Embed Size (px)

Citation preview

Theme: Accountability in Higher Education

Topic: Role of Internal Audit and Audit Committees

in Financial Management-(Friday, 21st April 2017)

Willis O. Okwacho

Internal Auditor-General Dept

The National Treasury

Presentation Outline

Course Objective Part1-introduction to Internal Auditing

and Audit Committees

Part2: Financial Management

Environment

Part 3-Fundamentals of Internal Audit

and Audit Committees

Part4-Internal Audit and Audit

Committee Environment

4/24/2017 2

Presentation Objectives

Highlight the value proposition that

stakeholders expect from the internal

audit function in financial management.

Highlight some of the frameworks used in

the practice of internal auditing and

audit committees.

Obtain a basic understanding of the

internal audit and audit committee

processes.

4/24/2017 3

PATRT 1

INTRODUCTION TO INTERNAL AUDITING AND

AUDIT COMMITTEES

4/24/2017 4

Opening QuoteIf silence is golden, speech is platinum. Itspreads wisdom, dispels ignorance, ventilatesgrievances, stimulates curiosity, lightens thespirits and lessens the fundamental loneliness ofthe soul.

A ABJECTU ULTERIORD DISCREPANCYI IST THROWN AWAY

Muhammad Faisal SiddiquiInternal Audit Officer Brookes Pharmaceutical

Laboratories (Pakistan) Limited

4/24/2017 5

Introduction The citizens of a nation are entitled to a timely and transparent

stewardship report of their country’s financial and other activities

through the officials saddled with such responsibility according to

constitutional provisions. In some jurisdictions, this is very rare in

practice.

The internal audit function would enhance transparency in public

financial management and reporting if the unit is given full

autonomy in terms of independence and well equipped with both

human capital and relevant infrastructural facilities.

In order to attain transparent financial management and reporting

in public offices, there should be strict adherence to the nation’s

constitutional framework in terms of preparation and presentation

of financial statements, submission and review as well as timely

report of the Auditor-general to the National Assembly Public

account committee. Also, the financial statements should be timely

published for easy accessibility by the citizens.

4/24/2017 6

Position Statement Audit committees and internal auditors have common

goals. A good working relationship with internal

auditors can assist the audit committee in fulfilling its

responsibility to the senior management, board of

directors, stakeholders, shareholders, and other

outside parties. This position statement summarizes the

appropriate relationship between audit committees

and internal auditing.

Audit committee responsibilities encompass activities

which are beyond the scope of this statement, and in

no way intends it to be a comprehensive description

of audit committee responsibilities.

4/24/2017 7

History of Audit Committees Until 1967, the concept of the audit committee

received very little support, and the functions of

this committee remained undefined.

In July 1967, the Executive Committee of the

American Institute of Certified Public Accountants

recommended that publicly held corporations

establish audit committees of members outside

the board of directors, because “the auditors

should communicate with the audit committee

whenever any significant question having material

bearing on the company’s financial statements

has not been satisfactorily resolved at the

management level

4/24/2017 8

History of Audit Committees Cont..

During the 1970s, the role and responsibilities of

audit committees in the United States received a

great deal of attention because of the post-

Watergate discoveries of corporate slush funds,

illegal political contributions, and overseas bribes.

Thus the investing public demanded greater

corporate accountability to increase the

confidence in the quality of financial reporting. In

view of the separation of ownership and

management, shareholders and other

constituencies needed more assurance with

respect to both the internal and external auditing

processes and the financial reporting process4/24/2017 9

History of Internal Auditing The word “audit” comes from the Latin word audire,

meaning “to hear”. This derivation refers to the shareholders

attendance of external auditors reports which, in effect,

started only at the advent of the 19 century. But, we know

that some type of auditing existed long before 1494 when

Luca Pacioli published his principles of double entry

bookkeeping system in Venice.

Internal auditing was in practice much earlier than external

audit. In spite of its earlier existence, however, internal

auditing did not emerge as a recognized field of

professional practice until the 1940s when two factors, the

rapid development and sophistication of business,

government services and the development of statutory

audit and the establishment of the IIA in 1941 in New York,

influenced its development as a distinguished profession.

4/24/2017 10

Establishment of Internal Audit in

the Public Sector

• Sects 73 and 155 of the PFM Act, 2012 stipulate

that every public entity shall have appropriate

arrangements in place for conducting internal

audit;

• The Act further stipulates the functions of internal

audit to include:

a) Reviewing the governance mechanisms of the

entity and mechanisms for transparency and

accountability with regard to finances and

assets of the entity;

b) Conducting risk-based, value for money and

systems audits aimed

4/24/2017 11

Establishment of Internal Audit in the Public Sector

c) Verifying the existence of assets administered by

the entity and ensuring that there are proper

safeguards for their protection;

d) Providing assurance that appropriate

institutional policies and procedures and good

practices are followed by the entity; and

e) Evaluating the adequacy and reliability of

information available to management for

making decisions with regard to the entity and its

operations.

4/24/2017 12

Audit Committee (PFM Act 2012 and Regulations 2015) Sect 73(5 and 155 (5) Every public entity shall establish

an audit committee whose composition and functions

shall be prescribed by the regulations;

Regulations 174(1) subject to paragraph (2) of this

regulation, each national government entity shall

establish an audit committee;

Regulation 175. the main functions of the audit

committee shall be to

(a) support Accounting Officers with regard to their

responsibilities for issues of risk, control and

governance and associated assurance..

(b) follow up on the implementation of the

recommendations of internal and external auditors

4/24/2017 13

Internal Audit and Audit Committees-

Public Audit Act 2015

Section 33 of the Public Audit Act 2015 stipulates

that:

(1) the final report by an internal auditor which

has been deliberated on and adopted by an

audit committee of a State Organ or public entity,

may be copied to the Auditor-General.

(2) the Auditor-General shall have unhindered

access to all internal audit reports of a State or

any public entity, which is subject to audit by the

Auditor-General as provided under Article 229(4)

of the Constitution.

4/24/2017 14

IA & AC in Mwongozo-The Code of

Governance for State Corporation

Chapter three of the Mwongozo is dedicated to

Accountability, Risk Management and Internal Control

Governance Statement- The Board has the

responsibility of ensuring that the organization has

adequate systems and processes of accountability,

risk management and internal controls.

Governance Parameters include-(1) Financial

Reporting, (2) Risk Management, (3) Internal Controls,

(4) Audit Committee and the External Auditor, (5)

Procurement Process, and (6) Information

Communication Technology (ICT)

4/24/2017 15

Mwongozo- Governance

Practice In Chapter 3 Governance Practice for Chapter 3 include:

The Board should receive from the Internal Auditfunction, a written assessment of the effectivenessof the system of internal controls and riskmanagement.

The Board should ensure that the internal auditfunction monitors for rectification, weaknessesnoted by the external auditor.

The Board Committee responsible for audit shouldoversee the internal audit function and theexternal audit.

The Board should establish an internal auditfunction.

4/24/2017 16

Internal Audit and Audit Committee in

Public Companies (Companies Act 2015)

Internal Audit is not mentioned in the Companies Act.

Sec 769. (1) The directors of a quoted company shallensure that the company has an audit committee

appointed by the shareholders of a size and capability

appropriate for the business conducted by the company.

Sec 770. (1) The audit committee of a quoted company

shall — (a) set out the corporate governance principles that are

appropriate for the nature and scope of the company's

business;

(b) establish policies and strategies for achieving them;

and

(c) annually assess the extent to which the company has

observed those policies and strategies.

4/24/2017 17

PART 2

FINANCIAL MANAGEMENT ENVIRONMENT

4/24/2017 18

The Basics of Financial Management

Article 201(e) of the Constitution stipulates that:

“Financial management shall be responsible and

fiscal reporting shall be clear”. Financial Management involves planning, organising,

controlling and monitoring financial resources in order

to achieve organisational objectives.

An organisation can only achieve effective financial

management if it has a sound organisational plan.

A plan in this context means having set objectives and

having agreed, developed and evaluated policies,

strategies, tactics and actions to achieve these

objectives, in the process, managing risks.

4/24/2017 19

Financial Management

Environment

Kenyan Public, Investors, Boards and Parliament

are interested in the way public funds are

managed

Instances of failure of financial management

control frameworks

Increasing complexity of transactions and

reporting requirements

Call from stakeholders for increased transparency

of financial and performance information

Insufficient financial management expertise and

capacity (skills and numbers) to match increasing

demand

4/24/2017 20

Where Are We Now

Public is frustrated, demands better

Public wants to know problems are being fixed

Public expects consequences

Not just fraud, money is spent wisely

How Do We Tackle This?

Leadership, Governance and Accountability

Three Interconnected Principles

Accountability

GovernanceLeadership

Accountability and Performance

Measurement Frameworks the three-e performance framework, which was

created for the public sector, is identified as an

appropriate starting point.

The framework is focused on a benefit-cost

decomposition around inputs, outputs, and outcomes.

It considers the relationships between efficiency and

effectiveness, concepts adapted from the private

sector, and economy, a concept unique to the public

sector.

Efficiency can be defined as a ratio of outputs to

inputs, with the goal being to maximize output for a

fixed level of input, minimize input for a fixed level of

output, or a combination of both

4/24/2017 23

Accountability and Performance Measurement Frameworks Cont.. Effectiveness is considered in terms of the

accomplishment of organizational objectives and can

be defined as a ratio of outcomes to outputs. From a

cost effectiveness perspective, economy can be

defined as a ratio of costs to outcomes. The notion of

economy was introduced to deal with specific control

issues related to public sector entities, being the

containment of costs within specified budget levels.

Efficiency and effectiveness are relative terms, not

absolutes, and require comparison with objectives

(particularly in the case of effectiveness), planned or

past performance, or the performance of similar

organizations

4/24/2017 24

PART 3

FUNDAMENTALS OF

INTERNAL AUDITING AND

AUDIT COMMITTEES

4/24/2017 25

Definition of Internal

Auditing

Internal auditing is an independent,

objective assurance and consulting

activity designed to add value and

improve an organization's operations. It

helps an organization accomplish its

objectives by bringing a systematic,

disciplined approach to evaluate and

improve the effectiveness of

governance risk management, and

control, processes.

4/24/2017 26

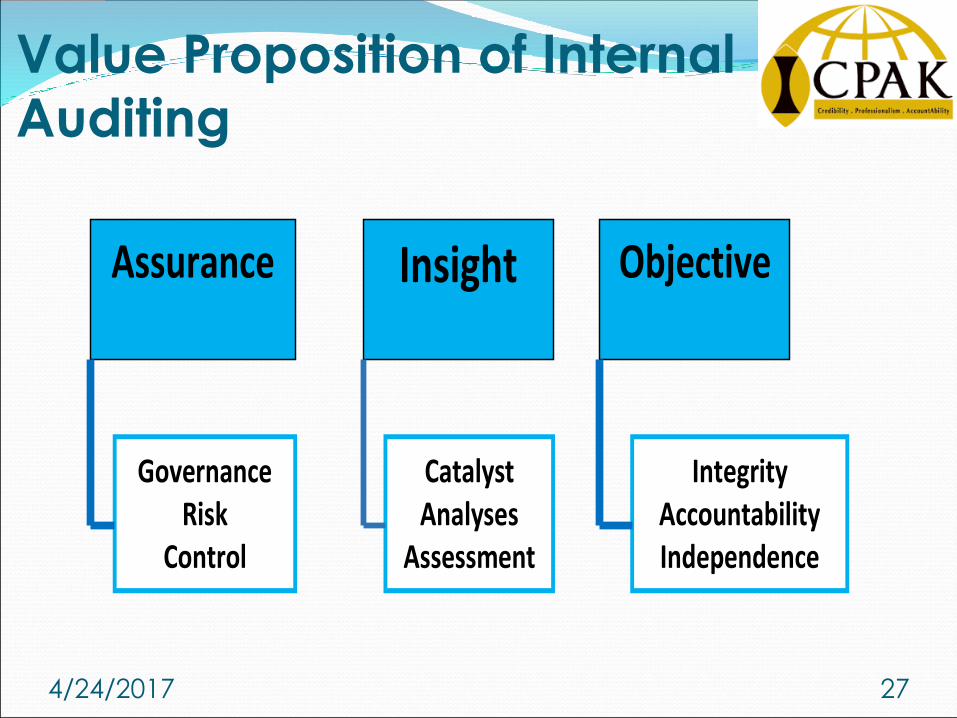

Value Proposition of Internal

Auditing

27

Assurance Insight Objective

Governance Risk

Control

Catalyst Analyses

Assessment

Integrity Accountability Independence

4/24/2017

Vision for Internal Audit

Provide fact based assurance to

Accounting Officers on the health of the

internal controls of their departments

Refocus on the basics and ensure

adequate audit coverage each year

Provide a base for balanced reporting

Make the IA function credible to

Parliamentarians and Kenyans and

other stakeholders.

4/24/2017 28

Key Pillars of the Internal Audit Vision

Reposition Internal Audit as critical for effective and

credible governance at departmental and

organisation wide levels

Qualified Chief Audit Executives (CAEs), audit

committee members and audit professionals

Standardized approaches, tools, methodologies,

periodic practice inspections

Independence and effective governance

arrangements, within departments and centrally:

Independent audit committees

Independent audit function

Accounting Officer responsibilities

Internal Auditor-General responsibilities

Timely, effective reporting and oversight.4/24/2017 29

Functions of Internal

Auditing

Internal audit is a dynamic profession

involved in helping organisations

achieve their objectives.

It is concerned with evaluating and

improving the effectiveness of risk

management, control and governance

processes in an organisation.

4/24/2017 30

Roles, responsibilities and

functions of Internal Audit

Internal audit should be the CEO and AO’s best

source of assurance about internal control. If

these officers must stand behind an entity-wide

opinion, it only makes sense that they ask for the

HIA opinion.

In public institutions internal auditors play the role

of consultants and assurance providers.

Consulting is a function of auditors in terms of

providing activities that add value and improve

the management of public organizations, its risks

management and internal control systems without

assuming the management responsibility.

4/24/2017 31

Roles, responsibilities and functions of Internal Audit Cont…

Consulting is a function is explained in the

dimensions namely (1) identification of obstacles

and causes preventing the normal unfolding of

processes, analyzing its consequences, and

finding its effective solutions; (2) getting additional

information to facilitate in-depth knowledge of

the operation of the standard system or of

regulatory stipulation by the relevant staff and (3)

training and professional development aimed to

increase skills and knowledge in management,

risks assessment and monitoring and internal

control systems.4/24/2017 32

Auditing and Internal Audit

Practices

Effective audit practices in the public sector is

very crucial as it protects the interests of the

citizens, strengthens governance by significantly

enhancing the citizens’ ability to hold their public

officers accountable.

Auditors’ duties are very important especially in

the aspect of promoting credibility, equity, and

appropriate behavior of public sector officials,

while reducing the risk of public corruption.

Audit practices entail but not limited to assurance

and advisory services (ranging from financial

attestation to performance and operational

efficiency).

4/24/2017 33

What is its value to the

Organisation?

Internal auditors help organisations to

achieve their objectives.

They do this through a combination of

assurance and consulting.

The assurance part of our work involves

telling managers and boards how well the

systems and processes designed to keep the

organisation on track are working.

Then, they offer consulting help to improve

those systems and processes where

necessary.344/24/2017

What is the role of Internal Audit and how it can help the Public Sector Organizations?

Internal audit performs three types of audits, namely;

system audit, performance audit and compliance audit.

System audit refers to an assessment of the

management and internal controls in order to determine

if they operate efficiently and effectively as they are

designed and respond to current environment of the

institutions.

In evaluating the system, internal auditors are to find the

deficiencies and provide remedial actions to be taken

on time so that they may not affect the achievement of

the set objectives. (It should be noted that accountability and

transparency in financial reporting, be it in the private sector orpublic sector, relies heavily on the adequacy and effectiveness

of the control environment and the control systems)

4/24/2017 35

What is the role of Internal Audit and how it can help the Public Sector Organizations?

Performance audit deals with examining the set

criteria of the implementation of the entity's activities

compared to the level of achievement of objectives.

Performance auditing distinguishes itself from other

forms of auditing because it focuses on the

performance of an organization, on the organizations´

projects or programmes and the systems and

procedures they use to control the performance.

Improving an organization’s efficiency and

effectiveness is one of the purposes of performance

auditing

4/24/2017 36

What is the role of Internal Audit and how it can help the Public Sector Organizations? In conducting compliance audit, internal auditors

show if the organizational activities are conducted in

line with the standards, principles, policies, and

procedures established in public spending.

Heightened pressure and accountability on corporate

governance actors, due to greater emphasis on

sound corporate governance have increased the

prominence and reliance on the internal audit

function

The internal audit function is a key component of a

entity’s corporate governance system and a resource

to a number of governance stakeholders, such as the

audit committee, and external auditors

4/24/2017 37

What is included in the audit

report?

What was found

Why it happened

What is required

What effect it has

Recommendation for improvement

Response – who, when and how

(Implementation action plan)

4/24/2017 38

What happens after the

audit?

Follow-up on the

implementation of the

action plan.

• Review corrective action

• Report to Audit Committee

4/24/2017 39

Responsibilities Of AC

• As far as Audit Committees are

concerned they generally exercise

responsibility in three important

areas:

Financial reporting.

Corporate governance.

Corporate control

4/24/2017 40

AC Responsibility in Financial

Reporting

• Provide assurance that financial disclosures made by

management reasonably portray the entity's: 1)

financial condition; 2) results of operations; and 3)

plans and long-term commitments.

• The specific steps involved in carrying out this

responsibility include:

Recommending the independent accountants.

Overseeing the external audit coverage,

including: Timing of auditor visits.

Coordination with internal auditing.

Monitoring of audit results. Review of auditorperformance.

Review of non audit services.

Reviewing accounting policies and policy decisions

4/24/2017 41

AC Responsibility in Financial Reporting Cont….

• Examining the financial statements,

including:

Interim financial statements.

Annual financial statements, auditors'

opinion, and management letters.

Other reports requiring approval by

the board prior to submission to the

other government agencies.

4/24/2017 42

AC Responsibility in Corporate Control

The responsibility of audit committees for

corporate control includes an

understanding of the organisation's key

financial reporting risk area and system

of internal control.

The committee should monitor the

control process through internal

auditing.

4/24/2017 43

PART 4

INTERNAL AUDIT

AND

AUDIT COMMITTEE ENVIRONMENT

4/24/2017 44

IA and AC Environment

1. Internal Control ComponentsControl environment:

Risk assessment and risk Management

FrameworksControl activities: policies and procedures

established to address risks and to achieve

the entity’s objectives.

Information and communication: full

recording, classification and

documentation of transactions and events.

4/24/2017 45

IA and AC Environment

Monitoring: assesses the quality of the

organization’s performance over time.

2. Tools to support implementation Staff regulations and rules, human resources

(HR) policies, sanctions and discipline, ethics

and standards of conduct, whistle-blower and

antifraud policies, integrity, management

philosophy and operating style, the way

management assigns responsibility and

authority and development of its staff (culture

of accountability).

4/24/2017 46

Gaps-Environment Risk register, risk assessment, action plan to

mitigate risks, enterprise risk management (ERM).

Enterprise resource planning, annual reports on

finance, oversight, operations/implementation

etc.

Information disclosure policy.

Internal audit, inspections, feedback and

implementation of audit/inspection

recommendations, performance assessments,

360- degree feedback on performances, senior

compacts (if applicable), scorecards.

4/24/2017 47

Conclusion The tasks, responsibilities, and goals of audit

committees and internal auditing are closely

intertwined in many ways. Certainly, as the

magnitude of the "corporate accountability" issue

increases, so does the significance of the internal

auditing/audit committee relationship.

The audit committee has a major responsibility in

assuring that the mechanisms for corporate

accountability are in place and functioning.

Clearly, one of these mechanisms is a solid, well-

orchestrated, cooperative relationship withinternal auditing.

4/24/2017 48

THE END

THANK YOU FOR LISTENING

ANY QUESTIONS?

4/24/2017 49

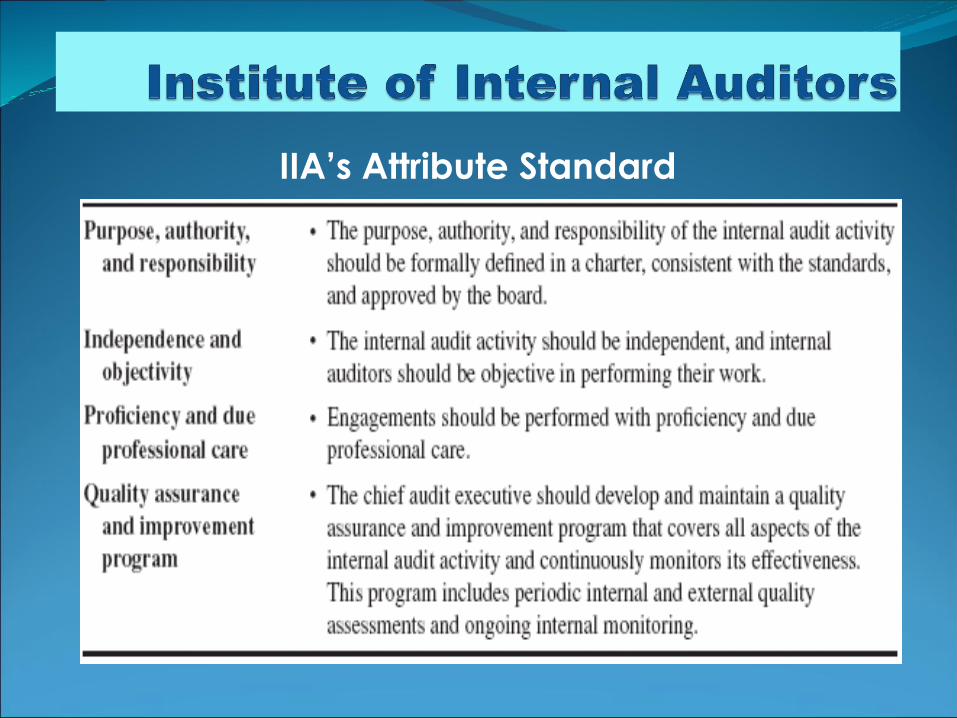

IIA’s Attribute Standard

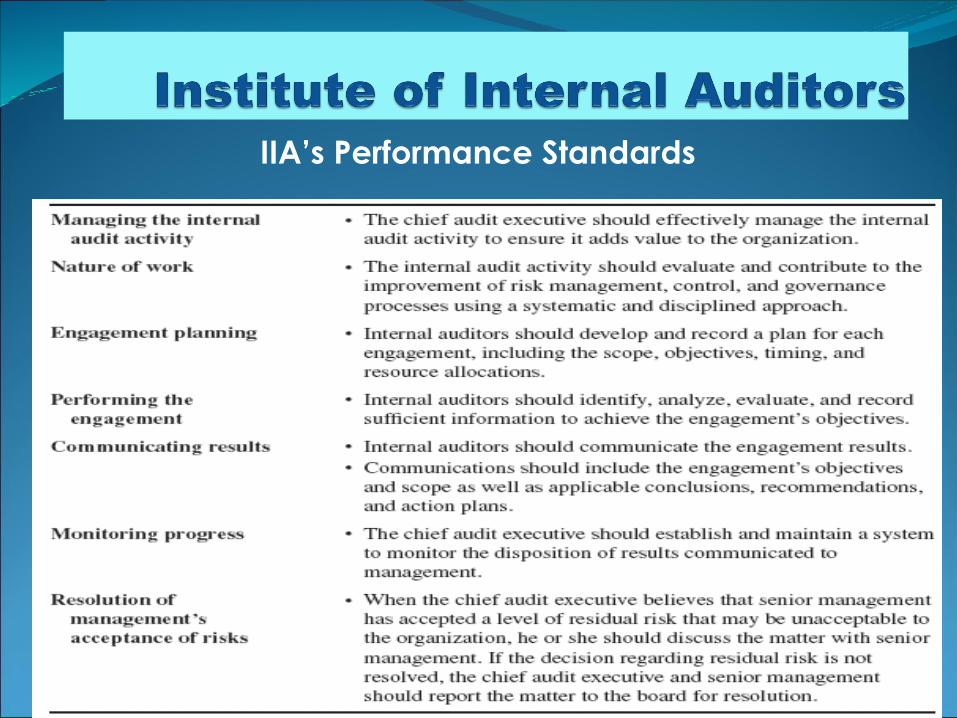

IIA’s Performance Standards