Embed Size (px)

Citation preview

Topic 6: Borrowing Money

Wealth Management

Mrs. Schroeder

• Credit - promise of future payment in exchange for money, goods, services, or anything else of value.

Topic 6.01: Explain the purposes and importance

of credit

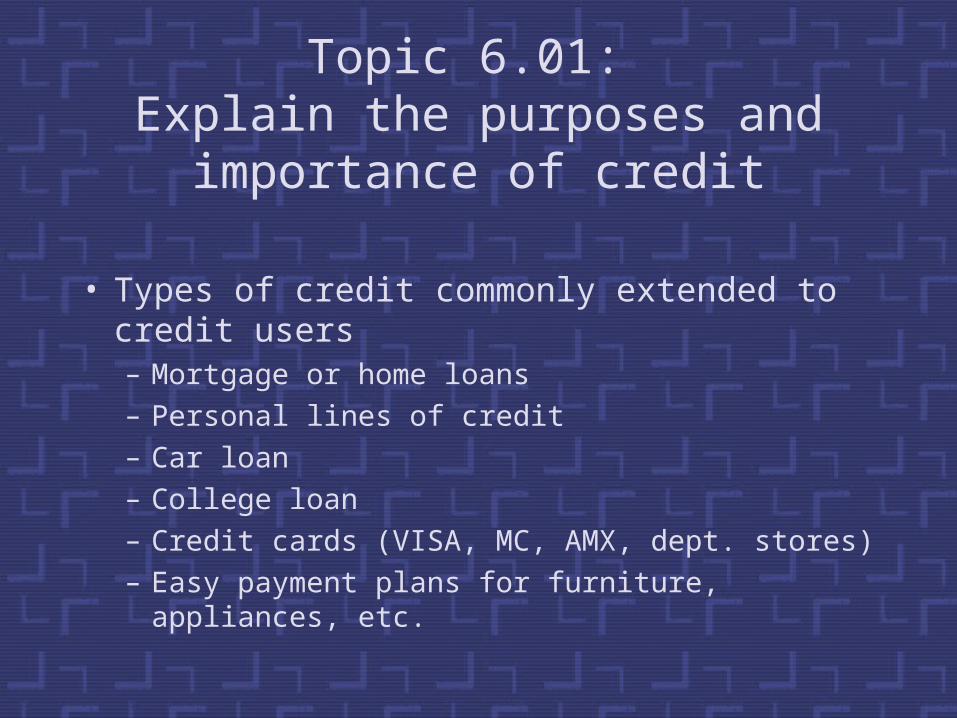

Topic 6.01: Explain the purposes and importance

of credit

• Types of credit commonly extended to credit users– Mortgage or home loans– Personal lines of credit– Car loan– College loan– Credit cards (VISA, MC, AMX, dept. stores)– Easy payment plans for furniture, appliances, etc.

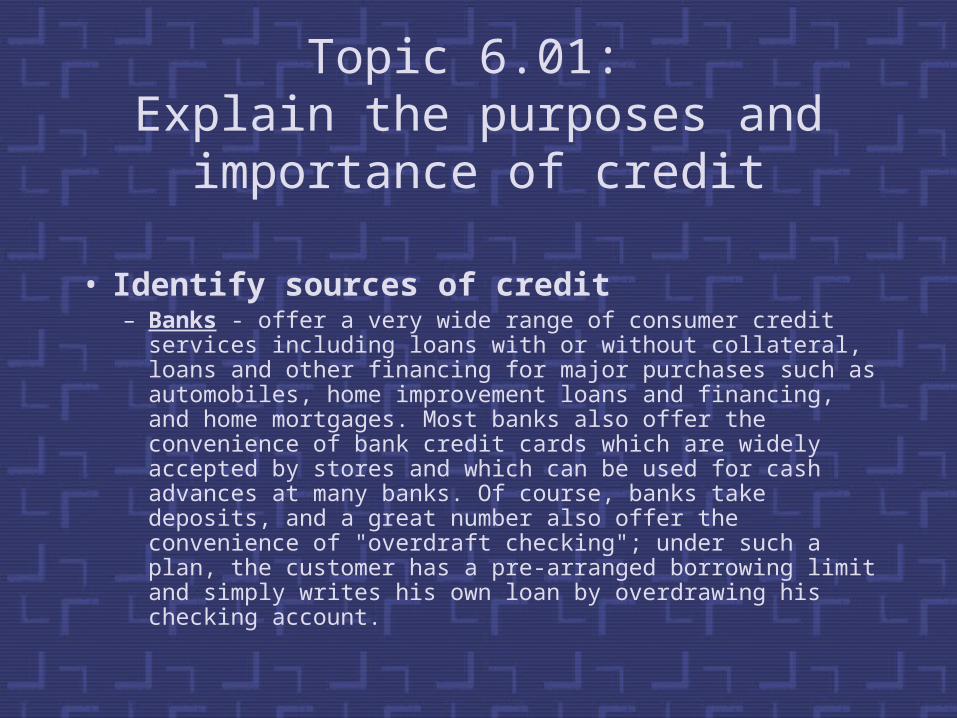

Topic 6.01: Explain the purposes and importance

of credit

• Identify sources of credit– Banks - offer a very wide range of consumer credit

services including loans with or without collateral, loans and other financing for major purchases such as automobiles, home improvement loans and financing, and home mortgages. Most banks also offer the convenience of bank credit cards which are widely accepted by stores and which can be used for cash advances at many banks. Of course, banks take deposits, and a great number also offer the convenience of "overdraft checking"; under such a plan, the customer has a pre-arranged borrowing limit and simply writes his own loan by overdrawing his checking account.

Topic 6.01: Explain the purposes and importance

of credit

– Credit unions - offer consumer loans designated "for any worthwhile purpose" to members only. Credit unions also take deposits and pay interest, offer share draft accounts and revolving loans, but, as yet do not offer credit cards.

– Finance companies - offer consumer loans and financing for all purposes to the general public. Most finance companies tend to limit the amount loaned to any one customer and do not take deposits, offer credit cards or overdraft checking.

Topic 6.01: Explain the purposes and importance

of credit

– Insurance companies - loans to holders of their policies. The loans are frequently limited to the cash value of the policy held by the borrower and must be applied for through the insurance agent or the company's home office. Rates are usually very low because you are, in essence, borrowing your own money.

Topic 6.01: Explain the purposes and importance

of credit

– Savings & Loans – mortgage loans, consumer loans (i.e., automobile)

– Merchants – Macy’s, Old Navy, American Eagle, JC Penney, Sears

Topic 6.01: Explain the purposes and importance

of credit

• Costs associated with the use of credit– Interest – When you use your credit card, the issuing bank

is really giving you a loan for the amount of your purchases. The bank charges a fee, called interest, for using its money. The credit card company pays the dress shop or the furniture store within a few days of the transaction, and you must begin repaying the loan when your monthly statement arrives in the mail. All interest charges can usually be avoided by paying the balance in full within the time limit specified on your statement. Obviously, the quicker the balance is paid in full, the less interest is paid. Be sure to learn about the terms and policies of your credit card.

Topic 6.01: Explain the purposes and importance

of credit

– Cash advances – the issuing bank or financial institution treats cash advances like loans, not like purchases of merchandise. When you take a cash advance, interest begins to accrue differently - sometimes without a grace period and at a higher rate. Check with your issuer for the cash advance details associated with your credit card.

– Annual fees – some cards, such as American Express, charge an annual fee between $75-$450

Topic 6.01: Explain the purposes and importance

of credit

• Costs associated with the extension of credit– Financial risk – customers order items they cannot afford, some

are not satisfied with what they receive and refuseto pay.

– Credit Bureau fees – When a business extends credit to a customer, it needs access to information regarding acustomer’s ability and willingness to pay for ordered items. Credit bureaus meet this need by providing a business with a customer’s payment history, banking record, and yearly income report. Information of this sort unfortunately costs money. However, this expense saves a businessmoney in the long run because credit bureaus identify customers which are financial liabilities.

Topic 6.01: Explain the purposes and importance

of credit

– Resolving disputes – Following up on late payments and tracking down delinquent customers are laborious activities which prevent businesses from focusing on more pertinent tasks. Resolving credit disputes can also give rise to expensive legal fees. If disputes are not settled peacefully, some businesses hire collections agencies or sometimes take customers to court.

http://www.bizoffice.com/library/files/credit_should.html

Topic 6.01: Explain the purposes and importance

of credit

• Reasons businesses extend credit– Increases customer loyalty– Indicates a business is financially stable– Increases sales– Guarantees satisfaction– Allows buyers to use cash for other purchases

(more likely to do business with those who extend credit)

Topic 6.01: Explain the purposes and importance

of credit

• Benefits from the use of credit– Immediate access – in case of an

emergency– Record keeping – itemized list of monthly

expenditures– Convenience – easy to use, widely

accepted– Rewards – earn benefits like free travel

Topic 6.01: Explain the purposes and importance

of credit

• Legislation affecting the extension of credit– Credit Cardholders’ Bill of Rights introduced by

Rep. Carolyn Maloney, D-NY in February 2008.– President Obama signs the bill into law on May 22,

2009.– Credit card issuers must give cardholders 45-days

advance notice of significant changes in terms and give 21 days to make monthly payments.

Activity• Locate a picture of an expensive product that you would buy on

credit (e.g., car, house, video game, big-screen TV, cell phone, etc.). Cut and paste the picture onto construction paper. Then, locate the product at three different businesses. Determine the item’s selling price, the annual percentage rate (APR) offered by a business or credit-card company, and the length of time it’d take to pay off the item if you made minimum monthly payments.

• Record your findings on the handout/worksheet entitled What’s the Cost?

• Compare the total cost of the items to determine where you’d buy the item. Paste the handout onto the construction paper with the item’s picture.

• Pair up with another student to discuss your findings.

Topic 6.02: Calculate Interest

Topic 6.02: Calculate Interest

Topic 6.02: Calculate Interest

Topic 6.03: Demonstrate Wise Use of Credit

Topic 6.04: Types of Loans

Topic 6.05: Complete Loan Application

Topic 6.06: Making Responsible Financial Decisions