thequality frameworks and thereby to deepen quality professionals own understandingon weaknesses as well as strengths of the quality frameworks.

With this consideration in background, I have chosen to investigatemanagement control theory – one of the main management theories – in orderto reflect the quality frameworks in light of management control view. Thus theoverall aim of the article is to compare the contemporary thinking withinmanagement control theories with the contents and basic concepts/principles ofone of the leading quality award models – the European excellence model (EEM).In this article, we will assume that the leading quality award models such as theMalcolm Baldrige Model and the EEM reflect the latest step in the evolution ofquality management theories.

The Europeanexcellence model

99

The purposes of this paper are to:. review some of the main management control theories, and based on the

literature review (sections 2 and 3);. investigate whether the EEM is comparable to the current thinking within

management control theories (sections 4 and 5);. investigate the adoptability as well as adaptability of the model as a

management control model (section 6).

2. Reviewing management control theoriesReview on selected literature on management control theories indicates that there arevarious approaches based on different assumptions, focus areas, different weighting ofimportance, etc.

Goal directed, adaptive, social structured, contingency (Berry et al., 1998),bureaucratic, market and clan (Ouchi, 1980), cybernetic, homeostatic and politicalparadigms (Hofstede, 1978), management principle, cybernetic, contingency, agency,psychological, and case view (Merchant and Simon, 1986), technical-rational andcollectivist view (Ansari and Bell, 1991) are some examples of the different paradigmsidentified in the management control theories. When taking time aspect inconsideration, we can observe several changes in wording.

The differences on definitions adopted by various experts reflect both thetheoreticians’ selection of a certain approach and the evolution aspect when the theoriesare reviewed from a historical perspective. Here we have selected some definitions, whichindicate different viewpoints held by theorists in the field. At the same time we canobserve how definitions have been evolving during the last several decades.

Management Control is the process by which managers assure that resources are obtainedand used effectively and efficiently in the accomplishment of the organisation’s objectives(Robert Anthony, 1965).

Management control is a social process in a social, or maybe socio-technical system (GeertHofstede, 1978).

Organizational Control is defined as the systematic process through which managers regulateorganizational activities to make them consistent with the expectations established in plansand to help them achieve all predetermined standards of performance (K.A. Merchant, 1985).

Management control systems are broadly defined as the formalized routines, reports,and procedures that use information to maintain or alter patterns in organizationalactivity (Robert Simon, 1991).

Management control refers to all organizational arrangements, formal and informal, designedto accomplish organizational objectives. It includes formal structure, operational controls,rewards, budgeting, planning and other similar activities (Shahis L. Ansari and Jan Bell,1991).

Management control is the process by which managers influence other members of theorganizations to implement the organization’s strategies (Robert Anthony and Govindarajan,2001).

The presented definitions indicate that there are both similarities and differencesbetween them. Here we assume that the similarities may be related to the core concepts

TQM20,2

100

of management control, while the differences may be related to the various adoptedparadigms as scholars’ ideas about organizations vary and thereby also theirtheorization vary. Another reason for various definitions may be related to theevolutional aspect of management control theories. As it is observable in generalmanagement as well as in organisation theories, people adopt new ideas and therebytheorization varies (see for instance the managerial watch, Dahlgaard-Park, 2006, p. 217).

Most definitions seem to include the concepts of (systematic) process, managers,objective(s)/goal(s)[2], strategy, effectiveness and efficiency, maintenance and assurance.As several theorists (see Merchant and Simon, 1986, p. 184; Ansari and Bell, 1991, pp. 5-6)point it out, most definitions of control seem to be centred on a few key issues; a focus onthe behaviour of organizational participants and a concern with the effect of thisbehaviour on organizational outcomes. Focus on behaviour of organizational participantis related to the concept of efficiency, and the concern with outcomes is related toeffectiveness. In line with these few key issues, most theorists (see Merchant, 1985; Loweand Machin, 1987) seem to agree, that some of the main functions of the managementcontrol processes involves planning, setting standards of performance, coordinating,communication information, evaluating, influencing people, and processing information.

If we focus on the differences between the definitions, we find several curiousphenomena. First, instead of organizational objective(s)/goal(s), the concept ofstrategies seems to be adopted in the later definitions. Second, the role of managersseems to be more explicitly expressed and rather narrowly defined in the earlydefinitions. For instance, Anthony in his latest definition from 1998 used “managementinfluence”, and in his early definition from 1965, he used “managers assure”. Third,while Simon (1991) focuses on formalized aspects of management control processesand the importance of using information, Hofstede (1978) considers the control processas a social process, and in line with Hofstede’s view, Ansari and Bell (1991) includeboth formal and informal aspects in the process. Fourth, in the earlier definitions, therole of predetermined organizational goal(s)/objective(s) is more explicitly expressed,while this aspect is presented somewhat more ambiguously in the later definitions. Asmentioned above, one possible reason for these different views can be explained byvarious paradigms held by the theorists and the evolutional aspects of organization,people and management as parts of changing society.

Many theoreticians in management as well as organisation fields have attempted tocategorise theories in order to get an overview. Outcomes of these attempts becamebasis for schools of management thought or management paradigms (see for instance,Morgan, 1997/1986; Dahlgaard-Park, 2006). Merchant and Simon (1986) have identifiedseveral approaches within the research field of management control. Those approachesor paradigms introduced by Merchant and Simon (1986) within management controlliterature are quite similar to the organisation paradigms introduced by Morgan, sameyear (Morgan, 1997/1986) under the term of metaphors. It may be natural when weconsider the management control as a part of organization theories.

The following six management control approaches have been elaborated inspiredby several organization theorists and Merchant and Simon’s literature overviewtogether with my own literature review. The elaborated six approaches, which arediscussed in section 3 below, will be adopted as a conceptual multidimensionalframework for analysing the European excellence model in evaluating whether themodel can be considered as an “excellent management control model”.

The Europeanexcellence model

101

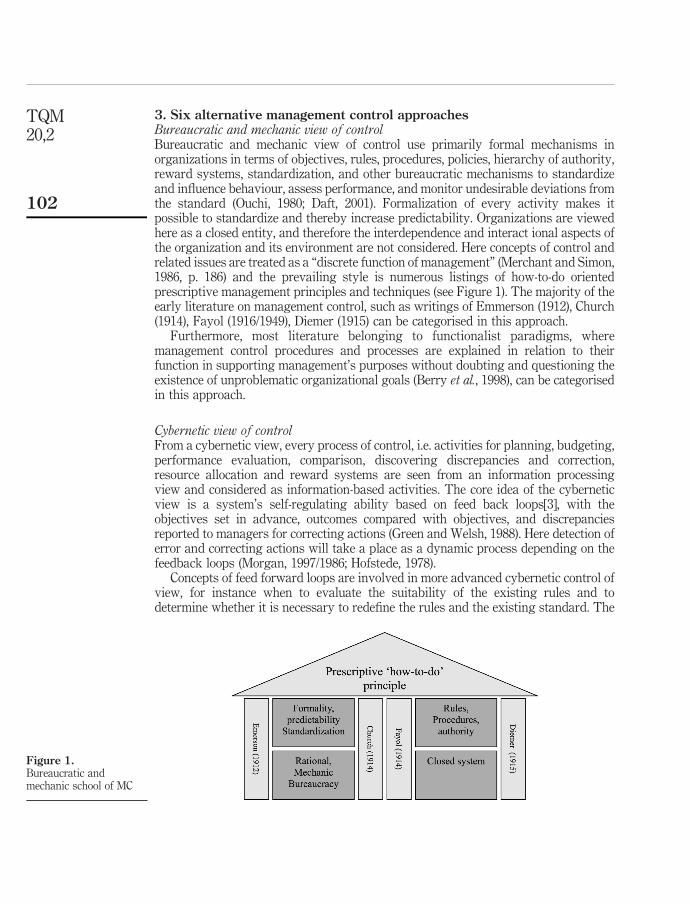

3. Six alternative management control approachesBureaucratic and mechanic view of controlBureaucratic and mechanic view of control use primarily formal mechanisms inorganizations in terms of objectives, rules, procedures, policies, hierarchy of authority,reward systems, standardization, and other bureaucratic mechanisms to standardizeand influence behaviour, assess performance, and monitor undesirable deviations fromthe standard (Ouchi, 1980; Daft, 2001). Formalization of every activity makes itpossible to standardize and thereby increase predictability. Organizations are viewedhere as a closed entity, and therefore the interdependence and interact ional aspects ofthe organization and its environment are not considered. Here concepts of control andrelated issues are treated as a “discrete function of management” (Merchant and Simon,1986, p. 186) and the prevailing style is numerous listings of how-to-do orientedprescriptive management principles and techniques (see Figure 1). The majority of theearly literature on management control, such as writings of Emmerson (1912), Church(1914), Fayol (1916/1949), Diemer (1915) can be categorised in this approach.

Furthermore, most literature belonging to functionalist paradigms, wheremanagement control procedures and processes are explained in relation to theirfunction in supporting management’s purposes without doubting and questioning theexistence of unproblematic organizational goals (Berry et al., 1998), can be categorisedin this approach.

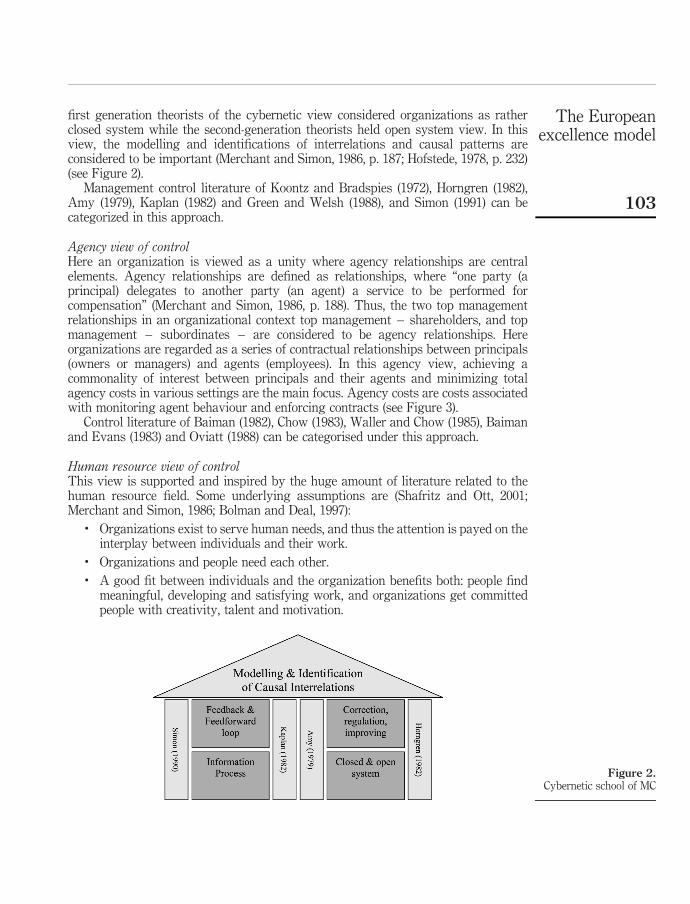

Cybernetic view of controlFrom a cybernetic view, every process of control, i.e. activities for planning, budgeting,performance evaluation, comparison, discovering discrepancies and correction,resource allocation and reward systems are seen from an information processingview and considered as information-based activities. The core idea of the cyberneticview is a system’s self-regulating ability based on feed back loops[3], with theobjectives set in advance, outcomes compared with objectives, and discrepanciesreported to managers for correcting actions (Green and Welsh, 1988). Here detection oferror and correcting actions will take a place as a dynamic process depending on thefeedback loops (Morgan, 1997/1986; Hofstede, 1978).

Concepts of feed forward loops are involved in more advanced cybernetic control ofview, for instance when to evaluate the suitability of the existing rules and todetermine whether it is necessary to redefine the rules and the existing standard. The

Figure 1.Bureaucratic andmechanic school of MC

TQM20,2

102

first generation theorists of the cybernetic view considered organizations as ratherclosed system while the second-generation theorists held open system view. In thisview, the modelling and identifications of interrelations and causal patterns areconsidered to be important (Merchant and Simon, 1986, p. 187; Hofstede, 1978, p. 232)(see Figure 2).

Management control literature of Koontz and Bradspies (1972), Horngren (1982),Amy (1979), Kaplan (1982) and Green and Welsh (1988), and Simon (1991) can becategorized in this approach.

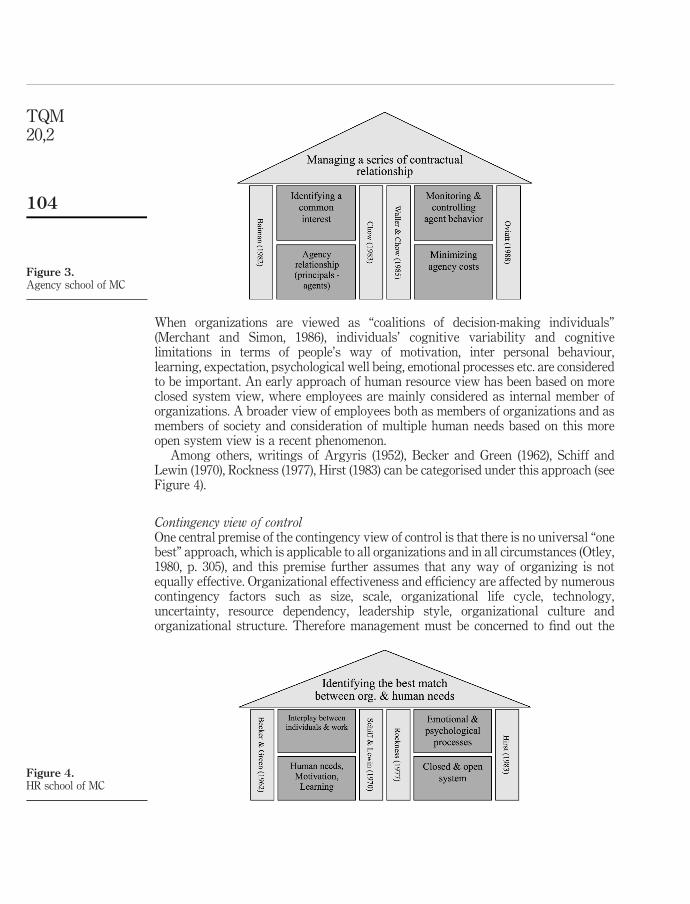

Agency view of controlHere an organization is viewed as a unity where agency relationships are centralelements. Agency relationships are defined as relationships, where “one party (aprincipal) delegates to another party (an agent) a service to be performed forcompensation” (Merchant and Simon, 1986, p. 188). Thus, the two top managementrelationships in an organizational context top management – shareholders, and topmanagement – subordinates – are considered to be agency relationships. Hereorganizations are regarded as a series of contractual relationships between principals(owners or managers) and agents (employees). In this agency view, achieving acommonality of interest between principals and their agents and minimizing totalagency costs in various settings are the main focus. Agency costs are costs associatedwith monitoring agent behaviour and enforcing contracts (see Figure 3).

Control literature of Baiman (1982), Chow (1983), Waller and Chow (1985), Baimanand Evans (1983) and Oviatt (1988) can be categorised under this approach.

Human resource view of controlThis view is supported and inspired by the huge amount of literature related to thehuman resource field. Some underlying assumptions are (Shafritz and Ott, 2001;Merchant and Simon, 1986; Bolman and Deal, 1997):

. Organizations exist to serve human needs, and thus the attention is payed on theinterplay between individuals and their work.

. Organizations and people need each other.

. A good fit between individuals and the organization benefits both: people findmeaningful, developing and satisfying work, and organizations get committedpeople with creativity, talent and motivation.

Figure 2.Cybernetic school of MC

The Europeanexcellence model

103

When organizations are viewed as “coalitions of decision-making individuals”(Merchant and Simon, 1986), individuals’ cognitive variability and cognitivelimitations in terms of people’s way of motivation, inter personal behaviour,learning, expectation, psychological well being, emotional processes etc. are consideredto be important. An early approach of human resource view has been based on moreclosed system view, where employees are mainly considered as internal member oforganizations. A broader view of employees both as members of organizations and asmembers of society and consideration of multiple human needs based on this moreopen system view is a recent phenomenon.

Among others, writings of Argyris (1952), Becker and Green (1962), Schiff andLewin (1970), Rockness (1977), Hirst (1983) can be categorised under this approach (seeFigure 4).

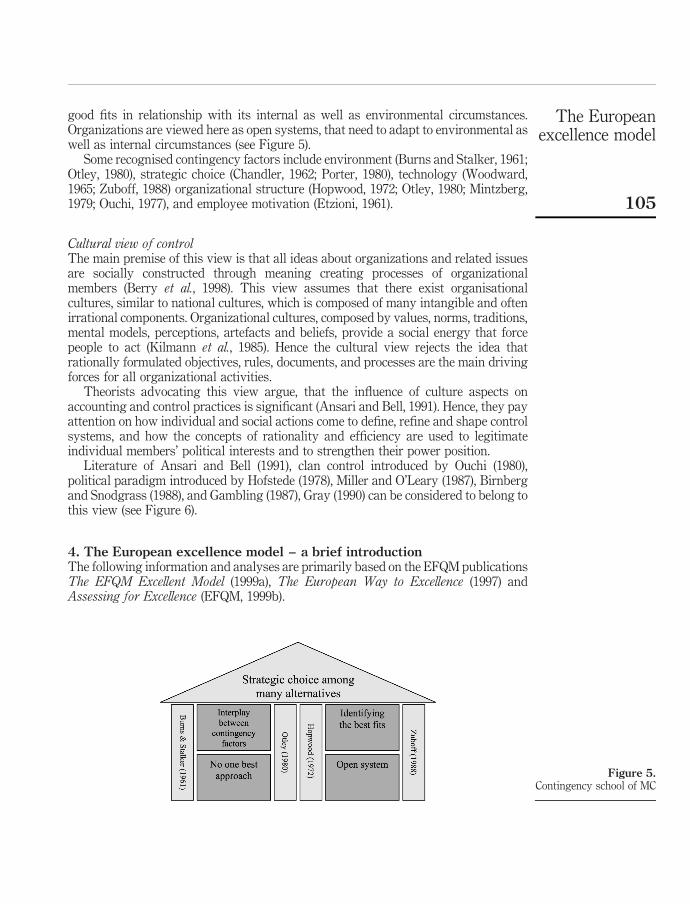

Contingency view of controlOne central premise of the contingency view of control is that there is no universal “onebest” approach, which is applicable to all organizations and in all circumstances (Otley,1980, p. 305), and this premise further assumes that any way of organizing is notequally effective. Organizational effectiveness and efficiency are affected by numerouscontingency factors such as size, scale, organizational life cycle, technology,uncertainty, resource dependency, leadership style, organizational culture andorganizational structure. Therefore management must be concerned to find out the

Figure 4.HR school of MC

Figure 3.Agency school of MC

TQM20,2

104

good fits in relationship with its internal as well as environmental circumstances.Organizations are viewed here as open systems, that need to adapt to environmental aswell as internal circumstances (see Figure 5).

Some recognised contingency factors include environment (Burns and Stalker, 1961;Otley, 1980), strategic choice (Chandler, 1962; Porter, 1980), technology (Woodward,1965; Zuboff, 1988) organizational structure (Hopwood, 1972; Otley, 1980; Mintzberg,1979; Ouchi, 1977), and employee motivation (Etzioni, 1961).

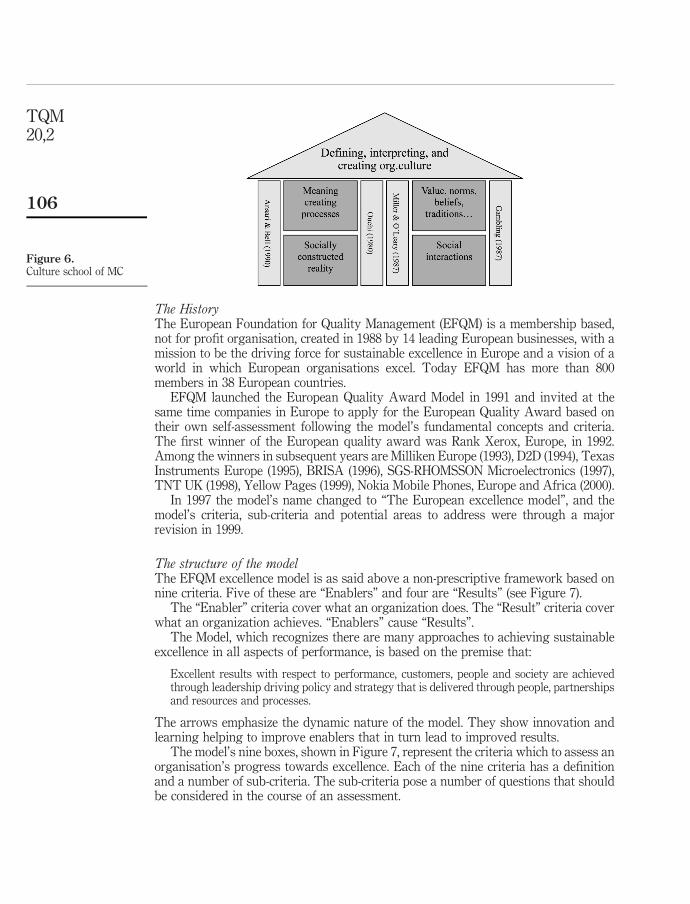

Cultural view of controlThe main premise of this view is that all ideas about organizations and related issuesare socially constructed through meaning creating processes of organizationalmembers (Berry et al., 1998). This view assumes that there exist organisationalcultures, similar to national cultures, which is composed of many intangible and oftenirrational components. Organizational cultures, composed by values, norms, traditions,mental models, perceptions, artefacts and beliefs, provide a social energy that forcepeople to act (Kilmann et al., 1985). Hence the cultural view rejects the idea thatrationally formulated objectives, rules, documents, and processes are the main drivingforces for all organizational activities.

Theorists advocating this view argue, that the influence of culture aspects onaccounting and control practices is significant (Ansari and Bell, 1991). Hence, they payattention on how individual and social actions come to define, refine and shape controlsystems, and how the concepts of rationality and efficiency are used to legitimateindividual members’ political interests and to strengthen their power position.

Literature of Ansari and Bell (1991), clan control introduced by Ouchi (1980),political paradigm introduced by Hofstede (1978), Miller and O’Leary (1987), Birnbergand Snodgrass (1988), and Gambling (1987), Gray (1990) can be considered to belong tothis view (see Figure 6).

4. The European excellence model – a brief introductionThe following information and analyses are primarily based on the EFQM publicationsThe EFQM Excellent Model (1999a), The European Way to Excellence (1997) andAssessing for Excellence (EFQM, 1999b).

Figure 5.Contingency school of MC

The Europeanexcellence model

105

The HistoryThe European Foundation for Quality Management (EFQM) is a membership based,not for profit organisation, created in 1988 by 14 leading European businesses, with amission to be the driving force for sustainable excellence in Europe and a vision of aworld in which European organisations excel. Today EFQM has more than 800members in 38 European countries.

EFQM launched the European Quality Award Model in 1991 and invited at thesame time companies in Europe to apply for the European Quality Award based ontheir own self-assessment following the model’s fundamental concepts and criteria.The first winner of the European quality award was Rank Xerox, Europe, in 1992.Among the winners in subsequent years are Milliken Europe (1993), D2D (1994), TexasInstruments Europe (1995), BRISA (1996), SGS-RHOMSSON Microelectronics (1997),TNT UK (1998), Yellow Pages (1999), Nokia Mobile Phones, Europe and Africa (2000).

In 1997 the model’s name changed to “The European excellence model”, and themodel’s criteria, sub-criteria and potential areas to address were through a majorrevision in 1999.

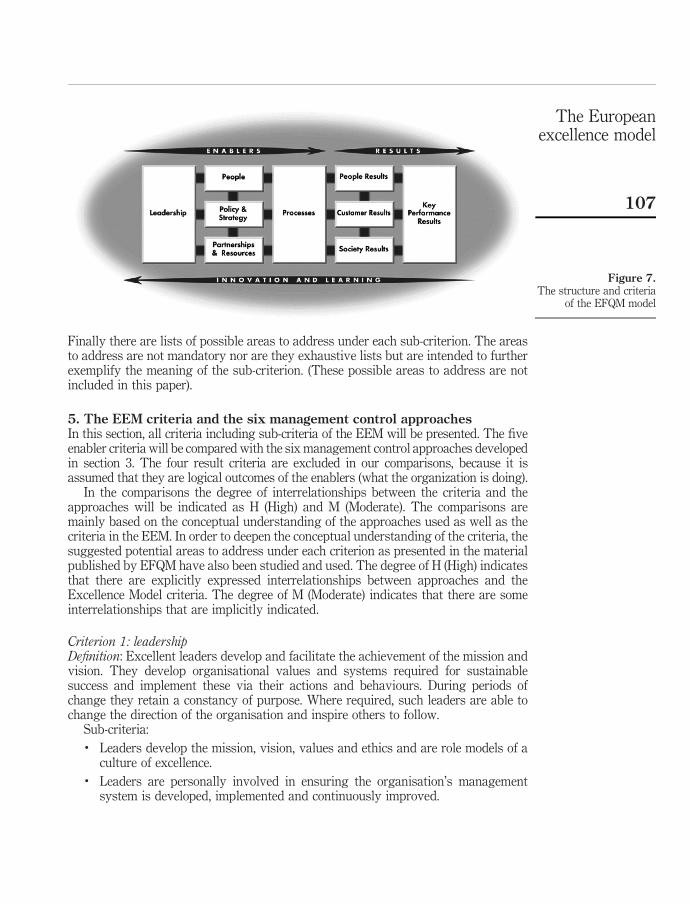

The structure of the modelThe EFQM excellence model is as said above a non-prescriptive framework based onnine criteria. Five of these are “Enablers” and four are “Results” (see Figure 7).

The “Enabler” criteria cover what an organization does. The “Result” criteria coverwhat an organization achieves. “Enablers” cause “Results”.

The Model, which recognizes there are many approaches to achieving sustainableexcellence in all aspects of performance, is based on the premise that:

Excellent results with respect to performance, customers, people and society are achievedthrough leadership driving policy and strategy that is delivered through people, partnershipsand resources and processes.

The arrows emphasize the dynamic nature of the model. They show innovation andlearning helping to improve enablers that in turn lead to improved results.

The model’s nine boxes, shown in Figure 7, represent the criteria which to assess anorganisation’s progress towards excellence. Each of the nine criteria has a definitionand a number of sub-criteria. The sub-criteria pose a number of questions that shouldbe considered in the course of an assessment.

Figure 6.Culture school of MC

TQM20,2

106

Finally there are lists of possible areas to address under each sub-criterion. The areasto address are not mandatory nor are they exhaustive lists but are intended to furtherexemplify the meaning of the sub-criterion. (These possible areas to address are notincluded in this paper).

5. The EEM criteria and the six management control approachesIn this section, all criteria including sub-criteria of the EEM will be presented. The fiveenabler criteria will be compared with the six management control approaches developedin section 3. The four result criteria are excluded in our comparisons, because it isassumed that they are logical outcomes of the enablers (what the organization is doing).

In the comparisons the degree of interrelationships between the criteria and theapproaches will be indicated as H (High) and M (Moderate). The comparisons aremainly based on the conceptual understanding of the approaches used as well as thecriteria in the EEM. In order to deepen the conceptual understanding of the criteria, thesuggested potential areas to address under each criterion as presented in the materialpublished by EFQM have also been studied and used. The degree of H (High) indicatesthat there are explicitly expressed interrelationships between approaches and theExcellence Model criteria. The degree of M (Moderate) indicates that there are someinterrelationships that are implicitly indicated.

Criterion 1: leadershipDefinition: Excellent leaders develop and facilitate the achievement of the mission andvision. They develop organisational values and systems required for sustainablesuccess and implement these via their actions and behaviours. During periods ofchange they retain a constancy of purpose. Where required, such leaders are able tochange the direction of the organisation and inspire others to follow.

Sub-criteria:. Leaders develop the mission, vision, values and ethics and are role models of a

culture of excellence.. Leaders are personally involved in ensuring the organisation’s management

system is developed, implemented and continuously improved.

Figure 7.The structure and criteria

of the EFQM model

The Europeanexcellence model

107

. Leaders interact with customers, partners and representatives of society.

. Leaders reinforce a culture of excellence with the organisation’s people.

. Leaders identify and champion organisational change.

. According to Table I it is clear that the dominating approaches or paradigmsbehind the main driver for “excellence” – Leadership – are the Cultural Viewand the Human Resource view of control.

Criterion 2: policy and strategyDefinition: Excellent organisations implement their mission and vision by developing astakeholder focused strategy that takes account of the market and sector in which itoperates. Policies, plans, objectives and processes are developed and deployed todeliver the strategy.

Sub-criteria:. Policy and strategy are based on the present and future needs and expectations

of stakeholders.. Policy and strategy are based on information from performance measurement,

research, learning and external related activities.. Policy and strategy are developed, reviewed and updated.. Policy and strategy are communicated and deployed through a framework of key

processes.

As seen from Table II, the two approaches, which seem to dominate the Policy andStrategy criterion, are the cybernetic approach and the contingency approach.As said above one central premise of the contingency view of control is that there is nouniversal “one best” approach applicable to all organizations and in all circumstances.Therefore management must be concerned to find out the good fits in relationship withits internal as well as environmental circumstances. The first two sub-criteria areexplicitly concerned on this issue.

From a cybernetic view, every process of control, i.e. activities for planning,budgeting, performance evaluation, comparison, discovering discrepancies and

Bureaucratic Cybernetic AgencyHumanresource Contingency Culture

M H M H

Notes: H ¼ High; M ¼ Moderate

Table I.Interrelationshipsbetween leadershipcriteria and the sixmanagement controlapproaches

Bureaucratic Cybernetic AgencyHumanresource Contingency Culture

M H M M H

Notes: H ¼ High; M ¼ Moderate

Table II.Interrelationshipsbetween policy andstrategy criteria and thesix management controlapproaches

TQM20,2

108

correction, resource allocation and reward systems are seen from an informationprocessing view and considered as information-based activities. The core idea of thecybernetic view is a system’s self-regulating ability based on both negative feedbackloops and feed forward loops. All sub-criteria reflect more or less the importance ofinformation flow and information based activities.

The problem here, as we see it, is how to balance these two dominating approaches?There seems to be a risk that the rational and top-down expert oriented cyberneticapproach will be the dominating approach when deciding on the strategies, policies,and overall goals, and also in the policy deployment process. When considering thatthere was no interrelationship identified concerning the cultural approach, this riskseems obvious.

Criterion 3: peopleDefinition: Excellent organisations manage, develop and release the full potential oftheir people at an individual, team-based and organisational level. They promotefairness and equality and involve and empower their people. They care for,communicate, reward and recognise, in a way that motivates staff and buildscommitment to using their skills and knowledge for the benefit of the organisation.

Sub-criteria:. People resources are planned, managed and improved.. People’s knowledge and competencies are identified, developed and sustained.. People are involved and empowered.. People and the organisation have a dialogue.

As seen from Table III, the two dominant approaches are the human resource approachand the cultural approach. We find that logical and consistent with the dominatingapproaches behind the Leadership Criterion. The fourth sub-criteria focusing on thenecessity of dialogue between people and organization is interpreted here as beingrelated to the agency approach, hence the interrelationship is indicated as M(moderate). Cybernetic approach is identified both in the first and second sub-criteria,because we interpreted that improvement of people resource and peoples’ knowledgeas well as competencies are only possible when the organizations systematicallymeasure and collect information concerning on these factors. As we regard the peoplecriterion to be one of the most important contingency factors, the interrelationship onthis approach is defined to be M (Moderate).

Criterion 4: partnerships and resourcesDefinition: Excellent organisations plan and manage external partnerships, suppliersand internal resources in order to support policy and strategy and the effective

Bureaucratic Cybernetic AgencyHumanresource Contingency Culture

M M H M H

Notes: H ¼ High; M ¼ Moderate

Table III.Interrelationships

between people criteriaand the six management

control approaches

The Europeanexcellence model

109

operation of processes. During planning and whilst managing partnerships andresources they balance the current and future needs of the organisation, the communityand the environment.

Sub-criteria:. External partnerships are managed.. Finances are managed.. Buildings, equipment and materials are managed.. Technology is managed.. Information and knowledge are managed.

As seen from Table IV, the dominating approach behind this criterion is the cyberneticapproach. We find that logical in relation to the management of finances, buildings,technology etc., i.e. in relation to management of hardware, but in relation to themanagement of external partnerships, and also to management of information andknowledge we do not find it logical. Here we need other approaches and assumptions,which can take part on more software including the informal dimension. The cultureand human resource approaches seem to have been neglected in these relationships.

Criterion 5: processesDefinition: Excellent organisations design, manage and improve processes in order tofully satisfy, and generate increasing value for, customers and other stakeholders.

Sub-criteria:. Processes are systematically designed and managed.. Processes are improved, as needed, using innovation in order to fully satisfy and

generate increasing value for customers and other stakeholders.. Products and services are designed and developed based on customer needs and

expectations.. Products and services are produced, delivered and serviced.. Customer relationships are managed and enhanced.

Here the dominating approach seems to be the Cybernetic (see Table V), while nointerrelationships are identified regarding the Culture approach. In order to havesuccess with process management including process improvements, creating anorganizational culture based on empowerment and trust are critical success factors,and these critical success factors do not seem to be presented here.

The dominating cybernetic view can be seen as an overly rational approach, whichfocuses and emphasizes the formal aspects of organizations. Here every process ofcontrol, i.e. activities for planning, budgeting, performance evaluation, comparison,

Bureaucratic Cybernetic AgencyHumanresource Contingency Culture

M H M M

Notes: H ¼ High; M ¼ Moderate

Table IV.Interrelationshipsbetween partnership andresources criteria and thesix management controlapproaches

TQM20,2

110

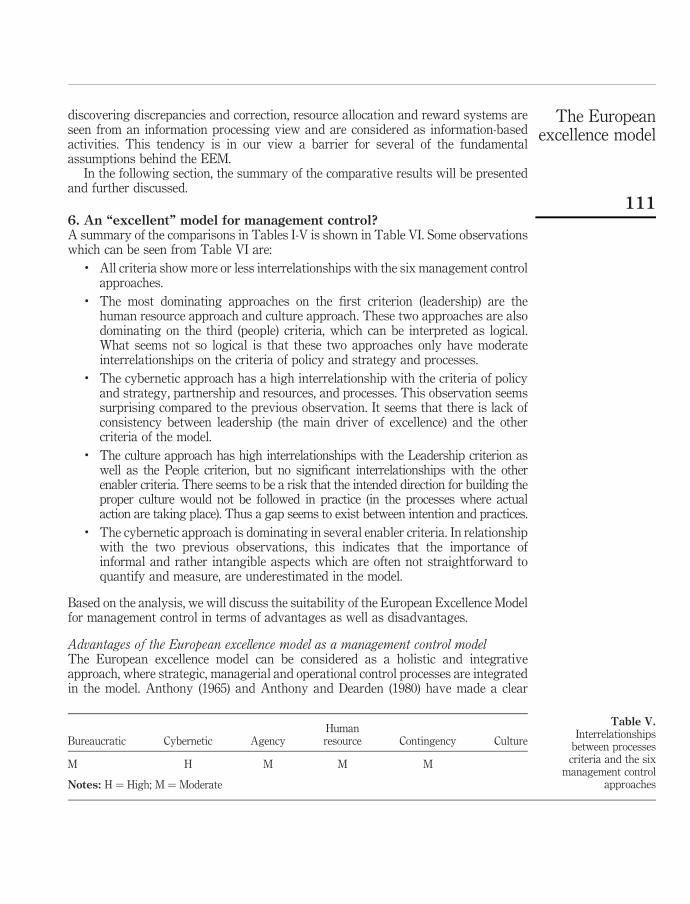

discovering discrepancies and correction, resource allocation and reward systems areseen from an information processing view and are considered as information-basedactivities. This tendency is in our view a barrier for several of the fundamentalassumptions behind the EEM.

In the following section, the summary of the comparative results will be presentedand further discussed.

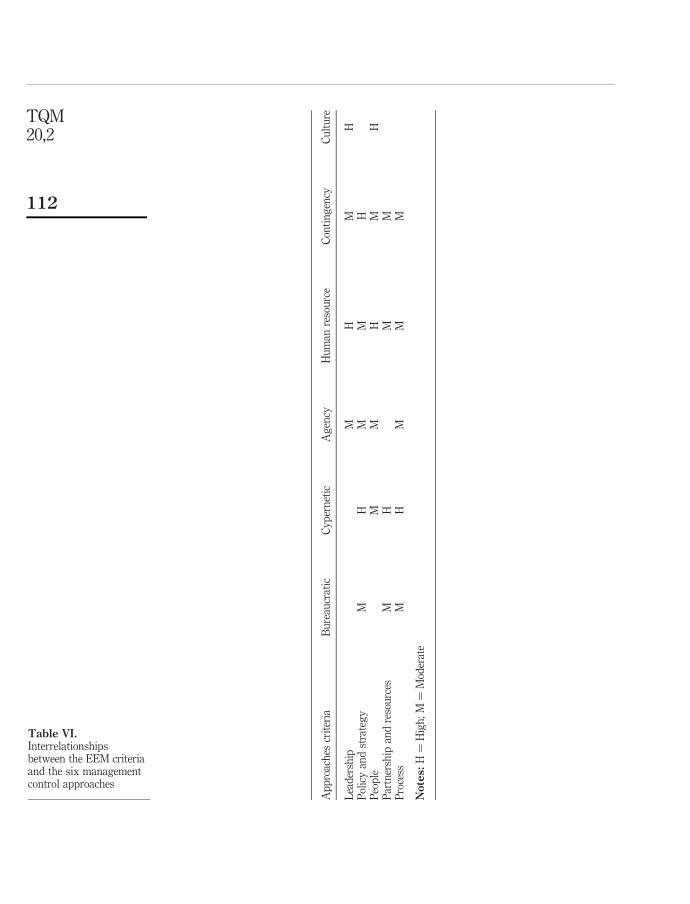

6. An “excellent” model for management control?A summary of the comparisons in Tables I-V is shown in Table VI. Some observationswhich can be seen from Table VI are:

. All criteria show more or less interrelationships with the six management controlapproaches.

. The most dominating approaches on the first criterion (leadership) are thehuman resource approach and culture approach. These two approaches are alsodominating on the third (people) criteria, which can be interpreted as logical.What seems not so logical is that these two approaches only have moderateinterrelationships on the criteria of policy and strategy and processes.

. The cybernetic approach has a high interrelationship with the criteria of policyand strategy, partnership and resources, and processes. This observation seemssurprising compared to the previous observation. It seems that there is lack ofconsistency between leadership (the main driver of excellence) and the othercriteria of the model.

. The culture approach has high interrelationships with the Leadership criterion aswell as the People criterion, but no significant interrelationships with the otherenabler criteria. There seems to be a risk that the intended direction for building theproper culture would not be followed in practice (in the processes where actualaction are taking place). Thus a gap seems to exist between intention and practices.

. The cybernetic approach is dominating in several enabler criteria. In relationshipwith the two previous observations, this indicates that the importance ofinformal and rather intangible aspects which are often not straightforward toquantify and measure, are underestimated in the model.

Based on the analysis, we will discuss the suitability of the European Excellence Modelfor management control in terms of advantages as well as disadvantages.

Advantages of the European excellence model as a management control modelThe European excellence model can be considered as a holistic and integrativeapproach, where strategic, managerial and operational control processes are integratedin the model. Anthony (1965) and Anthony and Dearden (1980) have made a clear

Bureaucratic Cybernetic AgencyHumanresource Contingency Culture

M H M M M

Notes: H ¼ High; M ¼ Moderate

Table V.Interrelationships

between processescriteria and the six

management controlapproaches

The Europeanexcellence model

111

Ap

pro

ach

escr

iter

iaB

ure

aucr

atic

Cy

per

net

icA

gen

cyH

um

anre

sou

rce

Con

tin

gen

cyC

ult

ure

Lea

der

ship

MH

MH

Pol

icy

and

stra

teg

yM

HM

MH

Peo

ple

MM

HM

HP

artn

ersh

ipan

dre

sou

rces

MH

MM

Pro

cess

MH

MM

M

Notes:

H¼

Hig

h;

M¼

Mod

erat

e

Table VI.Interrelationshipsbetween the EEM criteriaand the six managementcontrol approaches

TQM20,2

112

distinction between these three different control processes, where the managementcontrol process is rather narrowly defined without integrating other processes.However, several theorists (see Berry et al., 1998; Lowe and Puxty, 1989; Simon, 1991)argue for the necessity of a more integrated and a holistic management control viewseen from a system perspective. The excellence model incorporates the three differentcontrol processes as interrelated enablers. The strategic planning is explicitlyincorporated in the criterion of policy and strategy, the operational control is explicitlyincorporated in the process criterion, and the management control is embedded in allfour enabler criteria.

The excellence model’s integrative and holistic character can be supported byanother fact, observed in our analysis. As observed through the previous sections,elements of all six management control approaches are more or less incorporated in theexcellence model.

Another advantage of the model is the linkage between the various enabler criteria(leadership, people, policy and strategy, partnerships and resources and processes) andthe result criteria concerned with the achievement of organizational goals in terms ofpeople results, customer results, society results and key performance result criteria.The cause and effect relationships are clearly indicated in a dynamic process orientedsystem model. In addition, the cause and effect relationship is grounded in ideas aboutthe generation, processing and feedback mechanisms of information. Through theenabler criteria, information is expected to be generated and processed. The resultcriteria in terms of people and customer satisfaction, impact on society as well asbusiness results are expected to be utilised as feed forward loops in an ongoingprocess, and in this way, it is assumed to increase learning and improvement activitiesby reassessing goals, strategies and standards in the enabler criteria. Utilising bothfeedback and feed-forward loops in correcting, maintaining and improvingorganisational performances can be seen as a good usage of the cybernetic approachas it incorporates both the first and second generation of cybernetic ideas. The firstgeneration of cybernetic ideas in terms of feedback loop for correcting and maintainingthe current standards (morphostasis) and the second generation of cybernectic in termsof feedforward loop for improving and setting a new standard (morphogenesis).

Seen from a system approach, the model is based on an open system theory, whichfully recognises the importance of interaction between organisation and theenvironment in a broad sense.

Limitations and disadvantages of the EEMAs observed in the summary (Table VI), the model is based on the structure, modelcriteria and the eight fundamental concepts (see section 3), and these frameworks canbe a hindrance to accept and consider other alternative possibilities to achieveexcellence. Although the model is relatively complex, the model does not encompass allpossible variables. A model is in its nature always a simplified and generalised versionof a reality. Thus it cannot cover all aspects of real situation. Further the law ofrequisite variety (Ashby, 1963; Morgan, 1997/1986) warns us that any system’sinternal complexity and diversity level should correspond or match to the complexityand variety of its environments if the system shall deal challenges. It is then almostobvious that a simple model will not be able to cope the complexity of a system withhigh degree of uncertainty and unpredictability.

The Europeanexcellence model

113

Clear indications of cause and effect relationships in terms of enabler and resultscriteria may be questioned. Furthermore the model pays little attention tocontextual/contingency factors. For instance, the right approaches to implement mayvary depending on numerous contingency factors such as organizations size, age,business fields, maturity and motivation levels of employees, educational background ofemployees, organizational culture, speed of change in markets and customer demands etc.

The inconsistency between intention and practices discussed previously can be aproblem, when adopting the model. The inconsistency is observed between leadershipintention and the practices (processes), in particular. The culture aspect in terms ofvalue, vision and mission building was explicitly focused under Leadership, while thisfocus was more or less ignored in policy and strategy, partnership and resources aswell as in the process criterion. These inconsistencies seem to be a major defect of themodel and may have been the reason for many companies’ problems withimplementing the model as an overall framework for strategic planning andimprovement of the business. Political, psychological, and other behaviour resistanceswhich cause high failure rates in relationship with implementation of quality systemmay partly be connected to the inconsistencies between leadership intention and thepractices (processes). As a human being is basically also a political being, power andpolitical aspects together with psychological aspect have to be recognised and bethoroughly treated within the frameworks of quality management. Continuous“ignoring” these aspects, there will be continuous high rates of failures. Also in relationto an award approach these inconsistencies seem to be a major problem both forcompanies applying for the European Quality Award and for the examiners.

7. Conclusions and questions for further researchThrough this paper management control theories are examined in relationship with theEEM. We have further investigated whether the EEM is comparable to the currentthinking within management control theories. Based on the analysis, adaptability ofthe model as a management control model was examined by identifying anddiscussing advantages as well as disadvantages of the model.

Despite the recognized limitations and disadvantages of the EEM, we consider thatthe model may be a useful management control model as a guiding framework. Myrecommendation is that the best strategy for using the model as a management controlmodel is “adaptation” rather than “adoption”. This is the same conclusion, whichDahlgaard and Dahlgaard-Park (2006) came to after having compared the EEM’s criteriawith the critical success factors for innovation and new product development identifiedthrough a comprehensive literature review. Through this comparison it was obvious thatseveral major critical success factors were not addressed in the EEM. Hence beforeapplying the EEM for improving innovation and new product development it isrecommended to be critical first and to use all existing knowledge and experiences torevise the model so that it better fits with the given context. This is called adaptation.

Another recommendation for overcoming the limitation of the model is tosupplement with other approaches, for instance the four Ps (People, Partnership,Processes and Products/services) and the four aspects of organizational realities, seeTable VII (Dahlgaard-Park and Dahlgaard, 2006, 2007). In this approachorganisational realities are understood as a dynamic interplay and mutualinterrelationship between the micro-macro and the subjective-objective aspects.

TQM20,2

114

When we combine the EEM with this approach much of the problems caused by anoversimplification can be overcome as the four aspects and their interrelationshipsreflect the very complex nature of the organisational reality.

When we analyse EEM in relationship with the four organizational realities, it isalso obvious that EEM focuses on the macro-objective aspects of organisationalrealities and very little attention is paid to other aspects. This is another way toillustrate some possible reasons for high implementation failure rates of the EEM andquality management in general.

If organizations are aware of the limitations, inconsistencies and the risks connectedwith the application of the model, they may be able to overcome the problemsmentioned above.

As far as the literature review is concerned, there is no model from the area ofmanagement control, which is compatible to the EEM. Parallel with the launch andapplication of the EEM (1991) a considerable number of theoreticians and companieshave made efforts in adopting and integrating the balanced scorecard model (Kaplanand Norton, 1992, 1996) as a management control model.

The strength of the balanced scorecard is its simplicity, which maybe is the mainreason for its growing popularity all over the world. Its simplicity makes the balancedscorecard easy to understand and hence easy to communicate to people at all levels fromtop management to middle management and to the “shop floor level”. People understandeasily and accept that objectives (critical success factors), measures (key performanceindicators) and targets have to be established for each of the four perspectives of themodel (financial, customer, process and learning/growth). Its weakness is that it is noteasy to understand the linkages and hence the cause-effect relationships between the

Subjective/intangible Objective/tangible

Micro/individual Individual feelings, perceptions,assumptions, values, thoughts,intentions and will, beliefs, motives,meaning creations, desires, motivation,commitment, loyalty (Buildingleadership, Building people, Buildingpartnership)

Individuals’ patterns of behaviourLeadership behaviour and patternsPatterns of interactionsPatterns of partnershipIndividual workIndividual work performance (Buildingleadership, Building people, Buildingpartnership, Building processes)

Macro/collective Groups, departmental andorganizational norms, values, politicalinterest, power relationships, informalpower structure, conflicts,interpersonal-, inter group meaningcreations (Building leadership,Building people, Building partnership)

Vision, mission statement, Symbols,Ceremony, Traditions, Patterns of intergroup/inter departmental interactionand partnership, Patterns of interorganizational partnership, Groups,departmental and organizational workprocesses, Training and educationprogrammes, Rules, Techniques,Communication channel, Structures,Manuals, Technology, Routines,Products (Building Leadership,Building People, Building Partnership,Building Processes, Building Products)

Table VII.The four aspects of

organizational realities

The Europeanexcellence model

115

objectives (CSF), measures (KPI) and targets of the four perspectives. Thisunderstanding is important when implementing and using the balanced scorecard forcontrolling and improving daily operations. For that purpose a more detailed model isneeded such as the EEM shown in Figure 1. So the balanced scorecard is considered asless applicable as a management control model than the European excellence model.

The analysis and summary presented in section 5 and 6 are based on comparisons ofthe definitions, concepts and approaches of management control (section 2 and 3) and thefundamental concepts, structure and criteria of the EEM (section 4 and 5). In this way, wecan say that the conclusions are based on a systematic desk research approach, which ofcourse has its limitations. Hence further research is needed in order to supplement thetheoretical approach in this report with a collection of empirical evidence on:

. How various “ordinary” companies and award winning companies are using theEFQM excellence model as a management control model?

. Why they are using the model the way they are doing?

. What are major problems when using the model in a real set?

This paper is the first step in starting such a research project.

Notes

1. Frameworks, schools of thought, models, perspectives are some corresponding terms to theterm of paradigm (see more about paradigm – Kuhn, 1970; Burrell and Morgan, 1979;Morgan, 1997/1986; Scott, 2003, Dahlgaard-Park, 2002).

2. Anthony and Dearden (1980) made distinction between the two concepts of goals andobjectives. The concept of goals are used as overall aims of the organization in a broad term,while the concept of objectives are used as the more specific statements of plannedaccomplishments in a given time period.

3. Feed back loops assume that the system has capabilities to set goals, measure performance,compare performance with the goals (the standard), feed back information about negativediscrepancies into the process and take corrective actions in order to reduce discrepancies inthe future. Feed forward loops assume that interventions are programmed in advance andthe goals (standards) are continuously candidates for questioning and change.

References

Amy, L.R. (1979), Budget Planning and Control Systems, Pitman, London.

Ansari, S.L. and Bell, J. (1991), “Symbolism, collectivism and rationality in organisationalcontrol”, Accounting, Auditing & Accountability Journal, Vol. 4, pp. 4-27.

Anthony, R. (1965), Planning and Control System: Framework for Analysis, Harvard UniversityPress, Boston, MA.

Anthony, R.N. and Dearden, J. (1980), “The nature of management control”, Management ControlSystem, Irwin, Homewood, IL, pp. 3-20.

Anthony, R.N. and Govindarajan, V. (2001), Management Control Systems, MacGraw-Hill,Boston, MA.

Argyris, C. (1952), The Impact of Budgets on People, The Controllership Foundation, Ithaca, NY.

Ashby, W.R. (1963), Introduction to Cybernetics, John Wiley & Sons, New York, NY.

Baiman, S. (1982), “Agency research in managerial accounting: a survey”, Journal of AccountingLiterature, Spring.

TQM20,2

116

Baiman, S. and Evans, J.H. (1983), “Pre-decision information and participative managementcontrol systems”, Journal of Accounting Research, Autumn, pp. 371-95.

Becker, S. and Green, D. (1962), “Budgeting and employee behavior”, Journal of Business,October, pp. 392-402.

Berry, A.J., Broadbent, J. and Otley, D.T. (Eds) (1998), Management Control Theory, Ashgate,Aldershot.

Birnberg, J. and Snodgrass, C. (1988), “Culture and control: a field study”, Accounting,Organizations and Society, Vol. 13 No. 5, pp. 447-64.

Bolman, L.G. and Deal, T.E. (1997), Reframing Organizations: Artistry, Choice, and Leadership,Jossey-Bass, San Francisco, CA.

Burns, T. and Stalker, G.M. (1961), The Management of Innovation, Tavistock, London.

Burrell, G. and Morgan, G. (1979), Sociological Paradigms and Organizational Analysis,Heinemann, London.

Chandler, A. (1962), Strategy and Structure, MIT Press, Cambridge, MA.

Chow, C.W. (1983), “The effects of job standard difficulty and compensation schemes onperformance: an exploration of linkages”, Accounting Review, October, pp. 667-85.

Church, A.H. (1914), “The science and practice of management”, Engineering Magazine, pp. 44-5.

Daft, R.L. (2001), Organization Theory and Design, South-Western. Thomson Learning, London.

Dahlgaard, J.J. and Dahlgaard-Park, S.M. (2006), Measuring and Diagnosing InnovationExcellence, Proceedings of the 9th Int. QMOD Conference, 8-10 August 2006, Liverpool.

Dahlgaard-Park, S.M. (1999), “The evolution patterns of quality management”, Total QualityManagement, Vol. 10 No. 4, pp. 473-80.

Dahlgaard-Park, S.M. (2002), The Human Dimension in TQM Training, Learning andMotivation, Linkoping University Press, Linkoping.

Dahlgaard-Park, S.M. (2006), “Consistency and transformation in the quality movement”, TheTQM Magazine, Vol. 18 No. 3.

Dahlgaard-Park, S.M. and Dahlgaard, J.J. (2006), “In search of excellence – past, present andfuture”, in Schnauber, H. (Ed.), Kreativ und Konsequent, Vol. Ch. 6, Carl Hanser, Munchen,pp. 57-84.

Dahlgaard-Park, S.M. and Dahlgaard, J.J. (2007), “Excellence – 25 years evolution”, Journal ofManagement History, Vol. 13 No. 4, pp. 371-93.

Dahlgaard-Park, S.M., Bergman, B. and Hellgren, B. (2001), “Reflection on TQM for the newmillennium (1)”, in Sinha, M. (Ed.), The Best on Quality, Vol. 12, ASQ Quality Press,Milwaukee, WI, pp. 279-311.

Diemer, H. (1915), Industrial Organization and Management, La Salle Extention University,Chicago, IL.

EEM (1991), available at: www.wfqm.org

European Foundation for Quality Management (EFQM) (1999a), The EFQM Excellence Model,European Foundation for Quality Management, Brussels.

European Foundation for Quality Management (EFQM) (1999b), Assessing for Excellence: A PracticalGuide for Self-Assessment, European Foundation for Quality Management, Brussels.

EFQM (2003), Introducing Excellence, available at: www.efqm.org

Emmerson, H. (1912), “The twelve principles of efficiency”, Engineering Magazine, Vol. 39-41.

Etzioni, A. (1961), A Comparative Analysis of Complex Organizations, Free Press, New York, NY.

The Europeanexcellence model

117

Fayol, H. (1916/1949), General and Industrial Management, Pitman, London.

Gambling, T. (1987), “Accounting for rituals”, Accounting, Organizations and Society, Vol. 12No. 4, pp. 319-30.

Gray, B. (1990), “The enactment of management control systems: a critique of Simon”,Accounting, Organizations and Society, Vol. 15, pp. 145-8.

Green, S.G. and Welsh, M.A. (1988), “Cybernetics and dependents: reframing the controlconcepts”, Academy of Management Review, Vol. 13, pp. 287-301.

Hirst, M.K. (1983), “Reliance on performance measures, task uncertainty, and dysfunctionalbehaviour: some extensions”, Journal of Accounting Research, Autumn, pp. 596-605.

Hofstede, G. (1978), “The poverty of management control philosophy”, Academy of ManagementReview, Vol. 3, pp. 450-61.

Hopwood, A.G. (1972), “An empirical study of the role of accounting data in performanceevaluation, empirical research in accounting”, Journal of Accounting Research, pp. 156-82.

Horngren, C.T. (1982), Cost Accounting: A Managerial Emphasis, 5th ed., Prentice-Hall,Englewood Cliffs, NJ.

Kaplan, R.S. (1982), Advanced Management Accounting, Prentice-Hall, Englewood Cliffs, NJ.

Kaplan, R.S. and Norton, D.P. (1992), “The balanced scorecard – measures that driveperformance”, Harvard Business Review, Vol. 39, pp. 71-9.

Kaplan, R.S. and Norton, D.P. (1996), The Balanced Scorecard: Translating Strategy into Action,Harvard Business School Press, Boston, MA.

Kilmann, R.H., Saxton, M.J. and Serpa, R. (Eds) (1985), Gaining Control of the Corporate Culture,Jossey-Bass, San Francisco, CA.

Koontz, H. and Bradspies, R.W. (1972), “Managing through feedforward control”, BusinessHorizons, June, pp. 25-36.

Kuhn, T.S. (1970), The Structure of Scientific Revolutions, University of Chicago Press, Chicago.

Lowe, T. and Machin, J.L. (1987), New Perspectives on Management Control, Macmillan, NewYork, NY.

Lowe, T. and Puxty, T. (1989), “The problems of a paradigm: a critique of the prevailingorthodoxy in management control”, in Wai Fong Chua, Lowe, T. and Puxty, T. (Eds),Critical Perspectives in Management Control, Macmillan Press, Basingstoke, pp. 9-26.

Merchant, K.A. (1985), Control in Business Organizations, Pitman, Marshfield, MA.

Merchant, K.A. and Simon, R. (1986), “Research and control in complex organizations: anoverview”, Journal of Accounting Literature, Vol. 5, pp. 183-203.

Miller, P. and O’Leary, T. (1987), “Accounting and the construction of the governable person”,Accounting, Organizations and Society, Vol. 12, pp. 235-65.

Mintzberg, H. (1979), The Structuring of Organizations, Prentice-Hall, Englewood Cliffs, NJ.

Morgan, G. (1997/1986), 1986) Images of Organization, Sage, Thousand Oaks, CA.

Otley, D. (1980), “The contingency theory of management accounting: achievement andprognosis”, Accounting, Organizations and Society, Vol. 5 No. 4, pp. 413-28.

Ouchi, W.G. (1977), “The relationship between organizational structure and organizationalcontrol”, Administrative Science Quarterly, Vol. 22, pp. 95-113.

Ouchi, W.G. (1980), “Markets, bureaucracies, and clans”, Administrative Science Quarterly,Vol. 25, pp. 129-41.

TQM20,2

118

Oviatt, B.M. (1988), “Agency and transaction cost perspectives on the manager-shareholderrelationship: incentives for congruent interests”, Academy of Management Review, Vol. 13,pp. 214-25.

Porter, M. (1980), Competitive Strategy, Free Press, New York, NY.

Rockness, H.O. (1977), “Expectancy theory in a budgetary setting: an experimental evaluation”,The Accounting Review, October, pp. 893-903.

Schiff, M. and Lewin, A.Y. (1970), “The impact of people on budgets”, The Accounting Review,Vol. 45, pp. 259-68.

Scott, R. (2003), Organizations Rational, Natural and Open Systems, Prentice-Hall, London.

Scott, W.R. and Cole, R.E. (1999), “The quality movement and organization theory”, The QualityMovement & Organization Theory, Sage Publications, London.

Shafritz, J.M. and Ott, J.S. (Eds) (2001), Classics of Organization Theory, Harcourt, London.

Simon, R. (1991), “Strategic organizations and top management attention to control systems”,Strategic Management Journal, Vol. 12.

Waller, W.S. and Chow, C.W. (1985), “The self-selection and effort effects of standard-basedemployee controls: a framework and some empirical evidence”, The Accounting Review,July, pp. 458-76.

Woodward, J. (1965), Industrial Organization: Theory and Practice, Oxford University Press,London.

Zuboff, R. (1988), In The Age of The Smart Machine, Basic Books, New York, NY.

Further reading

Koontz, H.D. and O’Donnell, C.J. (1972), Principles of Management: An Analysis of ManagerialFunctions, McGraw-Hill, New York, NY.

About the authorSu Mi Dahlgaard-Park Lic. Econ., Dr. Phil., is currently Research Director and Professor atInstitute of Service Management, Lund University, Sweden. Her research areas have been humanresource management, quality management, organization theory, learning and knowledgemanagement, and organizational change. Within these areas she has published more than 100research papers and books. She has received several awards for her research, teaching andpublications, among others, Emerald Literati Award for outstanding paper. She is anacademician of IAQ (International Academy for Quality); co-founder and co-chair of theInternational QMOD (Quality Management and Organizational Development) Conference duringthe last ten years; member of editorial boards in scientific journals of TQM Magazine, EuropeanQuality, International Journal of Management History, The Asian Journal of Quality, Euro AsianJournal of Management and Chinese Management Studies. She is a frequent keynote speaker atconferences, universities and organizations throughout the world. Su Mi can be contacted at:[email protected]

The Europeanexcellence model

119

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints