Embed Size (px)

Citation preview

2016 IIABL Convention Recap

Louisiana Citizen’s has a new CEO

Top 10 Insurance Bills

IIABL STAFF

Jeff Albright

Chief Executive Officer [email protected]

Francine Berendson Director of Communications

& Events [email protected]

Mike Edwards, CPCU, AAI Director of Education

[email protected] Kim Jackson

Education & Membership [email protected]

Karen Kuylen Director of Accounting

E. Lee Mowe Marketing Representative [email protected]

Rhonda Martinez, CIC

Director of Insurance [email protected]

Jamie Newchurch Insurance Services

Lisa Young-Crooks Executive Assistant [email protected]

Ask Mike

19—23

Rate & Rule Filings

29

IIABL Calendar

27

IIABL Partners

34

114th IIABL Convention & Exposition 4-8

Louisiana Citizens New CEO 15-16

Talk to your Clients About Map Changes 16

Insurance Tax Bills Passed in 2nd Session 17

Top 10 Insurance Bills of the 2016 Session 24-29

Tech Tips 31

Auto Insurance Affordability Problems 30

Commissioner’s Corner

13—14

Louisiana Agent 3

Louisiana Agent 4

Continued page 5

114TH IIABL CONVENTION & EXPOSITION

Nearly 400 insurance professionals attended the IIABL Convention in Destin, Florida June 19-22, the largest annual insurance conference in the Louisiana insurance industry. Independent agents discussed business and had a great time with their insurance companies, brokers and vendors during business sessions, social func-tions, around the pool or beach and at the bar.

55 exhibitors filled the exhibit hall Sunday after-noon and during the Opening Reception. The event was packed as people visited over drinks and fabulous food.

At the Opening Business Session, Commissioner Donelon provided an update on the state of the Louisiana insurance market. Mary Belka outlined the future challenges of the insurance business, and how independent agencies must differenti-ate themselves in an increasingly competitive marketplace. Belka also conducted two continu-ing education seminars about Overcoming Ob-stacles to Success and Redefining the Order of Things.

There was plenty of time for fun as people golfed, fished, shopped, or just relaxed around the pool or at the beach. The weather was fan-tastic, with low humidity and not too hot.

IIABA Chairman-Elect, Spencer Houldin, talked about how the Big I is working to help independ-ent agents compete against other market chan-nels and about the success of Trust-edChoice.com. IIABL CEO, Jeff Albright, wrapped up the convention with a review of the highlights of the 2016 Regular Session of the Louisiana Legislature, including the Top 10 Most Important Insurance Bills, which are outlined in another article in this newsletter.

Those who attended the convention had a great time while learning valuable information and net-working with many of their business partners.

Centauri Insurance

Imperial PFS

Louisiana Workers Comp Corp

Progressive

UPC Insurance

Louisiana Agent 5

IIABL could not have a successful convention without our insurance companies and broker partners, and would like to thank the following exhibitors and sponsors:

Access Home Insurance

Amerisafe

Burns & Wilcox

FCCI Insurance Group

Gray Insurance Co

Interstate Ins Underwriters

LCI Workers’ Comp

LCTA Workers’ Comp

LA Restaurant WC SIF

Lighthouse Property Ins

Republic Group

Stonetrust Commercial Ins Co

Travelers

United Fire Group

Wright Flood

Louisiana Agent 6

HOMEBUILDERS SIF

LANE & ASSOCIATES

LIBERTY MUTUAL

LUBA WORKERS’ COMP

MAISON INSURANCE

MARKEL FIRSTCOMP

RISCOM

RPS COVINGTON

SAFECO INSURANCE

SOUTHERN STATES GENERAL AGENCY

SUMMIT CONSULTING, INC.

SWISS RE

AMERICAS INSURANCE CO

AmTRUST NORTH AMERICA

ASI

BANKERS INSURANCE CO

CNA INSURANCE

COMMERCIAL SECTOR INSURANCE

EMC INSURANCE COMPANIES

ENCOMPASS INSURANCE

FOREST INSURANCE FACILITIES

GEOVERA SPECIALTY INSURANCE

GULFSTREAM P&C INSURANCE

HANOVER INSURANCE

Louisiana Agent 7

CONVENTION PICS

AWARDS & RECOGNITION

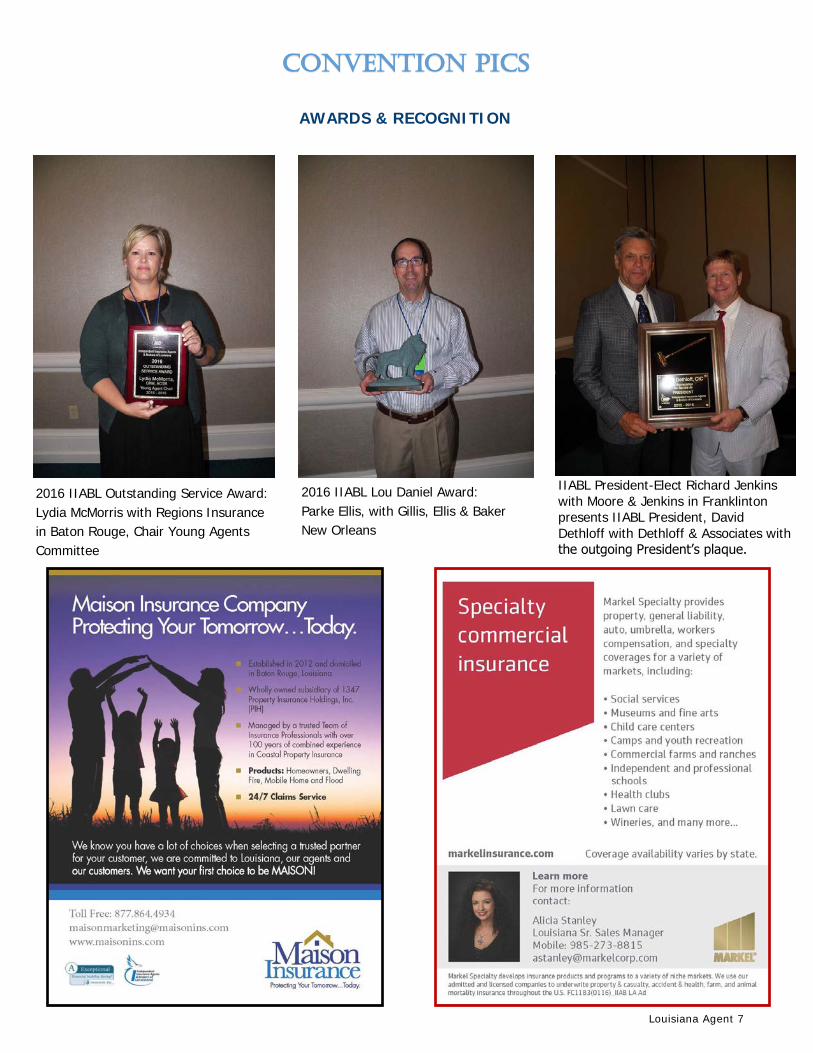

2016 IIABL Outstanding Service Award:

Lydia McMorris with Regions Insurance

in Baton Rouge, Chair Young Agents

Committee

2016 IIABL Lou Daniel Award:

Parke Ellis, with Gillis, Ellis & Baker

New Orleans

IIABL President-Elect Richard Jenkins

with Moore & Jenkins in Franklinton presents IIABL President, David

Dethloff with Dethloff & Associates with the outgoing President’s plaque.

Louisiana Agent 9

Department of Insurance Legislative Update

While legislators continue their

work in Baton Rouge during the

Special Legislative Session, the

Regular Session has concluded and I am pleased to

report progress in improving some of the licensing

processes here at the Louisiana Department of Insur-

ance (LDI). This month’s column provides a recap of

some of our legislative package, particularly those

bills which impact producers.

Act 315 made some changes in the process of ob-

taining a producer license and also in the registration

requirements. Currently an individual seeking a pro-

ducer license must first submit an application to the

Department and then take and pass a licensing ex-

amination. Under this legislation, an applicant has

the option of first taking the exam and once they

have passed the exam they can then apply for a li-

cense. Typically, the passage rate for first-time test

takers is about 50 percent. The intent of this legisla-

tion was to streamline the application process so that

applicants are not paying the $75 application fee and

then not passing the exam and ultimately deciding

they no longer wish to pursue a producer license.

Act 315 also requires that every member, partner,

officer, director and person who controls, directly or

indirectly, 10 percent or more of the business entity

to be registered with the LDI under that entity’s li-

cense. Currently, only individuals who are engaged

in the sale, solicitation and negotiation of insurance

are required to be licensed. Act 315 also adds a re-

quirement that every individual personally engaged

in soliciting or negotiating policies for a business

entity in Louisiana must be registered with the LDI

under that business entity’s license. If a person who

is registered has been convicted or pleaded guilty to

a felony or been convicted of any misdemeanor in-

volving moral turpitude or public corruption, this

law gives me authority to deny, non-renew or re-

voke the license of a business entity who refuses to

remove or discharge that person from the business.

The law further requires each licensee to notify the

LDI within 30 days if they have a change of ad-

dress, legal name, or any information submitted on

the application. Previously, each licensee was only

required to provide notification if a change of ad-

dress took place.

Two other measures passed by the Legislature align

Louisiana requirements with those in other states.

Act 367 authorizes only resident producers to sell

insurance policies issued by Louisiana Citizens Prop-

erty Corporation (Citizens). Previously, every pro-

Louisiana Agent 13

Continued page 14

Commissioner’s Corner

tion was granted to adjusters when we first started

licensing them following Hurricanes Katrina and Ri-

ta.

The law is also aimed at easing the licensing pro-

cess for Louisiana residents serving as adjusters in

the workers comp line of business. Previously, if

they were to go out of state to work as an adjuster,

and that state required a license, the Louisiana resi-

dent would have to deem that other state as their

home state for their workers comp license. That will

no longer be the case.

Another measure worth noting provides for the li-

censing and regulation of insurance consultants by

the LDI. Act 312 requires applicants seeking to be

licensed as consultants to pass a written exam, pass

a criminal background check and complete continu-

ing education requirements, among other things.

The law defines insurance consultant and sets an

initial license term of two years followed by renew-

als at two-year intervals.

You can find legislative digests on bills in their en-

tirety by logging onto the Legislature’s website at

www.legis.la.gov.

ducer licensed to sell property and casualty insur-

ance policies could sell policies issued by Citizens.

Similar residency requirements exist in Mississippi

and Texas regarding the sale of Mississippi Wind-

storm Underwriting Association and Texas Wind-

storm Insurance Association policies.

Under Act 174 all workers’ compensation adjusters

are now required to pass an exam and be licensed

in Louisiana. Previously individuals handling workers

compensation claims were exempt from licensure.

The intent of the legislation is to provide for uni-

formity in adjuster licensing. Act 174 adopts the

uniform lines of authority for adjuster licensing sug-

gested by the National Association of Insurance

Commissioners (NAIC) Uniform Adjuster licensing

guidelines and brings the licenses issued by Louisi-

ana in line with adjuster licenses issued by most

other states. The law becomes effective August 1,

2017 which will provide time to develop the exam.

There is a grandfathering provision providing an

exemption from the exam for those who have been

employed as workers comp adjusters for at least

three of the last five years. A similar exam exemp-

Louisiana Agent 14

Louisiana Agent 15

Insurance Commissioner Jim Donelon announced to-day that he has named Richard Newberry as the new Chief Executive Officer of Louisiana Citizens Property Insurance Corporation (Citizens).

“As the insurer of last resort, Citizens plays a vital role in our property insurance market and we conducted a nationwide search to find an individual who will build on the successes Citizens has seen over the last sev-eral years,” said Commissioner Donelon. “I’m pleased to bring on board a proven leader who has 23 years of insurance industry experience encompassing oper-ations, claims, technology implementation, financial reporting and much more.”

Newberry brings a wealth of experience to the posi-tion of CEO of Citizens. He has served in many capac-ities for Oklahoma Farm Bureau Mutual Insurance Company over his career. Beginning in 1993, he worked his way through the claims department from adjuster to Vice President of Claims. He currently serves as the Executive Vice President and General Manager of the Oklahoma Farm Bureau Mutual Insur-ance Company. He earned a Bachelor of Business Administration in Risk Management and Insurance from the University of Central Oklahoma.

Commissioner Donelon Names Richard Newberry CEO of Louisiana Citizens Property Insurance Corp.

“I’d also like to take the opportunity to thank Vi-jay Ramachandran, who has led Citizens as inter-im CEO since 2015, for his tireless service to Citi-zens Corporation and to the people of Louisiana,” added Commissioner Donelon.

According to Citizens operating policies, Commis-sioner Donelon is responsible for hiring top-level managers at the state-run insurer of last resort. Mr. Newberry’s compensation package will be presented for approval to the Louisiana Citizens Board of Directors at its meeting in July.

Fast Facts about Louisiana Citizens Property In-surance Corporation:

Over the nine rounds of the Depopulation Pro-

gram, Citizens has reduced its overall policy count by nearly 60 percent from an all-time high of 174,000 policies in 2008 to fewer than 70,000 policies today.

Insurance Commissioner Jim Donelon ap-

proved a statewide rate reduction for Citizens personal lines policies effective June 1, 2016. Alt-hough the impact of the filing will vary across

insured lender. Remind clients who do not have mortgages that they should still protect their in-vestment with flood insurance because they are more likely to experience a flood than a fire. Addi-tionally, you can may be able to save your clients money with the Newly Mapped procedure and through a process known as grandfathering provid-ed by the NFIP.

Did you know that more than 20 percent of NFIP claims come from areas outside mapped high-risk areas? If your clients’ flood risk has recently been reduced, they may find themselves no longer re-quired by their lender to maintain their flood insur-ance coverage. It is up to you to ensure that they continue coverage so they are financially protected in the event of a flood. Encourage your clients to take advantage of the lower premiums by offering them a Preferred Risk Policy.

How to Be FloodSmart on Flood Maps

Did you know that new or updated flood maps pro-vide a great opportunity for you to grow your flood business? Participate in open houses or other local events hosted by your local community officials. Position yourself as a knowledgeable, reliable source on the map changes, their impact, and op-tions your clients and prospects might have—both from an insurance and mitigation perspective. En-courage your current and potential clients to attend these events as well to ensure that they under-stand their current flood risk. FloodSmart has de-veloped an entire Flood Map Updates section on Agents.FloodSmart.gov that includes a searchable map update schedule as well as materials and talk-ing points to help you explain these changes to your clients.

Map updates can be confusing, so be a resource to your clients, prospects, and your community as a whole. Be your clients’ advocate by talking with your local floodplain manager to understand the changes in flood risk. You can help your clients make informed decisions on their insurance cover-age. Stay current on program changes by register-ing as a FloodSmart Agent at Agents.FloodSmart.gov and get updates straight in your inbox. For more tips and resources on market-ing and selling flood insurance, visit Agents.FloodSmart.gov.

Louisiana Agent 16

parishes, the overall impact is a -2.4 percent rate re-duction. Citizens attributed the rate cut to added competition in the homeowners market with some major insurers implementing rate decreases, as well as reduced reinsurance costs.

Citizens Board of Directors recently approved a

refinancing plan that will result in approximately $92 million in gross savings and a reduction in the assess-ment rate from 2.92 percent in 2016 to a projected 2.48 percent in 2017.

In June of 2015, Citizens received a two notch up-

grade to its bond rating from Moody’s Investor Ser-

vice. The upgrade from A3 to A1 reflects the state-

owned nonprofit agency’s increased stabilization.

How to Talk to Your Clients about Map Changes

Whether the result of new construction, updated levees, or even a major flooding event, flood risks across the nation are constantly changing. The Fed-eral Emergency Management Agency (FEMA) is working its way across the Nation to update the Flood Insurance Rate Maps (FIRMs) for communities that participate in the National Flood Insurance Pro-gram (NFIP). When new maps show changes in flood risk, flood insurance requirements for property owners can also change. As an agent, you need to understand what those changes can mean for your clients and ensure that they have the necessary flood insurance coverage to protect what matters—their home.

When an area receives new or updated flood maps, some of your clients may find themselves in a high-risk flood area (Zones A or V), while other clients may be in a moderate- to low-risk area (Zones B, C, or X). Will you know what to say when your clients come to you for advice on flood insurance? FloodSmart, the marketing and education campaign of the NFIP, has all the tools you need to prepare for those conversations.

How Map Changes Affect Your Clients

Clients whose properties are located in a high-risk flood

area are required to purchase flood insurance if they have a mortgage through a federally regulated or

Louisiana Agent 17

Several insurance related tax bills passed during the recent Second Special Session of the 2016 Louisiana Legislature. Following is a brief description of each of these bills:

Insurance Premium Tax Credit HB24 by Rep. Andy Anders, D-Vidalia, exempts HMOs from the 5 percent reduction to the insurance pre-mium tax credit that the Legislature passed in Act 10 of the first special session. It expands the defini-tion of "qualified Louisiana investments" for HMOs between January 2017 and January 2019. The legisla-tion is effective upon the governor’s signature. Legislative Process:

The House concurred in Senate amendments by a vote of 81-0

Passed the Senate 31-2 Passed the House 91-10

Insurance Tax Bills Passed In 2nd Special Session

Citizens Property Insurance HB25 by Rep. Rodney Lyons, D-Harvey, reduc-es the amount of the income tax credit for the Louisiana Citizens Property Insurance Cor-poration Assessment from 72 percent to 25 percent. The bill also removes the July 2018 sunset date to make it permanent. Legislative Process:

Passed the Senate 28-9 Passed the House 67-31 Passed the Ways and Means Committee 9-5 Annual Minimum Tax Rate for HMOs HB35 by Rep. Andy Anders, D-Vidalia, repeals the HMO annual license tax. It establishes the annual minimum tax rate for HMOs at $550 for every $10,000 of gross annual premi-ums collected. The legislation is applicable to tax periods beginning Jan. 1, 2016. Legislative Process:

Passed the Senate 35-1 Passed the House 83-13

Louisiana Agent 19

IIABL Director of Education, Mike Edwards is your source for technical questions. Contact

Mike at [email protected] or 678.513.4390

Q. I am trying to figure out the best way to cover a commercial trailer for a business that owns no au-

tos. My insured sells and services a wide variety of outdoor power equipment. I have written all their busi-ness insurance for years. Since they own no autos, we have Hired/Nonowned Auto coverage under the Commercial General Liability (CGL) policy. I stopped by yesterday to pick up a new blade for my riding mower. As I pulled into the parking lot, my heart skipped a beat when I saw a double-axle (5x10) cargo trailer, with a custom paint job featuring the company’s logo. When I asked my insured about the trailer, he explained that they were going to expand their services to include pickup and delivery of equipment needing service or repair, such as riding mowers, portable genera-tors, and any other equipment customers couldn’t bring to the shop themselves. He said he just got the trailer back from the paint shop, and had been meaning to call me about it. So far, none of my auto markets will write a Business Auto Policy (BAP) for just a trailer. However, one of my underwriters commented that if the business owned or leased just one auto, she could write the cover-age for the auto and the trailer. My thought is for my insured to lease his pickup truck to the business, which we could then add to a BAP, along with the trailer. As it turns out, I also write his personal insurance, so we would cancel his Personal Auto Policy (PAP), since he would have coverage under the BAP. What do you think of this arrangement?

A. If you cannot find a market that will write a BAP on just the trailer (“Plan A”), here are some “Plan

B” options, none of which is perfect. Assume your insured is Jack Smith, owner of Smithco Outdoor Power Equipment, Inc., covered by a CGL with a Hired/Nonowned Auto endorsement. Jack owns a Ford F-250, which is covered by a PAP in his per-sonal name. Coverage form excerpts and comments below are based on Insurance Services Office (ISO) forms and endorsements. Proprietary forms may be different. Coverage gaps under the current insurance in place.

Situation #1: Trailer (owned by Smithco) being towed by Jack’s F-250.

Personal Auto Policy

PP 00 01 01 05

Named Insured: Jack Smith

Part A – Liability Coverage

Insuring Agreement B. "Insured" as used in this Part means: 1. You or any "family member" for the ownership, maintenance or use of any auto or "trailer". 2. Any person using "your covered auto".

Subject: BAP vs PAP:

Coverage for a business with an owned trailer but no owned autos.

Continued page 20

parking lot, injuring a customer. No coverage under Smithco’s H/NO endorsement, since the trailer is owned by Smithco. “Plan B” Options. Option #1: Jack leases his Ford F-250 to his company.

Business Auto Coverage Form CA 00 01 1013 Named Insured: Smithco Outdoor Power, Inc. Section II – Covered Autos Liability Coverage 1. Who Is An Insured

The following are "insureds": a. You for any covered "auto". b. Anyone else while using with your per-mission a covered "auto" you own, hire or borrow except:

(1) The owner or anyone else from whom you hire or borrow a covered "auto".

This exception does not apply if the covered "auto" is a "trailer" connect-ed to a covered "auto" you own.

(2) Your "employee" if the covered "auto" is owned by that "employee" or a member of his or her household.

3. For "your covered auto", any person or organization but only with respect to legal responsibility for acts or omissions of a per-son for whom coverage is afforded under this Part. 4. For any auto or "trailer", other than "your covered auto", any other person or organi-zation but only with respect to legal respon-sibility for acts or omissions of you or any "family member" for whom coverage is af-forded under this Part. This Provision (B.4.) applies only if the person or organization does not own or hire the auto or "trailer".

Comments: (1) Jack is an insured under B.1. (2) Smithco is an insured under B.3., but only for their vicarious liability. However, there is no cover-age for Smithco for their sole legal liability, such negligent maintenance of their trailer, etc. (3) If Jack was pulling the trailer with an auto other than his truck (that is, an auto not within the defini-tion of “your covered auto” in his PAP), he is still covered under B.1., but Smithco is not covered un-der B.4. (No coverage for the owner of the trailer). Situation #2: Trailer not attached to an auto. Assume the trailer is in the parking lot of Smithco, not attached to an auto, and it rolls across the

Louisiana Agent 20

Louisiana Agent 21

Continued page 22

Comments: (1) Smithco is covered for the use of Jack’s pickup, under 1.a. above. (2) Jack is not an “insured” for his use of the pickup, under the exception for permissive users in 1.b.(1)(2)., which does not afford coverage to the owner of an auto which Smithco has hired or bor-rowed (“hired” includes leased). (3) Coverage for Jack can be provided with attach-ment of CA 99 47 – Employee As Lessor endorse-ment. However, coverage under this endorsement only applies as follows: “B. While any covered "auto" described in the Schedule is leased to you by one of your "employees", the Who Is An In-sured provision under Covered Autos Liability Cov-erage is changed to include that "employee" as an "insured". (4) Jack has no coverage under the BAP for his use of any other auto not owned, hired, or borrowed by Smithco. For example, he would have no cov-erage under Smithco’s BAP if he borrows a friend’s auto for a non-business errand, or rents an auto on vacation, etc. Such coverage would be availa-ble to Jack if he has a PAP. (5) But if Jack has no autos other than his pickup truck, and does not have coverage under a resi-

dent family member’s PAP, then Jack needs cover-age under either a Named Non-Owner PAP (PP 03 22), or the Drive Other Car (DOC) endorsement CA 99 10, for his use of autos he borrows or rents which are unrelated to Smithco business. (6) If Jack has a Personal Umbrella, some under-writers are reluctant to recognize the CA 99 47 Em-ployee As Lessor endorsement as acceptable under-lying coverage for the F-250. (7) If Jack’s pickup is finance or leased, the finance or leasing company might not be agreeable to Jack’s leasing of the truck to Smithco. Option #2: Smithco sells the trailer to Jack. Comments: (1) Referring to Situation #1 above, Smithco’s only exposure not covered under Jack’s PAP would be their sole negligence as owner of the trailer. By transferring the ownership of the trailer to Jack, Smithco has not only coverage under Jack’s PAP (as discussed above), but also has coverage for their sole negligence under their CGL H/NO endorsement. (2) Jack, however, has acquired additional expo-sures as the owner of the trailer. For example, in Situation #2 above, he is potentially liable for the

Louisiana Agent 23

Continued page 24

trailer at all times, even when not attached to his pickup truck. While his PAP does provide him cov-erage for “any auto or trailer” (see B.1. under “Insureds” in Jack’s PAP above), he now could have claims against him which he probably would not have had before. Option #3: Smithco buys a clunker. Recall the suggestion made by one of your under-writers was that Smithco either buy or lease an au-to, so the trailer could then be added to a BAP. While we’ve seen that Jack’s leasing of his truck to Smithco is a potential can of worms, I think this “clunker idea” has some merit, and certainly with less coverage complications than the leasing ar-rangement. Ironically, the day after I received your question, I was talking to an insurance-nerd colleague who had recently had a similar question. A BBQ restaurant wanted to branch out and do some on-site catering, so they bought a large grill and smoker, and had them attached to a custom commercial trailer. However, they had the same problem as your in-sured: since the business owned no autos, they were unable to procure a BAP. Here is the comment my colleague emailed to me about your situation: Mike-

The gaps you point out are exactly what I reference in class. When I teach the “Insurance & BBQ” class, I have a case where a BBQ joint has no power units but buys a trailer/smoker that they haul all over town…it is licensed. I point out the problem and suggest that the fix (a stand-alone BAP with only a trailer) is next to im-possible to find. I joke and say, “Buy a 1968 Crown Vic for $500 and put it on a BAP.” David. Sometimes, simpler is better! For reference: "Insuring Commercial Trailers Without Owned Au-tos" “The CGL and Trailers” “Personally-Owned Trailer Parked in Company’s Parking Lot” "Personal Vehicle Pulling Business-Owned Trailer" “Pulling a Personally-Owned Trailer with a Compa-ny Truck” "Leasing Your Personal Auto to Your Business" “Leasing a Company Car to Yourself” These materials are intended for educational purposes only and should not be relied upon as legal advice. Please consult a qualified at-torney for legal advice.

Louisiana Agent 24

However, there were some important bills that passed the legislature this year. Following is IIABL’s countdown of the top 10 most important insurance bills passed in the 2016 legislative ses-sion.

Please continue to page 26 for a synopsis of the top 10 insurance bills. You can click on the bill number for detailed information about any of the bills listed.

The 2016 Regular Session of the Louisiana Legis-lature is finally over.

It was a very busy session for insurance issues. IIABL tracked and lobbied 143 insurance related bills.

A significant number of bills were introduced that would have had negative consequences on inde-pendent insurance agents, the Louisiana insur-ance industry and/or our customers. IIABL worked with the rest of the insurance industry to amend or kill those bills, and we are extremely pleased to report that all of those bills were amended or killed.

59 insurance related bills were passed by the Louisiana Legislature. Most of those bills were technical corrections or of modest impact on the daily business of the insurance industry.

Top 10 Insurance Bills of 2016 Session

Continued page 26

Louisiana Agent 26

HB 184 Stokes, Julie(R)

Martiny, Danny(R)

Position: Bill History:

Requires provision of certain claims information to in-

sureds relative to homeowner insurance. HB 184 requires insurance companies to notify policy-

holders if a report of an claim with no payment is going to result in an increase in future premiums.

Support

05-27-16 G Effective

HB 596 Huval, Mike(R) Erdey, Dale(R)

Position:

Bill History:

Provides for notification and effectiveness of a ma-terial change in a contract between a health insur-ance issuer and a producer. HB 596 requires health insurance companies to provide producers with 90-days advance written notice of any changes in the terms of their agency agreement. Support 08-01-16 G Effective

HB 915 Davis, Paula(R)

Johns, Ronnie(R)

Position:

Bill History:

Provides relative to certain exemptions from the continuing education requirements for producers.

HB 932 reestablishes the “grandfather provision”

that exempts insurance producers over 65 years of

age from the requirement for continuing educa-

tion.

Support

05-10-16 G Effective

Continued page 28

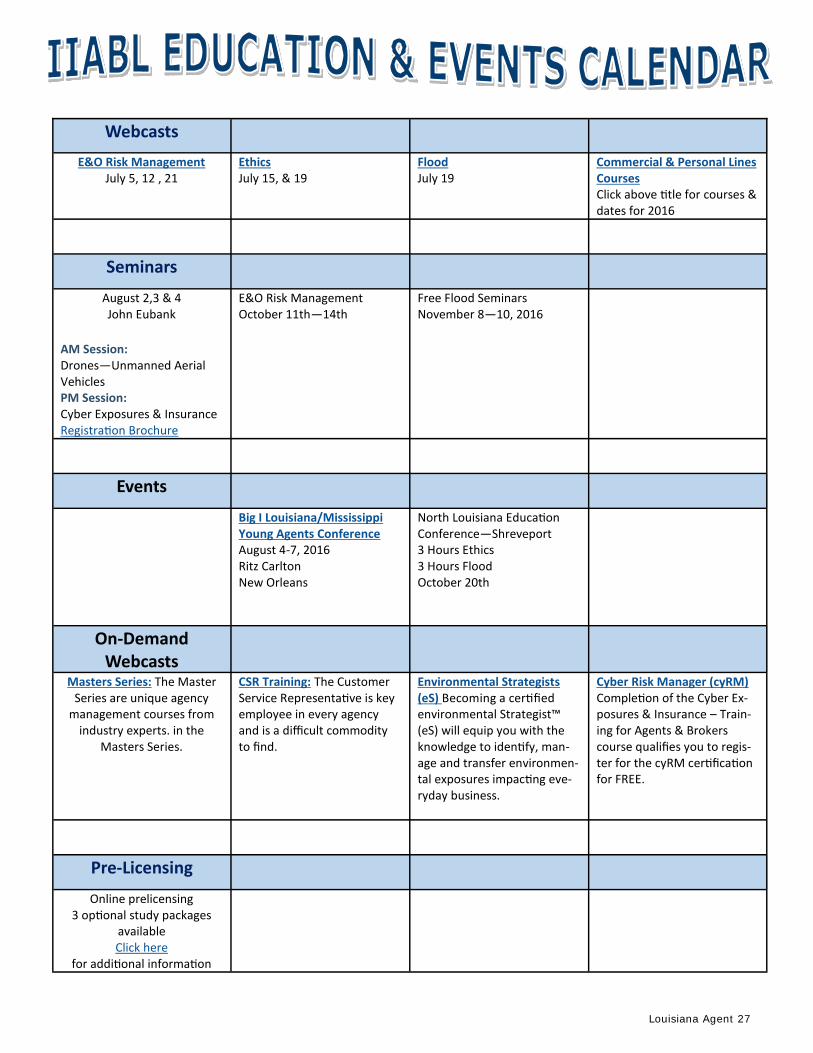

Webcasts

E&O Risk Management July 5, 12 , 21

Ethics July 15, & 19

Flood July 19

Commercial & Personal Lines Courses Click above title for courses & dates for 2016

Seminars

August 2,3 & 4 John Eubank

AM Session: Drones—Unmanned Aerial Vehicles PM Session: Cyber Exposures & Insurance Registration Brochure

E&O Risk Management October 11th—14th

Free Flood Seminars November 8—10, 2016

Events

Big I Louisiana/Mississippi Young Agents Conference August 4-7, 2016 Ritz Carlton New Orleans

North Louisiana Education Conference—Shreveport 3 Hours Ethics 3 Hours Flood October 20th

On-Demand Webcasts

Masters Series: The Master Series are unique agency

management courses from industry experts. in the

Masters Series.

CSR Training: The Customer Service Representative is key employee in every agency and is a difficult commodity to find.

Environmental Strategists (eS) Becoming a certified environmental Strategist™ (eS) will equip you with the knowledge to identify, man- age and transfer environmen-tal exposures impacting eve-ryday business.

Cyber Risk Manager (cyRM) Completion of the Cyber Ex-posures & Insurance – Train- ing for Agents & Brokers course qualifies you to regis-ter for the cyRM certification for FREE.

Pre-Licensing

Online prelicensing 3 optional study packages

available Click here

for additional information

Louisiana Agent 27

Louisiana Agent 28

Continued page 29

HB 932 Davis, Paula(R) Johns, Ronnie(R)

Position: Bill History:

Provides relative to certain exemptions from the continu-ing education requirements for producers. HB 932 reestablishes the “grandfather provision” that ex-empts insurance producers over 65 years of age from the requirement for continuing education. Support 05-10-16 G Effective

SB 95 Ward(R) Brown, Chad(D)

Position: Bill History:

Provides relative to evidence of compulsory motor vehicle insurance. SB 95 is the first state law in the country to allow a mo-torist to provide proof of compulsory automobile insur-ance by electronic means at the time law enforcement requests proof of coverage. This means that policyhold-ers may provide proof of coverage through traditional in-surance cards, a digital image of insurance cards, or via a text or email copy of proof of insurance sent to the policy-holder. Support 08-01-16 G Effective

HB 1165 Huval, Mike(R) Erdey, Dale(R)

Position:

Bill History:

Exempts mobile construction equipment from compulsory motor vehicle security requirements. HB 1165 clarifies that mobile equipment is not subject to the statutory au-tomobile financial responsibility requirements. Support 08-01-16 G Effective

Louisiana Agent 29

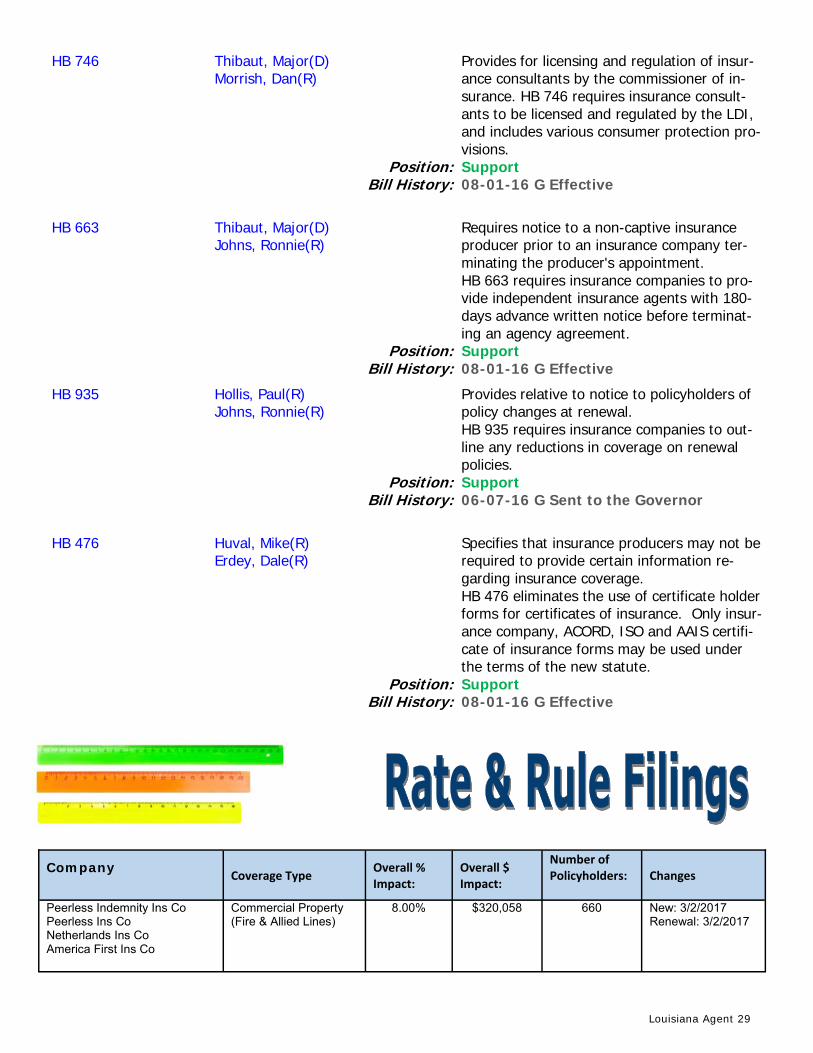

Company

Coverage Type Overall % Impact:

Overall $ Impact:

Number of Policyholders:

Changes

Peerless Indemnity Ins Co Peerless Ins Co Netherlands Ins Co America First Ins Co

Commercial Property (Fire & Allied Lines)

8.00% $320,058 660 New: 3/2/2017 Renewal: 3/2/2017

HB 746 Thibaut, Major(D) Morrish, Dan(R)

Position: Bill History:

Provides for licensing and regulation of insur-ance consultants by the commissioner of in-surance. HB 746 requires insurance consult-ants to be licensed and regulated by the LDI, and includes various consumer protection pro-visions. Support 08-01-16 G Effective

HB 663 Thibaut, Major(D) Johns, Ronnie(R)

Position: Bill History:

Requires notice to a non-captive insurance producer prior to an insurance company ter-minating the producer's appointment. HB 663 requires insurance companies to pro-vide independent insurance agents with 180-days advance written notice before terminat-ing an agency agreement. Support 08-01-16 G Effective

HB 935 Hollis, Paul(R) Johns, Ronnie(R)

Position:

Bill History:

Provides relative to notice to policyholders of policy changes at renewal. HB 935 requires insurance companies to out-line any reductions in coverage on renewal policies. Support 06-07-16 G Sent to the Governor

HB 476

Huval, Mike(R) Erdey, Dale(R)

Position: Bill History:

Specifies that insurance producers may not be required to provide certain information re-garding insurance coverage. HB 476 eliminates the use of certificate holder forms for certificates of insurance. Only insur-ance company, ACORD, ISO and AAIS certifi-cate of insurance forms may be used under the terms of the new statute. Support 08-01-16 G Effective

Louisiana Agent 30

Auto Insurance Affordability Problems

Linked to Underlying Cost Drivers

MALVERN, Pa.—Medical utilization rates exceeding national norms are a major contributor to high claim costs in eight of the 12 least affordable auto insurance systems, according to a new report from the Insurance Research Council (IRC). In these eight states (Delaware, Florida, Kentucky, Michigan, Nevada, New Jersey, New York, and West Virginia), the percentage of auto injury insurance claimants who received diag-nostic services, such as magnetic resonance imaging (MRI) and computed tomography (CT) scans, or were treated by specific types of providers, such as chiro-practors and physical therapists, was higher than the countrywide average. In many cases, utilization rates were much higher than countrywide averages. Higher medical utilization rates lead to higher injury claim costs, which contribute to higher insurance coverage costs. Other significant cost drivers in the systems ex-amined included high injury claim frequency rates, ex-tensive attorney involvement and high rates of claim abuse.

Several of the cost drivers discussed in the report often accompany each other in the states where they are identified. For example, half of the states with high medical utilization rates also experience above-average rates of attorney involvement. Every state, however, was found to face its own unique mix of cost-drivers. For example, only two of the states examined (Florida and Louisiana) were found to have bad-faith litigation environments contributing to high costs and affordabil-ity problems.

“Utilization of medical services inconsistent with evi-dence-based standards and national norms has been a well-known problem in the general health care system. The findings presented in this report suggest that simi-lar utilization patterns plague auto injury compensation systems in several states,” said Beth Sprinkel, senior vice president of the IRC. “Without effective action to address medical utilization issues in auto injury claims, high claim costs will continue to fuel affordability con-cerns.”

The IRC study, Affordability in Auto Injury Insurance: Cost Drivers in Twelve Jurisdictions, relied on data

from the IRC’s auto injury closed claim database and the Fast Track Monitoring System to meas-ure and compare injury claim outcomes and sys-tem performance in states where the cost of auto insurance, on average, is highest when compared with median household income. In these 12 juris-dictions, the cost of auto insurance is considered least affordable among all the states. However, in three of the states examined, below-average household income is a significant reason why au-to insurance costs are less affordable than in oth-er states.

For more detailed information on the study’s methodology and findings, contact David Corum at [email protected] or by phone at (484) 831-9046. For more information about how to purchase the report, visit the IRC’s website at www.insurance-research.org.

Louisiana Agent 31

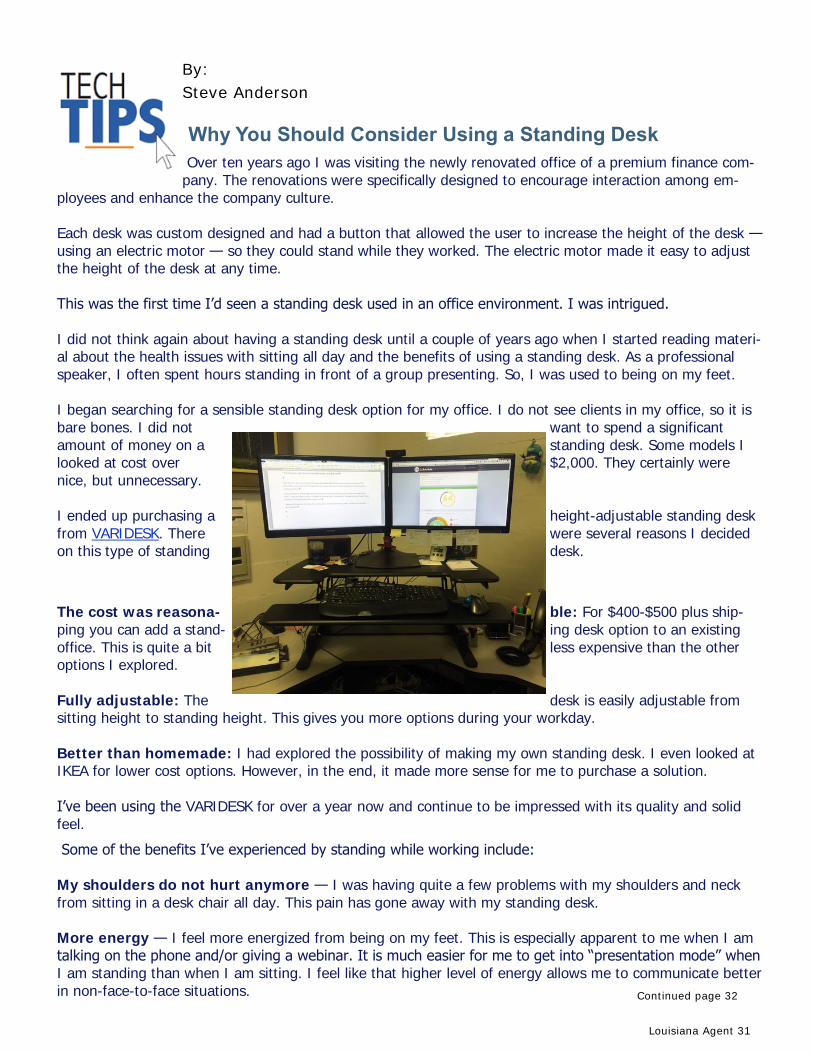

By:

Steve Anderson

Why You Should Consider Using a Standing Desk

Over ten years ago I was visiting the newly renovated office of a premium finance com-pany. The renovations were specifically designed to encourage interaction among em-

ployees and enhance the company culture. Each desk was custom designed and had a button that allowed the user to increase the height of the desk — using an electric motor — so they could stand while they worked. The electric motor made it easy to adjust the height of the desk at any time. This was the first time I’d seen a standing desk used in an office environment. I was intrigued. I did not think again about having a standing desk until a couple of years ago when I started reading materi-al about the health issues with sitting all day and the benefits of using a standing desk. As a professional speaker, I often spent hours standing in front of a group presenting. So, I was used to being on my feet. I began searching for a sensible standing desk option for my office. I do not see clients in my office, so it is bare bones. I did not want to spend a significant amount of money on a standing desk. Some models I looked at cost over $2,000. They certainly were nice, but unnecessary. I ended up purchasing a height-adjustable standing desk from VARIDESK. There were several reasons I decided on this type of standing desk.

The cost was reasona- ble: For $400-$500 plus ship-ping you can add a stand- ing desk option to an existing office. This is quite a bit less expensive than the other options I explored. Fully adjustable: The desk is easily adjustable from sitting height to standing height. This gives you more options during your workday. Better than homemade: I had explored the possibility of making my own standing desk. I even looked at IKEA for lower cost options. However, in the end, it made more sense for me to purchase a solution. I’ve been using the VARIDESK for over a year now and continue to be impressed with its quality and solid feel.

Some of the benefits I’ve experienced by standing while working include: My shoulders do not hurt anymore — I was having quite a few problems with my shoulders and neck from sitting in a desk chair all day. This pain has gone away with my standing desk. More energy — I feel more energized from being on my feet. This is especially apparent to me when I am talking on the phone and/or giving a webinar. It is much easier for me to get into “presentation mode” when I am standing than when I am sitting. I feel like that higher level of energy allows me to communicate better in non-face-to-face situations. Continued page 32

Louisiana Agent 32

More focus — I tend to think and concentrate better when I can move. I am standing and pacing while writing this article and using Dragon NaturallySpeaking voice recognition software to "type" the content. If you go online and search for “benefits of standing desk” you will see some articles talking about the ben-efits and the negatives of using a standing desk. I do believe there are health benefits to using a standing desk, but like anything, it can be overdone. I do recommend you explore the option of adding a standing desk to your office or workstation. For me, VARIDESK has been a great choice, and I recommend it. If you want to explore the do-it-yourself route, Bob Vila has an article on standing desk projects that you may find helpful. Do you use a standing desk? If not, why not? If yes, what have been the benefits you have experienced? Let me know.

Don’t miss out

on the fun!!

SAVE THE DATE

115th IIABL Annual

Convention & Exposition

June 18-21, 2017

GOLD LEVEL

BRONZE LEVEL

SILVER LEVEL

AMERISAFE AMERICAS INSURANCE AMTRUST GROUP

ASI

BANKERS INSURANCE

CNA INSURANCE

EMC INSURANCE FOREST INSURANCE GULFSTREAM P&C

HOMEBUILDERS SIF LANE & ASSOCIATES

LUBA WORKERS’ COMP

MAISON INSURANCE MARKEL FIRST COMP RPS COVINGTON

SUMMIT CONSULTING

Louisiana Agent 34

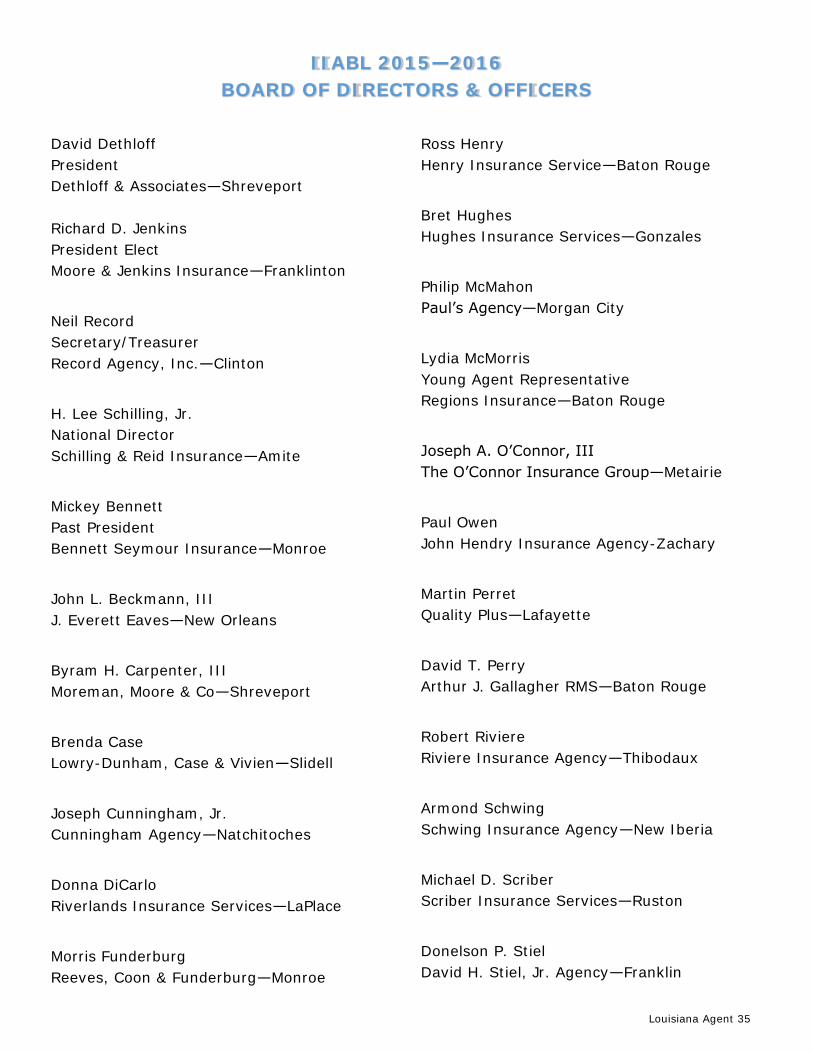

IIABL 2015—2016

BOARD OF DIRECTORS & OFFICERS

David Dethloff

President

Dethloff & Associates—Shreveport

Richard D. Jenkins

President Elect

Moore & Jenkins Insurance—Franklinton

Neil Record

Secretary/Treasurer

Record Agency, Inc.—Clinton

H. Lee Schilling, Jr.

National Director

Schilling & Reid Insurance—Amite

Mickey Bennett

Past President

Bennett Seymour Insurance—Monroe

John L. Beckmann, III

J. Everett Eaves—New Orleans

Byram H. Carpenter, III

Moreman, Moore & Co—Shreveport

Brenda Case

Lowry-Dunham, Case & Vivien—Slidell

Joseph Cunningham, Jr.

Cunningham Agency—Natchitoches

Donna DiCarlo

Riverlands Insurance Services—LaPlace

Morris Funderburg

Reeves, Coon & Funderburg—Monroe

Ross Henry

Henry Insurance Service—Baton Rouge

Bret Hughes

Hughes Insurance Services—Gonzales

Philip McMahon

Paul’s Agency—Morgan City

Lydia McMorris

Young Agent Representative

Regions Insurance—Baton Rouge

Joseph A. O’Connor, III

The O’Connor Insurance Group—Metairie

Paul Owen

John Hendry Insurance Agency-Zachary

Martin Perret

Quality Plus—Lafayette

David T. Perry

Arthur J. Gallagher RMS—Baton Rouge

Robert Riviere

Riviere Insurance Agency—Thibodaux

Armond Schwing

Schwing Insurance Agency—New Iberia

Michael D. Scriber

Scriber Insurance Services—Ruston

Donelson P. Stiel

David H. Stiel, Jr. Agency—Franklin

Louisiana Agent 35