Embed Size (px)

Citation preview

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 1 of 76

1

2

3

4

5

6

7

8

9

Version 2015-1 10

11

Exam Cram Instructions 12

13

You should watch all the Exam Cram Videos one time before reading 14

this outline. 15

Then read this Cram outline from beginning to end. 16

Then repeat the Day Before the Test Videos and the Test Taking Tips 17

Video. 18

Then reread this Cram outline from beginning to end. 19

The day before your state exam repeat the Day Before the Test Videos 20

and the Test Taking Tips Video and read the highlights from this Cram 21

outline. 22

If you have additional time available to study for the state exam then 23

repeat the Day Before the Test Videos and the Test Taking Tips Video 24

and read the highlights from this Cram outline. 25

26

27

Test Taking Tips 28

29

30

The state exam is a challenging test. Do not expect an easy test. Some questions will be easy. 31

Some questions will be tricky. While you are taking the test do not think about whether it is 32

difficult or easy. Instead, focus on each question. 33

34

Read the test. Really read it. Do not skim. Also, read all the answer choices. Some questions 35

have a pretty good answer in a prior answer choice, but a better answer in a later answer 36

choice. Always pick the best answer. 37

Tony Mesa Real

Estate School Inc.

1601 N. Palm Ave, Ste 114,

Pembroke Pines,

FL Florida 33026

(954) 590-0417

www.tonymesarealestateschool.com

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 2 of 76

Example: 1

A. Pretty good answer. 2

B. 3

C. 4

D. Better answer (Pick D because this is the best choice). 5

6

Do not add information into the questions. Do not assume information. Answer the question 7

based on only what is written. 8

9

Use the time allowed. You will have 3 ½ hours. Take a bathroom break(s) if you are losing 10

concentration or need to rest. Some students take as many as 4 breaks during the test. 11

12

Skip questions you are not sure about. Many students skip 10 to 25 questions. You will go back 13

to these once you finish going through the test the first time. The computer allows you to return 14

to the skipped questions. By doing this you will be able to concentrate better throughout the 15

exam because you are not getting bogged down by the difficult questions. Also, sometimes-16

skipped questions are answered by other test questions. 17

18

Do not second guess yourself and change a bunch of answers. Only change an answer if you are 19

100% sure you have made a mistake. 20

21

Use the answer choices. Use process of elimination. Use your knowledge to eliminate answer 22

choices that are incorrect. 23

24

Except Questions or Which is not true Questions 25

Ask yourself: “Are they asking me for what is true or what is false.” Mark each answer choice 26

true, false or question mark to clarify. If 3 answer choices are true and one answer choice is 27

false, then the question is asking for what is false. 28

Example: 29

A. T 30

B. T 31

C. F 32

D. T 33

34

Do not take it easy on the licensee. Do not go out of your way to get licensees out of trouble. The 35

exam is designed to teach you that if licensees do something wrong they will face penalties. 36

37

3 Answer Choices Similar and 1 Answer Choice Different Questions 38

Pick the different answer choice. 39

Example: 40

A. This is legal. 41

B. This is allowed by law. 42

C. This is illegal. 43

D. This is legal behavior. 44

45

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 3 of 76

3 Short Answer Choices and 1 Long Answer Choice Questions 1

If not sure pick the long answer choice. 2

3

Answer Choices with “and” 4

Both sides must be correct to have a correct answer choice. If one side is wrong then eliminate 5

the answer choice. 6

Example: An appraisal is an estimate of value and the appraiser determines the value. 7

An appraisal is an estimate of value is true. The appraiser determines the value is false. 8

Therefore, the entire answer choice is false. 9

10

Long Questions 11

Read the last sentence of the question. The last sentence usually tells you what the question is 12

about. 13

14

Look for key word in question or answer choice. If you say to yourself this is how they are 15

trying to “trick” me, then you will probably pick the correct answer choice. 16

17

In the end if you are not sure guess C. Do not leave unanswered questions. 18

19

You may have 103 questions. If you have 103 questions then 3 questions will not count towards 20

your score but these 3 are not the last 3 questions. You will not know which 3 questions do not 21

count. 22

23

CHAPTER 1 REAL ESTATE BUSINESS 24

25

Real Estate Business 26

The real estate business or industry consists of various areas of specialization including 27

brokerage, development and construction, investment, operations and government services. 28

29

Real Estate Brokerage 30

Brokerage involves real property transactions (sales or leasing) in which licensed real estate 31

professionals provide assistance to others in exchange for compensation. 32

Real estate brokers provide real estate services for others. Sales associates and broker 33

associates work under the supervision of brokers or owner developers or the government and 34

provide real estate services for others. 35

The term real estate licensee is a term which refers to a person with any of the real estate 36

licenses and may be a broker or a sales associate or a broker-associate. 37

The majority of licensees are involved in brokerage. 38

The licensee has expertise in 3 areas: 39

1. Details of property transfer. 40

2. Knowledge of market conditions. 41

3. Knowledge of how to market real estate or businesses (includes knowledge of finding 42

prospects). 43

Property that is sold by a licensee is normally sold faster and with less price reduction than 44

property sold by owner without involvement of a licensee (For Sale by Owner = FSBO). 45

Real estate brokerage may be divided into two areas: 46

Sales brokerage (seller = vendor, buyer = vendee). 47

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 4 of 76

Leasing brokerage (landlord = lessor, tenant = lessee). 1

2

When a word ends with “or” then giving and when a word ends with “ee” then receiving. For 3

example, a landlord gives a lease to tenant and a tenant receives a lease from the landlord. The 4

landlord is also called the lessor and the tenant is also called the lessee. Landlord and lessor are 5

synonymous. Tenant and lessee are synonymous. Two terms are synonymous if they mean the 6

same thing. 7

8

Five major sales brokerage specialties: 9

1. Residential (for example, houses, condominiums). 10

Advising buyers regarding financing is important because many homebuyers are not 11

familiar with the mortgage loan process. However, must have mortgage loan originator’s 12

license to arrange financing. 13

2. Commercial (for example, office buildings, strip centers). 14

Must be able to analyze income-producing properties. 15

3. Industrial (for example, manufacturing facilities, warehouses). 16

Must have technical knowledge of the requirements of different industries. For example, 17

energy requirements, transportation requirements, floor load-bearing capacity 18

requirements, etc. 19

4. Agricultural (farms and farm land). 20

Must understand farm operations and federal programs affecting farms. 21

5. Businesses. 22

When acting as a business broker a licensee is assisting in the purchase and sale of an 23

existing business. 24

Business opportunities are smaller businesses. For example, a neighborhood beauty salon or 25

pizzeria. 26

Business enterprises are larger businesses. For example, Ford Motor Company or Apple 27

Computer. 28

Memory Aid: Star Trek Starship Enterprise very big (enterprise = big). 29

In addition to understanding real property, a business broker must be able to understand 30

and value personal property and goodwill. 31

Goodwill is the name recognition and expected continued customer loyalty. Goodwill is an 32

intangible asset. An intangible asset is an asset that is not physical and cannot be touched. 33

Must have an active real estate license to engage in business brokerage (because an interest 34

in real property (title or lease) is usually transferred along with the sale of a business. 35

Farm Area 36

The geographic area and/or property type a licensee specializes in and becomes expert in and 37

markets to. 38

39

Follow-Up 40

Anything a licensee does after the sale (example: visit after closing, send cards during holidays, 41

provide information regarding March 1st homestead tax exemption application deadline, etc.). 42

It is very important that licensees do proper follow-up. 43

Follow-up is especially important in Florida because people move frequently. Proper follow up 44

will lead to repeat customers and referrals. 45

46

Property Management 47

Leasing, managing, marketing and maintenance of property for another. 48

Property manager’s primary goals are to protect an owner’s investment and to produce highest 49

net income over longest possible period of time. 50

Highest net income today and highest net income over the long run are at odds. 51

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 5 of 76

Achieve highest net income today by reducing spending, but this eventually leads to 1

deterioration of property, reduced rents and higher vacancy and collection losses. 2

Property manager’s functions: 3

Leasing, rent collection, maintenance, repair, tenant relations, advertising and 4

merchandising the space. 5

Services to be provided by property manager and compensation to property manager are 6

detailed in property management agreement between owner and property manager. 7

Reasons for growth of property management: 8

More complex properties. 9

Expertise required to manage properties and many investors (for example, doctors) are not 10

real property experts. 11

Time-consuming to manage properties. 12

Absentee ownership: owners do not personally manage or reside on the property. 13

Absentee ownership is the principal reason for growth of property management. 14

Compensation: Negotiated between owner and property manager but usually base amount plus 15

percentage of effective gross income or a percentage of effective gross income. 16

17

Appraising 18

Appraisal: Process of estimating (not determining) the value of real property. 19

Appraisal is an art, not a science (an appraiser uses mathematical calculations, but an appraiser 20

also uses judgment). 21

An appraisal must be defensible. 22

An appraiser performing an appraisal must conform to the Uniform Standards of Professional 23

Appraisal Practice (USPAP). Note: know exactly what USPAP stands for. 24

Appraiser paid a fee based on time and difficulty of appraisal, not a commission. A commission 25

would result in a conflict of interest. 26

The most common reason an appraisal is completed is that a lender requires an appraisal to 27

provide financing but appraisals are completed other reasons. For example, appraisals ordered 28

by government in eminent domain takings of properties during condemnation proceedings. 29

The Florida Real Estate Commission (FREC) regulates real estate licensees. FREC does not 30

regulate appraisers. The Florida Real Estate Appraisal Board (FREAB) regulates state-31

certified, licensed and registered trainee appraisers. 32

Licensees may perform an appraisal pursuant to 475 F.S. (are legally allowed to do so and may 33

be compensated for the appraisal): 34

A real estate licensee that is not also an appraiser may not refer to him or herself as an 35

appraiser. 36

A real estate licensee performing an appraisal must conform to the Uniform Standards of 37

Professional Appraisal Practice (USPAP). 38

If the real estate transaction is a federally related transaction then the appraisal must be 39

done by a state-certified or licensed appraiser (not a licensee). In reality, appraisals are 40

almost always performed by appraisers (and not by licensees). 41

Licensees more commonly perform a comparative market analysis (CMA). 42

A CMA is not required to conform to USPAP. 43

Usually performed for free to acquire a listing; however, may be compensated for a CMA. 44

May not refer to a CMA as an “appraisal.” 45

A Broker Price Opinion (BPO) is an estimate of value usually provided to a lender. 46

A BPO is not required to conform to USPAP. 47

A fee is usually charged for a BPO. 48

May not refer to a BPO as an “appraisal.” 49

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 6 of 76

If a sales associate or broker associate is performing a CMA or BPO and there is compensation 1

then compensation must be paid to the brokerage/broker and then brokerage/broker pays the 2

compensation to the sales associate or broker associate. 3

4

Financing 5

Most purchases involve financing. 6

It is important to understand how to help and advise buyers with financing. 7

However, must have mortgage loan originator’s license to arrange financing. 8

Must have a mortgage loan originator’s license to receive any compensation from a lender 9

for a loan. 10

11

Counseling 12

A counselor is paid to analyze problems and recommend solutions. 13

Usually complex problems. Therefore, counselor must have high degree of knowledge. 14

15

Development and construction 16

3 Phases: 17

1. Land acquisition: 18

Sometimes land is purchased using a purchase and sale contract but often option contracts 19

or contracts for deed are used to acquire rights to land. 20

Must study zoning and land-use plans to determine if can build desired improvements. 21

An improvement is the most general term for anything constructed on land by humans. For 22

example, an apartment building, house, mall, shed, etc. 23

2. Subdividing and development: 24

Subdividing = dividing land into smaller parcels. 25

Development = improving raw land. 26

Development includes clearing trees, excavating for roads and utilities, grading, street 27

paving, building curbs, storm drains, water systems and sewer systems. 28

Subdivision plat map (= plat map = plat): Map of subdivision that shows size and location of 29

individual lots, streets and public utilities. 30

The subdivision plat map must be approved by the government and it will be recorded 31

in the public records. 32

Dedication is a gift of land from an owner (= developer = private party) to the government 33

for public use (examples: street, park). 34

Concurrency of infrastructure and subdividing means that the local government will 35

require that infrastructure be in place as building of improvements proceeds. For example, 36

must put in sewer lines while building houses. If government tells a builder to stop building 37

this is called a moratorium. 38

Deed restrictions: Recorded in public records to achieve conformity and maintain values 39

(example: establishing minimum square footage of house that may be built). 40

A deed restriction affects one property and a subdivision restrictive covenant affects all 41

properties in a subdivision. 42

If all property owners cannot block view of lake because each deed includes this restriction 43

then these are deed restrictions. 44

3. Construction: 45

Construct improvements on the site. 46

3 categories of residential construction: 47

1. Spec homes: 48

Spec = on speculation. On speculation because construct before have buyers. The 49

builder is speculating that will find buyers. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 7 of 76

Spec building is on a smaller scale. For example, if buy three lots and will build 1

three houses. 2

2. Tract homes: 3

Also on speculation (build before have buyers), but on larger scale than spec homes. 4

For example, if building 200 houses. 5

Usually project includes model homes, internal sales force and possibly cooperation 6

with licensees. 7

3. Custom homes: 8

Construct for existing owner. 9

Not on speculation (already have the owner). 10

11

Each level of government has effects on real estate business: 12

Local government: 13

Property taxes: Property taxes paid to county, city and school board. 14

Occupational licenses. 15

Building permits. 16

Building moratoriums. A moratorium is when the government orders a builder to stop 17

building. For example, the government may impose a moratorium until more 18

infrastructure is completed. 19

Zoning. 20

The local government establishes the zoning code. 21

State government: 22

Owns and manages a large amount of property. 23

Identifies areas to be protected from development (examples: coastal areas, the everglades). 24

State documentary taxes on deed and/or intangible tax on the mortgage and/or note stamp 25

tax due when there is a transfer of title and/or financing of property. 26

These taxes are paid to the state. 27

Federal government: 28

Federal government’s fiscal and monetary policies affect real estate market. 29

Federal agencies: 30

Department of Housing and Urban Development (HUD). 31

Federal Housing Administration (FHA). 32

Insures loans by conventional lenders. 33

Department of Veterans Affairs (VA). 34

Guarantees loans by conventional lenders. 35

Environmental Protection Agency (EPA). 36

Internal Revenue Service (IRS). 37

Tax code provides for tax treatment of residential and investment property. 38

Federal Reserve System (the Fed). 39

Fed takes actions taken to control inflation or stimulate economy and these actions 40

affect the real estate market. 41

42

Professional Organizations 43

National Association of Realtors® (NAR): 44

The NAR is the largest trade organization in real estate industry. On the state exam, the 45

NAR is the largest trade organization in the world. 46

Join local board or association of Realtors® then automatically become a member of the 47

Florida Association of Realtors® (FAR) and the National Association of Realtors® (NAR). 48

Local boards provide education and operate the multiple-listing service (MLS). FAR and 49

NAR provide publications. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 8 of 76

“Realtor®” is a registered trademark and not the name of a real estate license. Must be a 1

Realtor® (be a member of the NAR) to use “Realtor®.” 2

All Realtors® are licensees, but not all licensees are Realtors®. 3

Realtor® is not synonymous with real estate licensee. 4

5

6

CHAPTER 2 LICENSE LAW AND QUALIFICATIONS FOR LICENSURE 7

8

Real Estate Law 9

Real estate business was very unorganized and competitive before Real Estate License Law. 10

Caveat Emptor (= let the buyer beware) prevailed. 11

Then Florida legislature passed the Real Estate License Law, Chapter 475 of the Florida 12

Statutes (= 475 F.S.) and created the Florida Real Estate Commission (= FREC = the 13

Commission). 14

FREC was later placed within the Department of Business and Professional Regulation (= 15

DBPR = BPR = the Department). 16

FREC is administratively within the DBPR, but has separate decision making powers. 17

The Division of Real Estate (= DRE = the Division) provides support to FREC and is one of the 18

divisions of the DBPR. 19

The DRE is not separate from the DBPR. The DBPR has many divisions and one of those 20

divisions is the DRE. 21

22

Purpose of regulation is to protect the public. 23

Protect the public by regulating licensees. 24

25

Theory of Regulation of Professions and Occupations 26

Entitled to engage in profession if qualified. 27

Qualified if meet certain: 28

Application requirements. 29

Academic requirements. Demonstrate minimal competence in the real estate business. 30

Regulation appropriate only if: 31

Unregulated practice can harm public. 32

Public not adequately protected by the laws. 33

Less restrictive means of regulation are not available. 34

35

Important Real Estate Laws and Rules 36

475 F.S. Real Estate License Law. This law deals specifically with the real estate business. 37

475 F.S. has 4 parts: 38

Part 1: applies to real estate licensees. 39

Part 2: applies to appraisers. 40

Part 3: applies to commercial sales transaction lien rights for commissions. 41

Part 4: applies to commercial leasing transaction lien right for commissions. 42

455 F.S. Regulation of Professions and Occupations. This law applies to all professions that the 43

DBPR regulates including the real estate profession. 44

120 F.S. Administrative Procedures Act. This law covers administrative proceedings. 45

61J2 F.A.C. Rules of Florida Real Estate Commission (rules, not law). 46

FREC writes rules to implement the law. 47

F.A.C. = Florida Administrative Code. 48

49

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 9 of 76

Law is superior to rules. If conflict between law and rules then law wins. For example, if 1

conflict between 475 F.S. (law) and 61J2 F.A.C. (rules) then 475 F.S. (law) wins. 2

Federal law is superior to state law. 3

4

3 Real Estate License Categories 5

Sales Associate, Broker, Broker-Associate 6

Sales Associate: 7

A sales associate may be inactive (not employed) or active (employed). 8

Initial license is voluntary inactive (= inactive when pass state exam). 9

Send in form to become active. Form is effective when received by DBPR/DRE. Not 10

active when broker sends the form. Active when DBPR/DRE receives the form. 11

To provide services of real estate for others and to be compensated you must be licensed 12

and active. If licensed and inactive cannot provide services of real estate for others and be 13

compensated. 14

A sales associate must be supervised by another. They may not work independently. 15

A sales associate may not open an office of their own but may manage an office for a 16

broker under the direction of a broker. 17

Broker: 18

A broker may be inactive (not operating an office) or active (operating an office) or a 19

broker-associate (working for another). 20

If a broker-associate becomes inactive then he or she is an inactive broker (not an 21

inactive broker-associate). 22

23

Sales Associate Qualifications for Licensure 24

Must be 18 years of age or older. 25

Must have social security number. 26

High school diploma or equivalent (GED: General Education Development). 27

Honest; truthful and trustworthy; good character; reputation for fair dealing. 28

Disclosures: 29

Criminal issues must be disclosed on application. 30

Licensing issues must be disclosed on application. 31

32

Application Requirements 33

Must submit completed application. 34

Must pay fee. 35

Must have electronic fingerprints taken. 36

DBPR/DRE has a 30-day period to check for errors and omissions on application and to notify 37

the applicant. 38

Applicant must be informed of approval or denial within 90 days of receipt of last correctly 39

submitted application. 40

41

Academic Requirements 42

FREC Course I for sales associates: 63 hours. 43

FREC Course II for brokers: 72 hours. 44

50-minute hours. 45

May not miss more than 8 hours (if you miss more than 8 hours, you may not take end-of-46

class exam): 47

Must make up missed class time above 8 hours and take end-of-class exam within 30 48

days from date that the end-of-class exam was scheduled. If do not, must take the entire 49

course again. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 10 of 76

Must pass end of class exam with 70% or higher. 1

If fail end-of-class exam must wait at least 30 days to take a different version of end-of-class 2

exam (or if course available repeat course) and take end-of-class exam. If fail end-of-class 3

exam a second time must repeat course. 4

State Exam: 5

Must pass state exam with 75% or higher. 6

Have 2 years to pass state exam from successful completion of course (= from date that 7

passed end-of-class exam). 8

Application is good for 2 years from the date submitted. 9

10

Nonresident Application Requirements 11

U.S. citizenship is not required. 12

Florida residency is not required. 13

If the applicant is not a resident of Florida, they must comply with all nonresident 14

requirements. 15

The applicant is a FL resident if he/she has resided in FL for 4 months within the preceding 16

year or currently resides in FL with intention to reside for 4 months or longer. 17

If you are a Florida resident and you become a nonresident you must notify DBPR/DRE and 18

comply with nonresident requirements within 60 days. 19

Comply with nonresident requirements means sign the irrevocable consent to service form 20

within 60 days. 21

If you do not then you may (not must) be issued a citation and $300 fine. 22

23

Mutual Recognition Agreements 24

Available to licensees of Florida and certain states that Florida has entered into mutual 25

recognition agreements with because similar education and experience requirements between 26

Florida and the mutual recognition states. 27

Do not need to take course. Instead, take a 40 question exam. 30 correct out of 40 (75%) 28

required to pass. 29

Mutual: available to Florida licensees who wish to become licensed in mutual recognition states 30

and to licensees in a mutual recognition states who wish to become licensed in Florida. 31

Mutual recognition is only available if not resident of the state in which you want to become 32

licensed. If you are already a resident of the state you want to become licensed in then must 33

complete entire course and state exam. 34

Florida does not have reciprocity with any state: never automatically licensed in Florida 35

because have license in another state. 36

37

Registration and Licensure 38

Registration: DBPR/DRE has records. 39

Sales associate or broker-associate can only be registered with one employer at a time. Only 40

one employer in real estate in Florida at a time. 41

Licensure: Have a license. 42

To provide services of real estate must be licensed and must have an active license. 43

May only have one employer in real estate at a time in Florida. 44

Cannot work for a broker weekdays and a developer weekends. 45

Everyone who is licensed is registered, not everyone who is registered is licensed (example: 46

unlicensed director or officer of a real estate brokerage corporation or an unlicensed general 47

partner of a real estate brokerage general partnership or real estate brokerage limited 48

partnership). 49

Unlicensed people involved in running a brokerage must be registered for identification 50

purposes. 51

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 11 of 76

1

License Periods 2

Licenses always expire on a March 31 or September 30. 3

Initial licenses are for 18-24 months. 4

Calculating the initial license expiration/renewal date: 5

Step 1: Determine date 2 years after pass exam. 6

Step 2: Go earlier in time to either the March 31 or Sept. 30 preceding this date. 7

After initial period license is always for 2 years. 8

9

Post-Licensing Education 10

Must be a completed before first renewal of license. 11

Must complete if active or inactive. 12

Post-licensing courses require end-of-class exams but not state exams. 13

14

Sales associate post-licensing is 45 hours. 15

If do not compete sales associate post-licensing then sales associate license is void. Initial 16

license is probationary or conditional. If do not complete post-licensing must begin from 17

the start (apply to state for license, complete FREC Course I and pass state exam). 18

Requalify for licensure means begin from the start. 19

Broker post-licensing is 60 hours. 20

Only required for brokers. 21

If do not complete broker post-licensing then broker license is null and void. 22

If a broker does not complete the broker post-licensing, they have 6 months to complete 23

continuing education requirements and receive a sales associate’s license but the broker 24

license is void. 25

26

Continuing Education 27

Every 2-year licensing period following the initial period must complete 14 hours of continuing 28

education. 29

2 options: 30

In class course: No test. 31

Home course (correspondence or online): open-book test. 32

Must complete if active or inactive. 33

34

Broker Experience Requirements 35

At least 24 months during previous 5 years active with broker or government. Time active 36

under an owner developer does not count, unless brokerage set up by owner developer and 37

working for brokerage. 38

Time active does not have to be continuous. Must add up to a total of 24 months during 5 years 39

prior to becoming a broker. 40

Experience from other states and some countries counts towards the experience requirement. 41

42

Broker Education Requirement: 43

Must complete FREC Course II and pass state exam. 44

Must fulfill sales associate’s post-licensing (if Florida sales associate) prior to becoming a 45

broker. 46

If applying experience from another state or country as a sales associate or broker and directly 47

become a broker without first becoming a FL sales associate then are not required to fulfill 48

sales associate’s post-licensing prior to becoming a broker. 49

50

Real Estate Services 51

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 12 of 76

Must have a real estate license in order to perform any of the 8 real estate services for another 1

for compensation or the expectation of compensation, unless exempted by law. 2

Must have FL real estate license to perform real estate services in FL. 3

Compensation means anything of value paid, promised to be paid or expected to be paid. 4

5

8 Services of Real Estate 6

A Advertise Real Estate Services. 7

B Buy. 8

A Appraise. 9

R Rent or Provide Rental Information or Lists. 10

S Sell. 11

A Auction. 12

L Lease. 13

E Exchange. 14

15

To auction real property must be an auctioneer and also must have a real estate license. 16

To assist others in the purchase or lease of mineral rights must have a real estate license. 17

Also need a real estate license to: 18

Engage in business brokerage. 19

To sell time-share (unless salary only or registered with Securities and Exchange 20

Commission). 21

22

Surveying is not one of the services of real estate. 23

24

Exemptions from 475 F.S. means situations in which do not need a real estate license. 25

Exempt from 475 F.S. in the following situations: 26

For yourself. Do not need a license to perform any of the 8 services of real estate for yourself. 27

Sell cemetery lots (are considered personal property). 28

Rent lots in mobile home parks or recreational travel park. 29

Radio and television announcers. 30

Radio, television or cable enterprises. 31

Will (personal representatives do not need real estate licenses to settle estates). 32

Instructed by a court of law. For example, if court of law instructs a farmer to appraise a farm 33

the farmer may appraise the farm and be compensated even though the farmer is not licensed 34

or if court of law instructs a gas station owner to appraise a gas station the gas station owner 35

may appraise the gas station and be compensated even though the gas station owner is not 36

licensed. 37

Manage a condominium or cooperative: 38

Salaried employees (not commission; not transactional basis; no bonuses) who rent 39

condominiums or cooperatives for no more than 1 year. 40

If either compensation on a transactional basis or leases for more than a year then need a 41

license. 42

Work for owner/developer and only receive salary: 43

If leasing for owner/developer more than one year lease ok without license but salary only 44

(no commission, bonus or payment per transaction). 45

Attorneys-in-fact. A person who has power of attorney to act on behalf of another is called an 46

attorney-in-fact. 47

Attorneys and accountants when acting within the normal scope of their work as attorneys or 48

accountants. 49

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 13 of 76

Mortgage loan originators. Mortgages are personal property not real property. Therefore, do 1

not need a real estate license to work in the loan business. 2

Appraisers do not need real estate license to perform appraisals. 3

Transient occupancy of any public lodging establishment (hotels/motels). 4

For people working in hotel/motel business license is not required even when compensated 5

by commission. 6

A property management firm or owner of an apartment complex may pay up to a $50 7

finder’s fee or referral fee to an unlicensed person who is a tenant in such apartment. 8

May not pay compensation to an unlicensed person for real estate services or referral of real 9

estate business. 10

If licensee pays compensation to unlicensed person then it is both illegal for licensee to pay 11

and illegal for unlicensed person to receive compensation. 12

May pay compensation to a party to the transaction with disclosure to all parties because not 13

providing service of real estate for another. For example, may pay buyer buying a property 14

part of the commission from the transaction in which the buyer is buying the property. 15

An unlicensed person may assist for free (no compensation). 16

For example: If friend at a party agrees to help me for free then no license is required. 17

May give compensation to out-of-state broker, but out-of-state broker may not assist in 18

transaction unless licensed in FL. 19

May not give compensation to out-of-state lawyer, but may give compensation to out-of-state 20

lawyer if in that state lawyers are considered brokers (however, out-of-state lawyer may not 21

assist in transaction unless licensed in FL). 22

May pay compensation to any person from a country without license law. 23

24

25

CHAPTER 3 LICENSE LAW AND ADMINISTRATION 26

27

Purpose of regulation (= laws and rules) is to protect the public by regulating licensees. 28

29

Florida Real Estate Commission (FREC) 30

Administratively part of DBPR but separate duties and powers. 31

Composition and Qualifications: 32

7 members: 33

4 must be brokers with active license during the 5 years prior to appointment. 34

1 must be either a broker or sales associate with active license 2 years prior to appointment. 35

2 must be consumer members who have never held a real estate license. 36

1 must be at least 60 years old. 37

Appointed by governor and confirmed by state senate. 38

Appointed to 4-year terms expiring on October 31 (maximum of 2 consecutive terms). 39

Accountable to Governor. 40

Exempt from civil liability while performing duties. 41

Reason: so that can impose penalties on licensees without fear of being sued. 42

43

Compensation: 44

Members of FREC do not receive a salary because they are not employees. FREC members 45

do receive compensation of $50 per day + expenses (for example travel and hotel). 46

47

Meetings: 48

Meetings (need quorum; 51%; 4 members). 49

FREC requires a quorum to make most of its decisions. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 14 of 76

Monthly meeting includes hearing disciplinary matters. 1

During annual meeting elect chairperson and vice chairperson. 2

3

Commission General Powers and Duties 4

Adopt a seal. The seal is prima facie evidence that document is authentic. 5

Prima facie means courts accept document as authentic on its face without need for 6

additional evidence. 7

Seals are no longer required on deeds, mortgages, notes or contracts. 8

Foster education of applicants and licensees (FREC specifies areas to be tested on 9

examinations). 10

Make determinations of violations. 11

Regulate professional practices (record keeping, escrow rules, escrow disbursement orders 12

(EDOs)). 13

Brokers must maintain records for 5 years. 14

Create and pass rules and regulations (61J2 F.A.C.). 15

Establish fees. 16

Fees collected may only be used for regulation of real estate. 17

Grant or deny applications for licensure. 18

Suspend (maximum 10 years) or revoke licenses. 19

Revocation is the most severe penalty FREC may impose. 20

Impose administrative fines: 21

Maximum fine per offense: 22

Under 475 F.S. is $5,000. 23

Under 455 F.S. is $5,000. 24

Up to $5,000 per violation. For example, if three separate violations then may face a 25

maximum of $15,000. 26

FREC can only impose administrative penalties. FREC cannot impose civil or criminal 27

penalties. 28

“Quasi” when added to the beginning of a word means resembling: 29

When FREC writes rules this is a quasi-legislative power because FREC is acting similarly 30

to a legislature. 31

When FREC imposes penalties this is a quasi-judicial power because FREC is acting similar 32

to a court. 33

34

Department of Business and Professional Regulation (DBPR) has Various Divisions 35

Division of Technology, Licensure and Testing. 36

Division of Regulation. 37

Division of Professions. 38

Division of Real Estate (DRE). 39

Division of Florida Condominiums, Timeshares and Mobile Homes. This division regulates 40

cooperatives even though Cooperatives is not in the name of the division. 41

42

The head person of DBPR is the Secretary of the DBPR. The Secretary of the DBPR is 43

appointed by the Governor and is subject to confirmation by the State Senate. 44

45

Division of Real Estate (a division of the DBPR) 46

Provides support services to FREC (examples: record keeping, investigations, etc.). 47

Funding (fees assessed by FREC used only to fund real estate regulation; may not be used in 48

other areas). 49

Employees: 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 15 of 76

Some employees of the DBPR are assigned to the DRE. 1

Director of DRE is a career official who serves as contact with FREC. 2

Director of DRE appointed by secretary of DBPR with approval by majority vote of 3

FREC. 4

5

Change of Mailing Address 6

Must notify DBPR/DRE within 10 days. 7

If fail to notify may (not must) receive a citation and $500 fine. 8

If move out of state must both notify of change in address within 10 days and comply with 9

nonresident requirements within 60 days. 10

11

License Renewal Periods 12

The 2-year renewal periods always end on either March 31 or Sept. 30. 13

The Initial license is for 18 to 24 months (at least 18 months but no longer than 24 months). 14

Military: military men and women with real estate licenses are exempt from renewal 15

requirements while on active duty in military + 6 months after (if military service is out of state 16

this exemption also applies to spouse of the member of the military). 17

Does not apply to member of military or spouse if provide services of real estate. 18

Spouse of a member of the military relocated to Florida may apply for a 6 month temporary 19

real estate license. 20

21

Inactive Status: 22

2 types of inactive status: voluntarily inactive vs. involuntarily inactive. 23

Voluntarily inactive (choose to be inactive; may be inactive indefinitely; may become active; 24

must complete post-licensing and CE (continuing education) even if inactive). 25

Involuntarily inactive (when do not renew, usually because do not complete CE). 26

After 2 years involuntary inactive, license expires automatically (null + void). 27

If involuntary inactive for 12 months or less must complete 14 hours of CE and an 28

additional 14 hours of CE prior to end of next 12 months. 29

If involuntarily inactive for more than 12 months but less than 24 months must take 28 30

hours of FREC I course (also called reactivation education) and a 50 question end-of-31

course exam (70% required to pass). 32

There is a late fee for late renewals. 33

If choose not to renew or choose not to complete continuing education, then are 34

involuntarily inactive. 35

36

If license lost or destroyed then need duplicate license. It is the same license number. Must pay 37

fee for duplicate license. 38

39

Cancellation: Licensee has not done anything wrong but will no longer be using license then this 40

is a cancellation. 41

42

Void and Ineffective Licenses 43

Void: 44

Void means license is gone forever (permanent). 45

A license is void if the license expires or is revoked or is cancelled. 46

Ineffective: 47

Ineffective means license cannot be used for some period of time (temporary). 48

A license is ineffective if the license is inactive or suspended. 49

50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 16 of 76

Cease to be in Force 1

License ceases to be in force until notify DBPR/DRE of change of business address of real estate 2

brokerage office or real estate school or change of employer for a sales associate, broker 3

associate or instructor. 4

10 days to notify DBPR/DRE of change. 5

6

Involuntarily Inactive 7

Sales associate or broker associate becomes involuntarily inactive when there is only one 8

employing broker and this broker is suspended or revoked or dies. 9

To become active again either the brokerage resolves the problem or the sales associate or 10

broker associate finds another employer and submits the appropriate form to the DBPR/DRE. 11

12

Multiple and Group Licenses 13

Multiple License: 14

A broker may acquire multiple licenses to operate more than one brokerage entity. 15

Only a broker may have multiple licenses. A sales associate or broker associate may not 16

have multiple licenses. A sales associate or broker associate may have only one employer in 17

real estate in Florida. 18

Group License: 19

A broker-associate or sales associate may acquire a group license to work at more than one 20

location. 21

Owner-developer owns properties under name of different entities but the ownership is 22

common. 23

Must work directly for a developer (not broker). 24

Are considered to have only one employer. 25

No distinction is made on the face of the license. 26

27

28

CHAPTER 4 AGENCY AND ETHICS 29

30

A Real Estate Licensee May Work In One of Three Capacities or Relationships with Customers 31

Single agency. 32

Transaction broker. 33

No brokerage relationship. 34

35

Law of Agency 36

Agent: A person entrusted with another’s business. 37

Principal: A person who authorizes the agent. 38

The agent represents a principal. 39

3 types of agents: 40

Universal Agent: Principal authorizes agent to perform all acts. 41

General Agent: Principal authorizes agent to perform all acts related to a particular 42

business or employment (example: property manager). 43

A sales associate or broker associate is a general agent to his or her broker. 44

Special Agent: Principal authorizes agent to perform only a specific business transaction or 45

specific act. 46

If single agency exists then real estate brokers are usually special agents. 47

48

Fiduciary Relationship 49

Relationship of trust and confidence (opposite of dealing at arm’s length). 50

Fiduciary: An agent is a fiduciary to his or her principal. 51

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 17 of 76

An agent owes a duty of loyalty to his or her principal. 1

2

Disclosure Requirements Apply Only in Residential Sales 3

Brokerage Relationship Disclosure Act is the section of 475 F.S. that covers allowed brokerage 4

relationships and under this act the disclosure notices are only mandatory in residential sales 5

transactions. 6

475 F.S defines a residential sale as sale of: 7

Improved property of 4 units or fewer. 8

Unimproved property (empty land) in which zoning only allows 4 or fewer units. 9

Property zoned agricultural of 10 acres or less. 10

11

Single Agent Representation 12

Duties: 13

Dealing honestly and fairly. 14

Loyalty. 15

Loyalty is a duty in single agent representation. 16

Loyalty is not a duty in a transaction broker relationship. 17

Loyalty is not a duty in no brokerage relationship. 18

Confidentiality. 19

Duty of confidentiality survives end of agency relationship. 20

Obedience. 21

Agent must obey all legal instructions from the principal. 22

Full disclosure. 23

Accounting for all funds. 24

Skill, care and diligence in the transaction. 25

Presenting all offers and counteroffers in a timely manner, unless instructed otherwise in 26

writing. 27

Disclosing to buyer all known facts that materially affect the value of residential real 28

property and are not readily observable (= must disclose all latent defects). 29

The duties of loyalty, confidentiality, obedience and full disclosure are single agent duties 30

and do not exist in the transaction broker and no brokerage relationships. 31

32

Dual agency is illegal: Prohibited to be an agent to both the seller and buyer in the same 33

transaction. 34

Principal may be held responsible for acts of agent. 35

A direct legal relationship exists between the customer (seller, buyer, landlord or tenant) and 36

the brokerage/broker. 37

Whichever brokerage relationship is established between the brokerage/broker and the 38

customer then all the sales associates and broker associates employed by this brokerage will 39

owe the same set of duties to the customer. 40

For example, if single agency established with a buyer the brokerage/broker owes the duties 41

of an agent to the buyer and all sales associates and broker associates employed by the 42

brokerage owe the same duties of a single agent to this buyer. 43

A sales associate is a subagent to the broker’s principal. 44

45

Transaction Broker Relationship 46

Transaction Broker represents a customer in limited manner. 47

On state exam limited representation = transaction broker relationship. 48

Duties: 49

Dealing honestly and fairly. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 18 of 76

Accounting for all funds. 1

Using skill, care and diligence in the transaction. 2

Disclosing to buyer all known facts that materially affect the value of real property and are 3

not readily observable to the buyer. 4

Presenting all offers and counteroffers in a timely manner, unless instructed otherwise in 5

writing. 6

Limited confidentiality, unless waived in writing by a party. 7

Confidentiality regarding price, terms and motivation. 8

Any additional duties that are mutually agreed to with a party. 9

10

May work as a transaction broker to both sides. 11

Customer is not responsible for acts of transaction broker. 12

If no notice given to customer then transaction broker is default relationship. 13

14

No Brokerage Relationship 15

Duties: 16

Dealing honestly and fairly. 17

Disclosing to buyer all known facts that materially affect the value of residential real 18

property and are not readily observable. 19

Accounting for all funds. 20

21

May work as a single agent to one side and no brokerage relationship to other side (owe 22

fiduciary duties to the side you are a single agent to). 23

24

Notices: 25

Single Agent Notice used to establish single agency. 26

Transaction Broker Notice used to establish transaction broker. 27

No Brokerage Relationship Notice used to establish no brokerage relationship. 28

Consent to Transition to Transaction Broker Notice: to change from single agency to transaction 29

broker. 30

31

Transitioning to another Relationship 32

May transition from any one of the three relationships to any of the other relationships. 33

To transition from Single Agency to Transaction Broker status must use the Consent to 34

Transition to Transaction Broker Notice. 35

This notice must be signed (the other notices must be presented). 36

If single agency with a seller and a buyer and then buyer becomes interested in seller’s home 37

must transition to transaction broker prior to showing the home to the buyer. 38

39

Buyer Representation 40

May represent a buyer as a single agent or as a transaction broker or no brokerage 41

relationship. 42

43

Allowed (Legal): 44

May be a transaction broker to both sides in the same transaction. 45

May be no brokerage relationship to both sides in the same transaction. 46

May be a single agent to one side and no brokerage relationship to the other side in the same 47

transaction. 48

May be a transaction broker to one side and no brokerage relationship to the other side in the 49

same transaction. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 19 of 76

1

Not allowed (Illegal): 2

May not be a single agent to both sides in the same transaction. 3

May not be a single agent to one side and transaction broker to the other side in the same 4

transaction. 5

6

Designated Sales Associate 7

This form of representation is not available in residential transactions. 8

Available in commercial transactions. 9

Buyer and seller must request in writing. 10

Buyer and seller must each have assets of 1 million or more. 11

One sales associate is the single agent to the buyer; one sales associate is single agent to the 12

seller. 13

Broker advises each sales associate but is not an agent to the buyer or seller. 14

15

Terminating a Brokerage Relationship 16

Brokerage relationship ends with: 17

Fulfillment of the brokerage relationship’s purpose. 18

Mutual agreement to terminate the brokerage relationship. 19

Expiration of the terms of the agreement. 20

Broker renunciation of the brokerage relationship by giving notice to the customer. 21

Revocation by the customer: The customer may be liable for damages (such as advertising 22

expenses) incurred by revoking the brokerage relationship prior to the termination date. 23

Death of the broker or seller customer or death of the broker or buyer customer. 24

Brokerage relationship is not terminated if other party to the transaction dies. 25

Example: If broker is agent to seller and the buyer dies then agency relationship 26

between broker and seller is not terminated. 27

Destruction of the property or condemnation by eminent domain. 28

Bankruptcy of the seller customer. 29

30

Misrepresentation and Fraud 31

Misrepresentation: A misstatement or omission or concealment of a factual matter. 32

Usual (not must) penalty for misrepresentation or concealment is revocation. 33

Fraud: In order to sustain a charge of fraud, must have all of the following 4 elements: 34

1. Misrepresentation: Misstatement or omission of material fact. 35

2. Licensee knew or should have known that was making a misrepresentation. 36

3. Buyer relied on misrepresentation. 37

4. Damages to buyer. 38

If there are no damages, then fraud does not exist. 39

Even if no damages and therefore no fraud for misrepresentation alone FREC will 40

usually revoke. 41

Example of fraud: if owner induces someone to buy with agreement that will buy property back 42

in the future. However, if actually do buy property back at agreed terms then not fraud. 43

Lotteries or raffles to win real property are illegal under Florida law. 44

45

Professional Ethics 46

Professionalism and a code of ethics. 47

The National Association of REALTORS® code of ethics has greatly affected laws and rules in 48

many states. 49

Being ethical is good for business. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 20 of 76

1

2

CHAPTER 5 REAL ESTATE BROKERAGE OPERATIONS 3

4

Brokerage Offices 5

An active broker must have an office. 6

Must have at least one enclosed room. 7

Office must be stationary. 8

A broker may have their office at home if allowed by the zoning code and sign requirements 9

are met. 10

Sales associates may not have an office (must work and be registered in office of employer). 11

12

Principal Office (= primary = main office) vs. Branch Office 13

Principal office registration is transferable form one location to another. 14

Branch office registration is not transferable. 15

A new registration must be acquired for a new location. 16

However, if time remains on a previous branch office registration may move back and use 17

time remaining on previous registration. 18

19

Temporary Shelter is Not a Branch Office 20

If trailer at a construction site is only for protection from elements then does not need to be 21

registered as a branch. 22

A location must be registered as a branch office if any of the following: 23

Advertising to the outside world leads people to the location. 24

Brochures stored in the location is not an example of advertising to outside world. 25

Therefore, does not have to be registered as a branch. 26

Sales associates are assigned to the location. 27

Transactions are concluded at the location. 28

29

Signs (on or about entrance) 30

Sign may be inside or outside but must be at principal office and any branch office and must be 31

easily observed as enter. 32

Must include brokerage name or trade name (if operating under a trade name), name of broker 33

and “Licensed Real Estate Broker” or “Lic. Real Estate Broker”. Realtor® is not on this sign. 34

May include other brokers, broker-associates and sales associates. 35

Space or line between mandatory information and allowed information. 36

License status must be disclosed next to name. 37

38

Advertising (includes ads in newspapers, television, radio, internet, business cards, pens, etc.) 39

All ads must include brokerage name (not name of broker). 40

False advertising: 41

Blind advertisement: No information given that are dealing with a broker. 42

Blind advertising is illegal. 43

2nd degree misdemeanor. 44

When advertising on the internet the name of brokerage firm must appear by point of contact 45

information (usually telephone number or email address). 46

If licensee places his name in advertising then must include real last name. For example, 47

Thomas Smith may advertise as Tom Smith. 48

Sales associate or broker associate is advertising under name of brokerage with permission of 49

brokerage. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 21 of 76

Sold signs are considered advertising. 1

Illegal to place Sold sign on For Sale sign prior to closing without written consent of seller. 2

Only at closing is property actually sold. 3

May place pending sale or under contract sign on For Sale sign once under contract without 4

written consent of seller. 5

6

Telephone cold calling restraints 7

No solicitation list (also called do not call list): 8

May be subject to fine if call someone on the no solicitation list. 9

Exceptions (no fine even if individual is on the no solicitation list): Past customers, 10

sellers who are advertising if you really have a buyer interested in the property. 11

FL Law 12

$10,000 per violation. 13

FSBO could be called without fine. 14

Past client could be called without fine. 15

Federal Law 16

$11,000 per violation. 17

If call FSBO subject to fine unless really have an interested buyer. 18

Past clients can be called for 18 months without being subject to fine. 19

20

Escrow or Trust Accounts 21

Escrow account = trust account. 22

Escrow money must be kept in an escrow account not in a personal or business account. 23

Funds must be deposited immediately: 24

Sales associate (or other employee: secretary or receptionist): Must give to 25

broker/employer no later than end of next business day. 26

Broker: Must deposit in escrow account not later than end of 3rd business day from original 27

receipt. 28

These are business day calculations: Saturdays, Sundays and legal holidays do not count. 29

On state exam immediately is a correct answer if other answers are incorrect. 30

Post-dated check or promissory note: Seller must approve a post-dated check or promissory 31

note before it is accepted by licensee. 32

Broker must be signatory on escrow account (others may be signatories). 33

Account may bear interest or not bear interest. 34

Must be in a Florida institution. 35

Broker must review and sign monthly reconciliation statement. 36

A broker is not required to maintain an escrow account. 37

Instead escrow money may be held by an attorney or a title company. 38

If attorney or title company is holding escrow funds then the sales contract (purchase and 39

sale contract) must state name, address and telephone number of attorney or title company. 40

If attorney or title company is holding escrow funds and attorney or title company chosen 41

by buyer then buyer’s broker must request within 10 business days in writing a written 42

verification from the attorney or title company verifying that they are holding the escrow 43

funds and provide a copy of such verification to seller’s broker. 44

To move money from one escrow account to another escrow account everyone must agree. 45

46

Disposition of Escrow Deposits 47

Commingling (also called intermingling): Mixing of escrow funds with any other funds is illegal. 48

Conversion: Converting another’s property for own use. 49

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 22 of 76

A broker may have a maximum of $1,000 of non escrow money in a sales escrow account and a 1

maximum of $5,000 of non escrow money in a property management escrow account. 2

If a broker has $5,000.01 of non escrow money in an escrow account then illegal. 3

4

Conflicting Demands on Escrow Funds or Good-faith Doubt Regarding Disposition of Escrow Funds 5

Notify FREC in 15 business days of conflicting demands or good faith doubt and follow one of 4 6

settlement or escape procedures in 30 business days of conflicting demands or good faith doubt. 7

8

4 settlement procedures: 9

1. Mediation. 10

Not binding. 11

2. Escrow Disbursement Order. 12

FREC may issue (in some cases FREC may decide not to issue an EDO). 13

If request EDO and escrow dispute is going to litigation or is settled broker must notify FREC 14

within 10 business days. 15

3. Arbitration. 16

Binding. 17

4. Litigation. 18

Declaratory Judgment: Broker asking for declaration that he/she is entitled to funds. 19

Interpleader: Deposit escrow funds in court. 20

Memory aid: Interpleader (In: Put money in the court). 21

Broker attempting to distance him or herself from litigation. 22

23

Rental lists and rental companies: 24

Notice must state: 25

Refund of 75% if list is not used to obtain rental. 26

75% refund even if the buyer of the list does not try to use list. 27

Refund of 100% if list is not current or inaccurate. 28

30 days to obtain refund. Request may be in writing or oral. After 30 days zero refund. 29

Violation is 1st degree misdemeanor. 30

May also face administrative penalties. 31

32

Licensee’s Role as an Expert 33

Opinions of title: 34

A licensee may not give an opinion of title. A licensee may acquire an opinion of title from an 35

attorney and convey the opinion of title to the purchaser or advise the purchaser to contact an 36

attorney or advise the purchaser to get title insurance. 37

A licensee should never state that title is ok. However, if licensee knows that title to property is 38

not marketable or lien exists then must inform purchaser. 39

Representation of value: 40

Must be careful not to misrepresent value. 41

42

Broker’s Commission 43

Antitrust laws (Sherman Act, Clayton Act and Federal Trade Commission Act) are designed to 44

promote fair competition. 45

Brokers may not conspire to fix commissions. 46

MLS may not fix commissions or commission splits. 47

Sales Associates and broker associates accept listings, deposits and commissions on behalf of 48

their broker with broker’s express consent. 49

Sales associates and broker associates may sue employer, but cannot sue seller or buyer. 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 23 of 76

Customer pays brokerage and then sales associate is paid by their brokerage. This includes all 1

compensation including BPOs. 2

3

Kickback 4

It is usually a kickback when a licensee receives money from someone other than the seller or 5

buyer. 6

If parties are informed then it is acceptable, unless category that is always illegal: 7

Insurance kickbacks are always illegal. 8

9

Policy Manual 10

States rules and regulations of office. 11

Provides information to new sales associates. 12

13

Change of Employer 14

Agency relationship duties survive the end of the agency relationship. 15

Confidential information learned during agency must be kept confidential after agency 16

relationship is terminated. 17

Must notify DBPR/DRE of change of employer within 10 calendar days. 18

A sales associate or broker associate may not divert buyer or sellers from completion of a 19

transaction. 20

Records: 21

Breach of trust: If duplicate records. 22

Larceny (theft): If take original records. 23

24

Membership in Organizations 25

Violation of 61J2 F.A.C. to claim membership in any real estate organization if you are not a 26

member. 27

28

These Business Entities May Register as Brokers or Brokerages 29

Sole Proprietorship. 30

Partnerships: 31

General Partnership. 32

Limited Partnership. 33

Limited Liability Partnership. 34

Corporation. 35

Limited Liability Company. 36

37

Business Arrangements and Entities That May Not Register as Brokers or Brokerages 38

Corporation Sole. 39

Joint Venture. 40

Business Trust. 41

Cooperative Association. 42

Unincorporated Association. 43

44

Types of Business Entities That May Register As Brokers or Brokerages 45

All brokerages no matter how structured must be registered with the DBPR. 46

All brokerages no matter how structured must have the name they operate under registered 47

with the DBPR. 48

49

Sole Proprietorship 50

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 24 of 76

Definition: Business owned by one person. 1

Taxation: Single. 2

Liability: Personal liability for business debts. 3

Real Estate Brokerage Sole Proprietorships: 4

Sole proprietor must be an active broker. 5

Sales associate or broker-associate may be employees only. 6

7

General Partnerships 8

Definition: Association of two or more persons for the purpose of jointly conducting business, 9

each being responsible for all debts incurred and having power to bind the other(s). 10

How formed: written agreement or oral agreement or implied by actions. 11

Structure: General partners run general partnerships. 12

Taxation: Single. 13

Partnership not taxed, individuals are taxed. 14

Liability: Unlimited liability (individuals are personally liable). 15

Real Estate Brokerage General Partnerships: 16

At least one general partner must be an active broker. 17

All general partners that will engage in the services of real estate with the general public 18

must be active brokers. 19

Other general partners that will not engage in services of real estate with general public 20

may be active brokers or inactive brokers or unlicensed but registered (unlicensed general 21

partners must be registered for identification purposes). 22

Sales associates or broker-associates may not be general partners. 23

Sales associates or broker-associates may be employees. 24

14-day rule applies. 25

26

Limited Partnership 27

How formed: File written instrument/register with Florida Department of State. 28

Structure: General partners run the business. Limited partners contribute money or property 29

but do not run the business. 30

Taxation: Partnership not taxed, individuals pay tax. 31

Liability: General partners are personally liable for partnership's debts; Limited partners have 32

limited liability. 33

Real Estate Brokerage Limited Partnership: 34

At least one general partner must be an active broker. 35

All general partners that engage in the services of real estate with the public must be active 36

brokers. 37

All general partners that do not engage in the services of real estate with the public must be 38

active brokers or inactive brokers or unlicensed but registered (unlicensed general partners 39

must be registered for identification purposes). 40

Sales associates or broker-associates may not be general partners. 41

Sales associates or broker associates may be limited partners or employees. 42

43

Both a general partnership and limited partnership must notify DBPR if add or subtract a general 44

partner (not a limited partner). 45

46

Limited Liability Partnerships (LLP) 47

Formed by filing with the Department of State. 48

Limited liability partners run a limited liability partnership. 49

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 25 of 76

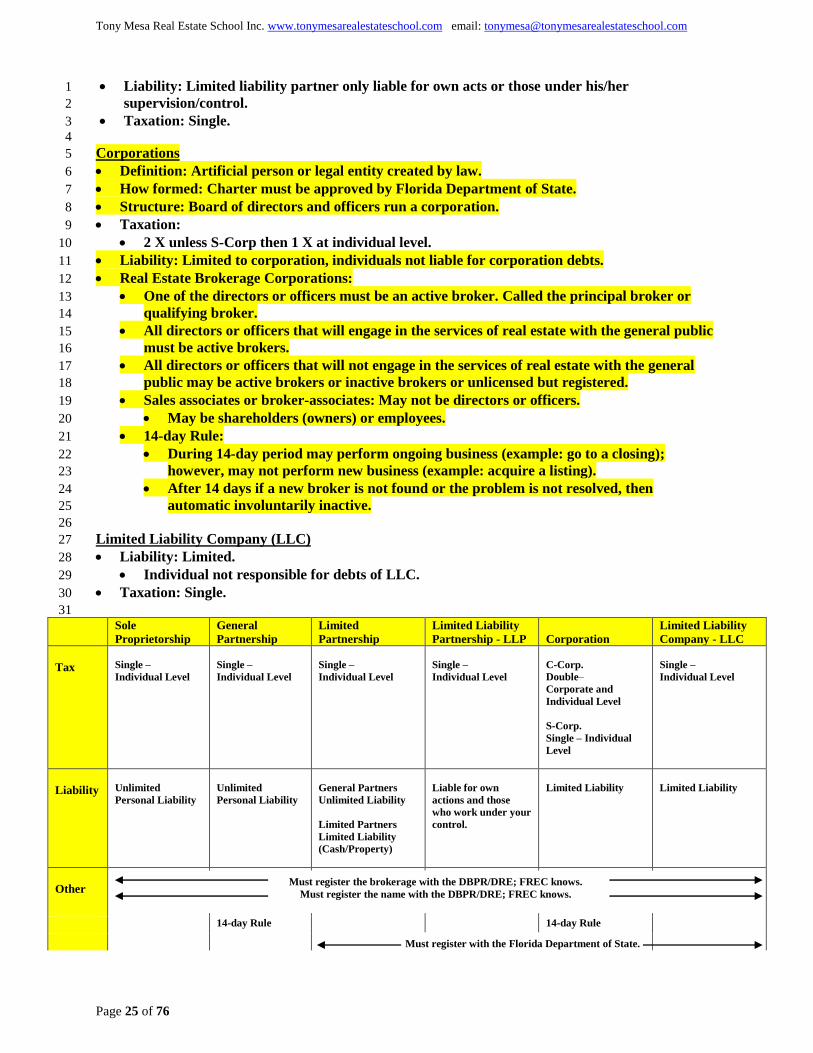

Liability: Limited liability partner only liable for own acts or those under his/her 1

supervision/control. 2

Taxation: Single. 3

4

Corporations 5

Definition: Artificial person or legal entity created by law. 6

How formed: Charter must be approved by Florida Department of State. 7

Structure: Board of directors and officers run a corporation. 8

Taxation: 9

2 X unless S-Corp then 1 X at individual level. 10

Liability: Limited to corporation, individuals not liable for corporation debts. 11

Real Estate Brokerage Corporations: 12

One of the directors or officers must be an active broker. Called the principal broker or 13

qualifying broker. 14

All directors or officers that will engage in the services of real estate with the general public 15

must be active brokers. 16

All directors or officers that will not engage in the services of real estate with the general 17

public may be active brokers or inactive brokers or unlicensed but registered. 18

Sales associates or broker-associates: May not be directors or officers. 19

May be shareholders (owners) or employees. 20

14-day Rule: 21

During 14-day period may perform ongoing business (example: go to a closing); 22

however, may not perform new business (example: acquire a listing). 23

After 14 days if a new broker is not found or the problem is not resolved, then 24

automatic involuntarily inactive. 25

26

Limited Liability Company (LLC) 27

Liability: Limited. 28

Individual not responsible for debts of LLC. 29

Taxation: Single. 30

31

Sole

Proprietorship

General

Partnership

Limited

Partnership

Limited Liability

Partnership - LLP

Corporation

Limited Liability

Company - LLC

Tax

Single –

Individual Level

Single –

Individual Level

Single –

Individual Level

Single –

Individual Level

C-Corp.

Double–

Corporate and

Individual Level

S-Corp.

Single – Individual

Level

Single –

Individual Level

Liability

Unlimited

Personal Liability

Unlimited

Personal Liability

General Partners

Unlimited Liability

Limited Partners

Limited Liability

(Cash/Property)

Liable for own

actions and those

who work under your

control.

Limited Liability

Limited Liability

Other

14-day Rule 14-day Rule

Must register the brokerage with the DBPR/DRE; FREC knows.

Must register the name with the DBPR/DRE; FREC knows.

Must register with the Florida Department of State.

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 26 of 76

A sales associate or

broker-associate may

be a limited partner.

A sales associate or

broker-associate may

be a shareholder or

stockholder.

1

Trade Name (= fictitious name) 2

Trade names must be registered with Florida Department of State. 3

Required by the Florida Fictitious Name Act. 4

Exception: Sole proprietorship only registered with the DBPR. 5

One name per brokerage (if operated under more than one name, public would be confused). 6

7

8

Business Arrangements and Entities That May Not Register as Brokers 9

Corporation Sole: An ecclesiastical or church organization. 10

Joint Venture: Two or more parties combine efforts to complete one or a fixed number of 11

business transactions. 12

Broker cooperation is a common joint venture in the real estate business. 13

Business Trust: A form of business entity that may be formed to engage in transactions 14

involving its own real property. 15

Cooperative Association (= cooperatives). 16

Unincorporated Association: Groups of people associated for some noncommercial purpose. 17

18

19

Real Estate Investment General Partnership 20

An investment general partnership is not a brokerage. Two or more persons buy and sell or 21

rent properties as investments. 22

Uneven profit splits. 23

Even profit splits acceptable even if some partners are licensed and some partners are not 24

licensed. 25

Uneven profit splits are prohibited if there is no written agreement and no one licensed and 26

equal contributions. 27

28

Ostensible Partnership (= quasi partnership) 29

Not intentionally created. Imposed by a court of law. 30

Act in a manner that the public would believe is a partnership. Therefore, courts will treat like 31

a partnership. 32

Are acting in violation of law. 33

34

Personal Assistants 35

Unlicensed assistants: 36

If work for sales associate then sales associate pays salary. 37

An unlicensed assistant may not show properties or negotiate. 38

An unlicensed assistant may not do anything that involves judgment. 39

An unlicensed assistant may be not give an opinion about values or repair costs. 40

An unlicensed assistant may attend an open house for security purposes, to distribute 41

flyers and to answer factual questions based on printed material. 42

43

Licensed assistants: 44

If work for sales associate then sales associate pays salary but broker pays any 45

commission. 46

May provide services of real estate. 47

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]

Page 27 of 76

1

2

CHAPTER 6 COMPLAINTS, VIOLATIONS AND PENALTIES 3

4

Complaint Process 5

The complaint Process involves the following steps: 6

Filing the complaint. 7

Investigation. 8

Probable Cause. 9

Formal Complaint. 10

Informal Hearing. 11

Formal Hearing. 12

Final Order. 13

Judicial Review (Appeal). 14

15

Filing the Complaint 16

Complaint: Alleges a violation of a law or rule. 17

Complaint is filed with DBPR. 18

Complaint is legally sufficient if it states the violation of Florida Statute, DBPR rule or FREC 19

rule. 20

If in writing and legally sufficient then must be investigated. 21

May be on a uniform complaint form. 22

23

Notice of non-compliance. 24

Given for 1st time minor offense (minor if not a threat to the public). 25

15 days to correct the offense/problem. 26

27

Investigation 28

The DBPR/DRE may investigate an anonymous complaint. 29

The DBPR/DRE may decide to investigate on its own. 30

The DBPR/DRE may continue investigation if complainant withdraws complaint. 31

Copy of complaint is sent to subject (= usually a licensee) when investigation begins. 32

Unless may jeopardize criminal investigation. 33

Subject may respond in writing to the complaint. 34

The DBPR/DRE produces an investigative report. 35

Investigative report submitted to probable cause panel. 36

37

Probable Cause 38

2 members of FREC. 39

1 may be a former member. 40

1 must be a professional member. 41

Panel Segregation: Those members of FREC on the probable cause panel may not be 42

involved in the informal hearing or the final order. 43

Determine if probable cause exists (reasonable grounds to prosecute). 44

If no probable cause exists then dismissal. 45

If probable cause exists then instructs DBPR to produce a formal complaint. 46

Once probable cause panel concluded notice sent to complainant and subject of investigation. 47

48

49

Tony Mesa Real Estate School Inc. www.tonymesarealestateschool.com email: [email protected]