Embed Size (px)

Citation preview

2

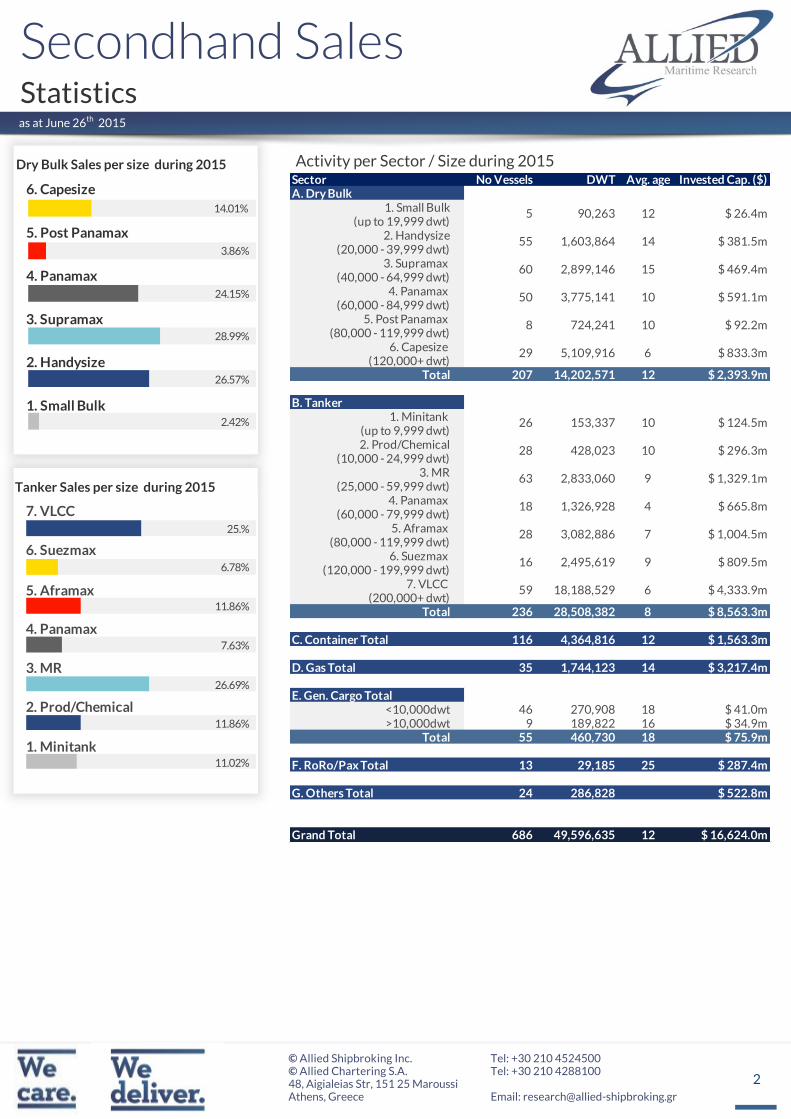

Sector No Vessels DWT Avg. age Invested Cap. ($)A. Dry Bulk

1. Small Bulk(up to 19,999 dwt)

2. Handysize(20,000 - 39,999 dwt)

3. Supramax (40,000 - 64,999 dwt)

4. Panamax (60,000 - 84,999 dwt)

5. Post Panamax (80,000 - 119,999 dwt)

6. Capesize (120,000+ dwt)

Total 207 14,202,571 12 $ 2,393.9m

B. Tanker1. Minitank

(up to 9,999 dwt)2. Prod/Chemical

(10,000 - 24,999 dwt)3. MR

(25,000 - 59,999 dwt)4. Panamax

(60,000 - 79,999 dwt)5. Aframax

(80,000 - 119,999 dwt)6. Suezmax

(120,000 - 199,999 dwt)7. VLCC

(200,000+ dwt)Total 236 28,508,382 8 $ 8,563.3m

C. Container Total 116 4,364,816 12 $ 1,563.3m

D. Gas Total 35 1,744,123 14 $ 3,217.4m

E. Gen. Cargo Total<10,000dwt 46 270,908 18 $ 41.0m>10,000dwt 9 189,822 16 $ 34.9m

Total 55 460,730 18 $ 75.9m

F. RoRo/Pax Total 13 29,185 25 $ 287.4m

G. Others Total 24 286,828 $ 522.8m

Grand Total 686 49,596,635 12 $ 16,624.0m

10

10

6

59 $ 4,333.9m6

7

9

28 $ 1,004.5m

16 $ 809.5m

18 $ 665.8m

$ 296.3m

10

10

1,326,928

28 428,023

9

4

63 $ 1,329.1m

5 $ 26.4m

55 $ 381.5m

60 $ 469.4m2,899,146

90,263

1,603,864

12

14

15

50 $ 591.1m

18,188,529

3,082,886

2,495,619

2,833,060

5,109,916

153,337

3,775,141

29 $ 833.3m

26 $ 124.5m

8 724,241 $ 92.2m

as at June 26th 2015

Dry Bulk Sales per size during 2015

7. VLCC

5. Aframax

4. Panamax

3. MR

2. Prod/Chemical

1. Minitank

6. Suezmax

25.%

6.78%

11.86%

7.63%

26.69%

11.86%

11.02%

6. Capesize

5. Post Panamax

4. Panamax

3. Supramax

2. Handysize

1. Small Bulk

14.01%

3.86%

24.15%

28.99%

26.57%

2.42%

Tanker Sales per size during 2015

3

as at June 26th 2015

0

50

100

150

200

250

Jan

ua

ry

Fe

bru

ary

Mar

ch

Ap

ril

Ma

y

Jun

e

July

Au

gu

st

Se

pte

mb

er

Oct

ober

No

vem

ber

De

cem

be

r

UNITS 2014 2015

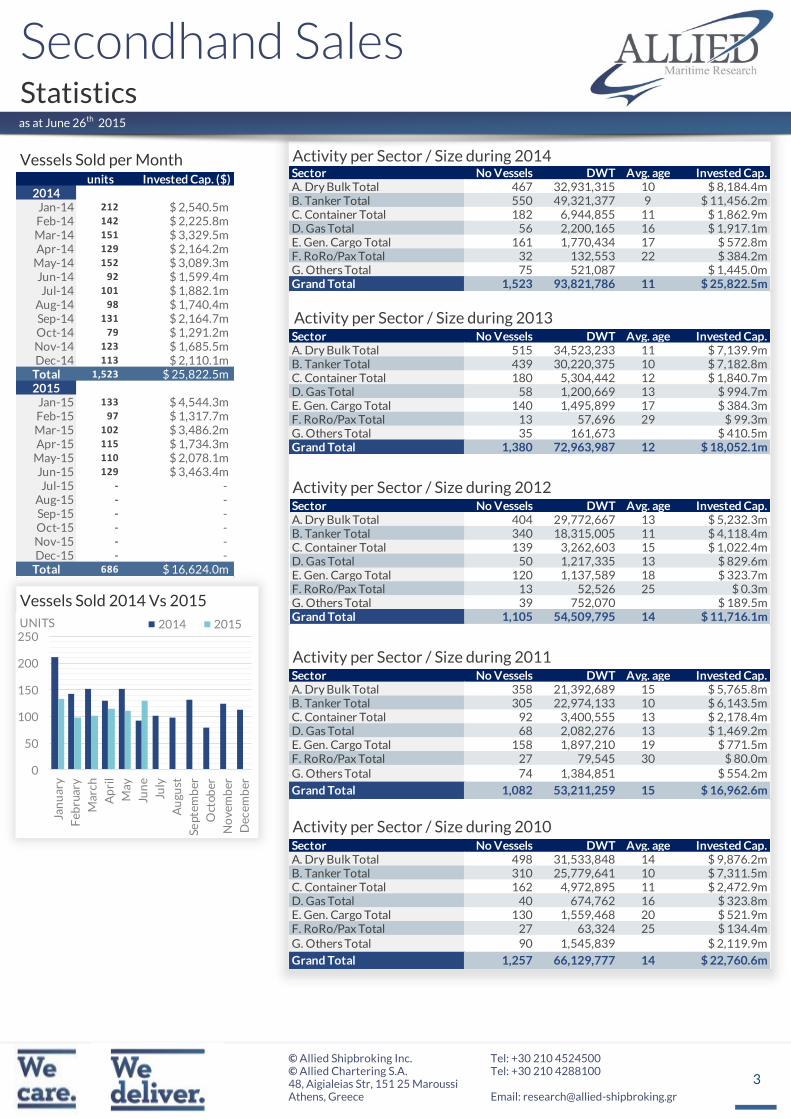

Vessels Sold per Month

Vessels Sold 2014 Vs 2015

units Invested Cap. ($)2014

Jan-14 212 $ 2,540.5m Feb-14 142 $ 2,225.8m Mar-14 151 $ 3,329.5m Apr-14 129 $ 2,164.2m

May-14 152 $ 3,089.3m Jun-14 92 $ 1,599.4m Jul-14 101 $ 1,882.1m

Aug-14 98 $ 1,740.4m Sep-14 131 $ 2,164.7m Oct-14 79 $ 1,291.2m Nov-14 123 $ 1,685.5m Dec-14 113 $ 2,110.1m

Total 1,523 $ 25,822.5m 2015

Jan-15 133 $ 4,544.3m Feb-15 97 $ 1,317.7m Mar-15 102 $ 3,486.2m Apr-15 115 $ 1,734.3m

May-15 110 $ 2,078.1m Jun-15 129 $ 3,463.4m Jul-15 - -

Aug-15 - - Sep-15 - - Oct-15 - - Nov-15 - - Dec-15 - -

Total 686 $ 16,624.0m

Sector No Vessels DWT Avg. age Invested Cap.A. Dry Bulk Total 467 32,931,315 10 $ 8,184.4mB. Tanker Total 550 49,321,377 9 $ 11,456.2mC. Container Total 182 6,944,855 11 $ 1,862.9mD. Gas Total 56 2,200,165 16 $ 1,917.1mE. Gen. Cargo Total 161 1,770,434 17 $ 572.8mF. RoRo/Pax Total 32 132,553 22 $ 384.2mG. Others Total 75 521,087 $ 1,445.0mGrand Total 1,523 93,821,786 11 $ 25,822.5m

Sector No Vessels DWT Avg. age Invested Cap.A. Dry Bulk Total 515 34,523,233 11 $ 7,139.9mB. Tanker Total 439 30,220,375 10 $ 7,182.8mC. Container Total 180 5,304,442 12 $ 1,840.7mD. Gas Total 58 1,200,669 13 $ 994.7mE. Gen. Cargo Total 140 1,495,899 17 $ 384.3mF. RoRo/Pax Total 13 57,696 29 $ 99.3mG. Others Total 35 161,673 $ 410.5mGrand Total 1,380 72,963,987 12 $ 18,052.1m

Sector No Vessels DWT Avg. age Invested Cap.A. Dry Bulk Total 404 29,772,667 13 $ 5,232.3mB. Tanker Total 340 18,315,005 11 $ 4,118.4mC. Container Total 139 3,262,603 15 $ 1,022.4mD. Gas Total 50 1,217,335 13 $ 829.6mE. Gen. Cargo Total 120 1,137,589 18 $ 323.7mF. RoRo/Pax Total 13 52,526 25 $ 0.3mG. Others Total 39 752,070 $ 189.5mGrand Total 1,105 54,509,795 14 $ 11,716.1m

Sector No Vessels DWT Avg. age Invested Cap.A. Dry Bulk Total 358 21,392,689 15 $ 5,765.8mB. Tanker Total 305 22,974,133 10 $ 6,143.5mC. Container Total 92 3,400,555 13 $ 2,178.4mD. Gas Total 68 2,082,276 13 $ 1,469.2mE. Gen. Cargo Total 158 1,897,210 19 $ 771.5mF. RoRo/Pax Total 27 79,545 30 $ 80.0mG. Others Total 74 1,384,851 $ 554.2m

Grand Total 1,082 53,211,259 15 $ 16,962.6m

Sector No Vessels DWT Avg. age Invested Cap.A. Dry Bulk Total 498 31,533,848 14 $ 9,876.2mB. Tanker Total 310 25,779,641 10 $ 7,311.5mC. Container Total 162 4,972,895 11 $ 2,472.9mD. Gas Total 40 674,762 16 $ 323.8mE. Gen. Cargo Total 130 1,559,468 20 $ 521.9mF. RoRo/Pax Total 27 63,324 25 $ 134.4mG. Others Total 90 1,545,839 $ 2,119.9m

Grand Total 1,257 66,129,777 14 $ 22,760.6m

4

as at June 26th 2015

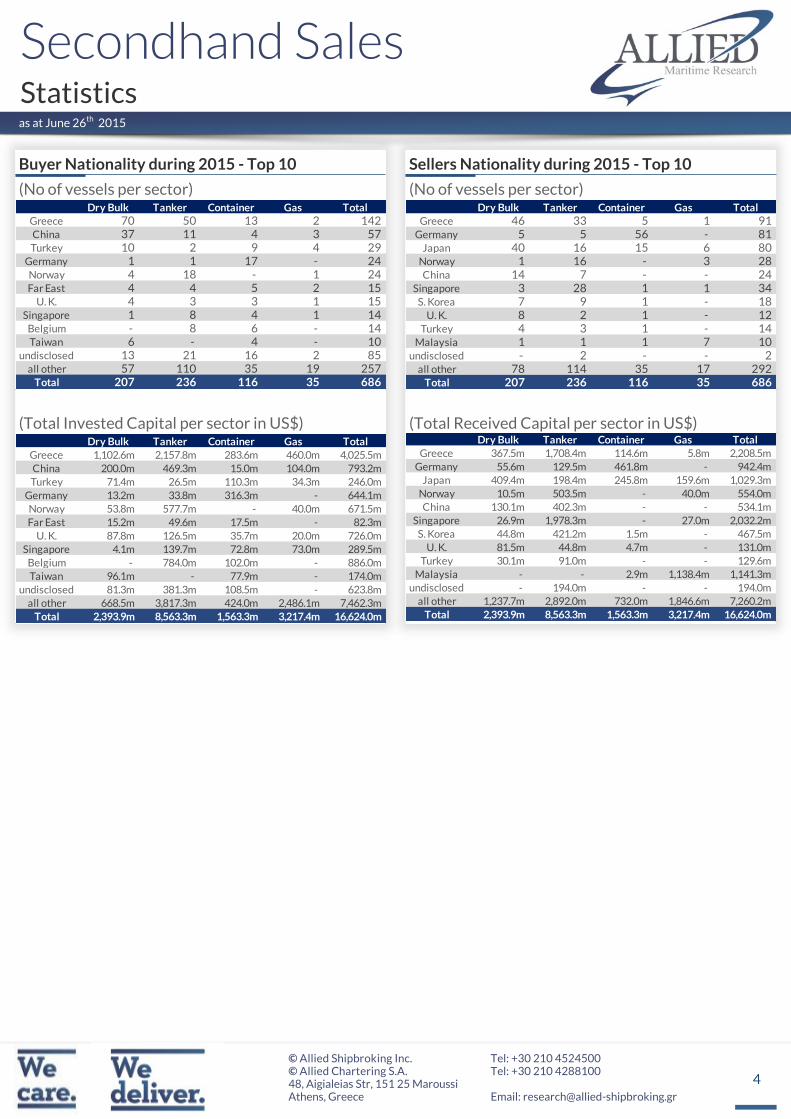

Buyer Nationality during 2015 - Top 10

(No of vessels per sector)

(Total Invested Capital per sector in US$)

Sellers Nationality during 2015 - Top 10

(No of vessels per sector)

(Total Received Capital per sector in US$)

Dry Bulk Tanker Container Gas Total

Greece 70 50 13 2 142 China 37 11 4 3 57 Turkey 10 2 9 4 29

Germany 1 1 17 - 24 Norway 4 18 - 1 24 Far East 4 4 5 2 15

U. K. 4 3 3 1 15 Singapore 1 8 4 1 14

Belgium - 8 6 - 14 Taiwan 6 - 4 - 10

undisclosed 13 21 16 2 85 all other 57 110 35 19 257

Total 207 236 116 35 686

Dry Bulk Tanker Container Gas Total

Greece 1,102.6m 2,157.8m 283.6m 460.0m 4,025.5m

China 200.0m 469.3m 15.0m 104.0m 793.2m

Turkey 71.4m 26.5m 110.3m 34.3m 246.0m

Germany 13.2m 33.8m 316.3m - 644.1m

Norway 53.8m 577.7m - 40.0m 671.5m

Far East 15.2m 49.6m 17.5m - 82.3m

U. K. 87.8m 126.5m 35.7m 20.0m 726.0m

Singapore 4.1m 139.7m 72.8m 73.0m 289.5m

Belgium - 784.0m 102.0m - 886.0m

Taiwan 96.1m - 77.9m - 174.0m

undisclosed 81.3m 381.3m 108.5m - 623.8m

all other 668.5m 3,817.3m 424.0m 2,486.1m 7,462.3m

Total 2,393.9m 8,563.3m 1,563.3m 3,217.4m 16,624.0m

Dry Bulk Tanker Container Gas Total

Greece 46 33 5 1 91 Germany 5 5 56 - 81

Japan 40 16 15 6 80 Norway 1 16 - 3 28 China 14 7 - - 24

Singapore 3 28 1 1 34 S. Korea 7 9 1 - 18

U. K. 8 2 1 - 12 Turkey 4 3 1 - 14

Malaysia 1 1 1 7 10 undisclosed - 2 - - 2

all other 78 114 35 17 292 Total 207 236 116 35 686

Dry Bulk Tanker Container Gas Total

Greece 367.5m 1,708.4m 114.6m 5.8m 2,208.5m

Germany 55.6m 129.5m 461.8m - 942.4m

Japan 409.4m 198.4m 245.8m 159.6m 1,029.3m

Norway 10.5m 503.5m - 40.0m 554.0m

China 130.1m 402.3m - - 534.1m

Singapore 26.9m 1,978.3m - 27.0m 2,032.2m

S. Korea 44.8m 421.2m 1.5m - 467.5m

U. K. 81.5m 44.8m 4.7m - 131.0m

Turkey 30.1m 91.0m - - 129.6m

Malaysia - - 2.9m 1,138.4m 1,141.3m

undisclosed - 194.0m - - 194.0m

all other 1,237.7m 2,892.0m 732.0m 1,846.6m 7,260.2m

Total 2,393.9m 8,563.3m 1,563.3m 3,217.4m 16,624.0m

5

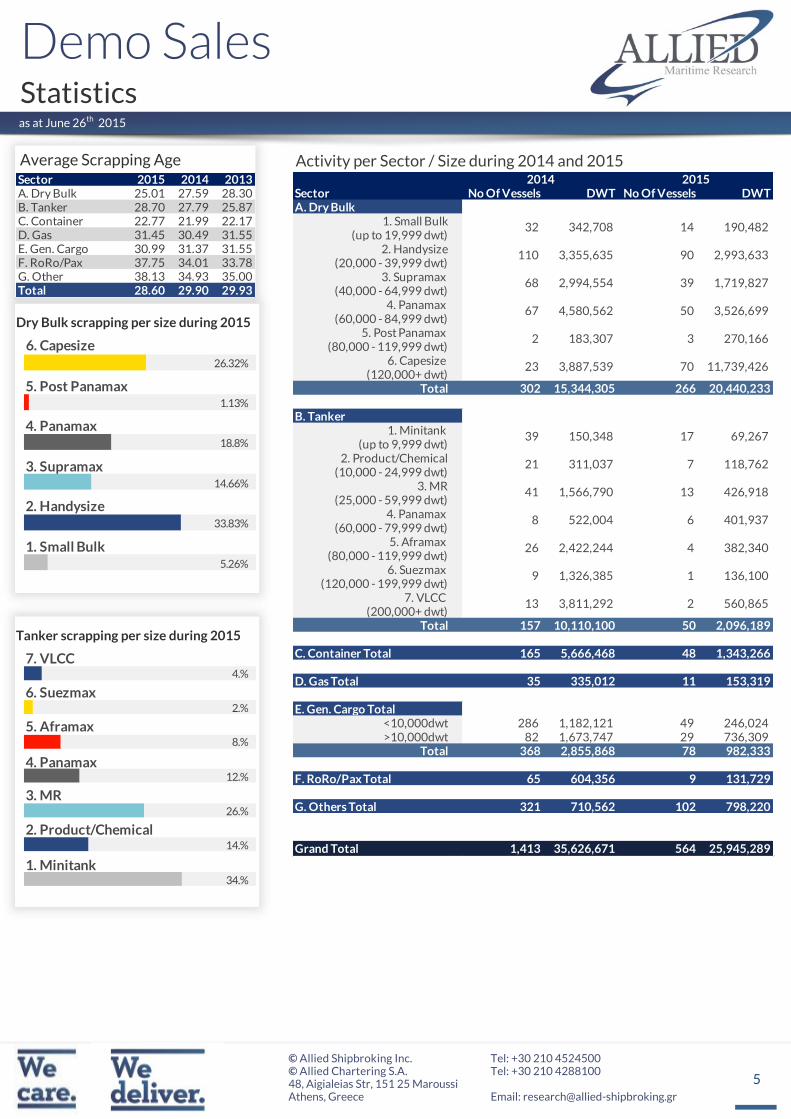

Sector No Of Vessels DWT No Of Vessels DWTA. Dry Bulk

1. Small Bulk(up to 19,999 dwt)

2. Handysize(20,000 - 39,999 dwt)

3. Supramax (40,000 - 64,999 dwt)

4. Panamax (60,000 - 84,999 dwt)

5. Post Panamax (80,000 - 119,999 dwt)

6. Capesize (120,000+ dwt)

Total 302 15,344,305 266 20,440,233

B. Tanker1. Minitank

(up to 9,999 dwt)2. Product/Chemical

(10,000 - 24,999 dwt)3. MR

(25,000 - 59,999 dwt)4. Panamax

(60,000 - 79,999 dwt)5. Aframax

(80,000 - 119,999 dwt)6. Suezmax

(120,000 - 199,999 dwt)7. VLCC

(200,000+ dwt)Total 157 10,110,100 50 2,096,189

C. Container Total 165 5,666,468 48 1,343,266

D. Gas Total 35 335,012 11 153,319

E. Gen. Cargo Total<10,000dwt 286 1,182,121 49 246,024 >10,000dwt 82 1,673,747 29 736,309

Total 368 2,855,868 78 982,333

F. RoRo/Pax Total 65 604,356 9 131,729

G. Others Total 321 710,562 102 798,220

Grand Total 1,413 35,626,671 564 25,945,289

67 4,580,562 50 3,526,699

90 2,993,633

68 2,994,554 39 1,719,827

13 3,811,292 2 560,865

9 1,326,385 1 136,100

26 2,422,244 4 382,340

8 522,004 6 401,937

3 270,166

41 1,566,790 13 426,918

21 311,037 7 118,762

23 3,887,539 70 11,739,426

2014 2015

32 342,708 14 190,482

110 3,355,635

39 150,348 17 69,267

2 183,307

as at June 26th 2015

Sector 2015 2014 2013A. Dry Bulk 25.01 27.59 28.30B. Tanker 28.70 27.79 25.87C. Container 22.77 21.99 22.17D. Gas 31.45 30.49 31.55E. Gen. Cargo 30.99 31.37 31.55F. RoRo/Pax 37.75 34.01 33.78G. Other 38.13 34.93 35.00Total 28.60 29.90 29.93

7. VLCC

6. Suezmax

5. Aframax

4. Panamax

3. MR

2. Product/Chemical

1. Minitank

4.%

2.%

8.%

12.%

26.%

14.%

34.%

6. Capesize

5. Post Panamax

4. Panamax

3. Supramax

2. Handysize

1. Small Bulk

26.32%

1.13%

18.8%

14.66%

33.83%

5.26%

Average Scrapping Age

Dry Bulk scrapping per size during 2015

Tanker scrapping per size during 2015

6

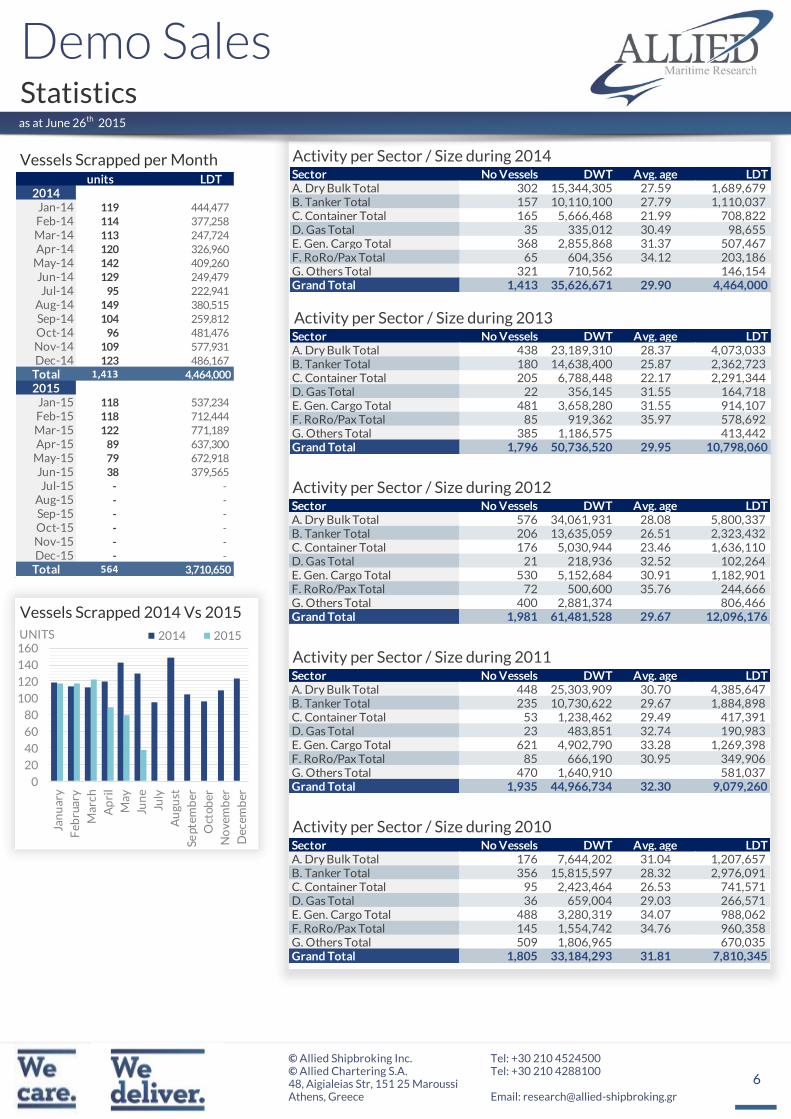

units LDT2014

Jan-14 119 444,477

Feb-14 114 377,258

Mar-14 113 247,724

Apr-14 120 326,960

May-14 142 409,260

Jun-14 129 249,479

Jul-14 95 222,941

Aug-14 149 380,515

Sep-14 104 259,812

Oct-14 96 481,476

Nov-14 109 577,931

Dec-14 123 486,167

Total 1,413 4,464,000

2015Jan-15 118 537,234

Feb-15 118 712,444

Mar-15 122 771,189

Apr-15 89 637,300

May-15 79 672,918

Jun-15 38 379,565

Jul-15 - -

Aug-15 - -

Sep-15 - -

Oct-15 - -

Nov-15 - -

Dec-15 - -

Total 564 3,710,650

as at June 26th 2015

0

20

40

60

80

100

120

140

160

Jan

ua

ry

Fe

bru

ary

Mar

ch

Ap

ril

Ma

y

Jun

e

July

Au

gu

st

Se

pte

mb

er

Oct

ob

er

No

ve

mb

er

De

cem

be

r

UNITS 2014 2015

Vessels Scrapped per Month

Vessels Scrapped 2014 Vs 2015

Sector No Vessels DWT Avg. age LDTA. Dry Bulk Total 302 15,344,305 27.59 1,689,679 B. Tanker Total 157 10,110,100 27.79 1,110,037 C. Container Total 165 5,666,468 21.99 708,822 D. Gas Total 35 335,012 30.49 98,655 E. Gen. Cargo Total 368 2,855,868 31.37 507,467 F. RoRo/Pax Total 65 604,356 34.12 203,186 G. Others Total 321 710,562 146,154 Grand Total 1,413 35,626,671 29.90 4,464,000

Sector No Vessels DWT Avg. age LDTA. Dry Bulk Total 438 23,189,310 28.37 4,073,033 B. Tanker Total 180 14,638,400 25.87 2,362,723 C. Container Total 205 6,788,448 22.17 2,291,344 D. Gas Total 22 356,145 31.55 164,718 E. Gen. Cargo Total 481 3,658,280 31.55 914,107 F. RoRo/Pax Total 85 919,362 35.97 578,692 G. Others Total 385 1,186,575 413,442 Grand Total 1,796 50,736,520 29.95 10,798,060

Sector No Vessels DWT Avg. age LDTA. Dry Bulk Total 576 34,061,931 28.08 5,800,337 B. Tanker Total 206 13,635,059 26.51 2,323,432 C. Container Total 176 5,030,944 23.46 1,636,110 D. Gas Total 21 218,936 32.52 102,264 E. Gen. Cargo Total 530 5,152,684 30.91 1,182,901 F. RoRo/Pax Total 72 500,600 35.76 244,666 G. Others Total 400 2,881,374 806,466 Grand Total 1,981 61,481,528 29.67 12,096,176

Sector No Vessels DWT Avg. age LDTA. Dry Bulk Total 448 25,303,909 30.70 4,385,647 B. Tanker Total 235 10,730,622 29.67 1,884,898 C. Container Total 53 1,238,462 29.49 417,391 D. Gas Total 23 483,851 32.74 190,983 E. Gen. Cargo Total 621 4,902,790 33.28 1,269,398 F. RoRo/Pax Total 85 666,190 30.95 349,906 G. Others Total 470 1,640,910 581,037 Grand Total 1,935 44,966,734 32.30 9,079,260

Sector No Vessels DWT Avg. age LDTA. Dry Bulk Total 176 7,644,202 31.04 1,207,657 B. Tanker Total 356 15,815,597 28.32 2,976,091 C. Container Total 95 2,423,464 26.53 741,571 D. Gas Total 36 659,004 29.03 266,571 E. Gen. Cargo Total 488 3,280,319 34.07 988,062 F. RoRo/Pax Total 145 1,554,742 34.76 960,358 G. Others Total 509 1,806,965 670,035 Grand Total 1,805 33,184,293 31.81 7,810,345

7

as at June 26th 2015

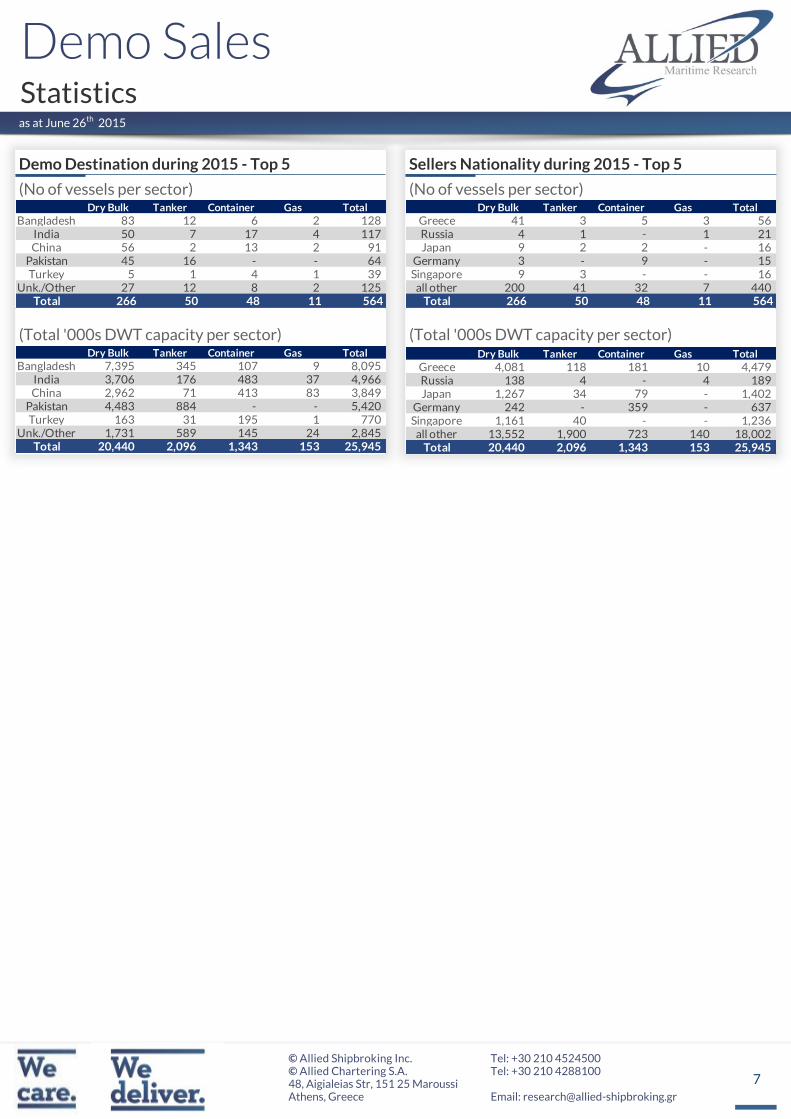

Demo Destination during 2015 - Top 5

(No of vessels per sector)

(Total '000s DWT capacity per sector)

Sellers Nationality during 2015 - Top 5

(No of vessels per sector)

(Total '000s DWT capacity per sector)

Dry Bulk Tanker Container Gas Total

Bangladesh 83 12 6 2 128 India 50 7 17 4 117 China 56 2 13 2 91

Pakistan 45 16 - - 64 Turkey 5 1 4 1 39

Unk./Other 27 12 8 2 125 Total 266 50 48 11 564

Dry Bulk Tanker Container Gas Total

Bangladesh 7,395 345 107 9 8,095 India 3,706 176 483 37 4,966 China 2,962 71 413 83 3,849

Pakistan 4,483 884 - - 5,420 Turkey 163 31 195 1 770

Unk./Other 1,731 589 145 24 2,845 Total 20,440 2,096 1,343 153 25,945

Dry Bulk Tanker Container Gas Total

Greece 41 3 5 3 56 Russia 4 1 - 1 21 Japan 9 2 2 - 16

Germany 3 - 9 - 15 Singapore 9 3 - - 16

all other 200 41 32 7 440 Total 266 50 48 11 564

Dry Bulk Tanker Container Gas Total

Greece 4,081 118 181 10 4,479 Russia 138 4 - 4 189 Japan 1,267 34 79 - 1,402

Germany 242 - 359 - 637 Singapore 1,161 40 - - 1,236

all other 13,552 1,900 723 140 18,002 Total 20,440 2,096 1,343 153 25,945

8

COSTAS KARAMANISMOBILE: +30 6941 54 14 65

MARGARITA TSALPATOUROU MOBILE: +30 6934 74 22 16

DIMITRIS KANELLOSMOBILE: +30 6945 07 47 85

PANOS ALEXOPOULOSMOBILE: +30 6944 34 66 15

ARISTOFANIS THEODOTOSMOBILE: +30 6951 79 82 89

DIMITRIS PATELISMOBILE: +30 6944 04 43 61

VASSILIS MANOLOPOULOS MOBILE: +30 6988 88 13 05

GEORGINA MAVRIKOUMOBILE: +30 697 4 18 07 84

ANGELIKI KAPPAMOBILE: +30 697 5 85 60 84

NATALIA KARAMANIMOBILE: +30 698 4 58 82 99

JOHN FLOURISMOBILE: +30 6955 80 15 03

NICOLAS PAPANTONOPOULOSMOBILE: +30 6945 23 21 88

STELLA FOUROULIMOBILE: +30 6947 35 68 48

Dry Cargo Chartering

Tanker Chartering

AERAKIS GEORGEMOBILE: +30 6946 04 57 37

BOLIS ILIASMOBILE: +30 6937 02 65 00

DASKALAKIS GEORGEMOBILE: +30 6932 24 80 07

DRAKOGIANNOPOULOS STAVROSMOBILE: +30 6932 20 15 65

DRAKOGIANNOPOULOS SAKISMOBILE: +30 6944 88 58 08

HATZIGEORGIOU NASSOSMOBILE: +30 6944 73 33 93

KARADIMAS COSTASMOBILE: +30 6932 20 15 64

KLONIZAKIS JOHNMOBILE: +30 6948 50 55 81

KOSTOYANNIS JOHNMOBILE: +30 6932 43 39 99

MANOLAS NIKOLASMOBILE: +30 6940 63 22 56

MOISSOGLOU THEODOROSMOBILE: +30 6932 45 52 41

PAPOUIS THASSOSMOBILE: +30 6944 29 49 89

PRACHALIAS ARGIRISMOBILE: +30 6947 62 82 62

STASSINAKIS JOHNMOBILE: +30 6972 60 92 09

TOBALOGLOU EVAGELOSMOBILE: +30 6932 40 56 20

TSALPATOUROS COSTISMOBILE: +30 6932 20 15 63

VARVAROS PLUTONMOBILE: +30 6937 25 15 15

GEORGE LAZARIDISMOBILE: +30 6946 95 69 40

Maritime Research & Valuations

Sale & Purchase

ALLIED SHIPBROKING INC. 48, Aigialeias Street, 4th Floor, Maroussi 151 25, Greece Tel: +30 210 45 24 500 Fax: +30 210 45 25 017/ 019 E-mail: [email protected]

ALLIED CHARTERING S.A. 48, Aigialeias Street, 4th Floor, Maroussi 151 25, Greece Tel : +30 210 42 88 100 Fax: +30 210 45 24 201

E-mail: [email protected]

E-mail: [email protected]

9

Disclaimer

The information contained within this report has been provided by Allied Shipbroking Inc. and Allied Chartering S.A. for general information pur-

poses.

All the information is compiled through Allied Shipbroking Inc. and Allied Chartering S.A. databases, as well as from other market sources. Despite

having taken reasonable care in the gathering, filtering and auditing of this information and believing that the information is accurate and correct,

it may still contain errors, as a lot of the views regarding market levels are partially derived from estimates and/or subject judgments while the

reported transaction activity is gathered from several sources and rumors, some of which are sometimes hard to validate in full their accuracy and

truthfulness. As such we advise that the information be taken cautiously, while advising that this information doesn’t not obviate the need to also

make further enquiries and seek further information in order to obtain a more accurate outlook. As we make no warranties of any kind, both ex-

pressed or implied, as to the completeness, accuracy, reliability or completeness of the information herein, Allied Shipbroking Inc. and its connect-

ed persons shall not be held liable to any loss or damage of any kind, including direct, indirect and/or consequential damages caused by negligence

of any kind on our part.

Any choice to rely on this information provided is strictly at the recipient’s own risk.

This report and its information is confidential and solely for the internal use of its recipients, while any re-production or re-distribution of the re-

port and its material is strictly prohibited without prior permission from Allied Shipbroking Inc.

If you wish to subscribe to this or any other report we produce, please contact us directly.

![Index [link.springer.com]978-81-322-1792...mersil 205, 207 metalaxyl 25 WP 203 miltox 203 N.F. 48 207 N.F. 65 207 panogen 205, 207 perenox 203 PMA-10 205, 207 polyram 203, 207 R-28921](https://img.pdfslide.us/doc/110x75/5b0597617f8b9aba168eaa25/index-link-978-81-322-1792mersil-205-207-metalaxyl-25-wp-203-miltox-203.jpg)