Embed Size (px)

Citation preview

Tony KnapPresident and Director

Bermuda Biological Station for ResearchSt. George’s, BERMUDA ([email protected])

Insurance sector needs: a personal view (Steve Lyons, 2004)

Insurance/re-insuranceInsurance/re-insurance Need information on long-term climate Need information on long-term climate

how it relates to riskshow it relates to risks

However only specific to a few regional However only specific to a few regional areasareas

Need better information to be used in Need better information to be used in commercial risk modelscommercial risk models

Where does an IOOS fit in ?Where does an IOOS fit in ?

A personal view of insuranceA personal view of insurance

Take in premiums - invest $ - gather the profits- Take in premiums - invest $ - gather the profits- have good underwriting so they don’t lose it !have good underwriting so they don’t lose it !

When the stock market and other financial When the stock market and other financial markets soften - so does profitmarkets soften - so does profit

5 years ago markets softened - companies tried to 5 years ago markets softened - companies tried to underwrite real time hurricane landfall as energy underwrite real time hurricane landfall as energy risk (degree day heating) - many got burnedrisk (degree day heating) - many got burned

Presently traditional reinsurance is relatively Presently traditional reinsurance is relatively strong so they now stick to traditional underwriting.strong so they now stick to traditional underwriting.

Different risks and InsuranceDifferent risks and Insurance

Life, health, auto, unemployment, Life, health, auto, unemployment, protection and indemnity, D & O, protection and indemnity, D & O, product liability, Terrorismproduct liability, Terrorism

IOOS - Property/catastrophic IOOS - Property/catastrophic insurance - long term view - can’t insurance - long term view - can’t dump customers because of a Bill dump customers because of a Bill Gray - bad forcast !Gray - bad forcast !

Risks of interest (re-insurersRisks of interest (re-insurers)) Tropical Cyclones-landfall (frequency and intensity) long term Tropical Cyclones-landfall (frequency and intensity) long term

- mainly US/Japan/Australia- mainly US/Japan/Australia

Earthquake (frequency and intensity) existing areas and Earthquake (frequency and intensity) existing areas and concerns about new areas - including underwater (Tsunamis)concerns about new areas - including underwater (Tsunamis)

Windstorms (europe) (frequency/seriality)Windstorms (europe) (frequency/seriality)

Flood (in europe) - US covered by Govt.Flood (in europe) - US covered by Govt.

TornadoTornado

Hail Hail

FireFire

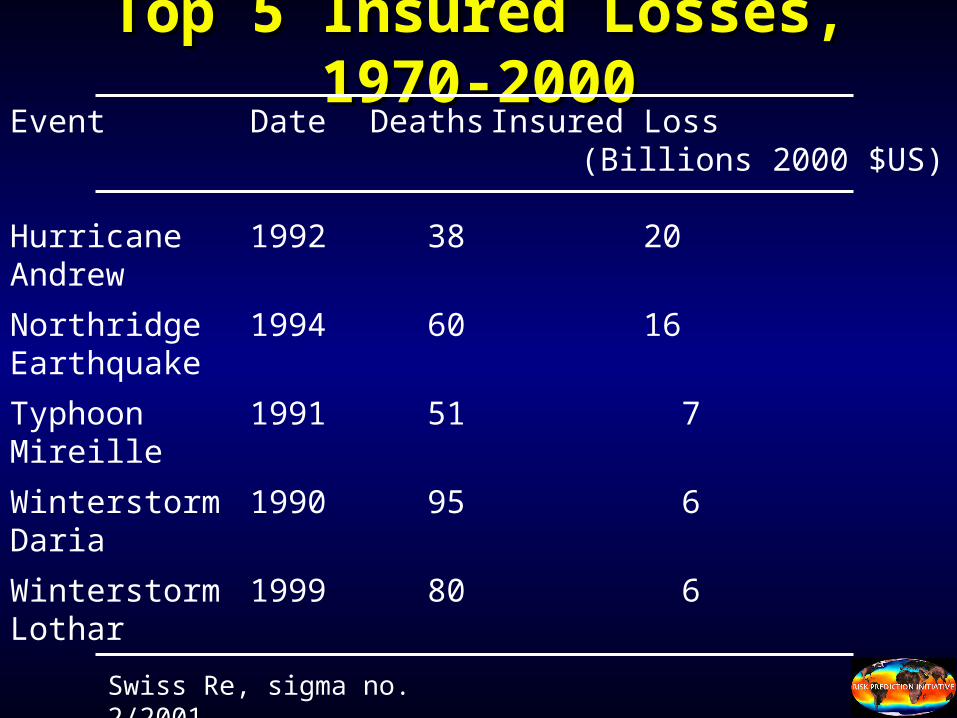

Top 5 Insured Losses, 1970-2000Top 5 Insured Losses, 1970-2000

Swiss Re, sigma no. 2/2001

Event Date Deaths Insured Loss (Billions 2000 $US)

Hurricane 1992 38 20Andrew

Northridge 1994 60 16Earthquake

Typhoon 1991 51 7Mireille

Winterstorm 1990 95 6Daria

Winterstorm 1999 80 6Lothar

CO

2 (p

pm

v)

Year

0

5

10

15

20

25

30

1925 1935 1945 1955 1965 1975 1985 1995

Year

Billions 1992 $US

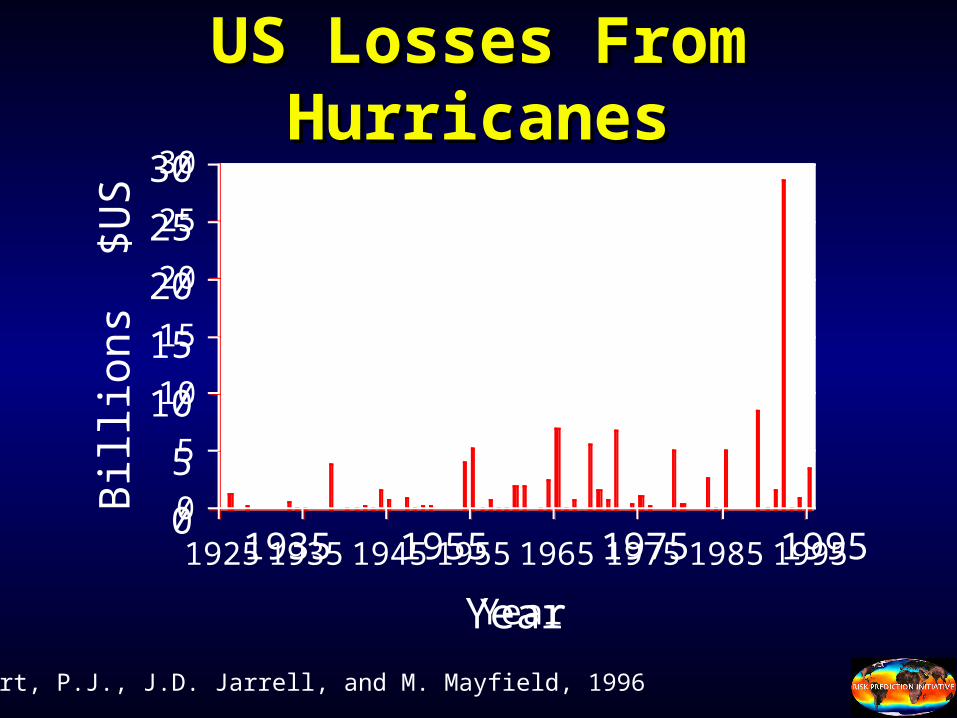

US Losses From HurricanesUS Losses From Hurricanes

Herbert, P.J., J.D. Jarrell, and M. Mayfield, 1996

1935 1955 1975 1995

30

25

20

15

10

5

0

Bill

ions

$U

S

Year

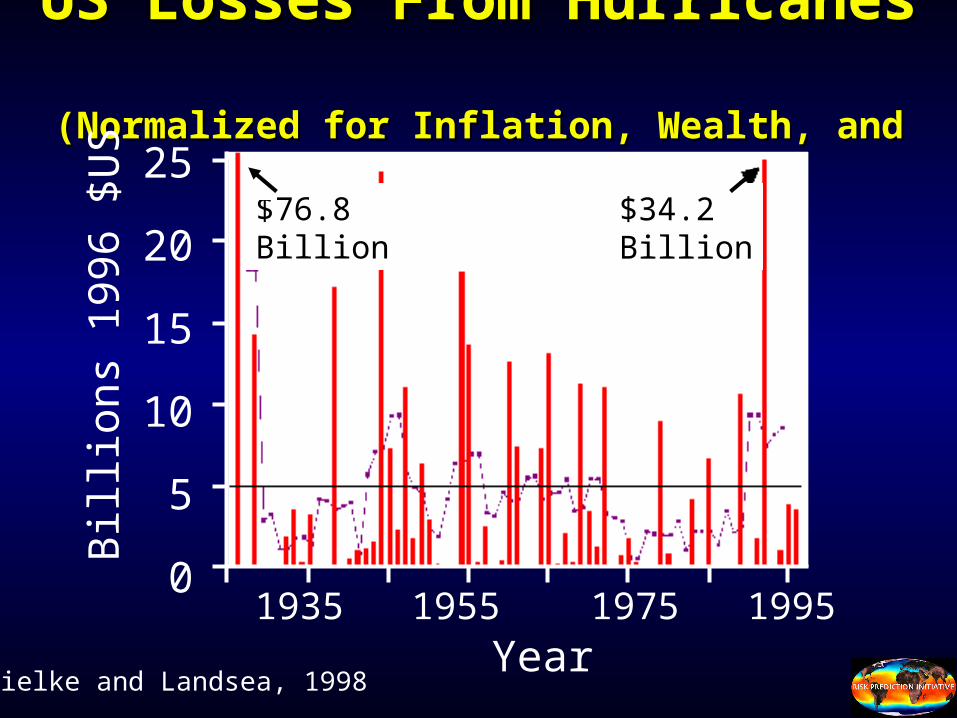

US Losses From Hurricanes US Losses From Hurricanes (Normalized for Inflation, Wealth, and Population)(Normalized for Inflation, Wealth, and Population)

1935 1955 1975 1995

25

20

15

10

5

0

Bill

ions

199

6 $U

S $76.8Billion

$34.2Billion

YearPielke and Landsea, 1998

Climate ResearchClimate Research

Wealth of new knowledgeWealth of new knowledge No knowledge of certainty about the future No knowledge of certainty about the future

climateclimate No certainty of how man’s actions will No certainty of how man’s actions will

influence the complicated climate systeminfluence the complicated climate system No methods to reliably predict the No methods to reliably predict the

behaviour of this complex systembehaviour of this complex system Do not know how to write for Climate Do not know how to write for Climate

change - no buyers - little interestchange - no buyers - little interest

Swiss Re have a more enlightened Swiss Re have a more enlightened approachapproach

Need to understand the climate Need to understand the climate system better through researchsystem better through research

Must tackle the uncertainty as a risk Must tackle the uncertainty as a risk which can be systematically which can be systematically analysed and overcomeanalysed and overcome

Global Climate ProtectionGlobal Climate Protection

Create adequate awareness of the Create adequate awareness of the problem (ignoring the problem will problem (ignoring the problem will not make it go away)not make it go away)

Industry needs to help pursue a Industry needs to help pursue a political solution (need to find ways political solution (need to find ways to implement climate protection to implement climate protection measures which are socially and measures which are socially and economically acceptable)economically acceptable)

Swiss Re’s climate change approachSwiss Re’s climate change approach Using research in products (RPI)Using research in products (RPI) Developing risk management strategies Developing risk management strategies

which exceed the boundaries of traditional which exceed the boundaries of traditional insurance cover - even a small change can insurance cover - even a small change can bring big casualties (dams, dykes)bring big casualties (dams, dykes)

Involved with UNEP - international climate Involved with UNEP - international climate conventionsconventions

Realization of the problem: political, social, Realization of the problem: political, social, economic, technical and cultural issueseconomic, technical and cultural issues

What can IOOS provide ?What can IOOS provide ?First Global insurance world cares about the US First Global insurance world cares about the US

- $’s drive the business- $’s drive the business

Improve historical and current data on risksImprove historical and current data on risks

Improve all aspects of the modelsImprove all aspects of the models

Provide information to the public about the Provide information to the public about the reality of changing climate. Public risk model ?reality of changing climate. Public risk model ?

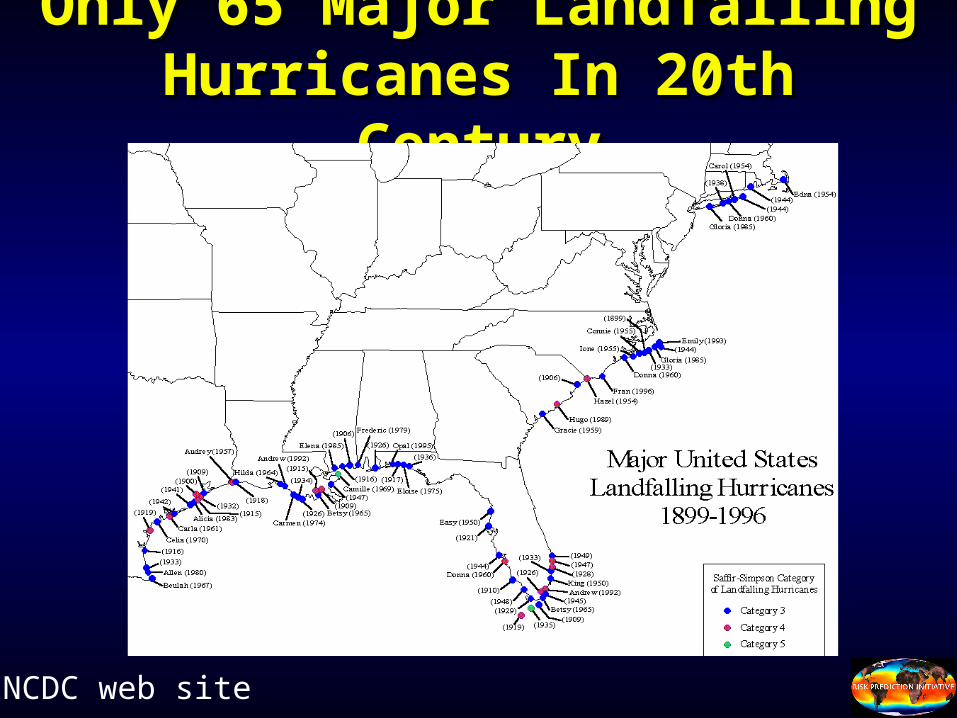

Only 65 Major Landfalling Only 65 Major Landfalling Hurricanes In 20th CenturyHurricanes In 20th Century

NCDC web site

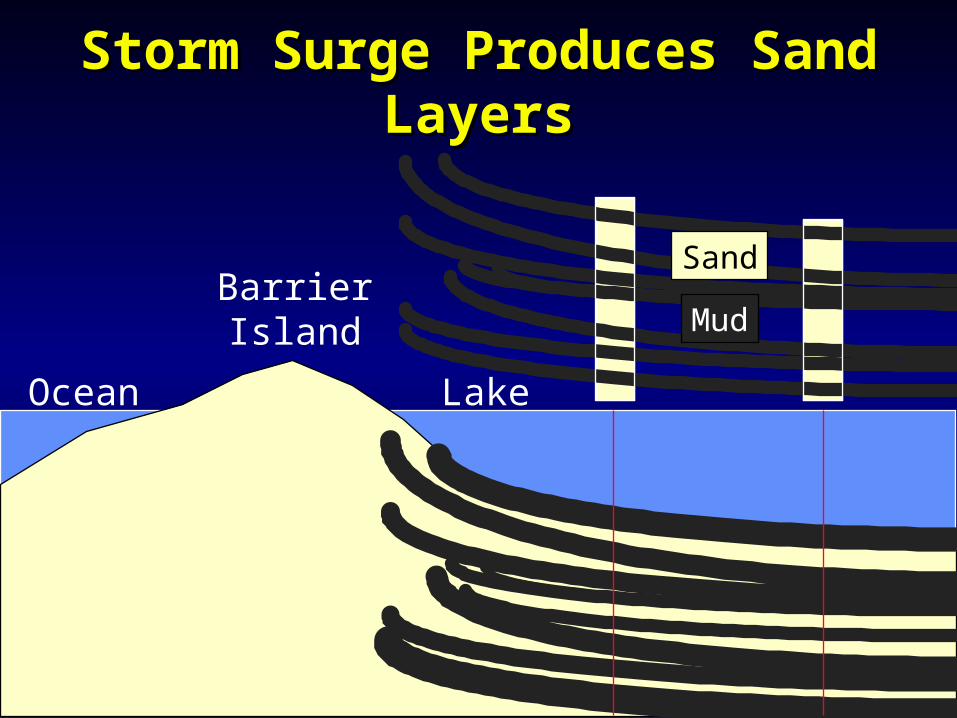

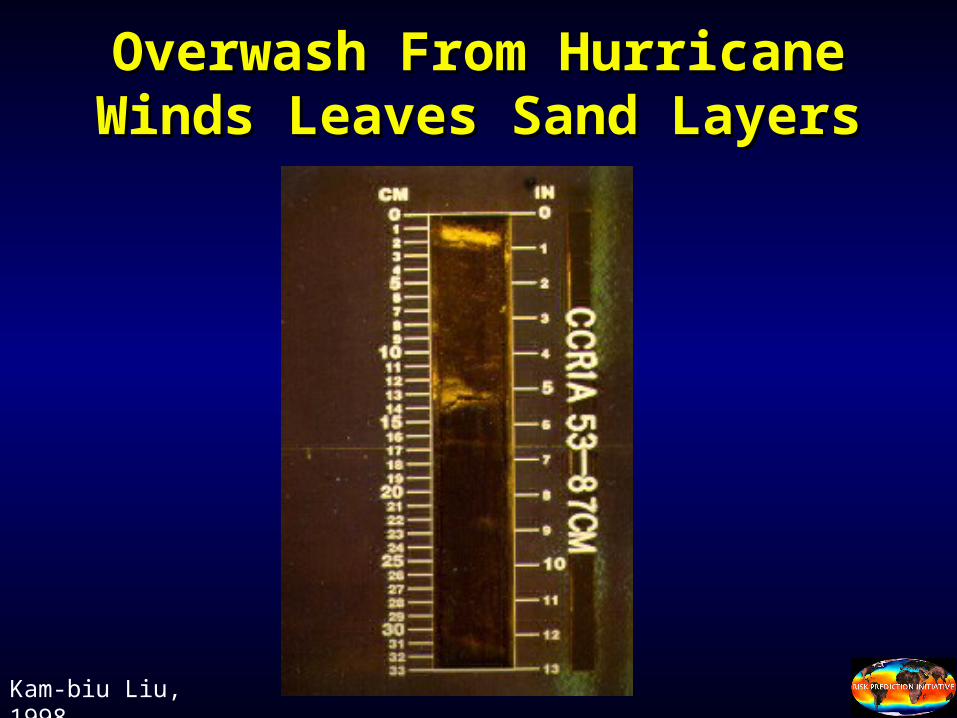

Storm Surge Produces Sand LayersStorm Surge Produces Sand Layers

BarrierIsland

Sand

Mud

Ocean Lake

Overwash From Hurricane Winds Overwash From Hurricane Winds Leaves Sand LayersLeaves Sand Layers

Kam-biu Liu, 1998

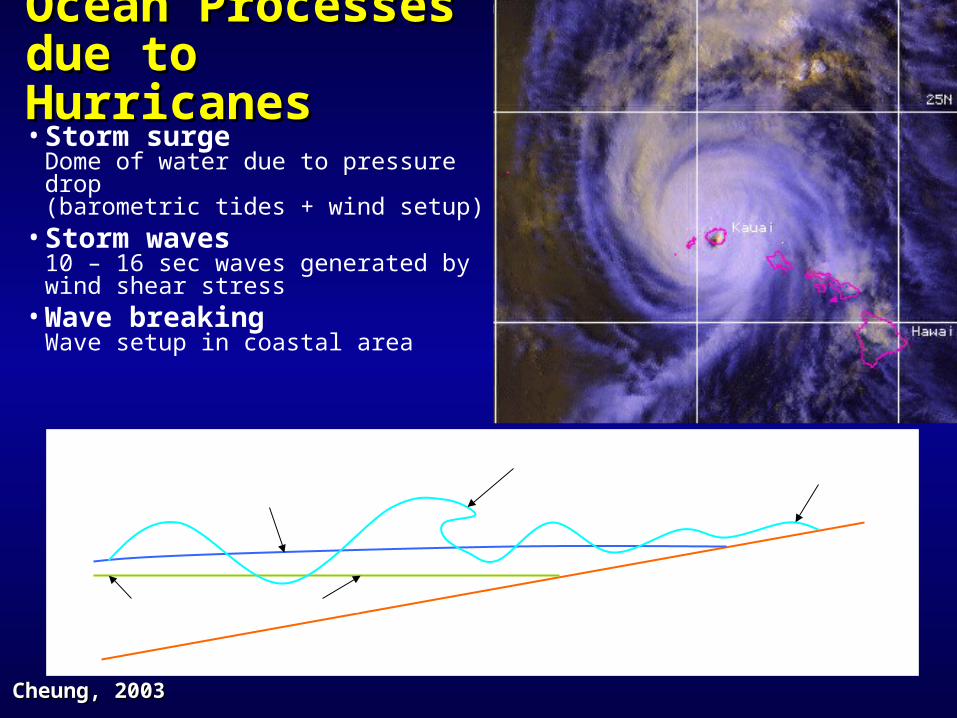

• Storm surge Dome of water due to pressure drop(barometric tides + wind setup)

• Storm waves10 – 16 sec waves generated by wind shear stress

• Wave breakingWave setup in coastal area

Ocean Processes Ocean Processes due to Hurricanesdue to Hurricanes

storm surgestorm waves wave setup

ILLUSTRATION

NOT TO SCALE

normal water level

Cheung, 2003Cheung, 2003

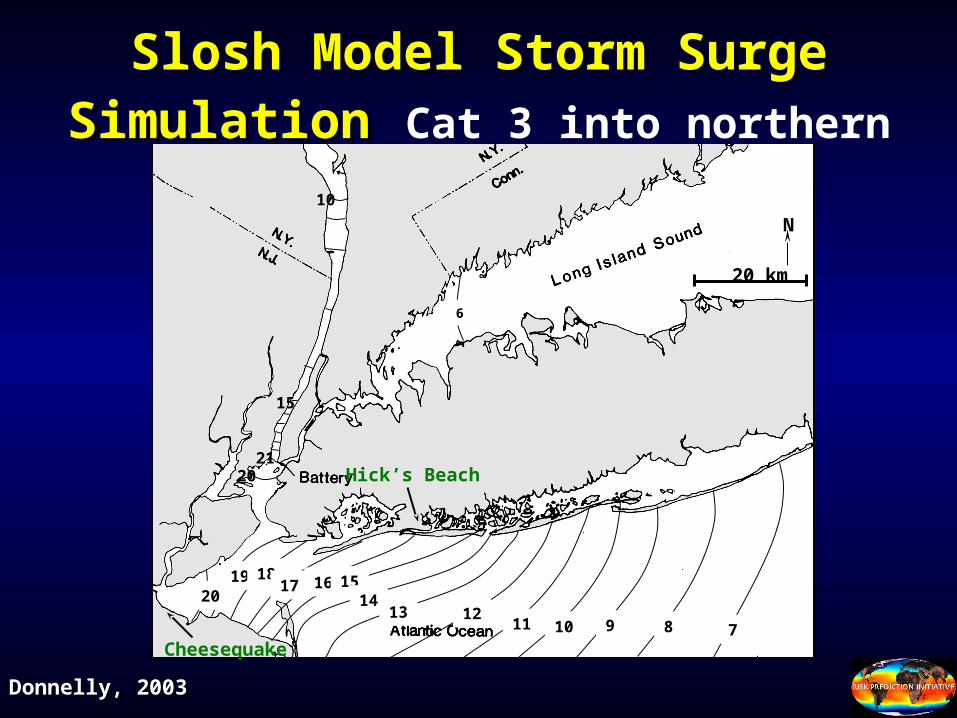

Slosh Model Storm Surge SimulationSlosh Model Storm Surge Simulation Cat 3 into northern New Jersey

20

2021

19 1817 16 15

1413 12

11 10 9 8 7

6

10

15

20 km

N

Hick’s Beach

Cheesequake

Donnelly, 2003Donnelly, 2003

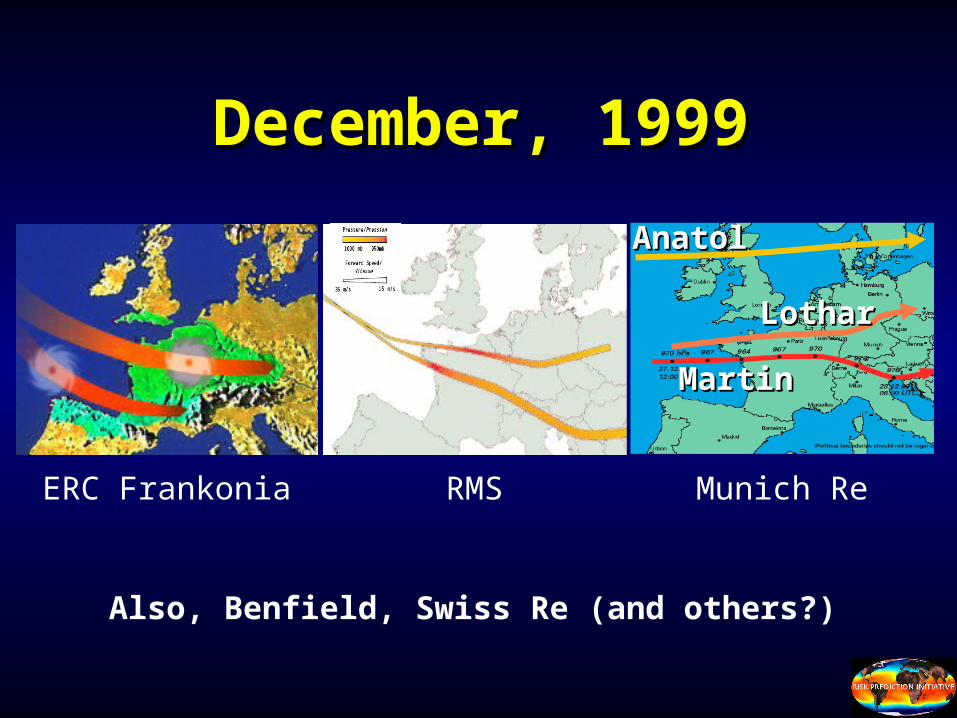

December, 1999December, 1999

ERC Frankonia Munich ReRMS

LotharLothar

MartinMartin

AnatolAnatol

Also, Benfield, Swiss Re (and others?)

Important QuestionsImportant Questions

• How clustered are European wind storms? The Bermuda bus concept !

• Why are they clustered? Are they 1 or 2 events ?

• Which factors are most important?

• Can seriality be predicted?

• Will seriality increase in the future?

• All require integrated ocean/atmos data

ENSO and U.S. Landfalling HurricanesENSO and U.S. Landfalling Hurricanes1900-19961900-1996

100

80

60

40

20

00 1 2 3 4 5 6 7

Pro

babi

lity

(%)

O’Brien et al., 1997 # of Storms

Cold Phase

Neutral

Warm Phase

US Hurricanes (1-Cumulative Frequency)

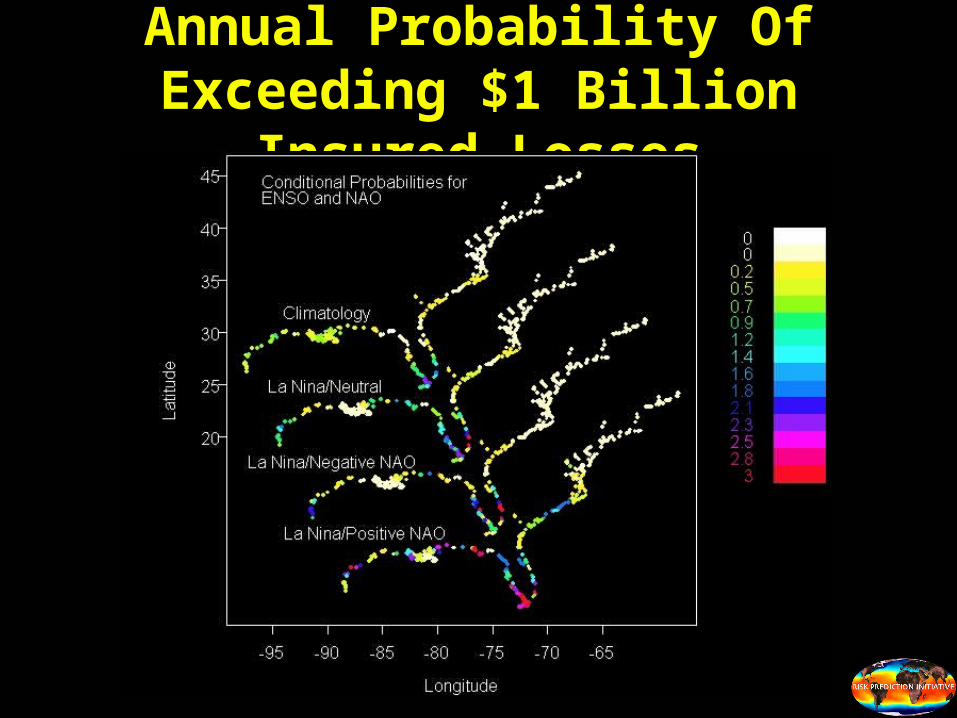

Annual Probability Of Exceeding $1 Billion Insured Losses

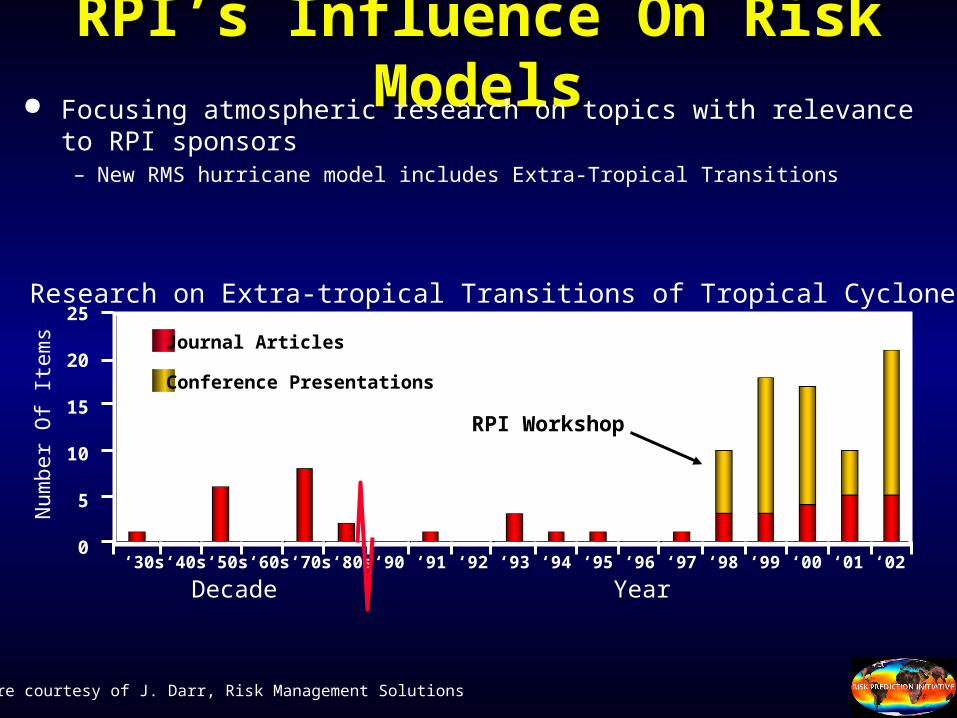

RPI’s Influence On Risk ModelsRPI’s Influence On Risk Models Focusing atmospheric research on topics with relevance to RPI sponsors

– New RMS hurricane model includes Extra-Tropical Transitions

Figure courtesy of J. Darr, Risk Management Solutions

Research on Extra-tropical Transitions of Tropical Cyclones

Year

Num

ber

Of I

tem

s

‘30s ‘40s ‘50s ‘60s ‘70s ‘80s ‘90 ‘91 ‘92 ‘93 ‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02

25

20

15

10

5

0

RPI Workshop

Journal Articles

Conference Presentations

Decade

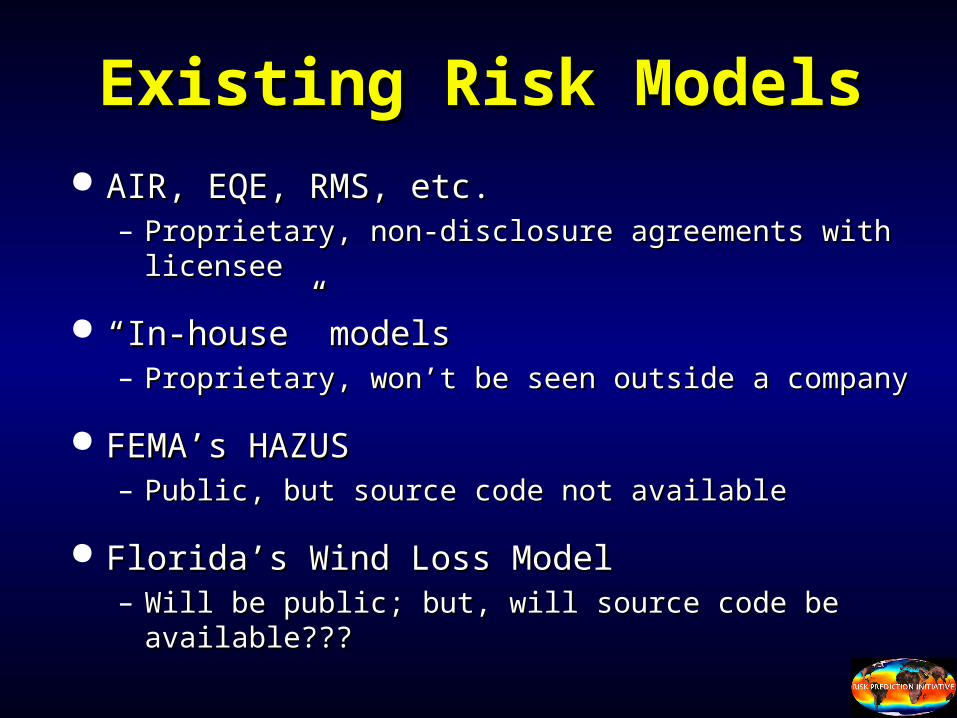

Existing Risk ModelsExisting Risk Models AIR, EQE, RMS, etc.AIR, EQE, RMS, etc.

– Proprietary, non-disclosure agreements with licenseeProprietary, non-disclosure agreements with licensee

““In-house” modelsIn-house” models– Proprietary, won’t be seen outside a companyProprietary, won’t be seen outside a company

FEMA’s HAZUS FEMA’s HAZUS – Public, but source code not availablePublic, but source code not available

Florida’s Wind Loss ModelFlorida’s Wind Loss Model– Will be public; but, will source code be available???Will be public; but, will source code be available???

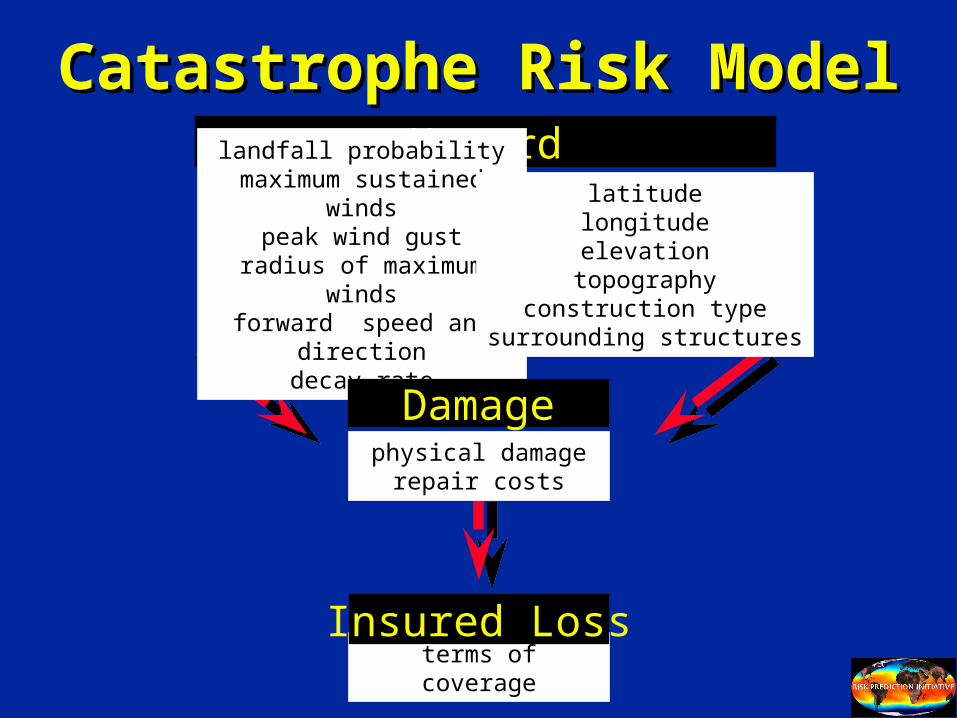

Catastrophe Risk ModelCatastrophe Risk Model

terms of coverage

Insured Loss

Hazardlandfall probability

maximum sustained windspeak wind gust

radius of maximum windsforward speed and direction

decay rate

latitudelongitudeelevation

topographyconstruction type

surrounding structures

physical damagerepair costs

Damage

How Good Are The Models?How Good Are The Models? Significant effort devoted to development of Significant effort devoted to development of

each model; but, do you know:each model; but, do you know:– Which model is better?Which model is better?– Which models, if any, have skill?Which models, if any, have skill?

Insurers essentially use multi-model Insurers essentially use multi-model ensemble forecasting to estimate uncertaintyensemble forecasting to estimate uncertainty

No “public” verification, but each company No “public” verification, but each company has their own opinion on which model is best has their own opinion on which model is best for a given situationfor a given situation

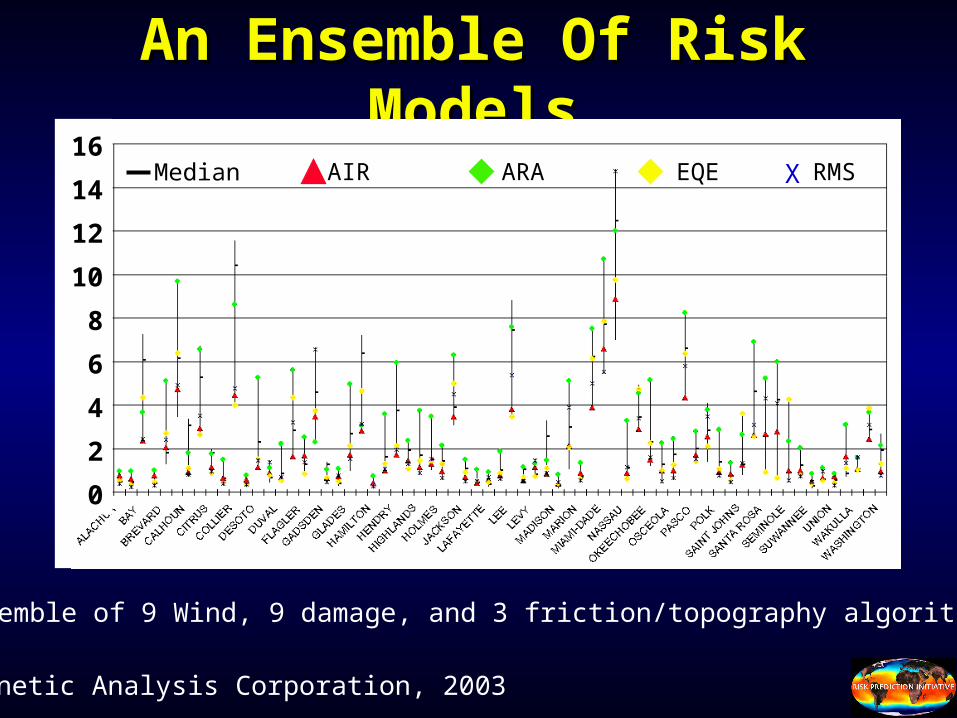

An Ensemble Of Risk ModelsAn Ensemble Of Risk Models

XMedian AIR ARA EQE RMS16

14

12

10

8

6

4

2

0

Ensemble of 9 Wind, 9 damage, and 3 friction/topography algorithms

Kinetic Analysis Corporation, 2003

What Are The Models Missing?What Are The Models Missing? StandardizationStandardization

– Not easy to incorporate new or alternate dataNot easy to incorporate new or alternate data

FlexibilityFlexibility– Not easy to change hazard or damage algorithmsNot easy to change hazard or damage algorithms

TransparencyTransparency– Proprietary aspects limit understanding and usesProprietary aspects limit understanding and uses

VerificationVerification– No public assessment of model skillNo public assessment of model skill

Why Do Insurers Need AnWhy Do Insurers Need AnOpen-Source Risk Model?Open-Source Risk Model?

Accelerate Development of Risk ModelsAccelerate Development of Risk Models– Access to latest scientific/engineering advancesAccess to latest scientific/engineering advances

Enhance Liquidity of Alternative Risk ProductsEnhance Liquidity of Alternative Risk Products– Direct Securitization, e.g., Cat BondsDirect Securitization, e.g., Cat Bonds

Rationalize Insurance RegulationRationalize Insurance Regulation– Florida Hurricane CommissionFlorida Hurricane Commission– California Earthquake AuthorityCalifornia Earthquake Authority

Promote Financing of Natural Catastrophes in Promote Financing of Natural Catastrophes in Developing CountriesDeveloping Countries– World Bank programsWorld Bank programs

IOOS and the Insurance sectorIOOS and the Insurance sector

Interested in prediction - realize that the Interested in prediction - realize that the ocean is an important driver of climateocean is an important driver of climate

Interested in reliable dataInterested in reliable data

Tools and products have to integrate Tools and products have to integrate with modelswith models

Future directions: An open-source risk Future directions: An open-source risk model ?model ?

http://www.bbsr.edu/rpi/On the web:On the web:

The Goal of the RPIThe Goal of the RPI

To support research on natural hazards To support research on natural hazards

and to transform science into knowledge and to transform science into knowledge

that our sponsors can use to assess risk.that our sponsors can use to assess risk.

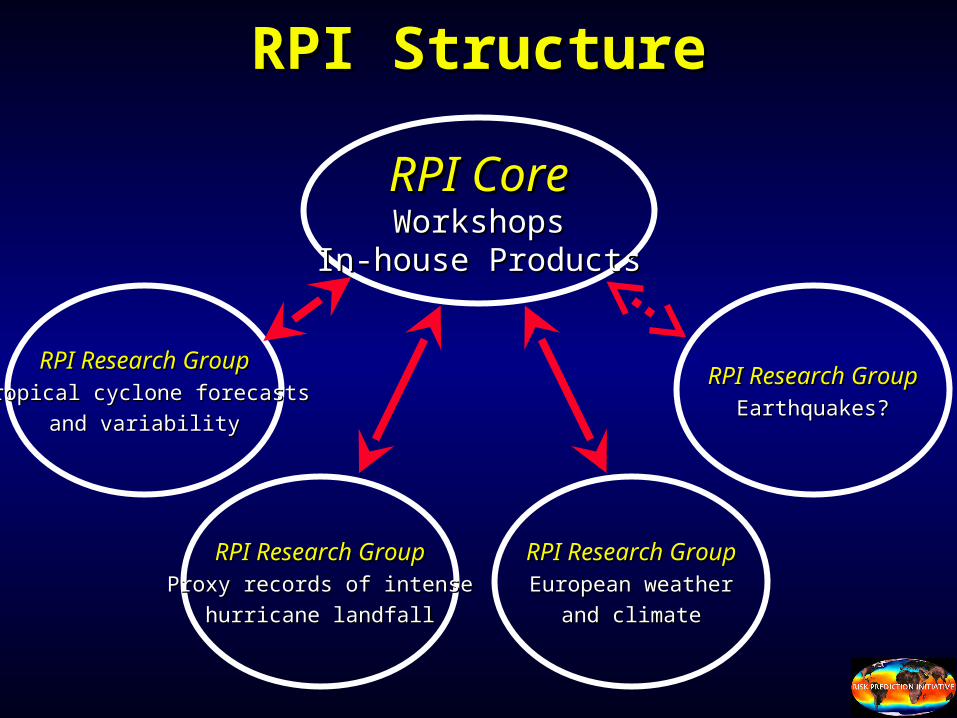

RPI StructureRPI Structure

RPI CoreRPI CoreWorkshopsWorkshops

In-house ProductsIn-house Products

RPI Research GroupRPI Research GroupTropical cyclone forecastsTropical cyclone forecasts

and variabilityand variability

RPI Research GroupRPI Research GroupProxy records of intenseProxy records of intense

hurricane landfallhurricane landfall

RPI Research GroupRPI Research GroupEuropean weatherEuropean weather

and climateand climate

RPI Research GroupRPI Research GroupEarthquakes?Earthquakes?

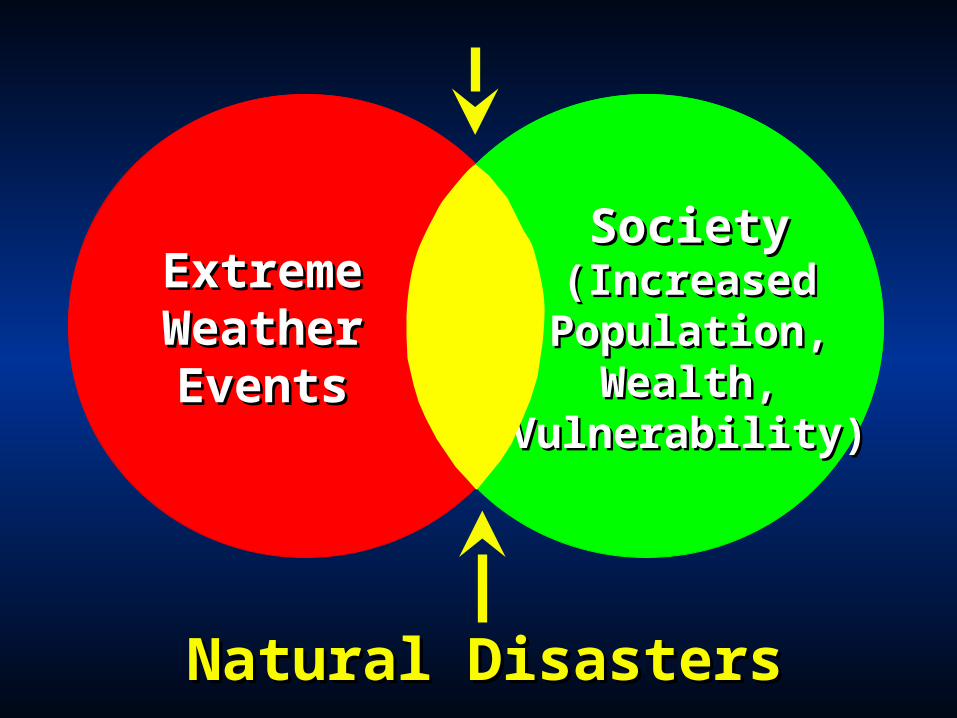

ExtremeExtremeWeatherWeatherEventsEvents

SocietySociety(Increased(IncreasedPopulation,Population,

Wealth,Wealth,Vulnerability)Vulnerability)

Natural DisastersNatural Disasters

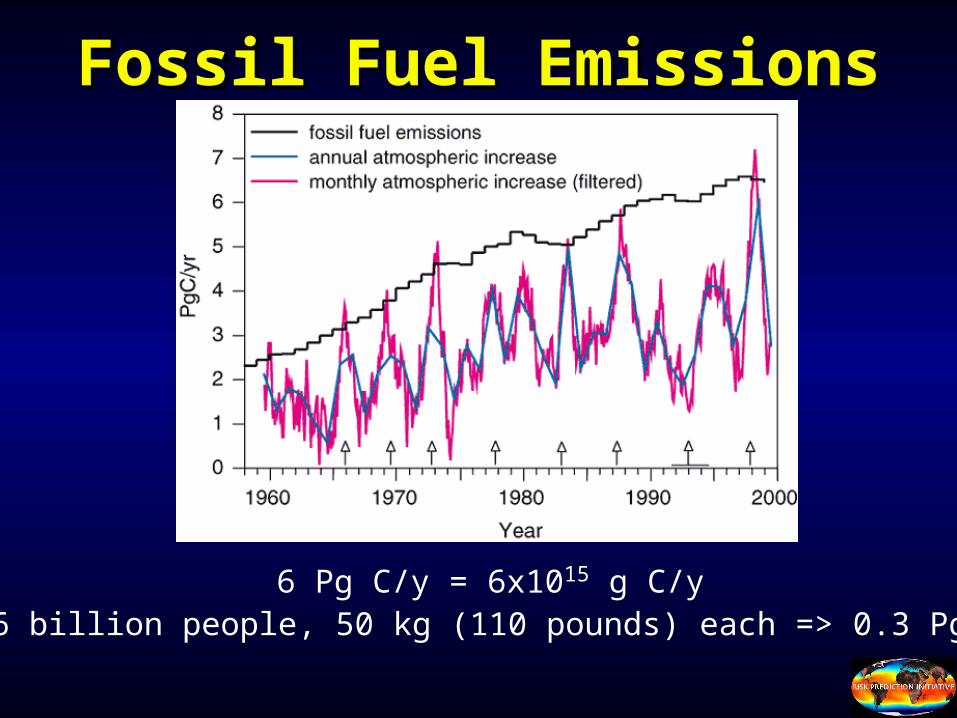

Fossil Fuel EmissionsFossil Fuel Emissions

6 Pg C/y = 6x1015 g C/y6 billion people, 50 kg (110 pounds) each => 0.3 Pg