Embed Size (px)

Citation preview

Top 10 Reasons U.S. Should Consider EMV January 27, 2010

Randy Vanderhoof, Executive Director, Smart Card Alliance

Deborah Baxley, Managing Principal, Keypoint Consulting

Nick Holland, Senior Analyst, Aite Group

Simon Hurry, Senior Business Leader, Visa Inc.

Dave Metcalfe, Director, Debit Payment Innovation & ScotiaCard Services, Bank of Nova Scotia

Top 10 Reasons U.S. Should Consider EMV

Welcome and Introduction

Randy Vanderhoof Executive Director, Smart Card Alliance

Who We Are

Smart Card Alliance mission To stimulate the understanding, adoption, use and widespread application of smart card technology through educational programs, market analysis, advocacy, and industry relations . . . .

Over 170 members, including participants from financial, retail, government, corporate, and transit industries and technology providers to those users

Major activities Industry and Technology Councils

Contactless and Mobile Payments Council Healthcare Council Identity Council Physical Access Council Transportation Council

Conferences, symposia, web seminars and educational workshops Web-based resources and email newsletters

Smart Card Alliance: Payments Council

Contactless and Mobile Payments Council Mission: education facilitating the adoption of contactless and mobile payments in the U.S. 37 member organizations Four active work groups:

• Consumer awareness and education • Merchant acceptance • Mobile payments • Security

Outreach to Industry Groups • Stds: GlobalPlatform, ISO/ANSI • Payment: ETA, NACHA • Security: EMVCo, FSTC • Mobile: NFC Forum, GSMA • Merchant: NRF, MAG

Today’s Agenda & Speakers

Randy Vanderhoof, Executive Director, Smart Card Alliance

Deborah Baxley, Managing Principal, Keypoint Consulting

Nick Holland, Senior Analyst, Aite Group

Simon Hurry, Senior Business Leader, Visa Inc.

Dave Metcalfe, Director, Debit Payment Innovation & ScotiaCard Services, Bank of Nova Scotia

EMV Introduction & Global Status

Deborah Baxley Managing Principal, Keypoint Consulting

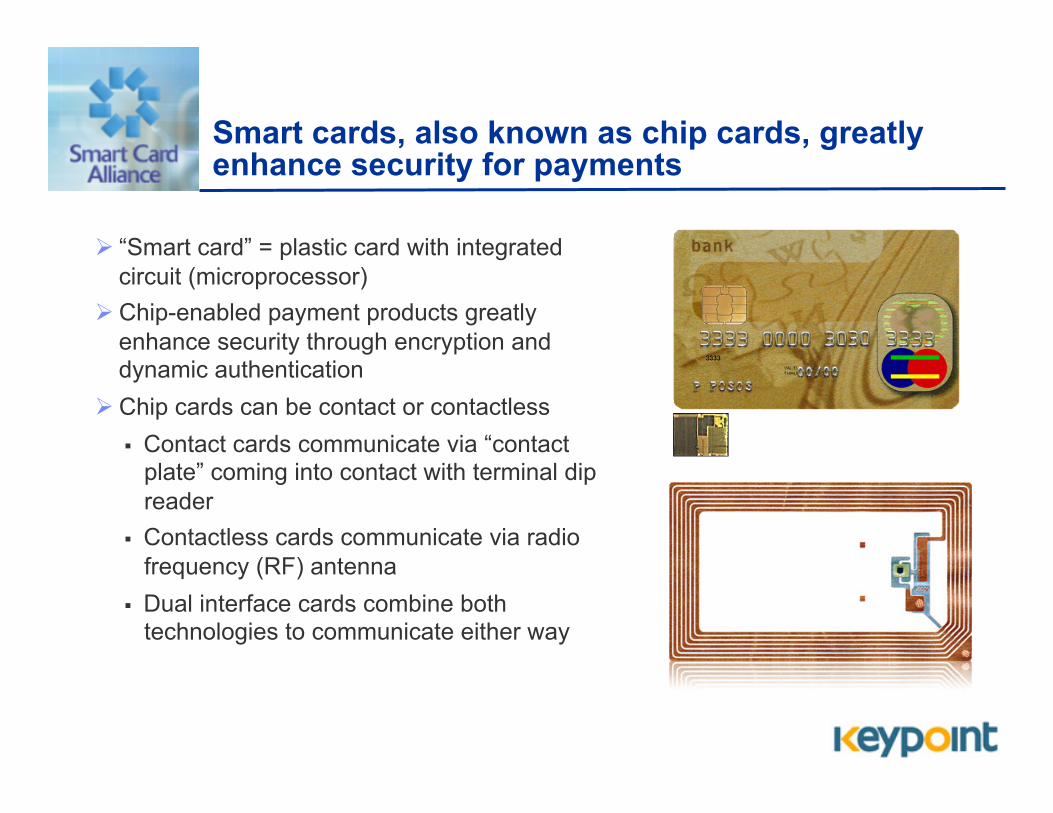

Smart cards, also known as chip cards, greatly enhance security for payments

“Smart card” = plastic card with integrated circuit (microprocessor)

Chip-enabled payment products greatly enhance security through encryption and dynamic authentication

Chip cards can be contact or contactless Contact cards communicate via “contact

plate” coming into contact with terminal dip reader

Contactless cards communicate via radio frequency (RF) antenna

Dual interface cards combine both technologies to communicate either way

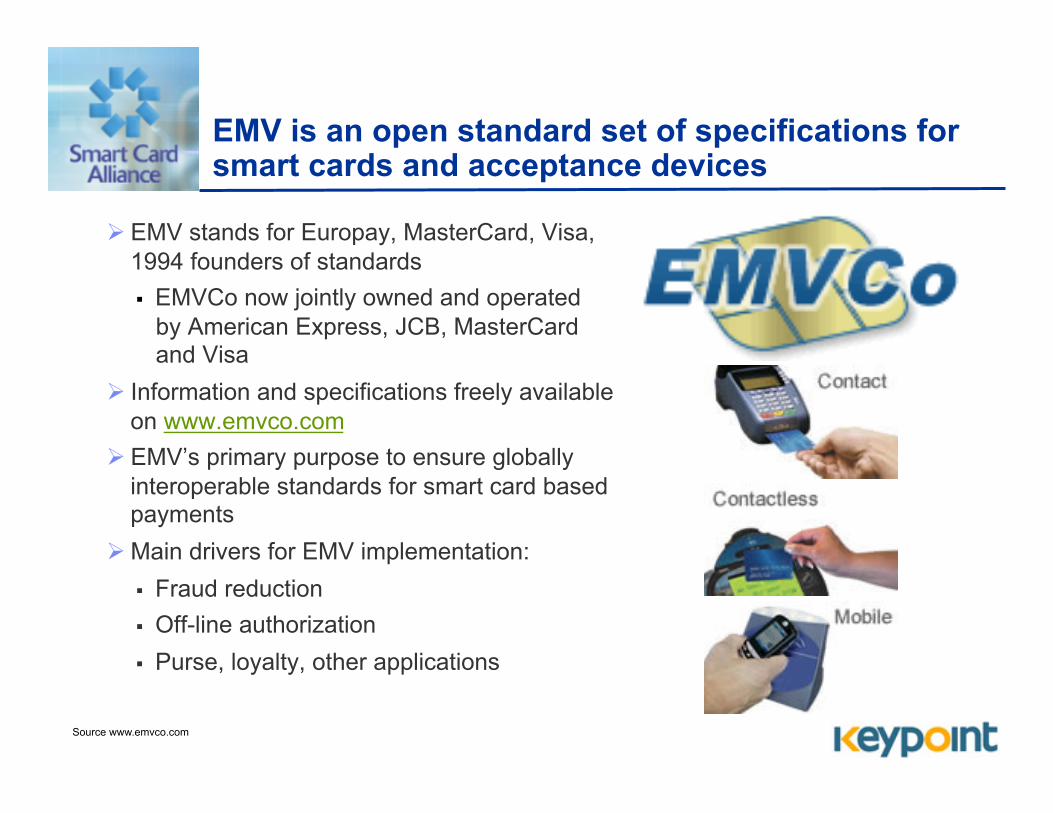

EMV is an open standard set of specifications for smart cards and acceptance devices

EMV stands for Europay, MasterCard, Visa, 1994 founders of standards EMVCo now jointly owned and operated

by American Express, JCB, MasterCard and Visa

Information and specifications freely available on www.emvco.com

EMV’s primary purpose to ensure globally interoperable standards for smart card based payments

Main drivers for EMV implementation: Fraud reduction Off-line authorization Purse, loyalty, other applications

Source www.emvco.com

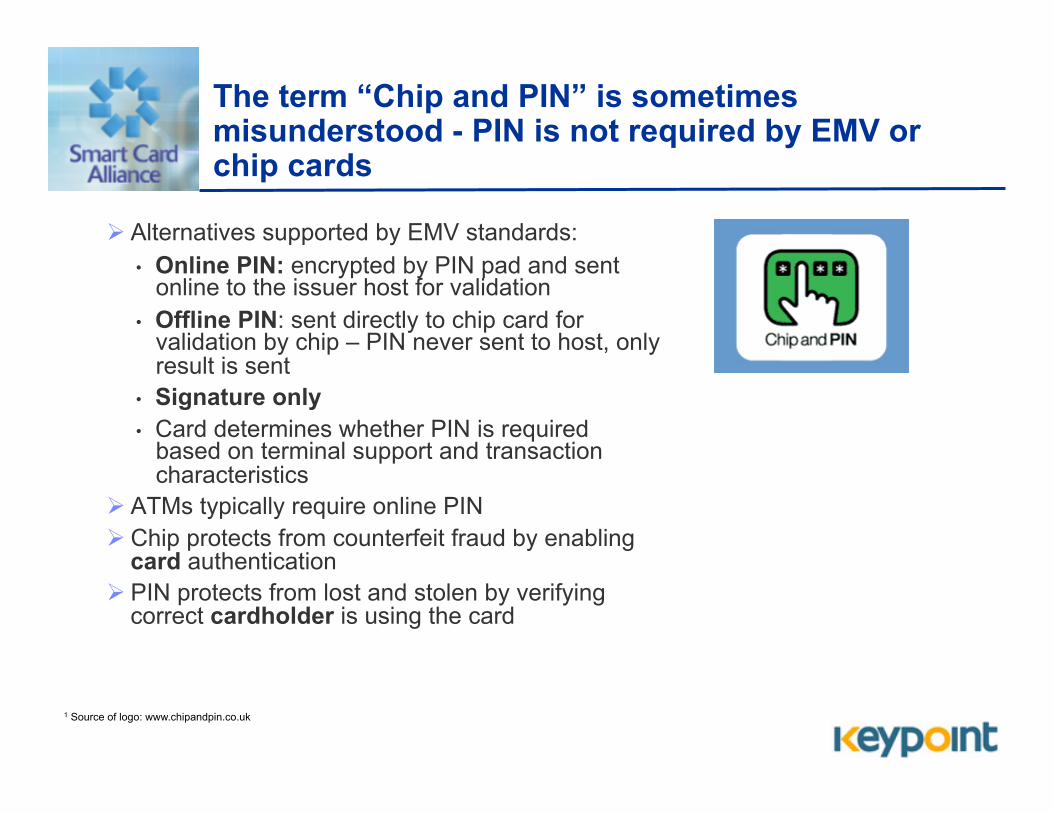

The term “Chip and PIN” is sometimes misunderstood - PIN is not required by EMV or chip cards

Alternatives supported by EMV standards: • Online PIN: encrypted by PIN pad and sent

online to the issuer host for validation • Offline PIN: sent directly to chip card for

validation by chip – PIN never sent to host, only result is sent

• Signature only • Card determines whether PIN is required

based on terminal support and transaction characteristics

ATMs typically require online PIN Chip protects from counterfeit fraud by enabling

card authentication PIN protects from lost and stolen by verifying

correct cardholder is using the card

1 Source of logo: www.chipandpin.co.uk

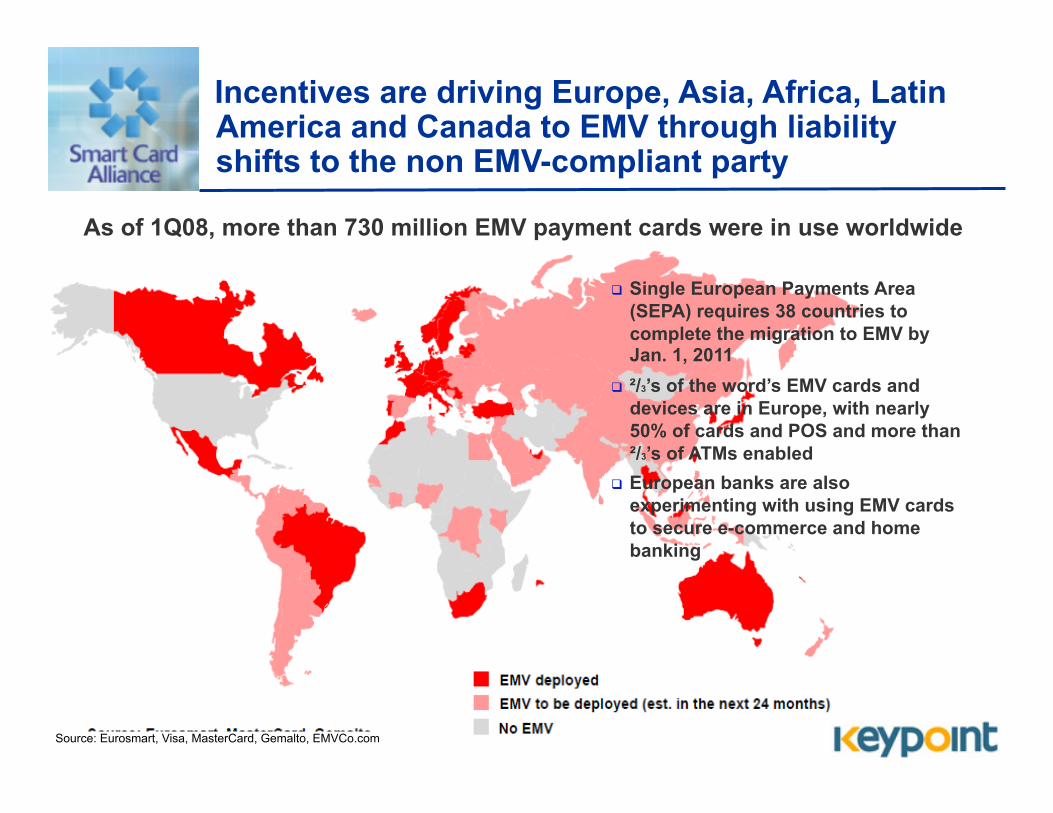

Incentives are driving Europe, Asia, Africa, Latin America and Canada to EMV through liability shifts to the non EMV-compliant party

As of 1Q08, more than 730 million EMV payment cards were in use worldwide

Source: Eurosmart, Visa, MasterCard, Gemalto, EMVCo.com

Single European Payments Area (SEPA) requires 38 countries to complete the migration to EMV by Jan. 1, 2011

²/3’s of the word’s EMV cards and devices are in Europe, with nearly 50% of cards and POS and more than ²/3’s of ATMs enabled

European banks are also experimenting with using EMV cards to secure e-commerce and home banking

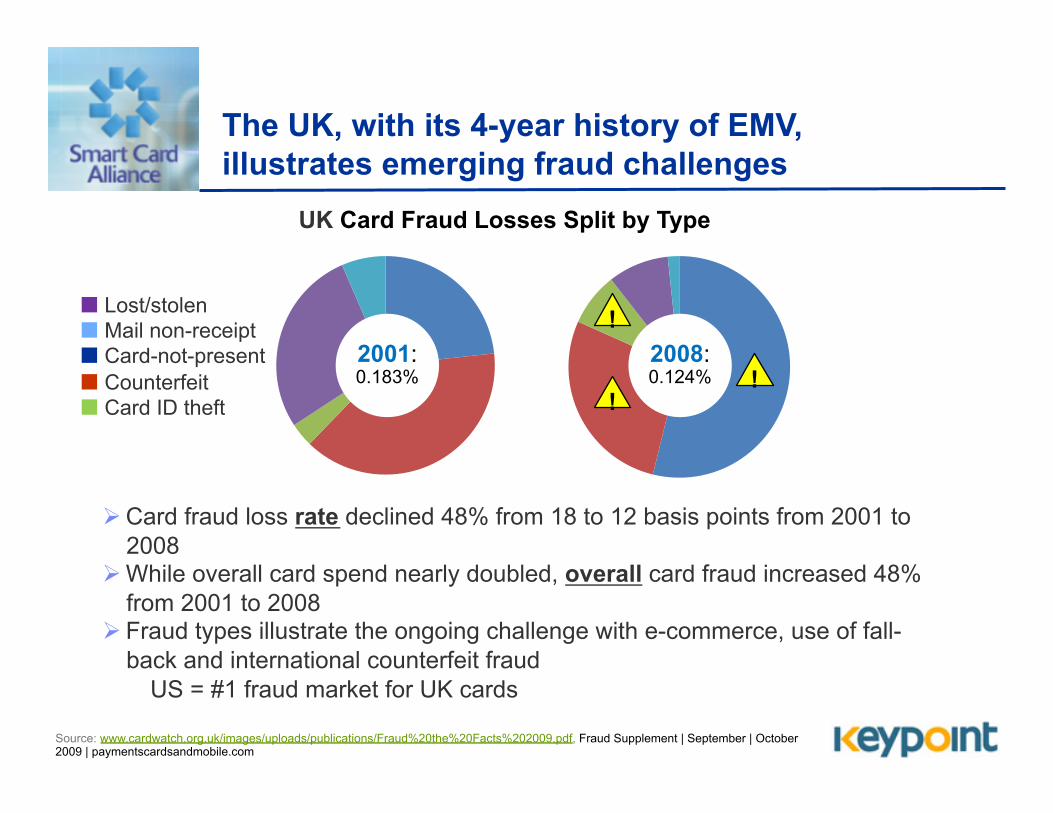

The UK, with its 4-year history of EMV, illustrates emerging fraud challenges

Source: www.cardwatch.org.uk/images/uploads/publications/Fraud%20the%20Facts%202009.pdf, Fraud Supplement | September | October 2009 | paymentscardsandmobile.com

Card fraud loss rate declined 48% from 18 to 12 basis points from 2001 to 2008

While overall card spend nearly doubled, overall card fraud increased 48% from 2001 to 2008

Fraud types illustrate the ongoing challenge with e-commerce, use of fall-back and international counterfeit fraud

US = #1 fraud market for UK cards

Lost/stolen Mail non-receipt Card-not-present Counterfeit Card ID theft

2001: 0.183%

2008: 0.124%

UK Card Fraud Losses Split by Type

!

! !

Deborah Baxley Managing Principal, Keypoint Consulting, www.keypoint123.com [email protected] 1.914.646.4732

Speaker Contact Information

The Experience of U.S. Cardholders Abroad

Nick Holland Senior Analyst, Aite Group

Methodology and Findings

In September 2009, Aite Group conducted a survey of over 1,000 U.S. cardholders that had traveled outside of the U.S. within the last three years.

Results indicated that the majority of cardholders had experienced some form of difficulty using U.S. cards while abroad.

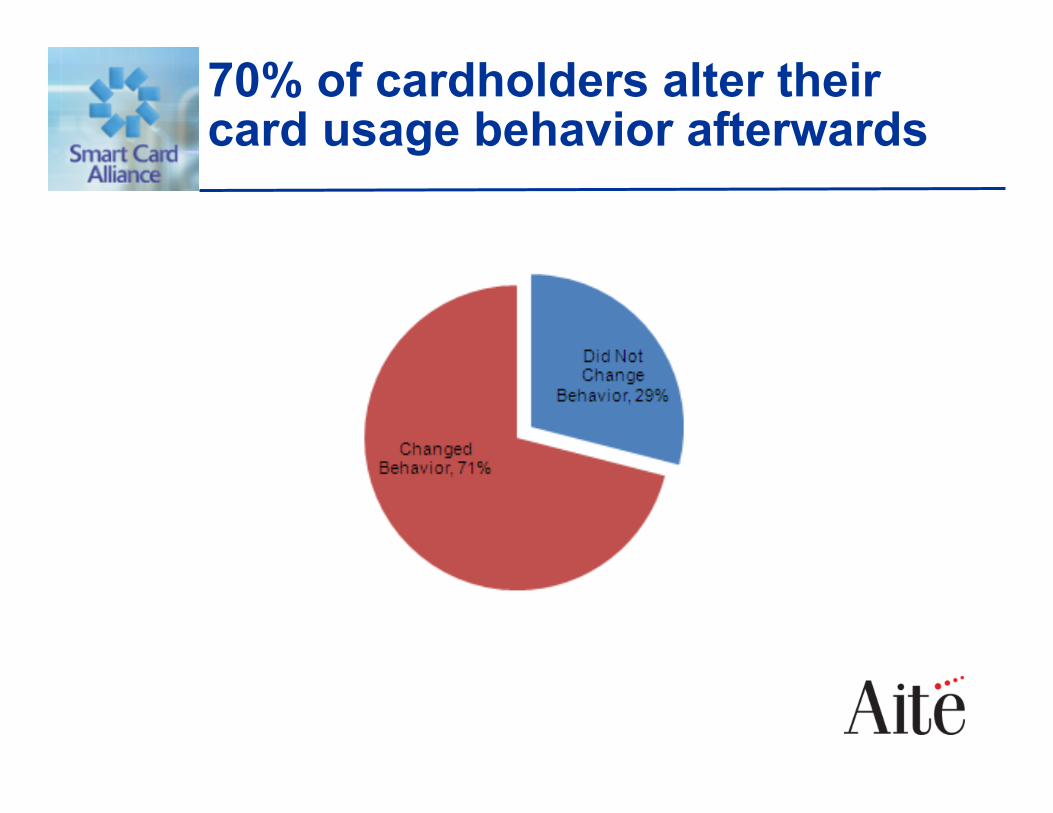

The majority of cardholders that experienced a problem would alter their payment activity after the trip to use the “bad” card less.

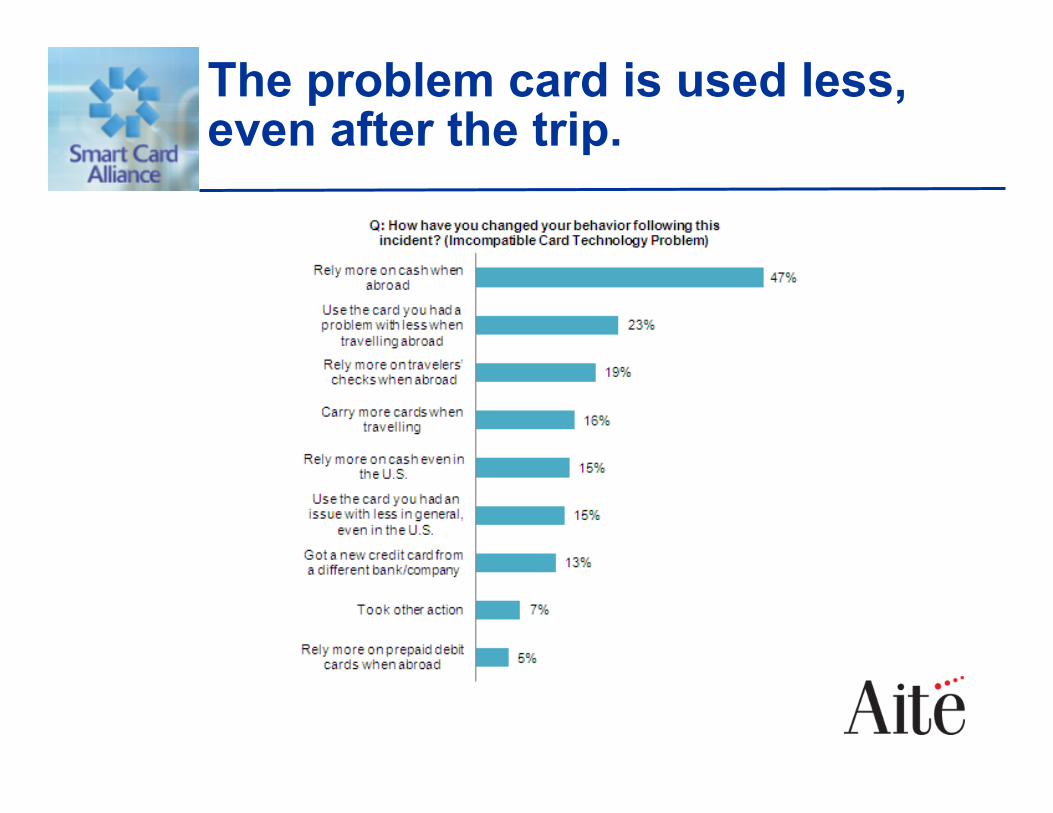

Issues caused by incompatible card technologies (ie: magnetic stripe not being accepted in EMV countries) caused the greatest cardholder dissatisfaction.

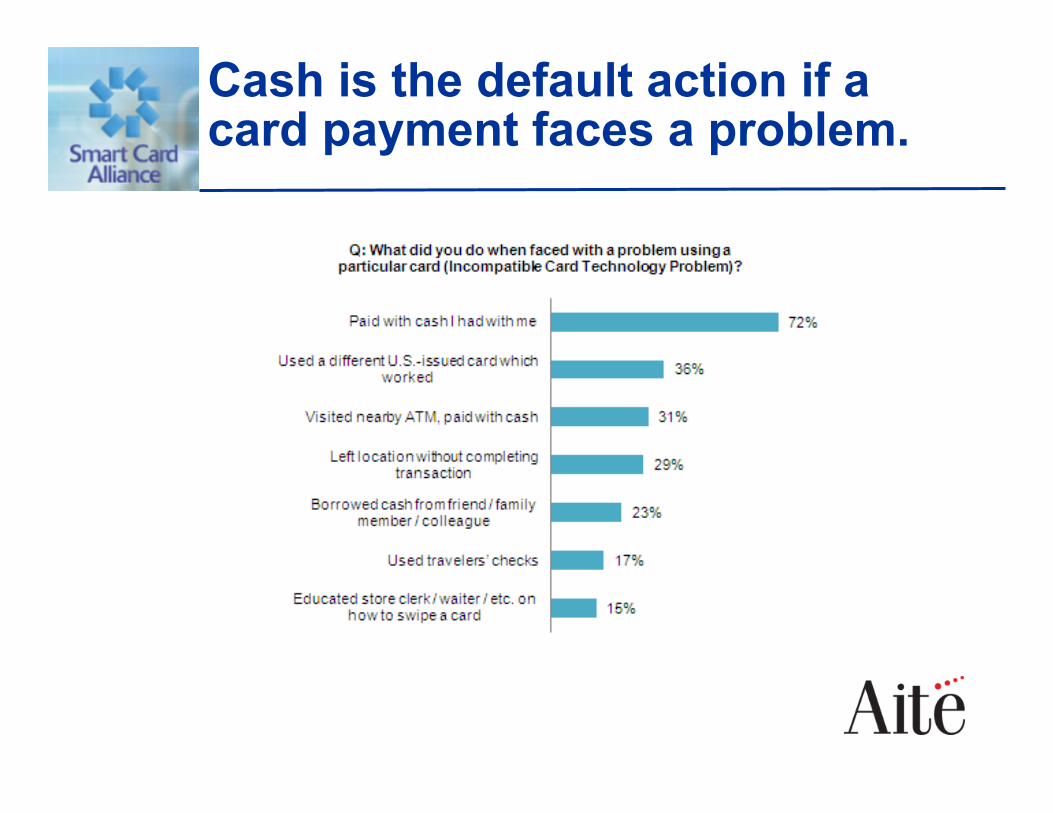

Cash is the default action if a card payment faces a problem.

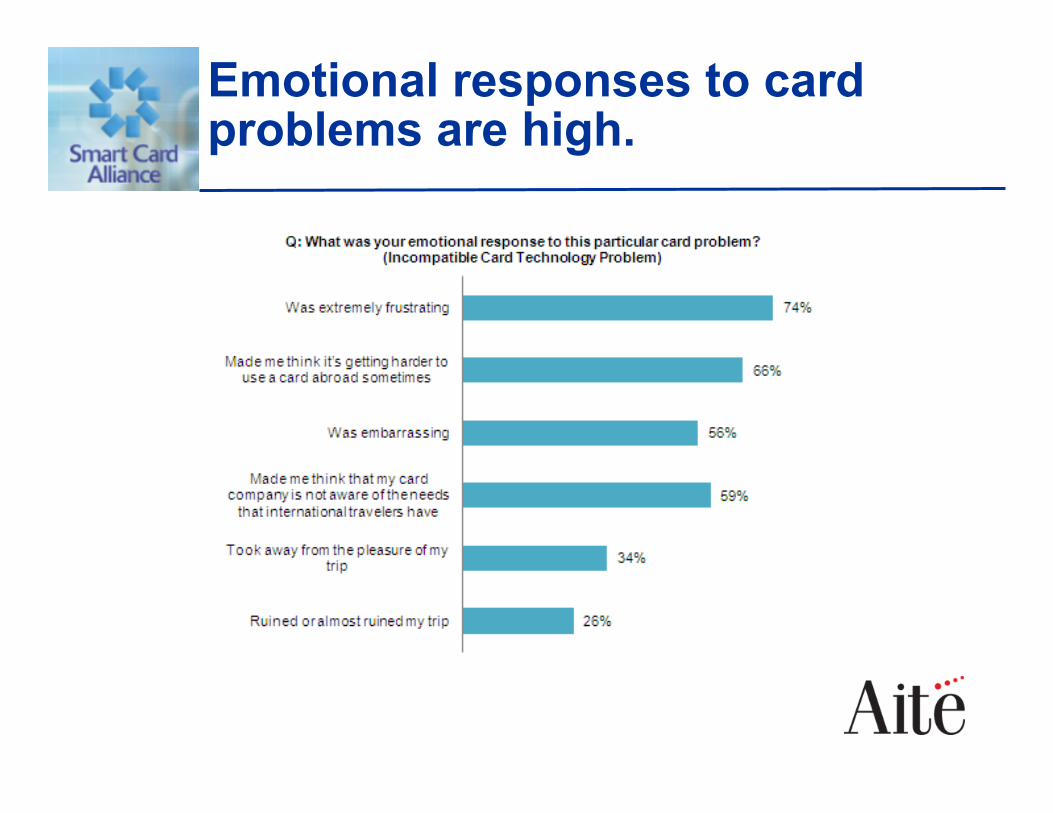

Emotional responses to card problems are high.

70% of cardholders alter their card usage behavior afterwards

The problem card is used less, even after the trip.

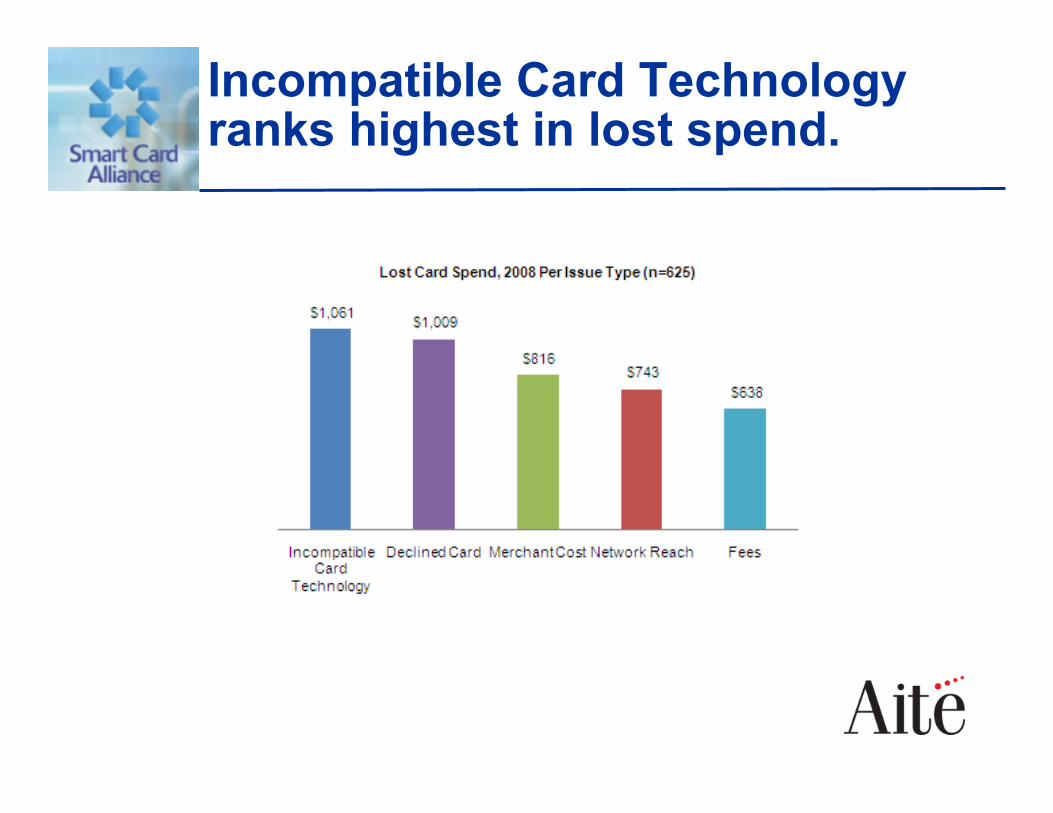

Incompatible Card Technology ranks highest in lost spend.

Takeaways

The magnetic stripe card is already facing acceptance problems outside the United States… this will only get worse.

Cardholders will “punish” a “bad” card by solitary confinement.

There is a considerable opportunity for forward-thinking issuers to capitalize on the gap in the market for an EMV compliant U.S. traveler card.

Implementation Options for US Issuers

Simon Hurry Senior Business Leader, Visa Inc.

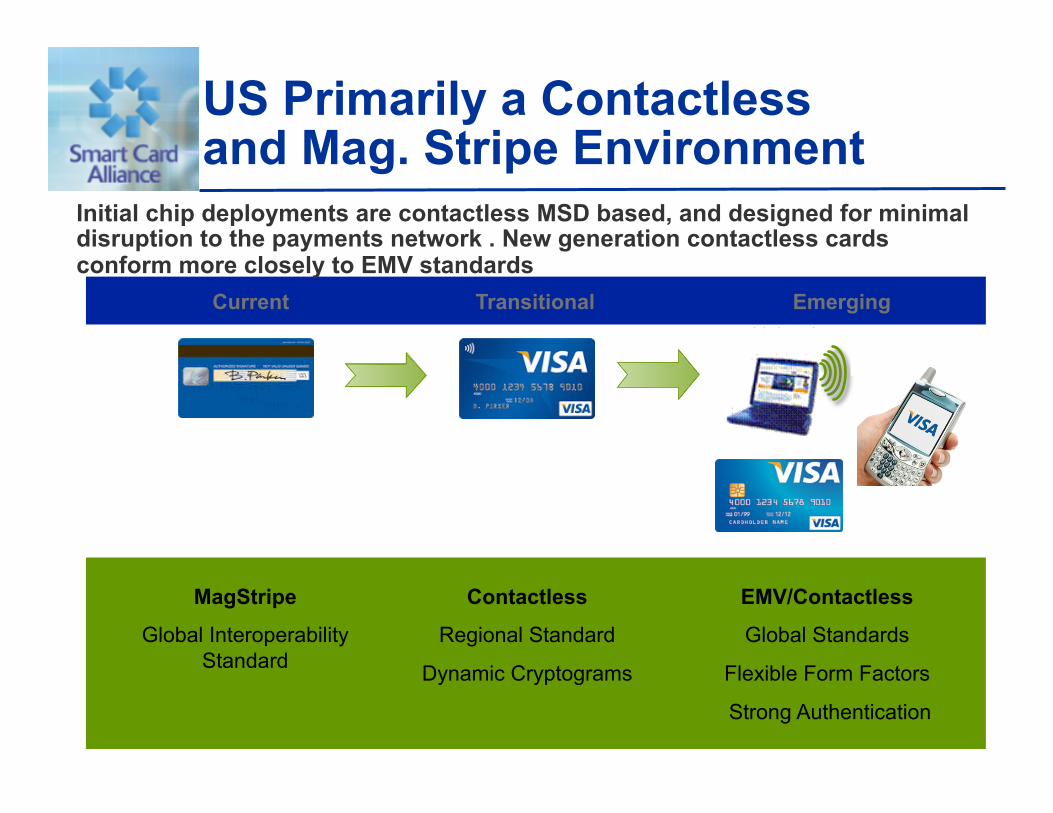

US Primarily a Contactless and Mag. Stripe Environment

Current Transitional Emerging

Initial chip deployments are contactless MSD based, and designed for minimal disruption to the payments network . New generation contactless cards conform more closely to EMV standards

MagStripe

Global Interoperability Standard

Contactless

Regional Standard

Dynamic Cryptograms

EMV/Contactless

Global Standards

Flexible Form Factors

Strong Authentication

Chip Interoperability The media have reported acceptance issues with magnetic stripe cards in mainly in European chip countries

Magnetic stripe remains the default technology for global interoperability

The card brands are actively educating merchants on the importance of continuing to accept magnetic stripe transactions

However…..

US neighbors, Canada, Mexico and Brazil, are migrating to contact chip

Contactless readers are not widely enough deployed outside the USA to offer a viable alternative to magnetic stripe

An option for US issuers is a contact chip for cardholders that travel overseas

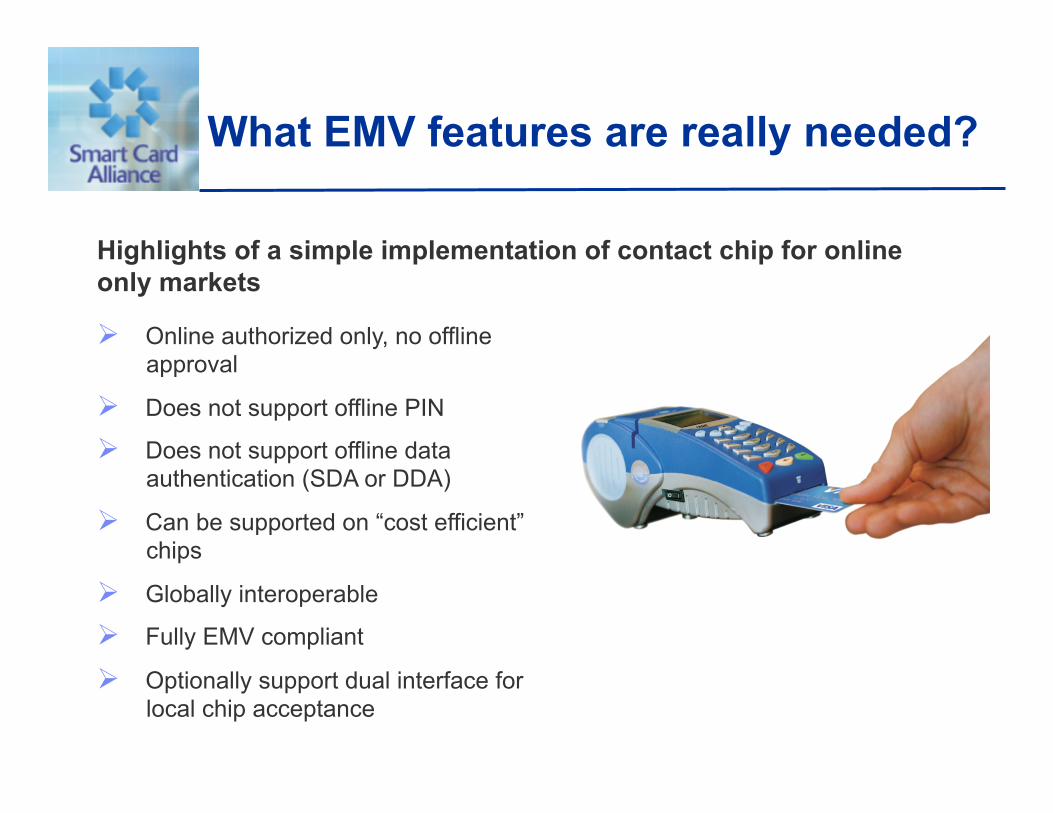

What EMV features are really needed?

Highlights of a simple implementation of contact chip for online only markets

Online authorized only, no offline approval

Does not support offline PIN

Does not support offline data authentication (SDA or DDA)

Can be supported on “cost efficient” chips

Globally interoperable

Fully EMV compliant

Optionally support dual interface for local chip acceptance

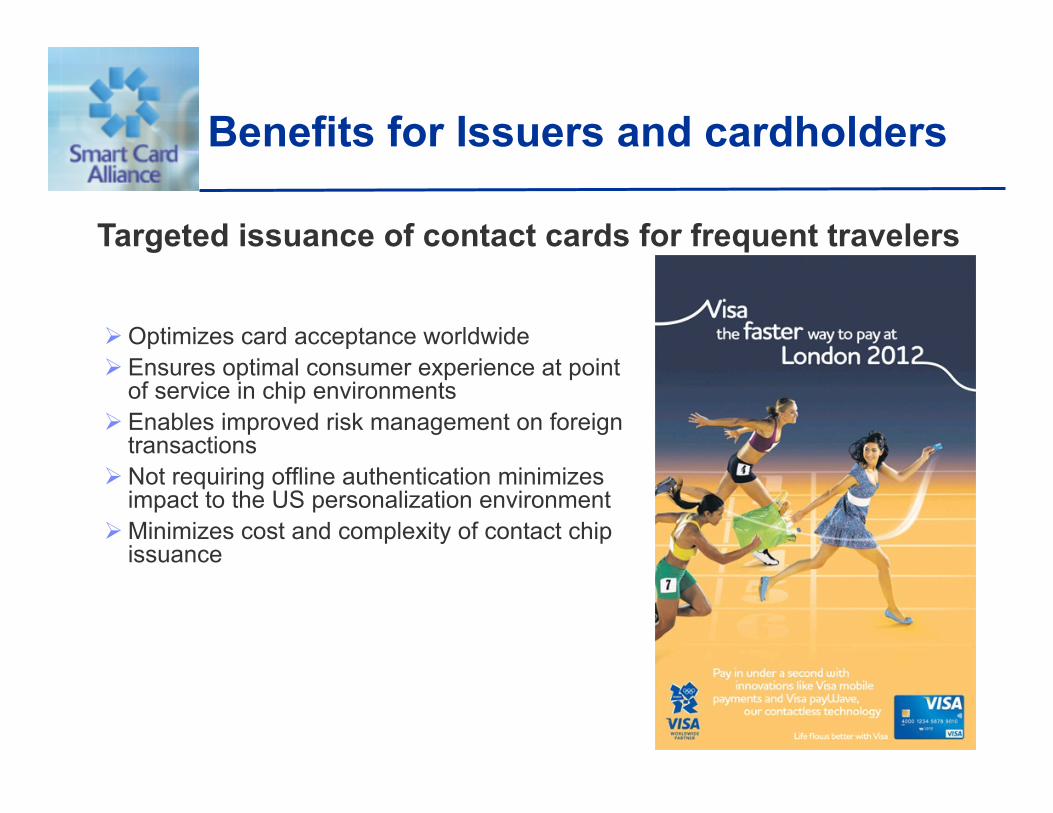

Benefits for Issuers and cardholders

Targeted issuance of contact cards for frequent travelers

Optimizes card acceptance worldwide Ensures optimal consumer experience at point

of service in chip environments Enables improved risk management on foreign

transactions Not requiring offline authentication minimizes

impact to the US personalization environment Minimizes cost and complexity of contact chip

issuance

EMV Implementation in Canada

David Metcalfe Director Debit Innovation and ScotiaCard Services, Bank of Nova Scotia

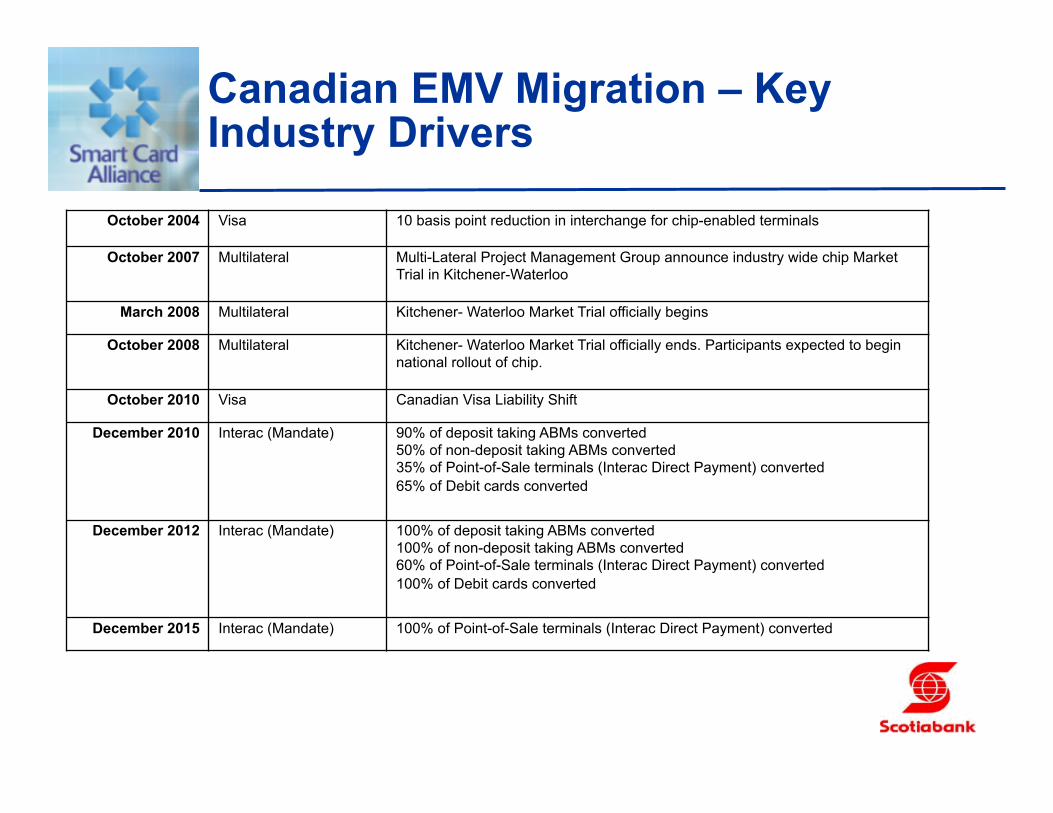

Canadian EMV Migration – Key Industry Drivers

October 2004 Visa 10 basis point reduction in interchange for chip-enabled terminals October 2007 Multilateral Multi-Lateral Project Management Group announce industry wide chip Market

Trial in Kitchener-Waterloo March 2008 Multilateral Kitchener- Waterloo Market Trial officially begins

October 2008 Multilateral Kitchener- Waterloo Market Trial officially ends. Participants expected to begin national rollout of chip.

October 2010 Visa Canadian Visa Liability Shift December 2010 Interac (Mandate) 90% of deposit taking ABMs converted

50% of non-deposit taking ABMs converted 35% of Point-of-Sale terminals (Interac Direct Payment) converted 65% of Debit cards converted

December 2012 Interac (Mandate) 100% of deposit taking ABMs converted 100% of non-deposit taking ABMs converted 60% of Point-of-Sale terminals (Interac Direct Payment) converted 100% of Debit cards converted

December 2015 Interac (Mandate) 100% of Point-of-Sale terminals (Interac Direct Payment) converted

Scotiabank EMV Project

Dedicated resources from Bank’s Project Management Office Creation of Chip

Chip Integration Office staff reporting directly to product areas (Credit Cards and Retail Deposits)

Dedicated development team with resources from all impacted systems

Scotiabank Early Data Pilot

EMV Early Data Pilot – Fall 2003 • Conducted pilot in small Canadian city with 15,000 Visa Cards • Used Early data with Visa • Minimal host changes required to approve transactions • Key learnings

Not enough terminals for customers to remember PIN

Industry Market Trial

VISA Canada, Interac Association, MasterCard, all major Canadian financial institutions, Point-of-Sale terminal providers/processors and many merchants took part in a market trial in Kitchener-Waterloo (K-W).

Kitchener-Waterloo was selected given its size, demographics and proximity to the Greater Toronto area.

Multilateral Project Management Group was established to manage the market trial.

The trial was an opportunity to test infrastructure to ensure interoperability of all systems and devices in a contained environment.

Trial announced in October 2007 (official start date: March 2008).

Trial was seen as the first phase of national conversion. There was an industry wide expectation that national rollout of chip would begin after the completion of the market trial in October 2008.

Scotiabank Market Trial Approach

Scotiabank participation was based on a phased approach due to systems implementation schedule

October 2007 – force issued limited number of Visa chip cards to staff and a select group of customers in the K-W area.

March 2008 – force issued remaining Visa chip cards in the K-W area March 2008 – started issuing debit chip cards using the following

approaches: • Branches – new, replacements, pro-active conversions plus card requests

as a result of Marketing Campaign • Marketing Campaign (direct mail and ScotiaOnline messages) – urged

customers to request cards through Call Centre, Online or by visiting branch

• Force issuance of cards through the mail

Scotiabank Key Learnings

Merchant chip education/acceptance was an issue. Significant improvement in education/acceptance as more chip cards hit the market.

Some customers unaware that a PIN is required to complete a VISA chip transaction at a chip terminal. Consumer awareness increased as media and industry attention increased. Scotiabank’s Visa communications improved awareness (Visa mailing sent out 90 days prior to card being issued, reminder mailing at 60 days).

Some customers expressed concern about having a PIN on their VISA card, as they are unable to remember a PIN. To address this issue, Chip & Signature card available (by request only).

Debit card activation for cards that were force issued was lower than anticipated. Measures are being taken with the national rollout to address this issue.

No major interoperability issues. Scotiabank took a very customer focus approach to the market trial which

proved to be very successful. Providing a positive customer experience was a key success factor.

Scotiabank National Rollout

National Rollout started January 2009. • Majority of Visa cards converted through the regular re-issue process

(conversion on expiry). • Debit cards reissued through regular process of new and replacement

cards at the branch. • August 2009 start of force conversion of remaining Debit cards.

Customer mailings prior to card conversion date. Reminder mailings sent prior to conversion date.

PIN assigned based on : 1. Existing Visa PIN 2. PIN synchronization with debit PIN 3. Random PIN

National conversion of Scotiabank Visa and Debit expected to be completed by end of 2010

David Metcalfe Director Debit Innovation and ScotiaCard Services, Bank of Nova Scotia [email protected]

Speaker Contact Information

Webinar Wrap Up and Q&A Session

Top 10 Reasons for Considering EMV in the U.S.

Fraud reduction Would improve U.S. payments infrastructure security vs. magnetic stripe infrastructure Potential exists for U.S. to become a destination for criminals and global fraud activity

U.S. and international cardholder satisfaction U.S. cardholder satisfaction diminishing when traveling internationally International cardholder satisfaction when traveling in the U.S. if EPC bans magnetic stripe

Interoperability Global migration to EMV using commercially available products and services = low risk,

proven approach to fraud reduction

Issuer positioning Potential for lost international transaction volume, customer satisfaction issues, loss of “top

of wallet” status

Innovation Initial investment in EMV is future proofing payments systems for security in long term Leverage EMV for security and interoperability of new payment methods and technologies

(ie: mobile payments, card-not-“presented” transactions

Cost-effective implementation Evolutionary approach with contactless and dual-interface cards Availability of early, online-only implementation solutions for issuers

Q&A Session

Smart Card Alliance 191 Clarksville Rd. · Princeton Junction, NJ 08550 · (800) 556-6828 www.smartcardalliance.org

Speaker Contact Information

Randy Vanderhoof, [email protected]

Deborah Baxley, [email protected]

Nick Holland, [email protected]

Simon Hurry, [email protected]

David Metcalfe, [email protected]