Embed Size (px)

Citation preview

Toward a Factor Model of Relative Valuation

Liuren Wujoint with Xiaolu Hu and Malick Sy

NUS Quantitative Finance Joint Seminar11 Dec 2020

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 1 / 23

Perform company valuation on a large universe

Investment and corporate decisions must start with an accurate assessmentof company valuation.

The finance literature talks little about (actual) company valuation, exceptfor textbook treatment.

Quants researchers are excited about new statistical techniques,robo-advisors, and machine learning...

What is the right question? What’s the right performance metric?

What do you feed the machines to learn?

This project contains a large amount of manual work, just so we can find aneffective way of using the machines/techniques

Target question: fair company valuation on a large universe

Efforts: what/how to feed into company valuation

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 2 / 23

Learn from the classics

Structural DCF valuation on a single company

Works off consensus to generate variant views based on in-depthmarket/industry/company analysis

Industry size, company share, industry trend, company position.

Top line growth projection

Profit margin and bottom line earnings projection

Investment and financing projection: discount rate

Potential for strategic game-changing decisions

Each analyst covers a small number of companies, and identify key(innovative) drivers for the top/bottom line

Value multiples

Used under highly controlled environments for “comparable” companies

Key is to find the right comparables — metrics defining “comparability”

Statistical valuation of a large universe — Make the universe comparable

Transform company value into a measure as cross-sectionallycomparable as possible

Construct value determinants and conditioning metricscross-sectionally comparable and generally available

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 3 / 23

A factor model of company relative valuation

Objective: statistical valuation of a large universe: Make the universe comparable

Transform value into a measure as cross-sectionally comparable as possible

Value multiples (PB, PE, PS) are good starting points

Valid relative value metrics themselves within a controlled groupIdentify conditions/metrics that make these multiples conditionallycomparable within a large universe

The q ratio (value/capital, or its variations) has been widely used:

Investment literature: q is the marginal value of capitalCorporate finance: q is a performance measureAsset pricing: q (BM equity) predicts future stock returns

We use an analogous q ratio to define the relative value of a company:q = ln((TA− BE + MC )/TA).

It reflects equity valuation, but is represented in company value space.

Company v. equity valuation (?)

The starting point of the residual income model, which considers bothwhat you will earn and what you have

One can, in principle, use other value multiples as the starting point...

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 4 / 23

A factor model of company relative valuation

Transform value into a measure as cross-sectionally comparable as possible

Construct determinants cross-sectionally comparable and generally available

Tons of ratios/metrics have been constructed to explain valuationMany are variations of closely-related conceptsEach has somewhat different coverage, relevance

We propose a two-step procedure in the determinant construction

Combine/average several descriptors (of similar concepts) to one factorThe averaging can increase coverage, reduce noise, and alleviatemulti-collinearity issue

Link relative value to the constructed factors via a cross-sectionalcontemporaneous regression

with controls on industry differences.

Each step has many choices/variations: Each choice raises more questionsthan answers ...

If we can establish this general approach as useful, researchers can keepworking/innovating on the details down the road.

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 5 / 23

The Literature: factor model of stock returns

Our factor model is analogous in construction to factor models of stock returns

Dates back to Fama & McBeth (1973): Regress future stock returns onsome risk factors cross-sectionally.

Has been well developed in the industry (Grinold & Kahn (1999)) as thestarting point for active portfolio management

“Risk factors” are standardized firm characteristics (either returnpredictors, or similarity measures).Slope estimate represents realized return on a “factor portfolio.”Time-series averages represent average “risk premium” estimates forthe risk factors.Widely used for constructing “robust” covariance matrices forportfolios optimization, and portfolio risk attribution.Many commercial packages are available (Barra, Axioma, Bloomberg...)

Our factor model of company valuation serves different purposes:

It is a model for contemporaneous valuation, not for return forecasting:R2 should be much higher...Coefficient estimate reflects market pricing of each valuation factor atthat time.

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 6 / 23

The Literature: company valuation

We teach DCF and maybe option-based equity valuation, but little empiricalwork on practical implementation

Accounting literature on empirical implementations and accountingvariations of the DCF (RIM, AEG) ...

Mainly a test of inputs and long-run stationarity assumptions

Statistical regressions:

Rhodes-Kropf, Robinson, and Viswanathan (2005): Variable motivatedby RIM: Book, net incomeBartram, Grinblatt (2018, 2020): (almost) non-discriminative list of(virtually) all BS/IS/CF entriesEdmans, Goldstein, Jiang (2012): nearest neighbors

The three papers capture three important dimensions for building a robuststatistical valuation model

Insights from structural models on value determinantsStatistical search (feature collection, construction, identification)All models are imperfect: Local averaging/Bias-correction with nearestneighbors — value similarity/distance measures

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 7 / 23

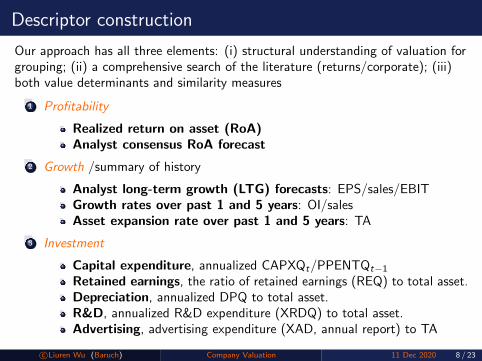

Descriptor construction

Our approach has all three elements: (i) structural understanding of valuation forgrouping; (ii) a comprehensive search of the literature (returns/corporate); (iii)both value determinants and similarity measures

1 Profitability

Realized return on asset (RoA)Analyst consensus RoA forecast

2 Growth /summary of history

Analyst long-term growth (LTG) forecasts: EPS/sales/EBITGrowth rates over past 1 and 5 years: OI/salesAsset expansion rate over past 1 and 5 years: TA

3 Investment

Capital expenditure, annualized CAPXQt/PPENTQt−1Retained earnings, the ratio of retained earnings (REQ) to total asset.Depreciation, annualized DPQ to total asset.R&D, annualized R&D expenditure (XRDQ) to total asset.Advertising, advertising expenditure (XAD, annual report) to TA

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 8 / 23

Descriptor construction

4 Liquidity

Working capital, working capital (WCAQ) to total asset.Slack ratio, cash and short-term investment (CHEQ) to total asset.Cash ratio, cash and short-term investment to current liabilities.Quick ratio, CHEQ + accounts receivable (RECTQ) to LCTQ.Current ratio, CHEQ+RECTQ+INVTQ to current liabilitiesTrading liquidity, the log ratio of average dollar trading volume tostock return idiosyncratic volatility (over past year).

5 Leverage: debt-to-book equity ratio

6 Market risk: 73-day daily regression beta

7 Size: log Total Asset

8 Momentum: 6-month and 12-month excluding last month

Other categories/measures/changes?

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 9 / 23

Constructing valuation factors from descriptors

At date t, there are j = 1, · · · , nk descriptors for the kth category, fork = 1, · · · ,K factors characterizing the behavior of i = 1, · · · ,N companies.

Standardize the raw values of each descriptor, x jt,i ,

z jt,i =(x jt,i −mj

t)

s jt. (1)

winsorize z jt,i ∈ (1, 99)% to estimate (mjt , s

jt ), truncate z jt,i ∈ [−2, 2].

Create the kth factor f kt,i by averaging the nk descriptors within the category,

f kt,i =

nk∑j=1

wt,jzjt,i (2)

with the weight estimated via a Bayesian regression:

wt =(Z>t Zt + Pt

)−1 (Z>t Ztw

ut + Ptw

0), (3)

wu the unconstrained estimator, w0 = 1nk

the prior, and Pt = 0.1⟨Z>t Zt

⟩.

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 10 / 23

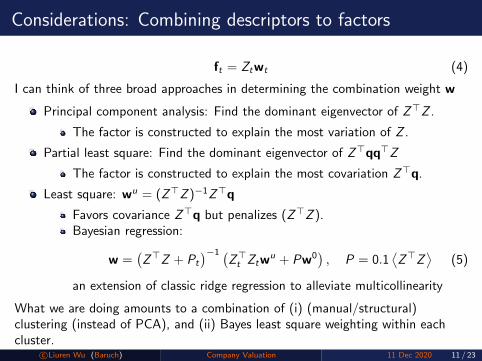

Considerations: Combining descriptors to factors

ft = Ztwt (4)

I can think of three broad approaches in determining the combination weight w

Principal component analysis: Find the dominant eigenvector of Z>Z .

The factor is constructed to explain the most variation of Z .

Partial least square: Find the dominant eigenvector of Z>qq>Z

The factor is constructed to explain the most covariation Z>q.

Least square: wu = (Z>Z )−1Z>q

Favors covariance Z>q but penalizes (Z>Z ).Bayesian regression:

w =(Z>Z + Pt

)−1 (Z>t Ztw

u + Pw0), P = 0.1

⟨Z>Z

⟩(5)

an extension of classic ridge regression to alleviate multicollinearity

What we are doing amounts to a combination of (i) (manual/structural)clustering (instead of PCA), and (ii) Bayes least square weighting within eachcluster.

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 11 / 23

Descriptor contribution to factors

Mean Std Auto Percentile values10 25 50 75 90

1. ProfitabilityRoA 0.73 0.36 0.99 0.23 0.32 1.00 1.00 1.00RoA forecast 0.72 0.10 0.84 0.61 0.66 0.71 0.78 0.87

2. GrowthLTG forecast 0.46 0.09 0.96 0.33 0.38 0.47 0.53 0.57Growth 5Y 0.12 0.08 0.91 0.01 0.08 0.13 0.17 0.21Growth 1Y 0.19 0.07 0.77 0.11 0.14 0.18 0.23 0.27Expansion 5Y 0.14 0.16 0.97 -0.03 0.03 0.10 0.23 0.40Expansion 1Y 0.17 0.08 0.86 0.07 0.11 0.15 0.22 0.27

3. InvestmentExpenditure 0.28 0.07 0.94 0.18 0.24 0.27 0.33 0.37Retained earnings 0.25 0.12 0.99 0.11 0.15 0.20 0.37 0.42Depreciation 0.11 0.08 0.97 0.01 0.05 0.10 0.16 0.23R&D 0.32 0.13 0.97 0.11 0.24 0.34 0.40 0.49Advertising 0.19 0.09 0.97 0.08 0.12 0.17 0.25 0.33

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 12 / 23

Descriptor contribution to factors

Mean Std Auto Percentile values10 25 50 75 90

4. LiquidityWorking capital 0.27 0.07 0.97 0.19 0.21 0.26 0.33 0.37Slack ratio 0.33 0.09 0.96 0.22 0.27 0.32 0.39 0.45Cash ratio 0.04 0.12 0.95 -0.11 -0.06 0.03 0.13 0.20Quick ratio 0.09 0.09 0.92 -0.02 0.02 0.08 0.14 0.21Current ratio -0.05 0.06 0.87 -0.14 -0.10 -0.05 -0.00 0.03Trading liquidity 0.32 0.09 0.98 0.18 0.25 0.34 0.38 0.41

8. MomentumMomentum 1Y 0.60 0.14 0.83 0.42 0.50 0.61 0.69 0.77Momentum 6M 0.40 0.14 0.83 0.23 0.31 0.39 0.50 0.58

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 13 / 23

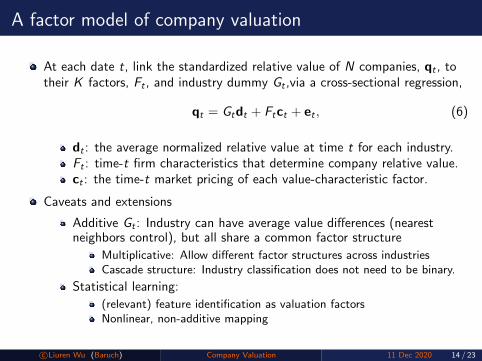

A factor model of company valuation

At each date t, link the standardized relative value of N companies, qt , totheir K factors, Ft , and industry dummy Gt ,via a cross-sectional regression,

qt = Gtdt + Ftct + et , (6)

dt : the average normalized relative value at time t for each industry.Ft : time-t firm characteristics that determine company relative value.ct : the time-t market pricing of each value-characteristic factor.

Caveats and extensions

Additive Gt : Industry can have average value differences (nearestneighbors control), but all share a common factor structure

Multiplicative: Allow different factor structures across industriesCascade structure: Industry classification does not need to be binary.

Statistical learning:

(relevant) feature identification as valuation factorsNonlinear, non-additive mapping

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 14 / 23

Model performance

A. Full-sample performance B. In and out-of-sample performance

Full-sample R2 average 68%, reasonably stable across market conditions

Some degeneration during recessions.

Out-of-sample: Divide the sample into two random halves. Estimate therelation on one half; measure performance on the other out-of-sample half.

Mild out-of-sample degeneration: 65% out-of-sample v. 68% in-sample

What’s the right out-of-sample setting/performance metric?

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 15 / 23

Market pricing of valuation factorsProfit and growth Investment and liquidity

Leverage and beta Size and momentum

Profit, growth, investment, liquidity have positive and stable contributions.

Momentum is another estimator for growth.

Contributions from leverage and beta are small, and compensate each other– intricate interactions between risk, growth, and profitability ...

Size effect is negative, declining marginal benefit of investment?c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 16 / 23

How do market pricing and performance vary over time?

Rate TS CS Vol Value Profitability Growth Leverage R2

Market pricing of valuation factorsProfitability 0.32 ( 0.25 ) 0.91 ( 2.40 ) -0.33 ( 0.73 ) -0.15 ( 0.25 ) -2.36 ( 2.62 ) -3.06 ( 2.24 ) 0.43 ( 1.13 ) -1.65 ( 1.85 ) 0.15Growth -1.84 ( 1.54 ) -1.07 ( 2.58 ) 0.84 ( 2.00 ) 0.04 ( 0.07 ) 3.24 ( 4.12 ) 1.21 ( 3.07 ) 0.56 ( 1.71 ) -0.51 ( 0.83 ) 0.14Investment -0.24 ( 0.42 ) 0.50 ( 1.28 ) -1.54 ( 3.53 ) 0.92 ( 1.71 ) -1.73 ( 2.36 ) 1.16 ( 1.39 ) 0.03 ( 0.04 ) 0.22 ( 0.32 ) 0.06Liquidity 0.90 ( 1.75 ) 0.32 ( 0.58 ) -0.52 ( 1.26 ) 0.42 ( 1.04 ) -0.24 ( 0.43 ) 1.23 ( 3.49 ) 0.34 ( 0.99 ) 0.64 ( 1.25 ) 0.05Leverage 1.03 ( 1.94 ) -0.09 ( 0.26 ) 0.24 ( 0.60 ) 0.49 ( 1.48 ) -4.04 ( 8.65 ) 0.65 ( 3.25 ) 0.49 ( 1.09 ) 0.14 ( 0.28 ) 0.21Market risk -1.64 ( 1.43 ) 0.31 ( 0.34 ) -0.17 ( 0.20 ) 2.63 ( 3.96 ) 6.37 ( 6.19 ) -0.88 ( 2.58 ) -1.02 ( 2.26 ) -0.38 ( 0.51 ) 0.17Size 0.34 ( 0.68 ) -0.44 ( 1.40 ) -0.66 ( 1.83 ) 0.28 ( 0.59 ) -0.84 ( 1.64 ) -1.14 ( 4.05 ) 0.03 ( 0.04 ) -0.64 ( 0.98 ) 0.05Momentum 2.30 ( 1.96 ) -0.67 ( 1.29 ) 1.61 ( 1.93 ) 1.39 ( 2.45 ) 3.42 ( 3.86 ) 0.97 ( 1.58 ) -0.01 ( 0.04 ) 0.10 ( 0.14 ) 0.08

Valuation model explanatory powerPerformance -1.25 ( 2.38 ) -0.42 ( 1.70 ) -0.11 ( 0.44 ) -0.27 ( 0.78 ) 3.15 ( 6.41 ) -0.55 ( 2.26 ) 0.09 ( 0.28 ) -0.02 ( 0.04 ) 0.19

hard to draw clear conclusions yet, but worth more research ...What are the market condition metrics that affect the pricing of differentfactors the most? Why?

The cross-sectional model defines “fairness” as fitting the average at thattime — What is actual is rationalHow to define and test the “fairness” of the pricing of each valuation factor?

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 17 / 23

Applications

Relative value decomposition:qt = Gtdt + Ftct + et , qt = Gt dt + Ft ct , qt = qt + et

qt — relative value, qt — fair value, et — misvalue

Outside investors can use the model to identify misvaluation as investmentopportunities — the definition of value investing

Profit-seeking trades can make previously-identified return predictingrelations disappear, but will make a valuation model “more accurate.”

Internal management can use the model in its corporate decisions:

Dynamic capital structure rebalancing: Increase debt/buy back stockwhen fair equity value appreciates

Should we compute dynamic hedging ratios on actual value or fairvalue of a contract?

Market-timing: Issue more stocks when stocks are over-valued — theopposite direction of rebalancing: risk on v risk off

Fair/mis-value effects on investments, merger and acquisitions, stocktakeovers, ...

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 18 / 23

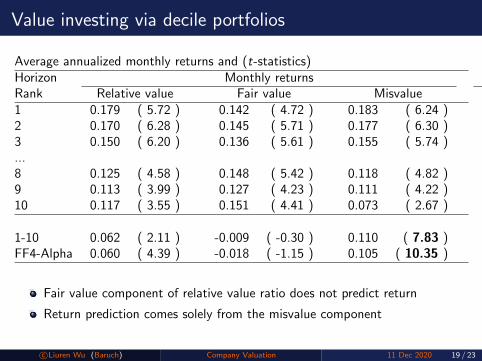

Value investing via decile portfolios

Average annualized monthly returns and (t-statistics)Horizon Monthly returns Quarterly returnsRank Relative value Fair value Misvalue Relative value Fair value Misvalue1 0.179 ( 5.72 ) 0.142 ( 4.72 ) 0.183 ( 6.24 ) 0.165 ( 5.85 ) 0.145 ( 5.37 ) 0.157 ( 6.80 )2 0.170 ( 6.28 ) 0.145 ( 5.71 ) 0.177 ( 6.30 ) 0.165 ( 6.60 ) 0.140 ( 6.25 ) 0.154 ( 6.92 )3 0.150 ( 6.20 ) 0.136 ( 5.61 ) 0.155 ( 5.74 ) 0.142 ( 6.74 ) 0.134 ( 6.41 ) 0.146 ( 6.73 )...8 0.125 ( 4.58 ) 0.148 ( 5.42 ) 0.118 ( 4.82 ) 0.120 ( 5.41 ) 0.132 ( 5.96 ) 0.121 ( 5.98 )9 0.113 ( 3.99 ) 0.127 ( 4.23 ) 0.111 ( 4.22 ) 0.110 ( 4.62 ) 0.120 ( 4.75 ) 0.110 ( 5.14 )10 0.117 ( 3.55 ) 0.151 ( 4.41 ) 0.073 ( 2.67 ) 0.117 ( 3.65 ) 0.138 ( 4.27 ) 0.084 ( 3.53 )

1-10 0.062 ( 2.11 ) -0.009 ( -0.30 ) 0.110 ( 7.83 ) 0.048 ( 1.44 ) 0.007 ( 0.19 ) 0.073 ( 5.27 )FF4-Alpha 0.060 ( 4.39 ) -0.018 ( -1.15 ) 0.105 ( 10.35 ) 0.041 ( 2.63 ) 0.000 ( 0.01 ) 0.064 ( 6.74 )

Fair value component of relative value ratio does not predict return

Return prediction comes solely from the misvalue component

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 19 / 23

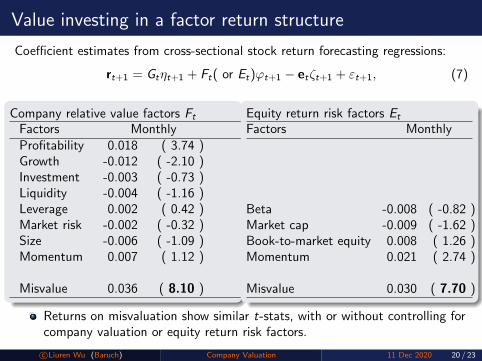

Value investing in a factor return structure

Coefficient estimates from cross-sectional stock return forecasting regressions:

rt+1 = Gtηt+1 + Ft( or Et)ϕt+1 − etζt+1 + εt+1, (7)

Company relative value factors Ft

Factors Monthly QuarterlyProfitability 0.018 ( 3.74 ) 0.016 ( 3.16 )Growth -0.012 ( -2.10 ) -0.014 ( -2.24 )Investment -0.003 ( -0.73 ) -0.001 ( -0.19 )Liquidity -0.004 ( -1.16 ) -0.005 ( -1.24 )Leverage 0.002 ( 0.42 ) 0.003 ( 0.76 )Market risk -0.002 ( -0.32 ) 0.001 ( 0.16 )Size -0.006 ( -1.09 ) -0.005 ( -0.96 )Momentum 0.007 ( 1.12 ) 0.009 ( 1.33 )

Misvalue 0.036 ( 8.10 ) 0.024 ( 5.18 )

Equity return risk factors Et

Factors Monthly Quarterly returns

Beta -0.008 ( -0.82 ) -0.005 ( -0.51 )Market cap -0.009 ( -1.62 ) -0.008 ( -1.52 )Book-to-market equity 0.008 ( 1.26 ) 0.009 ( 1.31 )Momentum 0.021 ( 2.74 ) 0.019 ( 2.29 )

Misvalue 0.030 ( 7.70 ) 0.019 ( 4.89 )

Returns on misvaluation show similar t-stats, with or without controlling forcompany valuation or equity return risk factors.

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 20 / 23

The role of valuation in equity financing decisions

Equity financing decision: Change from the previous quarter to nextquarter/total asset at valuation date

Misvaluation: de-biased from one-year moving average

Fair value MisvalueNet equity issuance -0.25 ( -2.52 ) 1.91 ( 10.02 )Equity issuance -1.18 ( -3.67 ) 3.77 ( 8.28 )Equity purchase 0.38 ( 5.92 ) -0.92 ( -7.81 )Issuance-purchase -1.38 ( -4.78 ) 4.41 ( 9.64 )

Effects of misvaluation: Strong and consistent across both net and separateissuance/purchase measures.

Issue more, purchase less when stocks are over-valued.

Effects of fair valuation: strong and opposite

Issue less, purchase more equity when the fair value becomes higher.

c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 21 / 23

Dynamic rebalancing v. market timing

Equity issuance/purchase can be used to serve two different purposes:

Dynamic rebalancing toward a leverage target

When MC/relative value increases, the company’s leverage declines.To rebalance toward its original leverage target, the firm needs toincrease its leverage and can do so via stock repurchase.Dynamic rebalancing can remove a lot risk without many contracts,wins Scholes/Merton a Nobel in hedging derivatives risk, and can be agood guide for corporate policy to the extent transactions are possible

Market timing to benefit from misvlauation

When market cap (and hence relative value) is higher than fair, thefirm can take advantage of the misvaluation opportunity by issuingmore equities at the higher-than-fair valuation.This market-timing operation makes the firm deviate further from itsleverage target (original leverage level) — (α/β) trade-off

Our results show that the rebalancing operation dominates when the relativevalue variation is fair and is hence more permanent.

The market timing operation dominates when the relative value variation isdriven by temporary misvaluation.

Net issuance depends positively on idiosyncratic relative value.c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 22 / 23

Concluding remarks

We strive to build a statistical company valuation factor model structurethat can be applied to a large universe

A detailed DCF projection needs domain expertise and works betterwith a singular focus on a selected number of companies.

The statistical valuation approach benefits from a large sample size formore robust estimation.

The two complement each other, and can help each other.

The valuation factor structure is analogous to the stock return factor modelstructure that has been widely adopted/commercialized in the industry.

The two factor models serve very much different objectives:One for valuation; the other for risk attribution.

The valuation factor model structure is much stronger, much more stable,and much better positioned to benefit from the many new statistical andstructural developments

and can be the starting point for investment, financial service, andcorporate policy analysis

A lot more can be done on target construction, feature selection, estimationsetting, performance metrics...c©Liuren Wu (Baruch) Company Valuation 11 Dec 2020 23 / 23