Embed Size (px)

Citation preview

Town of Black Mountain

Adopted Budget

Fiscal Year 2010-2011 (FY10-11)

Carl Bartlett, Mayor

Joan Brown, Vice Mayor

Ruth Brandon, Alderman

Tim Rayburn, Alderman

Carlos Showers, Alderman

C. Michael Sobol, Alderman

Marcia D. Onieal, Town Manager

Rick Shreve, Finance & Information Services Director

Town of Black Mountain

Adopted Budget

Fiscal Year 2010-2011 (FY10-11)

TABLE OF CONTENTS

BUDGET MESSAGE Section

Quick Guide to the Adopted Budget page 1 Budget Message page 2 FY10-11 Budget Ordinance page 15 Summary of Changes page 19 Total Funds Budget Summary page 20

GENERAL FUND Section

General Fund Budget Summary page 23 General Fund Revenues Summary page 26 Governing Board page 28 Administration Department page 30 Public Buildings Unit page 32 Police Department page 34 Fire Department page 36 Planning Department page 38 Public Services – Administration Division page 40 Public Services – Streets Division page 42 Public Services – Powell Bill Division page 44 Public Services – Sanitation Division page 46 Recreation & Parks Department page 48

WATER FUND Section

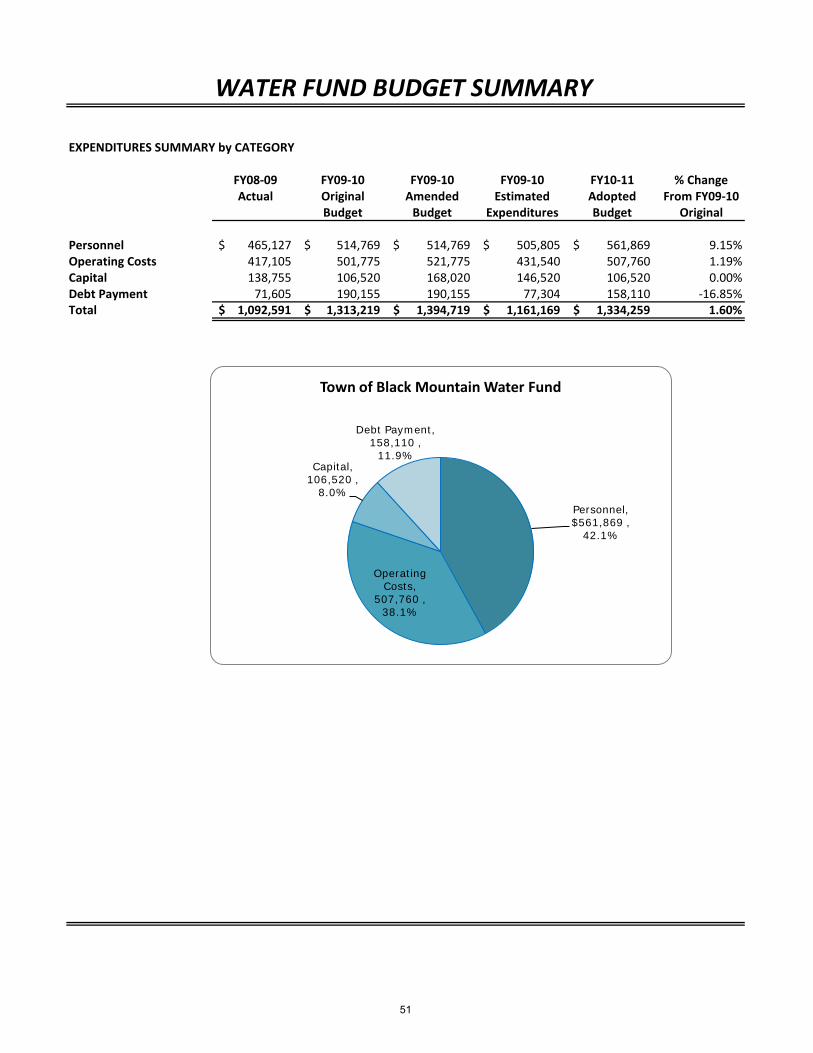

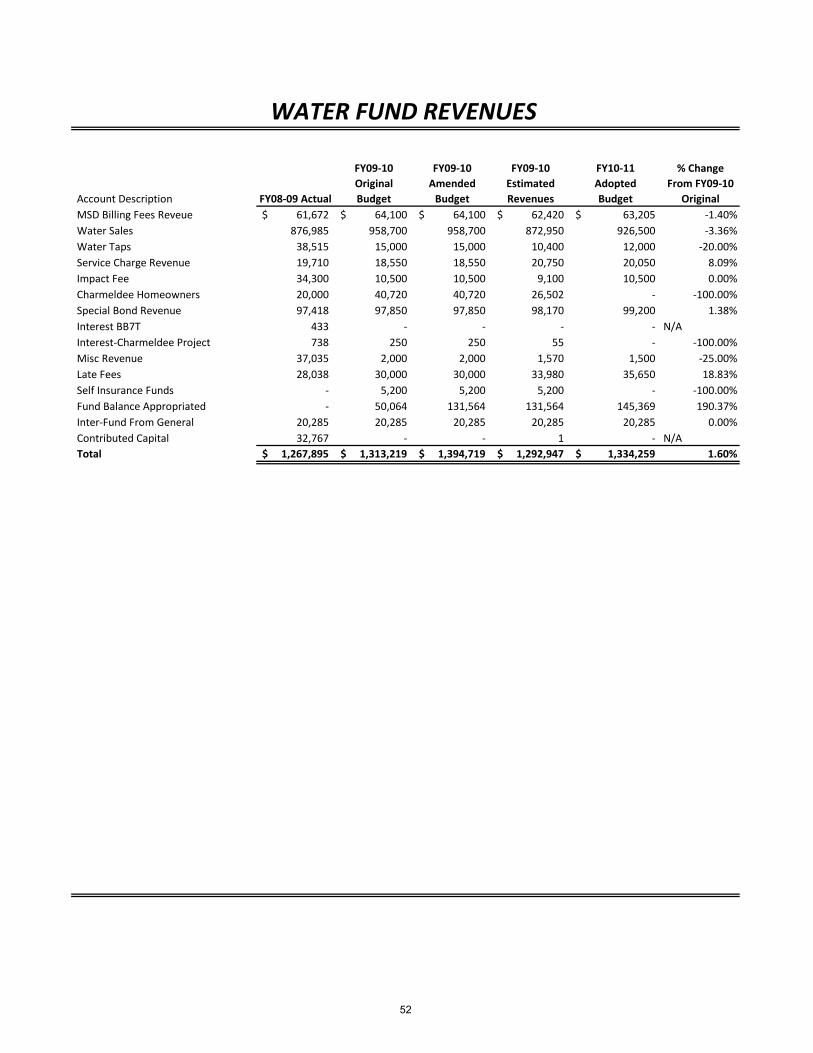

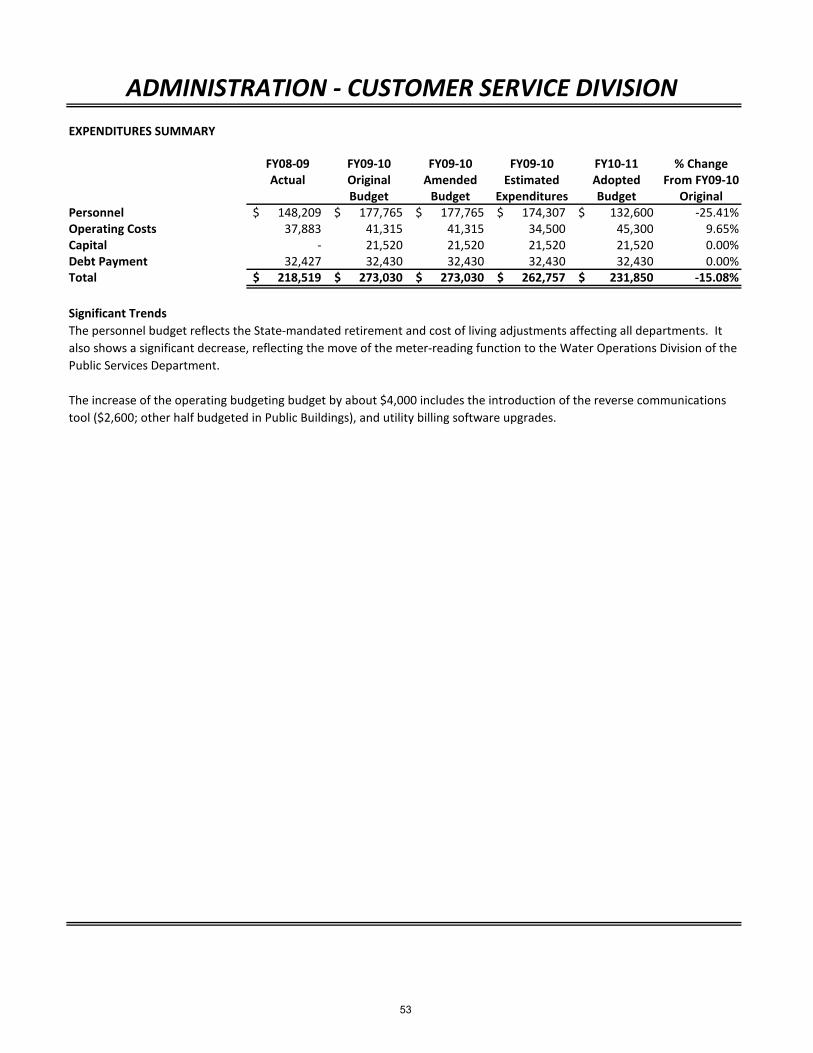

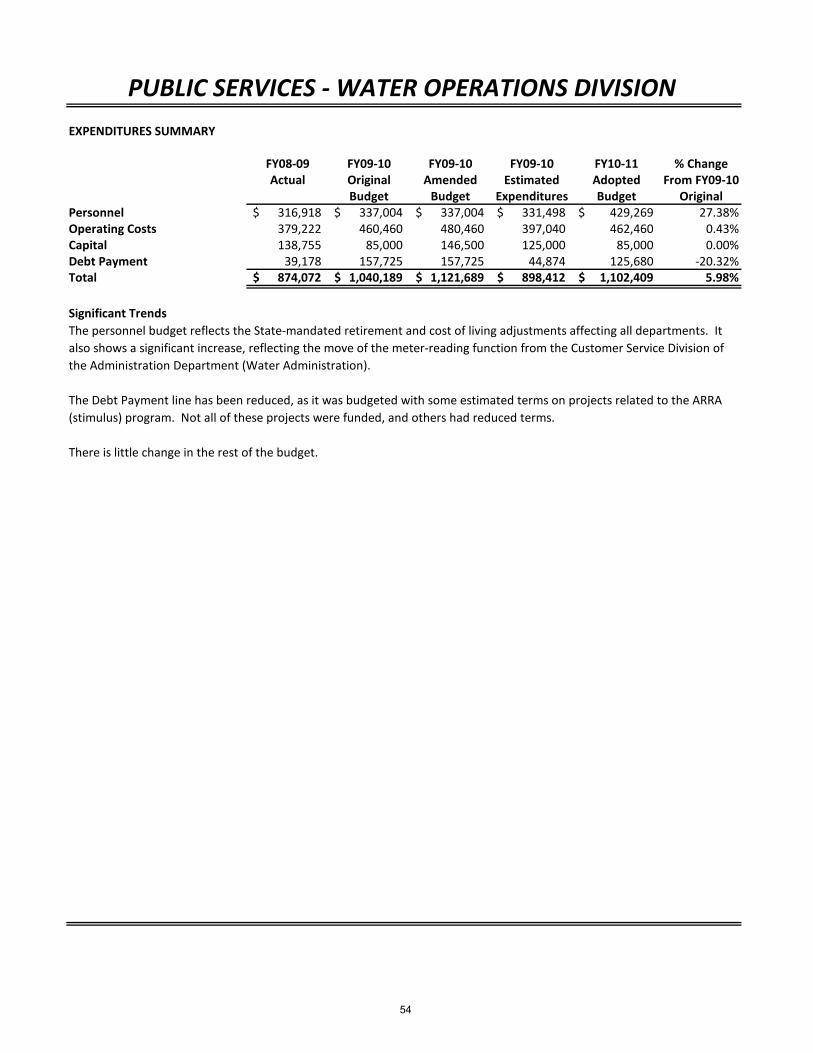

Water Fund Budget Summary page 51 Water Fund Revenues page 52 Administration – Customer Service Division page 53 Public Services – Water Operations Division page 54

GOLF FUND Section

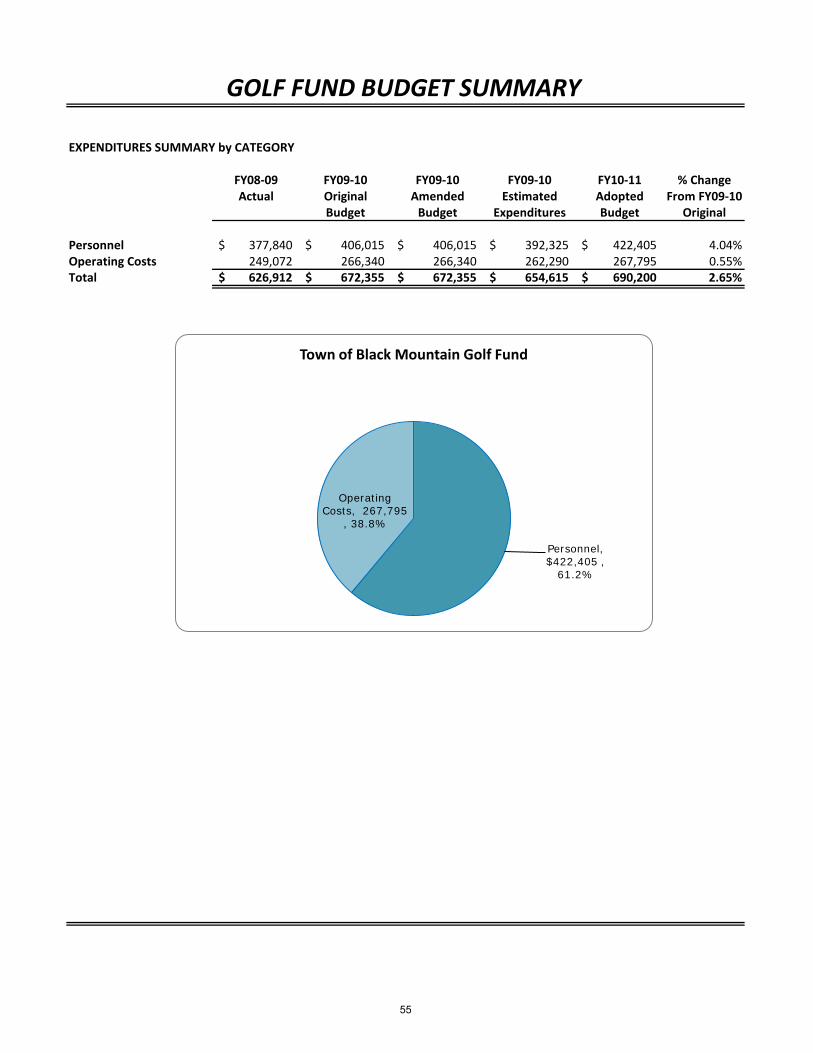

Golf Fund Budget Summary page 55 Golf Fund Revenues page 56 Golf Operations page 57 Golf Pro Shop page 58

APPENDICES Section

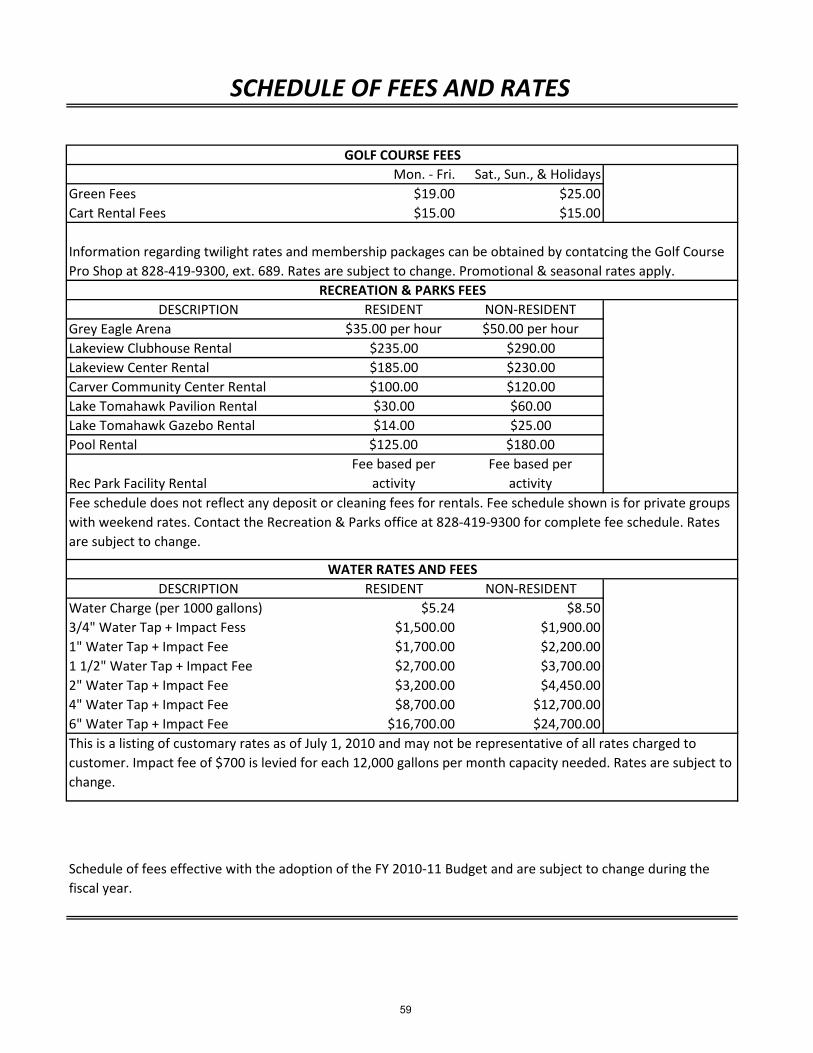

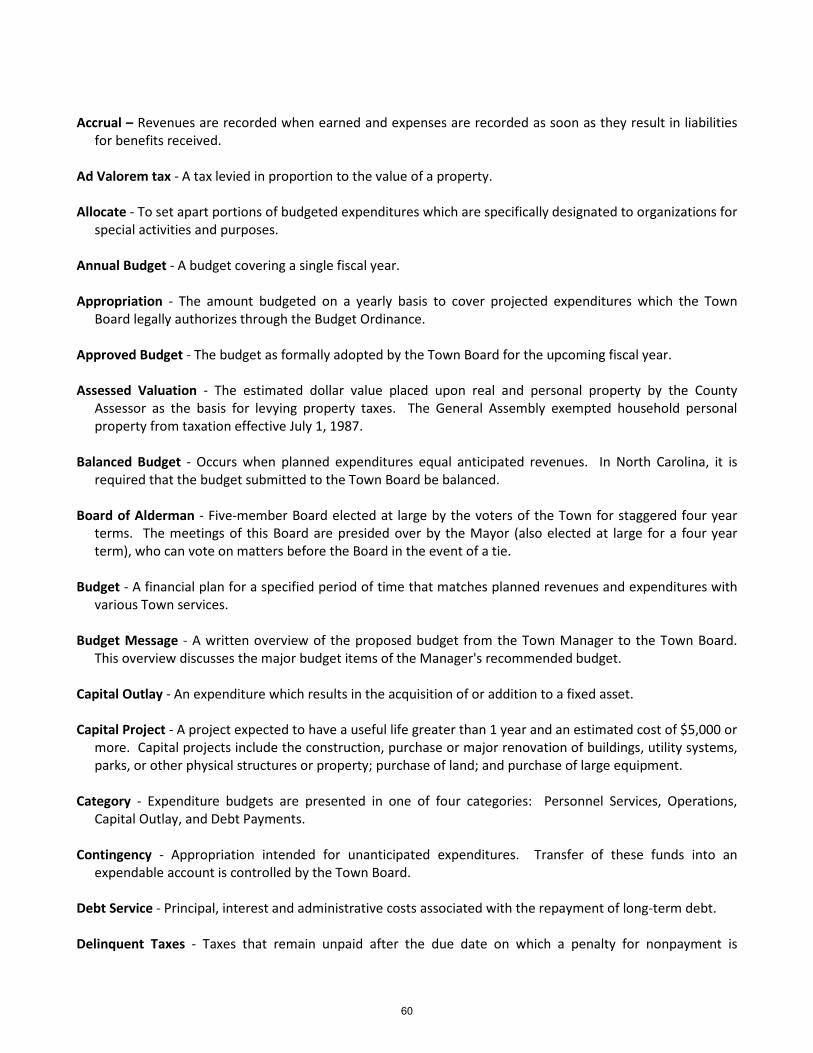

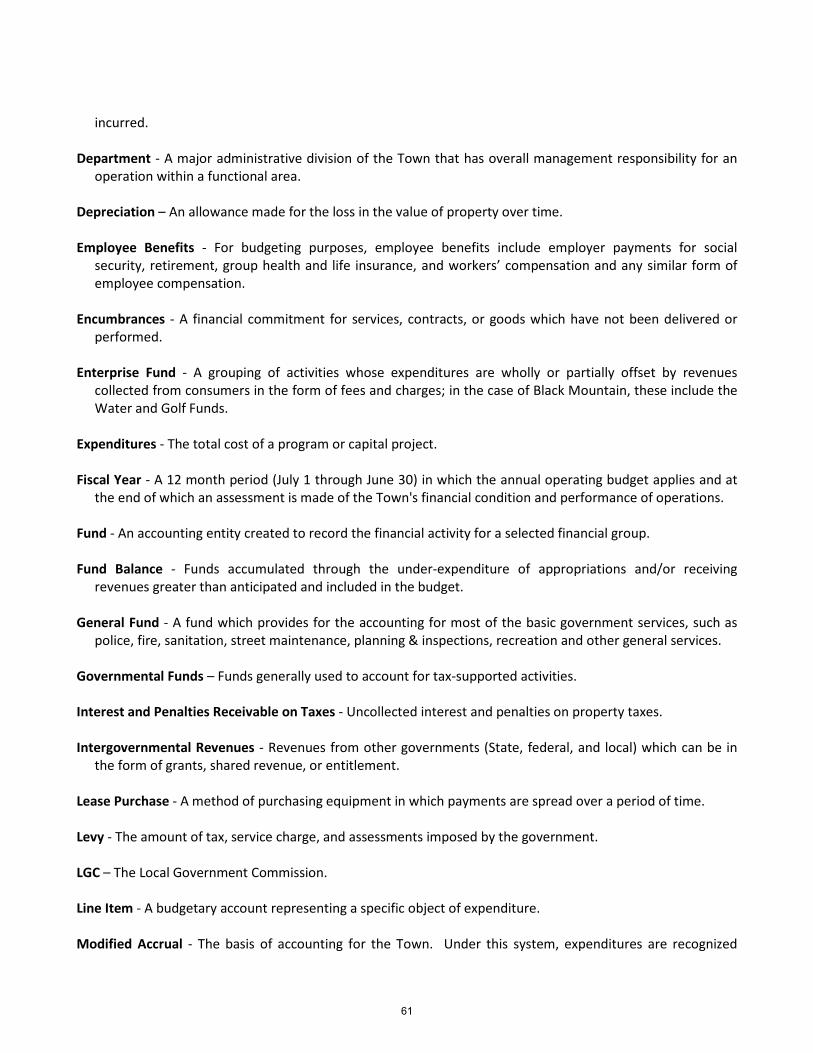

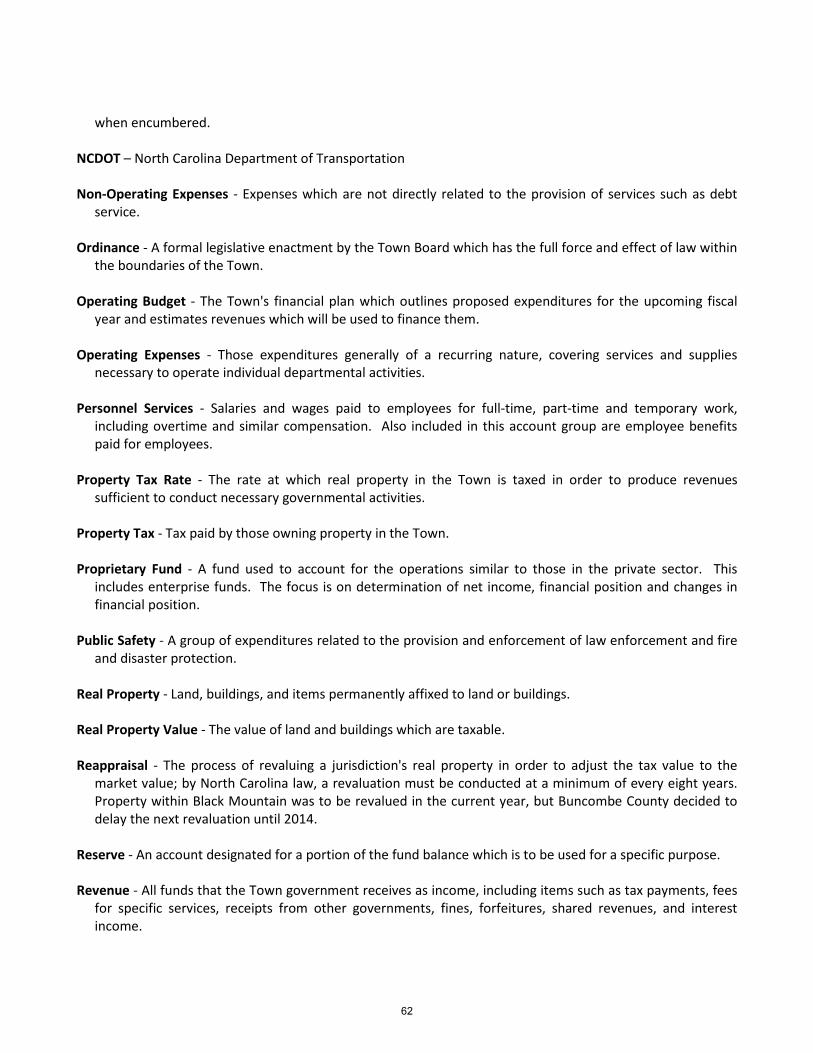

Schedule of Fees and Rates page 59 Glossary page 60

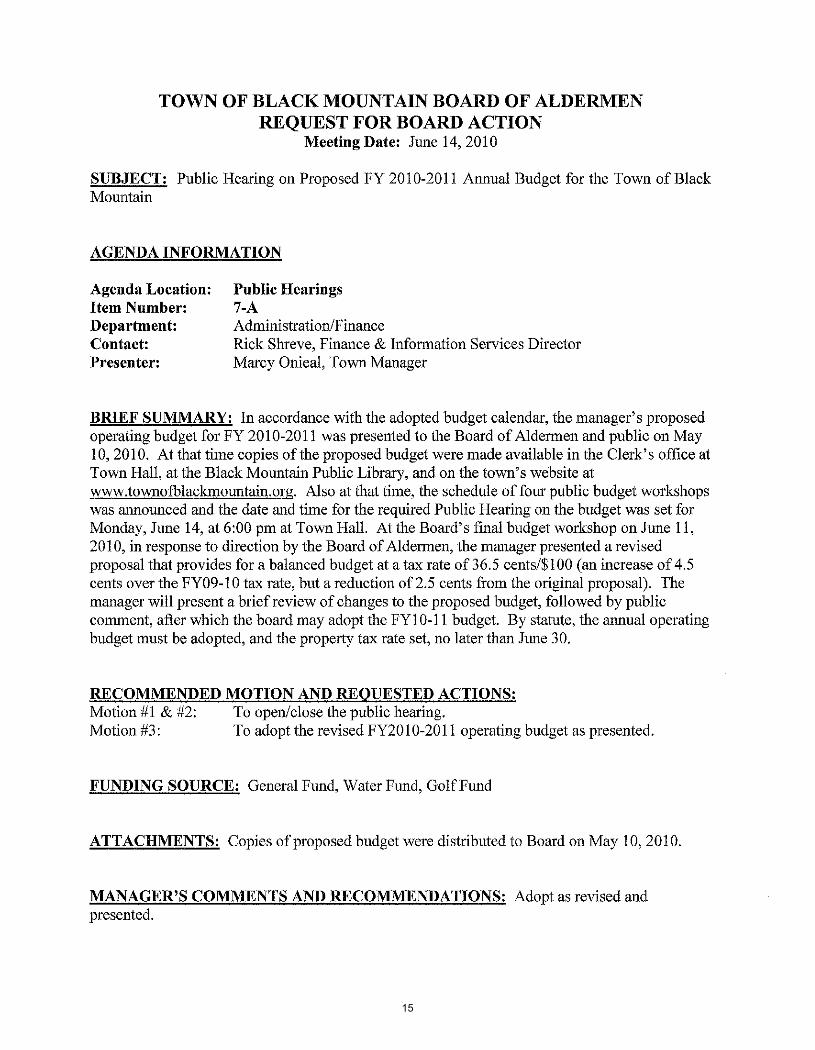

Quick Guide to the Adopted Budget document Herein for public review is the Fiscal Year 2010-11 budget for the Town of Black Mountain, adopted by the Board of Alderman on June 16, 2010. The final adopted tax rate for this year is 36.5 cents per $100 valuation. Below are a few useful tips for finding and understanding key elements of this document. A new reader of this budget document would be well-advised to peruse the Budget Message section in its entirety before focusing on additional details throughout the budget. Taken together, the Budget Message and other supporting pages in this section highlight the shifting economy and priorities of the Town as the budget process moved from the Manager’s Recommended Budget to the Board of Alderman’s final adopted budget. The Budget Message that accompanied the Manager’s Recommended Budget immediately follows this page; it is included in this section for posterity as well as to show the foundational budget from which the Board of Alderman built their adopted budget. Information on the Town’s major funds, revenue sources, and expenditure needs are discussed in this Budget Message as well. There are a few key items in this Budget Message section that serve to bridge the changes from the recommended budget to the adopted budget: Summary of Changes to Manager’s Recommended Budget: This piece details in

narrative format significant changes by department and division levels. Budget Ordinance: This is a copy of the legal document citing the action by the

Board of Alderman to adopt this budget for the Fiscal Year 2010-11. The Budget Message section also shows total adopted budgeted dollars for different functions within each of the major funds, as well as some charts and graphs to render the information in a more visual format. Thank you for your interest in the Town of Black Mountain. If you have questions, please contact the Finance Director, or Town Manager, at 828.419.9300.

1

Town of Black Mountain 160 Midland Avenue Black Mountain, North Carolina 28711

OFFICE OF THE TOWN MANAGER May 10, 2010 The Honorable Carl R. Bartlett, Mayor Board of Aldermen Town of Black Mountain, North Carolina Dear Mayor and Aldermen: I am pleased to submit for your consideration this proposed budget for Fiscal Year 2010-2011. This budget is balanced with respect to revenues and expenditures, and meets all requirements of the North Carolina Local Government Budget and Fiscal Control Act. INTRODUCTION The adoption of the annual budget by the Board of Alderman is one of the most important actions you take each year on behalf of the citizens of Black Mountain. The annual budget translates the values and priorities of this community into a plan of action for services, programs and projects. Furthermore, it identifies and allocates valuable limited resources to those priorities, and serves as a guide for staff in implementing those priorities throughout the year. Adopted Plans The Town’s Comprehensive Plan, first adopted by the Board of Aldermen in 2004, serves as the overarching long-range basis for guiding staff in the development of work plans and operating budgets. Similarly, staff is guided by other long-range project plans adopted by you or previous boards of aldermen, which include:

2004 Comprehensive Plan 2004 Recreation & Parks Master Plan 2005 Staffing Analysis/Classification & Pay Plan 2007 Lake Tomahawk Park Master Plan 2008 Pedestrian Transportation Plan 2008 Greenway Master Plan 2008 Clevenger Site Concept Plan 2008 NCDENR Water System Audit & Recommendations Report 2008 US 70 Corridor Study – Vision & Implementation Plan 2009 Stormwater Management Master Plan 2009 Strategic Energy Plan 2010 Historic District Plan (currently being updated) Ongoing 5-year Capital Improvement Plan (Major Facilities & Equipment)

2

Each of these plans has been developed with input from the public and elected officials, and with the guidance and technical assistance of town staff and outside professionals. Collectively, these adopted plans represent the “official vision” for our community. While some progress has been made in carrying out select strategies and programs, many of these plans call for capital or operational improvements which historically have not been funded at all, or have not been fully provided for in annual operating budgets. Budgetary Challenges The challenge in providing you with a balanced budget, which I am required by statute to do, is to balance the number, scope and quality of services demanded by the public, with the willingness of the public to pay for them. This challenge is both science and art -- simple math but a difficult and delicate juggling act intended to derive a mix of services and compromises between revenues and expenditures that can widely be supported by the public and at least a majority of you on the board. Reference is often made to “essential” services being most important when it comes to budgeting, but the fact is, that North Carolina municipalities are required to provide only one service, and that is building code enforcement. Towns may at their discretion, however, provide many services, which protect the safety, health and welfare of the public, serve to regulate behavior, or provide for enhanced quality of life in a community. Determining which services and programs the town should provide, and at what level, are largely policy decisions which arise over an extended period of time through public dialogue and the actions of successive boards of elected officials. Short- vs. Long-Term View While one Board of Aldermen cannot obligate a future board, the current mix of town programs and services, the comprehensive plans that have been adopted, the current level of budgetary obligation and state of the Town’s financial health, have all evolved over time in response to the needs, priorities and decisions of their day. Developing a budget for FY10-11 has been particularly challenging, due in part to the effects of a two-year downturn in the economy, from which we have yet to recover. More significantly, however, are the actions over the last two decades of successive administrations, failing to adjust revenues incrementally for the long-term health of the organization. For a number of years, the Town has favored short-term budget strategies, with an emphasis on cost cutting to fund new priorities, instead of revenue development to strengthen core services. This has resulted in routine neglect of town infrastructure, facilities, fleet and equipment, which we now address strictly on an emergency basis rather than with a plan for preventive maintenance and systematic replacement. This strategy has not provided for proper training or succession planning in personnel, because professional development is considered discretionary spending and is usually first to be cut, when in fact professional development is “most needed” when the budget is tight and more creative thinking is demanded. This strategy has limited the Town’s ability to change with the times and take advantage of best practices and appropriate technologies that would encourage proactive rather than reactive approach to service delivery. Furthermore, this strategy has not resulted in a plan to ensure equity of services across the entire jurisdiction. There comes a time when excessive cost-cutting becomes counter –productive, and failure to provide sufficient financial resources prevents long-term progress. I believe the Town of Black Mountain has already reached that point, through no fault of any single board, administration or staff, but simply out of habit and because greater emphasis has historically been placed on short-term interests rather than long-term vision, continuity and stability.

3

Changing Public Expectations The Town of Black Mountain has not raised the effective rate on property taxes in many years, and in fact has lowered tax rates during revaluation years, in one case even below what was considered “revenue neutral”. While Black Mountain has been fortunate to increase its property tax levy through genuine growth, as well as inflationary increases in property values associated with scarce supply and the free-flow of credit prior to the 2008 mortgage crisis, that “natural growth” engine has, at least temporarily, come to a screeching halt and is not likely to regain an aggressive pace in the near future. The fact remains, that due to topography, a scarcity of large tracts of developable land, and lack of adequate infrastructure in some areas of town, there simply are not many locations suitable for anything more than residential infill or modest commercial development. Meanwhile, population in Black Mountain has also grown (expected to be over 9,000 with the next census report) and our status as a haven for summer residents and vacationers means that we must maintain infrastructure and services suitable for a full seasonal population of approximately 42,000. We continue to experience an influx of retirees and residents moving here from other places, who in some cases, arrive with expectation for higher levels of service than what has traditionally been provided in Black Mountain. The public demand for more and “better” services continues to increase, while the willingness to pay for public services in the “Tea Party Era” continues to diminish. The FY10-11 budget also projects increases in certain fixed costs, over which the Town has no control, such as inflationary increases associated with emergence from the recession, utility increases and state mandates which could affect everything from retirement and health costs for employees to ABC profits. Considering these factors, the previous budget balancing formula, which relies on the hope of revenue growth without taking steps to ensure such growth, followed by repeated cost-cutting in the face of inadequate revenue streams, simply will no longer work, unless you are willing to seriously consider reducing personnel positions, and citizens are willing to accept less than the current scope and quality of services. Efficiency/Effectiveness Measures Undertaken The Town has made progress in improving efficiency and effectiveness of our operations, which has resulted in cost savings, large and small, in the last couple of years. In the current year, cross-training, departmental reorganizations, and employees taking on additional responsibilities have allowed us to do more without having to add additional fulltime employees. In the past seven years, only two new positions have been added – two firefighters in 2003 to accommodate the 2-in/2-out safety policy mandated by the state. With the transition of key leadership positions in the last two years (most notably, the Town Manager, Assistant Town Manager/Finance Director, Town Clerk and Public Works Director), and modest reductions in overtime and part-time positions, the Town saved over $75,000 in salary and benefits. Open positions were temporarily frozen for up to six months in order to save salary and benefits dollars. Cost of living and merit adjustments for employees were suspended in FY09-10, so that the Town could preserve its needed full-time positions, while saving an estimated $210,000. Also in FY09-10, refinancing existing debt allowed the Town to take on additional debt service, without significantly increasing the operating budget. Four successful applications through the American Reinvestment and Recovery Act allowed us to leverage town funds for capital projects we could not have undertaken otherwise on a 5:1 basis. Transferring to an internet-based phone service allowed the Town to save on long-distance and local service while adding many new needed lines and desk sets. Renegotiation of the sanitation contract with GDS is currently underway with regard to the annual CPI

4

adjustment and improving recycling collection and waste transfer/disposal, while saving on the existing contract. As a temporary measure, contributions to outside agencies were all but eliminated and all departmental operating expenditures were held at, or below, the previous year’s levels, while a moratorium was placed on all capital acquisitions and projects, except those covered by grant funding. While each of these measures allowed the Town to squeak through an extreme budget year, it was necessary to use roughly $95,000 in fund balance to break even, which is the equivalent of 1¢/$100 on the tax rate. Also over the last two years, the town absorbed significant increases in sanitation without raising revenues, and faced several unbudgeted emergency expenditures (snow removal, firetruck/HVAC/roof repairs). Without upfront expenditure for certain equipment, technology and training, any future efficiency measures will likely center around small incremental improvements in service, without an accompanying effect on budget, and these will not be sufficient to address the gap between the services citizens expect and those that the Town has been able to provide. All our departments have reached a critical stage in delivery of service, and are beyond being able to use budget cuts to balance and still deliver effective programs and services. What is ahead? The FY09-10 (current) budget was created in the midst of an economic crisis, and therefore reflected austere attempts to maintain core services for one more year. As I stated in last year’s budget message, I believed “we could accommodate such restrictive measures on a one-time basis, but under no circumstances should one consider the recommended level of cut-back to be sustainable over the long-term without having a severe impact on either the scope or quality of the public services the Town delivers.” Our staff helped to balance the current year’s budget largely through the elimination of virtually all capital and discretionary spending, while anticipating an economic turnaround that will allow for a return to more solid financial footing in FY10-11. The FY10-11 budget is a reflection of the burgeoning needs of the Town, and the demand for services, in a modestly improved economic climate. Board Direction I am grateful to the Board of Aldermen for providing significant guidance toward the development of this budget during the annual board and staff planning retreat in February, 2010. Indeed, the Board had even made decisions earlier in the current fiscal year obligating the town to specific capital projects and grant-related expenditures, with the clear understanding that those decisions would commit the Town to an increase in either the tax rate or other revenue sources as of July 1, 2010. Each one- cent increase in the tax rate in Black Mountain currently generates approximately $90,000 in additional revenue. In FY10-11, an increase in revenue will be required for the following items already approved by the Board outside the budget process (amounts here are rounded for simplicity): Acquisition of Town Square property ($210K), Sewer extensions to areas annexed in 1988 ($105K), SAFER grant (new firefighter costs) ($35K), replacement of out-of-service vehicles that would cost more to repair/maintain than the value ($65K), and FY10-11 retirement eligibility payouts ($15K). With regard to personnel , the State Health Plan and Retirement system are passing along increased costs with a reduction of benefit ($80K), and at the Board’s direction I have added a 2.9% cost of living adjustment ($90K), which brings employees nearly even with the 5-year cumulative CPI after going one year without an adjustment. The seven items above represent nearly $600K in new, but previously approved or communicated, fixed costs to the Town. Collectively they account for the vast majority of the proposed increase in the General Fund budget.

5

Recommended Fees & Tax Rate With the above commitments in place, it is imperative that the Board support its earlier decisions to increase general fund revenues in such a way as not to sacrifice core services. Although I have considered and did recommend other revenue adjustments last year, such as implementation of a sanitation fee, several of you have noted the logistical difficulty in implementing a new fee with little more than one year remaining on our sanitation contract. Furthermore, some of you have publicly expressed a clear preference for the more progressive property tax, which is a wealth-proportional charge designed to affect taxpayers more equitably than a flat fee for service. The proposed budget includes one new fee for the regulation of electronic gaming and some minor adjustments to existing fees that are expected to generate an additional $30,000 in general fund revenue. I submit for your consideration a balanced budget for FY10-11, recommending an ad valorem tax increase of 7 cents per $100 valuation, bringing the Town portion of the property tax bill to a total of 39 cents per $100 valuation. If adopted, this rate increase will generate about $650,000 in revenues for the Town, and will cost a resident who owns a $200,000 home an additional $139 annually, or the monthly equivalent of approximately $12. OVERVIEWS BY FUND Following are overviews of the proposed budgets for the Town's General Government Funds, which are largely supported by taxes and intergovernmental revenues, and for the Town’s Proprietary Funds (Water Fund and Golf Fund), which are supported almost entirely by fees for goods and services and operated as business-type activities. Each section provides a discussion of significant changes in revenues, expenditures, and general operations for the fund, with the remainder of the budget document containing the more specific numbers behind these highlights. You may notice a change in budget format from previous years, as our Finance staff is beginning to incorporate best budget practices as recommended by the Government Finance Officers Association, with a goal of improving transparency and user friendliness for board, staff and citizens. Budget Summaries The budget summary for each department provides a summary of significant budget changes in a brief narrative format. It also lists expenditures summarized in the categories of Personnel, Operating Costs, Capital, and Debt Payments. Revenues are also listed in a summary format based on revenue sources. These expenditure and revenue summaries provide historic and proposed figures as follows:

• 2008-09 Actual • 2009-10 Original Budget • 2009-10 Amended Budget • 2009-10 Estimated Year-End • 2010-11 Recommended Budget • % Change from 2009-10 Original Budget

GENERAL FUND The General Fund is the general operating fund of the Town and is used to account for all revenues and expenditures, except those required to be accounted for in another fund by statute, or by generally accepted accounting principles. The General Fund is the Town’s largest fund and is projected at $7.4 million in FY10-11, up 12% from the $6.6 million originally budgeted in FY09-10. The projected revenues

6

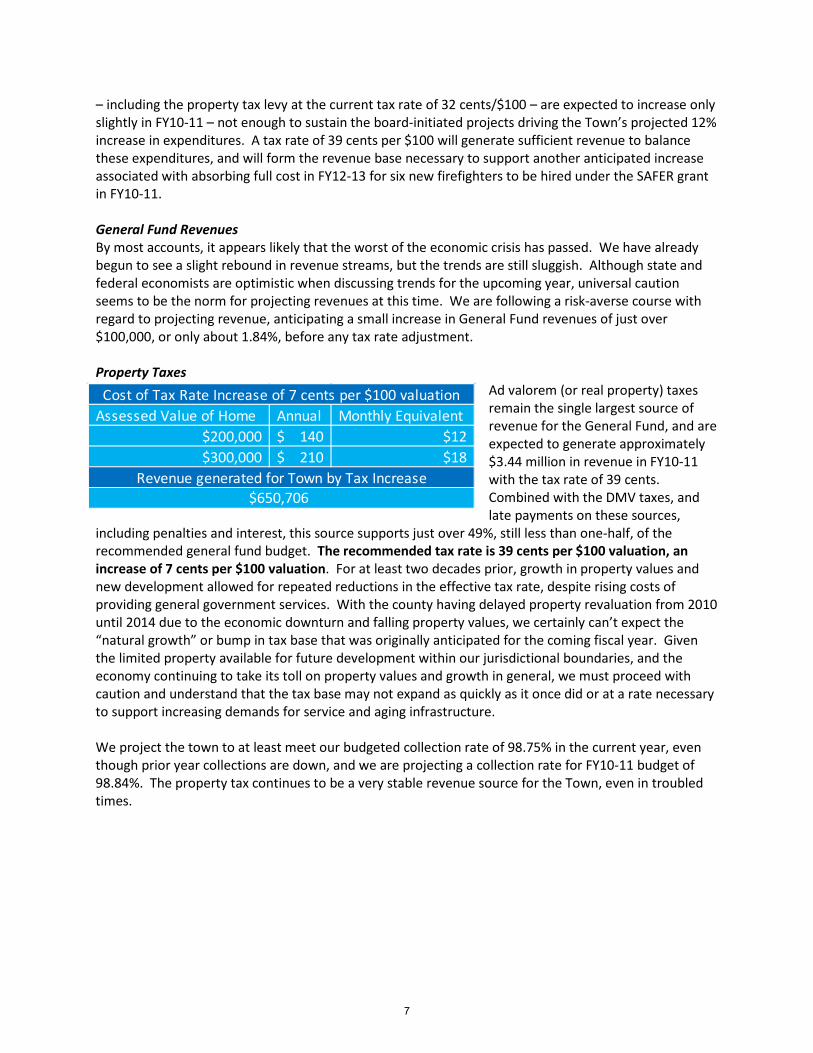

Assessed Value of Home Annual Monthly Equivalent$200,000 140$ $12$300,000 210$ $18

Cost of Tax Rate Increase of 7 cents per $100 valuation

Revenue generated for Town by Tax Increase$650,706

– including the property tax levy at the current tax rate of 32 cents/$100 – are expected to increase only slightly in FY10-11 – not enough to sustain the board-initiated projects driving the Town’s projected 12% increase in expenditures. A tax rate of 39 cents per $100 will generate sufficient revenue to balance these expenditures, and will form the revenue base necessary to support another anticipated increase associated with absorbing full cost in FY12-13 for six new firefighters to be hired under the SAFER grant in FY10-11. General Fund Revenues By most accounts, it appears likely that the worst of the economic crisis has passed. We have already begun to see a slight rebound in revenue streams, but the trends are still sluggish. Although state and federal economists are optimistic when discussing trends for the upcoming year, universal caution seems to be the norm for projecting revenues at this time. We are following a risk-averse course with regard to projecting revenue, anticipating a small increase in General Fund revenues of just over $100,000, or only about 1.84%, before any tax rate adjustment. Property Taxes

Ad valorem (or real property) taxes remain the single largest source of revenue for the General Fund, and are expected to generate approximately $3.44 million in revenue in FY10-11 with the tax rate of 39 cents. Combined with the DMV taxes, and late payments on these sources,

including penalties and interest, this source supports just over 49%, still less than one-half, of the recommended general fund budget. The recommended tax rate is 39 cents per $100 valuation, an increase of 7 cents per $100 valuation. For at least two decades prior, growth in property values and new development allowed for repeated reductions in the effective tax rate, despite rising costs of providing general government services. With the county having delayed property revaluation from 2010 until 2014 due to the economic downturn and falling property values, we certainly can’t expect the “natural growth” or bump in tax base that was originally anticipated for the coming fiscal year. Given the limited property available for future development within our jurisdictional boundaries, and the economy continuing to take its toll on property values and growth in general, we must proceed with caution and understand that the tax base may not expand as quickly as it once did or at a rate necessary to support increasing demands for service and aging infrastructure. We project the town to at least meet our budgeted collection rate of 98.75% in the current year, even though prior year collections are down, and we are projecting a collection rate for FY10-11 budget of 98.84%. The property tax continues to be a very stable revenue source for the Town, even in troubled times.

7

2010 Estimated Valuation 892,821,808

2010 Estimated Taxes @ .039 TAX RATE 3,482,005$

2010 Estimated Revenue @ 98.84% COLLECTION RATE 3,441,615$

2010 Estimated Valuation 50,978,130

2010 Estimated Taxes @ 0.39 TAX RATE 198,815$

2010 Estimated Revenue @ 92.42% COLLECTION RATE 183,744$

One cent on the tax rate = 92,958$

TAX RATE CALCULATION

AD VALOREM TAXES

DMV (VEHICLE) TAXES

Ad valorem tax collection rates for the Town of Black Mountain2006 2007 2008 2009 2010*

99.45% 99.55% 99.29% 98.84% 98.75%* 2010 is estimate used in budget development

Buncombe County, 57.38%

Town of Black Mountain,

42.62%

% Breakdown by Governing Body

Buncombe County Town of Black Mountain

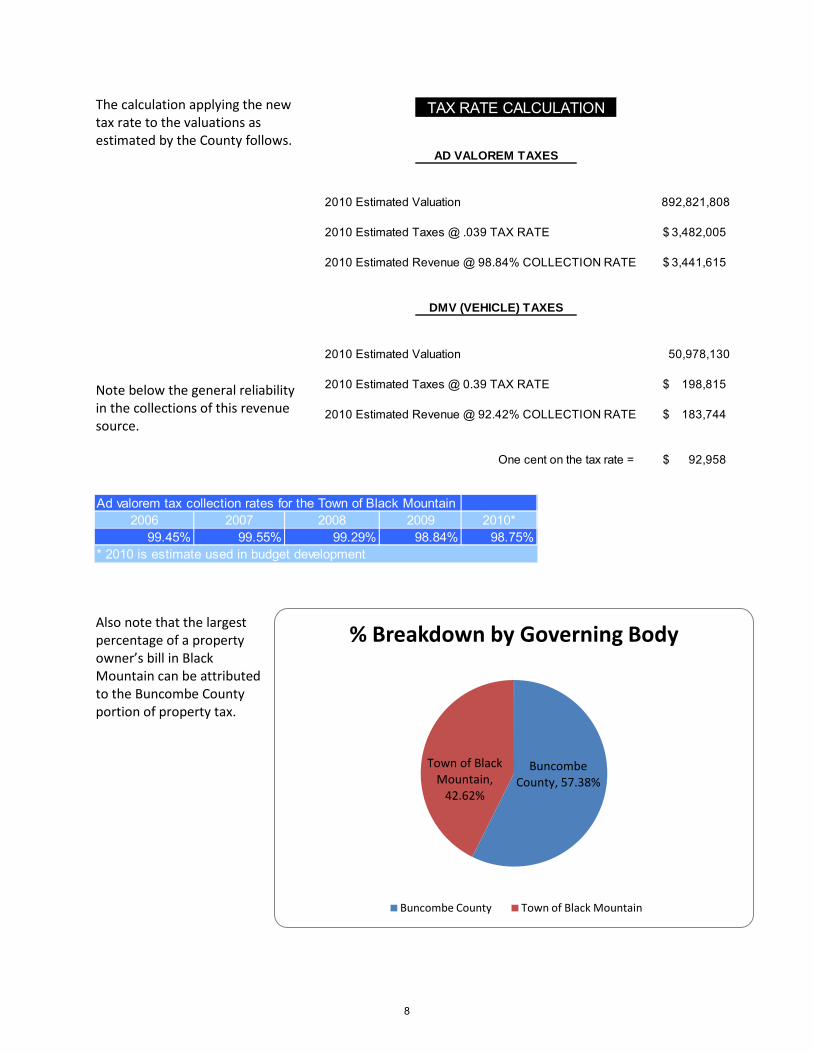

The calculation applying the new tax rate to the valuations as estimated by the County follows. Note below the general reliability in the collections of this revenue source.

Also note that the largest percentage of a property owner’s bill in Black Mountain can be attributed to the Buncombe County portion of property tax.

8

60,000.00

65,000.00

70,000.00

75,000.00

80,000.00

85,000.00

90,000.00

95,000.00

Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09

Sales Taxes: Monthly Distributions Jan. 2009 ->

Series1 3 per. Mov. Avg. (Series1) Linear (Series1)

Downtown Property Debt PaymentsFY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

208,320$ 203,154$ 197,988$ 192,822$ 187,656$ 182,490$ 177,324$ 172,158$ 166,992$ 161,826$ FY21 FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30

156,660$ 151,494$ 146,328$ 141,162$ 135,996$ 130,830$ 125,664$ 120,498$ 115,332$ 110,166$

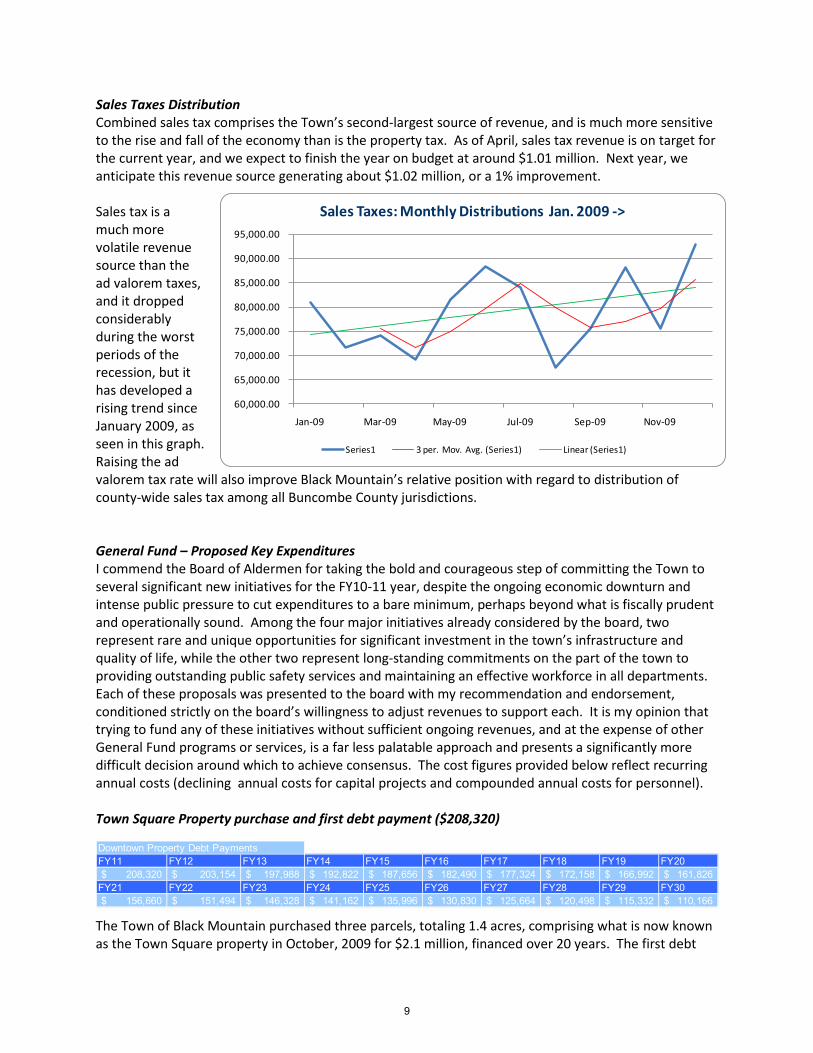

Sales Taxes Distribution Combined sales tax comprises the Town’s second-largest source of revenue, and is much more sensitive to the rise and fall of the economy than is the property tax. As of April, sales tax revenue is on target for the current year, and we expect to finish the year on budget at around $1.01 million. Next year, we anticipate this revenue source generating about $1.02 million, or a 1% improvement. Sales tax is a much more volatile revenue source than the ad valorem taxes, and it dropped considerably during the worst periods of the recession, but it has developed a rising trend since January 2009, as seen in this graph. Raising the ad valorem tax rate will also improve Black Mountain’s relative position with regard to distribution of county-wide sales tax among all Buncombe County jurisdictions. General Fund – Proposed Key Expenditures I commend the Board of Aldermen for taking the bold and courageous step of committing the Town to several significant new initiatives for the FY10-11 year, despite the ongoing economic downturn and intense public pressure to cut expenditures to a bare minimum, perhaps beyond what is fiscally prudent and operationally sound. Among the four major initiatives already considered by the board, two represent rare and unique opportunities for significant investment in the town’s infrastructure and quality of life, while the other two represent long-standing commitments on the part of the town to providing outstanding public safety services and maintaining an effective workforce in all departments. Each of these proposals was presented to the board with my recommendation and endorsement, conditioned strictly on the board’s willingness to adjust revenues to support each. It is my opinion that trying to fund any of these initiatives without sufficient ongoing revenues, and at the expense of other General Fund programs or services, is a far less palatable approach and presents a significantly more difficult decision around which to achieve consensus. The cost figures provided below reflect recurring annual costs (declining annual costs for capital projects and compounded annual costs for personnel). Town Square Property purchase and first debt payment ($208,320)

The Town of Black Mountain purchased three parcels, totaling 1.4 acres, comprising what is now known as the Town Square property in October, 2009 for $2.1 million, financed over 20 years. The first debt

9

payment is due in July, 2010. The parcel is the single most visible and important parcel in downtown Black Mountain, occupying one block along the northeast corner of the intersection of US 70 (State Street) and Hwy 9 (Montreat Road), bounded by Town Hall and Public Safety Buildings on two sides and the downtown historic district on the other. The decision to purchase the property was made after negotiating the price down from $2.8 million, without having a specific development plan in place, but with the intention of controlling the property for future development, either publicly, privately or through a public-private partnership. Due to the economic downturn, all prior attempts to develop the property privately had failed and lack of zoning restrictions would likely have left this parcel to develop as a convenience mart or chain store. The Board has appointed a diverse committee of community leaders to develop a process for soliciting, evaluating and responding to public input on potential uses, design and funding opportunities, with the general intent to develop an iconic gateway and public gathering space in the center of town. Construction of Sewer Extensions to1988 annexation areas ($105,000) In 1988, as part of annexations of six neighborhoods into the Black Mountain town limits, the Town adopted an annexation agreement promising, among other things, the extension of sewer lines into the annexed areas. Only two of the six sewer extensions were completed, and subsequently the Metropolitan Sewerage District took over the ownership, management and maintenance of all sewer systems in Buncombe County in the early 90’s. Still obligated to provide these extensions into the Avena, McCoy Cove, Blue Ridge Road and Cragmont/Highland Farms areas, the town completed acquisition of easements in early 2009 and spent this last year seeking design approval and sources of construction funding . After four unsuccessful attempts at acquiring funding through various programs associated with the American Reinvestment and Recovery Act, (funding denied due to ineligibility of new construction), the Town sought and received a low interest loan through NC Construction Grants and Loans to complete the project in three of the four remaining areas. MSD will provide 35% reimbursement for these projects, which should then provide adequate funding for construction of the fourth and final outstanding line in the Cragmont/Highland Farms area. Although the town will own the lines through the term of financing, MSD will maintain the lines under a maintenance agreement, which has already been executed. Advertisements for bids have already been published. Work is expected to commence shortly after the start of the new fiscal year The NC Local Government Commission worked with the town to develop favorable financing for both of these unusual circumstances on very short notice and deadlines, and is performing an oversight role to ensure that the Town fulfills its obligations under both programs. In the adoption of the financing agreements for these two projects, the Board of Aldermen pledged a 3¢ tax increase to cover debt service on the Town Square Property and a 1¢ increase for the sewer extension. SAFER Grant- firefighter operating costs ($35,100) In 2009, the American Reinvestment and Recovery Act provided additional monies and relaxed funding requirements for this grant, which is designed to provide for employment of new fulltime professional firefighters or re-employment of laid off firefighters by municipalities. If funded, the grant will provide Black Mountain 100% of salaries and benefits for six new firefighters for two years, with the requirement that the town pick up 100% costs in the third year after hire. Not covered by the grant are uniforms ($20,000), physicals ($1,500), radios ($3,600), and workers’ compensation coverage ($10,000). These cost will be obligated by the town only upon receipt of the grant, and the proposed budget makes no provision for hiring these positions if the grant is not received. Because of the commitment to retain the firefighters after the grant funding has expired, this program is expected to require roughly $ ½ million in additional general fund revenue by FY12-13.

10

Employee earning $30,000 at end of FY05FY06 FY07 FY08 FY09 FY10 FY11

COLA 3.00% 3.00% 3.00% 3.00% 0.00% 2.90%30,900 31,827 32,782 33,765 33,765 34,744

CPI-U 2004 2005 2006 2007 2008 20092.68% 3.39% 3.23% 2.85% 3.84% -0.36%

30,803 31,848 32,876 33,813 35,112 34,987

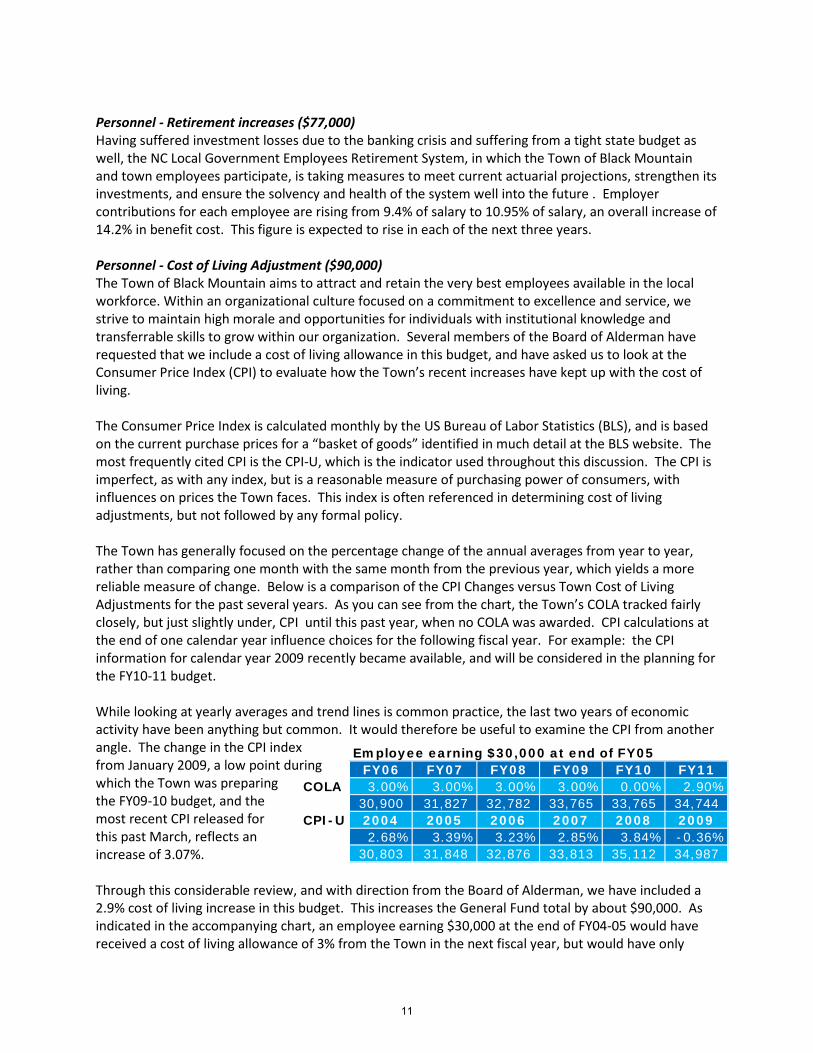

Personnel - Retirement increases ($77,000) Having suffered investment losses due to the banking crisis and suffering from a tight state budget as well, the NC Local Government Employees Retirement System, in which the Town of Black Mountain and town employees participate, is taking measures to meet current actuarial projections, strengthen its investments, and ensure the solvency and health of the system well into the future . Employer contributions for each employee are rising from 9.4% of salary to 10.95% of salary, an overall increase of 14.2% in benefit cost. This figure is expected to rise in each of the next three years. Personnel - Cost of Living Adjustment ($90,000) The Town of Black Mountain aims to attract and retain the very best employees available in the local workforce. Within an organizational culture focused on a commitment to excellence and service, we strive to maintain high morale and opportunities for individuals with institutional knowledge and transferrable skills to grow within our organization. Several members of the Board of Alderman have requested that we include a cost of living allowance in this budget, and have asked us to look at the Consumer Price Index (CPI) to evaluate how the Town’s recent increases have kept up with the cost of living. The Consumer Price Index is calculated monthly by the US Bureau of Labor Statistics (BLS), and is based on the current purchase prices for a “basket of goods” identified in much detail at the BLS website. The most frequently cited CPI is the CPI-U, which is the indicator used throughout this discussion. The CPI is imperfect, as with any index, but is a reasonable measure of purchasing power of consumers, with influences on prices the Town faces. This index is often referenced in determining cost of living adjustments, but not followed by any formal policy. The Town has generally focused on the percentage change of the annual averages from year to year, rather than comparing one month with the same month from the previous year, which yields a more reliable measure of change. Below is a comparison of the CPI Changes versus Town Cost of Living Adjustments for the past several years. As you can see from the chart, the Town’s COLA tracked fairly closely, but just slightly under, CPI until this past year, when no COLA was awarded. CPI calculations at the end of one calendar year influence choices for the following fiscal year. For example: the CPI information for calendar year 2009 recently became available, and will be considered in the planning for the FY10-11 budget. While looking at yearly averages and trend lines is common practice, the last two years of economic activity have been anything but common. It would therefore be useful to examine the CPI from another angle. The change in the CPI index from January 2009, a low point during which the Town was preparing the FY09-10 budget, and the most recent CPI released for this past March, reflects an increase of 3.07%. Through this considerable review, and with direction from the Board of Alderman, we have included a 2.9% cost of living increase in this budget. This increases the General Fund total by about $90,000. As indicated in the accompanying chart, an employee earning $30,000 at the end of FY04-05 would have received a cost of living allowance of 3% from the Town in the next fiscal year, but would have only

11

Fire: Quick response vehicle & Inspections vehicle 23,000$ Police: 3 patrol cars 22,000$ Planning: 4-Wheel Drive Inspections vehicle 5,000$ Public Services: New Director's truck 5,500$ Recreation & Parks: 4X4 Truck 8,000$

63,500$

received a 2.68% increase if their salary were pegged to the CPI average increase available at budget time. However, as the years have progressed, the Town’s cost of living adjustments have fallen behind the consumer price index, overall. Even though the average CPI change for 2009 was a slight decrease, an employee whose salary had been pegged to the CPI would still have fared better than under the Town’s COLAs. To that end, a 2.9% adjustment would be an effort towards closing that cost of living gap somewhat. Installment Debt ($63,500) The Town has the authority to finance purchases for major projects, buildings, renovations and major equipment. The underlying principal for this type financing is that the public can and should pay for capital investments over a long time frame in order to spread the cost among citizens over time and to better match the expected usefulness of the capital purchase. This method enables governments to undertake large capital projects without having to pay cash for the projects at the time they take place. It is in this interest that we are proposing to replace several vehicles in multiple departments, with an installment financing arrangement. Most of the vehicles these are scheduled to replace have recently required maintenance and repair funds that would have almost covered a first year installment payment, and they are likely to require more in the near future. In fact, two recently surplused trucks had so little value that we received more for them as scrap metal than attempting to sell them on Gov Deals. Some high-use/high-mileage vehicles, particularly those used in public safety, present safety risks to employees and citizens alike, if they fail at an inopportune time. In the past year, we lost two public safety vehicles altogether, had no spare and relied on the generosity of Buncombe County to donate one of their surplused vehicles as a replacement. This proposed debt package is one piece of the much-needed increase in this recommended budget, and the breakdown of vehicles follows: Customer Service Initiatives -- Additions to Budget ($40,000) Approximately ½¢ of the proposed tax rate increase is devoted to a variety of small increases in general fund expenditures related to professional development of staff in all departments and at all levels of the organization, anticipated utility increases, technology-based initiatives, and restoration of the modest contributions to outside agencies that were omitted in the current year. The proposed expenditures are individually insignificant in terms of dollars, but are extremely significant in terms of staff’s ability to continue “doing more with less” and to better serve the public. Each proposal is designed to directly provide improved customer service to, and communication with, the public. Altogether these proposals total approximately $40,000. Technology-based initiatives include reverse communications software to notify many individuals simultaneously of emergencies, events or meetings, additional IT support for improved integration of diverse applications, development of GIS databases, and financial services such as online bill-pay, bank draft, purchase cards and credit processing. We hope also to offer service request tracking and to conduct annual customer satisfaction surveys.

12

Fund Balance ($295,000 appropriated) Fund balance is basically the difference between expenditures and revenues at the end of the fiscal year, either from revenues coming in at higher-than-expected levels, or funds expended at lower-than-expected levels. Part of the balance may be reserved or designated for specific purposes. A portion of fund balance is reserved for specific purposes required by North Carolina statute and is not available for appropriation. The remaining amount is unreserved, undesignated fund balance. A part of undesignated, unreserved fund balance is intended to meet the cash flow and working capital needs of the Town in accordance with reserve recommendations of the North Carolina Local Government Commission, and part of the balance is retained to meet Town reserve policies. The remaining balance is available to be used for additional appropriation in the subsequent year’s budget. It is a Town goal to maintain fund balance at a level that will meet on-going cash flow needs and provide available funds to meet unexpected emergency situations. Town practices with regard to net assets include the following:

• While statues require that a town maintain a minimum reserve of 8% (or one month’s operating expenses) of unrestricted net assets, by policy, the Town seeks to maintain a minimum financial reserve of 30.5% of unrestricted net assets, consistent with the recommendations of the North Carolina Local Government Commission. The reserve is for cash flow, emergencies and unforeseen opportunities.

• The Town also seeks to maintain a level of net assets which is appropriate to retain its

creditworthiness with lending agencies. For FY10-11, we are recommending an appropriation of $295,000 of fund balance in order to balance the budget, a level consistent with recent years’ appropriations. The Town’s anticipated fund balance at the beginning of FY10-11 will be about $2.5 million, which is approximately 35% of the recommended General Fund expenditures, less Powell Bill funds. By appropriating $295,000 to balance the FY10-11 budget, the available fund balance, as a percentage of the General Fund, drops to 31%. WATER FUND The Water Fund is established as an enterprise-type activity for the Town, separate from the General Fund. It is a self sustaining enterprise with its own revenue stream. The Town operates its own water system, and purchases water wholesale from the City of Asheville to supplement the Town’s supply as needed. The estimated revenue from water sales in the current year is expected to fall off budget by about $85,000, primarily attributed to the reduction in outdoor water use, as we have had a good deal of precipitation over the past year in Black Mountain. As a result, we have some expenditures budgeted in the current year that will be delayed until next year. We have also had a lesser need to purchase water from the City of Asheville in the current year. The Water Fund budget for next year reflects a modest 1.6% increase overall. The Water Fund faces the same personnel increases as the General Fund related to State retirement and health costs (cost to Water Fund of about $6,000) and the 2.9% cost of living adjustment (cost to Water Fund of about $11,000). The Town is also facing increased costs related to the purchase of water wholesale from

13

Asheville, as Asheville is raising its rates by 5%. As a result, the proposed budget includes a 5% water rate increase as well. It has been customary in recent years to match the City of Asheville’s rate increases for the following reasons:

1) The Town’s costs from Asheville increase by that much; 2) like Asheville, the Town has fairly extensive unaddressed capital needs for which the system must build reserves; 3) approximately one-third of Black Mountain residents are actually Asheville water customers, so in order to provide equitable rates to all Black Mountain citizens, individual water rates are kept roughly in line with Asheville rates.

GOLF FUND The Golf Fund is another proprietary fund separate from the General Fund, with its own revenue stream. The Golf course, through the Recreation and Parks department, is participating in a new marketing effort towards increasing memberships, cart rentals, and other revenue generators. It is on the projections surrounding this marketing effort that we have based our revenue estimates for the current year, as well as the next. The Golf course activities were seriously hampered by a very wet fall, and a very cold and wet winter, depressing early revenues. With the new marketing efforts, we are seeing an influx of new memberships, and anticipate making budget in the current year. Next year we anticipate an increase of about $18,000. The recommended budget for next year reflects an increase of 2.65%, primarily the result of the State retirement and health costs (cost to Golf Fund of about $4,000) and the 2.9% cost of living adjustment (cost to Golf Fund of about $9,000). CONCLUSION The FY10-11 budget takes an important step toward ensuring adequate resources are available to pay for the recent investments in public facilities and continued demand for public services. While the Town has been able to avoid tax increases in recent decades, the pressure of higher costs and flat revenues, additional debt service, and initiation of significant capital projects necessitates a substantial tax rate increase. I am confident that the adopted budget for FY10-11 will maintain basic services at a level consistent with the 2007-08 fiscal year. In addition, with the 7 cent tax increase, this budget takes a major step toward addressing the Town’s ongoing operating expenses and debt service costs for new public facilities. I would like to express my appreciation to the Finance & Information Services staff, particularly Department Director Rick Shreve, Deputy Finance Officer Sherry Williams, and Budget Assistant Laurel Mabery for their diligence and hard work in preparing this document for your review. Copies of this document will be posted on the Town’s website and available for public review in the clerk’s office and public library Respectfully Submitted,

Marcy D. Onieal Town Manager

14

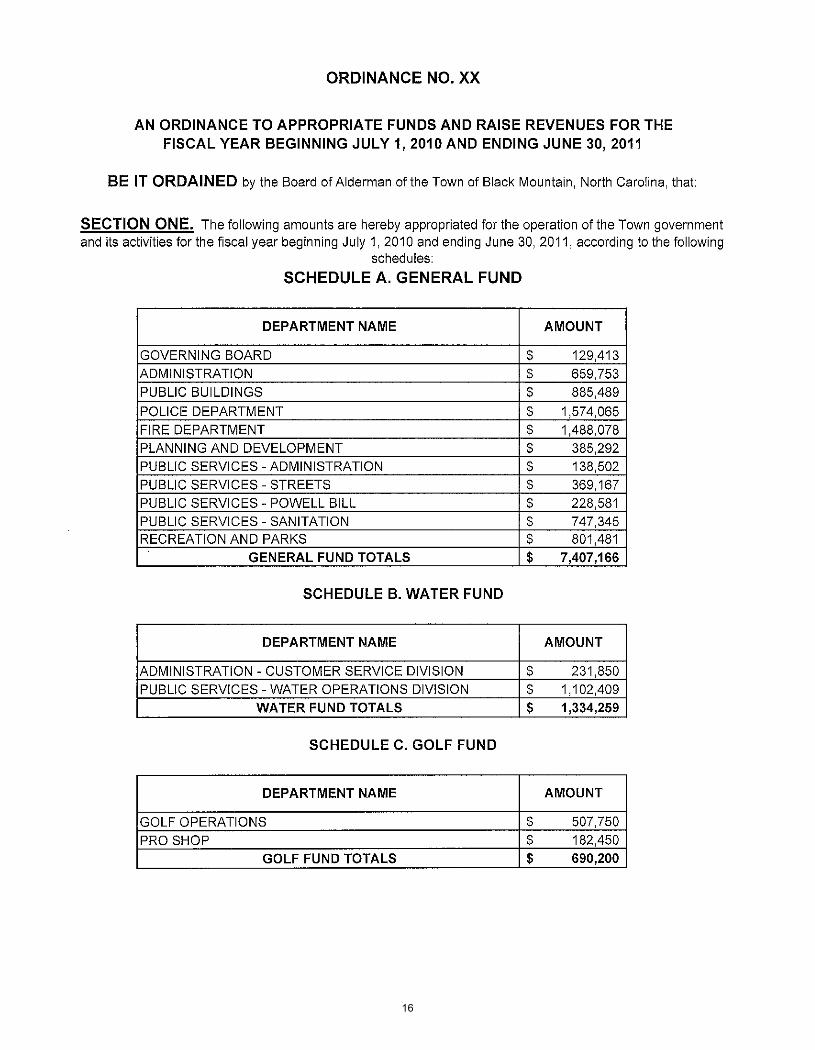

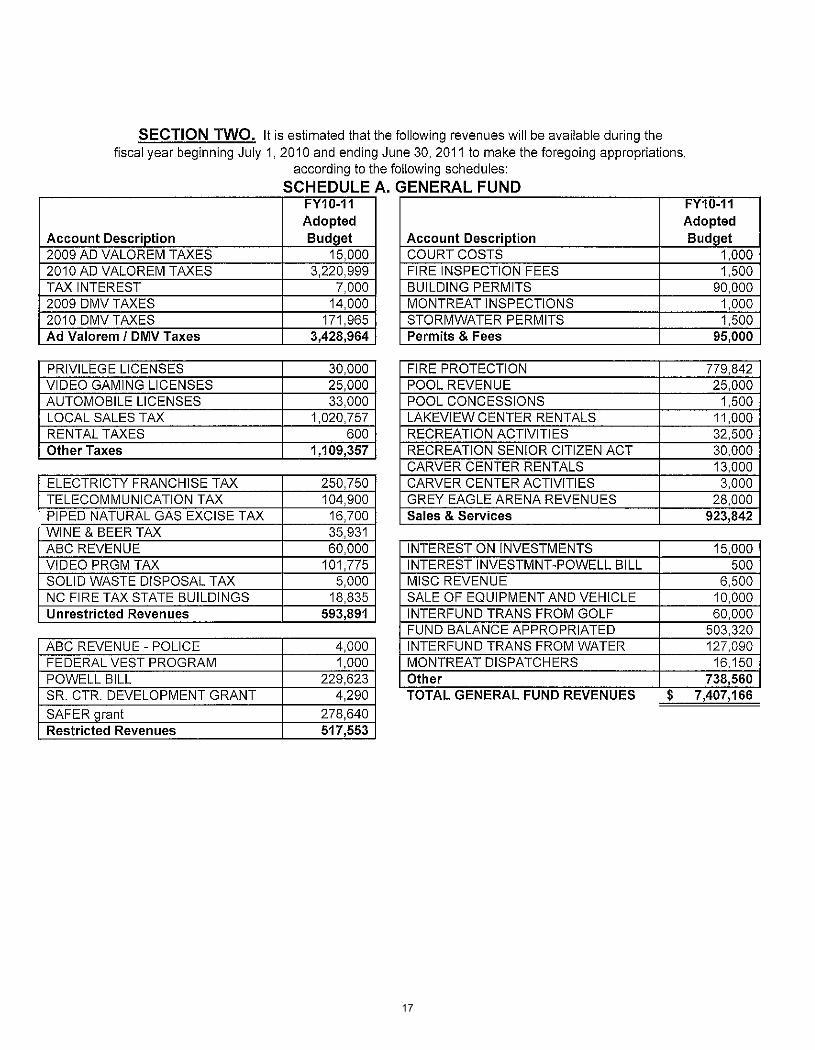

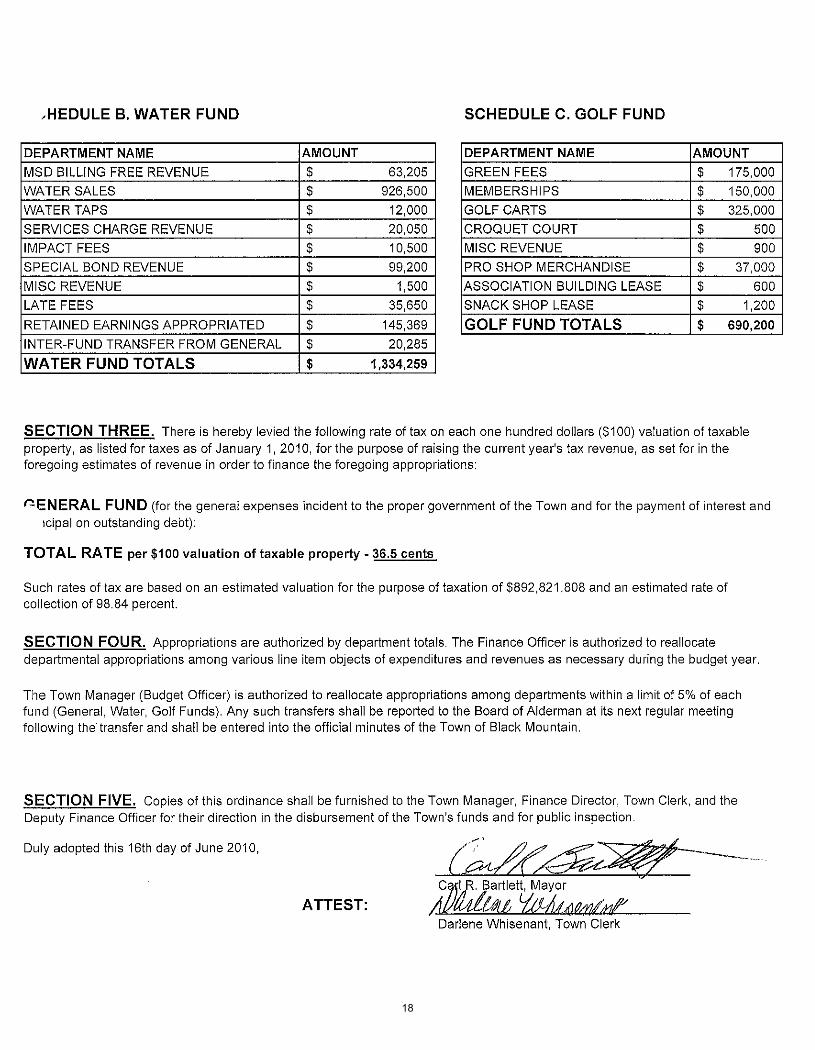

15

16

17

18

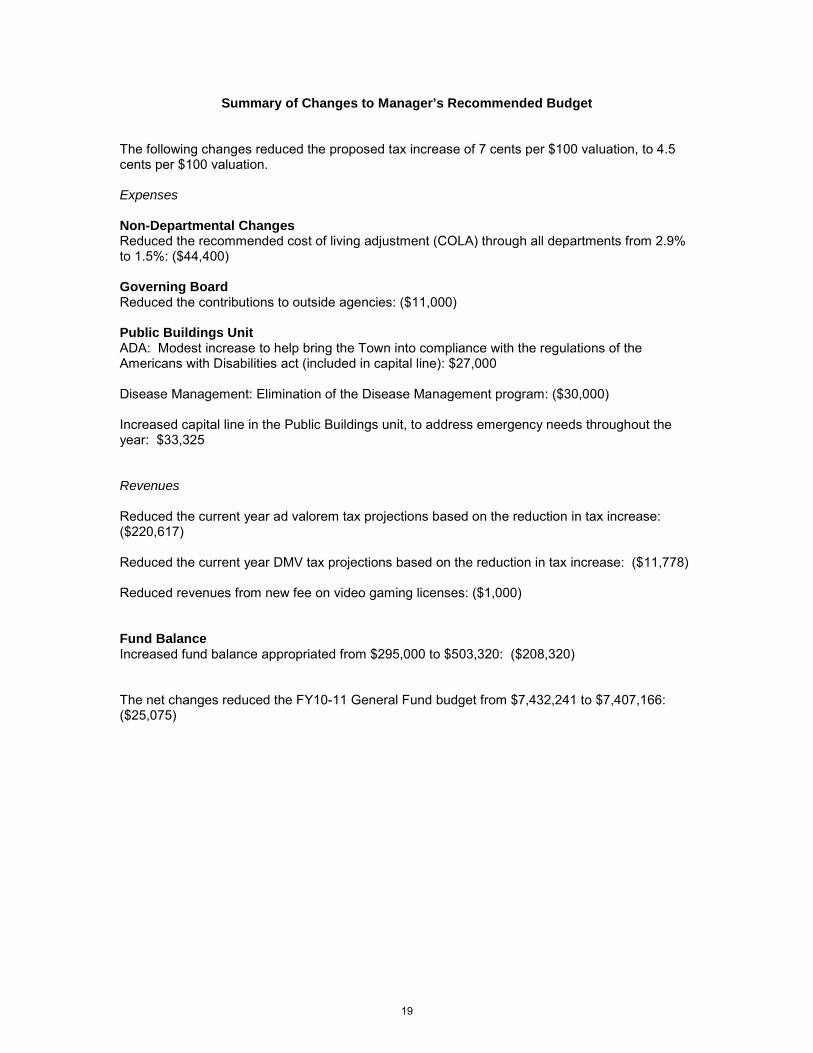

Summary of Changes to Manager’s Recommended Budget The following changes reduced the proposed tax increase of 7 cents per $100 valuation, to 4.5 cents per $100 valuation. Expenses Non-Departmental Changes Reduced the recommended cost of living adjustment (COLA) through all departments from 2.9% to 1.5%: ($44,400) Governing Board Reduced the contributions to outside agencies: ($11,000) Public Buildings Unit ADA: Modest increase to help bring the Town into compliance with the regulations of the Americans with Disabilities act (included in capital line): $27,000 Disease Management: Elimination of the Disease Management program: ($30,000) Increased capital line in the Public Buildings unit, to address emergency needs throughout the year: $33,325 Revenues Reduced the current year ad valorem tax projections based on the reduction in tax increase: ($220,617) Reduced the current year DMV tax projections based on the reduction in tax increase: ($11,778) Reduced revenues from new fee on video gaming licenses: ($1,000) Fund Balance Increased fund balance appropriated from $295,000 to $503,320: ($208,320) The net changes reduced the FY10-11 General Fund budget from $7,432,241 to $7,407,166: ($25,075)

19

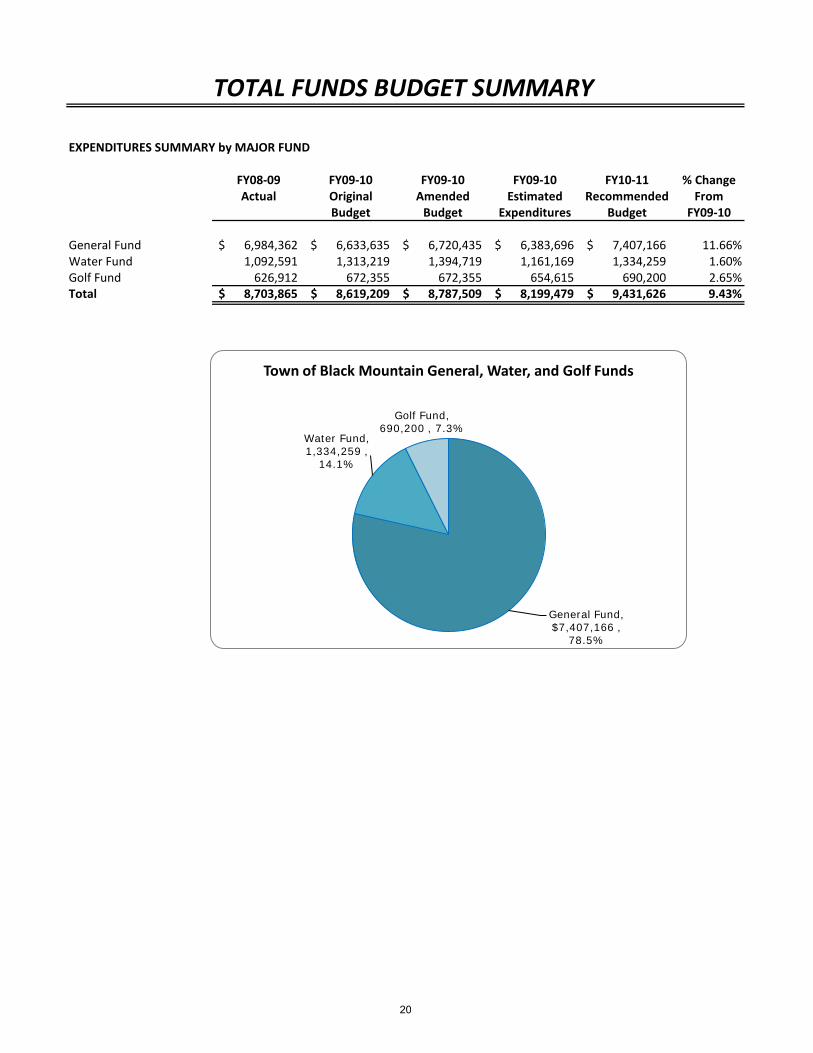

EXPENDITURES SUMMARY by MAJOR FUND

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Recommended From

Budget Budget Expenditures Budget FY09-10

General Fund 6,984,362$ 6,633,635$ 6,720,435$ 6,383,696$ 7,407,166$ 11.66%Water Fund 1,092,591 1,313,219 1,394,719 1,161,169 1,334,259 1.60%Golf Fund 626,912 672,355 672,355 654,615 690,200 2.65%Total 8,703,865$ 8,619,209$ 8,787,509$ 8,199,479$ 9,431,626$ 9.43%

TOTAL FUNDS BUDGET SUMMARY

General Fund, $7,407,166 ,

78.5%

Water Fund, 1,334,259 ,

14.1%

Golf Fund, 690,200 , 7.3%

Town of Black Mountain General, Water, and Golf Funds

20

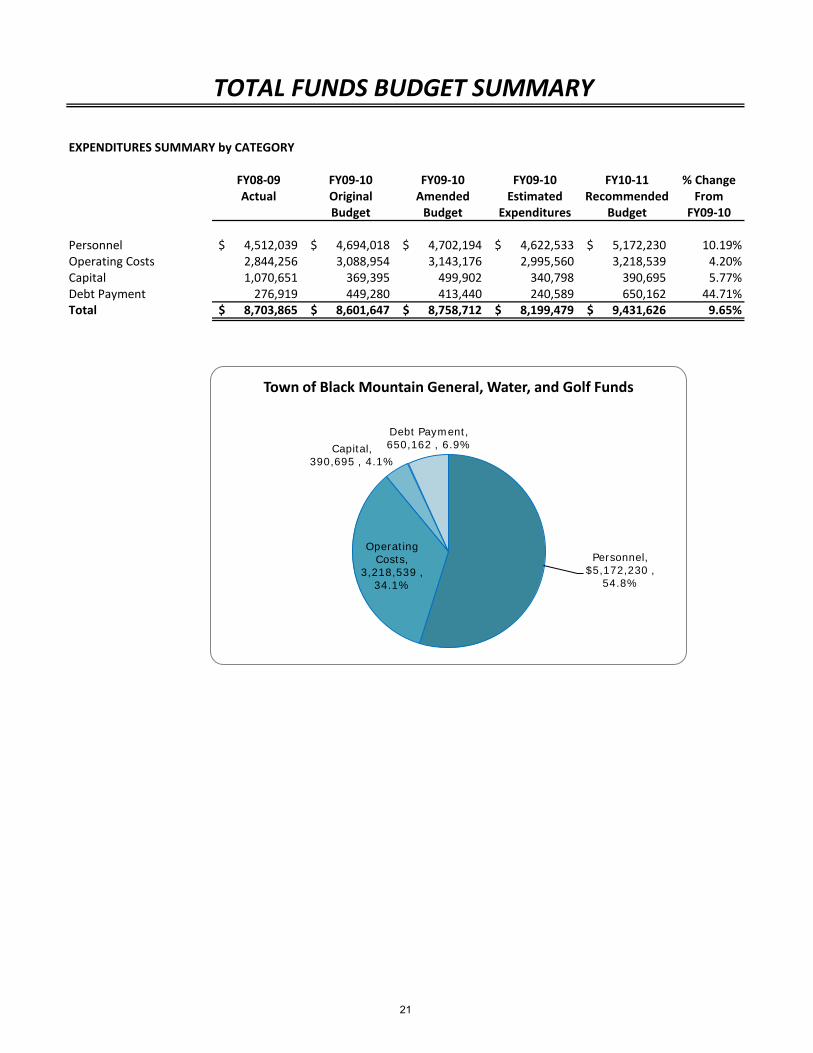

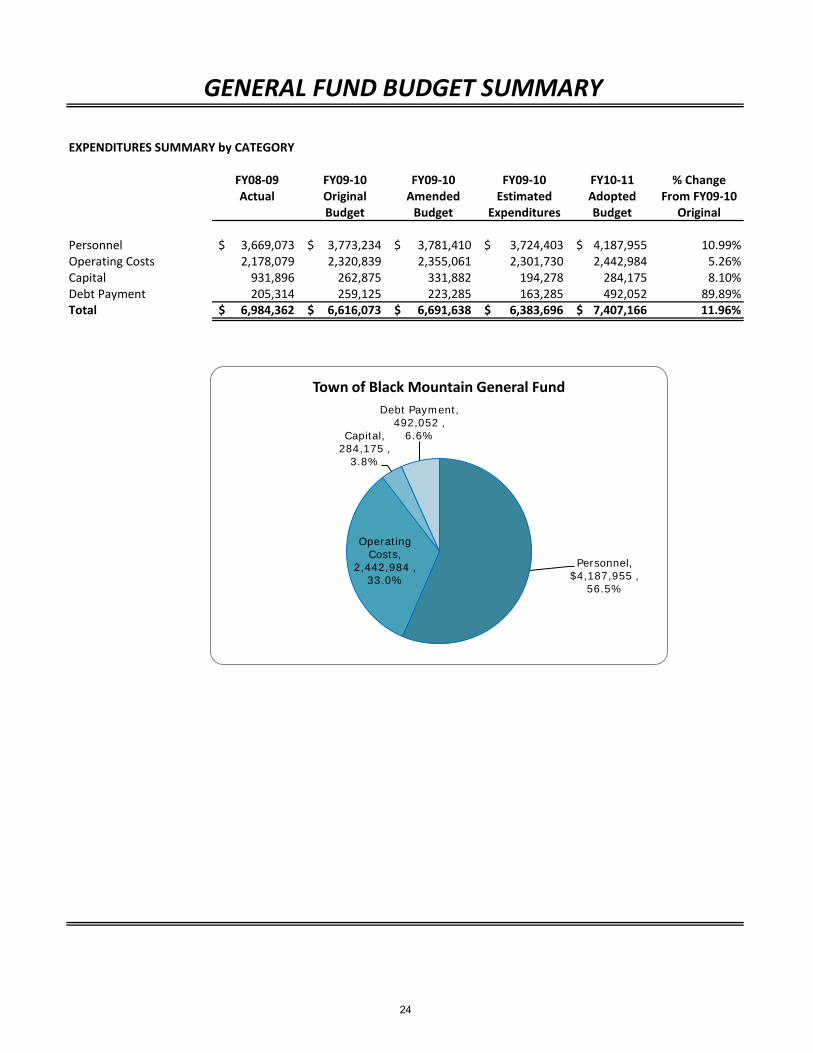

EXPENDITURES SUMMARY by CATEGORY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Recommended From

Budget Budget Expenditures Budget FY09-10

Personnel 4,512,039$ 4,694,018$ 4,702,194$ 4,622,533$ 5,172,230$ 10.19%Operating Costs 2,844,256 3,088,954 3,143,176 2,995,560 3,218,539 4.20%Capital 1,070,651 369,395 499,902 340,798 390,695 5.77%Debt Payment 276,919 449,280 413,440 240,589 650,162 44.71%Total 8,703,865$ 8,601,647$ 8,758,712$ 8,199,479$ 9,431,626$ 9.65%

TOTAL FUNDS BUDGET SUMMARY

Personnel, $5,172,230 ,

54.8%

Operating Costs,

3,218,539 , 34.1%

Capital, 390,695 , 4.1%

Debt Payment, 650,162 , 6.9%

Town of Black Mountain General, Water, and Golf Funds

21

THIS PAGE INTENTIONALLY LEFT BLANK.

22

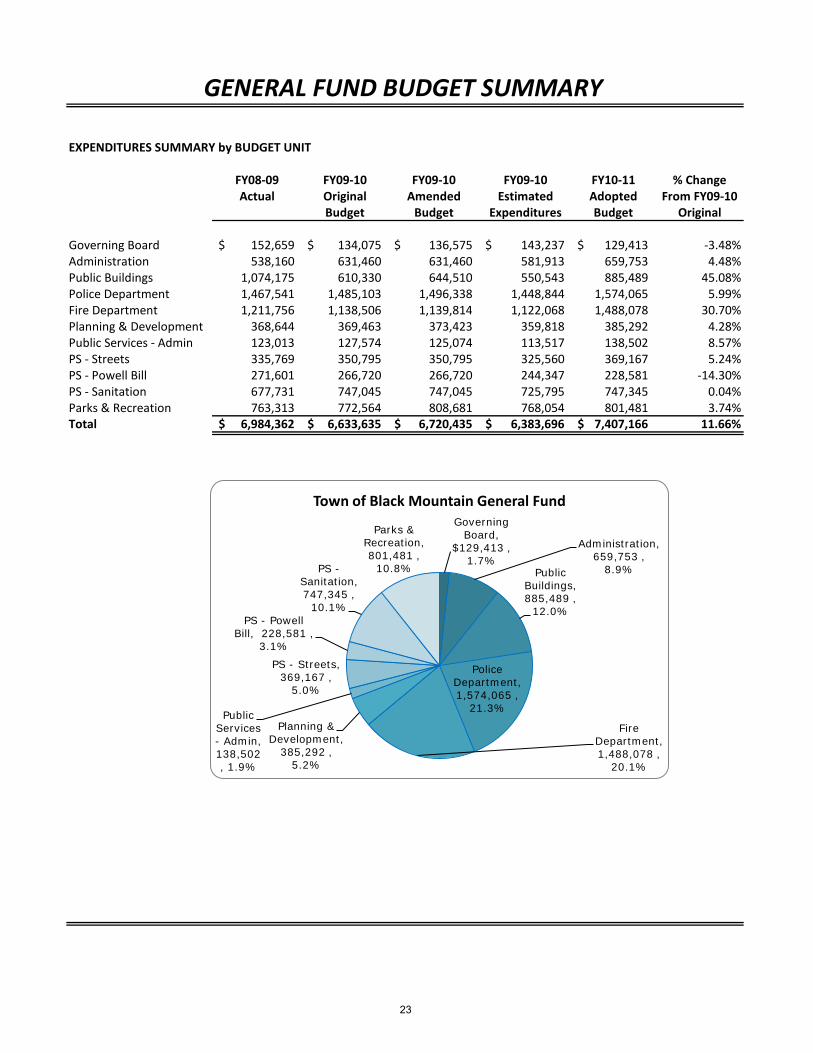

EXPENDITURES SUMMARY by BUDGET UNIT

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget Original

Governing Board 152,659$ 134,075$ 136,575$ 143,237$ 129,413$ -3.48%Administration 538,160 631,460 631,460 581,913 659,753 4.48%Public Buildings 1,074,175 610,330 644,510 550,543 885,489 45.08%Police Department 1,467,541 1,485,103 1,496,338 1,448,844 1,574,065 5.99%Fire Department 1,211,756 1,138,506 1,139,814 1,122,068 1,488,078 30.70%Planning & Development 368,644 369,463 373,423 359,818 385,292 4.28%Public Services - Admin 123,013 127,574 125,074 113,517 138,502 8.57%PS - Streets 335,769 350,795 350,795 325,560 369,167 5.24%PS - Powell Bill 271,601 266,720 266,720 244,347 228,581 -14.30%PS - Sanitation 677,731 747,045 747,045 725,795 747,345 0.04%Parks & Recreation 763,313 772,564 808,681 768,054 801,481 3.74%Total 6,984,362$ 6,633,635$ 6,720,435$ 6,383,696$ 7,407,166$ 11.66%

GENERAL FUND BUDGET SUMMARY

Governing Board,

$129,413 , 1.7%

Administration, 659,753 ,

8.9%Public Buildings, 885,489 ,

12.0%

Police Department, 1,574,065 ,

21.3%

Fire Department, 1,488,078 ,

20.1%

Planning & Development,

385,292 , 5.2%

Public Services - Admin, 138,502 , 1.9%

PS - Streets, 369,167 ,

5.0%

PS - Powell Bill, 228,581 ,

3.1%

PS -Sanitation, 747,345 ,

10.1%

Parks & Recreation, 801,481 ,

10.8%

Town of Black Mountain General Fund

23

EXPENDITURES SUMMARY by CATEGORY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget Original

Personnel 3,669,073$ 3,773,234$ 3,781,410$ 3,724,403$ 4,187,955$ 10.99%Operating Costs 2,178,079 2,320,839 2,355,061 2,301,730 2,442,984 5.26%Capital 931,896 262,875 331,882 194,278 284,175 8.10%Debt Payment 205,314 259,125 223,285 163,285 492,052 89.89%Total 6,984,362$ 6,616,073$ 6,691,638$ 6,383,696$ 7,407,166$ 11.96%

GENERAL FUND BUDGET SUMMARY

Personnel, $4,187,955 ,

56.5%

Operating Costs,

2,442,984 , 33.0%

Capital, 284,175 ,

3.8%

Debt Payment, 492,052 ,

6.6%

Town of Black Mountain General Fund

24

THIS PAGE INTENTIONALLY LEFT BLANK.

25

Account Description FY08-09 ActualFY09-10

Original Budget

FY09-10 Amended

Budget

FY09-10 Estimated Revenues

FY10-11 AdoptedBudget

% Change From FY09-10

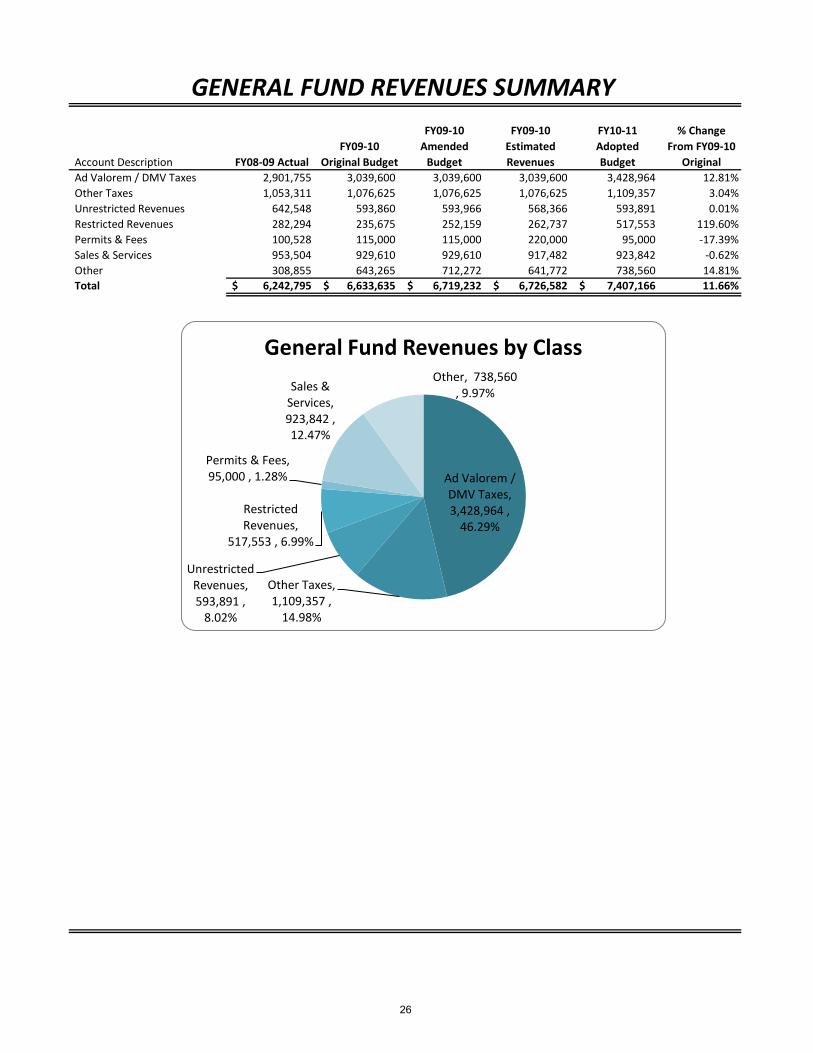

OriginalAd Valorem / DMV Taxes 2,901,755 3,039,600 3,039,600 3,039,600 3,428,964 12.81%Other Taxes 1,053,311 1,076,625 1,076,625 1,076,625 1,109,357 3.04%Unrestricted Revenues 642,548 593,860 593,966 568,366 593,891 0.01%Restricted Revenues 282,294 235,675 252,159 262,737 517,553 119.60%Permits & Fees 100,528 115,000 115,000 220,000 95,000 -17.39%Sales & Services 953,504 929,610 929,610 917,482 923,842 -0.62%Other 308,855 643,265 712,272 641,772 738,560 14.81%Total 6,242,795$ 6,633,635$ 6,719,232$ 6,726,582$ 7,407,166$ 11.66%

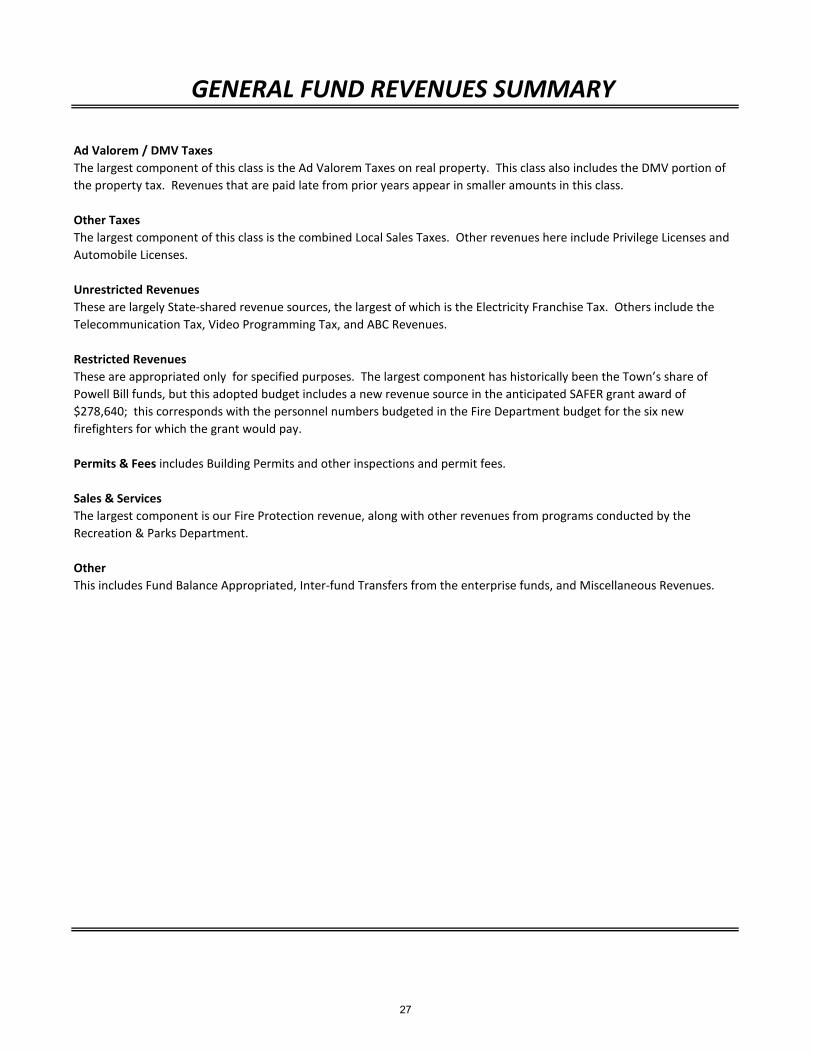

GENERAL FUND REVENUES SUMMARY

Ad Valorem / DMV Taxes, 3,428,964 ,

46.29%

Other Taxes, 1,109,357 ,

14.98%

Unrestricted Revenues, 593,891 ,

8.02%

Restricted Revenues,

517,553 , 6.99%

Permits & Fees, 95,000 , 1.28%

Sales & Services, 923,842 , 12.47%

Other, 738,560 , 9.97%

General Fund Revenues by Class

26

GENERAL FUND REVENUES SUMMARY

Ad Valorem / DMV TaxesThe largest component of this class is the Ad Valorem Taxes on real property. This class also includes the DMV portion of the property tax. Revenues that are paid late from prior years appear in smaller amounts in this class.

Other TaxesThe largest component of this class is the combined Local Sales Taxes. Other revenues here include Privilege Licenses and Automobile Licenses.

Unrestricted RevenuesThese are largely State-shared revenue sources, the largest of which is the Electricity Franchise Tax. Others include the Telecommunication Tax, Video Programming Tax, and ABC Revenues.

Restricted RevenuesThese are appropriated only for specified purposes. The largest component has historically been the Town’s share of Powell Bill funds, but this adopted budget includes a new revenue source in the anticipated SAFER grant award of $278,640; this corresponds with the personnel numbers budgeted in the Fire Department budget for the six new firefighters for which the grant would pay.

Permits & Fees includes Building Permits and other inspections and permit fees.

Sales & ServicesThe largest component is our Fire Protection revenue, along with other revenues from programs conducted by the Recreation & Parks Department.

OtherThis includes Fund Balance Appropriated, Inter-fund Transfers from the enterprise funds, and Miscellaneous Revenues.

27

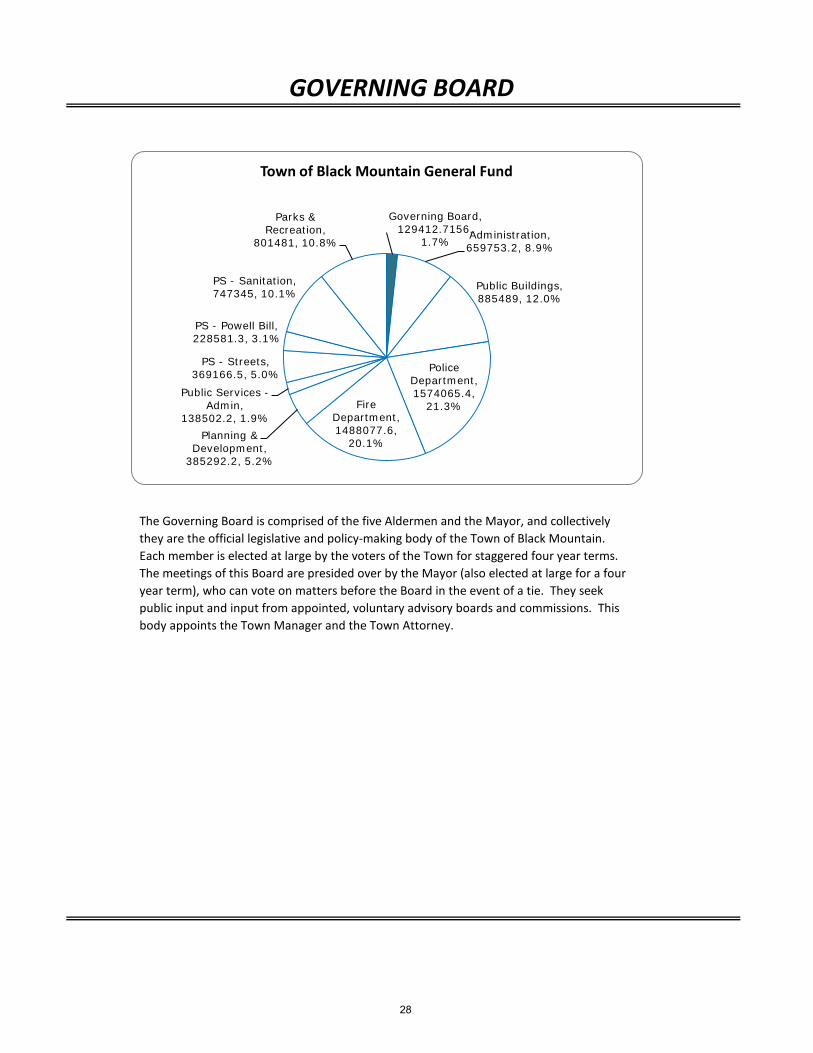

GOVERNING BOARD

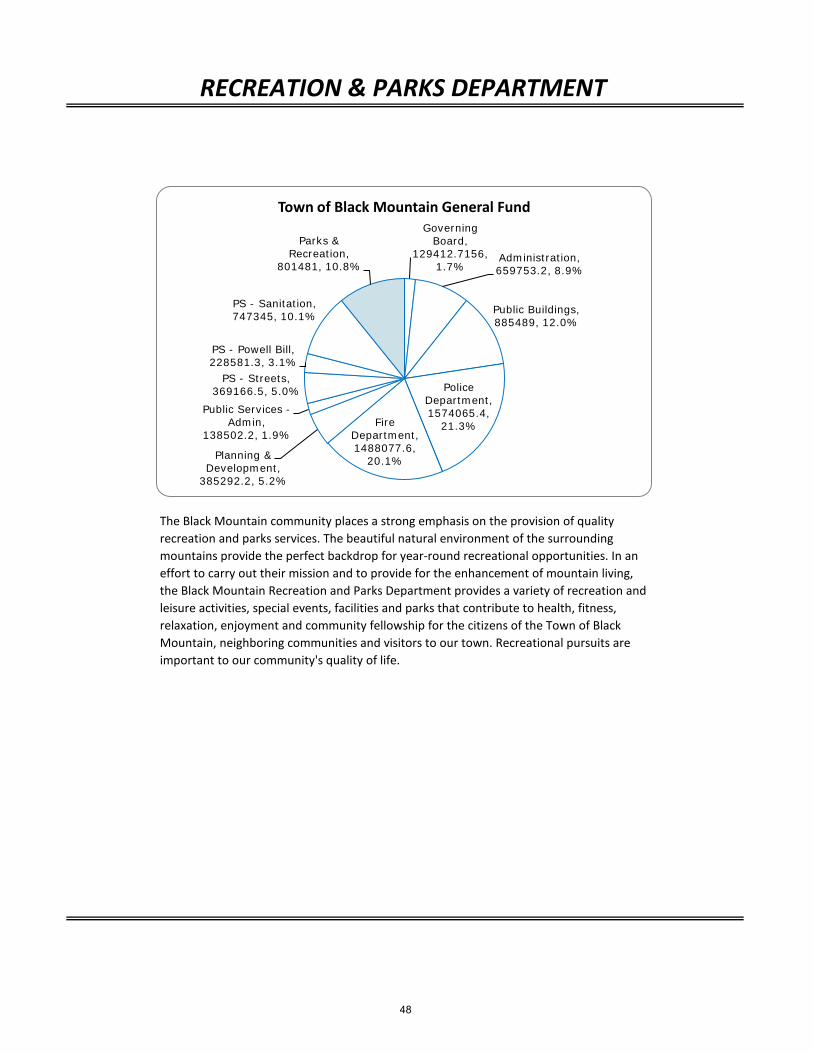

The Governing Board is comprised of the five Aldermen and the Mayor, and collectively they are the official legislative and policy-making body of the Town of Black Mountain. Each member is elected at large by the voters of the Town for staggered four year terms. The meetings of this Board are presided over by the Mayor (also elected at large for a four year term), who can vote on matters before the Board in the event of a tie. They seek public input and input from appointed, voluntary advisory boards and commissions. This body appoints the Town Manager and the Town Attorney.

Governing Board, 129412.7156,

1.7%Administration, 659753.2, 8.9%

Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire Department, 1488077.6,

20.1%Planning &

Development, 385292.2, 5.2%

Public Services -Admin,

138502.2, 1.9%

PS - Streets, 369166.5, 5.0%

PS - Powell Bill, 228581.3, 3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

28

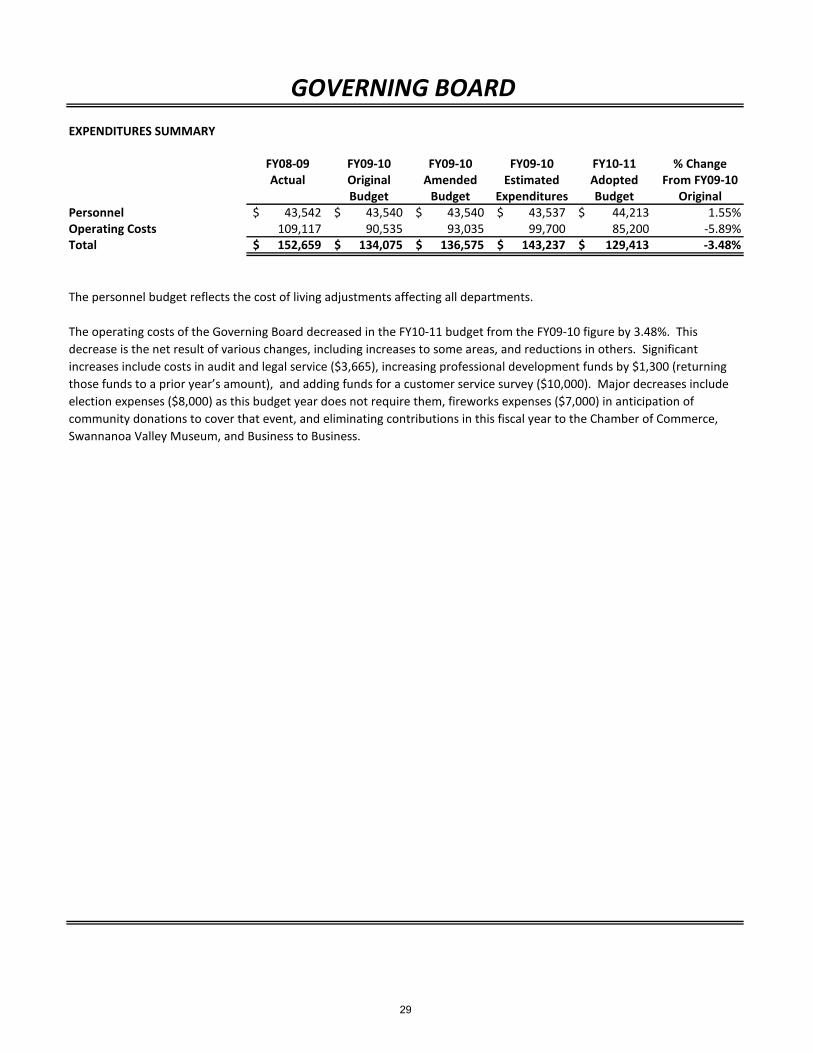

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 43,542$ 43,540$ 43,540$ 43,537$ 44,213$ 1.55%Operating Costs 109,117 90,535 93,035 99,700 85,200 -5.89%Total 152,659$ 134,075$ 136,575$ 143,237$ 129,413$ -3.48%

GOVERNING BOARD

The personnel budget reflects the cost of living adjustments affecting all departments.

The operating costs of the Governing Board decreased in the FY10-11 budget from the FY09-10 figure by 3.48%. This decrease is the net result of various changes, including increases to some areas, and reductions in others. Significant increases include costs in audit and legal service ($3,665), increasing professional development funds by $1,300 (returning those funds to a prior year’s amount), and adding funds for a customer service survey ($10,000). Major decreases include election expenses ($8,000) as this budget year does not require them, fireworks expenses ($7,000) in anticipation of community donations to cover that event, and eliminating contributions in this fiscal year to the Chamber of Commerce, Swannanoa Valley Museum, and Business to Business.

29

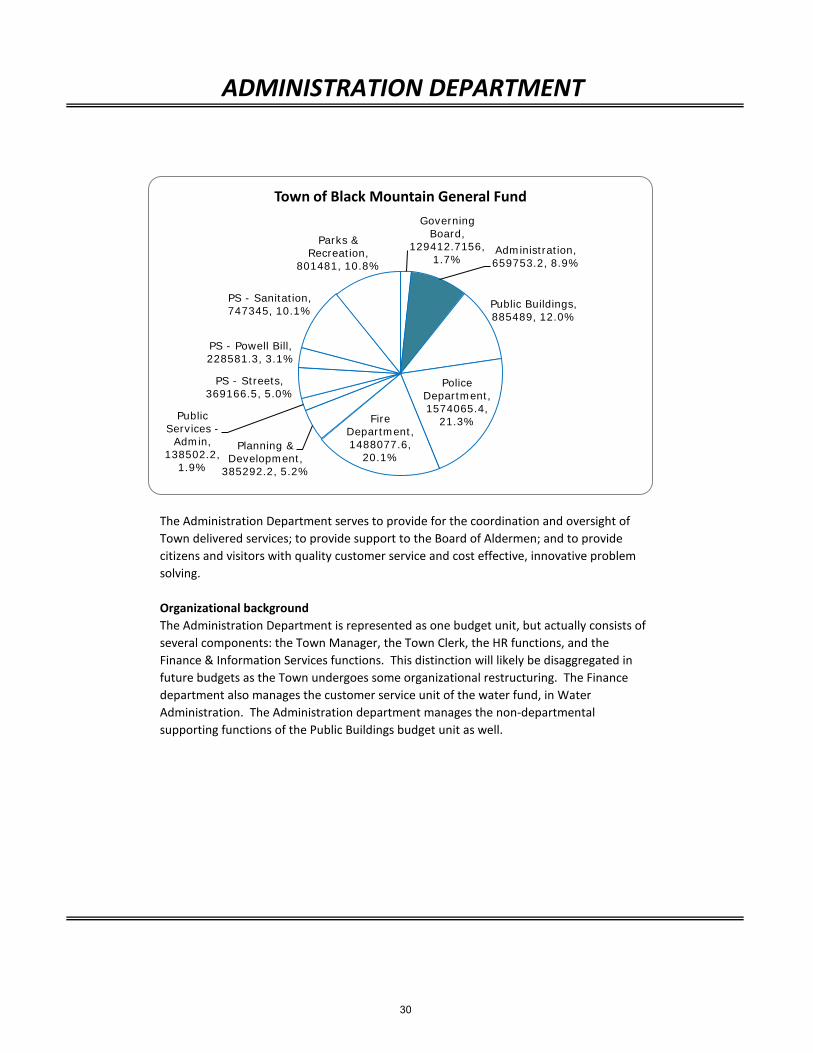

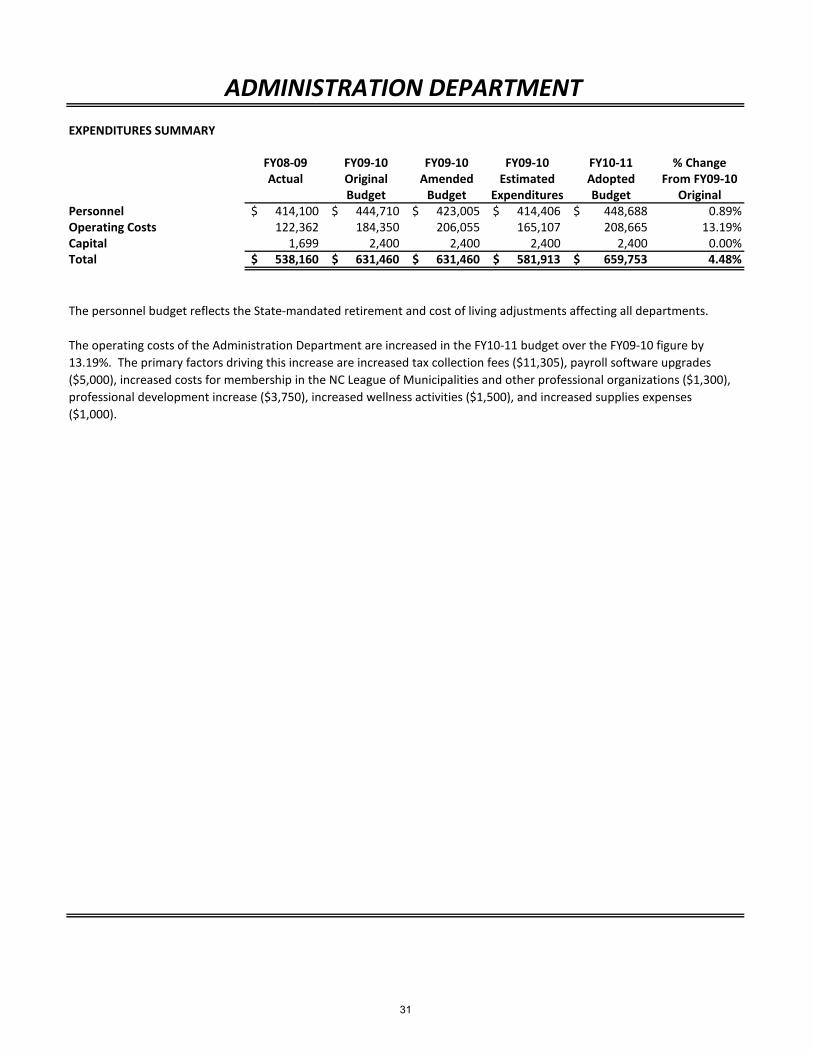

ADMINISTRATION DEPARTMENT

The Administration Department serves to provide for the coordination and oversight of Town delivered services; to provide support to the Board of Aldermen; and to provide citizens and visitors with quality customer service and cost effective, innovative problem solving.

Organizational backgroundThe Administration Department is represented as one budget unit, but actually consists of several components: the Town Manager, the Town Clerk, the HR functions, and the Finance & Information Services functions. This distinction will likely be disaggregated in future budgets as the Town undergoes some organizational restructuring. The Finance department also manages the customer service unit of the water fund, in Water Administration. The Administration department manages the non-departmental supporting functions of the Public Buildings budget unit as well.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2, 8.9%

Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire Department, 1488077.6,

20.1%Planning &

Development, 385292.2, 5.2%

Public Services -

Admin, 138502.2,

1.9%

PS - Streets, 369166.5, 5.0%

PS - Powell Bill, 228581.3, 3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

30

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 414,100$ 444,710$ 423,005$ 414,406$ 448,688$ 0.89%Operating Costs 122,362 184,350 206,055 165,107 208,665 13.19%Capital 1,699 2,400 2,400 2,400 2,400 0.00%Total 538,160$ 631,460$ 631,460$ 581,913$ 659,753$ 4.48%

ADMINISTRATION DEPARTMENT

The personnel budget reflects the State-mandated retirement and cost of living adjustments affecting all departments.

The operating costs of the Administration Department are increased in the FY10-11 budget over the FY09-10 figure by 13.19%. The primary factors driving this increase are increased tax collection fees ($11,305), payroll software upgrades ($5,000), increased costs for membership in the NC League of Municipalities and other professional organizations ($1,300), professional development increase ($3,750), increased wellness activities ($1,500), and increased supplies expenses ($1,000).

31

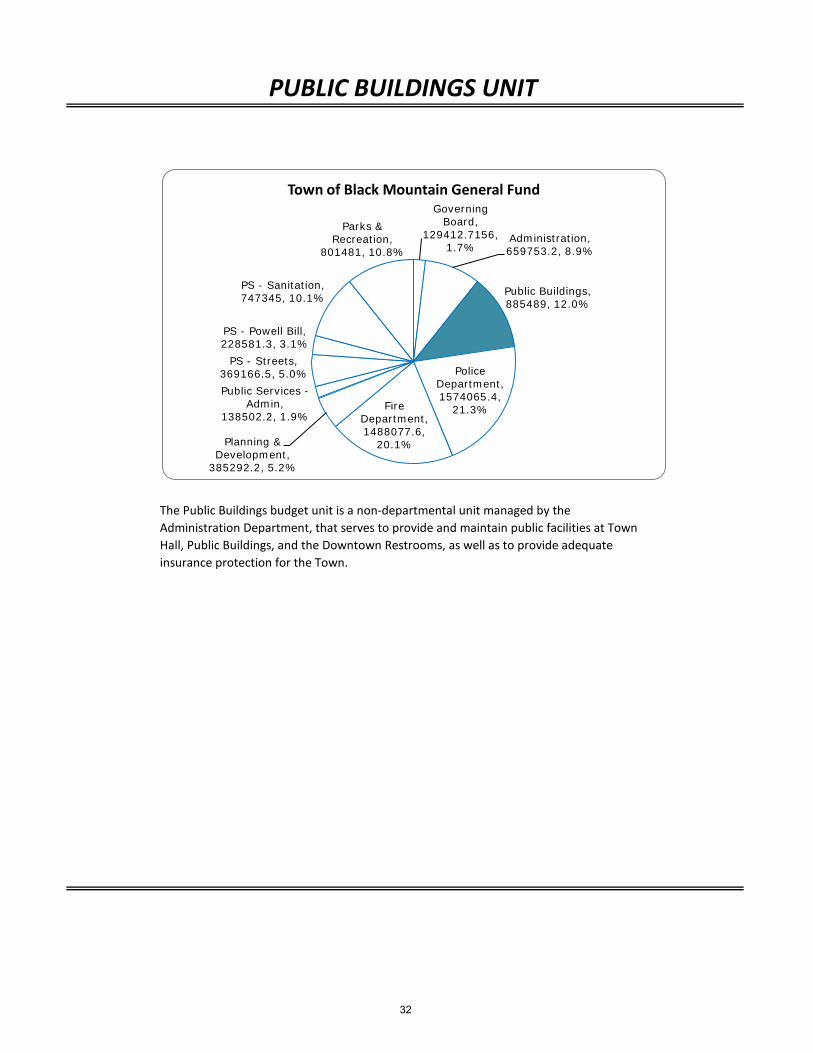

PUBLIC BUILDINGS UNIT

The Public Buildings budget unit is a non-departmental unit managed by the Administration Department, that serves to provide and maintain public facilities at Town Hall, Public Buildings, and the Downtown Restrooms, as well as to provide adequate insurance protection for the Town.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2, 8.9%

Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire Department, 1488077.6,

20.1%Planning & Development,

385292.2, 5.2%

Public Services -Admin,

138502.2, 1.9%

PS - Streets, 369166.5, 5.0%

PS - Powell Bill, 228581.3, 3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

32

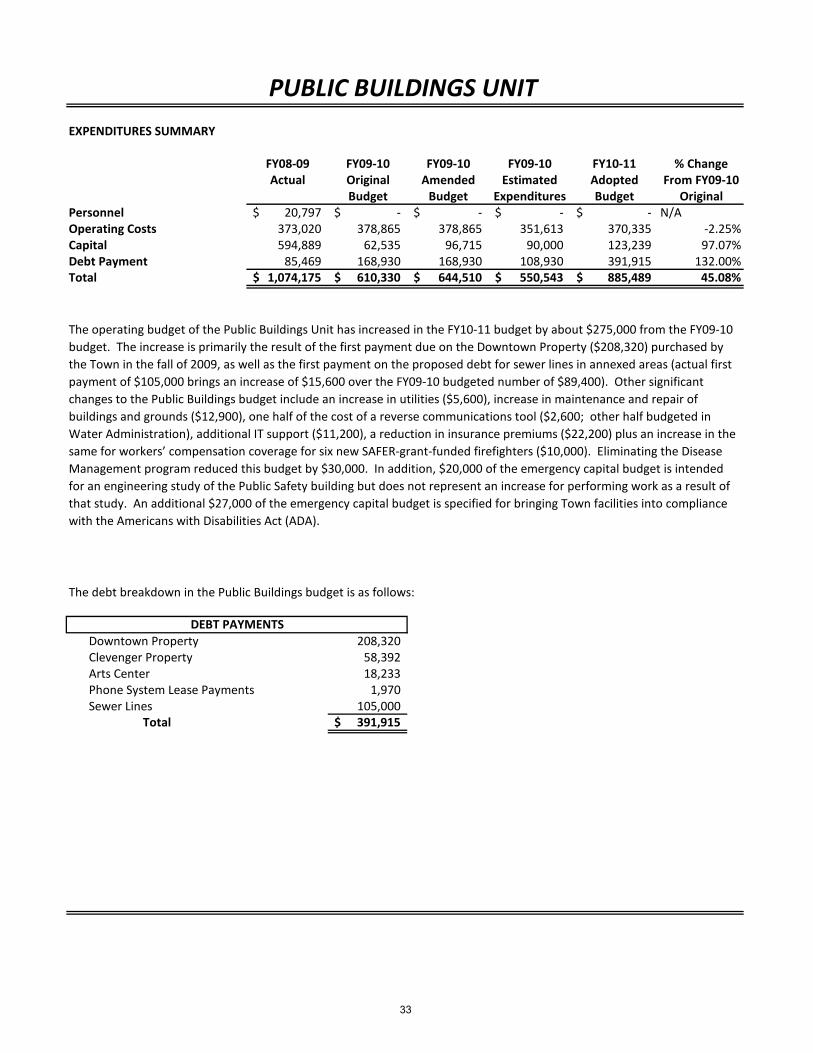

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 20,797$ -$ -$ -$ -$ N/AOperating Costs 373,020 378,865 378,865 351,613 370,335 -2.25%Capital 594,889 62,535 96,715 90,000 123,239 97.07%Debt Payment 85,469 168,930 168,930 108,930 391,915 132.00%Total 1,074,175$ 610,330$ 644,510$ 550,543$ 885,489$ 45.08%

The debt breakdown in the Public Buildings budget is as follows:

Downtown Property 208,320 Clevenger Property 58,392 Arts Center 18,233 Phone System Lease Payments 1,970 Sewer Lines 105,000

Total 391,915$

PUBLIC BUILDINGS UNIT

The operating budget of the Public Buildings Unit has increased in the FY10-11 budget by about $275,000 from the FY09-10 budget. The increase is primarily the result of the first payment due on the Downtown Property ($208,320) purchased by the Town in the fall of 2009, as well as the first payment on the proposed debt for sewer lines in annexed areas (actual first payment of $105,000 brings an increase of $15,600 over the FY09-10 budgeted number of $89,400). Other significant changes to the Public Buildings budget include an increase in utilities ($5,600), increase in maintenance and repair of buildings and grounds ($12,900), one half of the cost of a reverse communications tool ($2,600; other half budgeted in Water Administration), additional IT support ($11,200), a reduction in insurance premiums ($22,200) plus an increase in the same for workers’ compensation coverage for six new SAFER-grant-funded firefighters ($10,000). Eliminating the Disease Management program reduced this budget by $30,000. In addition, $20,000 of the emergency capital budget is intended for an engineering study of the Public Safety building but does not represent an increase for performing work as a result of that study. An additional $27,000 of the emergency capital budget is specified for bringing Town facilities into compliance with the Americans with Disabilities Act (ADA).

DEBT PAYMENTS

33

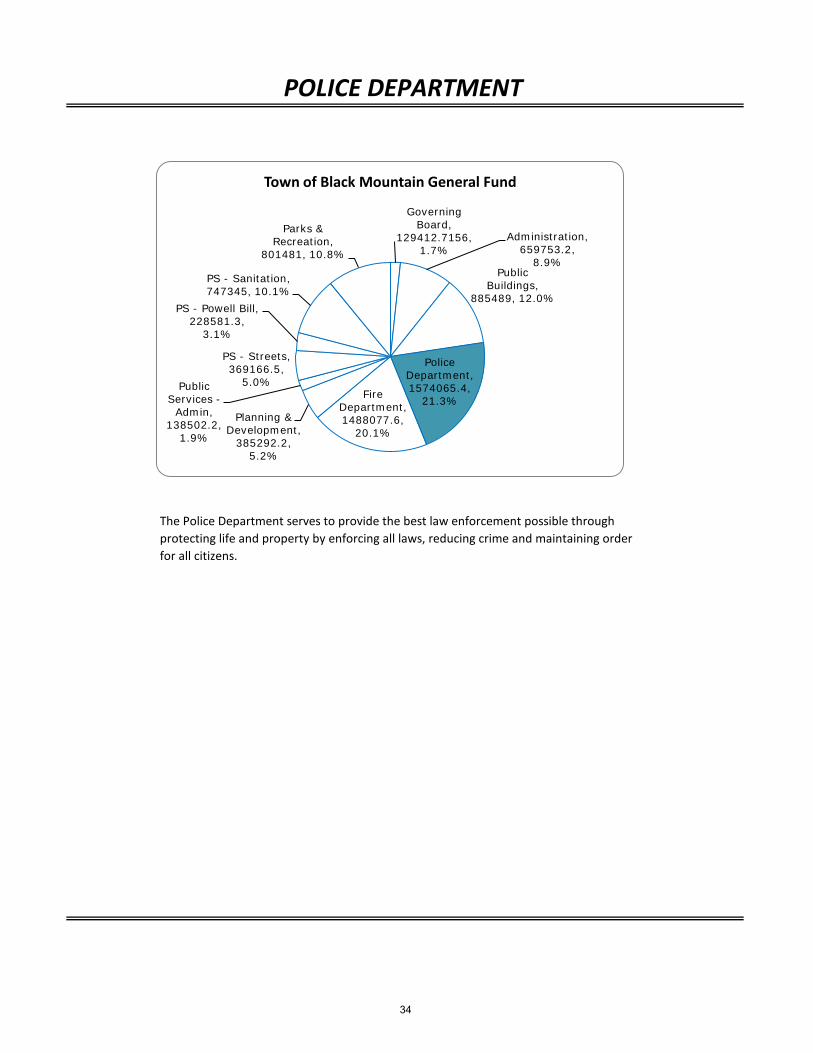

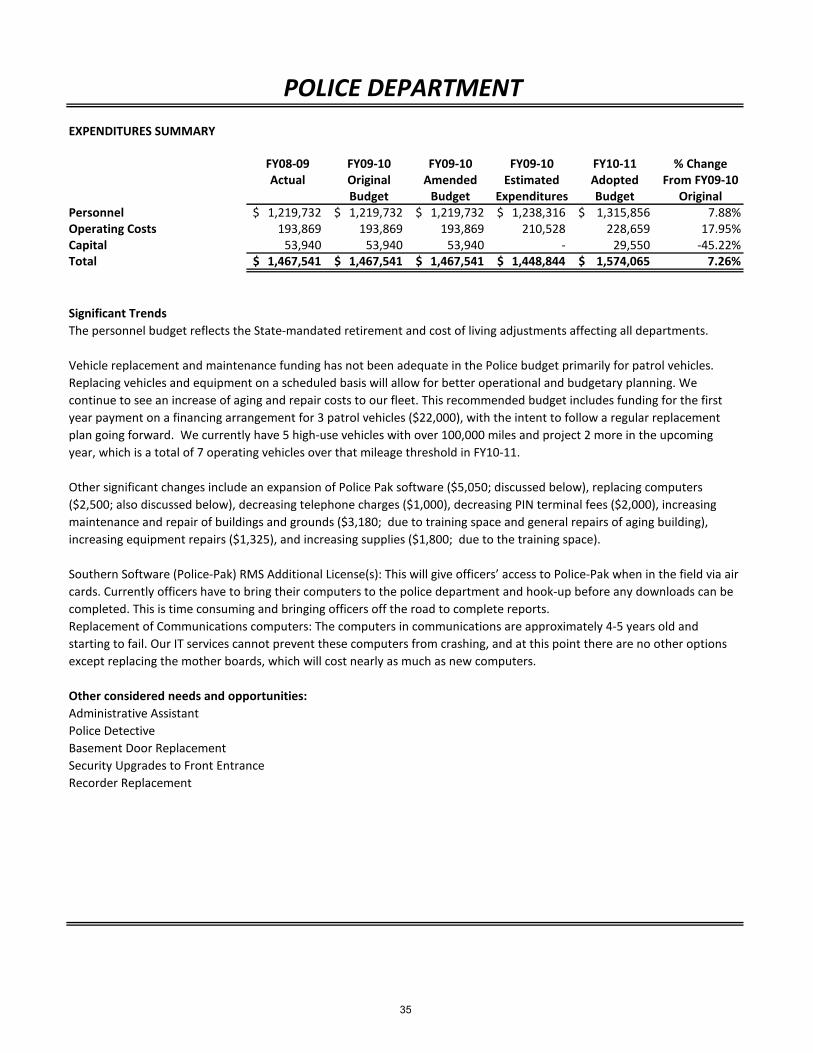

POLICE DEPARTMENT

The Police Department serves to provide the best law enforcement possible through protecting life and property by enforcing all laws, reducing crime and maintaining order for all citizens.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2,

8.9%Public

Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire

Department, 1488077.6,

20.1%Planning &

Development, 385292.2,

5.2%

Public Services -

Admin, 138502.2,

1.9%

PS - Streets, 369166.5,

5.0%

PS - Powell Bill, 228581.3,

3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

34

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 1,219,732$ 1,219,732$ 1,219,732$ 1,238,316$ 1,315,856$ 7.88%Operating Costs 193,869 193,869 193,869 210,528 228,659 17.95%Capital 53,940 53,940 53,940 - 29,550 -45.22%Total 1,467,541$ 1,467,541$ 1,467,541$ 1,448,844$ 1,574,065$ 7.26%

POLICE DEPARTMENT

Significant TrendsThe personnel budget reflects the State-mandated retirement and cost of living adjustments affecting all departments.

Vehicle replacement and maintenance funding has not been adequate in the Police budget primarily for patrol vehicles. Replacing vehicles and equipment on a scheduled basis will allow for better operational and budgetary planning. We continue to see an increase of aging and repair costs to our fleet. This recommended budget includes funding for the first year payment on a financing arrangement for 3 patrol vehicles ($22,000), with the intent to follow a regular replacement plan going forward. We currently have 5 high-use vehicles with over 100,000 miles and project 2 more in the upcoming year, which is a total of 7 operating vehicles over that mileage threshold in FY10-11.

Other significant changes include an expansion of Police Pak software ($5,050; discussed below), replacing computers ($2,500; also discussed below), decreasing telephone charges ($1,000), decreasing PIN terminal fees ($2,000), increasing maintenance and repair of buildings and grounds ($3,180; due to training space and general repairs of aging building), increasing equipment repairs ($1,325), and increasing supplies ($1,800; due to the training space).

Southern Software (Police-Pak) RMS Additional License(s): This will give officers’ access to Police-Pak when in the field via air cards. Currently officers have to bring their computers to the police department and hook-up before any downloads can be completed. This is time consuming and bringing officers off the road to complete reports.Replacement of Communications computers: The computers in communications are approximately 4-5 years old and starting to fail. Our IT services cannot prevent these computers from crashing, and at this point there are no other options except replacing the mother boards, which will cost nearly as much as new computers.

Other considered needs and opportunities:Administrative AssistantPolice DetectiveBasement Door ReplacementSecurity Upgrades to Front EntranceRecorder Replacement

35

FIRE DEPARTMENT

Established in 1919, the Black Mountain Fire Department is a combination paid and volunteer organization. The department has achieved a Class 4 rating for the Town’s fire protection. They provide fire suppression and prevention, rescue, confined space and search services to the community. They protect some 27 square miles which include two fire districts – the Town of Black Mountain and the East Buncombe Fire District – as well as the Town of Montreat. Several large manufacturing facilities, conference centers and state facilities are within our protection areas.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2, 8.9%

Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire Department, 1488077.6,

20.1%Planning &

Development, 385292.2, 5.2%

Public Services -Admin,

138502.2, 1.9%

PS - Streets, 369166.5, 5.0%

PS - Powell Bill, 228581.3, 3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

36

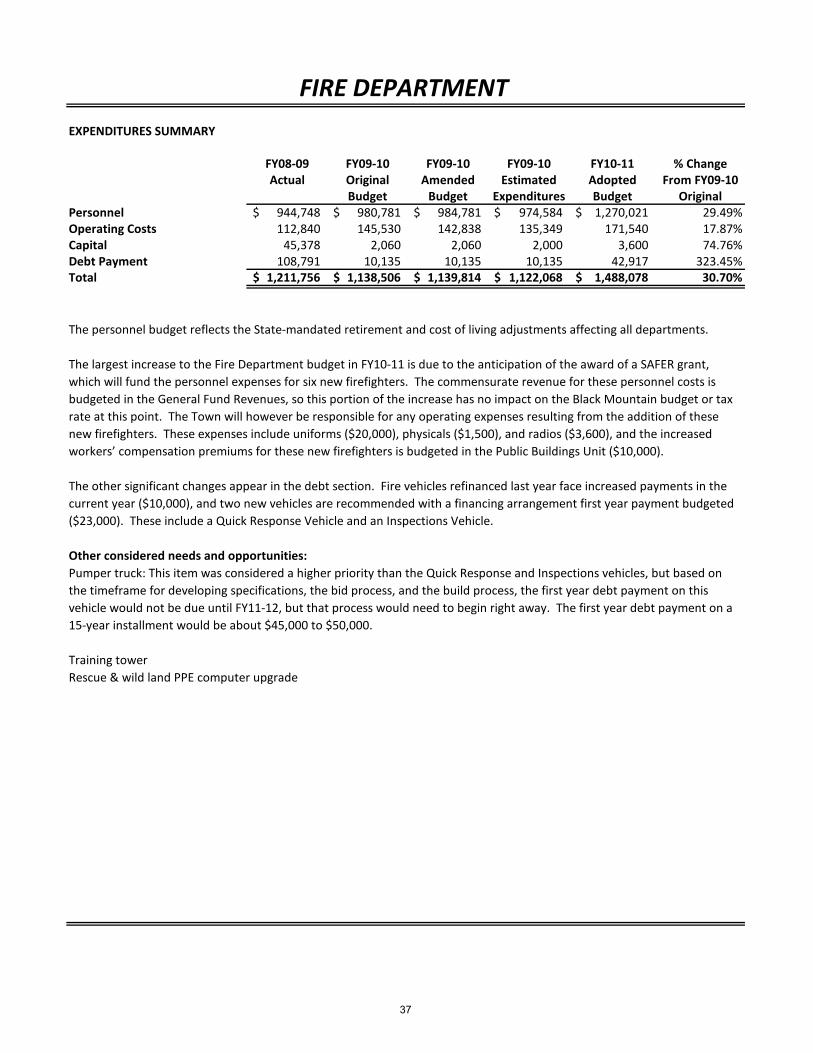

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 944,748$ 980,781$ 984,781$ 974,584$ 1,270,021$ 29.49%Operating Costs 112,840 145,530 142,838 135,349 171,540 17.87%Capital 45,378 2,060 2,060 2,000 3,600 74.76%Debt Payment 108,791 10,135 10,135 10,135 42,917 323.45%Total 1,211,756$ 1,138,506$ 1,139,814$ 1,122,068$ 1,488,078$ 30.70%

FIRE DEPARTMENT

The personnel budget reflects the State-mandated retirement and cost of living adjustments affecting all departments.

The largest increase to the Fire Department budget in FY10-11 is due to the anticipation of the award of a SAFER grant, which will fund the personnel expenses for six new firefighters. The commensurate revenue for these personnel costs is budgeted in the General Fund Revenues, so this portion of the increase has no impact on the Black Mountain budget or tax rate at this point. The Town will however be responsible for any operating expenses resulting from the addition of these new firefighters. These expenses include uniforms ($20,000), physicals ($1,500), and radios ($3,600), and the increased workers’ compensation premiums for these new firefighters is budgeted in the Public Buildings Unit ($10,000).

The other significant changes appear in the debt section. Fire vehicles refinanced last year face increased payments in the current year ($10,000), and two new vehicles are recommended with a financing arrangement first year payment budgeted ($23,000). These include a Quick Response Vehicle and an Inspections Vehicle.

Other considered needs and opportunities:Pumper truck: This item was considered a higher priority than the Quick Response and Inspections vehicles, but based on the timeframe for developing specifications, the bid process, and the build process, the first year debt payment on this vehicle would not be due until FY11-12, but that process would need to begin right away. The first year debt payment on a 15-year installment would be about $45,000 to $50,000.

Training towerRescue & wild land PPE computer upgrade

37

PLANNING DEPARTMENT

The Planning and Development Services work to protect the health, safety and welfare of the citizens of Black Mountain by developing and implementing local plans and regulations that guide building construction, subdivision and zoning district requirements within the Town.

This department also provides staff support for the Town’s Housing Commission, Historic Preservation Commission, Planning Board and Zoning Board of Adjustment. Conditional Use Permits, appeals, variances, rezoning requests and historic property designations are some of the requests we manage on behalf of these committees and boards. In conjunction with the Planning Board, the Department works on zoning amendments, new ordinances and other land use planning tools and documents.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2,

8.9%Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire

Department, 1488077.6,

20.1%

Planning & Development,

385292.2, 5.2%

Public Services -

Admin, 138502.2,

1.9%

PS - Streets, 369166.5,

5.0%

PS - Powell Bill, 228581.3,

3.1%

PS -Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

38

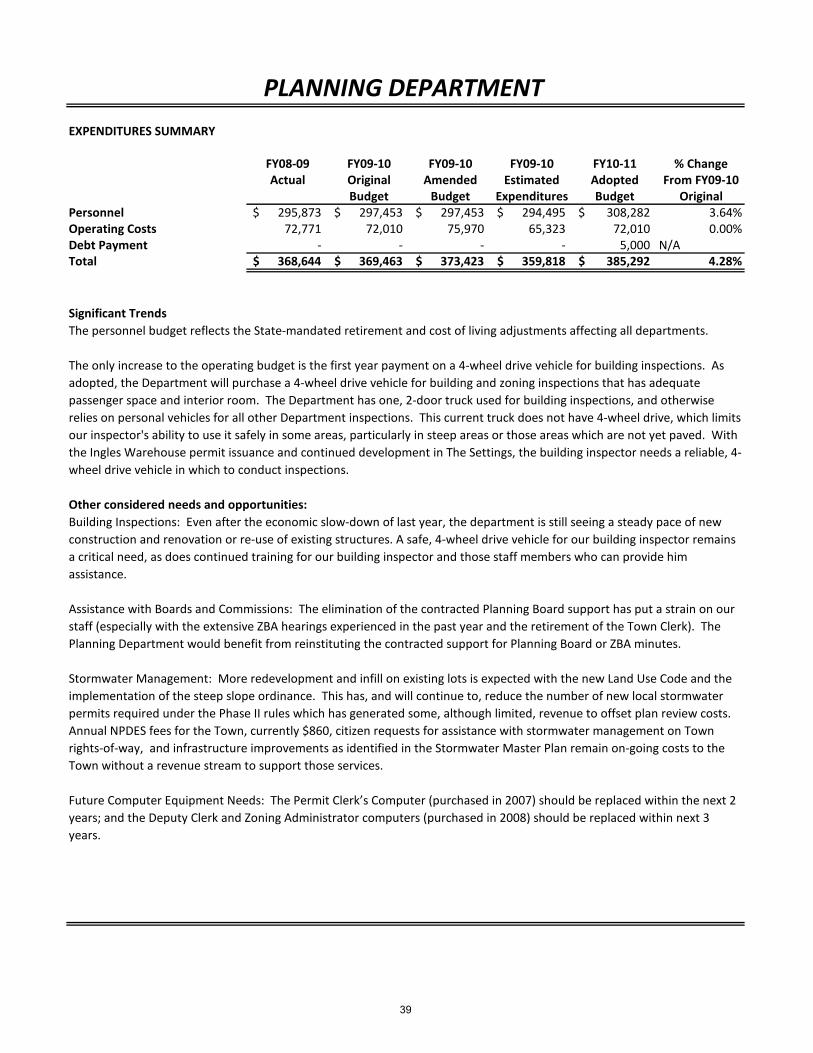

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 295,873$ 297,453$ 297,453$ 294,495$ 308,282$ 3.64%Operating Costs 72,771 72,010 75,970 65,323 72,010 0.00%Debt Payment - - - - 5,000 N/ATotal 368,644$ 369,463$ 373,423$ 359,818$ 385,292$ 4.28%

PLANNING DEPARTMENT

Significant TrendsThe personnel budget reflects the State-mandated retirement and cost of living adjustments affecting all departments.

The only increase to the operating budget is the first year payment on a 4-wheel drive vehicle for building inspections. As adopted, the Department will purchase a 4-wheel drive vehicle for building and zoning inspections that has adequate passenger space and interior room. The Department has one, 2-door truck used for building inspections, and otherwise relies on personal vehicles for all other Department inspections. This current truck does not have 4-wheel drive, which limits our inspector's ability to use it safely in some areas, particularly in steep areas or those areas which are not yet paved. With the Ingles Warehouse permit issuance and continued development in The Settings, the building inspector needs a reliable, 4-wheel drive vehicle in which to conduct inspections.

Other considered needs and opportunities:Building Inspections: Even after the economic slow-down of last year, the department is still seeing a steady pace of new construction and renovation or re-use of existing structures. A safe, 4-wheel drive vehicle for our building inspector remains a critical need, as does continued training for our building inspector and those staff members who can provide him assistance.

Assistance with Boards and Commissions: The elimination of the contracted Planning Board support has put a strain on our staff (especially with the extensive ZBA hearings experienced in the past year and the retirement of the Town Clerk). The Planning Department would benefit from reinstituting the contracted support for Planning Board or ZBA minutes.

Stormwater Management: More redevelopment and infill on existing lots is expected with the new Land Use Code and the implementation of the steep slope ordinance. This has, and will continue to, reduce the number of new local stormwater permits required under the Phase II rules which has generated some, although limited, revenue to offset plan review costs. Annual NPDES fees for the Town, currently $860, citizen requests for assistance with stormwater management on Town rights-of-way, and infrastructure improvements as identified in the Stormwater Master Plan remain on-going costs to the Town without a revenue stream to support those services.

Future Computer Equipment Needs: The Permit Clerk’s Computer (purchased in 2007) should be replaced within the next 2 years; and the Deputy Clerk and Zoning Administrator computers (purchased in 2008) should be replaced within next 3 years.

39

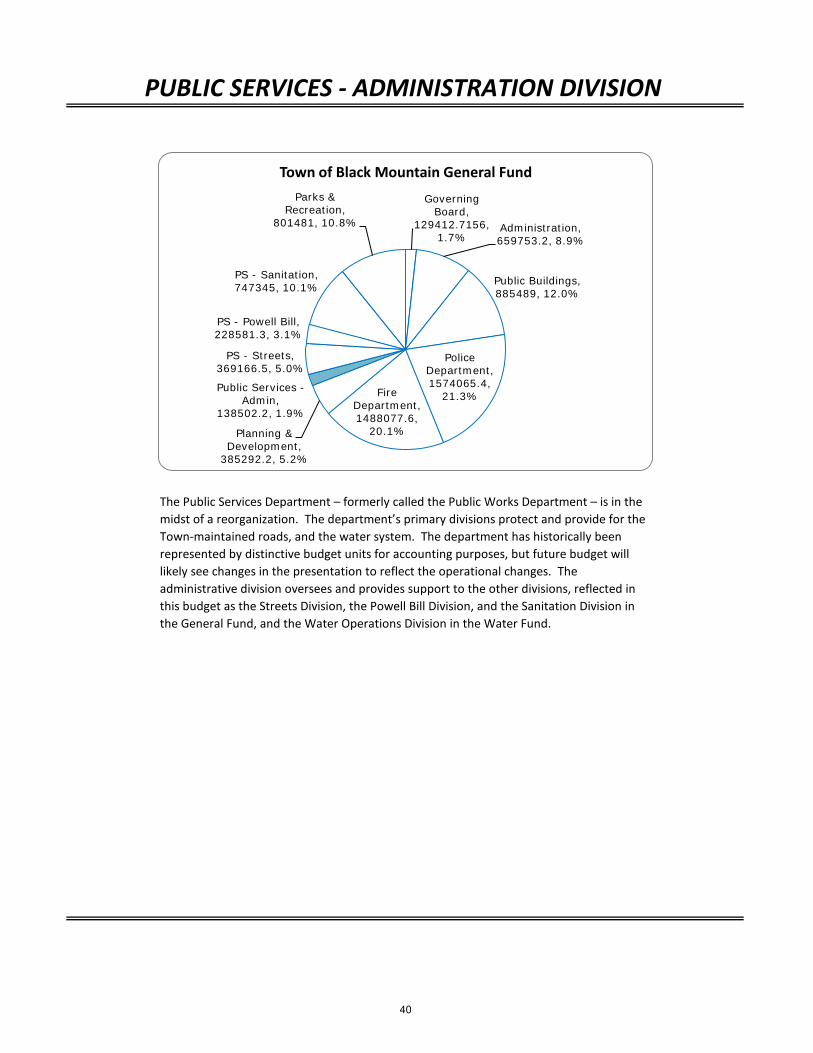

PUBLIC SERVICES - ADMINISTRATION DIVISION

The Public Services Department – formerly called the Public Works Department – is in the midst of a reorganization. The department’s primary divisions protect and provide for the Town-maintained roads, and the water system. The department has historically been represented by distinctive budget units for accounting purposes, but future budget will likely see changes in the presentation to reflect the operational changes. The administrative division oversees and provides support to the other divisions, reflected in this budget as the Streets Division, the Powell Bill Division, and the Sanitation Division in the General Fund, and the Water Operations Division in the Water Fund.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2, 8.9%

Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire Department, 1488077.6,

20.1%Planning & Development,

385292.2, 5.2%

Public Services -Admin,

138502.2, 1.9%

PS - Streets, 369166.5, 5.0%

PS - Powell Bill, 228581.3, 3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

40

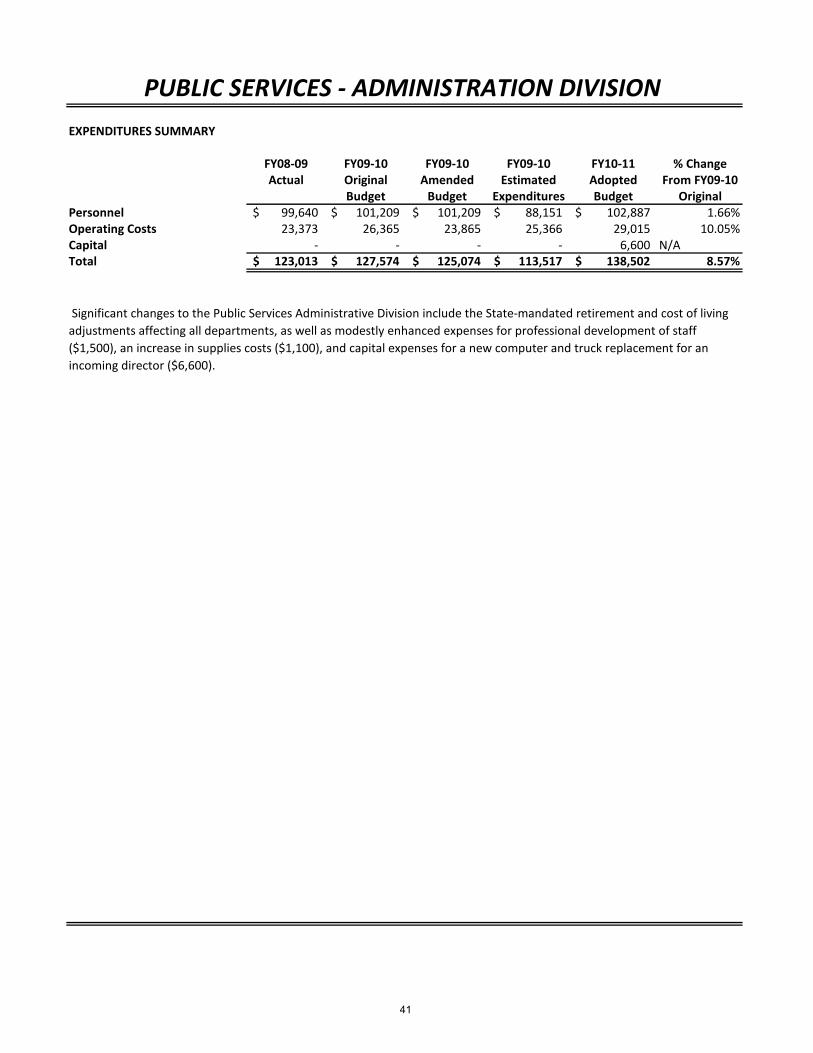

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 99,640$ 101,209$ 101,209$ 88,151$ 102,887$ 1.66%Operating Costs 23,373 26,365 23,865 25,366 29,015 10.05%Capital - - - - 6,600 N/ATotal 123,013$ 127,574$ 125,074$ 113,517$ 138,502$ 8.57%

PUBLIC SERVICES - ADMINISTRATION DIVISION

Significant changes to the Public Services Administrative Division include the State-mandated retirement and cost of living adjustments affecting all departments, as well as modestly enhanced expenses for professional development of staff ($1,500), an increase in supplies costs ($1,100), and capital expenses for a new computer and truck replacement for an incoming director ($6,600).

41

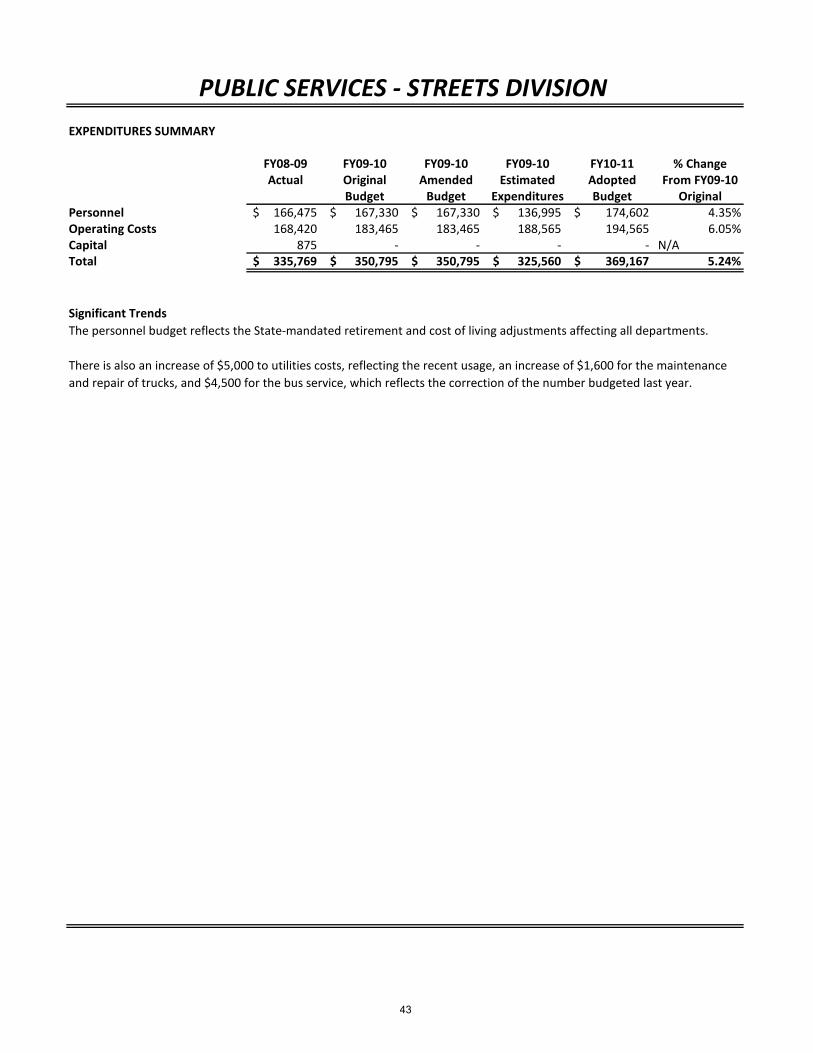

PUBLIC SERVICES - STREETS DIVISION

The Streets Division is one of the two major divisions of the Public Services Department.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2,

8.9%

Public Buildings,

885489, 12.0%

Police Department, 1574065.4,

21.3%Fire

Department, 1488077.6,

20.1%Planning &

Development, 385292.2,

5.2%

Public Services -

Admin, 138502.2,

1.9%

PS - Streets, 369166.5,

5.0%

PS - Powell Bill, 228581.3,

3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

42

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 166,475$ 167,330$ 167,330$ 136,995$ 174,602$ 4.35%Operating Costs 168,420 183,465 183,465 188,565 194,565 6.05%Capital 875 - - - - N/ATotal 335,769$ 350,795$ 350,795$ 325,560$ 369,167$ 5.24%

PUBLIC SERVICES - STREETS DIVISION

Significant TrendsThe personnel budget reflects the State-mandated retirement and cost of living adjustments affecting all departments.

There is also an increase of $5,000 to utilities costs, reflecting the recent usage, an increase of $1,600 for the maintenance and repair of trucks, and $4,500 for the bus service, which reflects the correction of the number budgeted last year.

43

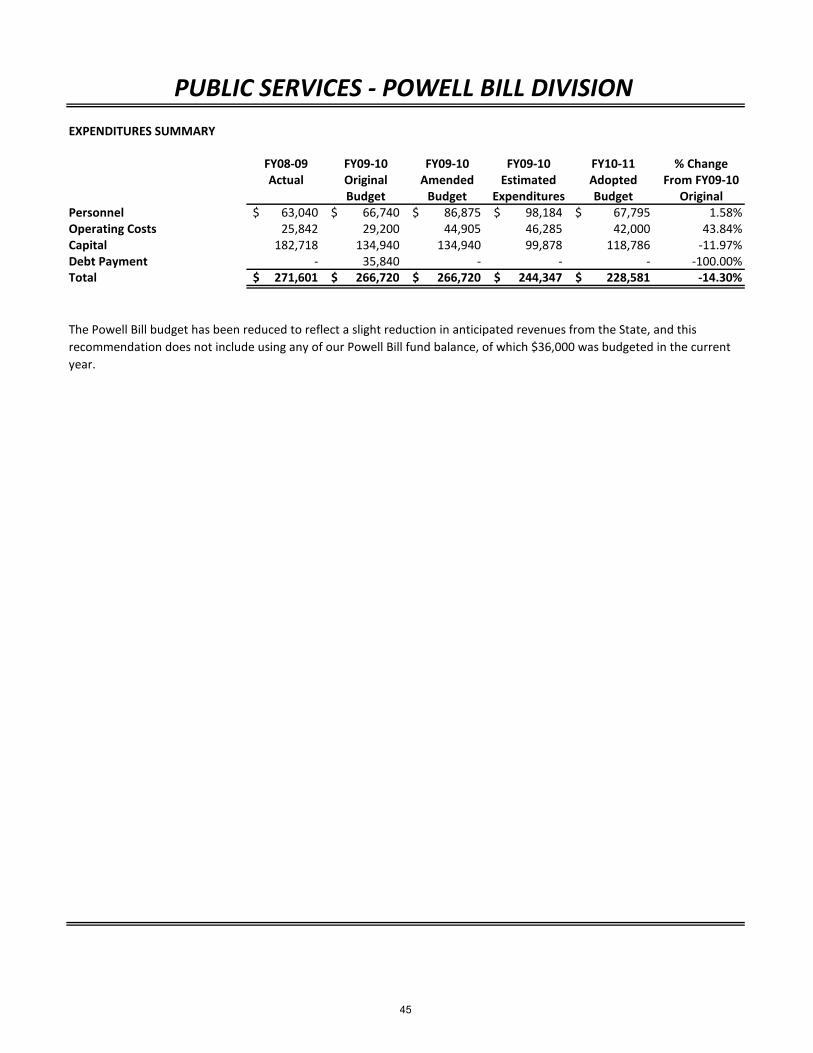

PUBLIC SERVICES - POWELL BILL DIVISION

Powell Bill – These grant revenues are generated from the State’s gasoline tax and a percentage of this tax is returned to the municipality through a formula based on population and street mileage. Powell Bill funds can only be used for street maintenance, construction, traffic signs, sidewalks, curbs, gutters, drainage and other related needs. This budget unit is managed as a function of the Streets Division of the Public Services Department.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2,

8.9%Public Buildings, 885489, 12.0%

Police Department, 1574065.4,

21.3%Fire

Department, 1488077.6,

20.1%

Planning & Development,

385292.2, 5.2%

Public Services -

Admin, 138502.2,

1.9%

PS - Streets, 369166.5,

5.0%

PS - Powell Bill, 228581.3,

3.1%

PS -Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

44

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel 63,040$ 66,740$ 86,875$ 98,184$ 67,795$ 1.58%Operating Costs 25,842 29,200 44,905 46,285 42,000 43.84%Capital 182,718 134,940 134,940 99,878 118,786 -11.97%Debt Payment - 35,840 - - - -100.00%Total 271,601$ 266,720$ 266,720$ 244,347$ 228,581$ -14.30%

PUBLIC SERVICES - POWELL BILL DIVISION

The Powell Bill budget has been reduced to reflect a slight reduction in anticipated revenues from the State, and this recommendation does not include using any of our Powell Bill fund balance, of which $36,000 was budgeted in the current year.

45

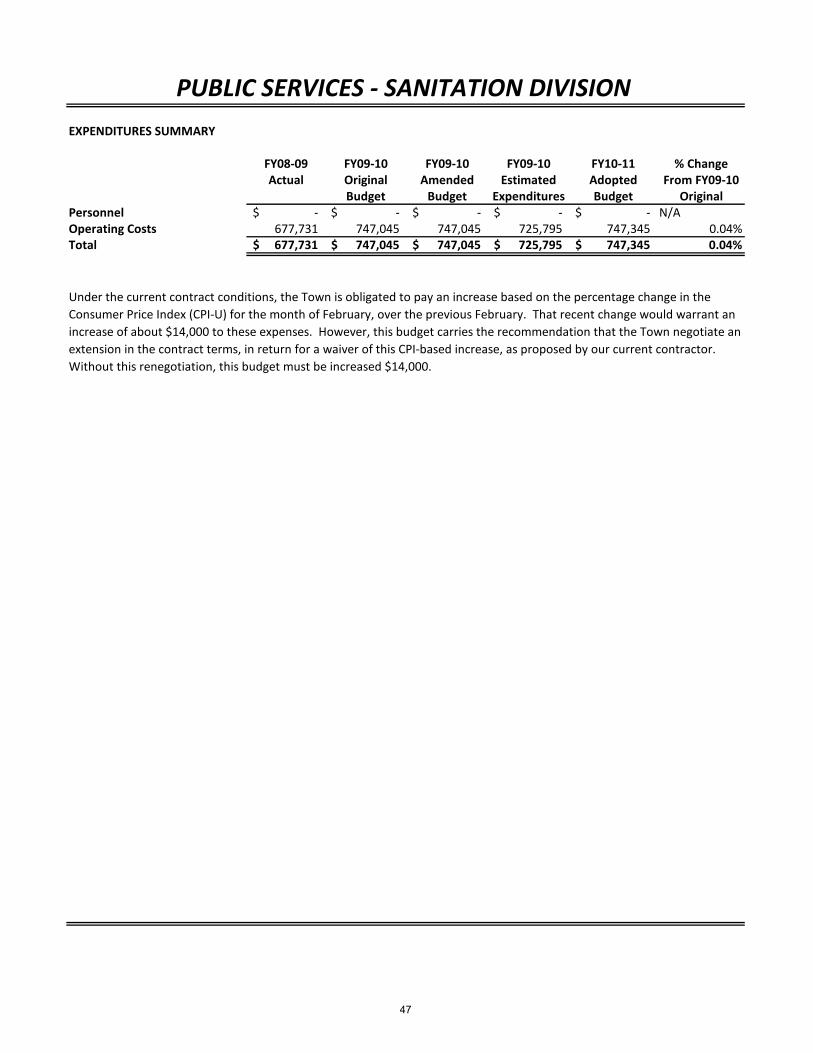

PUBLIC SERVICES - SANITATION DIVISION

The recycling, refuse, and solid waste pickup at residential curbside within Black Mountain is a service contracted by the Town. The management of this contract and related service calls currently resides with the Public Services Department. The purpose of this service is to assist in the maintenance of a clean and healthy community environment through the efficient and environmentally sensitive collection and removal of residential solid waste within the Town of Black Mountain.

Governing Board,

129412.7156, 1.7%

Administration, 659753.2,

8.9%

Public Buildings,

885489, 12.0%

Police Department, 1574065.4,

21.3%Fire

Department, 1488077.6,

20.1%

Planning & Development,

385292.2, 5.2%

Public Services - Admin,

138502.2, 1.9%

PS -Streets,

369166.5, 5.0%

PS - Powell Bill, 228581.3,

3.1%

PS - Sanitation, 747345, 10.1%

Parks & Recreation,

801481, 10.8%

Town of Black Mountain General Fund

46

EXPENDITURES SUMMARY

FY08-09 FY09-10 FY09-10 FY09-10 FY10-11 % ChangeActual Original Amended Estimated Adopted From FY09-10

Budget Budget Expenditures Budget OriginalPersonnel -$ -$ -$ -$ -$ N/AOperating Costs 677,731 747,045 747,045 725,795 747,345 0.04%Total 677,731$ 747,045$ 747,045$ 725,795$ 747,345$ 0.04%

PUBLIC SERVICES - SANITATION DIVISION

Under the current contract conditions, the Town is obligated to pay an increase based on the percentage change in the Consumer Price Index (CPI-U) for the month of February, over the previous February. That recent change would warrant an increase of about $14,000 to these expenses. However, this budget carries the recommendation that the Town negotiate an extension in the contract terms, in return for a waiver of this CPI-based increase, as proposed by our current contractor. Without this renegotiation, this budget must be increased $14,000.

47

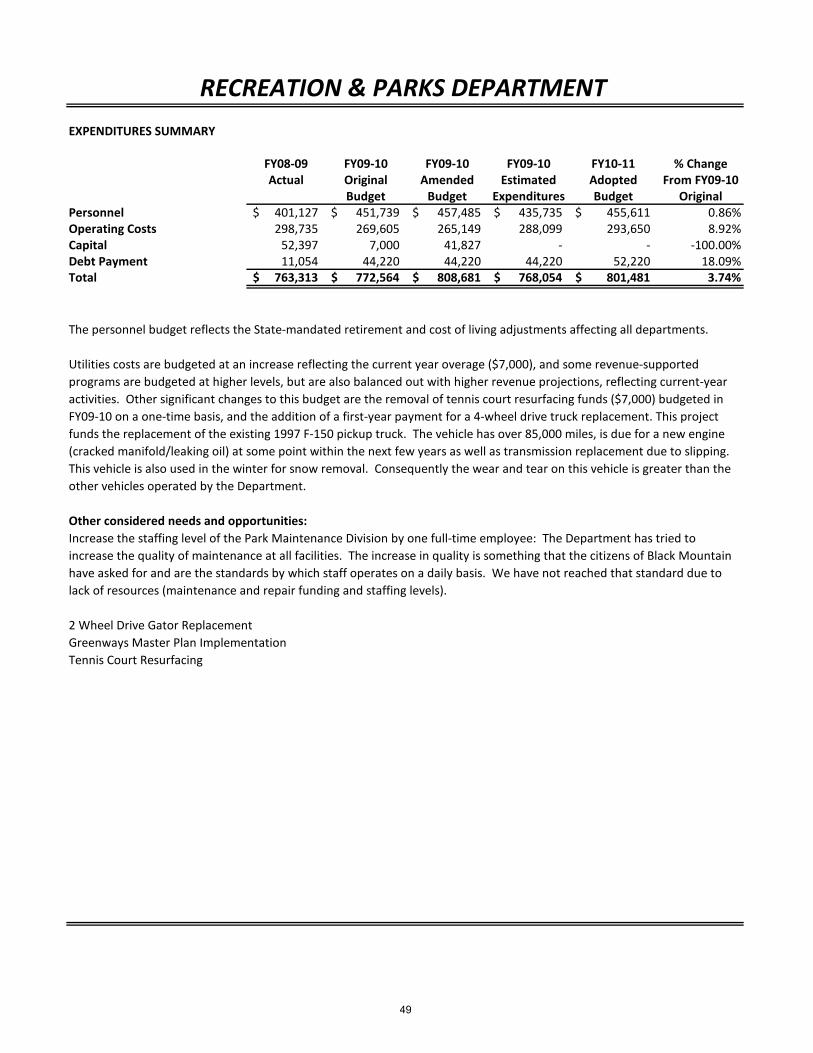

RECREATION & PARKS DEPARTMENT