Embed Size (px)

Citation preview

Tools for Business Decision-MakingFourth Canadian

Edition

Financial Financial Accounting:Accounting:

Prepared by: Peggy Coady

Memorial University of Newfoundland

&Catherine Seguin

University of Toronto

Reporting and Analyzing Reporting and Analyzing InvestmentsInvestments

Chapter 12

InvestmentsInvestments

• Investments include:– Debt securities (certificates of

deposit, treasury bills, commercial paper, government and corporate bonds)

– Equity securities (preferred and common shares)

Chapter 12 3

Classifying InvestmentsClassifying Investments

• Can be passive investments (to generate investment income) or strategic investments (to influence/control operations of another company)

Chapter 12 4

Passive InvestmentsPassive Investments

• Passive investments can be debt or equity securities– Held-for-trading (debt or equity)– Available-for-sale (debt or equity)– Held-to-maturity (debt)

Chapter 12 5

Held-For-Trading Held-For-Trading SecuritiesSecurities

• Held-for-trading securities are debt or equity securities

• Typically, they are actively traded with the objective of making a profit from changes in short-term market values

• Classified as short-term

Chapter 12 6

Available-for-Sale Available-for-Sale SecuritiesSecurities

• Available-for-sale securities are debt or equity securities that are held with the intention of selling them sometime in the future

• Classified as short- or long-term

Chapter 12 7

Chapter 12 8

Held-To-Maturity Held-To-Maturity Securities Securities

• Held-to-maturity securities are debt securities that the investor has the intention and ability to hold until maturity

• Classified as long-term (except within one year of maturity)

Accounting for Passive Accounting for Passive InvestmentsInvestments

• Recorded at purchase cost at acquisition

• After acquisition– Held-for-trading and available-for-

sale securities are valued at fair value

– Held-to-maturity securities are valued at (amortized) cost

Chapter 12 9

Fair ValueFair Value─HFT and AFS─HFT and AFS

• When investments are valued at their fair value, any increase or decrease in their market price changes the asset value

• Difference between fair value and cost (or carrying amount) while an investment is held is called an unrealized gain or loss

Chapter 12 10

Fair ValueFair Value ─HFT and AFS ─HFT and AFS

• Held-for-trading– Unrealized gain or loss reported

as other revenue/expense on statement of earnings

• Available-for-sale– Unrealized gain or loss reported

as Other Comprehensive Income (OCI) on statement of comprehensive income

Chapter 12 11

Cost─HTMCost─HTM

• Valued at amortized cost

• Fair value exception for impairment loss– If fair value falls below cost and

the decline is considered permanent, then the held-to-maturity security is adjusted to its fair value

Chapter 12 12

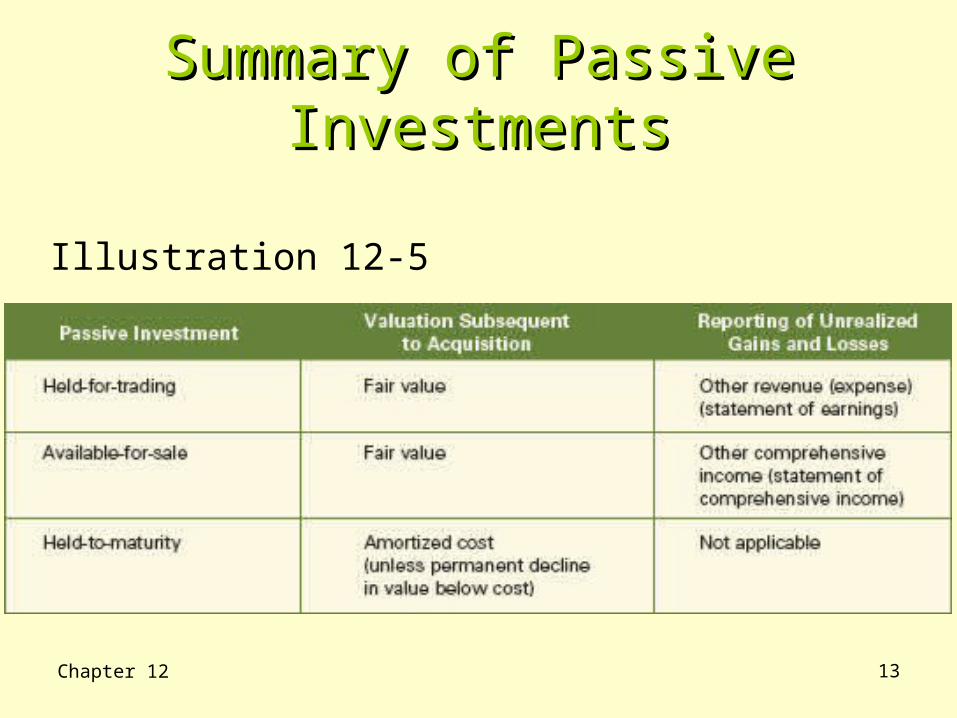

Summary of Passive Summary of Passive InvestmentsInvestments

Chapter 12 13

Illustration 12-5

Accounting for Passive Accounting for Passive InvestmentsInvestments

• Sale of investment– Compare proceeds to cost when

sold and record realized gain or loss

– Reversal of OCI for available-for-sale securities required

Chapter 12 14

Discussion QuestionDiscussion Question

What is the difference between unrealized gains and losses and realized gains and losses?

Chapter 12 15

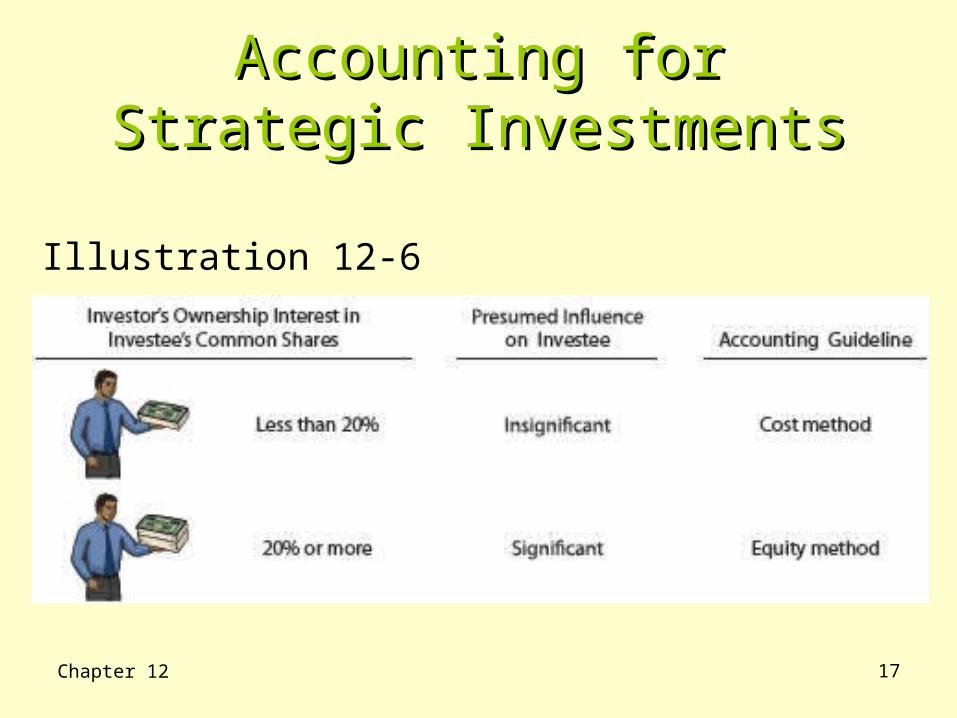

Accounting forAccounting forStrategic InvestmentsStrategic Investments

• Only equity securities can be strategic investments

• Accounting for investments in common shares is based on the extent of the investor's degree of influence over the issuing corporation (the investee)

Chapter 12 16

Accounting forAccounting forStrategic InvestmentsStrategic Investments

Chapter 12 17

Illustration 12-6

Cost MethodCost Method(Less than 20%)(Less than 20%)

• Record investment at the cost paid to acquire the investment

• Recognize revenue when cash dividends are declared

Chapter 12 18

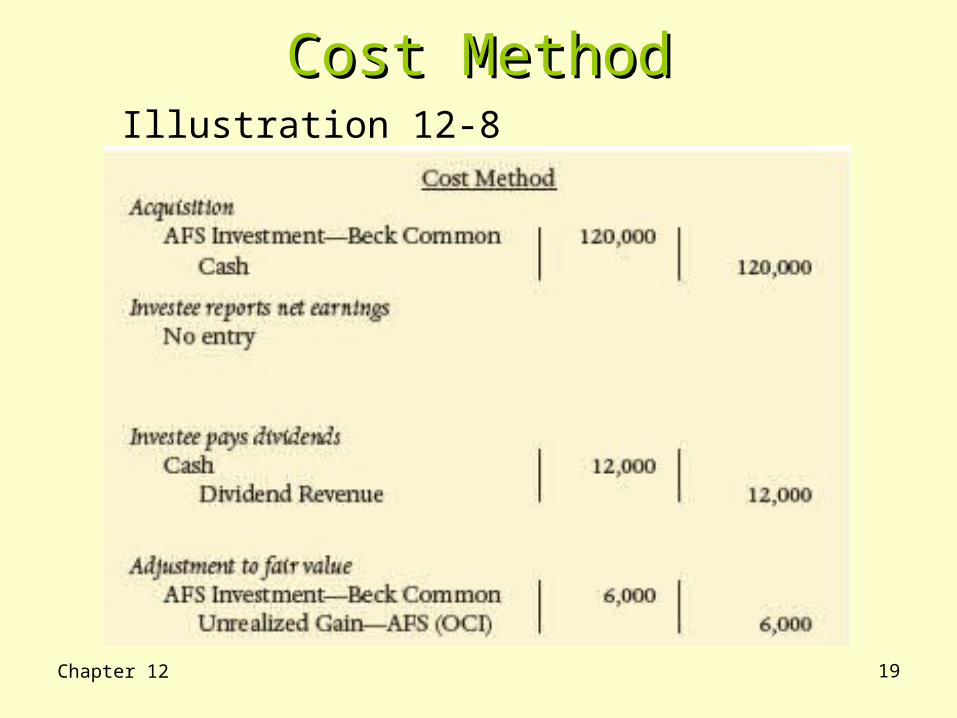

Cost MethodCost Method

Chapter 12 19

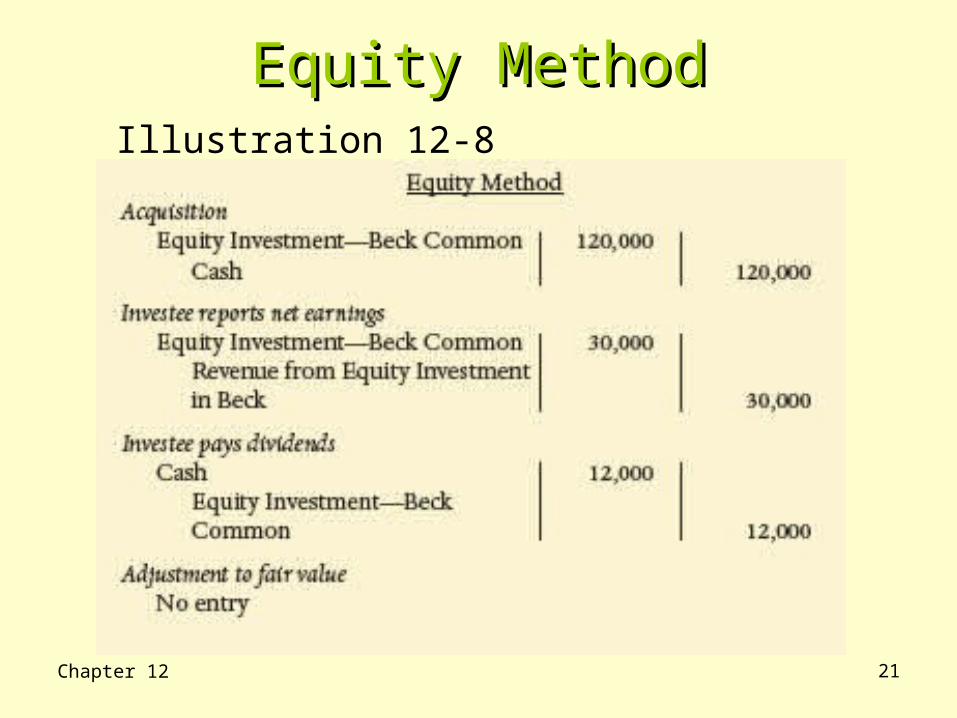

Illustration 12-8

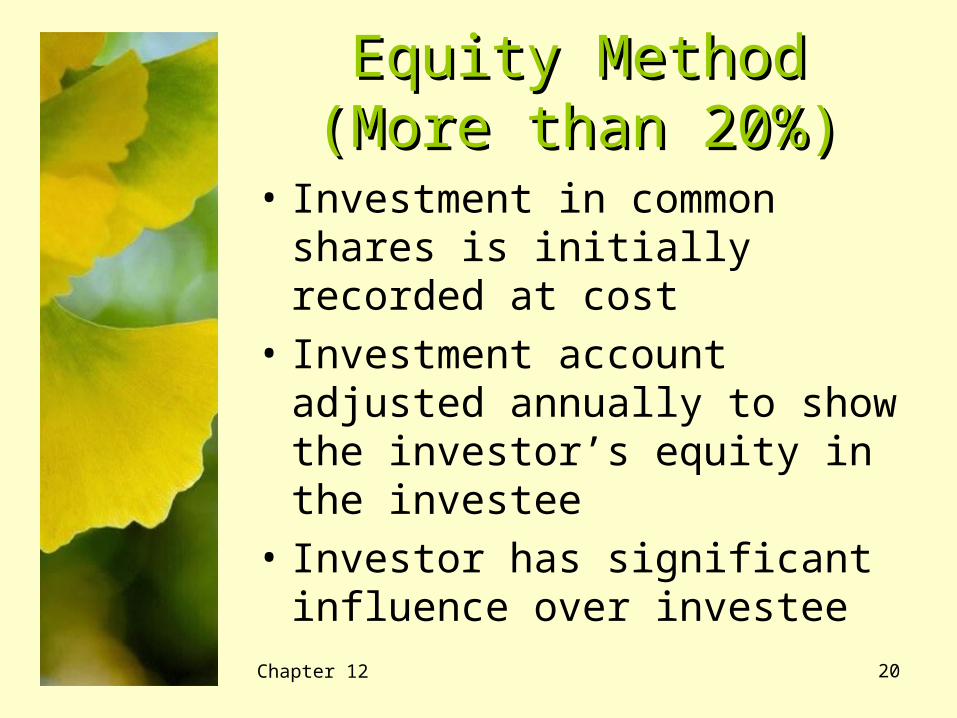

Equity MethodEquity Method(More than 20%)(More than 20%)

• Investment in common shares is initially recorded at cost

• Investment account adjusted annually to show the investor’s equity in the investee

• Investor has significant influence over investee

Chapter 12 20

Equity MethodEquity Method

Chapter 12 21

Illustration 12-8

Discussion QuestionDiscussion Question

When are equity investments written down?

Chapter 12 22

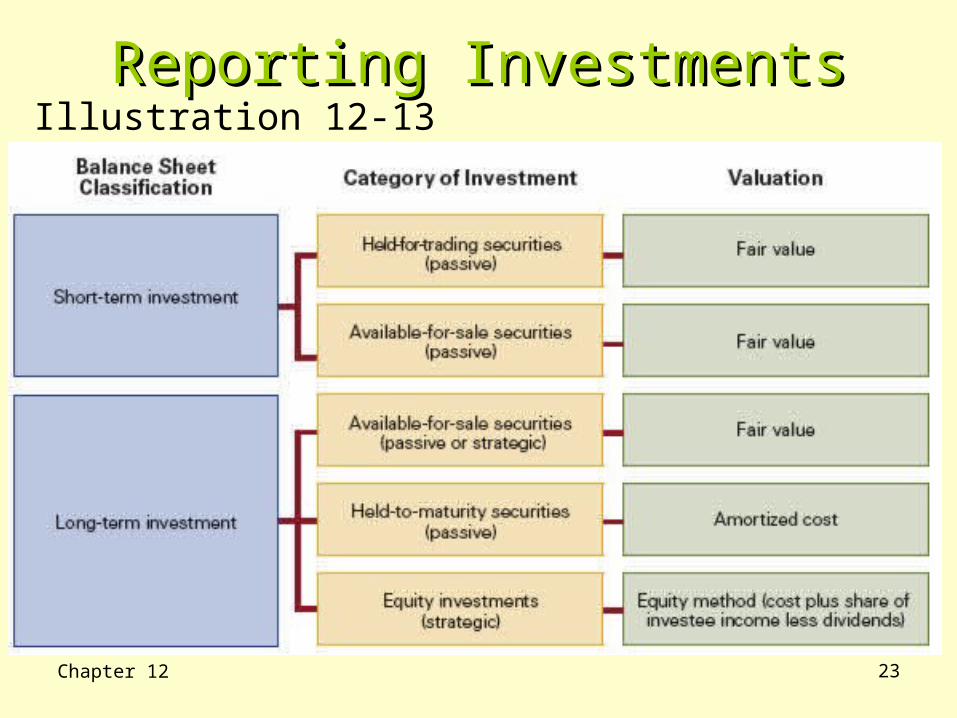

Reporting InvestmentsReporting Investments

Chapter 12 23

Illustration 12-13

Consolidated Consolidated Financial StatementsFinancial Statements

• When a company owns more than 50% or controls the common shares of another company a consolidated set of financial statements must be prepared

• Informs creditors, investors, and others of the magnitude and scope of operations of companies under common control

Chapter 12 24

Chapter 12 25

ConsolidatedConsolidatedFinancial StatementsFinancial Statements

• Present assets and liabilities controlled by parent and the aggregate profitability of subsidiary companies

• Prepared in addition to financial statements for individual parent and subsidiary companies

Appendix 12AAppendix 12AInvestment in BondsInvestment in Bonds

• The recording of bonds as an investment is similar to recording a bond liability

• Investor (purchaser of bonds)

• Investee (issuer of bonds)

Chapter 12 26

Appendix 12AAppendix 12AInvestment in BondsInvestment in Bonds

• In accounting for bond investments, entries are required to record:– Acquisition (at purchase cost net

premium/discount) – Investment revenue– Sale

Chapter 12 27

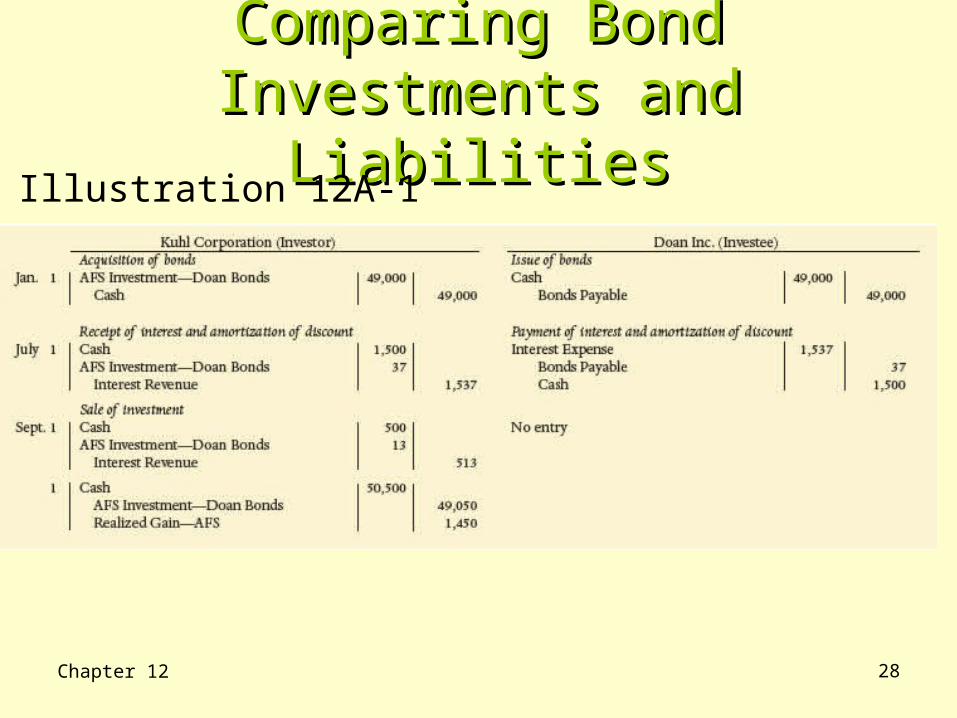

Comparing Bond Investments Comparing Bond Investments and Liabilitiesand Liabilities

Chapter 12 28

Illustration 12A-1

Copyright Notice

Copyright © 2009 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by Access Copyright (The Canadian Copyright Licensing Agency) is unlawful. Requests for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his or her own use only and not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages caused by the use of these programs or from the use of the information contained herein.