Embed Size (px)

Citation preview

1

Topic: Foreign Risk Management Techniques: Internal Hedging or External Hedging?

Paper Type: Dissertation

Word Count: 13000 words

Pages: 52 pages

Referencing Style: Harvard Referencing

Educational Level: Masters

Foreign Risk Management Techniques: Internal Hedging or External Hedging?

[Writer Name]

[Institute Name]

2

Foreign Risk Management Techniques: Internal Hedging or External Hedging?

Chapter 1: Introduction

Transnational organisations may be separated from the domestic corporations by the virtue of the

fact that they function in numerous national jurisdictions. One of the important monetary features

of different national jurisdictions is the existence of different national currencies. Foreign

exchange risk management has been an area of major focus in both the global financial

management and the international accounting study, further leading to the emergence of many

roles in recent years. Nevertheless, based upon the field research conducted on the practice of

foreign exchange risk management, Walsh (1986) suggests that the attention which foreign

exchange risk management has received in both educational and work circles is very low. In fact

during the 1980s a well-known body of empirical study suggested that models of exchange rate

developed during the 1970’s did not very well indicate the exchange rate movements in the short

run and further failed to provide an explanation (Vitale, 2007). Exchange rate economics is

branded by many aberrations, or confusions, which we find very hard to explain on the

foundation of either strong financial theory or sensible thinking. In simple sense, the global

economics business has not yet been able to construct theories and, as an effect, practical models

that provide us with the ability to describe the behaviour of exchange rates with a realistic degree

of accuracy do not seem to work effectively and this failure is displayed at different instances

(Sarno, 2005) .It is therefore identified that foreign exchange risk management needed a more

strict and stronger management. Marshall(1999,pp.186) proposes that “Although foreign

exchange risk is one of the many business risks faced by multinational companies (MNCs) its

management it has become one of the key factors in overall financial management. Whether the

objectives of MNCs are to minimise foreign exchange losses or maximise exchange gains, they

3

need to understand the extent of exposure they face and manage it to an acceptable level”. This

initiative towards a better management demands higher focus on the management of

translational, transactional and structural exposures, policies governing the economic exposures

and the factors that determine and shape the construction of hedging techniques with a further

need to make a choice between internal and external hedging techniques. Enterprises use an wide

range of internal and external techniques (including derivatives) to hedge foreign exchange and

interest rate exposures (Stanley and Block, 1980 cited in Joseph, 1999). Additionally, some

enterprises may not hedge plainly because they are not subjected to any form of exposures while

others may not hedge or partly hedge based upon on their perception about foreign exchange rate

behaviour or their confidence in utilizing derivatives (Dolde, 1993 cited in Joseph, 1999). These

reflections therefore have significant suggestions which could prove extremely beneficial in

developing a good strategic solution. This research aims to conduct a comparative study of the

internal and external hedging techniques used by transnational firms by laying focus on the

varying exposures that multinational firms are often subjected to, their benefits and drawbacks

and the degree to which these techniques can be used to balance the exposures.

1.1 Aim of Study

The study lays primary focus on what perspectives enterprises consider, when making the choice

of mechanisms which could possibly mitigate risks that are caused by the different exposures

(Hakkarainen et al., 1998). Even though the new inventions in the financial field can decrease the

demand for traditional types of hedging mechanisms and tools (Tufano, 1995), empirical data

suggests that enterprises do not focus towards the newer and more complex forms of derivatives.

4

This is mainly due to the fact that enterprises are hesitant about the banks’ commitment to those

commodities and their capability to supply practical solutions for hedging (Fairlamb, 1988;

Glaum and Belk, 1992). Additionally, the process of hedging can be implemented to different

levels based upon the degree of need. Thus, if the forward rate is an influenced predictor,

executives can change their hedging strategies to house this cause. Schooley and White (1995

cited in Joseph, 1999, pp.162) suggest that “a partial or no hedge or fully hedged strategy can be

optimal for both transaction and economic exposures. Since firms tend to place more emphasis

on transaction exposure than on economic and translation exposures, their use of hedging

techniques may reflect the types of exposures they hedge”. Therefore a more generic perception

that can be drawn is that presently hedging and its ways are under constant enquiry and

experimentation, with a possible conclusion not quite visibly near. With this overview, the chief

research question that forms an important part of the study is:

1. Which hedging technique-Internal or external can provide a more effective business solution

that can mitigate risks caused due to the different types of foreign risk exposures?

Therefore in short the aim of the study is to conclude on which hedging technique could be better

in negating the exposures that foreign exchange is subjected to –internal hedging techniques and

external hedging techniques .

5

Chapter 2: Literature Review

2.1 Introduction

Foreign exchange risks have been often listed amongst the critical risks in most business

processes however its management has been under constant supervision and forms an essential

component of financial management as a whole. Most multi-national companies often lose focus

on the extent of exposure they face, usually in the process of determining if their aim is to reduce

the exchange losses or enhance their exchange gains. Moreover, “there are statistically

significant regional differences in the objectives and importance of foreign exchange risk, the

emphasis in the management of translation and economic exposures, internal/external techniques

used in managing foreign exchange risk and the policies in dealing with economic

exposure”(Marshall,1999,pp.186). Keeping these factors in mind this proposed study attempts to

address the techniques and practices that can be adopted to efficiently manage foreign exchange

risk, the benefits they have to offer, their areas of improvisation and how each of these

techniques differ from each other. Based upon a detailed literature study of the common

mechanisms for hedging risks involved in dealing with foreign exchange, suitable suggestions

will be put forward specifically keeping in mind the organizational practices, which enterprises

follow worldwide. This chapter mainly runs through the need for global diversification, means of

rating foreign exchange risks, the varying forms of exposure and suitable hedging techniques that

can balance their effect.

2.2 Need for Global Expansion and its advantages

6

Walsh (1986, pp. 84) suggest that “the main economic justification for the existence of

diversification opportunities is the existence of correlations of less than one between different

national economies, [...] this finding is in accord with the intituitive explanation of higher

integration of geographically close economies in a relatively free trade zone”. Levy and Sarnat

(1970) suggest that being transnational aids an organisation with increased opportunities to take

advantage of the ‘commodity and factor market inadequacies’, in addition to the provision of

opportunities for risk diversification. Furthermore, Phillipatos et al. (1983 cited in Walsh, 1986)

suggests that in order to exploit the opportunities offered by global diversification specifically

with respect to the reduction of foreign exchange risks, it is quite necessary to create a balanced

and constant covariance matrix, and a suitable technique to further quantise the covariance’s

hence become necessary. However despite of the advantages or disadvantages global

diversification has to offer, it is widespread and hence in order to develop hedging mechanisms

to counter the risks that this form of an arrangement can pose, it is quite essential that one

understands the exposures that organisations are exposed to. This following section details the

different forms of exposures that transnational organisations often have to put up with.

2.3 Understanding and Measuring Foreign Exchange Risk

Trading in global markets across borders has brought about the involvement of more than one

currency and hence questions the management of multiple currencies. A transnational enterprise

dealing with sales abroad with prices being denominated in the domestic currency would actually

be prone to exchange rate exposure. In order to understand and determine the right set of

techniques and strategies that could be appropriate in hedging the risks it is necessary that one

7

understands the nature and the various forms of exposure. The understanding of different

exposures that pertain to foreign exchange demands exact measure of foreign exchange risks.

Exchange rate exposure is classified into three varying exposures: translation exposure,

transaction exposure, and operating/structural exposure (Eiteman, Stonehill, and Moffett, 2001).

2.3.1 Different forms of Global Market Exposures

Modification in the value of foreign assets and liabilities is often referred to as Translation

exposure. This form of exposure is often a resultant of the translation that occurs when an

organization’s disclosed financial results from the organization’s functional currencies to other

currencies for informative or indicative intentions. Nevertheless, translation exposure does not

show actual movements of money between diverse currency arrangements, but can evidently and

equally impact the merged profit and loss account and the affiliated balance sheet. The balance

sheet outcomes are quite often disregarded and assumed to be false and deceptive as they have

negligible monetary effect. However the degree of assets and liabilities may possess sufficient

capabilities to impact fiscal ratios evaluated by utilizing the numbers on balance sheets, which

often results in realistic logical dilemmas wherein the enterprise under consideration has

restriction on its limit of borrowings positioned by agreements.

Two chief arguments exist in the conversion of foreign exchange fiscal reports, firstly the one

that pertains to the translation technique which needs to be employed and the second deals with

determining whether the consequential profit or loss figures in the income declaration needs to

be reported, or detained and displayed in the section that pertains to the shareholders equity

section on the balance statement. The accounting standard which was formerly used in governing

8

the conduct of translation of foreign currency fiscal reports was SFAS 8 and needed

organizations to employ the sequential technique for translation. It further directed that any gains

and losses ensuing from translation needs to be incorporated in the income report which led to

the standard being strictly disapproved and removed primarily because few financial experts

claimed and accredited that this process created profits and losses, which were conflicting and

confused with the monetary actuality. SFAS 8 also marked the inception of the hedging

processes that pertained to translation exposure and was a resultant of the documenting the

unearthed profits and losses which in turn tapped the needless resources plagued by

unpredictability and inconsistency in returns and exchange rates which oscillated over phases.

The opening of FAS 52,the improvised accounting standard, initiated the approach which laid

emphasis on treating translation profits and losses as well as translation procedures to be more

dependent on the organization’s evaluation of the extent of fiscal association and empathy of the

secondary and parent company, i.e. on the functional currency of the overseas body. In the event

of the functional currency being a foreign currency, FAS 52 directs the employment of the

current rate technique with translation gains and losses being directly accredited to shareholders

equity, however in the case of the functional currency being the parent organization’s currency,

the regulations of FAS 8 come into play.

Studies demonstrate that the implementation of FAS 52 has largely condensed the call for

hedging of translation exposure (Smith and Stulz, 1985; Ziebart and Kim, 1987; Shalchi &

Hosseini, 1990).On the contrary C Olson Houston (1998) suggest that persists a lack of

confirmation and indication to sustain the affirmation that organizations have reduced hedging of

translation exposure due to of the implementation of FAS 52.On similar lines, Garlicki, Fabozzi

and Fonfeder (1987) found no considerable optimistic response to the modification or apparent

9

modification in reporting prerequisites for foreign currency translation from SFAS 8 to FAS

52.Numerous debates have often been raised on determining both the need and extent of hedging

translation exposure. Additionally, several experts’ debate that translation exposure is not viable,

as it depends on the documented values of transactions formerly carried out and as such it denies

the longer run inferences of exchange rate changes on the economical carriage and therefore the

effectiveness as well as the monetary value of an organization. The generic recommendation

often posed by financial literature is to keep any concerns pertaining to this type of exposure to a

given minimal and consequently not to hedge it.

Finance literature proposes that profits and losses resulting from conversion of foreign currency

fiscal reports have very small direct effect on an organization’s asset-supplies, and thus hedging

this revelation generates minute investor value through dipping expected price of concluding

taxes or under-investment issues. Additionally it is suggested that translation gains/losses are

underprivileged indicators of actual changes in enterprise value, which recommends that hedging

such exposures will be unproductive in dropping share price exposure. Glaum (1990), Kohn

(1990) and Belk and Glaum (1992) highlight that efficient management of foreign exchange

most imperatively requires the incorporation and application of financial exposure management.

In terms of accuracy and carefulness, the notion of economic exposure seems to be marginally of

lower magnitude than transaction and translation exposure, and is far more incompetent in

measuring and managing risks. Economic exposure comprises of both transaction and translation

outcomes but also integrates the economical state of affairs of the organization (Shapiro, 1992).

Economic exposure is characterized as the reactiveness and sensitivity of the enterprise’s

potential cash flows to unexpected and unanticipated exchange rate changes and amendments in

the combative atmosphere resulting due to the currency exchanges. The quantification of an

10

organization’s economic exposure demands comprehensive acquaintance of the enterprise

functions and exercises, and the effect of currency movements on anticipated prospective money

inflows and outflows over time. An organization's monetary currency exposure can be described

to the temperament of the enterprise's global processes, the essentiality of its overseas

competition, and the individuality of the commodity or service it fabricates (Booth and

Rotenberg, 1990). The degree, to which a corporation resources, contracts, advertises invests or

yields in overseas markets are the most noticeable and apparent determinants of its vulnerability

to currency upshots. The superior the performance of organizations in global markets, the

colossal its financial currency exposure is anticipated to be (Moles and Bradley, 2002). Monetary

exposure influences the functioning gains of organizations in internationally competition-spirited

businesses as well as organizations not affianced in the intercontinental market but face

competitors from overseas in their domestic market. Belk and Glaum (1990) ascertained that

organizations were less apprehensive about the factual effect of exchange rate modifications on

the competitive arrangement of the enterprises. Bradley and Moles (2002) suggest that there is an

important association between an organization’s exchange rate reactiveness and the level to

which it merchandises, markets and finances itself globally.

In the quest of managing economic currency exposure risk, organizations can implement either

functional or fiscal hedging mechanisms, or even an amalgamation of the two. (Srinivasulu,

1981; Aggarwal and Soenen, 1989; Soenen and Madura, 1991). Nevertheless, irrespective of the

extent of the hedging technique being classified as financial, the implementation of fiscal

hedging mechanisms demands a calculated and considered realignment of effective management

and administrative guidelines regarding assessment of financial value making its incorporation

quite operational and functional in process. Moffet and Karlsen (1994) depict the utilization of

11

fabrication, fiscal and promotional policies in the management of economic currency exposures

as `natural hedging'. Adding elements of heterogeneousness in conducting global processes is an

imperative attribute that needs to be considered in managing economic exposure, as it permits

organizations to respond competitively from the perspective of the currency movements. Since

exchange rate fluctuations have an effect on an organization’s outlay of fabrication and assembly

at home country relative to those of manufacturing in a foreign country, the enterprise may

reposition their production units between nations. The enterprise can also make subsidiary moves

in sourcing key-in or expanding the fabrication processes in a country whose currency has

diminished and reduce fabrication or sourcing inputs in countries with appreciating currencies.

Bringing about an element of heterogeneity in financing across currencies is an additional

operational strategy that can often prove beneficial in hedging economic currency exposure. This

form of strategy usually engages in assembling and fabricating the organization’s

accountabilities in a manner that alters the overseas assets values due to the fiscal exposure being

counterbalanced by connected modifications in the arrears service outlay in the same currency,

i.e. annexing debt in a currency in which the organization has recurrent cash inflow which is

divulged to economic exposure. Prevalent literature apprehends fiscal exposure management as a

vibrant notion that should be integrated into the far-sighted strategic forecasting and planning

system of the company and incorporated with all arenas of commercial decision-making (Glaum,

1990). Organizations should broaden their horizons specifically in terms of handling the markets

for both productivity and sources of provisions globally, this will permit the organization to be

accosted to be acquainted with non-equanimity when it transpires and acknowledges to it

competitively.

12

Interest rate divulgence has attained attention in current years as a consequence of a growing

tendency towards increasingly inconsistent interest rates and the mounting reputation of short-

term or variable-rate debt. Interest rates have become as unstable and unpredictable as exchange

rates over the last two decades. In the 1970s and 1980s, interest rates whether short or long term

has alternated by a marginal percentage on a month-to-month or even week-to-week basis. In the

US short term interest rate levels ranged from 5 to 18% and similar arrangements persisted in

other major nations nonetheless there is petite experiential work on interest rate exposure of non-

financial transnational organizations, with the narrow work being about the interest rate exposure

of fiscal enterprises (Choi and Eylasaini, 1997). Interest rate exposure can often be referred to

the risk that unforeseen alterations in interest rates can induce and hence unfavourably affects an

organization’s profit or currency flow; it hypothetically impacts the significance of non-financial

enterprises as well due to modifications in the monetary-flow and the importance of their fiscal

assets and liabilities. Interest rate vulnerability can also obliquely influence the competitive

position of organizations (Bantram, 2002).

The sole principal ‘interest-rate’ risk of non-fiscal organizations is debt service, with the second

being the holding of interest responsive securities (Eiteman, Stonehill and Moffett, 2000). As

transnational enterprises function in diverse nations, they probably acquire liabilities and

securities in varying currency denominations, with different interest rate arrangements (floating

versus fixed) and different maturities of debt.

The management of interest rate risks has gained an imperative place in today’s corporate world.

This is chiefly in retort to augmented competition and the accessibility of means to handle the

risk. Since 1977, a sequence of fiscal advancements has been initiated which allow organizations

to organize and manage the risk of interest rate volatility, these tools and mechanisms give

13

entrepreneurs the agility in organizing their cash flows by permitting them to transmit interest

rate risk to those better capable or more prepared to tolerate it( Farhi and Thurston,1988).

2.4 Experimentation with Hedging Techniques

The previous section highlights the existence of foreign exchange risks and that organisation are

exposed to it in varying forms demanding effective hedging techniques to retaliate and protect

firms from being plagued by such exposures. Walsh (1986, pp. 15) suggests “hedging is simply a

technique for altering the currency denomination of the firms liabilities”. Goh (2006) that

‘hedging’ behaviour is quite a followed standard in organisations that often deal with

cosmopolitan association and engagements. However as a notion is often misinterpreted and

needs an appropriate distinction from affiliated concepts of ‘balancing, containments, band

wagoning, buck passing’ and numerous allied comprehensive and strategic choices. “For

instance, while it may be argued that hedging strategies encompass balancing or containment,

they must be shown significantly engagement and reassurance components, or (more

importantly) the demonstration that apparent containment (such as alliances) are regarded as

means to ends that are substantively different from those of straight forward balancing or

containment” (Goh, 2006, pp.1). With this backdrop hedging can shortly be defined as an

assortment of strategies, techniques and practices that are developed with the sole intention of

deflecting or abstaining the development of consequences where in concerned stakeholders fail

to conclude upon choices of balancing or containment. Hedging provides a mid-st and that

circumvents or averts scenarios of making one-sided choices and hence leading to the

elimination of the other.

14

On the contrary, ‘hedging’ as a notion has been considered of less use by several literates. Logue

and Oldfield (1977, pp.352) suggest that “most foreign exchange hedging activity is ill

conceived and has little or no effect on the value of the firm. [A negative effect may even occur

as a result of hedging costs]. It appears then that corporate hedging activity in the foreign

exchange market is at best irrelevant and at worst costly”. They further propose that even in the

event of exchange rates being systematic; the act of hedging foreign exchange risks could at

most align an organisation along the security market line leading to a negligible increase in the

overall shareholder investments, thereby suggesting hedging to be a redundant activity. Walsh

(1986, pp.116) suggest that this activity is primarily extraneous became of the fact that any

“change in risk profile will be offset by an identical change in its expected return the logic is

simple. The value of a hedged firm will equal the value of an unhedged firm because the value of

hedge in equilibrium will be Zero”. Goh (2006) however suggest that the financial worth of

hedging primarily depends on the organisational size. For large firms adopting effective hedging

strategies there is a good probability of the returns exceeding the hedging costs from a fiscal

perspective, however for small sized and small to medium sized firms there is a bent towards the

hedging costs being comparatively higher. In order to obtain a better understanding on the need

for hedging and further apprehending the appropriate techniques it is quite essential to under the

market imperfections from the perspective of information non-congruence and the various forms

in which they materialize.

2.4.1 Market Imperfections

15

Logue and Oldfield (1977) suggest that the most primary and noticeable form of imperfection

that persists is the market is that of bankruptcy risk with quotable instances pertaining to those of

collapse of organisations due to exchange rate losses as in the cases of Herstatt bank and

Franklin bank being prevalent. “The underlying principle may be based on the possibility of the

firm encountering short run liquidity difficulties or breaching bond covenant because of foreign

exchange losses” (Walsh, 1986, pp.117). Warner (1977 a,b cited in Walsh 1986) suggest that

prevalent literary sources however do not suggest strong empirical evidence in this direction and

hence the cost pertaining to bankruptcy caused due to foreign exchange losses could be

considered diminutive and insignificant. Nevertheless, despite of the cost affiliated being

meagre, one needs to consider if the cost of hedging could in actually be marginally lower than

the anticipated costs pertaining to bankruptcy. Yet another imperfection is often caused by the

prevalence of organisational barriers, often barring individuals from making an entry into the

foreign market or could exist in the form of stringent transaction costs. The primary viewpoint

that holds this form of a debate is that shareholders would often want to make and deal in smaller

transactions and from an economical perspective; organisation would make an attempt to follow

these lines. However this transactional quantisation is more a function of the firm size, as large

organisational shareholders would attempt to make larger investments. A third probability

includes an internal approach of risk mediation within organisations with the primary intent of

maximization of monetary savings specifically with the intent of handling transactional costs.

Prindl (1976, cited in Walsh, 1986, pp. 118) proposes that hedging could either be “internal or

external. The former type of hedge is mediated through the firm of ‘hierarchy’ while the latter

hedge is mediated through markets. Examples of internal hedging techniques might include

adjusting intra-firm fund flows to decrease exposure, while examples of market based hedges

16

might include hedging in either forward or money markets”. The internal hedging techniques are

often employed owing to the high costs involved in transacting in markets and also due to the

presence of anomalies such as regulatory policies binding the capital market, taxation policies or

the lack of existence of a market.

Yet another imperfection which includes a very vital form of non-congruence and that persists in

the market is information asymmetry. The organisation as such seems to enjoy a higher

informational advantage and hence it would rather be beneficial if the firm hedges on behalf of

the shareholder. Moreover hedging also demands the transaction costs to be taken into

consideration.

In an idealistic capital market that possesses zero transaction costs with no market imperfections

and information non-congruence the need for hedging may seem unnecessary and irrelevant.

However the existence and role play of market anomalies is evidently prevalent in varying forms

such as bankruptcy costs, the existence of regulatory policies. Impediments to capital market

entry and taxation. Thus hedging but in a distributed and balanced manner can play a significant

role in suppressing risks arising due to fluctuating foreign exchange rates. The following section

details more on the choice of hedging techniques that can be implemented and the consequences

under which each technique would be most beneficial.

2.5 Types of Hedging Techniques

Joseph (1999) suggests that in order to understand the hedging behaviour of global firms,

specific focus needs to be laid on the extent to which the generic set of hedging technique are

employed, the arrangement and framework followed in the maturity of hedging mechanisms and

17

the exposures that need to largely focused when considering hedging. Smith and Stulz (1985)

propose that there persists a relationship between hedging and financial distress, wherein the act

of hedging can actually diminish any interest fiscal anguish by suppressing the volatility of

specific monetary measures, however simultaneously hedging can also bring about changeability

in the organisational cash flow. Froot et al. (1993) suggests that hedging also aids in the

mitigation of concerns caused due under-investment by deflating the price of extrinsic finance.

Joseph (1999, pp. 165) suggests that “firms that make greater use of: foreign currency

borrowing/lending, cross-currency interest rate swaps, and foreign currency swaps are expected

to exhibit greater variability on cash flow, liquidity and leverage, [...] in the absence of hedging,

the greater the growth opportunities of the firm the more will depend on external finance. Thus

firms are more likely to hedge the greater their growth options”.

2.5.1 Internal and External Hedging Techniques

As discussed earlier, hedging techniques can be classified as internal and external. Riehl and

Rodriguez (1977) suggest that enhanced utilization of internal techniques would be anticipated in

organisations owing to several factors such as transaction costs, inclined pricing and default risks

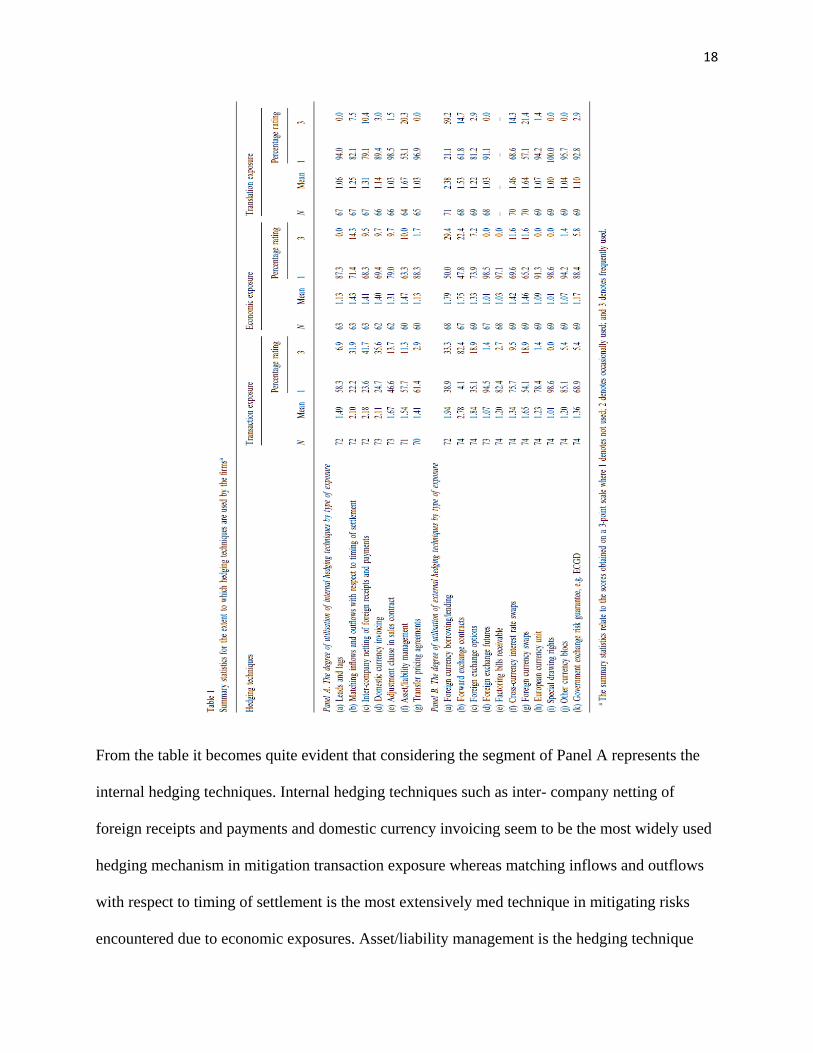

that are often affiliated to external techniques. Table 1 below details the extent of employment of

internal and external hedging mechanisms and their dependence on the nature of the exposure.

18

From the table it becomes quite evident that considering the segment of Panel A represents the

internal hedging techniques. Internal hedging techniques such as inter- company netting of

foreign receipts and payments and domestic currency invoicing seem to be the most widely used

hedging mechanism in mitigation transaction exposure whereas matching inflows and outflows

with respect to timing of settlement is the most extensively med technique in mitigating risks

encountered due to economic exposures. Asset/liability management is the hedging technique

19

utilized the most in warding off risks caused due to translation exposures. Based upon the

numerical investigation conducted by Khoury and Chan (1988) it was concluded that matching

was the most accepted and approved internal hedging mechanism comprehensively used by US

organisations and corporations is ‘Matching’, as they consider this technique to be extremely

agile and suggest that this technique poses to be one of the most self-dependant technique of

hedging foreign exchange risks.

A detailed analysis of Panel B which represents the various external hedging techniques,

suggests a similar trend of using a limited set of external hedging techniques in countering the

exposures. The most extensively used external hedging technique was concluded to be FX

forward contract which was primarily effective in hedging transaction exposure. This mechanism

is closely followed by the hedging technique of foreign currency borrowing/lending in mitigation

risks caused due to transaction exposure; however this technique also seems to be an extremely

efficient mechanism of hedging both economic and translation exposures. “The use of foreign

currency borrowing lending may reflect the desire of the firms to reduce the amount of

investment that abroad, but the degree of usage is stronger for translation exposure than for

economic exposure. Cross –currency interest rate swaps and foreign currency swaps are not

commonly used by firms” (Joseph, 2000, pp.168). Glaum and Belk (1992) suggest that the

degree of employment of FX options and futures shares a very small section of the over hedging

utilization however amongst the two, FX options seems to share a higher usage as a hedging

technique. The lesser inclination towards using FX futures could be the detrimental impact; this

mechanism could lay on the liquidity of enterprises due to the effects of daily resettlement.

20

2.5.2 Internal or External Hedging techniques: Choices and decisions

Joseph (2000, pp.168) proposes that “in general, external techniques appear to play a much more

important role in hedging decision than internal techniques. As the firms are large scale

economies in the use of external techniques and the availability of skilled treasury personnel may

contribute to greater use. However, the firms do not appear to be very selective in their use of the

techniques when hedging different types of exposures”. However taking into consideration the

complexity involved in matching the maturity of derivatives to those that are often concealed

beneath economic and translation exposures, it could be anticipated that organisations would opt

and utilize internal hedging techniques more. Based on the study conducted by Joseph (2000) it

was concluded that multinational enterprises worldwide adopt a stringent set of mechanisms in

order to conduct hedging of various exposures. The findings of the study performed suggest that

firms are gradually deviating from the conventional hedging techniques to the more fiscal

innovative hedging solutions introduced lately. The conclusions also suggested the transnational

firms across the globe laid greater emphasis on hedging transaction exposure and economic

exposure in comparison to translation exposure. One imperative proposition of the study

suggests “that like financial institutions, industrial firms are likely to make greater use of

derivatives (than internal techniques) in order to indirectly communicate their managerial ability

to operate in the derivates market” (Joseph, 2000, pp.179).

The choice of hedging techniques is also a determinant of the enterprises attributes and

characteristics which in turn impact the organisation prediction capabilities. Based upon the

findings of the study conducted (Joseph, 2000) it was deduced that extent of employment of

external hedging techniques is covered by strong annotation power of the traits of the enterprise.

It was also deduced that there existed a strong presence of a substantial cross sectional variation

21

in the features of the enterprises that were involved with hedging and affiliated activities. Also it

has been concluded through several empirical investigations that the extent of utilization of

certain hedging mechanisms often can be affiliated to an increase in the level of variation of

specific fiscal measures. However one needs to consider that the enterprises do not involve in a

setup that ensures complete hedging. The extent to which organisations hedge are based largely

on the characteristics of the firm and the kind of markets they are exposed to thus any

conclusions drawn are indeed a partial representation and any variations that can be noticed is

more a reflection of the effects of fragmented hedging. In addition to partial hedging, “maturity

mismatch of exposures and derivatives will normally give rise to some degree of variability in

financial measures” (Joseph, 2000, pp.180). A more detailed comparison of the techniques and

their usage will be conducted in Chapter 4 which revolves around an in-depth analysis of the

subject under study.

2.6 Conclusion

This chapter attempted to understand and infer from a detailed literature review of the current

state of currency volatility around the globe. To aid better apprehension a systemic and

structured approach was followed in deducing relevant information and data. Firstly the causes

and benefits of global diversification were reviewed which brought to light certain facts that

were extremely beneficial such as diversification being an organizational strategy utilized by

several transnational enterprises to diversify risk as well. Additionally global diversification also

permits in benefiting from the commodity and factor market inadequacies. An attempt was also

made to understand the quantization of foreign exchange risk by understanding the exposures

22

that this market is usually subjected to. It was concluded that on a generic basis there are three

types of exposures: translation exposure, transaction exposure and operational or structural

exposure which predominantly played an essential role in constructing and deciding upon certain

hedging techniques. The literature review conducted also made an attempt to conduct a

feasibility study of the need for hedging and how market imperfections play a role in the

deciding upon a suitable tool and mechanism.

23

Chapter 3 Research Methodology

3.1 Introduction

As the research being conducted involves the investigation and analysis of hedging techniques

and further understanding the causes of specific choices the research mechanism that was chiefly

adopted is that of ‘positivism’. Livesey (2006) proposes presence of an unequivocal association

between the ‘scientific’ and the notion of positivism. Positivism as a concept suggests

information as an entity is drawn through the appropriate recognition of actuality and the

understanding of the causes of particular social choices and characteristics, thereby promoting an

affiliation between evidence, certainty, creation of frameworks and drawing upon specific

findings through the apprehension of social (organisational) behaviour. Ever evolving hedging

techniques and their adoption by the multinational enterprises across the globe, is an innovative

and interesting area for exploration and the research conducted primarily followed the technique

of secondary data analysis. This technique was chosen primarily due to the detailed content this

mechanism offers and hence the study conducted aimed at attaining an enumerated analysis of

the need for hedging foreign exchange risks, the various hedging techniques prevalent and the

factors that determine their choice in transnational firms. The research conducted did not chiefly

demand any involvement with social entities that in any manner are allied to the management of

foreign exchange risks or those who design, construct and promote any form of hedging

techniques. Therefore the entire research was characterised by a ‘social distance’ which was

maintained throughout and any findings or conclusions drawn upon were entirely based on the

evaluation and exploration of the affiliated secondary data. This chapter primarily runs through

the subject of research, the research approach involved and the respective techniques in detail.

24

3.2 Area of Research

This research largely revolves around the current state of hedging foreign exchange risks within

the transnational corporations across the globe and a comparison of the prevalent hedging

techniques. The foreign exchange rate and its flexible behaviour has been an area of

bewilderment and ambiguity making its predictability quite difficult. Even models and theories

developed until date to understand the behaviour of the exchange rate does not deliver absolutely

accurate data (Sarno, 2005). This form of uncertainty exposes corporations and enterprises

operating at a multi-national level to risk of varying forms. This research firstly attempts to

understand the forms of exposures that persist within the foreign exchange market and

understand the order, priority and severity of susceptibility of the varying forms of exposures. An

apprehension of the different exposures further paves way in comprehending the construction

and employment of various hedging techniques within multinational firms. The research also

focuses on the different classifications of hedging techniques, why few techniques are considered

over the other, the factors that decide their usability and what organisational factor often effect

the employment of these hedging techniques. The research conducted also made every attempt to

analyse the information and data drawn through the detailed literature review to a more practical

scenario by considering a firm that implements hedging technique to retaliate and mitigate risks

caused due to foreign exchange and affiliated activities. Also a further attempt was made to

understand the factors that attributes to their choice of initiatives. Thus the research conducted in

all attempts to understand the prevalent hedging practices and the causes of making specific

choices.

25

3.3 Research Technique

The research technique that formed the essence of the study conducted demanded a sense of

engagement from the social world. More intricately, the research carried out did not involve any

direct form of communication or interaction with social entities affiliated with foreign exchange

risk management or hedging activities. The research was more developed on the basis of a

universal perspective of developments constructs and choices made and the manner in which

these mechanisms have evolved over time. This flavour of research displays typical

characteristics of the positivist approach.

Livesey (2006) puts forth that a positivistic approach affiliates and is greatly inclined to a more

epistemological approach and characterizes its designation on definitive, detailed and

hypothetical knowledge which inherently is both suggestive and descriptive. Therefore this

approach largely strengthens its hold due to its enumerating and affirming nature and emphasis

the significance of drawing conclusions to a greater extent partially sidelining the ‘what’ and

‘how’ of subjects. However on a more detailed level, the underlining research technique is that

of secondary data analysis. “Secondary analysis is the re-analysis of data for the purpose of

answering the original research questions with better statistical techniques, or answering new

questions with old data” (Glass, 1976. pp. 287) propose that secondary data analysis can be

described as “a research process or a set of endeavours that uses existing data to answer research

questions”. They further propose that often findings concluded upon have been extremely

rejuvenating and significant at certain instances that it has often outweighs the beneficial

conclusions drawn from the prevalent primary analysis. Also during the conduct of the research

at some point it became quite essential in understanding the distinction between primary and

secondary data. Boslaugh (2007) suggest that “the distinction between primary and secondary

26

data depends on the relationship between the person or research team who collected a data set

and the person who is analysing it. This is an important concept because the same data set could

be primary data in one analysis and secondary data in another”. In short, the manner in which the

data is acquired determines whether research technique corresponds to primary or secondary. In

the event the data is being documented and utilized by a researcher who is no manner directly

affiliates to the system under use or consideration, then the data is often referred to as secondary

data. The extensive utilization of secondary data analysis as a research technique is primarily due

to the high time efficiency and cost effectiveness this technique offers. This approach proffers an

extremely elevated level of fiscal benefit in the manner of data collection due to the information

being priory validated, authenticated and gathered. Even in scenarios wherein the required

secondary data is purchased, the overall cost paid may be marginally lower than the money

invested in the actual documentation of data during the primary analysis. During the collection of

primary data a lot of cost and effort is affiliated with activities that pertain to travelling, setting

up of interviews, paying individual participant etc. The massive benefits however still can be

accredited to the vast span of time that gets emancipated due to the data being priory prevalent.

This additional time margin in turn provides the researches and analyst an additional span of

time for an in depth and further exploration of ideas, theories, and concepts and hence construct

designs and frameworks igniting spirits of innovation. Yet another intensively significant benefit

of choosing secondary data analysis as a research technique is the wide span of data availability

this mechanism is capable of proffering. Varied literates and analysts have developed and

constructed varying journal, documents and literary artefacts which cover a diverse range of

subjects and hence mostly documentation is available for almost any given subject. “Other

advantages include the size of the sample, its representativeness, and the reduced likelihood of

27

bias due to for example, recall, non response and effect on the diagnostic process of attention

caused by the research question” (Sabroe , Sorensen and Olsen, 1996, pp. 435). Boslaugh (2007)

suggest that nevertheless there are several demerits affiliated to this technique. The data gathered

often does not intent to target or answer the question of the research for which it is being

considered and investigated as secondary data, therefore there persists every probability that the

data being considered may fail to the address the question or purpose of the researcher there may

also exist instances when the data needed may not be available for a particular geological terrain

as needed by the research analyst. Nevertheless even in the event of the information being

available, the research analyst is confined by data constraints and at times the entire study gets

enclosed and restricted by the data available. Additionally Sabroe, Sorensen and Olsen (1996,

pp. 435) suggest that “the disadvantages of secondary data are related to the fact that their

selection and quality and the methods of their collection are not under the control of the

researcher and that they are sometimes impossible to validate. Despite comprehensive use of

secondary data sources the literature concerning this is relatively modest”. Castle (2003, pp.287)

proposes that the applicability of secondary data could well suit scenarios wherein large samples

of data may be needed for analysis and exploration prior to concluding upon a definitive and

significant result and “may prove useful for descriptive studies, including exploratory and

correlation studies. In understanding the application and suitability of secondary data analysis as

a research technique needs a clear comprehension of what ‘descriptive’ study in actuality refers

to”. Burns and Groves (2001) suggest that descriptive form of research is primarily characterised

by an investigative and co-relative viewpoint. Descriptive studies greatly accentuate on the

abstraction and stipulation of accurate demonstration and illustration of characteristics relating to

a particular topic under study primarily through the inspection and examination of practices

28

scenarios in a meaningful attempt to analyse interpretations and annotations not acknowledged or

un investigated, to establish the pervasiveness and monotony of proceedings and happenings and

interlink or manage data. Another variant manner of acquiring descriptive information is through

the comprehensive variation and automization of prevalent data with the object of ascertaining

masked delineations, explications, interpretations and rationale often showcasing its probing

nature. The mechanism usually includes a systematic exploration that contemplates bringing out

inter connectivity through models or structures which form the basis for the abstraction as well

as affirmation of definitive conclusions.

Nicoll and Beyea (1999, cited in Castle 2003, pp. 288) suggest that “observation of trends and

changes over time using longitudinal data sets can occur with secondary data analysis. For

example secondary data analysis may be used for investigating health service utilization and

clinical outcome or effectiveness of treatment over time”. Furthermore they propose that

secondary data analysis taps specific features of research issues and concerns that often direct the

study under conduct to a deeper and far-reaching retrospection, research and inquiry, which

further creates and constructs scope for future research and proposals therefore paving way for

conducting related primary data analysis. Rew et al. (2000) proposes that realistically

implementing findings concluded upon through the means of secondary data analysis makes

efficient inputs towards the procedures of framework constructions. Nevertheless, irrespective of

all the advantages secondary data analysis proffers as a technique, the dearth of control over

information due to the sampling being massive causes the data to be marginally precise and

definitive. Also as the data being utilized for secondary data was collected and documented for a

different research purpose and objective at a time period different from the current research,

there may exist a good possibility of the information being outdated or the data sample being so

29

enormous or minute resulting in the abstraction of conclusions that relatively meaningless

(Nicoll and Beyea, 1999 Cited in Castle, 2003).

The study carried out in essentially ensured the crux elements of secondary data analysis largely

through the inspection of the varying exposures that foreign exchange poses to the multinational

firms across the globe, the classification of various hedging techniques and their applicability

through the examination and enquiry of the data gathered over the last few decades. During the

conduct of the research initial attempts were made to understand the origin and causes of foreign

exchange risks and what category of firms were often more susceptible to be these risks, the

different kinds of exposures organisations were open to and what hedging mechanisms would

effectively be beneficial in mitigating them. After an initial comprehension of the hedging

techniques and attributes that the study would lay emphasis upon, a profound research was

conducted to understand the method of analysis and practical case scenario to be considered in

order to aid a better understanding of the hedging activities that enterprises often get involved

with. Also after cautious inquiry, bearing in mind the massive data volume available for the

affiliated subject of study, stipulated duration of time and the various foreign exchange

exposures and hedging techniques to analyse it was decided the research would target to

understand the hedging activities adopted and pursued by multinational enterprises across the

globe, their retaliation techniques, how effective and efficient these mechanisms are and areas of

improvisation. Therefore the entire research conducted lays its basic on a detailed inspection and

scrutinization of the secondary data prevalent in the area of foreign exchange risk management

and the allied hedging mechanisms integral to it.

30

3.4 Research Approach

As the research is largely based on the affiliated secondary data available and includes no direct

interaction or communication with social subjects or enterprises, the study was marginally lesser

plagued by ambiguities or obscurities of any sorts that would otherwise be present such as setting

up of visits and meetings with either human participants or for observing an enterprise,

participants being influenced by affiliated yet irredundant frequencies or even data

confidentiality concerns. This significantly helped in conducting the research in more planned,

organized and ordered form and further aided in building and following a research strategy with

great ease thereby enabling in constructing a more defined research approach. In an attempt to

build the research approach is a manner that would uphold ease in carrying out; the entire study

was roughly categorized into four phases of constitution, quantisation, inspection and

scrutinization and amends and enhance.

The ‘constitution’ phase marks the inception of the complete study and is designated by

uncertainties and concerns that relate to funnelling down to a particular topic of study,

understanding and strategising as to in what manner the study needs to be carried out and

procedures and mechanisms, through which a presentable report could be constructed. This time

period was largely characterized by three main activities of constructing a research outline

inception of literature collection and study and finalizing the precise objective of the study. The

research outline built suggested a brief plan of conduct with a rough estimation of time period.

This outline also comprised of the elementary research questions that would form the core of the

entire exploration. This phase roughly spanned over the first two weeks.

31

The ‘quantisation’ phase marks the continuation of documenting and report construction which

was initially commenced during the constitution phase. The literature collected was further used

for recording the literature review which formed an essential part of the report and contained

arguments and propositions by researchers who have conducted a study on the affiliated subject

previously. The literature review was further segmented into phases to understand the different

foreign exchange exposures and suitable hedging techniques to retaliate them. During the same

time period the research approach was built and a detailed analysis of the probable research

techniques that could be utilized for the conduct of the research considered. Also the overall

research plan was designed at a very broad level and the same recorded. This period roughly

spanned over week three.

The ‘inspection and scrutinization’ phase in several ways characterises to be the most significant

and imperative phase of the entire research and directly affiliates to the conclusions and results

of the study. During this time span the secondary data gathered through the earlier phases was

explored, examined, assessed and elucidated. The data obtained was then arranged in a way such

that effective and precise results could be concluded upon. The exploration and investigation of

secondary data carried out during this time span stipulated a definitive base and accounted for

the first stipulated a definitive base and accounted for the first round of data analysis. The

conclusions drawn from this analysis were further recorded and a draft version of the report

constructed. This phase marked the longest duration of the entire research and roughly spanned

between week two to five.

The ultimate phase of this study was the ‘amend and enhance’ phase which largely involved

activities pertaining to the fine-tuning and substantiation processes. Also during this time period

a second round of data analysis was conducted and the final outline of the literature was

32

conducted upon. Chiefly this phase witnessed the report construction and largely focused on the

building of the dissertation.

3.5 Ethical Issues

Guillemin and Gillam (2004, pp. 261) propose that “ethical tensions are part of the everyday

practice of doing research- all kinds of research”. This dissertation primarily surrounds around

the different forms of exposures multinational firms across the globe are subjected to and the

nature of the hedging techniques that may be suitable in mitigating the risks that are often a

resultant of the exposures listed. Investigating the concerns and benefits of the hedging

techniques however did not hint towards the occurrence of any potential ethical concerns.

Furthermore the study conducted did not involve any form of interaction with human subjects or

any involvement with an organisation or enterprise hence the data deduced could in no manner

be termed as confidential or personal thereby leaving no space for mishappenings such as data

breaching. Furthermore as the secondary data utilized were not deduced using any quantitative

methods such as surveys or questionnaires, no consent was needed from any participants.

Therefore the overall study carried out did not pose any potential or noteworthy ethical issues.

3.6 Summary

The study carried out laid primary focus on abstracting notions through the exploration of priory

prevalent data by considering the subject of study to be distant and hence another fragment of the

system, thereby drawing an entirely unbiased worldview from an external perspective. It is this

33

characteristics of the study conducted that brings out its positivists nature as “a positivist

epistemology implies that the goal of research is to produce objective knowledge; that is

understanding that is impartial and unbiased, based on a view from ‘the outside’, without

personal involvement or vested interests on the part of the researches” (Willig, 2001, pp.3). This

chapter makes every attempt to provide an in-depth comprehension of the research approach that

was adopted and the research technique employed.

34

Analysis

Since this instrument is the more accessible for entrepreneurs, because it lessens the risk to

collect an export, pay a import or taking a loan in foreign currency. Understand foreign currency

to "checks, bills and other effects" business denominated in foreign currency. And by extension,

the revenue in all foreign currencies (convertible or non-convertible) "through the foreign

transactions". Currency does not necessarily have to be the currency in cash, but that is also

considered a document or electronic transactions that are backed by an institution. For technical

purposes - business will be taken by currency concept to all deposit in a financial institution in a

foreign country or to the documents giving right to such deposits. So it will be set at the rate of

Exchange as "the relationship of" equivalent between two currencies, as measured by the number

of units of a "country that need to be delivered to acquire one monetary entity of another".

All financial analyst must always take into account all the factors or variables individually or in

how macroeconomic Joint to the type of currency exchange rates, causing their appreciation or

depreciation.

The economic factors that influence the exchange rate are:

The current account balance: This account comprises four sub-accounts which are: the balance

of trade (imports and) (exports), balance of services, balance of income (investment and), and the

balance of transfers (income by) (unilateral transfers: donations, remittances, etc.). Thus a deficit

in the current account will cause a decrease of stocks and a fall in the exchange rate

(depreciation) and a surplus will bring with it an increase in the rate change (appreciation)

(Hakkarainen, 1998).

35

Interest Rates: The interest is simply the price of the money. It is a way of quantifying the

amounts that the debtor will have to pay to the creditor (in addition to the reimbursement of the

principal) as remuneration of the capital received credit. The difference in interest rate expresses

the relative profitability of the different currencies (Hung, 2001).

Higher interest rates attract foreign capital, this entry capital causes appreciation in the exchange

rate while that the outputs from the same will cause a depreciation of the currency.

Inflation

Inflation is known simply as "the rising" "sustained price" in a country and for a certain time.

The control of inflation today is the economic mechanism most commonly used for neoliberal

economic policies. When inflation rates rise in a country means that they are rising prices, which

leads to loss of competitiveness via prices in international trade. To correct this imbalance, the

effect on the Exchange rate is a depreciation of the national currency.

Some companies feel that the foreign exchange risk management is too complex, too costly or

requires too much time. Others claim not to know enough instruments and techniques cover, or

think that the hedging transactions are inherently speculative. However, companies that choose

not to manage their foreign exchange risk are in the facts to assume that exchange rates will

remain at their current level or will evolve in a meaning which will be favourable to them, a

decision that looks similar to the speculation. Numerous studies have established that it is

possible to mitigate foreign exchange risk by applying sound management practices. Foreign

exchange risk management provides the following benefits many companies:

• It minimizes the effects of fluctuations in the exchange rates on the margins.

36

• It increases the predictability of future cash flows.

• It eliminates the need to accurately predict in which direction will change rates Exchange.

• Facilitates the fixing of the prices of products sold on export markets.

• Temporarily protects the competitiveness of a business in a context appreciation of the dollar

(providing thereby business time) (to increase productivity). When it is possible to mitigate a risk

at a reasonable cost, it is generally accepted that company managers should take the measures

that are necessary to do it. The decision to purchase currency hedging instruments is similar to

the other forms of insurance underwriting. The insured risk, in this case, is the position of cash

and margins caused by an adverse trend of Exchange rate. Many companies protect without

hesitation their receivables against the risk of non-payment and all businesses to protect against

possible disaster purchase insurance on their property. They do this in order to protect their cash

position and to ensure that their efforts and talents are used first and to carry the business basis of

their enterprises. For many companies operating in international markets, the risk management of

Exchange is similar to the management of other insurable risks.

The first step is to define and measure the currency risk you want to mitigate. As mentioned

previously, most companies want specifically manage transaction risk. To measure the risk of

change, one for example, exporting company paid in U.S. dollars must subtract payments in US

$ it provides touch over a period of one year in the amount of $ Americans will need to make its

payments in US dollars during of the same period. The difference determines the risk to be

covered. If the company has already the US $ in the Bank, should also subtract the balance on

this account to establish NET exposure. Some companies include in their calculation only

37

transactions confirmed in foreign currency, while others also include the anticipated transactions

in foreign currencies.

When the risk has been measured, it must formulate policy exchange of company - it is the

second step. This policy should be endorsed by senior management and normally, it is expected

to respond in detail to the following questions:

• At what point does cover the exchange rate risk?

• What are the tools and instruments that can be used and under what circumstances?

• Who is responsible for managing this risk?

• How the company hedging results is measured?

• What are the obligations on the reporting of information relating to the currency risk hedging

activities?

The time from which a company has interest to cover the risk is a matter interesting. As above

methodology illustrates, transaction risk is present much more early in the process than the

accounting risk. Furthermore, the risk prior to the transaction does can be ignored, because once

the current state of global markets, selling prices, saw that they reported to the client, can rarely

be changed. Therefore, you must carefully assess at what point should cover your foreign

exchange risk.

The third step is to implement the policy covers of your business. You will want to perhaps, in

particular, increase the value of raw materials purchased from the United States to offset in part

the risk created by the sales conducted with American buyers. Another solution: you can also

obtain financial hedging instruments with a bank or a foreign exchange dealer. Financial hedging

38

instruments most frequently used are described a bit lower. The fourth step requires that you

assess periodically if hedging instruments in fact mitigate the risk to your business. The

formulation of objectives and clear reference points will facilitate this process. Which will also

minimize those to whom it responsibility to implement the policy, the feeling to have in any way

committed an error if the exchange rate moves favourably to the company and the instruments

coverage that they put in place preventing it to take advantage of this development favourable

exchange rate.

Companies have two ways to manage foreign exchange risk: natural cover and financial

coverage. Many companies employ both. The objective of the natural cover is to reduce the

difference between the sums received and the amounts paid in a given foreign currency. Take the

example of a manufacturing company that exports to the United States and is expected to reach

revenues of 5 million USD over the next year. If it provides for payments of 500 000 USD

During this period, the exhibition planned by the company to the US dollar will therefore be 4.5

million USD. To reduce this risk, the company may decide to borrow 1 million USD and

increase the value of his supplies from U.S. suppliers of 1.5 million USD. In this way, the

company is to reduce its exposure to risk $ 2 million. The company could also decide to build or

buy a production facility to the United States and thus almost completely eliminate the risk of

transaction. Natural hedging sometimes mitigate effectively the risk of changes, but their

implementation often requires long lead times (it happens that new) (suppliers in a foreign

country is difficult) and these operations often require a long term commitment (for example,

loans in USD) (Ferris, 2001).

The other method involves buying currency hedging instruments, usually with banks and foreign

exchange dealers. The most commonly used instruments of this kind are forward exchange

39

contracts, currency options and swaps. Futures contracts allow a company to fix the exchange

rates at which it buy or sell a given foreign currency amount (either at a fixed date, in) (fixed a

period inside). They are flexible instruments that can easily be paired with the future transaction

risk (typically up to a year in advance). For example, If the company plans over the coming year,

exposure to currency risk in the framework of which she will receive 350,000 USD more than it

needs to pay its bills every month, it can conclude a series of contracts for the sale at a rate term

Exchange out of this amount (or less) US $. In concluding these contracts, the company

eliminates the whole or the greater part transaction risk. Futures contracts are easy to use and

have no purchase price, this which makes them very popular with companies of all sizes.

However, the company is to contract to buy or sell to a bank or to a foreign exchange dealer a

predetermined amount in currency foreign at a later date. Otherwise, exchange contract is

terminated or extended, which may result in a cost for the company.

Currency options are another tool that can be used to mitigate the risk of transaction. These

options give a company the right, but not the obligation, to buy or sell at a later date of the

currency at an exchange rate fixed. As the options on currencies do not require the company to

sell or buy currency (unlike the) (futures contracts), they are the privileged instrument of

companies who bid to obtain a contract abroad. Currency options allow the company benefit

from favourable exchange rate fluctuations, which explains why the most of them have a

purchase cost. Take the example of a company that buys an option giving it the right to sell U.S.

dollars at an exchange rate of USD/CAD 0, 9635 in six months. If, in this time, the exchange rate

is USD/CAD 0, 9170, the company does not exercise his right to sell its US $ 0,9635 USD/CAD.

If, however, the exchange rate is 0, 9855 USD/CAD, while the company may exercise its right to

sell its US $ at the rate of 0,9635 USD/CAD. Businesses, and especially SMEs, have little

40

recourse to currency options because they perceive them as complex instruments and also

because most of the options include a purchase price. Yet, the basic options are not complex, and

some of these, commonly referred to as "tunnels at zero premium" or "Futures with participation.

», cost nothing to the purchase (although it happens that guarantees are required). The principle

behind this kind of options is simple. In consideration of the acceptance of some downside risks

(i.e., an adverse change in the exchange rate), your business will be able to benefit in part of a

favourable movement of the exchange rate. Finally, the swaps, which involve the sale and the

simultaneous purchase (or purchase and sale) a foreign currency, can help companies to match

the dates of the entries and outflows of foreign currency.

Hedging Against Currency Risk Behaviours

After studying the context, the characteristics of the undertakings in question and their

perception of the risk of Exchange, can study the knowledge that they have existing coverage

techniques, and observe their correlation with their size and their organization.

The element that appears in the vast majority of traders and producers (64%) (100% often use or

even always the euro and 85% have the choice of the currency in their contracts) is that they

have, for many, using a technique of total and non-expensive hedge against foreign exchange

risk: the choice of invoice currency, and more specifically the euro. This is good for them

because they have no problem of variation in the rates of currencies (Bodnar, and Gebhardt,

1999).

41

Still should not lose sight of when they will seek new customers, may that some importers,

fearing that the euro increases still against their currency, do not wish that the euro is the

currency of invoicing of their international purchase contracts. So that their trade relations began

well, the exporter will be so may need to adopt another currency of invoicing, and so to hedge

against any change in the course of it. This is why it is necessary that these exporters are made

aware of the different techniques that are available to them. In addition, another essential element

is to be considered by these exporters when they charge in Euros: If the importer accepts that the

euro is the currency of billing, it will sometimes bring down the sale price in negotiation (means

by which its costs related to the management of foreign exchange risk are cleared). This

opportunity cost that supports exporter to keep his client could be avoided by accepting another

currency of invoicing while covering against a possible risk. In trade relations, it is not enough to

defend its interests at any cost; it may make concessions, which may term yield many more to

the company (Hagelin, 2004).

The techniques of hedging against foreign exchange risk by producers are first insurance and to a

lesser extent the monetary clauses. Producers who have at least a technique of hedging against

currency risks have an average turnover of Euro 4 million (of which 41% average comes from

exports and 30% of the export turnover is made outside the euro area) and on average employ 12

employees. Among these, producers used four of these techniques: internal compensation, option

of currencies, borrowing in foreign currencies, which prove that some take advantage of the

opportunities offered by banks, insurance and foreign exchange market. On the other hand,

insurance, are, with the technique of factoring, the most known by producers (although factoring

is used by two of the 50 producers that responded). Overall, producers not (apart from the choice

of invoice currency) know the variety of techniques that they can put in place to cover.

42

Compensation (48% say they do not know this technique), termaillage (58%) and foreign

exchange (50%) options are, among all, the least known (Hagelin, 2004).

Traders seem rather more aware of these techniques, which seem logical given that their business

is the sale, while the producers 'produce' above all and sell or pass through an intermediary:

traders. The foreign exchange and insurance are the most used by the traders who responded to

the questionnaire, but some cite also borrowing in foreign currency, foreign currency options and

the monetary clauses. On the other hand, the termaillage is, as in products, the technique the least

used by traders. In addition, there are 4 traders on 7 (a small majority) that use one or more

coverage techniques.

Among producers, there is a fairly common response on insurance policies they use. These fonts

are not insurance against currency risk, which demonstrates once again the lack of information

on this risk producers. These responses show that producers take action when their exports, but

not to go against changes in currency. It is now, and finally, infers statistical studies previously

presented, of the theory and the replies to the questionnaires discussed just above, what are

techniques that are least well and the best producers and dealers (Joseph, 2000).

Following findings made in the part devoted to the statistical study of the sample, it was noted

that producers and traders together constituted a fairly heterogeneous group. Indeed, one side,

50% of producers are micro-enterprises and all are of small enterprises in terms of number of

employees but not in terms of realized CA, given that three of them have a CA between 7 and 16

million Euros. It goes so that the netting is not compatible with these companies that are not of

the multinational. On the other hand, not precluded, if the company is equipped with staff